Embed Size (px)

Citation preview

1

Brand management during a crisis: leveraging

insights for instant course correction

July 2011

Ravi Parmeswar

2

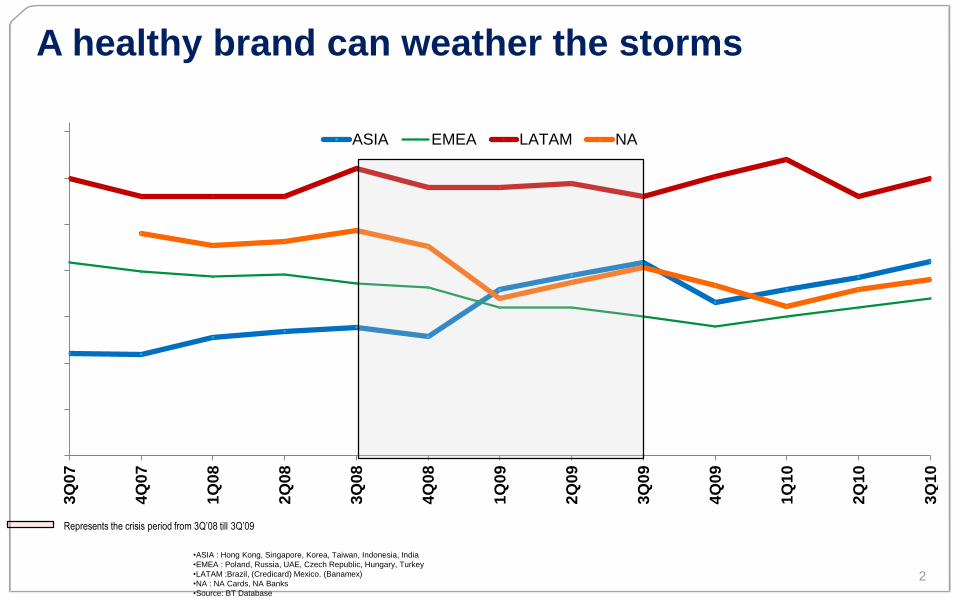

A healthy brand can weather the storms

0%

5%

10%

15%

20%

25%

30%

35%

3Q

07

4Q

07

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

ASIA EMEA LATAM NA

•ASIA : Hong Kong, Singapore, Korea, Taiwan, Indonesia, India

•EMEA : Poland, Russia, UAE, Czech Republic, Hungary, Turkey

•LATAM :Brazil, (Credicard) Mexico. (Banamex)

•NA : NA Cards, NA Banks

•Source: BT Database

Represents the crisis period from 3Q’08 till 3Q’09

3

Mobile formula for the future

3

4

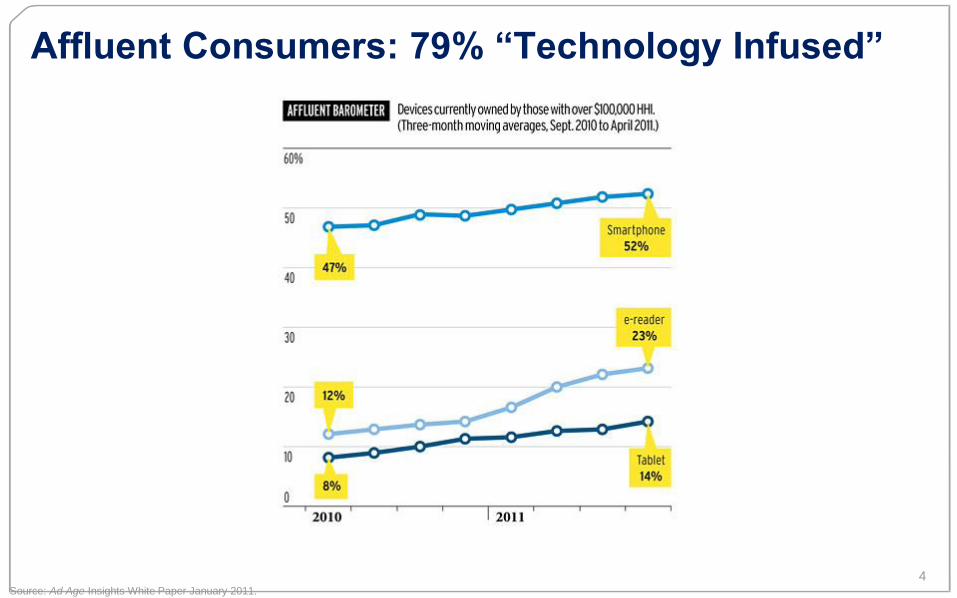

Affluent Consumers: 79% “Technology Infused”

Source: Ad Age Insights White Paper January 2011.

5

More complicated, more stressful

Source: Ad Age Insights White Paper January 2011.

6

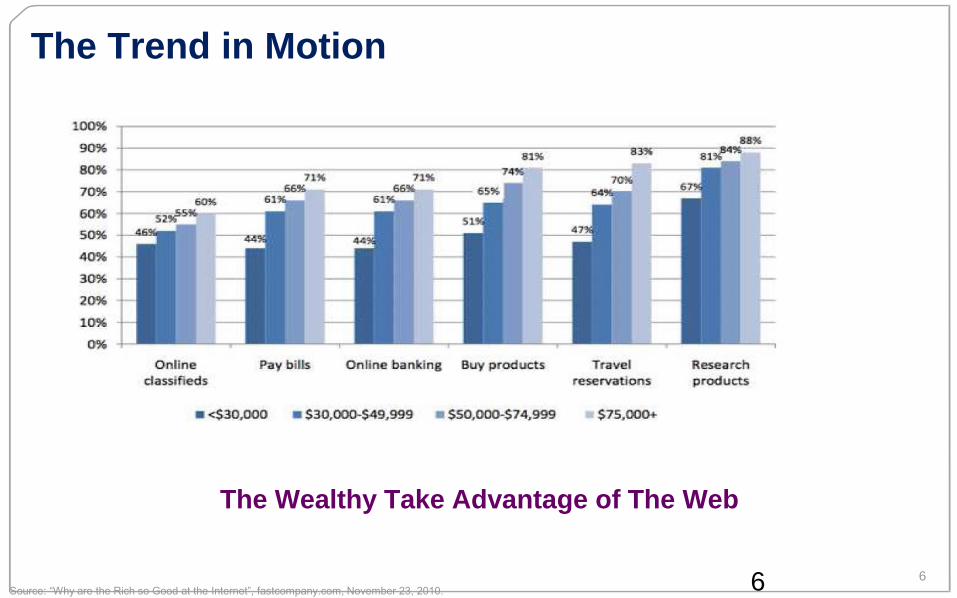

The Trend in Motion

6

The Wealthy Take Advantage of The Web

Source: “Why are the Rich so Good at the Internet”, fastcompany.com, November 23, 2010.

7

Younger Affluents’ Intensely Digital Media Behavior

• Wealthy, 35 and Under

70% own smart phones (40% iPhone, 24% Blackberry)

23% iPad

• 78% watch online video

More than read a printed magazine (76%) or newspaper (68%)

• 289 minutes watching live TV is less than

The combined time of 227 minutes watching DVR playback

And 100 minutes online videos

• Internet radio closing the gap

75 minutes pre week

vs. 150 minutes for terrestrial

7

Source: Luxury Institute, April 5, 2011

8

Younger Affluents’ Intensely Digital Media Behavior

• Use of mobile devices

Communicating

Consuming content

Music

Gaming

• Social networks

• Blogs

• Prefer apps to 411

Research restaurants

Recommend products

Get deals

8

Source: “Affluence in America: The New Consumer Landscape”, Digitas, May 25, 2011.

9

Burberry Art of the Trench

• 7.5 million views

• 150 countries

10

Top 50 Brands: New Face of Affluence

1

0

Source: The New Face of Affluence

11

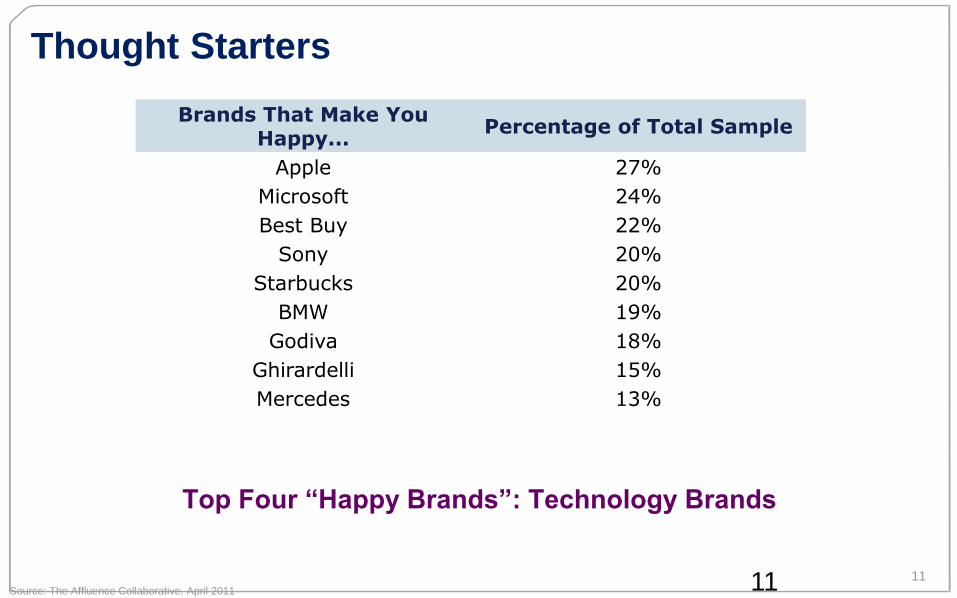

Thought Starters

11

Top Four “Happy Brands”: Technology Brands

HAPPY BRANDS

Brands That Make You Happy...

Percentage of Total Sample

Apple 27%

Microsoft 24%

Best Buy 22%

Sony 20%

Starbucks 20%

BMW 19%

Godiva 18%

Ghirardelli 15%

Mercedes 13%

Source: The Affluence Collaborative, April 2011

12

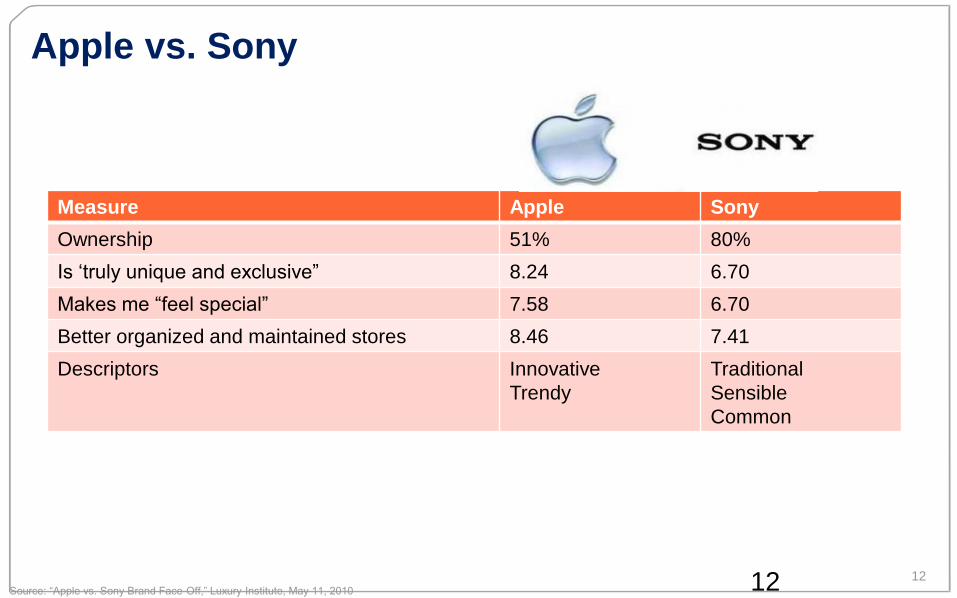

Apple vs. Sony

Measure Apple Sony

Ownership 51% 80%

Is ‘truly unique and exclusive” 8.24 6.70

Makes me “feel special” 7.58 6.70

Better organized and maintained stores 8.46 7.41

Descriptors Innovative

Trendy

Traditional

Sensible

Common

12Source: “Apple vs. Sony Brand Face-Off,” Luxury Institute, May 11, 2010

13

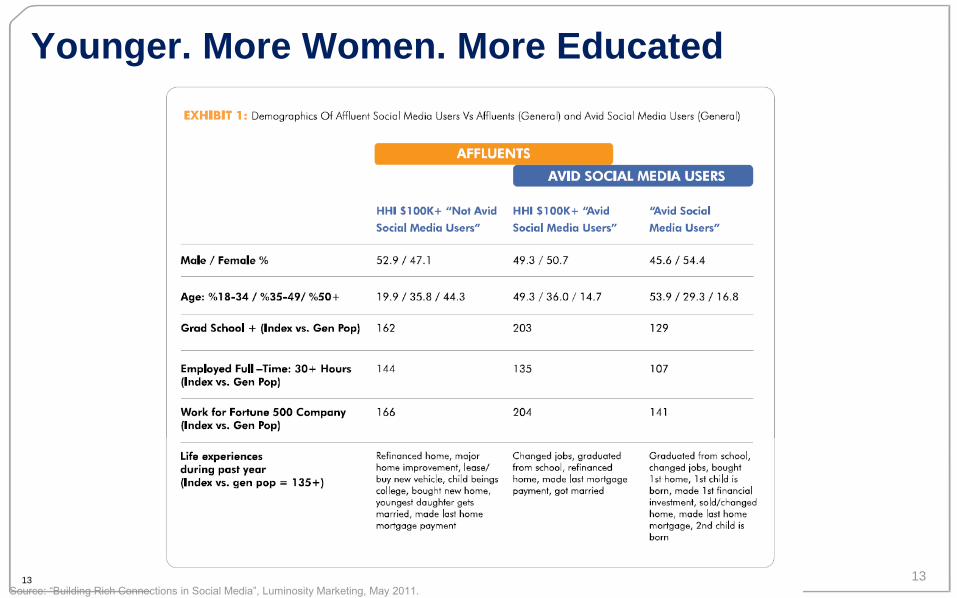

Younger. More Women. More Educated

13

.

Source: “Building Rich Connections in Social Media”, Luminosity Marketing, May 2011.

14

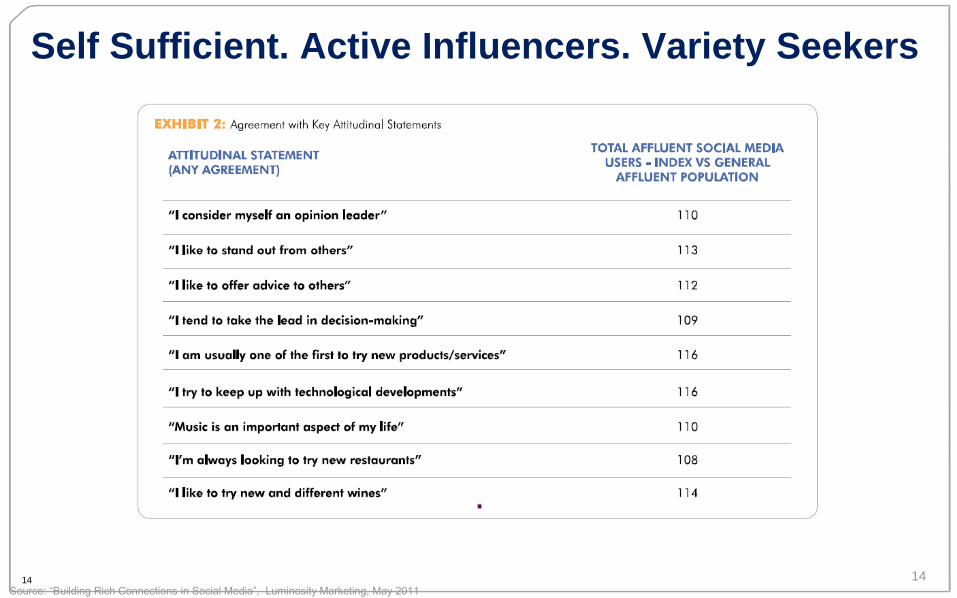

Self Sufficient. Active Influencers. Variety Seekers

14

.

Source: “Building Rich Connections in Social Media”, Luminosity Marketing, May 2011

15

Younger Wealthy Have Lost Faith

• > 1/3 lost faith in “fairness of market”

Believe individual doesn’t have a chance

• Younger wealthy especially skeptical

More than 25% of under-50s changed advisers

Vs only 7% of Boomers and 65+

15

Source: “Mark Zuckerberg’s Wealth Adviser – His Facebook Friends?”, Bloomberg News, March 30, 2011.

16

Facebook Tops Financial Advisers

• Under 50s don’t trust financial advisers

>50% use social networking for advice

2/3 interested in joining online investor communities

Boomers and older – far less interested

16

Source: “Mark Zuckerberg’s Wealth Adviser – His Facebook Friends?”, Bloomberg News, March 30, 2011.

17

Seeking Advice? Seek Alpha Stock Market Blog

17

18

The Trend in Motion

18

Social Networking … Plus

19

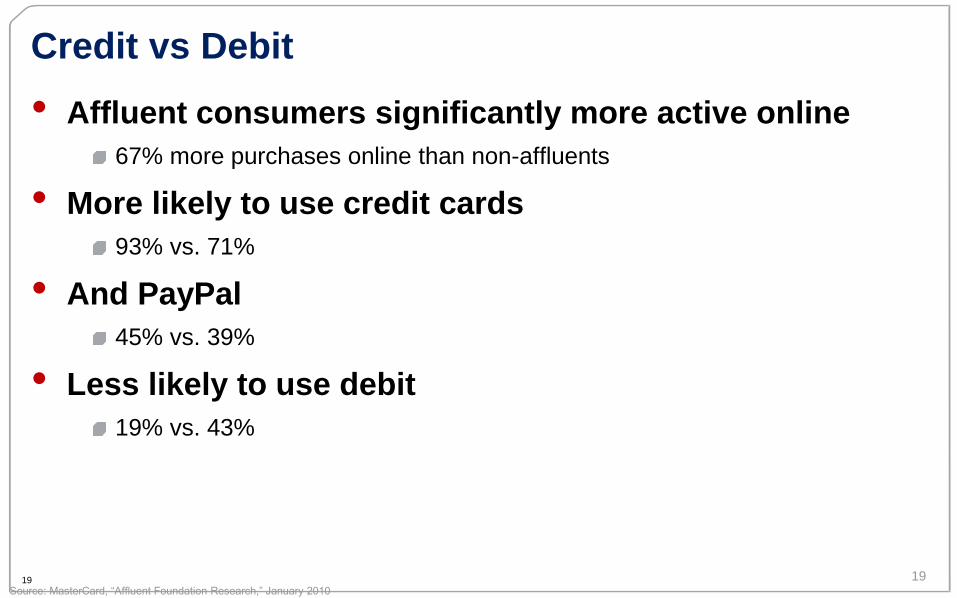

Credit vs Debit

• Affluent consumers significantly more active online

67% more purchases online than non-affluents

• More likely to use credit cards

93% vs. 71%

• And PayPal

45% vs. 39%

• Less likely to use debit

19% vs. 43%

19

Source: MasterCard, “Affluent Foundation Research,” January 2010

20

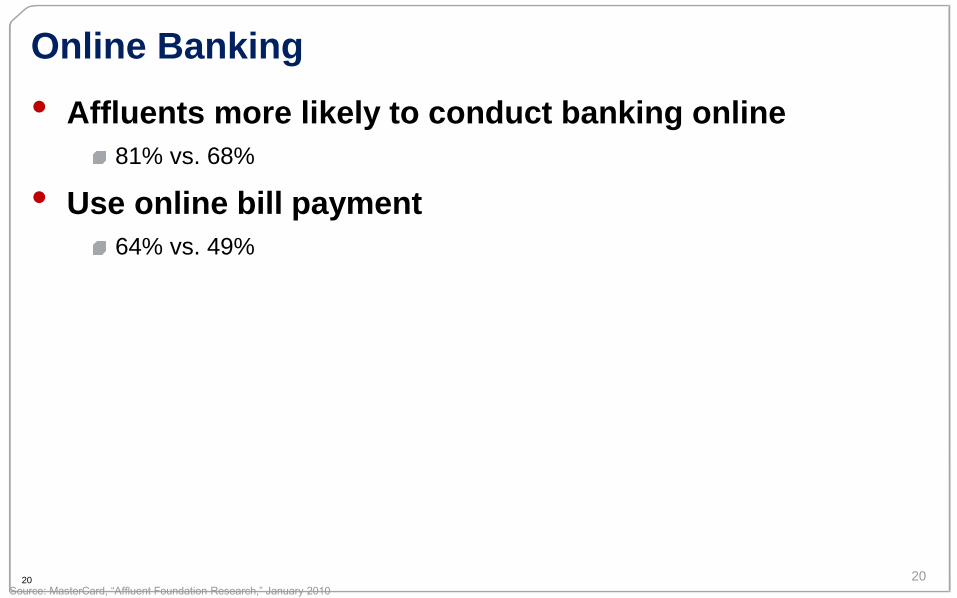

Online Banking

• Affluents more likely to conduct banking online

81% vs. 68%

• Use online bill payment

64% vs. 49%

20

Source: MasterCard, “Affluent Foundation Research,” January 2010

21

Anytime Anywhere Banking

Citi Mobile Apps Citi Mobile for Smartphones

22

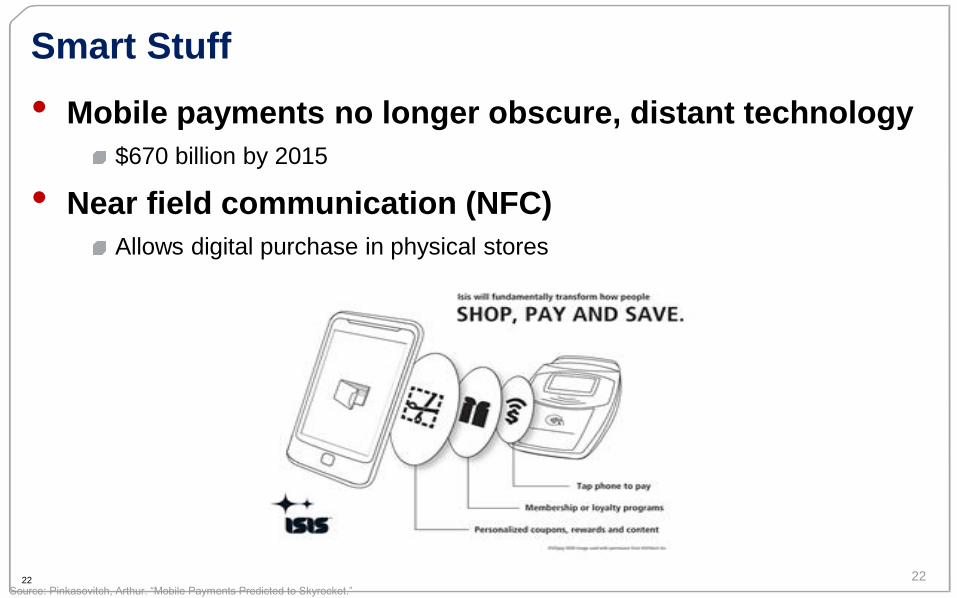

Smart Stuff

• Mobile payments no longer obscure, distant technology

$670 billion by 2015

• Near field communication (NFC)

Allows digital purchase in physical stores

22

Source: Pinkasovitch, Arthur. “Mobile Payments Predicted to Skyrocket.”

23

Citi Mobile Technology

• Omar Khan

• Meet the consumer

• Serve the consumer

• Serve businesses

24

Citi and Google Wallet

25

Citi and Shopkick

• Location Based Technology

Drives traffic t& medium businesses

Rewards shoppers

26

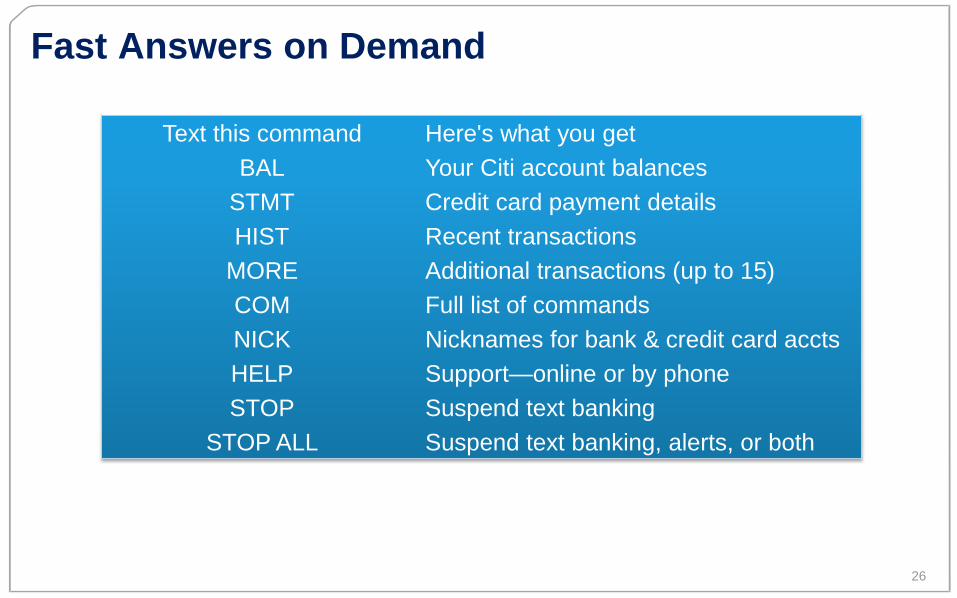

Fast Answers on Demand

Text this command Here's what you get

BAL Your Citi account balances

STMT Credit card payment details

HIST Recent transactions

MORE Additional transactions (up to 15)

COM Full list of commands

NICK Nicknames for bank & credit card accts

HELP Support—online or by phone

STOP Suspend text banking

STOP ALL Suspend text banking, alerts, or both

27

Citi Velocity

• App for institutional clients

28

Real-Time Mobile Access To IPO Orders

29

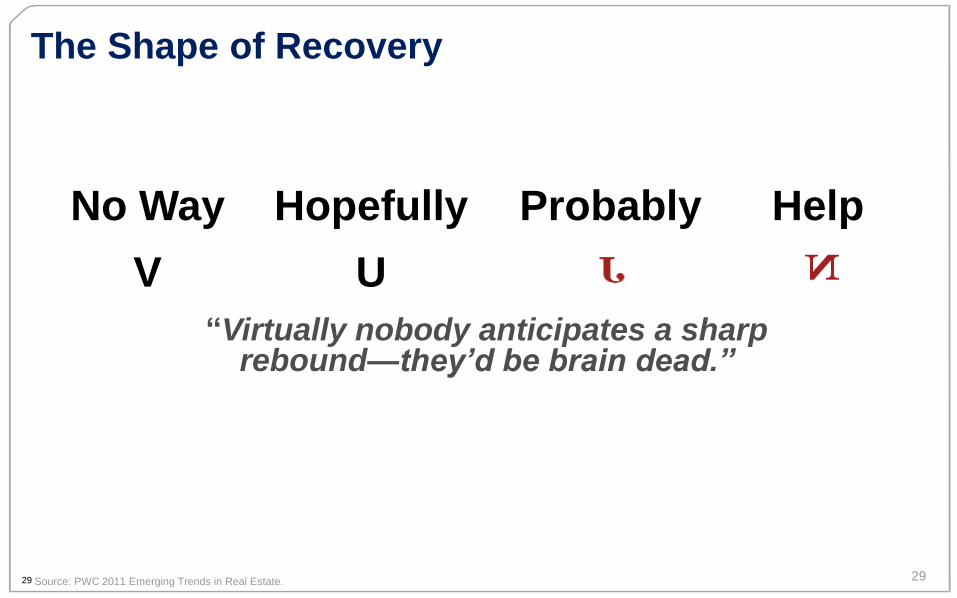

The Shape of Recovery

29

“Virtually nobody anticipates a sharp rebound—they’d be brain dead.”

No Way Hopefully Probably Help

V U

Source: PWC 2011 Emerging Trends in Real Estate.

30

Totally new Citi

• Heritage of the past

• Reality of the present

• Leadership for the future