Embed Size (px)

Citation preview

Module 6: Process Cost Systems

ACG 2071Created by M. Mari

Fall 2007-1

Process Cost Is the mass production of products in a continuous

flow of steps Products pass through a series of sequential

processes Each process is identified a separate production,

department, workstation, or work center. With the exception of the first process or

department, each receives the output from the prior department as a partially processed product.

Depending on the nature of the process, a company applies direct labor, overhead, and additional direct materials to move the product toward completion

Process Cost Accounting Assigns direct materials, direct labor, and

overhead to specific processes. Costs are allocated by department rather than

jobs Manufacturing costs are allocated to products

based on units of production Manufacturing costs are accumulated and

transferred by department The total costs associated with each process are

then divided by the number of units passing through that process to determine the cost per equivalent units for that process

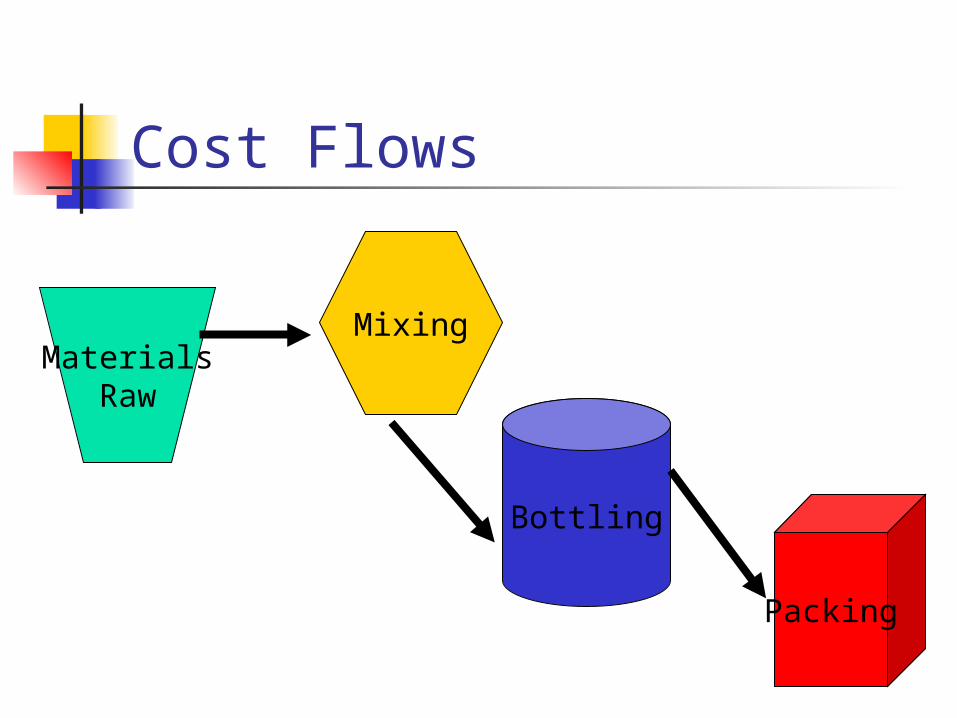

Cost Flows

MaterialsRaw

Mixing

Bottling

Packing

First –In, First Out Method Assume that the product moves in

order throughout the production process

Determine units to be assigned costs Units in beginning work in process Units started and completed during

period Units in ending work in process

FIFO Method Calculate Equivalent Units of

Production Process manufacturers often have

some partially processed materials remaining at the end of the period

EUP Number of units that could have been

completed within a given accounting period

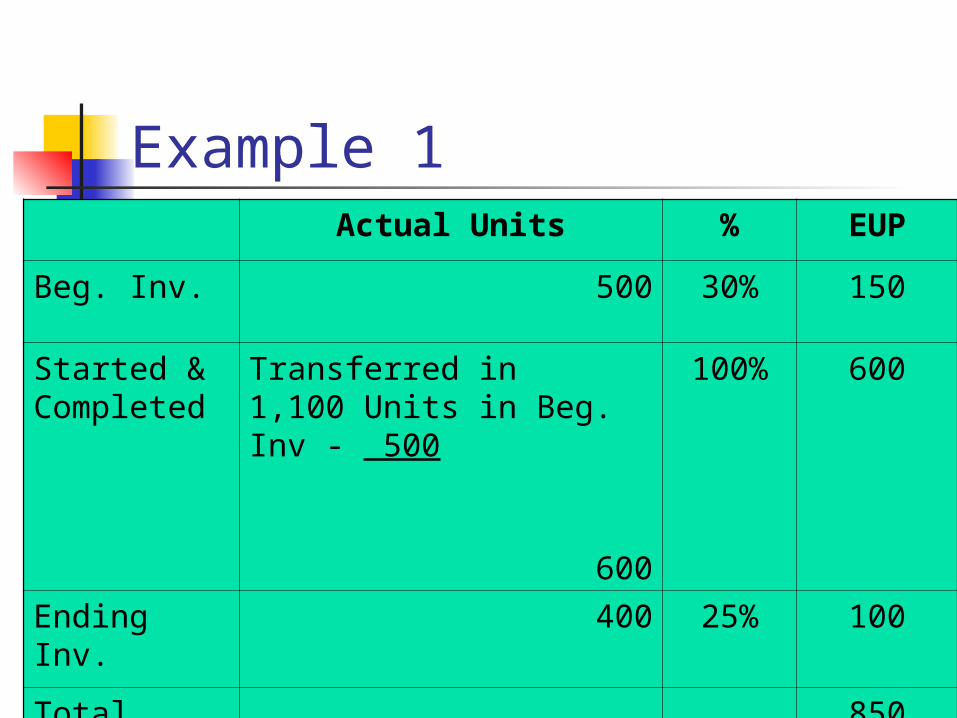

Example 1 A company processes their

production in two departments. Beginning inventory was 500 units that were 70% completed, 1,100 units transferred out to the next department and ending inventory consisted of 400 units 25% completed.

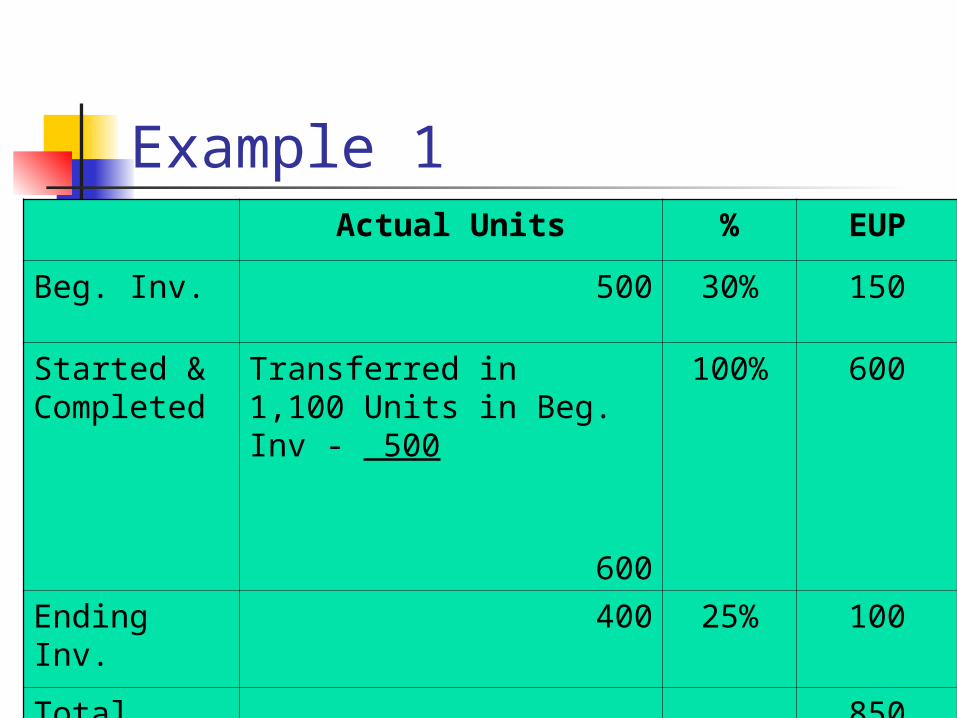

Example 1Actual Units % EUP

Beg. Inv. 500 30% 150

Started & Completed

Transferred in 1,100 Units in Beg. Inv - 500

600

100% 600

Ending Inv. 400 25% 100

Total 850

Example 3 A company process their

production in two departments. The beginning inventory was 4,000 units 50% completed, transferred into the department 5,000 units and an ending inventory of 2,000 units 40% completed.

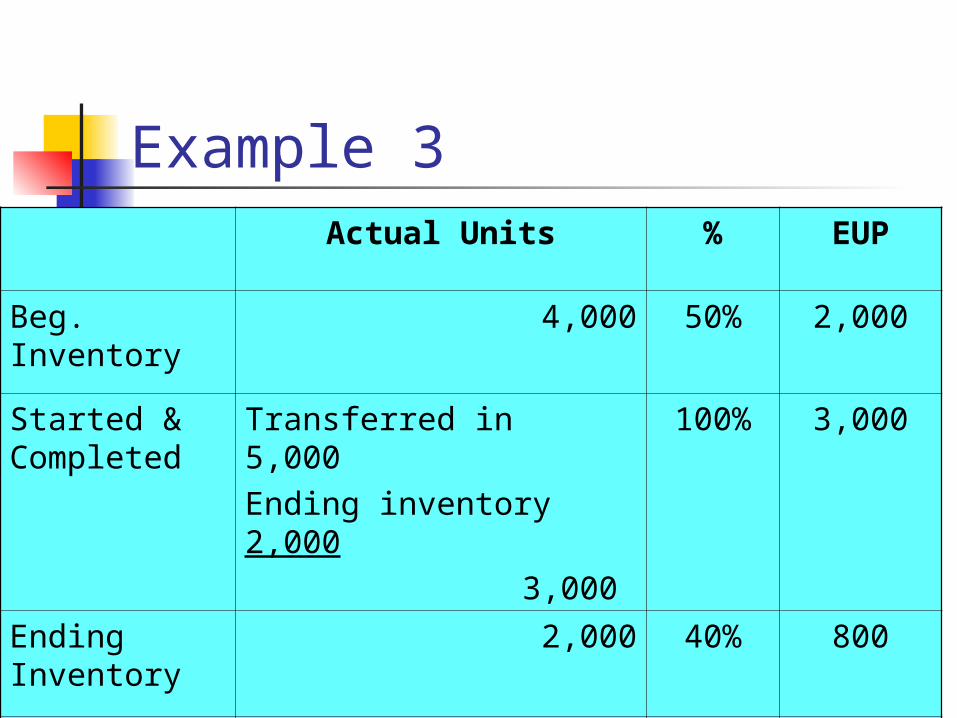

Example 3Actual Units % EUP

Beg. Inventory

4,000 50% 2,000

Started & Completed

Transferred in 5,000Ending inventory 2,000

3,000

100% 3,000

Ending Inventory

2,000 40% 800

Total 5,800

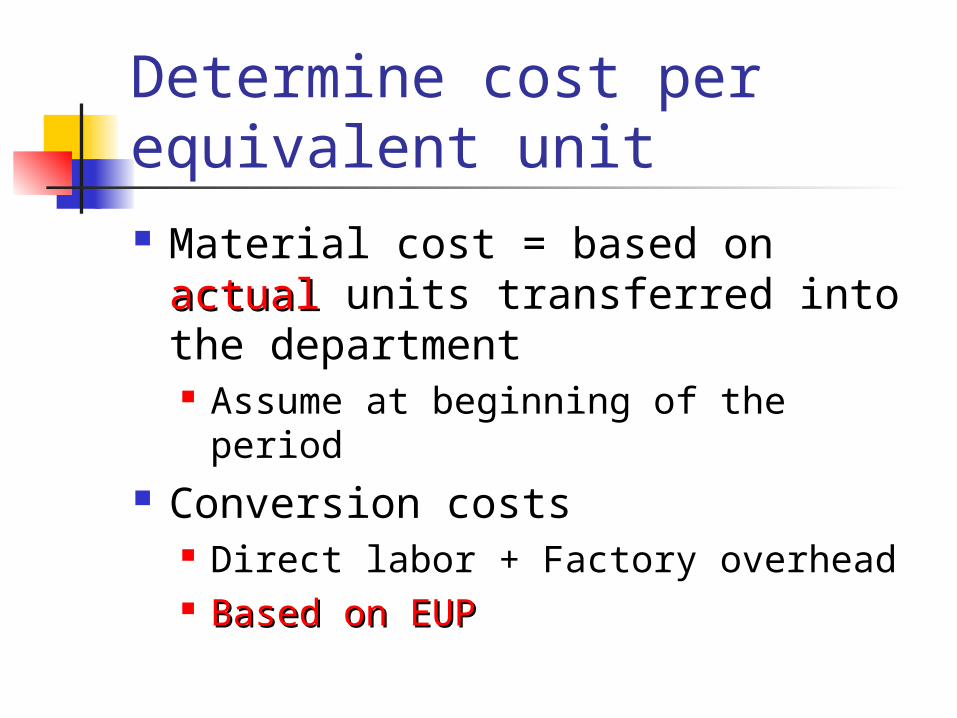

Determine cost per equivalent unit Material cost = based on actualactual

units transferred into the department Assume at beginning of the period

Conversion costs Direct labor + Factory overhead Based on EUPBased on EUP

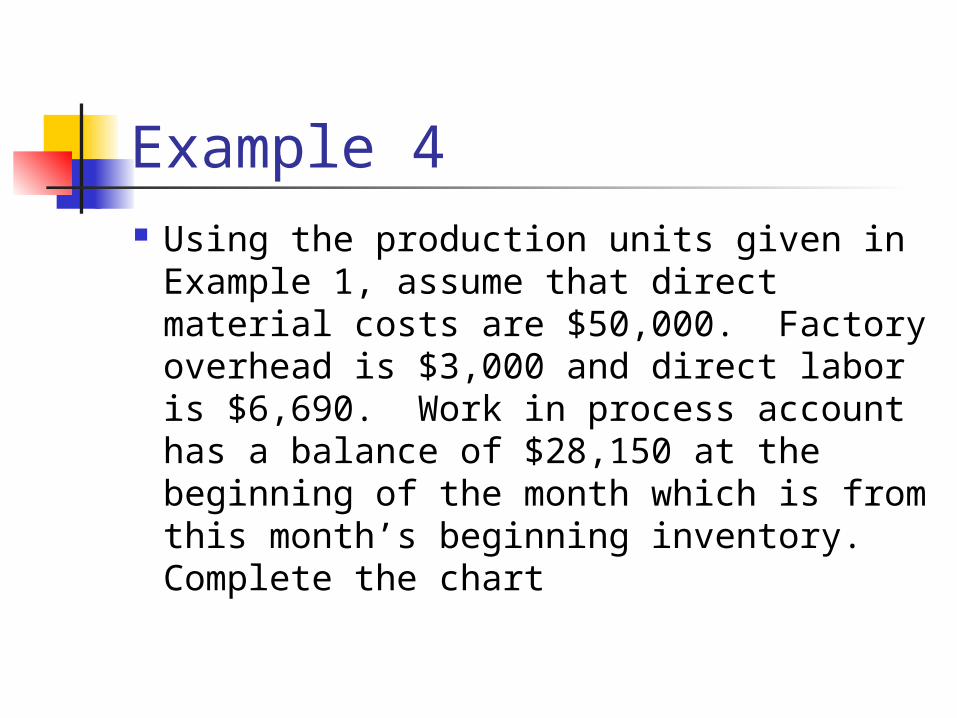

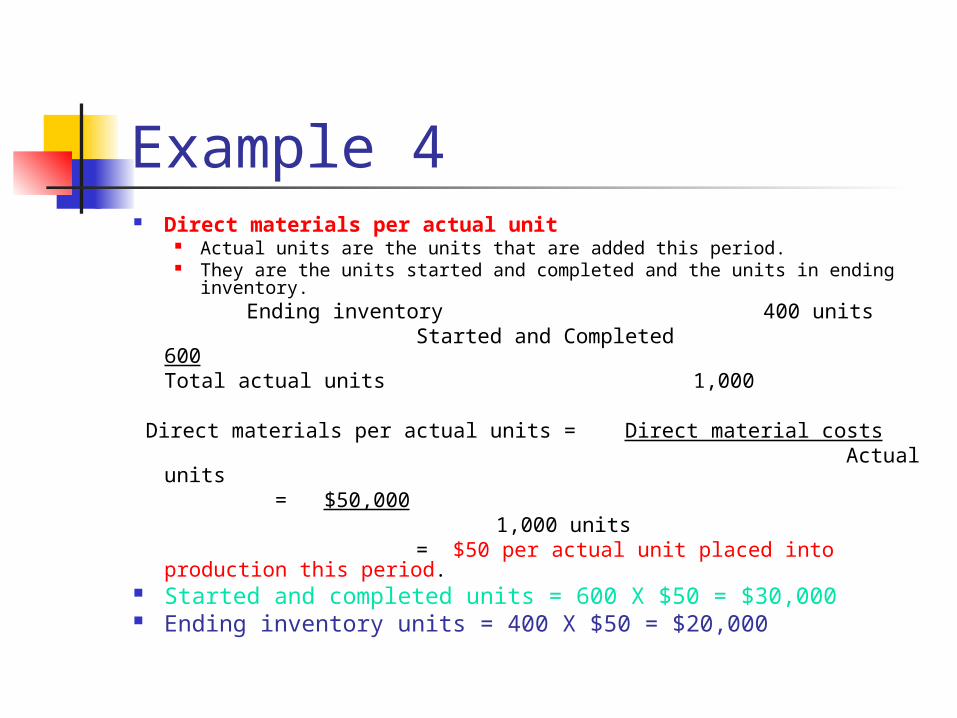

Example 4 Using the production units given in

Example 1, assume that direct material costs are $50,000. Factory overhead is $3,000 and direct labor is $6,690. Work in process account has a balance of $28,150 at the beginning of the month which is from this month’s beginning inventory. Complete the chart

Example 1Actual Units % EUP

Beg. Inv. 500 30% 150

Started & Completed

Transferred in 1,100 Units in Beg. Inv - 500

600

100% 600

Ending Inv. 400 25% 100

Total 850

Example 4 Direct materials per actual unit

Actual units are the units that are added this period. They are the units started and completed and the units in ending

inventory. Ending inventory 400 units Started and Completed 600

Total actual units 1,000 Direct materials per actual units = Direct material costs Actual units

= $50,000 1,000 units

= $50 per actual unit placed into production this period.

Started and completed units = 600 X $50 = $30,000 Ending inventory units = 400 X $50 = $20,000

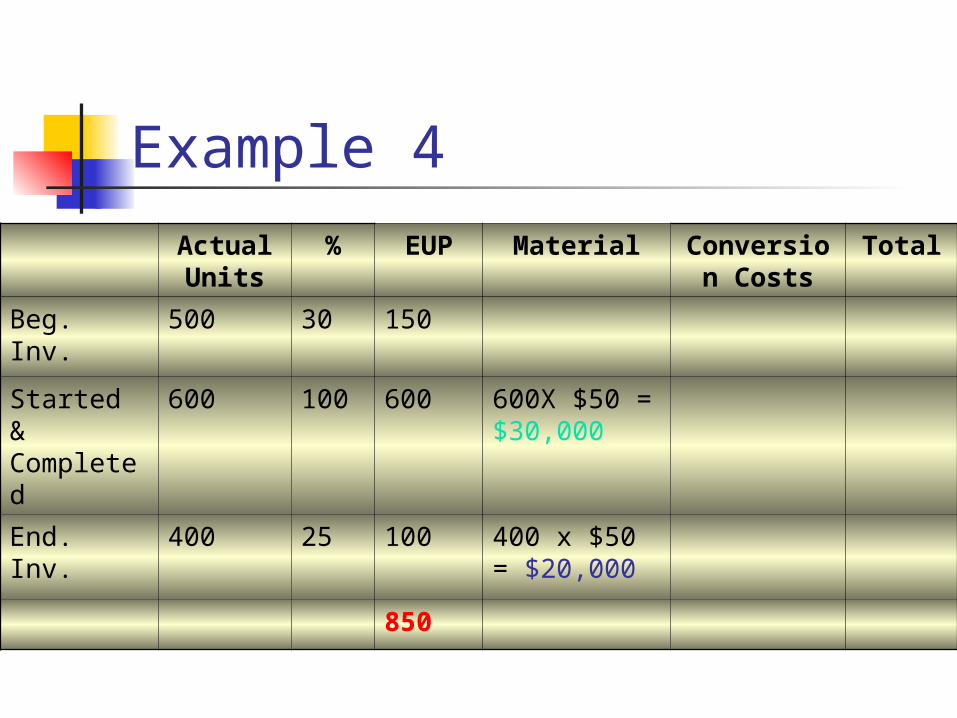

Example 4

Actual Units

% EUP Material Conversion Costs

Total

Beg. Inv. 500 30 150

Started & Completed

600 100 600 600X $50 = $30,000

End. Inv. 400 25 100 400 x $50 = $20,000

850

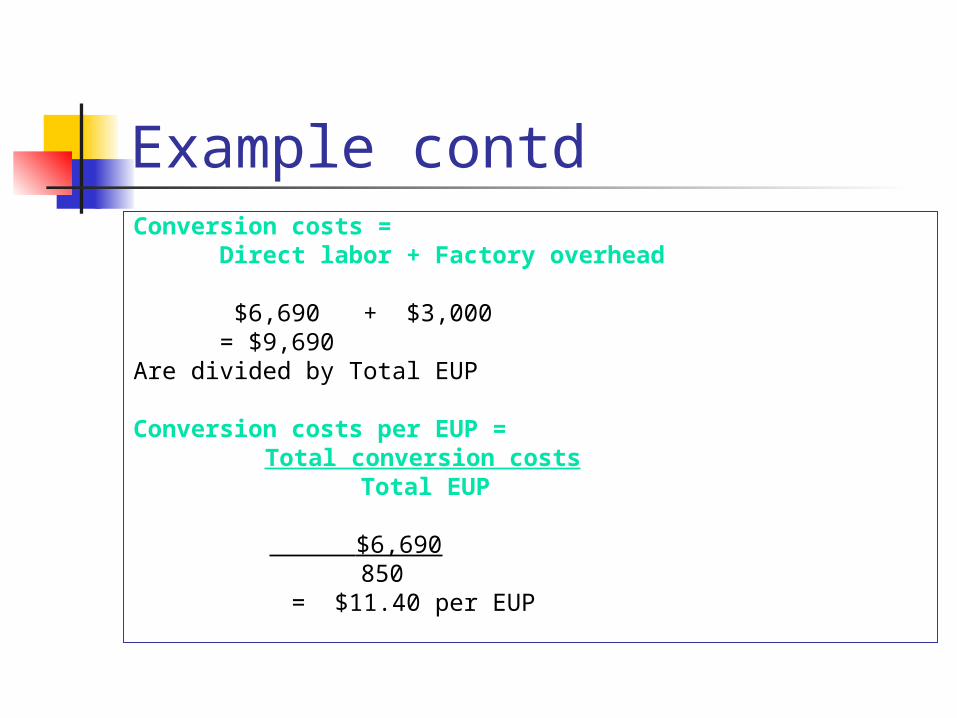

Example contdConversion costs = Direct labor + Factory overhead

$6,690 + $3,000 = $9,690Are divided by Total EUP

Conversion costs per EUP = Total conversion costs

Total EUP

$6,690850

= $11.40 per EUP

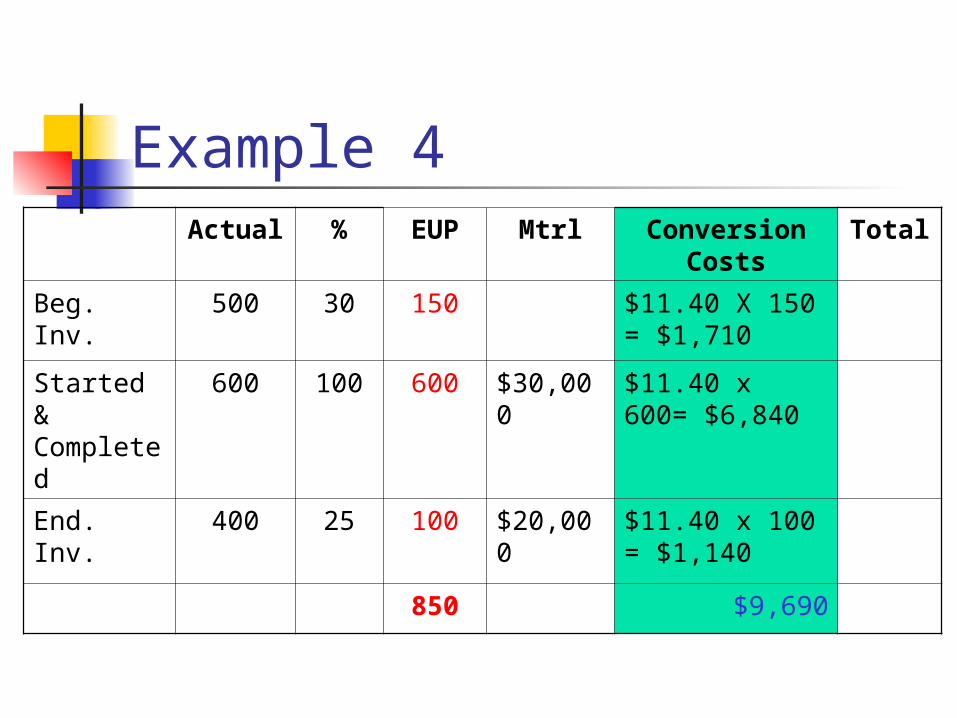

Example 4Actual % EUP Mtrl Conversion

CostsTotal

Beg. Inv. 500 30 150 $11.40 X 150 = $1,710

Started & Completed

600 100 600 $30,000

$11.40 x 600= $6,840

End. Inv. 400 25 100 $20,000

$11.40 x 100 = $1,140

850 $9,690

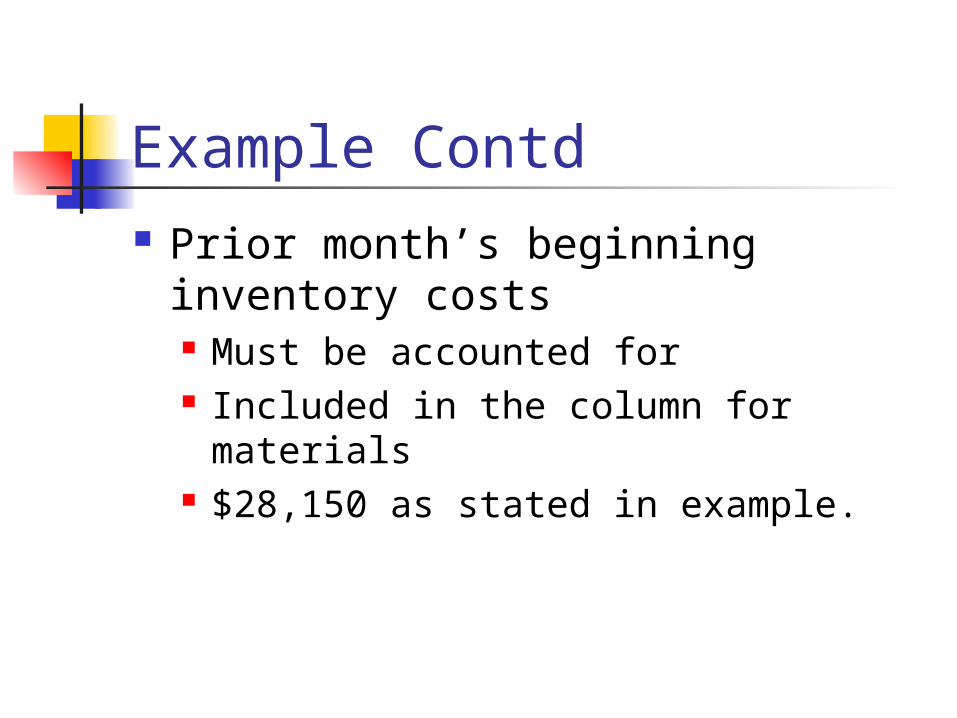

Example Contd Prior month’s beginning inventory

costs Must be accounted for Included in the column for materials $28,150 as stated in example.

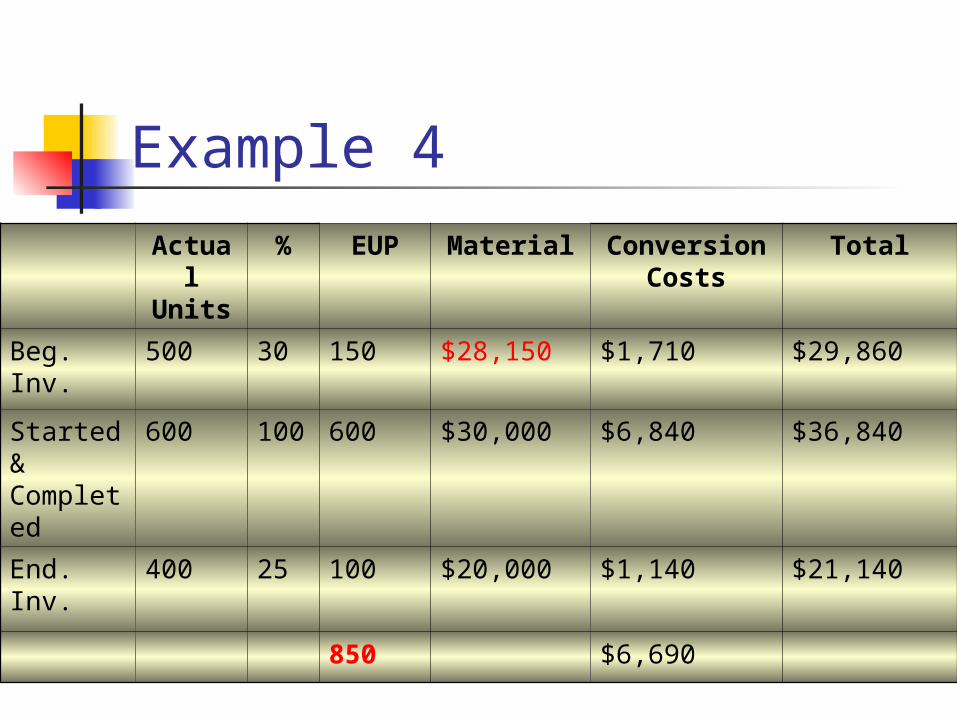

Example 4

Actual

Units

% EUP Material Conversion Costs

Total

Beg. Inv.

500 30 150 $28,150 $1,710 $29,860

Started & Completed

600 100 600 $30,000 $6,840 $36,840

End. Inv. 400 25 100 $20,000 $1,140 $21,140

850 $6,690

Questions What is the total cost of units

completed this period? How many actual units are in

ending inventory this period? How many actual units are in next

month’s beginning inventory?

Questions What is conversion costs per unit? What is the amount of work done

on this month’s beginning inventory?

What is the amount of work to be done next month on beginning inventory?

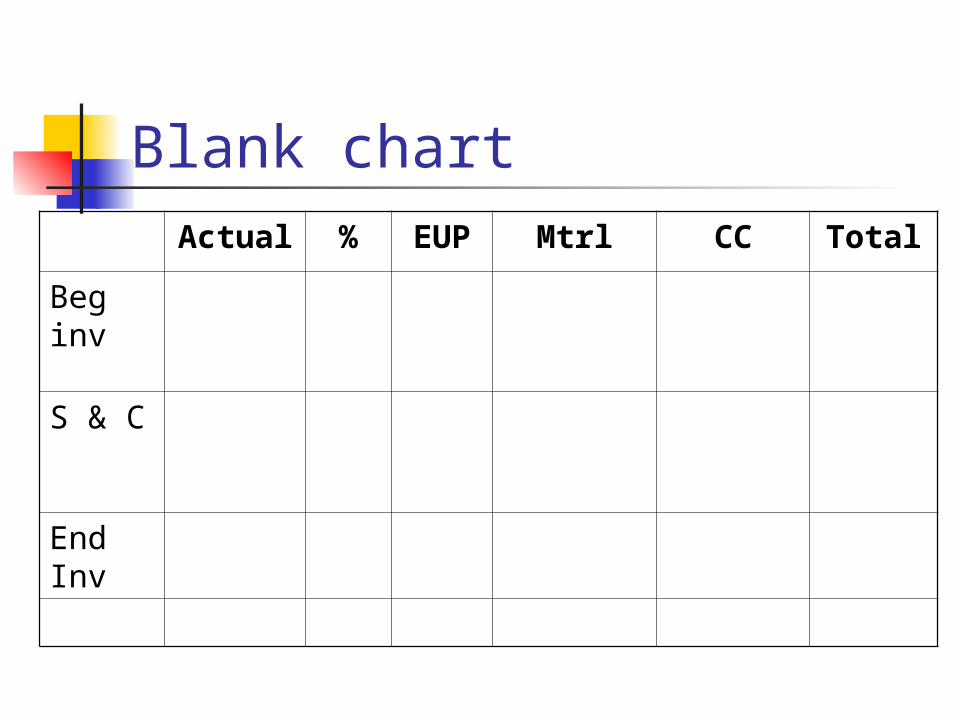

Blank chartActual % EUP Mtrl CC Total

Beg inv

S & C

End Inv