Embed Size (px)

Citation preview

Monetary policy implications for an oil-exportingeconomy of lower long-run international oil prices

Jesús Bejarano Franz Hamann Diego Rodríguez

Banco de la República

BIS CCA Research Network, Mexico 2015

Banco de la República Oil and Macro BIS CCA Conference 1 / 36

Outline

The policy question and the problem

Small scale Bewley ModelsSingle-good EconomyTwo-good EconomyOil Exporting Economy

Monetary policy modelsSimple New KeynesianSectoral Financial AcceleratorSectoral financial accelerator model

Final Remarks

Banco de la República Oil and Macro BIS CCA Conference 2 / 36

Motivation

Banco de la República Oil and Macro BIS CCA Conference 3 / 36

The question and the problem

I Small, open and commodity exporting economies are subject to largeand sudden commodity price swings.

I How does monetary policy in an oil-exporting economy cope with asudden and long-lasting reversal of international oil prices?

I We conduct a quantitative assessment of the impact of an unexpected

permanent change in oil prices in an oil-exporting economy and deriveits monetary policy implications.

I Our approach: first, understand the consequences on the economy’sNFA, usually assumed exogenous by many models which rely onapproximation solution methods. Then, couple it with monetary policymodels.

Banco de la República Oil and Macro BIS CCA Conference 4 / 36

The question and the problem

I Small, open and commodity exporting economies are subject to largeand sudden commodity price swings.

I How does monetary policy in an oil-exporting economy cope with asudden and long-lasting reversal of international oil prices?

I We conduct a quantitative assessment of the impact of an unexpected

permanent change in oil prices in an oil-exporting economy and deriveits monetary policy implications.

I Our approach: first, understand the consequences on the economy’sNFA, usually assumed exogenous by many models which rely onapproximation solution methods. Then, couple it with monetary policymodels.

Banco de la República Oil and Macro BIS CCA Conference 4 / 36

The question and the problem

I Small, open and commodity exporting economies are subject to largeand sudden commodity price swings.

I How does monetary policy in an oil-exporting economy cope with asudden and long-lasting reversal of international oil prices?

I We conduct a quantitative assessment of the impact of an unexpected

permanent change in oil prices in an oil-exporting economy and deriveits monetary policy implications.

I Our approach: first, understand the consequences on the economy’sNFA, usually assumed exogenous by many models which rely onapproximation solution methods. Then, couple it with monetary policymodels.

Banco de la República Oil and Macro BIS CCA Conference 4 / 36

The question and the problem

I Small, open and commodity exporting economies are subject to largeand sudden commodity price swings.

I How does monetary policy in an oil-exporting economy cope with asudden and long-lasting reversal of international oil prices?

I We conduct a quantitative assessment of the impact of an unexpected

permanent change in oil prices in an oil-exporting economy and deriveits monetary policy implications.

I Our approach: first, understand the consequences on the economy’sNFA, usually assumed exogenous by many models which rely onapproximation solution methods. Then, couple it with monetary policymodels.

Banco de la República Oil and Macro BIS CCA Conference 4 / 36

Bewley Endowment

Outline

The policy question and the problem

Small scale Bewley ModelsSingle-good EconomyTwo-good EconomyOil Exporting Economy

Monetary policy modelsSimple New KeynesianSectoral Financial AcceleratorSectoral financial accelerator model

Final Remarks

Banco de la República Oil and Macro BIS CCA Conference 5 / 36

Bewley Endowment

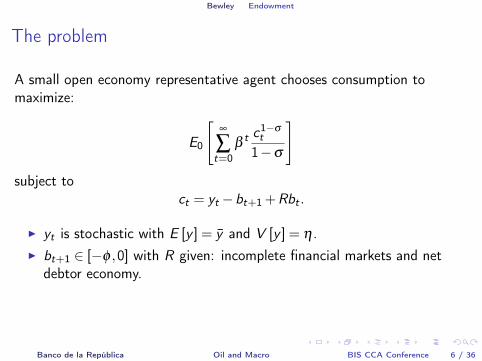

The problem

A small open economy representative agent chooses consumption tomaximize:

E

0

"•

Ât=0

b t

c

1�st

1�s

#

subject toc

t

= y

t

�b

t+1

+Rb

t

.

Iy

t

is stochastic with E [y ] = y and V [y ] = h .

Ib

t+1

2 [�f ,0] with R given: incomplete financial markets and netdebtor economy.

I If bR < 1 then, b has a LR distribution (PS/BAH model).

Banco de la República Oil and Macro BIS CCA Conference 6 / 36

Bewley Endowment

The problem

A small open economy representative agent chooses consumption tomaximize:

E

0

"•

Ât=0

b t

c

1�st

1�s

#

subject toc

t

= y

t

�b

t+1

+Rb

t

.

Iy

t

is stochastic with E [y ] = y and V [y ] = h .I

b

t+1

2 [�f ,0] with R given: incomplete financial markets and netdebtor economy.

I If bR < 1 then, b has a LR distribution (PS/BAH model).

Banco de la República Oil and Macro BIS CCA Conference 6 / 36

Bewley Endowment

The problem

A small open economy representative agent chooses consumption tomaximize:

E

0

"•

Ât=0

b t

c

1�st

1�s

#

subject toc

t

= y

t

�b

t+1

+Rb

t

.

Iy

t

is stochastic with E [y ] = y and V [y ] = h .I

b

t+1

2 [�f ,0] with R given: incomplete financial markets and netdebtor economy.

I If bR < 1 then, b has a LR distribution (PS/BAH model).

Banco de la República Oil and Macro BIS CCA Conference 6 / 36

Bewley Endowment

A global solution: discrete dynamic program

Let e = (y ,b), discretize it and find optimal rule b

t+1

= b (e) such that

v(e) = maxb(e)2[�f ,0]

(y �b

0+Rb)1�s

1�s+bP

⇣b (e)

⌘v(e). (1)

where P

⇣b (e)

⌘is the OTPM and depends on b , R , s , f , E [y ] and V [y ].

Experiment: expected income E [y ] falls unexpectedly and permanentlyfrom y to y , keeping V [y ] constant.

Banco de la República Oil and Macro BIS CCA Conference 7 / 36

Bewley Endowment

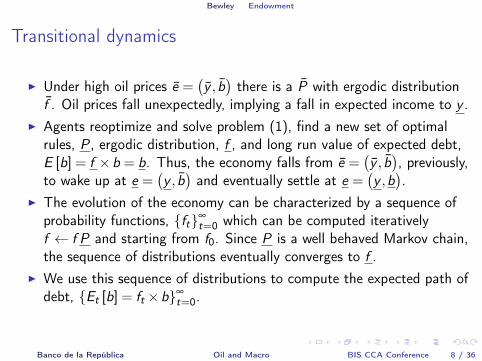

Transitional dynamics

I Under high oil prices e =�y , b�

there is a P with ergodic distributionf . Oil prices fall unexpectedly, implying a fall in expected income to y .

I Agents reoptimize and solve problem (1), find a new set of optimalrules, P , ergodic distribution, f , and long run value of expected debt,E [b] = f ⇥b = b. Thus, the economy falls from e =

�y , b�, previously,

to wake up at e =�y , b�

and eventually settle at e =�y ,b�.

I The evolution of the economy can be characterized by a sequence ofprobability functions, {f

t

}•t=0

which can be computed iterativelyf f P and starting from f

0

. Since P is a well behaved Markov chain,the sequence of distributions eventually converges to f .

I We use this sequence of distributions to compute the expected path ofdebt, {E

t

[b] = f

t

⇥b}•t=0

.

Banco de la República Oil and Macro BIS CCA Conference 8 / 36

Bewley Endowment

Transitional dynamics

I Under high oil prices e =�y , b�

there is a P with ergodic distributionf . Oil prices fall unexpectedly, implying a fall in expected income to y .

I Agents reoptimize and solve problem (1), find a new set of optimalrules, P , ergodic distribution, f , and long run value of expected debt,E [b] = f ⇥b = b. Thus, the economy falls from e =

�y , b�, previously,

to wake up at e =�y , b�

and eventually settle at e =�y ,b�.

I The evolution of the economy can be characterized by a sequence ofprobability functions, {f

t

}•t=0

which can be computed iterativelyf f P and starting from f

0

. Since P is a well behaved Markov chain,the sequence of distributions eventually converges to f .

I We use this sequence of distributions to compute the expected path ofdebt, {E

t

[b] = f

t

⇥b}•t=0

.

Banco de la República Oil and Macro BIS CCA Conference 8 / 36

Bewley Endowment

Transitional dynamics

I Under high oil prices e =�y , b�

there is a P with ergodic distributionf . Oil prices fall unexpectedly, implying a fall in expected income to y .

I Agents reoptimize and solve problem (1), find a new set of optimalrules, P , ergodic distribution, f , and long run value of expected debt,E [b] = f ⇥b = b. Thus, the economy falls from e =

�y , b�, previously,

to wake up at e =�y , b�

and eventually settle at e =�y ,b�.

I The evolution of the economy can be characterized by a sequence ofprobability functions, {f

t

}•t=0

which can be computed iterativelyf f P and starting from f

0

. Since P is a well behaved Markov chain,the sequence of distributions eventually converges to f .

I We use this sequence of distributions to compute the expected path ofdebt, {E

t

[b] = f

t

⇥b}•t=0

.

Banco de la República Oil and Macro BIS CCA Conference 8 / 36

Bewley Endowment

Transitional dynamics

I Under high oil prices e =�y , b�

there is a P with ergodic distributionf . Oil prices fall unexpectedly, implying a fall in expected income to y .

I Agents reoptimize and solve problem (1), find a new set of optimalrules, P , ergodic distribution, f , and long run value of expected debt,E [b] = f ⇥b = b. Thus, the economy falls from e =

�y , b�, previously,

to wake up at e =�y , b�

and eventually settle at e =�y ,b�.

I The evolution of the economy can be characterized by a sequence ofprobability functions, {f

t

}•t=0

which can be computed iterativelyf f P and starting from f

0

. Since P is a well behaved Markov chain,the sequence of distributions eventually converges to f .

I We use this sequence of distributions to compute the expected path ofdebt, {E

t

[b] = f

t

⇥b}•t=0

.

Banco de la República Oil and Macro BIS CCA Conference 8 / 36

Bewley Endowment

Calibration

I We set E [y ] = 1 and V [y ] = 0.0262 to match annual (HP-filtered)Colombian annual GDP moments. Fix R = 1.035 and take s = 4 fromestimated models at CB. And set b = 0.96 and f = 0.4 to match 30%external debt to GDP ratio and a fraction of international financialexclusion of 16%.

I Considering an autonomous level of absorption, which is present in thedata but not in the model economy, the model delivers a 31% debt toGDP and a ratio of financial exclusion of 12%.

I Consumption is procyclical and highly autocorrelated, as in the data,but is about one-third smoother. The current account and the tradebalance are also highly correlated in the model as in the data, howeverthe model results are at odds with a well-documented fact which isthat both are counter-cyclical in emerging economies.

Banco de la República Oil and Macro BIS CCA Conference 9 / 36

Bewley Endowment

Calibration

I We set E [y ] = 1 and V [y ] = 0.0262 to match annual (HP-filtered)Colombian annual GDP moments. Fix R = 1.035 and take s = 4 fromestimated models at CB. And set b = 0.96 and f = 0.4 to match 30%external debt to GDP ratio and a fraction of international financialexclusion of 16%.

I Considering an autonomous level of absorption, which is present in thedata but not in the model economy, the model delivers a 31% debt toGDP and a ratio of financial exclusion of 12%.

I Consumption is procyclical and highly autocorrelated, as in the data,but is about one-third smoother. The current account and the tradebalance are also highly correlated in the model as in the data, howeverthe model results are at odds with a well-documented fact which isthat both are counter-cyclical in emerging economies.

Banco de la República Oil and Macro BIS CCA Conference 9 / 36

Bewley Endowment

Calibration

I We set E [y ] = 1 and V [y ] = 0.0262 to match annual (HP-filtered)Colombian annual GDP moments. Fix R = 1.035 and take s = 4 fromestimated models at CB. And set b = 0.96 and f = 0.4 to match 30%external debt to GDP ratio and a fraction of international financialexclusion of 16%.

I Considering an autonomous level of absorption, which is present in thedata but not in the model economy, the model delivers a 31% debt toGDP and a ratio of financial exclusion of 12%.

I Consumption is procyclical and highly autocorrelated, as in the data,but is about one-third smoother. The current account and the tradebalance are also highly correlated in the model as in the data, howeverthe model results are at odds with a well-documented fact which isthat both are counter-cyclical in emerging economies.

Banco de la República Oil and Macro BIS CCA Conference 9 / 36

Bewley Endowment

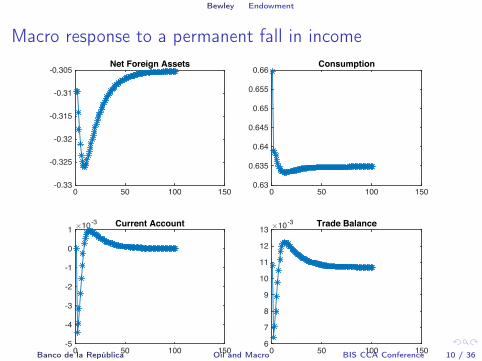

Macro response to a permanent fall in income

0 50 100 150-0.33

-0.325

-0.32

-0.315

-0.31

-0.305Net Foreign Assets

0 50 100 1500.63

0.635

0.64

0.645

0.65

0.655

0.66Consumption

0 50 100 150

#10-3

-5

-4

-3

-2

-1

0

1Current Account

0 50 100 150

#10-3

6

7

8

9

10

11

12

13Trade Balance

Banco de la República Oil and Macro BIS CCA Conference 10 / 36

Bewley T/N economy

Outline

The policy question and the problem

Small scale Bewley ModelsSingle-good EconomyTwo-good EconomyOil Exporting Economy

Monetary policy modelsSimple New KeynesianSectoral Financial AcceleratorSectoral financial accelerator model

Final Remarks

Banco de la República Oil and Macro BIS CCA Conference 11 / 36

Bewley T/N economy

The model

v(yT ,b) = maxb

02[�f ,0]

c

1�s

1�s+bE

y

T

v(⇣y

T

⌘0,b0)

�(2)

c

t

=

a

⇣c

T

t

⌘�µ+(1�a)

⇣c

N

t

⌘�µ�� 1

µ

c

T

t

= y

T

t

+p

N

t

y

N �b

t+1

+Rb

t

+A

T

c

N

t

= y

N +A

N

p

N

t

=1�a

a

✓c

T

t

c

N

t

◆1+µ

Banco de la República Oil and Macro BIS CCA Conference 12 / 36

Bewley T/N economy

Macro response to a permanent fall in income

0 20 40 600.66

0.67

0.68

0.69

0.7

0.71

0.72

0.73Output

0 20 40 600.314

0.316

0.318

0.32

0.322

0.324

0.326

0.328Consumption

0 20 40 601

1.02

1.04

1.06

1.08

1.1

1.12Real Exchange Rate

0 20 40 60

#10-4

-20

-15

-10

-5

0

5Current Account

0 20 40 60

#10-3

8.5

9

9.5

10

10.5

11Trade Balance

0 20 40 60-0.302

-0.3

-0.298

-0.296

-0.294

-0.292

-0.29Net Foreign Assets

Banco de la República Oil and Macro BIS CCA Conference 13 / 36

Bewley Oil economy

Outline

The policy question and the problem

Small scale Bewley ModelsSingle-good EconomyTwo-good EconomyOil Exporting Economy

Monetary policy modelsSimple New KeynesianSectoral Financial AcceleratorSectoral financial accelerator model

Final Remarks

Banco de la República Oil and Macro BIS CCA Conference 14 / 36

Bewley Oil economy

Oil prices and reserves

1926%

1927%

1928%1929% 1930%

1931%1932%

1933%

1934%1935%

1936%1937%

1938%

1939%1940%

1942%

1943%

1944%

1945%

1946%1947%1948%1949%

1950%

1952% 1953%1954%1955%

1956%1957%1958%

1959%1960%1966%

1967%

1968%1969%

1970%

1971%

1972%

1973% 1974%

1975%1976%1977%

1978%

1979%1980%1981%1982%1983%

1984%1985%1986%1987%1988% 1989% 1990%

1991%

1992%1993%

1994%1995% 1996%1997%

1998%

1999% 2000%2001%

2002% 2003% 2004%

2005%2006%

2007%

2008%2009% 2010%

2011%2012%2013%

0%

20%

40%

60%

80%

100%

120%

140%

0% 20% 40% 60% 80% 100% 120% 140%

Reserves/Produ

c,on

.(years).

Oil.Price.(Crude.Price.BP,.real.USD).

Banco de la República Oil and Macro BIS CCA Conference 15 / 36

Bewley Oil economy

Oil sector

Economy has a stock of oil s 2 [0, s] and every year d units can bediscovered randomly. A representative oil firm can extract x 2 [0,s] units ofoil at a cost C (s,x) to sell internationally at the relative price p

x

(in unitsot tradable). The stock of oil evolves as s

0 = s� x+d , and the firm seeksto:

v(s) = maxx2[0,s]

{pxx�C (s,x)+dEd

[v (s� x+d)]} .

Optimality requires that

p

x = C

x

(s,x)+dEd

[l (s� x+d)]

l (s) = C

s

(s,x)+dEd

[l (s� x+d)] .

Banco de la República Oil and Macro BIS CCA Conference 16 / 36

Bewley Oil economy

Non-oil economy

Associated with this program there is an optimal oil extraction policy, x (s),which the rest of the economy takes as given, thus the resource constraintof the economy becomes:

c

T

t

= y

T

t

+p

x

x (s)+p

N

t

y

N �b

t+1

+Rb

t

+A

T

andc

N

t

= y

N +A

N .

Thus, with two assets, optimal borrowing is b0 (s,b), and at any given pointin time, NFA are not only the summary of debt history but also of oilreserves history.

Banco de la República Oil and Macro BIS CCA Conference 17 / 36

Bewley Oil economy

Calibration I

41,76

11,55

0

10

20

30

40

50

60

70

80 19

27

1929

19

31

1933

19

35

1937

19

39

1941

19

43

1945

19

47

1949

19

51

1953

19

55

1957

19

59

1961

19

63

1965

19

67

1969

19

71

1973

19

75

1977

19

79

1981

19

83

1985

19

87

1989

19

91

1993

19

95

1997

19

99

2001

20

03

2005

20

07

2009

20

11

2013

Re

serv

es

to

Pro

du

ctio

n R

atio

(Y

ear

s)

Year

Mean 1927-1958 Mean 1959-2013

Banco de la República Oil and Macro BIS CCA Conference 18 / 36

Bewley Oil economy

Calibration of discoveries

0 5 10 15

x 105

0

0.1

0.2

0.3

0.4

0.5

Barrels (Thous.)

Banco de la República Oil and Macro BIS CCA Conference 19 / 36

Bewley Oil economy

Macro response to a permanent fall of oil prices

0 100 2002.4

2.6

2.8

3

3.2Optimal Reserves

0 100 200-0.36

-0.34

-0.32

-0.3Net Foreign Assets

0 100 2000.318

0.3185

0.319

0.3195

0.32

0.3205Consumption

0 100 2000.7

0.8

0.9

1

1.1Oil extraction

0 100 200

#10-3

-5

0

5

10

15Trade Balance

0 100 2001

1.005

1.01

1.015

1.02Real Exchange Rate

0 100 2000.4

0.5

0.6

0.7

0.8

0.9Oil profits

0 100 200

#10-3

-15

-10

-5

0

5Current Account

0 100 2000.318

0.3185

0.319

0.3195

0.32

0.3205Price of Nontradables

X: 150Y: -0.3179

Banco de la República Oil and Macro BIS CCA Conference 20 / 36

Bewley Oil economy

Main takeaways from small scale models

I The financial and real structure of the economy are important whenstudying the net foreign position of the economy.

I The differences between the one-good and two-good models pointthat RER appears to be a key variable in the adjustment process.

I The differences between the two-good model and the three-goodmodel stresses the point that the NFA adjustment may besubstantially different in an oil economy.

I However, these models leave aside many features of reality that are ofinterest to policy makers and central banks.

I We now turn to the reaction of monetary economies to unexpectedpermanent changes in oil prices, taking as given the NFA adjustmentof the oil economy.

Banco de la República Oil and Macro BIS CCA Conference 21 / 36

Bewley Oil economy

Main takeaways from small scale models

I The financial and real structure of the economy are important whenstudying the net foreign position of the economy.

I The differences between the one-good and two-good models pointthat RER appears to be a key variable in the adjustment process.

I The differences between the two-good model and the three-goodmodel stresses the point that the NFA adjustment may besubstantially different in an oil economy.

I However, these models leave aside many features of reality that are ofinterest to policy makers and central banks.

I We now turn to the reaction of monetary economies to unexpectedpermanent changes in oil prices, taking as given the NFA adjustmentof the oil economy.

Banco de la República Oil and Macro BIS CCA Conference 21 / 36

Bewley Oil economy

Main takeaways from small scale models

I The financial and real structure of the economy are important whenstudying the net foreign position of the economy.

I The differences between the one-good and two-good models pointthat RER appears to be a key variable in the adjustment process.

I The differences between the two-good model and the three-goodmodel stresses the point that the NFA adjustment may besubstantially different in an oil economy.

I However, these models leave aside many features of reality that are ofinterest to policy makers and central banks.

I We now turn to the reaction of monetary economies to unexpectedpermanent changes in oil prices, taking as given the NFA adjustmentof the oil economy.

Banco de la República Oil and Macro BIS CCA Conference 21 / 36

Bewley Oil economy

Main takeaways from small scale models

I The financial and real structure of the economy are important whenstudying the net foreign position of the economy.

I The differences between the one-good and two-good models pointthat RER appears to be a key variable in the adjustment process.

I The differences between the two-good model and the three-goodmodel stresses the point that the NFA adjustment may besubstantially different in an oil economy.

I However, these models leave aside many features of reality that are ofinterest to policy makers and central banks.

I We now turn to the reaction of monetary economies to unexpectedpermanent changes in oil prices, taking as given the NFA adjustmentof the oil economy.

Banco de la República Oil and Macro BIS CCA Conference 21 / 36

Bewley Oil economy

Main takeaways from small scale models

I The financial and real structure of the economy are important whenstudying the net foreign position of the economy.

I The differences between the one-good and two-good models pointthat RER appears to be a key variable in the adjustment process.

I The differences between the two-good model and the three-goodmodel stresses the point that the NFA adjustment may besubstantially different in an oil economy.

I However, these models leave aside many features of reality that are ofinterest to policy makers and central banks.

I We now turn to the reaction of monetary economies to unexpectedpermanent changes in oil prices, taking as given the NFA adjustmentof the oil economy.

Banco de la República Oil and Macro BIS CCA Conference 21 / 36

Monetary policy New Keynesian

Outline

The policy question and the problem

Small scale Bewley ModelsSingle-good EconomyTwo-good EconomyOil Exporting Economy

Monetary policy modelsSimple New KeynesianSectoral Financial AcceleratorSectoral financial accelerator model

Final Remarks

Banco de la República Oil and Macro BIS CCA Conference 22 / 36

Monetary policy New Keynesian

A channel outside the previous models

0

10

20

30

40

50

60

70

-200 -150 -100 -50 0 50 100 150 EMBI Colombia* relative to VIX index*

Oil

pric

e (B

rent

, US

$ re

al)

*January 2000 = 100

Banco de la República Oil and Macro BIS CCA Conference 23 / 36

Monetary policy New Keynesian

Key elements of the model

I Small open economy DSGE with three sectors: tradable, non-tradableand oil exporting sector

I The economy has a stock of oil reserves and extraction is endogenous.I T is an endowment and NT uses labor and imported inputs (gasoline)

to produce.I Sticky nominal prices in NT sector, flexible prices in T sector.I Central bank targets total inflationI Key: country risk premium depends on both b and p

x

s.Micro-founded version of this: Hamann and Restrepo (2015).

Banco de la República Oil and Macro BIS CCA Conference 24 / 36

Monetary policy New Keynesian

Key elements of the model

I Small open economy DSGE with three sectors: tradable, non-tradableand oil exporting sector

I The economy has a stock of oil reserves and extraction is endogenous.

I T is an endowment and NT uses labor and imported inputs (gasoline)to produce.

I Sticky nominal prices in NT sector, flexible prices in T sector.I Central bank targets total inflationI Key: country risk premium depends on both b and p

x

s.Micro-founded version of this: Hamann and Restrepo (2015).

Banco de la República Oil and Macro BIS CCA Conference 24 / 36

Monetary policy New Keynesian

Key elements of the model

I Small open economy DSGE with three sectors: tradable, non-tradableand oil exporting sector

I The economy has a stock of oil reserves and extraction is endogenous.I T is an endowment and NT uses labor and imported inputs (gasoline)

to produce.

I Sticky nominal prices in NT sector, flexible prices in T sector.I Central bank targets total inflationI Key: country risk premium depends on both b and p

x

s.Micro-founded version of this: Hamann and Restrepo (2015).

Banco de la República Oil and Macro BIS CCA Conference 24 / 36

Monetary policy New Keynesian

Key elements of the model

I Small open economy DSGE with three sectors: tradable, non-tradableand oil exporting sector

I The economy has a stock of oil reserves and extraction is endogenous.I T is an endowment and NT uses labor and imported inputs (gasoline)

to produce.I Sticky nominal prices in NT sector, flexible prices in T sector.

I Central bank targets total inflationI Key: country risk premium depends on both b and p

x

s.Micro-founded version of this: Hamann and Restrepo (2015).

Banco de la República Oil and Macro BIS CCA Conference 24 / 36

Monetary policy New Keynesian

Key elements of the model

I Small open economy DSGE with three sectors: tradable, non-tradableand oil exporting sector

I The economy has a stock of oil reserves and extraction is endogenous.I T is an endowment and NT uses labor and imported inputs (gasoline)

to produce.I Sticky nominal prices in NT sector, flexible prices in T sector.I Central bank targets total inflation

I Key: country risk premium depends on both b and p

x

s.Micro-founded version of this: Hamann and Restrepo (2015).

Banco de la República Oil and Macro BIS CCA Conference 24 / 36

Monetary policy New Keynesian

Key elements of the model

I Small open economy DSGE with three sectors: tradable, non-tradableand oil exporting sector

I The economy has a stock of oil reserves and extraction is endogenous.I T is an endowment and NT uses labor and imported inputs (gasoline)

to produce.I Sticky nominal prices in NT sector, flexible prices in T sector.I Central bank targets total inflationI Key: country risk premium depends on both b and p

x

s.Micro-founded version of this: Hamann and Restrepo (2015).

Banco de la República Oil and Macro BIS CCA Conference 24 / 36

Monetary policy New Keynesian

Macro response to a permanent fall of oil prices

5 10 15 2080

90

100Extraction

FlexibleSticky

5 10 15 206

8

10Reserves (years)

5 10 15 20100

110

120Reserves

5 10 15 2090

95

100GDP

5 10 15 2090

95

100Consumption

5 10 15 20100

110

120External debt

5 10 15 20100

105

110PT / PN

5 10 15 2090

100

110Employment

5 10 15 2095

100

105Non tradable output

5 10 15 203

3.5

4External interest rate

5 10 15 206

8

10Policy rate

5 10 15 202

4

6Total inflation

Banco de la República Oil and Macro BIS CCA Conference 25 / 36

Monetary policy T/N Financial accelerator

Outline

The policy question and the problem

Small scale Bewley ModelsSingle-good EconomyTwo-good EconomyOil Exporting Economy

Monetary policy modelsSimple New KeynesianSectoral Financial AcceleratorSectoral financial accelerator model

Final Remarks

Banco de la República Oil and Macro BIS CCA Conference 26 / 36

Monetary policy T/N Financial accelerator

Key elements of the model

I Small open economy DSGE with three sectors: tradable, non-tradableand oil exporting sector

I The economy has a stock of oil reserves and extraction is endogenous.I Sticky nominal prices in NT sector, flexible prices in T sector.I Capital is specific to both T and NT sectors, labor can move freely

between sectors.I Key: financial accelerator (BGG) in both sectors where net worth is

influenced by valuation effects.

Banco de la República Oil and Macro BIS CCA Conference 27 / 36

Monetary policy T/N Financial accelerator

Key elements of the model

I Small open economy DSGE with three sectors: tradable, non-tradableand oil exporting sector

I The economy has a stock of oil reserves and extraction is endogenous.

I Sticky nominal prices in NT sector, flexible prices in T sector.I Capital is specific to both T and NT sectors, labor can move freely

between sectors.I Key: financial accelerator (BGG) in both sectors where net worth is

influenced by valuation effects.

Banco de la República Oil and Macro BIS CCA Conference 27 / 36

Monetary policy T/N Financial accelerator

Key elements of the model

I Small open economy DSGE with three sectors: tradable, non-tradableand oil exporting sector

I The economy has a stock of oil reserves and extraction is endogenous.I Sticky nominal prices in NT sector, flexible prices in T sector.

I Capital is specific to both T and NT sectors, labor can move freelybetween sectors.

I Key: financial accelerator (BGG) in both sectors where net worth isinfluenced by valuation effects.

Banco de la República Oil and Macro BIS CCA Conference 27 / 36

Monetary policy T/N Financial accelerator

Key elements of the model

I Small open economy DSGE with three sectors: tradable, non-tradableand oil exporting sector

I The economy has a stock of oil reserves and extraction is endogenous.I Sticky nominal prices in NT sector, flexible prices in T sector.I Capital is specific to both T and NT sectors, labor can move freely

between sectors.

I Key: financial accelerator (BGG) in both sectors where net worth isinfluenced by valuation effects.

Banco de la República Oil and Macro BIS CCA Conference 27 / 36

Monetary policy T/N Financial accelerator

Key elements of the model

I Small open economy DSGE with three sectors: tradable, non-tradableand oil exporting sector

I The economy has a stock of oil reserves and extraction is endogenous.I Sticky nominal prices in NT sector, flexible prices in T sector.I Capital is specific to both T and NT sectors, labor can move freely

between sectors.I Key: financial accelerator (BGG) in both sectors where net worth is

influenced by valuation effects.

Banco de la República Oil and Macro BIS CCA Conference 27 / 36

Monetary policy T/N Financial accelerator

Key 1: Financial acceleratortradable and nontradable (j = N,T )

I Perfectly competitive banks make commercial loans to entrepreneurs,b

j

t

, by taking deposits from households, dt

, and borrowing frominternational financial markets, b?

t

.

I Financial intermediation subject to frictions (CSV problem) on theside of the asset side of the banks. Thus, spreads depend on firms’ networth, nj

t

and the value of capital, pkj

t

k

j

t

.

Et

hr

k

j

t+1

i=

n

j

t

p

k

j

t

k

j

t

!�n j

t

(1+ r

t

)(rpt

)

I We define a “regulation premium”, rpt

, as any policy that increasescredit costs.

Banco de la República Oil and Macro BIS CCA Conference 28 / 36

Monetary policy T/N Financial accelerator

Key 1: Financial acceleratortradable and nontradable (j = N,T )

I Perfectly competitive banks make commercial loans to entrepreneurs,b

j

t

, by taking deposits from households, dt

, and borrowing frominternational financial markets, b?

t

.I Financial intermediation subject to frictions (CSV problem) on the

side of the asset side of the banks. Thus, spreads depend on firms’ networth, nj

t

and the value of capital, pkj

t

k

j

t

.

Et

hr

k

j

t+1

i=

n

j

t

p

k

j

t

k

j

t

!�n j

t

(1+ r

t

)(rpt

)

I We define a “regulation premium”, rpt

, as any policy that increasescredit costs.

Banco de la República Oil and Macro BIS CCA Conference 28 / 36

Monetary policy T/N Financial accelerator

Key 1: Financial acceleratortradable and nontradable (j = N,T )

I Perfectly competitive banks make commercial loans to entrepreneurs,b

j

t

, by taking deposits from households, dt

, and borrowing frominternational financial markets, b?

t

.I Financial intermediation subject to frictions (CSV problem) on the

side of the asset side of the banks. Thus, spreads depend on firms’ networth, nj

t

and the value of capital, pkj

t

k

j

t

.

Et

hr

k

j

t+1

i=

n

j

t

p

k

j

t

k

j

t

!�n j

t

(1+ r

t

)(rpt

)

I We define a “regulation premium”, rpt

, as any policy that increasescredit costs.

Banco de la República Oil and Macro BIS CCA Conference 28 / 36

Monetary policy T/N Financial accelerator

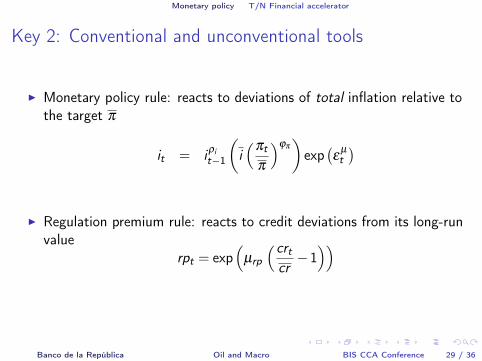

Key 2: Conventional and unconventional tools

I Monetary policy rule: reacts to deviations of total inflation relative tothe target p

i

t

= i

ri

t�1

✓i

⇣pt

p

⌘jp◆

exp�eµt

�

I Regulation premium rule: reacts to credit deviations from its long-runvalue

rp

t

= exp⇣

µrp

⇣cr

t

cr

�1⌘⌘

Banco de la República Oil and Macro BIS CCA Conference 29 / 36

Monetary policy T/N Financial accelerator

Key 2: Conventional and unconventional tools

I Monetary policy rule: reacts to deviations of total inflation relative tothe target p

i

t

= i

ri

t�1

✓i

⇣pt

p

⌘jp◆

exp�eµt

�

I Regulation premium rule: reacts to credit deviations from its long-runvalue

rp

t

= exp⇣

µrp

⇣cr

t

cr

�1⌘⌘

Banco de la República Oil and Macro BIS CCA Conference 29 / 36

Monetary policy T/N Financial accelerator

Key 2: Conventional and unconventional tools

I Monetary policy rule: reacts to deviations of total inflation relative tothe target p

i

t

= i

ri

t�1

✓i

⇣pt

p

⌘jp◆

exp�eµt

�

I Regulation premium rule: reacts to credit deviations from its long-runvalue

rp

t

= exp⇣

µrp

⇣cr

t

cr

�1⌘⌘

Banco de la República Oil and Macro BIS CCA Conference 29 / 36

Monetary policy

Outline

The policy question and the problem

Small scale Bewley ModelsSingle-good EconomyTwo-good EconomyOil Exporting Economy

Monetary policy modelsSimple New KeynesianSectoral Financial AcceleratorSectoral financial accelerator model

Final Remarks

Banco de la República Oil and Macro BIS CCA Conference 30 / 36

Monetary policy

Macro response to a permanent fall of oil prices I

5 10 15 20 25 30 35 4080

90

100Extraction

5 10 15 20 25 30 35 406

7

8Reserves (years)

5 10 15 20 25 30 35 40100

110

120Reserves

5 10 15 20 25 30 35 4097

98

99

100GDP

5 10 15 20 25 30 35 4094

96

98

100Consumption

5 10 15 20 25 30 35 4096

98

100

102External Debt

5 10 15 20 25 30 35 40100

105

110pT / PN

5 10 15 20 25 30 35 40100

105

110Tradable output

5 10 15 20 25 30 35 4094

96

98

100Non Tradable Output

5 10 15 20 25 30 35 406.5

7

7.5External Interest Rate

5 10 15 20 25 30 35 406.5

7

7.5Policy Rate

5 10 15 20 25 30 35 400

5

10Total Inflation

Financial Frictions W/o Financial Frictions

Banco de la República Oil and Macro BIS CCA Conference 31 / 36

Monetary policy

Macro response to a permanent fall of oil prices II

5 10 15 20 25 30 35 4099

100

101

102Total Credit

5 10 15 20 25 30 35 4095

100

105

110Tradable Credit

5 10 15 20 25 30 35 4096

98

100

102Non Tradable Credit

5 10 15 20 25 30 35 40100

102

104

106Total Investmet

5 10 15 20 25 30 35 40100

110

120Tradable Investment

5 10 15 20 25 30 35 4085

90

95

100Non Tradable Investment

5 10 15 20 25 30 35 40100

105

110Tradable Capital

5 10 15 20 25 30 35 4090

95

100Tradable Leverage

5 10 15 20 25 30 35 40100

102

104

106Non Tradable Leverage

5 10 15 20 25 30 35 4097

98

99

100Non Tradable Capital

5 10 15 20 25 30 35 408

8.5

9

9.5Tradable Spread

5 10 15 20 25 30 35 409

9.5

10

10.5Non Tradable Spread

Financial Frictions W/o Financial Frictions

Banco de la República Oil and Macro BIS CCA Conference 32 / 36

Monetary policy

What if the central bank targets NT inflation?

5 10 15 20 25 30 35 4080

90

100Extraction

5 10 15 20 25 30 35 406

7

8Reserves (years)

5 10 15 20 25 30 35 40100

110

120Reserves

5 10 15 20 25 30 35 4097

98

99

100GDP

5 10 15 20 25 30 35 4094

96

98

100Consumption

5 10 15 20 25 30 35 4095

100

105External Debt

5 10 15 20 25 30 35 40100

105

110pT / PN

5 10 15 20 25 30 35 40100

105

110Tradable output

5 10 15 20 25 30 35 4094

96

98

100Non Tradable Output

5 10 15 20 25 30 35 406.5

7

7.5External Interest Rate

5 10 15 20 25 30 35 405

6

7

8Policy Rate

5 10 15 20 25 30 35 400

5

10

15Headline Inflation

Headline Inflation Targeting Non-Tradable Inflation Targeting

Banco de la República Oil and Macro BIS CCA Conference 33 / 36

Monetary policy

What if the central bank targets NT inflation?

5 10 15 20 25 30 35 4099

100

101

102Total Credit

5 10 15 20 25 30 35 40100

102

104

106Tradable Credit

5 10 15 20 25 30 35 4096

98

100

102Non Tradable Credit

5 10 15 20 25 30 35 40100

102

104

106Total Investmet

5 10 15 20 25 30 35 40100

110

120

130Tradable Investment

5 10 15 20 25 30 35 4085

90

95

100Non Tradable Investment

5 10 15 20 25 30 35 40100

105

110Tradable Capital

5 10 15 20 25 30 35 4090

95

100Tradable Leverage

5 10 15 20 25 30 35 40100

102

104

106Non Tradable Leverage

5 10 15 20 25 30 35 4097

98

99

100Non Tradable Capital

5 10 15 20 25 30 35 408

8.5

9

9.5Tradable Spread

5 10 15 20 25 30 35 409

9.5

10

10.5Non Tradable Spread

Headline Inflation Targeting Non-Tradable Inflation Targeting

Banco de la República Oil and Macro BIS CCA Conference 34 / 36

Final Remarks

Final Remarks

I A two-stage approach to study macro consequences of unexpectedpermanent changes in oil prices

I Key: RER adjustment + endogenous oil extraction coupled withcountry risk

I The shock induces additional financial needs for the economy whereoil acts as a “collateral”

I It also implies a monetary policy dilemma: inflation jumps (ERpass-through) while activity tanks

I This happens even under more realistic conditions, like financialaccelerator (BGG) in both sectors where net worth is influenced byvaluation effects

I To do: fiscal implications. May be relevant if one drops Ricardianequivalence

Banco de la República Oil and Macro BIS CCA Conference 35 / 36

Final Remarks

Final Remarks

I A two-stage approach to study macro consequences of unexpectedpermanent changes in oil prices

I Key: RER adjustment + endogenous oil extraction coupled withcountry risk

I The shock induces additional financial needs for the economy whereoil acts as a “collateral”

I It also implies a monetary policy dilemma: inflation jumps (ERpass-through) while activity tanks

I This happens even under more realistic conditions, like financialaccelerator (BGG) in both sectors where net worth is influenced byvaluation effects

I To do: fiscal implications. May be relevant if one drops Ricardianequivalence

Banco de la República Oil and Macro BIS CCA Conference 35 / 36

Final Remarks

Final Remarks

I A two-stage approach to study macro consequences of unexpectedpermanent changes in oil prices

I Key: RER adjustment + endogenous oil extraction coupled withcountry risk

I The shock induces additional financial needs for the economy whereoil acts as a “collateral”

I It also implies a monetary policy dilemma: inflation jumps (ERpass-through) while activity tanks

I This happens even under more realistic conditions, like financialaccelerator (BGG) in both sectors where net worth is influenced byvaluation effects

I To do: fiscal implications. May be relevant if one drops Ricardianequivalence

Banco de la República Oil and Macro BIS CCA Conference 35 / 36

Final Remarks

Final Remarks

I A two-stage approach to study macro consequences of unexpectedpermanent changes in oil prices

I Key: RER adjustment + endogenous oil extraction coupled withcountry risk

I The shock induces additional financial needs for the economy whereoil acts as a “collateral”

I It also implies a monetary policy dilemma: inflation jumps (ERpass-through) while activity tanks

I This happens even under more realistic conditions, like financialaccelerator (BGG) in both sectors where net worth is influenced byvaluation effects

I To do: fiscal implications. May be relevant if one drops Ricardianequivalence

Banco de la República Oil and Macro BIS CCA Conference 35 / 36

Final Remarks

Final Remarks

I A two-stage approach to study macro consequences of unexpectedpermanent changes in oil prices

I Key: RER adjustment + endogenous oil extraction coupled withcountry risk

I The shock induces additional financial needs for the economy whereoil acts as a “collateral”

I It also implies a monetary policy dilemma: inflation jumps (ERpass-through) while activity tanks

I This happens even under more realistic conditions, like financialaccelerator (BGG) in both sectors where net worth is influenced byvaluation effects

I To do: fiscal implications. May be relevant if one drops Ricardianequivalence

Banco de la República Oil and Macro BIS CCA Conference 35 / 36

Final Remarks

Final Remarks

I A two-stage approach to study macro consequences of unexpectedpermanent changes in oil prices

I Key: RER adjustment + endogenous oil extraction coupled withcountry risk

I The shock induces additional financial needs for the economy whereoil acts as a “collateral”

I It also implies a monetary policy dilemma: inflation jumps (ERpass-through) while activity tanks

I This happens even under more realistic conditions, like financialaccelerator (BGG) in both sectors where net worth is influenced byvaluation effects

I To do: fiscal implications. May be relevant if one drops Ricardianequivalence

Banco de la República Oil and Macro BIS CCA Conference 35 / 36

Final Remarks

Supplementary figures I

87654

s

32100-0.05

-0.1-0.15

-0.2-0.25

b

-0.3-0.35

0.012

0.01

0.008

0.006

0.004

0.002

0-0.4

Prob

Banco de la República Oil and Macro BIS CCA Conference 36 / 36