Embed Size (px)

Citation preview

Module 2Accounting for Revenues and Expenses: Constructing the Income Statement and Statement of Stockholders’ Equity

PARt 4L e a r n i n g O b j e c t i v e s4. Explain revenue recognition, accrual accounting, and their effects on retained earnings. (p. 14)

5. Illustrate equity transactions and the statement of stockholders’ equity. (p. 19)

Accrual Accounting for Revenues and ExpensesThe income statement’s ability to measure a company’s periodic performance depends on the proper timing of revenues and expenses. Revenue should be recorded when it is earned, even if not yet received in cash. This is called revenue recognition. Similarly, expenses are recorded by matching them with revenues when incurred, even if not yet paid in cash, as assets are used or obligations cre-ated. Accrual accounting refers to this practice of recognizing revenues when earned and matching expenses when incurred.

An important consequence of accrual accounting for revenues and expenses is that the balance sheet depicts the resources of the company (besides cash) and the obligations which the company must fulfill in the future. Accrual accounting is required under U.S. GAAP and IFRS because it is considered to be the most useful information for making business decisions and evaluating busi-ness performance. (That is not to say that information on cash flows is not important—but it is conveyed by the statement of cash flows.)

Walgreens’ net sales in 2011 were $72,184 million. Cost of goods sold (cost of sales) is an ex-pense item in the income statements of manufacturing and merchandising companies. It represents the cost of products that are delivered to customers during the period. The difference between revenues (at selling prices) and cost of goods sold (at purchase price or manufacturing cost) is called gross profit. Gross profit for merchandisers and manufacturers is an important number as it represents the remain-ing income available to cover all of the company’s overhead and other expenses (selling, general and administrative expenses, interest, and so on). Walgreens’ gross profit in 2011 is calculated as total net revenues less cost of sales, which equals $20,492 million ($72,184 million 2 $51,692 million).

The principles of revenue and expense recognition are crucial to income statement reporting. To illustrate, assume a company purchases inventories for $100,000 cash, which it sells later in that same period for $150,000 cash. The company would record $150,000 in revenue when the inventory is delivered to the customer, because at that point, we say that it has been earned. Also assume that the company pays $20,000 cash for sales employee wages during the period. The income statement is designed to tell how effective the company was at generating more resources than it used, and it would appear as follows:

LO4 Explain revenue recognition, accrual accounting, and their effects on retained earnings.

Copyright 2014 Cambridge Business Publishers 14

02_FABC_ch02.indd 14 6/9/15 2:53 PM

Revenues . . . . . . . . . . . . . . $150,000Cost of goods sold . . . . . . 100,000

Gross profit . . . . . . . . . . . . 50,000Wages expense . . . . . . . . . 20,000

Net income (earnings) . . . . $ 30,000

In this illustration, there is a correspondence between each of the revenues/expenses and a cash inflow/outflow. Net income was $30,000 and the increase in cash was $30,000.

However, that need not be the case under accrual accounting. Suppose that the company sells its product on credit (also denoted as on account) rather than for cash. Does the seller still report sales revenue? The answer is yes. Under GAAP, revenues are reported when a company has earned those sales. Earned means that the company has done everything required under the sales agreement—no major contingencies remain—and cash is realized or realizable. The seller reports an accounts re-ceivable asset on its balance sheet, and revenue can be recognized without cash collection.

Credit sales mean that companies can report substantial sales revenue and assets without receiving cash. When such receivables are ultimately collected, no further revenue is recorded because it was recorded earlier when the revenue recognition criteria were met. The collection of a receivable merely involves the decrease of one asset (accounts receivable) and the increase of another asset (cash), with no resulting increase in net assets.

Next consider a different situation. Assume that the company sells gift cards to customers for $9,500. Should the $9,500 received in cash be recognized as revenue? No. Even though the gift cards were sold and cash was collected, the revenue has not been earned. The revenue from gift cards is recognized when the product or service is provided. For example, revenue can be recog-nized when a customer purchases an item of merchandise using the gift card for payment. Hence, the $9,500 is then recorded as an increase in cash and an increase in unearned revenue, a liability, with no resulting increase in net assets.

The proper timing of revenue recognition suggests that the expenses incurred in earning that revenue be recognized in the same fiscal period. Thus, if merchandise inventory is purchased in one period and sold in another, the cost of the merchandise should be retained in the accounting records until the items are sold. It would not be proper to recognize expense when the inventory was purchased or the cash was paid. Accurate income determination requires the proper timing of revenue and expense recognition, and the exchange of cash is not the essential ingredient.

We have already seen that when a company incurs a cost to acquire a resource that produces ben-efits in the future (for example, merchandise inventory for future sale), it recognizes an asset. That asset represents costs that are waiting to be recognized as expenses in the future, based on the match-ing principle. When inventory is delivered to a customer, we recognize that the asset no longer be-longs to the selling company. The inventory asset is decreased, and cost of goods sold is recognized.

The same principle applies when employees earn wages for work in one period, but are paid in the next period. Wages expense must be recognized when the cost is incurred, regardless of when they are paid. If the company in the illustration doesn’t pay its employees until the following reporting period, it recognizes a wages payable liability of $20,000 and, because this decreases net assets, it would recognize a wage expense of the same amount.

When wages are paid in the next reporting period, both cash and the wages payable liability are decreased. No expense is reported when the wages are paid, because the expense is recognized when the employees worked to generate sales in the prior period.

Accrual accounting principles are crucial for reporting the income statement revenues and expenses in the proper period, and these revenues and expenses provide a more complete view of the inflows and outflows of cash for the firm. Was an outflow of cash supposed to produce benefits in the current period or in a future period? Was an inflow of cash the result of past operations or current operations? The accrual accounting model uses the balance sheet and income statement to answer such questions and to enable users of financial statements to make more timely assess-ments of the firm’s economic performance.

However, accrual accounting’s timeliness requires management to estimate future events in determining the amount of expenses incurred and revenue earned. The precise amount of cash to

FYI Purchase of inventories on credit or on account means that the buyer does not pay the seller at the time of purchase . The buyer reports a liability (accounts payable) on its balance sheet that is later removed when payment is made . The seller reports an asset (accounts receivable) on its balance sheet until it is removed when the buyer pays .

FYI Sales on credit will not always be collected . The potential for uncollectable accounts introduces additional risk to the firm .

FYI Cash accounting recognizes revenues only when received in cash and expenses only when paid in cash . This approach is not acceptable under GAAP .

Copyright 2014 Cambridge Business Publishers

Module 2: Part 4 | Accounting for Revenues and Expenses: Constructing the Income Statement and Statement of Stockholders’ Equity

15

02_FABC_ch02.indd 15 6/9/15 2:53 PM

be received or disbursed cannot be known until a later date. In the case of wages, the amount of the accrual is known with certainty. In other cases (e.g., incentive bonuses), it may not and thus require an estimate.

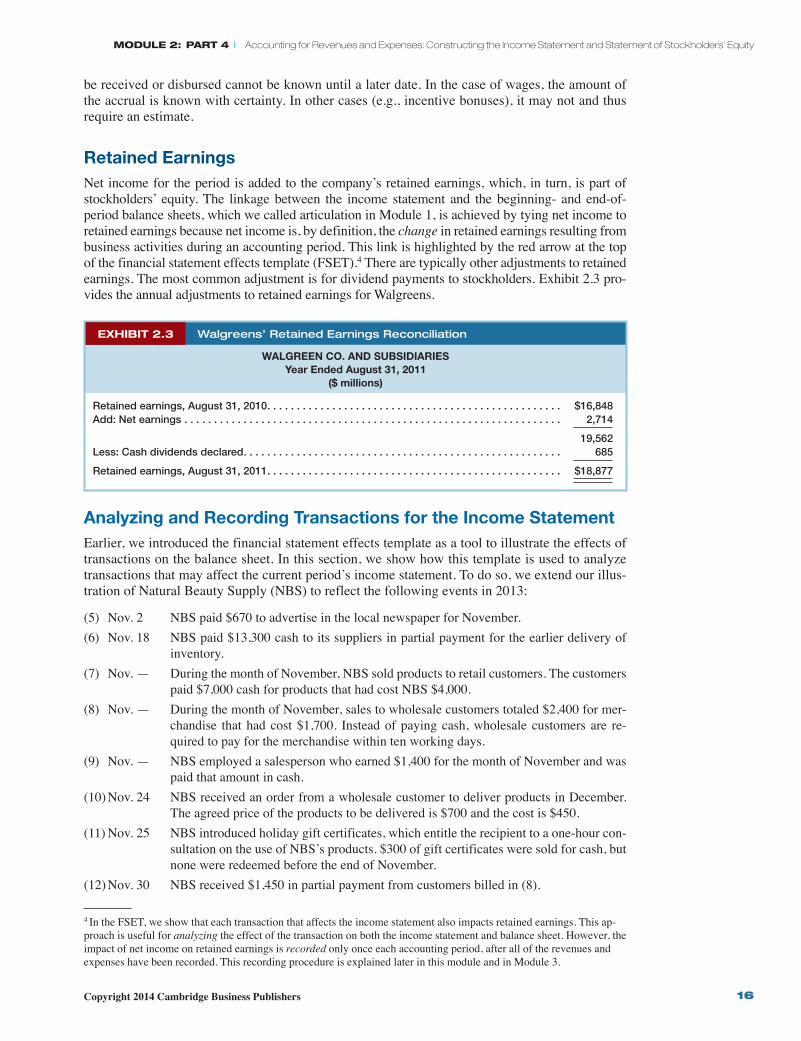

Retained EarningsNet income for the period is added to the company’s retained earnings, which, in turn, is part of stockholders’ equity. The linkage between the income statement and the beginning- and end-of-period balance sheets, which we called articulation in Module 1, is achieved by tying net income to retained earnings because net income is, by definition, the change in retained earnings resulting from business activities during an accounting period. This link is highlighted by the red arrow at the top of the financial statement effects template (FSET).4 There are typically other adjustments to retained earnings. The most common adjustment is for dividend payments to stockholders. Exhibit 2.3 pro-vides the annual adjustments to retained earnings for Walgreens.

EXHIBIT 2.3 Walgreens’ Retained Earnings Reconciliation

WAlgREEn Co. And SubSidiARiES Year Ended August 31, 2011

($ millions)

Retained earnings, August 31, 2010 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $16,848Add: Net earnings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,714

19,562Less: Cash dividends declared . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 685

Retained earnings, August 31, 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $18,877

Analyzing and Recording Transactions for the income StatementEarlier, we introduced the financial statement effects template as a tool to illustrate the effects of transactions on the balance sheet. In this section, we show how this template is used to analyze transactions that may affect the current period’s income statement. To do so, we extend our illus-tration of Natural Beauty Supply (NBS) to reflect the following events in 2013:

(5) Nov. 2 NBS paid $670 to advertise in the local newspaper for November.(6) Nov. 18 NBS paid $13,300 cash to its suppliers in partial payment for the earlier delivery of

inventory.(7) Nov. — During the month of November, NBS sold products to retail customers. The customers

paid $7,000 cash for products that had cost NBS $4,000.(8) Nov. — During the month of November, sales to wholesale customers totaled $2,400 for mer-

chandise that had cost $1,700. Instead of paying cash, wholesale customers are re-quired to pay for the merchandise within ten working days.

(9) Nov. — NBS employed a salesperson who earned $1,400 for the month of November and was paid that amount in cash.

(10) Nov. 24 NBS received an order from a wholesale customer to deliver products in December. The agreed price of the products to be delivered is $700 and the cost is $450.

(11) Nov. 25 NBS introduced holiday gift certificates, which entitle the recipient to a one-hour con-sultation on the use of NBS’s products. $300 of gift certificates were sold for cash, but none were redeemed before the end of November.

(12) Nov. 30 NBS received $1,450 in partial payment from customers billed in (8).

4 In the FSET, we show that each transaction that affects the income statement also impacts retained earnings. This ap-proach is useful for analyzing the effect of the transaction on both the income statement and balance sheet. However, the impact of net income on retained earnings is recorded only once each accounting period, after all of the revenues and expenses have been recorded. This recording procedure is explained later in this module and in Module 3.

Copyright 2014 Cambridge Business Publishers

Module 2: Part 4 | Accounting for Revenues and Expenses: Constructing the Income Statement and Statement of Stockholders’ Equity

16

02_FABC_ch02.indd 16 6/9/15 2:53 PM

(13) Nov. 30 NBS repaid the loan and interest in (2).(14) Nov. 30 NBS paid $1,680 for a twelve-month fire insurance policy. Coverage begins on De-

cember 1.(15) Nov. 30 NBS paid $1,500 to the landlord for November rent.

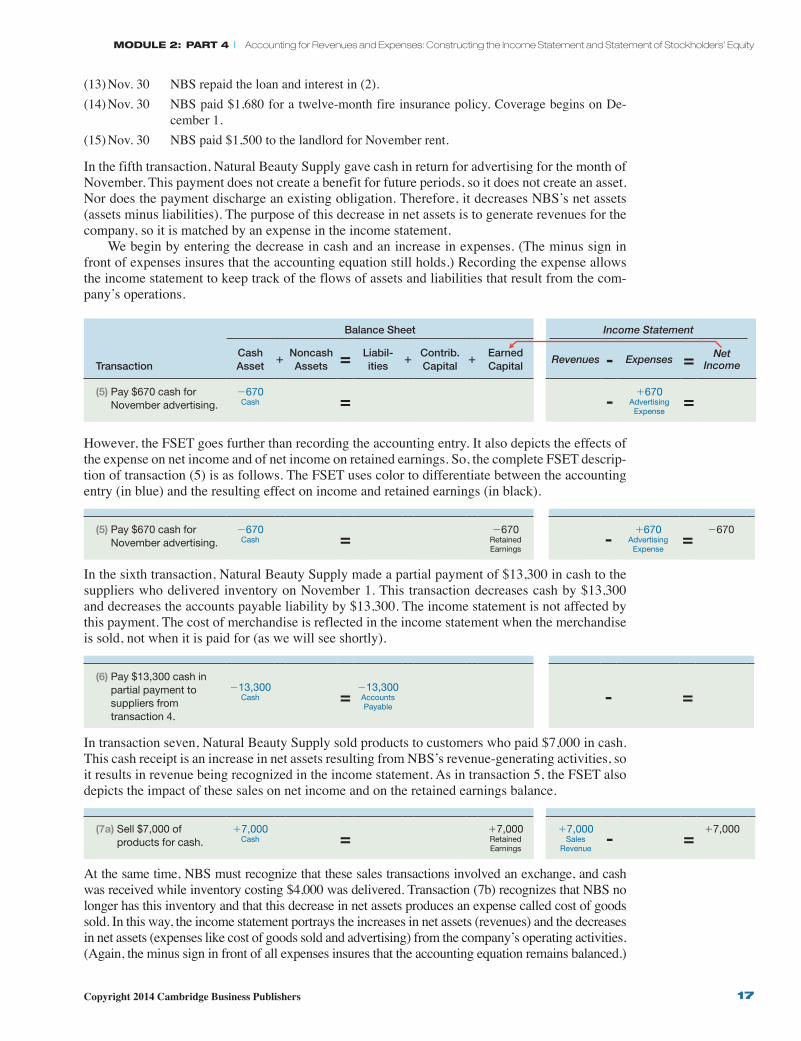

In the fifth transaction, Natural Beauty Supply gave cash in return for advertising for the month of November. This payment does not create a benefit for future periods, so it does not create an asset. Nor does the payment discharge an existing obligation. Therefore, it decreases NBS’s net assets (assets minus liabilities). The purpose of this decrease in net assets is to generate revenues for the company, so it is matched by an expense in the income statement.

We begin by entering the decrease in cash and an increase in expenses. (The minus sign in front of expenses insures that the accounting equation still holds.) Recording the expense allows the income statement to keep track of the flows of assets and liabilities that result from the com-pany’s operations.

Transaction

Balance Sheet Income Statement

Cash Asset

1Noncash Assets = Liabil-

ities1

Contrib . Capital

1Earned Capital

Revenues - Expenses = Net Income

(5) Pay $670 cash for November advertising.

2670Cash = -

1670Advertising

Expense=

However, the FSET goes further than recording the accounting entry. It also depicts the effects of the expense on net income and of net income on retained earnings. So, the complete FSET descrip-tion of transaction (5) is as follows. The FSET uses color to differentiate between the accounting entry (in blue) and the resulting effect on income and retained earnings (in black).

(5) Pay $670 cash for November advertising.

2670Cash =

2670Retained Earnings

-1670

Advertising Expense

=2670

In the sixth transaction, Natural Beauty Supply made a partial payment of $13,300 in cash to the suppliers who delivered inventory on November 1. This transaction decreases cash by $13,300 and decreases the accounts payable liability by $13,300. The income statement is not affected by this payment. The cost of merchandise is reflected in the income statement when the merchandise is sold, not when it is paid for (as we will see shortly).

(6) Pay $13,300 cash in partial payment to suppliers from transaction 4.

213,300Cash =

213,300Accounts Payable

- =

In transaction seven, Natural Beauty Supply sold products to customers who paid $7,000 in cash. This cash receipt is an increase in net assets resulting from NBS’s revenue-generating activities, so it results in revenue being recognized in the income statement. As in transaction 5, the FSET also depicts the impact of these sales on net income and on the retained earnings balance.

(7a) Sell $7,000 of products for cash.

17,000Cash =

17,000Retained Earnings

17,000Sales

Revenue- =

17,000

At the same time, NBS must recognize that these sales transactions involved an exchange, and cash was received while inventory costing $4,000 was delivered. Transaction (7b) recognizes that NBS no longer has this inventory and that this decrease in net assets produces an expense called cost of goods sold. In this way, the income statement portrays the increases in net assets (revenues) and the decreases in net assets (expenses like cost of goods sold and advertising) from the company’s operating activities. (Again, the minus sign in front of all expenses insures that the accounting equation remains balanced.)

Copyright 2014 Cambridge Business Publishers

Module 2: Part 4 | Accounting for Revenues and Expenses: Constructing the Income Statement and Statement of Stockholders’ Equity

17

02_FABC_ch02.indd 17 6/9/15 2:53 PM

Transaction

Balance Sheet Income Statement

Cash Asset

1Noncash Assets = Liabil-

ities1

Contrib . Capital

1Earned Capital

Revenues - Expenses = Net Income

(7b) Record $4,000 for the cost of merchandise sold in transaction 7a.

24,000Inventory =

24,000Retained Earnings

-14,000

Cost of Goods Sold

=24,000

The eighth transaction is very similar to the previous one, except that Natural Beauty Supply’s customers will pay for the products ten days after they were delivered. Should NBS recognize revenue on these sales? The products have been delivered, so the revenue has been earned.5 There-fore, NBS should recognize that it has a new asset—accounts receivable—equal to $2,400, and that it has earned revenue in the same amount. As above, NBS would also record cost of goods sold to recognize the cost of inventory delivered to the customers.

(8a) Sell $2,400 of products on account.

12,400Accounts

Receivable=

12,400Retained Earnings

12,400Sales

Revenue- = 12,400

(8b) Record $1,700 for the cost of merchandise sold in transaction 8a.

21,700Inventory =

21,700Retained Earnings

-11,700

Cost of Goods Sold

= 21,700

The ninth entry records wage expense. In this case, wages were paid in cash. Cash is decreased by $1,400, and this decrease in net assets results in a recognition of wages expense in the income statement (with resulting decreases in net income and retained earnings).

(9) Record $1,400 in wages to employees.

21,400Cash =

21,400Retained Earnings

-11,400

Wages Expense

=21,400

Transaction ten involves a customer order for products to be delivered in December. This transac-tion is an example of an executory contract, which does not require a journal entry. NBS has not earned revenue, because it has not yet delivered the products.

(10) Receive customer order. Memorandum entry for customer order

In transaction eleven, Natural Beauty Supply sold gift certificates for $300 cash, but none were re-deemed. In this case, NBS has received cash, but revenue cannot be recognized because it has not yet been earned. Rather, NBS has accepted an obligation to provide services in the future when the gift certificates are redeemed. This obligation is recognized as a liability titled unearned revenue.

(11) Sell gift certificates for $300 cash.

1300Cash =

1300Unearned Revenue

- =

In transaction twelve, NBS received $1,450 cash as partial payment from customers billed in transaction eight. Cash increases by $1,450 and accounts receivable decreases by $1,450. Recall that revenues are recorded when earned (transaction 8), not when cash is received.

(12) Receive $1,450 cash as partial payment from customers billed in transaction 8.

11,450Cash

21,450Accounts

Receivable= - =

5 For the time being, we assume that the receivables’ collectability is assured.

Copyright 2014 Cambridge Business Publishers

Module 2: Part 4 | Accounting for Revenues and Expenses: Constructing the Income Statement and Statement of Stockholders’ Equity

18

02_FABC_ch02.indd 18 6/9/15 2:53 PM

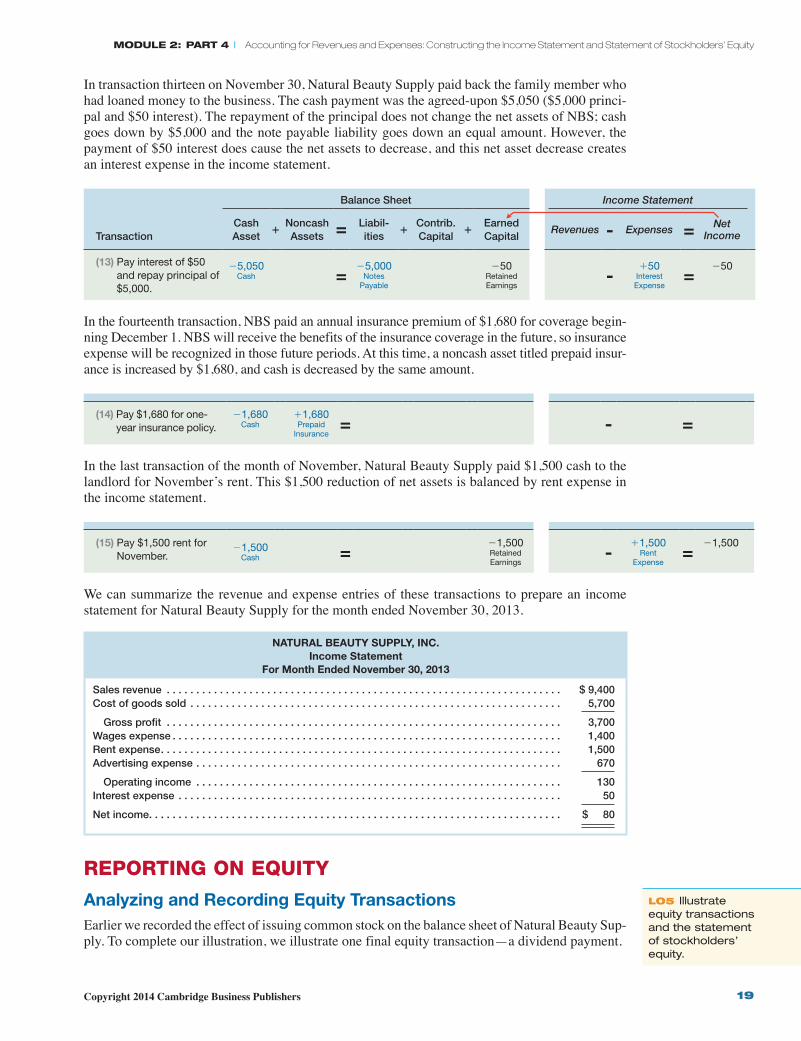

In transaction thirteen on November 30, Natural Beauty Supply paid back the family member who had loaned money to the business. The cash payment was the agreed-upon $5,050 ($5,000 princi-pal and $50 interest). The repayment of the principal does not change the net assets of NBS; cash goes down by $5,000 and the note payable liability goes down an equal amount. However, the payment of $50 interest does cause the net assets to decrease, and this net asset decrease creates an interest expense in the income statement.

Transaction

Balance Sheet Income Statement

Cash Asset

1Noncash Assets = Liabil-

ities1

Contrib . Capital

1Earned Capital

Revenues - Expenses = Net Income

(13) Pay interest of $50 and repay principal of $5,000.

25,050Cash =

25,000Notes

Payable

250Retained Earnings

-150

Interest Expense

=250

In the fourteenth transaction, NBS paid an annual insurance premium of $1,680 for coverage begin-ning December 1. NBS will receive the benefits of the insurance coverage in the future, so insurance expense will be recognized in those future periods. At this time, a noncash asset titled prepaid insur-ance is increased by $1,680, and cash is decreased by the same amount.

(14) Pay $1,680 for one-year insurance policy.

21,680Cash

11,680Prepaid

Insurance= - =

In the last transaction of the month of November, Natural Beauty Supply paid $1,500 cash to the landlord for November’s rent. This $1,500 reduction of net assets is balanced by rent expense in the income statement.

(15) Pay $1,500 rent for November.

21,500Cash =

21,500Retained Earnings

-11,500

Rent Expense

=21,500

We can summarize the revenue and expense entries of these transactions to prepare an income statement for Natural Beauty Supply for the month ended November 30, 2013.

nATuRAl bEAuTY SuPPlY, inC. income Statement

For Month Ended november 30, 2013

Sales revenue . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 9,400Cost of goods sold . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5,700

Gross profit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,700Wages expense . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,400Rent expense . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,500Advertising expense . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 670

Operating income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 130Interest expense . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

Net income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 80

repOrting On equity

Analyzing and Recording Equity TransactionsEarlier we recorded the effect of issuing common stock on the balance sheet of Natural Beauty Sup-ply. To complete our illustration, we illustrate one final equity transaction—a dividend payment.

LO5 Illustrate equity transactions and the statement of stockholders’ equity.

Copyright 2014 Cambridge Business Publishers

Module 2: Part 4 | Accounting for Revenues and Expenses: Constructing the Income Statement and Statement of Stockholders’ Equity

19

02_FABC_ch02.indd 19 6/9/15 2:53 PM

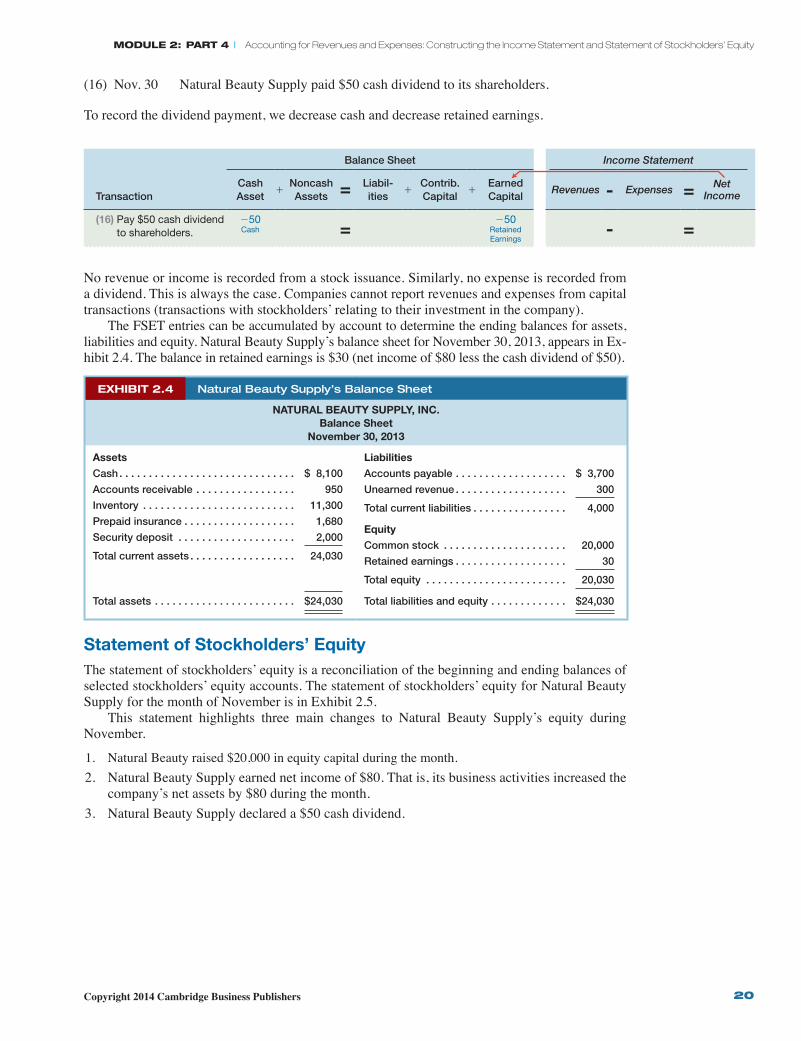

(16) Nov. 30 Natural Beauty Supply paid $50 cash dividend to its shareholders.

To record the dividend payment, we decrease cash and decrease retained earnings.

Transaction

Balance Sheet Income Statement

Cash Asset

1Noncash Assets = Liabil-

ities1

Contrib . Capital

1Earned Capital

Revenues - Expenses = Net Income

(16) Pay $50 cash dividend to shareholders.

250Cash =

250Retained Earnings

- =

No revenue or income is recorded from a stock issuance. Similarly, no expense is recorded from a dividend. This is always the case. Companies cannot report revenues and expenses from capital transactions (transactions with stockholders’ relating to their investment in the company).

The FSET entries can be accumulated by account to determine the ending balances for assets, liabilities and equity. Natural Beauty Supply’s balance sheet for November 30, 2013, appears in Ex-hibit 2.4. The balance in retained earnings is $30 (net income of $80 less the cash dividend of $50).

EXHIBIT 2.4 Natural Beauty Supply’s Balance Sheet

nATuRAl bEAuTY SuPPlY, inC. balance Sheet

november 30, 2013

Assets

Cash . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 8,100

Accounts receivable . . . . . . . . . . . . . . . . . 950

Inventory . . . . . . . . . . . . . . . . . . . . . . . . . . 11,300

Prepaid insurance . . . . . . . . . . . . . . . . . . . 1,680

Security deposit . . . . . . . . . . . . . . . . . . . . 2,000 Total current assets . . . . . . . . . . . . . . . . . . 24,030

Total assets . . . . . . . . . . . . . . . . . . . . . . . . $24,030

liabilities

Accounts payable . . . . . . . . . . . . . . . . . . . $ 3,700

Unearned revenue . . . . . . . . . . . . . . . . . . . 300 Total current liabilities . . . . . . . . . . . . . . . . 4,000

Equity

Common stock . . . . . . . . . . . . . . . . . . . . . 20,000

Retained earnings . . . . . . . . . . . . . . . . . . . 30 Total equity . . . . . . . . . . . . . . . . . . . . . . . . 20,030

Total liabilities and equity . . . . . . . . . . . . . $24,030

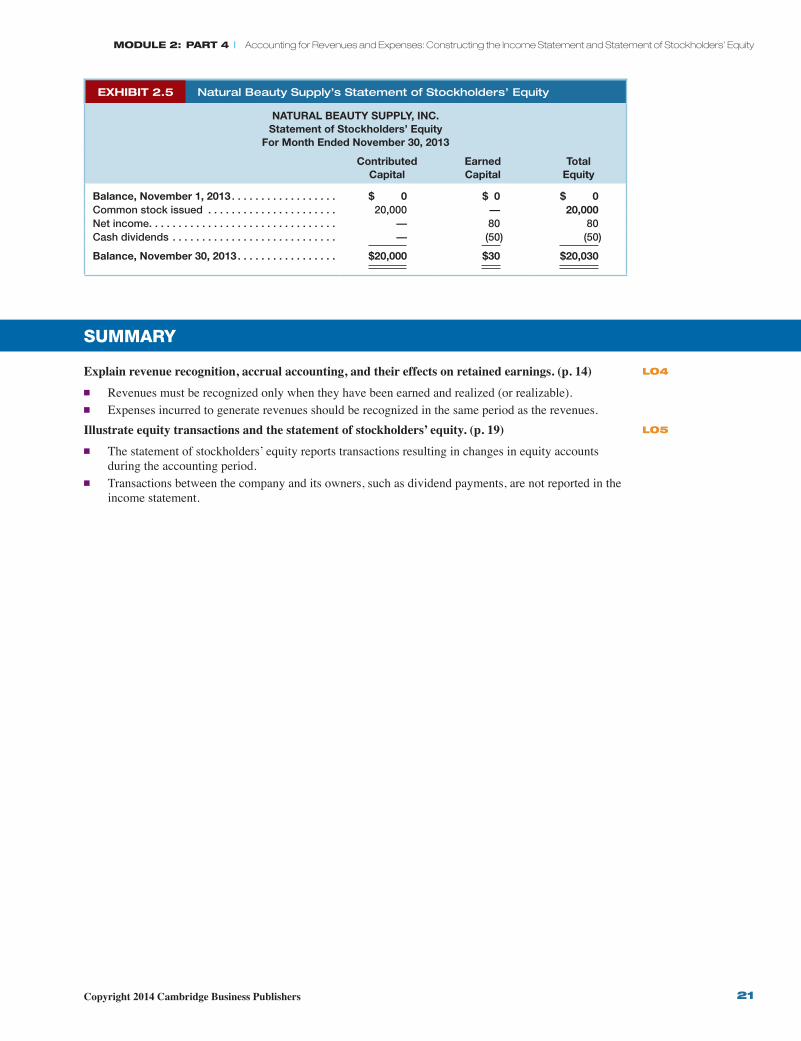

Statement of Stockholders’ EquityThe statement of stockholders’ equity is a reconciliation of the beginning and ending balances of selected stockholders’ equity accounts. The statement of stockholders’ equity for Natural Beauty Supply for the month of November is in Exhibit 2.5.

This statement highlights three main changes to Natural Beauty Supply’s equity during November.

1. Natural Beauty raised $20,000 in equity capital during the month. 2. Natural Beauty Supply earned net income of $80. That is, its business activities increased the

company’s net assets by $80 during the month. 3. Natural Beauty Supply declared a $50 cash dividend.

Copyright 2014 Cambridge Business Publishers

Module 2: Part 4 | Accounting for Revenues and Expenses: Constructing the Income Statement and Statement of Stockholders’ Equity

20

02_FABC_ch02.indd 20 6/9/15 2:53 PM

EXHIBIT 2.5 Natural Beauty Supply’s Statement of Stockholders’ Equity

nATuRAl bEAuTY SuPPlY, inC.Statement of Stockholders’ Equity

For Month Ended november 30, 2013

Contributed Capital

Earned Capital

Total Equity

balance, november 1, 2013 . . . . . . . . . . . . . . . . . . $ 0 $ 0 $ 0Common stock issued . . . . . . . . . . . . . . . . . . . . . . 20,000 — 20,000Net income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . — 80 80Cash dividends . . . . . . . . . . . . . . . . . . . . . . . . . . . . — (50) (50)

balance, november 30, 2013 . . . . . . . . . . . . . . . . . $20,000 $30 $20,030

summary

Explain revenue recognition, accrual accounting, and their effects on retained earnings. (p. 14)■ Revenues must be recognized only when they have been earned and realized (or realizable).■ Expenses incurred to generate revenues should be recognized in the same period as the revenues.Illustrate equity transactions and the statement of stockholders’ equity. (p. 19)■ The statement of stockholders’ equity reports transactions resulting in changes in equity accounts

during the accounting period.■ Transactions between the company and its owners, such as dividend payments, are not reported in the

income statement.

LO4

LO5

Copyright 2014 Cambridge Business Publishers

Module 2: Part 4 | Accounting for Revenues and Expenses: Constructing the Income Statement and Statement of Stockholders’ Equity

21

02_FABC_ch02.indd 21 6/9/15 2:53 PM

![[123] - Statement of Environmental Effects](https://img.pdfslide.us/doc/110x75/62842958781a8e2ed36d6d17/123-statement-of-environmental-effects.jpg)