Embed Size (px)

Citation preview

1

MONETARY POLICY COMMITTEE STATEMENT FOR

FOURTH QUARTER 2017

Governor’s Presentation to the Media

21st February, 2018

INTRODUCTION

2

The presentation is structured as follows:

1. Decision of the Monetary Policy Committee

2. Overview

3. Global economic developments

4. Domestic economic developments

5. Macroeconomic outlook

MONETARY POLICY DECISION3

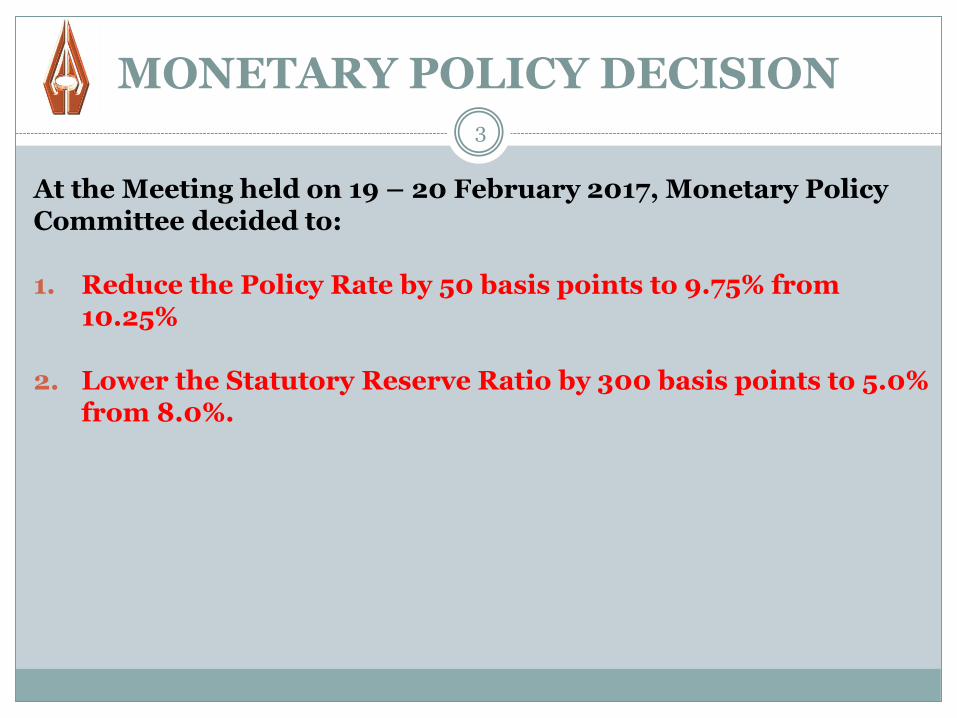

At the Meeting held on 19 – 20 February 2017, Monetary Policy Committee decided to:

1. Reduce the Policy Rate by 50 basis points to 9.75% from 10.25%

2. Lower the Statutory Reserve Ratio by 300 basis points to 5.0% from 8.0%.

MONETARY POLICY DECISION4

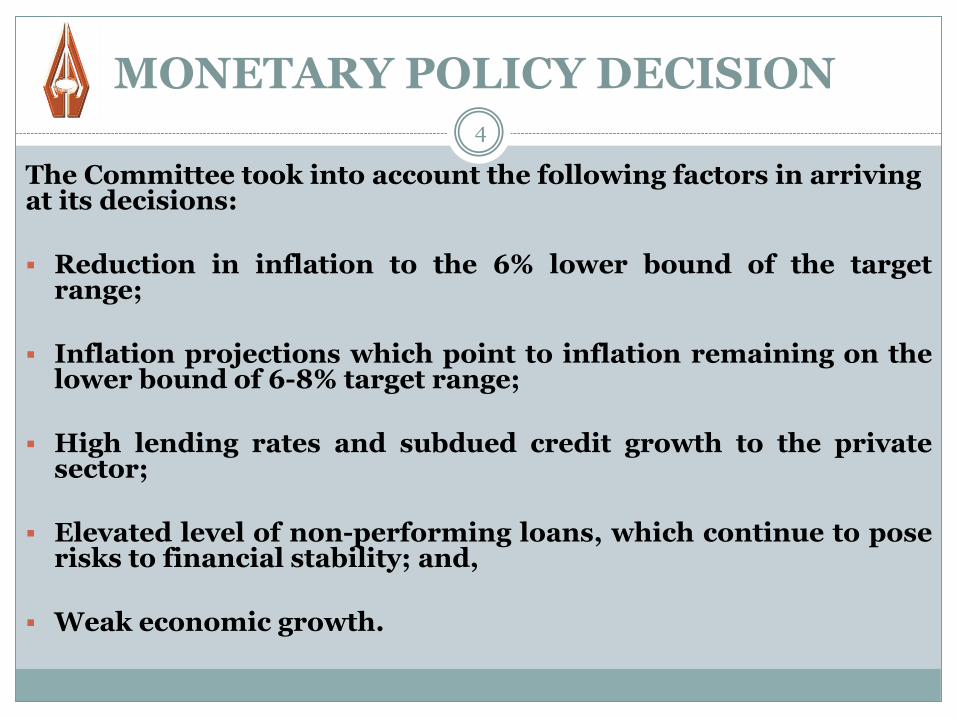

The Committee took into account the following factors in arriving at its decisions:

Reduction in inflation to the 6% lower bound of the targetrange;

Inflation projections which point to inflation remaining on thelower bound of 6-8% target range;

High lending rates and subdued credit growth to the privatesector;

Elevated level of non-performing loans, which continue to poserisks to financial stability; and,

Weak economic growth.

OVERVIEW

5

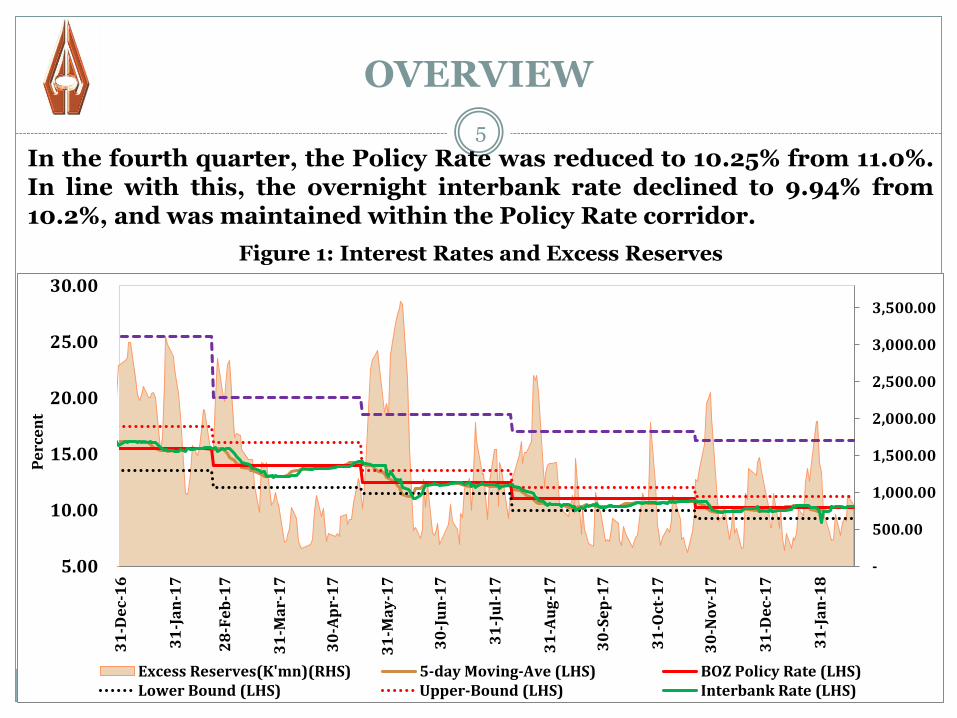

In the fourth quarter, the Policy Rate was reduced to 10.25% from 11.0%.In line with this, the overnight interbank rate declined to 9.94% from10.2%, and was maintained within the Policy Rate corridor.

Figure 1: Interest Rates and Excess Reserves

-

500.00

1,000.00

1,500.00

2,000.00

2,500.00

3,000.00

3,500.00

5.00

10.00

15.00

20.00

25.00

30.00

31

-De

c-1

6

31

-Ja

n-1

7

28

-Fe

b-1

7

31

-Ma

r-1

7

30

-Ap

r-1

7

31

-Ma

y-1

7

30

-Ju

n-1

7

31

-Ju

l-1

7

31

-Au

g-1

7

30

-Se

p-1

7

31

-Oct

-17

30

-No

v-1

7

31

-De

c-1

7

31

-Ja

n-1

8

Pe

rce

nt

Excess Reserves(K'mn)(RHS) 5-day Moving-Ave (LHS) BOZ Policy Rate (LHS)Lower Bound (LHS) Upper-Bound (LHS) Interbank Rate (LHS)

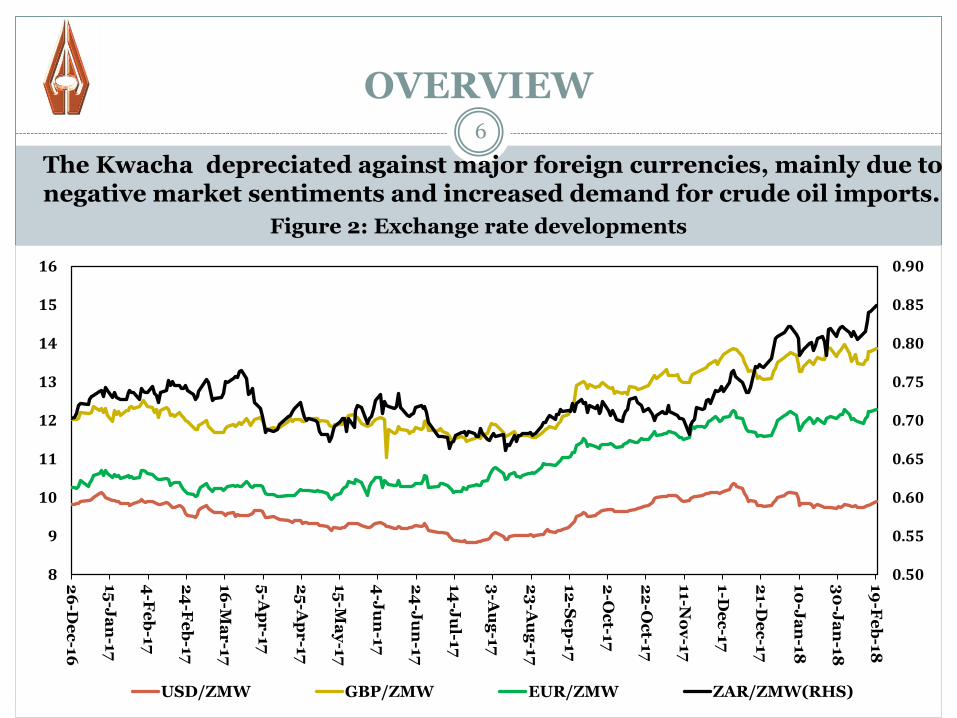

The Kwacha depreciated against major foreign currencies, mainly due to negative market sentiments and increased demand for crude oil imports.

OVERVIEW6

Figure 2: Exchange rate developments

0.50

0.55

0.60

0.65

0.70

0.75

0.80

0.85

0.90

8

9

10

11

12

13

14

15

16

26

-De

c-1

6

15

-Ja

n-1

7

4-F

eb

-17

24

-Fe

b-1

7

16

-Ma

r-1

7

5-A

pr

-17

25

-Ap

r-1

7

15

-Ma

y-1

7

4-J

un

-17

24

-Ju

n-1

7

14

-Ju

l-17

3-A

ug

-17

23

-Au

g-1

7

12

-Se

p-1

7

2-O

ct-1

7

22

-Oc

t-17

11-N

ov

-17

1-D

ec

-17

21-D

ec

-17

10

-Ja

n-1

8

30

-Ja

n-1

8

19

-Fe

b-1

8

USD/ZMW GBP/ZMW EUR/ZMW ZAR/ZMW(RHS)

OVERVIEW

7

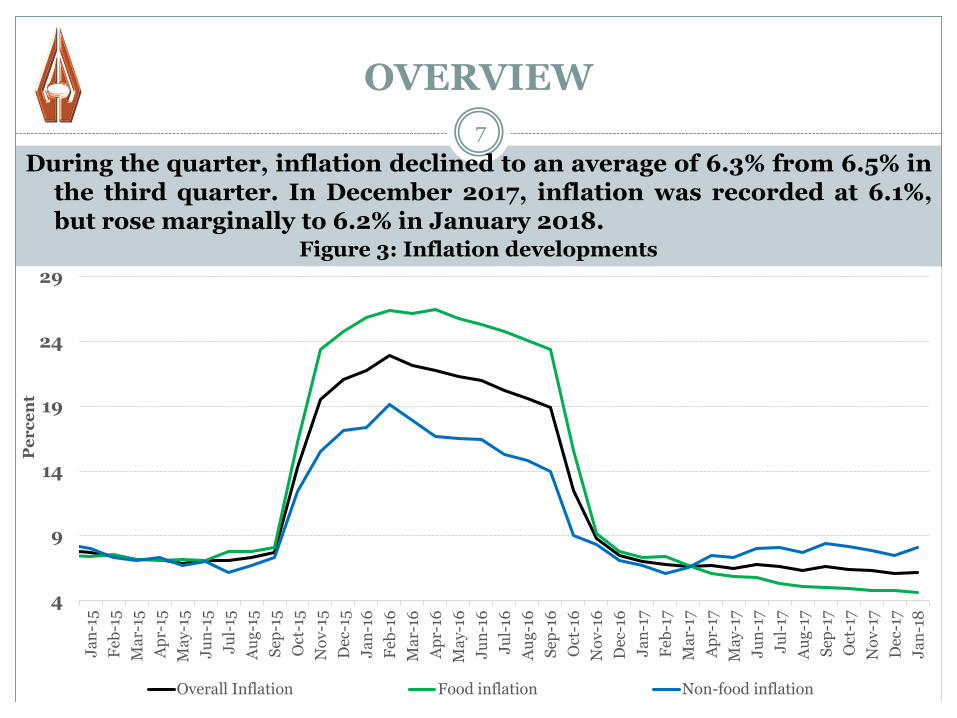

During the quarter, inflation declined to an average of 6.3% from 6.5% inthe third quarter. In December 2017, inflation was recorded at 6.1%,but rose marginally to 6.2% in January 2018.

Figure 3: Inflation developments

4

9

14

19

24

29

Ja

n-1

5

Feb

-15

Ma

r-15

Ap

r-15

Ma

y-1

5

Ju

n-1

5

Ju

l-15

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5

Dec

-15

Ja

n-1

6

Feb

-16

Ma

r-16

Ap

r-16

Ma

y-1

6

Ju

n-1

6

Ju

l-16

Au

g-1

6

Sep

-16

Oct

-16

No

v-1

6

Dec

-16

Ja

n-1

7

Feb

-17

Ma

r-17

Ap

r-17

Ma

y-1

7

Ju

n-1

7

Ju

l-17

Au

g-1

7

Sep

-17

Oct

-17

No

v-1

7

Dec

-17

Ja

n-1

8

Pe

rc

en

t

Overall Inflation Food inflation Non-food inflation

GLOBAL ECONOMIC DEVELOPMENTS

8

In the fourth quarter, global economic growth continued with the global economy ending 2017 on a strong footing.

Factors explaining continued growth include:

improved global trade and manufacturing output;

continued higher global commodity prices;

increased global demand;

strong growth in the US, driven by robust consumer spending;

strong growth in China; and,

stronger consumer sentiments

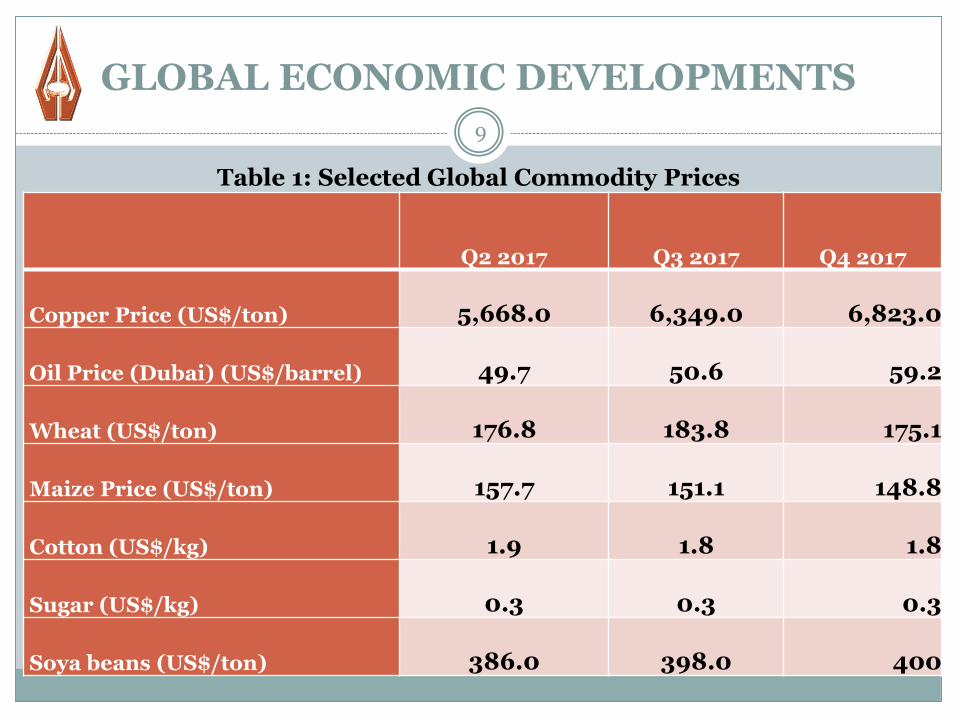

Commodity prices were mixed in the fourth quarter of 2017, butcopper and crude oil prices continued to rise (Table 1).

GLOBAL ECONOMIC DEVELOPMENTS

9

Table 1: Selected Global Commodity Prices

Q2 2017 Q3 2017 Q4 2017

Copper Price (US$/ton) 5,668.0 6,349.0 6,823.0

Oil Price (Dubai) (US$/barrel) 49.7 50.6 59.2

Wheat (US$/ton) 176.8 183.8 175.1

Maize Price (US$/ton) 157.7 151.1 148.8

Cotton (US$/kg) 1.9 1.8 1.8

Sugar (US$/kg) 0.3 0.3 0.3

Soya beans (US$/ton) 386.0 398.0 400

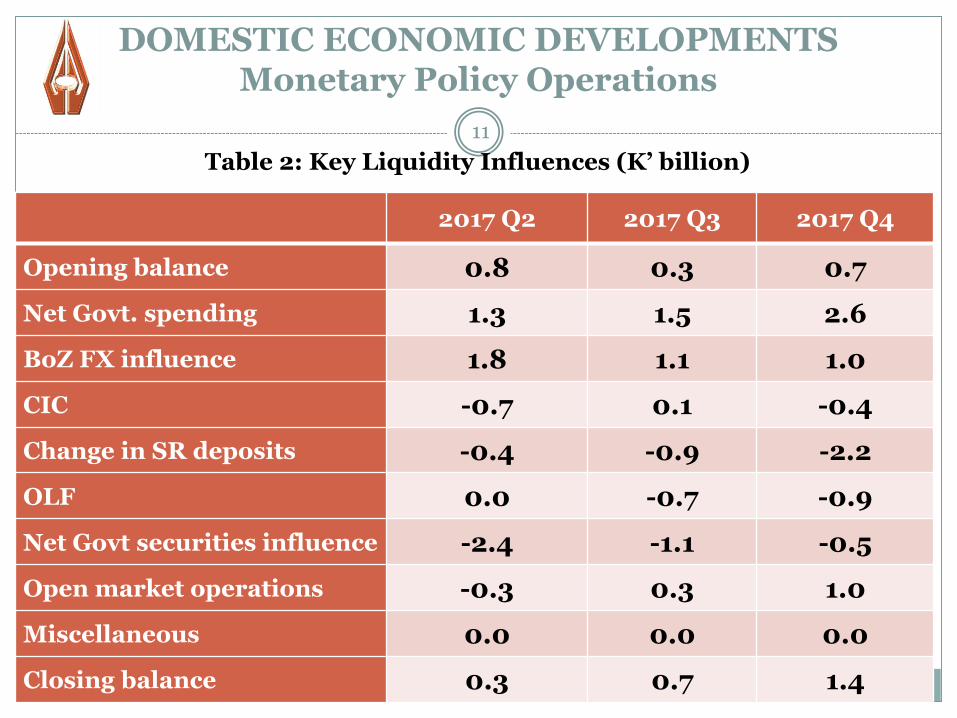

DOMESTIC ECONOMIC DEVELOPMENTSMonetary Policy Operations

10

The focus of monetary policy operations remained on containingthe overnight interbank rate within the Policy Rate corridor andanchoring inflationary expectations.

Market liquidity increased following net Government spending andBank of Zambia’s purchases of foreign exchange for internationalreserves (Table 2).

Following the further easing of monetary policy in November 2017,the interbank rate declined to 9.94% at the end-December 2017from 10.2% at end-September 2017 (Figure 1).

To keep the interbank rate within the Policy Rate corridor, theBank withdrew K8.8 billion through open market operations,which was lower than K20.0 billion in the third quarter.

DOMESTIC ECONOMIC DEVELOPMENTSMonetary Policy Operations

11

Table 2: Key Liquidity Influences (K’ billion)

2017 Q2 2017 Q3 2017 Q4

Opening balance 0.8 0.3 0.7

Net Govt. spending 1.3 1.5 2.6

BoZ FX influence 1.8 1.1 1.0

CIC -0.7 0.1 -0.4

Change in SR deposits -0.4 -0.9 -2.2

OLF 0.0 -0.7 -0.9

Net Govt securities influence -2.4 -1.1 -0.5

Open market operations -0.3 0.3 1.0

Miscellaneous 0.0 0.0 0.0

Closing balance 0.3 0.7 1.4

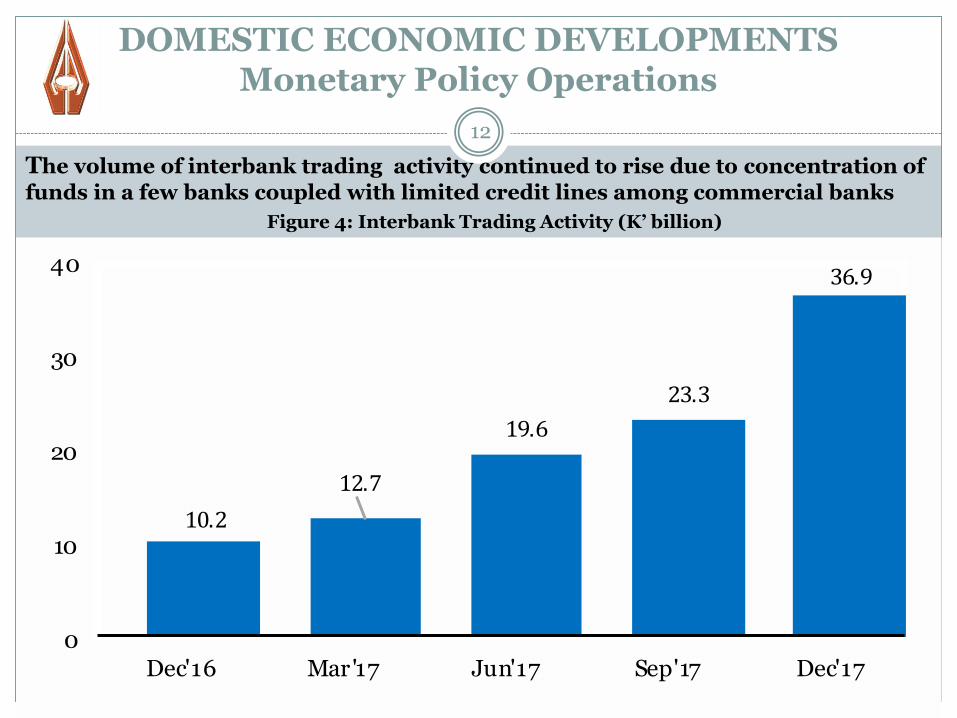

DOMESTIC ECONOMIC DEVELOPMENTSMonetary Policy Operations

12

Figure 4: Interbank Trading Activity (K’ billion)

The volume of interbank trading activity continued to rise due to concentration of

funds in a few banks coupled with limited credit lines among commercial banks

10.2

12.7

19.6

23.3

36.9

0

10

20

30

40

Dec'16 Mar'17 Jun'17 Sep'17 Dec'17

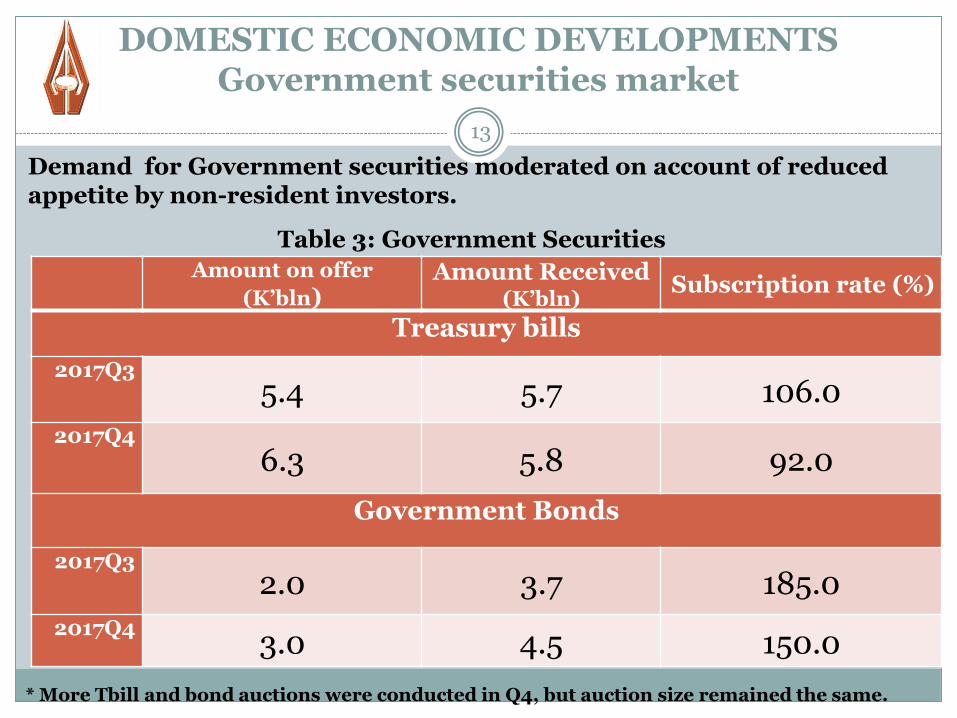

DOMESTIC ECONOMIC DEVELOPMENTSGovernment securities market

13

Table 3: Government Securities Auctions

Demand for Government securities moderated on account of reduced appetite by non-resident investors.

* More Tbill and bond auctions were conducted in Q4, but auction size remained the same.

Amount on offer

(K’bln)Amount Received

(K’bln) Subscription rate (%)

Treasury bills

2017Q35.4 5.7 106.0

2017Q4

6.3 5.8 92.0

Government Bonds

2017Q32.0 3.7 185.0

2017Q43.0 4.5 150.0

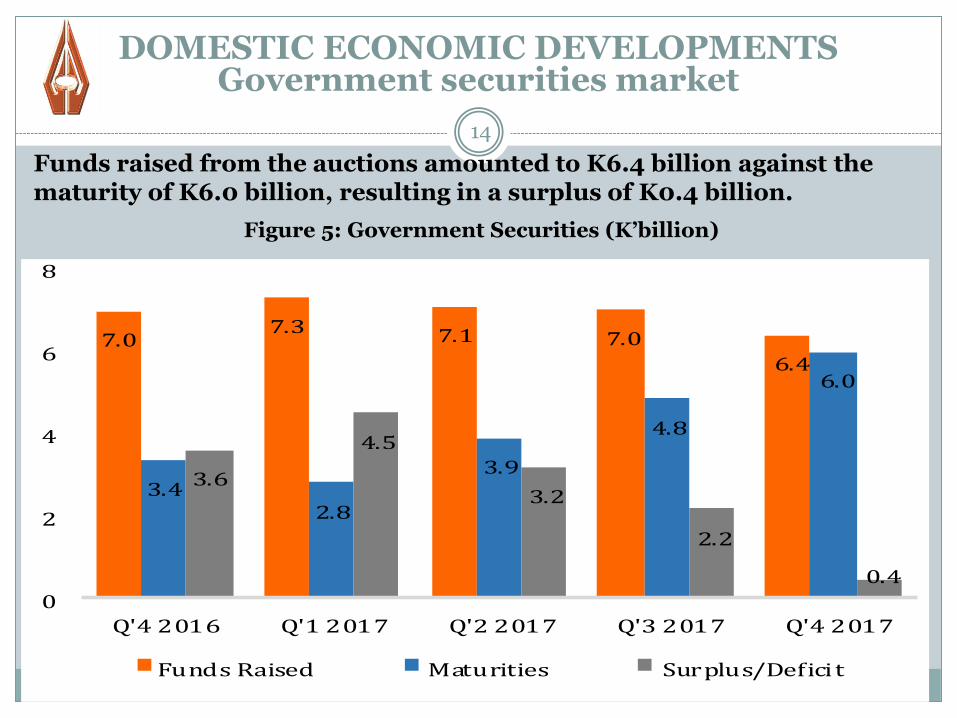

Funds raised from the auctions amounted to K6.4 billion against the maturity of K6.0 billion, resulting in a surplus of K0.4 billion.

14

Figure 5: Government Securities (K’billion)

DOMESTIC ECONOMIC DEVELOPMENTSGovernment securities market

7.07.3 7.1 7.0

6.4

3.42.8

3.9

4.8

6.0

3.6

4.5

3.2

2.2

0.4

0

2

4

6

8

Q'4 2016 Q'1 2017 Q'2 2017 Q'3 2017 Q'4 2017

Funds Raised Maturities Surplus/Deficit

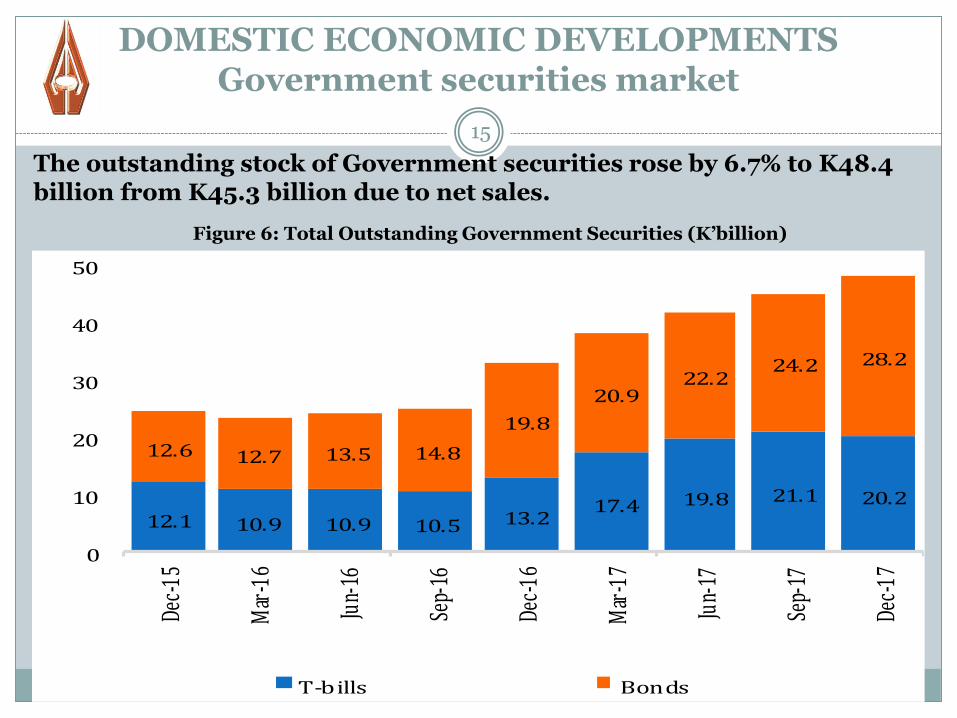

DOMESTIC ECONOMIC DEVELOPMENTSGovernment securities market

15

The outstanding stock of Government securities rose by 6.7% to K48.4 billion from K45.3 billion due to net sales.

Figure 6: Total Outstanding Government Securities (K’billion)

12.1 10.9 10.9 10.5 13.217.4 19.8 21.1 20.2

12.6 12.7 13.5 14.8

19.8

20.922.2

24.2 28.2

0

10

20

30

40

50

Dec-

15

Mar

-16

Jun-

16

Sep-

16

Dec-

16

Mar

-17

Jun-

17

Sep-

17

Dec-

17

T-bills Bonds

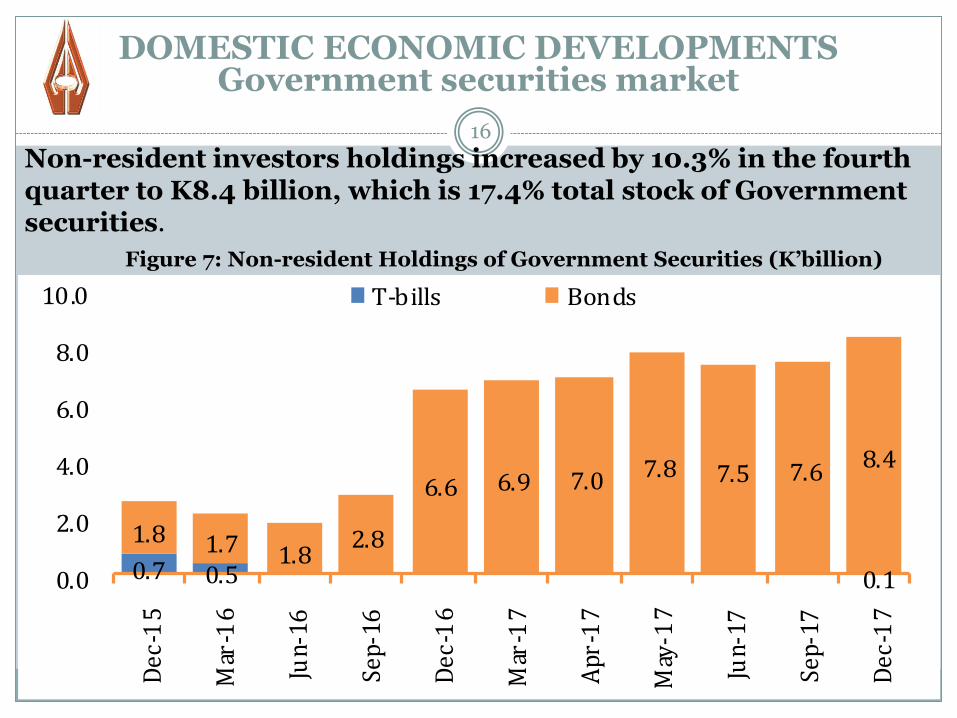

16

Figure 7: Non-resident Holdings of Government Securities (K’billion)

DOMESTIC ECONOMIC DEVELOPMENTSGovernment securities market

Non-resident investors holdings increased by 10.3% in the fourth quarter to K8.4 billion, which is 17.4% total stock of Government securities.

0.7 0.5 0.1

1.8 1.7 1.82.8

6.6 6.9 7.0 7.8 7.5 7.68.4

0.0

2.0

4.0

6.0

8.0

10.0

Dec

-15

Mar

-16

Jun-

16

Sep-

16

Dec

-16

Mar

-17

Apr

-17

May

-17

Jun-

17

Sep-

17

Dec

-17

T-bills Bonds

DOMESTIC ECONOMIC DEVELOPMENTSGovernment securities market

17

Movements in yield rates on Government securities were mixed in the fourth quarter, with yield rates on Treasury bills remaining virtually unchanged while yield rates on Government bonds edged upwards (Figure 8).

The weighted average Treasury bills yield rate closed the fourth quarter at 15.0%, same level as at end-September 2017.

However, the weighted average yield rate on Government bonds rose to 18.6% from 17.2%.

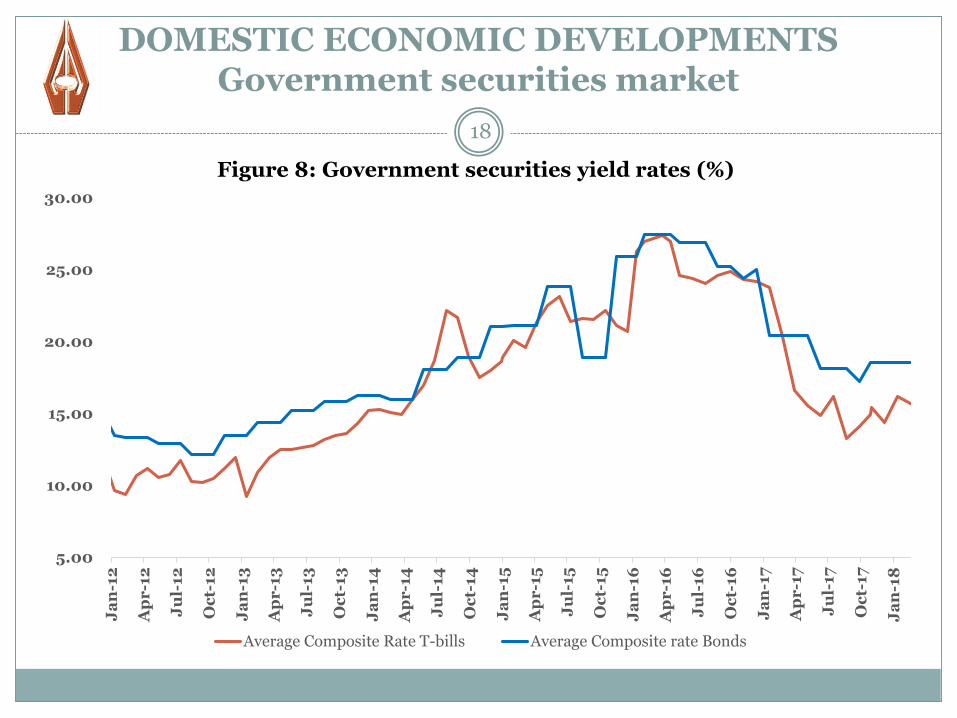

DOMESTIC ECONOMIC DEVELOPMENTSGovernment securities market

18

Figure 8: Government securities yield rates (%)

5.00

10.00

15.00

20.00

25.00

30.00

Ja

n-1

2

Ap

r-1

2

Ju

l-12

Oc

t-12

Ja

n-1

3

Ap

r-1

3

Ju

l-13

Oc

t-13

Ja

n-1

4

Ap

r-1

4

Ju

l-14

Oc

t-14

Ja

n-1

5

Ap

r-1

5

Ju

l-15

Oc

t-15

Ja

n-1

6

Ap

r-1

6

Ju

l-16

Oc

t-16

Ja

n-1

7

Ap

r-1

7

Ju

l-17

Oc

t-17

Ja

n-1

8

Average Composite Rate T-bills Average Composite rate Bonds

DOMESTIC ECONOMIC DEVELOPMENTSBanks’ Nominal Interest Rates

19

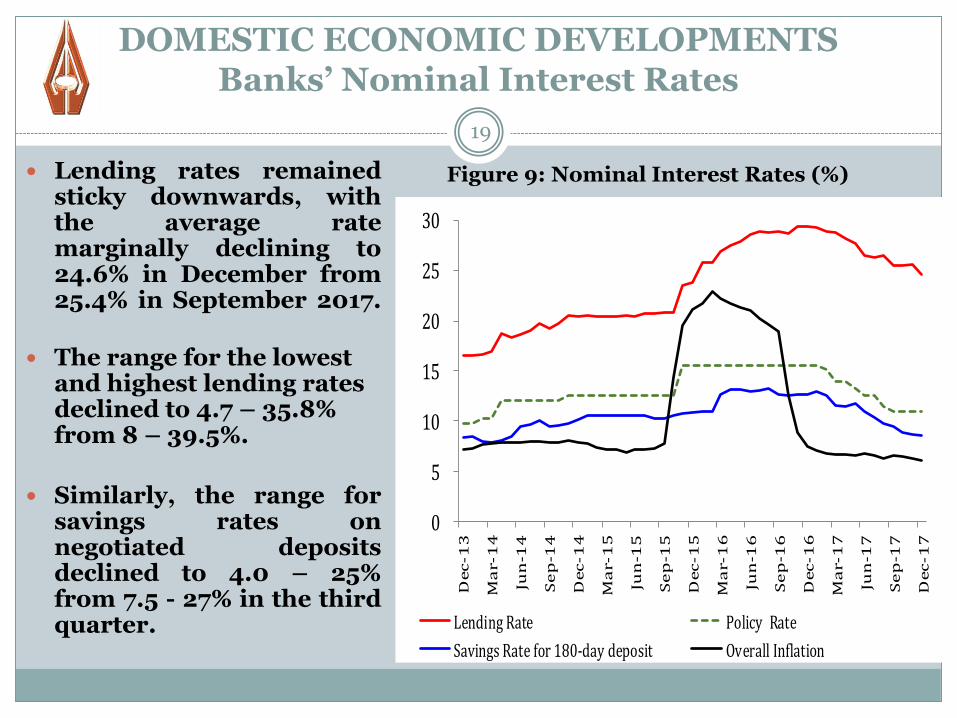

Lending rates remainedsticky downwards, withthe average ratemarginally declining to24.6% in December from25.4% in September 2017.

The range for the lowest and highest lending rates declined to 4.7 – 35.8% from 8 – 39.5%.

Similarly, the range forsavings rates onnegotiated depositsdeclined to 4.0 – 25%from 7.5 - 27% in the thirdquarter.

Figure 9: Nominal Interest Rates (%)

0

5

10

15

20

25

30

Dec-1

3

Ma

r-1

4

Jun

-14

Se

p-1

4

Dec

-1

4

Ma

r-1

5

Jun

-15

Se

p-1

5

Dec

-1

5

Ma

r-1

6

Jun

-16

Se

p-1

6

Dec-1

6

Ma

r-1

7

Jun

-17

Se

p-1

7

Dec

-1

7

Lending Rate Policy Rate

Savings Rate for 180-day deposit Overall Inflation

DOMESTIC ECONOMIC DEVELOPMENTSMoney supply and credit

20

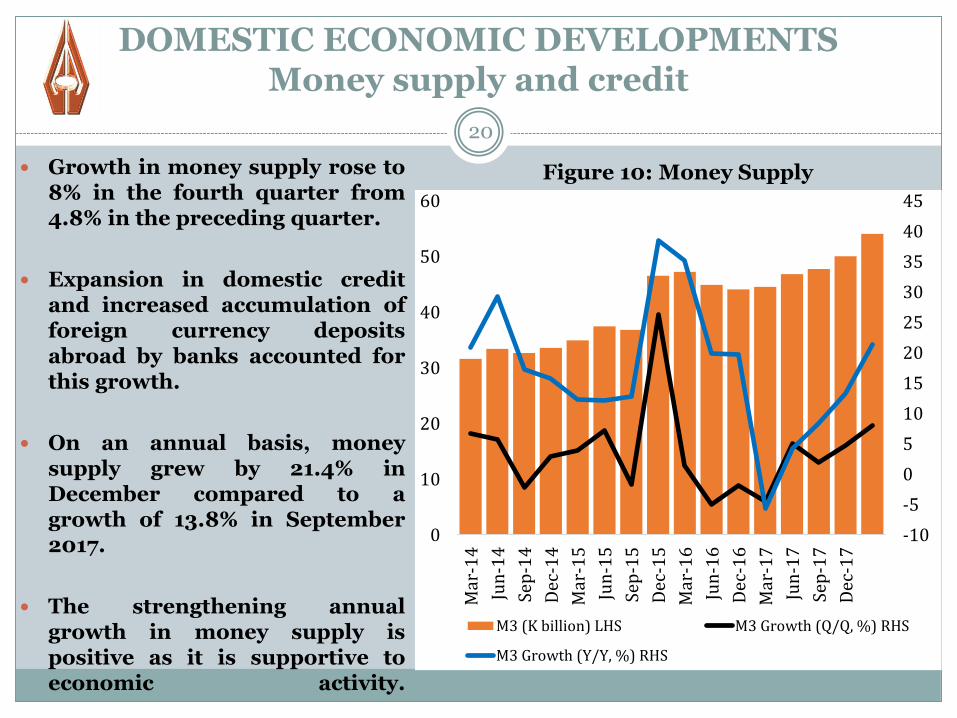

Growth in money supply rose to8% in the fourth quarter from4.8% in the preceding quarter.

Expansion in domestic creditand increased accumulation offoreign currency depositsabroad by banks accounted forthis growth.

On an annual basis, moneysupply grew by 21.4% inDecember compared to agrowth of 13.8% in September2017.

The strengthening annualgrowth in money supply ispositive as it is supportive toeconomic activity.

Figure 10: Money Supply

-10

-5

0

5

10

15

20

25

30

35

40

45

0

10

20

30

40

50

60

Mar

-14

Jun

-14

Sep

-14

Dec

-14

Mar

-15

Jun

-15

Sep

-15

Dec

-15

Mar

-16

Jun

-16

Dec

-16

Mar

-17

Jun

-17

Sep

-17

Dec

-17

M3 (K billion) LHS M3 Growth (Q/Q, %) RHS

M3 Growth (Y/Y, %) RHS

DOMESTIC ECONOMIC DEVELOPMENTSMoney supply and credit

21

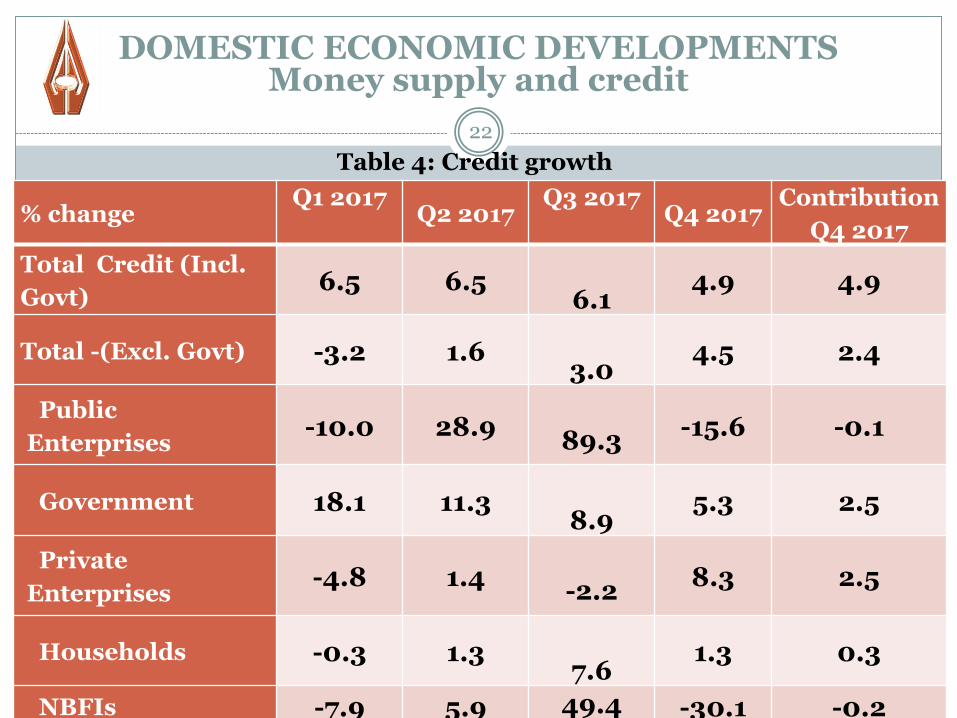

Total domestic credit continued to expand in the fourth quarter, albeit at a slower pace, growing by 4.9% compared to 6.1% in the third quarter (Table 4).

Growth in credit to Government further slowed down to 5.3% from 8.9%.

Credit to private enterprises grew by 8.3%, reversing a contraction of 2.2% in the third quarter.

However, growth in credit to households slowed down to 1.3% in the fourth quarter from a growth of 7.6% recorded in the third quarter.

Despite a pick up in growth in private sector credit, this growth remains below the levels required for sustaining strong private sector economic activity.

22

Table 4: Credit growth

DOMESTIC ECONOMIC DEVELOPMENTSMoney supply and credit

% changeQ1 2017

Q2 2017Q3 2017

Q4 2017Contribution

Q4 2017

Total Credit (Incl.

Govt)6.5 6.5

6.14.9 4.9

Total -(Excl. Govt) -3.2 1.6 3.0

4.5 2.4

Public

Enterprises-10.0 28.9

89.3-15.6 -0.1

Government 18.1 11.3 8.9

5.3 2.5

Private

Enterprises-4.8 1.4

-2.28.3 2.5

Households -0.3 1.3 7.6

1.3 0.3

NBFIs -7.9 5.9 49.4 -30.1 -0.2

23

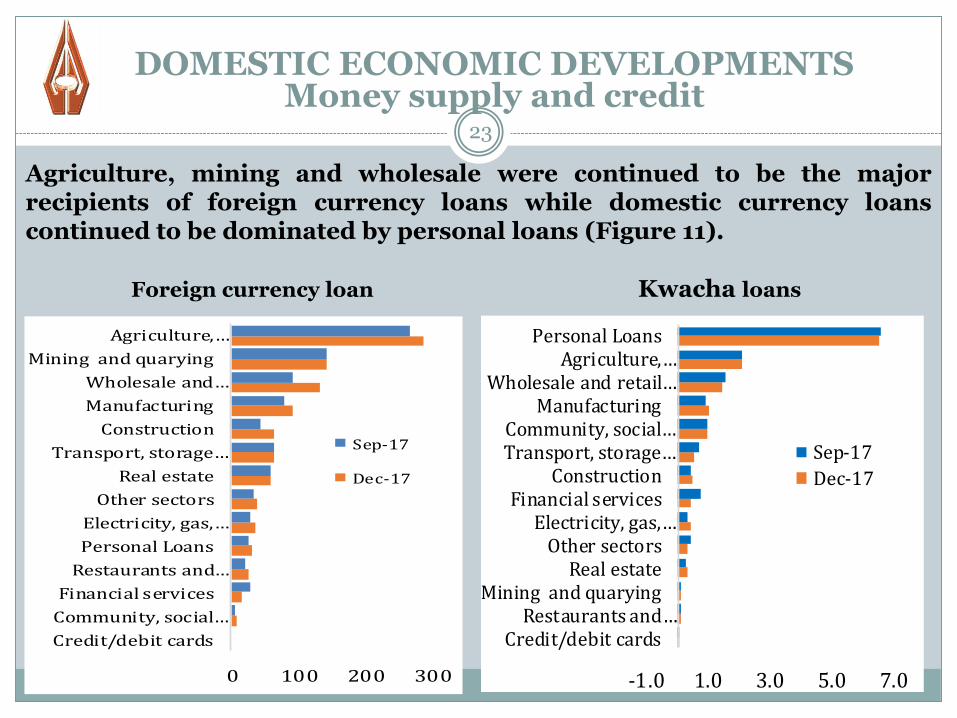

Agriculture, mining and wholesale were continued to be the majorrecipients of foreign currency loans while domestic currency loanscontinued to be dominated by personal loans (Figure 11).

DOMESTIC ECONOMIC DEVELOPMENTSMoney supply and credit

0 100 200 300

Credit/debit cards

Community, social…

Financial services

Restaurants and…

Personal Loans

Electricity, gas,…

Other sectors

Real estate

Transport, storage…

Construction

Manufacturing

Wholesale and…

Mining and quarying

Agriculture,…

Sep-17

Dec-17

-1.0 1.0 3.0 5.0 7.0

Credit/debit cardsRestaurants and…

Mining and quaryingReal estate

Other sectorsElectricity, gas,…

Financial servicesConstruction

Transport, storage…Community, social…

ManufacturingWholesale and retail…

Agriculture,…Personal Loans

Sep-17

Dec-17

Foreign currency loan Kwacha loans

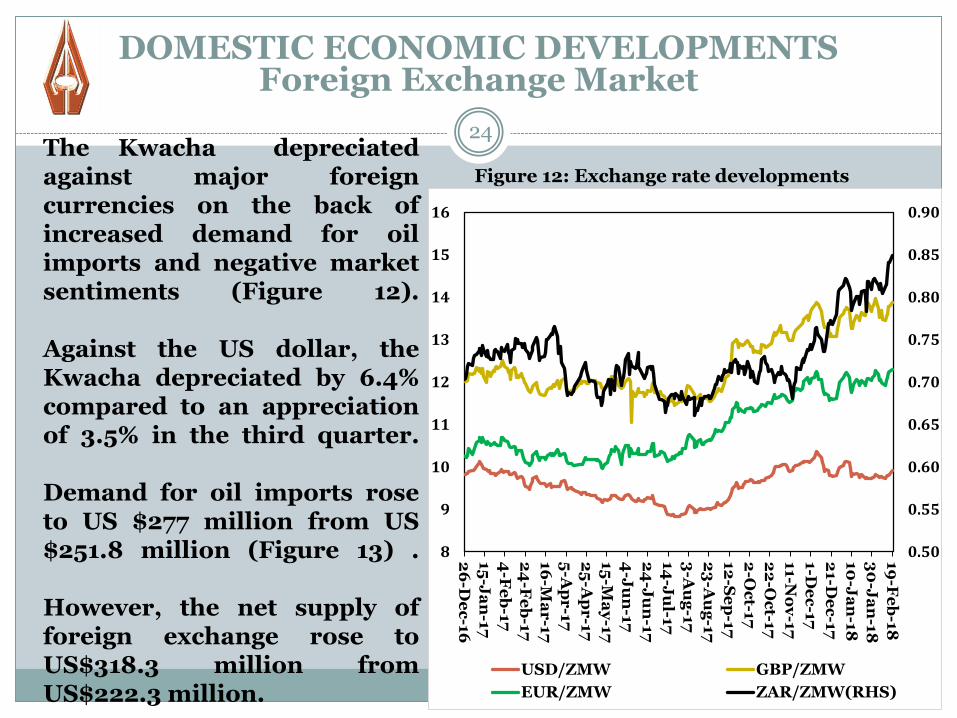

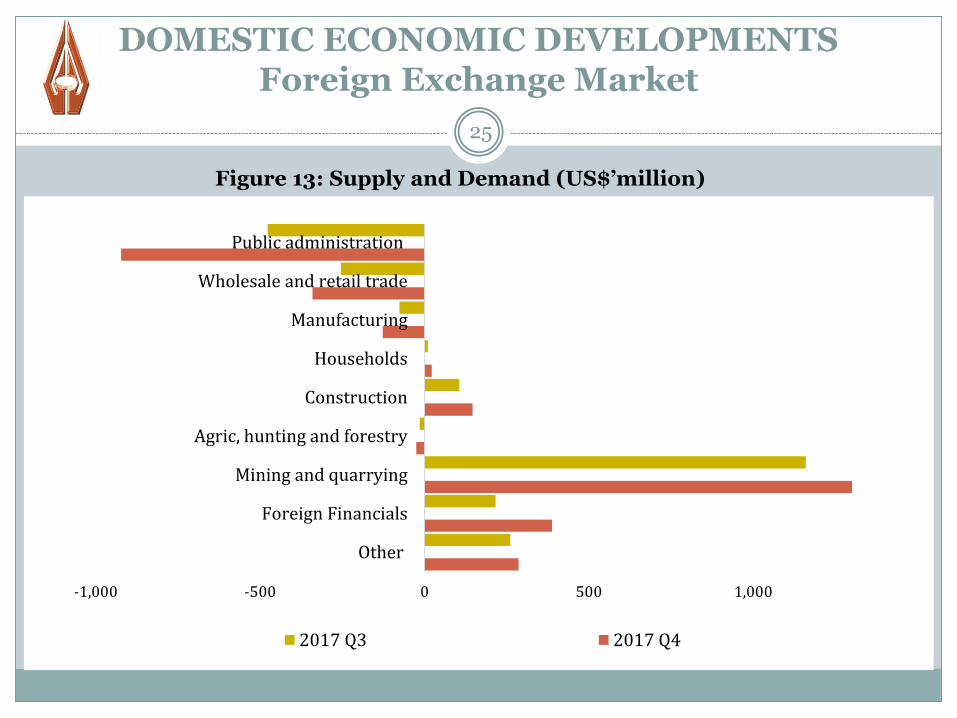

The Kwacha depreciatedagainst major foreigncurrencies on the back ofincreased demand for oilimports and negative marketsentiments (Figure 12).

Against the US dollar, theKwacha depreciated by 6.4%compared to an appreciationof 3.5% in the third quarter.

Demand for oil imports roseto US $277 million from US$251.8 million (Figure 13) .

However, the net supply offoreign exchange rose toUS$318.3 million fromUS$222.3 million.

24

Figure 12: Exchange rate developments

DOMESTIC ECONOMIC DEVELOPMENTSForeign Exchange Market

0.50

0.55

0.60

0.65

0.70

0.75

0.80

0.85

0.90

8

9

10

11

12

13

14

15

16

26

-De

c-1

6

15

-Ja

n-1

7

4-F

eb

-17

24

-Fe

b-1

7

16

-Ma

r-1

7

5-A

pr

-17

25

-Ap

r-1

7

15

-Ma

y-1

7

4-J

un

-17

24

-Ju

n-1

7

14

-Ju

l-17

3-A

ug

-17

23

-Au

g-1

7

12

-Se

p-1

7

2-O

ct-1

7

22

-Oc

t-17

11-N

ov

-17

1-D

ec

-17

21-D

ec

-17

10

-Ja

n-1

8

30

-Ja

n-1

8

19

-Fe

b-1

8

USD/ZMW GBP/ZMW

EUR/ZMW ZAR/ZMW(RHS)

DOMESTIC ECONOMIC DEVELOPMENTSForeign Exchange Market

25

Figure 13: Supply and Demand (US$’million)

-1,000 -500 0 500 1,000

Other

Foreign Financials

Mining and quarrying

Agric, hunting and forestry

Construction

Households

Manufacturing

Wholesale and retail trade

Public administration

2017 Q3 2017 Q4

DOMESTIC ECONOMIC DEVELOPMENTSReal Sector Activity

26

GDP is estimated to have grown by 3.3% in Q3 (3.2% in Q2), drivenby agriculture, education, and construction sectors.

Growth in 2017 has been slower than 2016 largely due to sluggishgrowth in construction and ICT sectors.

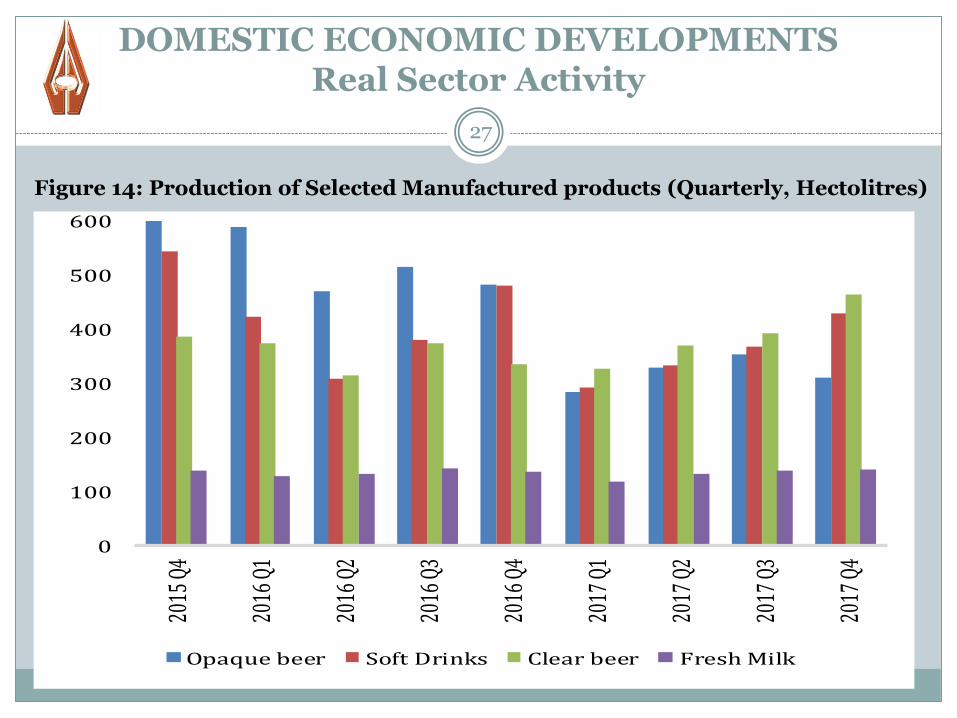

However, production of some manufactured products (food andbeverages, leather, chemicals, plastic and rubber basic andfabricated metals) rose in the fourth quarter (Figure 14).

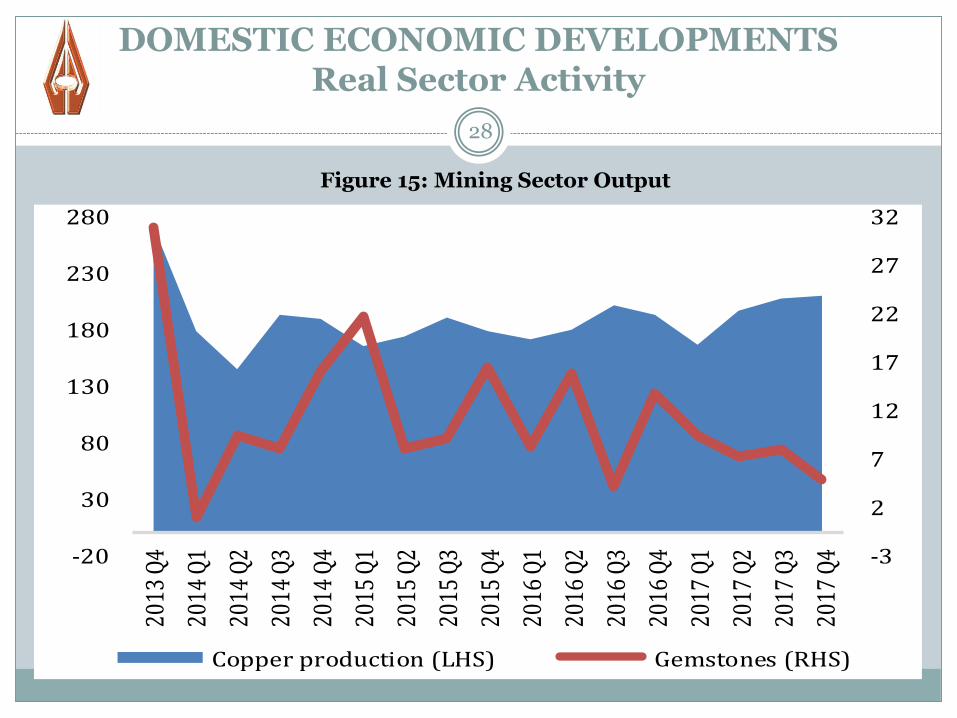

In addition, copper output at 786,731mt is estimated to havebeen 2% higher in 2017 than in 2016 (Figure 15).

27

DOMESTIC ECONOMIC DEVELOPMENTSReal Sector Activity

0

100

200

300

400

500

600

2015

Q4

2016

Q1

2016

Q2

2016

Q3

2016

Q4

2017

Q1

2017

Q2

2017

Q3

2017

Q4

Opaque beer Soft Drinks Clear beer Fresh Milk

Figure 14: Production of Selected Manufactured products (Quarterly, Hectolitres)

DOMESTIC ECONOMIC DEVELOPMENTSReal Sector Activity

28

Figure 15: Mining Sector Output

-3

2

7

12

17

22

27

32

-20

30

80

130

180

230

280

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

2016

Q2

2016

Q3

2016

Q4

2017

Q1

2017

Q2

2017

Q3

2017

Q4

Copper production (LHS) Gemstones (RHS)

DOMESTIC ECONOMIC DEVELOPMENTSReal Sector Activity

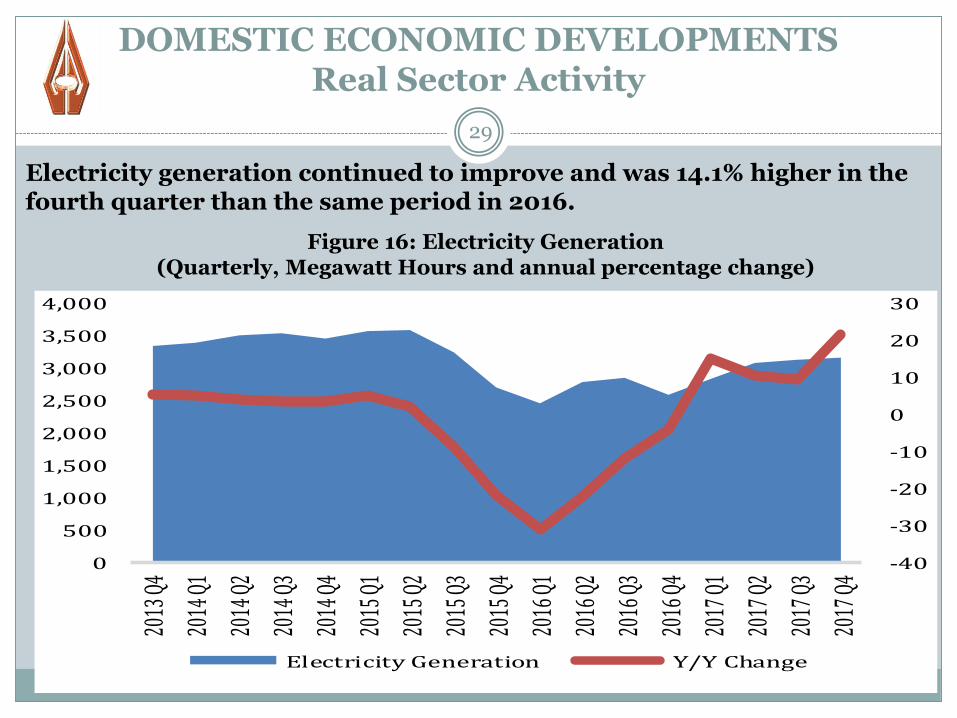

29

Figure 16: Electricity Generation (Quarterly, Megawatt Hours and annual percentage change)

Electricity generation continued to improve and was 14.1% higher in the fourth quarter than the same period in 2016.

-40

-30

-20

-10

0

10

20

30

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

2016

Q2

2016

Q3

2016

Q4

2017

Q1

2017

Q2

2017

Q3

2017

Q4

Electricity Generation Y/Y Change

30

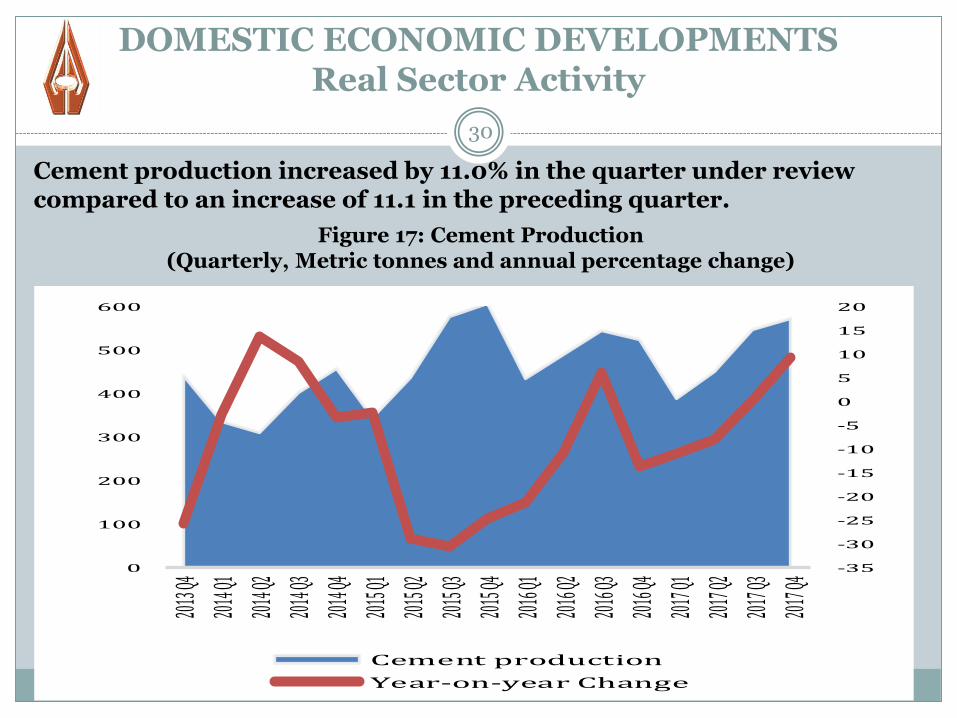

DOMESTIC ECONOMIC DEVELOPMENTSReal Sector Activity

Figure 17: Cement Production (Quarterly, Metric tonnes and annual percentage change)

Cement production increased by 11.0% in the quarter under review compared to an increase of 11.1 in the preceding quarter.

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

20

0

100

200

300

400

500

600

2013 Q

4

2014 Q

1

2014 Q

2

2014 Q

3

2014 Q

4

2015 Q

1

2015 Q

2

2015 Q

3

2015 Q

4

2016 Q

1

2016 Q

2

2016 Q

3

2016 Q

4

2017 Q

1

2017 Q

2

2017 Q

3

2017 Q

4

Cement production

Year-on-year Change

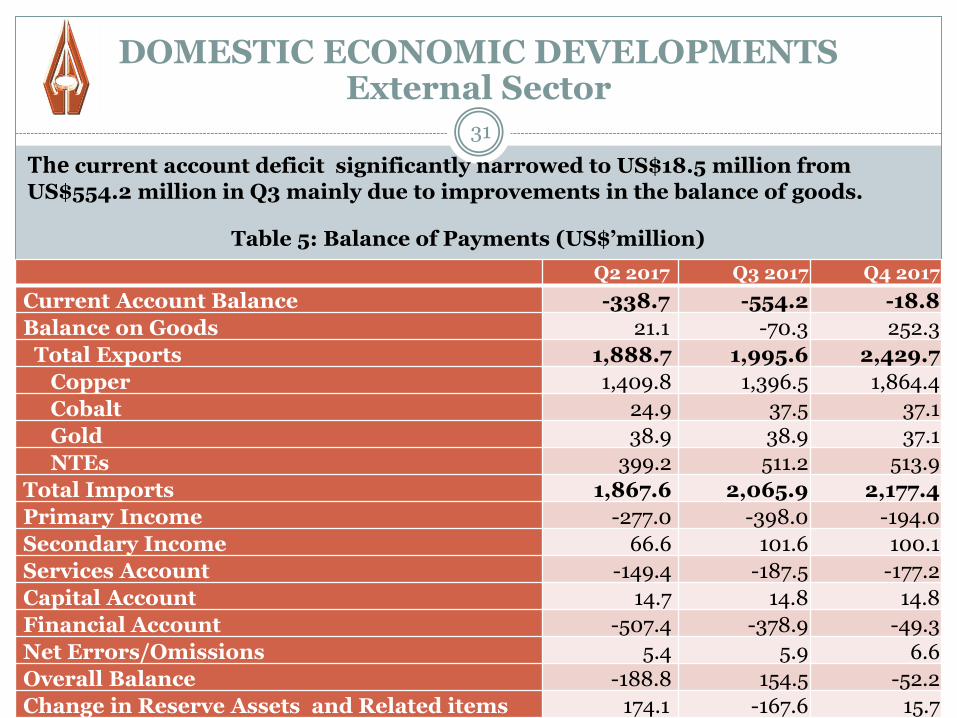

The current account deficit significantly narrowed to US$18.5 million from

US$554.2 million in Q3 mainly due to improvements in the balance of goods.

31

Table 5: Balance of Payments (US$’million)

DOMESTIC ECONOMIC DEVELOPMENTSExternal Sector

Q2 2017 Q3 2017 Q4 2017

Current Account Balance -338.7 -554.2 -18.8

Balance on Goods 21.1 -70.3 252.3

Total Exports 1,888.7 1,995.6 2,429.7

Copper 1,409.8 1,396.5 1,864.4

Cobalt 24.9 37.5 37.1

Gold 38.9 38.9 37.1

NTEs 399.2 511.2 513.9

Total Imports 1,867.6 2,065.9 2,177.4

Primary Income -277.0 -398.0 -194.0

Secondary Income 66.6 101.6 100.1

Services Account -149.4 -187.5 -177.2

Capital Account 14.7 14.8 14.8

Financial Account -507.4 -378.9 -49.3

Net Errors/Omissions 5.4 5.9 6.6

Overall Balance -188.8 154.5 -52.2

Change in Reserve Assets and Related items 174.1 -167.6 15.7

DOMESTIC ECONOMIC DEVELOPMENTSFiscal performance

32

Preliminary data indicate that Government spending remainedlower than budgeted in the fourth quarter due to shortfalls onnet external financing.

The deficit continued to be domestically financed throughGovernment securities.

In the fourth quarter, net domestic financing through issuanceof Government securities amounted to K2.5 billion, a declinefrom K3.0 billion in the third quarter.

DOMESTIC ECONOMIC DEVELOPMENTSInflation

33

During the fourth quarter, inflation declined to an average of 6.3% from 6.5% in third quarter of 2017.

In December, inflation was 6.1%, 0.5 percentage point lower than the September 2017 outturn of 6.6%. In January 2018, inflation marginally rose to 6.2% (Figure 18).

During the review period, both food and non-food inflationdeclined to averages of 4.8% and 7.8% from 5.1% and 8.1% in thethird quarter.

Abundant supply of food items and subdued demand in theeconomy accounted for the reduction in inflation in the fourthquarter of 2017.

34

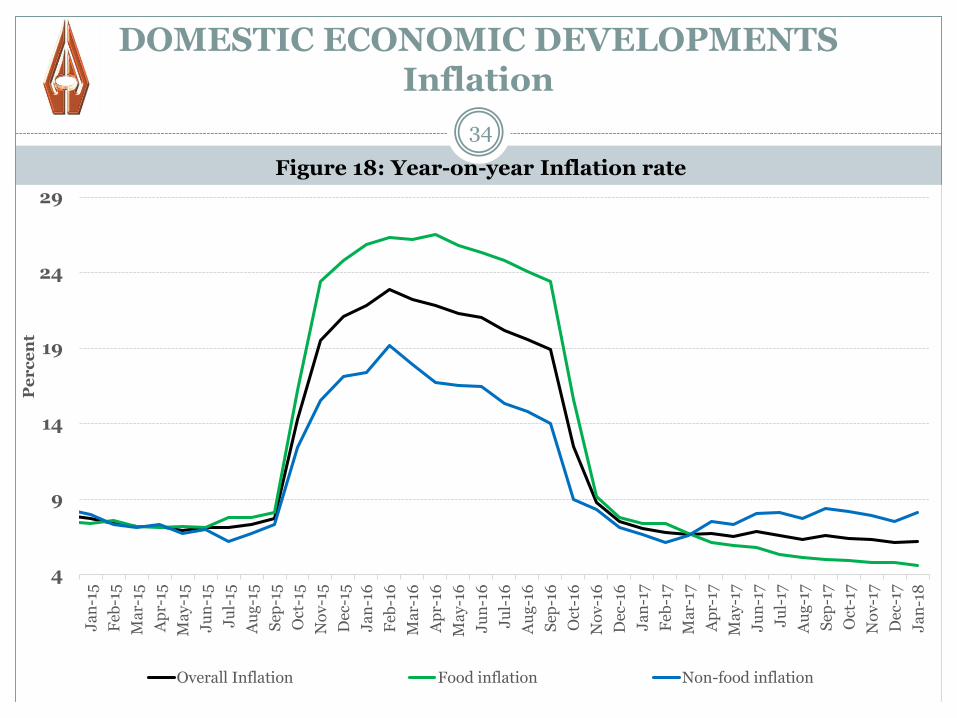

DOMESTIC ECONOMIC DEVELOPMENTSInflation

Figure 18: Year-on-year Inflation rate

4

9

14

19

24

29

Ja

n-1

5

Feb

-15

Ma

r-15

Ap

r-15

Ma

y-1

5

Ju

n-1

5

Ju

l-15

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5

Dec

-15

Ja

n-1

6

Feb

-16

Ma

r-16

Ap

r-16

Ma

y-1

6

Ju

n-1

6

Ju

l-16

Au

g-1

6

Sep

-16

Oct

-16

No

v-1

6

Dec

-16

Ja

n-1

7

Feb

-17

Ma

r-17

Ap

r-17

Ma

y-1

7

Ju

n-1

7

Ju

l-17

Au

g-1

7

Sep

-17

Oct

-17

No

v-1

7

Dec

-17

Ja

n-1

8

Pe

rc

en

t

Overall Inflation Food inflation Non-food inflation

DOMESTIC ECONOMIC DEVELOPMENTSInflation

35

However, month-on-month inflation rose to an average of0.8% from an average of 0.1% in the third quarter of 2017 (seeFigure 19).

In December 2017, monthly inflation was recorded at 0.7%, upfrom 0.3% in September 2017 reflecting a rise in both food andnon-food inflation.

seasonal factors accounted for the increase in food inflationwhile increase in the prices of petroleum products was themain driver of non-food inflation.

DOMESTIC ECONOMIC DEVELOPMENTSInflation

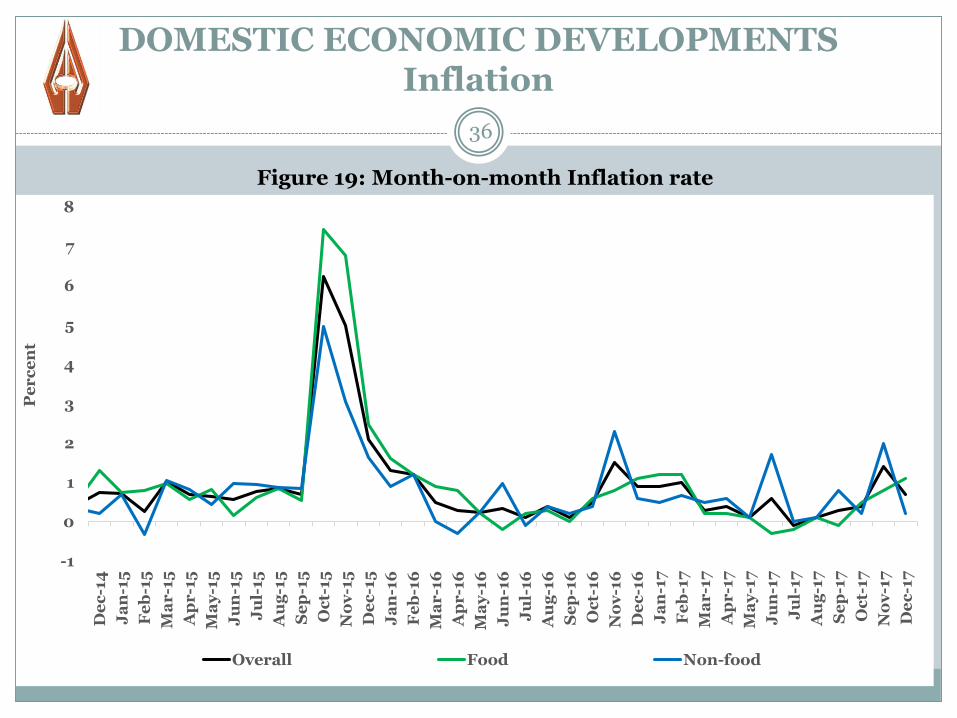

36

Figure 19: Month-on-month Inflation rate

-1

0

1

2

3

4

5

6

7

8

De

c-1

4

Ja

n-1

5

Fe

b-1

5

Ma

r-1

5

Ap

r-1

5

Ma

y-1

5

Ju

n-1

5

Ju

l-15

Au

g-1

5

Se

p-1

5

Oc

t-15

No

v-1

5

De

c-1

5

Ja

n-1

6

Fe

b-1

6

Ma

r-1

6

Ap

r-1

6

Ma

y-1

6

Ju

n-1

6

Ju

l-16

Au

g-1

6

Se

p-1

6

Oc

t-16

No

v-1

6

De

c-1

6

Ja

n-1

7

Fe

b-1

7

Ma

r-1

7

Ap

r-1

7

Ma

y-1

7

Ju

n-1

7

Ju

l-17

Au

g-1

7

Se

p-1

7

Oc

t-17

No

v-1

7

De

c-1

7

Pe

rc

en

t

Overall Food Non-food

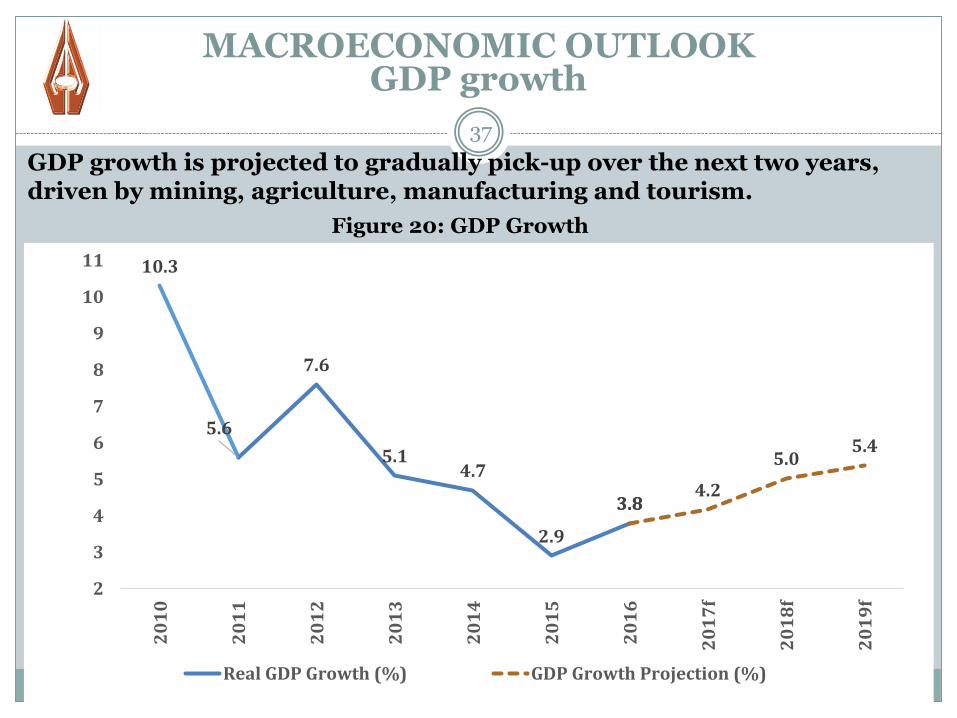

GDP growth is projected to gradually pick-up over the next two years, driven by mining, agriculture, manufacturing and tourism.

37

Figure 20: GDP Growth

MACROECONOMIC OUTLOOKGDP growth

10.3

5.6

7.6

5.14.7

2.9

3.83.84.2

5.05.4

2

3

4

5

6

7

8

9

10

11

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

f

20

18

f

20

19

f

Real GDP Growth (%) GDP Growth Projection (%)

MACROECONOMIC OUTLOOKInflation Outlook

38

Inflation is projected to remain low over the next eightquarters, around the 6% lower bound of the inflation targetrange.

However, risks to inflation are assessed to be on the upside,and these include the projected higher crude oil prices andpotentially lower agriculture production.

Despite these risks, inflation is projected to remain anchoredwithin the target range of 6-8% over the next two years.

39

In closing, the MPC noted that inflation has been decliningsince March 2016 following significant tightening of monetarypolicy in the fourth quarter of 2015.

Inflation projections have consistently been pointing to lowinflation, and this gave an opportunity to the MPC to commencethe loosening of monetary policy in February 2017.

This policy stance was and is still intended to support growthand promote financial stability.

The latest decision to further easy monetary policy should beseen in this context.

MACROECONOMIC OUTLOOKInflation Outlook

40

THANK YOU AND GOD BLESS…