Upload

adam-thierer

View

217

Download

0

Embed Size (px)

Citation preview

8/14/2019 Mobile TV Primer (Kraemer-PFF)

1/31

Progress on PointRelease 15.11 July 2008 Periodic Commentaries on the Policy Debate

A Primer On the US Mobile Television Market

by Joseph S. Kraemer, Ph. D.*

I. INTRODUCTION

The title of this paper identifies it as a primer, that is, a document that sets forththe basic state and potential for mobile television as of mid-2008.1 The objective is toeducate the reader as to the environment and the opportunity for mobile video. Forthose not familiar with the jargon of mobile television, at the rear this paper contains aglossary of terms and acronyms.

Mobile television involves the transmission of video content to, and reception by,mobile/ handheld devices such as TV-capable cellular phones, vehicle-mounted TVsystems, laptop computers, and/or handheld video players. The content may betraditional TV programming, traditional programming re-formatted for small screens,and/or new formats such as user-generated content.2

Most importantly, mobile digital television is a logical extension of the digitally-

driven development of television from passive entertainment to an interactive, highvalue, versatile medium (see Exhibit 1). 3 Each stage builds upon the set of earlier

stages. Personal television adds functionality and value to web TV which did thesame to digital television which, in turn, did the same to analog broadcast television.The development process is additive and cumulative. Although critically important,mobile television is just one aspect of the evolving personal television stage.

The market for mobile video is forecasted to explode over the next four or fiveyears. The primary factors that are contributing to this are:

*Joseph S. Kraemer, Ph.D. is an Adjunct Fellow at The Progress & Freedom Foundation and a Directorat Law and Economics Consulting Group. He has worked with, and served as counselor to, senior

management at communications, media, and high-tech companies in Asia, Europe, and the Americasand is the author of numerous publications on communications issues. The views expressed in thisreport are his own, and are not necessarily the views of the PFF board, fellows or staff.

1 This paper expands upon certain aspects of another paper: Study of the Impact of Multiple Systems forMobile/Handheld Digital Television, that was co-authored with Dr. Richard Ducey and Dr. Mark Fratrik.

2Mobile television differs from ordinary over-the-air television. The current digital standard for U.S. over-the-air broadcasts was engineered to deliver a digital signal to fixed locations. A proposed mobilestandard will be designed for broadcasters to transmit to mobile devices moving up to vehicular speed.

3 Television in this context refers to video carried over all local distribution platforms (e.g., over-the-air,cable, microwave, telco, and satellite).

1444 EYE STREET, NW SUITE 500 WASHINGTON, D.C. 20005PHONE: 202-289-8928FACSIMILE: 202-289-6079E-MAIL: [email protected] INTERNET: http://www.pff.org

8/14/2019 Mobile TV Primer (Kraemer-PFF)

2/31

Progress on Point 15.11 Page 2

1. The expanding use of cellular telephones, laptops, and other mobile /handheld platforms as entertainment devices used to view bothprofessionally created content (e.g., movies, TV programs) and user-generated content (e.g., YouTube). This phenomenon is especiallyprevalent among population segments under 35 years of age, a

demographic of special interest to many advertisers.

4

2. The increasing availability of spectrum to be used for mobile video.Examples include: (a) the former television channel 55 being used byQualcomms MediaFLO service for mobile television; (b) the potential useby Sprint and Clearwire of spectrum in the 2 GHz range for mobile video;and (c) the expected near-term development of a mobile standard that willfacilitate traditional over-the-air broadcasters targeting mobile receivers fordigital broadcasts as of late 2009.

3. The willingness of mobile device manufacturers to incorporate video

receive functionality into their equipment (e.g., laptops, cellularphones). The incentives for manufacturers are: (a) increased prices due toexpanded functionality; and (b) the potential for consumers to pay toupgrade their devices in order to acquire the new functionality.

Exhibit 1:30 Years of Change and Challenge

Analog Broadcast Television

Centralized; passive; limited channels; single location viewing; limitedvariety of content; emergence of subscription channels

Digital Television

Builds on digital architecture; TV set as display device; high resolution;optional multicasting

Web TV

Cross referral to web sites with video content; TV set or computer asplayer; interactivity; tailored advertising

Personal TelevisionVideo available on demand with display across multiple devices andlocations (mobile television); tailored to the individual; user-generated

content; transactions-enabled (T-Commerce)

Migration Path1980 - 2010

Year2010

Year1980

Analog Broadcast Television

Centralized; passive; limited channels; single location viewing; limitedvariety of content; emergence of subscription channels

Digital Television

Builds on digital architecture; TV set as display device; high resolution;optional multicasting

Web TV

Cross referral to web sites with video content; TV set or computer asplayer; interactivity; tailored advertising

Personal TelevisionVideo available on demand with display across multiple devices andlocations (mobile television); tailored to the individual; user-generated

content; transactions-enabled (T-Commerce)

Migration Path1980 - 2010

Year2010

Year1980

4 For a summary of relevant trends, see Deloittes The State of Media Democracy, based on anOctober 2007 survey.

8/14/2019 Mobile TV Primer (Kraemer-PFF)

3/31

Page 3 Progress on Point 15.11

With respect to a mobile television business model, two major revenue sourcesare in trial: (1) subscription fee-based service (e.g., Verizons V-Cast service); and (2)an advertising-based revenue model in which the video is free to the audience butpaid for by advertisers, depending on the size and/or demographics of the audience. Ingeneral, cellular network operators are more comfortable with, and emphasize, the

subscription model. On the other hand, traditional television broadcasters rely on theadvertising model. Note that the models are not mutually exclusive but could becombined as do cable television system operators.

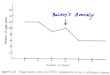

Mobile advertising delivers its messages over devices, such as cellular phones.Mobile advertising is projected to grow at the highest growth rate (41%) in the 2006-2010 period of any media category5 (although off a small base). Other forecasts for thegrowth of mobile advertising are even more optimistic. IDG has published a forecastassigning an annual compounded growth rate of over 100% through 2012. 6 Exhibit 2shows projected mobile advertising spend based on eMarketers review of trends andthird party forecasts. An analysis of these trends shows: (1) a rapid increase is expected

in mobile ad spend; (2) mobile is a key focus area for advertisers and their agents; and(3) mobile video is a key component in the overall growth of mobile advertising. 7

Exhibit 2:Mobile Advertising Spending

$Millions

Source: eMarketer

$421

$903

$1,602

$2,395

$3,415

$4,758

2006(a) 2007(a) 2008(e) 2009(e) 2010(e) 2011(e)

$Millions

Source: eMarketer

$421

$903

$1,602

$2,395

$3,415

$4,758

2006(a) 2007(a) 2008(e) 2009(e) 2010(e) 2011(e)

5 IBM Global Business Services, The End of Advertising As We Know It (2007), Figure 1, p. 5.6

Mobile Advertising Prepares for Take-Off, InfoWorld(September 11, 2007).7 Traditional television broadcasters have extensive experience selling advertising. Broadcasters could

sell and deliver multi-platform advertising programs (on air, web sites, and mobile) that would enhancethe value broadcasters deliver to advertisers, as well as communicate that broadcast television cancombine elements of both new and old media.

8/14/2019 Mobile TV Primer (Kraemer-PFF)

4/31

Progress on Point 15.11 Page 4

Furthermore, cellular phones and vehicles with GPS allow location-basedadvertising, a more focused approach to general mobile advertising. The governmentrequires cellular operators to be able to locate subscribers making emergency calls.Given that location can be determined, there is the potential to tailor advertising to thatlocation (e.g., daily specials offered to carriers of mobile phones within one mile of a

store or shopping center). Market research suggests that several location-basedformats can drive store traffic including: (1) sale alerts; (2) store finder services; (3) giftfinder services; and (4) downloaded coupons/vouchers. 8

In addition to the business model (i.e., advertising and/or subscription), the key

determinants of mobile television economics include the following:

1. Network Capital Requirements

To build out a national network requires substantial capital. As thecapital investment increases, the return on that investment must, by

necessity, also increase.

Operators of existing networks that can be modified to carry mobilevideo (e.g., over-the-air television broadcasters) have an advantage overnetwork operators that must build out a new network (e.g., MediaFLO).For example, in order to launch MediaFLO as a national service,Qualcomm purchased spectrum at auction, purchased additional spectrumfrom third parties that controlled 700 MHz spectrum in other markets, andnow is in the process of building out a nationwide 700 MHz broadcastservice. In its annual report, Qualcomm states that it had an asset base of$457 million as of the 2007 fiscal year end, up from $329 million as of theend of the prior year.9

On the other hand, for over-the-air broadcasters the incrementalcapital cost (i.e., variable cost after the sunk cost of the analog-to-digitalconversion) at the transmitter to send a mobile video signal could be aslow as $100,000.10 Therefore, to incorporate mobile television capabilityinto 1,700 broadcast transmitters11 would cost approximately $170 million,a capital cost that would be spread among all owners of broadcastproperties based on the number of transmitters in service. Furthermore,broadcasters already have the spectrum necessary for digital

8Enpocket, Mobile Marketing: A Vertical Perspective (2006), p. 17. One of the best known mobilemarketing firms, Enpocket was purchased by Nokia in September 2007.

9 Qualcomm Annual Report (2007), p. F-27.10

The cost will be for a non-redundant exciter and multiplexer. Some observers have noted thatbroadcasters may also need to purchase and deploy gap filler low power transmitters to deliverreliable mobile broadcast services in certain markets. Cost estimates range from $100,000 to a high of$350,000.

11Includes commercial and public broadcasting transmitters; excludes low power stations and translators.

8/14/2019 Mobile TV Primer (Kraemer-PFF)

5/31

Page 5 Progress on Point 15.11

broadcasting and do not have to participate in any spectrum auctionsand/or buy/aggregate spectrum from any other source(s).12

2. Access to Receive Devices

There are four major categories of potential receive devices formobile video (i.e., cellular handsets, laptops, vehicles, and portable videoplayers). Each of the four has a dominant set of manufacturers that differby receive device category. These manufacturers must be convinced thatit is in their economic interest to build mobile television receivefunctionality into their devices. Furthermore, it is likely that themanufacturers will include only one receive system on their devices, andthe selection of that single system will be driven by the manufacturersperception of their own economic interest.

3. Access to, and Cost of, Video Content

Content ranges from high-end professionally produced (e.g.,network television programs) to user-generated content. To be successful,content must be so compelling to an audience that the audience will pay asubscription fee and/or advertisers will pay for access to that audience.

At least as far as professionally produced content, the pattern isone of concentration and vertical integration. The producers of suchcontent (e.g., Fox, NBC, CNN, TNT) license the same content to multipledistributors, each of which would have different rights and exclusivewindows-in-time for distribution. That makes it difficult for any mobiletelevision service to have continual access to compelling programming onan exclusive, or even near-exclusive, basis.13

From a public policy perspective, the market-focused wireless broadband policiesof the U.S. have been successful. These policies have made it possible for mobiletelevision to progress rapidly from a general concept to a business that is poised togenerate billions in revenue from tens of millions of users. The reports of the demise ofU.S. technical and business innovation are just plain wrong (at least with respect tomobile television).

Admittedly, the Congress and the FCC made sure that abundant wirelessspectrum became available through auctions, lotteries, or administrative procedures.

But, after that, it has all been market driven. Technology from multiple sources

12 The capital required is often measured in terms of cost per person served. This cost per POP iscalculated by dividing the projected/actual cost to provide a mobile video service to an area, divided bythe total population of that area.

13 In local markets, over-the-air broadcasters have established access to content from: (a) their affiliatednetworks; and (b) local production (especially local news). Other local distributors of mobile televisionservices (e.g., cellular operators, MediaFLO) must license and pay for such content and/or developcontent production capability of their own.

8/14/2019 Mobile TV Primer (Kraemer-PFF)

6/31

Progress on Point 15.11 Page 6

facilitated the convergence of the mobile telephone and traditional television industriesto allow mobile television. The effort is global, especially among the various suppliers ofthe hardware and software platforms that support mobile television. The variousstakeholders appear to be willing to compete without asking for special interestprotection from Washington. Finally, and potentially most important, the millions of

expected mobile television users in the U.S. can be reasonably expected to enjoy lowerprices, more choices, and faster new technology introductions.

II. MOBILE TELEVISION: STAKEHOLDERS AND MARKETS

Within two or three years, mobile television will distribute video content to a massaudience equipped with a range of portable/movable devices. Most likely, mobiletelevision will be distributed using two or more competitive transmission systems (e.g.,WiMAX, MediaFLO, over-the-air digital broadcast systems optimized for mobilereception).

This section describes the range of relevant receive devices and potentialtransmission systems. The final choices for reception and transmission will be driven bya limited number of stakeholders acting in their own best economic interests over thenext 24 to 36 months.

A. Mobile Television Industry Structure and Supply Chain

There are multiple, overlapping layers of the television industry supplychain (see Exhibit 3). These stages remain the same in concept, but may differ in

execution, for traditional television versus mobile television.

1. Program/Content Production: Creates programming for saleto, or under contract from, content aggregators/networks/localdistributors; negotiates with and organizes talent; may or may notretain an ownership interest; includes first run and off-networksyndication, may be national or local (e.g., news); emergingsources include user-generated content.

2. Network Packaging/Content Aggregation: Includesacquisition and scheduling of programming; traditionally sent to a

single affiliate in a market for local redistribution; usually includesmarketing and sale of national/regional advertising; includesbroadcast, cable, satellite, and web-based networks; may besubscriber-supported and/or advertiser-supported; new entrantsinclude Internet-based packagers like YouTube (owned byGoogle).

8/14/2019 Mobile TV Primer (Kraemer-PFF)

7/31

Page 7 Progress on Point 15.11

3. Local Distribution: Involves delivery of one or more videochannels to a fixed or mobile receiver; often includes some localproduction, as well as marketing and sale of local advertisingand/or subscriptions; local infrastructure distribution may bewireless or wired (e.g., via cable or optic fiber); Internet-based

distribution has also emerged.

4. National/Local Advertisers: Pay local/national distributors foraccess to audiences; usually use agents to negotiate withdistributors; source of ads and product placements that are insertedinto programs; the major source of revenue for over-the-airbroadcasters.14

5. Receive Device Manufacturers: Produce devices (e.g.,televisions, laptop computers, cellular phones, handheld videoplayers) used by consumers to view video content; prefer a single

standard against which to manufacturer; classified as consumerelectronics companies; operate as high volume, economies-of-scale producers; usually sell through national and local retail stores,both online and offline; includes companies that provide softwarethat operates on mobile devices (e.g., Google).

Exhibit 3:Stages of the Local Television Supply Chain

NationalContent

Creation

Local Distribution

Broadcast

Subscription(multicast)

On Demand

(unicast)

National

Content

Creation

National

Content

Creation

National

Advertisers

Content

Aggregation

National

Distribution

Local

Advertisers

Local Content

Creation

Traditional:

Fixed

Receivers

Receive Device

Manufacturers/

Retailers

Mobile:

M/H

Receivers

Receive Device

Manufacturers/

Retailers

= Content

= Aggregation/National Distribution

= Advertising

= Local Distribution/Reception

= Consumer Electronics Companies/Retailers

NationalContent

Creation

Local Distribution

Broadcast

Subscription(multicast)

On Demand

(unicast)

National

Content

Creation

National

Content

Creation

National

Advertisers

Content

Aggregation

National

Distribution

Local

Advertisers

Local Content

Creation

Traditional:

Fixed

Receivers

Receive Device

Manufacturers/

Retailers

Mobile:

M/H

Receivers

Receive Device

Manufacturers/

Retailers

= Content

= Aggregation/National Distribution

= Advertising

= Local Distribution/Reception

= Consumer Electronics Companies/Retailers

NationalContent

Creation

Local Distribution

Broadcast

Subscription(multicast)

On Demand

(unicast)

National

Content

Creation

National

Content

Creation

National

Advertisers

Content

Aggregation

National

Distribution

Local

Advertisers

Local Content

Creation

Traditional:

Fixed

Receivers

Receive Device

Manufacturers/

Retailers

Mobile:

M/H

Receivers

Receive Device

Manufacturers/

Retailers

= Content

= Aggregation/National Distribution

= Advertising

= Local Distribution/Reception

= Consumer Electronics Companies/Retailers

NationalContent

Creation

NationalContent

Creation

Local Distribution

Broadcast

Subscription(multicast)

On Demand

(unicast)

National

Content

Creation

National

Content

Creation

National

Content

Creation

National

Content

Creation

National

Advertisers

National

Advertisers

Content

Aggregation

Content

Aggregation

National

Distribution

National

Distribution

Local

Advertisers

Local

Advertisers

Local Content

Creation

Local Content

Creation

Traditional:

Fixed

Receivers

Traditional:

Fixed

Receivers

Receive Device

Manufacturers/

Retailers

Receive Device

Manufacturers/

Retailers

Mobile:

M/H

Receivers

Mobile:

M/H

Receivers

Receive Device

Manufacturers/

Retailers

Receive Device

Manufacturers/

Retailers

= Content= Content

= Aggregation/National Distribution= Aggregation/National Distribution

= Advertising= Advertising

= Local Distribution/Reception

= Consumer Electronics Companies/Retailers

14 Other revenue sources may include: (a) retransmission fees; and (b) advertising revenues from station

web sites.

8/14/2019 Mobile TV Primer (Kraemer-PFF)

8/31

Progress on Point 15.11 Page 8

Participants may be active at one or more levels in the supply chain (i.e.,vertical integration). For example, the television broadcast networks operate ascontent aggregators but own and operate TV stations (i.e., local distribution) anddevelop/own programs (i.e., content creation) that may be distributed locally overbroadcast, cable, or Internet networks. Likewise, local broadcast stations often

produce programs (primarily news) for broadcast on the station, as well asoccasional feeds to an affiliated broadcast network, a local cable news channel,or a co-owned local station.

B. Receiver Categories

There are four general types of portable video devices (i.e., devicescapable of receiving mobile video) in the U.S. market. These four are: (a) cellulartelephones; (b) vehicles; (c) laptop computers; and (d) portable video players.Each of the four is expanded upon below.

1. Cellular Telephones

The number of U.S. cellular phone subscribers is estimated at 257million (Exhibit 4) with an overall population penetration rate of 84.5%15and a subscription rate of 90%+ for the U.S. population segment between20 and 49 years of age. In 2007, U.S. consumers purchasedapproximately 156 million handsets, which means that the embeddedbase of U.S. handsets turns over in less than two years. 16

There are four major U.S. cellular network operators:17

a. AT&T (70 million subscribers);

b. Verizon Wireless (66 million subscribers);

c. Sprint/Nextel (45 million subscribers); and

d. T-Mobile (29 million subscribers).

In addition, there is a set of primarily regional carriers, such as AlltelWireless (13 million subscribers).18

15U.S. population estimated at 304 million based on April 2008 data available from the U.S. CensusBureau. This penetration calculation may overstate actual penetration because of second phones, data-only devices, and other services, such as GMs OnStar.

16 Dr. Joseph S. Kraemer and Richard O. Levine, Study of the Potential for FM Radio to be a UniversalFeature on Cellular Handsets(May 2008), p. 6.

17 Subscriber counts based on 2007 Annual Reports or other operator filings/news releases, and are as ofyear-end 2007.

18 Verizon Wireless has concluded a deal to buy Alltel Wireless (subject to certain regulatory and antitrustreviews).

8/14/2019 Mobile TV Primer (Kraemer-PFF)

9/31

Page 9 Progress on Point 15.11

Exhibit 4:U.S. Cellular Subscribers

0

30

50

70

90

110

130

150

1999 2000 2001 2002

MillionsofSubscribers

170

2003 2004 2005

190

210

2006 2007

220

230

250

0

30

50

70

90

110

130

150

170

190

210

220

230

250

270

Apr. 2008

257

Note: All figures are end of year except 2008; Net U.S. subscriber add rate (2007) = 1.8M/month

Source: Cellular Telecommunications & Internet Association

0

30

50

70

90

110

130

150

1999 2000 2001 2002

MillionsofSubscribers

170

2003 2004 2005

190

210

2006 2007

220

230

250

0

30

50

70

90

110

130

150

170

190

210

220

230

250

270

Apr. 2008

257

Note: All figures are end of year except 2008; Net U.S. subscriber add rate (2007) = 1.8M/month

Source: Cellular Telecommunications & Internet Association

As background, it is important to understand that cellular operatorsin the U.S. have deployed two incompatible cellular telephonetechnologies: CDMA (Verizon Wireless and Sprint) and GSM (AT&T andT-Mobile). Phones that use one of these two technologies cannot work on

a network using the other technology.

19

Furthermore, in general, cellularnetwork operators will not permit consumers to use their phones evenwhen switching between two carriers that use the same networktechnology (e.g., from Sprint to Verizon or vice versa). The operatorsrequire consumers to purchase new phones that are authorized for use ontheir network. The carriers justify these restrictions because they subsidizethe price of handsets, a practice that began in the late 1980s and early1990s, when unsubsidized handset prices were high and constituted abarrier to a mass market for cellular service.

The U.S. closed cellular network model is becoming somewhat

more open.

20

There are three reasons, all interrelated, that are pushingexisting network operators toward a more open model. These are: (a) the

19 For additional detail, see the article by Walter Mossberg, Free My Phone, Wall Street Journal(October 22, 2007), p. R1.

20Closed is used in the sense that the cellular operators control the functionality of handsets that areauthorized for use on their networks. An open network model would be one in which handsetfunctionality is driven by consumer demand and handset device manufacturers responding to thatdemand, as well as testing new functionalities in the market. In the open model, handset subsidies bynetwork operators are reduced substantially over their current levels or eliminated entirely.

8/14/2019 Mobile TV Primer (Kraemer-PFF)

10/31

Progress on Point 15.11 Page 10

Federal Communications Commission required an open model for the keyC block in the Q1 2008 spectrum auctions; (b) Google has announcedthe Android, a Google-designed open model handset; 21 and (c) Verizonhas announced that, no later than December 2008, it will open itswireless network by publishing technical interface standards and allow

subscribers to use wireless devices not provided by Verizon so long asthese devices meet the published standards.22 The move to a more opennetwork model will be an evolution over time.

The cellular industry is competitive. Operators compete on price,network coverage, customer service, and functionality (e.g., voice, data,music, video). The average monthly cellular bill has remained in the $48-$50 range since 2002.23 However, the voice component of operatorrevenue has been decreasing while the non-voice component (primarilydata, especially text messages) has been increasing. For example,Verizon reported that Verizon Wireless experienced a 44% increase in

data revenue per customer in 2007, driven by increased use of messagingand other data services.24 Similarly, AT&T reported a 46.9% increase in2007 in data revenue per wireless customer, and a 4.1% decrease invoice revenue per subscriber.25

What is important here is that non-voice services are the growth area forU.S. cellular operators, while voice services are decreasing as apercentage of the average subscribers monthly spend. Consequently,cellular operators are competing to increase their range of non-voice(including, and especially video) network services.26

Under the current closed model, cellular operators subsidize the

handsets that are sold to subscribers. In very simple terms, if a handsetmanufacturer prices a handset at $400 that is sold to a subscriber by anetwork operator at $50 (with a commitment to a 24-month servicecontract), the $350 difference is a subsidy by the operator that must beamortized (i.e., recovered) over the subscribers life. The total amount ofthe handset subsidy is not trivial. For example, for 2007, Sprint/Nextelreported an equipment net subsidy (i.e., cost of equipment sold inexcess of payments received) of $2.4 billion.27

21

The New York Times, For Google, Advertising and Phones Go Together (October 8, 2007).22

Wall Street Journal, Verizon to Open Cell Network to Others Phones (November 28, 2007), p. B1.23Cellular Telecommunications and Internet Association (CTIA), 2007 Year-End Survey (as of December2007).

24 Verizon Communications, Inc., Form 10-K for the fiscal year ended December 31, 2007 (p. 57).25 AT&T, Form 10-K for the fiscal year ended December 31, 2007 (p. 11).26

While younger consumers (up to age 25) make up a large portion of cellular data/video service usage,there is an increasing number of older mobile Internet users with high-end smartphones, includingBlackberry and Palm handsets. See the Mobile Marketing Associations Understanding MobileMarketing (May 2007).

27Sprint, Form 10-K, for the fiscal year ended December 31, 2007 (p. 46).

8/14/2019 Mobile TV Primer (Kraemer-PFF)

11/31

Page 11 Progress on Point 15.11

Both U.S. consumers and cellular handset manufacturers (e.g.,Motorola, Samsung, LG) are hooked on these subsidies. 28 Consumersprefer to buy a $400 phone for $50 (often rebated) in exchange for aperiod-certain service contract. On the other hand, manufacturers prefer to

build handsets to network operator specifications with both the minimumvolume and price guaranteed by the operator.29 For manufacturers, thetransaction is essentially riskless while the operators are assured thatphones used on its networks have the functionality to support the services(especially non-voice services) sold, or planned to be sold, by the networkoperators.

Cellular operators have launched mobile video services. At thispoint in time, the services seem to be in the advanced beta test businessmodel stage with operators experimenting with a mix of content,subscription price, subscriber contract terms, handset functionality/price,

and incentives/subsidizes. The general consensus among industryobservers is: (a) the current price (around $20 per month) for mobile videoservice is aimed at early adopters (i.e., not sustainable for a massmarket); (b) the coverage is not ubiquitous; and (c) churn (i.e., customersabandoning the service as a percentage of total service takers) is too high(allegedly in double digits per month). There also appears to be aconsensus that over the long term, the ultimate penetration for a mobiletelevision service among cellular users will be approximately 20% at aprice point in the $5-$10 range.30

When looking at the potential revenue from delivery to cellular

handsets, it is important to understand the size of the potential market forcellular-based mobile television. Forecasts vary, but the overall consensusis that mobile television will be a material business for cellular operators. Asample of forecasts is provided below.

ABI Research31

2011: 27 million wireless customers spend$2.3 billion to subscribe to broadcast mobile videoservices from cellular operators (approximatespend per month = $7 per customer)

28

The U.S. subsidy and associated closed network structure is unique and provides almost absolutecontrol to the cellular network operators of the functionality, type, and manufacturer(s) of handsets to beused on their networks.

29 Nokia is an exception. The company prefers to build and sell phones without operator constraints. Theresult is that Nokia has 39% of the world handset market but only 10% of the U.S. market.

30For example, Mercer Management Consulting projected average revenue per unit (ARPU) per month of$4.90 for users of mobile TV over cellular networks. Mercer expects the revenue to be sourced 50-50between advertisers and subscribers with revenue sharing among network operators and contentproviders.

31ABIResearch, U.S. Mobile Broadcast Video Market: Five Predictions (July 26, 2006).

8/14/2019 Mobile TV Primer (Kraemer-PFF)

12/31

Progress on Point 15.11 Page 12

IDC32

2011: 24 million audience to watch video on mobile phones

Veronis Suhler Stevenson33

2011: over 50 million mobile TV subscriptions

OVUM34

2011: 49 million cellular subscribers spending$1.7 billion on mobile video (approximatespend per month = $3 per customer)

With some differences, the key consensus points among theforecasters are as follows:

(a) Mobile television in the U.S. will be a viable business;

(b) Subscribers will ramp up in the 2009-2011 period;

(c) The worst case forecast is for a steady state market of 20+million subscribers and an annual subscription spend over$1 billion; and

(d) The forecasts indicate a low monthly subscription fee paid tothe cellular operators, probably in the range of $5 persubscriber.35

2. Vehicles

Total U.S. sales for new vehicles are estimated to be in the rangeof 15 to 16 million with General Motors having the largest share of themarket (about 25%). Toyota and Ford are expected to be #2 and #3,respectively. Factory-installed video players (primarily for DVDs) havebeen optional equipment in certain new vehicles for a number of years.Such players are not visible by the driver and are located in the rearpassenger area as an in-vehicle entertainment center, most oftenmarketed for use by children. The fact that video screens are not to bevisible by the driver means that mobile television receivers would not be a

32IDC, U.S. Mobile Commercial Video and Television 2007-2011 Forecast (March 2007), quoted bySprint on their web page (posted September 26, 2007) as part of the Sprint announcement that sevenprimetime broadcast hits will be available on-demand over the Sprint network.

33Veronis Suhler Stevenson, Communications Industry Forecast 2007-2011, 21

stedition (2007), p. 325.

34 OVUM, Wireless Content Forecast(U.S. only), custom data run prepared for an NAB report, Study ofthe Impact of Multiple Systems for Mobile/Handheld Digital Television(released January 2008).

35 The low spend per month is the prerequisite for creating a mass mobile television market. The current$20/month subscription fee is not considered viable in the long term.

8/14/2019 Mobile TV Primer (Kraemer-PFF)

13/31

Page 13 Progress on Point 15.11

general, all-vehicle option, but would be an option on a limited number ofmodels within each manufacturers total set of models.

For factory installed options (fully integrated by a manufacturer atthe assembly plant), there are usually two launch windows in each model

year. The absolute best case elapsed time to be included in one of thesewindows would be 18 months (from the time the new product proposal ispresented, through the evaluation process, incorporation into themanufacturing process and concluding when available as an option todealers). The more likely elapsed time would be 24 to 30 months. Theparty proposing the integration of a new product into a manufacturersvehicles must know the precise market for the product which translatesinto the exact set of cars and/or trucks for which the product would beconsidered (e.g., if the buyers are expected to be middle class womenwith children then the relevant vehicle set would be vans and certainSUVs).

This is very important because the ultimate decision is based onfinancial criteria that relate to the economics of each vehicle segment.36For example, if the production level of the relevant vehicle is near thecompanys production capacity, then the decision to include a vehicleenhancement is based on return on variable cost per vehicle (e.g., cost of$200 must return $220 in wholesale dealer price). If the production levelof the relevant vehicle is below capacity, then the decision will involve anassessment of whether the new product will increase sales towardscapacity in which case the decision is not based on incremental cost buton stimulating overall sales and recovery of fixed vehicle costs.

Another route to introduce mobile video receive capability intovehicles would be as a dealer or third party-installed option. 37 This stillmay require a manufacturer to evaluate the new product and may involvedesign work in the manufacturing process. For example, with respect to atelevision, a manufacturer may have to design in a mount or allow forroom in a wiring harness even though the actual installation is done by thedealer or a third party installer.

There is resistance to incorporating new products into currentvehicle lines. This is because the manufacturing process is very complex.For example, the Ford Focus has 34,000 build combinations that reflectthe different vehicles that could be produced given the range of options,colors, and extras available as factory installs. Using the Focus as anexample, if installing a television with over-the-air receive capability

36 Based on interviews with automobile industry representatives.37 To provide some perspective, the projected after market for automobile sound systems is

approximately $2.0 billion, an amount that is 40% of the forecast for factory-installed optionalautomobile sound systems. See CEAs Digital America 2007, p. 47.

8/14/2019 Mobile TV Primer (Kraemer-PFF)

14/31

Progress on Point 15.11 Page 14

became an option, then the number of build combinations would increaseto 68,000 (i.e., the previously cited 34,000 each now with and without theTV option).

The absolutely critical issue is: What is in this for the

manufacturer? If the answer is either unclear or not much, thenincorporation of the new product is a dead issue. In a situation wherethere is a subscription service linked to the new vehicle enhancement(e.g., subscription TV), then the manufacturer would most likely expect toshare in the revenues, including and especially renewals.

Both Ford and GM are known to be experimenting with increasingthe digital-functionality available to drivers. For example, working withMicrosoft, Ford has introduced an option (named SYNC) that integratescellular telephones and portable music players in cars so that a driver canuse voice recognition to call up songs and make/receive calls.38 GM

already has relevant experience in this area because of its On Star servicethat is now available in all new GM vehicles with Qualcomm as a businesspartner. GM also has an equity interest in, and works with, XM Radio,while Ford has an equity interest in Sirius Satellite Radio.

In addition to video reception by a vehicle, there is also datacastingto vehicles. While not requiring much bandwidth, datacasting wouldrequire that the transmission technology be robust such that it could bereceived reliably by vehicles moving at high speed.

GM has been developing a business case for a datacastingserviceto GM vehicles. This plan focuses on how to generate revenue for GMover the useful life of each GM vehicle sold. 39 In order to execute thebusiness plan, GM needs a business partner that has the capability tobroadcast local content (e.g., weather, traffic, gas prices by location) toon-the-road vehicles with relatively robust reception and ubiquitous in-market coverage.40

3. Laptop Computers

Laptops are mobile devices and are replacing desktops as thepersonal computer of choice,41 particularly in the home market, and are

38Ford, Microsoft Create Car System That Lets You Ask for a Song, Wall Street Journal(November 8,2007), p. B1. The estimated price to the consumer is approximately $400.

39 The primary revenue source would be fees paid to advertisers for access to the in-vehicle population ineach separate market in the U.S.

40GM rejected a streaming video service because there appeared to be no ongoing revenue stream.For GM, the rear seat [video] entertainment center was strictly one more option for certain types ofvehicles purchased by a specific segment of buyers as opposed to a driver information data servicethatwould generate monthly revenues after the vehicle was sold.

41Desktops are so Twentieth Century, Business Week(December 18, 2006).

8/14/2019 Mobile TV Primer (Kraemer-PFF)

15/31

Page 15 Progress on Point 15.11

acquiring capabilities to support wireless Internet access and multimediaapplications. Moreover, laptop users are upscale, with demographics thatare attractive to advertisers. For example, wireless laptop users have anaverage household income of $86,600, compared to $60,300 for onlineusers generally.

Laptops may serve as receivers for mobile television services. 42 Atpresent in the U.S., the penetration of analog TV tuners in laptops isminimal. Only two to three percent of laptops today have TV tuners.43Laptop computers are expected to be a growing platform for videoentertainment. Overall laptop penetration is projected to reach 54 percentof U.S. households by 2011 (up from an estimated 41 percent in 2007). 44

Intel predicts that 20 million laptops purchased specifically for the

home will be used for viewing video content by 2010, a 20 percent annualgrowth rate.45 Laptops with video capabilities and issued by corporations

to their employees (and available for out-of-office use) are in addition toIntels forecast. Also, by 2009, 93 percent of all laptops in use areexpected to have wireless Internet connectivity. 46 The marriage of mobiledigital programming with the storage and processing power of the laptopenables collaborative development of potentially compelling applicationsthat can deliver value to both users and advertisers.

It is important to note that the expected useful life of a laptop isapproximately three years (vs. almost three times that for a conventionaltelevision). This means that the embedded base of laptops turns overthree times as fast as the base of television sets. 47 Therefore, a newfunctionality can spread further and faster in the base of U.S. householdlaptops than would be possible, for example, in the base of U.S.household televisions.

42 The potential for mobile reception of video by laptops was analyzed extensively in a January 2007report, prepared for NAB. The January 2007 report noted the need for a more robust reception systemso that laptops could receive reliably broadcast video. See NAB Technology Advocacy Program:Scenario Assessment & Economic Framework(January 2007), prepared by Law & EconomicsConsulting Group (LECG), Chapter V (Reception of DTV Broadcasts on Laptop Computers).

43

This situation contrasts strongly with the situation abroad where cable penetration is less and industry-wide efforts to deploy TV reception capabilities in laptops exist. For example, 50 percent of laptops inGermany have over-the-air digital reception capabilities, as do 100 percent of Japanese laptops.

44 Using multiple sources, OMVC estimates that 30 million laptops that are video-capable are soldannually in the U.S. OMVC, Roadmap, p. 4.

45Note that video content is projected to be viewed. Television is one form of video content with asubset of television programs being provided by broadcasters.

46 Laptops are also capable of wired Internet connectivity (e.g., via an Ethernet port).47 While rapid, the embedded base turn over for laptops (three years) is slower than that for the

embedded base of cellular phones (two years).

8/14/2019 Mobile TV Primer (Kraemer-PFF)

16/31

Progress on Point 15.11 Page 16

Exhibit 5:Household Laptop Penetration

107 108 109 110 111112 114 115 116

117 119

Exhibit 6:Laptop Wireless Connectivity

1416

18

2632

40

4855

5962

64

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Households (mil.) With Laptops (mil.)

Source: Forrester Research, The State of Consumers and Technology: Benchmark 2006

120

100

80

60

40

20

0

U.S.Households(millions)

120

100

80

60

40

20

0

U.S.Households

107 108 109 110 111112 114 115 116

117 119

1416

18

2632

40

4855

5962

64

1416

18

2632

40

4855

5962

64

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Households (mil.) With Laptops (mil.)

107 108 109 110 111112 114 115 116

117 119

1416

18

2632

40

4855

5962

64

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Households (mil.) With Laptops (mil.)

Source: Forrester Research, The State of Consumers and Technology: Benchmark 2006

120

100

80

60

40

20

0

U.S.Households(millions)

120

100

80

60

40

20

0

U.S.Households

107 108 109 110 111112 114 115 116

117 119

1416

18

2632

40

4855

5962

64

1416

18

2632

40

4855

5962

64

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Households (mil.) With Laptops (mil.)

Source: Gartner Group, Telephony (October 23, 2006)

Average WirelessLaptop User HHIncome (2006):

$86,60046%

55%

64%

73%

84%

93%

2004 2005 2006 2007 2008 2009

Average WirelessLaptop User HHIncome (2006):

$86,60046%

55%

64%

73%

84%

93%

2004 2005 2006 2007 2008 2009

Source: Gartner Group, Telephony (October 23, 2006)

Average WirelessLaptop User HHIncome (2006):

$86,60046%

55%

64%

73%

84%

93%

2004 2005 2006 2007 2008 2009

Average WirelessLaptop User HHIncome (2006):

$86,60046%

55%

64%

73%

84%

93%

2004 2005 2006 2007 2008 2009

8/14/2019 Mobile TV Primer (Kraemer-PFF)

17/31

Page 17 Progress on Point 15.11

4. Portable Video Devices

A portable video device is defined as a device that can receiveover-the-air video directly. This type of device is a subset of the MP3

category of electronic devices that, according to the Consumer ElectronicsAssociation (CEA), let consumers listen to music, watch TV programs ormovies, and access content whenever and wherever they want. 48 Inaddition, U.S. sales of video-capable MP3 devices are projected toincrease at a compounded annual growth rate of 65.9% (2006-2010). 49

Mobile devices continue to benefit from rapid advances in

maturization and the decreasing cost of storage technology. One examplewould be the i-series50 devices from Apple. The iPod is a single purposeportable music player that sold 51.6 million units in 2007, and accountedfor $8.3 billion in 2007 net sales revenue. 51 In 2005-2006, cellular

operators introduced proprietary music download services that combinedmusic and telephone functionality in a single device (the cellular telephonehandset). Although none of these cellular download services achieved thesuccess of the iPod, Apple responded to the competitive threat byintroducing (2007) the iPhone that also combined music and telephonefunctionalities.52 The bottom line was that Apples management believedthat there was a material competitive threat from the cellular operators andresponded with entry into the telephone handset business. 53

Another example of a portable video receiver would be the Nokia

N92.54 The N92 can:55 (a) receive over-the-air television broadcasts; (b)

download video content from a computer; (c) record and store TVprograms; (d) download programs from the Internet via a wireless LAN-type connection; (e) provide limited interactivity, such as requesting VoDservice downloads; (f) make/send videos using an integrated videocamera; and (g) play music by means of a player or receive over-the-airradio stations by means of an integrated FM tuner. Nokia claims that theN92s battery can support four hours of TV viewing without recharging.

48Digital America 2007, p. 1.49Digital America 2007, p. 16.50

MP3 devices began as audio players, but now have audio, photograph, and video play-backcapabilities. FM radio broadcasters already work with Apple in that OTA songs are tagged for later

download to iPods.51Apple Inc., Annual Report (Form 10-K) for the fiscal year ended September 29, 2007 (p. 42). iPod salesrevenue includes music downloads and ancillary equipment, as well as the iPods themselves.

52 iPhone unit sales in Apples fiscal year 2007, were 1.4 million units and $123 million in recognizedrevenue. See Apples 10-K, pp. 42-43.

53For additional detail, read the Harvard Business School case, iPod vs. Cell Phone: A Mobile MusicRevolution? (August 2006).

54 The N92 (and successor models) is designed to work with the European video standard (DVB-H).55 Nokia, One Device; Many Opportunities, A Descriptive Brochure on the N92 (2006). The N92 also

serves as a GSM phone that, in Europe, can roam across national networks.

8/14/2019 Mobile TV Primer (Kraemer-PFF)

18/31

Progress on Point 15.11 Page 18

C. Mobile Video Competitive Transmission Options

Local distribution to mobile receivers is just emerging. The potential localnetwork transmission options are:

1. Cellular telephone networks that carry video through their 3G digitalnetworks;

2. Local broadcasters using a portion of their DTV signal that isoptimized for mobile and handheld receivers;

3. Other terrestrial networks (e.g., L-Band, WiMAX) that operateoutside the traditional networks of either local television broadcasters orthe cellular operators; and

4. Distribution by satellite to terrestrial mobile receivers.56

The local transmission of mobile television to mobile receivers remains influx. For example, although cellular operators are developing mobile videoservices, distribution of video programs in the broadcast mode to a massaudience via cellular networks appears wasteful of bandwidth, would lead tonetwork congestion, and may result in lower-than-required quality of service formore profitable products, such as text messaging.57 To avoid that problem andleave the economics of cellular networks intact and unburdened by massaudience broadcast video, cellular operators, such as Verizon Wireless, havenegotiated for network capacity outside their core cellular network.

1. Cellular Networks

The major U.S. cellular network operators operate 3G networks thatare based on GSM (AT&T and T-Mobile) or CDMA (Verizon and Sprint)technology. All four offer high-speed data and video services to theirmobile subscribers. At this point in time, the only one of the four to puttheir video service on a separate network from their cellular network isVerizon (via the MediaFLO 700 MHz network). The others offer videoservice through their cellular networks.

Both CDMA (via Evolution-Data Only [EV-DO] technology) and

GSM (via High-Speed Downlink Packet Access [HSDPA] technology)

56 A distribution option that is being used more in Asia than the U.S. In the U.S., satellites have beenproposed for use as a national distribution channel to interconnect terrestrial local distribution systems(e.g., HiWire with SES Americom, Clearwire with ICO Global).

57 Yoram Solomon, The Economics of Mobile Broadcast TV. Solomon is President of the Mobile DTVAlliance, an organization that advocates use of the DTV-H standard. For additional data on the currentand expected future consumer spend patterns on mobile services, see the Veronis Shuler StevensonCommunications Industry Forecast 2007-2011, pp. 151, 299, and Chart 11.30 (pp. 330-31).

8/14/2019 Mobile TV Primer (Kraemer-PFF)

19/31

Page 19 Progress on Point 15.11

networks can be modified to mix high-speed data/video with voiceservices.58 However, real-time, broadcast (one-to-many) televisionprogramming sent to cellular customers over the cellular network tends toincrease network congestion and cause problems for voice and textusers.59 The bottom line is that broadcast (one-to-many) or multicast (one-

to-some) video traffic through a cellular network may be technicallyfeasible but economically suboptimal.

One solution for cellular network operators is to offload video traffic(especially real-time broadcast video traffic such as could occur during atelevised sports event) onto a second, video-capable network. Assuming adual-mode receive device (i.e., receipt of both the cellular and the videonetworks by a single mobile device transparent to the user) was in-use, anancillary benefit to the use of dual networks would be the potential forinteractivity with the cellular network providing the return channel. 60 Thedual network solution assumes that mobile video delivers real-time video

programs that are popular and available on a broadcast basis to a massaudience using mobile devices. Note that a dual network solution isconsistent with the attempts by cellular operators (e.g., Verizon Wirelesswith MediaFLO, AT&T with Aloha spectrum, Sprint with Clearwire) tosecure a parallel network to deliver mobile video service without tying upcellular network bandwidth.

2. Over-the-Air Broadcast Television

Over-the-air television broadcasting in the United States is poisedfor the scheduled shut-off date of all high power analog transmissions in

February, 2009. From then on, the broadcast television industry will be alldigital.

Broadcasters are developing business models that are possiblewith digital television. In addition to sending their main programmingsignal, television broadcasters are able to use the remainder of their 6MHz channel for other purposes. Broadcasters are already takingadvantage of that flexibility with multicasting several signals, datacasting,and other applications.

One potential additional usage of the digital channel is to broadcast

directly to mobile and/or handheld receivers.

61

Currently, receiving the58

Kumar, Mobile TV, Chapter 4.59 Solomon, The Economics of Mobile Broadcast TV.60 TV on a Mobile: Extending the Entertainment Concept by Bringing Together the Best of Both Worlds,

IBM Institute for Business Value (2006), p. 9.61 An indication of the optimism and interest of the broadcasting industry for introducing mobile service is

the creation and subsequent actions of the Open Mobile Video Coalition (OMVC). As of earlyDecember 2007, the OMVC had over 420 commercial television stations among its members, as wellas the support of broadcast trade organizations and public television. Its purpose is simply to

8/14/2019 Mobile TV Primer (Kraemer-PFF)

20/31

Progress on Point 15.11 Page 20

over-the-air television signal in a mobile environment is possible but is notreliable. Therefore, an important step for mobile broadcasting is thedevelopment of technological standards for use in the United States.62

Through the Advanced Television Systems Committee (ATSC), this

process of standard setting for a mobile broadcast service is underway.Because of the interests of many of the parties involved, thestandardization process has been sped up in order to have a systemdeployable in a relatively short time. Broadcasters have stated an intentionto put a mobile standard in place by early 2009. 63 As part of the drive toaccelerate the standards selection process, the two leading contenders,Samsung and LG Electronics, announced (May 2008) that they would beteaming to provide a jointly-developed system, rather than two competingsystems.

It should be pointed out, that other non-standard setting activities

must also be going on at the same time as the ATSC standard settingprocess, in order to have mobile video become a meaningful source ofrevenue for the broadcast television industry in the next five years. Theseinclude:

a. Broadcasters intending to offer mobile video programservices which are simulcasts of their main channels (HDTVor SDTV) must clarify their rights to do so with programowners.

b. Companies must negotiate reasonable and non-discriminatory rights to intellectual property associated withthe selected mobile standard.

c. Reliable audience measurement procedures must be put inplace to measure the mobile audiences in order forbroadcasters to sell advertising on those services.

d. Broadcasters must install and use transmission equipmentthat can transmit programming optimized for mobile

accelerate the development of mobile digital broadcast television ... in the United States. This grouphas made great strides in moving this process along already such as sponsoring and leading the testingof several proposed mobile systems.

62 The setting of standards is a complex process involving companies on many different sides of aparticular technology (including broadcasters, transmitter companies, consumer electronicscompanies). When there are multiple candidate systems vying to become the standard, the processbecomes even more involved and lengthy. Often a standard setting process from the initiation throughthe publication of the final standards can take four years, if not longer.

63 Without early entry by broadcasters into the mobile video market, it will be very difficult to gain marketshare from those entering the market before them.

8/14/2019 Mobile TV Primer (Kraemer-PFF)

21/31

Page 21 Progress on Point 15.11

reception.64

e. There must be promotion of the mobile service so thatconsumers are aware of what programs are available.65

f. Finally, and potentially most important, the broadcastindustry has to assume a leadership position and negotiatewith manufacturers of mobile receivers (i.e., cellulartelephones, laptops, vehicles, and other portable videodevices) to ensure that these devices may receive over-the-air digital programs transmitted by broadcasters.66

3. 700 MHz Service (MediaFLO)

Spectrum at 700 MHz offers multiple advantages for mobiletelevision transmission including, and especially, the best in-building

coverage among the spectrum blocks being used or considered for mobilevideo applications. Another key advantage is that fewer cell sites arerequired in order to cover a specific metropolitan area.

The primary service now being offered at 700 MHz is the multicastMediaFLO service of Qualcomm. MediaFLO USA is deploying and intendsto operate a national network that will broadcast video and audioprogramming to wireless subscribers in the U.S. The spectrum for theservice is at 700 MHz and was acquired primarily at auction byQualcomm.

This wholesale service is now deployed in the U.S. with VerizonWireless as a customer and MediaFLO may also be utilized by AT&TMobility. The spectrum used corresponds to UHF channel 55 that is in theprocess of being cleared as part of the analog-to-digital conversion ofbroadcast television.67

MediaFLOs business model involves aggregation and distributionof content in packages that the company makes available on a wholesale

64The cost of such equipment is estimated to be in the range of $100,000-$200,000 per station. Inaddition, locations with a potentially high volume of mobile users (e.g., airports) may be at a significant

distance from transmitters. In-building reception may be possible only with a repeater. The cost ofsuch repeaters could be borne by building owners/facility operators, but that has yet to be determined.

65Ideally, such promotion would be coordinated with the February 2009 cut-off of analog broadcastservice.

66 Mobile devices may not be able to efficiently support antennas and tuners for multipleservices, sothere may be competition among program suppliers to have a laptop support their services ormodulation schemes (e.g., DVB-H) on an exclusive basis.

67 MediaFLO has apparently paid some incumbents to accelerate the movement out of the channel 55slot. COFDM is completely incompatible with the ATSC DTV modulation standard and could not betransmitted by U.S. broadcasters.

8/14/2019 Mobile TV Primer (Kraemer-PFF)

22/31

Progress on Point 15.11 Page 22

basis to wireless operators.68 The distribution, marketing, billing andcustomer [subscriber] relationships are provided by the wireless carrierswho buy the MediaFLO service at wholesale from Qualcomm. The modelis similar to a provider of cable television channels who sells at wholesalemultiple channels (usually for so many cents per subscriber per month) to

a direct broadcast satellite (DBS) system operator. Qualcomm operatesMediaFLO in the United States as part of its Strategic Initiatives SegmentThe 2007 annual report of Qualcomm listed $457M in assets forMediaFLO USA and a $118 million increase in pre-tax losses in 2007 over2006.69

With respect to the existing MediaFLO service, the service carries

some of the national broadcast television networks, such as Fox and NBC.The programming is time shifted and not simulcast with local broadcastertransmission of broadcast network feeds. Commercials remain in theMediaFLO service to the extent that such commercials were present in the

source programming. Currently, there is no provision for the insertion oflocal content or local advertising. However, reports are that MediaFLO isin its infancy and that local insertions are one of the possible futurescenarios. It appears that Qualcomm is still experimenting with revenuemodels including charging wireless operators for some combination of usefees, per subscriber fees, and/or revenue sharing.

In 2006, AT&T Wireless announced its intention to also launch aretail video service that would use the MediaFLO service as its networkcarrier. Originally, this service was to have launched in 2007, but, inOctober, AT&T announced a launch delay until 2008. 70

AT&T purchased two 700 MHz UHF channels (54 and 59) from

Aloha Partners, a company that at one point, planned to launch a mobiletelevision service to compete with MediaFLO. The Aloha system was to bebased on DVB-H technology. AT&T will pay approximately $2.5 billion forthe Aloha Partners licenses. The purchased spectrum (12 MHz permarket in most markets) covers 196 million people in 281 markets,including 72 of the top 100 markets and all ten of the top ten markets. 71There appears to be no public disclosure of what AT&T intends to do withthe Aloha spectrum (i.e., communications and/or mobile television).

In Q1 2008, the FCC auctioned additional 700 MHz spectrum. Thisspectrum is considered highly desirable for use across the full range of

68 Primary Source: Qualcomm Inc. Form 10-K filed with the SEC for FY 2007 ending September 2007.See pages 4, 12, 28, 45, 54, F-27.

69 Qualcomm Inc., Annual Report (form 10-K) for the fiscal year ended September 30, 2007, pp. 54 andF-26/27.

70 AT&T Delays Mobile TV Launch, Daily Wireless(posted October 29, 2007).71

AT&T press release, AT&T Acquires Wireless Spectrum from Aloha Partners (October 9, 2007).

8/14/2019 Mobile TV Primer (Kraemer-PFF)

23/31

Page 23 Progress on Point 15.11

mobile services, including video.72 Kagan estimated that a 700 MHznational, 20 video channel network covering 200 million in populationcould be built out for $450 million (excluding the cost of spectrumacquisition).73 Kagan concluded that such a network could get [cellular]carriers into a robust mobile video business fast.

4. L-Band Service (Modeo)74

In early 2006, Modeo, a subsidiary of Crown Castle International, 75

announced that it would deliver mobile TV to the top 30 markets in theU.S. This announcement followed a pilot test in Pittsburgh. At one point(mid-2006), Modeo was negotiating a joint mobile TV venture with AT&T,but the deal never closed. Modeo attempted to go it alone and launched aNew York City trial in January 2007. The Modeo business model wassimilar to that of MediaFLO, namely, build out a national mobile TVnetwork and then sell capacity at wholesale to one or more of the cellular

operators that would then sell mobile TV service to subscribers at a retailprice.

In July 2007, Crown Castle announced that it would close Modeoand take a write off. The L-band spectrum was then leased to aninvestment group for $13 million annually from 2007 to 2013 with a back-end buyout provision by the lessee organization.76 Trade pressspeculation was that the demise of Modeo resulted from: (a) a lack ofcapital to complete a nationwide network build-out; (b) too little spectrumin comparison to MediaFLO and Aloha Partners; and (c) no cellularpartner/anchor tenant for the proposed service.

Based on propagation characteristics and transmitter power, Kaganestimated that, to cover 200 million of the U.S. population, it would take 15times the number of transmit sites using L-band as it would at 700 MHz.77In this scenario, Kagan further estimated that the capital spend required atL-Band would be five times that at 700 MHz for the same coverage, whichled Kagan to conclude that use of 700 MHz for mobile video wascompelling (and by comparison, the use of L-Band was not economically

72 The total paid for the spectrum was approximately $19 billion. The major winners were Verizon, AT&T,and EchoStar. The spectrum won by AT&T may be consolidated with the spectrum purchased fromAloha Partners to provide fourth generation mobile services (including video). See What 700 MHz

Winners Can Do With Their Spectrum (April 15, 2008), published by Stifel Nicolaus, an InvestmentBanker.

73Kagan Research, 700 MHz Players Ready to Play Ball (2006), p. 7.

74 The term L-Band is used to denote spectrum in the one to two GHz range. Crown Castles Modeoservice used spectrum at about 1.7 GHz.

75Crown Castle operates and manages over 20,000 cellular towers for U.S. cellular operators. Toweraccess would have facilitated the build out of the proposed Modeo video service.

76 Crown Castle press release, Crown Castle Announces Long-Term Modeo Spectrum Lease (July 23,2007).

77Kagan Research, 700 MHz Players Ready to Play Ball (2006), p. 7.

8/14/2019 Mobile TV Primer (Kraemer-PFF)

24/31

Progress on Point 15.11 Page 24

viable). The comparative cost estimates generated by Kagan go a longway toward explaining the demise of the Modeo venture.

5. Sprints WiMAX Service

Sprint controls substantial spectrum in the 2.5 GHz band and hasannounced plans to provide high-speed data service using the WiMAXstandard.78 Service was supposed to begin in 2008 in a limited number ofmajor markets and then expand in 2009. The upfront capital cost wasprojected to be equal to, or greater than, $5 billion, which amounts toapproximately $50 per person for each of the almost 100 million people tobe covered.

There had been speculation that Sprint would use its 2.5 GHzspectrum for a mobile TV service. 79 The business logic to use thespectrum for video was that: (a) a one-way broadcast service would

require less capital to build out than a two-way data service; (b) use of itsown spectrum would provide more control to Sprint than signing a dealwith MediaFLO; and (c) Sprint had close relationships with cable televisioncompanies that could be a source of video content. 80

For a time, financial difficulties at Sprint called into question the

companys ability to build out the planned WiMAX network.81 However, inMay 2008, Sprint announced that an agreement with ClearwireCorporation to combine their 2.5 GHz spectrum to form a new wirelesstelecommunications company.82 The new company will be calledClearwire. In addition, five strategic investors (Intel, Google, Comcast,

Time Warner Cable, and Bright House Networks) have agreed to invest$3.2 billion for approximately 22% of the new company. Sprint will own51% of the company.

By the end of 2010, Clearwire is to have in place, a WiMAX networkthat will serve 120 to 140 million people. While the range of expected

78Sprint-Nextel Corp., Annual Report (Form 10-K) for the fiscal year ended December 31, 2006, p. 5.

79For example, see ABI Research, U.S. Mobile Broadcast Video Market: Five Predictions (July 2006).

On the other hand, there has also been public speculation that Sprint lacks the financial capacity tobuild out the WiMAX service.

80Currently, Sprints relationship with the cable industry appears to have cooled. See Sprint FreezesPivot, Multichannel News(July 20, 2007). Pivot is a Sprint mobile phone service marketed byComcast, Cox, Time Warner, and Bright House.

81In the meantime, Sprint continued to sell its Sprint Power Vision TV Pack for $20 per month thatdelivers 20 TV channels including seven popular prime time programs (e.g., CSI: NY, DesperateHousewives, Greys Anatomy) over its cellular/ PCS network.

82 Sprint and Clearwire to Combine WiMAX Businesses, Creating a New Mobile Broadband Company,Sprint Press Release (May 7, 2008).

8/14/2019 Mobile TV Primer (Kraemer-PFF)

25/31

Page 25 Progress on Point 15.11

services is still under development, most likely mobile video via high-speed Internet connection will be a featured service.83

The propagation characteristics of 2.5 GHz for mobile video are not

as ideal as those at 700 MHz. On the other hand, Clearwire will have

access to the 60,000 existing cell sites of Sprint so that will enable arobust local WiMAX overbuild on top of the existing Sprint cellular network.

6. Satellite Service

In 2006, HiWire and satellite operator SES Americom announcedthat the two companies would act as partners for mobile video servicetrials.84 The satellite operator was to aggregate and process content in itsNew Jersey operations center. Then SES Americom would uplink thecontent from there to Aloha Partners receive locations where that contentwould be tailored to the local market and sent out over HiWire 700 MHz

spectrum to handheld, mobile devices of participating cellular operators.85

There is no public indication that the SES Americom partnership survivedthe business termination of Aloha Partners.

A more recent instance of the potential use of a satellite platform aspart of a mobile video service was the joint announcement of ICO Global(a provider of satellite services) and Clearwire Corporation (prior to theSprint transaction discussed above) to collaborate on a mobile videotrial.86 Clearwire is controlled by Craig McCaw and holds terrestriallicenses for 2.5 GHz spectrum. ICO is also controlled by McCaw andlaunched a geo-stationary satellite into orbit (April 2008). One announced

purpose of the joint test is to determine whether there are spectrumefficiencies in the two companies working together.87

In neither the SES Americom-Aloha venture nor the Clearwire-ICO

Global announced test, is there any indication of a direct satellite-to-handheld device video service. It appears that the satellite component isused for national distribution to local redistribution sites, a use very similarto that made of satellites by traditional over-the-air broadcast networks.88

83 Access via the Internet would involve linking to websites where video content would be available (e.g.,

NBC.com) on a subscription or free basis. Clearwire could also develop its own broadcast servicesuch as that deployed by MediaFLO.

84

SatNews Daily, HiWire Teams with SES Americom for Broadcast Mobile TV Trial (April 26, 2006).85The primary cellular partner was to be T-Mobile.

86Clearwire-ICO Global Joint Press Release (October 9, 2007).

87 ICO has also applied to the FCC for permission to build out terrestrial facilities that would re-use thespectrum assigned to ICO for its space segment. Such a re-use is termed an ancillary terrestrialcomponent (ATC) and allows a satellite company like ICO (probably with one or more partners, suchas cellular or cable operators) to operate a communications segment in which voice and data trafficmay be passed between ground and receivers without transiting through a satellite.

88 Note that this approach is different than that used in Korea and Japan, where there are direct broadcasttransmissions from the satellite to mobile devices.

8/14/2019 Mobile TV Primer (Kraemer-PFF)

26/31

Progress on Point 15.11 Page 26

The situation could change when XM Satellite Radio and SiriusSatellite Radio merge.89 In combination, at year-end 2007, the two hadapproximately 17 million subscribers.90 When merged, the two would mostlikely eliminate redundant audio channels, thereby freeing up bandwidth

that could be used to transmit video to mobile receivers (with a potentialemphasis on reception by vehicles given the existing relationships amongthe satellite radio companies and the automobile manufacturers).

89 The agreement was signed in February 2007. The Department of Justice approved the merger inMarch 2008.

90See the 2007 Form 10-Ks for both XM Satellite Radio Inc. and Sirius Satellite Radio Inc.

8/14/2019 Mobile TV Primer (Kraemer-PFF)

27/31

Page 27 Progress on Point 15.11

III. APPENDIX: GLOSSARY

3G: The third generation wireless service promises to provide high data speeds,always-on data access and greater voice capacity. The high data speeds enable fullmotion video, high-speed Internet access and video-conferencing, and are measured in

Mbps. 3G technology standards include UMTS, based on WCDMA technology (quiteoften the two terms are used interchangeably), and CDMA2000, which is the evolutionof the earlier CDMA 2G technology. UMTS standard is generally preferred by countriesthat use GSM network.

ARPU: Average revenue per user.

ATSC: The Advanced Television Systems Committee is a digital television standardused in North America, Korea, and some other countries. It uses 6-MHz channelspreviously used for NTSC analog TV to carry a number of digital TV channels. It isbased on the use of MPEG-2 compression and transport stream, Dolby digital audio,

and 8-VSB modulation.

CDMA (Code Division Multiple Access): A technology used to transmit wireless callsby assigning them codes. Calls are spread out over the widest range of availablechannels. Then codes allow many calls to travel on the same frequency and also guidethose calls to the correct receiving phone.

CDMA2000: Code division multiple access is a 3G evolution of the 2G cdmaOnenetworks under the IMT2000 framework. It consists of different air interfaces suchCDMA20001X (representing use of one 1.25-MHz carrier) and CDMA 2000 3X, etc.

Cell: The basic geographic unit of wireless coverage. Also, shorthand for genericindustry term cellular. A region is divided into smaller cells, each equipped with alow-powered radio transmitter/receiver. The radio frequencies assigned to one cell canbe limited to the boundaries of that cell. As a wireless call moves from one cell toanother, a computer at the Mobile Telephone Switching Office (MTSO) monitors the calland at the proper time, transfers the phone call to the new cell and new radio frequency.The handoff is performed so quickly that its not noticeable to the callers.

COFDM: Coded OFDM employs channel coding and interleaving in addition to theOFDM modulation to obtain higher resistance against multipath fading or interference(see OFDM). Channel coding involves forward error correction and interleaving involvesthe modulation of adjacent carriers by noncontiguous parts of the signal to overcomebursty errors.

DAB: Digital audio broadcasting is an international standard for audio broadcasting indigital format. It has been standardized under ETSI EN 300 401 (also known as Eureka147 based on the name of the project). DAB uses a multiplex structure for transmitting arange of data and audio services at fixed or variable rates.

8/14/2019 Mobile TV Primer (Kraemer-PFF)

28/31

Progress on Point 15.11 Page 28

DMB: Digital multimedia broadcasting is an ETSI standard for broadcasting ofmultimedia using either satellites or terrestrial transmission. DMB is a modification of thedigital audio broadcasting standards. The DMB services were first launched in Korea.

Dual Band: A wireless handset that works on more than one spectrum frequency (e.g.,

in the 800 MHz frequency and 1900 MHz frequency bands.

DVB-H: Digital video broadcasting-handhelds is a DVB standard for mobile TV andmultimedia broadcasting. DVB-H is a modification of digital terrestrial standards byadding features for power saving and additional error resilience for mobiles. The DVB-Hsystems can use the same infrastructure as digital terrestrial TV under DVB-T. DVB-Hservices have been launched in Italy, Germany, and other countries.

ETSI: European Telecommunications Standards Institute.

EV-DO: Evolution data optimized is an evolution of the CDMA2000 (3G) standards and

provides for high-speed data applications.

GPS (Global Positioning System): A worldwide satellite navigational system, madeup of 24 satellites orbiting the earth and their receivers on the earths surface. The GPSsatellites continuously transmit digital radio signals, with information used in locationtracking, navigation and other location or mapping technologies.

GSM: Group Special Mobile, which established recommendations for a global systemof mobile communications, adapted initially in Europe and worldwide shortly thereafter.

HSDPA: High-speed downlink packet access is an evolution of 3G-UMTS technologiesfor higher data speeds. HSDPA can provide speeds of up to 7.2 Mbps at the currentstage of evolution.

IMT2000: The ITUs framework for 3G services. It covers both CDMA-evolved services(CDMA2000) and 3G-GSM-evolved services (3G-UMTS). Different air interfaces suchas WCDMA, TD-CDMA, IMT-MC (CDMA2000), DECT, and EDGE form a part of theIMT2000 framework.