Embed Size (px)

Citation preview

Module 15

Cost-Volume-Profit Analysis and Planning

Profitability Analysis

Involves examining the relationships among revenues, costs, and profits

Widely used in the economic evaluation of existing or proposed products or services

Performed before decisions are finalized • Selling prices

• Behavior of activity cost drivers

What you need to understand to

perform profitability analysis

What you need to understand to

perform profitability analysis

CVP Assumptions

1. All costs are classified as fixed or variable.

2. The total cost function is linear within the relevant range.

3. The total revenue function is linear within the relevant range.

4. The analysis is for a single product, or the sales mix of multiple products is constant.

5. There is only one activity cost driver: unit or dollar sales volume.

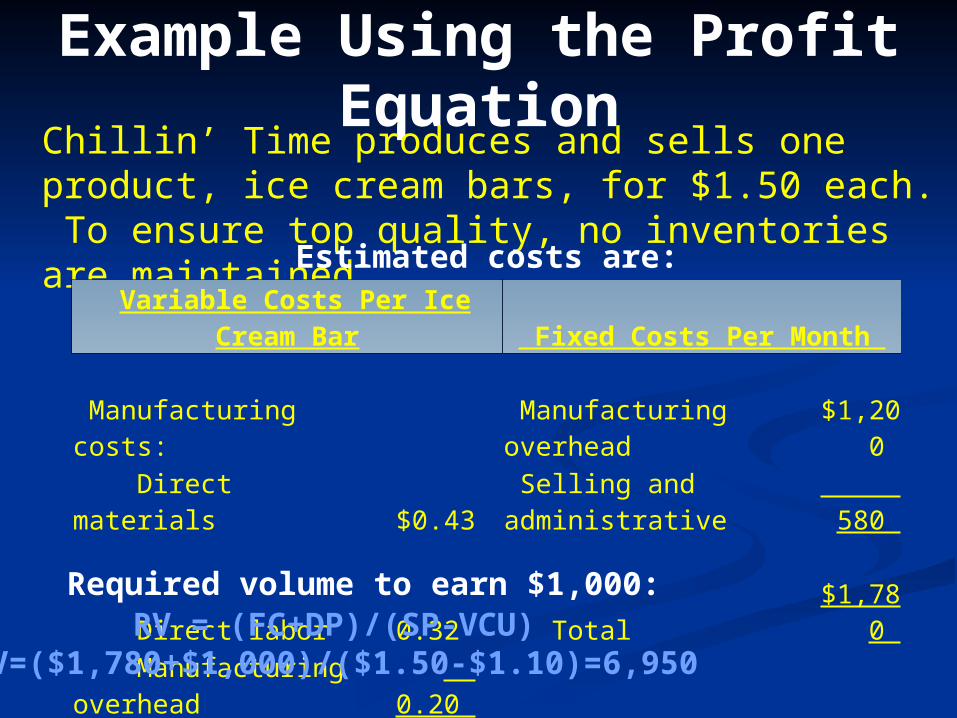

Example Using the Profit Equation

Chillin’ Time produces and sells one product, ice cream bars, for $1.50 each. To ensure top quality, no inventories are maintained.

Variable Costs Per Ice Cream Bar Fixed Costs Per Month Manufacturing costs: Manufacturing overhead $1,200 Direct materials $0.43 Selling and administrative 580 Direct labor 0.32 Total $1,780 Manufacturing overhead 0.20 $0.95 Selling and administrative 0.15 Total $1.10

RV = (FC+DP)/(SP-VCU)RV=($1,780+$1,000)/($1.50-$1.10)=6,950

Estimated costs are:

Required volume to earn $1,000:

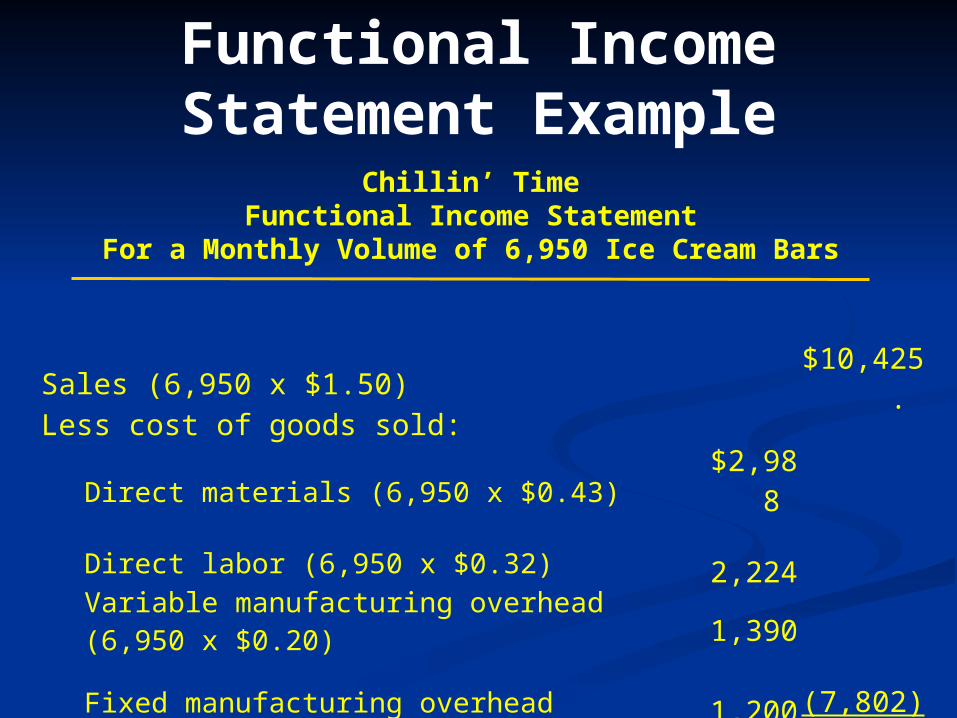

Functional Income Statement Example

Chillin’ TimeFunctional Income Statement

For a Monthly Volume of 6,950 Ice Cream Bars

Sales (6,950 x $1.50) $10,425. Less cost of goods sold:

Direct materials (6,950 x $0.43) $2,988 Direct labor (6,950 x $0.32) 2,224 Variable manufacturing overhead (6,950 x $0.20) 1,390 Fixed manufacturing overhead 1,200 (7,802)

Gross margin 2,623. Less other expenses:

Variable selling and administrative (6,950 x $0.15) 1,043 Fixed selling and administrative 580 (1,623)

Profit $ 1,000.

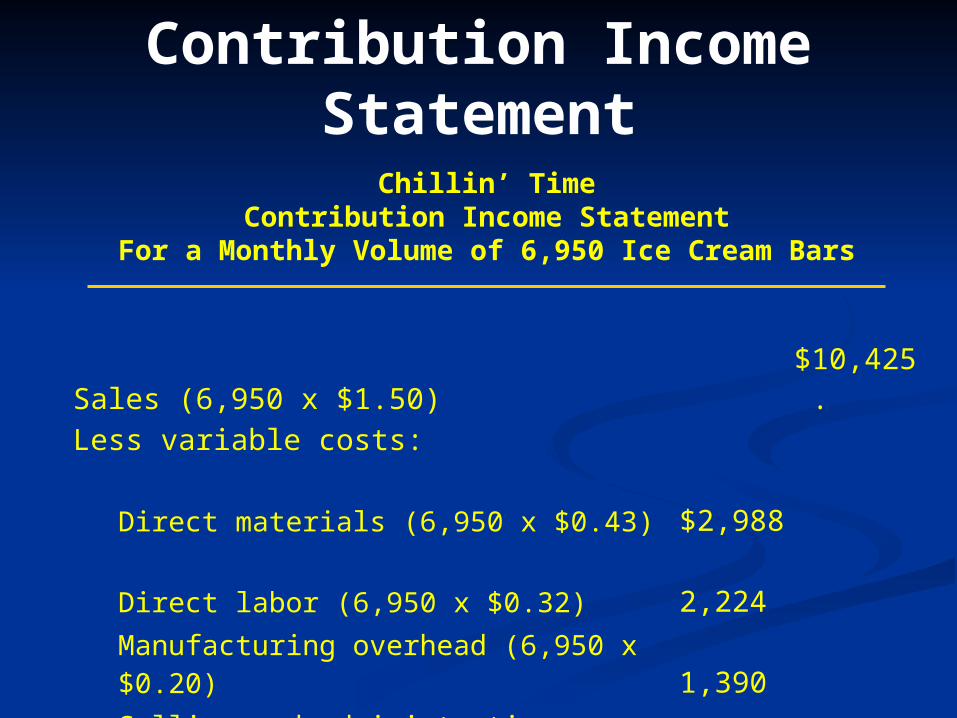

Contribution Income Statement

Sales (6,950 x $1.50) $10,425.

Less variable costs:

Direct materials (6,950 x $0.43) $2,988 Direct labor (6,950 x $0.32) 2,224 Manufacturing overhead (6,950 x $0.20) 1,390 Selling and administrative (6,950 x $0.15) 1,043 (7,645)

Contribution margin (6,950 x $0.40) 2,780.Less fixed costs:

Manufacturing 1,200 Selling and administrative 580 (1,780)

Profit $ 1,000.

Chillin’ TimeContribution Income Statement

For a Monthly Volume of 6,950 Ice Cream Bars

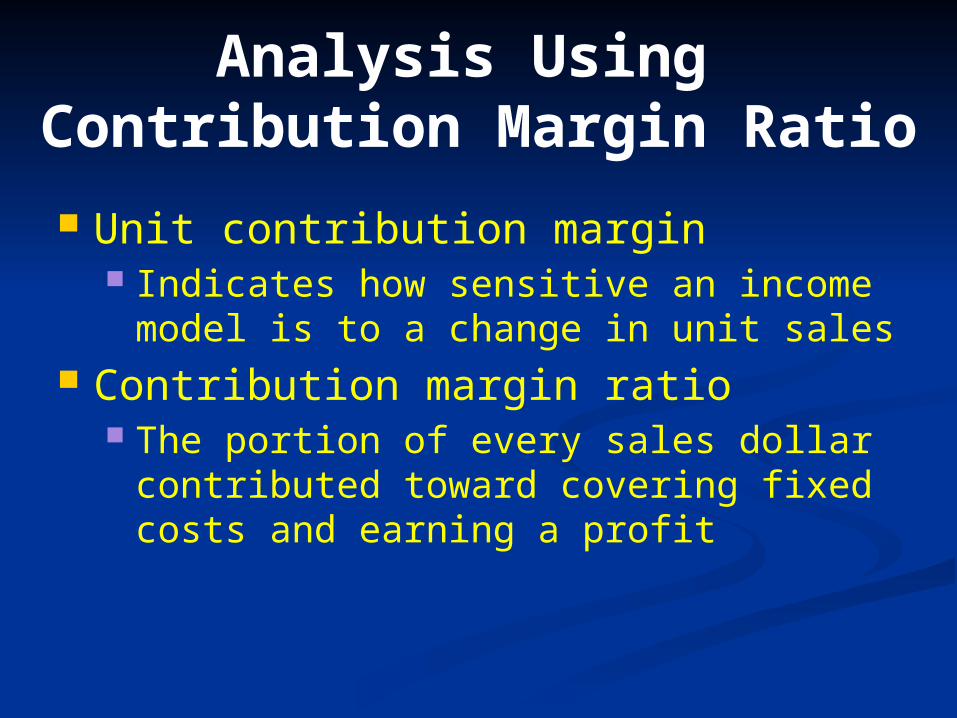

Analysis Using Contribution Margin Ratio

Unit contribution margin Indicates how sensitive an income

model is to a change in unit sales Contribution margin ratio

The portion of every sales dollar contributed toward covering fixed costs and earning a profit

Contribution Margin Example

$1.50 – $1.10 = $0.40

Total Per Unit

Sales (6,950 units) $ 10,425. $ 1.50 Variable costs (7,645) -1.10Contribution margin 2,780. $ 0.40 Fixed costs (1,780)Profit $ 1,000.

[$1.50 – $1.10] ÷ $1.50 = 0.2667

Contribution margin per unit:Contribution margin per unit:

Contribution margin ratio:Contribution margin ratio:

Chillin’ Time’s contribution income appears below:

Sensitivity Analysis

100 × $0.40 = $40

If sales increase by 100 ice cream bars per month, by how much will net income increase?

Total Per Unit Ratio to Sales Sales (6,950 units) $10,425. $ 1.50 1.000Variable costs (7,645) (1.10) (0.733)Contribution margin 2,780. $ 0.40 0.267 Fixed costs (1,780)Profit $ 1,000.

$1,050 × 0.2667= $280

If sales increase by $1,050 per month, by how much will net income increase?

EXAMPLE:

Break-Even Point Example

Chillin’ Time’s Break-Even Unit =

Sales Volume

= Fixed costsContribution margin per unit

$1,780$1.50 – $1.10 = 4,450 units

When Chillin’ Time sells 4,450 ice cream bars per month, it will break even.

Chillin’ Time sells ice cream bars with a $1.10 unit variable cost for $1.50 each.

How many bars must it sell to break even?

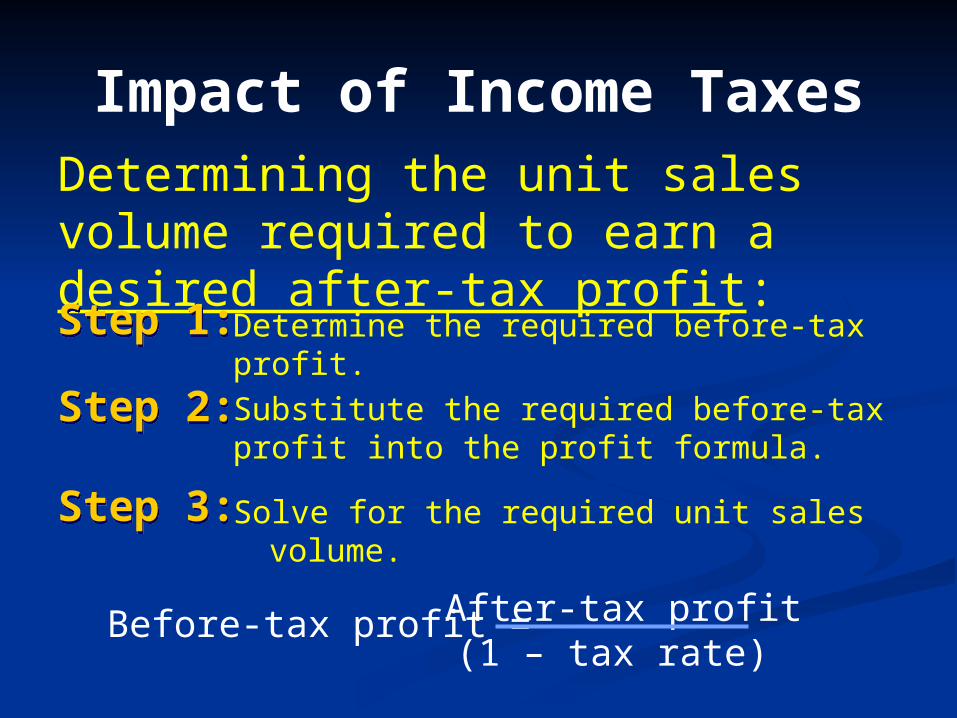

Impact of Income TaxesDetermining the unit sales volume required to earn a desired after-tax profit:

Solve for the required unit sales volume.

Step 1:Step 1: Determine the required before-tax profit.

Substitute the required before-tax profit into the profit formula.

Step 2:Step 2:

Step 3:Step 3:

Before-tax profit = After-tax profit(1 – tax rate)

Impact of Income Taxes Example

Before-tax profit = After-tax profit(1 – tax rate)

Chillin’ Time sells ice cream bars with a $1.10 unit variable cost for $1.50 each. It is subject to a 30 percent income tax rate. How many ice cream bars must Chillin’ Time sell to earn a desired monthly after-tax profit of $840?

$840(1 – 0.30) = = $1,200

Target unit sales volume = $1,780 + $1,200

$1.50 – $1.10

= 7,450 ice cream bars

Multiple Product Break-Even Point

Applicable when unit information is not available or when a company sells more

than one product.

= Fixed costs

Contribution margin ratio

= Fixed costs + Desired profit

Contribution margin ratio

Dollar break-even pointDollar break-even point

Target dollar sales volumeTarget dollar sales volume

Sales Mix Analysis

Sales mix The relative portion of unit or dollar

sales that are derived from each product

When sales mix is constant, the basic cost-volume-profit model can be used effectively

When sales mix is not constant, must determine average unit contribution margin or average contribution margin ratio for each alternative mix

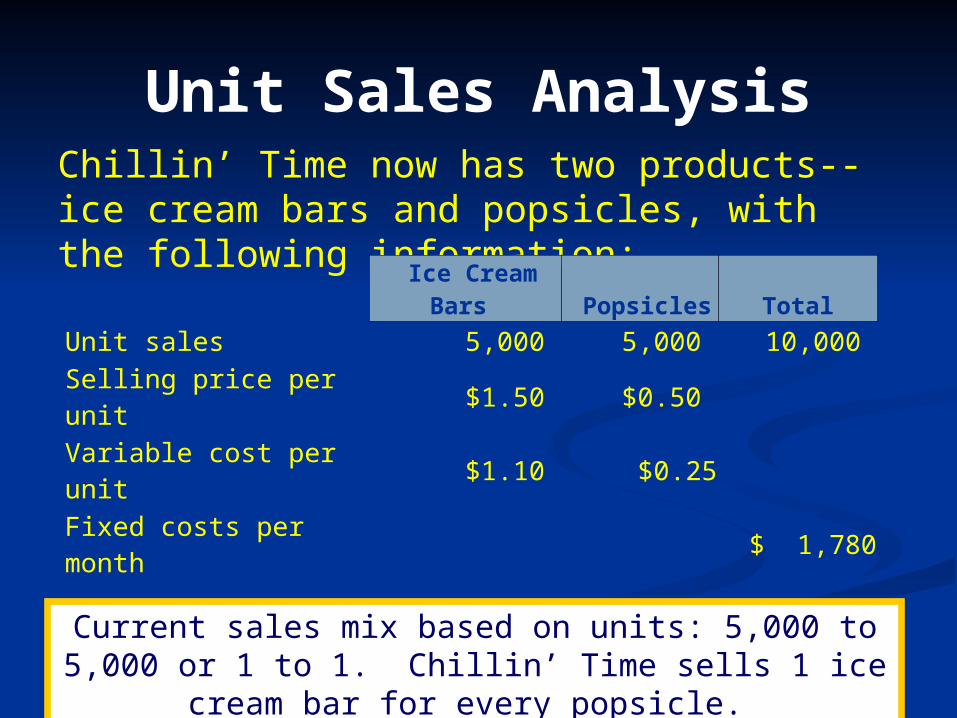

Unit Sales AnalysisChillin’ Time now has two products--ice cream bars and popsicles, with the following information: Ice Cream Bars Popsicles Total Unit sales 5,000 5,000 10,000 Selling price per unit $1.50 $0.50 Variable cost per unit $1.10 $0.25Fixed costs per month $ 1,780

Sales revenue $7,500 $2,500 $10,000 Variable costs 5,500 1,250 6,750 Contribution margin $ 2,000 $1,250 $ 3,250

Contribution margin ratio 0.267 0.500 0.325

Current sales mix based on units: 5,000 to 5,000 or 1 to 1. Chillin’ Time sells 1 ice cream bar for every popsicle.

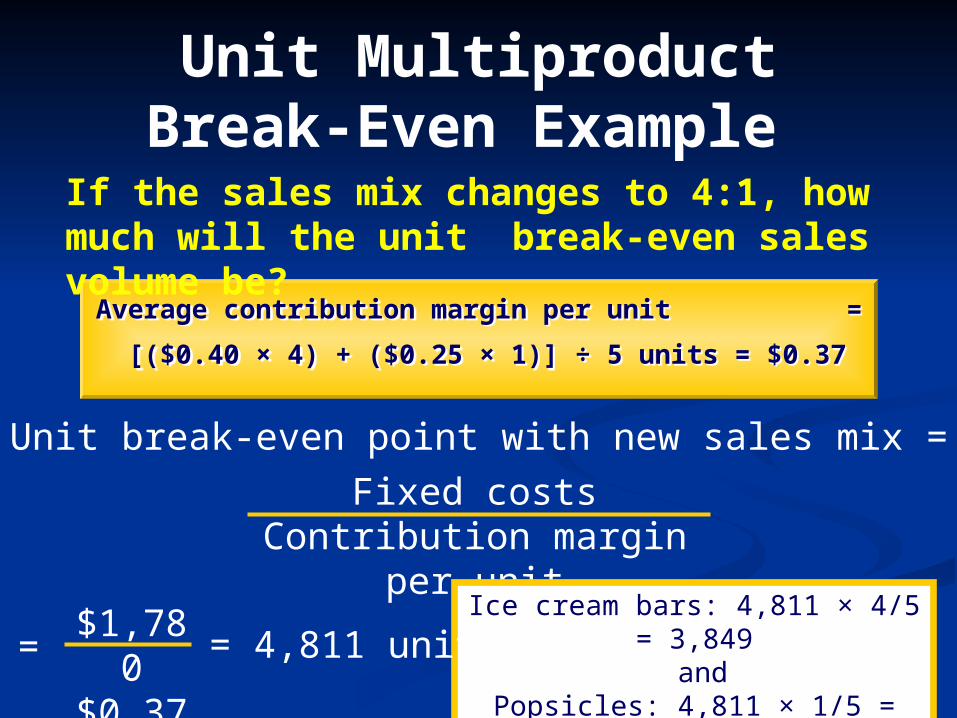

Unit Multiproduct Break-Even Example

Average contribution margin per unit = [($0.40 × 1) + ($0.25 × 1)] ÷ 2 units= $0.325Average contribution margin per unit

= [($0.40 × 1) + ($0.25 × 1)] ÷ 2 units= $0.325

Unit break-even point =Fixed costs

Contribution margin per unit

Ice cream bars: 5,477 × 1/2 = 2,739* and

Popsicles: 5,477 × 1/2 = 2,739*

= 5,476.9 ≈ 5,477 units$1,780$0.325

=

Unit Multiproduct Break-Even Example

Average contribution margin per unit =

[($0.40 × 4) + ($0.25 × 1)] ÷ 5 units = $0.37

Average contribution margin per unit =

[($0.40 × 4) + ($0.25 × 1)] ÷ 5 units = $0.37

Unit break-even point with new sales mix =

Fixed costsContribution margin per unit

Ice cream bars: 4,811 × 4/5 = 3,849 and

Popsicles: 4,811 × 1/5 = 962= 4,811 units

$1,780$0.37

=

If the sales mix changes to 4:1, how much will the unit break-even sales volume be?

Comparing Break-Even Example

Sales mix 1 to 1

Sales mix 1 to 1

Ice cream bars: 5,477 × 1/2 = 2,739* and

Popsicles: 5,477 × 1/2 = 2739*

Ice cream bars: 4,811 × 4/5 = 3,849 and

Popsicles: 4,811 × 1/5 = 962

The change in sales mix causes the total number of units needed to break even to change because of the

different contribution margins for the two products.

Break-even unitsBreak-even units

Sales mix 4 to 1

Sales mix 4 to 1

Dollar Multiproduct Break-Even Example

Current sales mix in dollars is 7,500 to 2,500 or 75% to 25%. How much is the break-even sales volume in dollars?

=Fixed costs

Contribution margin per unit

$1,7800.325

= $5,477=

Ice cream bars:$5,477 × 0.75 =

$4,108 and

Popsicles: $5,477 × 0.25 =

$1,369

Dollar break-even point with new sales mix =

Average contribution margin ratio = $3,250 ÷ $10,000 = 0.325

Average contribution margin ratio = $3,250 ÷ $10,000 = 0.325

Operating Leverage

What is operating leverage? Extent to which income will change

with a change in sales High degree of operating leverage

Signals the existence of a high portion of fixed costs

Degree of operating leverage

Contribution margin

Income before taxes=

Measuring Expected Change in Profit

Taco King and Mexi Land are competitors and reported the same sales revenue and before-tax profit during May: Taco King Mexi Land

Sales $40,000 $40,000. Variable costs (22,000) (8,000) Contribution margin 18,000 32,000. Fixed costs (8,000) (22,000) Before-tax profit $10,000. $10,000.

If sales drop by 20% for both, which company suffers more?

Degree of operating leverage

Taco King Mexi Land

$18,000$10,000

= 1.8 $32,000$10,000 = 3.2

Decrease in profit

1.8 × 20% = 36%Decline in Profit

3.2 × 20% = 64%Decline in Profit

Mexi Land’s higher operating leverage results in a larger profit decline.

Margin of Safety

Margin of Safety: Revenues – Breakeven Revenues

Margin of Safety Ratio: (Sales – BE Sales)/Sales

Margin of SafetyTaco King and Mexi Land are competitors and reported the same sales revenue and before-tax profit during May: Taco King Mexi Land

Sales $40,000 $40,000. Variable costs (22,000) (8,000) Contribution margin 18,000 32,000. Fixed costs (8,000) (22,000) Before-tax profit $10,000. $10,000.

CM% $18,000/40,000=45%

$32,000/40,000=80% Taco King Mexi Land

Break-even sales $8,000/45%=$17,778 $22,000/80%=$27,500

Margin of Safety $40,000-$17,778=22,222 $40,000-$27,500=$12,500

Margin of Safety Ratio* $22,222/$40,000 = 55.6% $12,500/$40,000=31.3%*Note that MSR = 1/OL