Embed Size (px)

Citation preview

Monetary Policies in the United States since 1950: Some Implications of the Retreat toOrthodoxyAuthor(s): Ervin MillerSource: The Canadian Journal of Economics and Political Science / Revue canadienned'Economique et de Science politique, Vol. 27, No. 2 (May, 1961), pp. 205-222Published by: Wiley on behalf of Canadian Economics AssociationStable URL: http://www.jstor.org/stable/139141 .

Accessed: 19/06/2014 02:51

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

Wiley and Canadian Economics Association are collaborating with JSTOR to digitize, preserve and extendaccess to The Canadian Journal of Economics and Political Science / Revue canadienne d'Economique et deScience politique.

http://www.jstor.org

This content downloaded from 185.44.78.129 on Thu, 19 Jun 2014 02:51:29 AMAll use subject to JSTOR Terms and Conditions

MONETARY POLICIES IN THE UNITED STATES SINCE 1950: SOME IMPLICATIONS OF THE

RETREAT TO ORTHODOXY"

ERVIN MILLER University of Pennsylvania

MONETARY policy in the United States since 1950 has involved the abdication of fairly traditional powers by the authorities and a retreat to an orthodoxy reminiscent of the earlier years of this century. In the course of this retreat the monetary (and fiscal) authorities have sought to reduce federal debt to a quasi-private character, while, in contrast, the government has elevated vast amounts of private debt to a quasi-federal status. It will be argued here that in the light of the changing institutional environment, the drive to monetary orthodoxy plus an undue preoccupation with inflation are in large measure responsible for making exasperatingly difficult the maintenance of orderly Treasury finances and may be self-defeating with respect to the control of inflation.

I. THE HIsTORIcAL RECORD: SOME HIGHLIGHTS

The Drive for Quasi-Free Markets For our purposes, modern Federal Reserve policy has its roots in the bond

support policy of the Second World War. Actions taken after the War until 1950 showed an attitude of increasing restiveness with that policy and involved " chipping away" at individual items in the policy. With the outbreak of the Korean War in 1950, Federal Reserve relations with the Treasury, which sought to maintain a "pegged" market, reached a low point. In March, 1951, came the famous Accord,' with virtually unconditional surrender by the Treasury in matters of the level and structure of interest rates. In 1952 came the revival of large-scale discounting and the fostering of its use by the authorities.

In 1953 a series of important policies was adopted, some involving severe limitation of the area in which the monetary authorities were willing to co- ordinate actions with the Treasury. The authorities abandoned the policy (dating back to 1937) of "maintaining orderly conditions in the government security market," and substituted a policy of "correcting a disorderly situation in the government securities market." They adopted the now famous "bills- only" policy (or "bills-preferably" in current Federal Reserve phraseology), that is, the policy that, "except in the correction of disorderly markets," open

*This paper was written while the author held a Ford Foundation fellowship. The Foundation, of course, has no responsibility for the conclusions, opinions or other statements in it.

'For a detailed discussion of the period beginning with the Accord, see Asher Achin- stein, Federal Reserve Policy and Economic Stability, 1951-1957, Report prepared for the Committee on Banking and Currency, Senate (Washington, 1958).

205

Vol. XXVII, no. 2, May, 1961

This content downloaded from 185.44.78.129 on Thu, 19 Jun 2014 02:51:29 AMAll use subject to JSTOR Terms and Conditions

206 Canadian Journal of Economics and Political Science

market operations were to be conducted in short-term securities, essentially bills. The authorities no longer supported Treasury securities during offering periods. Finally, the Open Market Committee directed that

transactions for the System account in the open market shall be entered into solely for the purpose of providing or absorbing reserves (except in the correction of dis- orderly markets), and shall not include offsetting pulrchases and sales of securities for the purpose of altering the maturity pattern of the System's portfolio.2

Thus a security in short supply in the market would not be sold by the Reserve authorities with an offsetting purchase of one in plentiful supply. Meanwhile the determination of the authorities-Federal Reserve and Treasury-to bring about what they viewed as free markets in government securities and in the money markets generally was expressed not only in actions but in public pronouncements by high officials.

Another significant development was the apparent determination of the authorities to move to secularly lower levels of reserve requirements.3 Aside from other considerations, this would presumably involve less 'interference in the allocation of resources by banks and less participation by the central bank in the market for Treasury securities. Finally, there was a clear break by the authorities with selective credit controls other than on security market credit.

The Drive Again-st Inflation The overwhelming concern of our monetary authorities in recent years with

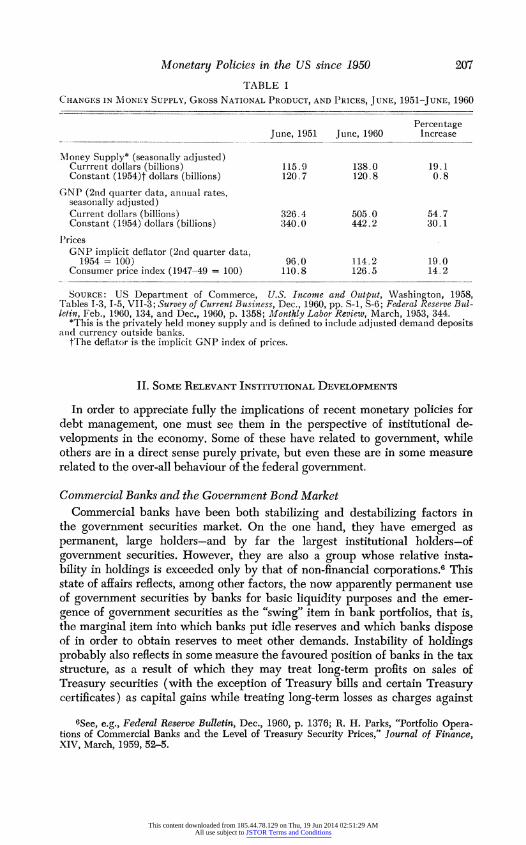

the problems of inflation is so familiar that documentation of the record is hardly necessary. The quantitative impact of the Federal Reserve Board's restraint on the growth of the money supply relative to certain other economic magnitudes may be seen in Table I.

The fact appears to be that the Board has subordinated full employment as a goal of policy. This seems evident from its willingness to "tighten the vice" in the presence of appreciable excess capacity both at the end of prosperity in 1956-7 and in the recovery of 1958-9. Between January and July, 1957, as money was becoming tighter, seasonally adjusted unemployment was less than 4 per cent in only one month, whereas in all of 1956 in only one month was it as high as 4 per cent.4 At the end of 1958, as money was tightening, seasonally adjusted unemployment was 6.1 per cent and by March, 1959, was still 5.8 per cent.5

2Annual Report of the Board of Governors of the Federal Reserve System, 1953, 103. See also 6-8, 86-105.

3Although the Reserve Board chairman has denied having this goal, he in fact has virtually acknowledged it by indirection. (See Employment, Growth, and Price Levels, Hearings, Joint Economic Committee, part 6C (Washington, 1959), 1777; see also part 6A, 1458, 1465-6.)

4See US Dept. of Commerce, Business Statistics, 1959 (Washington), 59. The recession "had been preceded by a major expansion in productive capacity without a corresponding increase in utilization. . . . In manufacturing alone spending on new plant and equipment between 1953 and 1957 had increased capacity by about one-fourth, but production had increased by only 7 per cent." Economic Report of the President, Jan., 1959 (Washington), 3, 12.

WFederal Reserve Bulletin, Dec., 1959, p. 1536.

This content downloaded from 185.44.78.129 on Thu, 19 Jun 2014 02:51:29 AMAll use subject to JSTOR Terms and Conditions

Monetary Policies in the US since 1950 207

TABLE I

CHANGES IN MONFE,Y SUPPLY, GROSS NATIONAL PRODUCT, AND PRICES, JUNE, 1951-JUNE, 1960

Percentage June, 1951 june, 1960 Increase

M1\oney Supply* (seasonally adjusted) Currrenit dollars (billionis) 115.9 138.0 19.1 Constant (1954)t dollars (billions) 120.7 120.8 0.8

GNP (2nd quarter data, anntiual rates, seasonially adjusted) Currenit dollars (billions) 326.4 505.0 54.7 Constant (1954) dollars (billions) 340.0 442.2 30.1

P'rices GNP implicit deflator (2nd quarter data,

1954 = 100) 96.0 114.2 19.0 Consumer price index (1947-49 = 100) 110.8 126.5 14.2

SOURCE: US Department of Commerce, U.S. Income and Output, Washington, 1958, TIables 1-3, 1-5, VII-3; Survey of Current Business, Dec., 1960, pp. S-i, S-6; Federal Reserve Bul- letin, Feb., 1960, 134, and Dec., 1960, p. 1358; Monthly Labor Review, March, 1953, 344.

*This is the privately held money supply aIld is defined to inicluide adjuLsted demand deposits anid currency outside batnks.

tThe deflator is the implicit GNP index of prices.

II. SOME RELEVANT INSTITUTIONAL DEVELOPMENTS

In order to appreciate fully the implications of recent monetary policies for debt management, one must see them in the perspective of institutional de- velopments in the economy. Some of these have related to government, while others are in a direct sense purely private, but even these are in some measure related to the over-all behaviour of the federal government.

Commercial Banks and the Government Bond Market Commercial banks have been both stabilizing and destabilizing factors in

the government securities market. On the one hand, they have emerged as permanent, large holders-and by far the largest institutional holders-of government securities. However, they are also a group whose relative insta- bility in holdings is exceeded only by that of non-financial corporations.6 This state of affairs reflects, among other factors, the now apparently permanent use of government securities by banks for basic liquidity purposes and the emer- gence of government securities as the "swing" item in bank portfolios, that is, the marginal item into which banks put idle reserves and which banks dispose of in order to obtain reserves to meet other demands. Instability of holdings probably also reflects in some measure the favoured position of banks in the tax structure, as a result of which they may treat long-term profits on sales of Treasury securities (with the exception of Treasury bills and certain Treasury certificates) as capital gains while treating long-term losses as charges against

6See, e.g., Federal Reserve Bulletin, Dec., 1960, p. 1376; R. H. Parks, "Portfolio Opera- tions of Commercial Banks and the Level of Treasury Security Prices," Journal of Finance, XIV, March, 1959, 52-5.

This content downloaded from 185.44.78.129 on Thu, 19 Jun 2014 02:51:29 AMAll use subject to JSTOR Terms and Conditions

208 Canadian Journal of Economics and Political Science

current income.7 Thus, banks may sell Treasury securities at a maximum capital gains tax of 25 per cent on long-term (over six months) profits while long-term losses are shared by the Treasury to the extent of 52 per cent. In turn, banks are presented with the opportunity of playing the game of "tax swaps," that is, the realization of capital losses on Treasury securities in order to reduce taxes on current income, with a concomitant switch into similar securities or a wait of thirty days prior to repurchasing the original or sub- stantially identical type of securities. They may then be in a position to establish long-term capital gains on a bargain tax basis.

Finally, since the economic environment induces bankers to operate largely in unison,8 there is good reason to believe that banks are probably the most important private participant in the price-making process for government securities.9

The Strengthened Competitive Position of the Market for Stocks vis-a-vis the Market for Treasury Securities

Important to the plight of the Treasury in managing its debt is a group of developments related to the competitive pressures of other areas for the financial savings of society.10 One important area is the market for common stocks. Perhaps most spectacular here has been the popularization and enor- mous growth of the open-end investment company, or so-called mutual fund."1 Aside from the obvious direct competition given to the Treasury,12 mutual funds doubtless stimulate additional competition by introducing persons of modest means to common stocks and popularizing them as a direct outlet for savings.'3

7See Internal Revenue Code of 1954, sec. 582 (C); R. H. Parks, "Income and Tax Aspects of Commercial Bank Portfolio Operations in Treasury Securities," National Tax Journal, XI, March, 1958, 21-34; Ervin Miller, "Monetary Policy in a Changing World," Quarterly Journal of Economics, LXX, Feb., 1956, 31. For an interesting empirical study of tax losses of banks see Federal Reserve Bank of Kansas City Monthly Review, June, 1960, 9-16.

8See C. R. Whittlesey, "Monetary Policy and Economic Change," Review of Economic Statistics, XXXIX, Feb., 1957, 34.

9See R. H. Parks, Portfolio Operations of Commercial Banks in the U.S. Treasury Securities Market, unpublished PhD thesis, University of Pennsylvania, 1958, chaps. 2, 5, and Appendix B.

1OFor a picture of recent shifts in the relative importance of the various forms of financial assets held by specific sectors of the US economy, see flow of funds data, Federal Reserve Bulletin, Aug., 1960, 941-6.

11Industry assets grew from $1.3 billions at the end of 1945 to $15.8 billions at the end of 1959. (Arthur Wiesenberger, Investment Companies, 1960 ed. (New York), 94.)

12Admittedly, mutual funds also acquire US government securities, but the holdings tend to be minor in volume. For example, the largest mutual fund, Massachusetts Investors Trust, held only 0.1 per cent ($2.0 millions) of its assets in Treasury obligations at the end of 1959. On the other hand, another large unit, the Wellington Fund at the same time held 12.7 per cent ($128.7 millions) of its assets in Treasury obligations. The industry as a whole had an aggregate in cash, short-term holdings and US securities of $988.2 millions at the end of October, 1960. (See ibid., 389, 405, and National Association of Investment Com- panies, Open-End Company Monthly Statistics, Oct., 1960.)

13Mutual funds are also probably partly responsible for the mushrooming of investment clubs all over the country. In essence these are miniature mutual funds devoted to the investment of members' funds in common stocks on a regular basis. In a recent report

This content downloaded from 185.44.78.129 on Thu, 19 Jun 2014 02:51:29 AMAll use subject to JSTOR Terms and Conditions

Monetary Policies in the US since 1950 209

A similar indirect influence has been that of the monthly investment plan of the New York Stock Exchange. Although the dollar volume involved is not large,14 the over-all promotional effect for common stock purchases regardless of the medium used-monthly investment plan, mutual fund, or direct purchase -may be very important.

Another influence in diverting money to the market for stocks has probably been the employee pension fund, which has had spectacular growth in recent years. Those controlled by trustees are of chief importance in this connection, for here the leeway to devote assets to common stocks is greatest and this leeway has been utilized.15

Developments in personal trusts administered by the nation's banks and trust companies have been of some consequence in the market for common stocks. Not only has there been appreciable aggregate growth in recent years, but in addition trustees have successfully promoted common trust funds designed to appeal to persons of modest means and to facilitate investment in common stocks. In the aggregate, there has apparently been a heavy shift into common stocks,"' facilitated, no doubt, by a steady erosion throughout the United States in the once frequent requirement of fairly rigid adherence to legal lists for investment. There has been a steady widening in the use of the "prudent man" rule, according to which a trustee has freedom to select the types of securities and the specific issues.17

Life insurance companies are a force of growing importance in the market for common stocks. They have been assisted-by the liberalization of state laws

(New York Times, Jan. 10, 1960, sec. 3, pp. 1, 7) it was estimated that there were about 16,000 clubs in the US of which 56 per cent were less than two years old. Although total holdings (estimated to exceed $130,000,000) were not great, the "demonstration effect" may be an important stimulus to direct purchases of stocks by individuals.

14Total investment under this plan was over $154 million on Jan. 25, 1960 (New York Stock Exchange Fact Book, 1960, 30).

15Assets of these funds at book values at the end of 1959 were reported to be $25.3 billions by the SEC. Common stocks at book values represented 30 per cent of the port- folio, compared to 12 per cent in 1951. At market value common stocks at the end of 1959 represented 43 per cent of the total portfolio value. In 1959, 50 per cent of net receipts were used to buy common stocks. (US Securities and Exchange Commission, Statistical Bulletin, June, 1960, 3-6; June, 1959, 5.)

16A recent survey (American Bankers Association, 1958) of personal trust funds ad- ministered by US banks and trust companies indicated assets of nearly $50 billion. 61.7 per cent was in common stocks, 5.1 per cent in Treasury securities and 15.7 per cent in state and municipal securities. (See "$50 Billion in Personal Trusts," Trusts and Estates, 98, Aug., 1959, 736.) Fully comparable figures for earlier years are not available. How- ever, an estimate of growth has been made by linking this recent estimate to earlier ones (see Federal Reserve Bank of Philadelphia, Business Review, Oct., 1959, insert).

On the assumption that the proportionate asset mixes indicated in earlier estimates are reasonably accurate and that they may fairly be compared with the proportionate asset mix shown in the 1958 survey, the shift from Treasury securities may be shown. In 1949, it was estimated that 30 per cent of the assets of personal trust funds were in government securities, in contrast to the 5.1 per cent indicated for 1958. Meanwhile, the proportions of stocks held have moved up from 40 per cent to over 64 per cent. (See R. W. Goldsmith, Financial Intermediaries in the American Economy (Princeton, 1958), Table A-16, 384-5.) Obviously some of this movement is explained by capital gains.

17See M. A. Shattuck and J. F. Farr, An Estate Planner's Handbook (2nd ed., Boston, 1953), 157-64, for a brief account of the development of the "prudent man" rule in the United States.

This content downloaded from 185.44.78.129 on Thu, 19 Jun 2014 02:51:29 AMAll use subject to JSTOR Terms and Conditions

210 Canadian Journal of Economics and Political Science

governing their investment portfolios.18 Recently the drive by certain sectors of the industry for authorization of the sale of variable annuities scored a major breakthrough in New Jersey. This development is likely to be of considerable significance for the future of common stock purchases by life insurance companies.'-

The tax structure has strengthened the position of stocks vis-'a-vis Treasury bonds in the competition for the smaller saver's dollar. There is favoured treat- ment by exemption of the first fifty dollars in dividend income (or of a hundred dollars in the case of the joint return for husband and wife) and a tax credit of 4 per cent on additional dividend income.20 There is also, of course, the capital gains tax, which makes profits taxable at only half the rate applic- able to ordinary income (up to the 50 per cent bracket and thereafter at a flat 25 per cent maximum). In short, the smaller, middle-income saver who in recent years has bought stock which has risen along with the market as a whole has had full or partial tax-exemption on his dividend income plus "speculative" profits subject to only half the ordinary tax rate. On the other hand, a comparable buyer of series "E" US savings bonds would have been subject to the full regular tax on income payable either currently or upon redemption of bonds. Needless to add, tax considerations also make common stocks much more attractive than Treasury securities to large, upper-income savers.

Finally, there is an intangible factor that may well be of some importance in the competition provided by the stock market to the market for government securities. This is the fact that great proportions of investment monies are administered with more skill than ever before. The great growth of institutional investors is particularly relevant here, but it is probably also true that the general public is better educated with respect to the implications of govern- mental economic and financial policies. For example, the fact that the federal government is in a real sense committed to preventing a major depression may well influence institutional investors and the general public to allocate more funds than would otherwise be the case to common stocks.

The Strengthened Competitive Position of Other Debt Markets vis-a-vis the Market for Government Bonds

Well-known developments in the markets for non-Treasury debt have also put pressures on the Treasury. For example, the government has conferred gilt-edge status on certain assets and enhanced the attractiveness of certain savings outlets for individuals through insurance of bank accounts and savings and loan association accounts, and through insurance and guaranty of mort- gages.2' In effect, the government has elevated private debts of home-buyers,

18Common stocks held by life insurance companies increased from $357 million to $2.954 billion between the end of 1947 and the end of 1959 at market values. (Institute of Life Insurance, 1960 Life Insurance Fact Book (New York), 79.) In 1959 the gain in common stocks held was $406 million of which roughly one-third represented capital gains.

19See G. E. Johnson, "The Future of Variable Annuities" in Trusts and Estates, 98, Nov., 1959, pp. 1086-8.

2OInternal Revenue Code of 1954, secs. 34, 116. 2lInsured and guaranteed mortgages outstanding on non-farm 1- to 4-family properties

as of September, 1960, were estimated to be $55.8 billion. (Federal Reserve Bulletin, Dec., 1960, p. 1383.) Insured project mortgages outstanding were estimated to be $5.4 billion at

This content downloaded from 185.44.78.129 on Thu, 19 Jun 2014 02:51:29 AMAll use subject to JSTOR Terms and Conditions

Monetary Policies in the US since 1950 211

project developers, and savings institutions to virtual qualitative equality with Treasury debt,22 and has sharply raised the total effective demand for mortgage money (through measures to lower its cost and improve the convenience of contracts).

Housing bonds, issued by local communities with the equivalent of a full guarantee by the federal government and having the added attraction of being tax-exempt, have gradually attained some importance in the investment world.23 Indeed, the whole tax-exempt sector of state and local government securities is particularly significant in view of its rapid growth and obvious appeal in a world of high taxes.24

While not one of the fastest-growing debt sectors, long-term corporate debt has nonetheless grown greatly since 1946, tripling in thirteen years, a period in which net federal debt increased very slightly. As a result, the corporate total was about 18 per cent of net federal debt at the end of 1946, but about 52 per cent of net federal debt at the end of 1959.25 Quantitatively, it is clear, the government bond market has been meeting rapidly increasing competition from this sector in recent years.26 Part of this competition, it is usually con- tended, stems from the corporations' ability to charge off interest as an expense in determining federal income taxes. Thus issuance of bonds is presumably favoured over preferred or common stock. Qualitatively, too, it is claimed that high-grade corporate bonds have been competing with Treasury issues more closely. As a result the differentials in yield have diminished in recent years.27

the end of 1959 (Housing and Home Finance Agency, Thirteenth Annual Report, 1959, 330).

22A dramatic illustration of the de facto acknowledgment of this may be seen in the attempt of the Treasury to exchange guaranteed and insured mortgages held by the Federal National Mortgage Association for outstanding Treasury debt. (See New York Times, Dec. 5, 1959, 31, 36.)

23As of Dec. 31, 1959, there were $2.5 billion in New Housing Authority bonds out- standing. They were first issued in 1951. (See Housing and Home Finance Agency, 13th Annual Report, 207.)

24The holding of Treasury securities by "personal trust accounts and individuals in the upper income brackets . . . declined . . . from $34 billion in December 1946 to $21 billion now. It is in this group where competition with tax-exempt state and local obligations becomes most important." Secretary of the Treasury Anderson, Public Debt Ceiling and Interest Rate Ceiling on Bonds, Hearings, Committee on Ways and Means, House of Representatives, June, 10-12, 1959 (Washington, 1959), 6. Meanwhile between 1946 and 1959 the net volume of state and local government debt outstanding rose from $13.6 billion to an estimated $55.6 billion (June 30 figures. See Survey of Current Business, July, 1960, 35).

25See ibid. and Economic Report of the President, Jan., 1960, 210. These figures over- state the case somewhat, since logically only high-grade corporate bonds should be com- pared with government bonds.

26The competition faced by the Treasury is shown by the shifts in the portfolios of the insurance sector of the flow of funds accounts. Between year-end 1946 and year-end 1959 federal obligations (in billions) fell from $27.0 to $16.6 while corporate bonds (in billions) rose from $15.1 to $62.6. (See Federal Reserve Bulletin, Aug., 1960, 945.)

27"Yield spreads between corporate and long-term Treasury bonds narrowed significantly during the postwar period as a whole and averaged very much less than spreads during the war or prewar period. Moody's indexes show that yields on long-term corporate Baa bonds averaged roughly 2-5 per cent in excess of yields on long-term Treasury bonds before World War II; the spread between corporate Aaa bonds and Treasury bonds averaged about 1 per cent. In contrast, by the 1950's the spread between corporate Baa bonds and Treasury bonds had narrowed to average a little over 1 per cent, while the spread between corporate Aaa bonds and Treasury bonds had narrowed to average less than one-half of 1 per cent." Parks, "Portfolio Operation," 60.

This content downloaded from 185.44.78.129 on Thu, 19 Jun 2014 02:51:29 AMAll use subject to JSTOR Terms and Conditions

212 Canadian Journal of Economics and Political Science

The extraordinary growth of consumer instalment credit (involving a recent large-scale spread to areas other than durable goods) has put pressure on Treasury finances. Not only have financing institutions competed with the Treasury in the issuing of securities, but banks have readily "dumped" government securities on a large scale to switch into consumer credit, as in 1955 and 1959.

Finally, one should note the partial responsibility of the federal government for some of the quantitative and qualitative developments in corporate, con- sumer, and state and local government debt (aside from the guarantees and tax exemption already noted) These developments cannot be adequately explained without reference to the government's role in maintaining an economic environment of considerable stability at generally high levels of aggregate demand. In addition the federal government has been an influence on state and local government by helping to stimulate acceptance of wider public responsibilities (largely through subsidies).

The Non-deflationary World Monetary policy and debt management have operated in a non-deflationary

world in recent years and there is little reason to expect that this environment will change greatly in the future. Here we should note briefly the quantitative magnitudes involved in the price movements and their significance. Omitting the inflation associated with the start of the Korean War, we use the period June, 1951, to June, 1960, to illustrate the past and to indicate possible ex- pectations with respect to the future. During this period (see Table I) the increase in consumer prices was at the rate of roughly 1.6 per cent per annum, measured by the June, 1951, price level.

However, those greatly concerned about the threat of inflation usually con- sider the period beginning with 1955 as most significant. Between June, 1955, and June, 1960, the consumer price index rose from 114.4 to 126.5, or about 2.4 per cent per annum, measured by the June, 1955, level. On this basis the threat would be somewhat greater than indicated above.

On the other hand, it is of questionable logic to infer the likelihood of long- term trends on the basis of such brief historical experiences. It does not follow that the forces primarily responsible for recent price developments will act in precisely the same fashion in the future. In this connection the changing be- haviour of the consumer price index between 1951 and 1960 is of interest. Using June index numbers and commencing with 1951-2, one finds that annual changes as a percentage of the index numbers of the preceding year are 2.3, 1.0, 0.5 -0.6, 1.6, 3.4, 2.9, 0.6, and 1.6. On the basis of these historical figures (and such insight and other information as may be mustered), who can say with confidence whether the future will bring another 1951-55, another 1955-60, an average of the entire period 1951-60, or some other configuration?

Not only are we interested in movements recorded by our indices, but we must be concerned about the reliability of those indices. Unfortunately, our measuring devices are imperfect; while fairly valid for measuring year-to-year changes, they are wholly inadequate for measuring a change over, say, ten years (assuming no degree of price change that is akin to hyper-inflation or is

This content downloaded from 185.44.78.129 on Thu, 19 Jun 2014 02:51:29 AMAll use subject to JSTOR Terms and Conditions

Monetary Policies in the US since 1950 213

obviously sharp). The defects involved are not only serious technically, but also-and very important-concern the probable inability of any price index to allow adequately for the continuous product improvement and product re- volutions of a modern dynamic industrial economy. Any statement indicating that the cost of living has risen, say, 10 per cent over a ten-year period, must be regarded as almost meaningless as a generalization for society. In such a period, for a given family, short-lived cottons and woollens may have given way to long-wearing synthetics or composite blends; the maid and commercial laundry may have given way to the automated home and to "wash and wear" fabrics; steel for home accessories may have given way to rust-proof and nearly maintenance-free aluminum. The truth is that even after allowing for offsetting forces such as quality deterioration or forced obsolescence, the con- sumer price index probably is biased upwards.28 We conclude that although the existence of the non-deflationary world must be acknowledged, the seriousness of inflationary threats has been exaggerated.

III. SOME RESPONSES OF THE MARKET AND SOME EFFECTS ON THE ECONOMY

From the interplay of institutional developments in the economy (including those in which government has had a hand) and actions by the monetary (and fiscal) authorities, a host of financial consequences have followed. Here we deal with some of the more important and less happy ones.

Instability in the Government Bond Market29 Central to this problem has been the attempt of the Federal Reserve to

bring a large measure of laissez-faire to a market that is inherently not free. The Treasury is the overwhelmingly dominant issuer of securities in the country, by far the dominant debtor of the country, and an important holder of its own issues.30 The Federal Reserve, another arm of the government, controls the money supply, the availability of a major share of credit in the country, and is a major holder of government securities. Abdication by government of any responsibility for the behaviour of the market in which it is a towering giant can only lead to increased instability and, at times perhaps, chaos in that market.

If the Federal Reserve authorities fail to support massive issues of govern- ment securities during their offering periods, "indigestion" of the security

28See A. E. Rees, "Price Level Stability and Economic Policy" in The Relationship of Prices to Economic Stability and Growth, Compendium, Joint Economic Committee (Wash- ington, 1958), 651-3; Richard Ruggles and N. D. Ruggles, "Prices, Costs, Demand and Output in the United States, 1947-57" in ibid., 297-308; Staff Report on Employment, Growth, and Price Levels, Joint Economic Committee (Washington, 1959), 106-9.

29For discussions of the instability in the government bond market, see Parks, Portfolio Operations of Commercial Banks in the U. S. Treasury Securities Market, chap. xv; Treasury- Federal Reserve Study of the Government Securities Market, Part I (Washington, 1959), 2-5, and Part II (Washington, 1960), 78; W. L. Smith, Debt Management in the United States, Study Paper No. 19, Joint Economic Committee (Washington, 1960), 63-4, 123-4.

3OAs of September 1960, US Government agencies and trust funds held $55.6 billion of Treasury obligations (Federal Reserve Bulletin, Dec., 1960, p. 1376).

This content downloaded from 185.44.78.129 on Thu, 19 Jun 2014 02:51:29 AMAll use subject to JSTOR Terms and Conditions

214 Canadian Journal of Economics and Political Science

markets can be the only logical result (assuming conditions of relatively good employment and relatively restrictive monetary policy). It should occasion no surprise, therefore, that in recent years it has been commonplace for new Treasury securities to fall below par virtually at time of issuance. If the Federal Reserve will not move into a security market until near-disaster is at hand, the authorities condemn the market-by definition-to greater instability.31

No matter how hard the Reserve authorities try to avoid being an influence in the market, they cannot succeed: neutrality is an impossibility! Their attempted abdication from the market simply means that a rudderless giant is being cast adrift in the high seas and other lesser vessels have little choice but to take appropriate evasive (or opportunistic) action to avoid a collision (or to gain some predatory end). Evasive action in the government securities market might mean that true savers would avoid acquiring government securities; opportunistic action might involve speculative operations in these securities. When one now adds the inducements provided by the tax laws to banks, the use by banks of Treasury securities as a large-scale "swing" item, the absence of legal margin requirements for transactions in government securities, and the professionalization and institutionalization of investment throughout the economy, it comes as little surprise that the US bond market is unstable. Moreover, the intermittent statements by Treasury and Federal Reserve officials have hardened the expectations of instability and, therefore, the realized instability in that market'2 Their very pronouncements that they will act as though the market were free must bring almost automatic reactions from a sophisticated market. In the particular case with which we deal, the opportunity for speculative forces to dominate the market is enhanced by the length of the period in which Federal Reserve policy has been retreating. The full financial implications of Federal Reserve policies have had sufficient time to become known even in non-professional circles and to minimize (although not eliminate) uncertainties for operators in the market.

The Federal Reserve's excessive concern for inflation has given speculative forces assistance in predicting and thus accentuating the movement of bond prices. This is especially true in view of the vast increase in the quantity of economic data available over the past generation, and because these data are being disseminated with growing rapidity (developments for which the federal government is mainly responsible). To illustrate, assume that the economy has been on a modest down-slide for some time (with bond prices rising) and that the figures pouring forth from our statistical factories indicate a turning point has been reached. Under the circumstances assumed one can expect a sharp reversal in bond prices. The market would presumably act in anticipation of a quick resumption of monetary pressure by the Federal Reserve authorities, for, given the preoccupation with inflation, the authorities, as indicated earlier, apparently feel that they must move long before any possible boom gets under way, even though unemployment may still be sub-

31For a discussion of the late and limited Federal Reserve intervention in the disorderly bond market of the summer of 1958, see Treasury-Federal Reserve Study of the Govern- ment Securities Market, Part I, 14-16, and Part II, 80-4.

32Cf. ibid., Part I, 3.

This content downloaded from 185.44.78.129 on Thu, 19 Jun 2014 02:51:29 AMAll use subject to JSTOR Terms and Conditions

Monetary Policies in the US since 1950 215

stantial, and despite the fact that no boom might ever materializel38 Were there not this idee fixe about inflation, were the authorities to consider each cycle and each cyclical phase separately on its own merits (that is, were there a truly flexible monetary policy and flexibility of policy formation rather than the almost automatic application of a policy pointed in an anti-cyclical direction), then the market would be more prone to adopt a "wait and see" course, for no longer would the central Bank's programme be viewed as a predictable "sitting duck" for speculators.

Stimulus to Market for Common Stocks In so far as the Reserve authorities have succeeded in limiting increases in

price levels and shown determination to act vigorously in this direction, they have doubtless had some salutary effect in restraining the spread of an infla- tionary psychology. On the other hand, through their apparent exaggeration of the inflationary threat and through the great and incessant publicity given to their stern appraisal of that threat, the Reserve authorities have probably offset that salutary effect. Indeed, on balance it appears to this writer that the Reserve activities have stimulated unduly the spread of the psychology of "inflation for ever." This has found its way throughout much of society and left an unfortunate imprint in the form of a widespread search by individual savers for a hedge against inflation. Needless to add, with the members of the New York Stock Exchange operating in high gear to sell everyone "shares in the future of America," with a tax law favouring capital gains and giving advantages on dividend income to stock-owing individuals, and with mutual funds waiting in the wings to bring the virtues of diversification and profes- sional management even to small savers, there is a clear stimulus to individuals to acquire common stocks.34

The successful efforts of important institutional investors to gain wider powers to invest have been prompted in part by the inflationary psychology. On earlier pages we have seen the consequences in the form of enlarged holdings of common stocks by personal trusts, pension funds, and insurance companies. Even without an inflationary psychology, however, the great economic growth and high levels of employment would probably have been sufficient to ensure a growing interest in common stocks and something of a stock market boom in the last ten years. In addition to these obvious pressures, the quasi-under-

33In the 1958 "turnabout" US bill rates rose from 0.881 to 2.814 between June and December! Yields on 3-5 year taxable government securities rose from 2.25 to 3.65 in the same period. Yields on long-term taxable government bonds rose from a low of 3.12 per cent in April to 3.84 per cent in December (Business Statistics, 1959, 86, 102).

In this connection, cf. the following from Committee on the Working of the Monetary System, Report, Cmnd. 827 (London, 1959), 208: "The importance of expectations in influencing the structure of interest rates and the level of interest rates has been stressed in economic literature, and the arguments commonly developed there afford some support for the monetary authorities in their stress on expectations. Our view is that expectations have been overrated as independent market forces, and that at times the influence of the authori- ties themselves on those expectations has been correspondingly underrated." (Italics mine) Cf. also Smith, Debt Management, 72-3.

34Estimates of the number of individual shareowners for 1952, 1956, and 1959, respec- tively are 6.5 million, 8.6 million, and 12.5 million (US Bureau of the Census, Statistical Abstract of the United States: 1960 (Washington, 1960), 469).

This content downloaded from 185.44.78.129 on Thu, 19 Jun 2014 02:51:29 AMAll use subject to JSTOR Terms and Conditions

216 Canadian Journal of Economics and Political Science

writing of high employment levels by government has apparently improved the quality of common stocks as investment media and hence their appeal to both institutional investors and individuals. With the addition of the inflation psychology to these other factors, long-run common stock prices appear to have been put on something of a skyward-bound escalator.

In short, the monetary (and fiscal) authorities have succeeded in increasing unduly the competitive disadvantage of the government vis-'a-vis the stock market in the race for savings.35

The Level of Interest Rates Institutional and other factors described on earlier pages have clearly been

an influence making for higher interest rates on federal obligations and, indeed, on many other debt claims. As we have seen, the government, partly because of its own behaviour (both desirable and undesirable), has met growing com- petition for funds. Monetary policies described earlier have also made for a generally higher level of interest rates. To the extent that Reserve policy accentuates the instability of government bond prices, it increases purchasers' risks, which implies higher interest costs to the Treasury. Indeed, the narrowing of spreads between government and high-grade corporate bonds in recent years may reflect as much (or more) the increase in short-term risk associated with government securities as it does the apparent improvement in quality of corporate bonds.36 If the basis for secular growth in the money supply is pro- vided mainly through lower reserve requirements rather than open market purchases, clearly a portion of the firm market for government securities is permanently removed. With the Federal Reserve's excessive preoccupation with inflation and its implications for monetary restriction, costs to the Treasury must on the average be pushed still higher. In a society committed to generally high employment levels, periods of falling economic activity will presumably be, on the average, relatively shorter-lived and have relatively smaller ampli- tude than in the past. In turn, since periods of rising economic activity pre- sumably carry the seeds of inflation in far greater measure, one can expect the ratio of tight to easy money spans to be greater than in the past.

The upshot of all this should be an average level of interest rates higher than would exist without the drive to orthodoxy and the excessive emphasis on inflation. Monetary policy may be thought of as being caught up in a develop- ment somewhat analogous to the popular conception of creeping inflation, with each period of rising economic activity leading to a higher level of interest

35An examination of total financial assets of the consumer and non-profit organizations sector in the flow of funds accounts shows corporate stock to have increased from 27.5 per cent at year-end 1946 to 44.1 per cent at year-end 1959, at market values. Dis- proportionate growth of stock holdings is also shown in the holdings of other important sectors. (See Federal Reserve Bulletin, Aug., 1960, 941-6.)

As indicated earlier, this situation reflects important amounts of capital gains on common stock which could be succeeded by capital losses. However, the pervasive nature of the movements over a considerable period of time helps to confirm the judgment that a secular realignment in the proportionate composition of the financial assets of society has been taking place.

36Cf. Staff Report on Employment, Grotwth, and Price Levels, 415-16, 426; cf. also Smith, Debt Management, 64-8.

This content downloaded from 185.44.78.129 on Thu, 19 Jun 2014 02:51:29 AMAll use subject to JSTOR Terms and Conditions

Monetary Policies in the US since 1950 217

rates than in the corresponding phase of the previous cycle and with each period of recession having interest rates falling, but to a higher minimum level than in the preceding recession.

Fiscal Implications If the arguments presented above are valid, it follows that cumulative net

interest costs to the federal government (and to non-federal governmental units) have been substantially higher than necessary in recent years, even assuming the desirability of generally restrictive policies.37 At the same time modest net amounts of income have probably been lost to the Treasury. For example, note the effect of inducing secular growth in the money supply mainly by lowering reserve requirements rather than through open market operations.88 Admittedly, to the extent that a lower level of reserve require- ments and an accompanying smaller Federal Reserve portfolio of Treasury securities implies higher interest rates on such securities, Federal Reserve earnings-and so the Treasury's large dollar share in them-will also rise and offset to an unknown extent the effect of a smaller portfolio.

It is usually argued that the losses on incremental Treasury outlays for interest (excluding intra-governmental) are much smaller on a net basis than implied by the budgetary expenditure statement, since the Treasury pre- sumably recoups in taxes much of the interest paid out. But this argument is, in large part, quite misleading. Not only may increased income of corporate bond-holders be used in part to raise expenses (such as salaries, interest on time deposits, and advertising expenses), but, as observed earlier, commercial banks may offset added income with capital losses taken in periods of tight money as they switch out of Treasury securities or engage in tax "swaps."89 On

37Net interest paid by the federal Government (i.e., total paid less total received) as shown in the national income accounts rose from $4.7 billion in 1951 to an annual rate (seasonally adjusted) of $7.3 billion in the third quarter of 1960 (preliminary). Net public debt (i.e., gross public debt minus holdings of agencies and trust funds) was $217.1 billion at year-end 1951 and $233.0 billion at the end of August, 1960. (See Treasury Bulletin, Nov., 1960, 1, 56; US Dept. of Commerce, U.S. Income and Output (Washington, 1958), 164; Survey of Current Business, Nov., 1960, 13.)

Highest grade state and local tax-exempt bonds have been selling in recent years at interest levels just a shade under those on US government bonds, which, of course, are fully taxable. For example, between October, 1958 and October, 1959, yields on long-term (ten years or more to maturity or call date) Treasury securities varied from a low of 3.76 per cent to a high of 4.26 per cent. Yields of highest grade (Moody's Aaa) state and local bonds during this period varied from a low of 3.06 per cent to a high of 3.60 per cent (Federal Reserve Bulletin, Nov., 1959, p. 1380). Implied here for the state and local govern- ment bonds are equivalent yields on taxable bonds of 6 to well over 7 per cent for corporate investors in the typical 52 per cent tax bracketl Cf. Staff Report on Employment, Growth, and Price Levels, which suggests that "tight money, by keeping the bank market from expanding more rapidly, has made it necessary for State and local governments to obtain funds from investors subject to lower tax rates than the 52 per cent applicable to com- mercial banks" (p. 385).

35See A. H. Hansen, "Bankers and Subsidies," Review of Economics and Statistics, XL, Feb., 1958, 50-1.

39As pointed out by Parks in "Income and Tax Aspects of Commercial Bank Operations in Treasury Securities," taxable profits and taxes paid by banks were both substantially less in prosperous 1955 than in recession-ridden 1954 (pp. 30-2). A comparison of the prosper- ous first half of 1959 (with tight money) with the recession-ridden first half of 1958 (with easy money) shows similar results. For all member banks in the United States in the more

This content downloaded from 185.44.78.129 on Thu, 19 Jun 2014 02:51:29 AMAll use subject to JSTOR Terms and Conditions

218 Canadian Journal of Economics and Political Science

the other hand, as just indicated, the Treasury does recoup heavily on its incre- mental interest payments to the Federal Reserve banks.40

Finally, if restrictive official policies have in fact held down levels of real national income, then on this score, too, they have probably reduced the real tax revenues of the Treasury and possibly raised outlays (for relief, as an example).

Except for occasional brief periods of monetary ease, the implications of official policies for the orderly conduct of the Treasury's business, and, in turn, the implications of fiscal disorder for the behaviour of the economy, are serious. Simply put, the United States government, except in interludes of recession (and excluding resort to extraordinarily high rates of interest), faces ever- increasing difficulty in refunding marketable securities as they mature (at the gross rate of over $70 billion per year), in selling new securities, and in persuad- ing holders of savings bonds not to redeem them.4' Since the government must meet its obligations, the final outcome could be that the Federal Reserve would have no choice (aside from the equally difficult one of lending directly to the Treasury) but to make large-scale reserves available to commercial banks intermittently under awkward circumstances in order to enable and induce them to buy Treasury issues. Thus the present course of policy in Washington-continuous abdication from responsibilities by governmental units, continuous excessive concern for an inflation whose degree appears to be exaggerated, and fighting the presumed danger by almost continuous monetary restraint-carries within itself the threat of producing the very infla- tion it seeks to avoid.

In the process, even the possibilities of the application of compensatory finance are threatened. If the government engages in substantial deficit spend- ing through automatic stabilizers or otherwise, then, given recent policies (as observed earlier), as soon as the economy shall have clearly turned toward recovery-and while deficits are at their peak-the bond market may be ex- pected to behave in such fashion as to threaten the ability of the Treasury to conduct its affairs in orderly fashion.42

IV. SOME IMPLICATIONS FOR POLICY

The Fetish of Laissez-Faire At the outset, an important generalization is that the Reserve authorities

should avoid doctrinaire positions. Since the System cannot avoid being a prosperous period total current earnings rose 9.4 per cent, total current expenses rose 9.9 per cent and net current earnings rose 8.6 per cent. In contrast, net profits before income taxes fell 33.6 per cent, taxes on net income fell 40.6 per cent, net profits after taxes fell 27.8 per cent, while cash dividends declared rose 6.2 per cent! (See Federal Reserve Bank of San Francisco, Monthly Review, Sept., 1959, 130-5.)

4OPayments by the Reserve Banks to the Treasury rose from $255 million in 1951 to $897 million in 1960. Treasury obligations held rose from $23.8 billion at year-end 1951 to $27.2 billion at year-end (December 28) 1960. (Federal Reserve Bulletin, Jan., 1952, 31, 45; New York Times, Jan. 6, 1961, 35, 41.)

41Between Dec. 1955, and Nov., 1960, the volume of savings bonds outstanding declined from $57.9 billion to $47.4 billion (Federal Reserve Bulletin, Dec., 1960, p. 1376).

42This was essentially the state of affairs faced by the Treasury in mid-1958. Unemploy- ment (seasonally adjusted) reached a peak of 7.6 per cent in August, a cash deficit of

This content downloaded from 185.44.78.129 on Thu, 19 Jun 2014 02:51:29 AMAll use subject to JSTOR Terms and Conditions

Monetary Policies in the US since 1950 219

powerful oligopsonist, the authorities should accept the greater duties that accompany vast market power and adopt policies designed to make them responsible, not irresponsible, oligopsonists. This implies not laissez-faire but positive, enlightened interventionism.

A second important generalization is that appropriate actions should not be avoided merely because they will yield the by-product of helping the Treasury. Reserve authorities frequently appear to have a double standard for banks and the Treasury; if appropriate Reserve policies are unusually helpful to banks, all is considered satisfactory while if otherwise appropriate Reserve policies are unusually helpful to the Treasury, they may be used sparingly (as, for example, in a choice between lower reserve requirements and open market pur- chases).

With respect to specific items, the "bills-only" policy, whose abandonment has just been announced,48 should not have been instituted and, one may hope, will not soon again be resurrected. Such a policy constitutes an abdication of modern central bank responsibility. In the voluminous literature which the policy has brought forth in the economics journals, it has been attacked by virtually all economists outside the Reserve system.

The drive for secularly lower reserve requirements should be ended. Its appeal on free-market grounds is hardly realistic. Certain other defences, too, are questionable. It is argued that lower ratios permit greater leverage in terms of end results as a consequence of any specific amount of open market sales or purchases by the Federal Reserve. Part of the answer here is that the need for high leverage is very important only in a world of small government debt. There a low reserve ratio would conserve "ammunition" (though the central bank could buy and sell items other than government debt). On the other hand, it must be conceded that since a lower level of reserve require- ments necessitates smaller open market operations to obtain any given effect on the money supply, there will be a smaller impact on government bond prices at lower reserve ratios.44 This virtue would be most useful when restraint is required in the presence of a large government debt. However, in rebuttal, restraining action today may well take the course, not of lowering the money supply, but of reducing or stopping its growth. Significant open-market sales would then be unnecessary. Also, this argument for lower reserve ratios relates essentially to a short-run situation, which hardly seems to have the importance attaching to the secular situation.

Another argument for lower reserve ratios holds that high ratios give little room for raising them in event of future need. This again is largely an argument applicable in cases of small government debt. There is now little possibility of the authorities' being unable to curtail credit potentials severely owing to lack of Treasury securities to sell. Yet another argument for lower reserve ratios involves coping with serious falls in gold stocks. While there is clearly merit

about $13 billion was developing for the fRscal year 1959 and tight money was viewed as on the way back! (See Economic Report of the President, Jan., 1959, 159; and Federal Reserve Bulletin, Nov., 1959, p. 1390.)

43See New York Times, Feb. 21, 1961, 49, 58. 44See A. N. McCleod, "Security-Reserve Requirements in the United States and the

United Kingdom: A Comment," Journal of Finance, XIV, Dec., 1959, 532.

This content downloaded from 185.44.78.129 on Thu, 19 Jun 2014 02:51:29 AMAll use subject to JSTOR Terms and Conditions

220 Canadian Journal of Economics and Political Science

in this argument, more basic solutions are probably preferable. Viewing the situation as a whole, we conclude that in a world of permanent big government debt, it would appear more appropriate to strive for a fairly high secular level of reserve requirements.45

The free-market appeal of the Federal Reserve's failure to support govern- ment securities during offering periods also is unrealistic. Such support is owed by virtue of the enormous impact of huge Treasury operations on the private sector of the market, let alone the public sector. It is an inadequate defence to contend, as is sometimes done, that the Reserve authorities may support new Treasury issues indirectly by assuring adequacy of bank reserves at times of issue. Admittedly this is true. The effectiveness, however, is con- tingent upon reserves being made available on a clearly noticeable scale and as part of a general policy move (as in the lowering of reserve requirements in mid-1953 coincident with the imminent issuance of new Treasury securities and the widespread expectation of recession). It is quite another story if the release of reserves is virtually unnoticeable and if the expectation is for a resumption of tight money pressures.

The Reserve policy of not intervening in Treasury security markets except to correct disorderly conditions should be abandoned. A policy of preventing disorderly markets would make less likely a massive run on government securi ties and might actually reduce the extent of Federal Reserve intervention necessary. There appears to be a parallel here to the case of bank runs, where official intervention to prevent a run is likely to be of considerably smaller magnitude than official action to stop one.

It is often contended that the government bond market (excluding short- term securities) is thin. If this is true, it implies that the Federal Reserve could influence the market considerably with small purchases of longer-term securi- ties. It implies, too, the great importance of expectations concerning official policy for the formation of interest rates. Given a thin market, it is difficult to avoid the conclusion that with very little difference in actual availability of free reserves-but with a reversal in attitudes and accompanying policies-the Reserve authorities could sharply simplify the problems of debt management and save money for taxpayers.46

The Preoccupation with Inflation Official quarters should adopt a sense of humility and perspective withb

respect to the issue of inflation. As observed earlier, the rise in the consumer price index between 1951 and 1960 was at the rate of roughly 1.6 per cent per annum measured by the June, 1951, price level. This is not a serious amount of inflation. As noted earlier, too, this rise represents an estimate made by a seriously imperfect measuring device with an apparently upward bias.

However, if one chooses to disregard the imperfections in the yardstick and object to the minor degree of inflation recorded by it, then it would seem

45For a discussion of some of the issues in the level of reserve requirements see the exchange between Senator Douglas and Reserve Board Chairman Martin in Employment, Growth, and Price Levels, Part 6A, 1455-66, 1493-1500; see also 1483-92.

46Cf. ibid., 1250-1.

This content downloaded from 185.44.78.129 on Thu, 19 Jun 2014 02:51:29 AMAll use subject to JSTOR Terms and Conditions

lMonetary Policies in the US since 1950 221

appropriate to consider further the costs which may be involved in attempts to stop some given price level dead in its tracks. If this involves revising our notions of minimum permissible unemployment upward by an average of, say, 500,000 to 1,000,000 persons in non-recession years and if it entails some in- crease in the duration and amplitude of unemployment in recession, the cumulative cost of a fairly rigid price level may prove to be heavily dispropor- tionate to the benefits conferred.

Other Implications We turn very briefly now to several other implications for policy. In the

interest of effective monetary-fiscal management, certain tax situations should be remedied. Specifically, the dividend exemption for stock as well as the 4 per cent dividends tax credit ought to be removed, or alternatively (although inherently less desirable), some tax exemption should be granted on US bonds. The "double taxation" justification for the present treatment of dividends on stock is highly questionable in any event, and this increases the importance of debt management in determining whether to continue such tax concessions. Related here is the availability of capital gains treatment to stock appreciation; some form of tax exemption or capital gains treatment for savings bonds might help to reduce the competitive advantages of stocks in this respect. Con- sideration should be given to measures which would end the game of "tax swaps" and special tax losses in general for banks. Within a general framework of reform and consistent with other parts of the package, tax exemption should be removed from state and municipal securities. (Admittedly the political difficulties would be great.)

Serious consideration should be given some form of security reserve require- ments for banks and other financial institutions.47 To the extent that banks now tend to acquire Treasury issues in recession and sell them in boom, they have an escape hatch for expanding private credit, in a very significant sense, at the expense of government credit. Moreover, in so far as banks and other financial institutions are beneficiaries of governmental actions, especially those which confer guarantees on their assets and liabilities, it seems hardly unreasonable that they be asked to hold modest amounts of Treasury securities as a quid pro quo.

As is being suggested widely, it might be desirable for the Treasury to experiment with new techniques in the issuance of securities. A key purpose would be to minimize the glutting of the market with issues of overwhelming size.

Finally, we mention the desirability of stand-by selective controls on con- sumer credit and real estate credit.48 The argument for them-or against them- scarcely needs repetition here.

47See Miller, "Monetary Policy," 38-42. That security reserve requirements have limita- tions is undeniable. However, it is difficult to find any single control without limitations. Moreover, no one would expect any single control to do the whole job. Critics of security reserve proposals have in essence failed to appreciate these points.

48See ibid., 34-8. See also Staf Report on Employment, Growth and Price Levels, 398- 401, where it is recommended that selective controls be extended to include inventory loans through a variable asset reserve requirement.

This content downloaded from 185.44.78.129 on Thu, 19 Jun 2014 02:51:29 AMAll use subject to JSTOR Terms and Conditions

222 Canadian Journal of Economics and Political Science

V. CONCLUSION

At the outset the problem of debt management seems to be one which should not be unusually difficult. Here is a situation (at the end of 1960) in which net national debt has not grown appreciably since 1946, while the total of net public and private debt has more than doubled, while gross national product has increased nearly 150 per cent in current dollars and over 50 per cent in constant dollars, while population has increased by nearly 40 million, and while the real value of the national debt has diminished sharply, owing mainly to the inflation of 1946-8 engendered by the Second World War and the Korean War inflation of 1950-51. The fact that debt management problems have been agonizingly difficult appears in large measure to result from the actions of the monetary authorities themselves. They have purported in recent years to give the United States a flexible monetary policy. This, however, is a misnomer! Instead there has been a rigidity of monetary policy, a dispensing of a brand of semi-automatism based on narrow guides to policy and much more relevant to a world of long ago than today.

This content downloaded from 185.44.78.129 on Thu, 19 Jun 2014 02:51:29 AMAll use subject to JSTOR Terms and Conditions