Embed Size (px)

Citation preview

MOJAKOE UAS - AKUNTANSI KEUANGAN LANJUTAN

Dilarang memperbanyak MOJAKOE ini tanpa seijin SPA FEUI. Download MOJAKOE dan SPA Mentoring di : http://spa-feui.com

AKL UAS 2014

spa-feui.com

Question 1 (12.5%) - UTS AKL 2013/2014

Saia Corp acquired 80% ownership of Sakato Corp at book value on January 1, 2010. On

acquisition date, Sakato Corp Common Stock and Retained Earnings were $250,000 and

$150,000, respectively. The following are separate earnings and dividend for Saia Corp and

Sakato Corp.

Year

Saia Corp Sakato Corp

Earnings Dividend Earnings Dividend

2010 140,000 75,000 75,000 30,000

2011 180,000 80,000 90,000 40,000

2012 210,000 100,000 100,000 45,000

a. On January 1, 2012, Sakato Corp bought an equipment from Saia Corp for $85,000 which

cost Saia Corp $100,000. Saia Corp purchased this equipment on December 31, 2009

from non-affiliate, with expected useful life of 10 years and no residual value. Saia Corp

used straight line method to depreciate the equipment. Sakato Corp management decided

to continue depreciating the equipment using the straight line method with no residual

value and 8 years expected useful life.

Required :

Prepare journal entries for Saia Corp and eliminating entries at the end of 2012 assuming

that Saia Corp used cost method to account its investment on Sakato Corp. See the hints

below. (12.5%)

Hints:

The above transactions are independent of each other. Except for the BV Sakato

Corp, separate earnings, and dividend information, please use the information on

each transaction only to do the requirement.

Journal entries that you have to make : recognize income from subsidiary, dividend

from subsidiary and intercompany transaction adjustment.

Eliminating entries that you have to make : basic elimination entry and

intercompany transaction elimination entry.

AKL UAS 2014

spa-feui.com

Question 2 (20%) - UTS AKL 2013/2014

PT Siang Miang issued to PT Bariton Rp400,000 par value, 10 year bonds with a coupon rate

of 12% on January 1, 2005, the bonds are issued at a premium, Rp420,000 to yield the current

market interest rate of 11%. The bonds pay interest semiannually on July 1 and January 1.

On January 1, 2008, PT Propoti purchased Rp 100,000 of the bonds from PT Bariton for

Rp104,900. Note that PT Propoti’s purchase price reflects the current market interest rate of

10% when the bonds have 14 payments left to maturity. PT Propoti owns 65% of the voting

commfdcon shares of PT Siang Miang and prepares consolidated financial statement. Both PT

Propoti and PT Siang Miang amortized bonds premiums using the effective interest method.

Additional information :

Bond Premium Amortization table, when PT Siang Miang issued to PT Bariton

Payment Period Interest Interest Amortization Carrying Value

Number End Payment Expense Premium of Bonds

01/01/05 420,000

1 01/07/05 24,000 23,100 (900) 419,100

2 01/01/06 24,000 23,051 (949) 418,151

3 01/07/06 24,000 22,998 (1,002) 417,149

4 01/01/07 24,000 22,943 (1,057) 416,092

5 01/07/07 24,000 22,885 (1,115) 414,977

6 01/01/08 24,000 22,824 (1,176) 413,801

7 01/07/08 24,000 22,759 (1,241) 412,560

8 01/01/09 24,000 22,691 (1,309) 411,251

9 01/07/09 24,000 22,619 (1,381) 409,870

10 01/01/10 24,000 22,543 (1,457) 408,413

11 01/07/10 24,000 22,463 (1,537) 406,876

etc

Bond Premium Amortization table, when PT Propoti purchased from PT Bariton

Payment Period Interest Interest Amortization Carrying Value

Number End Payment Expense Premium of Bonds

01/01/08 104,900

1 01/07/08 6,000 5,245 (755) 104,145

2 01/01/09 6,000 5,207 (792) 103,352

3 01/07/09 6,000 5,168 (832) 102,520

4 01/01/10 6,000 5,126 (874) 101,646

5 01/07/10 6,000 5,082 (918) 100,728

etc

AKL UAS 2014

spa-feui.com

Required :

A. Assume PT Propoti use equity method to record its investment in PT Siang Miang (15%)

1. Prepare the worksheet elimination entry or entries needed to remove the effects of

the incorporate bond ownership in preparing consolidated financial statement for

2008.

2. Assuming that PT Siang Miang reports net income of Rp 20,000 for 2008, compute

the amount of income assigned to noncontrolling shareholders in the 2008

consolidated income statement.

3. Prepare the worksheet elimination entry or entries needed to remove the effects of

the intercorporate bond ownership in preparing consolidated financial statement

for 2009.

B. Assume PT Propoti use cost method to record its investment in PT Siang Miang (5%)

Prepare the worksheet elimination entry or entries to remove the effects of the

intercorporate bond ownership in preparing consolidated financial statement for 2009.

AKL UAS 2014

spa-feui.com

Question 3 (20%) - UAS AKL 2013/2014

Part A – 10%

PT Blankko Periklanan acquired 60% of PT Qufoty Pabrikan’s shares on December 31, 2001,

at underlying book value of $180,000. At that date, the fair value of the non controlling interest

was equal to 40% of the book value of PT Qufoty Pabrikan. PT Qufoty’s statement of financial

position on January 1, 2007, contained the following balances:

Cash $ 80,000 Accounts Payable $ 60,000

Accounts Receivable 100,000 Bonds Payable 240,000

Inventory 160,000 Share Capital-Ordinary 100,000

Buildings & Equipment 700,000 Share Premium-Ordinary 150,000

Less: Accumulated Depreciation (240,000) Retained Earnings 250,000

________ ________

Total Assets $800,000 Total Liabilities & Equities $800,000

======= =======

On January 1, 2007, PT Qufoty purchased 2,000 of its own $10 par value common shares from

Nonaffiliated Corporation for $42 per share. PT Blankko Periklanan uses the fully adjusted

equity method.

Required:

a. Compute the change in the book value of the equity attributable to the parent as a result of

the repurchase of shares it holds. (3%)

b. Give the entry to be recorded on PT Blankko Periklanan’s books to recognize the change

in book value of shares it holds. (2%)

c. Give the elimination entry needed in preparing a consolidated statement of financial

position immediately following the purchase of shares by PT Qufoty. (5%)

Part B – 10%

PT Yanfoz Pabrikan issued stock with par value of $67,000 and a market value of $503,500 to

acquire 95% of PT Suonab’s common stock on August 30, 2011. At that date, the fair value of

the non controlling interest was $26,500. On January 1, 2011, PT Suonab reported the

following stockholders’ equity balance:

AKL UAS 2014

spa-feui.com

Share Capital – Ordinary $150,000

Share Premium – Ordinary 50,000

Retained Earnings 300,000

_________

Total Stockholders’ Equity $500,000

========

PT Suonab reported net income of $60,000 in 2011, earned uniformly throughout the year, and

declared and paid dividends of $10,000 on June 30 and $25,000 on December 1, 2011. PT

Yanfoz accounts for its investment in PT Suonab using the fully adjusted equity method.

PT Yanfoz reported retained earnings of $400,000 on January 1, 2011, and had 2011 income

of $140,000 from its separate operation. PT Yanfoz paid dividends of $80,000 on December

31, 2011.

Required:

a. Compute consolidated retained earnings as of January 1. 2011, as it would appear in

comparative consolidated financial statement presented at the end of 2011. (2%)

b. Compute consolidated net income and income to the controlling interest for 2011. (3%)

c. Compute consolidated retained earnings as of December 31, 2011. (2%)

d. Give the December 31, 2011, balance of PT Yanfoz Pabrikan’s investment in PT Suonab.

(3%)

AKL UAS 2014

spa-feui.com

Question 4 (25%) - UAS AKL 2013/2014

On January 2, 2012, PT Parent, a Japan Company, acquired a 65% ownership in PT Sons, an

Indonesia company at book value. In 2012, the financial highlights of PT Sons are as follow:

PT Sons declared and paid dividends for IDR 52.000.000, - on September 1, 2013. Functional

Currency of PT Sons is Rupiah and PT Parent is Yen. PT Sons trial balance at December 31,

2013 and the related exchange rate (IDR / 1 JPY) are as follow:

Required :

1. Determine whether the financial statements are translated with translation or remeasurement

method! Why? (5%)

2. Complete the translation or remeasurement working paper in 2013 (see attachment). (15%)

3. Prepare the investment journal entries for PT Parent in 2013 assuming the translation

adjustment at the end of 2012 is amount to JPY 100.000 (Credit Balance). PT Parent use

the fully adjusted equity method. (5%)

IDR

R/E Jan 2, 2012 1,640,000,000

Net Income 2012 106,050,000

Dividend, Sept 15, 2012 (50,000,000)

R/E Dec 31, 2012 1,696,050,000

Date Rate

January 2, 2012 111

September 15, 2012 114

December 31, 2012 120

Average 2012 115

September 1, 2013 113

December 31, 2013 110

Average 2013 112

IDR

Cash 390,000,000

Account Receivable 534,000,000

Inventory 1,320,000,000

Plant & Equipment 2,520,000,000

Account Payable 516,000,000

Capital Stock 2,500,000,000

Retained Earning, Jan 1 1,696,050,000

Sales 1,012,500,000

COGS 621,000,000

Operating Expenses 195,750,000

Depreciation Expense 51,300,000

Income tax exp 40,500,000

Dividend 52,000,000

AKL UAS 2014

spa-feui.com

ATTACHMENT

NAME : ………………………………….. NPM: …………………..

Working Paper

Accounts IDR Rate JPY

Cash

Account Receivable

Inventory

Plant & Equipment

COGS

Operating Expenses

Depreciation Expense

Income tax exp

Dividend

Total

Account Payable

Capital Stock

Retained Earning, Jan 1

Sales

Total

AKL UAS 2014

spa-feui.com

Answers

Question 1 (12.5%) - UTS AKL 2013/2014

Chapter 7 Intercompany Transfers of Noncurrent Assets and Services

Prepare journal entries for Saia Corp and eliminating entries at the end of 2012 assuming

that Saia Corp used cost method to account its investment on Sakato Corp.

The calculation

Original cost to Saia Corp. 100,000

Accumulated depreciation on January 1, 2012

Annual depreciation (100,000 : 10 years) 10,000

Number of years x2 (20,000)

Book value on January 1, 2012 80,000

Sale price of the equipment 85,000

Less : Book value of the equipment (80,000)

Gain on sale of the equipment 5,000

Journal entries for Saia Corp and eliminating entries at the end of 2012

Record sale of equipment :

Cash 85,000

Accumulated Depreciation 20,000

Equipment 100,000

Gain on Sale of Equipment 5,000

Record dividend :

Cash 36,000*

Dividend Income 36,000

* 36,000 = 80% x 45,000

AKL UAS 2014

spa-feui.com

The calculation

Equipment (January 1, 2012)

Price - Acc. Depreciation = Book Value

If transferred 85,000 - 0 = 85,000

If not transferred 100,000 - 20,000 = 80,000

Differential (15,000) (20,000) 5,000

Understated Understated

Depreciation

If transferred 10,625*

If not transferred 10,000**

Differential 625 -> Overstated

*10,625 = 85,000/8 years

**10,000 = 100,000/10 years

Elimination Entries

Acc. Depreciation 625

Depreciation Expense 625

Eliminate Asset Purchase from Saia Corp

Gain on Sale 5,000

Equipment 15,000

Accumulated Depreciation 20,000

Investment elimination entry :

Common Stock 150,000

Retained Earnings 250,000

Investment in Sakato Corp 320,000

NCI in NA of Sakato Corp 80,000

AKL UAS 2014

spa-feui.com

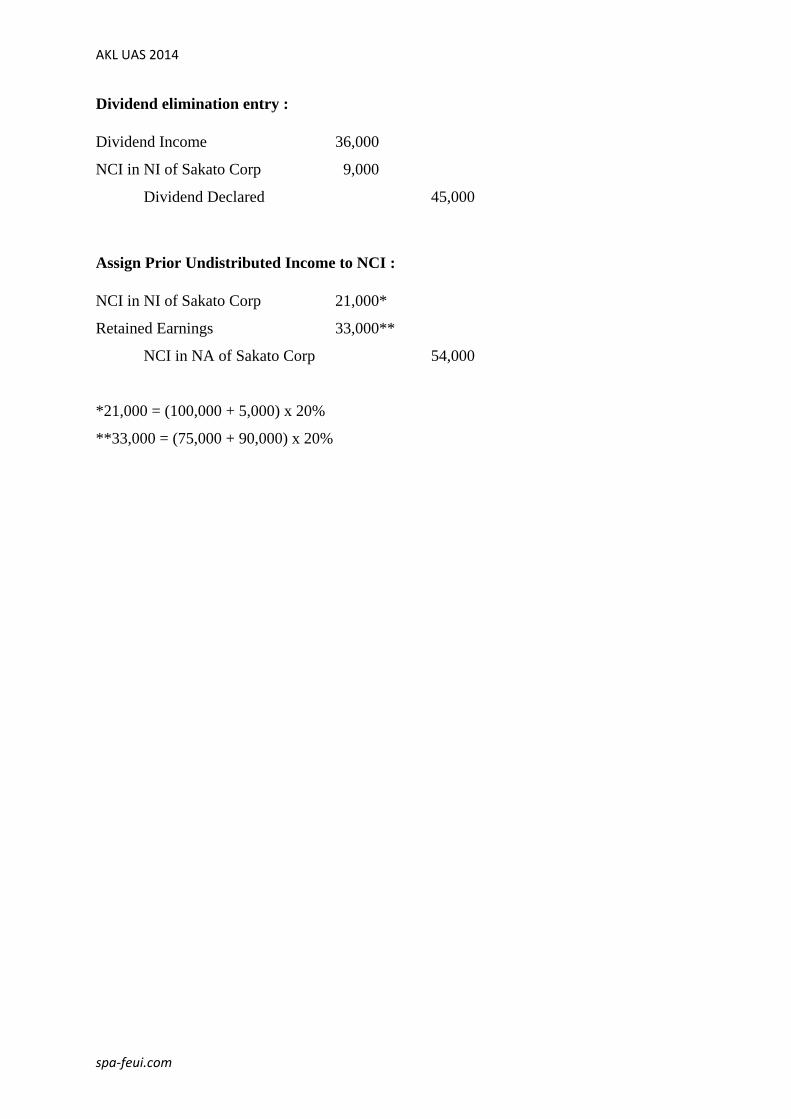

Dividend elimination entry :

Dividend Income 36,000

NCI in NI of Sakato Corp 9,000

Dividend Declared 45,000

Assign Prior Undistributed Income to NCI :

NCI in NI of Sakato Corp 21,000*

Retained Earnings 33,000**

NCI in NA of Sakato Corp 54,000

*21,000 = (100,000 + 5,000) x 20%

**33,000 = (75,000 + 90,000) x 20%

AKL UAS 2014

spa-feui.com

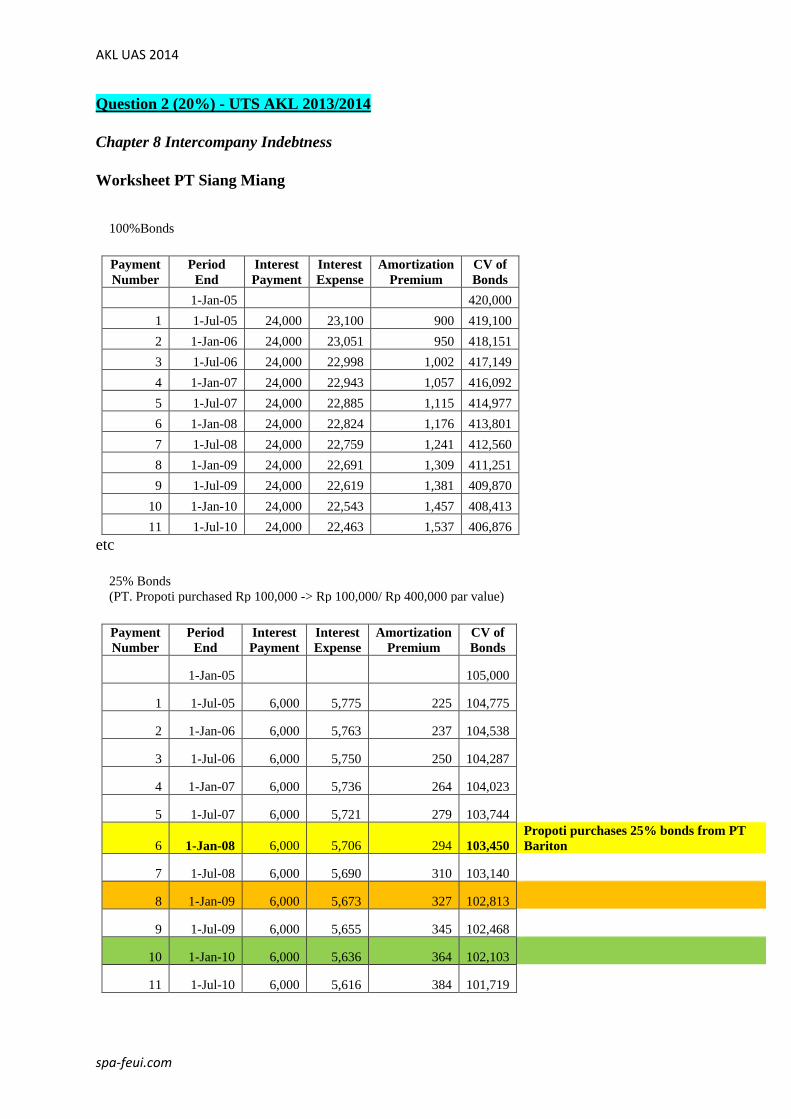

Question 2 (20%) - UTS AKL 2013/2014

Chapter 8 Intercompany Indebtness

Worksheet PT Siang Miang

100%Bonds

Payment

Number

Period

End

Interest

Payment

Interest

Expense

Amortization

Premium

CV of

Bonds

1-Jan-05 420,000

1 1-Jul-05 24,000 23,100 900 419,100

2 1-Jan-06 24,000 23,051 950 418,151

3 1-Jul-06 24,000 22,998 1,002 417,149

4 1-Jan-07 24,000 22,943 1,057 416,092

5 1-Jul-07 24,000 22,885 1,115 414,977

6 1-Jan-08 24,000 22,824 1,176 413,801

7 1-Jul-08 24,000 22,759 1,241 412,560

8 1-Jan-09 24,000 22,691 1,309 411,251

9 1-Jul-09 24,000 22,619 1,381 409,870

10 1-Jan-10 24,000 22,543 1,457 408,413

11 1-Jul-10 24,000 22,463 1,537 406,876

etc

25% Bonds

(PT. Propoti purchased Rp 100,000 -> Rp 100,000/ Rp 400,000 par value)

Payment

Number

Period

End

Interest

Payment

Interest

Expense

Amortization

Premium

CV of

Bonds

1-Jan-05 105,000

1 1-Jul-05 6,000 5,775 225 104,775

2 1-Jan-06 6,000 5,763 237 104,538

3 1-Jul-06 6,000 5,750 250 104,287

4 1-Jan-07 6,000 5,736 264 104,023

5 1-Jul-07 6,000 5,721 279 103,744

6 1-Jan-08 6,000 5,706 294 103,450

Propoti purchases 25% bonds from PT

Bariton

7 1-Jul-08 6,000 5,690 310 103,140

8 1-Jan-09 6,000 5,673 327 102,813

9 1-Jul-09 6,000 5,655 345 102,468

10 1-Jan-10 6,000 5,636 364 102,103

11 1-Jul-10 6,000 5,616 384 101,719

AKL UAS 2014

spa-feui.com

Worksheet PT Propoti

Payment

Number Date

Interest

Receipt

Interest

Revenue

Amortization

Premium

CV of

Bonds

1-Jan-08 104,900

Propoti purchases 25% bonds from PT

Bariton

1 1-Jul-08 6,000 5,245 755 104,145

2 1-Jan-09 6,000 5,207 792 103,352

3 1-Jul-09 6,000 5,168 832 102,520

4 1-Jan-10 6,000 5,126 874 101,646

5 1-Jul-10 6,000 5,082 918 100,728

A.Assume PT Propoti use equity method to record its investment in PT Siang Miang

(15%)

1. Prepare the worksheet elimination entry or entries needed to remove the effects of the

incorporate bond ownership in preparing consolidated financial statement for 2008.

Computation Gain (Loss)

BV of Siang Miang's Bonds 103,450

Price Paid by Proporti 104,900

Gain (Loss) -1,450

Premium of Siang Miang 3,450

Premium of Propoti 4,900

Gain (Loss) -1,450

Eliminate intercorporate bond holdings:

Bonds Payable 102,813

Interest Income 10,452

Constructive Loss on Bond Retirement 1,450

Investment in PT Siang Miang Bonds 103,352

Interest Expense 11,363

Interest Income : 10,452 = 5,245 + 5,207

Interest Expense : 11,363 = 5,690 + 5,673

AKL UAS 2014

spa-feui.com

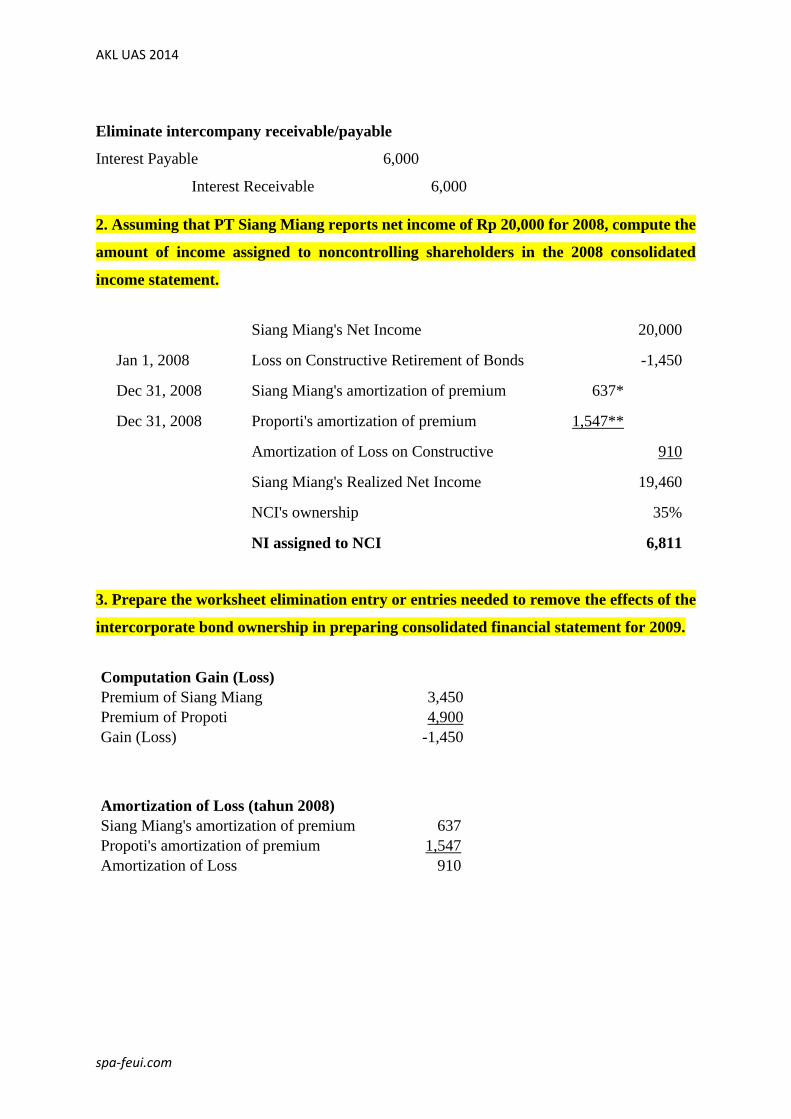

Eliminate intercompany receivable/payable

Interest Payable 6,000

Interest Receivable 6,000

2. Assuming that PT Siang Miang reports net income of Rp 20,000 for 2008, compute the

amount of income assigned to noncontrolling shareholders in the 2008 consolidated

income statement.

Siang Miang's Net Income

20,000

Jan 1, 2008 Loss on Constructive Retirement of Bonds

-1,450

Dec 31, 2008 Siang Miang's amortization of premium 637*

Dec 31, 2008 Proporti's amortization of premium 1,547**

Amortization of Loss on Constructive

910

Siang Miang's Realized Net Income

19,460

NCI's ownership

35%

NI assigned to NCI

6,811

3. Prepare the worksheet elimination entry or entries needed to remove the effects of the

intercorporate bond ownership in preparing consolidated financial statement for 2009.

Computation Gain (Loss)

Premium of Siang Miang 3,450

Premium of Propoti 4,900

Gain (Loss) -1,450

Amortization of Loss (tahun 2008)

Siang Miang's amortization of premium 637

Propoti's amortization of premium 1,547

Amortization of Loss 910

AKL UAS 2014

spa-feui.com

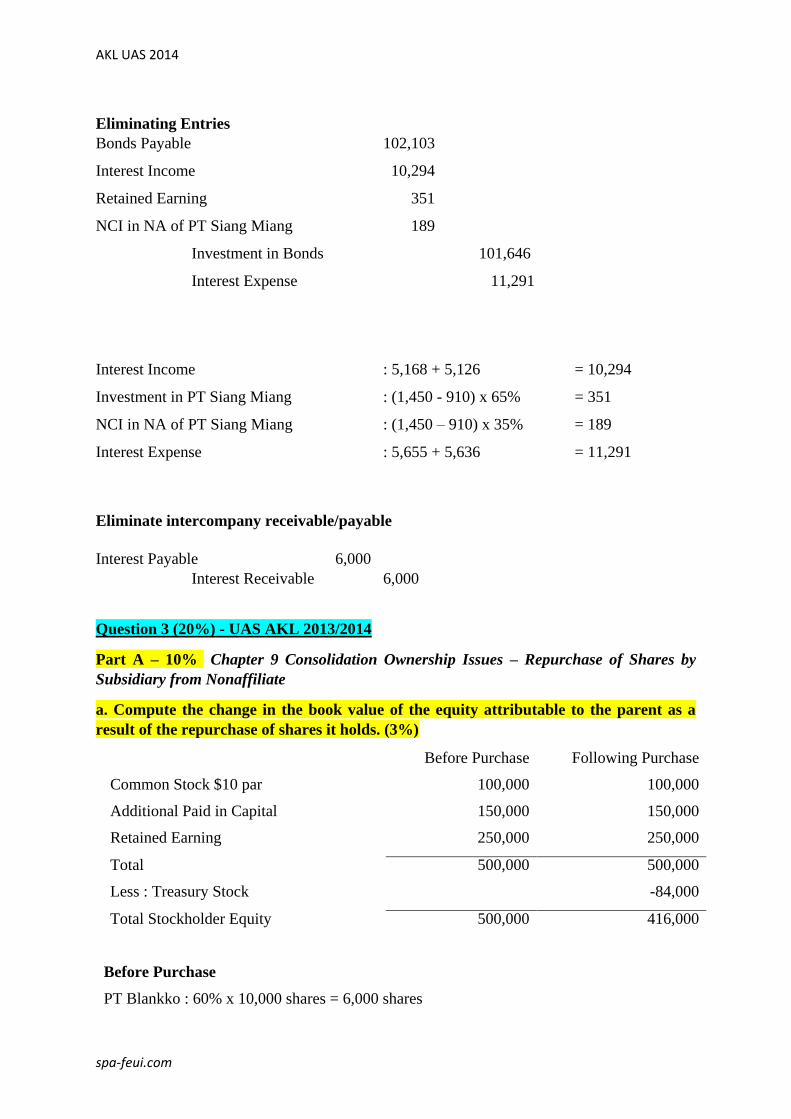

Bonds Payable 102,103

Interest Income 10,294

Investment in PT Siang Miang 351

NCI in NA of PT Siang Miang 189

Investment in Bonds 101,646

Interest Expense 11,291

Interest Income : 5,168 + 5,126 = 10,294

Investment in PT Siang Miang : (1,450 - 910) x 65% = 351

NCI in NA of PT Siang Miang : (1,450 – 910) x 35% = 189

Interest Expense : 5,655 + 5,636 = 11,291

Eliminate intercompany receivable/payable

Interest Payable 6,000

Interest Receivable 6,000

B. Assume PT Propoti use cost method to record its investment in PT Siang Miang (5%)

Prepare the worksheet elimination entry or entries to remove the effects of the

intercorporate bond ownership in preparing consolidated financial statement for 2009.

Computation Gain (Loss)

Premium of Siang Miang 3,450

Premium of Propoti 4,900

Gain (Loss) -1,450

Amortization of Loss (tahun 2008)

Siang Miang's amortization of premium 637

Propoti's amortization of premium 1,547

Amortization of Loss 910

AKL UAS 2014

spa-feui.com

Eliminating Entries

Bonds Payable 102,103

Interest Income 10,294

Retained Earning 351

NCI in NA of PT Siang Miang 189

Investment in Bonds 101,646

Interest Expense 11,291

Interest Income : 5,168 + 5,126 = 10,294

Investment in PT Siang Miang : (1,450 - 910) x 65% = 351

NCI in NA of PT Siang Miang : (1,450 – 910) x 35% = 189

Interest Expense : 5,655 + 5,636 = 11,291

Eliminate intercompany receivable/payable

Interest Payable 6,000

Interest Receivable 6,000

Question 3 (20%) - UAS AKL 2013/2014

Part A – 10% Chapter 9 Consolidation Ownership Issues – Repurchase of Shares by

Subsidiary from Nonaffiliate

a. Compute the change in the book value of the equity attributable to the parent as a

result of the repurchase of shares it holds. (3%)

Before Purchase Following Purchase

Common Stock $10 par 100,000 100,000

Additional Paid in Capital 150,000 150,000

Retained Earning 250,000 250,000

Total 500,000 500,000

Less : Treasury Stock -84,000

Total Stockholder Equity 500,000 416,000

Before Purchase

PT Blankko : 60% x 10,000 shares = 6,000 shares

AKL UAS 2014

spa-feui.com

PT Qufoty : 40% x 10,000 shares = 4,000 shares

After Purchase

PT Blankko : 6,000 shares /8,000 shares x 100% = 75%

PT Qufoty : (4,000 shares – 2,000 shares) /8,000 shares x 100% = 25%

Before Purchase Following Purchase

PT Qufoty' total stockholders' equity 500,000 416,000

PT Blankko' proportionate share 60% 75%

BV of PT Blankko proportionate investment in PT

Qufoty 300,000 312,000

Change in the book value of the equity attributable to the parent as a result of the repurchase

of shares it holds = 312,000 – 300,000 = 12,000

b. Give the entry to be recorded on PT Blankko Periklanan’s books to recognize the

change in book value of shares it holds. (2%)

Investment in PT Qufoty 12,000

Additional Paid in Capital 12,000

c. Give the elimination entry needed in preparing a consolidated statement of financial

position immediately following the purchase of shares by PT Qufoty. (5%)

Book Value Calculations:

NCI

25%

+ Blatant

75%

= Com.

Stock

+

Add.

Paid-In

Capital

+ Treasury

Stock

+ Retained

Earnings

Original book value 200,000 300,000 100,000 150,000 250,000

Shares repurchased (96,000) 12,000 (84,000)

Ending book value 104,000 312,000 100,000 150,000 (84,000) 250,000

Common stock 100,000

Additional paid-in capital 150,000

Retained earnings 250,000

Treasury stock 84,000

Investment in PT Qufoty 312,000

NCI in NA of PT Qufoty 104,000

AKL UAS 2014

spa-feui.com

Part B – 10% Additional Consolidation reporting Issues -Midyear Acquisition

a. Compute consolidated retained earnings as of January 1. 2011, as it would appear in

comparative consolidated financial statement presented at the end of 2011. (2%)

The retained earnings balance reported for the consolidated entity as of January 1, 2011, would

be $400,000.

b. Compute consolidated net income and income to the controlling interest for 2011. (3%)

Separate earnings of PT Yanfoz $140,000

Net income reported by PT Suonab $60,000

Portion of year ownership was held by PT Yanfoz x 4/12

Income earned following acquisition 20,000

Consolidated net income $160,000

Income to noncontrolling interest ($20,000 x 0.05) (1,000)

Income to controlling interest $159,000

c. Compute consolidated retained earnings as of December 31, 2011. (2%)

Consolidated retained earnings, January 1, 2011 $400,000

Income to controlling interest 159,000

Dividends paid by PT Yanfoz (80,000)

Consolidated retained earnings, December 31, 2011 $479,000

d. Give the December 31, 2011, balance of PT Yanfoz Pabrikan’s investment in PT

Suonab. (3%)

Purchase price on August 30, 2011 $503,500

Equity method income 19,000*

Dividends received from PT Suonab ($25,000 x 0.95) (23,750)

Balance in investment account December 31, 2011 $498,750

*19,000 = Income earned following acquisition – Income to NCI

19,000 = 20,000 – (5% x 20,000)

AKL UAS 2014

spa-feui.com

Question 4 (25%) - UAS AKL 2013/2014

Chapter 12 Multinational Accounting : Issues in Financial Reporting and Translation of

Foreign Entity Statements

1. Determine whether the financial statements are translated with translation or

remeasurement method! Why? (5%)

Financial statements are translated with translation, because PT Sons has recorded with its

functional currency (Functional Currency = Local Currency). Therefore, we only need to

translate it.

2. Complete the translation or remeasurement working paper in 2013 (see attachment).

(15%)

Working Paper

Accounts IDR Rate JPY

Cash 390,000,000 110 3,545,455

Account Receivable 534,000,000 110 4,854,545

Inventory 1,320,000,000 110 12,000,000

Plant & Equipment 2,520,000,000 110 22,909,091

COGS 621,000,000 112 5,544,643

Operating Expenses 195,750,000 112 1,747,768

Depreciation Expense 51,300,000 112 458,036

Income tax exp 40,500,000 112 361,607

Dividend 52,000,000 113 460,177

Total 5,724,550,000 51,881,321

Account Payable 516,000,000 110 4,690,909

AKL UAS 2014

spa-feui.com

*Retained Earning

IDR Rate JPY

R/E Jan 2,2012 1,640,000,000 111 14,774,775

Net Income 2012 106,050,000 115 922,174

Dividend, Sept 15, 2012 -50,000,000 114 -438,596

R/E Dec 31,2012 1,696,050,000 15,258,352

3. Prepare the investment journal entries for PT Parent in 2013 assuming the translation

adjustment at the end of 2012 is amount to JPY 100.000 (Credit Balance). PT Parent use

the fully adjusted equity method. (5%)

1. Investment in PT Sons 603.281*

Income from PT Sons 608.281

*608.281,25 = 65% x Net Income

608.281,25 = 65% x 928,125

Net Income = Sales – COGS – Operating Expense – Depreciation Expense – Income Tax

Expense

Net Income = 9,040,179 - 5,544,643 - 1,747,768 - 458,036 - 361,607

Net Income = 928,125

2. Cash 299,115*

Investment in PT Sons 299,115

*299,115 = 65% x Dividend

299,115 = 65% x 460,177

3. Investment in PT Sons 140,083*

Other Comprehensive Income – Translation Adjustment 140,083

Capital Stock 2,500,000,000 111 22,522,523

Retained Earning, Jan 1 1,696,050,000 15,258,352*

Sales 1,012,500,000 112 9,040,179

Acc.OCI –Translation Adjustment 369,359

Total 5,724,550,000 51,881,321

AKL UAS 2014

spa-feui.com

OCI 2012 100,000

Adjustment 140,083

OCI 2013 240,083 -> 65% x 369,359