-

8/2/2019 modifed sa

1/34

TOPIC-SECTORAL ANALYSIS-ONBANKING SECTOR & FMCG SECTOR

List of sectors in india stock market?1)Metals

2) Auto

3) Banking

4)Breweries and distilleries

5)Power

6)Telecom

7)Cement

8)Chemicals

9)Computers10) IT

11)Construction

12) FMCG

13) Electronics

14)Engineering

15) Entertainment/Media

16)Finance and Investments

17) Hotel

18) Food processing

19) Healtcare

20) Pharma

21) Paint

22) paper

23) Petrochemicals

24) Plastic

25) Refineries

26) Sugar

27) Tea

28) Airlines

-

8/2/2019 modifed sa

2/34

-

8/2/2019 modifed sa

3/34

A comparison of these rankings with other information developed

by the money

manager provides a powerful tool in selection of specific

equities for inclusion in the

portfolio or the elimination of existing holdings.

sector

DefinitionA distinct subset of a market, society, industry, or

economy, whose components share

similar characteristics. Stocks are often grouped into different

sectors depending upon

the company's business. Standard & Poor's breaks the market

into 11 sectors. Two of

these sectors, utilities and consumer staples, are said to be

defensive sectors, while therest tend to be more cyclical in

nature. The other nine sectors are: transportation,

technology, health care, financial, energy, consumer cyclicals,

basic materials, capital

goods, and communications services. Other groups break up the

market into different

sector categorizations, and sometimes break them down further

into subsectors.

-

8/2/2019 modifed sa

4/34

ABSTRACT

Banking Sector in India is one of the growing sectors with great

dynamics. There are

various factors which affect the share prices of Banking

Companies. This report is all

about how various factors (Internal and External) affect the

Banking Sector Share

Prices. In this report a detailed analysis of the factors

affecting the share prices is

carried on and a model is developed to study the effect of

various factors on the share

prices. Here, various internal factors (Banks Profitability,

Income, Expenses, and News

about the Bank.) and external factors (Government policies, CRR,

Repo Rate, Reverse

Repo Rate, Rules and Regulations.) are considered which affect

the prices of theshares of Bank. Datas are collected for all the

quantifiable factors and for the rest

factors a theoretical explanation is given in detail. Using SPSS

a model is developed

which shows the regression and correlation co-efficient between

the share prices and

various factors affecting the same.

-

8/2/2019 modifed sa

5/34

INTRODUCTIONMARKETS DEFINED

STOCK MARKET IN INDIA The Indian security market has become

one

of the most dynamic and efficient security markets in Asia

today. The

Indian market now conforms to International Standards in terms

of

operating efficiency. During the latter half of 19th century,

shares of

companies used to be floated in India occasionally. There were

share

brokers in Bombay who assisted in the floatation of shares of

companies. Asmall group of stock brokers in Bombay joined together

in 1875 to form an

association called Native Share & Stockbrokers Association.

The

association drew up codes of conduct for brokerage business

and

mobilizes private funds for investment in the corporate sector.

It was this

association which later became the Bombay Stock Exchange, Mumbai

or

BSE Later on in 1894 the brokers of Ahmedabad formed the

Ahmedabad

Stock Exchange, the second stock exchange of the country. During

the

1900s Kolkata became another major center of share trading and

as a

result Kolkata Stock Exchange was formed in 1908. Later on

Chennai

Stock Exchange was started in 1920. However, by 1923, it ceased

to exist.

Then the Madras Stock Exchange was started in 1937. Three more

stock

exchanges were established before independence, at Indore in

1930, at

Hyderabad in 1943 and at Delhi in 1947.

Thus along with the increase in number of stock exchanges, the

number of

listed companies and the capital of listed companies grown

tremendously

after 1985 which results into growth and development of stock

market inIndia.

ABOUT BSE SENSEXBSE SENSEX or Bombay Stock Exchange Sensitive

Index is a value-weighted index composed of 30 stocks started in 01

of January, 1986. Itconsists of the 30 largest and most actively

traded stocks, representative of

-

8/2/2019 modifed sa

6/34

various sectors, on the Bombay Stock Exchange. These

companiesaccount for around one-fifth of the market capitalization

of the BSE. Thebase value of the SENSEX is 100 on April 1, 1979,

and the base year ofBSE-SENSEX is 1978-79. At irregular intervals,

the Bombay StockExchange (BSE) authorities review and modify its

composition to makesure it reflects current market conditions. The

index is calculated based ona free-float capitalization method; a

variation of the market cap method.Instead of using a company's

outstanding shares it uses its float, or sharesthat are readily

available for trading. The free-float method, therefore, doesnot

include restricted stocks, such as those held by company

insiders.The index has increased by over ten times from June 1990

to the present.Using information from April 1979 onwards, the

long-run rate of return onthe BSE SENSEX works out to be 18.6% per

annum, which translates toroughly 9% per annum after compensating

for inflation. There are five

major indices in BSE, thirteen sector specific indices and a BSE

DollexIndex for dollar prices and movements.

ABOUT NSE AND NIFTY 50The National Stock Exchange of India

Limited (NSE) is a Mumbai-basedstock exchange. It is the largest

stock exchange in India in terms of dailyturnover and number of

trades, for both equities and derivative trading.Though a number of

other exchanges exist, NSE and the Bombay StockExchange are the two

most significant stock exchanges in India and

between them are responsible for the vast majority of share

transactions.The NSE's key index is the S&P CNX Nifty, known as

the Nifty, an index offifty major stocks weighted by market

capitalization.NSE is mutually-owned by a set of leading financial

institutions, banks,insurance companies and other financial

intermediaries in India but itsownership and management operate as

separate entities. There are atleast 2 foreign investors NYSE Euro

next and Goldman Sachs who havetaken a stake in the NSE. As of

2006, the NSE VSAT terminals, 2799 intotal, cover more than 1500

cities across India. In October 2007, the equitymarket

capitalization of the companies listed on the NSE was US$ 1.46

trillion, making it the second largest stock exchange in South

Asia. NSE isthe third largest Stock Exchange in the world in terms

of the number oftrades in equities. It is the second fastest

growing stock exchange in theworld with a recorded growth of

16.6%

-

8/2/2019 modifed sa

7/34

The Standard & Poor's CRISIL NSE Index 50 or S&P CNX

Nifty nicknamed

Nifty 50 or simply Nifty, is the leading index for large

companies on the

National Stock Exchange of India. The Nifty is a well

diversified 50 stock

index accounting for 22 sectors of the economy. It is used for a

variety of

purposes such as benchmarking fund portfolios, index based

derivativesand index funds. There are seven major Indices in NSE

and fifteen sector

specific Indices. CNX BANK INDEX or BANK NIFTY is the index

which has

17 banks listed on it and is a separate index to look upon price

movements

of banks share prices. A brief account of the same is given

below.

CNX Bank Index The Indian banking Industry has been

undergoing

major changes, reflecting a number of underlying

developments.

Advancement in communication and information technology has

facilitated

growth in internet-banking, ATM Network, Electronic transfer of

funds and

quick dissemination of information. Structural reforms in the

banking sector

have improved the health of the banking sector. The reforms

recently

introduced include the enactment of the Securitization Act to

step up loan

recoveries, establishment of asset reconstruction companies,

initiatives on

improving recoveries from Non-performing Assets (NPAs) and

change in

the basis of income recognition has raised transparency and

efficiency in

the banking system. Spurt in treasury income and improvement in

loan

recoveries has helped Indian Banks to record better

profitability. In order to

have a good benchmark of the Indian banking sector, India Index

Service

and Product Limited (IISL) has developed the CNX Bank Index. CNX

Bank

Index is an index comprised of the most liquid and large

capitalized Indian

Banking stocks. It provides investors and market intermediaries

with a

benchmark that captures the capital market performance of Indian

Banks.The index will have 12 stocks from the banking sector which

trade on the

National Stock Exchange. The average total traded value for the

last six

months of CNX Bank Index stocks is approximately 95.85% of the

traded

value of the banking sector. CNX Bank Index stocks represent

about

86.06% of the total market capitalization of the banking sector

as on

-

8/2/2019 modifed sa

8/34

January 30, 2009. The average total traded value for the last

six months of

all the CNX Bank Index constituents is approximately 14.86% of

the traded

value of all stocks on the NSE. CNX Bank Index constituents

represent

about 8.63% of the total market capitalization on January 30,

2009.

-

8/2/2019 modifed sa

9/34

OBJECTIVE OF THE STUDY

The objective of the project is to identify, understand and

analyze the impact of various

factors that affect the Indian Equity Market (BANKING SECTOR).

The main focus will

be on understanding, analyzing and providing a valid explanation

both theoretically and

technically, that how various factors affect the share prices of

BNAKING SECTOR. By

undertaking this study I would like to keep my first step in the

field of research. This

project will help me in enhancing my analytical skills and will

give me a better

understanding of how things move on and are to be studied. At

the same time with this

study I will be providing the organization a list of factors

that affect the market, so that

they can keep a watch on the same and use the same for the

benefit of clients and

company and also increase their accuracy and profits. This will

be my contribution tothis huge company

PURPOSE, SCOPE AND LIMITATIONS

The PURPOSE of the report is to analyze how various factors

affect the prices of abanks share. The share prices are highly

affected by various internal and externalfactors. It is of great

importance to understand, learn and analyze the same. Thus,

this

report is a move in path of understanding those factors and

analyzing the impact of thesame.Banks are a major part of any

economic system. They provide a strong base to Indian

economy too. Even in share markets, the performance of bank

shares is of great

importance. This is justified by the proof that in both BSE and

NSE we haveseparate

index for Banking Sector Shares. But for our study we have taken

only Bank Nifty which

is a part of NSE. Thus, the performance of share market, the

rise Page | and the fall of

market is greatly affected by the performance of Banking Sector

Shares and this report

revolves around all those factors, their understanding and a

theoretical and technical

analysis of the same.

SCOPE OF STUDYIt gave me an opportunity to study the banking

sector in a detailed manner.

I got knowledge of prevailing Market Scenario.

It helped me in learning the market dynamics, study the movement

of share prices andto give a proper justification for the same,

theoretically and technically.

-

8/2/2019 modifed sa

10/34

It helped me in understanding and learning the corporate culture

And above all, theconcerned organization can get some valuable

recommendations, which can definitelyimprove the performance of the

organization.

LIMITATIONS OF THE STUDY

Though the resources seem sufficient enough to achieve high

standard for thisresearch, still we foresee the following

limitations of study.The Sectoris very vast and it was not possible

to cover every nook and corner of this sector.

The variability and availability of data was also a

limitation.

The data were linear and possessed multi collinearity, so each

and every data was notconsidered for analysis.

The objective which we want to fulfill in this project is really

good, but the major demeritto our study is the availability of time

for our search and analysis, but then also, I havetried my level

best to show a glimpse of my Research in tune with the

objectives.

11.. wwhhaatt iiss BBaannkkiinngg

Section 5(b) defines banking Accepting for the purpose of

lending or investmentof deposits or money repayable on demand or

otherwise and withdrawable bycheque, draft, order or otherwise

BBaannkkss ggeett aaffffeecctteedd bbyyy Actions of Central

Banksy Actions of the Governmenty Domestic and International

Disturbancesy Inflation

DDeerreegguullaattiioonn

y Banks are now operating in a fairly deregulated environment

and arerequired to determine on their own, interest rates on

deposits andadvances

y Intense competition for business involving both the assets and

liabilities

-

8/2/2019 modifed sa

11/34

together with increasing volatility in the interest rates has

brought pressureon the management of banks to maintain a good

balance among spreads

RRiisskkss FFaacceedd bbyy BBaannkkss

y Credit Risky Market Risk

o Liquidity Risko Interest Rate Risk

y Operational Risk

EEffffeeccttss ooffRRiisskk FFaaccttoorrss

y Loss of Market Valuey Loss of Reservesy Loss of stakeholders

confidence

y BANKING SECTORy

y Indian banks, the dominant financial intermediaries in India,

have made goodprogress over the last five years, as is evident from

several parameters, includingannual credit growth, profitability,

and trend in gross non-performing assets(NPAs). While the annual

rate of credit growth clocked 23% during the last five

years, profitability (average Return on Net Worth) was

maintained at around 15%during the same period, and gross NPAs fell

from 3.3% as ony March 31, 2006 to 2.3% as on March 31, 2011. Good

internal capital generation,

reasonably active capital markets, and governmental support

ensured goodcapitalisation for most banks during the period under

study, with overall capitaladequacy touching 14% as on March 31,

2011. At the same time, high levels ofpublic deposit ensured most

banks had a comfortable liquidity profile.

yy While banks have benefited from an overall good economic

growth over the last

decade, implementation of SARFAESI1, setting up of credit

information bureaus,internal improvements such as upgrade of

technology infrastructure, tightening of

the appraisal and monitoring processes, and strengthening of the

riskmanagement platform have also contributed to the improvement.

Significantly,the improvement in performance has been achieved

despite several hurdlesappearing on the way, such as temporary

slowdown in economic activity (in thesecond half of 2008-09), a

tightening liquidity situation, increases in wagesfollowing

revision, and changes in regulations by the Reserve Bank of

India(RBI), some of which prescribed higher credit provisions

-

8/2/2019 modifed sa

12/34

y or higher capital allocations. Currently, Indian banks face

several challenges,such as increase in interest rates on saving

deposits, possible deregulation ofinterest rates on saving

deposits, a tighter monetary policy, a large governmentdeficit,

increased stress

y in some sectors (such as, State utilities, airlines, and

microfinance), restructured

loan accounts, unamortised pension/gratuity liabilities,

increasing infrastructureloans, and implementation of Basel III.yy

1 The Securitisation and Reconstruction of Financial Assets and

Enforcementy of Security Interest Act, 2002y ICRA Researcbbbbby

bbbbbby

ybahBackgro

undyy ba

nnnjhdiuysduisydhsi

The Indian financial sector (including banks, non-banking

financial companies, or

NBFCs, and housing finance companies, or HFCs) reported a

compounded annualgrowth rate (CAGR) of 19% over thelast three years

and their credit portfolio stood atclose to Rs. 49 trillion (around

62% of 2010-11 GDP) as on March 31, 2011. Banksaccounted for nearly

86% of the total credit, NBFCs for around 10%, and HFCs foraround

4%. Within banks, public sector banks (PSBs), on the strength of

their country-wide presence, continued to be the leader, accounting

for around 76% of the total creditportfolio, while within the NBFC

sector, large infrastructure financing institutions2accounted for

more than half the total NBFC credit portfolio; NBFCs that are into

retail

-

8/2/2019 modifed sa

13/34

financing took up the rest. While the Indian banking sector

features a large number ofplayers competing against each other, the

top 10 banks accounted for a significant 57%share of the total

credit as on March 31, 2011

Key Players In Banking Sector

Strong growth in infrastructure creditdrives creditgrowth in

2010-11; pace ofdepositgrowth slows

Total banking credit4 stood at close to Rs. 39 trillion as on

March 25, 2011 and reporteda strong 21.4% growth in 2010-11, led by

credit to the infrastructure sector and toNBFCs. In 2011-12,

although the pace of credit growth has been subdued in the

firsttwomonths (up just 0.2% from March 2011 levels), it is in line

with the pattern noticed in theprevious years (0.1% in 2010-11 and

0.4% in 2009-10). According to ICRAsestimates, private banks

reported a higheroverall credit growth of around 26% in2010-11 (10%

in previous year) as compared with PSBs, which achieved around 22%

(20%in previous year). Historically, the banking sectors credit

portfolio has been growing at

Name ofBank

CreditPortfolioasin March2011 (Rs.billion)

MarketShare(%)

NIMs(2010-11)

Tier ICapital% as inMarch2011

Returnon NetWorth(2010-11)

GrossNPA %as inMarch2011

State Bankof India

7,567 18% 2.9% 7.8% 13% 3.3%

PunjabNationalBank

2,421 6% 3.5% 8.4% 24% 1.8%

Bank ofBaroda

2,287 5% 2.8% 10.0% 24% 1.4%

ICICI Bank 2,164 5% 2.3% 13.2% 10% 4.5%Bank ofIndia

2,131 5% 2.5% 8.3% 17% 2.2%

CanaraBank

2,125 5% 2.6% 10.9% 26% 1.5%

HDFCBank

1,600 4% 4.2% 12.2% 17% 1.1%

IDBI Bank 1,571 4% 1.8% 8.1% 16% 1.8%Axis Bank 1,424 3% 3.1%

9.4% 19% 1.1%CentralBank ofIndia

1,297 3% 2.7% 6.4% 18% 2.2%

Totalbankingsector

42,874 100% 2.9% 9.7% 17% 2.3%

-

8/2/2019 modifed sa

14/34

over 20% per annum over the last several years (except in

2009-10, when the growthrate moderated to 17% mainly because of the

decline in ICICI Banks credit portfolio).Over the years, credit

growth has outpaced deposits growth; the credit portfolio reporteda

CAGR of 24% over the last eight years, while deposits achieved a

CAGR of 19% andthe investment portfolio of 14% over the same

period. The higher growth in credit could

be achieved because of the slower growth in investments and the

increase in capital. In 2010-11, while deposits growth for SCBs

slowed down to 17%, credit growth wasmaintained at 21% with the

growth in investments being just 13%. The higher creditgrowth

versus deposits growth led to an increase in the credit deposits

ratio (CD ratio)from 72.2% as in March 2010 to 75.7% as in March

2011, although the CD ratiomoderated to 74.2% as on May 27, 2011,

largely because of the slow credit growth incomparison with

deposits duringthe first two months of 2011-12.

During 2010-11, the infrastructure sector, particularly power,

and NBFCs were the keydrivers of the credit growth achieved by the

banking sector. Credit to the power sector

reported a growth of 43%, while other infrastructure credit grew

by 34% during 2010-11,against an overall credit growth of 21%. As

in March 2011, the infrastructure sector(including power) accounted

for 14% of the total credit portfolio of banks.

Within the power sector, historically banks have been taking

exposure to State powerutilities as well asindependent power

producers (IPPs). Going forward, with many banksapproaching the

exposure cap on lending to the power sector and given the

concernshovering over the prospects of the sector itself, the pace

of growth of credit to this

-

8/2/2019 modifed sa

15/34

segment could slow down. However, in the short to medium term,

the undisbursedsanctions to power projects are likely to provide

for a moderate growth.

As for bank credit to NBFCs, the same increased by 55% in

2010-11 and accounted foraround 5% of the banks total credit

portfolio as in March 2011. Moreover, around half

of this went to infrastructure relatedentities, and the rest

mainly to NBFCs engaged inretail financing. Most of the NBFCs are

focused on secured assets classes, havereported low NPA

percentages, and are well-capitalised. As for banks retail

lending,this continued to lag overall credit growth during 2010-11.

Retail credit grew by 17% in2010-11 against the overall credit

growth of 21%, although the 17% figure marked asignificant increase

over the 4.1% reported in 2009-10. Credit to commercial real

estatealso increased in 2010-11, reporting a 21% growth that year

as against nil in 2009-10.

Large governmentborrowings may allow for just17-18% creditgrowth

in 2011-

12

Since March 2010, the RBI has raised the repo rate by 275 basis

points (bps), which inturn has been transmitted by the banking

system via increases in the base and primelending rates, besides

deposit rates. Going forward, while the RBIs tight monetarystance

may exert a downward pressure on the demand for credit, considering

theanticipated GDP growth (around 8%), investments in

infrastructure and lower funds flowfrom the capital markets, credit

demand could still remain high. However, bankscapacity to meet

credit demand could get constrained by the volume of deposits

theyare able to mobilise and by the large amount of funds they

would need to keep aside tofund the government deficit. In case the

government deficit is in line with the Budget

numbers, the net borrowing of the Government of India (GOI) and

the Stategovernments via bonds would reach an estimated Rs. 4.7

trillion in 2011-12 (Rs.4.1trillion in 2010-11). As banks fund

around 40% of these bonds, they would need to setaside Rs. 1.9

trillion for the purpose. If deposits were to grow by 17%, the

balance funds(incremental deposits + internal capital generation +

fresh external capital increase ininvestments in government bonds)

would supportonly 17-18% credit growth. Any highergrowth would

require intervention from the RBI. Further, in case the government

deficitis higher because of lower tax collection and underprovided

fuel & food subsidies, themaximum possible credit growth would

be still lower. At the same time, a higher-than-expected deposit

growth could allow banks expand their credit base.

On assetquality, PSBs reportsome deterioration while private

banks showImprovement

The Gross NPA percentage of SCBs did not increase by the extent

that the stress in theIndian market during 2008-09 would warrant

because of large loan restructuring overlast 2-3 years (4-5% of

total advances); Gross NPAs declined marginally from 2.4% as

-

8/2/2019 modifed sa

16/34

in March 2010 to 2.3% as in March 2011.However, higher

provisioning led to areduction in Net NPAs from 1.1% as in March

2010 to 0.9% as inMarch 20

Higher interest rates could ensure better deposits growth in

2011-12

Higher interest rates could ensure better deposits growth in

2011-12

In the banking system,historically, there has

-

8/2/2019 modifed sa

17/34

been a positive correlation between growth in deposits base and

increase in interestrates; periods with high interest rates have

seen relatively high deposits growth, as inhigh interest rate

regime bank fixed depositsbecome more attractive than many other

instruments. At present, it appears that giventhe outlook on

interest rates, banks may be able to mobilise retail deposits at a

higher

pace in 2011-12 than in the previous year. In 2010-11, according

to ICRA In 2010-11,according to ICRAs estimates, the overall

deposits of private banks increased by 22%,while that of PSBs

increased by 18%. Within deposits, low cost deposits (CASA,

currentand saving accounts) increased by 27% for private sector

banks, and by 15% for PSBs.CASA deposits represented 41% of the

total deposits for private banks, and for a lower33% for PSBs. For

banks, having significant low cost deposits (CASA) as a

proportionof total deposits could help them keep their cost of

funds under control even in ascenario of rising interest rates in

the system.

High proportion of certificates of deposits could impactNIM and

liquiditynegatively

ICRAs analysis of the current liquidity situation shows that

Indian banks have beenraising bulk funds in the form of

certificates of deposit (CDs) and high-cost depositsfrom corporate

entities mostly for short tenures. The share of CDs

outstandingincreased to 8.2% as in March 2011 from 7.2% as in

September 2010 and 7.6% as inMarch 2010, with the total CDs

outstanding increasing from Rs. 3.4 trillion to Rs. 4.2trillion

during this period. The high proportion of CDs (instead of retail

deposits) couldadversely impact the liquidity profile of banks and

their NIMs in a scenario of risinginterest rates.

Mostbanks may not require significantcapital now

During 2010-11, the GOI infused Rs. 165 billion in PSBs to

improve their Tier I capital to8% and take up its stake in the PSBs

to at least 58%. After this, the Tier I capital ofmost of the PSBs

has improved. Therefore, these banks (apart from SBI) may

notrequire significant Tier I capital in the short term. The GOI

has budgeted for Rs. 60billion capital for PSBs in 2011-12. As for

SBI, it plans to raise significant capital througha rights issue,

and therefore, under the current regulations and market valuations,

theGOI may need to infuse substantial capital into it to maintain

its stake in the bank at58%. As for private banks, these are well

capitalised, although some may need equity to

fund their growth plans.Some banks may require capitalto

meetBasel III norms

As can be seen in table 4 below, banks will need to maintain

higher regulatory capitalunder BASEL-IIInorms versus the existing

RBI norms.

-

8/2/2019 modifed sa

18/34

FACTORS AFFECTING BANKING SECTOR

Starting off with the project, in the initial phase of SIP, I

learnt the basics of the stockmarket. As I had to work here in this

market for 3.5 months this was the basic necessity.In that phase I

had a nice exposure of how to deal with clients, how to handle

the

queries of the investors, it was a practical exposure to learn

the working of the market,how the market moves and all about the

corporate culture. Also I had learnt what factorsbasically affect

the equity market. Then I decided to limit my project to just

BankingSector, because it is one of the most dynamic sector and

also availability of time wasnot permitting me to go beyond

this.

There are N number of factors which affect the share prices.

They can be broadlyclassified into two:

INTERNAL FACTORS

EXTERNAL FACTORS

INTERNAL FACTORS:As the name suggests, Internal Factors are

those whichaffect the share prices internally, i.e. they are

internal to the company or morespecifically bank. Some of the major

internal factors that affect the share prices of abank are as

follows:

-

8/2/2019 modifed sa

19/34

EARNINGS OF THE COMPANY:How much Profit a company earns acts as

a significant factor in price movements. If the

quarterly results are good for a bank, then the price goes up,

and if the results are not

good, the investors show no interest in such banks share and

thus price

falls. Investors invest money in the companies who earn well and

in turn give goodreturn on investment. Thus, a wealthy and a

profitable company have gooinvestors and

thus have positive price movements. Price/Earnings Ratio also

gives us idea about the

same.

MARKET CAPITALIZATION: Generally we commit one mistake that we

guess the

companys worth from the price of its stock. It is the market

capitalization of the

company, rather than the stock price, that is more important

when it comes to

determining the worth of the company. We need to multiply the

stock price with the total

number of outstanding stocks in the market to get the market

capitalization of a

company and that is the worth of the company. Thus, a company or

bank with high

Market Capitalization turns out to be more popular among

investors. For example,

HDFC BANK, ICICI BANK and SBI are more popular among investors

than other banks

because they have huge market share and market capitalization.

As market

capitalization increases, the share price tends to increase and

as market capitalization

decreases, the share price tends to decrease

PRICE/EARNINGS RATIO: Price/Earnings ratio or the P/E ratio

gives us a fairidea of how a company's share price compares to its

earnings. If the price of the shareis too much lower than the

earning of the company, the stock is undervalued and it hasthe

potential to rise in the near future. On the other hand, if the

price is way too muchhigher than the actual earning of the company

and then the stock is said to overvaluedand the price can fall at

any point. The earnings also have a direct relation with pricewhich

is already explained above.

INTERNAL AFFAIRS OF THE COMPANY:Any happening inside the company

or any internal news does affect its share price. For

example any key person moving out of the company, acquisition or

takeover or mergernews, share split, employee strike and any other

thing internal to the affairsof the bank

affects the share price. A positive note from the internal

affairs takes the price to new

highs and a negative does vice versa.

INTERST RATES: Interest rates play a major role in determining

stock markettrends. Bull markets (those in an upward market) are

usually associated with low

-

8/2/2019 modifed sa

20/34

interest rates and high Capital Gains, and bear markets (those

in a downward trend)

with high interest rates and low Capital gains. Interest rates

are determined by the

demand for capital pushes them up and normally indicates that

the economy is

thriving and that shares probably expensive. Low interest

indicate low demand for

capital, thus liquidity builds up on the economy, driving share

price down. Otherinterest rates like that of on Deposits and

Borrowings also have impact on share prices.

OTHER FACTORS: Other factors like Growth of the company, figures

of deposits,

advances, balance sheet, Profit and Loss Account, etc.. also

affect the share prices

drastically. A discussion for the same is done in later part of

the report

EXTERNAL FACTORS:After studying the internal factors, lets take

a lookat some External Factors which affect the Share Prices.

SENTIMENTS:Investor sentiment is almost impossible to predict

and can be infuriating if, for example,

you have bought shares in a company that you think is a good buy

but the price

remains flat. Investor sentiment is influenced by a wide variety

of factors. Share prices

can, for example, be flat during the summer simply because so

manmajor investors are

on holiday or attending major sporting events such as Royal

Ascot and Wimbledon,

hence the adage sell in May and go away. Investor sentiment can

lead to irrational

buying or selling of shares and result in bull and bear markets.

A bull market is when

share prices rise while a bear market is when they fall. In the

technology boom of thelate 1990s, for example, investors paid

extremely high prices for shares and ignored

traditional valuation measures, such as P/E ratios. This carried

on until 2000 when

investors belatedly realized these shares has risen too far and

resulted in a three year

bear market in shares. Thus, Sentiments of investors affect the

share prices a lot and

this is something unpredictable and immeasurable factor, but

still the most important

one.

COMPANY NEWS and OTHER NEWS: The way investors interpret

newscoming out of companies is also a major influence on share

prices. If, for example, acompany puts out a warning that business

conditions are tough, shares will often dropin value. If, however,

a director buys shares in the firm, it may be a signal that

thecompanys prospects are improving. Companies put out a great deal

of news and mostof the major announcements are covered by the

financial press. But someannouncements not regarded as so important

and sometimes, particularly amongsmaller firms that are monitored

less by investors and financial journalists, indicators of

-

8/2/2019 modifed sa

21/34

the companys health can be missed. Takeovers or even rumors of

takeovers alsohave a big influence on prices. This is because

investors expect the bidder to pay apremium to shareholders. Also

any other news or speculation about factors like changein Repo

Rate, Cash Reserve Ratio, Reverse Repo Rate, any change or likely

change inthe policies of government or RBI or SEBI, any new

guidelines issued by the concerned

authority, etc. affect the price of the share. A positive news

in any of these respectsleads to a rise in must always remember

that often times, despite amazingly good news,a stock can show

least movement. It is the overall performance of the company

that

matters more than news. It is always wise to take a wait and

watch policy in avolatile market or when there is mixed reaction

about a particular stock.

DEMAND AND SUPPLY: This fundamental rule of economics holds good

for theequity market as well. The price is directly affected by the

trend of stock market trading.When more people are buying a certain

stock, the price of that stock increases andwhen more people are

selling the stock, the price of that particular stock falls. Now it

isdifficult to predict the trend. Thus, we should be very careful

while dealing in stocks as

buying or selling pressure may lead to steep rise or fall in

price of the shares.Thus, news in any respect is undoubtedly a huge

factor when it comes to stock price.

Positive news about a company can increase buying interest in

the market while a

negative press release can ruin the prospect of a stock. Having

said that, we

-

8/2/2019 modifed sa

22/34

CAPITAL ADEQUACY & CALCULATIONS

SummaryCapital adequacy ratios are a measure of the amount of a

bank's capital expressed as apercentage of its risk weighted credit

exposures. An international standard whichrecommends minimum

capital adequacy ratios has been developed to ensure banks

canabsorb a reasonable level of losses before becoming

insolvent.

Applying minimum capital adequacy ratios serves to protect

depositors and promote thestability and efficiency of the financial

system.

Two types of capital are measured - tier one capital which can

absorb losses without a bankbeing required to cease trading, e.g.

ordinary share capital, and tier two capital which canabsorb losses

in the event of a winding-up and so provides a lesser degree of

protection to

depositors, e.g. subordinated debt.

Measuring credit exposures requires adjustments to be made to

the amount of assets shownon a bank's balance sheet. The loans a

bank has made are weighted, in a broad brush manner,according to

their degree of riskiness, e.g. loans to Governments are given a 0

percentweighting whereas loans to individuals are weighted at 100

percent.

Off-balance sheet contracts, such as guarantees and foreign

exchange contracts, also carrycredit risks. These exposures are

converted to credit equivalent amounts which are alsoweighted in

the same way as on-balance sheet credit exposures. On-balance sheet

andoffbalance sheet credit exposures are added to get total risk

weighted credit exposures.

The minimum capital adequacy ratios that apply are:y tier one

capital to total risk weighted credit exposures to be not less than

4 percent;y total capital (tier one plus tier two less certain

deductions) to total risk weighted

creditexposures to be not less than 8 percent.

IntroductionBanks registered in Our country are required to

publish quarterly disclosure statements whichinclude a range of

financial and prudential information. (For an explanation of the

disclosurearrangements, see the Reserve Bank Bulletin of March

1996). A key part of these statementsis the disclosure of the

banks' "capital adequacy ratios". These ratios are a measure of

theamount of a bank's capital in relation to the amount of its

credit exposures. They are usually

expressed as a percentage, e.g. a capital adequacy ratio of 8

percent means that a bank'scapital is 8 percent of the size of its

credit exposures. Capital and credit exposures are bothdefined and

measured in a specific manner which is explained in this

article.

An international standard has been developed which recommends

minimum capital adequacyratios for international banks. The purpose

of having minimum capital adequacy ratios is toensure that banks

can absorb a reasonable level of losses before becoming insolvent,

andbefore depositors funds are lost.

-

8/2/2019 modifed sa

23/34

Applying minimum capital adequacy ratios serves to promote the

stability and efficiency ofthe financial system by reducing the

likelihood of banks becoming insolvent. When a bankbecomes

insolvent this may lead to a loss of confidence in the financial

system, causingfinancial problems for other banks and perhaps

threatening the smooth functioning offinancial markets. Accordingly

applying minimum capital adequacy ratios in Banks assists in

maintaining a sound and efficient financial system.

It also gives some protection to depositors. In the event of a

winding-up, depositors' fundsrank in priority before capital, so

depositors would only lose money if the bank makes a losswhich

exceeds the amount of capital it has. The higher the capital

adequacy ratio, the higherthe level of protection available to

depositors.

This article provides an explanation of the capital adequacy

ratios applied by the ReserveBank and a guide to their calculation.

For more detail, the Reserve Bank policy documentCapital Adequacy

Framework, issued in January 1996, available from the Reserve

BankLibrary, should be consulted.Development of Minimum Capital

Adequacy Ratios

The "Basle Committee" (centred in the Bank for International

Settlements), which wasoriginally established in 1974, is a

committee that represents central banks and financialsupervisory

authorities of the major industrialised countries (the G10

countries). Thecommittee concerns itself with ensuring the

effective supervision of banks on a global basisby setting and

promoting international standards. Its principal interest has been

in the area ofcapital adequacy ratios. In 1988 the committee issued

a statement of principles dealing withcapital adequacy ratios. This

statement is known as the "Basle Capital Accord". It contains

arecommended approach for calculating capital adequacy ratios and

recommended minimumcapital adequacy ratios for international banks.

The Accord was developed in order toimprove capital adequacy ratios

(which were considered to be too low in some banks) and tohelp

standardise international regulatory practice. It has been adopted

by the OECD countries

and many developing countries. The Reserve Bank applies the

principles of the Basle CapitalAccord in Our country.

CapitalThe calculation of capital (for use in capital adequacy

ratios) requires some adjustments tobe made to the amount of

capital shown on the balance sheet. Two types of capital

aremeasured in Our country - called tier one capital and tier two

capital. Tier one capital iscapital which is permanently and freely

available to absorb losses without the bank beingobliged to cease

trading. An example of tier one capital is the ordinary share

capital of thebank. Tier one capital is important because it

safeguards both the survival of the bank andthe stability of the

financial system.

Tier two capital is capital which generally absorbs losses only

in the event of a winding-up ofa bank, and so provides a lower

level of protection for depositors and other creditors. Itcomes

into play in absorbing losses after tier one capital has been lost

by the bank. Tier twocapital is sub-divided into upper and lower

tier two capital. Upper tier two capital has nofixed maturity,

while lower tier two capital has a limited life span, which makes

it lesseffective in providing a buffer against losses by the bank.

An example of tier two capital issubordinated debt. This is debt

which ranks in priority behind all creditors except

-

8/2/2019 modifed sa

24/34

shareholders. In the event of a winding-up, subordinated debt

holders will only be repaid if allother creditors (including

depositors) have already been repaid.

The Basle Capital Accord also defines a third type of capital,

referred to as tier three capital.Tier three capital consists of

short term subordinated debt. It can be used to provide a

bufferagainst losses caused by market risks if tier one and tier

two capital are insufficient for this.

Market risks are risks of losses on foreign exchange and

interest rate contracts caused bychanges in foreign exchange rates

and interest rates. The Reserve Bank does not requirecapital to be

held against market risk, so does not have any requirements for the

holding oftier three capital. The composition and calculation of

capital are illustrated by the first stepof the capital adequacy

ratio calculation example shown later in this article.

Credit ExposuresCredit exposures arise when a bank lends money

to a customer, or buys a financial asset (e.g.a commercial bill

issued by a company or another bank), or has any other arrangement

withanother party that requires that party to pay money to the bank

(e.g. under a foreignexchange contract). A credit risk is a risk

that the bank will not be able to recover the moneyit is owed. The

risks inherent in a credit exposure are affected by the financial

strength of

the party owing money to the bank. The greater this is, the more

likely it is that the debt willbe paid or that the bank can, if

necessary, enforce repayment.

Credit risk is also affected by market factors that impact on

the value or cash flow of assetsthat are used as security for

loans. For example, if a bank has made a loan to a person to buya

house, and taken a mortgage on the house as security, movements in

the property markethave an influence on the likelihood of the bank

recovering all money owed to it. Even forunsecured loans or

contracts, market factors which affect the debtor's ability to pay

the bankcan impact on credit risk.

The calculation of credit exposures recognises and adjusts for

two factors:

y On-balance sheet credit exposures differ in their degree of

riskiness (e.g.Government Stock compared to personal loans).

Capital adequacy ratiocalculations recognise these differences by

requiring more capital to be heldagainst more risky exposures. This

is done by weighting credit exposures accordingto their degree of

riskiness. Abroad brush approach is taken to defining degrees

ofriskiness. The type of debtor and the type of credit exposures

serve as proxies fordegree of riskiness (e.g. Governments are

assumed to be more creditworthy thanindividuals, and residential

mortgages are assumed to be less risky than loans tocompanies). The

Reserve Bank defines seven credit exposure categories into

whichcredit exposures must be assigned for capital adequacy ratio

calculation purposes.

y Off-balance sheet contracts (e.g. guarantees, foreign exchange

and interest ratecontracts) also carry credit risks. As the amount

at risk is not always equal to thenominal principal amount of the

contract, off-balance sheet credit exposures arefirst converted to

a "credit equivalent amount". This is done by multiplying

thenominal principal amount by a factor which recognises the amount

of risk inherentin particular types of off-balance sheet credit

exposures. After deriving creditequivalent amounts for off-balance

sheet credit exposures, these are weightedaccording to the

riskiness of the counterparty, in the same way as on-balancesheet

credit exposures. Nine credit exposure categories are defined to

cover alltypes of off-balance sheet credit exposures. The credit

exposure categories and

-

8/2/2019 modifed sa

25/34

the risk weighting process are illustrated by the second step of

the calculationexample.

Minimum Capital Adequacy RatiosThe Basle Capital Accord sets

minimum capital adequacy ratios that supervisoryauthorities

are encouraged to apply. These are:y tier one capital to total

risk weighted credit exposures to be not less than 4 percent;y

total capital (i.e. tier one plus tier two less certain deductions)

to total risk weighted

credit exposures to be not less than 8 percent;

There are some further standards applicable to tier two

capital:

y tier two capital may not exceed 100 percent of tier one

capital;y lower tier two capital may not exceed 50 percent of tier

one capital;y lower tier two capital is amortised on a straight

line basis over the last five years

of its life.

The Reserve Bank will not register banks in Our country that do

not meet these standards- and maintaining the minimum standards is

always made a condition of registration.

y If the registered bank is incorporated in Our country, then

the minimum standardsapply to the financial reporting group of the

bank.

y If the registered bank is a branch of an overseas bank, then

it is the capitaladequacy ratios of the whole overseas bank (and

not the branch) which arerelevant. Overseas banks which operate as

branches are registered in Our countryon the condition that they

comply with the capital adequacy ratio requirementsimposed by the

financial authorities in their home country and that

theserequirements are no less than those recommended by the Basle

Capital Accord.

When a registered bank falls below the minimum requirements it

must present a plan to

the ReserveBank (which is publicly disclosed) aimed at restoring

capital adequacy ratiosto at least the minimum level required.

Even though a bank may have capital adequacy ratios above the

minimum levelsrecommended by the Basle Capital Accord, this is no

guarantee that the bank is "safe".Capital adequacy ratios are

concerned primarily with credit risks. There are also othertypes of

risks which are not recognised by capital adequacy ratios e.g..

inadequateinternal control systems could lead to large losses by

fraud, or losses could be made onthe trading of foreign exchange

and other types of financial instruments. Also capitaladequacy

ratios are only as good as the information on which they are based,

e.g. ifinadequate provisions have been made against problem loans,

then the capital adequacyratios will overstate the amount of losses

that the bank is able to absorb. Capital

adequacy ratios should not be interpreted as the only indicators

necessary to judge abank's financial soundness.

Calculation ExampleBecause off-balance sheet credit exposures

are included in calculations, capital adequacyratios cannot be

calculated by reference to the balance sheet alone. Even the

calculation ofcapital adequacy ratios to cover on-balance sheet

credit exposures usually cannot be done byusing published balance

sheets, as these will probably not provide sufficient detail about

whothe bank has lent to, or the issuers of securities held by the

bank. However, the disclosure

-

8/2/2019 modifed sa

26/34

statements of the bank should contain the information necessary

to confirm the bank's capitaladequacy ratio calculations. To

illustrate the process a bank goes through in calculating

itscapital adequacy ratios, a simple worked example is contained in

Figures 1 to 5. The steps inthe calculation are explained below.

The balance sheet information and the off-balance sheetcredit

exposures on which the calculations are based are set out in

Figures 1 and 2.

-

8/2/2019 modifed sa

27/34

First Step - Calculation ofCapital

The composition of the categories of capital is as follows:

Tier One Capital

In general, this comprises:y the ordinary share capital (or

equity) of the bank; andy audited revenue reserves e.g.. retained

earnings; lessy current year's losses;y future tax benefits;

and

y intangible assets, e.g. goodwill.

Upper Tier Two Capital

In general, this comprises:

y unaudited retained earnings;y

revaluation reserves;y general provisions for bad debts;y

perpetual cumulative preference shares (i.e. preference shares with

no maturity date

whose dividends accrue for future payment even if the bank's

financial condition doesnot support immediate payment);

y perpetual subordinated debt (i.e. debt with no maturity date

which ranks in prioritybehind all creditors except

shareholders).

Lower Tier Two Capital

In general, this comprises:

y subordinated debt with a term of at least 5 years;

y redeemable preference shares which may not be redeemed for at

least 5 years.

Total CapitalThis is the sum of tier 1 and tier 2 capital less

the following deductions:

y equity investments in subsidiaries;y shareholdings in other

banks that exceed 10 percent of that bank's capital;y unrealised

revaluation losses on securities holdings.

Figure 3 shows an example of a calculation of capital.

Figure 3

-

8/2/2019 modifed sa

28/34

Second Step - Calculation of Credit Exposures

On-Balance Sheet Exposures

The categories into which all credit exposures are assigned for

capital adequacy ratiopurposes, and the percentages the balance

sheet numbers are weighted by, are as follows:

Off-Balance Sheet Credit Exposures

(1) Calculation of Credit Equivalents

-

8/2/2019 modifed sa

29/34

Listed below are the categories of credit exposures, and their

associated "credit conversionfactor". The nominal principal amounts

in each category are multiplied by the creditconversion factor to

get a "credit equivalent amount":

The final category of off-balance sheet credit exposures, market

related contracts (i.e.interest rate and foreign exchange rate

contracts), is treated differently from the othercategories. Credit

equivalent amounts are calculated by adding the following:

(a)current exposure - this is the market value of a contract

i.e.. the amount the bank

could get by selling its rights under the contract to another

party (counted as zero forcontracts with a negative value); and

(b)potential exposure i.e.. an allowance for further changes in

the market value, which iscalculated as a percentage of the nominal

principal amount as follows:

Although the nominal principal amount of market related

contracts may be large, the creditequivalent amounts are usually

small, and so may add very little to the amount of creditexposures

to be risk weighted.

(2) Calculation of Risk Weighted Credit Exposures

The credit equivalent amounts of all off-balance sheet exposures

are multiplied by the samerisk weightings that apply to on-balance

sheet exposures (i.e. the weighting used depends on

-

8/2/2019 modifed sa

30/34

the type of counterparty), except that market related contracts

that would otherwise beweighted at 100 percent are weighted at 50

percent.

Figure 4 shows an example of a calculation of risk weighted

assets.

-

8/2/2019 modifed sa

31/34

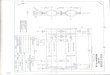

Figure 4 (Contd.)

-

8/2/2019 modifed sa

32/34

Third Step - Calculation of Capital Adequacy Ratios

Capital adequacy ratios are calculated by dividing tier one

capital and total capital by riskweighted credit exposures.Figure 5

shows an example of a calculation of capital adequacy ratios.

Conclusions

Capital adequacy ratios measure the amount of a bank's capital

in relation to the amount of

its risk weighted credit exposures. The risk weighting process

takes into account, in a stylisedway, the relative riskiness of

various types of credit exposures that banks have, andincorporates

the effect of off-balance sheet contracts on credit risk. The

higher the capitaladequacy ratios a bank has, the greater the level

of unexpected losses it can absorb beforebecoming insolvent.

The Basle Capital Accord is an international standard for the

calculation of capital adequacyratios. The Accord recommends

minimum capital adequacy ratios that banks should meet.

The Reserve Bank applies the minimum standards specified in the

Accord to banks registeredin Our country. This helps to promote

stability and efficiency in the financial system, andensures that

Our country banks comply with generally accepted international

standards.

-

8/2/2019 modifed sa

33/34

-

8/2/2019 modifed sa

34/34