Embed Size (px)

Citation preview

Corporate Sector

Summer Exam-2016

ModelSolutions

MODEL SOLUTIONS – DISCLAIMER

INTRODUCTION

The Model Solutions are provided to students for clear understanding of relevant subject and ithelps them to prepare for their examinations in organized way.

These Model Solutions are prepared only for the guidance of students that how they shouldattempt the questions. The solutions are not meant for assessment criteria in the same patternmentioned in the Model Solution. The purpose of Model Solution is only to guide the students intheir future studies for appearing in examination.

The students should use these Model Solutions as a study aid. These have been prepared by theprofessionals on the basis of the International Standards and laws applicable at the relevant time.These solutions will not be updated with changes in laws or Standards, subsequently. The laws,standards and syllabus of the relevant time would be applicable. PIPFA is not supposed torespond to individual queries from students or any other person regarding the Model Solutions.

DISCLAIMER

The Model Solutions have been developed by the professionals, based on standards, laws, rules,regulations, theories and practices as applicable on the date of that particular examination. Nosubsequent change will be applicable on the past papers solutions.

Further, PIPFA is not liable in any way for an answer being solved in some other way orotherwise of the Model Solution nor would it carry out any correspondence in this regard.

PIPFA does not take responsibility for any deviation of views, opinion or solution suggested byany other person or faculty or stake holders. PIPFA assumes no responsibility for the errors oromissions in the suggested answers. Errors or omissions, if noticed, should be brought to thenotice of the Executive Director for information.

If you are not the intended recipient, you are hereby notified that any dissemination, copying,distributing, commenting or printing of these solutions is strictly prohibited.

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

BusinessEconomics

(Level-2)

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

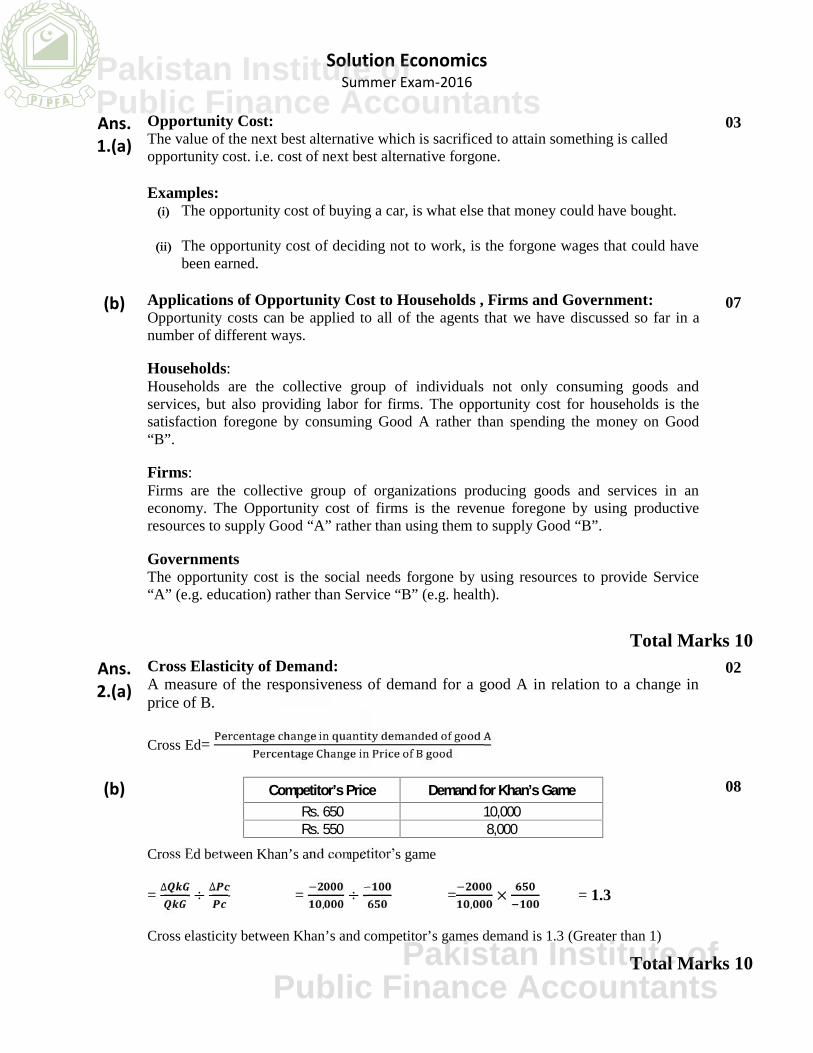

Solution EconomicsSummer Exam-2016

Ans.1.(a)

Opportunity Cost:The value of the next best alternative which is sacrificed to attain something is calledopportunity cost. i.e. cost of next best alternative forgone.

Examples:(i) The opportunity cost of buying a car, is what else that money could have bought.

(ii) The opportunity cost of deciding not to work, is the forgone wages that could havebeen earned.

03

(b) Applications of Opportunity Cost to Households , Firms and Government:Opportunity costs can be applied to all of the agents that we have discussed so far in anumber of different ways.

Households:Households are the collective group of individuals not only consuming goods andservices, but also providing labor for firms. The opportunity cost for households is thesatisfaction foregone by consuming Good A rather than spending the money on Good“B”.

Firms:Firms are the collective group of organizations producing goods and services in aneconomy. The Opportunity cost of firms is the revenue foregone by using productiveresources to supply Good “A” rather than using them to supply Good “B”.

GovernmentsThe opportunity cost is the social needs forgone by using resources to provide Service“A” (e.g. education) rather than Service “B” (e.g. health).

07

Total Marks 10

Ans.2.(a)

Cross Elasticity of Demand:A measure of the responsiveness of demand for a good A in relation to a change inprice of B.

Cross Ed=

02

(b) Competitor’s Price Demand for Khan’s GameRs. 650 10,000Rs. 550 8,000

Cross Ed between Khan’s and competitor’s game

=∆ ÷ ∆ = , ÷ = , × = 1.3

Cross elasticity between Khan’s and competitor’s games demand is 1.3 (Greater than 1)

08

Total Marks 10

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution EconomicsSummer Exam-2016

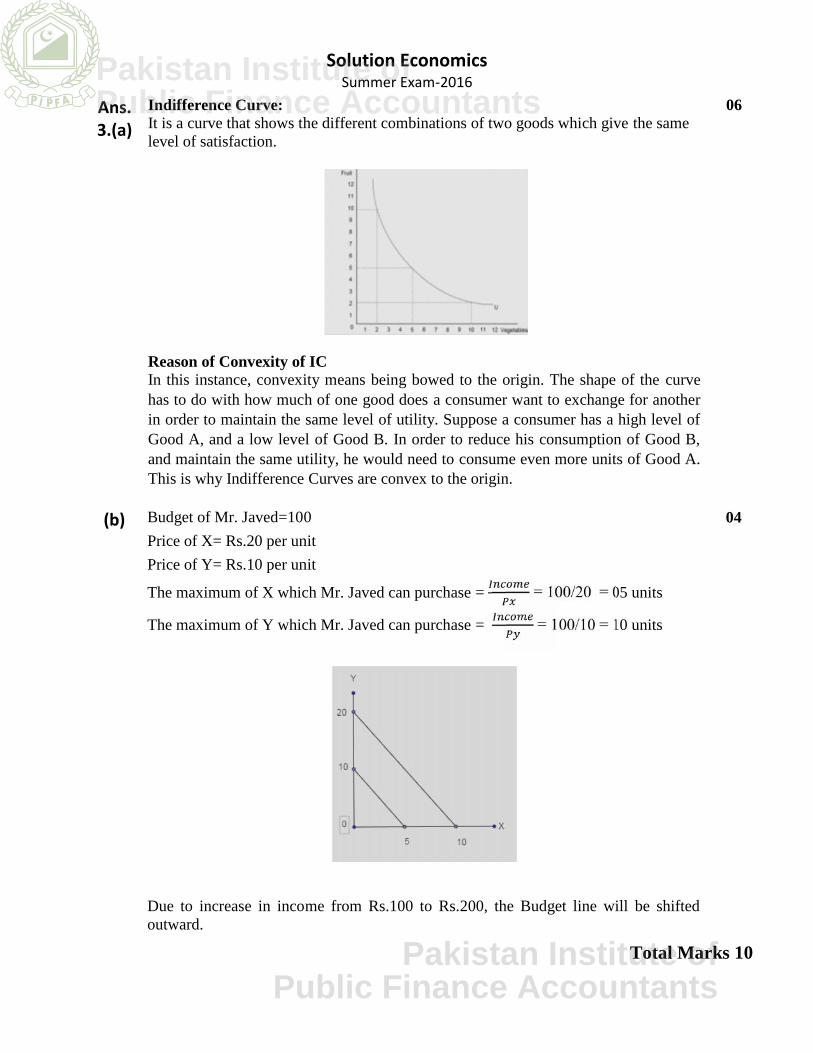

Ans.3.(a)

Indifference Curve:It is a curve that shows the different combinations of two goods which give the samelevel of satisfaction.

Reason of Convexity of ICIn this instance, convexity means being bowed to the origin. The shape of the curvehas to do with how much of one good does a consumer want to exchange for anotherin order to maintain the same level of utility. Suppose a consumer has a high level ofGood A, and a low level of Good B. In order to reduce his consumption of Good B,and maintain the same utility, he would need to consume even more units of Good A.This is why Indifference Curves are convex to the origin.

06

(b) Budget of Mr. Javed=100

Price of X= Rs.20 per unit

Price of Y= Rs.10 per unit

The maximum of X which Mr. Javed can purchase = = 100/20 = 05 units

The maximum of Y which Mr. Javed can purchase = = 100/10 = 10 units

Due to increase in income from Rs.100 to Rs.200, the Budget line will be shiftedoutward.

04

Total Marks 10

Solution EconomicsSummer Exam-2016

Ans.3.(a)

Indifference Curve:It is a curve that shows the different combinations of two goods which give the samelevel of satisfaction.

Reason of Convexity of ICIn this instance, convexity means being bowed to the origin. The shape of the curvehas to do with how much of one good does a consumer want to exchange for anotherin order to maintain the same level of utility. Suppose a consumer has a high level ofGood A, and a low level of Good B. In order to reduce his consumption of Good B,and maintain the same utility, he would need to consume even more units of Good A.This is why Indifference Curves are convex to the origin.

06

(b) Budget of Mr. Javed=100

Price of X= Rs.20 per unit

Price of Y= Rs.10 per unit

The maximum of X which Mr. Javed can purchase = = 100/20 = 05 units

The maximum of Y which Mr. Javed can purchase = = 100/10 = 10 units

Due to increase in income from Rs.100 to Rs.200, the Budget line will be shiftedoutward.

04

Total Marks 10

Solution EconomicsSummer Exam-2016

Ans.3.(a)

Indifference Curve:It is a curve that shows the different combinations of two goods which give the samelevel of satisfaction.

Reason of Convexity of ICIn this instance, convexity means being bowed to the origin. The shape of the curvehas to do with how much of one good does a consumer want to exchange for anotherin order to maintain the same level of utility. Suppose a consumer has a high level ofGood A, and a low level of Good B. In order to reduce his consumption of Good B,and maintain the same utility, he would need to consume even more units of Good A.This is why Indifference Curves are convex to the origin.

06

(b) Budget of Mr. Javed=100

Price of X= Rs.20 per unit

Price of Y= Rs.10 per unit

The maximum of X which Mr. Javed can purchase = = 100/20 = 05 units

The maximum of Y which Mr. Javed can purchase = = 100/10 = 10 units

Due to increase in income from Rs.100 to Rs.200, the Budget line will be shiftedoutward.

04

Total Marks 10

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution EconomicsSummer Exam-2016

Ans.4.(a)

Price discrimination:Price discrimination is a microeconomic pricing strategy where identical or largelysimilar goods or services are transacted at different prices by the same providerin different markets. Discount in fee and concession to soldier families in joy land arethe examples of price discrimination. i.e. Charging different prices for the sameproduct with different persons, places or times.

04

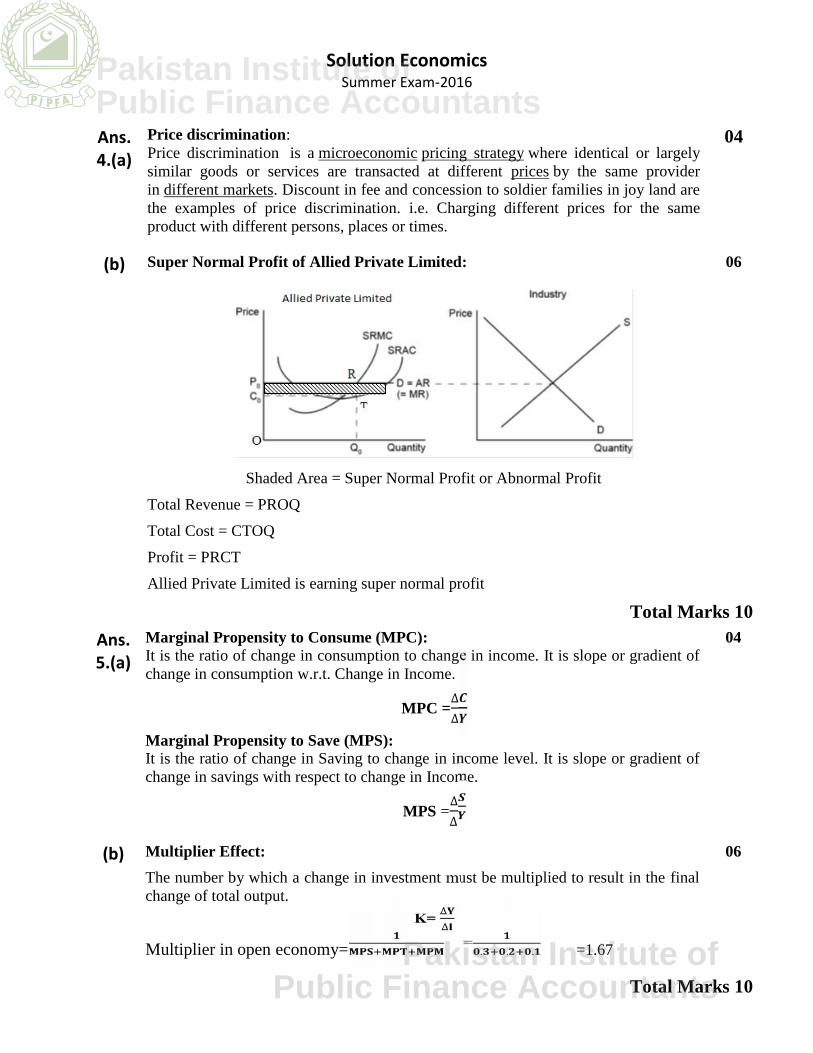

(b) Super Normal Profit of Allied Private Limited:

Shaded Area = Super Normal Profit or Abnormal Profit

Total Revenue = PROQ

Total Cost = CTOQ

Profit = PRCT

Allied Private Limited is earning super normal profit

06

Total Marks 10

Ans.5.(a)

Marginal Propensity to Consume (MPC):It is the ratio of change in consumption to change in income. It is slope or gradient ofchange in consumption w.r.t. Change in Income.

MPC =∆∆

Marginal Propensity to Save (MPS):It is the ratio of change in Saving to change in income level. It is slope or gradient ofchange in savings with respect to change in Income.

MPS =∆∆

04

(b) Multiplier Effect:

The number by which a change in investment must be multiplied to result in the finalchange of total output.

K=∆∆

Multiplier in open economy= = . . . =1.67

06

Total Marks 10

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution EconomicsSummer Exam-2016

Ans.6.(a)

Direct Tax:A Tax paid directly to the Government by the person on which it was imposed. Themain example of this is income tax. From a government’s perspective, the followingare the advantages of Direct Tax. Examples are Property Tax, Wealth Tax and CapitalGain Tax.

Advantages:

Cost of collection is low:Meaning it is an economical way of raising revenue, and saving expense.

Relative certainty:The Government can estimate how much it will receive allowing better planning ofprojects.

Flexible:If a government needs to raise revenues quickly, it can do so by raising Direct Taxes.

05

(b) Fiscal policy:

Policies undertaken by a government to influence macroeconomic conditions, andtherefore economic activity, through the use of taxation and spending.

The main objectives of fiscal policy are:

1. Keep Inflation Low

2. Keep Employment High

3. Steady Economic Growth

4. Equilibrium in Balances of Payments

05

Total Marks 10

Ans.7.(i)

Gross Domestic Product (GDP)GDP= C+I+G+(X-M)=20, 500 + 4,920+ 8,000+(7,450-6,340) =Rs. 34,530 million

03

(ii) Gross National Product (GNP)GNP= GDP+ Net Foreign Income= 34,530+ 1,500 = Rs. 36,030 million

02

(iii) Net National Product. (NNP)NNP= GNP- Depreciation of capital= 36,030-1,830 = Rs. 34,200 million

02

(iv) GDP at Factor CostGDP at factor cost = GDP at Market Prices – Indirect Tax + Subsidies= 34,530-3,260+500 = Rs. 31,77 million

03

Total Marks 10

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution EconomicsSummer Exam-2016

Ans.8.

(a)(i)

Open Market Operation:

The Central Bank can buy or sell Government Securities on the open market, tochange the level of reserves that are held by Commercial Banks. This action ofCentral Bank is called Open Market Operation.

02

(ii) Change in Reserve Ratio:

Every Commercial Bank has to keep reserves to meet the cash demand of depositors.In order that the reserves are kept safe, Commercial Banks will have them depositedat the central bank. This minimum reserve ratio is fixed by Central Bank. Bymanipulating this Reserve Central Bank controls the money supply and aggregatedemand.

02

(b) Suggestion to correct the current Account Deficit

1. Deflation: By bringing down the price level domestically, this can increasethe attractiveness of goods on the international market, thereby increasingexports.

2. Exchange control: In an extreme version, a monetary authority maycommand that exporters relinquish foreign exchange reserves to the centralbank. This has the effect of restricting the level of imports that are possible.

3. Tariffs: These are duties placed upon imports. This directly increases theprice of imports, making them less attractive to the domestic market. This alsogives domestic suppliers more protection to increase the supply of their owngoods.

06

Total Marks 10

Ans.9.

(a)(i)

Common Stock:

An instrument issued by companies that can be obtained via the primary or secondarymarket. Investment in the business means part-ownership of the company, and alsorights and privileges – such as voting power, and the ability to hold a position. Aninvestor in debt is entitled to interest payments; the equity holder may or may not bepaid dividend, depending on the company’s policy. There is a high risk factorinvolved, as the price of the stock can fluctuate greatly. Holders of the instrumentrank at the bottom of the scale if the company were to go into liquidation.

03

(ii) Preference Shares:

An instrument issued by companies that rank higher than common stock in terms ofscale of preference. They possess the same characteristics as equity in that its value isbased upon the share price fluctuating. However it also acts similar to debtinstrument, in those dividends are fixed, and the holder does not hold any votingrights. In case of liquidation of a company, preferred shared are preferred overcommon stocks.

03

(b) Commercial Banks create credit through advancing loans. The capacity of their creditcreation depends upon the money or credit multiplier. And the credit multiplierfurther depends upon the reserve ratio.

The multiple of credit that can be created by an initial deposit is:Money multiplier=1/RR

04

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution EconomicsSummer Exam-2016

Reserve Ratio:The portion of depositors’ funds that a bank must keep for immediate delivery to itsowner. The greater the reserve ratio, the lesser will be the amount of credit created bythe commercial banks. And the lesser will be the reserve ratio, the greater will be theamount of credit. There is inverse relation between Reserve Ratio & Credit Creation.

For example if initial deposit is Rs. 100 and RR is 10%, then

Total credit creation= 1/10% * 100= Rs. 1000

And if reserve ratio increases to 20% then

Total Credit creation=1/20% *100= Rs. 500

Total Marks 10

Ans.10.(i)

Foreign Exchange Rate

The foreign exchange rate is the price of one currency expressed in terms of anothercurrency.

02

(ii) Demand for Money

Total amount of money which people prefer to hold in cash or liquid form is calleddemand for money.3 Motives are Transactionary Motive, Speculative Motive andPrecautionary Motive.

02

(iii) Balance of Trade

It is the difference between the monetary value of exports and imports of tangiblegoods in an economy over a certain period, measured in the currency of that economyA positive balance is known as a trade surplus and negative is trade deficit.

02

(iv) Consumer Credit

A Consumer Credit agreement often occurs between a retailer and a consumer. Inexchange for store credit (i.e. currency to spend at the establishment) a consumer canpay the amount back over a certain period of time.

02

(v) Capital Market

The Financial Market which is largely used to raise long-term finance (more than ayear) and capital is called Capital Market. There are a number of different instrumentsthat can be bought or sold. These broadly fit into two categories: Debt and Equity.

02

Total Marks 10

*****************************

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

BusinessLaws

(Level-2)

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Business LawsSummer Exam-2016

Ans.1.

Alternate Dispute Resolution is any type of procedure of combination of proceduresvoluntarily used to resolve issues in controversy, other than court based adjudication.e.g. Mediation, Conciliation, Arbitration.

02

Advantages of ADR

i) Speedy.Arbitration is often faster than litigation in court.

ii) Cheaper and FlexibleArbitration can be cheaper and more flexible for businesses.

iii) Privacy.The public and the press have no right to attend a hearing before an arbitrator.

iv) Appeal.In most legal systems, there are very limited avenues for appeal of an arbitralaward.

v) Service of an expert.The parties may choose the person who is an expert in the particularcommercial field that they are in to settle their dispute.

(one mark each for any three correct answers)

03

Disadvantages of ADR

i) AppealLimited Avenue for appeal means that an erroneous decision cannot be easilyoverturned.

ii) Expensive.in countries where the cost of court action is not so high this might be moreexpensive to go to arbitration.

iii) Application of law.Rules of applicable law are not necessarily binding on the arbitrators, althoughthey cannot disregard the law.

iv) Delay.When there are multiple arbitrators on the panel, manage their schedules forhearing dates in long cases can lead to delays.

(one mark each for any three correct answers)

03

Total Marks 08

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Business LawsSummer Exam-2016

Ans.2.(a)

Baber can recover the amount of water charges as this is quasi contract situation aspayment by interested person as discussed below.

Payment by interested personA person, who is interested in the payment of money which another is bound by lawto pay, and who therefore pays it, is entitled to be reimbursed by the other.Thus the essential requirement of the section is:

The payment made should be bona fide for the protection of one’s interest.

The payment should not be a voluntary one.

The payment must be such as the other party was bound by law to pay.

0101

01

01

01

01

(b) Differences between contract of indemnity and contract of guarantee.

S. No. Contract of indemnity Contract of guarantee

1. Number of partiesThere are two parties, indemnifier andindemnity holder.

There are three parties, principaldebtor, creditor and surety.

2. Number of contractsThere is only one contract. There are three contracts.

3. Object.The indemnifier undertakes to save theindemnity holder from any loss.

The surety undertakes for thepayment of debts of principaldebtor in case of his default.

4. Nature of liabilityThe liability of indemnifier is primary andunconditional.

The liability of surety issecondary and conditional andco-extensive.

5. Commencement of liabilityThe liability arises only on the happening ofa contingency.

The liability arises only on thenon-performance of an existingpromise or non-payment of anexisting debt.

6. Right to sueThe indemnifier cannot sue a third party inhis own name because of absence of privityof contract between him and third party.

A surety, on discharging the debtof principal debtor, can sue theprincipal debtor in his own name.

(1.5 mark for each correct identification with maximum of 06 marks)

06

Total Marks 12

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Business LawsSummer Exam-2016

Ans.3.(a)

i) Wrong 0.75ii) Correct 0.75iii) Wrong 0.75iv) Wrong 0.75v) Wrong 0.75vi) Correct 0.75vii) Correct 0.75viii) Wrong 0.75

(b) Following are the cases where suit for specific performance is not maintainablewhere:

Monetary compensation is considered as an adequate remedy. Contract is of personal nature, e.g. contract of services. Court cannot supervise the performance of the contract e.g. construction of

building. One of the parties is a minor. Contract is inequitable to either party.

(one mark for each correct answers with maximum of four)

04

Total Marks 10

Ans.4.(a)

Yes supplier can sue all three partners jointly or sue B alone.

Every partner is liable jointly with all the other partners and also severally meansseparately, to third parties for all acts of the firm done while he is a partner. The thirdparty may take legal action for non-payment of a debt or losses incurred as a result ofa breach of contract against.

All the partners jointly, or Any individual partner A, B or C

If supplier chooses to sue B personally, and succeeds with his claims, B will berequired to pay the supplier. It will then be for B to obtain from his partners A & Ctheir share of the liability that they now owe. i.e. he will recover Rs. 50,000 each fromA & C.

02

01

0101

0101

(b) The mandatory duties of a partner that cannot be changed by an agreement are;

i) Duty to be just and faithful.ii) Duty to carry on business to the greatest common advantage.iii) Duty to render true accounts.iv) Duty to provide full information.v) Duty to indemnify for loss caused by fraud.vi) Duty to be liable jointly and severally.vii) Duty to act within authority.viii) Duty in case of emergency.

(0.5 mark for each correct answer with maximum 03)

03

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Business LawsSummer Exam-2016

(c) Where a partner has died or has ceased to be a partner by retirement, expulsion,insolvency or any other cause, the surviving or continuing partners may carry on thebusiness with the property of the firm without any final settlement of accounts asbetween them and the outgoing partner. In such a case in the absence of a contract tothe contrary, legal representative of the deceased partner or the outgoing partner, isentitled at his option to:

Such share of the profits as in proportionate to his share in the property of thefirm or

Interest at the rate of 6% on the amount of his share in the property of the firmprovided continuing partners do not settle accounts.

01

01

1.5

1.5

Total Marks 15

Ans.5.(a)

Bela will have to bear the loss as discussed below.

Where there is an unconditional contract for the sale of special goods in a deliverablestate, the property in the goods passes to the buyer when the contract is made, and it isimmaterial whether the time of payment of the price or time of delivery of the goods,or both, is postponed. It is a case of bailment as well.

01

010101

(b) Subject to the provisions of this Act and of any law for the time being in force,notwithstanding that the property in the goods may have passed to the buyer, theunpaid seller of goods, as such, has by implication of law.

a) A lien on the goods for the period while he is in possession of them,b) In case of the insolvency of the buyer a right of stopping the goods in transit

after he has parted with the possession of them.c) A right of re-sale.

where the property in goods has not passed to the buyer, the unpaid seller has, inaddition to his other remedies, a right of withholding delivery similar to and co-extensive with his rights of lien and stoppage in transit where the property has passedto the buyer.

01

0101

01

0101

Total Marks 10

Ans.6.(a)

Raja and Rehan should apply to Commission to get registered and work as a limitedliability company without using the word limited.

Restrictions Such Association shall apply its profits, if any, or other income in promoting

its objects, and

Such Association shall prohibit the payment of any dividend to its members.

01

01

01

Privileges and benefitsThe association shall on registration enjoy all the privileges of a limited companyand be subject to all its obligations, except those of using the word or words“Limited”, “(Private) Limited” or “Guarantee) Limited”, as the case may be, aspart of its name.

01

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Business LawsSummer Exam-2016

(b) Such association may be set up for any of the following purposes.

Commerce, Art, Science, Religion, Sports, Social services, Charity or Any other useful object.

(0.5 mark for any six correct answer)

03

(c) Zee Foods Limited can change its name by passing a special resolution and obtainingwritten permission of the registrar for the new name.

02

Upon the change of name, the registrar shall enter the new name on the register inplace of the former name and shall issue a ‘Certificate of Incorporation on change ofname’. On the issue of this certificate, the change of name shall be complete.

02

After the change of name, the former shall also be mentioned for one year from thedate of issue of the certificate outside every office or place of business of the companyand on every document and notice of the company.

02

The change of name shall not affect any legal proceedings that might havecommenced by or against the company under its former name. It would also not affectthe rights and obligations of the company.

02

Total Marks 15

Ans.7.(a)

The books containing the minutes of proceedings of the general meetings shall beopen to inspection by members for at least two hours on each day without chargeduring the business hours.Members of the company can demand a certified copy of the minutes of generalmeeting which the company shall provide to him within seven working days of receiptof his request.

02

02

(b) Directors shall exercise the following powers by ‘passing a resolution I boardmeeting:

To call the uncalled an unpaid share capital of the company. To issue shares, debentures or other redeemable capital or to otherwise borrow

money or invest the funds of the company. To make loans, provided in case of banking companies , the acceptance of

deposits and other amounts from account holders and placements of own fundsin other banking companies shall not be considered as incurring or making of aloan.

To approve annual and periodical accounts and to approve bonus foremployees.

06

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Business LawsSummer Exam-2016

To incur capital expenditure exceeding or undertake leasing obligationsexceeding Rupee one million or to sell/dispose of assets having book valueexceeding Rupees one hundred thousand.

To undertake leasing obligation exceeding one million rupees. To declare interim dividend. To authorize any of the following for entering into transactions with the

company.

Director of the company. Partnership firm in which director of the company is a partner. Private Company in which director of the company is a director.

If the amount is material as per generally accepted accounting principles. To write off bad debts. To write of inventories and other assets.

(one mark for each correct answer with maximum of 06 marks)

Total Marks 10

Ans.8.

(i)

First Chief ExecutiveDirectors shall appoint first chief executive within fifteen days of the date ofincorporation or right on the day of commencement of the business whichever isearlier.

First Chief Executive can be appointed for a period of maximum up to the first AGM.He may earlier resign or be removed from his office.

010101

01

(ii) Removal of Chief ExecutiveChief Executive can be removed through any of the following modes at any point intime regardless of any provisions in the articles of association or in his appointment tothe contrary.

by passing a special resolution in general meeting of the company or by passing a resolution of board of directors with there at least three fourth

majority of the directors.

01

1.51.5

(iii) Company is required to file all special resolutions passed by it with the registrar. Thecompany shall file all the special resolutions passed by it within fifteen days ofpassing the same with the registrar. Such copy to be filed shall be authenticated by theChief Executive or Secretary of the company.

0101

01

Total Marks 11

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Business LawsSummer Exam-2016

Ans.9.

(i)

Private CompanySuch type of a company can be registered by at least two members and it restricts.

The maximum number of members to fifty, members jointly holding sharesshall be counted as one member,

The right to transfer the shares by its members, The invitation of subscriptions from general public for its shares or other

securities.

01

01

0101

(ii) Public Unlisted CompanyPublic Unlisted Companies have not made an offer of their shares to general publichence there shares are not traded on a Stock Exchange.

A Public Unlisted Company however is entitled to make an offer to the general publicas and when it thinks fit unlike private companies which are forbidden to invitesubscriptions from general public.

02

01

(iii) Holding companyIt means a company or body corporate which holds (directly or indirectly) more thanfifty percent (50%) in the voting securities of any other company, or has a power toelect and appoint majority of the directors of such other company.

0101

Total Marks 09

**********************

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

CostAccounting

(Level-2)

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

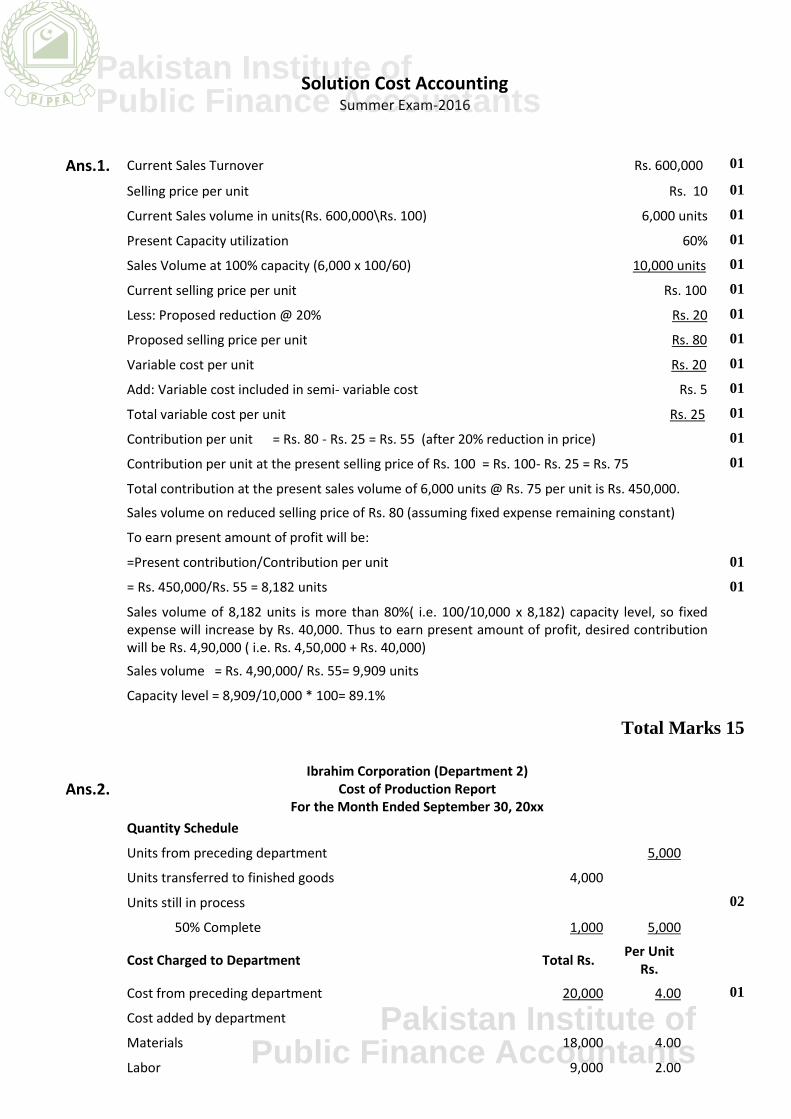

Solution Cost AccountingSummer Exam-2016

Ans.1. Current Sales Turnover Rs. 600,000 01

Selling price per unit Rs. 10 01

Current Sales volume in units(Rs. 600,000\Rs. 100) 6,000 units 01

Present Capacity utilization 60% 01

Sales Volume at 100% capacity (6,000 x 100/60) 10,000 units 01

Current selling price per unit Rs. 100 01

Less: Proposed reduction @ 20% Rs. 20 01

Proposed selling price per unit Rs. 80 01

Variable cost per unit Rs. 20 01

Add: Variable cost included in semi- variable cost Rs. 5 01

Total variable cost per unit Rs. 25 01

Contribution per unit = Rs. 80 - Rs. 25 = Rs. 55 (after 20% reduction in price) 01

Contribution per unit at the present selling price of Rs. 100 = Rs. 100- Rs. 25 = Rs. 75 01

Total contribution at the present sales volume of 6,000 units @ Rs. 75 per unit is Rs. 450,000.

Sales volume on reduced selling price of Rs. 80 (assuming fixed expense remaining constant)

To earn present amount of profit will be:

=Present contribution/Contribution per unit 01

= Rs. 450,000/Rs. 55 = 8,182 units 01

Sales volume of 8,182 units is more than 80%( i.e. 100/10,000 x 8,182) capacity level, so fixedexpense will increase by Rs. 40,000. Thus to earn present amount of profit, desired contributionwill be Rs. 4,90,000 ( i.e. Rs. 4,50,000 + Rs. 40,000)Sales volume = Rs. 4,90,000/ Rs. 55= 9,909 units

Capacity level = 8,909/10,000 * 100= 89.1%

Total Marks 15

Ans.2.Ibrahim Corporation (Department 2)

Cost of Production ReportFor the Month Ended September 30, 20xx

Quantity Schedule

Units from preceding department 5,000

Units transferred to finished goods 4,000

Units still in process 02

50% Complete 1,000 5,000

Cost Charged to Department Total Rs. Per UnitRs.

Cost from preceding department 20,000 4.00 01

Cost added by department

Materials 18,000 4.00

Labor 9,000 2.00

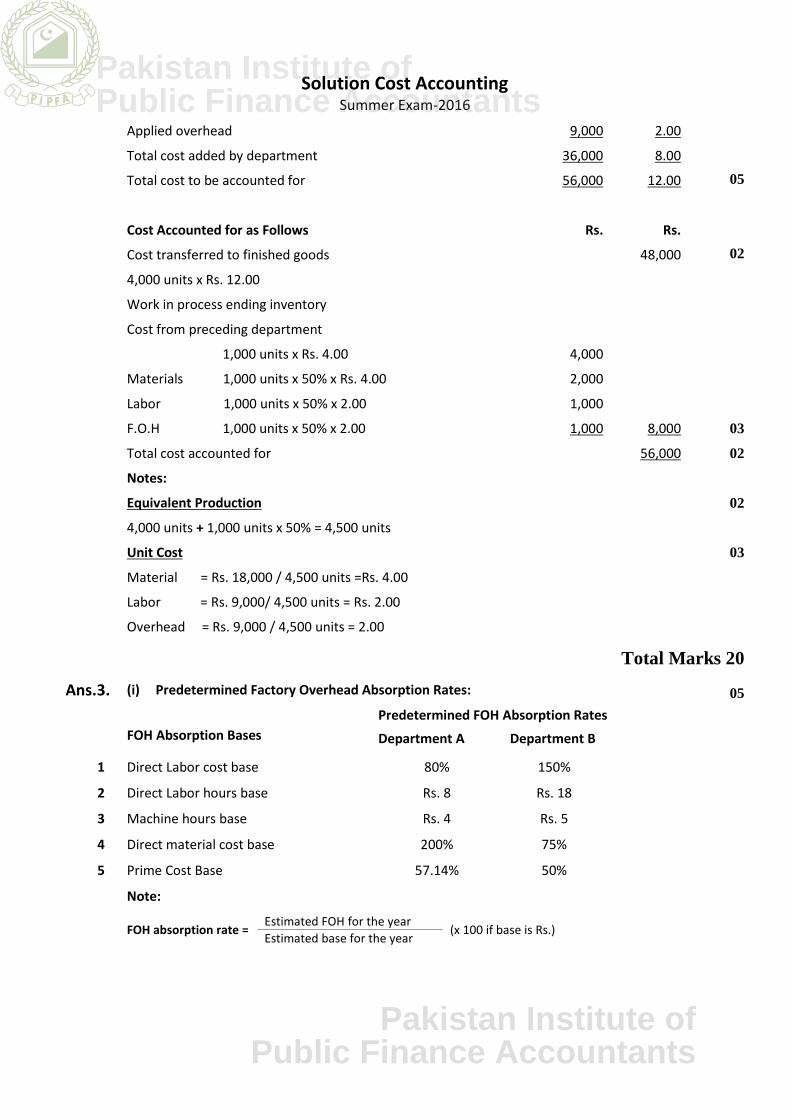

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Cost AccountingSummer Exam-2016

Applied overhead 9,000 2.00

Total cost added by department 36,000 8.00

Total cost to be accounted for 56,000 12.00 05

Cost Accounted for as Follows Rs. Rs.

Cost transferred to finished goods 48,000 02

4,000 units x Rs. 12.00

Work in process ending inventory

Cost from preceding department

1,000 units x Rs. 4.00 4,000

Materials 1,000 units x 50% x Rs. 4.00 2,000

Labor 1,000 units x 50% x 2.00 1,000

F.O.H 1,000 units x 50% x 2.00 1,000 8,000 03

Total cost accounted for 56,000 02

Notes:

Equivalent Production 02

4,000 units + 1,000 units x 50% = 4,500 units

Unit Cost 03

Material = Rs. 18,000 / 4,500 units =Rs. 4.00

Labor = Rs. 9,000/ 4,500 units = Rs. 2.00

Overhead = Rs. 9,000 / 4,500 units = 2.00

Total Marks 20

Ans.3. (i) Predetermined Factory Overhead Absorption Rates: 05

FOH Absorption BasesPredetermined FOH Absorption Rates

Department A Department B

1 Direct Labor cost base 80% 150%

2 Direct Labor hours base Rs. 8 Rs. 18

3 Machine hours base Rs. 4 Rs. 5

4 Direct material cost base 200% 75%

5 Prime Cost Base 57.14% 50%

Note:

FOH absorption rate =Estimated FOH for the year

(x 100 if base is Rs.)Estimated base for the year

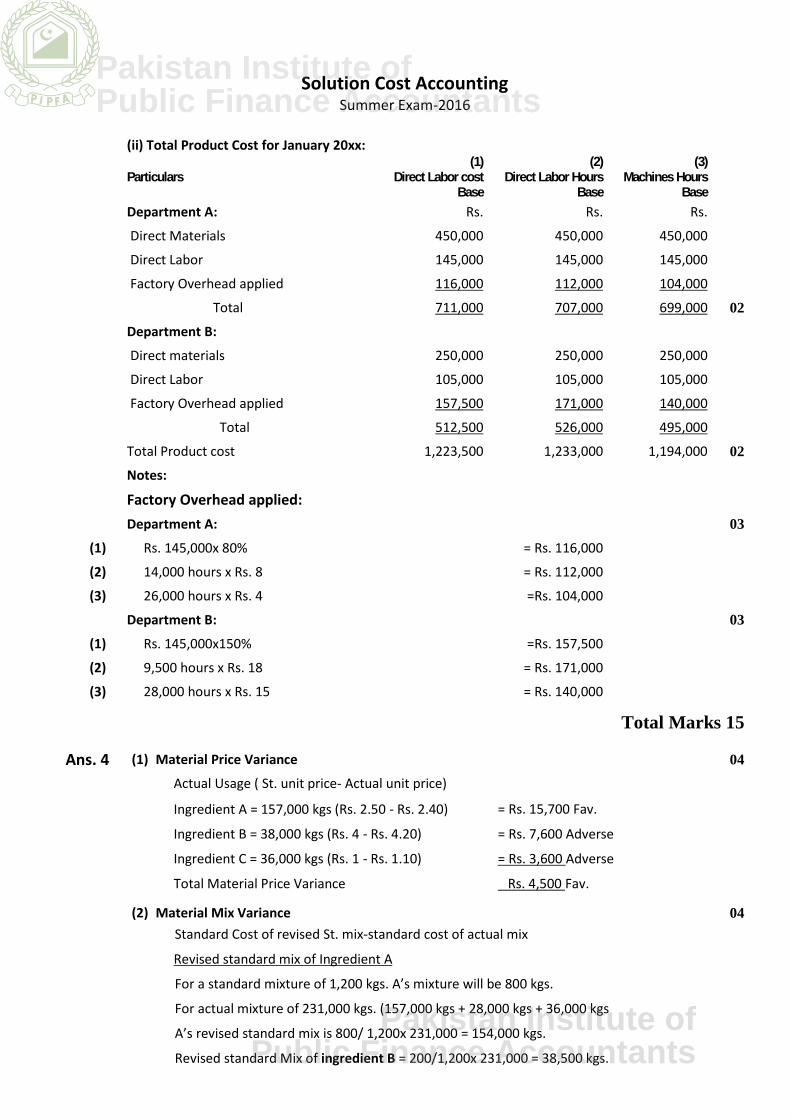

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Cost AccountingSummer Exam-2016

(ii) Total Product Cost for January 20xx:

Particulars(1)

Direct Labor costBase

(2)Direct Labor Hours

Base

(3)Machines Hours

BaseDepartment A: Rs. Rs. Rs.

Direct Materials 450,000 450,000 450,000

Direct Labor 145,000 145,000 145,000

Factory Overhead applied 116,000 112,000 104,000

Total 711,000 707,000 699,000 02

Department B:

Direct materials 250,000 250,000 250,000

Direct Labor 105,000 105,000 105,000

Factory Overhead applied 157,500 171,000 140,000

Total 512,500 526,000 495,000

Total Product cost 1,223,500 1,233,000 1,194,000 02

Notes:

Factory Overhead applied:Department A: 03

(1) Rs. 145,000x 80% = Rs. 116,000

(2) 14,000 hours x Rs. 8 = Rs. 112,000

(3) 26,000 hours x Rs. 4 =Rs. 104,000

Department B: 03

(1) Rs. 145,000x150% =Rs. 157,500

(2) 9,500 hours x Rs. 18 = Rs. 171,000

(3) 28,000 hours x Rs. 15 = Rs. 140,000

Total Marks 15

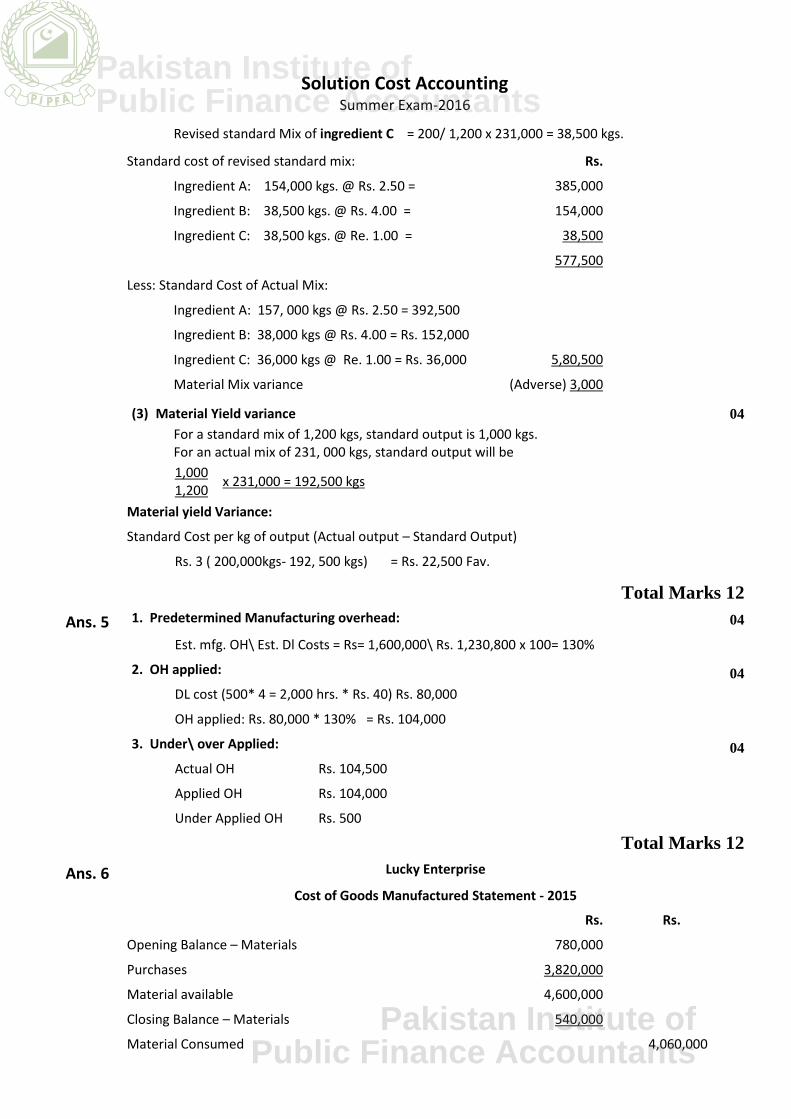

Ans. 4 (1) Material Price Variance 04

Actual Usage ( St. unit price- Actual unit price)

Ingredient A = 157,000 kgs (Rs. 2.50 - Rs. 2.40) = Rs. 15,700 Fav.

Ingredient B = 38,000 kgs (Rs. 4 - Rs. 4.20) = Rs. 7,600 Adverse

Ingredient C = 36,000 kgs (Rs. 1 - Rs. 1.10) = Rs. 3,600 Adverse

Total Material Price Variance Rs. 4,500 Fav.

(2) Material Mix Variance 04Standard Cost of revised St. mix-standard cost of actual mix

Revised standard mix of Ingredient A

For a standard mixture of 1,200 kgs. A’s mixture will be 800 kgs.

For actual mixture of 231,000 kgs. (157,000 kgs + 28,000 kgs + 36,000 kgs

A’s revised standard mix is 800/ 1,200x 231,000 = 154,000 kgs.

Revised standard Mix of ingredient B = 200/1,200x 231,000 = 38,500 kgs.

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Cost AccountingSummer Exam-2016

Revised standard Mix of ingredient C = 200/ 1,200 x 231,000 = 38,500 kgs.

Standard cost of revised standard mix: Rs.

Ingredient A: 154,000 kgs. @ Rs. 2.50 = 385,000

Ingredient B: 38,500 kgs. @ Rs. 4.00 = 154,000

Ingredient C: 38,500 kgs. @ Re. 1.00 = 38,500

577,500

Less: Standard Cost of Actual Mix:

Ingredient A: 157, 000 kgs @ Rs. 2.50 = 392,500

Ingredient B: 38,000 kgs @ Rs. 4.00 = Rs. 152,000

Ingredient C: 36,000 kgs @ Re. 1.00 = Rs. 36,000 5,80,500

Material Mix variance (Adverse) 3,000

(3) Material Yield variance 04For a standard mix of 1,200 kgs, standard output is 1,000 kgs.For an actual mix of 231, 000 kgs, standard output will be1,000 x 231,000 = 192,500 kgs1,200

Material yield Variance:

Standard Cost per kg of output (Actual output – Standard Output)

Rs. 3 ( 200,000kgs- 192, 500 kgs) = Rs. 22,500 Fav.

Total Marks 12

Ans. 5 1. Predetermined Manufacturing overhead: 04

Est. mfg. OH\ Est. Dl Costs = Rs= 1,600,000\ Rs. 1,230,800 x 100= 130%

2. OH applied: 04DL cost (500* 4 = 2,000 hrs. * Rs. 40) Rs. 80,000

OH applied: Rs. 80,000 * 130% = Rs. 104,000

3. Under\ over Applied: 04Actual OH Rs. 104,500

Applied OH Rs. 104,000

Under Applied OH Rs. 500

Total Marks 12

Ans. 6 Lucky Enterprise

Cost of Goods Manufactured Statement - 2015

Rs. Rs.

Opening Balance – Materials 780,000

Purchases 3,820,000

Material available 4,600,000

Closing Balance – Materials 540,000

Material Consumed 4,060,000

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Cost AccountingSummer Exam-2016

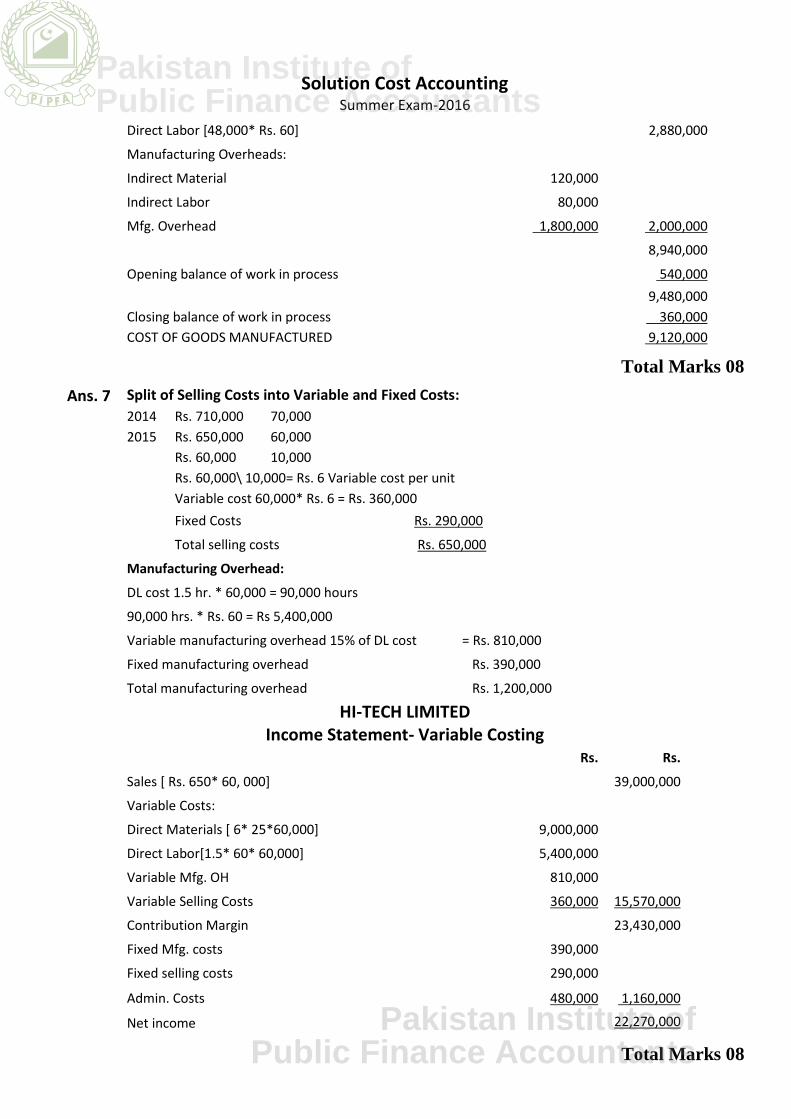

Direct Labor [48,000* Rs. 60] 2,880,000

Manufacturing Overheads:

Indirect Material 120,000

Indirect Labor 80,000

Mfg. Overhead 1,800,000 2,000,000

8,940,000

Opening balance of work in process 540,0009,480,000

Closing balance of work in process 360,000COST OF GOODS MANUFACTURED 9,120,000

Total Marks 08

Ans. 7 Split of Selling Costs into Variable and Fixed Costs:2014 Rs. 710,000 70,0002015 Rs. 650,000 60,000

Rs. 60,000 10,000Rs. 60,000\ 10,000= Rs. 6 Variable cost per unitVariable cost 60,000* Rs. 6 = Rs. 360,000Fixed Costs Rs. 290,000

Total selling costs Rs. 650,000

Manufacturing Overhead:

DL cost 1.5 hr. * 60,000 = 90,000 hours

90,000 hrs. * Rs. 60 = Rs 5,400,000

Variable manufacturing overhead 15% of DL cost = Rs. 810,000

Fixed manufacturing overhead Rs. 390,000

Total manufacturing overhead Rs. 1,200,000

HI-TECH LIMITEDIncome Statement- Variable Costing

Rs. Rs.

Sales [ Rs. 650* 60, 000] 39,000,000

Variable Costs:

Direct Materials [ 6* 25*60,000] 9,000,000

Direct Labor[1.5* 60* 60,000] 5,400,000

Variable Mfg. OH 810,000

Variable Selling Costs 360,000 15,570,000

Contribution Margin 23,430,000

Fixed Mfg. costs 390,000

Fixed selling costs 290,000

Admin. Costs 480,000 1,160,000

Net income 22,270,000

Total Marks 08

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Cost AccountingSummer Exam-2016

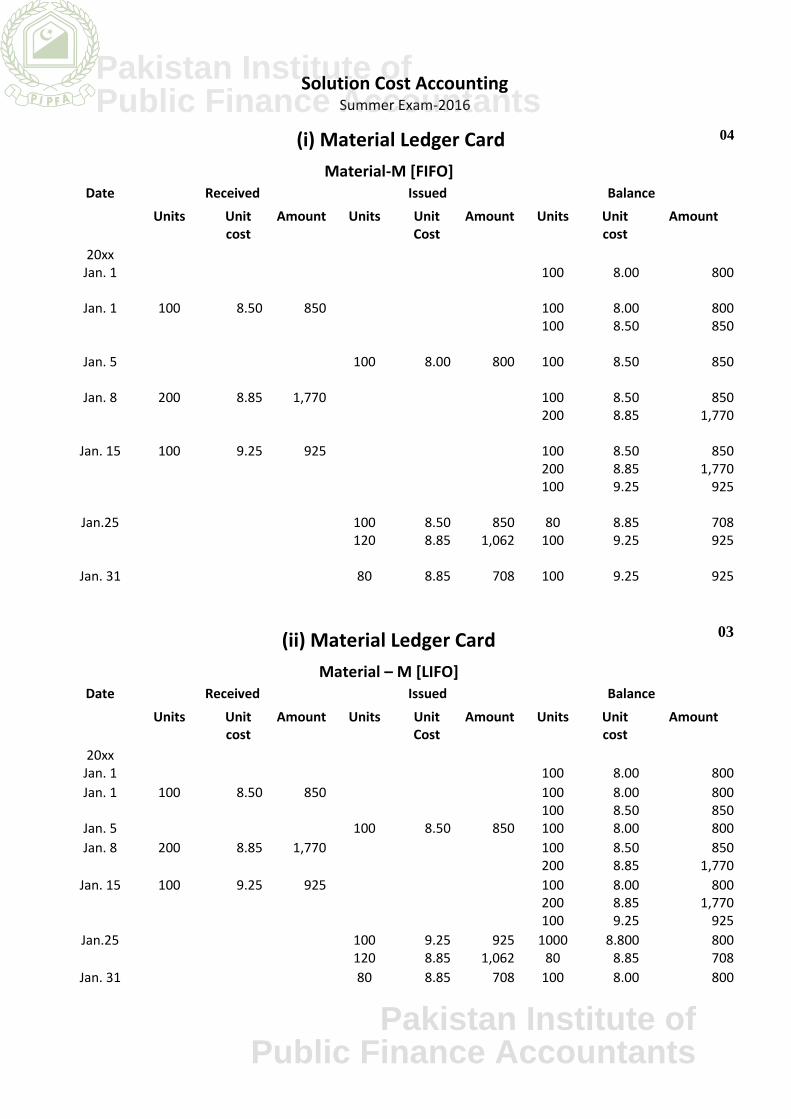

(i) Material Ledger CardMaterial-M [FIFO]

04

Date Received Issued BalanceUnits Unit

costAmount Units Unit

CostAmount Units Unit

costAmount

20xxJan. 1 100 8.00 800

Jan. 1 100 8.50 850 100 8.00 800100 8.50 850

Jan. 5 100 8.00 800 100 8.50 850

Jan. 8 200 8.85 1,770 100 8.50 850200 8.85 1,770

Jan. 15 100 9.25 925 100 8.50 850200 8.85 1,770100 9.25 925

Jan.25 100 8.50 850 80 8.85 708120 8.85 1,062 100 9.25 925

Jan. 31 80 8.85 708 100 9.25 925

(ii) Material Ledger CardMaterial – M [LIFO]

03

Date Received Issued BalanceUnits Unit

costAmount Units Unit

CostAmount Units Unit

costAmount

20xxJan. 1 100 8.00 800Jan. 1 100 8.50 850 100 8.00 800

100 8.50 850Jan. 5 100 8.50 850 100 8.00 800Jan. 8 200 8.85 1,770 100 8.50 850

200 8.85 1,770Jan. 15 100 9.25 925 100 8.00 800

200 8.85 1,770100 9.25 925

Jan.25 100 9.25 925 1000 8.800 800120 8.85 1,062 80 8.85 708

Jan. 31 80 8.85 708 100 8.00 800

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Cost AccountingSummer Exam-2016

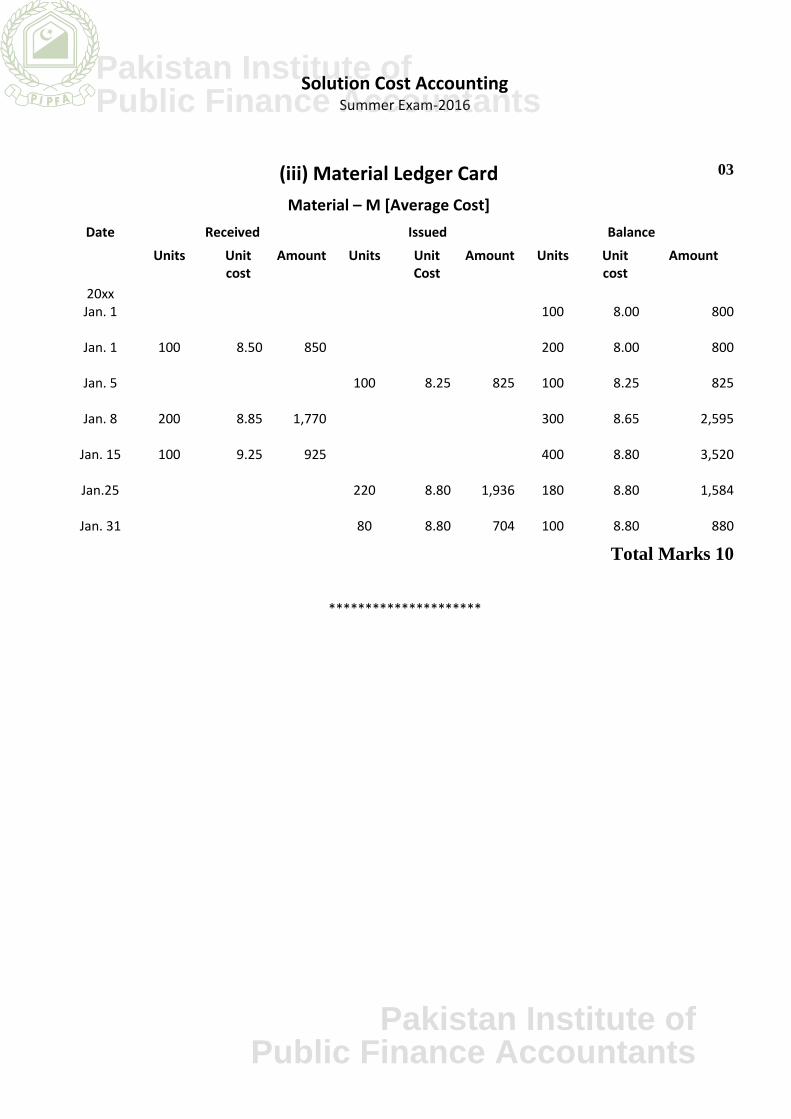

(iii) Material Ledger CardMaterial – M [Average Cost]

03

Date Received Issued BalanceUnits Unit

costAmount Units Unit

CostAmount Units Unit

costAmount

20xxJan. 1 100 8.00 800

Jan. 1 100 8.50 850 200 8.00 800

Jan. 5 100 8.25 825 100 8.25 825

Jan. 8 200 8.85 1,770 300 8.65 2,595

Jan. 15 100 9.25 925 400 8.80 3,520

Jan.25 220 8.80 1,936 180 8.80 1,584

Jan. 31 80 8.80 704 100 8.80 880

Total Marks 10

*********************

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

FinancialAccounting

(Level-3)

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

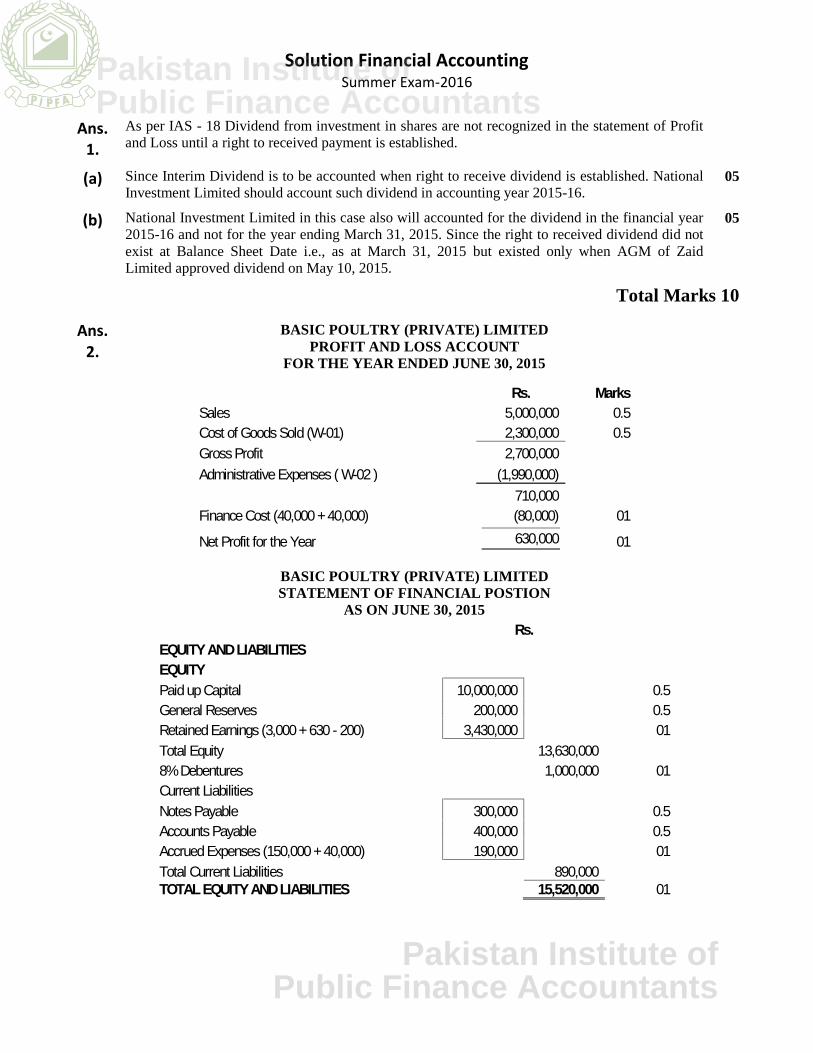

Solution Financial AccountingSummer Exam-2016

Ans.1.

As per IAS - 18 Dividend from investment in shares are not recognized in the statement of Profitand Loss until a right to received payment is established.

(a) Since Interim Dividend is to be accounted when right to receive dividend is established. NationalInvestment Limited should account such dividend in accounting year 2015-16.

05

(b) National Investment Limited in this case also will accounted for the dividend in the financial year2015-16 and not for the year ending March 31, 2015. Since the right to received dividend did notexist at Balance Sheet Date i.e., as at March 31, 2015 but existed only when AGM of ZaidLimited approved dividend on May 10, 2015.

05

Total Marks 10

Ans.2.

BASIC POULTRY (PRIVATE) LIMITEDPROFIT AND LOSS ACCOUNT

FOR THE YEAR ENDED JUNE 30, 2015

Rs. MarksSales 5,000,000 0.5Cost of Goods Sold (W-01) 2,300,000 0.5Gross Profit 2,700,000Administrative Expenses ( W-02 ) (1,990,000)

710,000Finance Cost (40,000 + 40,000) (80,000) 01

Net Profit for the Year 630,000 01

BASIC POULTRY (PRIVATE) LIMITEDSTATEMENT OF FINANCIAL POSTION

AS ON JUNE 30, 2015Rs.

EQUITY AND LIABILITIESEQUITYPaid up Capital 10,000,000 0.5General Reserves 200,000 0.5Retained Earnings (3,000 + 630 - 200) 3,430,000 01Total Equity 13,630,0008% Debentures 1,000,000 01Current LiabilitiesNotes Payable 300,000 0.5Accounts Payable 400,000 0.5Accrued Expenses (150,000 + 40,000) 190,000 01Total Current Liabilities 890,000TOTAL EQUITY AND LIABILITIES 15,520,000 01

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Financial AccountingSummer Exam-2016

ASSETSNon-current assets (W-03 ) 13,100,000 01Preliminary Expenses (100,000-10,000) 90,000Current AssetsClosing Stocks 500,000 0.5Accounts recently less: Provision Receivables(1,200,000 - 60,000) 1,140,000 0.5Prepaid Expenses (100,000 + 50,000) 150,000 0.5Cash and Bank Balance 540,000 0.5Total Current Assets 2,330,000Total Assets 15,520,000 01

WORKING NOTESWorking - 01 (COST OF GOODS SOLD)Opening Stock 800,000 0.5Add Purchases 2,000,000 0.5Goods Available for Sales 2,800,000 0.5Less Closing Stocks 500,000Cost of Goods Sold 2,300,000 0.5Working - 02 (ADMINISTRATIVE EXPENSES)Salaries (1,200,000 + 150,000 -50,000) 1,300,000 0.5General Expenses 100,000 0.5Insurance Expenses (300,000 - 100,000) 200,000 0.5Preliminary Expenses(100,000%10) 10,000 0.5Bad Debt Expenses (50,000 + 30,000) 80,000 0.5Depreciation Expenses 300,000 0.5Total Administrative Expenses 1,990,000

Working - 03 (NON-CURRENT ASSETS)Land Plant Total

Opening Balance 10,400,000 3,000,000 13,400,000Less Accumulated Depreciation - - -Written Down Value 10,400,000 3,000,000 13,400,000Depreciation Rate 10%Depreciation for the Year - 300,000 300,000 01Accumulated Depreciation - 300,000 300,000

Written Down Value as on June-30-2015 10,400,000 2,700,000 13,100,000 01

Total Marks 20

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Financial AccountingSummer Exam-2016

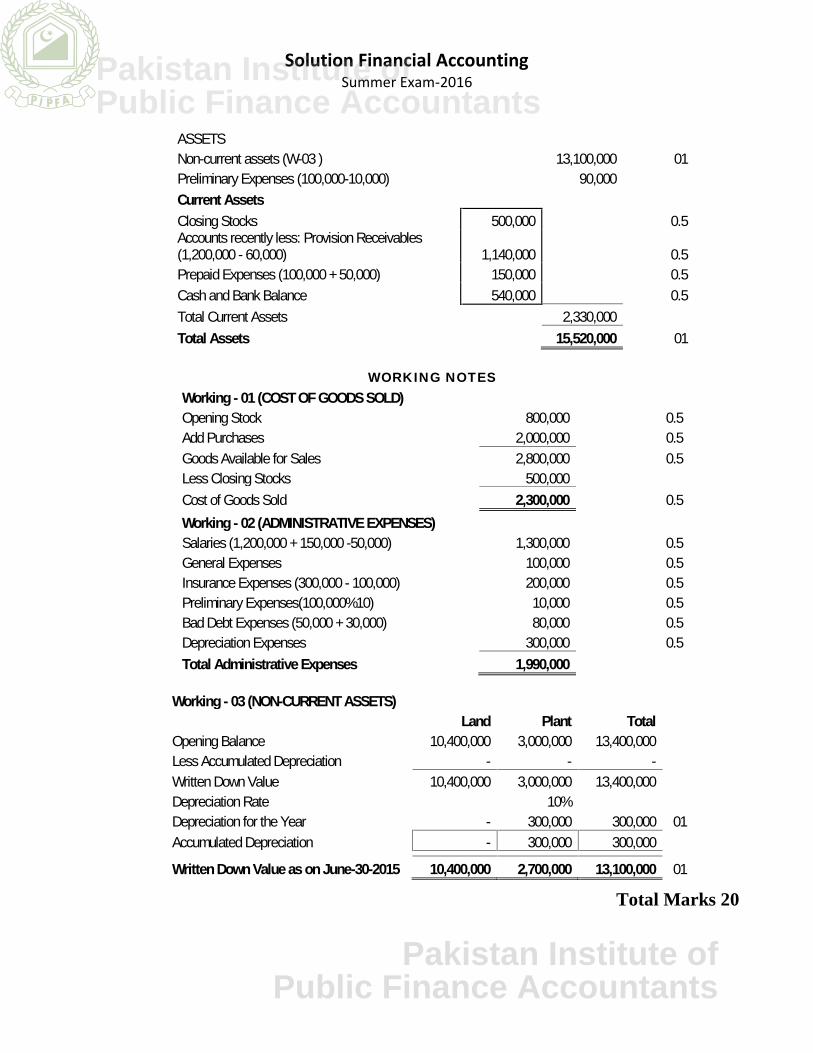

Ans.3.

FRIENDS COMMODITIES (PRIVATE) LIMITEDSTATEMENT OF CASH FLOW

FOR THE YEAR ENDED JUNE 30, 2015Rs.

CASH FLOWS FROM OPERATING ACTIVITIESProfit before Taxes 110,000 01Adjustments for :Depreciation 60,000 0.5Loss on Disposal of Equipments (20,000 - 17,000) 3,000 63,000 0.5

Operating Profit before Working Capital Changes 173,000 0.5Decrease in Accounts Receivable (410,000 - 460,000) 50,000 0.5Decrease in Inventory (300,000 - 320,000) 20,000 0.5Increase in Prepaid Expenses (20,000 - 15,000) (5,000) 0.5Increase in Accounts Payable (300,000 - 120,000) 180,000 0.5Decrease in Accrued Liabilities (40,000 - 50,00) (10,000) 235,000 0.5Cash Flow from Operating Activities 408,000

Cash Flow from Investing ActivitiesSale Proceeds of Fixed Assets 17,000 0.5Purchase of Investments (50,000 - 25,000) (25,000) 0.5Purchase of Land (560,000 - 300,000) (260,000) (268,000) 0.5Cash used in Investing Activities 140,000

Cash Flow from Financing ActivitiesPayment of Dividends (60,000) 0.5Repayment of Bonds (300,000) 0.5Increase in Share Capital 200,000 (160,000) 0.5Net Decrease in Cash and Cash Equivalents (20,000) 0.5Opening Balance of Cash and Cash Equivalents 50,000 0.5Closing Balance of Cash and Cash Equivalents 30,000 01

Total Marks 10

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Financial AccountingSummer Exam-2016

Ans.4.

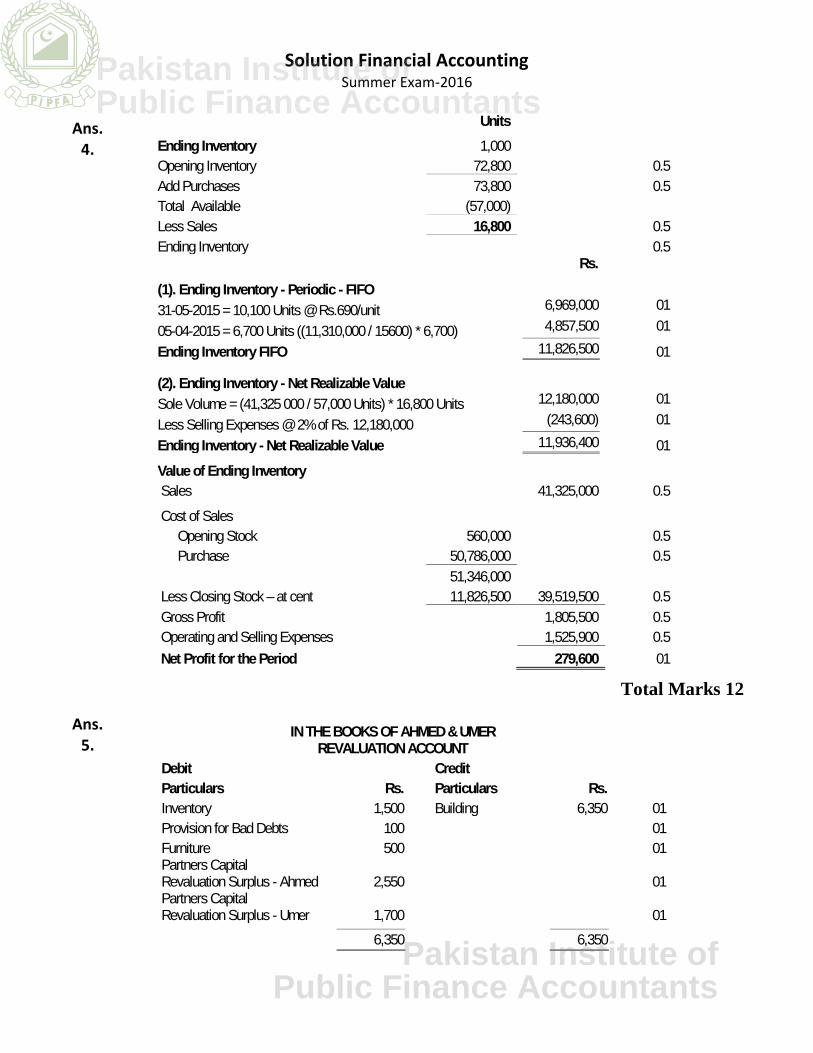

UnitsEnding Inventory 1,000Opening Inventory 72,800 0.5Add Purchases 73,800 0.5Total Available (57,000)Less Sales 16,800 0.5Ending Inventory 0.5

Rs.

(1). Ending Inventory - Periodic - FIFO31-05-2015 = 10,100 Units @ Rs.690/unit05-04-2015 = 6,700 Units ((11,310,000 / 15600) * 6,700)Ending Inventory FIFO

6,969,000 014,857,500 01

11,826,500 01

(2). Ending Inventory - Net Realizable ValueSole Volume = (41,325 000 / 57,000 Units) * 16,800 UnitsLess Selling Expenses @ 2% of Rs. 12,180,000Ending Inventory - Net Realizable Value

12,180,000 01(243,600) 01

11,936,400 01Value of Ending InventorySales 41,325,000 0.5Cost of Sales

Opening Stock 560,000 0.5Purchase 50,786,000 0.5

51,346,000Less Closing Stock – at cent 11,826,500 39,519,500 0.5Gross Profit 1,805,500 0.5Operating and Selling Expenses 1,525,900 0.5Net Profit for the Period 279,600 01

Total Marks 12

Ans.5.

IN THE BOOKS OF AHMED & UMERREVALUATION ACCOUNT

Debit CreditParticulars Rs. Particulars Rs.Inventory 1,500 Building 6,350 01Provision for Bad Debts 100 01Furniture 500 01Partners CapitalRevaluation Surplus - Ahmed 2,550 01Partners CapitalRevaluation Surplus - Umer 1,700 01

6,350 6,350

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Financial AccountingSummer Exam-2016

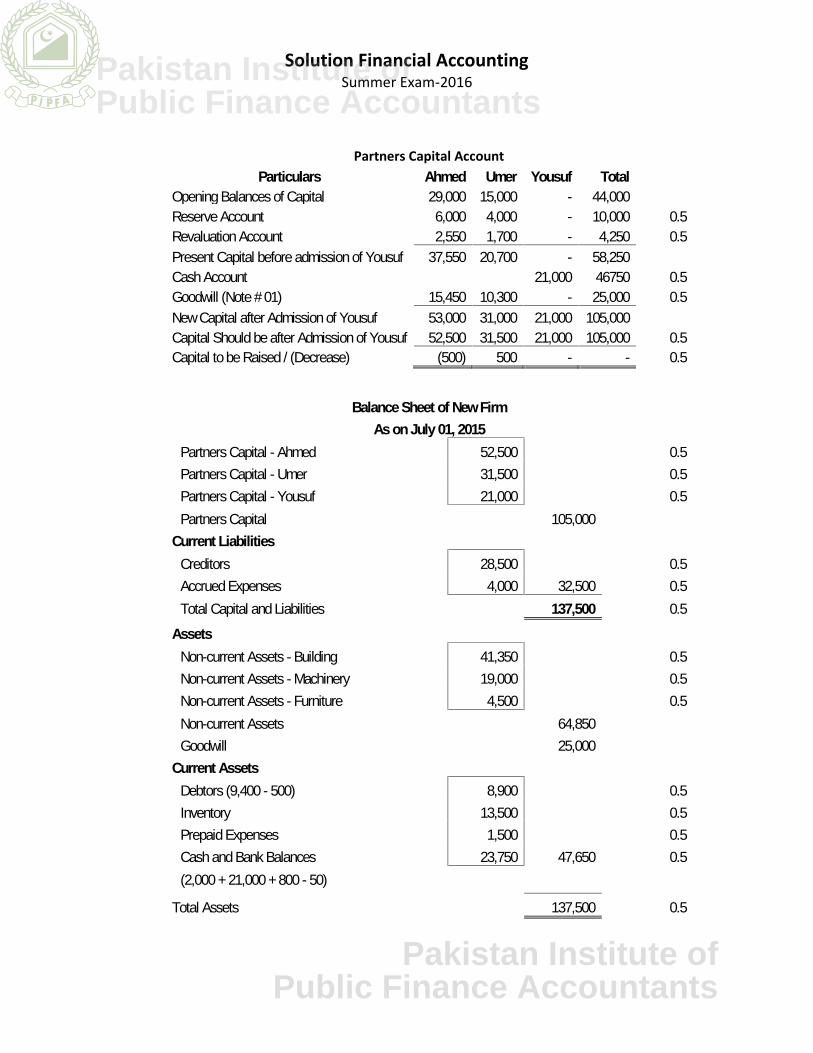

Partners Capital AccountParticulars Ahmed Umer Yousuf Total

Opening Balances of Capital 29,000 15,000 - 44,000Reserve Account 6,000 4,000 - 10,000 0.5Revaluation Account 2,550 1,700 - 4,250 0.5Present Capital before admission of Yousuf 37,550 20,700 - 58,250Cash Account 21,000 46750 0.5Goodwill (Note # 01) 15,450 10,300 - 25,000 0.5New Capital after Admission of Yousuf 53,000 31,000 21,000 105,000Capital Should be after Admission of Yousuf 52,500 31,500 21,000 105,000 0.5Capital to be Raised / (Decrease) (500) 500 - - 0.5

Balance Sheet of New FirmAs on July 01, 2015

Partners Capital - Ahmed 52,500 0.5Partners Capital - Umer 31,500 0.5Partners Capital - Yousuf 21,000 0.5Partners Capital 105,000

Current LiabilitiesCreditors 28,500 0.5Accrued Expenses 4,000 32,500 0.5Total Capital and Liabilities 137,500 0.5

AssetsNon-current Assets - Building 41,350 0.5Non-current Assets - Machinery 19,000 0.5Non-current Assets - Furniture 4,500 0.5Non-current Assets 64,850Goodwill 25,000

Current AssetsDebtors (9,400 - 500) 8,900 0.5Inventory 13,500 0.5Prepaid Expenses 1,500 0.5Cash and Bank Balances 23,750 47,650 0.5(2,000 + 21,000 + 800 - 50)

Total Assets 137,500 0.5

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Financial AccountingSummer Exam-2016

Working NotesCapital of Yousuf = Rs. 21,000 for 2/10th /shareTherefore Total Capital of Firm = 21,000 x 2 / 5 105,000 01Ahmed's Capital = Rs. 105,000 X 5 /10 = 52,500 01Umer's Capital = Rs. 105,000 x 3 /10 31,500 - 01Combined Capital of Ahmed and Umer 84,000Less Present Capital of Ahmed and Umer afterRevaluation of Assets 58,250 01Goodwill to be raised 25,750 01

Total Marks 20

Ans.6.

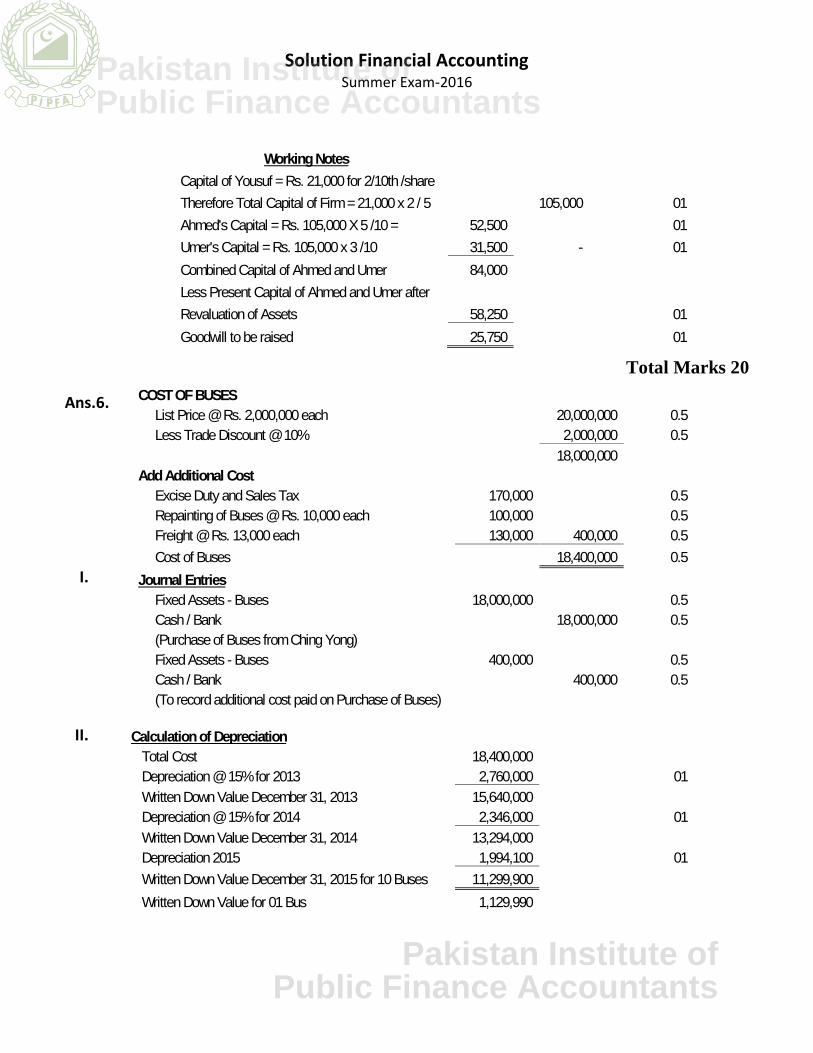

I.

COST OF BUSESList Price @ Rs. 2,000,000 each 20,000,000 0.5Less Trade Discount @ 10% 2,000,000 0.5

18,000,000Add Additional Cost

Excise Duty and Sales Tax 170,000 0.5Repainting of Buses @ Rs. 10,000 each 100,000 0.5Freight @ Rs. 13,000 each 130,000 400,000 0.5Cost of Buses 18,400,000 0.5

Journal EntriesFixed Assets - Buses 18,000,000 0.5Cash / Bank 18,000,000 0.5(Purchase of Buses from Ching Yong)Fixed Assets - Buses 400,000 0.5Cash / Bank 400,000 0.5(To record additional cost paid on Purchase of Buses)

II. Calculation of DepreciationTotal Cost 18,400,000Depreciation @ 15% for 2013 2,760,000 01Written Down Value December 31, 2013 15,640,000Depreciation @ 15% for 2014 2,346,000 01Written Down Value December 31, 2014 13,294,000Depreciation 2015 1,994,100 01Written Down Value December 31, 2015 for 10 Buses 11,299,900Written Down Value for 01 Bus 1,129,990

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Financial AccountingSummer Exam-2016

GAIN / LOSS ON DISPOSAL OF BUSES

Written Down Value (1,1299,900 x 5) 5,649,950 0.5Cash received 6,650,000 0.5Gain on Sale of 05 Buses 1,000,050 01

Journal Entries DR CRCash 6,650,000 0.5Accumulated Depreciation 3,550,150 0.5Fixed Assets Buses 9,200,000 0.5Gain on sale of Fixed Assets - Buses 1,000,050 0.5(To record gain on disposal of 05 Buses)

Total Marks 12

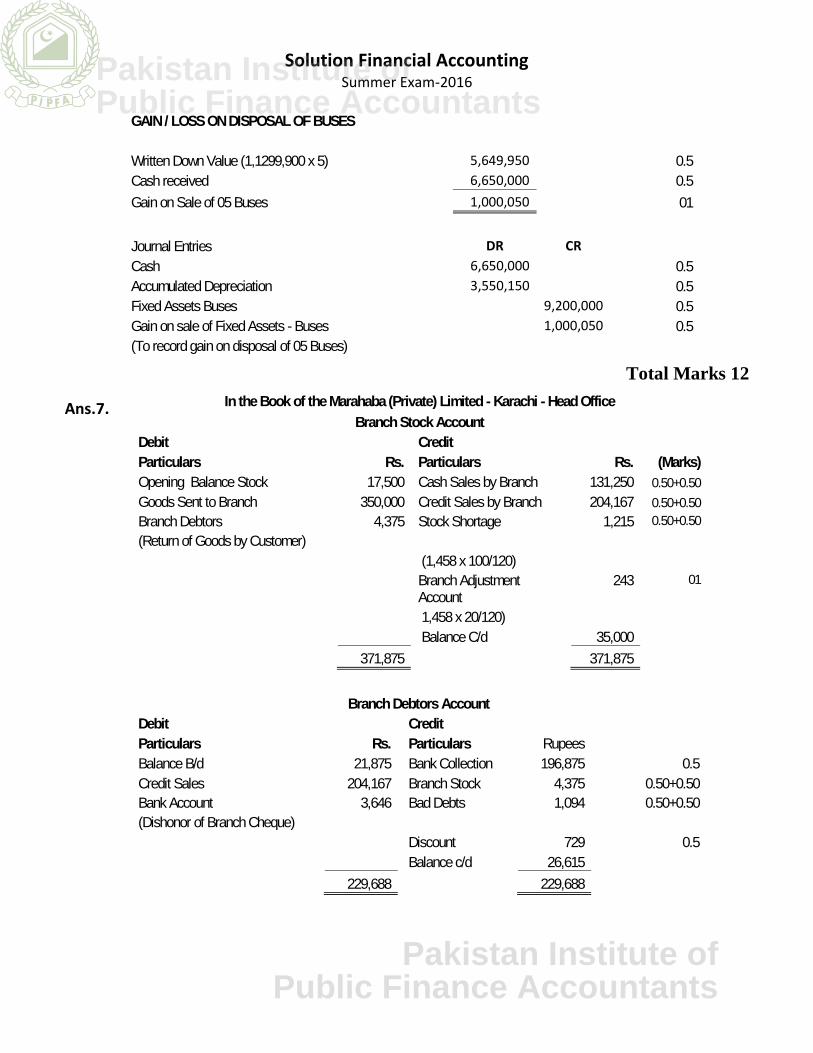

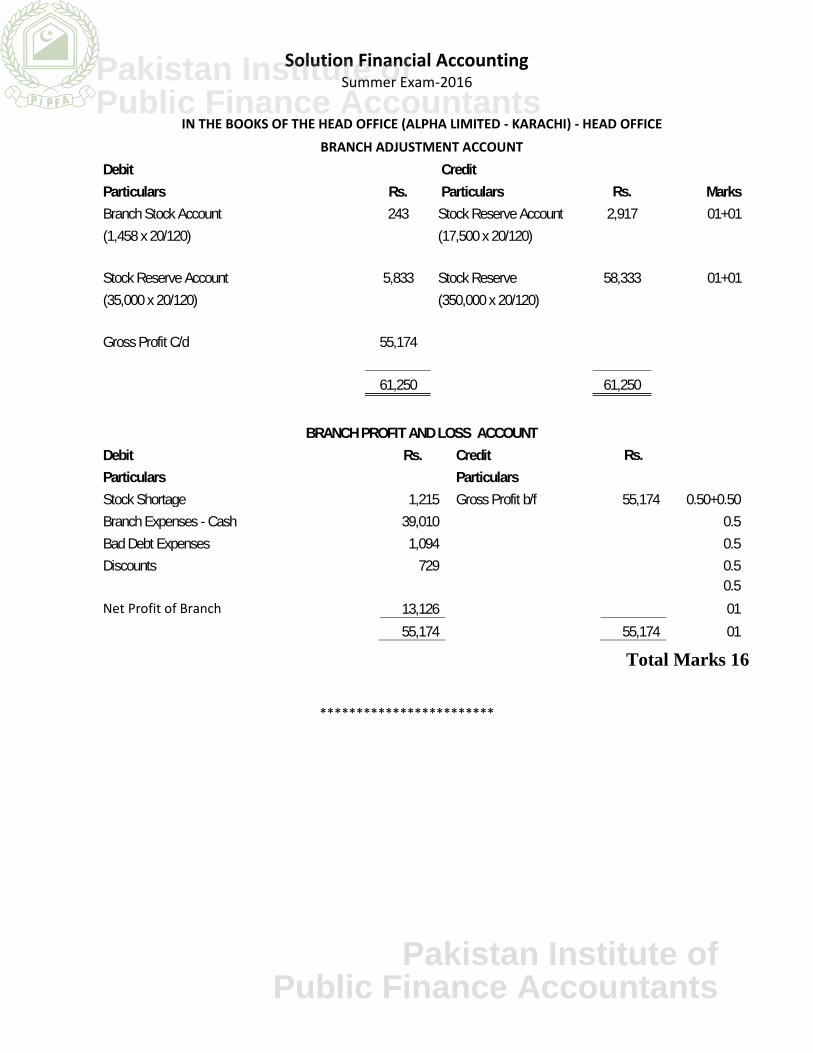

Ans.7. In the Book of the Marahaba (Private) Limited - Karachi - Head OfficeBranch Stock Account

Debit CreditParticulars Rs. Particulars Rs. (Marks)Opening Balance Stock 17,500 Cash Sales by Branch 131,250 0.50+0.50Goods Sent to Branch 350,000 Credit Sales by Branch 204,167 0.50+0.50Branch Debtors(Return of Goods by Customer)

4,375 Stock Shortage 1,215 0.50+0.50

(1,458 x 100/120)Branch AdjustmentAccount

243 01

1,458 x 20/120)Balance C/d 35,000

371,875 371,875

Branch Debtors AccountDebit CreditParticulars Rs. Particulars RupeesBalance B/d 21,875 Bank Collection 196,875 0.5Credit Sales 204,167 Branch Stock 4,375 0.50+0.50Bank Account(Dishonor of Branch Cheque)

3,646 Bad Debts 1,094 0.50+0.50

Discount 729 0.5Balance c/d 26,615

229,688 229,688

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Financial AccountingSummer Exam-2016

IN THE BOOKS OF THE HEAD OFFICE (ALPHA LIMITED - KARACHI) - HEAD OFFICEBRANCH ADJUSTMENT ACCOUNT

Debit CreditParticulars Rs. Particulars Rs. MarksBranch Stock Account 243 Stock Reserve Account 2,917 01+01(1,458 x 20/120) (17,500 x 20/120)

Stock Reserve Account 5,833 Stock Reserve 58,333 01+01(35,000 x 20/120) (350,000 x 20/120)

Gross Profit C/d 55,174

61,250 61,250

BRANCH PROFIT AND LOSS ACCOUNTDebit Rs. Credit Rs.Particulars ParticularsStock Shortage 1,215 Gross Profit b/f 55,174 0.50+0.50Branch Expenses - Cash 39,010 0.5Bad Debt Expenses 1,094 0.5Discounts 729 0.5

0.5Net Profit of Branch 13,126 01

55,174 55,174 01

Total Marks 16

************************

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Business Commn. &Report Writing

(Level-3)

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Business Communication & Report WritingSummer Exam-2016

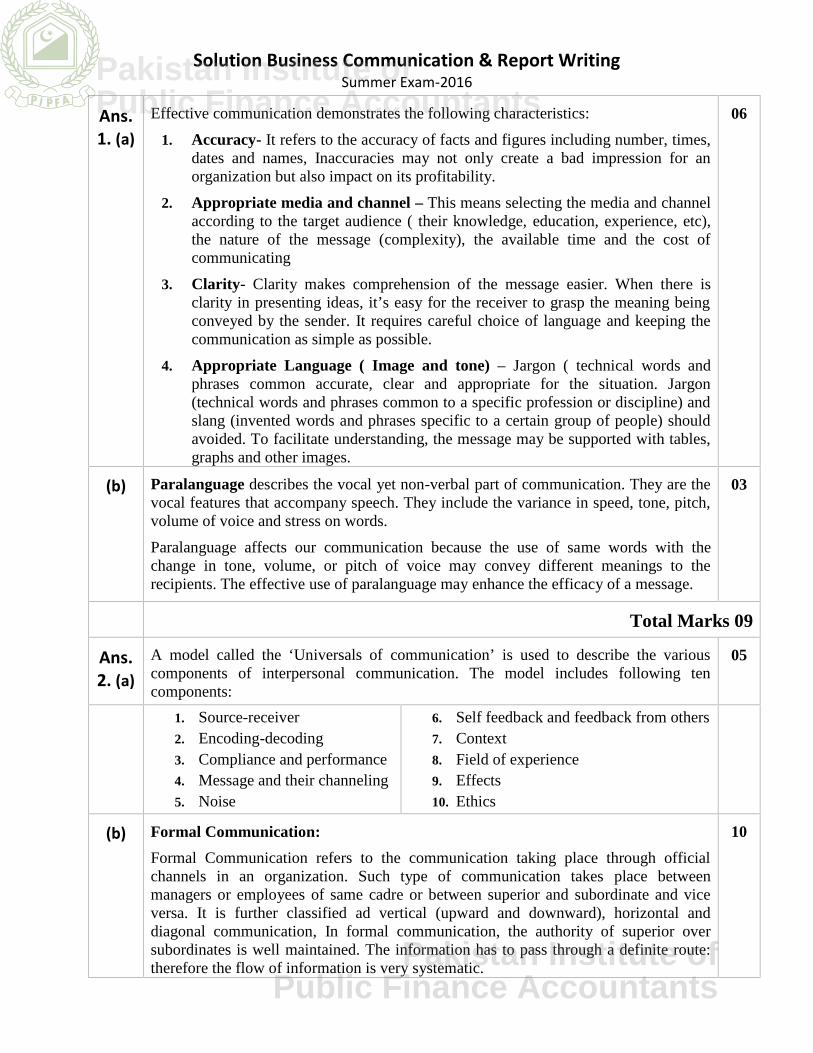

Ans.1. (a)

Effective communication demonstrates the following characteristics:

1. Accuracy- It refers to the accuracy of facts and figures including number, times,dates and names, Inaccuracies may not only create a bad impression for anorganization but also impact on its profitability.

2. Appropriate media and channel – This means selecting the media and channelaccording to the target audience ( their knowledge, education, experience, etc),the nature of the message (complexity), the available time and the cost ofcommunicating

3. Clarity- Clarity makes comprehension of the message easier. When there isclarity in presenting ideas, it’s easy for the receiver to grasp the meaning beingconveyed by the sender. It requires careful choice of language and keeping thecommunication as simple as possible.

4. Appropriate Language ( Image and tone) – Jargon ( technical words andphrases common accurate, clear and appropriate for the situation. Jargon(technical words and phrases common to a specific profession or discipline) andslang (invented words and phrases specific to a certain group of people) shouldavoided. To facilitate understanding, the message may be supported with tables,graphs and other images.

06

(b) Paralanguage describes the vocal yet non-verbal part of communication. They are thevocal features that accompany speech. They include the variance in speed, tone, pitch,volume of voice and stress on words.

Paralanguage affects our communication because the use of same words with thechange in tone, volume, or pitch of voice may convey different meanings to therecipients. The effective use of paralanguage may enhance the efficacy of a message.

03

Total Marks 09

Ans.2. (a)

A model called the ‘Universals of communication’ is used to describe the variouscomponents of interpersonal communication. The model includes following tencomponents:

05

1. Source-receiver2. Encoding-decoding3. Compliance and performance4. Message and their channeling5. Noise

6. Self feedback and feedback from others7. Context8. Field of experience9. Effects10. Ethics

(b) Formal Communication:

Formal Communication refers to the communication taking place through officialchannels in an organization. Such type of communication takes place betweenmanagers or employees of same cadre or between superior and subordinate and viceversa. It is further classified ad vertical (upward and downward), horizontal anddiagonal communication, In formal communication, the authority of superior oversubordinates is well maintained. The information has to pass through a definite route:therefore the flow of information is very systematic.

10

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Business Communication & Report WritingSummer Exam-2016

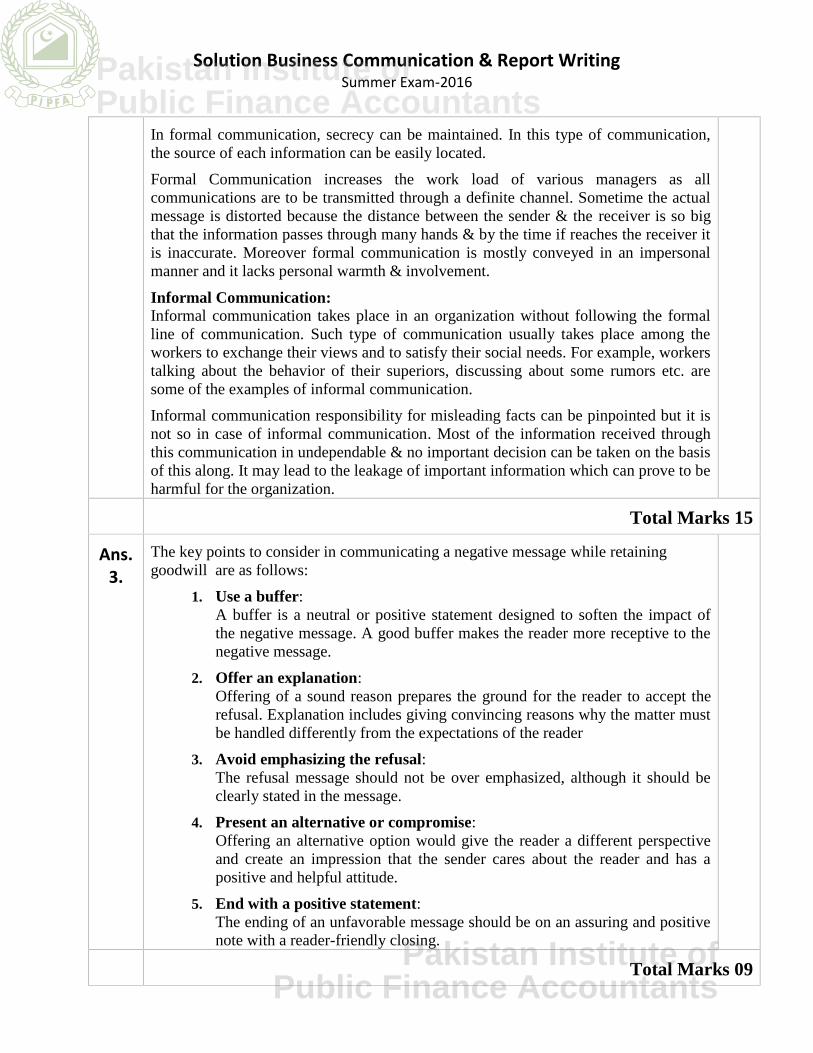

In formal communication, secrecy can be maintained. In this type of communication,the source of each information can be easily located.

Formal Communication increases the work load of various managers as allcommunications are to be transmitted through a definite channel. Sometime the actualmessage is distorted because the distance between the sender & the receiver is so bigthat the information passes through many hands & by the time if reaches the receiver itis inaccurate. Moreover formal communication is mostly conveyed in an impersonalmanner and it lacks personal warmth & involvement.

Informal Communication:Informal communication takes place in an organization without following the formalline of communication. Such type of communication usually takes place among theworkers to exchange their views and to satisfy their social needs. For example, workerstalking about the behavior of their superiors, discussing about some rumors etc. aresome of the examples of informal communication.

Informal communication responsibility for misleading facts can be pinpointed but it isnot so in case of informal communication. Most of the information received throughthis communication in undependable & no important decision can be taken on the basisof this along. It may lead to the leakage of important information which can prove to beharmful for the organization.

Total Marks 15

Ans.3.

The key points to consider in communicating a negative message while retaininggoodwill are as follows:

1. Use a buffer:A buffer is a neutral or positive statement designed to soften the impact ofthe negative message. A good buffer makes the reader more receptive to thenegative message.

2. Offer an explanation:Offering of a sound reason prepares the ground for the reader to accept therefusal. Explanation includes giving convincing reasons why the matter mustbe handled differently from the expectations of the reader

3. Avoid emphasizing the refusal:The refusal message should not be over emphasized, although it should beclearly stated in the message.

4. Present an alternative or compromise:Offering an alternative option would give the reader a different perspectiveand create an impression that the sender cares about the reader and has apositive and helpful attitude.

5. End with a positive statement:The ending of an unfavorable message should be on an assuring and positivenote with a reader-friendly closing.

Total Marks 09

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Business Communication & Report WritingSummer Exam-2016

Ans.4.

There are generally three types of listeners we find in an organizational setting. Theyare as follows.

1. Results-oriented– Typically low on patience, these listeners are focused onachieving their goals as quickly and efficiently as possible. Speakers wholike listeners to demonstrate empathy and logical thought often see results-oriented listeners as arrogant and impatient. Conversely results-orientedwould see many speakers as unfocused and become frustrated at speakerstaking too long to make their point.

2. Information-oriented – These listeners like to build a full picture, collectand consolidate all relevant information in order to make the right decision.The risk is that an overly analytical approach can overlook emotionalattitudes and appear unsympathetic to some speakers.

3. People-focused – The priority of this type of listener is not the businessoutcome or a technical solution, but rather a focus on supporting the speakerand being attentive to their feelings and needs. People-focused listeners havelots of patience and are naturally gifted at providing feedback and reflectivequestions that make the speaker feel good and confident about themselves.

The speaker really feels listened-to although a result-oriented orinformation-oriented speaker may feel that a people-focused listener isvague and inconclusive with too much of an emphasis on feelings.

Total Marks 06

Ans.5.

Answers will vary but must meet the following requirements.

1. Opening paragraph: Explain the general background to your enquiry sothat the reader is clear what the letter is about.

2. Body: Must provide specific details about the enquiry and list your questionsin a logical order.

3. Close: Close should contain the ‘call to action’. State clearly what the readershould do and exactly by when.

Total Marks 10

Ans.6.

Answers will vary but the contents of an agenda for a formal meeting would includethe following:

1. Title, date, time and place of the meeting.

2. Purpose of the meeting.

3. Minutes of the previous meeting: Matters arising from the last meeting – how any action points or

outstanding issues have been resolved.

4. Apologies for absence.

5. Main body:(i) HR issues(ii) Finance matters

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Business Communication & Report WritingSummer Exam-2016

(iii) Marketing items(iv) Quality Control issues

6. Any other Business.

7. Date of next meeting.

Total Marks 10

Ans.7.

Answers will vary but must contain the following:

1. Introduction

2. SWOT Analysis

3. Conclusion

4. Recommendation

Total Marks 15

Ans.8.

Answers will vary but CV must:

(i) Be restricted to ONE page in length or two pages at maximum.

(ii) Convey the candidate’s key experience and skills quickly.(iii) Order information within sections with the most recent and relevant first.

(iv) Provide an overview of experience and other qualifications.

(v) Highlight the applicant’s special talents and background that will benefit theemployer.

(vi) Should demonstrate that the applicant can make a positive contributiontowards the company’s business objectives.

Total Marks 10

Ans.9.

Benefits of email:

1. An audit trail of messages is automatically retained (and can be for longperiods). This can be invaluable in disputes or simply to check the details ofan email conversation or client order.

2. The sending and receiving of emails is virtually instantaneous anywhere in theworld. This enables managers to communicate with colleagues and companiesto communicate with clients or suppliers incredibly quickly.

3. Recipients can access emails anywhere and anytime at their convenience.

4. Traditional and expensive mail shots to multiple recipients can be replaced bysignificantly quicker and cheaper multi-recipient email communicationsachieving much greater penetration.

5. Easy to use and organize daily correspondence.

6. Low cost.

7. Good for the environment – doesn’t use paper.

Total Marks 07

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution Business Communication & Report WritingSummer Exam-2016

Ans.10.

Video conferencing is on the rise and just about every company utilizes it to somedegree. There are various reasons for its popularity few have been discussed below:

1. Improved lower-cost technology with greater bandwidth2. Wider variety of video conferencing tools available associated with

increasingly more powerful PCs.3. Environmentally friendly IT initiatives such reduced air travel.4. High travel costs combined with austerity related cost saving initiatives.5. Reliability: One can hold meeting regardless of weather, flight delays, or many

other reasons. One can always be able to connect with the members no matterwhere they are.

6. Increase Productivity: Meet as much as one to get the job done instead of onlywhen it is scheduled. It is so easy to bring someone into the conversation thatthere’s no pressure to fill up an hour to justify the scheduling.

7. Improve Employee Morale: The employees may contribute to decision makingwhich increases their morale.

8. Improve safety and security both for people as well as information.

Total Marks 09

***********************

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Taxation

(Level-3)

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution TaxationSummer Exam-2016

Ans.1. (i)

Filer: A taxpayer whose name is appears in the ‘active taxpayer’ list’ or is the holder ofa ‘taxpayer’s card’s is termed as ‘filer’. The active taxpayers’ list is issued by FBR fromtime to time. Sec 2-(23A)

02

(ii) Imputable Income: ‘Imputable income’ has been defined in relation to an amountwhich is subject to ‘final tax’ and means the income which would have resulted in thesame tax, had this amount not been subject to final tax. Sec 2-(28A)

02

(iii) Small Company: Small Company’ means a company which fulfills the followingconditions:

1. It is a company registered under the Companies Ordinance, 1984;

2. It is registered on or after 1st July, 2005; and

3. The Company:(i) Has paid-up capital plus undistributed reserves up to rupees fifty (50) million;

(ii) Has employees not exceeding two hundred and fifty (250) at any time during theyear;

(iii) Has total annual turnover up to rupees two hundred and fifty (250) million; and

(iv) Is not formed by the splitting up or the reconstitution of company already inexistence. 2(59A)

02

Total Marks 06

Ans.2.

Power of Parliament to impose tax on the income of certain Corporations:

1. Parliament has, and shall be deemed always to have had, the power to make a lawto provide for the levy and recovery of a tax on the income of a corporation,company or other body or institution established by or under a Federal law or aProvincial law or an existing law or a corporation, company or other body orinstitution owned or controlled, either directly or indirectly, by the FederalGovernment or a Provincial Government, regardless of the ultimate destination ofsuch income.

2. All orders made, proceedings taken and acts done by any authority or person,which were made, taken or done, or purported to have been made, taken or done,before the commencement of the Constitution (Amendment) Order 1985, inexercise of the powers derived from any law referred to in clause (1), or inexecution of any orders made by any authority in the exercise or purportedexercise of powers as aforesaid, shall, notwithstanding any judgment of any courtor tribunal, including the Supreme Court and a High Court, be deemed to be andalways to have been validly made, taken or done and-shall not be called inquestion in any court, including the Supreme Court and a High Court, on anyground whatsoever.

3. Every judgment or order of any court or tribunal, including the Supreme Courtand a High Court, which is repugnant to the provisions of clause (1) or clause (2)shall be, and shall be deemed always to have been, void and of no effectwhatsoever.

Total Marks 09

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution TaxationSummer Exam-2016

Ans.3.

Unexplained Incomes or Assets:

The value of any income, expenditure, investment, article or asset, etc., shall bechargeable to tax under the head “Income from Other Sources” if the followingconditions are met:

1. It is any:

(i) Amount which is credited in a person’s books of account;(ii) Investment made by a person;

(iii) Money or valuable article owned by a person;

(iv) Expenditure incurred by a person; or

(v) Concealment of any income or furnishing of inaccurate particulars of income,which includes:

a) The suppression of any production, sales or any amount chargeable totax; or

b) The suppression of any item of receipt liable to tax in whole or inpart;

2. The person offers no explanation about the nature or source of the transaction,concealment of income or furnishing of inaccurate particulars of income or theexplanation offered by him is not, in the opinion of the Commissioner, satisfactory;and

3. Where a person claims the ‘Agricultural income’ as his source of investment,expenditure, etc, than it shall be accepted only to the extent of agricultural incomeworked back on the basis of agricultural income tax paid under the relevantprovincial law.

4. The amount shall be included in person’s income chargeable to tax in the tax yearto which such amount relates.

5. If the foreign remittance is received from outside Pakistan through normal bankingchannels which is encashed into rupee by a scheduled bank and certificate fromsuch bank is produced to that effect, the section 111 on such amount or assetscreated from such amount , shall not be applicable

Total Marks 10

Ans.4.

Name of Tax Payer : Mr. AKRAMNational Tax Number : XXXTax Year Ended : 30th June 2015Tax Year : 200APersonal Status : Individual, Non-SalariedResidential Status : Non-Resident

Taxable Income and Tax LiabilityTaxpayer has incomes under different heads. Their taxability is as below:

Contd…

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

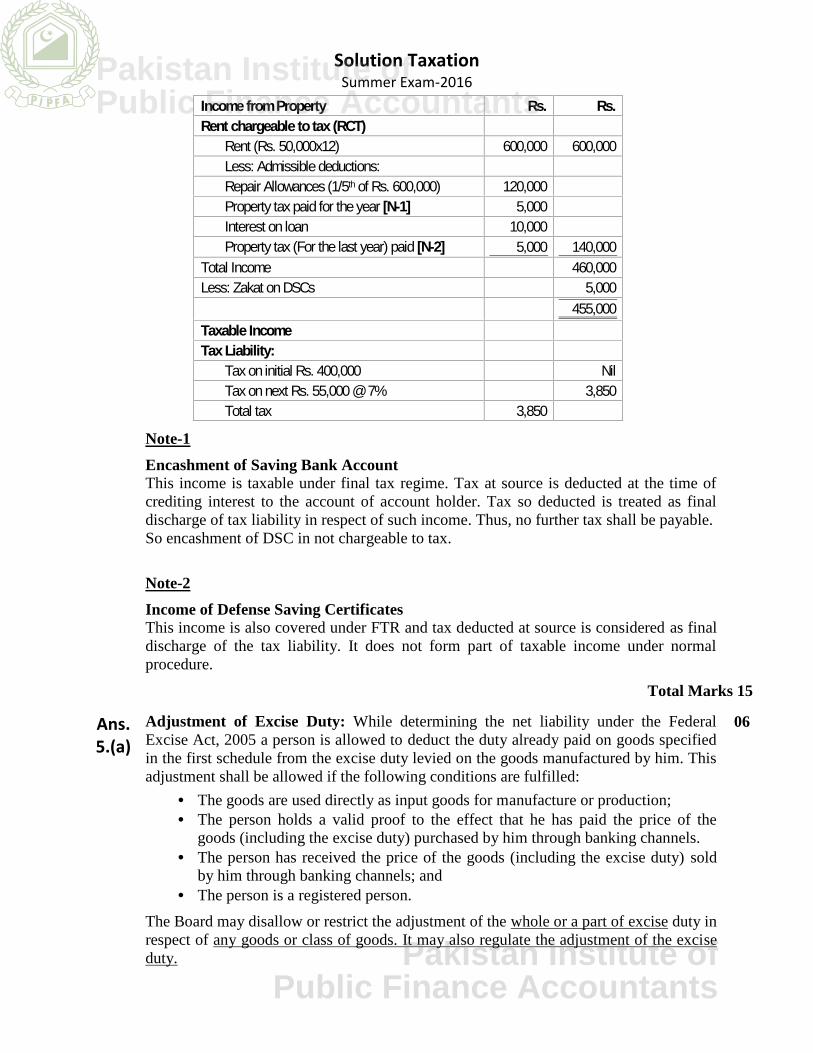

Solution TaxationSummer Exam-2016

Income from Property Rs. Rs.Rent chargeable to tax (RCT)

Rent (Rs. 50,000x12) 600,000 600,000Less: Admissible deductions:Repair Allowances (1/5th of Rs. 600,000) 120,000Property tax paid for the year [N-1] 5,000Interest on loan 10,000Property tax (For the last year) paid [N-2] 5,000 140,000

Total Income 460,000Less: Zakat on DSCs 5,000

455,000Taxable IncomeTax Liability:

Tax on initial Rs. 400,000 NilTax on next Rs. 55,000 @ 7% 3,850Total tax 3,850

Note-1

Encashment of Saving Bank AccountThis income is taxable under final tax regime. Tax at source is deducted at the time ofcrediting interest to the account of account holder. Tax so deducted is treated as finaldischarge of tax liability in respect of such income. Thus, no further tax shall be payable.So encashment of DSC in not chargeable to tax.

Note-2

Income of Defense Saving CertificatesThis income is also covered under FTR and tax deducted at source is considered as finaldischarge of the tax liability. It does not form part of taxable income under normalprocedure.

Total Marks 15

Ans.5.(a)

Adjustment of Excise Duty: While determining the net liability under the FederalExcise Act, 2005 a person is allowed to deduct the duty already paid on goods specifiedin the first schedule from the excise duty levied on the goods manufactured by him. Thisadjustment shall be allowed if the following conditions are fulfilled:

The goods are used directly as input goods for manufacture or production; The person holds a valid proof to the effect that he has paid the price of the

goods (including the excise duty) purchased by him through banking channels. The person has received the price of the goods (including the excise duty) sold

by him through banking channels; and The person is a registered person.

The Board may disallow or restrict the adjustment of the whole or a part of excise duty inrespect of any goods or class of goods. It may also regulate the adjustment of the exciseduty.

06

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution TaxationSummer Exam-2016

Ans.5.(b)

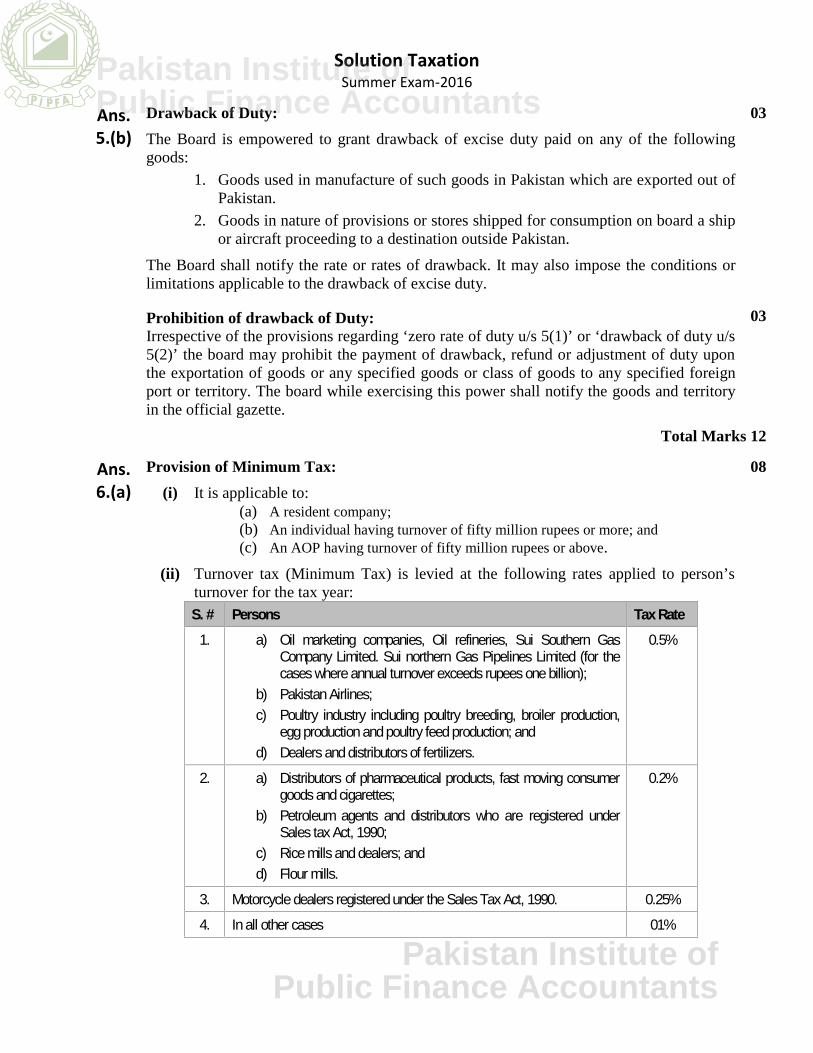

Drawback of Duty:

The Board is empowered to grant drawback of excise duty paid on any of the followinggoods:

1. Goods used in manufacture of such goods in Pakistan which are exported out ofPakistan.

2. Goods in nature of provisions or stores shipped for consumption on board a shipor aircraft proceeding to a destination outside Pakistan.

The Board shall notify the rate or rates of drawback. It may also impose the conditions orlimitations applicable to the drawback of excise duty.

Prohibition of drawback of Duty:Irrespective of the provisions regarding ‘zero rate of duty u/s 5(1)’ or ‘drawback of duty u/s5(2)’ the board may prohibit the payment of drawback, refund or adjustment of duty uponthe exportation of goods or any specified goods or class of goods to any specified foreignport or territory. The board while exercising this power shall notify the goods and territoryin the official gazette.

03

03

Total Marks 12

Ans.6.(a)

Provision of Minimum Tax:

(i) It is applicable to:(a) A resident company;(b) An individual having turnover of fifty million rupees or more; and(c) An AOP having turnover of fifty million rupees or above.

(ii) Turnover tax (Minimum Tax) is levied at the following rates applied to person’sturnover for the tax year:S. # Persons Tax Rate

1. a) Oil marketing companies, Oil refineries, Sui Southern GasCompany Limited. Sui northern Gas Pipelines Limited (for thecases where annual turnover exceeds rupees one billion);

b) Pakistan Airlines;c) Poultry industry including poultry breeding, broiler production,

egg production and poultry feed production; andd) Dealers and distributors of fertilizers.

0.5%

2. a) Distributors of pharmaceutical products, fast moving consumergoods and cigarettes;

b) Petroleum agents and distributors who are registered underSales tax Act, 1990;

c) Rice mills and dealers; andd) Flour mills.

0.2%

3. Motorcycle dealers registered under the Sales Tax Act, 1990. 0.25%4. In all other cases 01%

08

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution TaxationSummer Exam-2016

(iii) Where any of above referred persons has no tax liability under the normal taxprocedure is less than the tax as per above table, than the person shall be required topay this tax. In other words the tax liability of a person for any tax year shall be thehigher of the tax determine under NTR or tax computed by applying the above ratesto the person’s turnover for the tax year.

(iv) The reasons for no Tax Liability or less Tax Liability may be all or any of thefollowing:

(a) Sustaining of a loss;(b) Setting off of a loss of an earlier years;(c) Exemption from tax;(d) Application of credits or rebates; or(e) Claiming of allowances or deductions (including depreciation and

amortization) allowed under Income tax Ordinance or any other law.

“Tax payable or paid” does not include the tax already paid or payable in respect ofdeemed income which is covered under final tax regime (FTR).

(b) Benefits and Conditions of Section 65(B)

A tax credit equal to 10% of the amount invested by a company in purchase of plant andmachinery shall be allowed against the tax payable by it.

Other provisions in this regard are:

1. The plant and machinery is purchased by the company for purposes of extension,expansion, balancing, modernization and replacement (BMR) of the plant andmachinery already installed.

2. The plant and machinery is for an industrial undertaking set up in Pakistan and isowned by the company making the investment.

3. The plant and machinery should be purchased between 01-07-2010 and 30-06-2016.

4. The amount of tax credit shall be deducted from the tax for tax year in which plantor machinery.

5. Where there is no tax payable for the year in which plant or machinery is installedor tax payable for that year is less than the amount of tax credit, the unadjusted taxcredit shall be carried forward and deducted against tax payable for following taxyears.

6. The amount of unadjusted tax credit may be carried forward maximum for the two(2) tax years.

7. The Commissioner may re-compute the tax payable for the relevant tax payablefor the tax years if subsequently it is found by him that any of the above-referredconditions was not fulfilled. Under this case it shall be deemed that tax credit waswrongly allowed.

08

Total Marks 16

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution TaxationSummer Exam-2016

Ans.7.

Provisional Assessment 122 (C)

The Income Tax Ordinance, 2001 contain the two different sections regarding to provisionalassessment. These sections deal with two different situations in which the commissionermay make provisional assessment order. Each of these provisions is below:

Provisional assessment for non-filing of return [122(C)]

The commissioner may makes the provision assessment if a person fails to furnish a returnof income in response to a notice issued by the commissioner u/s 114 (3) and 114(4) of theincome tax ordinance, 2001. Other provision in this regard is:

1. The Commissioner shall make the provisional assessment on the basis of anyavailable information of material and to the best of his judgment.

2. The provisional assessment order shall specify the assessed taxable income andamount of tax due.

3. The provisional assessment shall be treated as final assessment after the expiryof forty – five (45) days from the date of service of provisional assessment order.

4. The provisional assessment shall not be treated as final assessment if the person(being an individual or an AOP) files the following documents within the above–referred period of forty-five (45) days:

(i) A Wealth Statement;

(ii) A Wealth Reconciliation Statement ; and

(iii) An explanation of Source of Assets or Income

The provisional assessment shall not be treated as final assessment if the companyelectronically files the return of income along with audited account or final within the above–referred period forty-five (45) days.

Provisional Assessment for Concealed Assets 123

Where the taxpayer has a concealed assets and that asset is impounded by any governmentdepartment or agency, the commissioner may make an order assessing there in the taxableincome and the tax liability of the taxpayer. This assessment is subject to the followingconditions:

1. A provisional assessment may be made before an assessment or amendedassessment is made u/s 121 or 122.

2. It is to be made in writing

3. The commissioner shall finalize the provisional assessment as soon as practicable

4. It is made on basis on the value of the ‘concealed asset’.5. The provisional assessment order is issued for the last completed tax year.

07

03

Total Marks 10

Ans.8.

ASSESSMENT OF TAX U/S 11 OF SALES TAX ACT 1990

Under the following circumstances, an authorized officer of Inland Revenue shall make anorder for assessment of tax, including imposition of penalty and default surcharge:

Pakistan Institute ofPublic Finance Accountants

Pakistan Institute ofPublic Finance Accountants

Solution TaxationSummer Exam-2016

1. Where a person who is required to file a return has failed to file it by due date;

2. Where a person, due to some miscalculations, pays a lesser amount than actuallypayable;

3. Where a has not paid the tax due on supplies made by him;

4. Where a person has claimed a credit or refund of an input tax which was notadmissible under the Sales Tax Act, 1990;

5. Where by reasons of some collusion or a deliberate act any tax or charge has notbeen levied or made or has been short-levied or has been erroneously refunded;

6. Where by reason of any inadvertence, error or misconstruction, any tax or chargehas not been levied or made or short-levied or has been erroneously refunded.

The officer of Inland Revenue shall give a show-cause notice within five years and providean opportunity of being heard to a person before making an order for assessment of tax, etc.Where a person files the return after a due date and pays the amount of tax payable alongwith default surcharge and penalty, the show-cause notice and the order of assessment shallabate.

Provided: