Embed Size (px)

Citation preview

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A

FINAL (July 30, 2010)

MODEL INSURANCE FINANCIAL STATEMENTS

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A

FINAL (July 30, 2010)

MICPA STATEMENT MODEL INSURANCE FINANCIAL STATEMENTS

The Council of the Institute has approved the publication of this Statement, Model Insurance Financial Statements for members’ guidance. The Model Insurance Financial Statements have incorporated accounting standards issued and pronouncements announced by the Malaysian Accounting Standards Board (MASB) up to October 1, 2009. ------------------------------------------------------------------------------------------------------------------------------------------------------- ACKNOWLEDGEMENT

Special appreciation is expressed to the following persons for their contributions and technical input towards the production of the Model Insurance Financial Statements: Mr Ken Pushpanathan (Chairman)

Ms Chong Kooi Wah / Ms Tong Seuk Ying (Project Managers)

Mr Koh Kong Yong / Ms Avinder Sandhu / Ms Toh Ying Ying / Mr Peter Lee Eng Boon / Cik Wan Malawati Wan Mansor

(Bank Negara Malaysia)

Ms Tan Bee Leng / Ms Stephanie Lip / Cik Mas Sukmawati / Ms Wong Chee Cheng

(Malaysian Accounting Standards Board)

Ms Rachel Chee / Mr Lim Kian Tong (Malaysian Institute of Accountants)

Mr Tang Loon Koon (Life Insurance Association of Malaysia)

Mr Clarence Heng (Persatuan Insurans Am Malaysia)

En Muhammad Fikri Mohamad Rawi / Ms Maggie Chong Cik Noraidawati Hanapi

(Malaysia Takaful Association)

Mr Teh Loo Hai (Teh Actuarial Services Sdn Bhd)

Ms Teoh Bee Lan (Malaysian Re-Insurance Berhad)

Mr Gan Hock Soon / Mr Lum Chiew Mun (BDO Binder)

Mr Brandon Bruce Sta Maria (Ernst & Young)

Mr Alex Khaw / Mr Loh Kam Hian (KPMG)

Mr Tang Kin Kheong / Mr Francis Joseph (Mazars)

Mr Sridharan Nair / Ms Choo Mei Ping / Ms Chan Suit Lye (PricewaterhouseCoopers)

Copyright @ July 2010 by The Malaysian Institute of Certified Public Accountants (MICPA). All rights reserved. No part of this publication may be reproduced, stored in retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise without the prior permission of the MICPA. This Statement is published by The Malaysian Institute of Certified Public Accountants (3246 – U) No. 15, Jalan Medan Tuanku, 50300 Kuala Lumpur, Malaysia Tel No : 03-2698 9622 Fax No : 03-2698 9403 E-mail : [email protected] Website : www.micpa.com.my

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A

FINAL (July 30, 2010)

M O D E L I N S U R A N C E B E R H A D ( 8 8 2 0 0 9 - A )

(Incorporated in Malaysia)

Directors‟ Report and Audited Financial Statements

31 December 2010

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A

FINAL (July 30, 2010)

CONTENTS PAGE

Directors’ report 1 - 4

Statement by directors 5

Statutory declaration 5

Independent auditors' report 6 - 7

Balance sheet 8

Income statement 9

Statement of comprehensive income 10

Statement of changes in equity 11

Cash flow statement 12

Notes to the financial statements 13 - 78

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A

DIRECTORS' REPORT FINAL (July 30, 2010)

- 1 -

DIRECTORS' REPORT CA169(5)-(13)

The Directors have pleasure in presenting their report together with the audited financial statements of the Company for the financial year ended 31 December 2010.

169(5)

PRINCIPAL ACTIVITIES

The Company is engaged principally in the underwriting of life insurance and general insurance business.

169(6)(b) 101.126(b)

There have been no significant changes in the nature of the principal activities during the financial year.

RESULTS RM‟000

Net profit for the year 9,464 169(6)(c)

There were no material transfers to or from reserves or provisions during the financial year other than as disclosed in the financial statements.

169(6)(d)

In the opinion of the Directors, the results of the operations of the Company during the financial year were not substantially affected by any item, transaction or event of a material and unusual nature.

169(6)(p) 169(7)

DIVIDENDS

The amount of dividends* declared and paid by the Company since the end of the previous financial year were as follows:

169(6)(h)

RM‟000

In respect of the financial year ended 31 December 2009 as reported in the Directors’ Report of that year:

Final dividend of 3.9% less 25% taxation, on 100,000,000 Ordinary Shares, declared on 30 April 2010 and paid on 5 May 2010

2,960

[* Insert particulars for declaration and payment of Interim dividends, if applicable.

In respect of the financial year ended 31 December 2010: Interim dividend of X% less 25% taxation, on 100,000,000 Ordinary Shares, declared on dd/mm 2010 and paid on dd/mm 2010

XXX]

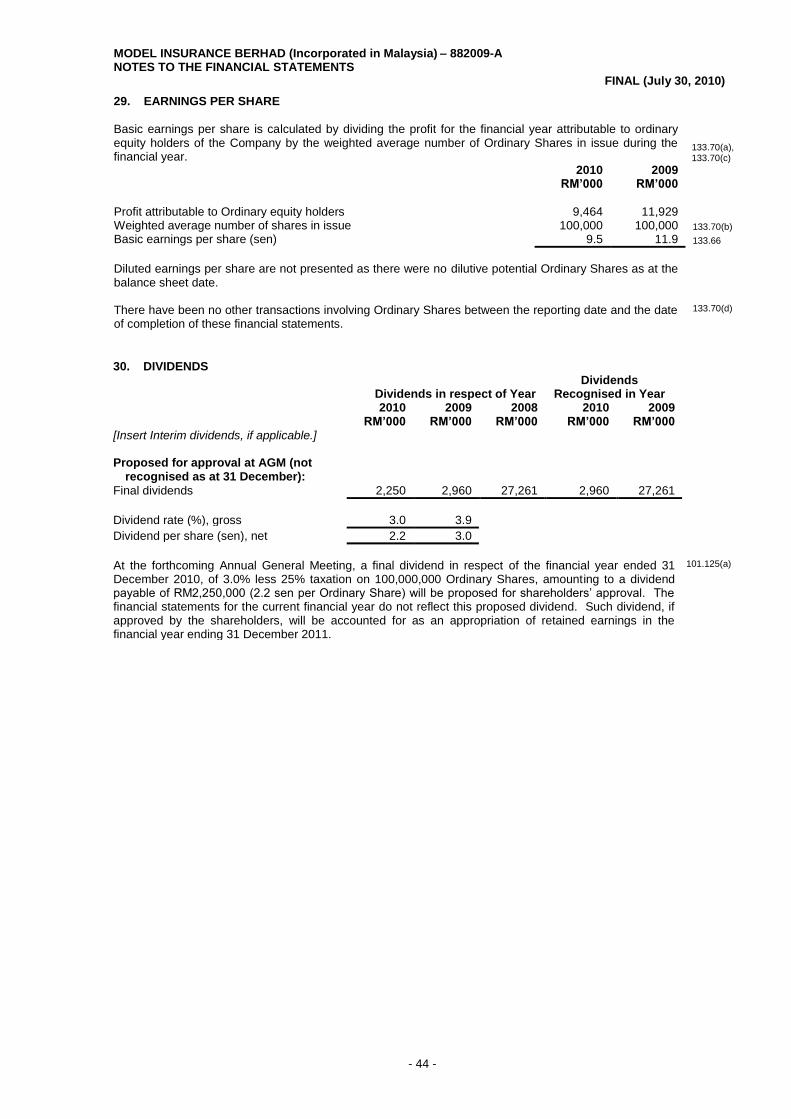

At the forthcoming Annual General Meeting, a Final dividend in respect of the financial year ended 31 December 2010, of 3.0% less 25% taxation on 100,000,000 Ordinary Shares, amounting to a dividend payable of RM2,250,000 (2.2 sen net per Ordinary Share) will be proposed for shareholders’ approval. The financial statements for the current financial year do not reflect this proposed dividend. Such dividend, if approved by the shareholders, will be accounted for in equity as an appropriation of retained earnings in the financial year ending 31 December 2011.

110.12 110.13

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A

DIRECTORS' REPORT FINAL (July 30, 2010)

- 2 -

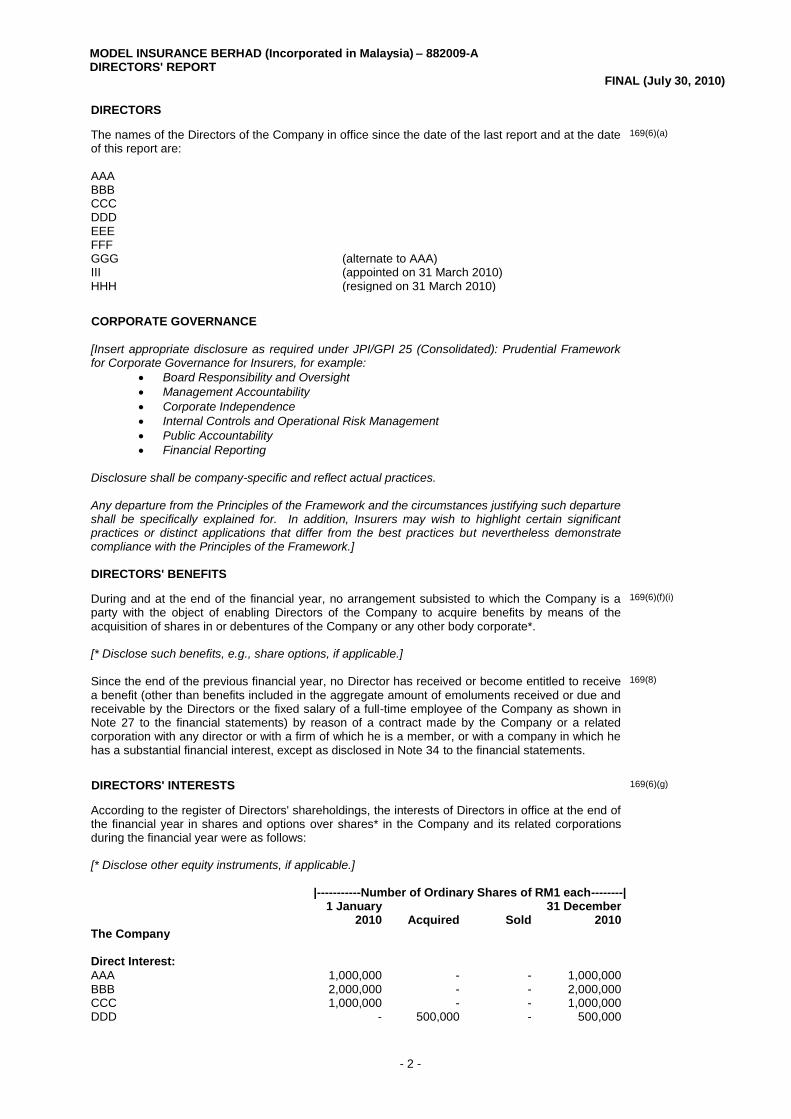

DIRECTORS

The names of the Directors of the Company in office since the date of the last report and at the date of this report are:

169(6)(a)

AAA BBB CCC DDD EEE FFF GGG (alternate to AAA) III (appointed on 31 March 2010) HHH (resigned on 31 March 2010)

CORPORATE GOVERNANCE

[Insert appropriate disclosure as required under JPI/GPI 25 (Consolidated): Prudential Framework for Corporate Governance for Insurers, for example:

Board Responsibility and Oversight

Management Accountability

Corporate Independence

Internal Controls and Operational Risk Management

Public Accountability

Financial Reporting Disclosure shall be company-specific and reflect actual practices. Any departure from the Principles of the Framework and the circumstances justifying such departure shall be specifically explained for. In addition, Insurers may wish to highlight certain significant practices or distinct applications that differ from the best practices but nevertheless demonstrate compliance with the Principles of the Framework.]

DIRECTORS' BENEFITS

During and at the end of the financial year, no arrangement subsisted to which the Company is a party with the object of enabling Directors of the Company to acquire benefits by means of the acquisition of shares in or debentures of the Company or any other body corporate*. [* Disclose such benefits, e.g., share options, if applicable.]

169(6)(f)(i)

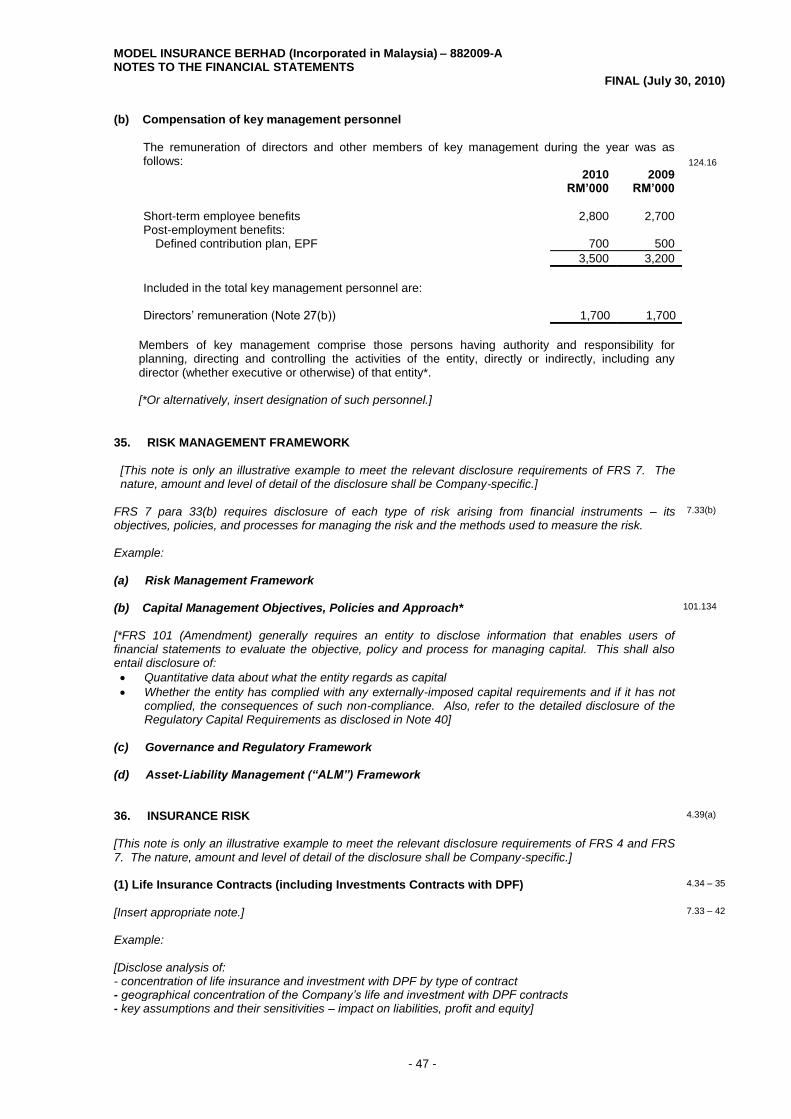

Since the end of the previous financial year, no Director has received or become entitled to receive a benefit (other than benefits included in the aggregate amount of emoluments received or due and receivable by the Directors or the fixed salary of a full-time employee of the Company as shown in Note 27 to the financial statements) by reason of a contract made by the Company or a related corporation with any director or with a firm of which he is a member, or with a company in which he has a substantial financial interest, except as disclosed in Note 34 to the financial statements.

169(8)

DIRECTORS' INTERESTS 169(6)(g)

According to the register of Directors' shareholdings, the interests of Directors in office at the end of the financial year in shares and options over shares* in the Company and its related corporations during the financial year were as follows: [* Disclose other equity instruments, if applicable.]

|-----------Number of Ordinary Shares of RM1 each--------| 1 January

2010

Acquired

Sold 31 December

2010

The Company Direct Interest: AAA 1,000,000 - - 1,000,000 BBB 2,000,000 - - 2,000,000 CCC 1,000,000 - - 1,000,000 DDD - 500,000 - 500,000

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A

DIRECTORS' REPORT FINAL (July 30, 2010)

- 3 -

|----------Number of Ordinary Shares of RM1 each----------| 1 January

2010

Acquired

Sold 31 December

2010

The Company Deemed Interest * AAA 500,000 - - 500,000 Holding Company Ins Holdings Berhad Direct Interest: AAA 250,000 - - 250,000

Other than as disclosed, none of the Directors in office at the end of the financial year had any interest in shares in the Company or its related corporations during the financial year.

[* In accordance with the requirements of Section 134 of the Companies Act, 1965 (as amended).] OTHER STATUTORY INFORMATION

(a) Before the balance sheet and income statement of the Company were made out, the Directors

took reasonable steps:

(i) to ascertain that proper action had been taken in relation to the writing off of bad debts

and the making of provision for doubtful debts and satisfied themselves that all known bad debts had been written off and that adequate provision had been made for doubtful debts; and

169(6)(i)

(ii) to ensure that any current assets which were unlikely to realise their value as shown in

the accounting records in the ordinary course of business had been written down to an amount which they might be expected so to realise.

169(6)(k)

(b) At the date of this report, the Directors are not aware of any circumstances which would render:

(i) the amount written off for bad debts or the amount of the provision for doubtful debts in

the financial statements of the Company inadequate to any substantial extent; and

169(6)(j)

(ii) the values attributed to the current assets in the financial statements of the Company

misleading.

169(6)(l)(i)

(c) At the date of this report, the Directors are not aware of any circumstances which have arisen

which would render adherence to the existing method of valuation of assets or liabilities of the Company misleading or inappropriate.

169(6)(l)(ii)

(d) At the date of this report, the Directors are not aware of any circumstances not otherwise dealt

with in this report or financial statements of the Company which would render any amount stated in the financial statements misleading.

169(6)(o)

(e) As at the date of this report, there does not exist:

(i) any charge on the assets of the Company which has arisen since the end of the financial year which secures the liabilities of any other person; or

169(6)(m)(i)

(ii) any contingent liability of the Company which has arisen since the end of the financial

year.

169(6)(m)(ii)

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A

DIRECTORS' REPORT FINAL (July 30, 2010)

- 4 -

(f) In the opinion of the Directors:

(i) no contingent or other liability has become enforceable or is likely to become enforceable within the period of twelve months after the end of the financial year which will or may affect the ability of the Company to meet its obligations when they fall due; and

169(6)(n)

(ii) no item, transaction or event of a material and unusual nature has arisen in the interval

between the end of the financial year and the date of this report which is likely to affect substantially the results of the operations of the Company for the financial year in which this report is made.

169(6)(q)

For the purpose of paragraphs (e) and (f), contingent and other liabilities do not include liabilities arising from contracts of insurance underwritten in the ordinary course of business of the Company.

(g) Before the income statement and balance sheet of the Company were made out, the Directors

took reasonable steps to ascertain that there was adequate provision for its insurance liabilities in accordance with the valuation methods specified in the risk-based capital framework for insurers issued by Bank Negara Malaysia.

AUDITORS

The Auditors, XYZ & Co., have expressed their willingness to continue in office. 172(2)

Signed on behalf of the Board in accordance with a resolution of the Directors dated dd/mm/yyyy. 169(5)

AAA CCC

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A

FINAL (July 30, 2010)

- 5 -

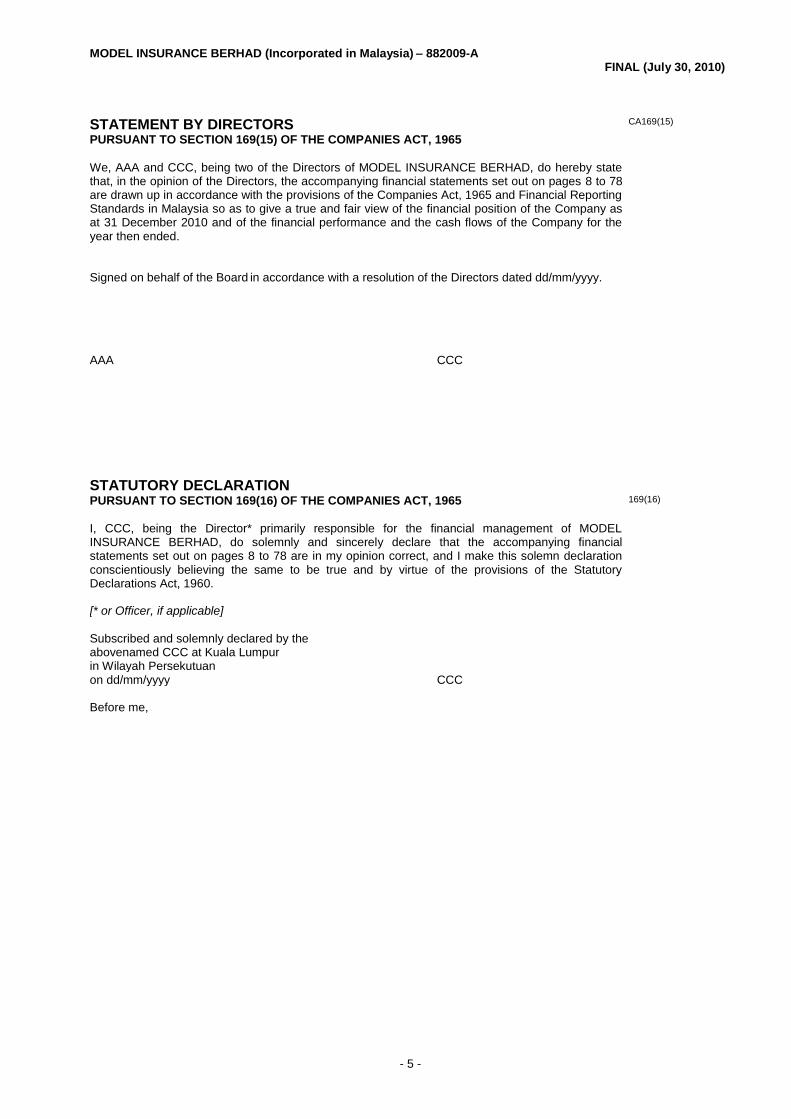

STATEMENT BY DIRECTORS CA169(15)

PURSUANT TO SECTION 169(15) OF THE COMPANIES ACT, 1965

We, AAA and CCC, being two of the Directors of MODEL INSURANCE BERHAD, do hereby state that, in the opinion of the Directors, the accompanying financial statements set out on pages 8 to 78 are drawn up in accordance with the provisions of the Companies Act, 1965 and Financial Reporting Standards in Malaysia so as to give a true and fair view of the financial position of the Company as at 31 December 2010 and of the financial performance and the cash flows of the Company for the year then ended.

Signed on behalf of the Board in accordance with a resolution of the Directors dated dd/mm/yyyy. AAA CCC

STATUTORY DECLARATION PURSUANT TO SECTION 169(16) OF THE COMPANIES ACT, 1965 169(16)

I, CCC, being the Director* primarily responsible for the financial management of MODEL INSURANCE BERHAD, do solemnly and sincerely declare that the accompanying financial statements set out on pages 8 to 78 are in my opinion correct, and I make this solemn declaration conscientiously believing the same to be true and by virtue of the provisions of the Statutory Declarations Act, 1960.

[* or Officer, if applicable]

Subscribed and solemnly declared by the abovenamed CCC at Kuala Lumpur in Wilayah Persekutuan on dd/mm/yyyy CCC Before me,

FINAL (July 30, 2010)

- 6 -

INDEPENDENT AUDITORS‟ REPORT TO THE MEMBERS OF CA174(2)

MODEL INSURANCE BERHAD (Incorporated in Malaysia) Report on the Financial Statements

We have audited the financial statements of MODEL INSURANCE BERHAD, which comprise the balance sheet as at 31 December 2010 of the Company, the income statement, statement of changes in equity and cash flow statement of the Company for the year then ended, and a summary of significant policies and explanatory notes, as set out on pages 8 to 78.

Directors‟ Responsibility for the Financial Statements

The Directors of the Company are responsible for the preparation and fair presentation of these financial statements in accordance with Financial Reporting Standards and the Companies Act, 1965 in Malaysia. This responsibility includes: designing, implementing and maintaining internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

Auditors‟ Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with Approved Standards on Auditing in Malaysia. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on our judgement, including the assessment of risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, we consider internal control relevant to the Company’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control. An audit also includes evaluating the appropriateness of the accounting policies used and the reasonableness of accounting estimates made by the Directors, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the financial statements have been properly drawn up in accordance with Financial Reporting Standards and the Companies Act, 1965 in Malaysia so as to give a true and fair view of the financial position of the Company as at 31 December 2010 and of its financial performance and cash flows of the Company for the year then ended.

174(2)(a)

Reporting on Other Legal and Regulatory Requirements

In accordance with the requirements of the Companies Act, 1965 in Malaysia, we also report that in our opinion, the accounting and other records and the registers required by the Act to be kept by the Company have been properly kept in accordance with the provisions of the Act.

174(2)(b)

FINAL (July 30, 2010)

- 7 -

INDEPENDENT AUDITORS‟ REPORT TO THE MEMBERS OF

MODEL INSURANCE BERHAD

(Incorporated in Malaysia)

Other Matters

This report is made solely to the members of the Company, as a body, in accordance with Section 174 of the Companies Act, 1965 in Malaysia and for no other purpose. We do not assume responsibility to any other person for the content of this report.

XYZ & Co. XYZ AF: 0888 No. 1888/08/12(J/PH) Chartered Accountants Chartered Accountant

Kuala Lumpur, Malaysia dd/mm/yyyy

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A

FINAL (July 30, 2010)

- 8 -

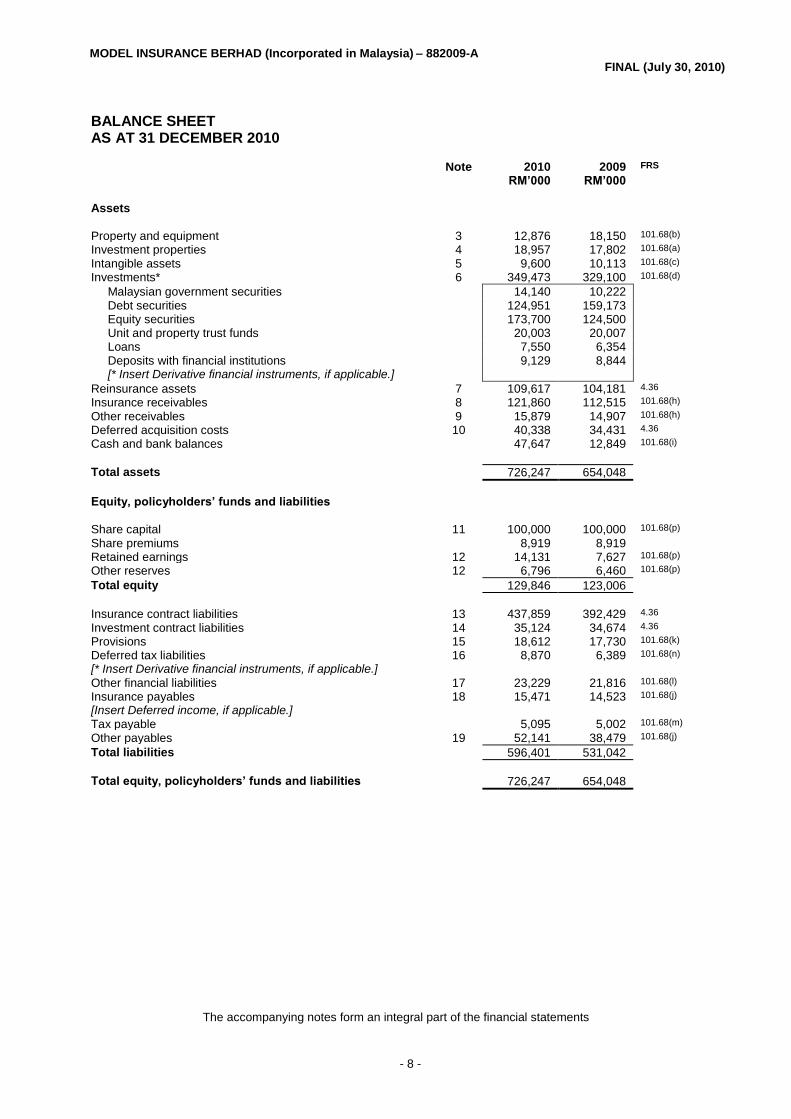

BALANCE SHEET

AS AT 31 DECEMBER 2010

Note 2010 2009 FRS

RM‟000 RM‟000 Assets

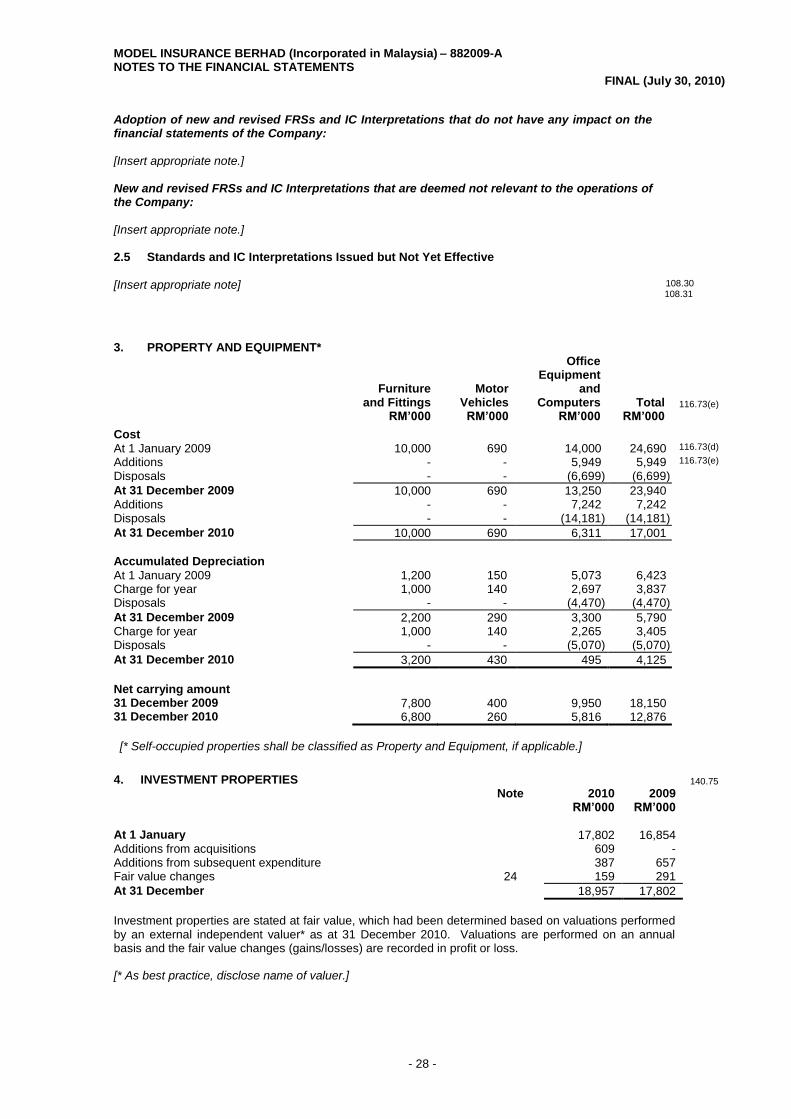

Property and equipment 3 12,876 18,150 101.68(b)

Investment properties 4 18,957 17,802 101.68(a)

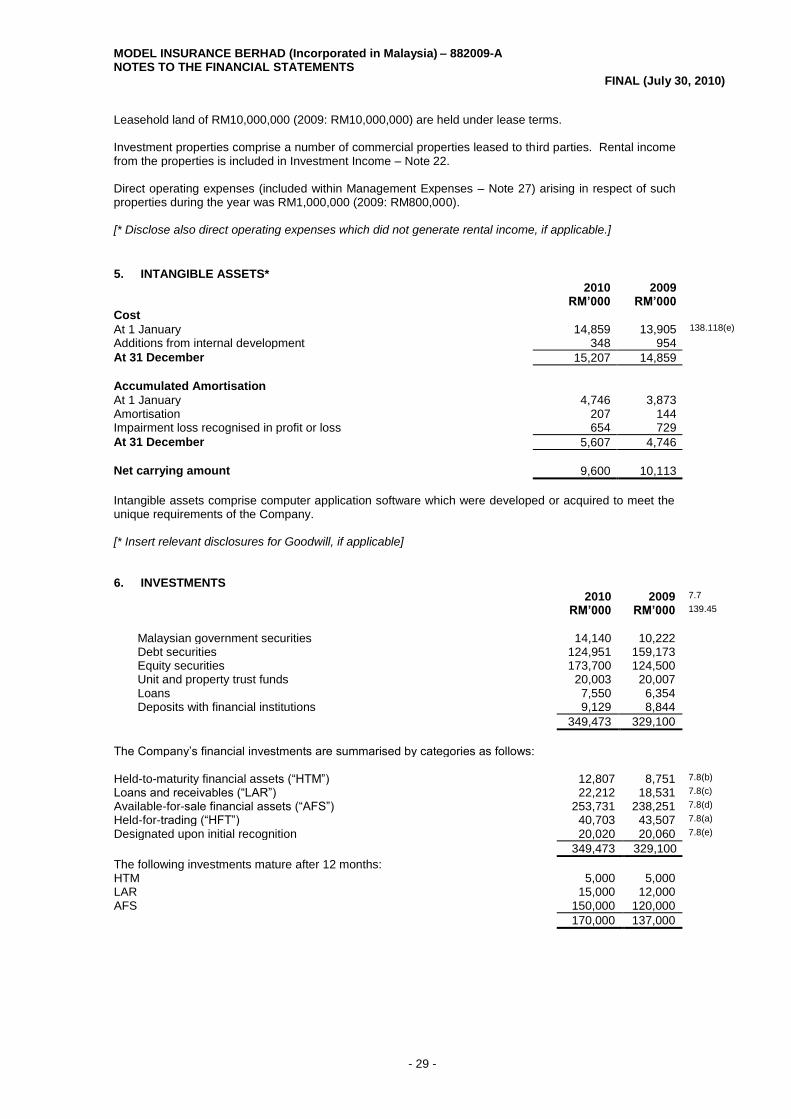

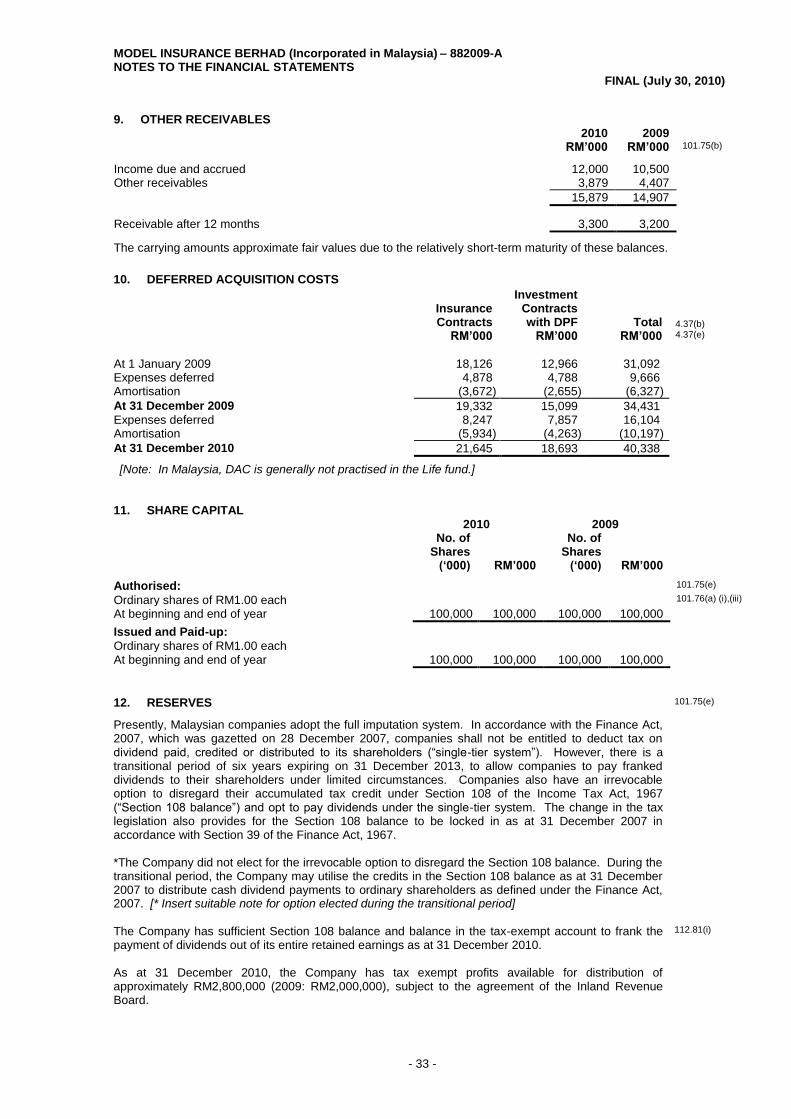

Intangible assets 5 9,600 10,113 101.68(c)

Investments* 6 349,473 329,100 101.68(d)

Malaysian government securities 14,140 10,222 Debt securities 124,951 159,173 Equity securities 173,700 124,500 Unit and property trust funds 20,003 20,007 Loans 7,550 6,354 Deposits with financial institutions 9,129 8,844 [* Insert Derivative financial instruments, if applicable.]

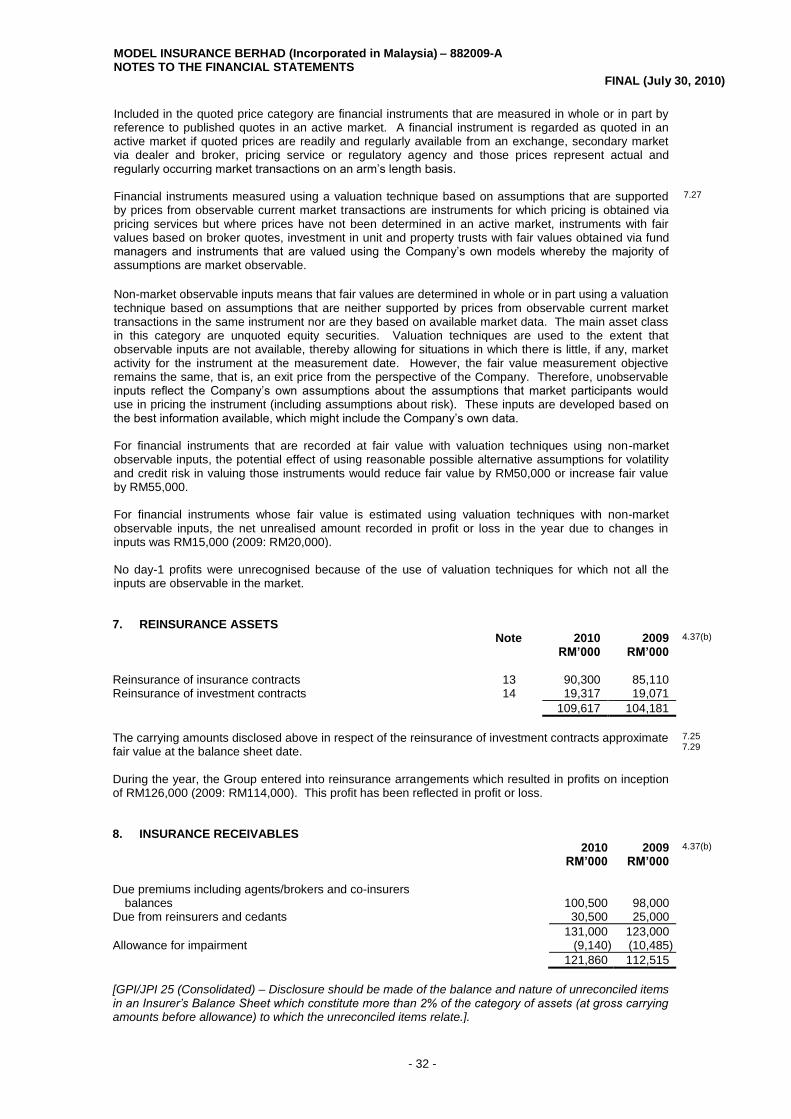

Reinsurance assets 7 109,617 104,181 4.36

Insurance receivables 8 121,860 112,515 101.68(h)

Other receivables 9 15,879 14,907 101.68(h)

Deferred acquisition costs 10 40,338 34,431 4.36

Cash and bank balances 47,647 12,849 101.68(i)

Total assets 726,247 654,048

Equity, policyholders‟ funds and liabilities

Share capital 11 100,000 100,000 101.68(p)

Share premiums 8,919 8,919 Retained earnings 12 14,131 7,627 101.68(p)

Other reserves 12 6,796 6,460 101.68(p)

Total equity 129,846 123,006

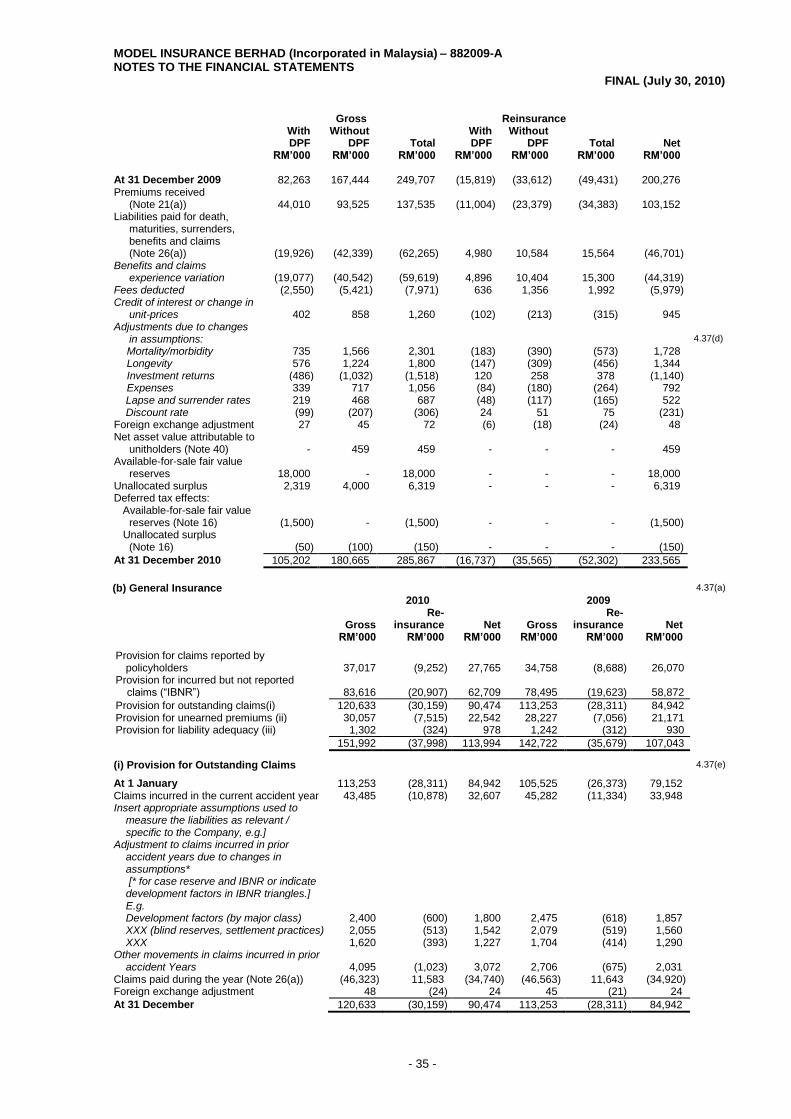

Insurance contract liabilities 13 437,859 392,429 4.36

Investment contract liabilities 14 35,124 34,674 4.36

Provisions 15 18,612 17,730 101.68(k)

Deferred tax liabilities 16 8,870 6,389 101.68(n)

[* Insert Derivative financial instruments, if applicable.] Other financial liabilities 17 23,229 21,816 101.68(l)

Insurance payables 18 15,471 14,523 101.68(j)

[Insert Deferred income, if applicable.] Tax payable 5,095 5,002 101.68(m)

Other payables 19 52,141 38,479 101.68(j)

Total liabilities 596,401 531,042

Total equity, policyholders‟ funds and liabilities 726,247 654,048

The accompanying notes form an integral part of the financial statements

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A

FINAL (July 30, 2010)

- 9 -

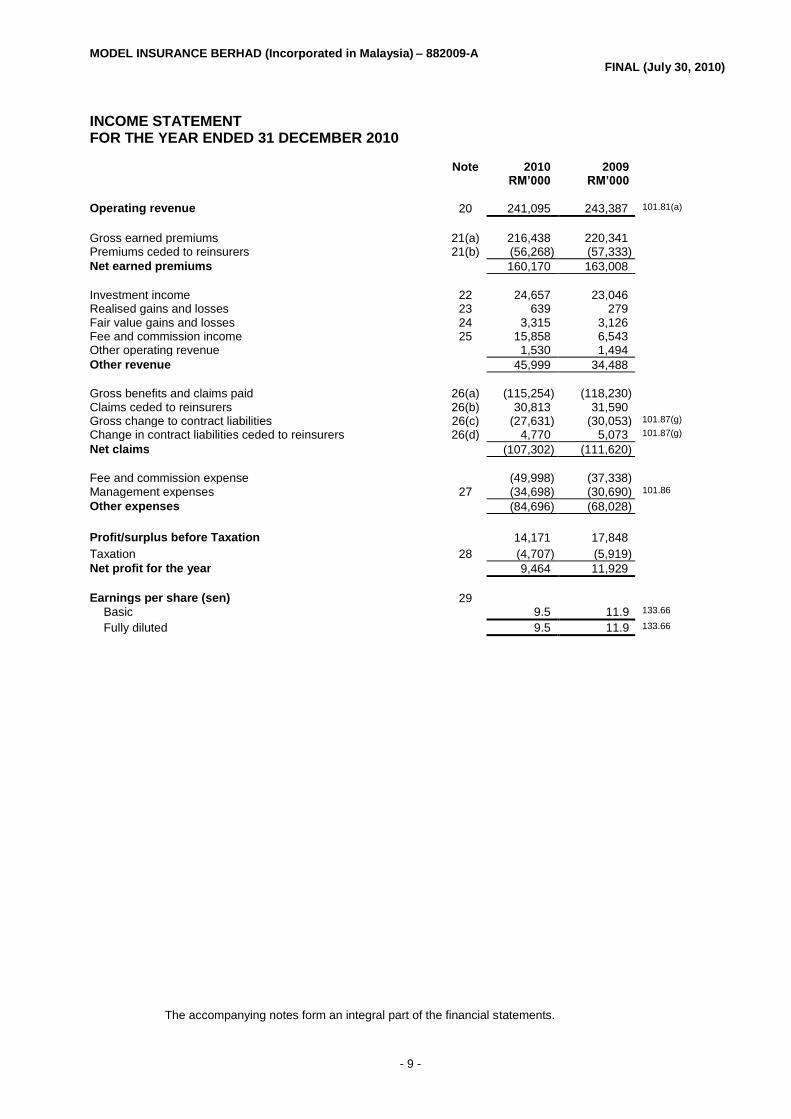

INCOME STATEMENT FOR THE YEAR ENDED 31 DECEMBER 2010

Note 2010 2009

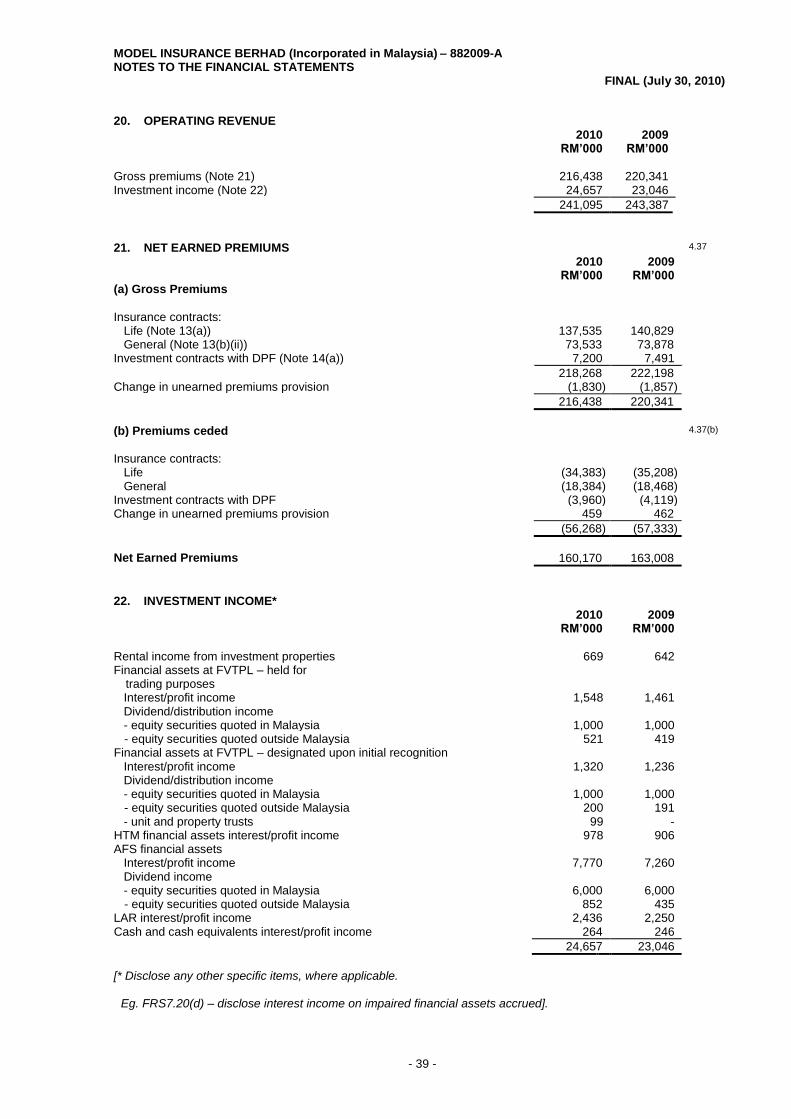

RM‟000 RM‟000 Operating revenue 20 241,095 243,387 101.81(a)

Gross earned premiums 21(a) 216,438 220,341 Premiums ceded to reinsurers 21(b) (56,268) (57,333)

Net earned premiums 160,170 163,008

Investment income 22 24,657 23,046 Realised gains and losses 23 639 279 Fair value gains and losses 24 3,315 3,126 Fee and commission income 25 15,858 6,543 Other operating revenue 1,530 1,494

Other revenue 45,999 34,488

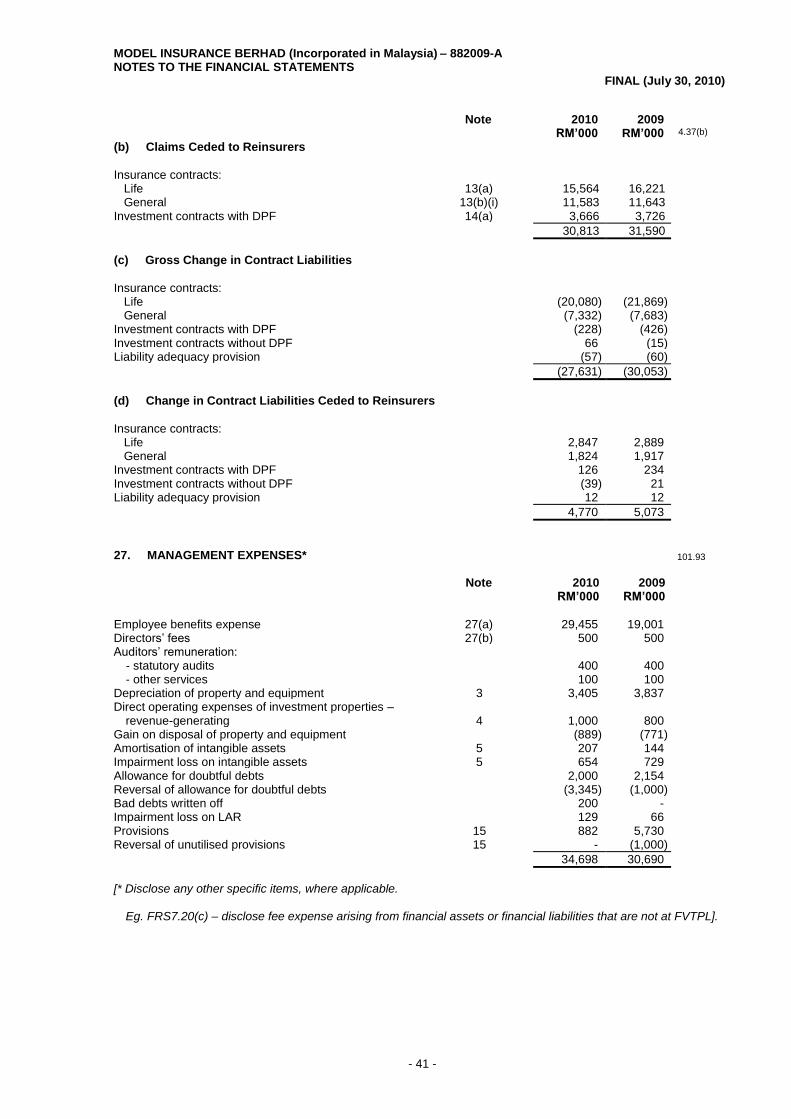

Gross benefits and claims paid 26(a) (115,254) (118,230) Claims ceded to reinsurers 26(b) 30,813 31,590 Gross change to contract liabilities 26(c) (27,631) (30,053) 101.87(g)

Change in contract liabilities ceded to reinsurers 26(d) 4,770 5,073 101.87(g)

Net claims (107,302) (111,620)

Fee and commission expense (49,998) (37,338) Management expenses 27 (34,698) (30,690) 101.86

Other expenses (84,696) (68,028)

Profit/surplus before Taxation 14,171 17,848

Taxation 28 (4,707) (5,919)

Net profit for the year 9,464 11,929

Earnings per share (sen) 29

Basic 9.5 11.9 133.66

Fully diluted 9.5 11.9 133.66

The accompanying notes form an integral part of the financial statements.

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A

FINAL (July 30, 2010)

- 10 -

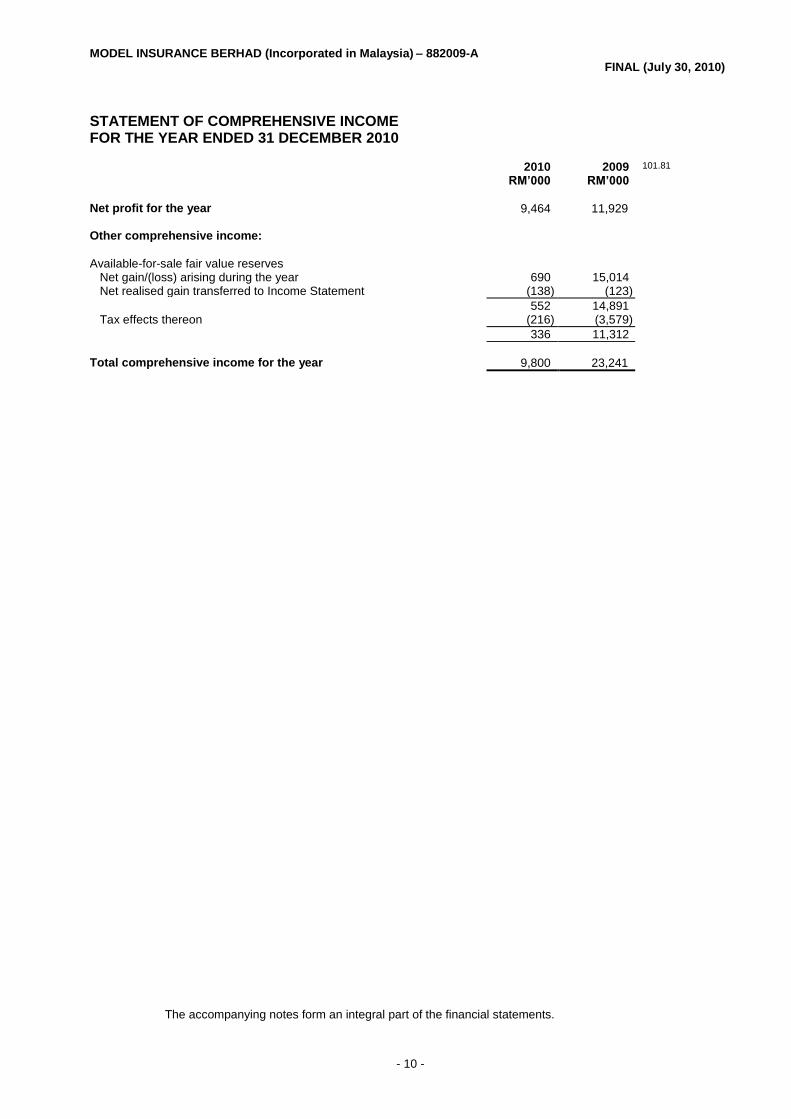

STATEMENT OF COMPREHENSIVE INCOME FOR THE YEAR ENDED 31 DECEMBER 2010

2010 2009 101.81

RM‟000 RM‟000 Net profit for the year 9,464 11,929 Other comprehensive income: Available-for-sale fair value reserves Net gain/(loss) arising during the year 690 15,014 Net realised gain transferred to Income Statement (138) (123)

552 14,891 Tax effects thereon (216) (3,579)

336 11,312

Total comprehensive income for the year 9,800 23,241

The accompanying notes form an integral part of the financial statements.

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A

FINAL (July 30, 2010)

- 11 -

STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 31 DECEMBER 2010

|-----Non-Distributable-----| Distributable

Share Capital

Share Premiums

Available-for-sale Fair

Value Reserves*

Retained Earnings

Total Equity

Note (Note 11) (Note 12)

RM‟000 RM‟000 RM‟000 RM‟000 RM‟000

At 1 January 2009 100,000 8,919 (4,852) 22,959 127,026 101.97(b)&(c)

Total comprehensive income for the year - - 11,312 11,929 23,241

Dividends paid during the year 30 - - - (27,261) (27,261) 101.97(a)

At 31 December 2009 100,000 8,919 6,460 7,627 123,006

At 1 January 2010 100,000 8,919 6,460 7,627 123,006

Total comprehensive income for the year - - 336 9,464 9,800

Dividends paid during the year 30 - - - (2,960) (2,960) 101.97(a)

At 31 December 2010 100,000 8,919 6,796 14,131 129,846

[* Insert additional columns for Other Reserves, if applicable. E.g., there may be Cash Flow Hedging Reserve if Hedge Accounting is applied.]

The accompanying notes form an integral part of the financial statements.

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A FINAL (July 30, 2010))

- 12 -

CASH FLOW STATEMENT FOR THE YEAR ENDED 31 DECEMBER 2010

Note 2010 2009

RM‟000 RM‟000

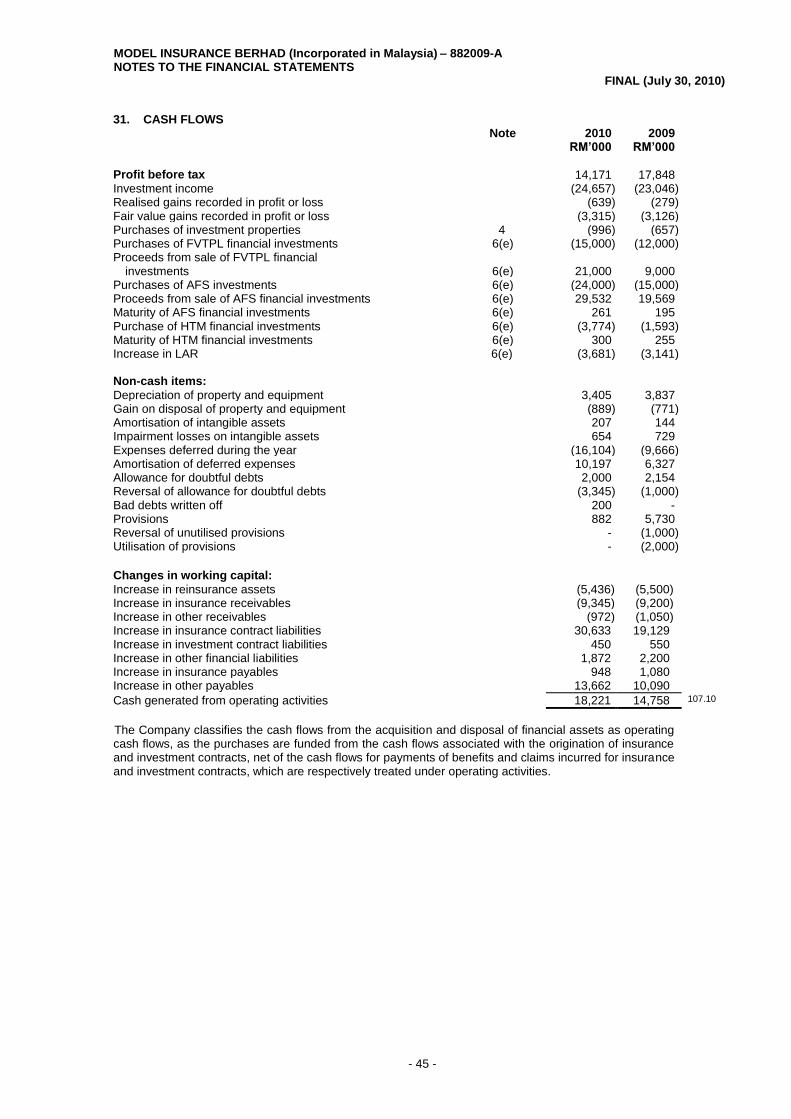

Operating Activities* 107.10

Cash generated from operating activities 31 18,221 14,758 107.10

Dividend/distribution income received 8,500 9,090 107.33

Interest/profit income received 12,027 14,200 107.33

Rental income on investment properties received 650 600

Income tax paid (4,050) (5,500) 107.35

Net cash flows from operating activities 35,348 33,148

Investing Activities 107.10

Proceeds from disposal of property and equipment 10,000 3,000 107.16

Purchase of property and equipment 3 (7,242) (5,949) 107.16 Purchase of intangibles 5 (348) (954) 107.16 Net cash flows from investing activities 2,410 (3,903)

Financing Activities 107.10

Dividends paid to equity holders 30 (2,960) (27,261) 107.31

Net cash flows from financing activities (2,960) (27,261)

Net increase in cash and cash equivalents 34,798 1,984

Cash and cash equivalents at beginning of year 12,849 10,865

Cash and cash equivalents at end of year 47,647 12,849 107.45

Cash and cash equivalents comprise:

Fixed and call deposits (with maturity of less than three months): CA Sch 9(m)(vii)

Licensed financial institutions 2,000 1,000

Others - 1,000

Cash and bank balances 45,647 10,849

47,647 12,849 107.45

Cash and cash equivalents of the Life fund of RM27,818,000 (2009: RM9,934,000) are not available for the general use of the Company other than to meet the obligations under the insurance fund).

[* If the direct method is used, disclosures in accordance with FRS4.37(b) is required.]

The accompanying notes form an integral part of the financial statements.

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A NOTES TO THE FINANCIAL STATEMENTS

FINAL (July 30, 2010)

- 13 -

NOTES TO THE FINANCIAL STATEMENTS FRS

31 DECEMBER 2010 101.8(e), 101.103

1. CORPORATE INFORMATION

The Company is an unquoted public limited liability company, incorporated and domiciled in Malaysia. The registered office of the Company is located at Level 8, Plaza Model, Jalan Model, 50088 Kuala Lumpur.

101.126(a)

The immediate and ultimate holding company of the Company is Ins Holdings Bhd., which is incorporated in Malaysia and produces financial statements available for public use.

101.126(c)

The Company is engaged in the underwriting of life insurance and general insurance business. There have been no significant changes in the nature of the principal activities during the financial year.

101.126(b)

The financial statements were authorised for issue by the Board of Directors in accordance with a resolution of the directors on dd/mm/yyyy.

110.17

2. SIGNIFICANT ACCOUNTING POLICIES

2.1 Basis of Preparation 110.14

The financial statements comply with the Financial Reporting Standards (“FRS”) in Malaysia and the provisions of the Companies Act, 1965, the Insurance Act, 1996 and Guidelines/Circulars issued by Bank Negara Malaysia (“BNM”).

At the beginning of the current financial year, the Company had adopted new and revised FRSs which are mandatory for financial periods beginning on or after 1 January 2010 as described fully in Note 2.4.

101.105(a)

The financial statements of the Company have also been prepared on a historical cost basis, except for investment properties and those financial instruments that have been measured at their fair values and insurance liabilities in accordance with the valuation methods specified in the risk-based capital framework for insurers issued by BNM (“the Framework”). The Company has met the minimum capital requirements as prescribed by the framework as at the balance sheet date.

101.108(a)

Financial assets and financial liabilities are offset and the net amount reported in the balance sheet only when there is a legally enforceable right to offset the recognised amounts and there is an intention to settle on a net basis, or to realise the assets and settle the liability simultaneously. Income and expense will not be offset in the income statement unless required or permitted by any accounting standard or interpretation, as specifically disclosed in the accounting policies of the Company.

The financial statements are presented in Ringgit Malaysia (RM) and all values are rounded to the nearest thousand (RM’000) except when otherwise indicated.

101.46(d)&(e)

2.2 Summary of Significant Accounting Policies

(a) Property and Equipment 116.73(a)

All items of property and equipment are initially recorded at cost. Subsequent costs are included in the asset’s carrying amount or recognised as a separate asset, as appropriate, only when it is probable that future economic benefits associated with the item will flow to the Company and the cost of the item can be measured reliably. The carrying amount of the replaced part is derecognised. All other repairs and maintenance are charged to the profit or loss during the financial period in which they are incurred.

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A NOTES TO THE FINANCIAL STATEMENTS

FINAL (July 30, 2010)

- 14 -

Subsequent to recognition, property and equipment are stated at cost less accumulated depreciation and any accumulated impairment losses.

116.73(a)

Depreciation of property and equipment is provided for on a straight-line basis to write off the cost of each asset to its residual value over the estimated useful life, at the following annual rates:

116.73(a)

Furniture and fittings 10% 116.73(c)

Motor vehicles 20%

Office equipment and computers 25%

The residual values, useful lives and depreciation method are reviewed at each financial year-end to ensure that the amount, method and period of depreciation are consistent with previous estimates and the expected pattern of consumption of the future economic benefits embodied in the items of property and equipment.

116.51

An item of property and equipment is derecognised upon disposal or when no future economic benefits are expected from its use or disposal. The difference between the net disposal proceeds, if any and the net carrying amount is recognised in profit or loss.

116.71

(b) Investment Properties 140.5

Investment properties are properties which are held either to earn rental income or for capital appreciation or for both.

Such properties are measured initially at cost, including transaction costs.

Subsequent to initial recognition, investment properties are stated at fair value*. Fair value is based on active market prices, adjusted, if necessary, for any difference in the nature, location or condition of the specific asset. If this information is not available, the Company uses alternative valuation methods such as recent prices on less active markets or discounted cash flow projections. Fair value is reviewed at every balance sheet date and a formal valuation by an independent professional valuer is carried out once in every three years or earlier if the carrying value of the investment properties is materially different from the market value. [* If Cost model is adopted, insert appropriate accounting policy.]

140.33 140.36

Gains or losses arising from changes in the fair values of investment properties are recognised in profit or loss in the year in which they arise.

140.35

A property interest under an operating lease is classified and accounted for as an investment property on a property-by-property basis when the Company holds it to earn rentals or for capital appreciation or both. Any such property interest under an operating lease classified as an investment property is carried at fair value.

140.30

Investment properties are derecognised when either they have been disposed of or when the investment property is permanently withdrawn from use and no future economic benefit is expected from its disposal. Any gains or losses on the retirement or disposal of an investment property are recognised in profit or loss in the year in which they arise.

140.66 140.69

(c) Intangible Assets* 138.118

[* Insert appropriate Accounting Policy on Goodwill, if applicable.]

Other Intangible Assets Intangible assets acquired separately are measured on initial recognition at cost. Following initial recognition, intangible assets are carried at cost less accumulated amortisation and any accumulated impairment losses. Internally generated intangible assets are not capitalised and expenditure is reflected in profit or loss in the period in which the expenditure is incurred. The useful lives of intangible assets are assessed to be either finite or indefinite. Intangible assets with finite lives are amortised over the useful economic life and assessed for impairment whenever there is an indication that the intangible asset may be impaired. The amortisation period and the amortisation method for an intangible asset with a finite useful life are reviewed at least at each financial year-end. Changes in the expected useful life or the expected pattern of consumption of future economic benefits embodied in the asset is accounted for by changing the amortisation period or method, as appropriate, and are treated as changes in accounting estimates.

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A NOTES TO THE FINANCIAL STATEMENTS

FINAL (July 30, 2010)

- 15 -

Acquired computer software licences* are capitalised on the basis of the costs incurred to acquire and bring to use the specific software. These costs are amortised over their estimated useful lives of three to five years.

Costs associated with maintaining computer software programmes are recognised as an expense when incurred. Costs that are directly associated with identifiable and unique software products controlled by the Company, and that will probably generate economic benefits exceeding costs beyond one year, are recognised as intangible assets. Costs include employee costs incurred as a result of developing software and an appropriate portion of relevant overheads. Computer software development costs recognised as assets are amortised using the straight line method over their estimated useful lives, not exceeding a period of 3 years.

[* Insert notes on other specific intangible assets, as applicable.] Intangible assets with indefinite useful lives are tested for impairment annually either individually or at the cash-generating-unit level. Such intangibles are not amortised. The useful life of an intangible asset with an indefinite life is reviewed annually to determine whether indefinite life assessment continues to be supportable. If not, the change in the useful life assessment from indefinite to definite is made on a prospective basis.

138.88

138.121

Gains or losses arising from derecognition of an intangible asset are measured as the difference between the net disposal proceeds and the carrying amount of the asset and are recognised in profit or loss when the asset is derecognised.

(d) Impairment of Non-Financial Assets* 136.134

Assets that have an indefinite useful life are not subject to amortisation and are tested annually for impairment. The carrying amounts of assets are reviewed at each balance sheet date to determine whether there is any indication of impairment. If any such indication exists, the asset’s recoverable amount is estimated to determine the amount of impairment loss. Non-financial assets other than goodwill that suffered an impairment are reviewed for possible reversal of the impairment at each reporting date.

136.9

For the purpose of impairment testing of these assets, recoverable amount is determined on an individual asset basis unless the asset does not generate cash flows that are largely independent of those from other assets. If this is the case, recoverable amount is determined for the cash-generating unit (“CGU”) to which the asset belongs.

An asset’s recoverable amount is the higher of an asset’s or CGU’s fair value less costs to sell and its value in use. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset. Where the carrying amount of an asset exceeds its recoverable amount, the asset is considered impaired and is written down to its recoverable amount. Impairment losses recognised in respect of a CGU or groups of CGUs are allocated first to reduce the carrying amount of any goodwill allocated to those units or groups of units and then, to reduce the carrying amount of the other assets in the units or groups of units on a pro-rata basis.

An impairment loss is recognised in profit or loss in the period in which it arises, unless the asset is carried at a revalued amount, in which case the impairment loss is accounted for as a revaluation decrease to the extent that the impairment loss does not exceed the amount held in the asset revaluation reserve for the same asset.

An impairment loss for an asset other than goodwill is reversed if, and only if, there has been a change in the estimates used to determine the asset’s recoverable amount since the last impairment loss was recognised. The carrying amount of an asset other than goodwill is increased to its revised recoverable amount, provided that this amount does not exceed the carrying amount that would have been determined (net of amortisation or depreciation) had no impairment loss been recognised for the asset in prior years. A reversal of impairment loss for an asset is recognised in profit or loss, unless the asset is carried at revalued amount, in which case, such reversal is treated as a revaluation increase.

[* Insert appropriate note for impairment of Goodwill, if applicable.]

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A NOTES TO THE FINANCIAL STATEMENTS

FINAL (July 30, 2010)

- 16 -

(e) Investments and Other Financial Assets*

The Company classifies its investments into financial assets at fair value through profit or loss (“FVTPL”), held-to-maturity financial assets (“HTM”), loans and other receivables (“LAR”) and available-for-sale financial assets (“AFS”).

139.9 7.21

The classification depends on the purpose for which the investments were acquired or originated. Management determines the classification of its investments at initial recognition and re-evaluates this at every reporting date. Financial assets are classified as fair value through profit or loss where the Company’s documented investment strategy is to manage financial assets on a fair value basis, because the related liabilities are also managed on this basis. The available-for-sale and held-to-maturity categories are used when the relevant liability (including shareholders’ funds) are passively managed and/or carried at amortised cost. All regular way purchases and sales of financial assets are recognised on the trade date which is the date that the Company commits to purchase or sell the asset. Regular way purchases or sales of financial assets require delivery of assets within the period generally established by regulation or convention in the market place.

FVTPL Financial assets at FVTPL include financial assets held for trading and those designated at fair value through profit or loss at inception. Investments typically bought with the intention to sell in the near future are classified as held-for-trading. For investments designated as at fair value through profit or loss, the following criteria must be met:

the designation eliminates or significantly reduces the inconsistent treatment that would otherwise arise from measuring the assets or liabilities or recognising gains or losses on a different basis, or

the assets and liabilities are part of a group of financial assets, financial liabilities or both which are managed and their performance evaluated on a fair value basis, in accordance with a documented risk management or investment strategy.

These investments are initially recorded at fair value. Subsequent to initial recognition, these investments are remeasured at fair value. Fair value adjustments and realised gains and losses are recognised in profit or loss.

HTM Non-derivative financial assets with fixed or determinable payments and fixed maturities are classified as HTM when the Company has the positive intention and ability to hold until maturity. These investments are initially recognised at cost, being the fair value of the consideration paid for the acquisition of the investment. After initial measurement, HTM financial assets are measured at

amortised cost, using the effective yield method, less provision for impairment. Gains and losses are

recognised in profit or loss when the investments are derecognised or impaired, as well as through the amortisation process.

LAR LAR are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. These investments are initially recognised at cost, being the fair value of the consideration paid for the acquisition of the investment. All transaction costs directly attributable to the acquisition are also included in the cost of the investment. After initial measurement, loans and receivables are measured at amortised cost, using the effective yield method, less provision for impairment. Gains and losses are recognised in profit or loss when the investments are derecognised or impaired, as well as through the amortisation process.

139.70 139.9

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A NOTES TO THE FINANCIAL STATEMENTS

FINAL (July 30, 2010)

- 17 -

AFS AFS are non-derivative financial assets that are designated as available-for-sale or are not classified in any of the three preceding categories. These investments are initially recorded at fair value. After initial measurement, AFS are remeasured at fair value. Fair value gains and losses of monetary and non-monetary securities are reported as a separate component of equity until the investment is derecognised or investment is determined to be impaired except that for the life business, such fair value gains and losses are reported as a separate component of contract liabilities. Fair value gains and losses of monetary securities denominated in a foreign currency are analysed between translation differences resulting from changes in amortised cost of the security and other changes in the carrying amount of the security. The translation differences on monetary securities are recognised in profit or loss; translation differences on non-monetary securities are reported as a separate component of equity until the investment is derecognised. On derecognition or impairment, the cumulative fair value gains and losses previously reported in equity is transferred to profit or loss.

139.67 – 70

[* Insert Derivative Financial Instruments, if applicable.]

(f) Fair Value of Financial Instruments 139.48 & 48A

The fair value of financial instruments that are actively traded in organised financial markets is determined by reference to quoted market bid prices for assets and offer prices for liabilities, at the close of business on the balance sheet date.

7.27

For investments in unit and real estate investment trusts, fair value is determined by reference to published bid values.

For financial instruments where there is not an active market, the fair value is determined by using valuation techniques. Such techniques include using recent arm’s length transactions, reference to the current market value of another instrument which is substantially the same, discounted cash flow analysis and/or option pricing models making maximum use of market inputs and relying as little as possible on entity-specific inputs. For discounted cash flow techniques, estimated future cash flows are based on management’s best estimates and the discount rate used is a market related rate for a similar instrument. Certain financial instruments are valued using pricing models that consider, among other factors, contractual and market prices, co-relation, time value of money, credit risk, yield curve volatility factors and/or prepayment rates of the underlying positions. The use of different pricing models and assumptions could produce materially different estimates of fair values.

The fair value of floating rate and over-night deposits with financial institutions is their carrying value. The carrying value is the cost of the deposit/placement and accrued interest/profit. The fair value of fixed interest/yield-bearing deposits is estimated using discounted cash flow techniques. Expected cash flows are discounted at current market rates for similar instruments at the balance sheet date.

If the fair value cannot be measured reliably, these financial instruments are measured at cost, being the fair value of the consideration paid for the acquisition of the instrument or the amount received on issuing the financial liability. All transaction costs directly attributable to the acquisition are also included in the cost of the investment.

(g) Impairment of Financial Instruments 139.58

The Company assesses at each balance sheet date whether a financial asset or group of financial assets is impaired.

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A NOTES TO THE FINANCIAL STATEMENTS

FINAL (July 30, 2010)

- 18 -

Assets Carried at Amortised Cost If there is objective evidence that an impairment loss on assets carried at amortised cost has been incurred, the amount of the impairment loss is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows (excluding future expected credit losses that have not been incurred) discounted at the financial asset’s original effective interest rate/yield. The carrying amount of the asset is reduced and the loss is recorded in profit or loss.

139.63

The Company first assesses whether objective evidence of impairment exists individually for financial assets that are individually significant, and individually or collectively for financial assets that are not individually significant. If it is determined that no objective evidence of impairment exists for an individually assessed financial asset, whether significant or not, the asset is included in a group of financial assets with similar credit risk characteristics and that group of financial assets is collectively assessed for impairment. Assets that are individually assessed for impairment and for which an impairment loss is or continues to be recognised are not included in a collective assessment of impairment. The impairment assessment is performed at each balance sheet date.

If, in a subsequent period, the amount of the impairment loss decreases and the decrease can be related objectively to an event occurring after the impairment was recognised, the previously recognised impairment loss is reversed. Any subsequent reversal of an impairment loss is recognised in profit or loss, to the extent that the carrying value of the asset does not exceed its amortised cost at the reversal date.

AFS Investments

134.67 - 70

If an AFS financial asset is impaired, an amount comprising the difference between its cost (net of any principal repayment and amortisation) and its current fair value, less any impairment loss previously recognised in other comprehensive income, is transferred from other comprehensive income to profit or loss. Reversals in respect of equity instruments classified as AFS are not recognised in profit or loss. Reversals of impairment losses on debt instruments classified as AFS are reversed through profit or loss if the increase in the fair value of the instruments can be objectively related to an event occurring after the impairment losses were recognised in profit or loss.

(h) Derecognition of Financial Assets 139.16 - 23

Financial assets are derecognised when the rights to receive cash flows from them have expired or where they have been transferred and the Company has also transferred substantially all risks and rewards of ownership.

(i) Equity Instruments

Ordinary Share Capital

The Company has issued ordinary shares that are classified as equity. Incremental external costs that are directly attributable to the issue of these shares are recognised in equity, net of tax.

132.60

Dividends on Ordinary Share Capital Dividends on ordinary shares are recognised as a liability and deducted from equity when they are approved by the Company’s shareholders. Interim dividends are deducted from equity when they are paid. Dividends for the year that are approved after the balance sheet date are dealt with as an event after the balance sheet date.

132.35

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A NOTES TO THE FINANCIAL STATEMENTS

FINAL (July 30, 2010)

- 19 -

(j) Product Classification

The Company issues contracts that transfer insurance risk or financial risk or both. Financial risk is the risk of a possible future change in one or more of a specified interest rate, financial instrument price, commodity price, foreign exchange rate, index of price or rate, credit rating or credit index or other variable, provided in the case of a non-financial variable that the variable is not specific to a party to the contract. Insurance risk is the risk other than financial risk. Insurance contracts are those contracts that transfer significant insurance risk. An insurance contract is a contract under which the Company (the insurer) has accepted significant insurance risk from another party (the policyholders) by agreeing to compensate the policyholders if a specified uncertain future event (the insured event) adversely affects the policyholders. As a general guideline, the Company determines whether it has significant insurance risk, by comparing benefits paid with benefits payable if the insured event did not occur.

4 Appx A 4.37(a)

Investment contracts are those contracts that do not transfer significant insurance risk.

4 Appx A 4.37(a)

Once a contract has been classified as an insurance contract, it remains an insurance contract for the remainder of its life-time, even if the insurance risk reduces significantly during this period, unless all rights and obligations are extinguished or expire. Investment contracts can, however, be reclassified as insurance contracts after inception if insurance risk becomes significant.

4 Appx B. 29 & 30

Insurance and investment contracts are further classified as being either with or without discretionary participation features (“DPF”). DPF is a contractual right to receive, as a supplement to guaranteed benefits, additional benefits that are:

likely to be a significant portion of the total contractual benefits;

whose amount or timing is contractually at the discretion of the issuer; and

that are contractually based on the: o performance of a specified pool of contracts or a specified type of contract; o realised and/or unrealised investment returns on a specified pool of assets held by the

issuer; or o the profit or loss of the company, fund or other entity that issues the contract.

Under the terms of the contracts, surpluses in the DPF funds can be distributed on a 90/10* basis to the policyholders and the shareholders respectively. The Company has the discretion over the amount and timing of the distribution of these surpluses to policyholders. All DPF liabilities, including unallocated surpluses, both guaranteed and discretionary, at the end of the reporting period are held within insurance or investment contract liabilities, as appropriate.

[*State basis which comply with statutory requirements and Company’s actual experience.]

4 Appx A 4.34

For financial options and guarantees which are not closely related to the host insurance contract and/or investment contract with DPF, bifurcation is required to measure these embedded derivatives separately at fair value through profit or loss. However, bifurcation is not required if the embedded derivative is itself an insurance contract and/or investment contract with DPF, or if the host insurance contract and/or investment contract itself is measured at fair value through profit or loss.

4.7 – 4.9

When insurance contracts contain both a financial risk component and a significant insurance risk component and the cash flows from the two components are distinct and can be measured reliably, the underlying amounts are unbundled. Any premiums relating to the insurance risk component are accounted for on the same bases as insurance contracts and the remaining element is accounted for as a deposit through the balance sheet similar to investment contracts.

(k) Reinsurance 4.37(a)

The Company cedes insurance risk in the normal course of business for all of its businesses. Reinsurance assets represent balances due from reinsurance companies. Amounts recoverable from reinsurers are estimated in a manner consistent with the outstanding claims provision or settled claims associated with the reinsurer’s policies and are in accordance with the related reinsurance contracts. Ceded reinsurance arrangements do not relieve the Company from its obligations to policyholders. Premiums and claims are presented on a gross basis for both ceded and assumed reinsurance.

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A NOTES TO THE FINANCIAL STATEMENTS

FINAL (July 30, 2010)

- 20 -

Reinsurance assets are reviewed for impairment at each reporting date or more frequently when an indication of impairment arises during the reporting period. Impairment occurs when there is objective evidence as a result of an event that occurred after initial recognition of the reinsurance asset that the Company may not receive all outstanding amounts due under the terms of the contract and the event has a reliably measurable impact on the amounts that the Company will receive from the reinsurer. The impairment loss is recorded in profit or loss.

4.20

Gains or losses on buying reinsurance are recognised in profit or loss immediately at the date of purchase and are not amortised *. [* Policy option in FRS 4 para 37(b)(ii) could also be used.]

4.37(b)(i)

The Company also assumes reinsurance risk in the normal course of business for life insurance and general (non-life) insurance contracts when applicable. Premiums and claims on assumed reinsurance are recognised as revenue or expenses in the same manner as they would be if the reinsurance were considered direct business, taking into account the product classification of the reinsured business. Reinsurance liabilities represent balances due to reinsurance companies. Amounts payable are estimated in a manner consistent with the related reinsurance contract.

Reinsurance assets or liabilities are derecognised when the contractual rights are extinguished or expire or when the contract is transferred to another party.

4.14(c)

Reinsurance contracts that do not transfer significant insurance risk are accounted for directly through the balance sheet. These are deposit assets or financial liabilities that are recognised based on the consideration paid or received less any explicit identified premiums or fees to be retained by the reinsured. Investment income on these contracts is accounted for using the effective yield method when accrued.

[Note : policies on reinsurance inwards is included in insurance contracts]

4 Appx B.20

(l) Life Insurance Underwriting Results

The surplus transferable from the Life fund to the income statement is based on the surplus determined by an annual actuarial valuation of the liabilities to policyholders.

Gross Premiums Gross premiums are recognised as soon as the amount of the premiums can be reliably measured. First premium is recognised from inception date and subsequent premium is recognised when it is due. At the end of the financial period, all due premiums are accounted for to the extent that they can be reliably measured.

4.37(a)

Reinsurance Premiums Gross reinsurance premiums are recognised as an expense when payable or on the date on which the policy is effective.

4.14(d)

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A NOTES TO THE FINANCIAL STATEMENTS

FINAL (July 30, 2010)

- 21 -

Benefits, Claims and Expenses Benefits and claims that are incurred during the financial period are recognised when a claimable event occurs and/or the insurer is notified. Benefits and claims, including settlement costs, are accounted for using the case-by-case method and for this purpose, the amounts payable under a policy are recognised as follows:

maturity and other policy benefit payments due on specified dates are treated as claims payable on the due dates;

death, surrender and other benefits without due dates are treated as claims payable, on the date of receipt of intimation of death of the assured or occurrence of contingency covered; and

bonus on DPF policy upon its declaration Reinsurance claims are recognised when the related gross insurance claim is recognised according to the terms of the relevant contracts.

4.37(a) 4.14(d)

Commission and Agency Expenses

Gross commission and agency expenses, which are costs directly incurred in securing premium on insurance policies, and income derived from reinsurers in the course of ceding of premiums to reinsurers, are charged to profit or loss in the period in which they are incurred.

(m) General Insurance Underwriting Results The general insurance underwriting results are determined for each class of business after taking into account reinsurances, commissions, unearned premiums and claims incurred.

Gross Premiums Gross premiums are recognised in a financial period in respect of risks assumed during that particular financial period.

4.37(a)

Reinsurance Premiums Inwards facultative reinsurance premiums are recognised in the financial period in respect of the facultative risks assumed during that particular financial period, as in the case of direct policies, following the individual risks’ inception dates. Inwards treaty reinsurance premiums comprise both proportional and non-proportional treaties. In respect of reinsurance premiums relating to proportional treaties, it is recognised on the basis of periodic advices received from the cedants given that the periodic advices reflect the individual underlying risks being incepted and reinsured at various inceptions dates of these risks and contractually accounted for, as such to reinsurers under the terms of the proportional treaties. In respect of reinsurance premiums relating to non-proportional treaties which cover losses occurring during a specified treaty period, the inwards treaty reinsurance premiums are recognised based on the contractual premiums already established at the start of the treaty period under the non-proportional treaty contract. [Note: Insert policy on Open Underwriting method, if applicable].

4.37(b)

Unearned Premium Reserves Unearned premium reserves (“UPR”) represent the portion of the net premiums of insurance policies written that relate to the unexpired periods of the policies at the end of the financial period. In determining UPR at balance sheet date, the method that most accurately reflects the actual unearned premiums used is as follows:

25% method for marine cargo, aviation cargo and transit

1/24th

method (or other more accurate) method for all other classes of Malaysian general policies

1/8th

method for all other classes of overseas inward treaty business

Non-annual policies are time-apportioned over the period of the risks

4.37(a)

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A NOTES TO THE FINANCIAL STATEMENTS

FINAL (July 30, 2010)

- 22 -

Claims and Expenses A liability for outstanding claims is recognised in respect of both direct insurance and inward reinsurance. The amount of outstanding claims is the best estimate of the expenditure required together with related expenses less recoveries to settle the present obligation at the balance sheet date. Provision is also made for the cost of claims, together with related expenses, incurred but not reported at balance sheet date, using a mathematical method of estimation.

4.37(a)

Acquisition Costs and Deferred Acquisition Cost (“DAC”)

4.37(a)

The gross costs of acquiring and renewing insurance policies and income derived from ceding reinsurance premiums are recognised as incurred and properly allocated to the periods in which it is probable they give rise to income.

Those costs are deferred to the extent that these costs are recoverable out of future premiums. All other acquisition costs are recognised as an expense when incurred.

Subsequent to initial recognition, these costs are amortised on a straight-line basis based on the term of expected future premiums. Amortisation is recognised in profit or loss.

Changes in the expected useful life or the expected pattern of consumption of future economic benefits embodied in these assets are accounted for by changing the amortisation period and are treated as a change in an accounting estimate.

An impairment review is performed at each reporting date or more frequently when an indication of impairment arises. When the recoverable amount is less than the carrying value, an impairment loss is recognised in profit or loss. DAC is also considered in the liability adequacy test for each accounting period. DAC is derecognised when the related contracts are either settled or disposed of.

4.37(e)

(n) Insurance Receivables

Insurance receivables are recognised when due and measured on initial recognition at the fair value of the consideration received or receivable. Subsequent to initial recognition, insurance receivables are measured at amortised cost, using the effective yield method. If there is objective evidence that the insurance receivable is impaired, the Company reduces the carrying amount of the insurance receivable accordingly and recognises that impairment loss in profit or loss. The Company gathers the objective evidence that an insurance receivable is impaired using the same process adopted for financial assets carried at amortised cost. The impairment loss is calculated under the same method used for these financial assets. These processes are described in Note 2.2 (g). Insurance receivables are derecognised when the derecognition criteria for financial assets, as described in Note 2.2(h), have been met.

4.37(a)

(o) Insurance Contract Liabilities

Life Insurance Contract Liabilities Life insurance liabilities are recognised when contracts are entered into and premiums are charged.

These liabilities are measured by using a prospective actuarial valuation method. The liability is determined as the sum of the present value of future guaranteed and, in the case of a participating life policy, appropriate level of non-guaranteed benefits, and the expected future management and distribution expenses, less the present value of future gross considerations arising from the policy discounted at the appropriate risk discount rate. The liability is based on best estimate assumptions and with due regard to significant recent experience. An appropriate allowance for provision of risk margin for adverse deviation from expected experience is made in the valuation of non-participating life policies, the guaranteed benefits liabilities of participating life policies, and non-unit liabilities of investment-linked policies.

4.15

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A NOTES TO THE FINANCIAL STATEMENTS

FINAL (July 30, 2010)

- 23 -

The liability in respect of policies of a participating insurance contract is taken as the higher of the guaranteed benefit liabilities or the total benefit liabilities at the contract level derived as stated above. In the case of a life policy where a part of, or the whole of the premiums are accumulated in a fund, the accumulated amount, as declared to the policy owners, are set as the liabilities if the accumulated amount is higher than the figure as calculated using the prospective actuarial valuation method.

Where policies or extensions of a policy are collectively treated as an asset at the fund level under the valuation method adopted, the value of such asset is eliminated through zerorisation. In the case of a 1-year life policy or a 1-year extension to a life policy covering contingencies other than death or survival, the liability for such life insurance contracts comprises the provision for unearned premiums and unexpired risks, as well as for claims outstanding, which includes an estimate of the incurred claims that have not yet been reported to the Company.

RBC Framework

Adjustments to the liabilities at each reporting date are recorded in profit or loss. Profits originated from margins of adverse deviations on run-off contracts, are recognised in profit or loss over the life of the contract, whereas losses are fully recognised in profit or loss during the first year of run-off. The liability is derecognised when the contract expires, is discharged or is cancelled. At each reporting date, an assessment is made of whether the recognised life insurance liabilities are adequate, net of present value of in-force business (“PVIF”) and DAC by using an existing liability adequacy test.

Any inadequacy is recorded in profit or loss, initially by impairing PVIF and DAC, and subsequently by establishing technical reserves for the remaining loss. In subsequent periods, the liability for a block of business that has failed the adequacy test is based on the assumptions that are established at the time of the loss recognition. Impairment losses resulting from liability adequacy testing can be reversed in future years if the impairment no longer exists.

General (Non-Life) Insurance Contract Liabilities General insurance contract liabilities are recognised when contracts are entered into and premiums are charged.

4.15

These liabilities comprise outstanding claims provision and provision for unearned premiums. Outstanding claims provision are based on the estimated ultimate cost of all claims incurred but not settled at the balance sheet date, whether reported or not, together with related claims handling costs and reduction for the expected value of salvage and other recoveries. Delays can be experienced in the notification and settlement of certain types of claims, therefore, the ultimate cost of these claims cannot be known with certainty at the balance sheet date. The liability is calculated at the reporting date using a range of standard actuarial claim projection techniques based on empirical data and current assumptions that may include a margin for adverse deviation. The liability is not discounted for the time value of money. No provision for equalisation or catastrophe reserves is recognised. The liabilities are derecognised when the contract expires, is discharged or is cancelled.

The provision for unearned premiums represents premiums received for risks that have not yet expired. Generally, the reserve is released over the term of the contract and is recognised as premium income.

At each reporting date, the Company reviews its unexpired risks and a liability adequacy test is performed to determine whether there is any overall excess of expected claims and deferred acquisition costs over unearned premiums. This calculation uses current estimates of future contractual cash flows (taking into consideration current loss ratios) after taking account of the investment return expected to arise on assets relating to the relevant general insurance technical provisions. If these estimates show that the carrying amount of the unearned premiums less related deferred acquisition costs is inadequate, the deficiency is recognised in profit or loss by setting up a provision for liability adequacy.

(p) Investment Contract Liabilities

Investment contracts are classified between contracts with and without DPF. The accounting policies for investment contract liabilities with DPF are the same as those for life insurance contract liabilities.

4.15

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A NOTES TO THE FINANCIAL STATEMENTS

FINAL (July 30, 2010)

- 24 -

Investment contract liabilities without DPF are recognised when contracts are entered into and premiums are charged. These liabilities are initially recognised at fair value being the transaction price excluding any transaction costs directly attributable to the issue of the contract. Subsequent to initial recognition, investment contract liabilities are remeasured at fair value through profit or loss*. [* If at amortised cost, insert appropriate note.] [Note: Insert appropriate note for non-unitised contracts, if applicable.]

Deposits and withdrawals are recorded directly as an adjustment to the liability in the balance sheet.

Fair value adjustments are performed at each reporting date and are recognised in profit or loss. Fair value is determined through the use of prospective discounted cash flow techniques. For unitised contracts, fair value is calculated as the number of units allocated to the policyholder in each unit-linked fund multiplied by the unit-price of those funds at the balance sheet date. The fund assets and fund liabilities used to determine the unit-prices at the balance sheet date are adjusted to take into account the effect of deferred tax on unrealised gains and losses on assets in the fund.

The liability is derecognised when the contract expires, is discharged or is cancelled. For a contract that can be cancelled by the policyholder, the fair value cannot be less than the surrender value.

(q) Other Revenue Recognition

118.35

Revenue is recognised to the extent that it is probable that the economic benefits will flow to the Company and the revenue can be reliably measured. The following specific recognition criteria must also be met before revenue is recognised.

Rental Income Rental income from investment property is recognised on a straight-line basis over the term of the lease. The aggregate cost of incentives provided to lessees is recognised as a reduction of rental income over the lease term on a straight-line basis.

117.50

Interest and Profit Income Income is recognised on an accrual basis using the effective yield method. Fees and commissions that are an integral part of the effective yield of the financial asset or liability are recognised as an adjustment to the effective yield of the instrument.

118.30(a)

Dividend Income

Dividend income is recognised when the Company’s right to receive payment is established.

Realised Gains and Losses on Investments Realised gains and losses recorded in profit or loss on investments include gains and losses on financial assets and investment properties. Gains and losses on the sale of investments are calculated as the difference between net sales proceeds and the original or amortised cost and are recorded on occurrence of the sale transaction.

118.30(c)

Fees and Commission Income

Insurance and investment contract policyholders are charged for policy administration services, investment management services, surrenders and other contract fees. These fees are recognised as revenue over the period in which the related services are performed. If the fees are for services to be provided in future periods, then, they are deferred and recognised over those future periods.

118.20

(r) Income Tax

112.44

Income tax on the profit or loss for the year comprises current and deferred tax. Current tax is the expected amount of income taxes payable in respect of the taxable profit and surplus for the year and is measured using the tax rates that have been enacted at the balance sheet date.

112.12 112.46

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A NOTES TO THE FINANCIAL STATEMENTS

FINAL (July 30, 2010)

- 25 -

Deferred tax is provided for, using the liability method. In principle, deferred tax liabilities are recognised for all taxable temporary differences and deferred tax assets are recognised for all deductible temporary differences, unused tax losses and unused tax credits to the extent that it is probable that taxable profit will be available against which the deductible temporary differences, unused tax losses and unused tax credits can be utilised. Deferred tax is not recognised if the temporary difference arises from the initial recognition of an asset or liability in a transaction which is not a business combination and at the time of the transaction, affects neither accounting profit nor taxable profit.

112.15 112.24

Deferred tax is measured at the tax rates that are expected to apply in the period when the asset is realised or the liability is settled, based on tax rates that have been enacted or substantively enacted at the balance sheet date. Deferred tax is recognised as income or an expense and included in the profit or loss for the period, except when it arises from a transaction which is recognised directly in equity, in which case the deferred tax is also recognised directly in equity. Deferred tax is also provided in the Life insurance contract liabilities for the shareholders’ portion of the unallocated surpluses.

112.45 112.46 112.58 112.61

(s) Provisions

137.36

Provisions are recognised when the Company has a present obligation as a result of a past event and it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation, and a reliable estimate of the amount can be made. Provisions are reviewed at each balance sheet date and adjusted to reflect the current best estimate. Where the effect of the time value of money is material, provisions are discounted using a current pre-tax rate that reflects, where appropriate, the risks specific to the liability. Where discounting is used, the increase in the provision due to the passage of time is recognised as finance cost.

137.45 137.47 137.14

(t) Employee Benefits

Short-Term Benefits Wages, salaries, bonuses and social security contributions are recognised as an expense in the year in which the associated services are rendered by employees. Short-term accumulating compensated absences such as paid annual leave are recognised when services are rendered by employees that increase their entitlement to future compensated absences. Short-term non-accumulating compensated absences such as sick leave are recognised when the absences occur.

119.11

Defined Contribution Plans Defined contribution plans are post-employment benefit plans under which the Company pays fixed contributions into separate entities or funds and will have no legal or constructive obligation to pay further contributions if any of the funds do not hold sufficient assets to pay all employee benefits relating to employee services in the current and preceding financial years. Such contributions are recognised as an expense in the profit or loss as incurred. As required by law, the Company makes such contributions to the Employees Provident Fund (“EPF”).

119.8 119.45

(u) Foreign Currencies

The financial statements are presented in Ringgit Malaysia which is also the functional currency of the Company.

121.9

Transactions in foreign currencies are initially recorded at the functional currency rate prevailing at the date of the transaction. Monetary assets and liabilities denominated in foreign currencies are re-translated at the functional currency rate of exchange ruling at the balance sheet date. All differences are taken to profit or loss.

121.21

Non-monetary items that are measured in terms of historical cost in foreign currency are not subsequently restated. Non-monetary items measured at fair value in a foreign currency are translated using the exchange rates at the date when the fair value was determined. All foreign exchange differences are taken to profit or loss, except for differences relating to items where gains or losses are recognised directly in equity, in which case, the gain or loss is recognised net of the exchange component in equity.

121.23 121.30

MODEL INSURANCE BERHAD (Incorporated in Malaysia) – 882009-A NOTES TO THE FINANCIAL STATEMENTS

FINAL (July 30, 2010)

- 26 -

(v) Other Financial Liabilities and Insurance Payables

Other liabilities and payables are recognised when due and measured on initial recognition at the fair value of the consideration received less directly attributable transaction costs. Subsequent to initial recognition, they are measured at amortised cost using the effective yield method.

(w) Cash and Cash Equivalents

Cash and cash equivalents consist of cash in hand, deposits held at call with financial institutions with original maturities of three months or less. It excludes deposits which are held for investment purpose.

107.46

2.3 Significant Accounting Judgements, Estimates and Assumptions

101.113

The preparation of the Company’s financial statements requires management to make judgements, estimates and assumptions that affect the reported amounts of revenue, expenses, assets and liabilities and the disclosure of contingent liabilities, at the reporting date. However, uncertainty about these assumptions and estimates could result in outcomes that could require a material adjustment to the carrying amount of the asset or liability affected in the future. These factors could include:

(a) Critical Judgements Made in Applying Accounting Policies

101.113

In the process of applying the Company’s accounting policies, management has made the following judgements, apart from those involving estimations and assumptions, which have the most significant effect on the amounts recognised in the financial statements. [E.g. – “significant insurance risk” in respect of classification of insurance/investment contracts, classification of Investment Properties.]

Operating Lease Commitments – the Company as Lessor

The Group has entered into commercial property leases on its investment property portfolio. The Group has determined that it retains all the significant risks and rewards of ownership of these properties which are leased out on operating leases.

(b) Key Sources of Estimation Uncertainty and Assumptions 101.116

The key assumptions concerning the future and other key sources of estimation uncertainty at the balance sheet date, that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year are discussed below.

Valuation of Life Insurance Contract Liabilities (including Investment Contract Liabilities with DPF)

4.37(c)