Embed Size (px)

Citation preview

Money and Money and BankingBankingEl Dorado High El Dorado High SchoolSchool20152015

Chapter 10Chapter 10

$ Money $

• Money is the only commodity that is good for nothing, but to be gotten rid of.

• It will not feed you, clothe you, shelter you, or amuse you unless you spend it or invest it.

• It imparts value only in parting.

• People will do almost anything for money and money will do almost anything for people.

• Money is a captivating, circulating, masquerading puzzle.

Chapter Objectives

• The functions of money

• Components of the money supply

• What “backs” the money supply

• The Federal Reserve and the U.S. banking system

• The functions and responsibilities of the Federal Reserve

13-3

Functions of Money • What are the functions of money?

• It is a medium of exchange- Usable for buying goods and services– Money is readily acceptable as payment– Allows societies to escape the barter system– A convenient way of exchanging goods

• It is a unit of account- Usable as a yardstick to measure the relative value of goods, services, and resources. – We gauge the value of goods in dollars– Additionally, it allows us to define debt obligations, determine taxes owed, and calculate

the nations’ GDP.

• It also serves as a store of value- Enables people to transfer purchasing power from the present to the future– People don’t normally spend all their income so they hold some wealth in money to allow

for future use. – Money is liquid ( immediately spendable) and therefore is the preferred store of value

because it allows you to obtain your money instantly and spend it immediately on goods/ services.

13-4

Money Defined: M1• M1 is the narrowest definition of the U.S. money supply

• Consists of: Money, M1= Currency + Checkable Deposits

• Currency: Coins and paper money ( in the hands of the public)– Token money: All U.S. coins in circulation are considered token money. The

intrinsic value, the actual value of the metal contained in the coin, is less than the face value of the coin (This prevents people from melting down the metal for its value)

– Paper money: About 46 % of U.S. money supply (all of it in the form of Federal Reserve Notes). Issued by the Federal Reserve System (U.S. central banks)

• Checkable deposits: Deposits in commercial banks and thrift or savings institutions on which checks of any size can be drawn.– Largest component of the M1 money supply(52%) due to the safety and

convenience checks allow.– Example: You don’t mail currency to pay a bill, it is safer and convenient to

send a check instead. 13-5

Money Defined, cont. – In the United States there are several types of financial institutions that

allow customers the ability to write checks in the amount reflecting the funds they have deposited

– Institutions offering checkable deposits:

Commercial banks: The primary depository institution.Accept deposits from businesses and households; in turn use it to make a

variety of loans.

Savings and loan associations, mutual savings banks, credit unions: These institutions supplement commercial banks and are widely known as Thrift Institutions or thrifts.

They also accept business and household deposits and use these funds to finance mortgages and other types of loans.

Money Defined: M2• A 2nd ( and broader) definition of money includes:

– M1 + near-monies

– Near-monies: Certain highly liquid financial assets that do not function directly or fully as a medium of exchange, but can be readily converted into currency or checkable deposits.

(3) Categories of near-monies in the M2 definition of money:

1. Savings deposits including money market deposit accounts (MMDA)

• MMDA: An interest bearing account where banks/thrifts can pool together

• Individual accounts to buy a variety of interest-bearing short term securities.

2. Small time deposits (less than $100,000)

3. Money market mutual funds (MMMF)

13-7

Money Defined: M3

• M3 includes large ($100,000) time deposits, usually owned by businesses as certificates of deposits.

• The market for these certificates allows for the quick liquidity; however, at the risk of taking a loss.

• Are normally used by businesses as large time deposits for saving and not necessarily as money

• These deposits can be converted into checkable deposits, therefore, they may also be considered to be near-money.

• M3= M2 + Large ($100,000 or more) time deposits

Money Supply• Are credit cards money?• No, however, they are a means of

obtaining a short term loan from a commercial bank or financial institution issuing the card.

• How does credit work?• When you purchase an item the bank that

issued the card will reimburse the store, later you will reimburse the bank.

• Your reimbursement may be subject to sizeable interest charges if you pay in installments and an annual fee may apply to some credit offers

• What “backs” the money supply?– Nothing!– The Government’s ability to keep the

value of money relatively stable is the only guarantee that we are given.

• Why is money valuable?– Acceptability: Currency and checkable

deposits are the acceptable medium of exchange because people feel confident that the paper money they accept for real goods, services, and resources will be equally exchangeable for other things (Remember: We believe that the government is backing the value of our currency)

– Legal tender: Our government has designed currency known as legal tender (coin & paper money). Each particular bill contains the following,” this note is legal tender for all debts, public and private.”

– The paper money in our economy is fiat money ( i.e., it is money because the government says so! Not because its actual physical value is can be redeemed for precious metals)

– Relative scarcity: The value of money depends on its supply and demand. Money derives its value from its scarcity relative to its use.

13-9

Money and Prices• Prices affect purchasing power of money

– When the Consumer Price Index (CPI) or cost of living goes up, the value of the dollar goes down, and vice versa

– Common sense, higher prices lower the value of the dollar are needed to buy goods and services. Lower prices increase the purchasing power of the dollar because fewer dollars are needed to purchase goods and services

• Hyperinflation renders money unacceptable– Think in terms of Germany (post- WW1, example in book) and Mexico’s

Peso devaluation several decades ago.

• Stabilizing money’s purchasing power1. Intelligent management of the money supply – monetary policy. In short,

effective control over the money supply)2. Appropriate fiscal policy

13-10

Next:

The Federal Reserve System

a.k.a., The Central Bank

FIRST LOOK inside the FEDERAL RESERVEhttp://www.youtube.com/watch?v=I2m3t2Yr8Vg

Federal Reserve System

• Historical background

• Decentralized and unregulated banking became inconvenient. The multiple private banking notes became confusing; coupled with money mismanagement that led to inappropriate money supplies to address the needs of the economy.

• In 1907, in response to a banking crisis, Congress appointed the National Monetary Commission to study the monetary and banking problems present in our economy, as well as to outline a congressional course of action

• The result was the Federal Reserve Act of 1913.

• In response, The Federal Reserve System (the Fed) was created in the early twentieth century, following a congressional decision that a more efficient banking system, with centralization and public control had become essential.

13-12

Federal Reserve System• Board of Governors

• The Federal Reserve System’s central authority for the U.S. money and banking system rests with its Executively appointed Board of Governors.

• The (7) member Board of Governors is appointed by the U.S. President with Senatorial confirmation for staggered terms of 14 years (Staggered so that one member gets replaced every 2 years).

• The President selects the chairperson and vice-chairperson of the board from among the (7) members; they may serve (4) year terms and can be reappointed by the President for (4) more.

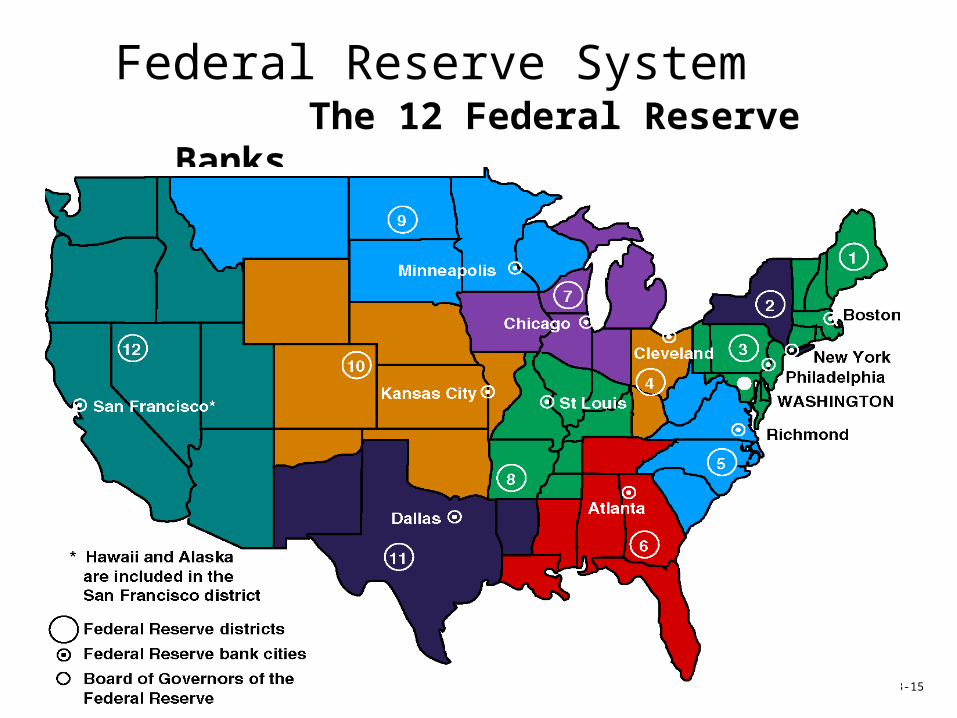

Federal Reserve System• 12 Federal Reserve Banks

• These 12 banks collectively serve as the nations, “ Central Bank.”

• These banker’s banks represent a blend of private ownership and public control.

• These 12 banks are distributed into distinct districts across the nation to accommodate the size and economic diversity of the United States.

• The Fed’s Board of Governors implement their basic monetary guidelines thru these banks by coordinating the policies that these banks must carry out.

Federal Reserve System The 12 Federal Reserve Banks

Source: Federal Reserve Bulletin 13-15

Federal Reserve System• Quasi-public banks• banks because the blend private ownership under private control.

• Each one of these Fed banks is owned by the commercial banks in their districts; commercial banks are required to purchase shares of stock in the Fed bank that serves its district.

• However, the owners (shareholders) of these central banks can neither control the bank’s policies or bank officials because the Board of Governors (appointed by the President) set the banks policies and procedures.

• These banks are not meant to be motivated by profit, but by designing policies meant benefit the economic well-being of the nation as a whole. (They do not compete with commercial banks, but rather interact primarily with the government, commercial, and thrift banks)

Federal Reserve System• Banker’s bank

• These central banks are referred to as banker’s banks because the perform relatively the same functions for commercial banks and thrifts that these banks themselves do for the public. ( the central bank accepts deposits and makes loans to banks and thrifts)

• An Additional Function: The Central Banks issue currency when they are directed to do so by the Federal Reserve Board.

• In essence, Congress authorizes the Federal Reserve Banks to put into circulation Federal Reserve Notes which constitutes the economy’s paper money supply

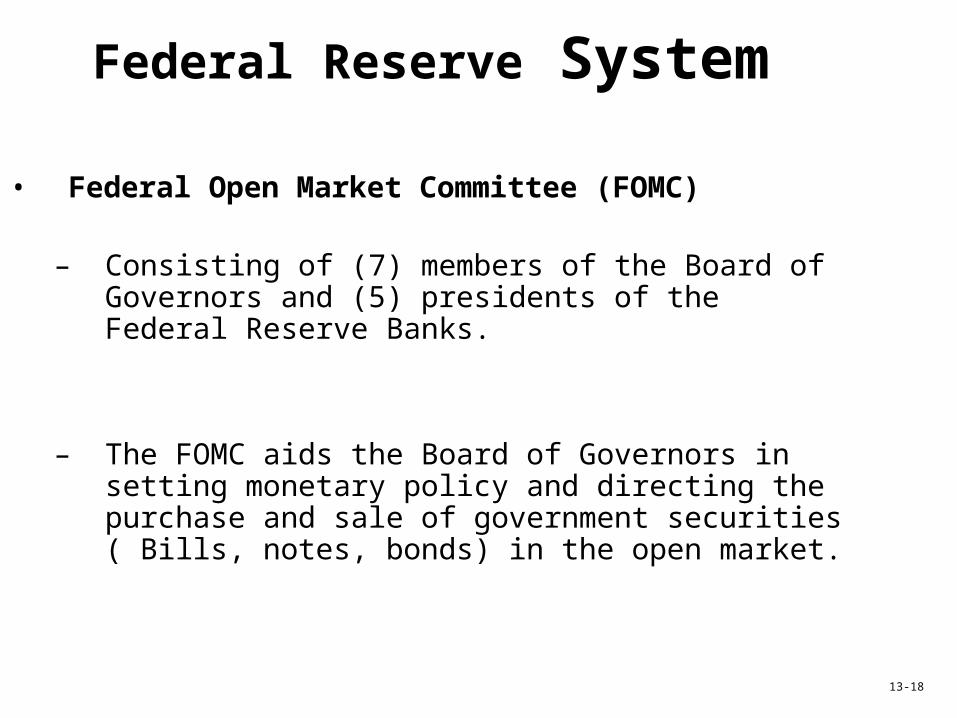

Federal Reserve System

• Federal Open Market Committee (FOMC)

– Consisting of (7) members of the Board of Governors and (5) presidents of the Federal Reserve Banks.

– The FOMC aids the Board of Governors in setting monetary policy and directing the purchase and sale of government securities ( Bills, notes, bonds) in the open market.

13-18

Federal Reserve System• Advisory Council

– There are (3) advisory councils composed of private citizens that meet periodically with the Board of Governors to voice their views on banking and monetary policy.

– These advisory councils have no policymaking powers and the Board has no obligation to take their advice.

1. The Federal Advisory Council is composed of composed of (12) commercial bankers (one selected annually by each of the (12) Federal Reserve Banks)

2. The Thrift Institutions Advisory Council consists of representatives from savings and loan associations, savings banks, and credit unions.

3. The Consumer Advisory Council consists of a 30 member group with representation ranging from consumers of financial services to academic and legal specialists in consumer matters.

• Commercial banks and thrifts– 7,300 commercial banks

– 11,000 thrifts

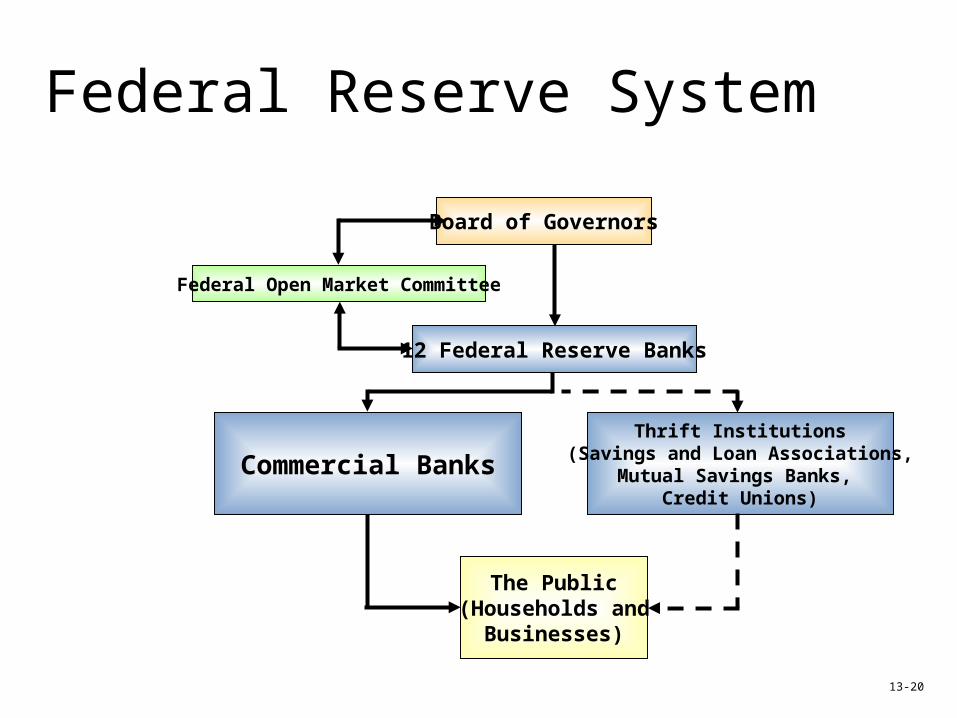

Federal Reserve System

Commercial BanksThrift Institutions

(Savings and Loan Associations,Mutual Savings Banks,

Credit Unions)

The Public(Households and

Businesses)

12 Federal Reserve Banks

Board of Governors

Federal Open Market Committee

13-20

Federal Reserve Functions

• Issue currency– The paper currency used in the U.S. monetary system are known as Federal

Reserve Notes and are issued by the Federal Reserve Banks. – Each bill issued has a black identifier in the upper left of the front of a newly

designed bill (Ex. A1=Boston Fed, B2= New York Fed)

• Set reserve requirements• Lend money to banks

– The Fed lends money to banks an thrifts and charges them an interest rate called the discount rate

• Set discount rate• Check collection• Fiscal agent for U.S. government• Supervise banks• Control the money supply

13-21

Federal Reserve System

• Federal Reserve independence

• Recent developments– Relative decline of banks and thrifts– Consolidation – Convergence of services provided by

financial institutions– Globalization of financial markets– Electronic payments

13-22

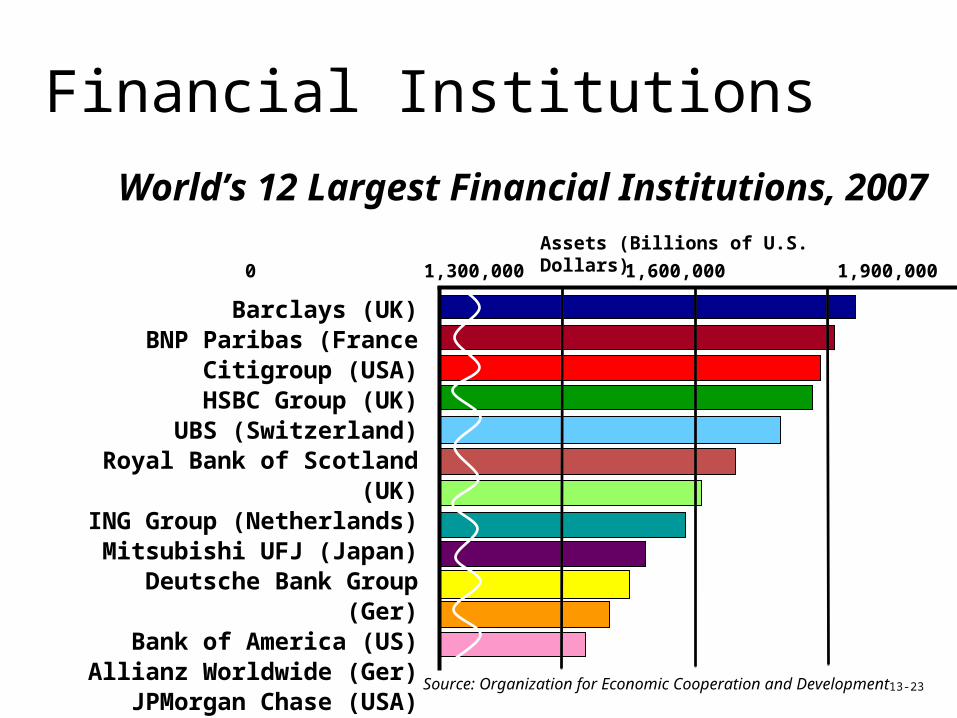

Financial InstitutionsWorld’s 12 Largest Financial Institutions, 2007

Barclays (UK)BNP Paribas (France

Citigroup (USA)HSBC Group (UK)UBS (Switzerland)

Royal Bank of Scotland (UK)ING Group (Netherlands)

Mitsubishi UFJ (Japan)Deutsche Bank Group (Ger)

Bank of America (US)Allianz Worldwide (Ger)JPMorgan Chase (USA)

0 1,300,000 1,600,000 1,900,000

Source: Organization for Economic Cooperation and Development

Assets (Billions of U.S. Dollars)

13-23

The Global Greenback• U.S. currency circulating abroad

– Russia $80 billion– Argentina $50 billion– $450 billion total– 60% of total US currency circulates at any

given time.

• U.S. profits from dollars leaving (global devaluation)

• Black markets and illegal activities

• Dollar offers stable purchasing power

• Exchange rate risk

13-24

Key Terms• medium of exchange• unit of account• store of value• M1• Federal Reserve Notes• token money• checkable deposits• commercial banks• thrift institutions• near-monies• M2• savings account• money market deposit account

(MMDA)

• time deposits• money market mutual fund

(MMMF)• legal tender• Federal Reserve System• Board of Governors• Federal Reserve Banks• Federal Open Market

Committee (FOMC)• financial services industry• electronic payments

13-25