Embed Size (px)

Citation preview

Monetary Policy

Instruments, Targets, and Goals

The Federal Reserve System

• The Federal Reserve System was created in 1913. The Fed’s responsibilities include:– Controlling the supply of money– Monitoring & Regulating Commercial Banks– Facilitate Checks Clearing

Who Owns the Federal Reserve System

• The Federal Reserve System is a joint enterprise between the government and the private sector– The Fed’s operating budget is not part of the

Federal budget– National banks are required by law to be

members of the federal reserve system (membership is optional for state banks), but are also “owners” of the Fed.

Leadership of the Federal Reserve

• The Federal Reserve is divided into twelve districts. Each district has a Regional Federal Reserve Bank

Federal Reserve Districts

Leadership of the Federal Reserve

• The Federal Reserve is divided into twelve districts. Each district has a Regional Federal Reserve Bank

• Regional bank presidents are elected by member banks, local businesses, and the Board of Governors for 5 year terms (renewable)

• The Board of Governors has seven members. Each is appointed by the president and confirmed by the senate for a 14 year non-renewable term

• A member of the board is appointed chairman for a 4 year (renewable) term.

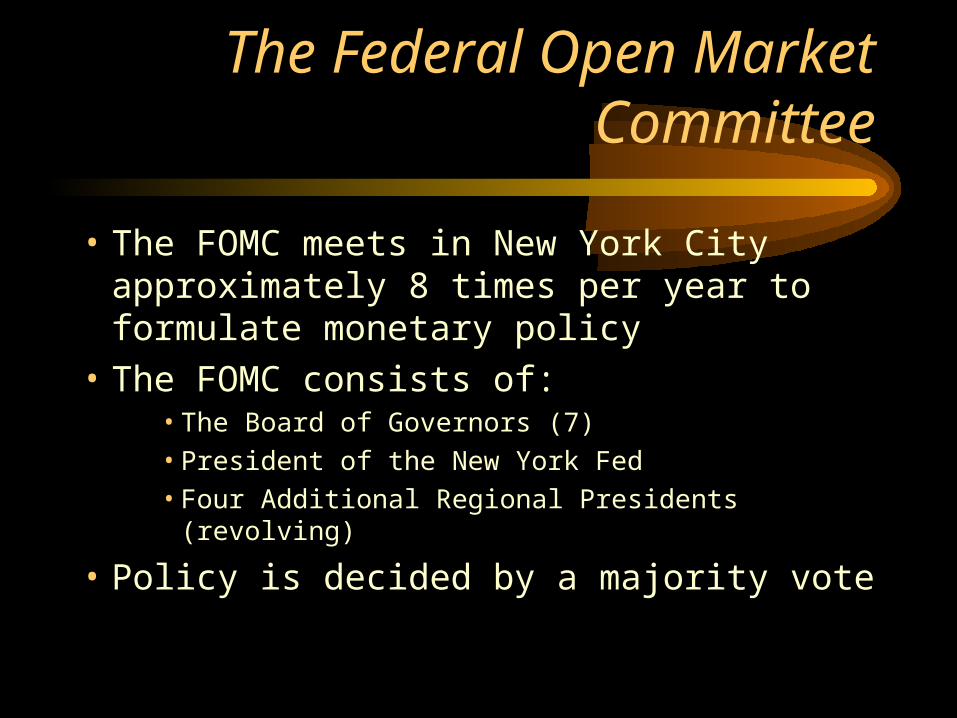

The Federal Open Market Committee

• The FOMC meets in New York City approximately 8 times per year to formulate monetary policy

• The FOMC consists of:• The Board of Governors (7)

• President of the New York Fed

• Four Additional Regional Presidents (revolving)

• Policy is decided by a majority vote

Monetary Policy

• Monetary policy is characterized by four criterion:– Goals: The desired result of monetary policy– Instruments: The methods used to influence the

supply of money– Targets: Attempts to quantify the size of a

policy decision– Discretion: The degree of flexibility in

monetary policy

Monetary Policy Goals

• What are central banks trying to accomplish through monetary policy?– Low, stable rates of inflation (long run)– Full employment (short run)

• Are these goals compatible with each other? (Phillips curve)

• Internal objectives vs. external objectives

Monetary Policy Instruments

• How does the Federal Reserve “control” the supply of money?– Open Market Operations (M0 & M1)– Discount Rate (M0 & M1)– Reserve Requirement ( M1)

The Fed’s Balance Sheet

AssetsUS Treasuries: $500B

Other Assets: $60B

Gold: $12B

Loans to Commercial Banks (Discount Window): $.1B

Total: $572.1B

LiabilitiesCurrency

In Circulation: $500B

Vault Cash: $40B

Bank Deposits: $20B

Net Worth: $12.1B

Total: $572.1B

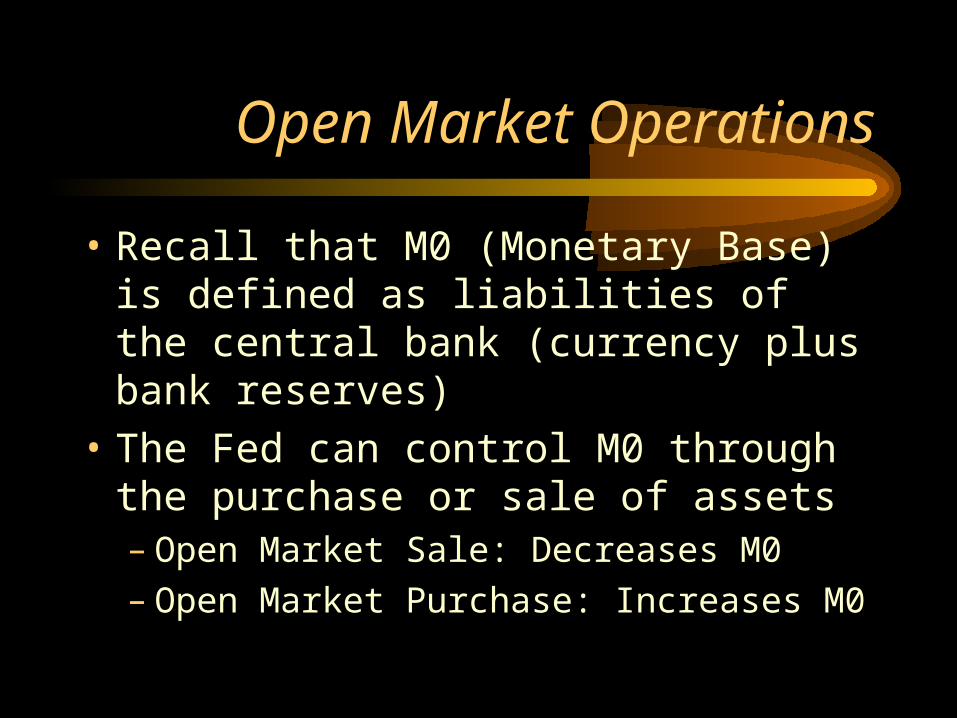

Open Market Operations

• Recall that M0 (Monetary Base) is defined as liabilities of the central bank (currency plus bank reserves)

• The Fed can control M0 through the purchase or sale of assets– Open Market Sale: Decreases M0– Open Market Purchase: Increases M0

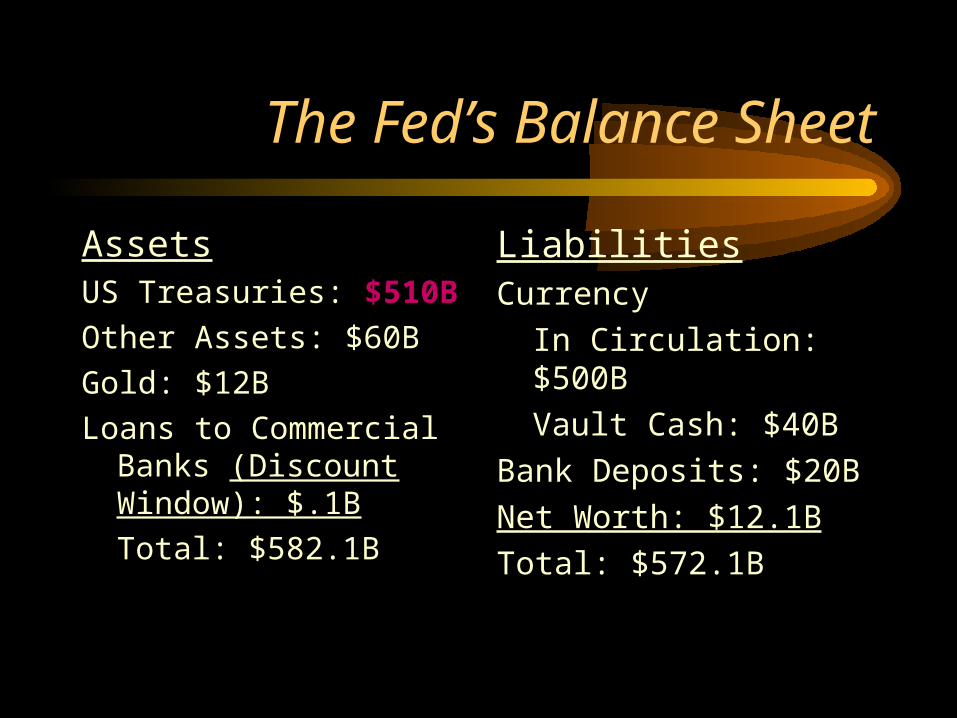

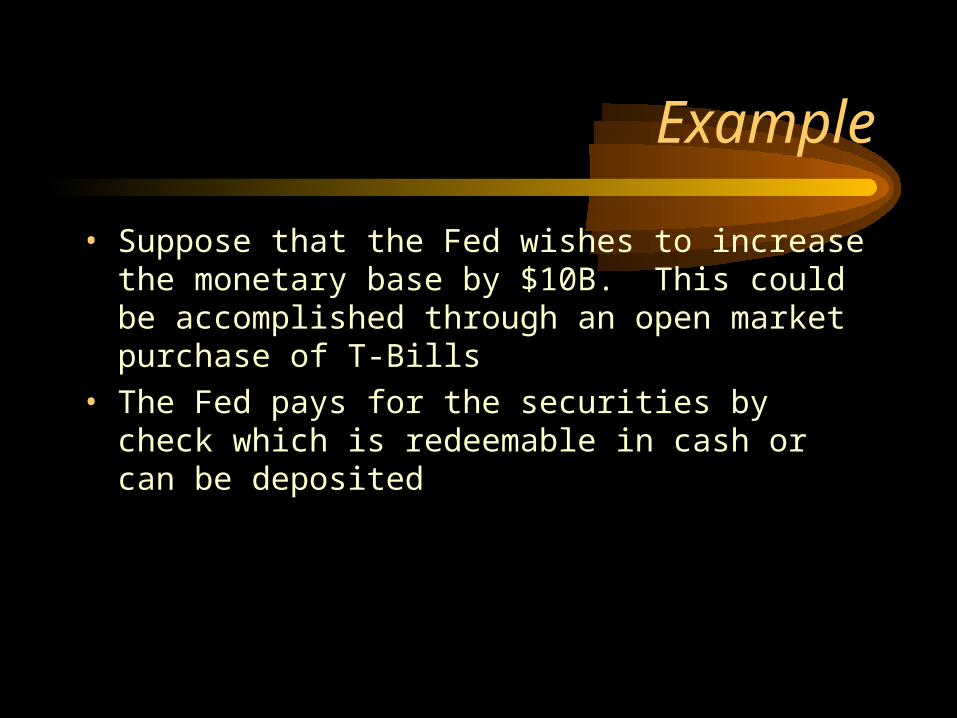

Example

• Suppose that the Fed wishes to increase the monetary base by $10B. This could be accomplished through an open market purchase of T-Bills

The Fed’s Balance Sheet

AssetsUS Treasuries: $510B

Other Assets: $60B

Gold: $12B

Loans to Commercial Banks (Discount Window): $.1B

Total: $582.1B

LiabilitiesCurrency

In Circulation: $500B

Vault Cash: $40B

Bank Deposits: $20B

Net Worth: $12.1B

Total: $572.1B

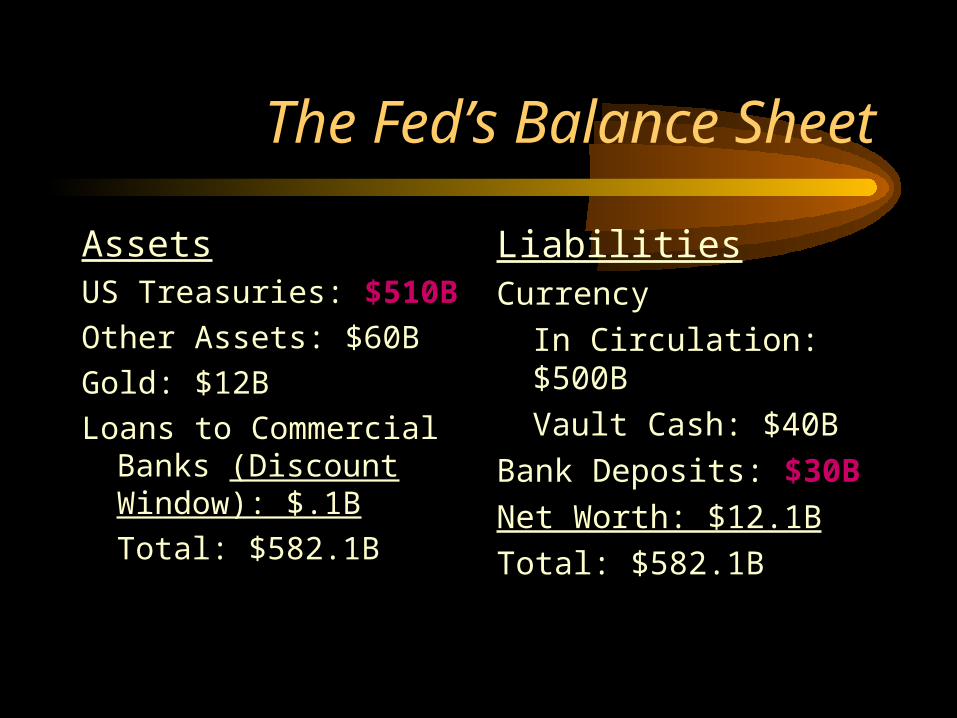

Example

• Suppose that the Fed wishes to increase the monetary base by $10B. This could be accomplished through an open market purchase of T-Bills

• The Fed pays for the securities by check which is redeemable in cash or can be deposited

The Fed’s Balance Sheet

AssetsUS Treasuries: $510B

Other Assets: $60B

Gold: $12B

Loans to Commercial Banks (Discount Window): $.1B

Total: $582.1B

LiabilitiesCurrency

In Circulation: $500B

Vault Cash: $40B

Bank Deposits: $30B

Net Worth: $12.1B

Total: $582.1B

Example

• Suppose that the Fed wishes to increase the monetary base by $10B. This could be accomplished through an open market purchase of T-Bills

• The Fed pays for the securities by check which is redeemable in cash or can be deposited

• Suppose the Fed wishes to lower M0 by $5– it could accomplish this by selling some of its gold

The Fed’s Balance Sheet

AssetsUS Treasuries: $510B

Other Assets: $60B

Gold: $7B

Loans to Commercial Banks (Discount Window): $.1B

Total: $577.1B

LiabilitiesCurrency

In Circulation: $500B

Vault Cash: $40B

Bank Deposits: $30B

Net Worth: $12.1B

Total: $582.1B

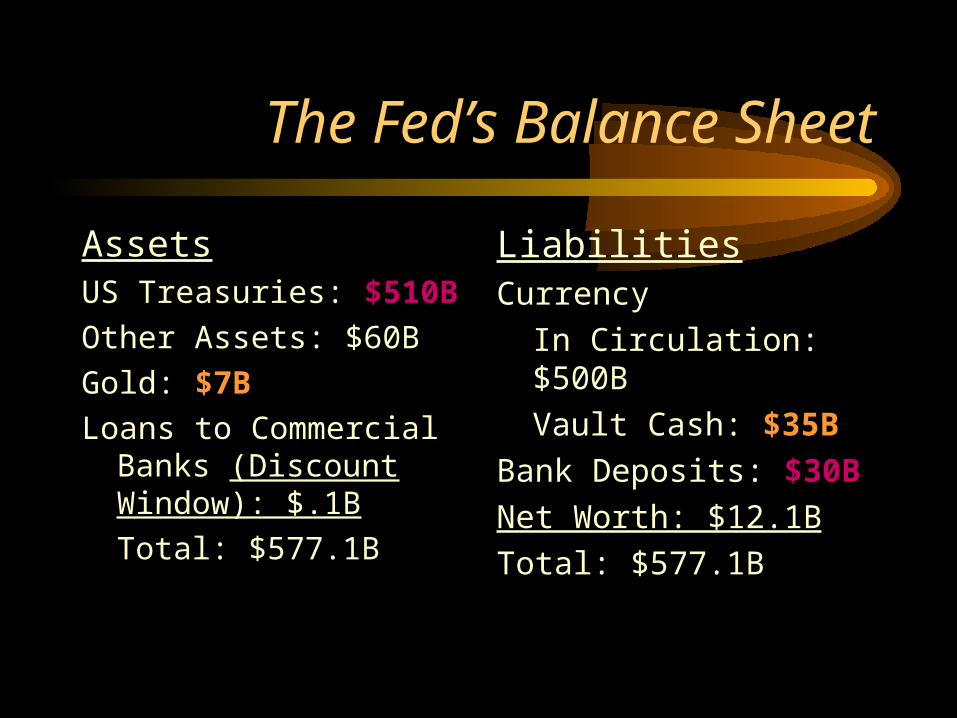

Example

• Suppose that the Fed wishes to increase the monetary base by $10B. This could be accomplished through an open market purchase of T-Bills

• The Fed pays for the securities by check which is redeemable in cash or can be deposited

• Suppose the Fed wishes to lower M0 by $5– it could accomplish this by selling some of its gold

• The gold is paid for by check, which is drawn from either the bank’s reserve cash or its account at the Fed

The Fed’s Balance Sheet

AssetsUS Treasuries: $510B

Other Assets: $60B

Gold: $7B

Loans to Commercial Banks (Discount Window): $.1B

Total: $577.1B

LiabilitiesCurrency

In Circulation: $500B

Vault Cash: $35B

Bank Deposits: $30B

Net Worth: $12.1B

Total: $577.1B

Commercial Banking and M1

• Recall that M1 is composed of Currency in circulation and checking accounts. The Fed can control currency directly, but checking accounts are controlled by commercial banks

Commercial Banking and M1

• Recall that M1 is composed of Currency in circulation and checking accounts. The Fed can control currency directly, but checking accounts are controlled by commercial banks

• The fed can influence the creation of checking accounts through the reserve requirement and the discount rate

Banks, like any other business, exist to earn profits

• Banks accept deposits and then use those funds to create loans

• Profit = Interest Collected on Loans – Interest Paid to Deposits

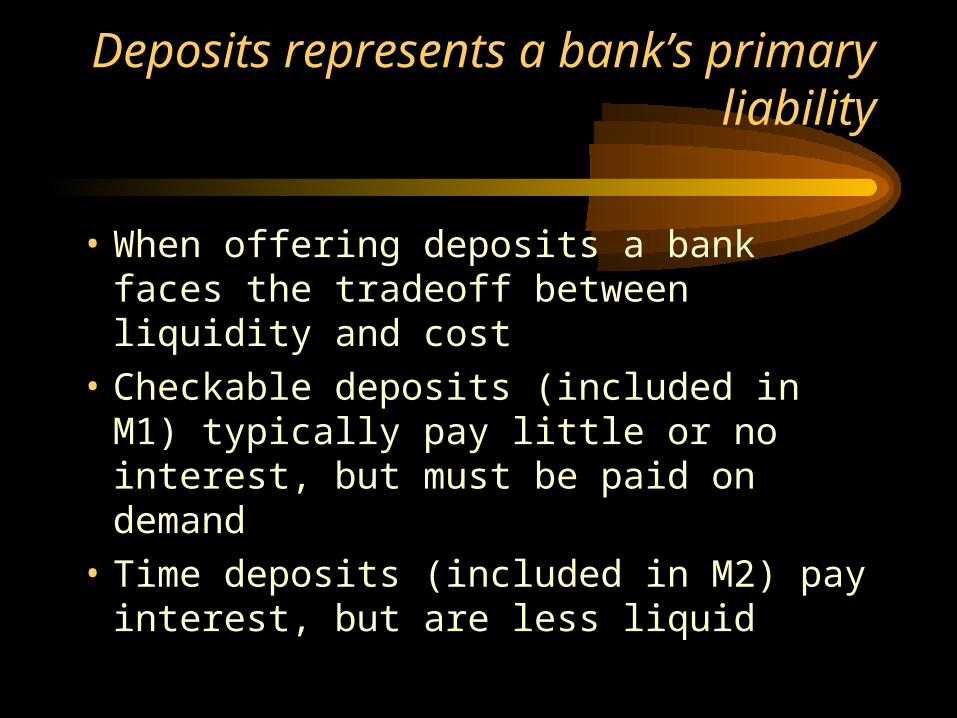

Deposits represents a bank’s primary liability

• When offering deposits a bank faces the tradeoff between liquidity and cost

• Checkable deposits (included in M1) typically pay little or no interest, but must be paid on demand

• Time deposits (included in M2) pay interest, but are less liquid

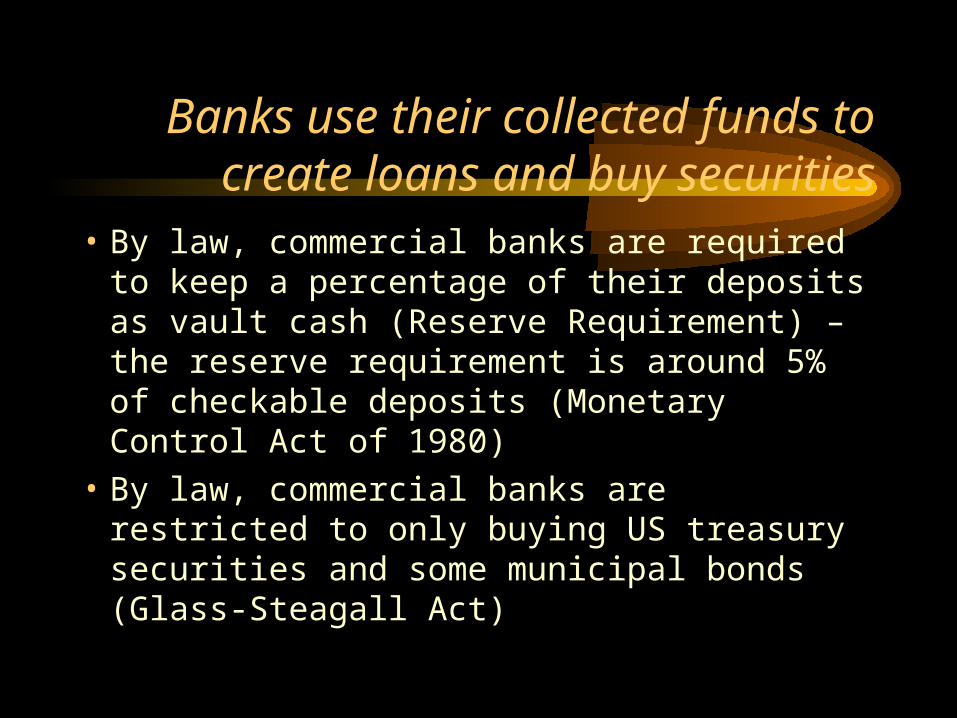

Banks use their collected funds to create loans and buy securities

• By law, commercial banks are required to keep a percentage of their deposits as vault cash (Reserve Requirement) – the reserve requirement is around 5% of checkable deposits (Monetary Control Act of 1980)

• By law, commercial banks are restricted to only buying US treasury securities and some municipal bonds (Glass-Steagall Act)

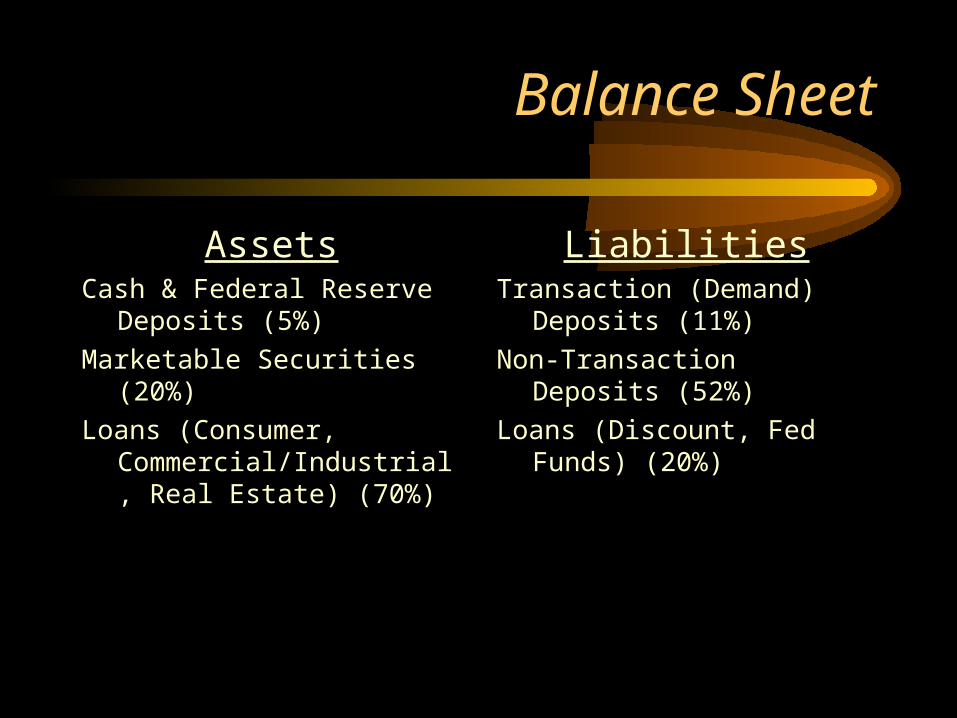

Balance Sheet

AssetsCash & Federal Reserve Deposits

(5%)

Marketable Securities (20%)

Loans (Consumer, Commercial/Industrial, Real Estate) (70%)

LiabilitiesTransaction (Demand) Deposits

(11%)

Non-Transaction Deposits (52%)

Loans (Discount, Fed Funds) (20%)

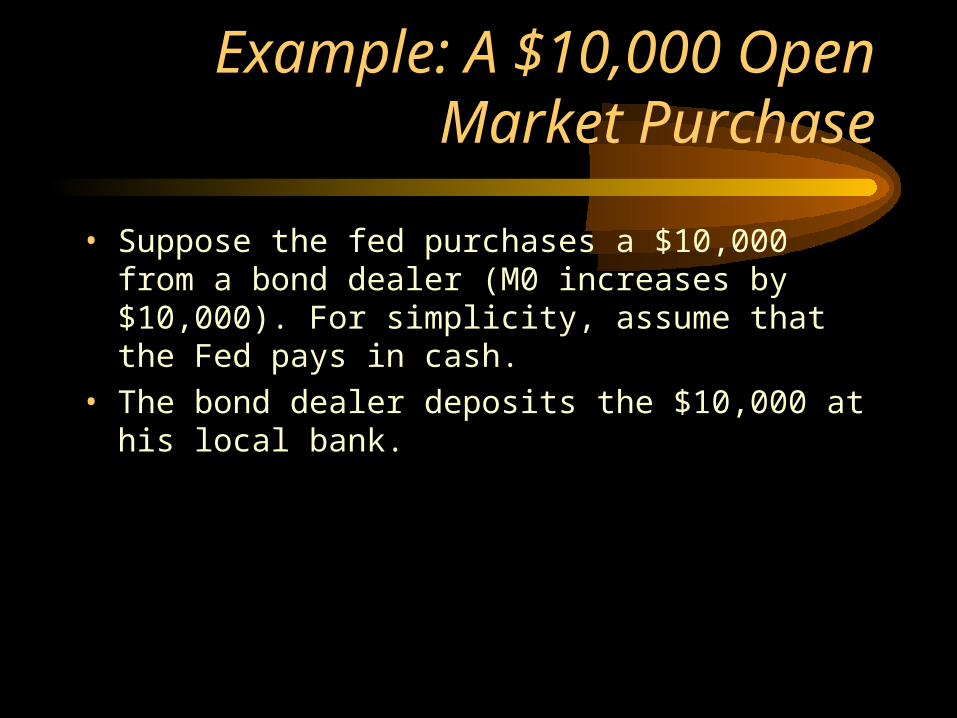

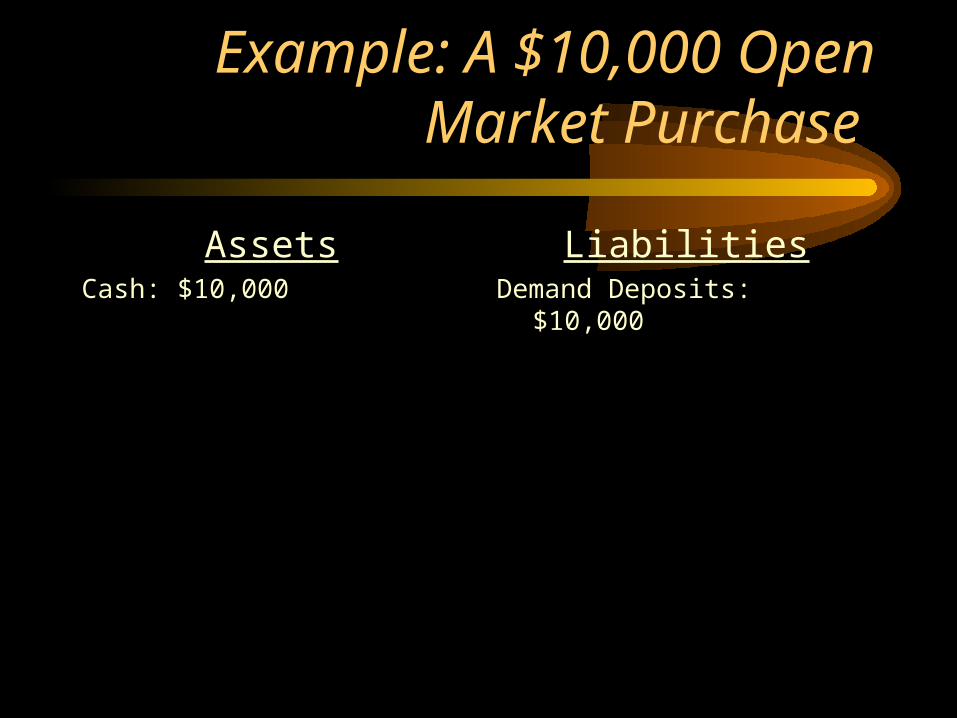

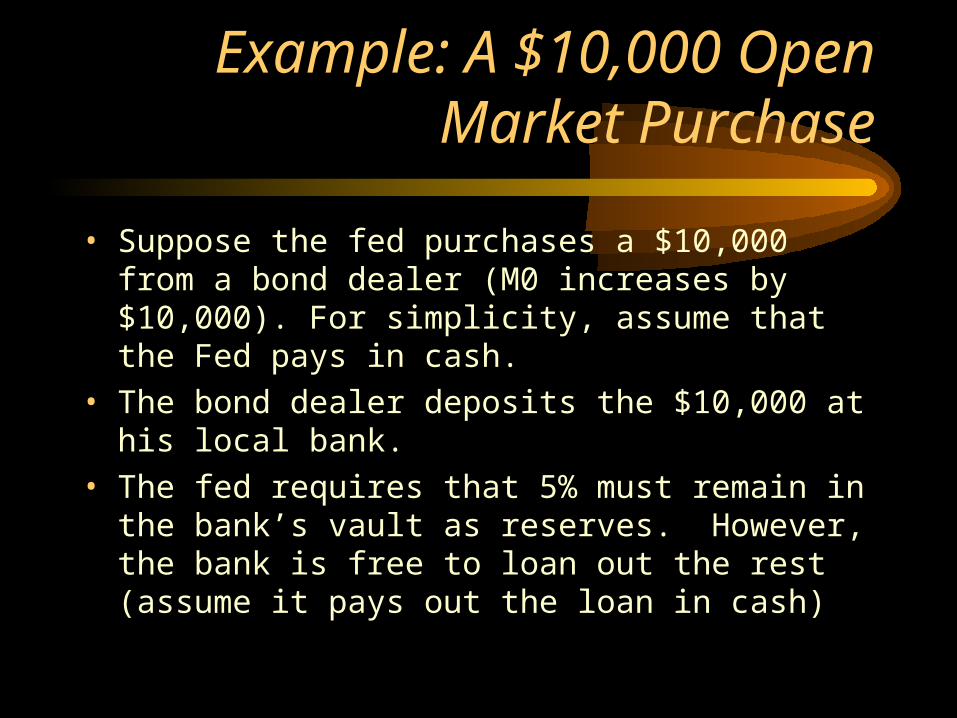

Example: A $10,000 Open Market Purchase

• Suppose the fed purchases a $10,000 from a bond dealer (M0 increases by $10,000). For simplicity, assume that the Fed pays in cash.

Example: A $10,000 Open Market Purchase

• Suppose the fed purchases a $10,000 from a bond dealer (M0 increases by $10,000). For simplicity, assume that the Fed pays in cash.

• The bond dealer deposits the $10,000 at his local bank.

Example: A $10,000 Open Market Purchase

AssetsCash: $10,000

LiabilitiesDemand Deposits: $10,000

Example: A $10,000 Open Market Purchase

• Suppose the fed purchases a $10,000 from a bond dealer (M0 increases by $10,000). For simplicity, assume that the Fed pays in cash.

• The bond dealer deposits the $10,000 at his local bank.

• The fed requires that 5% must remain in the bank’s vault as reserves. However, the bank is free to loan out the rest (assume it pays out the loan in cash)

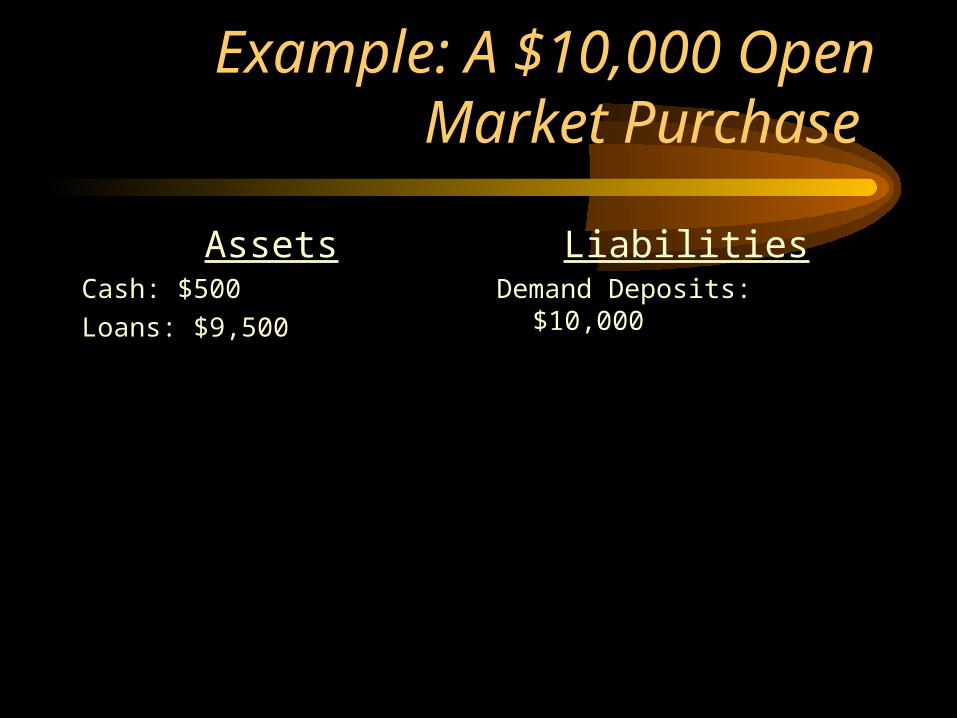

Example: A $10,000 Open Market Purchase

AssetsCash: $500

Loans: $9,500

LiabilitiesDemand Deposits: $10,000

Example: A $10,000 Open Market Purchase

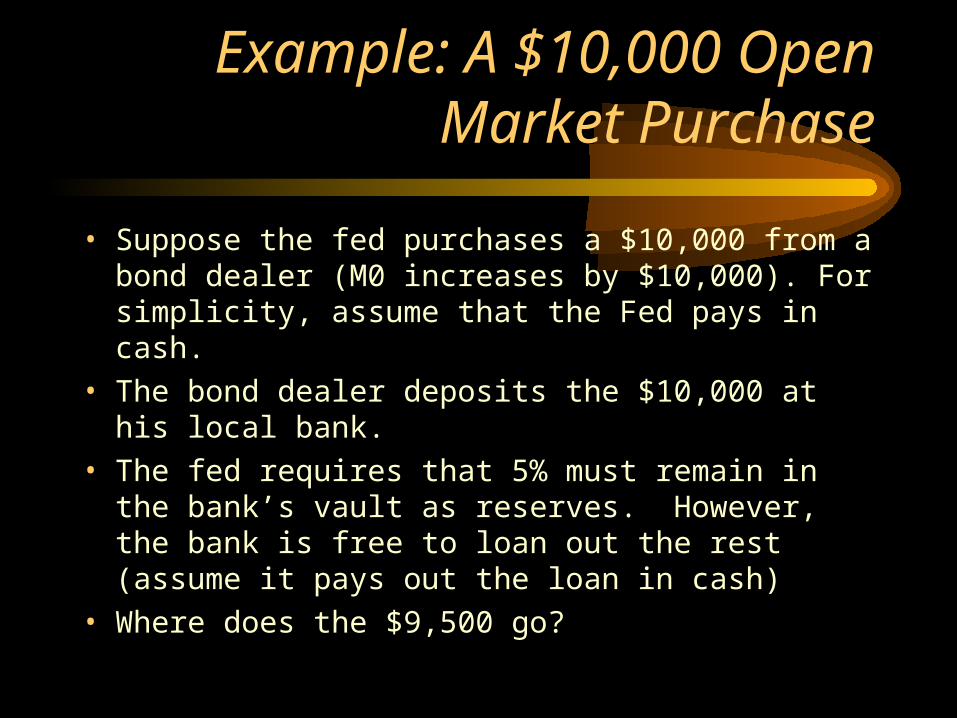

• Suppose the fed purchases a $10,000 from a bond dealer (M0 increases by $10,000). For simplicity, assume that the Fed pays in cash.

• The bond dealer deposits the $10,000 at his local bank.

• The fed requires that 5% must remain in the bank’s vault as reserves. However, the bank is free to loan out the rest (assume it pays out the loan in cash)

• Where does the $9,500 go?

Example: A $10,000 Open Market Purchase

• Suppose the fed purchases a $10,000 from a bond dealer (M0 increases by $10,000). For simplicity, assume that the Fed pays in cash.

• The bond dealer deposits the $10,000 at his local bank.

• The fed requires that 5% must remain in the bank’s vault as reserves. However, the bank is free to loan out the rest (assume it pays out the loan in cash)

• Where does the $9,500 go?

• It ends up in another bank!

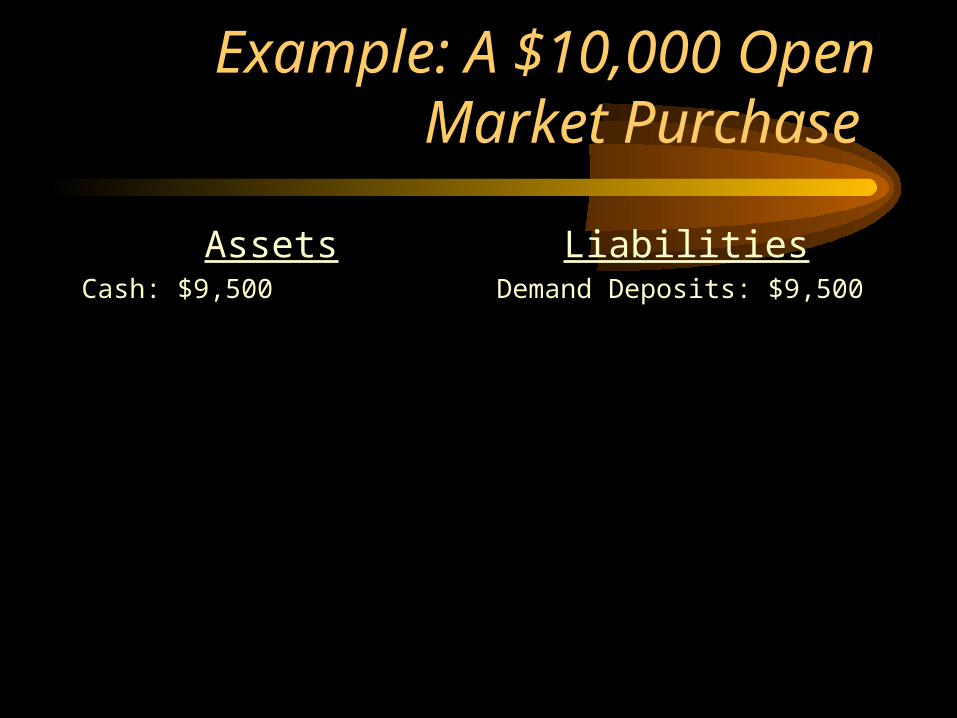

Example: A $10,000 Open Market Purchase

AssetsCash: $9,500

LiabilitiesDemand Deposits: $9,500

Example: A $10,000 Open Market Purchase

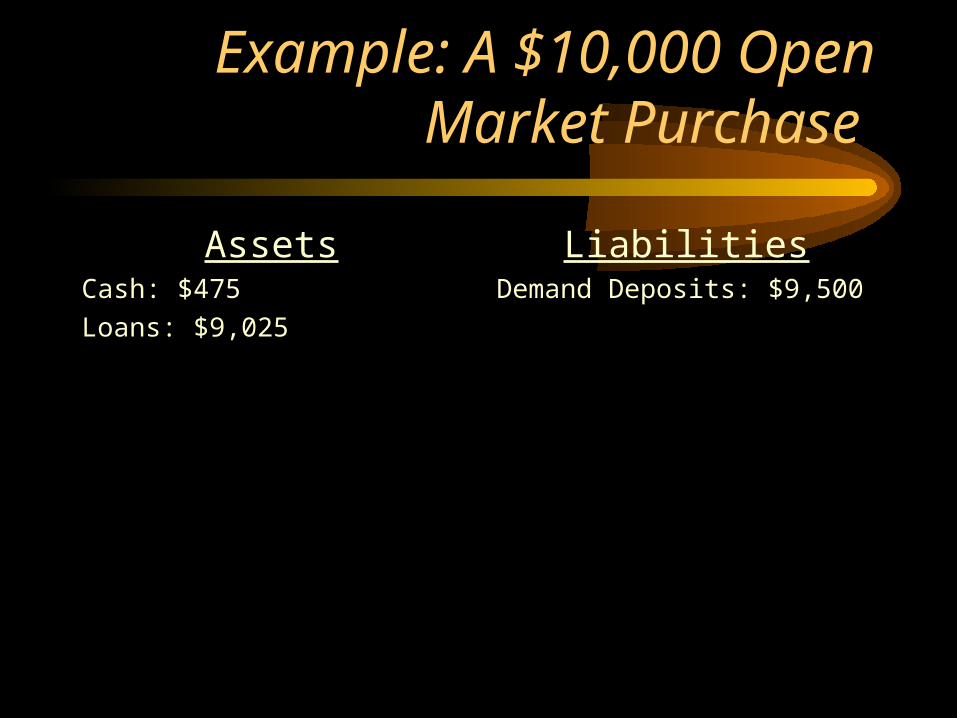

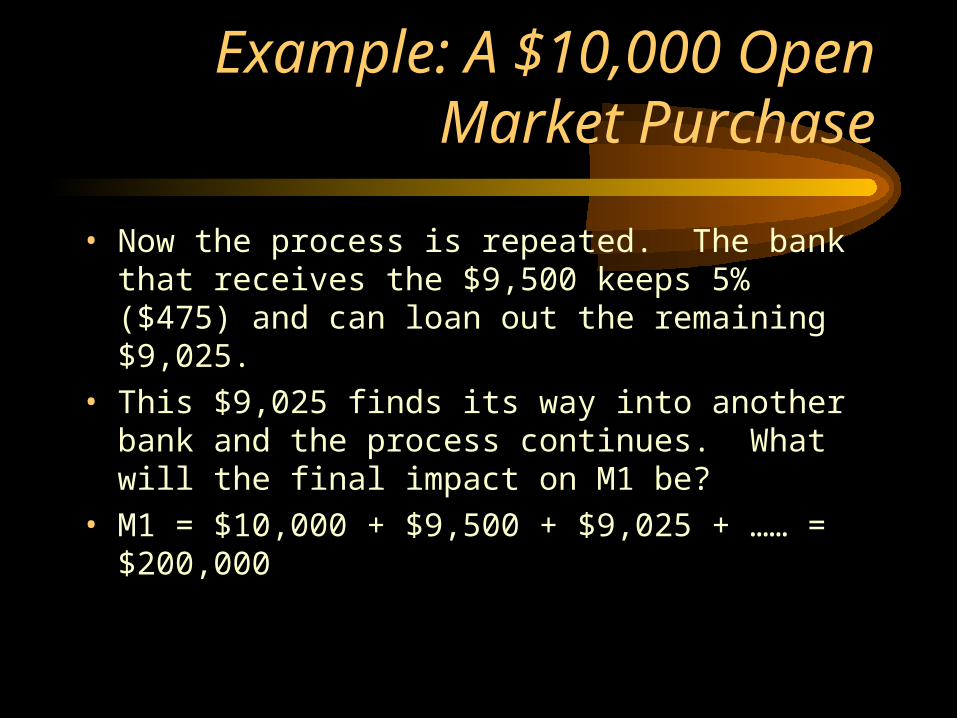

• Now the process is repeated. The bank that receives the $9,500 keeps 5% ($475) and can loan out the remaining $9,025.

Example: A $10,000 Open Market Purchase

AssetsCash: $475

Loans: $9,025

LiabilitiesDemand Deposits: $9,500

Example: A $10,000 Open Market Purchase

• Now the process is repeated. The bank that receives the $9,500 keeps 5% ($475) and can loan out the remaining $9,025.

• This $9,025 finds its way into another bank and the process continues. What will the final impact on M1 be?

Example: A $10,000 Open Market Purchase

• Now the process is repeated. The bank that receives the $9,500 keeps 5% ($475) and can loan out the remaining $9,025.

• This $9,025 finds its way into another bank and the process continues. What will the final impact on M1 be?

• M1 = $10,000 + $9,500 + $9,025 + …… = $200,000

Example: A $10,000 Open Market Purchase

• Now the process is repeated. The bank that receives the $9,500 keeps 5% ($475) and can loan out the remaining $9,025.

• This $9,025 finds its way into another bank and the process continues. What will the final impact on M1 be?

• M1 = $10,000 + $9,500 + $9,025 + …… = $200,000

• (Change in M1)/(Change in M0) = money multiplier = 20 = 1/Reserve Requirement

Example: A $10,000 Open Market Purchase

• Now the process is repeated. The bank that receives the $9,500 keeps 5% ($475) and can loan out the remaining $9,025.

• This $9,025 finds its way into another bank and the process continues. What will the final impact on M1 be?

• M1 = $10,000 + $9,500 + $9,025 + …… = $200,000• (Change in M1)/(Change in M0) = money multiplier = 20

= 1/Reserve Requirement (1/.05)• Note that this scenario assumes that consumers never

withdraw any cash. Suppose that the average consumer likes to keep 10% of their deposits as cash.

Example: A $10,000 Open Market Purchase

• Of the initial $10,000 bond purchase, only $9,000 finds its way into a bank.

• The $9,000 deposit will generate $450 in reserves and $8,550 in new loans.

• Of the $8,550 in loans, $7,695 is deposited, and so on

• M1 = $9,000 + $8,550 + ….. = $73,000.• M1/M0 = multiplier = 7.3 = (1+cd)/(cd + rr)• cd (cash/deposits ratio) = .1 , rr (reserve req) = .05

The Money Multiplier

• The money multiplier is currently around 2.5 (a $1 increase in the monetary base increases M1 by $2.50)

• The size of the multiplier is influenced by – Consumer behavior: If consumers hold onto more cash (cash to

deposits ratio increases) the multiplier falls.

– Commercial banks: Many banks choose to hold excess reserves (reserves above the 5% requirement). As excess reserves increase, the multiplier decreases.

– The Federal Reserve: The federal reserve can restrict loan creation directly by raising the reserve requirement or indirectly by increasing the discount rate (this raises the bank’s cost of capital)

Fed Instruments and Money Supply

• If the federal reserve wishes to increase the M1 money supply, it has three choices:– An open market purchase of securities– A decrease in the reserve requirement– A decrease in the discount rate

The Discount Rate vs. the Federal Funds Rate

• The discount rate is the interest rate charged by the Fed on loans to commercial banks.

– The discount rate is a non-market rate. It is a policy instrument determined by the Fed.

– Current policy states that the discount rate is chosen to be approximately 100 basis points above the Federal Funds rate.

The Discount Rate vs. the Federal Funds Rate

• The discount rate is the interest rate charged by the Fed on loans to commercial banks.

– The discount rate is a non-market rate. It is a policy instrument determined by the Fed.

– Current policy states that the discount rate is chosen to be approximately 100 basis points above the Federal Funds rate.

• The federal funds rate is the interest charged by commercial banks for very short term (usually overnight) loans to other commercial banks.

– The Fed Funds rate is a market rate of interest. Therefore, it is determined by supply and demand, but is heavily influenced by the Fed.

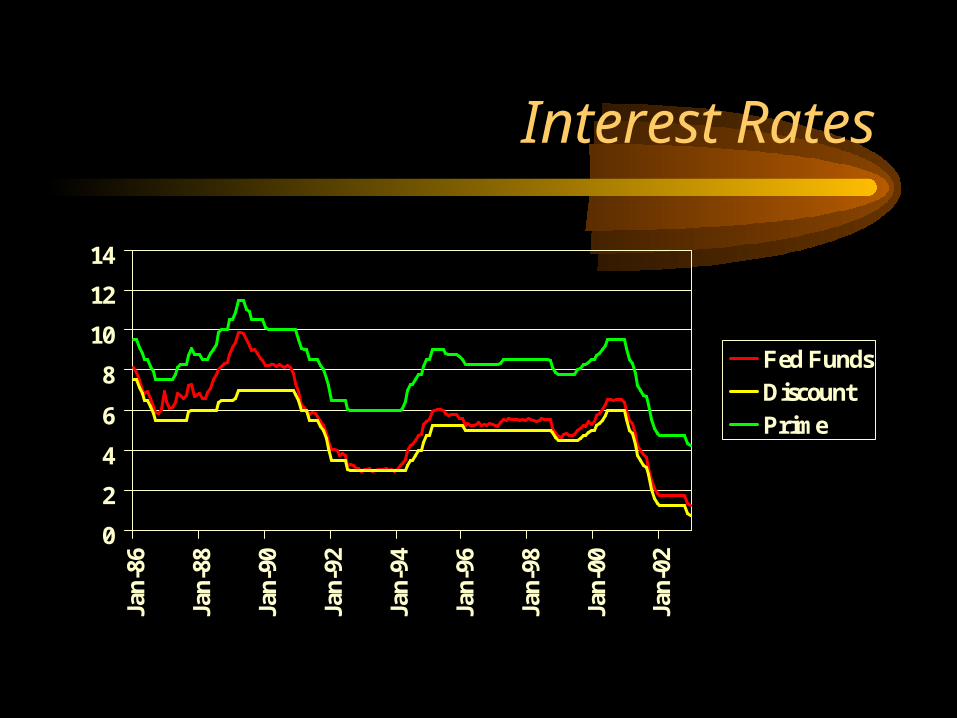

Interest Rates

0

2

4

6

8

10

12

14

Jan-

86

Jan-

88

Jan-

90

Jan-

92

Jan-

94

Jan-

96

Jan-

98

Jan-

00

Jan-

02

Fed FundsDiscountPrime

Intermediate Targets

• An intermediate target is a variable not controlled by the fed, but heavily and predictably influenced by the Fed. Targets are used to quantify fed policy decisions (by how much will money supply be increased/decreased)

Intermediate Targets

• An intermediate target is a variable not controlled by the fed, but heavily and predictably influenced by the Fed. Targets are used to quantify fed policy decisions (by how much will money supply be increased/decreased)

• We know that increasing the money supply lowers interest rates. Therefore, an expansionary policy can be stated two ways:– (Money target) We will increase the M1 money supply by 5%.

– (Interest rate target) We will increase M1 by enough to lower the federal funds rate by 50 basis points.

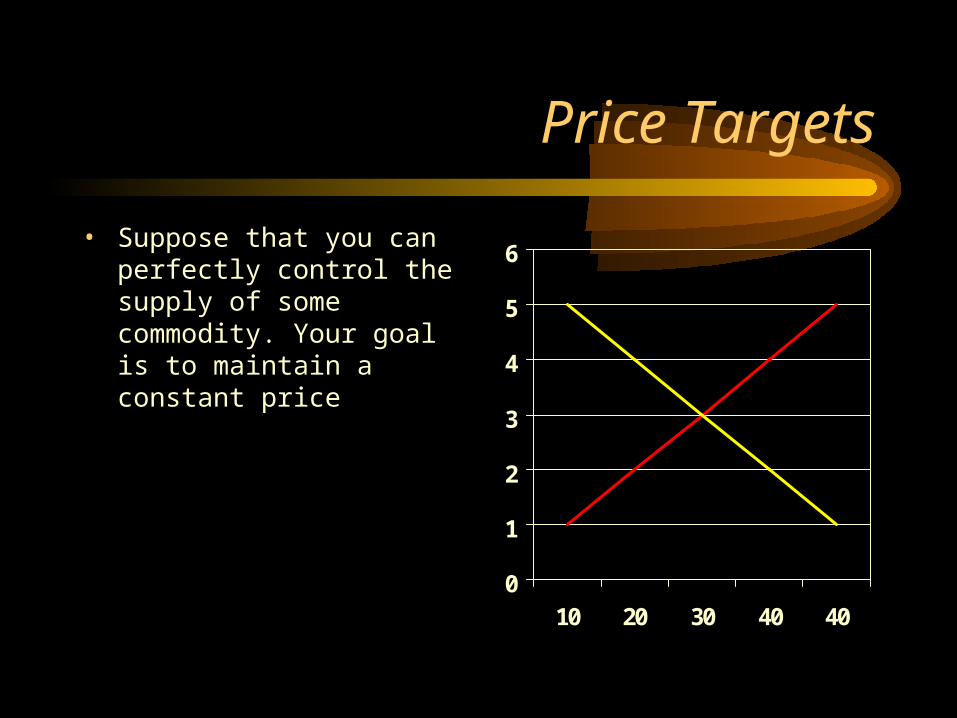

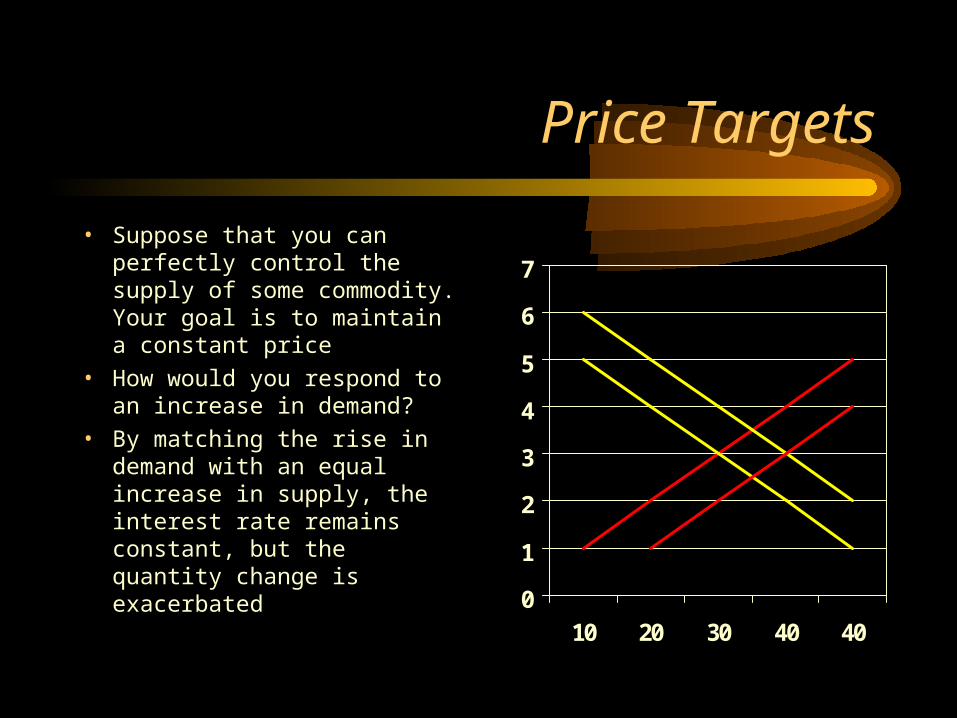

Price Targets

• Suppose that you can perfectly control the supply of some commodity. Your goal is to maintain a constant price

0

1

2

3

4

5

6

10 20 30 40 40

Price Targets

• Suppose that you can perfectly control the supply of some commodity. Your goal is to maintain a constant price

• How would you respond to an increase in demand?

0

1

2

3

4

5

6

7

10 20 30 40 40

Price Targets

• Suppose that you can perfectly control the supply of some commodity. Your goal is to maintain a constant price

• How would you respond to an increase in demand?

• By matching the rise in demand with an equal increase in supply, the interest rate remains constant, but the quantity change is exacerbated

0

1

2

3

4

5

6

7

10 20 30 40 40

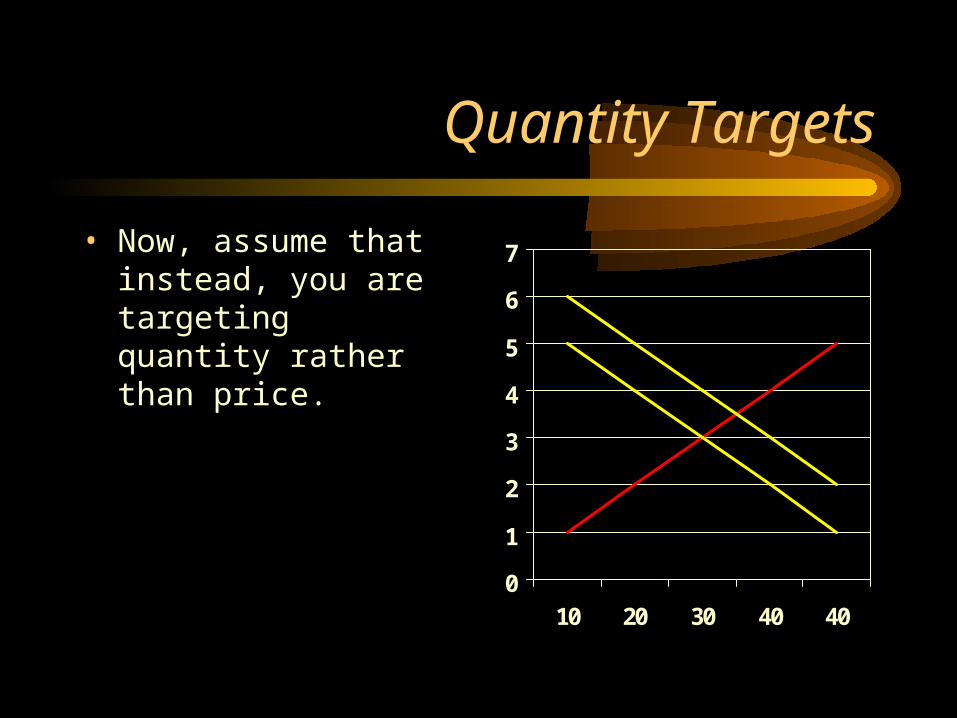

Quantity Targets

• Now, assume that instead, you are targeting quantity rather than price.

0

1

2

3

4

5

6

7

10 20 30 40 40

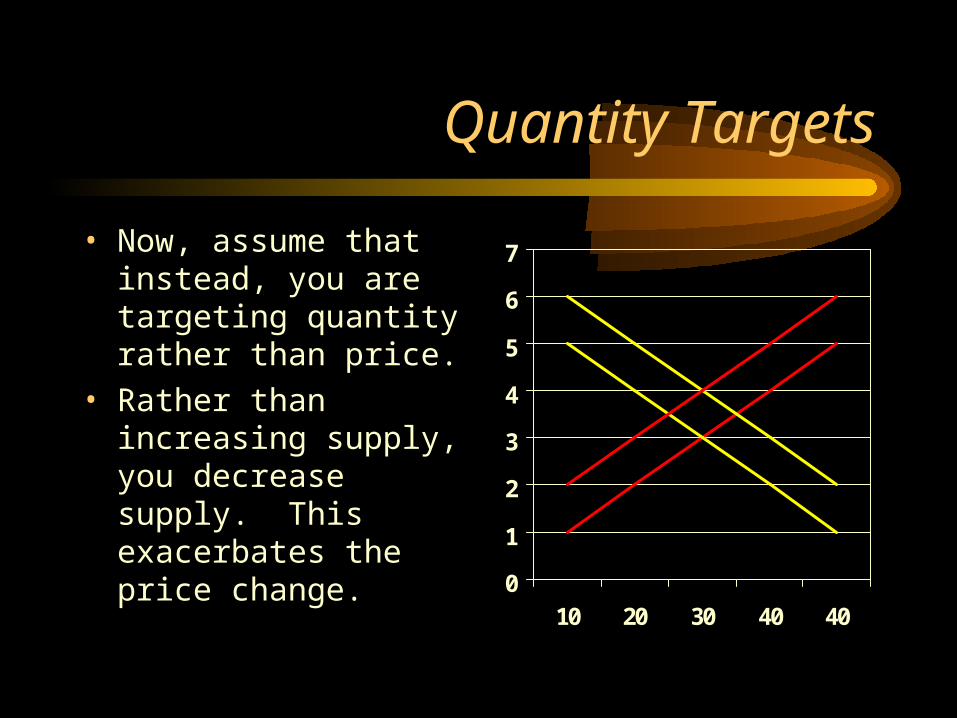

Quantity Targets

• Now, assume that instead, you are targeting quantity rather than price.

• Rather than increasing supply, you decrease supply. This exacerbates the price change.

0

1

2

3

4

5

6

7

10 20 30 40 40

Intermediate Targets

• In 1975, the Federal Reserve announced a change in Fed policy. Rather than targeting interest rates, the Fed would begin targeting growth rates of M1, M2, and M3.

Intermediate Targets

• In 1975, the Federal Reserve announced a change in Fed policy. Rather than targeting interest rates, the Fed would begin targeting growth rates of M1, M2, and M3.

• Due to significant financial innovation in the late 70’s, money demand became very unstable and unpredictable. Maintaining constant monetary aggregates created wildly fluctuating interest rates.

Interest Rates: 1970 – 1985

0

5

10

15

20

25

Jan-

70

Jan-

72

Jan-

74

Jan-

76

Jan-

78

Jan-

80

Jan-

82

Jan-

84

Fed FundsDiscountPrime

Intermediate Targets

• In 1975, the Federal Reserve announced a change in Fed policy. Rather than targeting interest rates, the Fed would begin targeting growth rates of M1, M2, and M3.

• Due to significant financial innovation in the late 70’s, money demand became very unstable and unpredictable. Maintaining constant monetary aggregates created wildly fluctuating interest rates.

• Money Targets were de-emphasized in 1982 and eliminated completely by 1993.

• Currently, the Fed uses an interest rate target (Fed Funds)

Rules vs. Discretion

• A monetary policy rule is a system by which the central bank’s actions are defined in advance. – Simple (Non-Contingent) Rules

– Contingent Rules

Rules vs. Discretion

• A monetary policy rule is a system by which the central bank’s actions are defined in advance. – Simple (Non-Contingent) Rules

– Contingent Rules

• The Federal Reserve currently operates under a discretionary system.

Rules vs. Discretion

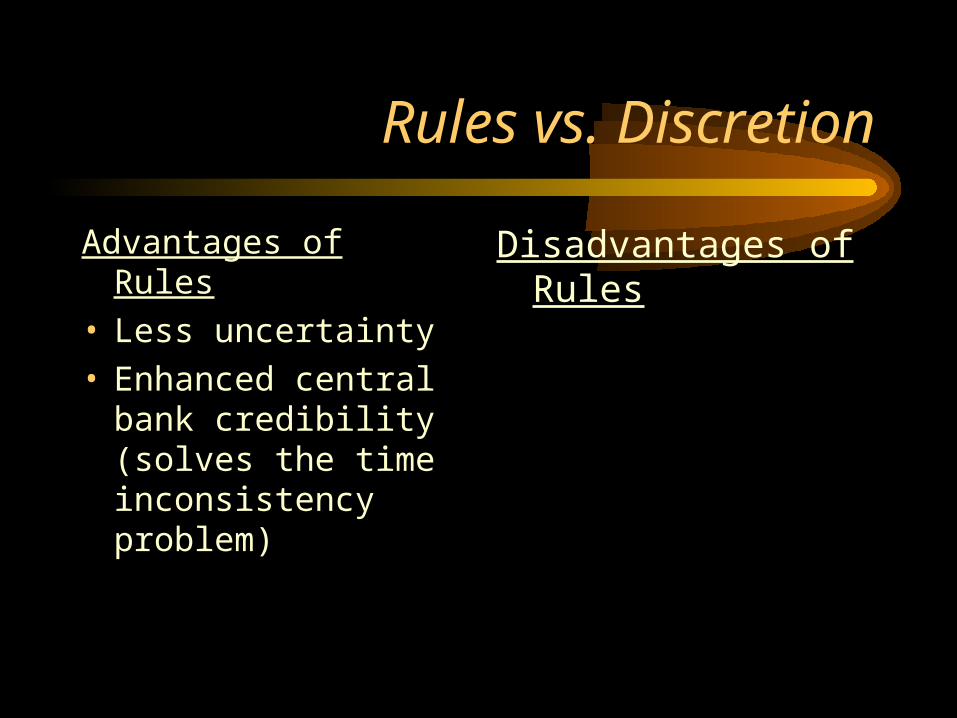

Advantages of Rules Disadvantages of Rules

Rules vs. Discretion

Advantages of Rules• Less uncertainty• Enhanced central bank

credibility (solves the time inconsistency problem)

Disadvantages of Rules

Rules vs. Discretion

Advantages of Rules• Less uncertainty• Enhanced central bank

credibility (solves the time inconsistency problem)

Disadvantages of Rules• Less flexibility to deal

with new situations• Rules can be subjected

to speculative attacks

Monetary Policy in the US

• Prior to 1971, the US followed a gold standard.

Monetary Policy in the US

• Prior to 1971, the US followed a gold standard.

• Under this system, the price of gold was set at $20.67/oz (Roosevelt raised the price to $35 in 1934)

• The US Government was required to buy or sell gold from anyone at the official gold price (convertibility)

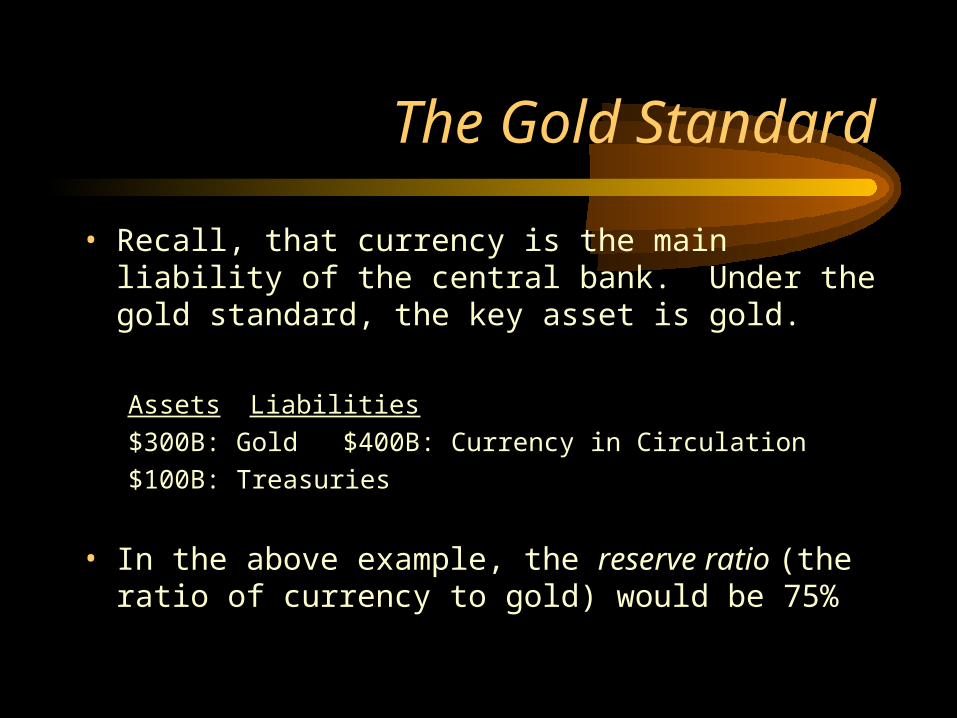

The Gold Standard

• Recall, that currency is the main liability of the central bank. Under the gold standard, the key asset is gold.

Assets Liabilities

$300B: Gold $400B: Currency in Circulation

$100B: Treasuries

• In the above example, the reserve ratio (the ratio of currency to gold) would be 75%

The Gold Standard

• Recall, that currency is the main liability of the central bank. Under the gold standard, the key asset is gold.

Assets Liabilities$300B: Gold $400B: Currency in Circulation$100B: Treasuries

• In the above example, the reserve ratio (the ratio of currency to gold) would be 75%

• To maintain the gold standard, the reserve ratio must stay “sufficiently high”

The Gold Standard

• The gold standard restricts the supply of money to be tied to the supply of gold. This promotes a stable long run price level.

The Gold Standard

• The gold standard restricts the supply of money to be tied to the supply of gold. This promotes a stable long run price level.

• However, in the short run, the gold standard created significant instability by tying monetary policy to fluctuations in the gold market.

Example: A rise in the supply of gold

• Suppose that a new gold deposit was discovered.

0

10

20

30

40

50

60

10 20 30 40 50

Example: A rise in the supply of gold

• Suppose that a new gold deposit was discovered.

• The increase in supply puts downward pressure on gold prices

0

10

20

30

40

50

60

10 20 30 40 50

Example: A rise in the supply of gold

• Suppose that a new gold deposit was discovered.

• The increase in supply puts downward pressure on gold prices

• As people buy gold in private markets and sell to the central bank, the money supply expands

0

10

20

30

40

50

60

10 20 30 40 50

Example: A rise in the demand for gold

• Suppose that demand for gold increases. Rising gold prices cause people to buy gold from the central bank.

0

10

20

30

40

50

60

70

10 20 30 40 50

Example: A rise in the demand for gold

• Suppose that demand for gold increases. Rising gold prices cause people to buy gold from the central bank.

• This forces a contraction in the money supply.

0

10

20

30

40

50

60

70

10 20 30 40 50

Current Monetary Policy

• Currently, the Federal Reserve follows a discretionary monetary policy

Current Monetary Policy

• Currently, the Federal Reserve follows a discretionary monetary policy– Interest Rate (Fed Funds) Targets– Primary Goal: Maintain a full employment, low

inflation economy

Current Monetary Policy

• Currently, the Federal Reserve follows a discretionary monetary policy– Interest Rate (Fed Funds) Targets– Primary Goal: Maintain a full employment, low

inflation economy

• This type of monetary policy can be summarized by a Taylor rule

The Taylor Rule

• The Taylor rule explicitly models the two fed goals:

FF = 2% + (Inflation) + .5(Output Gap) + .5(Inflation – 2%)

The Taylor Rule

• The Taylor rule explicitly models the two fed goals:

FF = 2% + (Inflation) + .5(Output Gap) + .5(Inflation – 2%)

An economy with full employment and a 2% annual inflation rate (the fed’s goal) would have a Fed Funds rate equal to 4%.

Using Okun’s law, we can write the Taylor rule in terms of unemployment (1% cyclical unemployment = 2.5% output gap)

FF = 2% + (Inflation) + 1.25(Unemployment – 5%) + .5(Inflation – 2%)

The Taylor Rule

• The Taylor rule explicitly models the two fed goals:

FF = 2% + (Inflation) - 1.25(Unemployment – 5%) + .5(Inflation – 2%)

Ex) Currently, Unemployment is 6% and core inflation is 1%.

Target FF = 2% + 1% - 1.25(1.0) - .5(1.0) = 1.25%

Interest Rate Targeting

• To Target the interest rate, the central bank must correctly identify the nature of market disturbances and then act accordingly

Interest Rate Targeting

• To Target the interest rate, the central bank must correctly identify the nature of market disturbances and then act accordingly– Capital Market (IS)– Labor Market (FE)– Money Market (LM)

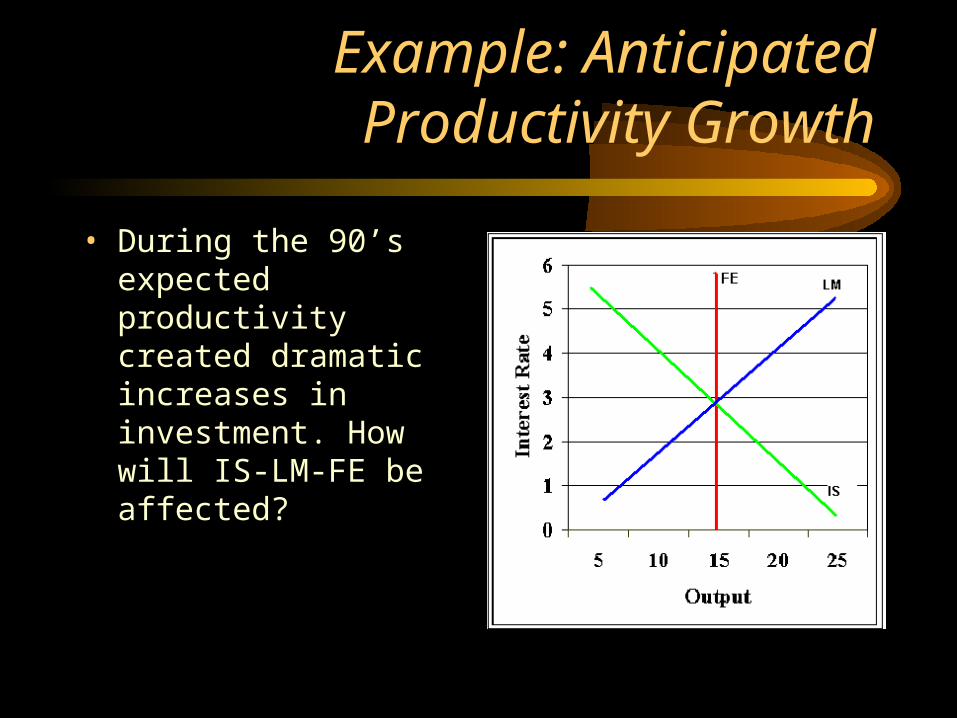

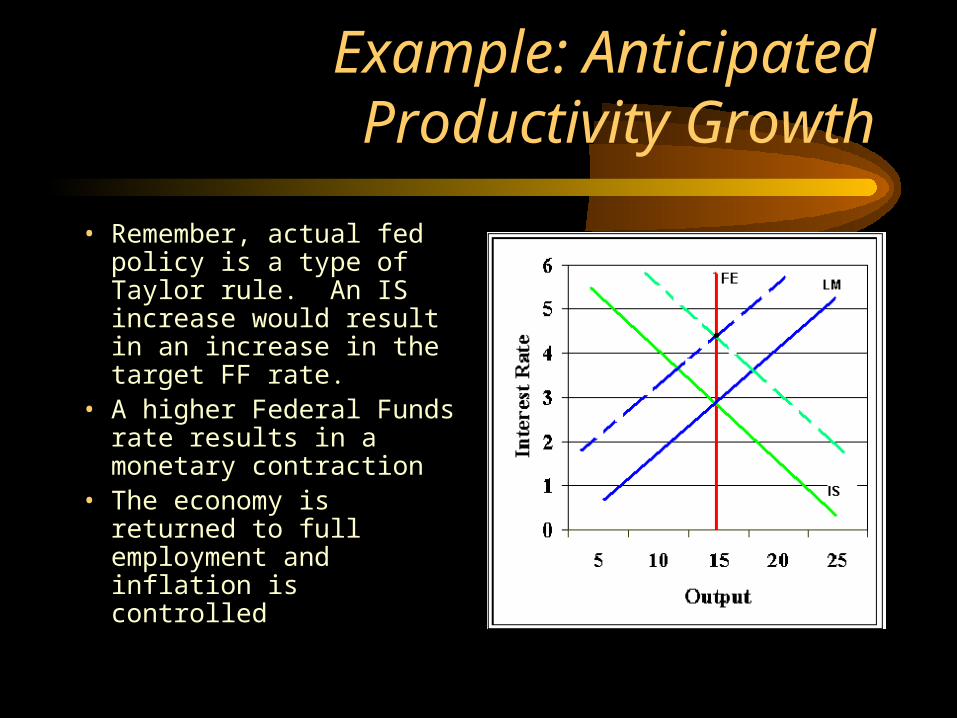

Example: Anticipated Productivity Growth

• During the 90’s expected productivity created dramatic increases in investment. How will IS-LM-FE be affected?

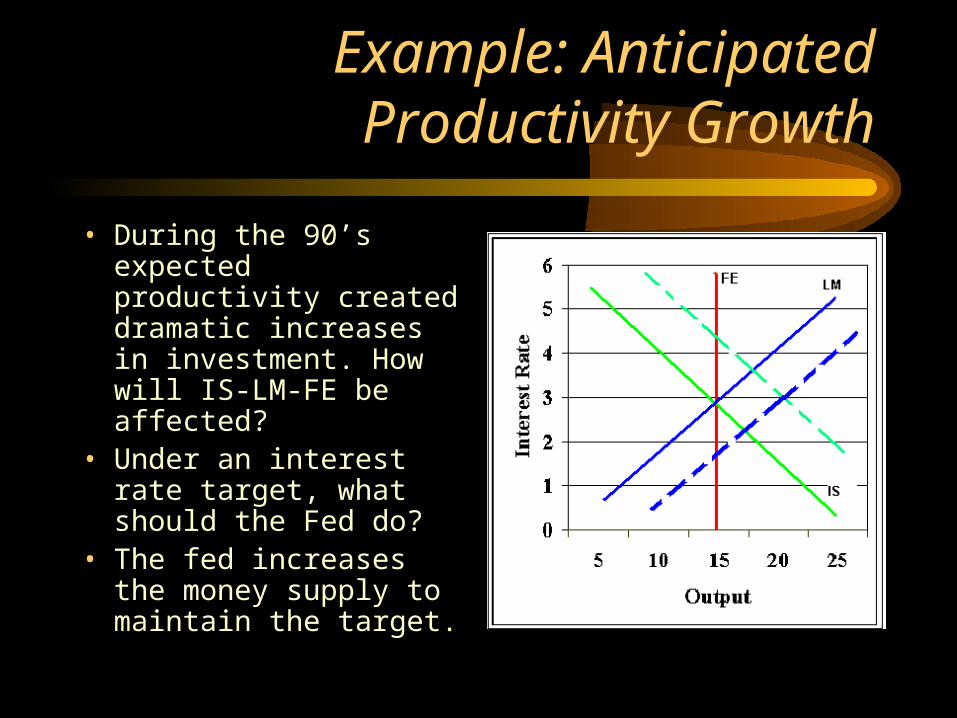

Example: Anticipated Productivity Growth

• During the 90’s expected productivity created dramatic increases in investment. How will IS-LM-FE be affected?

• Under an interest rate target, what should the Fed do?

Example: Anticipated Productivity Growth

• During the 90’s expected productivity created dramatic increases in investment. How will IS-LM-FE be affected?

• Under an interest rate target, what should the Fed do?

• The fed increases the money supply to maintain the target.

Example: Anticipated Productivity Growth

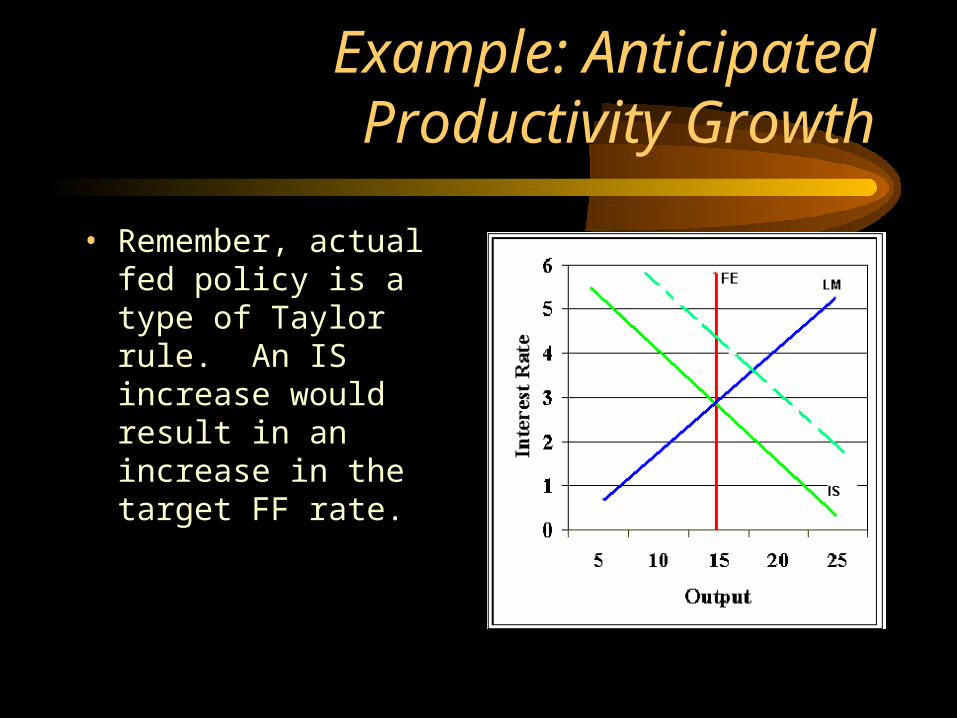

• Remember, actual fed policy is a type of Taylor rule. An IS increase would result in an increase in the target FF rate.

Example: Anticipated Productivity Growth

• Remember, actual fed policy is a type of Taylor rule. An IS increase would result in an increase in the target FF rate.

• A higher Federal Funds rate results in a monetary contraction

• The economy is returned to full employment and inflation is controlled

Monetary Policy: 1995 - 2000

22.5

33.5

44.5

55.5

66.5

7

Jan-9

4

Jul-9

4

Jan-9

5

Jul-9

5

Jan-9

6

Jul-9

6

Jan-9

7

Jul-9

7

Jan-9

8

Jul-9

8

Jan-9

9

Jul-9

9

Jan-0

0

Fed FundsDiscount

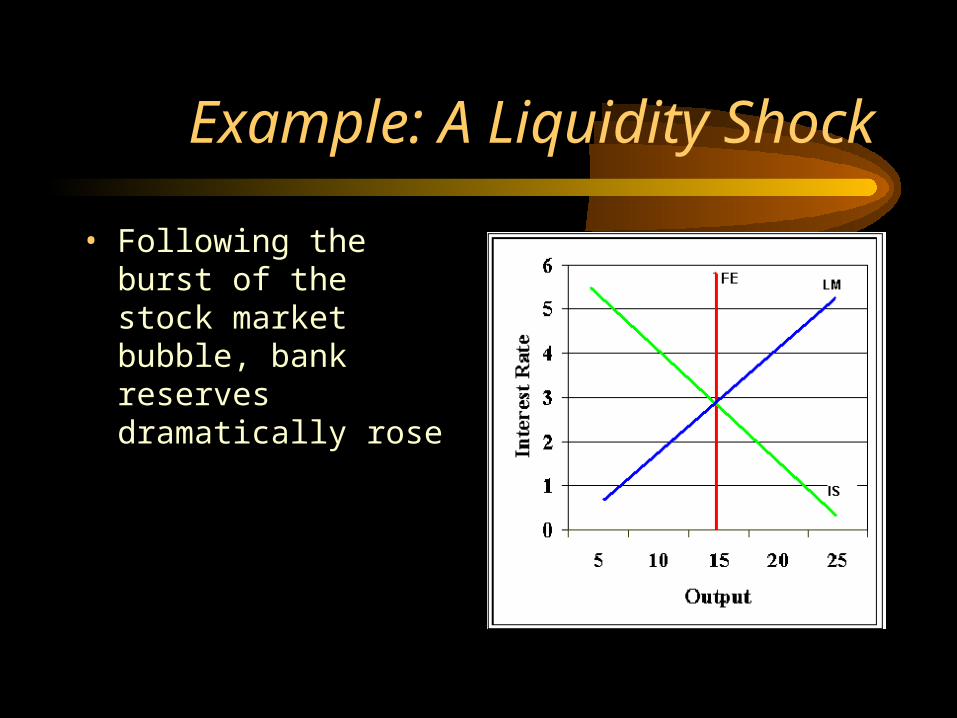

Example: A Liquidity Shock

• Following the burst of the stock market bubble, bank reserves dramatically rose

US Bank Reserves

Example: A Liquidity Shock

• Following the burst of the stock market bubble, bank reserves dramatically rose

• A rise in reserves lowers the multiplier which, in turn lowers M1

• An increase in the money supply is required to prevent a recession and deflation.

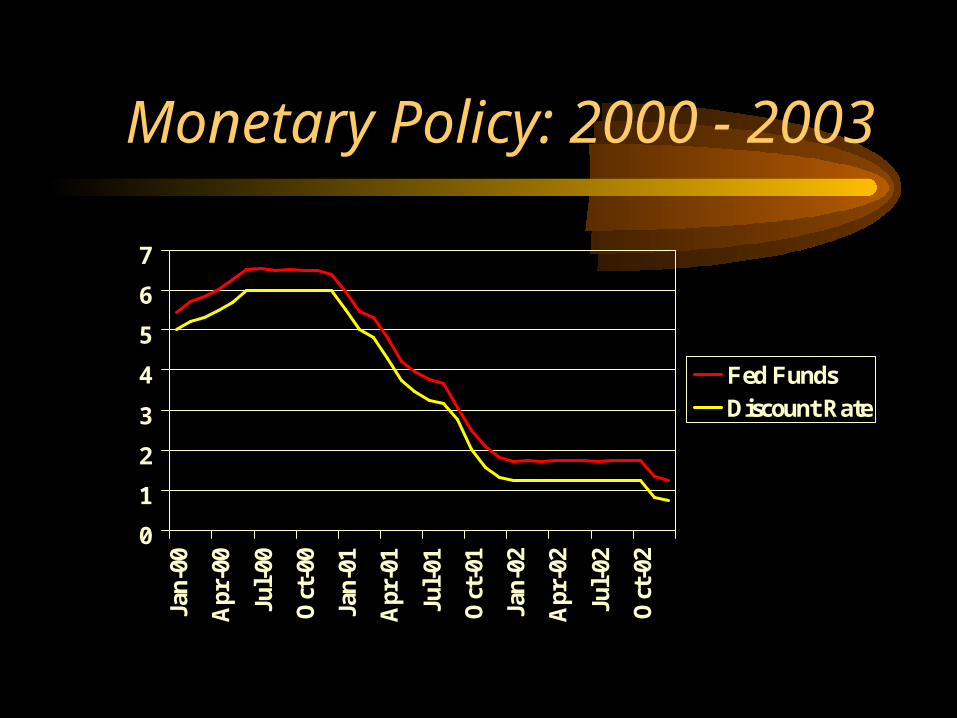

Monetary Policy: 2000 - 2003

0

1

2

3

4

5

6

7

Jan-

00

Apr

-00

Jul-

00

Oct

-00

Jan-

01

Apr

-01

Jul-

01

Oct

-01

Jan-

02

Apr

-02

Jul-

02

Oct

-02

Fed FundsDiscount Rate

Problems

• Obviously, we can’t observe IS, LM, FE curves. Instead, we have to look at the data and guess at the underlying cause.

• The outside lag (the amount of time for a policy to impact the economy) is “long and variable”