Embed Size (px)

DESCRIPTION

misrepresentation, non disclosure abd breach of warranty by the insured

Citation preview

DAMODARAM SANJIVAYYA NATIONAL LAW UNIVERSITY

VISAKHAPATNAM, A.P, INDIA

MISREPRESENTATION, NON DISCLOSURE AND BREACH OF WARRANTY

BY THE INSURED.

LAW OF INSURANCE

Mrs. BHAGYA LAXMI

SUBMITTED BY

MAURYA KALLEPALLI

(201120)

EIGHTH SEM.

1

ACKNOWLEDGEMENT

I would like to express my gratitude towards our law of Insurance Professor Mrs. Bhagyalaxmi

Mam for giving me the opportunity to work on this topic and guiding towards completing the

project in an appropriate manner. I would like to thank everyone who has supported me and

guided me towards completing this project.

Maurya Kallepalli

(201120)

2

TABLE OF CONTENTS

S.No Title Page No.

1 TABLE OF CASES 4

2 TABLE OF STATUTES 4

3 INTRODUCTION 5

4 RESEARCH

METHODOLOGY

6

5 MISREPRESENTATION 7

6 DISCLOSURE 9

7 WARRANTY 15

8 CONCLUSION 21

9 BIBLIOGRAPHY 22

3

TABLE OF CASES

St. Paul Fire and Marine Insurance Co. (UK) Ltd. v. Mc Connell Dowell Constructors Ltd

Elton v. Larkins

Economides v. Commercial Union Assurance Co. plc

LIC v. Shakunthalabai

Bhagwani Bai v. LIC of India

Life Insurance Corporation of India v. Shakuntala

Bhagwati Bai v. LIC

Bank of Nova Scotia v. Hellenic War Risks Assn. (Bermuda) Ltd., The Good Luck

Banque Finaciere de la Cite v. Westgate Insurance Co. Ltd

Brownlie v. Campbell

Rozanes v. Bowen

United India Insurance Co. Ltd. v. MKJ Corpn

Joel v. Law Union

TABLE OF STATUTES

Insurance Act, 1938

Motor Vehicle Act, 1988

Marine Insurance Act, 1963

4

AIMS AND OBJECTIVES OF THE STUDY:

Through this paper the researcher aims at understanding the concept of misrepresentation, non

disclosure and breach of warranty by the insured as it appears in a new chapter inserted into both

Insurance act, 1938 and as well as marine insurance from which the researcher has tried to

understand as to what is meant by misrepresentation and non disclosure, who will be liable upon

such misrepresentation and related questions and issues.

Also the objective of this paper is to see why proper and good faith in required in the terms of

insurance.

RESEARCH QUESTIONS:

What is a misrepresentation and whether the insured’s interest are effected through the

misrepresentation?

What is meant by non disclosure and who will be principally liable upon such act?

When the breach of warranty in a insurance arises?

INTRODUCTION

In insurance contract, all the information shall be disclosed by the parties. If a party fails to

adhere to the principle of utmost good faith then the outcome of claim may be affected. The

parties must disclose all relevant information. A false or misleading statement that, if intentional

and material, can allow the insurer to void the insurance contract. Some insurance policies and

state laws that govern insurance contract provisions vary on the exact details of the conditions

under which coverage may be voided; these variations are usually denoted in state amendatory

endorsements.

Insurers need information from consumers to decide whether to offer (and renew) insurance, and

to decide the price or other terms of the insurance to be offered to the consumer. The law

imposes a duty of disclosure on policyholders when they seek to take out new insurance cover or

to renew existing insurance cover.

5

Insurers may be able to refuse to pay a claim or part of a claim under an insurance policy if the

policyholder has not complied with their duty of disclosure. However, an insurer must first

establish that:

the insurer clearly informed the policyholder in writing about the duty of disclosure and the

consequences of non-disclosure;

the policyholder knew or should have known that the insurer required information about

certain matters;

the policyholder failed to provide information, or misrepresented the information; and

the insurer would not have offered insurance, or would have offered insurance on different

terms, had the policyholder properly disclosed the information.

SCOPE AND LIMITATIONS OF THE STUDY:

The scope of this research paper is to understand the concept of misrepresentation, non

disclosure and breach of warranty by the insured as it appears under the Insurance Act. The

researcher has limited himself to discussing the substantial law aspects of the paper which are

connected with law of insurance and has kept the discussion of the procedural aspects at a

minimum.

RESEARCH METHODOLOGY

METHOD OF WRITING:

The researcher has used both a descriptive and analytical method of writing in order to

understand the issues better. The researcher has also relied on case law, to get an in depth

understanding of the topic.

MODE OF CITATION:

A uniform mode of citation has been followed throughout this project.

SOURCES OF DATA :

6

The researcher has used secondary sources in order to obtain sufficient data for this project,

namely, books, articles and the internet.

Chapterization:

Chapter 1: this chapter deals with the misrepresentation, material facts and

misrepresentation of material facts.

Chapter 2: this chapter deals with the Disclosure, Facts which need to be disclosed, facts

which need not be disclosed and Facts which need not be disclosed.

Chapter 3: this chapter deals with the Warranty, Breach of warranty and Conclusion &

Suggestions.

CHAPTER 1:

Misrepresentation

Getting into a contract with a person or a company by making statements that are not in

accordance with the facts is known as misrepresentation.

Definition: Getting into a contract with a person or a company on false grounds by making

statements that are not in accordance with the facts is known as misrepresentation. In an

insurance policy, misrepresentation on the behalf of the insured gives the insurance company a

right to terminate the policy.

In case of health insurance if the applicant is aware of the inaccuracy of the clause(s) in an

insurance statement and he/she does not disclose it before signing the contract, then he/she can

be denied coverage for the same. An insurer can refuse a claim only if the misrepresentation is

unjustifiable or in other words the risk is substantial.

Material Fact

Another problem arises as to the definition of the term material fact. What may be material for

one may be immaterial for the other and vice-versa. But, generally speaking, a material fact is

one which affects the judgmental capacity of a person. It must be such that a different

7

consequence would have occurred had it not been disclosed. The following cases illustrate the

different theories evolved by the judiciary regards this.

In the case of St. Paul Fire and Marine Insurance Co. (UK) Ltd. v. Mc Connell Dowell

Constructors Ltd,1

Two major questions were decided in this case. The first was the test of materiality according to

which the fact in question must have been of interest to a prudent insurer. Secondly, as regards

the presumption of inducement, it was held that the test would be satisfied if the insurer could

show that he was influenced in whole or in part by the assureds misleading presentation of the

risk.

The Prudent insurer test has been adopted in S.149(6) of Indian MV Act,1988 and S. 149(5) of

English Road Traffic Act, 1972.

Misrepresentation of Material Facts

This is the offence most often thought of when the term fraud is used. Misrepresentation cases

can be prosecuted criminally or civilly under a variety of statutes or they might be the basis for

common law claims. The gist of the offence is the deliberate making of false statements to

induce the intended victim to part with money or property.

The specific elements of proof of misrepresentation vary whether the case is prosecuted as a

criminal or civil action. The elements normally include:

• Material false statement;

• Knowledge of its falsity;

• Reliance on the false statement by the victim;

• (A loss) Damages suffered;

• A deceit or fraud constituting a false statement made willfully or recklessly, which causes

loss to another.1 45 Con LR 89

8

Not only is a misrepresentation fraudulent if it was known or believed by the maker of the

representation to be false when made, but mere non-belief in the truth is also indicative of fraud.

Thus whenever a person makes a false statement which he does not actually and honestly believe

to be true, for purposes of civil liability, that statement is as fraudulent as if he had stated that

which he did not know to be true, or knew or believed to be false. The motive of the person

making the representation is irrelevant.

The maker of the representation will not, however, be fraudulent if he believed the statement to

be true as he perceived it, provided that perception was one that might reasonably be held,

though the court later holds that the representation objectively bears another meaning.

CHAPTER 2:

Disclosure

The assured must disclose to the insurer, before the contract is concluded, every material

circumstance which is known to be assured and the assured is deemed to know every material

circumstances which, in the ordinary course of business ought to be known to him.

Usually, the parties to the contract can examine the items or service, which is the subject matter

of the contract. Each party can verify the correctness of the statements of the other party. There

is no need to take the statements on trust.

Assignment of Interest-Section 17 of the Marine Insurance Act, 1963 provides: 'Where the

assured assigns or otherwise pans with his interest in the subject-matter insured, he does not

thereby transfer to the assignee his rights under the contract of insurance, unless there be an

express or implied agreement with the assignee to that effect. But the provisions of this section

do not affect transmission of interest by operation of law." Disclosure and Representation I.

Disclosure Marine insurance is uberrimae files (utmost good faith) Section 19 of the Marine

Insurance Act, 1963 provides that: "A contract of marine insurance is a contract based upon the

utmost good faith, and if the utmost good faith be not observed by either party, the contract may

be avoided by the other party.' The doctrine of caveat emptor (let the buyer beware) applies to

commercial contracts, but insurance contracts are based upon the legal principle of uherrimae

fidel (utmost good faith) If this is not observed by either of the parties, the contract can be

avoided by the other party. In marine insurance the material facts are as to the subject matter,

the .ship and the perils to which the ship is exposed; knowing these facts the underwriter must

9

form his own judgment of the premium and other people's judgment is quite immuterial. Thus in

a marine proposal it is not material to disclose wnether any other office has refused the proposal.

The duty of the utmost faith applies to the insurer. He may not urge Ae proposer to affect an

insurance which he knows is not legal or has run off safety. But, the duty of disclosure of

material facts rests highly on the insured because he is aware of the material common in other

branches of insurance are not used in the marine insurance. Disclosure by assured Section 20 of

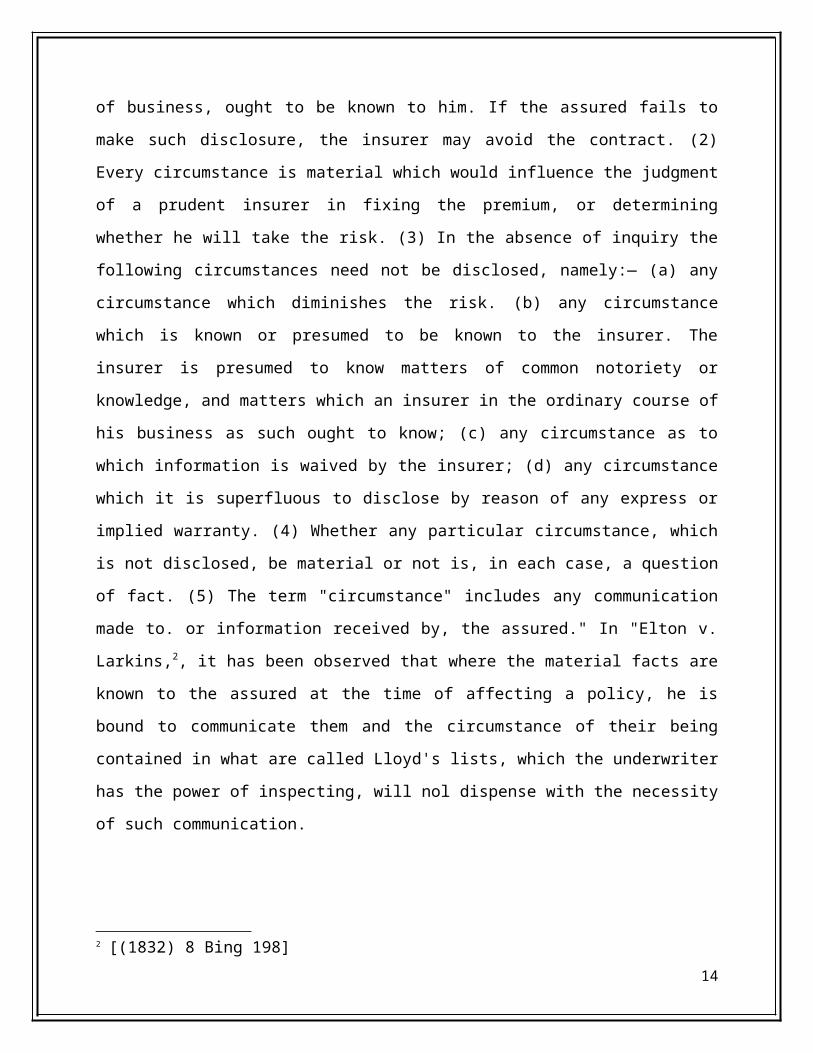

the Marine Insurance Act, 1963 provides that: "(1) Subject to the provisions of this section, the

assured must disclose to the insurer, before the contract is concluded, every material

circumstance which, is known to the assured, and the assured is deemed to know every

circumstance which, in the ordinary course of business, ought to be known to him. If the assured

fails to make such disclosure, the insurer may avoid the contract. (2) Every circumstance is

material which would influence the judgment of a prudent insurer in fixing the premium, or

determining whether he will take the risk. (3) In the absence of inquiry the following

circumstances need not be disclosed, namely:— (a) any circumstance which diminishes the risk.

(b) any circumstance which is known or presumed to be known to the insurer. The insurer is

presumed to know matters of common notoriety or knowledge, and matters which an insurer in

the ordinary course of his business as such ought to know; (c) any circumstance as to which

information is waived by the insurer; (d) any circumstance which it is superfluous to disclose by

reason of any express or implied warranty. (4) Whether any particular circumstance, which is not

disclosed, be material or not is, in each case, a question of fact. (5) The term "circumstance"

includes any communication made to. or information received by, the assured." In "Elton v.

Larkins,2, it has been observed that where the material facts are known to the assured at the time

of affecting a policy, he is bound to communicate them and the circumstance of their being

contained in what are called Lloyd's lists, which the underwriter has the power of inspecting, will

nol dispense with the necessity of such communication.

Facts which need to be disclosed and facts which need not be disclosed-

Facts required to be disclosed-

2 [(1832) 8 Bing 198]

10

1. A fact which is earlier immaterial but becomes material later on must be disclosed if it has

been expressly mentioned in the terms and conditions of the policy. Eg. Fire insurance of ones

house. Earlier, vacant plot located nearby. Later on a petrol pump is constructed on such plot.

2. A fact which increases the risk must be disclosed in all circumstances. E.g. incase of theft

insurance, if a person lives alone in an isolated place, the same needs to be compulsorily

disclosed as it increases the risk.

3. Previous losses incurred and claims under previous policies needs to be disclosed. This is

mainly in case of double insurance where it needs to be ascertained as to whether the subsequent

insurance company is willing to insure and to what extent.

4. Special terms and conditions under previous policies if any.

5. Fact of existence of non-indemnity is to be disclosed. This relates to any charge or

encumberance on the policy in the form of a loan security or otherwise.

6. The description of the subject matter must be stated properly. This is mainly to locate the

property if it is immovable and to recognize it if it is movable.

7. Facts which suggest any special motive to take the insurance.

8. Facts which suggest the existence of any moral hazards which relate to the moral integrity of

the proposer, etc.

CASE:

In Economides v. Commercial Union Assurance Co. plc,3

It was held that the duty of the assured to disclose all material facts required an assured only to

disclose facts known to him. There is no obligation on the assured to make enquiries as to the

factual basis of his belief.

Facts which need not be disclosed-

1. Fact lessening the risk need not be disclosed.

2. Public knowledge. E.g. facts regarding govt. policies, taxes, subsidies, etc. which are expected

to be known to all.

3 (1997) 3 All ER 636

11

3. Fact of law like rules, regulations, etc. which have already been made available to all by way

of the notification in the official gazette.

4. Superfluous facts or such information which is not logical.

5. Facts which are inferred information.

6. Fact waived by the insurer himself.

7. Facts governed by the policy itself.

In LIC v. Shakunthalabai,4 In this case, the insured had failed to disclose that he suffered from

indigestion for a few days and took chooram from an ayurvedic doctor. He died within that year

due to jaundice. The insurer repudiated the claim on this account. The court did not approve of

the repudiation as the insurer did not establish by clear and cogent evidence that the question was

properly explained to the insured and that he was told that illness included such casual

disturbances to health and medicines included tablets that could be purchased at the nearest

coffee store.

In Bhagwani Bai v. LIC of India,5

The insurer cannot avoid or repudiate an insurance policy on the ground of non-disclosure of

lapsed policies by the assured which had no bearing on the risk taken by the insurer.

Does Silence Amounts To Non-Disclosure?

A policy of life insurance of a person who at the time of insurance is in good state of health, is

not vitiated by the non-disclosure by such person of the fact that few years back he had some

disease or he had been suffering from headaches or body aches all such things are presumed to

be known to the company. What an insured undergoes in his normal course of life needn’t be

told to the company.6

How Is Section 45, Being Misused By The Insurer?

4 AIR 1975 AP 68

5 AIR 1984 MP 126(130)6 BrijAnand Singh, ‘New Insurance Law’, University Book agency, 4th ed., 2000, Allahabad.

12

The section was enacted to prevent immense loss and hardships caused to the insured and his

legal representatives because the insurers avoided contract of life insurance policy due to

incorrect statements whether material or not made by the insured even after the policy had been

in force for several years and all the premium paid by the insured was forfeited by the insurer.

Thus the provision in effect mitigated the rule of uberrima fides, i.e., utmost good faith.

Obligation to deal fairly and honestly with each other is upon both the parties equally.

In the past, problems have arisen with misrepresentation or non-disclosure by the insured. In this

context, the issue is when would failure to make such a disclosure render the contract void or

voidable. There have been several judgments of the Hon’ble Supreme Court in this regard which

have underscored the importance of the burden of proof shifting to the insurer after the expiry of

two years from effective date of the policy, if the insurer seeks to repudiate the claim on the basis

of fraud or suppression of facts which were material to be disclosed.7

Life Insurance Corporation of India v. Shakuntala.8

Facts Of The Case: Jamanadas died of jaundice on 4-11-1986 who had an insurance policy with

appellants, one and half years after he died. This policy was taken on the grounds of his personal

statement that he had not suffered from any illness and had not consulted any medical

practitioner within last five years, but had once suffered from indigestion for few days and had

taken “chooranam” from an ayurvedic practitioner.

Arguments Raised: Learned Counsel for respondents as usually relied on Section 45 of the

Insurance Act and stated that insurer had right to repudiate a policy on the grounds that statement

made in proposal for insurance or any documents which leads to policy was inaccurate or false.

Judgment: Court was of the view that, treating occasional headaches or a bout of indigestion as

a ‘material fact’ which an insured was under an obligation to disclose would be extremely

unreasonable. No reasonable man would deem it material to tell an insurance company of all the

casual headaches he had in his life, and if he knew that it was an ordinary casual headache, there

would be no breach of his duty towards the insurance company in not disclosing it.

7 ww.iirmworld.org.in/conference/red-hyd/sv%20krishna%20mohan.ppt visited on March 15, 2015.8 AIR 1975 A.P 68.

13

The confidential report made by the medical officer of the insurance Company shows that the

appellant was in ‘first class life’. And the jaundice of which he died had nothing to do with the

undisclosed indigestion from which he suffered 18 months earlier. And the only connection

between them would be the advantage life insurance was seeking. Therefore non-disclosure

would not amount to an untrue statement and Life Insurance Company was held not justified in

repudiating the policy. And therefore his wife was entitled to the insurance claim.

Comments: - This case puts forth the principle that the non-disclosure of ‘material facts’ only

provides power to repudiate the contract by the company, but other ordinary facts which are

unconnected to the main contract entered into by the insured cannot be ignored. Here for the

same reason Company was restrained from taking such step, on the bases of facts which were

irrelevant to be disclosed (i.e. indigestion) by the insured to effect of the contract.

Bhagwati Bai v. LIC .9

FACTS OF THE CASE: Plaintiff is (beneficiary of the policy) and her husband late Moolchand

insured himself with the defendant on 28-3-1972 for the sum of Rs. 25,000/- he also had filed a

proposal form and personal statement on the same date, and died within a month on 16-4-71.

Division manager refused the claim by the appellant on the fact that he had concealed the fact

that before filing for the present policy he had three policies in March 1965, which had lapsed in

March 1970.

Issues: Now it’s to be observed under two broad issues:-

· Whether the deceased deliberately concealed the fact of the existence of earlier three policies in

hand?

· Was the fact concealed material to the bearing of risk undertaken by the company i.e. if it still

would have insured the life of the insurer if the corporation was made aware of the fact of the

facts alleged to be concealed?

Arguments Raised: But plaintiff stated that the fact was told but the same was not recorded by

the agent, and contended that even if it was not disclosed it’s not material to the disentitle the

defendant. Plaintiff therefore claims interest amounting to 11,000/-, w.e.f. 16-4-1972 at the rate

of 12 % per annum. Corporation contended that if it would have known the fact of existence of 9 AIR 1984 M.P 126.

14

three policies with the insured it wouldn’t have issued the same to him, and therefore money paid

by him would stand forfeited. Being mis-represented by the deceased the contract would stand

void under section 45 of the Insurance Act.

Judgment: - Court applied Section 17 and 19 of the Contract Act and held that the Insurer

cannot repudiate the liability by showing only some inaccuracy or falsity of the statement, nor

can avoid the policy for a material misrepresentation if it has no bearing on the risk. Thus on

every misrepresentation or concealment of a fact a contract cannot be avoided merely on trivial

and inconsequential misstatement or non-disclosure That the non-disclosure about the lapsed

policies had no bearing on the risk and didn’t amount to fraudulent misrepresentation as no

undue advantage was derived by the concealment of facts and the corporation was made liable to

pay the insurance amount with interest at the rate of 6% per annum w.e.f. 29-12-1973 till

payment.

Comments: - This case upholds the same principle of materiality of facts; this principle is

widely misused by the companies to discharge themselves from liability of paying the insured.

Prior policies though disclosed were firstly, not recorded by the insurer’s agent and secondly

even if proved to be concealed had no bearing on the claim made by the insured. What is

important is the nexus between the materiality of the facts and the risk borne by the insurance

company and everything else is the way of its escape from the responsibility it bears towards the

public.

CHAPTER 3

Warranty

It is a guarantee or security that goods are of the quality stated. It may be defined as stipulation

or engagement by a party insured that certain matters relating to the subject matters affecting risk

exist or shall exist or have been done or shall be done.

Breach of warranty

The Effect of Breach of Warranty A breach of warranty has the same effect as a breach of

15

condition in other branches of law. The assured is discharged from further liability on proof of

breach of warranty. Section 36(2) of the Marine Insurance Act provides that Where a warranty is

broken, the assured cannot avail himself of the defence that the breach has been remedied, and

the warranty complied with before toss". But the assured may prove that a breach of warranty is

waived. Regarding the effect of breach of warranty, in Bank of Nova Scotia v. Hellenic War

Risks Assn. (Bermuda) Ltd., The Good Luck10, it has been stated that "A warranty, is a condition

which must be exactly complied with, whether it is material to the risk or not. If it not be so

complied with, then, subject to any express provision in the policy, the insurer is discharged from

liability as from the date of the breach of warranty, but without prejudice to any liability incurred

by him before that date." Relating to the extent to which a contract would survive breach of

warranty it was stated in this case, "It does not have the effect of avoiding the contract ab initio.

Not, strictly speaking, does it have the effect of bringing the contract to an end. It is possible that

this may be obligation of the assured under the contract which will survive the discharge of the

insurer from liability as for example a continuing liability to pay a premium". The insurer derives

the following advantages from breach of warranty by insured: 1 The breach of warranty gets the

insurer, an option or a right to avoid the contract. 2. Where the insurer decides to avoid the

contract he can repudiate his liability. The effects of breach of warranty are the same whether it

is an express warranty or an implied one. The insurer is the person who alleges the breach of

warranty and the burden of proof lies on him to prove the breach. It is common practice in

modem contracts of marine insurance to include a special clause that in case a particular

warranty is covered the assured can still be covered inspite of its breach if he pays an additional

premium to be arranged. Breach when excused Non-compliance with a warranty is excused in

the following cases: when, on account of change of circumstances, the warranty ceases to be

applicable to the circumstances of the contract; when compliance with the warranty is rendered

unlawful by any subsequent law; and a breach of warranty may be waived by the insurer. Waiver

may be expressed or implied, but must be intentional.

Principle of utmost good faith under the Marine Insurance Act, 1963-

The Marine Insurance Act, 1963 is somewhat relaxed in application when it comes to the

principle of utmost good faith. This is mainly because of the problems of access to the vessel,

10 [(1992) 1 AC 233]

16

cargo, etc. as well as the jurisdictional problems associated with international waters. If at any

point of time, the vessel or cargo is destroyed on high seas, the time when the same came to the

knowledge of the parties needs to be considered rather than the general principles of insurance

contract. Ss. 19-23 of the act talk about the principle of utmost good faith by using the terms

disclosure and representation. S.19 lays down the general principle and says that in absence of

utmost good faith, the contract may be avoided by the parties. S.20(1) says that the assured must

disclose every material circumstance he knows. Thus, the knowledge of the insured is more

important than the actual happening of the event. S.22(1) says that the representation made by

the insured must be true, which is again dependent on the capacity of the insured to know the

truth and is hence subjective. Finally, S.22 also says that whether the assured failed to disclose

intentionally or innocently or inadvertently is immaterial.

In a insurance contract, the parties have to act in a good faith and follow the principle of

ubberima fides- the utmost good faith.

Insurance contracts are a special class of contracts which are guided by certain basic principles

like those of utmost good faith, insurable interest, proximate cause, indemnity, subrogation and

contribution. As such, an insurance contract is generally a combination of more than one of these

principles and no single principle can be used at one time. The rest is dependent on the contract

between the parties. These principles are mostly guided by common law principles from which

they have developed. They have also been modified by principles of contract and by statutes as

in the case of the Marine Insurance Act, 1963 which has to a certain extent relaxed the basic

principles of insurance law.

General Principle of Utmost Good Faith

Out of all the abovementioned principles, the principle of utmost good faith remains one of the

most important doctrines underlying the law of insurance. In Banque Finaciere de la Cite v.

Westgate Insurance Co. Ltd.,11, it was held that-The duty of disclosure is neither contractual, nor

tortuous, fiduciary or statutory in character but is founded on the jurisdiction originally exercised

by the courts of equity to prevent impositions.

The term good faith has been mentioned in the Indian Penal Code and it signifies good intention

and due care and caution. However, this principle under insurance law needs to be examined in

11 (1989) 2 All ER 982

17

the contractual context. In every contract in general, both parties owe no positive duty toward

each other beyond showing ordinary good faith. This emanates from the right of every person to

know about every material fact associated with the subject matter of the contract and there is no

escape to this. This follows from the maxim Caveat Emptor or buyer beware as under the Sale of

Goods Act. It means that each party must be given a reasonable opportunity to make independent

enquiries about the subject matter in question so that they may take a decision. Thus, all material

facts must be disclosed or made available to the party so that he or she may reasonably enquire

about the same.

In the case of Brownlie v. Campbell,12it was held that:

If one knows any circumstance at all which may influence the underwriters opinion as to the risk

he is incurring, there is an obligation to disclose that which one knows and the concealment of

any material circumstance whether you thought of it as being material or not, avoids the policy.

This further puts a duty on the party making the subject matter accessible to the person

enquiring, not to play fraud or misrepresent the same, else it would be hit by S.19 of the Indian

Contract Act, making the contract voidable at the option of the innocent party. But, S.19 also

clarifies that misrepresentation or even silence amounting to fraud will not entitle a party to

avoid the contract if he had the means of discovering the truth with ordinary diligence and did

not do so. Hence, there must thus be free consent and the parties must understand the same

things in the same sense.

The burden of proof to show non-disclosure or misrepresentation is on the insurance company

and the onus is a heavy one. The duty of good faith is of a continuing nature in as much no

material alteration can be made to the terms of the contract without the mutual consent of the

parties.

In the case of Rozanes v. Bowen,13

The principle of utmost good faith was laid down here. It was said that since it is to be presumed

that the underwriter knows nothing and the assured knows all, the latter must disclose the same.

Thus, an insurance contract is a contract uberrima fides.

12 (1880), 5 App Cas 92513 (1928), 32 L.I.L.R. 98

18

Good Faith expected from both parties-

Good faith is expected from the insured or assured as well as the insurer. It is the buyer's duty to

disclose all facts related to the risk to be covered. Similarly, it is the insurer's duty to inform the

insured of all the terms of the contract. However, it is generally the assured person on whom

there is a bigger duty to disclose. This is primarily because very often the insurer has to depend

upon what details the insured mentions in his form. If the insured gives wrong details or details

of goods which are actually not in existence, the insurer may end up paying for the wrong claims

in the future. The insurer faces a lot of problems trying to verify all such details, even though the

advent of technology has made the task comparatively easier now a days. Wrong information

given not only affects the insurer but also the other people involved in the insurance pool whose

premiums may be wrongly utilized to satisfy the claims. It is therefore an implied condition or

principle of insurance that the Assured be required to make a full disclosure of all material

particulars within his knowledge about the risk. Further, considering the increase in new

businesses in which insurance is being taken, it becomes mandatory for the assured to inform the

insurer if there are any alterations or changes to the business which increases the risk during the

validity of the policy and get his permission. If no disclosure is made, the insurer has every right

to avoid the contract.

In United India Insurance Co. Ltd. v. MKJ Corpn.,14 it was held that,

Just as the insured has a duty to disclose, it is the duty of the insurers and their agents, to

disclose, all material facts within their knowledge, since obligation of good faith applies to them

equally with the assured.

In Banque Finaciere de la Cite v. Westgate Insurance Co. Ltd.,15

In this case, the plaintiff bank had agreed to lend some 30 million pounds securities in the form

of some gemstones and some credit insurance policies. The gemstones when valued did not

prove to be worth much. So, the bank sought to rely on the insurance policies. The policies had

been brokered by a major firm of brokers who resorted to a series of false covers due to inability

to obtain full cover. On making claims under the policies, the bank discovered severe shortage in

cover. It was held that the insurers were under an obligation to disclose the same. It was also held

14 (1998) 92 Comp Cases 331 (333)

15 (1989) 2 All ER 982

19

that the only remedy available to the insured is to rescind the policy and claim the premium. No

other damages may be awarded.

In Joel v. Law Union,16 it was held that

The duty to show good faith falls on the insured as well as the insurer to an equal degree in all

types of insurance contracts.

Conclusion & Suggestions

Even though law seems to be clear in constituting a balance between the insuring party and

insured, but in reality, there is no equality between the two, as insurer is the richest corporation

and the individual is an ordinary individual. Insured has no legal knowledge about the

ambiguous language used in the company’s policy with intention to waive them from liability to

pay insured on happening of an agreed event. On discussion on these cases we can observe how

the companies willfully neglects reimbursing the insured, who later instead of getting their

amount from the company have to pay the courts for getting their rights enforced.

It’s pertinent to note that the position of disclosure is different between India and England where

the insured is only bound to answer the questions being put to him in the policy. As all the

questions relevant for the contract are been put before the insured therefore there’s more

accuracy of facts before the contract comes to force. This reduces the chances of confusion later

when the claim is made by the insured on his policy. This system must be adopted by the India

also to reduce the chances of ambiguity, and hence the burden of cases on the courts and insured

to get the agreed amount. The malpractice and arbitrary use of power by the insurance companies

must be restrained by incorporating provisions in the Act similar to the one adopted by the

English law to reduce the chances of ambiguity at later date. Else the insurer would keep taking

advantage of the insured by falsely repudiating the claims made by the insured. The change if

brought in the Act would not only reduce the hardship caused to the insured, but also reduce the

burden of courts over the insurance cases flooding on the false rejection of claims been made by

the companies, where most of the insured from the rural locality are not even aware of their

present rights under the Act.

Great care must be taken in deciding what would constitute illness or material change in health

or what ordinary simple disorder is, there’s a great chance for one being take for another by the

16 77 LJKB 1108

20

insurance companies. Therefore courts must take due care in identifying if the fact of which

insurance company is tending to repudiate the claim is of material nature, or not before deciding

the claim. Liberal interpretation must be adopted to further the object of the Act in favor of

insurer, for fulfillment of the claim raised by him, which depends on case to case bases. The

ambiguity lying in the Act must be removed, and in addition to that the time frame under the Act

must be reduced to one year instead of two years, as the premiums paid by the insured would be

at great risk if the time limit provided under, Section 45 is increased in accordance to the Law

Commission’s report.

Insurance is all about serving the consumers, therefore the Act must try furthering the purpose as

the greater trust of the consumers would only hamper the business of the insurer. Therefore for

its own sake it must try gaining the trust of the insured to gain business at a larger level.

BIBLIOGRAPHY

BOOKS REFFERED:

21

Dr. Avtar Singh, “Principles of Insurance Law”, 17th ed., 2002,Wadhwa& Co., Nagpur.

BrijAnand Singh, “New Insurance Law”, University Book agency, 4th ed., 2000, Allahabad.

Dr. S.R. Myneni, “Law of Insurance”, Asia Law House, First Edition,2014,Hyderabad.

WEBSITES REFFERED:

ww.iirmworld.org.in/conference/red-hyd/sv%20krishna%20mohan.ppt visited on March 17th, 2015.

www.Indian kanoon.com www.westlaw.com

ARTICLES REFFERED

http://www.mondaq.com/x/78140/The+Duty+Of+Disclosure+Part+1+of+2

http://www.indialaw.in/non-disclosure-material-facts-good-ground-insurance-

company-repudiate-claim/

http://m.businesstoday.in/story/why-accurate-disclosures-are-must-for-insurance-

policies/1/186559.html

22