Embed Size (px)

Citation preview

Building Momentum for Digital Disruption in Insurance

Raymond G. Farmer NAIC Vice President and Director, South Carolina Department of Insurance

MODERATOR

Peggy FuAssociate Director,

Market Conduct, Hong Kong Insurance

Authority

Andrew CandlandHead of Division, Insurance

Supervision Directorate, Central Bank of Ireland

Erika Bothma Program Director –

Hartford InsurTech Hub Powered by

Startupbootcamp

Sonja Larkin-ThorneConsumer Advocate

Mojgan LefebvreSenior Vice President and Chief Information Officer, Liberty Mutual

Global Specialty

Building momentum for digital disruption in insuranceNAIC International Forum, 14 May 2018

The regulator’s role

■ Given objectives and legal framework

■ Example – the Central Bank of Ireland’s Mission Statement: 'Safeguarding Stability, Protecting Consumers'

■ A balancing act

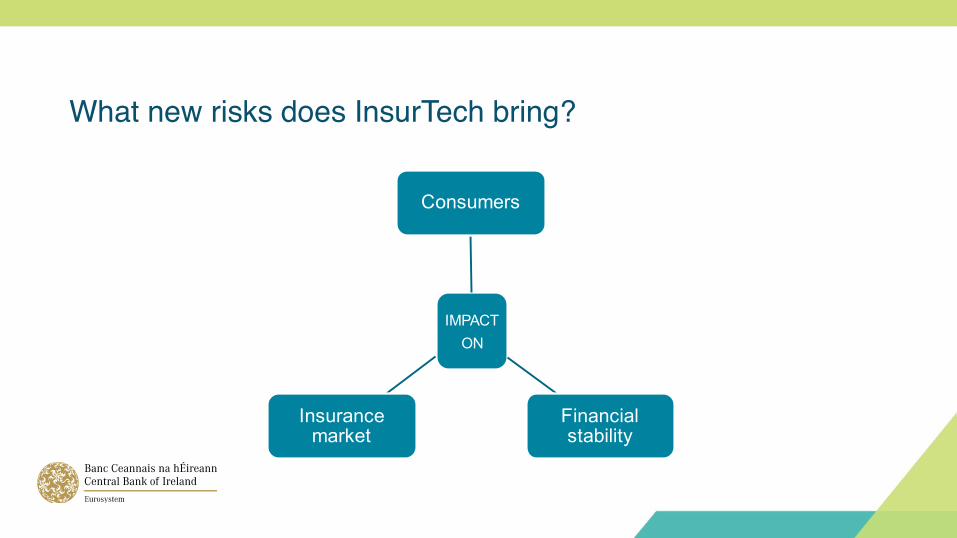

What new risks does InsurTech bring?

IMPACT ON

Consumers

Financial stability

Insurance market

Challenges to and responses by regulators

■ Not new, but very different

■ Ireland, Europe and the World

■ What’s in it for me?

NAIC International Insurance Forum Building Momentum for Digital Disruption in Insurance

14-15 May 2018 Washington D.C.

Peggy Fu

FinTech/Insurtech

• Seems like everyone in the insurance industry is talking about FinTech or Insurtech.

• But how much we really know about it? – Startups – Big data, mobile internet technology, blockchain technology, facial

recognition technology, ….. – IoTs like wearable devices for health insurance, sensors for home

and motor insurance, ……. – Use of AI to collect new data and chatbots to improve customer

experience – Data privacy and cyber security

Benefits to Customers

To name a few:

• Insurers are paying more attention to customer experience and improving their communication modes.

• Underwriters are able to gather more up-to-date information through technologies and to offer better policy terms to good customers.

• Emergence of online comparison platforms enhances market transparency which in turns drives market competition.

• Wider choices of insurance products and greater personalization of policies.

• Online submission of insurance claims speeds up processing of straightforward claims.

Potential Risks to Customers

• Whether customers accessing insurance product or claim information through online platforms especially mobile devices will pay sufficient attention to key terms and conditions?

• How customers can assure the products they buy online are suitable?

• Whether client services will be seriously disrupted due to issues such as technical problems where operations are highly automated?

• Whether customers are fully aware of the use of their personal data collected via technology like IoTs or used in blockchain technology?

• Whether customers understands the implication of unauthorized use of their personal data and data breach?

• Whether premiums for high-risk customers will be unaffordable?

Understanding of Development is Important

• Inherent risk of innovation – reliability, integrity and privacy risks

• Startups’ low level of awareness of regulatory and compliance requirements.

• Impact on customers – recognition of different reaction of different kinds of customers, in particular,

retail customers – vulnerable customers’ needs – consumer habits, expectations and preferences may change rapidly when new

technology emerges

• Readiness of insurers – senior management’s responsibility and security awareness of staff – internal controls to prevent data breaches and safeguards against cyber

attacks

Latest Developments in Hong Kong

• Insurance agents and brokers continue to be the major distribution channels but online insurance sales are expected to grow.

• Despite no material change in the major types of online insurance products (which are still mainly simple personal products such as travel, household, personal accident and term life insurance), the following changes are seen:

– user interface design for mobile websites is significantly improved; – development of user-friendly mobile apps; and – a wider choices of coverage to cater for different client needs;

to elevate customer experience.

Latest Developments in Hong Kong

• Emergence of more insurance mobile apps for different purposes: – selling of insurance products to the public directly; – assisting insurance intermediaries’ selling of insurance products; – enabling policyholders to check policy details; and – facilitating lodgment of claims by policyholders.

• Life insurers have increasingly equipped insurance agents with tablets loaded with proprietary software to record client information, conduct FNA (financial needs analysis), submit applications and perform necessary administrative tasks for issue of life policies.

• Use of GPS technology in helping save Mainland clients’ time to meet the physical presence requirements for procurement of life insurance.

Latest Developments in Hong Kong

• Digital KYC for online insurance application – Use of technologies for client identity verification:

• Document forensic algorithms • Facial recognition technology

• Investment in an established insurer by a giant tech firm to launch a digital insurer.

• Insurance comparison websites/apps with different business strategies and target clients:

– Selling of products/provision of advice to the public – Provision of product and other information to insurance

intermediaries (insurance agents/brokers)

Latest Developments in Hong Kong

• Fraud Prevention

– Insurance Claims Database • Focus on motor, medical and accident insurance at the initial

stage. • Collect and analyze claims data with a view to identifying

fraudulent insurance claims at an early stage. • Detect patterns of fraudulent insurance claims using big data

analytics technology to enable early preventive measures to be taken.

– E-Cover Notes • Fake motor insurance policies sold by fake insurers/insurance

intermediaries. • Inclusion of QR codes for verification of genuineness of motor

insurance policies using blockchain technology. • Facilitate checking by Transport Department and Police.

IA’s Response to FinTech/Insurtech Developments

• Insurtech Facilitation Team – Proactively assists startups (local and overseas) in understanding the regulatory

requirements relevant to their proposed operations relating to insurance. – Ascertain regulatory requirements which may be relaxed to facilitate digital

operations.

• Fast Track for applications authorization of new insurers using solely digital distribution channels

– Review of existing regulatory requirements relating to FNA to facilitate online distribution of certain endowment and universal life insurance products.

→Exemption to be granted if certain conditions are met.

• Insurtech Sandbox for pilot run of existing insurers’ digital operations – Review of existing regulatory requirements relating to benefit illustrations

provided to policyholders. →Requirements to be simplified if certain conditions are met.

IA’s Response to FinTech/Insurtech Developments

• Cybersecurity – Insurers are encouraged to join the Cyber Intelligence Sharing

Platform to share cyber incidents with other industry players.

• Conduct Requirements – Review of conduct requirements for online platforms:

• Adequate financial, human and technology resources • Adequate staff with sufficient expertise and understanding of

relevant technology and algorithms used • Proper procedures and internal controls for:

– Collecting and validating client information – Ensuring reasonableness of recommendation – Conducting regular reviews of recommendations given

on the platforms – Keeping proper audit trails and records

Thank You

Program Director – Hartford InsurTech Hub

Powered by Startupbootcamp

ERIKA BOTHMA

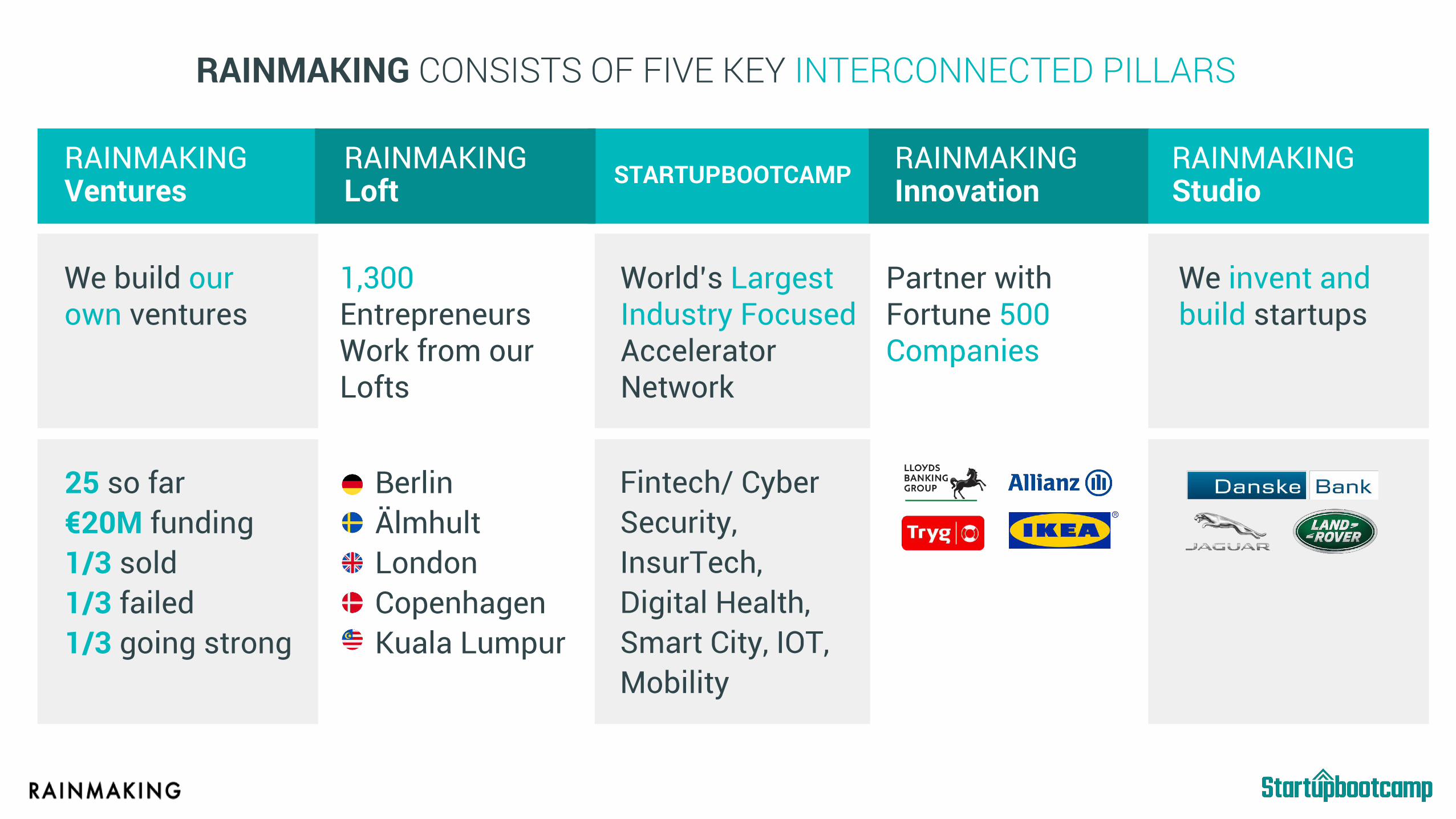

RAINMAKING CONSISTS OF FIVE KEY INTERCONNECTED PILLARS

RAINMAKING

Innovation

Partner with

Fortune 500

Companies

RAINMAKING

Studio

We invent and

build startups

STARTUPBOOTCAMP

World’s Largest

Industry Focused

Accelerator

Network

Fintech/ Cyber

Security,

InsurTech,

Digital Health,

Smart City, IOT,

Mobility

RAINMAKING

Ventures

We build our

own ventures

25 so far

€20M funding

1/3 sold

1/3 failed

1/3 going strong

RAINMAKING

Loft

1,300

Entrepreneurs

Work from our

Lofts

Berlin

Älmhult

London

Copenhagen

Kuala Lumpur

Miami

Mexico

City

Barcelona Rome

Amsterdam

Istanbul

Australia

San Francisco Hartford

Dubai

London

Berlin

New York

Mumbai

Chengdu

Singapore

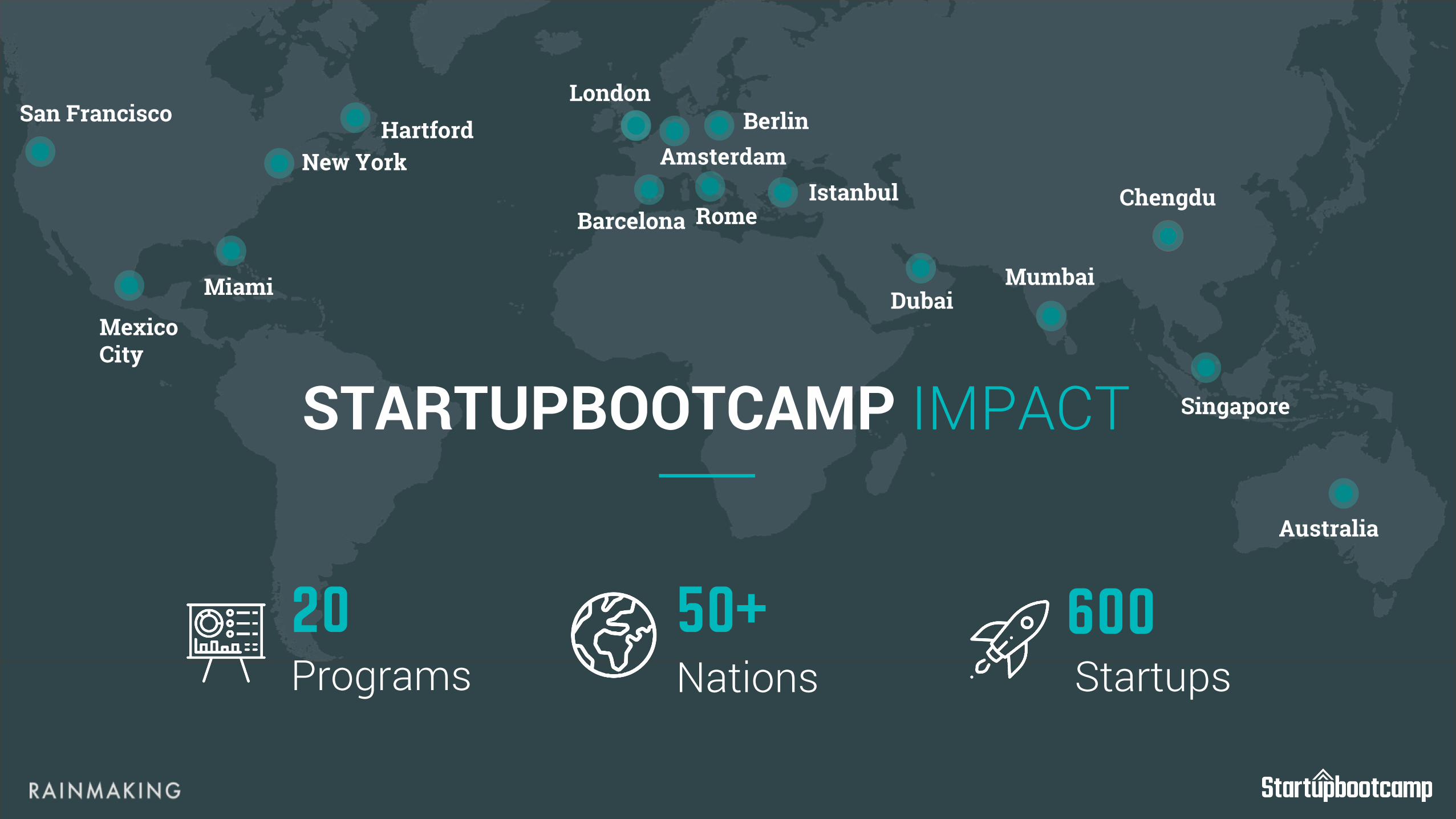

Programs20

Nations50+

Startups600

STARTUPBOOTCAMP IMPACT

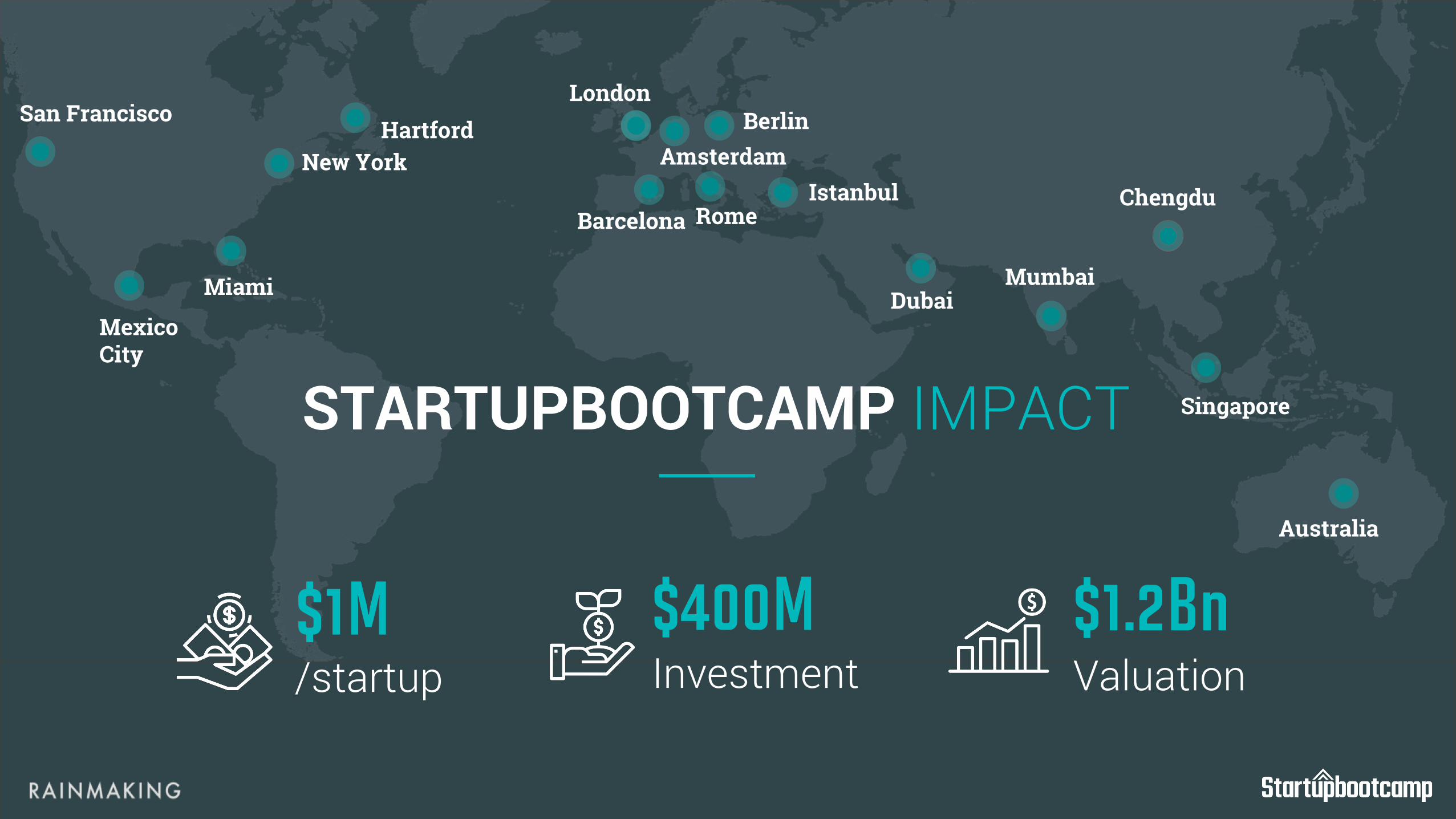

/startup$1M

Investment$400M

Valuation$1.2Bn

STARTUPBOOTCAMP IMPACT

Miami

Mexico

City

Barcelona Rome

Amsterdam

Istanbul

Australia

San Francisco Hartford

Dubai

London

Berlin

New York

Mumbai

Chengdu

Singapore

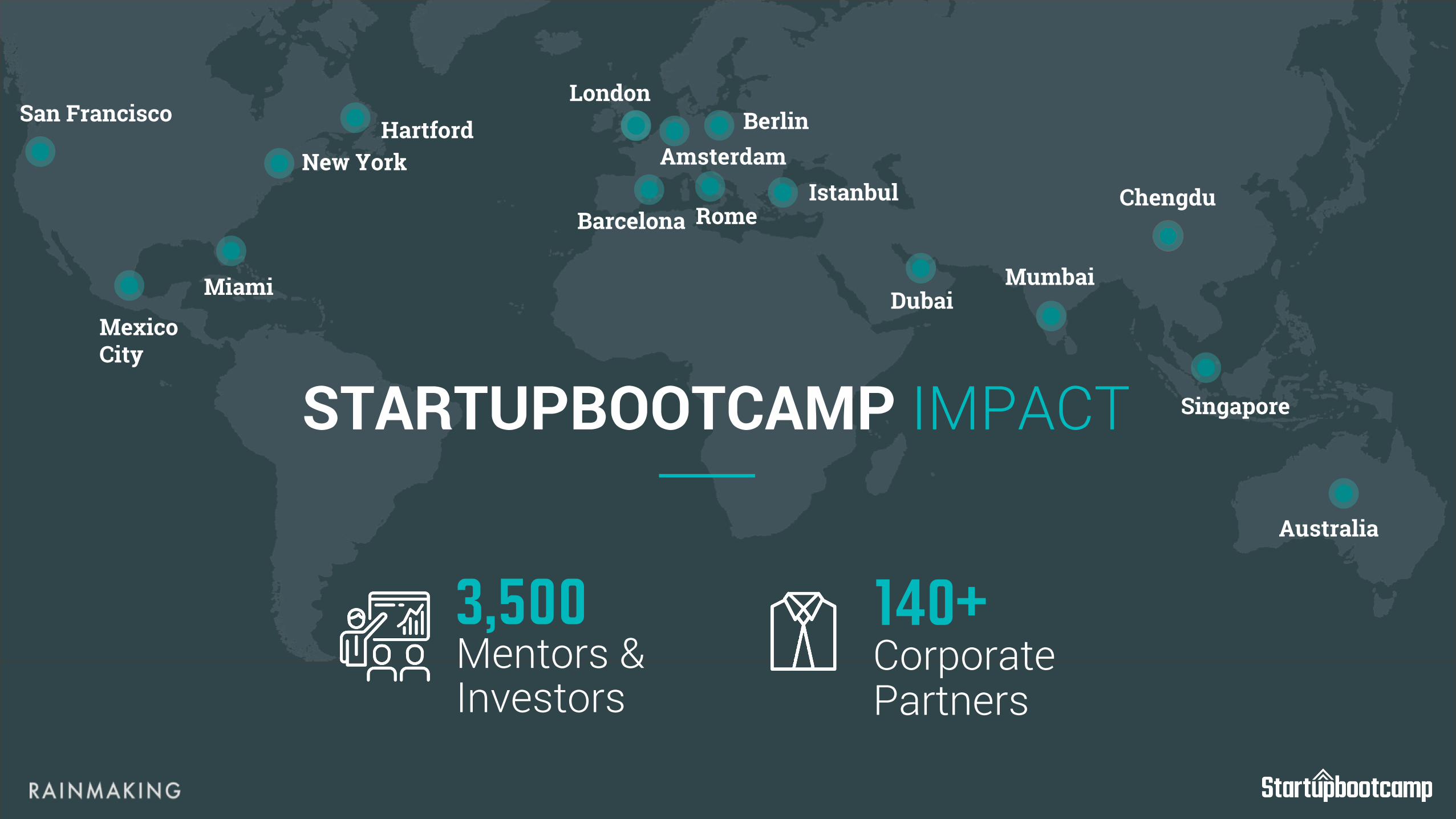

Mentors &Investors

3,500Corporate Partners

140+

STARTUPBOOTCAMP IMPACT

Miami

Mexico

City

Barcelona Rome

Amsterdam

Istanbul

Australia

San Francisco Hartford

Dubai

London

Berlin

New York

Mumbai

Chengdu

Singapore

Startupbootcamp -TODAY

OUR FINANCIAL SERVICES PARTNERSINSURTECH & FINTECH

Technology-enabled innovationTargeted at the insurance sector

New business models, applications, processes, productsEmerging technologies transforming insurance business

INSURTECH

INSURANCE VALUE CHAINS RESHUFFLED & RECONFIGURED

Technology is at the core of our world

Enabling seamless and frictionless experiences

AI BlockchainRoboticsCyber

Security

Internet of

Things

Sharing

Economy

API

InfrastructureOn Demand Internet First

Wealth TechLegal Tech Prop TechMed Tech

AREAS OF ACTIVITY

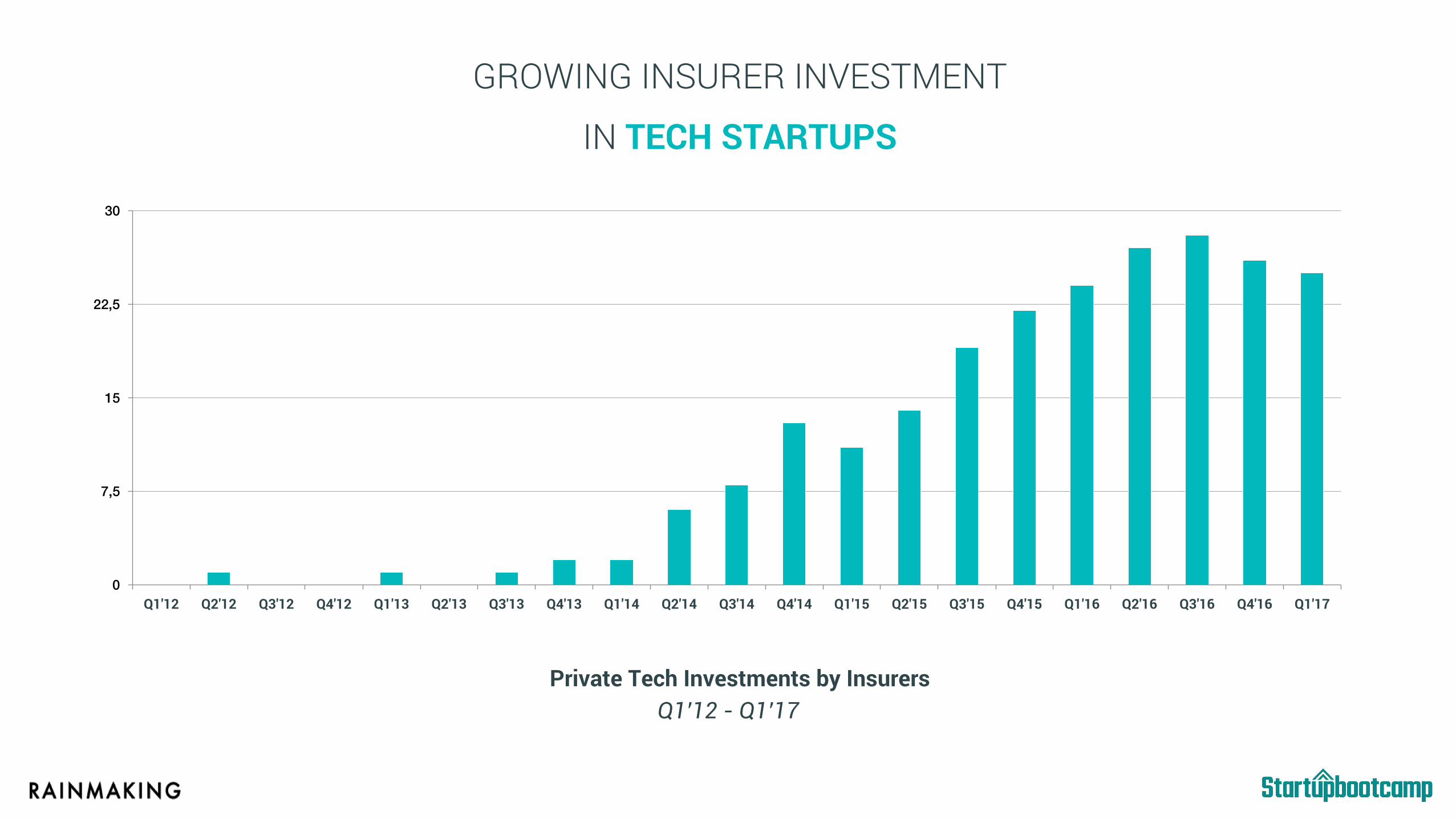

GROWING INSURER INVESTMENT

IN TECH STARTUPS

0

7,5

15

22,5

30

Q1'12 Q2'12 Q3'12 Q4'12 Q1'13 Q2'13 Q3'13 Q4'13 Q1'14 Q2'14 Q3'14 Q4'14 Q1'15 Q2'15 Q3'15 Q4'15 Q1'16 Q2'16 Q3'16 Q4'16 Q1'17

Private Tech Investments by InsurersQ1’12 - Q1’17

This represents around 30% of the total number of startups

$11Bn

Property & Casualty Life, Annuity & Retirement

PEER TO PEER

DISTRIBUTION

DATA & UNDERWRITING

INTERNET FIRST BUSINESSES

STARTUPS APPEARING ACROSSP&C AND L.A.R SECTORS

SHANGHAIGuoquan North Road

MEXICO CITYGoldsmith 40

MIAMI22nd Street

NEW YORK1412 Broadway

LONDON25 Luke Street

HARTFORD20 Church Street

MUMBAISitaram Jadhav Marg

SINGAPORE80 Robinson Road

SAN FRANCISCOAddress

COPENHAGENDanneskiold-Samsøes Allé

Program Director – Hartford InsurTech Hub

Powered by Startupbootcamp

ERIKA BOTHMA

2018 International Insurance Forum

Sonja Larkin-Thorne Consumer Advocate

May 14, 2018

Building Momentum for Digital Disruption in Insurance

“You do what you think is right and let the law catch up” Thurgood Marshall, First African American Associate Justice of the Supreme Court of the United States

“The policy of being too cautious is the greatest risk of all” Jawaharial Nehru, The first Prime Minister of India

Building Momentum for Digital Disruption in Insurance

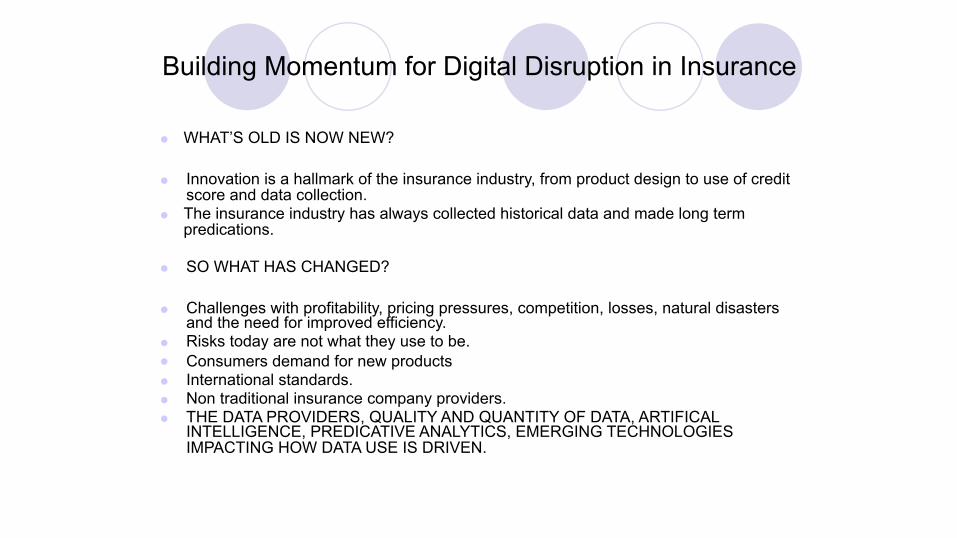

● WHAT’S OLD IS NOW NEW?

● Innovation is a hallmark of the insurance industry, from product design to use of credit score and data collection.

● The insurance industry has always collected historical data and made long term predications.

● SO WHAT HAS CHANGED?

● Challenges with profitability, pricing pressures, competition, losses, natural disasters and the need for improved efficiency.

● Risks today are not what they use to be. ● Consumers demand for new products ● International standards. ● Non traditional insurance company providers. ● THE DATA PROVIDERS, QUALITY AND QUANTITY OF DATA, ARTIFICAL

INTELLIGENCE, PREDICATIVE ANALYTICS, EMERGING TECHNOLOGIES IMPACTING HOW DATA USE IS DRIVEN.

Building Momentum for Digital Disruption in Insurance

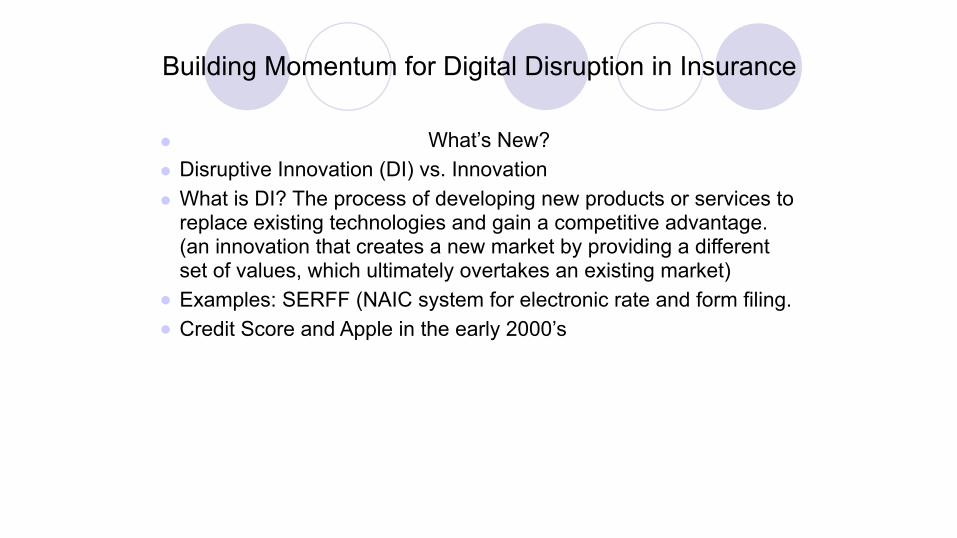

● What’s New? ● Disruptive Innovation (DI) vs. Innovation ● What is DI? The process of developing new products or services to

replace existing technologies and gain a competitive advantage. (an innovation that creates a new market by providing a different set of values, which ultimately overtakes an existing market)

● Examples: SERFF (NAIC system for electronic rate and form filing. ● Credit Score and Apple in the early 2000’s

Building Momentum for Digital Disruption in Insurance

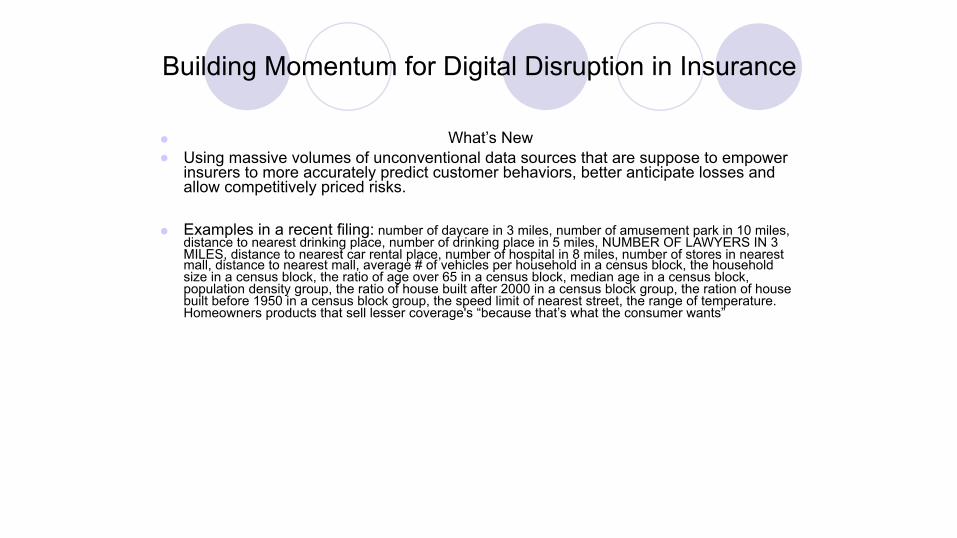

● What’s New ● Using massive volumes of unconventional data sources that are suppose to empower

insurers to more accurately predict customer behaviors, better anticipate losses and allow competitively priced risks.

● Examples in a recent filing: number of daycare in 3 miles, number of amusement park in 10 miles, distance to nearest drinking place, number of drinking place in 5 miles, NUMBER OF LAWYERS IN 3 MILES, distance to nearest car rental place, number of hospital in 8 miles, number of stores in nearest mall, distance to nearest mall, average # of vehicles per household in a census block, the household size in a census block, the ratio of age over 65 in a census block, median age in a census block, population density group, the ratio of house built after 2000 in a census block group, the ration of house built before 1950 in a census block group, the speed limit of nearest street, the range of temperature. Homeowners products that sell lesser coverage's “because that’s what the consumer wants”

Building Momentum for Digital Disruption in Insurance

● CONSUMER and REGULATORY CONCERN’S

● Lack of TRANSPARENCY, consumer EDUCATION and the ability to SHOP and COMPARE the PRICE and Product being purchase.

NAIC: Building Momentum for Digital Disruption in Insurance 05.14.18

Mojgan LefebvreSVP & CIO, Global Risk Solutions Liberty Mutual Insurance

SVP & CIO, Liberty Mutual, Global Risk Solutions SVP & CIO, Liberty Mutual, Global Specialty SVP & CIO, Liberty Mutual, Commercial Insurance

CIO, bioMerieux

CIO, TeleTech

Team Leader, Bain

Developer, BellSouth

Lived and worked in US, France, Tunisia, Israel, Russia and Iran

Mojgan Lefebvre Liberty Mutual

Large, globally-diversified P&C insurance carrier

30 Countries 55K Employees $122B Assets

$37.6B Revenue #75 Fortune 100

Market Trends

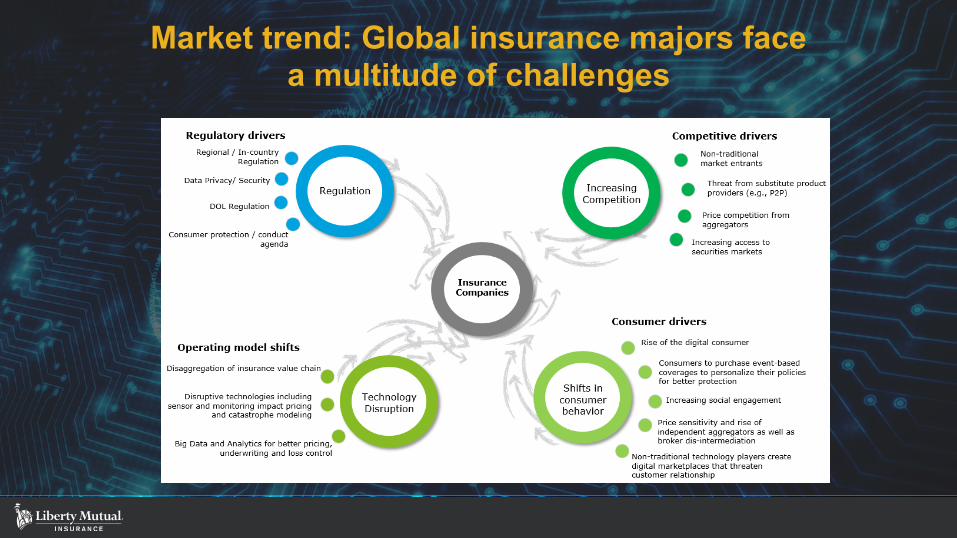

Market trend: Global insurance majors face a multitude of challenges

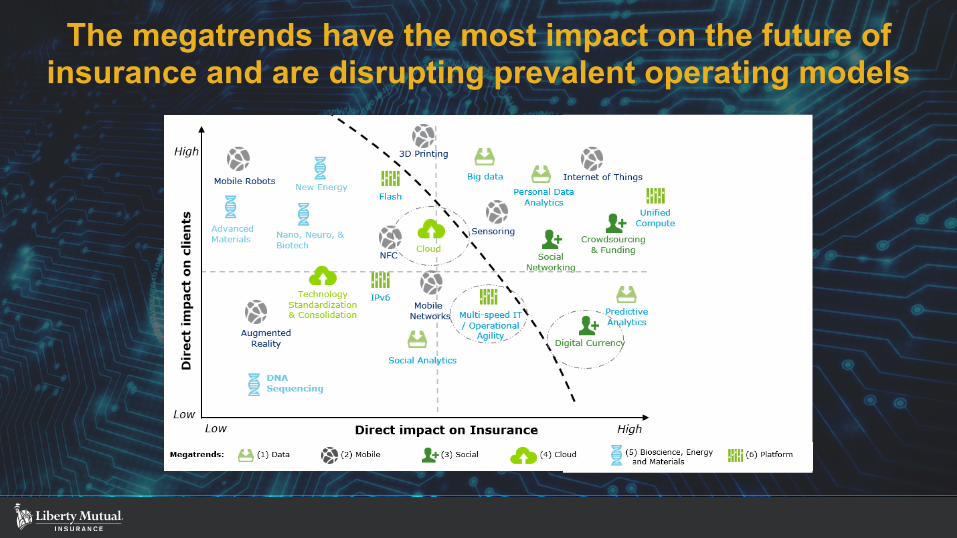

The megatrends have the most impact on the future of insurance and are disrupting prevalent operating models

$352B $3B$20B $20B

Customers will experience shifts in risk, from human to machine, as well as emergence of new risks

Future of risk where exponential change and disruption are creating opportunity

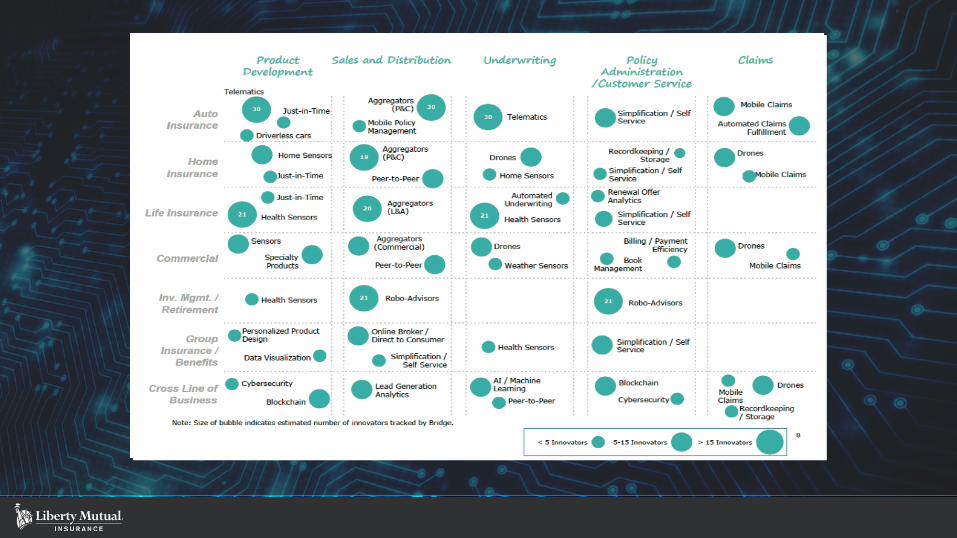

P&C carriers are exhibiting an increased focus on leveraging technology, data, and analytics to boost

profits and satisfy customers

Emphasis on analytics to

improve performance

Exploration / adoption of

the ‘Internet of Things’

Focus on customer

experience improvement

Investment in technology to

refine operating

model

Slow evolution of distribution

channels

Changing market

dynamics and demographics

Positioning for change in the industry

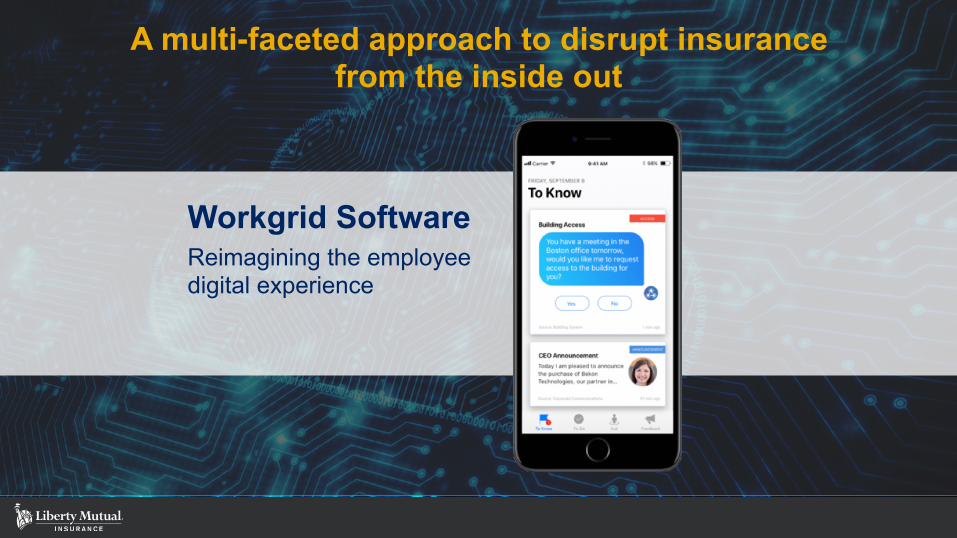

A multi-faceted approach to disrupt insurance from the inside out

Workgrid Software Reimagining the employee digital experience

Telematics enable us to provide an on-demand, personalized offering

ByMile™ enables continuous customer engagement paired with dynamic, behavior-based pricing.

Emerging Technology Exploration

Blockchain – exploring use cases within reinsurance and subrogation AI-based deep learning engine improves billing accuracy Robotics Process Automation (Blue Prism) to automate manual tasks

Increased focus on customer journey and experience

Increased focus on the customer journey and experience Our journey towards agile

#TechAtLiberty

@mojganlefebvre