Embed Size (px)

Citation preview

1

Molson Coors Equity Evaluation

Nathan Dormann [email protected]

Josh Lantz [email protected]

Jacqueline Otieno [email protected]

David Haley [email protected]

Ravi Patel [email protected]

2

Molson Coors Brewing Company Equity Evaluation

Table of Contents

Executive Summary 1 Molson Coors Firm Overview 3 Industry Structure and Profitability Overview 5 Accounting Analysis 13

Financial Statement Ratio Analysis 23 Forecasting 31 Valuation Analysis 34 Valuation Results 40 Appendices 42 References 53

3

Investment Recommendation: Overvalued, HOLD 11/01/2006

Ticker Symbol TAP S&P 500 Price 71.4

52 Week Range 60.45-74.10 Market Cap 6.24B Shares Outstanding 86,280,000 Divedend Yield 1.28% Average Book Value 6.8 ROE 2.50% ROA 1.10%

EPS Forecast 2005 2006 2007 2008 1.7 3.29 3.68(e) 3.82(e) Intrinsic Valuations Actual Price $71 Residual Income $62 AEG $61 LRRI $69 Beta 1 R2 0.1

4

Executive Summary

Molson Coors has been brewing the finest quality beers for people around

the world for almost two centuries now. It is no wonder that Molson Coors is the

third largest brewer in the United States and fifth largest brewer in the world. By

producing the finest quality beers Molson Coors has created a loyal and

dedicated customer base. Only recently did Coors merge with Molson to create

one of the largest and oldest brewing companies in the world. But Coors has

been expanding their market share through acquisitions and internal growth for

years before the merger. Molson Coors competes in an industry with few true

competitors, with Anheuser Busch and Miller being the only real challengers to

Molson Coors market share. The threat of new competitors is low because of

several barriers to entry, including economy of scale which keeps many of the

smaller breweries from challenging the larger power houses. Molson Coors

business strategy has been to sell the best quality ingredients at low affordable

prices. Molson Coors also includes many promotions and advertisements to

attract new customers and to insure old customers remain loyal. By owning most

of their own packaging facilities Molson Coors is able to offer lower prices while

making sure their products are bottled at a higher quality than their competition.

The accounting practices of Molson Coors are fairly conservative. Their

accounting disclosure is very transparent, making it easier for investors to

decipher the financial situation of the company. Molson Coors accounting is more

transparent and conservative than its industry competitors, which says a lot for a

industry that is highly regulated. Molson Coors is not afraid to disclose negative

information about the firm; they just make sure to let investors know how they

plan to rectify the problem.

The financial information of Molson Coors shows that the company has

been increasing sales in a rapid manner as of recent years. This has to do with

the large growth of the company. While an increase in sales is good, it has

5

translated into only a smaller increase in gross profit. This is because in order to

sustain their large growth rate Molson Coors has had to sacrifice liquidity and

take on a lot more debt. The effect of this is Molson Coors has a lower current

ratio, has more accounts receivable, and is less efficient in turning sales into

cash. The company is well aware of their liquidity and plans to slow growth in

future periods and work on becoming more liquid and paying off debt. While the

company has taken on a lot of debt to pay for the acquisitions they have done a

fairly good job of balancing their debt to equity ratio. Molson Coors financial

strategy to grow through acquisition and effect advertisement has been a

success. It is now up to the managers of Molson Coors to balance the new level

of growth.

Through our own analysis we have found Molson Coors value to be

slightly overvalued. The price we found through the use of valuation models

shows Molson Coors to be slightly below the current market price. We value

Molson Coors to be a strong HOLD security. Even though almost all are models

have shown that its stock should be cheaper than the current market rate, it is

important to understand that many of the financials are distorted due to the

merger and previous acquisitions. We have faith in the competency of the

management to continue to create value for Molson Coors shareholders.

Molson Coors Firm Overview

Adolph Coors came to the United States in 1868 to follow a dream of

starting his own brewing company. The dream is now a reality as Molson Coors

is one of the third largest brewing companies in the United States and the fifth

largest brewing company in the world. The Company was established in 1880

with an annual output of 3,500 barrels, and just ten years later an annual out

put of 17,600 barrels. Molson Coors’s operates primarily in the alcohol

beverage industry dealing mainly in beers and malt liquors.

6

Molson Coors’s main competitors are Miller and Anheuser-Busch. So in

order to stay a float in the business their strategy are as follows:

A) In the US. Their main focus is to re-establish consistent growth trends for

Coors light.

B) In Canada, continue to drive accelerated growth for Coors light and rebuild

momentum behind the Molson Canadian brand

C) In Europe, focus is on core larger brands.

Molson Coors assets have been increasing rapidly over the past 5 yrs as

shown in the graph below. There is a dramatic increase in total current assets

between the years 2001 and 2002 due to Coors’s acquisition of The Carling

Brewing division of Interbrew UK.

year 2001 2002 2003 2004 2005

Total Current Assets (millions) 606.53 1,053.9 1,078.85 1,268.22 1,468.24

The sales volume of Molson Coors over the last five years has been

increasing steadily with a recent high in volume in 2005. This is due to Coors’s

Merger with Molson Brewing Company. On the other hand the sales growth over

the last five years has been fluctuating and not very consistent. As illustrated in

the table below.

Year: Sales Volume: Sales Growth: 2001 $2,842,752,000 .01% 2002 $4,956,947,000 42.6% 2003 $5,387,220,000 7.9% 2004 $5,819,727,000 7.4% 2005 $7,417,702,000 21.5%

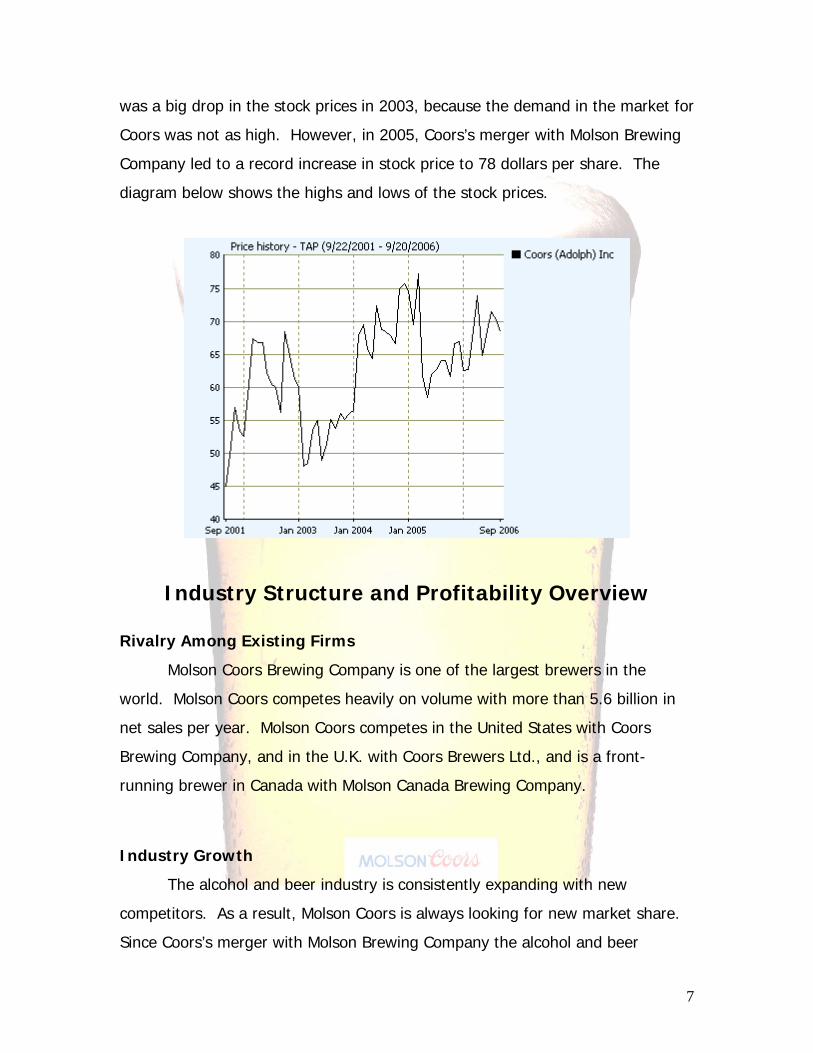

The stock prices have fluctuated quite a bit over the last 5 years. In 2001 the

stock price was 45 dollars per share and is currently 68 dollars per share. There

7

was a big drop in the stock prices in 2003, because the demand in the market for

Coors was not as high. However, in 2005, Coors’s merger with Molson Brewing

Company led to a record increase in stock price to 78 dollars per share. The

diagram below shows the highs and lows of the stock prices.

Industry Structure and Profitability Overview

Rivalry Among Existing Firms

Molson Coors Brewing Company is one of the largest brewers in the

world. Molson Coors competes heavily on volume with more than 5.6 billion in

net sales per year. Molson Coors competes in the United States with Coors

Brewing Company, and in the U.K. with Coors Brewers Ltd., and is a front-

running brewer in Canada with Molson Canada Brewing Company.

Industry Growth

The alcohol and beer industry is consistently expanding with new

competitors. As a result, Molson Coors is always looking for new market share.

Since Coors’s merger with Molson Brewing Company the alcohol and beer

8

industry has reached $200 billion dollars in worth. This market is ever-expanding

and highly competitive. In order to compete, it is extremely important that

Molson Coors seize as much market share as possible. Differentiation and

market concentration are among some of the techniques used by Molson Coors

in order to remain one of the main players in a highly competitive market. The

larger the share of the market Molson Coors is able to acquire the easier it will

be to keep costs low.

Concentration and Balance of Competitors

Molson Coors Brewing Company, after merging with the Canadian

company Molson, is now the fifth largest brewing company by volume,

competing with such brands as Anheuser- Busch, Scottish & Newcastle UK Ltd.,

Inbev UK Ltd., and Carlsberg UK Ltd.. While there are only about 10 major

players in the world, Molson Coors holds about 42% percent of the market share

in Canada and 11% percent of the market share in the United States, (ranking

them #3 in the U.S.).

Degree of Differentiation Differentiation is a competitive strategy used by Molson Coors in order to

set them apart from other similar competitors. Molson Coors not only offers a

wide variety of beer and malt liquor, but they also differentiate themselves by

using only quality raw materials, and premium packaging, helping them provide

services and product at lowest price possible. Below is a list of all Molson Coors

Brewing Company’s products.

9

Top Brewers Ranked by Volume In the United States

Company Name Ticker Symbol Sales (31 Gal

Barrels)

Percentage of

Major Market

Anheuser-Busch

Inc.

BUD

101,800,000

62%

Miller Brewing Co.

SBMRY.PK

London Stock

Exchange

39,660,000

24%

Coors Brewing Co.

TAP

22,688,000

14%

Learning Economies

The alcohol and beer industry within which Molson Coors Brewing

Company competes includes only a few large players. Since there are only a

small number of large competitors combating for as much market share as

possible, the learning curve seems to be quite steep in the beer industry.

Because of this fact, the competition for market share is far more aggressive and

competitive; pressure for larger market share is greatly increasing.

10

Excess Capacity and Exit Barriers At the time, excess capacity and exit barriers do not impose a problem to

any players in the industry. This is due to the past and current high demand for

beer as well as a low degree of specialization. These factors make exit barriers

low.

Threat of New Entrants

Scale Economies

Economies of scale is a major factor to consider when entering this

industry. A large economy of scale works to the advantage of Molson Coors by

helping them stay a large competitor in the market. It also makes new entry

into the market expensive and very difficult for companies who often have

inferior resources.

First Mover Advantage

Although Adolph Coors Company and Molson Inc. were recently merged in

February 2005, both are two of the oldest brewing companies ever formed;

(Adolph Coors founded in 1873 and Molson in 1786), helping them set industry

standards and keep supplier and customer loyalty.

Channels of Distribution and Relationships

Molson Coors’ channel of distribution is well established and maintained

due to their market position and reputation. Customer loyalty and international

name recognition help Coors keep already established channels of distribution,

while also helping them keep distributing prices down.

11

Legal Barriers

The alcohol business in the U.S. is highly regulated by federal, state and

local governments. They govern and overlook much of the operations such as,

brewing, marketing, sales, environmental issues, distributor relationships, and

transportation. Various permits must also be maintained in order to operate

within certain boundaries. These government entities also control the tax rate

faced by Coors and their competitors, which are quite high. (Federal tax is

currently $18 dollars a barrel and State excise taxes vary by state).

Threat of Substitute Products

While Molson Coors’ main objective is the brewing and selling of beer

product, they also reach out and cover many other different types of industries.

Starting in November 2001, Molson Coors partnered up with the Ernest and Julio

Gallo Winery Company, this was the first time Coors has ever teamed up with a

winery company internationally, and this offered Coors the benefit of being able

to sell a wide array of table wines, beverage wines, and distilled spirits. This

significantly decreases the chances of consumers making a switch to substitute

products.

Relative Price and Performance

One of the main priorities of Molson Coors is that they offer a premium

quality product at the most affordable price possible. Molson Coors wide variety

of products allows them to sell premium quality at an affordable price. Molson

Coors contains ownership of popular product brands such as Coors Original and

Coors Light, Keystone, Zima, Aspen Edge, Blue Moon, and Killians. Coors also

offers a wide variety of different Ale’s and Lager. Covering a large spectrum of

beer and other beverages allow Coors to not only compete at a very high

performance, but it also allows Coors the ability to offer their products at

12

reasonably affordable prices. Having premium quality with low pricing is a virtue

that most companies in the industry can’t afford.

Buyers Willingness to Switch

Many of Coors’ customers are repeat customers due to loyalty and Coors

ability to give the consumer what they want. Molson Coors advertising and

promotions along with their great taste and good pricing keeps most customers

coming back for more. Much of the buyers’ willingness to switch is based on

personal taste preference and pricing which Molson Coors puts a premium on.

Bargaining Power in Input and Output Markets

Switching Costs

Switching costs are relatively not high when it comes to this industry. The

networks needed to distribute and package are already well solidified. Many of

the products produced by Coors and other Companies are somewhat similar,

causing switching costs to be low.

Price Sensitivity

13

Switching costs and prices sensitivity go hand and hand when it comes to

consumers choosing which brand of beer to buy. Since other products are

somewhat similar, it is possible that many consumers will switch from one brand

to another based on difference in price.

Relative Bargaining Power of Consumer

One of the strongholds that Molson Coors contains is their bargaining

power that they have achieved over the years. While there are many different

types of beer on the market, Coors’ reputation and longevity of business gives

them the bargaining power over their consumer. As long as they are able to keep

prices reasonable there is no reason for their loyal customers to switch. While

other products are quite similar, much of the bargaining power and willingness to

stay or switch brands lies in the hands of the consumer.

Relative Bargaining Power of Suppliers

While advertisements and the reputation of the company make up most of

the supplier bargaining power, much of the bargaining power lies in the hands of

the consumer to make a decision on their purchases whether that is based on

price or taste preference.

Value Chain Analysis

One of the main reasons why Coors has such great success lies in the

manufacturing department. On January 22, 1959, Bill Coors and his brewing

company introduced the first two-piece aluminum beverage can. Coors now

owns and is a partner in operating the nation’s largest aluminum can

manufacturing plant which is located in Golden, Colorado. In April 2005, Coors

came out with the first 8-ounce serving of beer ever produced. With the new

can also came the wide-mouth opening for easier drinking. Also in April 2005,

Coors introduced the Coors Light 18-pack plastic bottle cooler box which is the

first ice-ready plastic bottle package. The plastic bottles allowed consumers to

14

take beer where glass insn’t allowed. In 1993 Coors introduced ZIMA, the first

flavored malt beverage available to the public. There are also many unique

products that Coors has to offer. Extra Gold Lager is full-flavored lager that is

available in select markets. They also have a seasonal brew called Winterfest is

available during the holiday season and also pumpkin flavored ale sold only in

the autumn. Coors also offers a nonalcoholic beverage, which appeals to the

large group of people who don’t consume alcohol. Coors offers 15 different

brands and many varieties of beverages such as lagers, ales and flavored malt

beverages. Coors has brewing companies in five international countries including

China, the biggest beer-consuming country in the world. By expanding the

operations throughout the world, along with improving quality and decreasing

costs Coors should be able to stay competitive for years to come.

Competitive Advantage

Molson Coors brewing company executes several different strategies in

order to differentiate their product line from the competition. They are known

across the world for offering a wide variety of products of the utmost quality. A

diverse assortment of lagers, ales, and flavored malt beverages has helped them

to become the third largest brewery in the United States and the fifth largest in

the world. In order to maintain this significant share in the market segment

Coors has created fifteen unique brands that have grown to define the

company’s high standards of excellence. These standards have earned Coors a

reputation for brewing the finest quality beers with the highest quality

ingredients. Coors is also aiming to produce their products at a lower cost

without sacrificing their quality and image. They have done this by attempting

to better optimize business processes. Costs have been lowered by shortening

their business cycle, eliminating process complexities, and encouraging better

employee performance. Because of the size of Coors Company, it is possible for

them to efficiently out produce most of their competitors; in fact, just three

United States breweries, Coors being one of them, are responsible for seventy

15

eight percent or the market share. It is extremely important that Coors is able to

make more profit on each item sold then most of their competitors. This allows

for Coors to spend more money on advertisements and product innovations

which has created significant company growth and market share. Also, Coors

financial strategy has been to expand their operations by purchasing and

merging with other companies. In 2002, Coors Brewing Company purchased

assets from Bass Brewers located in the U.K. This allowed for Coors to compete

on a national scale. The acquisition increased the company’s sales volume by

forty percent. In addition, Coors merged with Molson in 2005 to create a

company that was able to produce more efficiently. Coors-Molson is now one of

the world’s largest and most successful brewing companies.

Accounting Analysis

When doing the accounting analysis of Molson Coors, we used the

qualitative and quantitative methods to determine the quality and reliability of

the accounting practices that are implemented at Molson Coors. When evaluating

Molson Coors with the qualitative method of accounting analysis, we determined

its credibility using these five steps: 1. Identify Key Accounting Policies, 2. Assess

Degree of Potential Accounting Flexibility, 3. Evaluate Actual Accounting

Strategy, 4. Evaluate the Quality of Disclosure, and 5. Identify Potential “Red

Flags”. In the course of our evaluation of Molson Coors’ accounting analysis, we

did not find it necessary to modify any information presented. Based on the

information taken from various financial statements and the corresponding

footnotes provided, we do not feel that Molson Coors has inadequate accounting

practices or misleading information presented in the financial statements.

16

Step One: Identify Key Accounting Policies

The accounting policies of Molson Coors are of utmost importance to the

success of the company. Estimates are required to be made for the preparation

of the consolidated financial statements in regards to accounts such as assets,

liabilities, revenues, and expenses. Managers are given a degree of flexibility in

the type of accounting policies they want to implement. Although there are many

different styles of accounting they all show the financial situation of a company,

and play a vital role to the company’s success.

Key Accounting Policies

Molson Coors was able to become the fifth largest brewer in the world

through product differentiation and low cost producing and pricing. In order to

maintain there competitive advantage Molson Coors has followed these

accounting guidelines.

Revenue Recognition

Molson Coors makes billions of dollars in sales throughout a given fiscal

year. Many of the sales are accounted for in foreign markets which Coors has

ventured. When the revenue is recognized is very important to how the company

looks financially. Molson Coors typically recognizes revenue when “the significant

risks and rewards of ownership are transferred to the customer or distributor”.

This usually occurs at the time of shipment to a distributor or at the time of

delivery to a retail customer, in the case that Molson Coors is the distributing

company. This allows for revenues to be quickly accounted for making Molson

Coors operations more efficient. To compensate for damaged products or lost

17

goods Molson Coors keeps a reserve account which estimates the amount that

Coors might have to expense.

Allowance for Doubtful Accounts

Molson Coors allows many of the sales it makes to go on credit. In order

to stay competitive in the industry it is essential that some of the larger, highly

trusted distributors and retailers be allowed to purchase inventory on credit. In

order to account for some of the accounts not being paid Molson Coors estimates

a reserve account to help negate the risk. It is important that Molson Coors not

have too many accounts on credit, so that it doesn’t damage its liquidity. Having

free cash flows is essential for Molson Coors to maintain its low cost strategy.

Pension and Postretirement Benefits

Molson Coors has implemented defined benefit plans for the majority of

their employees in the United States, Canada and the United Kingdom.

Postretirement welfare plans have also been implanted in the United States and

Canada to provide for medical benefits and life insurance for retirees. The

accounting policies used by Molson Coors in regards to pension and

postretirement benefit plans conform with Statement of Financial Accounting

Standards No. 87, “Employers’ Accounting for Pensions” (SFAS No.87) and

Statement of Financial Accounting Standards No. 106, “Employers’ Accounting

for Postretirement Benefits Other than Pensions” (SFAS No.106). These

statements require management to make assumptions in relation to long-term

rate of return on plan assets, discount rates used to measure future obligations

and expenses, salary increases, inflation, and health care expense trend rates.

These standards and policies implemented by Molson Coors are highly critical in

relation to their accounting because they are highly susceptible to change from

period to period, depending on market conditions.

18

Goodwill and Other Intangible Assets

Molson Coors performs evaluation of goodwill and other intangibles

annually. Intangible assets are required to be evaluated to identify the possibility

of impairment, estimated future cash flows to be generated by such assets, and

the rate that is to be used to discount the cash flows. Recently, the allocation of

Goodwill has become a very important policy for Molson Coors in regards to the

merger between Molson and Coors. The now joint entity of Molson Coors has

allocated approximately $1.1 billion of goodwill from the merger. This amount of

goodwill was allocated to realize expected synergy savings that will result from

the merger. Allocation of goodwill puts pressure on firms in the US market to

achieve these synergy savings to avoid impairment on goodwill. This style of

accounting makes for larger future long term assets.

Inventories

Molson Coors states inventories at the lower of cost or market. Cost is

determined by the last in, first out (LIFO) method for inventories in the United

States. However, cost is determined by the first in, first out (FIFO) method in the

United Kingdom and Canada. The shelf lives of inventories are assessed regularly

and inventories are reserved when it becomes likely that the product will not be

sold by the specifications relating to the freshness of the product. It is important

that Molson Coors maintain a high inventory turnover because of the risk of

spoilage. By being able to convert inventory into sales more quickly Molson Coors

will be better able to lower their product cost.

Income Tax Assumptions

Molson Coors accounts for income taxes in accordance with Statement of

Financial Accounting Standards No. 109, “Accounting for Income Taxes” (SFAS

No. 109). However, there are several uncertainties and estimates that must be

taken into consideration when determining worldwide provision of income taxes.

The rate at which Molson Coors pays on taxes throughout the global market

19

affects many of the accounting policies it chooses in the specific areas it

operates. There decision to use the (LIFO) inventory method in the United States

and the (FIFO) method in Europe probably has to do with income taxes.

Step Two: Assess Degree of Potential Accounting Flexibility

Molson Coors has a considerable amount of flexibility when choosing their

key accounting policies. There are many accounting policies that Molson Coors

use in regards to their accounting style. Molson Coors uses the LIFO method in

the United States and the FIFO method in the United Kingdom and Canada. This

method is implemented because Molson Coors wants to cut cost, in order to

lower their prices. It is important that Molson Coors stay cost competitive with

industry leader Anheuser Busch. By changing inventory accounting Molson Coors

can manipulate the amount of taxes it incurs. Another way Molson Coors has

flexibility is in the way they allocate goodwill. When Molson and Coors merged

they allocated approximately $1.1 billion of goodwill from the merger. This

amount of goodwill was allocated to realize expected synergy savings from the

merger. Allocation of goodwill puts pressure on firms in the US market to achieve

these synergy savings to avoid impairment on goodwill. Because Molson Coors

has a history of acquisitions it this accounting decision is extremely important to

how Molson Coors financials appear. By allowing their acquisitions to be

accounted for as goodwill the future value of their assets will be significantly

higher, because they will not have to account for the amortization on the asset.

They will however check regularly for any impairment to the asset. Another

accounting policy Molson Coors has control over is their payment on debt. In

most cases the shorter the loan the lower the interest rate. Molson Coors is able

to influence how much interest the pay on debt by how quickly they pay their

debt off. It is very possible for managers to influence important ratios such as

working capital by allocating short term debt into long term debt. The amount of

20

interest paid on the long term debt will be significantly higher then what is paid

in the short term. By having less short term debt Molson Coors could improve

their credit rating and financial position, but end up paying more in the long run.

This will be important to watch with Molson Coors because of the merger. In

order to acquire Molson, Coors took on a large amount of short term debt, if

Molson Coors is unable to pay off this debt it may allocate it to longer term more

expense debt.

Step Three: Evaluation of Actual Accounting Strategy

The accounting strategy of Molson Coors Brewing Company attempts to

present the company’s financial condition in a very transparent manner rather

than conceal their financial situation from the public. Molson Coors wants the

public to be able to look at the company and get a clear view of where the

company stands. With the exception of years in which large acquisitions take

place, Molson Coors financials are transparent. For the most part Molson Coors

accounting is fairly conservative, any estimates made in the financial statements

are done so using the management’s best judgment. Also, any approximation

and uncertainty is fully divulged to the public. The results of their operations and

cash flows presented in the financial statements for Molson Coors are prepared

on a continuous basis, and strictly abide with accounting principles generally

accepted in the United States of America. They are continuously adapting to new

and better accounting methods in order to more efficiently disclose the

company’s financial information and position in the market. Coors is far more

transparent then the rest of the industry. Its financials are much easier to

decipher than its main competitors Anheuser Busch and Miller. Many of the

accounting practices of Molson Coors and Anheuser Busch are very similar

because of GAAP regulations. Regulations on advertisement and media make

21

sure that costs are expensed as they occur. These guidelines make sure that this

expense is not manipulated. This helps keep Molson Coors conservative due to a

large part of their revenue going to advertising expense.

Step Four: Quality of Disclosure

Molson Coors displays adequate information for analysts and investors to

assess the company’s growth. Their income statements and balance sheets are

available in a four year range, thus making it easy to assess the company’s

profitability at a glance.

Molson Coors reveals reports showing their failures in certain areas and

what action they are taking to correct the problem. Unlike some of the industry

competitors Molson Coors is not afraid to reveal negatives of the company.

Molson Coors just makes sure they tell investors what they are doing to fix the

problem. As an example, in the third quarter of 2006, marketing, general and

administrative expenses rose by 0.4 percent. To make up for that loss they are

implementing merger-related synergies and cost cutting programs across the

company, and achieved approximately $27 million in synergies.

Because Molson Coors has international branches of their company it is

important that they disclose the success factors and obstacles they face in those

different markets that they compete in. Canada sales increased by 3.5 percent

due to improved weather and extensive price promotions. The U.S market had

low overhead and manufacturing cost, but also suffered high energy cost and

high packaging material costs. In the Europe market sales went down by nearly

24.2 percent from the previous year, due to extensive price discounting. The

European market is currently impacted negatively by the ongoing adverse mix,

which affects the sales of highly flavored alcoholic beverages, thus the low sales.

Business is not always the same from one country to another, because

there are laws, taxes, and restrictions that affect the business either positively or

22

negatively. Molson Coors discuss all these factors in order to let investors know

what to expect while doing business in those markets and how Molson Coors

plans to manage those markets as a whole. In Europe, part of the low sales is

because of the increasing distribution costs due to the working time legislation

for drivers. The high increase in the Canada market was accelerated because the

Canadian dollar appreciated by 8 percent year over year versus the U.S dollar,

thus boosting the Canada operating results by almost 10 million that quarter. By

competing on a global scale Molson Coors is subject to all these changes, they

make sure to report all the information and changes that they are making to

account for the uncertain global environment.

Quantitative Measures

Sales Manipulation Diagnostics

Sales Manipulation 2001 2002 2003 2004 2005Net Sales/Net A/R 22.34 5.35 5.33 5.17 6.64Net Sales/Inventory 21.10 20.45 19.09 18.34 17.50

Molson Coors has been decreasing its liquidity in the more recent years as

its accounts receivable and inventory have increased in proportion to net sales.

This shows that Molson Coors has had to account for an increase in assets due

to their acquisitions. The accounting that is done for these measures seems to be

fairly consistent in that there are not many large drastic changes in the numbers.

In terms of the industry standard Molson Coors has had an overload on Accounts

Receivable as seen in the chart below. This however is due to the merger and

acquisitions not poor accounting practices. Molson Coors Net Sales to Inventory

ratio is on par with the rest of the industry.

23

Core Expense Manipulation Diagnostics

Core Expense Manipulation 2001 2002 2003 2004 2005Declining Asset Turnover 4.01 3.58 3.71 3.40 3.75Changes in CFFO/OI 1.28 0.87 1.72 1.43 1.00Changes in CFFO/NOA -4.54 -14.39 -13.31 4.83 -5.05

The negative and low numbers in the cash flow diagnostics are something to be

worried about. Molson Coors has had to use a lot of their free cash flows to

account for such large growth. Having less free cash flows makes it more difficult

to deal with unsuspected changes.

Step Five: Identify Potential “Red Flags”

Companies often take advantage of potential accounting flexibility by

overstating revenues and decreasing expense accounts. The method of

identifying these misstatements is by running the sales manipulation diagnostics

and core manipulation diagnostics such as the quantitative measures presented

Sales Manipulation

0.00

5.00

10.00

15.00

20.00

25.00

2001 2002 2003 2004 2005

Net

Sal

es/A

/R

TAPBUD

24

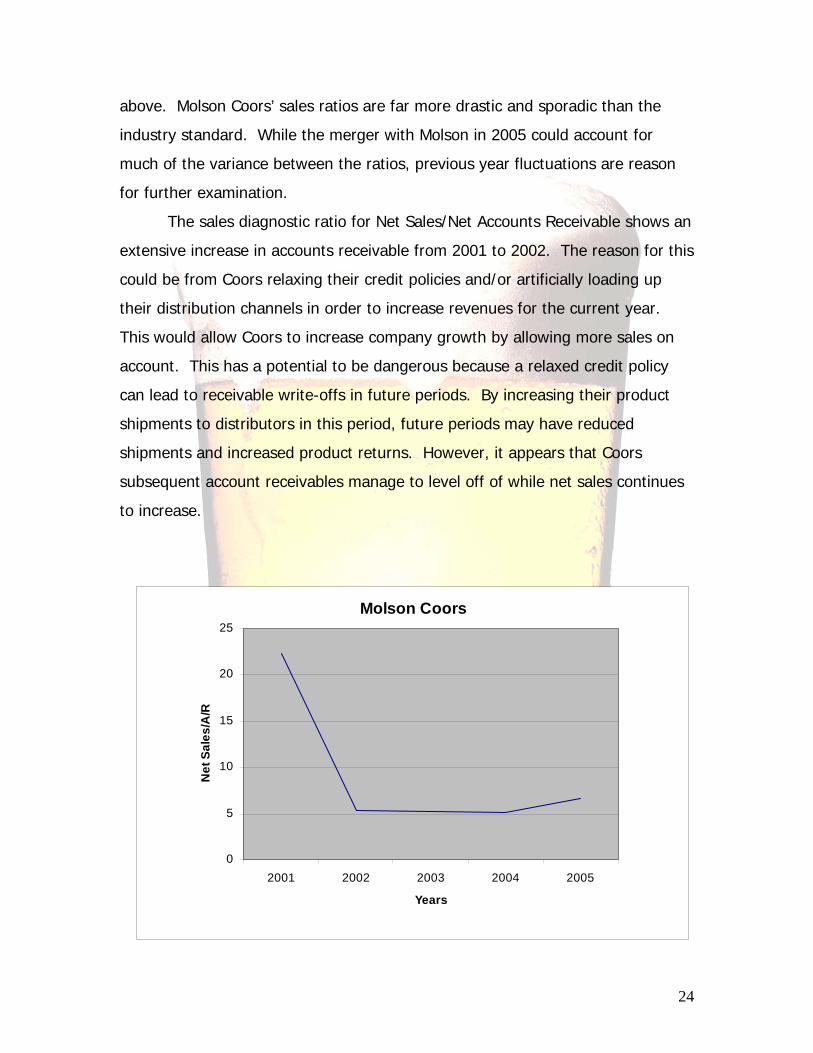

above. Molson Coors’ sales ratios are far more drastic and sporadic than the

industry standard. While the merger with Molson in 2005 could account for

much of the variance between the ratios, previous year fluctuations are reason

for further examination. The sales diagnostic ratio for Net Sales/Net Accounts Receivable shows an

extensive increase in accounts receivable from 2001 to 2002. The reason for this

could be from Coors relaxing their credit policies and/or artificially loading up

their distribution channels in order to increase revenues for the current year.

This would allow Coors to increase company growth by allowing more sales on

account. This has a potential to be dangerous because a relaxed credit policy

can lead to receivable write-offs in future periods. By increasing their product

shipments to distributors in this period, future periods may have reduced

shipments and increased product returns. However, it appears that Coors

subsequent account receivables manage to level off of while net sales continues

to increase.

Molson Coors

0

5

10

15

20

25

2001 2002 2003 2004 2005

Years

Net

Sal

es/A

/R

25

Step Six: Undo Accounting Distortions

Based on the information that we have compiled according to Molson

Coors’ accounting data, we have determined that there is no misleading

information presented in the quality of disclosure. The statements of income,

balance sheet, and cash flows all provide adequate footnotes and supplemental

information which accurately portrays the company’s financial status. As a result

of the lack of accounting distortions and misstatements we have concluded that

there is no need for any further accounting modifications.

Financial Statement Ratio Analysis

The main objective of this analysis is to examine Molson Coors’ financial

ratios and to forecast the next 10 years of Molson’s financial statements. With

these ratios we can see the overall standing of our company in the brewing

industry. The tables below allow us to view the companies’ liquidity, profitability,

and capital structure so that we are able to value this firm more accurately.

Liquidity Analysis

Liquidity Analysis 2001 2002 2003 2004 2005

Current Ratio (CA/CL) 1.17 0.92 0.95 1.08 0.66

Quick Asset Ratio 0.78 0.59 0.56 0.69 0.33

Accounts Rec. T/O 29.93 7.98 8.72 8.41 10.71

Days Sales Outstanding 12.20 45.74 41.86 43.40 34.08

Inventory Turnover 13.36 13.07 12.35 11.68 10.51

Inventory Days 27.32 27.93 29.55 31.25 34.73 Working Capital

(Sales/WC) 31.95 N/A N/A 63.73 N/A

26

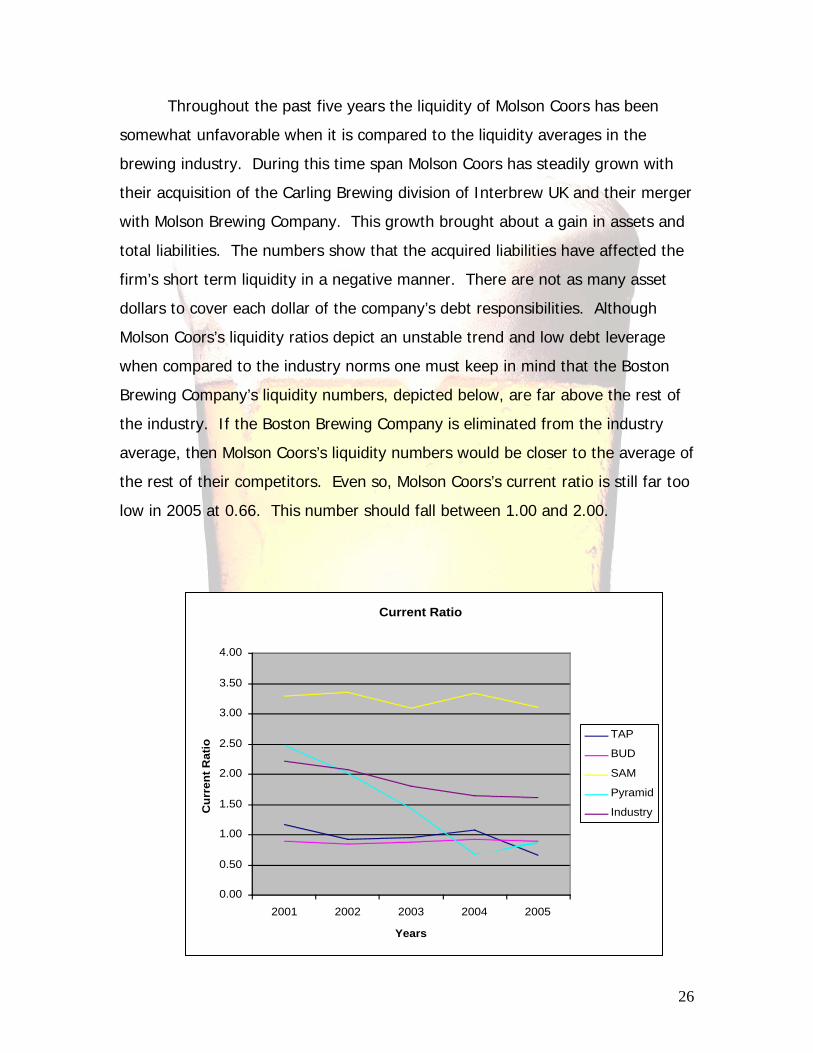

Throughout the past five years the liquidity of Molson Coors has been

somewhat unfavorable when it is compared to the liquidity averages in the

brewing industry. During this time span Molson Coors has steadily grown with

their acquisition of the Carling Brewing division of Interbrew UK and their merger

with Molson Brewing Company. This growth brought about a gain in assets and

total liabilities. The numbers show that the acquired liabilities have affected the

firm’s short term liquidity in a negative manner. There are not as many asset

dollars to cover each dollar of the company’s debt responsibilities. Although

Molson Coors’s liquidity ratios depict an unstable trend and low debt leverage

when compared to the industry norms one must keep in mind that the Boston

Brewing Company’s liquidity numbers, depicted below, are far above the rest of

the industry. If the Boston Brewing Company is eliminated from the industry

average, then Molson Coors’s liquidity numbers would be closer to the average of

the rest of their competitors. Even so, Molson Coors’s current ratio is still far too

low in 2005 at 0.66. This number should fall between 1.00 and 2.00.

Current Ratio

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

2001 2002 2003 2004 2005

Years

Cur

rent

Rat

io

TAP

BUD

SAM

Pyramid

Industry

27

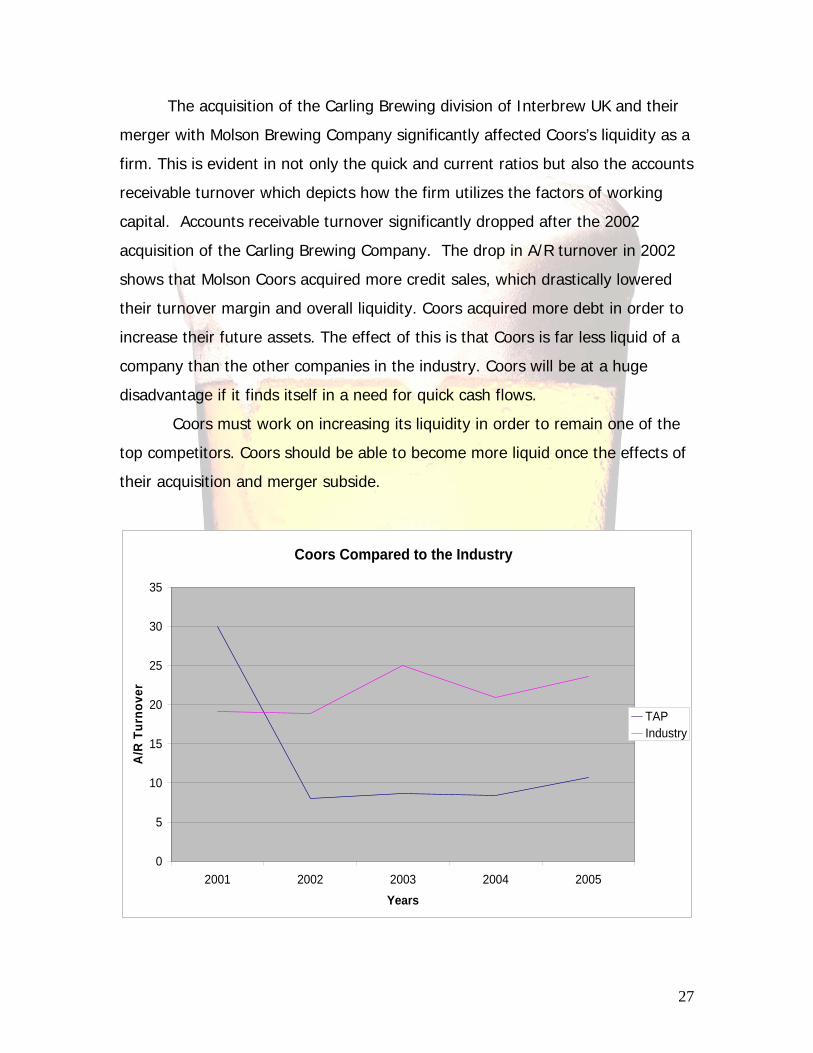

The acquisition of the Carling Brewing division of Interbrew UK and their

merger with Molson Brewing Company significantly affected Coors’s liquidity as a

firm. This is evident in not only the quick and current ratios but also the accounts

receivable turnover which depicts how the firm utilizes the factors of working

capital. Accounts receivable turnover significantly dropped after the 2002

acquisition of the Carling Brewing Company. The drop in A/R turnover in 2002

shows that Molson Coors acquired more credit sales, which drastically lowered

their turnover margin and overall liquidity. Coors acquired more debt in order to

increase their future assets. The effect of this is that Coors is far less liquid of a

company than the other companies in the industry. Coors will be at a huge

disadvantage if it finds itself in a need for quick cash flows.

Coors must work on increasing its liquidity in order to remain one of the

top competitors. Coors should be able to become more liquid once the effects of

their acquisition and merger subside.

Coors Compared to the Industry

0

5

10

15

20

25

30

35

2001 2002 2003 2004 2005Years

A/R

Tur

nove

r

TAPIndustry

28

Profitability Analysis The gross profit margin has made a slight increase from recent years to

2005, but incurred a decrease from years 2001 to 2004. The reason for the

slight decrease from 2001 to 2004 could be from increased pricing pressure from

increasing competition and/or a weakened economy after 9/11/01. Increasing

cost of goods sold compared to competitors such as Anheuser-Busch, could also

be a factor in the decreasing gross profit margin.

Gross Profit Margin Percentage

0

0.1

0.2

0.3

0.4

0.5

0.6

2001 2002 2003 2004 2005

Years

Gro

ss P

rofit

Mar

gin

TAPBUDSAMPMOIndustry

While the gross profit margin dropped from 2001 to 2004 and a slight increase in

2005, the large increase of cost of goods sold from 2001 to 2002 was about

39%, with another large increase in cost of goods sold from 2004 to 2005 of

about 83%. Along with the increasing cost of goods sold, Coors has had a large

increase in sales between 2001 and 2005. However, the large percentage of

cost of goods sold still lowers their overall gross profit, below their main

competitor Anheuser-Busch. While gross profit margin has increased slightly

from 2004 to 2005, Coors operating expense has decreased steadily over the

29

past couple of years, with a slight increase in 2005. A concern with Coors’ is that

their net profit margin has decreased from 2001 to 2002, remained constant

through 2004, and once again slightly decreasing in 2005. Another concern is

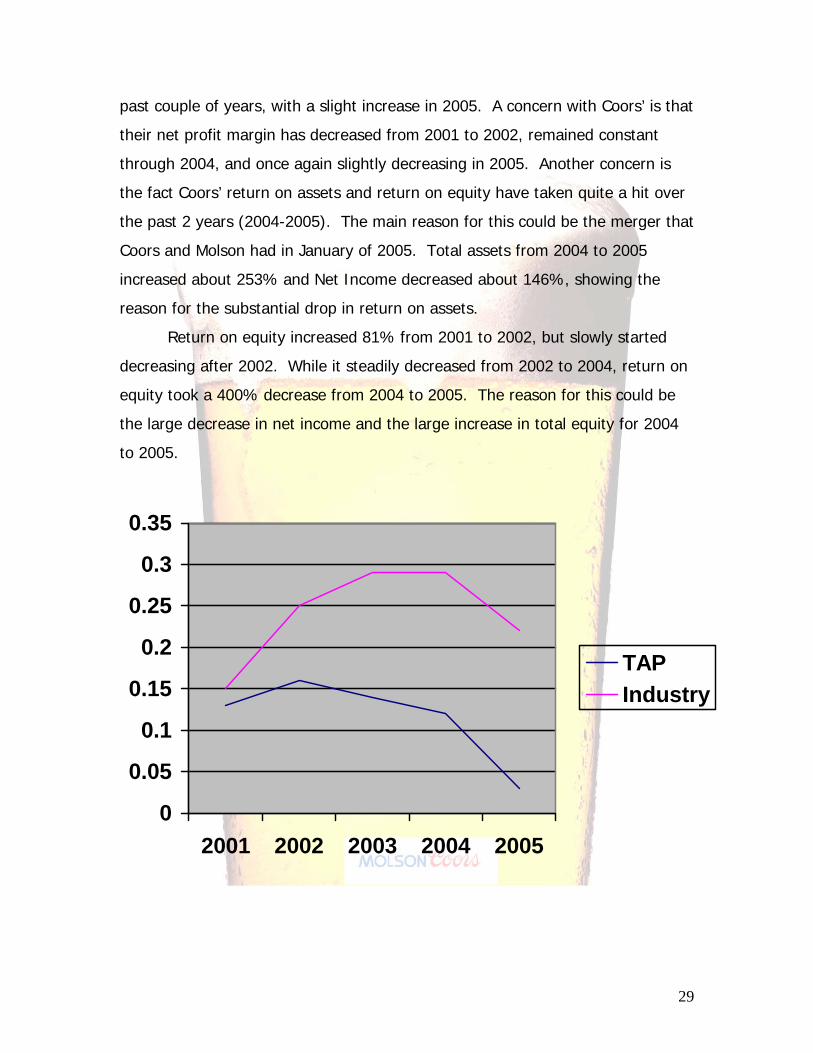

the fact Coors’ return on assets and return on equity have taken quite a hit over

the past 2 years (2004-2005). The main reason for this could be the merger that

Coors and Molson had in January of 2005. Total assets from 2004 to 2005

increased about 253% and Net Income decreased about 146%, showing the

reason for the substantial drop in return on assets.

Return on equity increased 81% from 2001 to 2002, but slowly started

decreasing after 2002. While it steadily decreased from 2002 to 2004, return on

equity took a 400% decrease from 2004 to 2005. The reason for this could be

the large decrease in net income and the large increase in total equity for 2004

to 2005.

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

2001 2002 2003 2004 2005

TAPIndustry

30

While it is alarming for return on equity to decrease that rapidly, the substantial

increase in total equity and decrease in net income can conclusively be

associated with the acquisition and merger in 2005. With the merger, the

company nearly doubled in size, which caused total equity to shoot through the

roof with and increase of 300%. A substantial decrease in operating efficiency

and increase in cost of goods sold is most likely the reason for the decrease in

net income. Anheuser-Busch, who had a steady increase in the return on equity

from 2001 to 2004, also incurred a decrease of ROE of 65%. The reason for this

could very well be the effect of 9/11/05, which also played a role the decrease of

Coors’ ROE. Compared to its competitors in the industry, Coors’ ROE is not really

up to “par” but remember to take into consideration the acquisition and merger

of 2005, and look for ROE to steadily increase starting in 2006.

Capital Structure Analysis

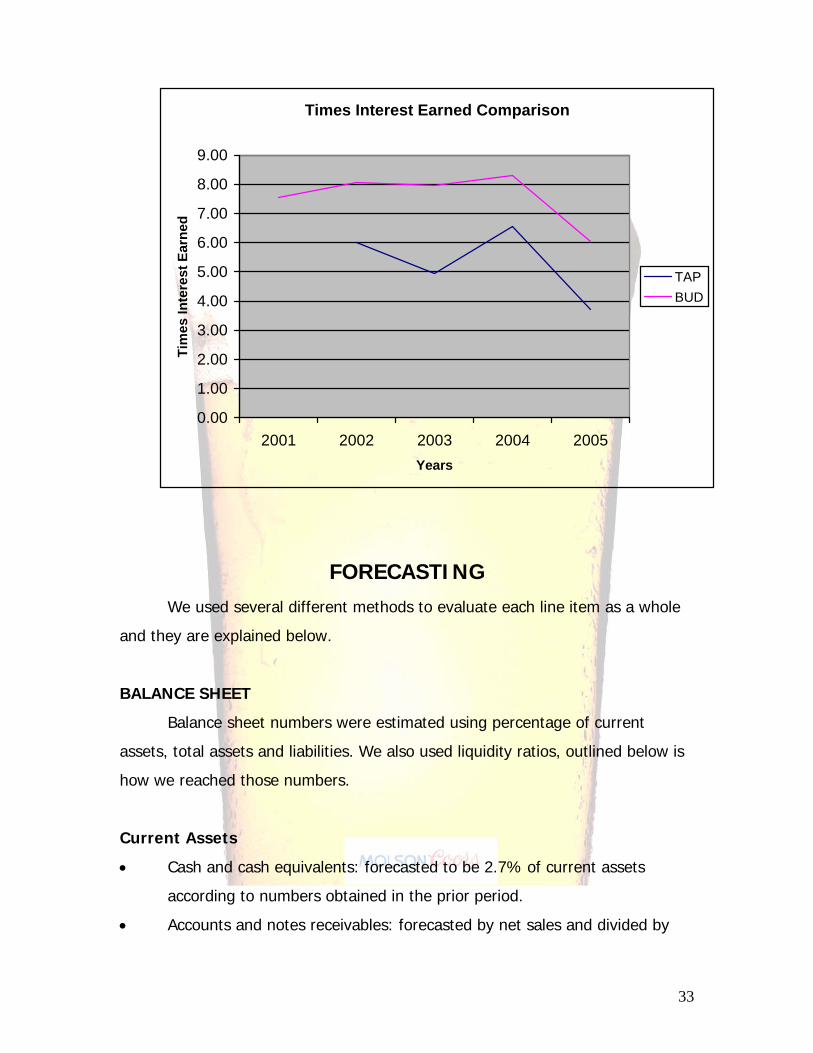

Capital Structure Analysis 2001 2002 2003 2004 2005 Debt to Equity Ratio 0.83 3.38 2.51 1.91 1.22 Times Interest Earned N/A 6.00 4.96 6.55 3.72 Debt Service Margin N/A N/A 24.82 39.99 30.16 Analysis of Molson-Coors Capital Structure shows inconsistent results. Coors

starts out with a very low debt to equity ratio in 2001. Coors was using a large

amount of equity financing as compared to debt in 2001. In 2002 the debt to

equity ratio increases with Coors having nearly four times the amount of debt

31

financing than equity financing. This is due in part to the acquisition of the

Carling Brewing division. Having a higher debt to equity ratio is not always bad,

while it makes for an increase in credit risk and higher interest expense, having

more debt also allows for acquisitions of assets that can help the companies

overall net income grow. By acquiring Carling Brewery, Coors took on more debt

in order to achieve the acquisition, the larger amount of debt to equity actually

helped increase Coors Net Income. The Times Interest Earned Ratio shows that

Coors was able to generate six times as much income before interest and taxes

then interest expense in 2002. This shows for every dollar that Coors acquires in

debt financing it is earning six times the amount in operating income. Having a

higher amount of debt to equity financing increases the company’s Return on

Equity. A higher Return on Equity increases value for the shareholder. After 2002

Coors debt to equity ratio begins to normalize back to 1. This is not because

Coors has acquired less debt but instead because it has had a large increase in

equity financing. This means Coors is relying on funds from shareholders to

finance many of their activities. This gives Coors a lower credit risk and a more

financial stable company. From 2003 to 2004 Coors also is able to finance their

debt more efficiently with cash flows from their operations. This is shown with

the increasing Debt to Service Margin numbers. In 2005 the debt to equity

margin continues to decrease closer to one, but Coors’ Times Interest Earned

also decreases by nearly 50%, their Debt Service Margin also decreases. This is

not a good sign for the company and these negative ratios are reflected by the

large decrease in Net Income, Return on Assets, and Return on Equity. Drop offs

in the companies financial may be due to the merger that took place in February

2005. These numbers will most likely get turned around once the company has

settled from the merger. Therefore 2005 is a very tough year to get an accurate

view of Molson-Coors financials.

When comparing Coors to the rest of the Industry their debt to equity

ratio is consistent with the industry, with the Ratio starting out higher and then

stabilizing around 1.

32

Debt To Equity Ratio

0.00

1.00

2.00

3.00

4.00

5.00

6.00

2001 2002 2003 2004 2005

Years

Deb

t/Equ

ity

TAPBUDSAMPMOIndustry

Anheuser Busch has a much larger Debt to Equity ratio than the rest of

the industry. Anheuser Busch is able to finance most of their company with debt

because of their great credit rating. Investors trust in Anheuser Busch to pay

back the debt that they borrow. This is reflected by the fact that Anheuser Bush

does not have any cash from operating activities going towards Note Payable.

Their ability to sustain such a high debt to equity ratio is also reflected in their

Times Interest Earned ratio. Anheuser Busch is able to earn a much more

operating income compared to their interest expense than Coors. This means

that Coors is at a huge disadvantage, Anheuser is able to acquire more debt with

less credit risk and make more of a profit off that debt.

33

FORECASTING We used several different methods to evaluate each line item as a whole

and they are explained below.

BALANCE SHEET

Balance sheet numbers were estimated using percentage of current

assets, total assets and liabilities. We also used liquidity ratios, outlined below is

how we reached those numbers.

Current Assets

• Cash and cash equivalents: forecasted to be 2.7% of current assets

according to numbers obtained in the prior period.

• Accounts and notes receivables: forecasted by net sales and divided by

Times Interest Earned Comparison

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

2001 2002 2003 2004 2005Years

Tim

es In

tere

st E

arne

d

TAPBUD

34

the prior year’s accounts receivables turnover liquidity ratio.

• Inventory: forecasted numbers obtained by dividing the cost of goods sold

by the inventory turnover liquidity ratio.

• Maintenance and operating supplies: calculated at 2% of the total assets

• Deferred taxes: were forecasted at 40% of the prior year’s income tax

expense.

Fixed Assets

• Properties: properties are 20% of the total fixed assets

• Goodwill: is 24% of total assets

Current liabilities

• Accounts payable: were 6% of the total liabilities

• Accrued salaries and vacations: an average of past 5 years

• Accrued excise tax: calculated by the 5.2 % of net sales of the prior years

• Accrued expenses and other liabilities: were 3.4 % of total liabilities

• Accrued portions of long-term debt: were forecasted by assumptions

because of fluctuations over the past 5 years

Long-term Liabilities

• Deferred pension and post retirement: were 13% of total liabilities

• Retained earnings: calculated retained earnings plus net income minus

dividends paid.

• Class A and B common stock: calculated by a 5 year average from 2001 -

2005

INCOME STATEMENT

The income statements were mainly based on the growth of sales over

the last five years. Sustainable growth was low at 0.01 because of the merger in

35

2005. Also because of the merger Molson Coors paid out a high amount of

dividends so dividends per share was high, however earnings per share were

low. The other forecast were done as follows:

• Net sales: were forecasted by finding average growth rate of 6.78% times

the previous year’s net sales. This growth rate does not take into include

2 outliers in 2002 and 2005.

• Cost of goods sold: were calculated by the cost of goods percentage only

• Marketing, general and administrative expenses: forecasts were calculated

by finding the growth rate of the market, general and administrative

expenses. This percentage also disregards the 2 outliers in 2002 and

2005.

• Interest Income: was calculated by finding an average of the past 5 years.

• Interest expense: was calculated by an average of the past years

excluding an outlier in 2001.

• Income tax expense: is also an average of the last 5 years.

CASH FLOWS

• Depreciation and Amortization: were calculated by 0.17* properties form

the balance sheet. 0.17 is calculated by depreciation and amortization/

properties

• Loss/ Gain of properties and intangibles: is an average starting with 2001-

2005

• Receivables: forecasted by subtracting accounts receivables that are

forecasted for the next year.

• Payables: calculated by subtracting accounts receivable in the current year

from accounts receivable that are forecasted from the next year.

• Inventories: are forecasted by subtracting next years forecasted

inventories on the balance sheet from the current year’s inventories.

36

• Additions to properties and intangibles: are calculated by an average of

the years 2001 - 2005.

• Proceeds from sales or properties: calculated by an average of the years

2001-2005.

• Dividends paid: are forecasted with a 19% dividends payout rate. This

payout rate was calculated as an average from years 2001-2004 as a

result of an outlier in the 2005.

Valuation Analysis

This section’s purpose is to determine the true value of Molson-Coors.

There are many different methods of valuation used to determine the true value

of Molson-Coors and they are all important. Most of the valuation models rely on

data from the forecasted information in the previous section. It is critically

important that these forecasted values are estimated accurately because our

intrinsic value Molson-Coors is derived from the forecasts. By analyzing the

different methods we will be able to determine whether or not Molson-Coors is

fairly valued, under valued, or over valued. These methods include comparables

method, discounted dividends, discounted free cash flows, discounted residual

income, abnormal earnings growth, and the long residual income perpetuity.

Using all these models allows for the factors of forecasted values to be

considered. Having several different models allows for compensation of an

individual model’s deficiency. The results from these models will be compared

with Molson-Coors current stock price, as well as with its Molson Coors

competition.

Comparables Valuation

In determining the method of comparables we found that many of the

companies had ratios that were well below or above the industry standard. It is

37

unfair to value Molson-Coors against many of the smaller companies that do not

hold near the market share that Coors does. We felt that using Anheuser Busch

and Sam Adams in order to evaluate the industry average would give a more

accurate analysis of the information. We made sure to exclude Molson Coors

from the industry average.

Comparables P/E P/B D/P P/S TAP 41.76 1.04 0.18 1.11BUD 20.29 11.09 0.02 2.47SAM 86.75 5.76 N/A 2.07Industry Average 53.00 8.40 0.02 2.27Value 41.76 8.762 59.28 28.11

The D/P ratio gave the closest estimate to the real share price. We where unable

to include Sam Adams into the D/P valuation because they didn’t pay dividends

in the valuation year. The P/B ratio was by far the worst method in valuing

Molson Coors $8.76 is no where near the current share price. Overall method of

comparables is not a good way to value a firm, because it is hard to get a large

enough sample size to get an accurate industry average. Also the numbers used

in some of calculations do not always exist.

Cost of Equity

In order to compute the evaluation models it was important that we

calculate our WACC and Cost of Equity. The most commonly used to way to find

the cost of equity is the Capital Asset Pricing Model. In order to determine the

cost of equity it was essential that we find our companies Beta. We calculated

Molson-Coors Beta to be 1.031 which was very close to what the 1.00 Beta that

the market had Molson-Coors listed at. This Beta estimate shows that Molson-

Coors fluctuates very symmetrically with the S&P 500. In order to determine the

cost of equity we also had to calculate the Market Risk Premium and the Risk

Free Rate of Return. These calculations are shown in Appendix … We then

38

determined our cost of equity to be 5.17% which seemed very favorable and on

par with industry leader Anheuser Busch.

WACC and Cost of Debt

Now that our cost of equity was determined we had to find our Cost of

Debt in order to determine the WACC. We calculated Molson-Coors Cost of Debt

by determining the percentages at which debt was allocated and estimating an

effective interest rate for each level of debt. Through this evaluation we

determined Molson-Coors Cost of Debt 5.17%. We were then able to calculate

that our WACC of capital was .04. These number valuations are necessary in

order to use in the valuation models to accurately evaluate our company.

Sensitivity Analysis

All of the models that we implement are evaluated using the cost of equity

and WACC of capital that we computed. The models also assume a zero percent

growth rate initially. Sensitivity analysis aims to analyze how different

fluctuations in Cost of Equity, WACC, and growth rate affect our firm’s values.

When doing the sensitivity analysis we noticed that there are very few

combinations of growth rates and cost of capital that give us a price close to the

current market price.

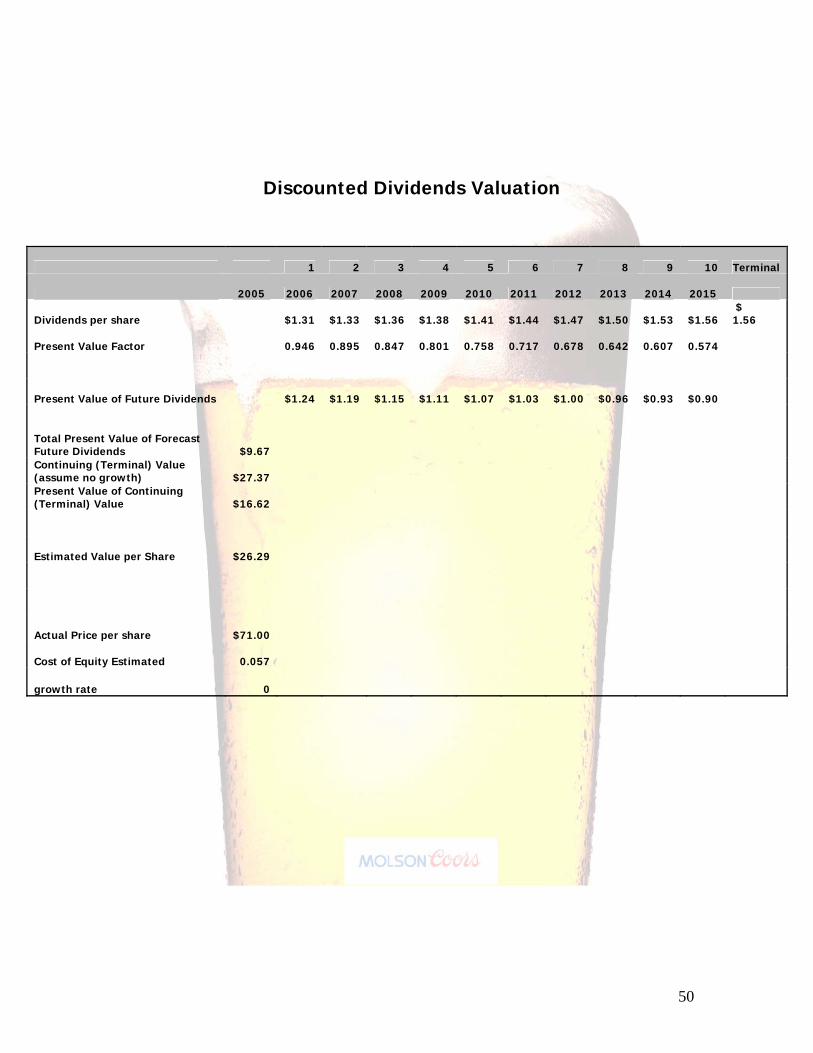

Discounted Dividends

The discounted dividends model attempts to value a firm by finding the

value of forecasted dividends. After taking into account our cost of equity, we

found the firms value to be $26.29 which is significantly under the current

market price of $71.00. This is one of the worst models for analyzing our

company. The low value could be because of the lack of large increase in

dividends in future years. The model is also shows an off price because it is

known to be one of the least accurate valuations. Looking at the sensitivity

39

analysis it is easy to see that only the best cost of equity and growth rate give us

an evaluation remotely close to the market value.

Sensitivity Analysis g - 0.02 0.03 0.04

Ke 0.06 26.29 35.27 44.76 65.39 0.10 14.66 16.31 17.49 19.07 0.15 9.58 10.04 10.32 10.66 0.20 7.08 7.25 7.35 7.46 0.25 5.60 5.68 5.72 5.76

Discounted Free Cash Flows

This method estimates the company’s value by using forecasted free cash

flows and the WACC that we computed. On this model we decided to use a 1%

growth rate on the terminal value perpetuity because we felt that free cash

would continue to grow but at a very slow rate. After looking at the figures it

appears that this model doesn’t give us an accurate evaluation either. It appears

that this model has our firm significantly undervalued with a price at $155.13.

This could be from the increase of our cash flow from operations relative to our

cash flow from investment. Looking at the sensitivity only high WACC give

valuations close to he current market price. A WACC of capital of nearly 9% is

needed for a $71 value.

Sensitivity Analysis g 0 0.01 0.02 0.03

WACC 0.05 155.13 187.61 241.74 350.01 0.06 123.48 143.55 173.66 223.84 0.07 100.95 114.25 132.87 160.80 0.08 84.12 93.38 105.72 123.01 0.09 71.08 77.77 86.37 97.84 0.1 60.69 65.66 71.88 79.88

40

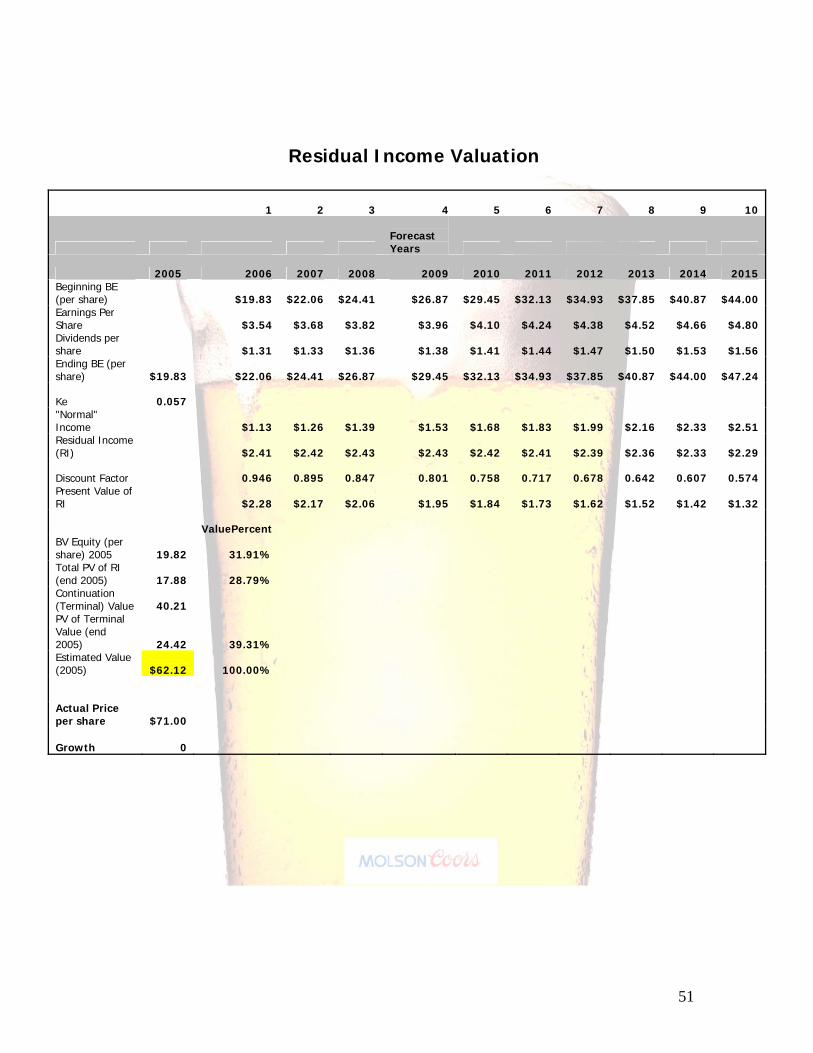

Residual Income

The Residual Income model which uses future book value of equity and

required rate of return to determine present value was fairly accurate in

evaluating our company. As long our cost of equity stays at what we estimated it

to be the firm’s value is $62.12 and with a 1.5%growth rate the firm is equal to

the market value. Sensitivity analysis shows that fluctuations in the cost of equity

would lead to drastic changes in the value of the company.

Sensitivity Analysis g 0 0.009 0.015 0.02

Ke 0.04 83.64 95.32 107.78 123.87 0.057 62.12 66.69 70.84 75.31 0.07 51.73 54.35 56.58 58.85 0.08 45.66 47.48 48.97 50.44 0.09 40.71 42.01 43.05 44.05

Abnormal Earning Growth Model

The AEG model uses earnings per share and dividends per share to value

the company. The mode uses reinvested dividends and forecasted earnings to

get a present value. Using our computed cost of equity we found the company to

be valued at $61.24 fairly close to the market rate. Lowering the cost of equity to

3% will give a value equal to the market. This model is by far the least sensitive

in valuing our company. The model gives reasonably close estimates with every

given cost of equity and growth rate.

41

Sensitivity Analysis g 0 0.02 0.03 0.04

Ke 0.01 77.36 78.94 79.73 80.52 0.03 69.67 71.08 71.78 72.49 0.057 61.24 62.46 63.06 63.67 0.07 57.83 58.97 59.54 60.11 0.09 53.27 54.31 54.83 55.34

Long Run Residual Income

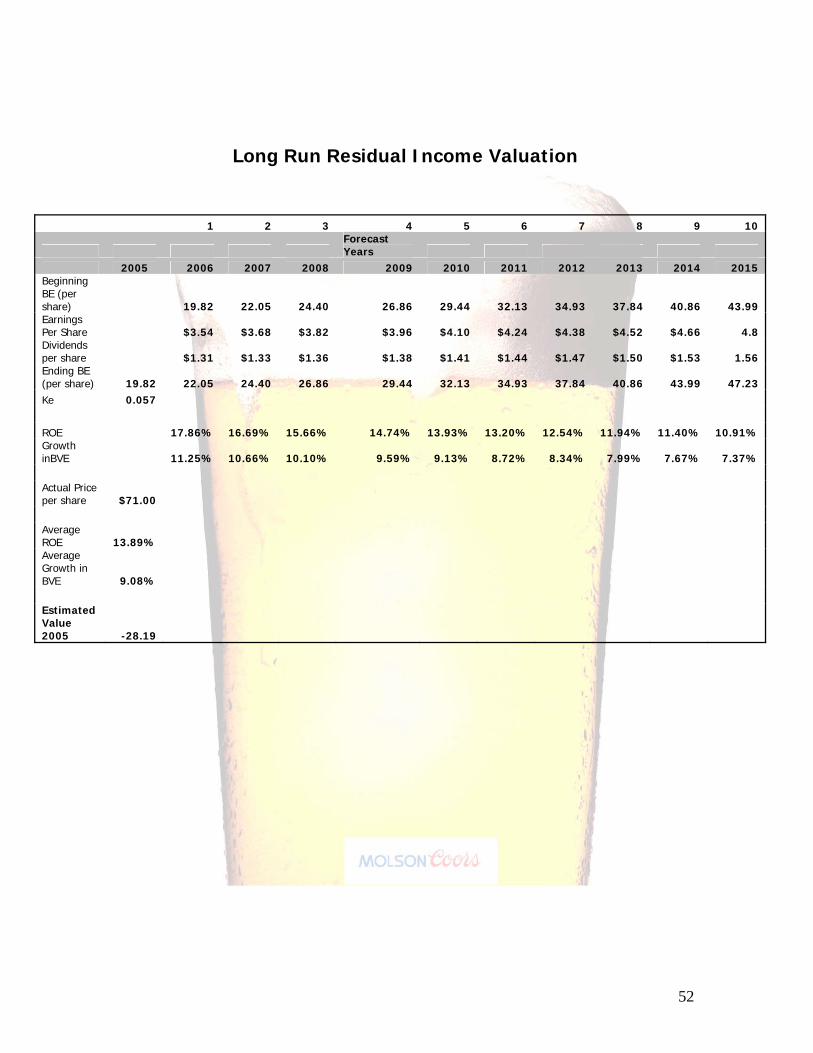

This model evaluates the company by taking the perpetuity out of a

formula derived from residual income model. Because of this the model is very

closely linked with the residual income model. Using our computed estimate of

cost of equity this model gives us a value of $68.81 which is very close to the

market value of $71. This model is very sensitive to changes in the growth rate,

with larger growth rates resulting in negative values.

Sensitivity Analysis g 0 0.02 0.04 0.06 0.0908

0.04 68.81 117.8 N/A N/A N/A0.057 48.29 63.68 115.27 N/A N/A

0.07 39.32 47.12 65.32 156.32 N/A0.08 34.41 39.27 48.99 78.16 N/A0.09 30.58 33.66 39.19 52.11 N/A

Credit Risk Analysis

In order to determine the credit risk of Molson Coors we used the Altman

Z score calculation, a method commonly used by bankers. The Z score is a

computation using weighted financial ratios to determine how efficient a

42

company can pay back debt. The higher the Z score the better and more likely

banks are to give out loans. We found that Molson Coors Z score is 2.1 which is

considered fairly risky; this is because Molson Coors has acquired a lot of short

term debt in order to pay for their recent merger. We feel that bankers will have

faith in Molson Coors and will continue to loan out money at fair rates, while not

down grading their bonds.

Valuation Results After looking at all the model evaluation it seems that the Long Run

Residual Income model gives the best estimate and Free Cash Flows gives the

worst. Long Run Residual Income is also extremely sensitive to growth rate, and

Free Cash Flows is sensitive to WACC. The AEG model is the least sensitive to

changes in growth rate and cost of equity. When trying to value our company we

feel that it was best to throw out the outlining models, the Discount Dividends

and Free Cash Flow models. After removing those inaccurate outliers we found

that our company should be valued at $64.06 which makes Molson Coors slightly

overvalued compared to its current market price of $71.00. We feel that the

models we have produced are accurate in the conclusion that Molson Coors is

slightly undervalued, but not so much to make us recommend that Molson Coors

shares be sold.

43

Appendix 1

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

CONSOLIDATED STATEMENTS OF CASHFLOWS(In Thousands)

Cash flows from operating activities

Net Income $122,964 $161,653 $174,657 $196,736 $134,944 $327,777 $343,951 $360,535 $377,502 $394,824 $412,463 $430,376 $448,512 $466,808 $485,197

Depreciation and amortization $121,091 $230,299 $236,821 $265,921 $392,814 $408,039 $424,793 $442,235 $460,393 $479,297 $498,977 $519,465 $540,794 $562,999 $586,115

amortization of debt insurance $6,790 $2,456 $34,843

loss (gain) of properties and intangibles ($30,467) ($9,816) ($4,580) ($15,027) $11,416 ($9,695) ($5,540) ($4,685) ($4,706) ($2,642) ($5,454) ($4,606) ($4,419) ($4,365) ($4,297)

Deferred income tax ($19,176) ($2,819) $53,497 $6,215 ($23,049)

(gain) loss on FX fluctuations $294 $2,576 $1,252 ($5,740) ($9,266)

Net of tax $3,676

Equity in net earnings of unconsolidated affiliates ($43,630) ($54,958) ($65,542) ($59,653) ($37)

Distributions from unconsolidated affiliates $39,453 $66,616 $70,900 $72,754 $8,612

Minotiry interest earnings $16,218 $14,491

Tax benefit from equity compensation plans $412 $8,398 $6,688

Receivables $9,499 ($254,425) $31,067 ($35,671) $9,071 $143,571 ($37,250) ($39,777) ($42,476) ($45,358) ($48,435) ($51,721) ($55,230) ($58,976) ($62,978)

Payables ($27,544) $83,493 $97,761 $4,575 $16,724 $15,288 $15,915 $16,569 $17,249 $17,957 $18,695 $19,462 $20,261 $21,093 $21,959

Inventory ($5,199) $39,210 ($5,549) ($3,441) $47,233 ($21,269) ($22,795) ($24,341) ($25,993) ($27,756) ($29,639) ($31,650) ($33,797) ($36,090) ($38,538)

Accrued expenses and other liabilities ($50,703) $24,386 ($285,808)

Other $23,562 $792 ($17,955) $21,781 ($17,955)

Operating cash flows of discountinued operations $62,563

NET CASH PROVIDED BY OPERATING ACTIVITIES $193,396 $258,545 $528,828 $499,908 $422,275 $863,710 $719,074 $750,534 $781,970 $816,322 $846,607 $881,327 $916,122 $951,469 $987,459

CASH FLOWS FROM INVESTING ACTIVITIES

Additions to properties and intangibles ($1,545) ($7,295) ($240,458) ($211,530) ($406,045) ($173,375) ($173,375) ($173,375) ($173,375) ($173,375) ($173,375) ($173,375) ($173,375) ($173,375) ($173,375)

Proceeds from sales or properties $63,529 $27,357 $16,404 $72,063 $42,450 $44,361 $44,361 $44,361 $44,361 $44,361 $44,361 $44,361 $44,361 $44,361 $44,361

Cash recognized on merger with molson $73,540

cash expended for merger-related costs ($20,382)

acquisition of subsidiaries , net of cash required ($1,587,800) ($16,561)

Trade loan repayments from customer $51,863 $54,048 $42,460

Trade loan advanced to customer ($36,553) ($25,961) ($25,369)

cash received from pension settlement with UK subsidiary $25,836

cash recognized on initial consolidation of joint ventures $20,840

Investment in molson USA, LLC ($65,000) ($2,750) ($5,240) ($2,744)

Other $9,414 ($7,561) ($630) $16

Investing cash flows of discountinued operatona ($2,817)

NET CASH USED IN INVESTING ACTIVITIES ($196,749) ($1,584,338) ($214,614) ($67,448) ($312,708) ($129,014) ($129,014) ($129,014) ($129,014) ($129,014) ($129,014) ($129,014) ($129,014) ($129,014) ($129,014)

CASH FLOWS FROM FINANCING ACTIVITIES

Issuances of stock under equity compensation plans $10,701 $15,645 $2,491 $66,764 $55,229

Dividends paid ($29,510) ($29,669) ($29,820) ($30,535) ($109,960) ($61,414.43) ($64,444.99) ($67,552.16) ($70,731.34) ($73,976.87) ($77,281.88) ($80,638.18) ($84,036.11) ($87,464.34) ($90,909.70)

dividends paid to minority interest ($7,218) ($10,569)

Proceeds from issuance of long-term debt $2,391,934 $1,037,814

payments on long-term and capital lease ($1,587,300) ($462,547) ($114,629) ($584,056)

Proceeds from short-term borrowings ($880,770) ($188,718) ($1,887,558)

Net payments on proceeds from commercial paper $249,645 ($250,000) $165,795

net proceeds from revolving credit facilities $151,273

settlement on debt-related derivatives ($11,285)

Debt issuance costs ($10,074) ($11,457)

change in overdraft balances and other $51,551 ($27,783) ($32,992) $8,715 $8,159

financing cash flows of discontinued operations ($42,846)

NET CASH USED IN FINANCING ACTIVITIES ($38,844) $1,291,668 ($357,393) ($335,664) ($188,775) ($61,414.43) ($64,444.99) ($67,552.16) ($70,731.34) ($73,976.87) ($77,281.88) ($80,638.18) ($84,036.11) ($87,464.34) ($90,909.70)

CASH AND CASH EQUIVALENTS

net (decrease) increase in cash equivalents ($42,197) ($34,125) ($43,179) $96,796 ($79,208)

effect of exchange rate changeson cash ($431) $16,159 $3,452 $6,777 ($4,392)

balance at beginning of year $119,761 $77,133 $59,167 $19,440 $123,013 $39,413 $41,031 $42,716 $44,470 $46,296 $48,197 $50,176 $52,236 $54,381 $56,614

BALANCE AT END OF YEAR $77,133 $59,167 $19,440 $123,013 $39,413 $41,031 $42,716 $44,470 $46,296 $48,197 $50,176 $52,236 $54,381 $56,614 $58,938

Divident Payout -0.24 -0.18 -0.17 -0.16 -0.8148565 -0.19d/a 17.04%

Actual Financial Statements Forecast Financial Statements

44

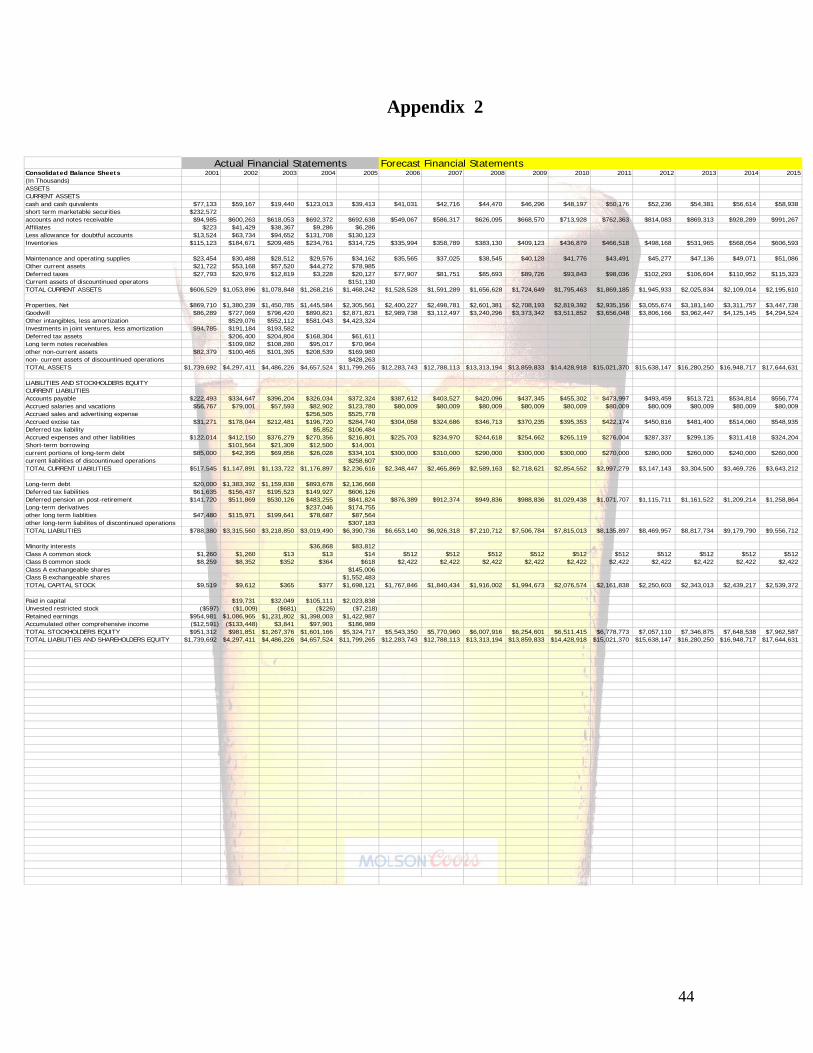

Appendix 2

������������������������Consolidated Balance Sheets 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015(In Thousands)ASSETSCURRENT ASSETScash and cash quivalents $77,133 $59,167 $19,440 $123,013 $39,413 $41,031 $42,716 $44,470 $46,296 $48,197 $50,176 $52,236 $54,381 $56,614 $58,938short term marketable securities $232,572accounts and notes receivable $94,985 $600,263 $618,053 $692,372 $692,638 $549,067 $586,317 $626,095 $668,570 $713,928 $762,363 $814,083 $869,313 $928,289 $991,267Affiliates $223 $41,429 $38,367 $9,286 $6,286Less allowance for doubtful accounts $13,524 $63,734 $94,652 $131,708 $130,123Inventories $115,123 $184,671 $209,485 $234,761 $314,725 $335,994 $358,789 $383,130 $409,123 $436,879 $466,518 $498,168 $531,965 $568,054 $606,593

Maintenance and operating supplies $23,454 $30,488 $28,512 $29,576 $34,162 $35,565 $37,025 $38,545 $40,128 $41,776 $43,491 $45,277 $47,136 $49,071 $51,086Other current assets $21,722 $53,168 $57,520 $44,272 $78,985Deferred taxes $27,793 $20,976 $12,819 $3,228 $20,127 $77,907 $81,751 $85,693 $89,726 $93,843 $98,036 $102,293 $106,604 $110,952 $115,323Current assets of discountinued operatons $151,130TOTAL CURRENT ASSETS $606,529 $1,053,896 $1,078,848 $1,268,216 $1,468,242 $1,528,528 $1,591,289 $1,656,628 $1,724,649 $1,795,463 $1,869,185 $1,945,933 $2,025,834 $2,109,014 $2,195,610

Properties, Net $869,710 $1,380,239 $1,450,785 $1,445,584 $2,305,561 $2,400,227 $2,498,781 $2,601,381 $2,708,193 $2,819,392 $2,935,156 $3,055,674 $3,181,140 $3,311,757 $3,447,738Goodwill $86,289 $727,069 $796,420 $890,821 $2,871,821 $2,989,738 $3,112,497 $3,240,296 $3,373,342 $3,511,852 $3,656,048 $3,806,166 $3,962,447 $4,125,145 $4,294,524Other intangibles, less amortization $529,076 $552,112 $581,043 $4,423,324Investments in joint ventures, less amortization $94,785 $191,184 $193,582Deferred tax assets $206,400 $204,804 $168,304 $61,611Long term notes receivables $109,082 $108,280 $95,017 $70,964other non-current assets $82,379 $100,465 $101,395 $208,539 $169,980non- current assets of discountinued operations $428,263TOTAL ASSETS $1,739,692 $4,297,411 $4,486,226 $4,657,524 $11,799,265 $12,283,743 $12,788,113 $13,313,194 $13,859,833 $14,428,918 $15,021,370 $15,638,147 $16,280,250 $16,948,717 $17,644,631

LIABILITIES AND STOCKHOLDERS EQUITYCURRENT LIABILITIESAccounts payable $222,493 $334,647 $396,204 $326,034 $372,324 $387,612 $403,527 $420,096 $437,345 $455,302 $473,997 $493,459 $513,721 $534,814 $556,774Accrued salaries and vacations $56,767 $79,001 $57,593 $82,902 $123,780 $80,009 $80,009 $80,009 $80,009 $80,009 $80,009 $80,009 $80,009 $80,009 $80,009Accrued sales and advertising expense $256,505 $525,778Accrued excise tax $31,271 $178,044 $212,481 $196,720 $284,740 $304,058 $324,686 $346,713 $370,235 $395,353 $422,174 $450,816 $481,400 $514,060 $548,935Deferred tax liability $5,852 $106,484Accrued expenses and other liabilities $122,014 $412,150 $376,279 $270,356 $216,801 $225,703 $234,970 $244,618 $254,662 $265,119 $276,004 $287,337 $299,135 $311,418 $324,204Short-term borrowing $101,564 $21,309 $12,500 $14,001current portions of long-term debt $85,000 $42,395 $69,856 $26,028 $334,101 $300,000 $310,000 $290,000 $300,000 $300,000 $270,000 $280,000 $260,000 $240,000 $260,000current liabilities of discountinued operations $258,607TOTAL CURRENT LIABILITIES $517,545 $1,147,891 $1,133,722 $1,176,897 $2,236,616 $2,348,447 $2,465,869 $2,589,163 $2,718,621 $2,854,552 $2,997,279 $3,147,143 $3,304,500 $3,469,726 $3,643,212

Long-term debt $20,000 $1,383,392 $1,159,838 $893,678 $2,136,668Deferred tax liabilities $61,635 $156,437 $195,523 $149,927 $606,126Deferred pension an post-retirement $141,720 $511,869 $530,126 $483,255 $841,824 $876,389 $912,374 $949,836 $988,836 $1,029,438 $1,071,707 $1,115,711 $1,161,522 $1,209,214 $1,258,864Long-term derivatives $237,046 $174,755other long term liablities $47,480 $115,971 $199,641 $78,687 $87,564other long-term liabilites of discontinued operations $307,183TOTAL LIABILITIES $788,380 $3,315,560 $3,218,850 $3,019,490 $6,390,736 $6,653,140 $6,926,318 $7,210,712 $7,506,784 $7,815,013 $8,135,897 $8,469,957 $8,817,734 $9,179,790 $9,556,712

Minority interests $36,868 $83,812Class A common stock $1,260 $1,260 $13 $13 $14 $512 $512 $512 $512 $512 $512 $512 $512 $512 $512Class B common stock $8,259 $8,352 $352 $364 $618 $2,422 $2,422 $2,422 $2,422 $2,422 $2,422 $2,422 $2,422 $2,422 $2,422Class A exchangeable shares $145,006Class B exchangeable shares $1,552,483TOTAL CAPITAL STOCK $9,519 $9,612 $365 $377 $1,698,121 $1,767,846 $1,840,434 $1,916,002 $1,994,673 $2,076,574 $2,161,838 $2,250,603 $2,343,013 $2,439,217 $2,539,372

Paid in capital $19,731 $32,049 $105,111 $2,023,838Unvested restricted stock ($597) ($1,009) ($681) ($226) ($7,218)Retained earnings $954,981 $1,086,965 $1,231,802 $1,398,003 $1,422,987Accumulated other comprehensive income ($12,591) ($133,448) $3,841 $97,901 $186,989TOTAL STOCKHOLDERS EQUITY $951,312 $981,851 $1,267,376 $1,601,166 $5,324,717 $5,543,350 $5,770,960 $6,007,916 $6,254,601 $6,511,415 $6,778,773 $7,057,110 $7,346,875 $7,648,538 $7,962,587TOTAL LIABILITIES AND SHAREHOLDERS EQUITY $1,739,692 $4,297,411 $4,486,226 $4,657,524 $11,799,265 $12,283,743 $12,788,113 $13,313,194 $13,859,833 $14,428,918 $15,021,370 $15,638,147 $16,280,250 $16,948,717 $17,644,631

Total Liabilities = 54.16%SE = 45.13%

Current Liabilities % of Liabilities = 105.00%

Total Assets 3.98% 147.02% 4.39% 3.82% 153.34% 4.06%

Avg minus two outliers = 0 4% 104%

Actual Financial Statements Forecast Financial Statements

����

45

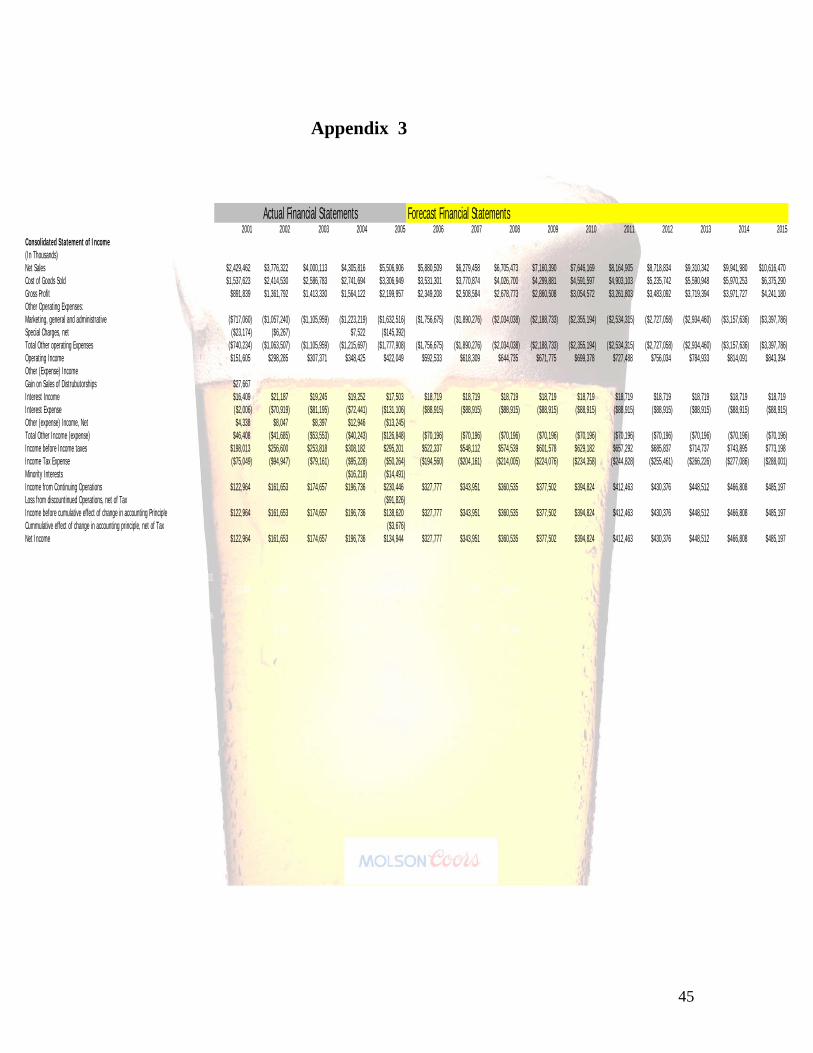

Appendix 3

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015Consolidated Statement of Income(In Thousands)Net Sales $2,429,462 $3,776,322 $4,000,113 $4,305,816 $5,506,906 $5,880,509 $6,279,458 $6,705,473 $7,160,390 $7,646,169 $8,164,905 $8,718,834 $9,310,342 $9,941,980 $10,616,470Cost of Goods Sold $1,537,623 $2,414,530 $2,586,783 $2,741,694 $3,306,949 $3,531,301 $3,770,874 $4,026,700 $4,299,881 $4,591,597 $4,903,103 $5,235,742 $5,590,948 $5,970,253 $6,375,290Gross Profit $891,839 $1,361,792 $1,413,330 $1,564,122 $2,199,957 $2,349,208 $2,508,584 $2,678,773 $2,860,508 $3,054,572 $3,261,803 $3,483,092 $3,719,394 $3,971,727 $4,241,180Other Operating Expenses:Marketing, general and administrative ($717,060) ($1,057,240) ($1,105,959) ($1,223,219) ($1,632,516) ($1,756,675) ($1,890,276) ($2,034,038) ($2,188,733) ($2,355,194) ($2,534,315) ($2,727,058) ($2,934,460) ($3,157,636) ($3,397,786)Special Charges, net ($23,174) ($6,267) $7,522 ($145,392)Total Other operating Expenses ($740,234) ($1,063,507) ($1,105,959) ($1,215,697) ($1,777,908) ($1,756,675) ($1,890,276) ($2,034,038) ($2,188,733) ($2,355,194) ($2,534,315) ($2,727,058) ($2,934,460) ($3,157,636) ($3,397,786)Operating Income $151,605 $298,285 $307,371 $348,425 $422,049 $592,533 $618,309 $644,735 $671,775 $699,378 $727,488 $756,034 $784,933 $814,091 $843,394Other (Expense) IncomeGain on Sales of Distrubutorships $27,667Interest Income $16,409 $21,187 $19,245 $19,252 $17,503 $18,719 $18,719 $18,719 $18,719 $18,719 $18,719 $18,719 $18,719 $18,719 $18,719Interest Expense ($2,006) ($70,919) ($81,195) ($72,441) ($131,106) ($88,915) ($88,915) ($88,915) ($88,915) ($88,915) ($88,915) ($88,915) ($88,915) ($88,915) ($88,915)Other (expense) Income, Net $4,338 $8,047 $8,397 $12,946 ($13,245)Total Other Income (expense) $46,408 ($41,685) ($53,553) ($40,243) ($126,848) ($70,196) ($70,196) ($70,196) ($70,196) ($70,196) ($70,196) ($70,196) ($70,196) ($70,196) ($70,196)Income before Income taxes $198,013 $256,600 $253,818 $308,182 $295,201 $522,337 $548,112 $574,539 $601,578 $629,182 $657,292 $685,837 $714,737 $743,895 $773,198Income Tax Expense ($75,049) ($94,947) ($79,161) ($95,228) ($50,264) ($194,560) ($204,161) ($214,005) ($224,076) ($234,358) ($244,828) ($255,461) ($266,226) ($277,086) ($288,001)Minority Interests ($16,218) ($14,491)Income from Continuing Operations $122,964 $161,653 $174,657 $196,736 $230,446 $327,777 $343,951 $360,535 $377,502 $394,824 $412,463 $430,376 $448,512 $466,808 $485,197Loss from discountinued Operations, net of Tax ($91,826)Income before cumulative effect of change in accounting Principle $122,964 $161,653 $174,657 $196,736 $138,620 $327,777 $343,951 $360,535 $377,502 $394,824 $412,463 $430,376 $448,512 $466,808 $485,197Cummulative effect of change in accounting principle, net of Tax ($3,676)Net Income $122,964 $161,653 $174,657 $196,736 $134,944 $327,777 $343,951 $360,535 $377,502 $394,824 $412,463 $430,376 $448,512 $466,808 $485,197

Sustainable Growth Rate = 0.01Sales Growth Rate = 55.44% 5.93% 7.64% 27.89% Average Growth Rate = 6.78% 106.78%

Cost of Goods Sold Percentage Of Sales Plus Growth = 60%Marketing, general and administrative Growth Rate = 47.44% 4.61% 10.60% 33.46% avg = 7.61% 107.61%Average Interest Income = $18,719Average Interest Expense without outlier = ($88,915)Provision for income tax Avg = -37.25%

Actual Financial Statements Forecast Financial Statements

46

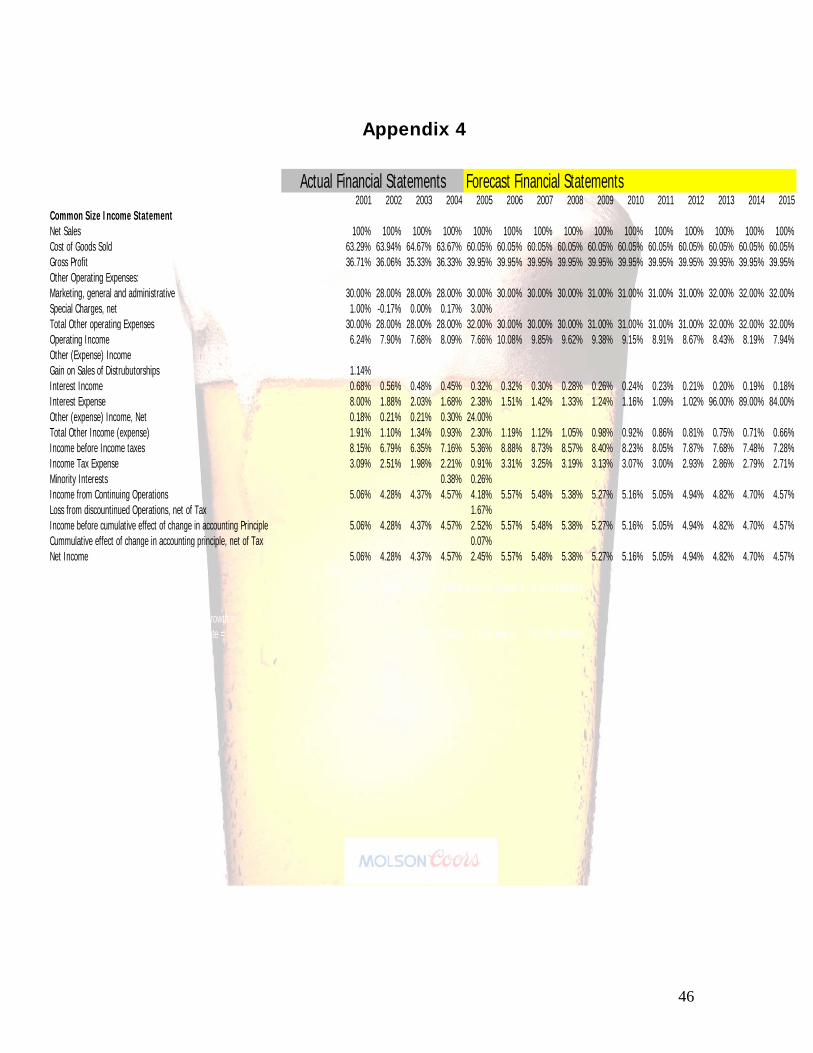

���������������������������� Appendix 4������������������