Embed Size (px)

Citation preview

“Too Good To Be True”

September 9, 2009

Jeffrey GundlachChief Investment Officer, The TCW Group

Portfolio Manager, TCW Total Return Bond Fund (TGLMX)

2

Too Good to be TrueJeffrey Gundlach

Table of Contents

I. Market Overview

II. Fixed Income Market Valuations

III. Housing Market Update

The information contained herein may include estimates, projections, and other “forward-looking” statements.Actual events may differ substantially from those presented herein. TCW assumes no duty to update any such statements.

Any opinions expressed are current only as of the time made and are subject to change without notice. The views expressed hereinare solely those of the author and do not represent the views of TCW as a firm or of any other portfolio manager or employee of TCW.

I. Market Overview

4

Too Good to be TrueJeffrey Gundlach

4

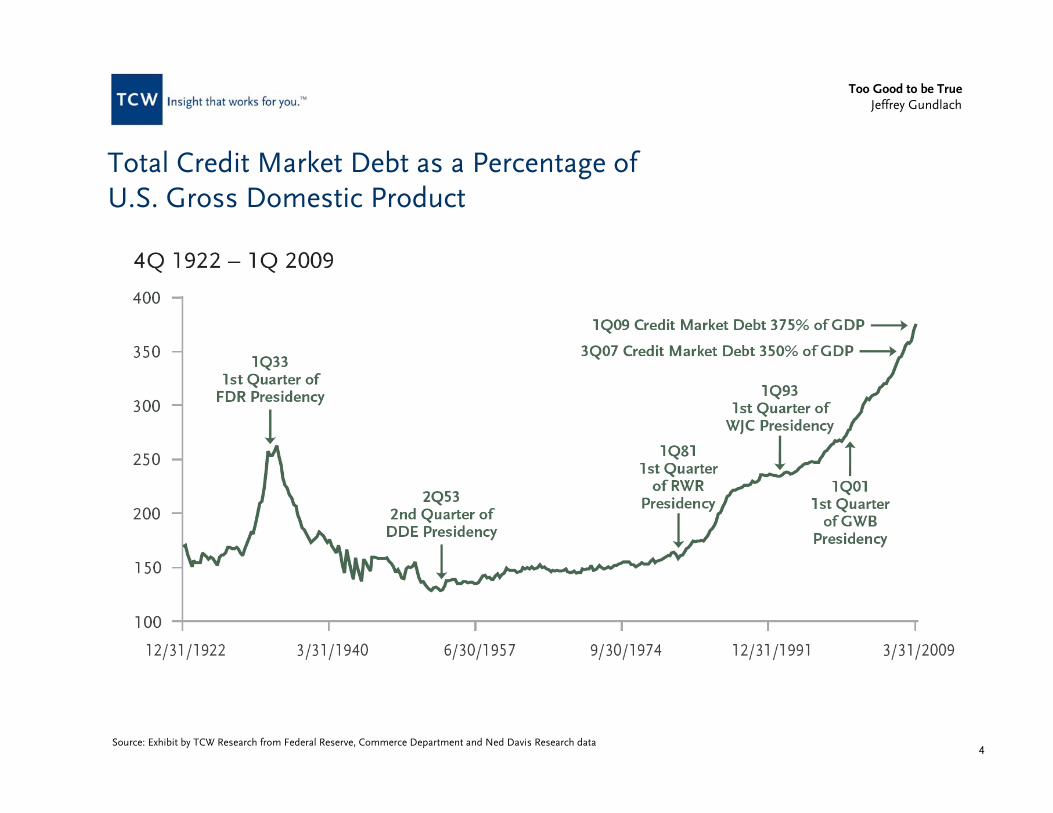

Total Credit Market Debt as a Percentage of U.S. Gross Domestic Product

Source: Exhibit by TCW Research from Federal Reserve, Commerce Department and Ned Davis Research data

Cash For Clunkers Program

Most Purchased – Toyota CorollaMost Traded-In “clunker” – Ford Explorer

6

Too Good to be TrueJeffrey Gundlach

6

U.S. Liability Map

The Federal Government Post CrisisHow exposed are public finances?

Certain Conditional Uncertain

ContractualObligation

Policy Commitment

PotentialPolicy

commitment

How

firm

is th

e co

mm

itmen

t?

FederalGovernment

Debt($9.0 trillion, FY10)

ContingentLiabilities

(guarantees)($5.0 trillion+) Public Sector

PensionLiabilities

($5.4 trillion, FY07)

Social Security and Medicare

($46 trillion, FY07)Value of expenses versus revenues

over the next 75 years under unchanged policiesState/Local

Government Debt($3 trillion+, FY10)

Net cost of Recapitalization(Depends on Asset Values-Initial Injection

of $700 billion+?)

U.S. GDP$14 trillion

Source: Moody’s, U.S. Treasury

7

Too Good to be TrueJeffrey Gundlach

7

U.S. Government Current Liabilities and Unfunded Promises-To-Pay($ Trillions)

$3.6 $3.9 $4.3 $4.6 $4.9 $5.1 $5.8 $8.5

$26.5

$43.3$46.4

$50.1$52.8

$56.5

$63.4

$30.1

$0

$10

$20

$30

$40

$50

$60

$70

$80

FY2002 FY2003 FY2004 FY2005 FY2006 FY2007 FY2008 FY2009E

Current Liabilities & Unfunded Promises of the U.S. Government

Publicly Held Debt

Source: TCW Research, U.S. Treasury

8

Too Good to be TrueJeffrey Gundlach

Nominal GDP

Source: Bloomberg Financial Services

9

Too Good to be TrueJeffrey Gundlach

$0

$500

$1,000

$1,500

$2,000

$2,500

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

Healthcare Expenditures 1960 – 2007($ Billions)

Source: Federal Reserve

2007$2.24

Ten Years Ago – 1997$1.12

Twenty Years Ago – 1987$513

10

Too Good to be TrueJeffrey Gundlach

Healthcare Expenditures Percentage of GDP

Source: Federal Reserve

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

200716.2%

11

Too Good to be TrueJeffrey Gundlach

S&P 500 – Last Seven Years

Source: Bloomberg Financial Services

12

Too Good to be TrueJeffrey Gundlach

S&P 500 vs. TGLMX – Last 10 Years

Source: Bloomberg Financial Services

13

Too Good to be TrueJeffrey Gundlach

S&P 500 – Year-End 2007 through September 8, 2009

Source: Bloomberg Financial Services

14

Too Good to be TrueJeffrey Gundlach

U.S. Dollar Index Futures – Last Seven Years

Source: Bloomberg Financial Services

15

Too Good to be TrueJeffrey Gundlach

U.S. Dollar Index Futures – Year End 2007 through September 8, 2009

Source: Bloomberg Financial Services

16

Too Good to be TrueJeffrey Gundlach

Gold – Year End 2007 through September 8, 2009

Source: Bloomberg Financial Services, CMX-Commodity Exchange, Inc.

17

Too Good to be TrueJeffrey Gundlach

Commodity Prices – Last Seven Years

Source: Bloomberg Financial Services, Commodities Research Bureau

18

Too Good to be TrueJeffrey Gundlach

Commodity Prices – Year-End 2007 through September 4, 2009

Source: Bloomberg Financial Services, Commodities Research Bureau

II. Fixed Income Market Valuations

20

Too Good to be TrueJeffrey Gundlach

10-Year U.S. Treasury vs. Fed Funds

Source: Bloomberg Financial Services. Data ending September 4, 2009.

!8.00%

!6.00%

!4.00%

!2.00%

0.00%

2.00%

4.00%

6.00%

1/31/1971

1/31/1973

1/31/1975

1/31/1977

1/31/1979

1/31/1981

1/31/1983

1/31/1985

1/31/1987

1/31/1989

1/31/1991

1/31/1993

1/31/1995

1/31/1997

1/31/1999

1/31/2001

1/31/2003

1/31/2005

1/31/2007

1/31/2009

21

Too Good to be TrueJeffrey Gundlach

Merrill Corporate IndexYield Spread to the Merrill Treasury IndexDecember 1985 to September 4, 2009

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

Dec-85Dec-86

Dec-87Dec-88

Dec-89Dec-90

Dec-91Dec-92

Dec-93Dec-94

Dec-95Dec-96

Dec-97Dec-98

Dec-99Dec-00

Dec-01Dec-02

Dec-03Dec-04

Dec-05Dec-06

Dec-07Dec-08

Yield Spread Average Yield Spread

Source: Merrill Lynch Indices, Bloomberg

22

Too Good to be TrueJeffrey Gundlach

Merrill ABS Floating IndexYield Spread to 1 Month LIBORSeptember 1994 to September 4, 2009

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

Oct-94Oct-95

Oct-96Oct-97

Oct-98Oct-99

Oct-00Oct-01

Oct-02Oct-03

Oct-04Oct-05

Oct-06Oct-07

Oct-08

Yield Spread Average Yield Spread

Source: Merrill Lynch Indices, Bloomberg

23

Too Good to be TrueJeffrey Gundlach

Merrill CMBS Fixed Rate IndexYield Spread to the Merrill Treasury IndexDecember 1997 to September 4, 2009

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

Dec-97Dec-98

Dec-99Dec-00

Dec-01Dec-02

Dec-03Dec-04

Dec-05Dec-06

Dec-07Dec-08

Yield Spread Average Yield Spread

Source: Merrill Lynch Indices, Bloomberg

24

Too Good to be TrueJeffrey Gundlach

Merrill High Yield IndexYield Spread to the Merrill Treasury IndexDecember 1985 to September 4, 2009

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

Dec-85Jun-87

Dec-88Jun-90

Dec-91Jun-93

Dec-94Jun-96

Dec-97Jun-99

Dec-00Jun-02

Dec-03Jun-05

Dec-06Jun-08

Yield Spread Average Yield Spread

Source: Merrill Lynch Indices, Bloomberg

25

Too Good to be TrueJeffrey Gundlach

Merrill Mortgage IndexYield Spread to the Merrill Treasury IndexDecember 1985 to September 4, 2009

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

Dec-85Jun-87

Dec-88Jun-90

Dec-91Jun-93

Dec-94Jun-96

Dec-97Jun-99

Dec-00Jun-02

Dec-03Jun-05

Dec-06Jun-08

Yield Spread Average Yield Spread

Source: Merrill Lynch Indices, Bloomberg

III. Housing Market Update

27

Too Good to be TrueJeffrey Gundlach

27

S&P/Case Shiller 20-City Monthly CompositeJanuary 2000 – June 2009

Source: Prepared by TCW from data from Standard & Poor’s

75

100

125

150

175

200

225

Jan!00

Jul!00

Jan!01

Jul!01

Jan!02

Jul!02

Jan!03

Jul!03

Jan!04

Jul!04

Jan!05

Jul!05

Jan!06

Jul!06

Jan!07

Jul!07

Jan!08

Jul!08

Jan!09

!25

!20

!15

!10

!5

0

5

10

15

20

S&P/Case!Shiller"20!City"Index YoY"% "Chg

July 2006207

June 2009141

Decline of 31% from peak through February 2009

Aug 200417.1% YoY

June 2009-15.4% YoY

28

Too Good to be TrueJeffrey Gundlach

28Source: Prepared by TCW from data from Standard & Poor’s and Mortgage Bankers Association

S&P/Case Shiller National Quarterly House Price Index vs. MBA Survey Subprime Delinquencies as % of Subprime Mortgage Loans

60

80

100

120

140

160

180

200

Mar-98

Sep-98

Mar-99

Sep-99

Mar-00

Sep-00

Mar-01

Sep-01

Mar-02

Sep-02

Mar-03

Sep-03

Mar-04

Sep-04

Mar-05

Sep-05

Mar-06

Sep-06

Mar-07

Sep-07

Mar-08

Sep-08

Mar-09

Hou

se P

rice

Inde

x

10

12

14

16

18

20

22

24

26

28

% S

ubpr

ime

Loan

Cou

nt

S&P/Case Shiller House Price Index Subprime Delinquencies % of Subprime Mortgages Outstanding

S&P/Case-Shille r HPIPeak @ 190 2Q06

Subprime Delqs25.4% 2Q09

RecessionMarch-Nov 2001

Subprime De lqs 10.3%2Q00, 4Q04, 2Q05

Subprime De lqs15.0% 2Q02

RecessionStarts

Dec 2007

Positive HPAduring 2001 recession

S&P/Case-Shille r HPI@ 133 2Q09

29

Too Good to be TrueJeffrey Gundlach

60

80

100

120

140

160

180

200

Mar-98

Sep-98

Mar-99

Sep-99

Mar-00

Sep-00

Mar-01

Sep-01

Mar-02

Sep-02

Mar-03

Sep-03

Mar-04

Sep-04

Mar-05

Sep-05

Mar-06

Sep-06

Mar-07

Sep-07

Mar-08

Sep-08

Mar-09

Hou

se P

rice

Inde

x

1

2

3

4

5

6

7

% P

rime

Loan

Cou

nt

S&P/Case Shiller House Price Index Prime Delinquencies % of Prime Mortgages Outstanding

Prime Delqs6.4% 2Q09

RecessionMarch-Nov 2001

Prime Delqs2.9% 2Q01

RecessionStarts

Dec 2007

Positive HPAduring 2001 recession

S&P/Case-Shiller HPIPeak @ 190 2Q06

S&P/Case-Shiller HPI@ 133 2Q09

29Source: Prepared by TCW from data from Standard & Poor’s and Mortgage Bankers Association

S&P/Case Shiller National Quarterly House Price Index vs. MBA Survey Prime Delinquencies as % of Prime Mortgage Loans

30

Too Good to be TrueJeffrey Gundlach

Source: TCW Research and Deutsche Bank ABX 2006-2 AAA tranche data through September 4, 2009.1. The boxes in the chart represent typical stages of market cycles. However, this is not a prediction of when the stages will begin or end, or of valuation, or of when any TCW Strategy will invest or realize on investments.

The Four Stages Of Market Opportunity – Senior Tranche

$25.0

$35.0

$45.0

$55.0

$65.0

$75.0

$85.0

$95.0

1/2/2007

5/2/2007

9/2/2007

1/2/2008

5/2/2008

9/2/2008

1/2/2009

5/2/2009

9/2/2009

Price

Belief

Concern

Liquidation

Recovery

• Significant repricing of mortgage credit risk is currently underway- Creating credit pockets of inefficiency, and - Discounting of select credit

• Some mortgage and mortgage-related assets have become “very cheap” as a result1

31

Too Good to be TrueJeffrey Gundlach

ABX 2006-2 A-Tranche

$0.0

$10.0

$20.0

$30.0

$40.0

$50.0

$60.0

$70.0

$80.0

$90.0

$100.0

Jan-07Mar-07

May-07

Jul-07Sep-07

Nov-07Jan-08

Mar-08May-0

8Jul-08

Sep-08Nov-08

Jan-09Mar-09

May-09

Jul-09Sep-09

Pri

ce

Source: TCW Research and JP Morgan ABX 2006-2 A tranche data through September 4, 2009.

32

Too Good to be TrueJeffrey Gundlach

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

1/1/20

00

6/1/20

00

11/1/200

0

4/1/20

01

9/1/20

01

2/1/20

02

7/1/20

02

12/1/200

2

5/1/20

03

10/1/200

3

3/1/20

04

8/1/20

04

1/1/20

05

6/1/20

05

11/1/200

5

4/1/20

06

9/1/20

06

2/1/20

07

7/1/20

07

12/1/200

7

5/1/20

08

10/1/200

8

3/1/20

09

8/1/20

09

32

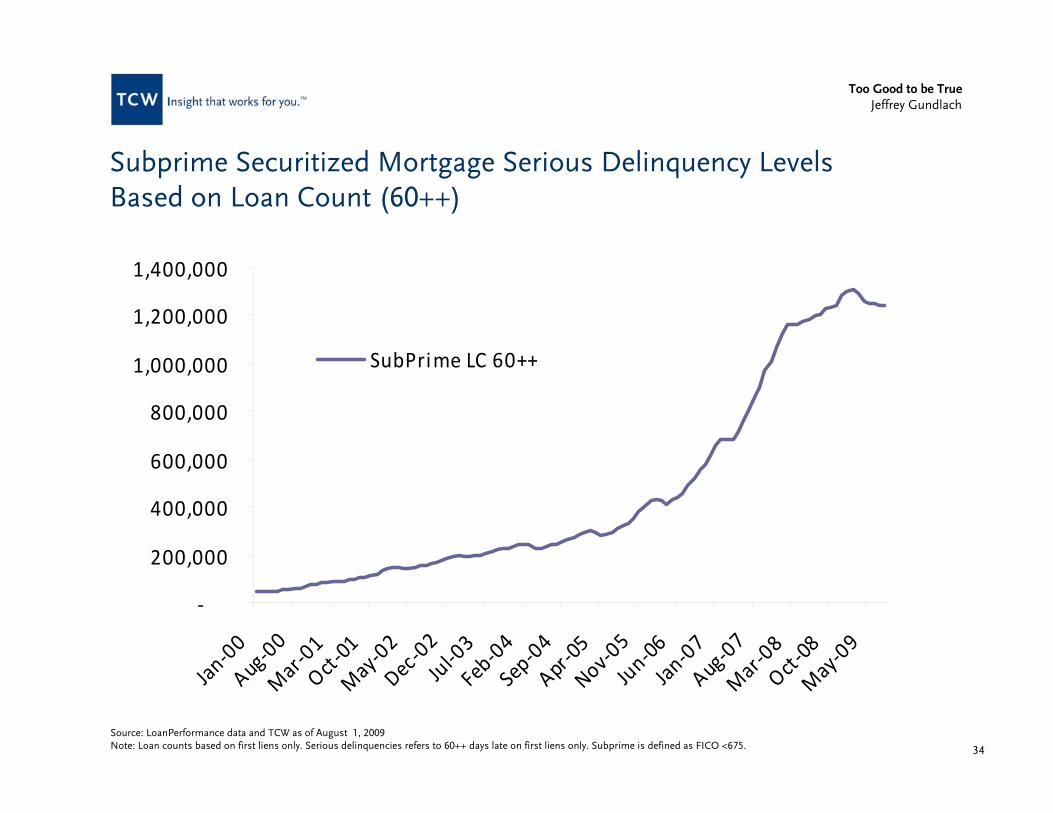

Subprime Securitized Mortgage Serious Delinquency Levels (60++)

Constant Default Rate (CDR)60++

15.1%

44.3%

Source: LoanPerformance data and TCW as of August 1, 2009 Note: Serious delinquencies refers to 60++ days late on first liens only. CDR on first liens only. Subprime is defined as FICO <675. Based as a percentage of unpaid principal balance.

33

Too Good to be TrueJeffrey Gundlach

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

1/1/

2000

7/1/

2000

1/1/

2001

7/1/

2001

1/1/

2002

7/1/

2002

1/1/

2003

7/1/

2003

1/1/

2004

7/1/

2004

1/1/

2005

7/1/

2005

1/1/

2006

7/1/

2006

1/1/

2007

7/1/

2007

1/1/

2008

7/1/

2008

1/1/

2009

7/1/

2009

33

Subprime Securitized Mortgages Serious Delinquency Levels (Foreclosures + REO + Bankruptcy)

Foreclosure + REO + Bankruptcy

15.1%

24.9%Constant Default Rate (CDR)

Source: LoanPerformance data and TCW as of August 1, 2009 Note: Foreclosure+REO+Bankruptcy, CDR on first liens only. Subprime is defined as FICO <675. Based as a percentage of unpaid principal balance.

34

Too Good to be TrueJeffrey Gundlach

34

Subprime Securitized Mortgage Serious Delinquency LevelsBased on Loan Count (60++)

!

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

Jan!00

Aug!00

Mar!01

Oct!01

May!02

Dec!02

Jul!03

Feb!04

Sep!04

Apr!05

Nov!05

Jun!06

Jan!07

Aug!07

Mar!08

Oct!08

May!09

SubPrime"LC"60++

Source: LoanPerformance data and TCW as of August 1, 2009 Note: Loan counts based on first liens only. Serious delinquencies refers to 60++ days late on first liens only. Subprime is defined as FICO <675.

35

Too Good to be TrueJeffrey Gundlach

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

1/1/

2000

7/1/

2000

1/1/

2001

7/1/

2001

1/1/

2002

7/1/

2002

1/1/

2003

7/1/

2003

1/1/

2004

7/1/

2004

1/1/

2005

7/1/

2005

1/1/

2006

7/1/

2006

1/1/

2007

7/1/

2007

1/1/

2008

7/1/

2008

1/1/

2009

7/1/

2009

35

Alt-A Securitized Mortgage Serious Delinquency Levels (60++)

Constant Default Rate (CDR)60++

10.6%

24.4%

Source: LoanPerformance data and TCW as of August 1, 2009 Note: Serious delinquencies refers to 60++ days late on first liens only. CDR based on first liens only. Alt-A is defined as FICO 675-725, LTV >=75. Based as a percentage of unpaid principal balance.

36

Too Good to be TrueJeffrey Gundlach

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

1/1/20

00

7/1/20

00

1/1/20

01

7/1/20

01

1/1/20

02

7/1/20

02

1/1/20

03

7/1/20

03

1/1/20

04

7/1/20

04

1/1/20

05

7/1/20

05

1/1/20

06

7/1/20

06

1/1/20

07

7/1/20

07

1/1/20

08

7/1/20

08

1/1/20

09

7/1/20

09

36

Alt-A Securitized Mortgages Serious Delinquency Levels (Foreclosures + REO + Bankruptcy)

Constant Default Rate (CDR)Foreclosure + REO + Bankruptcy

10.6%

15.4%

Source: LoanPerformance data and TCW as of August 1, 2009 Note: Foreclosure + REO + Bankruptcy, CDR based on first liens only. Alt-A is defined as FICO 675-725, LTV >=75. Based as a percentage of unpaid principal balance.

37

Too Good to be TrueJeffrey Gundlach

37

Alt-A Securitized Mortgage Serious Delinquency LevelsBased on Loan Count(60++) vs. Constant Default Rate (CDR)

!

100,000

200,000

300,000

400,000

500,000

600,000

700,000

Jan!00

Aug

!00

Mar!01

Oct!01

May!02

Dec!02

Jul!0

3

Feb!04

Sep!04

Apr!05

Nov

!05

Jun!06

Jan!07

Aug

!07

Mar!08

Oct!08

May!09

Al t!A"LC"60++

Source: LoanPerformance data and TCW as of August 1, 2009 Note: Loan counts based on first liens only. Serious delinquencies refers to 60++ days late on first liens only. Alt-A is defined as FICO 675-725, LTV >=75.

38

Too Good to be TrueJeffrey Gundlach

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

1/1/

2000

7/1/

2000

1/1/

2001

7/1/

2001

1/1/

2002

7/1/

2002

1/1/

2003

7/1/

2003

1/1/

2004

7/1/

2004

1/1/

2005

7/1/

2005

1/1/

2006

7/1/

2006

1/1/

2007

7/1/

2007

1/1/

2008

7/1/

2008

1/1/

2009

7/1/

2009

38

Prime Securitized Mortgage Serious Delinquency Levels (60++)

Constant Default Rate (CDR)60++

2.1%

6.2%

Source: LoanPerformance data and TCW as of August 1, 2009 Note: Serious delinquencies refers to 60++ days late on first liens only. CDR based on first liens only. Prime is defined as FICO >725 and LTV <75.Based as a percentage of unpaid principal balance.

39

Too Good to be TrueJeffrey Gundlach

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

1/1/20

00

7/1/20

00

1/1/20

01

7/1/20

01

1/1/20

02

7/1/20

02

1/1/20

03

7/1/20

03

1/1/20

04

7/1/20

04

1/1/20

05

7/1/20

05

1/1/20

06

7/1/20

06

1/1/20

07

7/1/20

07

1/1/20

08

7/1/20

08

1/1/20

09

7/1/20

09

39

Prime Securitized Mortgages Serious Delinquency Levels (Foreclosures + REO + Bankruptcy)

Constant Default Rate (CDR)Foreclosure + REO + Bankruptcy

2.1%

3.7%

Source: LoanPerformance data and TCW as of August 1, 2009 Note: Foreclosure + REO + Bankruptcy, CDR based on first liens only. Prime is defined as FICO >725 and LTV <75.Based as a percentage of unpaid principal balance.

40

Too Good to be TrueJeffrey Gundlach

!

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Jan!00Jul!00

Jan!01Jul!01

Jan!02Jul!02

Jan!03Jul!03

Jan!04Jul!04

Jan!05Jul!05

Jan!06Jul!06

Jan!07Jul!07

Jan!08Jul!08

Jan!09Jul!09

Prime"LC"60++

40

Prime Securitized Mortgages Serious Delinquency Levels (60++) Based on Loan Count

Source: LoanPerformance data and TCW as of August 1, 2009 Note: Loan counts based on first liens only. Serious delinquencies refers to 60++ days late on first liens only. Prime is defined as FICO >725, LTV <75.

41

Too Good to be TrueJeffrey Gundlach

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

1/1/20

05

6/1/20

05

11/1/200

5

4/1/20

06

9/1/20

06

2/1/20

07

7/1/20

07

12/1/200

7

5/1/20

08

10/1/200

8

3/1/20

09

8/1/20

09

Source: Loan Performance data based on FICO and LTV. August servicing reported as of September 4, 2009. Prime: FICO > 725 and LTV <75Alt-A: FICO 675-725; and FICO > 725 and LTV >= 75Subprime: FICO < 675

Historical Voluntary Prepayment Rates (VPR) on First Liens Securitized Mortgages

7.59%

2.47%

21.7%

Alt-A

Prime

Subprime

42

Too Good to be TrueJeffrey Gundlach

0%

10%

20%

30%

40%

50%

60%

70%

80%

2005

!01

2005

!04

2005

!07

2005

!10

2006

!01

2006

!04

2006

!07

2006

!10

2007

!01

2007

!04

2007

!07

2007

!10

2008

!01

2008

!04

2008

!07

2008

!10

2009

!01

2009

!04

2009

!07

Prime Alt"A Sub"Prime

January 2005 – August 2009

Loss Severities on First Liens

56.4%

66.4%

41.9%

Source: Loan Performance data based on FICO and LTV. August servicing reported as of September 4, 2009. Prime: FICO > 725 and LTV <75Alt-A: FICO 675-725; and FICO > 725 and LTV >= 75Subprime: FICO < 675

43

Too Good to be TrueJeffrey Gundlach

Mortgage Refinancing Index

Source: Bloomberg Financial Services

44

Too Good to be TrueJeffrey Gundlach

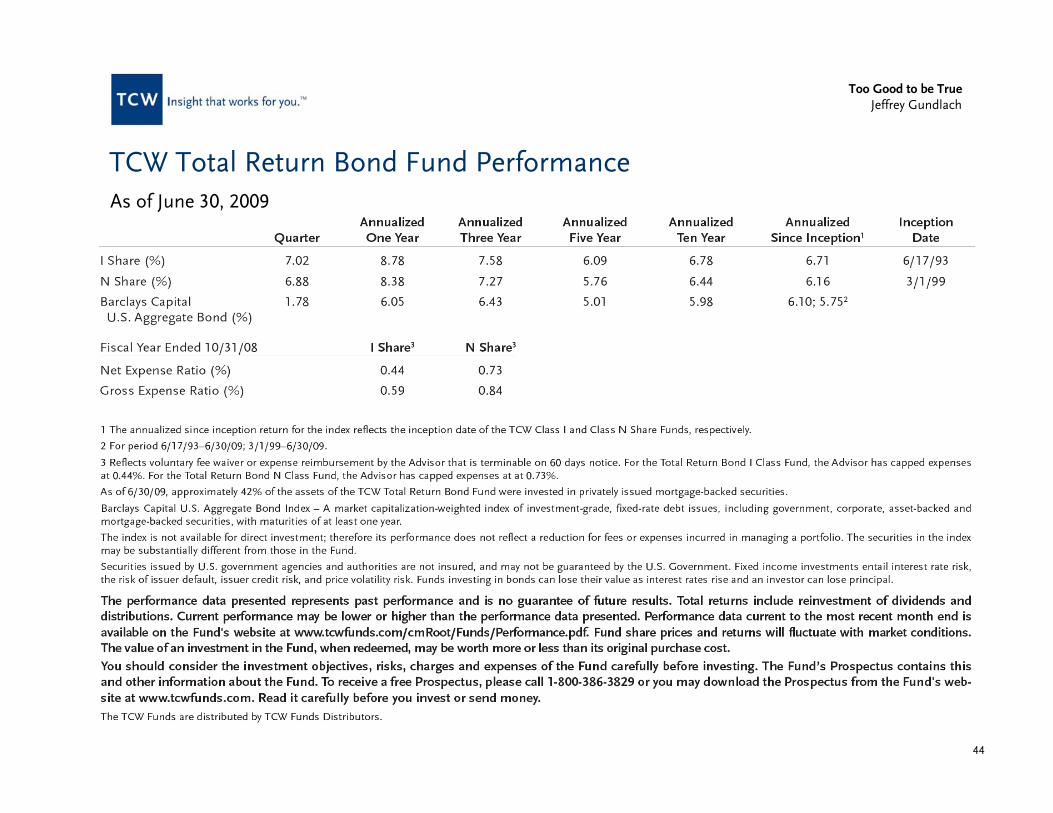

TCW Total Return Bond Fund PerformanceAs of June 30, 2009

45

Too Good to be TrueJeffrey Gundlach

A Word About Risk

• Interest rate risk refers to the possibility that the value of the Fund’s portfolio investments may fall since fixed income securities generally fall in value when interest rates rise.

– Extension risk is the possibility that rising interest rates may cause owners of the underlying mortgagesto pay off their mortgages at a slower than expected rate. This particular risk may effectively change a security whichwas considered short or intermediate term into a long-term security. Long-term securities generally drop in value more dramatically in response to rising interest rates than short or intermediate-term securities.

– Prepayment risk refers to the possibility that falling interest rates may cause owners of the underlying mortgages topay off their mortgages at a faster than expected rate. This tends to reduce returns since the funds prepaid will haveto be reinvested at the then lower prevailing rates.

• Liquidity risk refers to the possibility that the Fund may lose money or be prevented from earning capital gains if it cannotsell a security at the time and price that is most beneficial to the Fund.

• Market risk is the possibility that the returns from the types of securities that the Fund invests in will underperform returnsfrom the various general securities markets or different asset classes.

• Credit risk refers to the loss in the value of a security based on a default in the payment of principle and/or interest of the security, or the perception of the market of such default. The value of the Fund’s share price will fluctuate up or down basedon the value of the portfolio holdings, which can be affected by these risks.

The information contained herein may include estimates, projections, and other “forward-looking” statements. Actual events may differ substantially from those presented herein. TCW assumes no duty to update any such statements.

Any opinions expressed are current only as of the time made and are subject to change without notice. The views expressed herein are solely those of the author and do not represent the views of TCW as a firm or of any other portfolio manager or employee of TCW.

The primary risks affecting this Fund are “interest rate risk” (including “extension risk” and “prepayment risk”), “liquidity risk,” “market risk,” and “credit risk.”

46

Too Good to be TrueJeffrey Gundlach

Biography

Jeffrey GundlachChief Investment OfficerThe TCW Group, Inc.

Mr. Gundlach is the Chief Investment Officer and a member of the Board of Directors of the TCW Group, Inc. In addition, he oversees fixed income investments as Chairman of the TCW Multi-Strategy Fixed Income Committee and is the Co-Founder and lead portfolio manager of the Mortgage-Backed Securities group. His investment strategies have been featured in leading publications including the New York Times, the Wall Street Journal, Barrons, Forbes and Institutional Investor. In 2007, Morningstar named Mr. Gundlach Fixed Income Fund Managerof the Year and Standard & Poor’s/BusinessWeek gave its Excellence in Fund Management Awardto TGLMX, the only bond fund to win the prestigious award five years in a row. Mr. Gundlach joined the firm in 1985, prior to which he was associated with Transamerica Corporation's Los Angeles based Property/Casualty Insurance division. He worked in the Finance Department as Senior Loss Reserve, Analyst, responsible for investment discount and funding strategies. He is a graduate of Dartmouth College summa cum laude holding a BA in Mathematics and Philosophy. He attended Yale University as a PhD candidate in Mathematics.

47

Too Good to be TrueJeffrey Gundlach

Questions and Answers

Conference Call Attendees:

• If you have a question, please press star then 1 (*1) on your touch tone phone.

• If you wish to be removed from the queue, please press star then 2 (*2).

• If you are using a speakerphone, you may need to pick up the handset firstbefore pressing the numbers.

Webcast Attendees:

• For those of you wishing to submit a question via the Webcast, please enteryour question in the Question and Answer block to the left of this screen andpress submit.

![Gundlach Presentation: Penny For Your Thoughts [SLIDES]](https://img.pdfslide.us/doc/110x75/55cf96ee550346d0338eb3ce/gundlach-presentation-penny-for-your-thoughts-slides.jpg)