Embed Size (px)

Citation preview

Slide subtitle

Trevarin GovenderMcommerce, Ericsson

Mobile Payments| Implementation Considerations

Mobile Payments and NFC | Ericsson Internal | 2014-03-25 | Page 2

2,2B

6Bmobile phone users in

the world

prepaid accounts

served by Ericsson

Charging System

2,5Bpeople lack bank

accounts in the world

50Breal-time transactions

handled per day

Slide subtitle

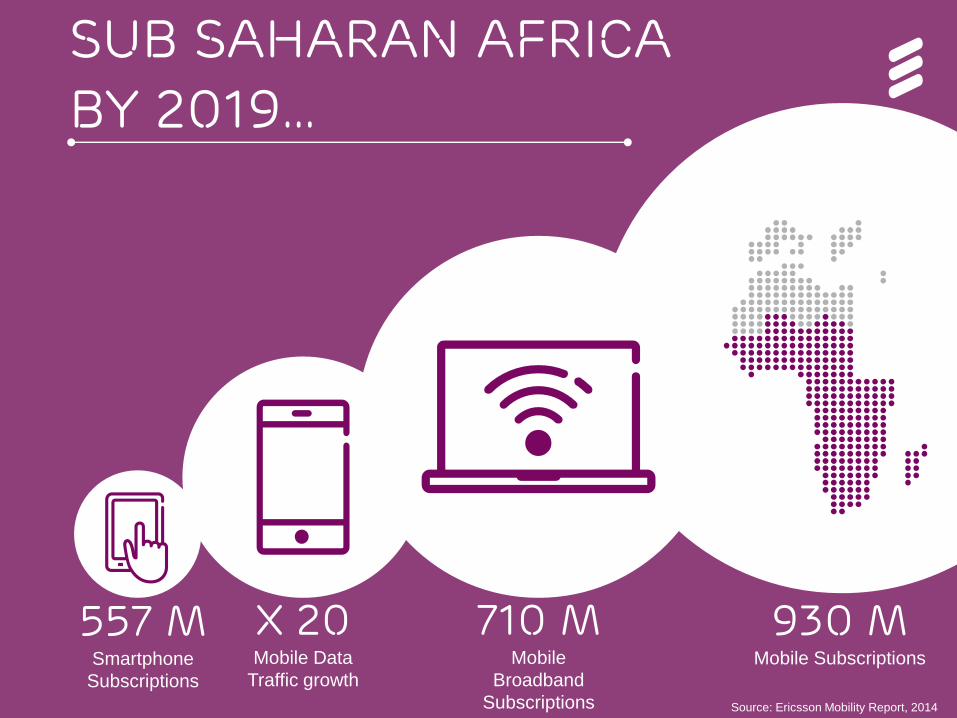

Sub saharan africa

By 2019…

557 MSmartphone

Subscriptions

930 MMobile Subscriptions

X 20Mobile Data

Traffic growth

710 MMobile

Broadband

Subscriptions Source: Ericsson Mobility Report, 2014

Mobile Payments and NFC | Ericsson Internal | 2014-03-25 | Page 4

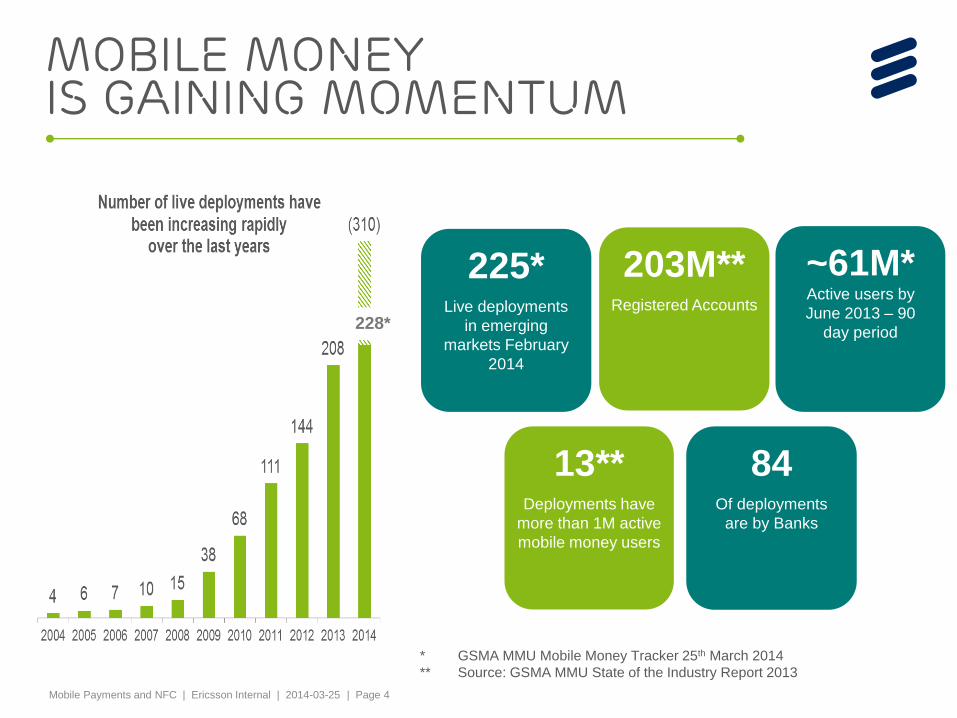

Mobile moneyis gaining momentum

* GSMA MMU Mobile Money Tracker 25th March 2014

** Source: GSMA MMU State of the Industry Report 2013

228*

203M**Registered Accounts

~61M*Active users by

June 2013 – 90

day period

225*Live deployments

in emerging

markets February

2014

13**Deployments have

more than 1M active

mobile money users

84Of deployments

are by Banks

Mobile Payments and NFC | Ericsson Internal | 2014-03-25 | Page 5

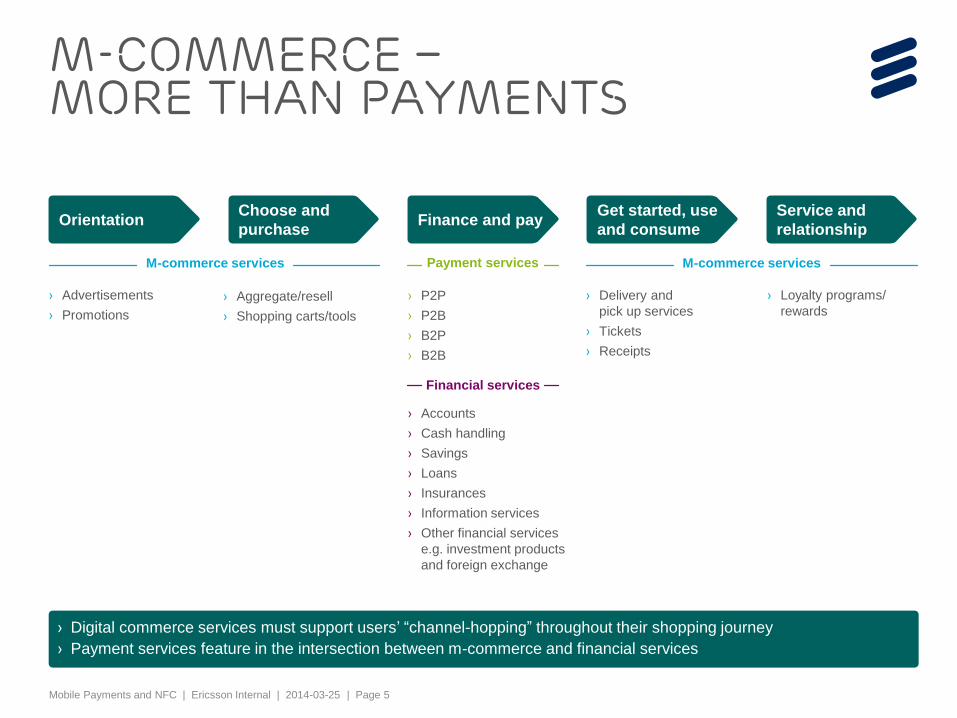

M-commerce –more than payments

Orientation

M-commerce services

Financial services

Payment services

Choose and

purchaseFinance and pay

Get started, use

and consume

Service and

relationship

› Advertisements

› Promotions

› Aggregate/resell

› Shopping carts/tools

› P2P

› P2B

› B2P

› B2B

› Accounts

› Cash handling

› Savings

› Loans

› Insurances

› Information services

› Other financial services

e.g. investment products

and foreign exchange

› Digital commerce services must support users’ “channel-hopping” throughout their shopping journey

› Payment services feature in the intersection between m-commerce and financial services

› Delivery and

pick up services

› Tickets

› Receipts

› Loyalty programs/

rewards

M-commerce services

Mobile Payments and NFC | Ericsson Internal | 2014-03-25 | Page 6

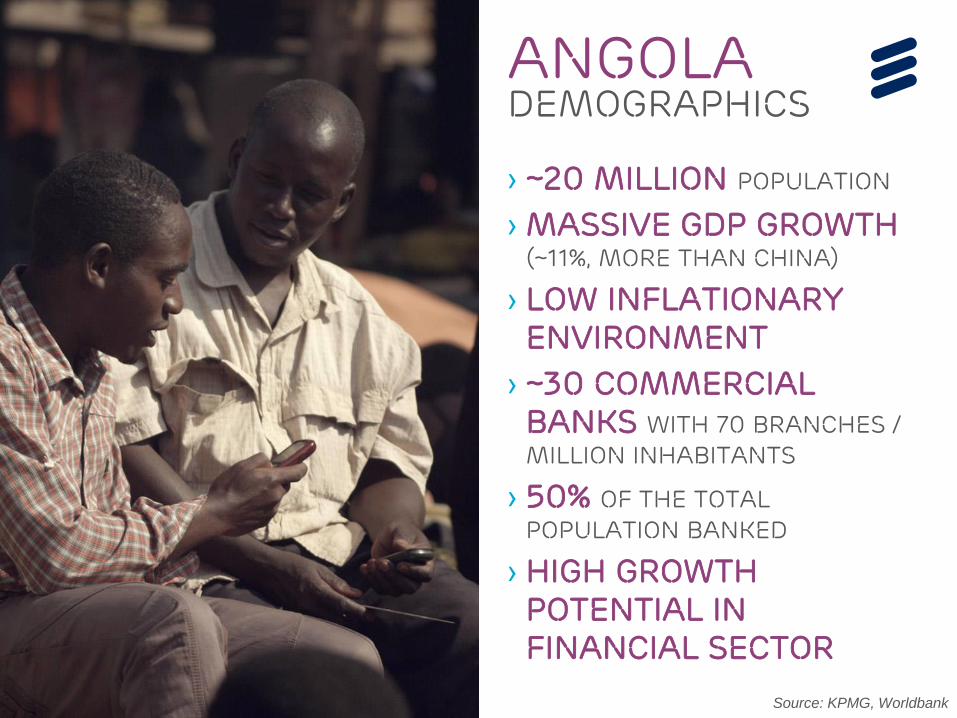

Angolademographics

› ~20 million population

› Massive GDP growth (~11%, more than China)

› Low Inflationary Environment

› ~30 Commercial Banks with 70 Branches /

Million inhabitants

› 50% of the total

population Banked

› High growth potential in Financial Sector

Source: KPMG, Worldbank

Mobile Payments and NFC | Ericsson Internal | 2014-03-25 | Page 7

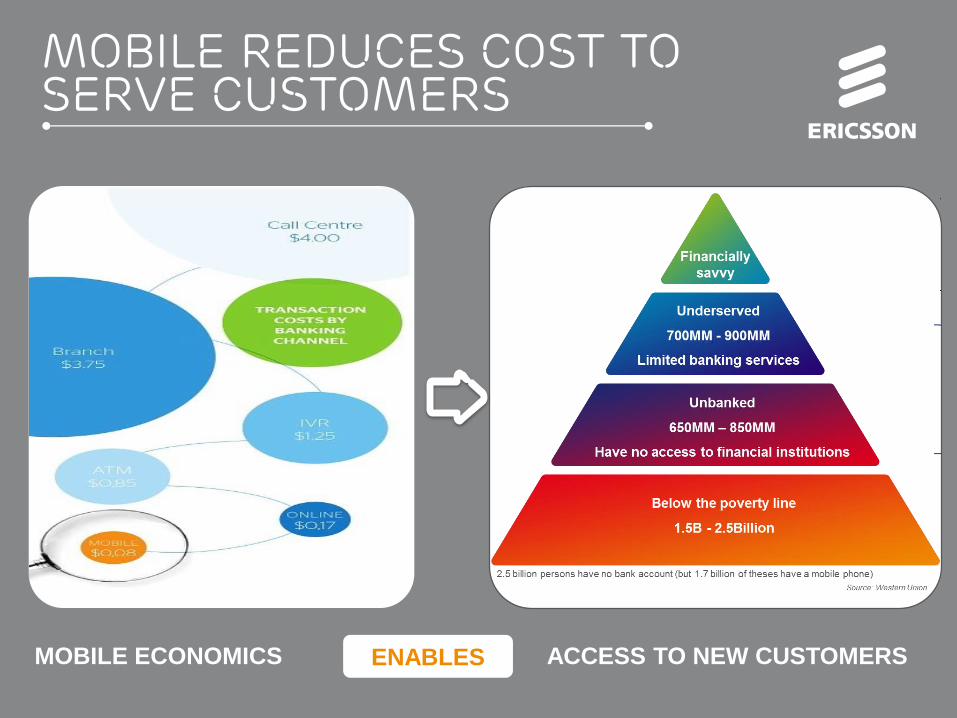

Mobile reduces cost to serve customers

MOBILE ECONOMICS ACCESS TO NEW CUSTOMERSENABLES

Mobile Payments and NFC | Ericsson Internal | 2014-03-25 | Page 8

Remittance opportunity

› Inflows coming into

Africa

› Pan-Africa estimated

to be large

› Price levels vary

$31B

Source: Boston Consulting Group

5-25%

Mobile Payments and NFC | Ericsson Internal | 2014-03-25 | Page 9

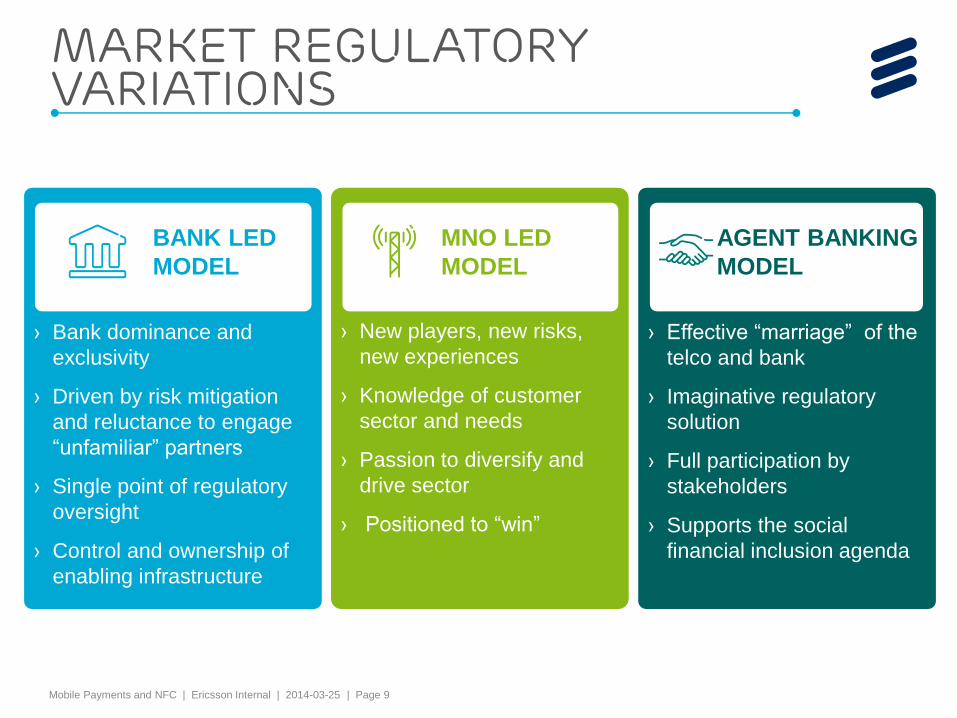

Market regulatory variations

WALLET

PLATFOR

M

› Bank dominance and

exclusivity

› Driven by risk mitigation

and reluctance to engage

“unfamiliar” partners

› Single point of regulatory

oversight

› Control and ownership of

enabling infrastructure

WALLET

PLATFOR

M

› Effective “marriage” of the

telco and bank

› Imaginative regulatory

solution

› Full participation by

stakeholders

› Supports the social

financial inclusion agenda

WALLET

PLATFOR

M

› New players, new risks,

new experiences

› Knowledge of customer

sector and needs

› Passion to diversify and

drive sector

› Positioned to “win”

BANK LED

MODEL

MNO LED

MODEL

AGENT BANKING

MODEL

Mobile Payments and NFC | Ericsson Internal | 2014-03-25 | Page 10

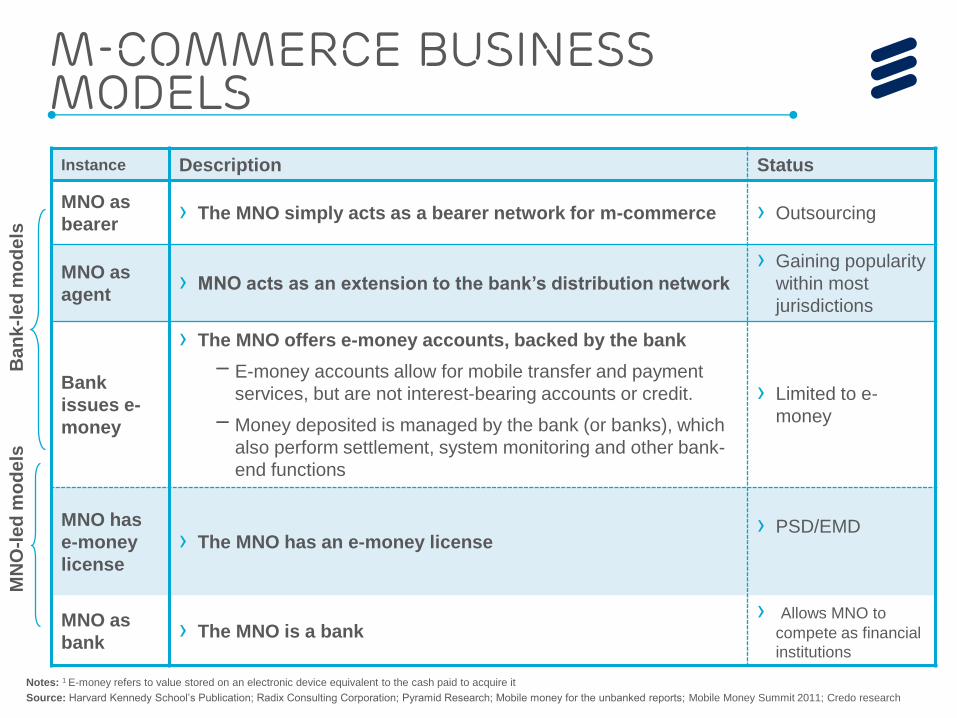

M-commerce business models

Instance Description Status

MNO as

bearer› The MNO simply acts as a bearer network for m-commerce › Outsourcing

MNO as

agent › MNO acts as an extension to the bank’s distribution network

› Gaining popularity

within most

jurisdictions

Bank

issues e-

money

› The MNO offers e-money accounts, backed by the bank

– E-money accounts allow for mobile transfer and payment

services, but are not interest-bearing accounts or credit.

– Money deposited is managed by the bank (or banks), which

also perform settlement, system monitoring and other bank-

end functions

› Limited to e-

money

MNO has

e-money

license

› The MNO has an e-money license› PSD/EMD

MNO as

bank› The MNO is a bank

› Allows MNO to

compete as financial

institutions

Notes: 1 E-money refers to value stored on an electronic device equivalent to the cash paid to acquire it

Source: Harvard Kennedy School’s Publication; Radix Consulting Corporation; Pyramid Research; Mobile money for the unbanked reports; Mobile Money Summit 2011; Credo research

Ba

nk-l

ed

mo

de

lsM

NO

-led

mo

de

ls

Mobile Payments and NFC | Ericsson Internal | 2014-03-25 | Page 11

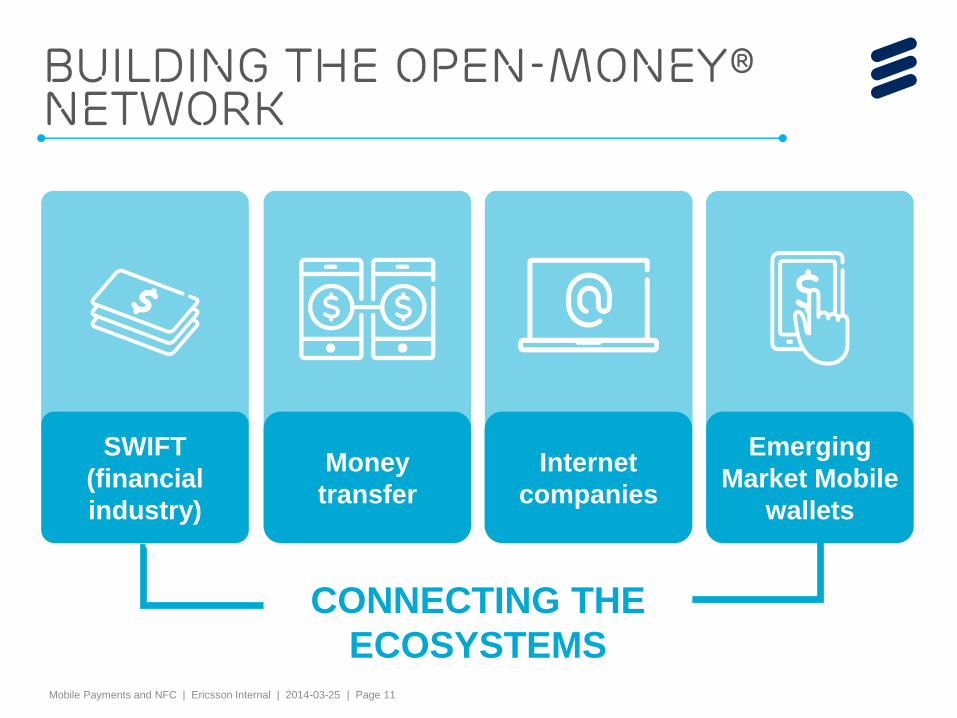

SWIFT

(financial

industry)

Money

transfer

Internet

companies

Emerging

Market Mobile

wallets

CONNECTING THE

ECOSYSTEMS

building the open-money®network

Mobile Payments and NFC | Ericsson Internal | 2014-03-25 | Page 12

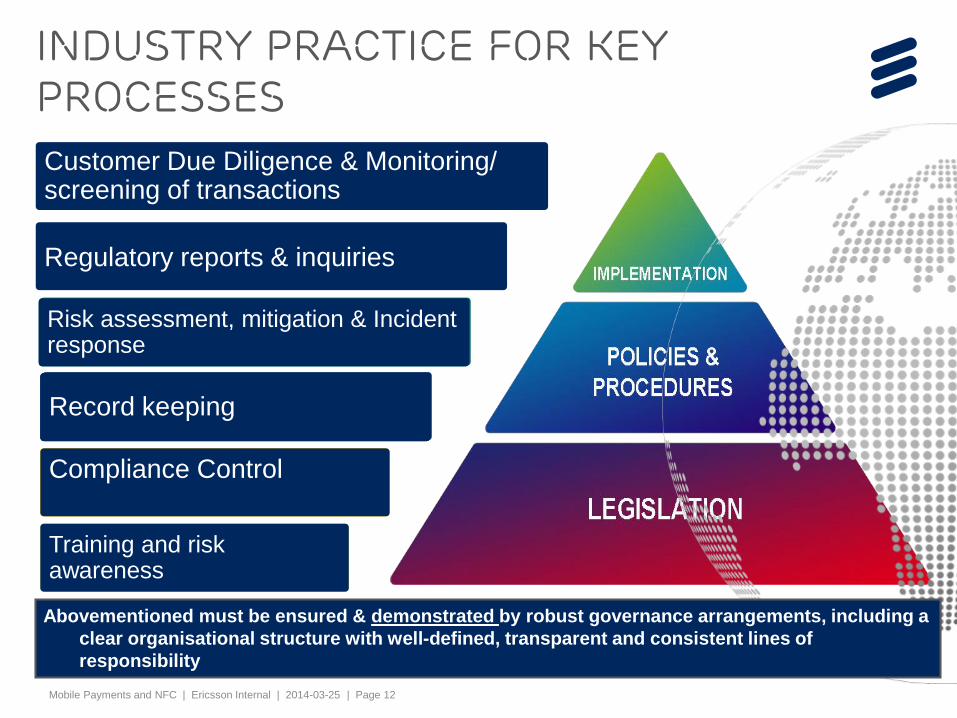

Industry practice for Key processes

Record keeping

Compliance Control

Training and risk awareness

Abovementioned must be ensured & demonstrated by robust governance arrangements, including a

clear organisational structure with well-defined, transparent and consistent lines of

responsibility

Risk assessment, mitigation & Incident response

Record keeping

Risk assessment, mitigation & Incident response

Compliance Control

Record keeping

Risk assessment, mitigation & Incident response

Training and risk awareness

Compliance Control

Record keeping

Risk assessment, mitigation & Incident response

Regulatory reports & inquiries

Customer Due Diligence & Monitoring/ screening of transactions

Mobile Payments and NFC | Ericsson Internal | 2014-03-25 | Page 13

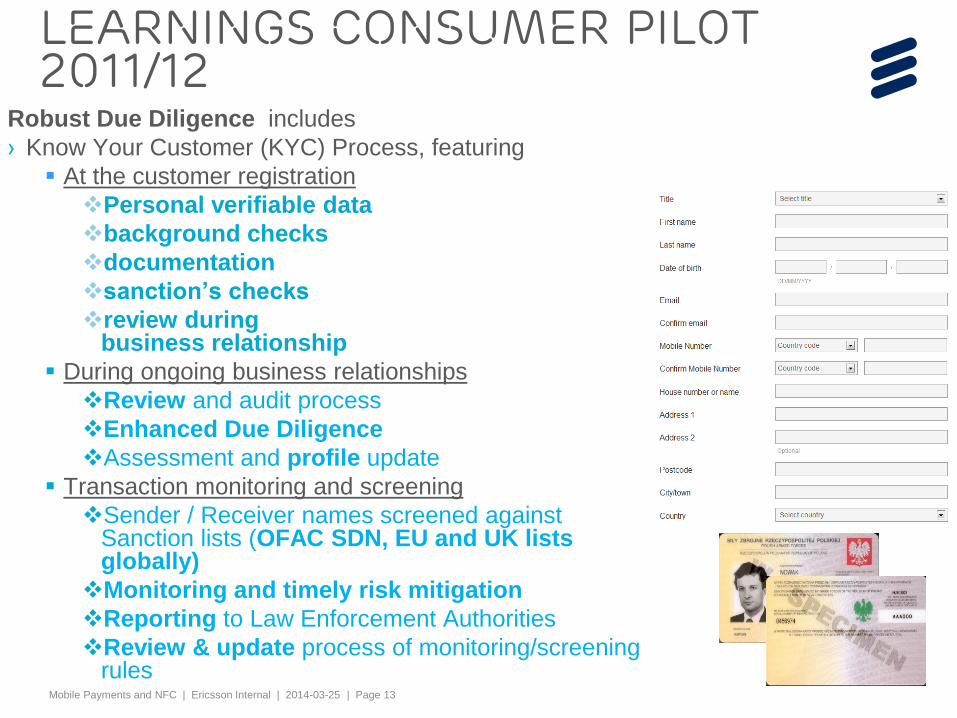

Learnings Consumer pilot 2011/12

Robust Due Diligence includes

› Know Your Customer (KYC) Process, featuring

At the customer registration

Personal verifiable data

background checks

documentation

sanction’s checks

review during business relationship

During ongoing business relationships

Review and audit process

Enhanced Due Diligence

Assessment and profile update

Transaction monitoring and screening

Sender / Receiver names screened against Sanction lists (OFAC SDN, EU and UK lists globally)

Monitoring and timely risk mitigation

Reporting to Law Enforcement Authorities

Review & update process of monitoring/screening rules

Slide subtitle

Business partner

Mobile Payments and NFC | Ericsson Internal | 2014-03-25 | Page 15

Our ecosystem partners

Ericsson Wallet Platform (and Converged Wallet) is fully

Western Union certified enabling users to send and receive

money across international borders directly from their

mobile phone

Partnership to launch m-wallet services in Africa and the

Middle East. MTN has more than 6 million Mobile Money

subscribers in 12 countries

A strategic partnership to enable a “one-stop-shop” for

Eurogiro members sending to mobile wallets via Ericsson

Interconnect Services

Partnership to receive money transfer via Ericsson

Interconnect Services

Project to launch m-wallet services in Senegal. Ongoing

discussions in other countries.

Mobile Wallet Solution Implementation for Telkomcel

Making open loop solutions possible and connectivity to

global payment network that support NFC enabled services

Mobile Payments and NFC | Ericsson Internal | 2014-03-25 | Page 16

Partnership with western union› Alliance to accelerate the interconnection

between the potential m-commerce

ecosystem and the existing financial world

› Certification of Ericsson platform for Western

Union (WU) Mobile Money Transfer Network

to support mobile operators in further

accelerating their launch of mobile money

› Current cooperation on sales: WU further

enhances the functionally of our platform.

Ericsson adds an important channel to

MNOs and the telecom-grade platform

› The medium-term ambition is to provide

turnkey solution to MNOs

Link to press release

Mobile Payments and NFC | Ericsson Internal | 2014-03-25 | Page 17

partnership with Eurogiro

› Established in 1989, Eurogiro is a

cooperation of postal organizations,

banks and financial service providers,

covering more than 500,000 branches

around the world

› The partnership will provide an

interconnecting path between banks and

other payment service providers, money

transfer organizations, mobile network

operators and mobile handsets

› It is a strategic partnership to enable a

one-stop-shop for Eurogiro members

sending to mobile wallets

Link to press release

Mobile Payments and NFC | Ericsson Internal | 2014-03-25 | Page 18

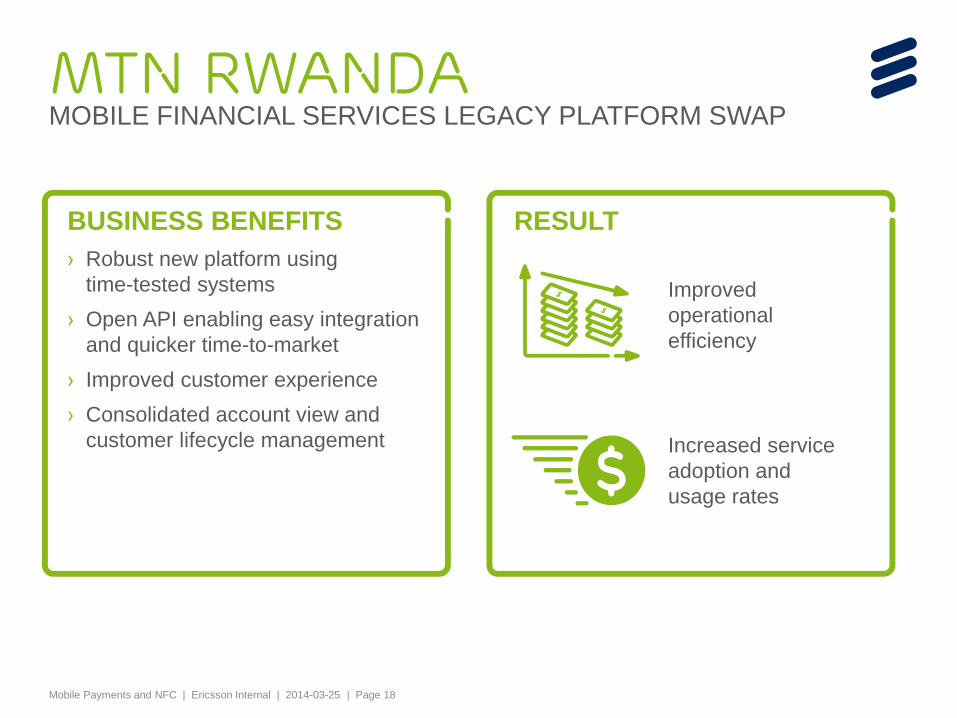

RESULTBUSINESS BENEFITS

› Robust new platform using

time-tested systems

› Open API enabling easy integration

and quicker time-to-market

› Improved customer experience

› Consolidated account view and

customer lifecycle management

MTN RwandaMOBILE FINANCIAL SERVICES LEGACY PLATFORM SWAP

Improved

operational

efficiency

Increased service

adoption and

usage rates

Mobile Payments and NFC | Ericsson Internal | 2014-03-25 | Page 19

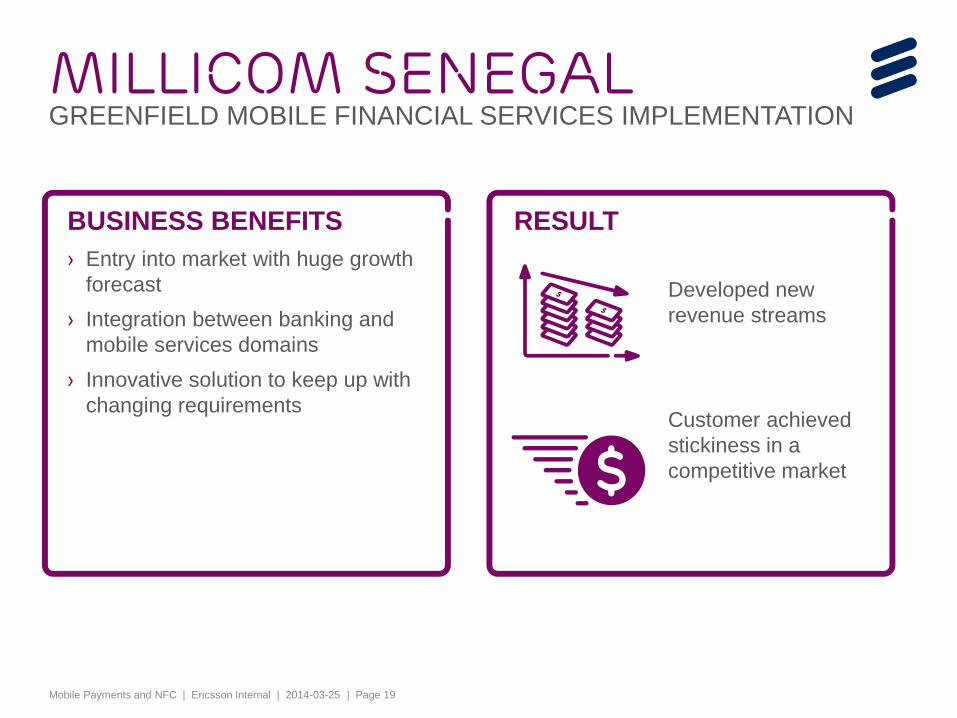

RESULTBUSINESS BENEFITS

› Entry into market with huge growth

forecast

› Integration between banking and

mobile services domains

› Innovative solution to keep up with

changing requirements

Millicom SenegalGREENFIELD MOBILE FINANCIAL SERVICES IMPLEMENTATION

Developed new

revenue streams

Customer achieved

stickiness in a

competitive market

Mobile Payments and NFC | Ericsson Internal | 2014-03-25 | Page 20

› The social promise of

Financial Inclusion is

attainable through effective

partnerships

› Fit-for-purpose regulations

needed to create the

enabling environment

required for imaginative

participation

› New players bring

innovation, direction and

drive

summary

Mobile Payments and NFC | Ericsson Internal | 2014-03-25 | Page 21

Let’s Create an Open Money SocietyBring finance and telecom together

to empower people and businesses

everywhere.