Embed Size (px)

Citation preview

Sensitive – BRF20/2100838 3

c. working to address infrastructure funding and financing issues – we will discuss the wider urban work programme, including infrastructure funding and financing with you in early 2021

d. other tax measures which relate to housing or land that are on the Government’s tax policy work programme – these are being considered over a longer timeframe

e. changing local council rating bases to land-only – the Department of Internal Affairs (DIA) has been asked to provide advice to the Minister of Local Government in early 2021

f. working with the Ministry for the Environment (MfE) to ensure the Resource Management Act (RMA) reform improves housing supply – over the next two years.

11. The Large-Scale Projects in Auckland and Eastern Porirua will also contribute to increased housing supply and are the subject of a separate budget bid.

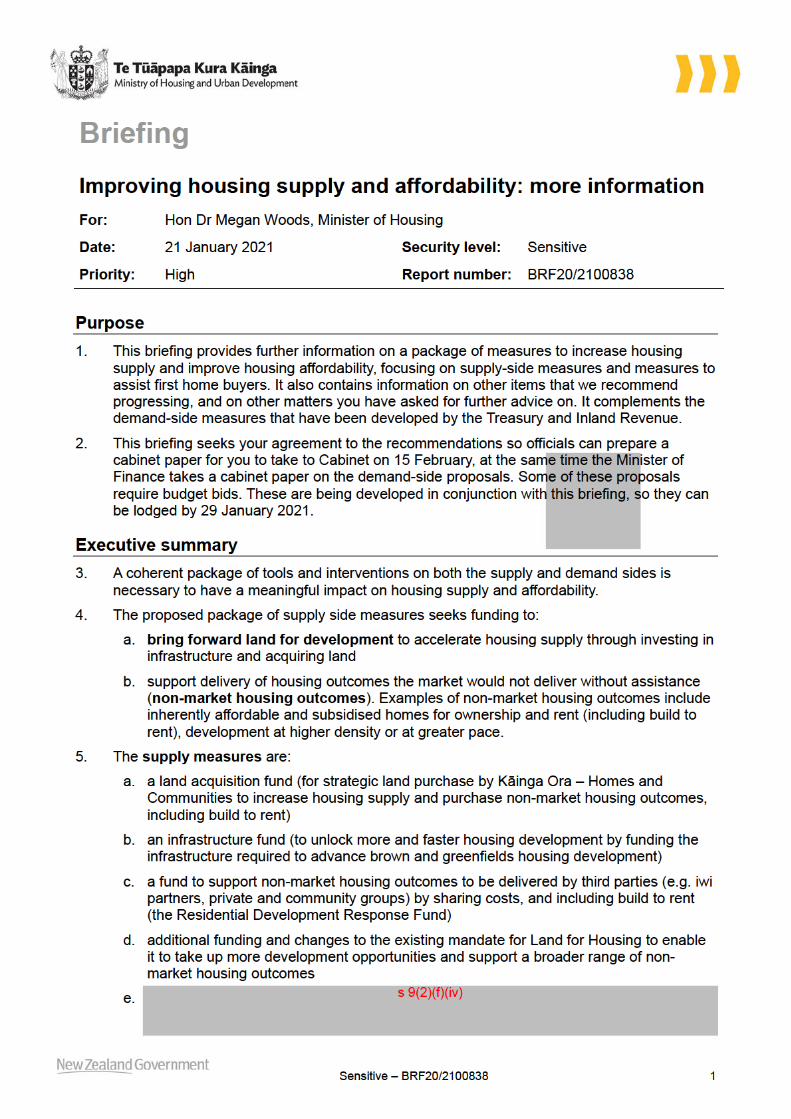

12. The briefing also contains advice on other matters, including capitalising AS or Working for Families, responding to a suggestion the Government use land acquisition powers to punish land bankers, and an update on the scale of empty homes.

Next steps 13. The Minister of Finance is intending to take a cabinet paper on two tax measures to Cabinet

on 15 February 2021. If you wish to proceed with any of the supply and first home buyer assistance measures in this paper, the Ministry of Housing and Urban Development (HUD) will provide you with a draft cabinet paper on 4 February for that same Cabinet meeting. It may also be useful to have a short overarching paper highlighting the need for a coherent package of demand and supply side measures, including the impact of demand side measures on new builds.

14. Budget bids are being prepared for this funding and financing package, and you discussed these with the Minister of Finance in your Budget bilateral in December 2020. On 21 December 2020, the Minister of Finance invited you to submit a package of interventions to improve housing supply and affordability. The February cabinet paper could seek pre-commitments against Budget 2021 for this package, or an in-principle agreement to allow you to announce some supply-side measures when the Minister of Finance announces demand measures.

Implementation

15. If you wish to proceed with the funding and financing package, we will work closely with Kāinga Ora on implementation and design issues, including a drawdown framework for funding, objectives, and detailed criteria for the non-market housing outcomes to be advanced, and the monitoring framework for tracking progress and reporting.

16. For the infrastructure fund, we will work with the Treasury, DIA, and the Ministry of Transport (MOT) and Crown Infrastructure Partners to ensure the proposed approach supports reforms already underway.

17. In developing and implementing this package, we will be informed by the relationships established under the urban growth partnerships, place-based approach, and MAIHI partnerships to ensure that this package works for a range of parties including Māori.

18. We will provide further advice in April 2021, on the above matters, including how best to ensure investment is prioritised across places and to areas where funding is reinforced by complementary commitments by local government and developers.

Sensitive – BRF20/2100838 4

Recommended actions 19. It is recommended that you:

Measures to increase supply

Funding and financing package

1. Agree to a funding and financing package to increase the pace and scale of overall housing supply, ensure that this housing is affordable for a range of households (whether for ownership or rental), and make sure it is in the right places, through:

a. securing access to land and securing non-market outcomes on that land e.g. affordable housing including build to rent (through providing funding to Kāinga Ora ( per annum) and Land for Housing ($29 million per annum) for this purpose)

b. supporting infrastructure provision ($1.7 billion over four years) (with Kāinga Ora administering this funding as agent of the Crown); and

c. supporting housing provision for those who cannot afford to pay a market rent or house price (the Residential Development Response Fund ($350 million total,

, with Kāinga Ora administering this funding.

Agree / Disagree

Adjusting the mandate of Land for Housing and reallocating some KiwiBuild funding

2. Note that Land for Housing has programme level targets of delivering 40 per cent KiwiBuild homes and 20 per cent public homes (with a minimum of 30 percent KiwiBuild and/or public housing per development).

Noted

3. Note that the Programme has recently been allocated o pay for upfront development costs (such as planning, consenting, earthworks and other land investment costs), to mitigate the impact of COVID-19 – costs to be recouped when the land is on-sold – CAB-20-MIN-0337 refers.

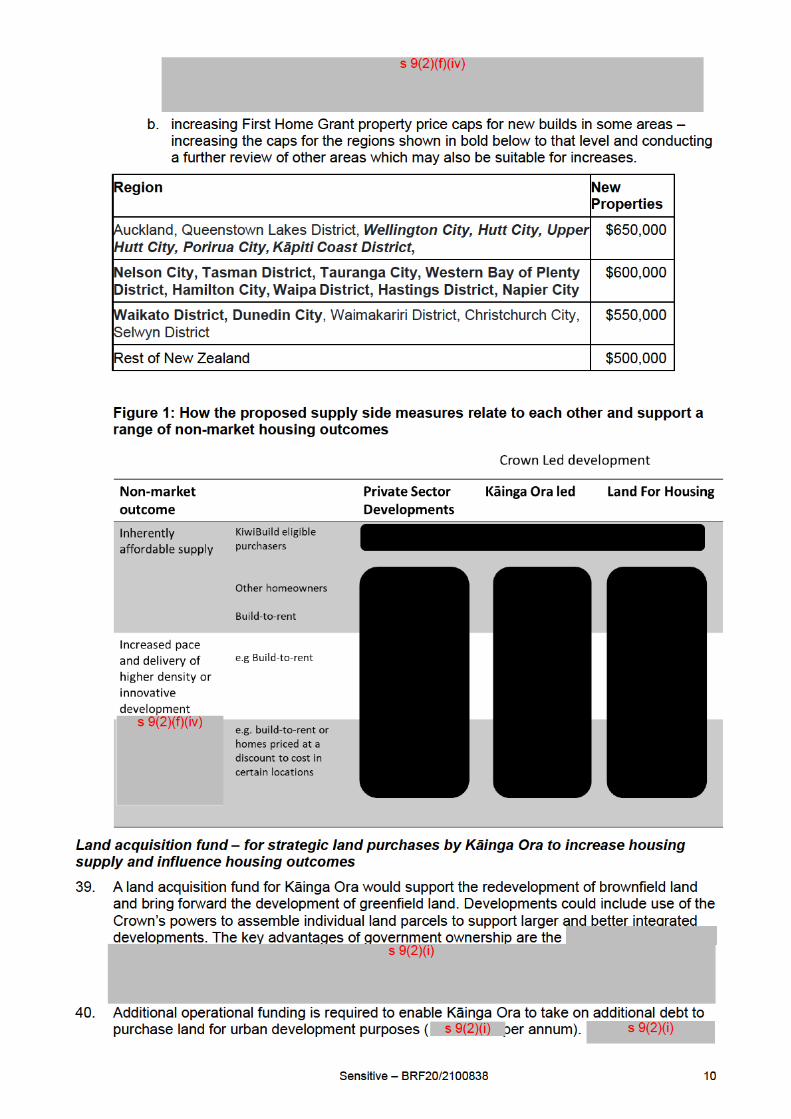

Noted

4. Noted

5. Agree / Disagree

6. Note that if you agree to recommendation 5 we will provide you and the Minister of Finance with a short paper to give effect to the decision above.

Noted

Noted

s 9(2)(f)(iv)

s 9(2)(f)(iv)

s 9(2)(f)(iv)

s 9(2)(f)(iv)

s 9(2)(i)

Sensitive – BRF20/2100838 5

Measures to assist first home buyers

8.

Noted

9. Agree / Disagree

10 Agree / Disagree

11 Noted

First Home Products (First Home Grant and First Home Loan) property price caps for new builds

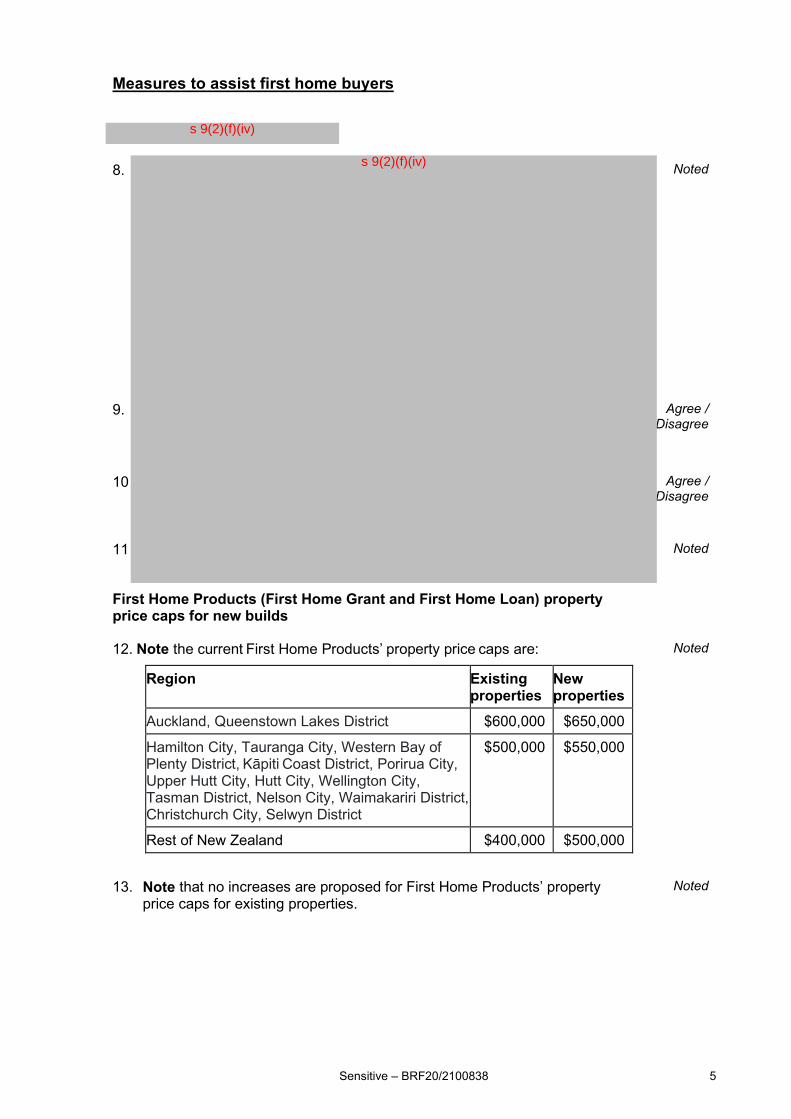

12. Note the current First Home Products’ property price caps are:

Region Existing properties

New properties

Auckland, Queenstown Lakes District $600,000 $650,000

Hamilton City, Tauranga City, Western Bay of Plenty District, Kāpiti Coast District, Porirua City, Upper Hutt City, Hutt City, Wellington City, Tasman District, Nelson City, Waimakariri District, Christchurch City, Selwyn District

$500,000 $550,000

Rest of New Zealand $400,000 $500,000

Noted

13. Note that no increases are proposed for First Home Products’ property price caps for existing properties.

Noted

s 9(2)(f)(iv)

s 9(2)(f)(iv)

Sensitive – BRF20/2100838 6

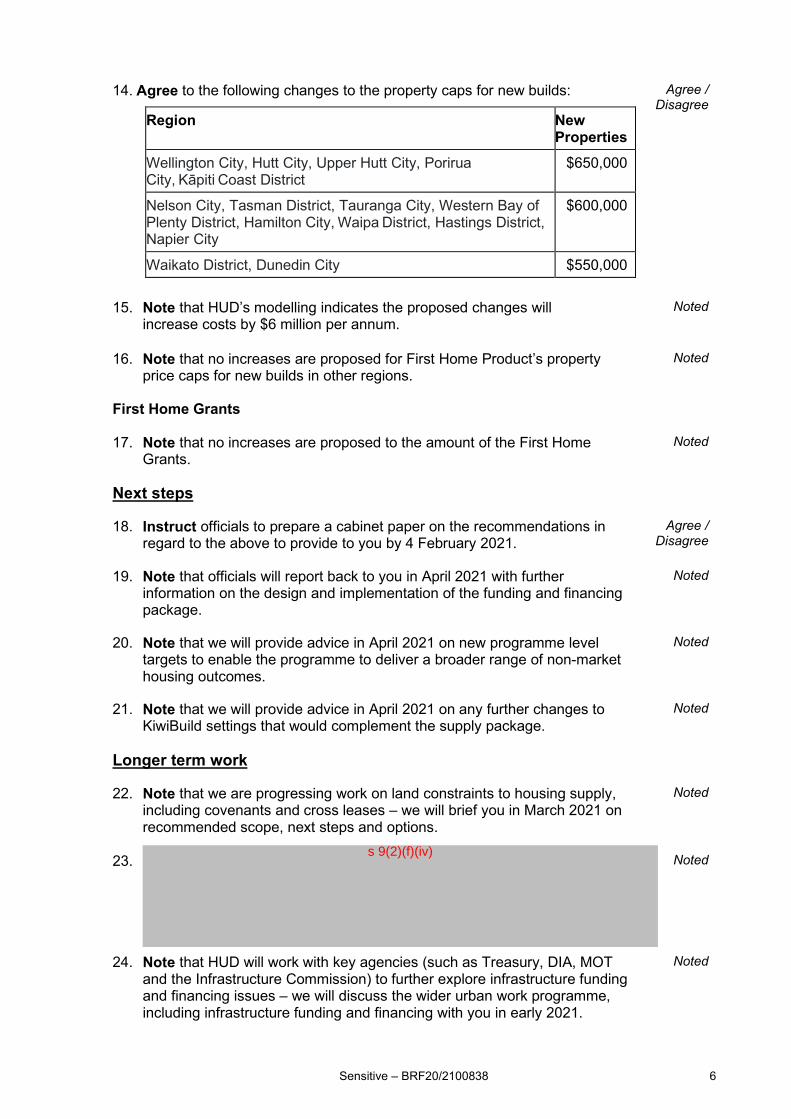

14. Agree to the following changes to the property caps for new builds:

Region New Properties

Wellington City, Hutt City, Upper Hutt City, Porirua City, Kāpiti Coast District

$650,000

Nelson City, Tasman District, Tauranga City, Western Bay of Plenty District, Hamilton City, Waipa District, Hastings District, Napier City

$600,000

Waikato District, Dunedin City $550,000

Agree / Disagree

15. Note that HUD’s modelling indicates the proposed changes will increase costs by $6 million per annum.

Noted

16. Note that no increases are proposed for First Home Product’s property price caps for new builds in other regions.

Noted

First Home Grants

17. Note that no increases are proposed to the amount of the First Home Grants.

Noted

Next steps

18. Instruct officials to prepare a cabinet paper on the recommendations in regard to the above to provide to you by 4 February 2021.

Agree / Disagree

19. Note that officials will report back to you in April 2021 with further information on the design and implementation of the funding and financing package.

Noted

20. Note that we will provide advice in April 2021 on new programme level targets to enable the programme to deliver a broader range of non-market housing outcomes.

Noted

21. Note that we will provide advice in April 2021 on any further changes to KiwiBuild settings that would complement the supply package.

Noted

Longer term work

22. Note that we are progressing work on land constraints to housing supply, including covenants and cross leases – we will brief you in March 2021 on recommended scope, next steps and options.

Noted

23. Noted

24. Note that HUD will work with key agencies (such as Treasury, DIA, MOT and the Infrastructure Commission) to further explore infrastructure funding and financing issues – we will discuss the wider urban work programme, including infrastructure funding and financing with you in early 2021.

Noted

s 9(2)(f)(iv)

Sensitive – BRF20/2100838 7

25. Note that the Government’s tax policy work programme includes a review of the current land rules, particularly in relation to investment property and speculators, land banking, and vacant land.

Noted

26. Note that DIA will provide the Minister of Local Government with advice in early 2021 on requiring local government to move to a land-only ratings basis (rather than land and capital improvements).

Noted

27. Note that HUD will continue to work with the Ministry for the Environment to ensure the Resource Management Act reform improves housing supply by expanding opportunities for housing development and reducing some of the barriers to development and the costs associated with them.

Noted

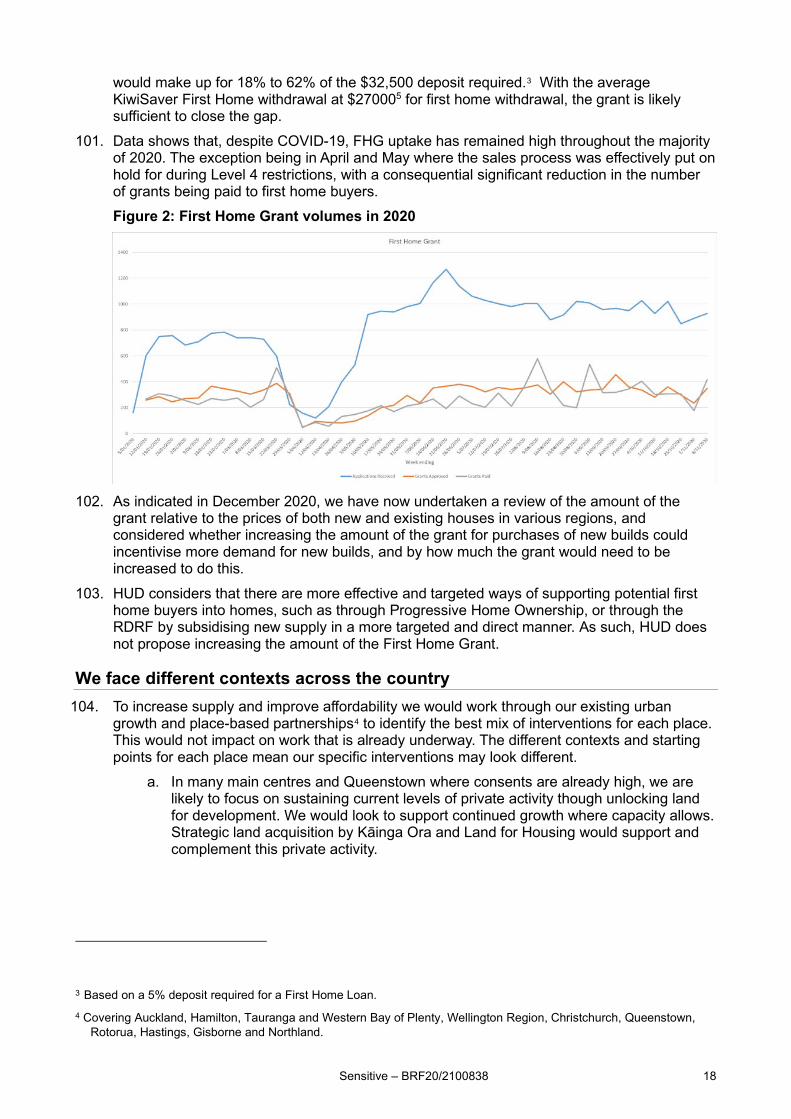

Other

28. Note that capitalising Accommodation Supplement or Working for Families is unlikely to be effective in supporting lower income households into home ownership as low incomes mean these households cannot service a mortgage.

Noted

29. Note the Government’s progressive home ownership scheme would be more effective in supporting low to middle income renters into ownership.

Noted

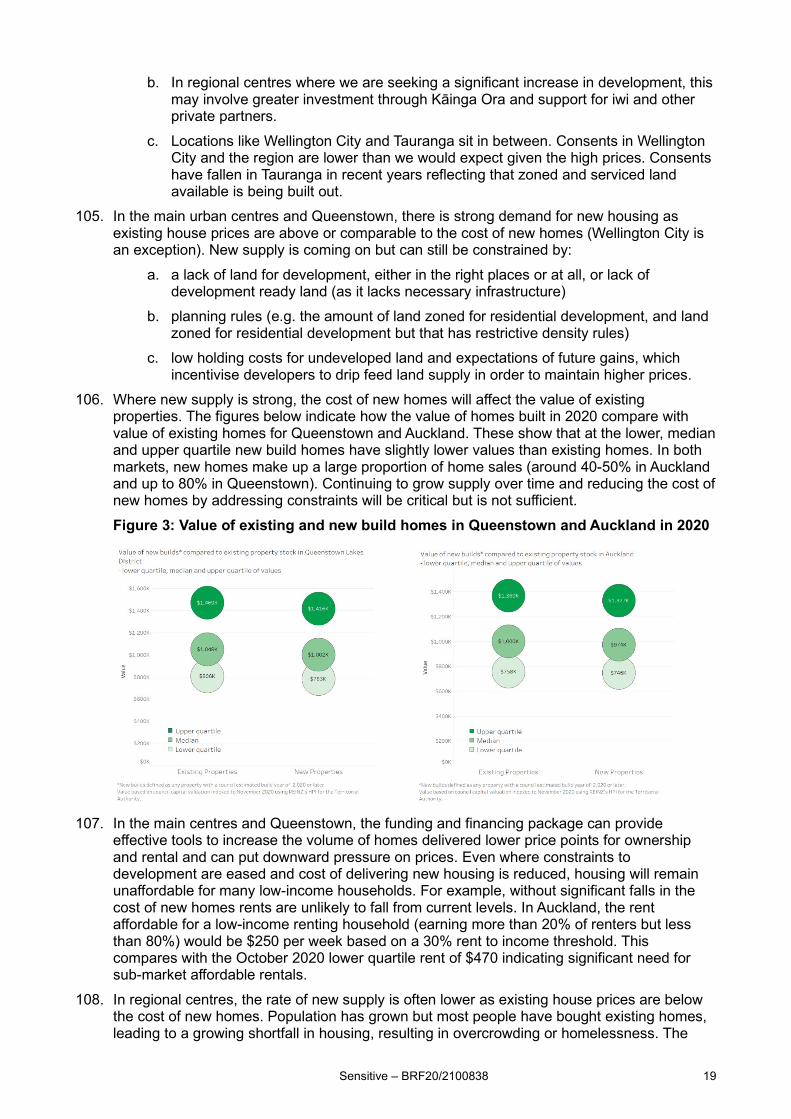

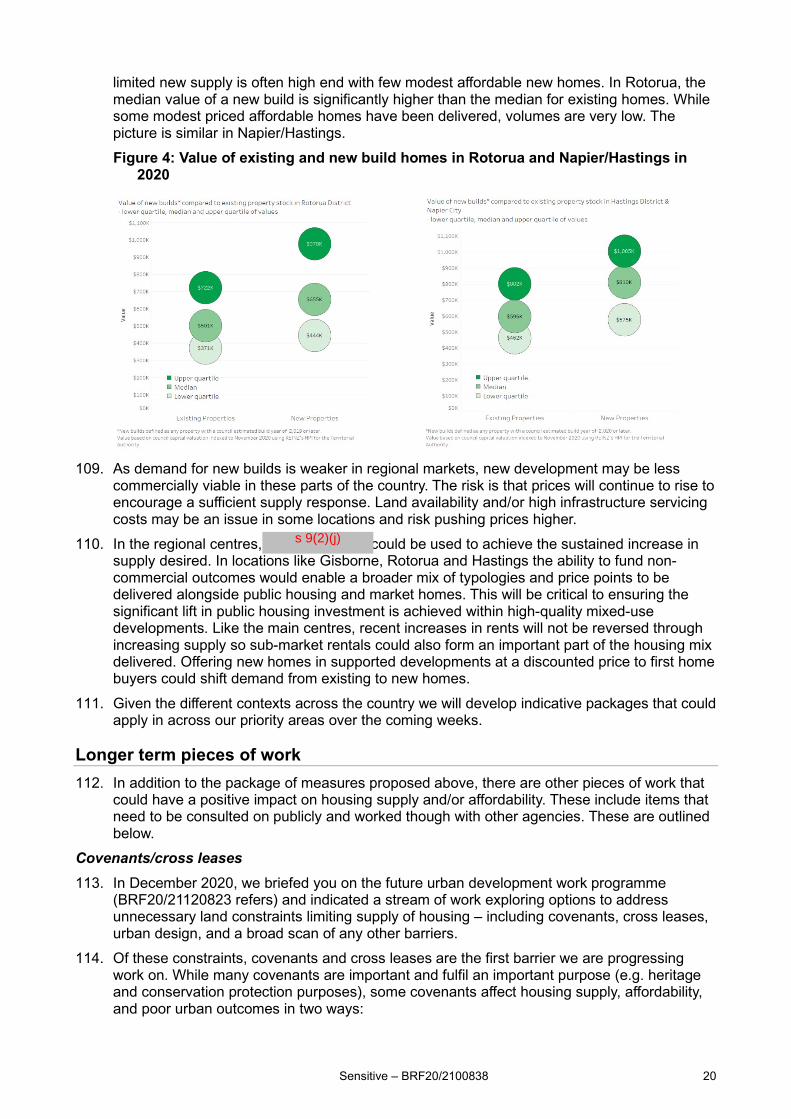

30. Agree that no further work is required on options to capitalise Working for Families or the Accommodation Supplement.

Agree / Disagree

31. Note that HUD will keep you updated on progress and results of the Empty Home Initiative to be conducted by Wise Group.

Noted

32. Refer this briefing to the Ministers of Finance and Building and Construction noting Cabinet delegated detailed policy, design, and implementation decisions for the RDRF to joint Ministers.

Agree / Disagree

Brad Ward Deputy Chief Executive, Place-based Policy and Programmes

..... / ...... / ......

Hon Dr Megan Woods

Minister of Housing

..... / ...... / ......

Sensitive – BRF20/2100838 8

Background 20. On 18 November 2020, we reported to you on our intention to provide you a work

programme by early February 2021, on increasing housing supply and improving housing affordability over the short-term (from 6 months to three years) (BRF20/21110795 refers).

21. We reported again on 4 December 2020, providing initial high-level advice on a potential package of options to increase housing supply and improve affordability over the short-term (BRF20/21120809 refers). We committed to reporting back to you in more detail on the package in February 2021 – this briefing contains that detail.

22. We have worked closely with the Treasury and Inland Revenue who have also developed options to moderate house price growth. The Treasury reported to the Minister of Finance on 7 December 2020 (T2020/3529 refers) on a range of measures, and we provided feedback on the potential impact on existing landlords and tenants of some of those measures to you on 22 December (AMI20/21120425 refers).

23. The Treasury reported again jointly with Inland Revenue on 12 January on a smaller number of tax measures (T2020/3844 IR2021/009 refers). A copy of this report was forwarded to you. We provided you an Aide Memoire on 15 January on the importance of an exemption for new builds from the tax measures being developed by the Treasury and Inland Revenue (AMI20/21010427 refers).

Context 24. The long-term affordability of the property market is reliant on significantly increasing supply.

Medium to long-term partial solutions are underway to address the situation, such as implementation of the National Policy Statement on Urban Development (NPS-UD), implementation of the Urban Development Act 2020 (UDA), Infrastructure Funding and Financing Act 2020 (IFF) and reform of the Resource Management Act 1991 (RMA).

25. The market is not delivering enough housing fast enough, and in many areas, the new housing delivered is not affordable to many people. This is resulting in more people struggling to buy a house and pay market rent, a growing public housing register, and an increase in Emergency Housing Special Needs Grants (EH-SNGs) and homelessness, with Māori disproportionately represented.

26. Recent increases in prices have been fuelled by increased demand due to low interest rates, removal of loan to value ratios restrictions, the attractiveness of housing as an investment, few listings in the property market, and general economic and confidence indicators being stronger than predicted.

Objectives 27. The proposed package of measures seeks funding to:

a. bring forward land for development to accelerate housing supply through investing in infrastructure and acquiring land

b. support delivery of housing outcomes the market would not deliver without assistance (non-market housing outcomes). Examples of non-market housing outcomes include inherently affordable and subsidised homes for ownership and rent, development at higher density or at greater pace.

28. Measures to bring forward land for development should support reforms already underway through the NPS-UD, the IFF, the UDA and proposed RMA reforms.

29. Support for non-market outcomes reflects the need to increase the supply of new homes that are inherently affordable through modest design, and that further subsidy may be needed to enable these homes to be affordable to some buyers or renters. Funding sought would build on existing KiwiBuild, First Home Products, and Progressive Home Ownership schemes (PHO), and provide flexibility to procure a mix of housing typologies and price points within Crown led, iwi and private developments in priority locations. Funding can also support

Sensitive – BRF20/2100838 9

taking on greater levels of development risk to deliver at higher density and/or delivery at greater pace.

30. The specific mix of interventions will differ across the country depending on the opportunities and market context. A key difference will be the extent we are seeking to boost supply compared to sustaining current levels of activity.

31. We also recommend specific changes to irst Home Grant (FHG) property price caps to better reflect the cost of new housing in each location and to support this supply side package.

Proposed package 32. A coherent package of tools and interventions is necessary to have a meaningful impact on

housing supply and affordability in the shorter term. Credible commitments now around supply alongside measures on demand can affect expectations of future price gains now dampening speculative demand and incentives to land bank.

33. Increasing the overall supply of new build housing in the right places will have the greatest impact on affordability over time. Consents are at their highest level since 1973, but due to population increase we are only building 7.5 new homes per 1000 people, compared to 13.4 homes per 1000 people in 1973. The rate of consents varies across the country with 9.5 consents per 1000 people in Auckland, 24.5 per 1000 in Queenstown and only 2 per 1000 in Rotorua.

34. Even if all of the tools and interventions in the package are implemented, we will not see a significant number of houses built immediately. However, there will be visible progress along the way (e.g. land acquired, infrastructure completed and sod turnings). Despite the lag, these interventions are necessary to start addressing the underlying causes of housing shortages and affordability pressures.

35. Over time, the implementation of the supply-side measures will help to ensure an ongoing pipeline of housing supply to meet a diverse range of needs and aspirations. In the meantime, the demand-side measures proposed by the Treasury and Inland Revenue will assist to take some of the heat out of current price increases, and the measures to assist first home buyers will enable some to purchase who otherwise might not have been able to.

36. The proposed supply measures are: a. a land acquisition fund (for strategic land purchase by Kāinga Ora to increase

housing supply and purchase non-market housing outcomes, including build to rent) b. an infrastructure fund (to unlock more and faster housing development by funding

the infrastructure required to advance brown and greenfields housing development) c. a fund to support non-market housing outcomes to be delivered by third parties (e.g.

iwi partners, private and community groups) by sharing costs, and including build to rent (the Residential Development Response Fund)

d. additional funding and changes to the existing mandate for Land to Housing to enable it to take up more development opportunities and support a broader range of non-market outcomes

e. 37.

38.

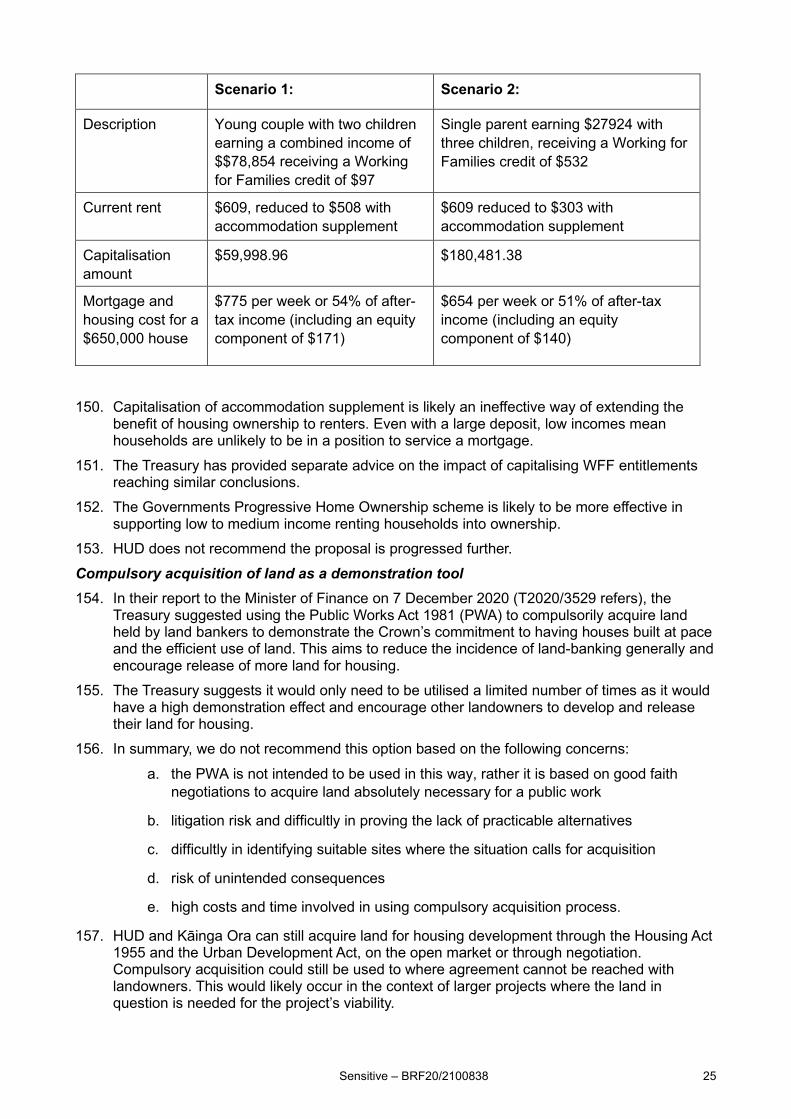

s 9(2)(f)(iv)

s 9(2)(f)(iv)

s 9(2)(f)(iv)

Sensitive – BRF20/2100838 12

49. Building infrastructure that enables more urban development to occur in the future creates a credible threat to the value of development-ready land that owners are currently holding in anticipation of future capital gain.

50. We will provide further advice in April 2021 on how we will prioritise investment in projects across places. This would take account of alignment with emerging spatial plans, the NPS-UD, potential yield and impact on the supply and affordability in a location. To mitigate the risk that government will continue to fund local infrastructure into the future in an ad hoc way, investment could also be prioritised to areas where funding is reinforced by complementary commitments by local government and developers. We will also look to fund projects in whole or part depending on what is required to get projects underway including where Crown funding could support the use of new tools like the IFF.

51.

52. We propose a fund of $1.7-1.8 billion over four years to be administered by Kāinga Ora. HUD would develop an expenditure framework and support Kāinga Ora in its implementation of that framework.

Residential Development Response Fund (RDRF) 53. To increase supply and affordability we also need to support private led developments. Even

though consents to government agencies are at 40 year high, these remain a small proportion of overall supply. Supporting a range of non-market housing outcomes through private developments, in the same way as we are proposing for Crown led projects is critical. This would include developments delivered by iwi, CHPs and private developers.

54. The RDRF was established to support the current, elevated, level of operation in the residential construction sector following COVID-19. It was a response to concerns that COVID-19 related impacts on the economy would negatively impact the residential construction sector, leading to loss of employment, loss of skills / apprenticeships and decreased housing supply in the midst of a housing shortage.

55. Given the residential construction sector has been more buoyant than expected, in

56.

57. The RDRF is currently funded with $250 million capex which must be recycled and returned to the Crown after 10 years, and $100 million opex from the COVID-19 response fund. We

58.

s 9(2)(j)

s 9(2)(f)(iv)

s 9(2)(f)(iv)

Sensitive – BRF20/2100838 13

59.

60.

61.

Expand the mandate of the Land for Housing Programme 62. HUD already operates the Land for Housing Programme (the Programme), which purchases

Crown land from other government departments and Crown entities, as well as private land, at market values and on-sells it to iwi or private development partners requiring each site to be developed subject to conditions, so that its development contributes to addressing the Government’s social objectives in relation to housing. Over 70 per cent of currently contracted developments are in partnership with iwi development partners.

63.

64.

65.

66.

s 9(2)(f)(iv)

s 9(2)(j)

Sensitive – BRF20/2100838 15

Measures to assist first home buyers 81. Increasing the support available to potential first home buyers, especially for purchases pf

new builds will help demand for new builds. Updating these settings will reinforce and support the supply package but will be less effective if the supply measures are not adopted.

s 9(2)(f)(iv)

s 9(2)(f)(iv)

s 9(2)(f)(iv)

Sensitive – BRF20/2100838 16

s 9(2)(f)(iv)

Sensitive – BRF20/2100838 17

Increasing the First Home Grant (FHG) property price cap (for new builds)

93. FHG’s are intended to help first home buyers overcome the deposit barrier. The grants are available to first home buyers who have contributed to Kiwisaver for three years or more, with income cap set at $85,000 for single buyers and $130,000 for 2 or more buyers. There are also caps on property price, discussed below.

94. The changes to the FHG are different to the KiwiBuild caps. FHG is targeted at helping first home buyers into the property market by overcoming the deposit barrier, while KiwiBuild caps are designed to provide a stretch target for developers.

Increasing the caps for new builds

95. HUD recommends that the price is adjusted in priority areas that have experienced persistent increase in lower quartile house prices. Similarly, HUD recommends that the increase is applied to new build only, to incentivise new supply. These changes will align with the proposed changes with the KiwiBuild price cap.

96. These are the current FHG (First Home Grant) caps:

Region Existing properties

New properties

Auckland, Queenstown Lakes District $600,000 $650,000 Hamilton City, Tauranga City, Western Bay of Plenty District, Kāpiti Coast District, Porirua City, Upper Hutt City, Hutt City, Wellington City, Tasman District, Nelson City, Waimakariri District, Christchurch City, Selwyn District

$500,000 $550,000

Rest of New Zealand $400,000 $500,000

97. No changes to the price caps recommended for existing properties. This is to ensure there is a focus of bring on new supply and not inflating already stressed housing markets. HUD’s recommended changes to the new build caps are shown below:

Region New Properties

Auckland, Queenstown Lakes District, Wellington City, Hutt City, Upper Hutt City, Porirua City, Kāpiti Coast District,

$650,000

Nelson City, Tasman District, Tauranga City, Western Bay of Plenty District, Hamilton City, Waipa District, Hastings District, Napier City

$600,000

Waikato District, Dunedin City, Waimakariri District, Christchurch City, Selwyn District

$550,000

Rest of New Zealand $500,000 The bold indicates Territorial Authorities that we recommend change tier

98. There are a number of other areas that HUD identified where the price caps could be increased. The evidence on increasing the cap in these areas is mixed. At this stage further investigation would be required to inform the decisions in these areas. Locations include, Whakatane District, Taupo District, Masterton District, Whangarei District, Kaipara District and Matamata Piako District.

99. It is difficult to quantify the impact of raising the cap with any accuracy as there is no data on unmet demand. HUD’s modelling indicates the proposed changes will increase cost by $6 million per annuum and deliver 330 homes. If the additional areas are included, then the cost will increase by approximately $500,000 and would provide additional grants for approximately 40 homes.

Increasing First Home Grant amount for new builds 100. The grants at current levels are still contributing to address the deposit barrier many first

home buyers face. At the capped house price of $650,000, the grant for an eligible couple

Sensitive – BRF20/2100838 18

would make up for 18% to 62% of the $32,500 deposit required.3 With the average KiwiSaver First Home withdrawal at $270005 for first home withdrawal, the grant is likely sufficient to close the gap.

101. Data shows that, despite COVID-19, FHG uptake has remained high throughout the majority of 2020. The exception being in April and May where the sales process was effectively put on hold for during Level 4 restrictions, with a consequential significant reduction in the number of grants being paid to first home buyers. Figure 2: First Home Grant volumes in 2020

102. As indicated in December 2020, we have now undertaken a review of the amount of the

grant relative to the prices of both new and existing houses in various regions, and considered whether increasing the amount of the grant for purchases of new builds could incentivise more demand for new builds, and by how much the grant would need to be increased to do this.

103. HUD considers that there are more effective and targeted ways of supporting potential first home buyers into homes, such as through Progressive Home Ownership, or through the RDRF by subsidising new supply in a more targeted and direct manner. As such, HUD does not propose increasing the amount of the First Home Grant.

We face different contexts across the country 104. To increase supply and improve affordability we would work through our existing urban

growth and place-based partnerships4 to identify the best mix of interventions for each place. This would not impact on work that is already underway. The different contexts and starting points for each place mean our specific interventions may look different.

a. In many main centres and Queenstown where consents are already high, we are likely to focus on sustaining current levels of private activity though unlocking land for development. We would look to support continued growth where capacity allows. Strategic land acquisition by Kāinga Ora and Land for Housing would support and complement this private activity.

3 Based on a 5% deposit required for a First Home Loan. 4 Covering Auckland, Hamilton, Tauranga and Western Bay of Plenty, Wellington Region, Christchurch, Queenstown,

Rotorua, Hastings, Gisborne and Northland.

Sensitive – BRF20/2100838 19

b. In regional centres where we are seeking a significant increase in development, this may involve greater investment through Kāinga Ora and support for iwi and other private partners.

c. Locations like Wellington City and Tauranga sit in between. Consents in Wellington City and the region are lower than we would expect given the high prices. Consents have fallen in Tauranga in recent years reflecting that zoned and serviced land available is being built out.

105. In the main urban centres and Queenstown, there is strong demand for new housing as existing house prices are above or comparable to the cost of new homes (Wellington City is an exception). New supply is coming on but can still be constrained by:

a. a lack of land for development, either in the right places or at all, or lack of development ready land (as it lacks necessary infrastructure)

b. planning rules (e.g. the amount of land zoned for residential development, and land zoned for residential development but that has restrictive density rules)

c. low holding costs for undeveloped land and expectations of future gains, which incentivise developers to drip feed land supply in order to maintain higher prices.

106. Where new supply is strong, the cost of new homes will affect the value of existing properties. The figures below indicate how the value of homes built in 2020 compare with value of existing homes for Queenstown and Auckland. These show that at the lower, median and upper quartile new build homes have slightly lower values than existing homes. In both markets, new homes make up a large proportion of home sales (around 40-50% in Auckland and up to 80% in Queenstown). Continuing to grow supply over time and reducing the cost of new homes by addressing constraints will be critical but is not sufficient. Figure 3: Value of existing and new build homes in Queenstown and Auckland in 2020

107. In the main centres and Queenstown, the funding and financing package can provide

effective tools to increase the volume of homes delivered lower price points for ownership and rental and can put downward pressure on prices. Even where constraints to development are eased and cost of delivering new housing is reduced, housing will remain unaffordable for many low-income households. For example, without significant falls in the cost of new homes rents are unlikely to fall from current levels. In Auckland, the rent affordable for a low-income renting household (earning more than 20% of renters but less than 80%) would be $250 per week based on a 30% rent to income threshold. This compares with the October 2020 lower quartile rent of $470 indicating significant need for sub-market affordable rentals.

108. In regional centres, the rate of new supply is often lower as existing house prices are below the cost of new homes. Population has grown but most people have bought existing homes, leading to a growing shortfall in housing, resulting in overcrowding or homelessness. The

Sensitive – BRF20/2100838 20

limited new supply is often high end with few modest affordable new homes. In Rotorua, the median value of a new build is significantly higher than the median for existing homes. While some modest priced affordable homes have been delivered, volumes are very low. The picture is similar in Napier/Hastings. Figure 4: Value of existing and new build homes in Rotorua and Napier/Hastings in

2020

109. As demand for new builds is weaker in regional markets, new development may be less

commercially viable in these parts of the country. The risk is that prices will continue to rise to encourage a sufficient supply response. Land availability and/or high infrastructure servicing costs may be an issue in some locations and risk pushing prices higher.

110. In the regional centres, could be used to achieve the sustained increase in supply desired. In locations like Gisborne, Rotorua and Hastings the ability to fund non-commercial outcomes would enable a broader mix of typologies and price points to be delivered alongside public housing and market homes. This will be critical to ensuring the significant lift in public housing investment is achieved within high-quality mixed-use developments. Like the main centres, recent increases in rents will not be reversed through increasing supply so sub-market rentals could also form an important part of the housing mix delivered. Offering new homes in supported developments at a discounted price to first home buyers could shift demand from existing to new homes.

111. Given the different contexts across the country we will develop indicative packages that could apply in across our priority areas over the coming weeks.

Longer term pieces of work 112. In addition to the package of measures proposed above, there are other pieces of work that

could have a positive impact on housing supply and/or affordability. These include items that need to be consulted on publicly and worked though with other agencies. These are outlined below.

Covenants/cross leases 113. In December 2020, we briefed you on the future urban development work programme

(BRF20/21120823 refers) and indicated a stream of work exploring options to address unnecessary land constraints limiting supply of housing – including covenants, cross leases, urban design, and a broad scan of any other barriers.

114. Of these constraints, covenants and cross leases are the first barrier we are progressing work on. While many covenants are important and fulfil an important purpose (e.g. heritage and conservation protection purposes), some covenants affect housing supply, affordability, and poor urban outcomes in two ways:

s 9(2)(j)

Sensitive – BRF20/2100838 21

a. increasing the cost (and subsequent price) of new housing by imposing minimum size restrictions and design criteria (e.g. requiring minimum floor areas, a certain number of gables or an attached garage)

b. limiting redevelopment and further subdivision because they exist in perpetuity (e.g. setting a height limit or minimum subdivision size).

115. Covenants and cross leases have the potential to undermine the intent of the NPS-UD to increase the quantity and quality of development capacity in urban areas and undermine objectives of the RMA reform, which will build on the NPS-UD.

116. We do not know the prevalence or details of covenants that impact housing supply and affordability across New Zealand, but case studies in Auckland and Rolleston highlight the scale of possible impact of land titles with covenants.

a. There are approximately 437,038 restrictive covenants operative in the Auckland region, many of which are surrounding Auckland’s inner-city, hindering densification in areas where it is most desirable.

b. In 2009, Selwyn District Council and Lincoln University examined the impact of restrictive covenants in Rolleston, Christchurch. The study found that around 75 per cent of the new subdivisions are subject to restrictive covenants requiring houses to have a specific floor area that potentially limit intensification.

117. We are progressing work in this area and will brief you in March 2021 on recommended scope, next steps and options to address land constraints, including covenants and cross leases. Work in this space will need to have cross-agency involvement and we will engage MfE, Land Information New Zealand (LINZ) and the Ministry of Justice (MoJ) in our next steps.

118. Covenants are governed under the Property Law Act (administered by MoJ), with their details managed through the Land Transfer Act (administered by LINZ). This means any changes to the legislation that sets out how they work would need to be agreed to and progressed by the Minister of Justice, and possibly the Minister for Land Information, with MoJ leading any changes to the Property Law Act

5 For the purposes of this briefing, we have used the words ‘Crown-owned’ land to describe land held and/or administered by Government departments and other Crown bodies, whether in the name of Her Majesty the Queen or otherwise.

s 9(2)(f)(iv)

Sensitive – BRF20/2100838 22

s 9(2)(f)(iv)

Sensitive – BRF20/2100838 23

132.

Working to continue to address constraints within the infrastructure funding system 133. Local councils are responsible for providing water, transport and community infrastructure to

support housing and urban development, but face funding and financing constraints. Many councils have under-invested over past decades in infrastructure maintenance, renewal and growth, fuelled by political pressures to keep rates (and hence debt) low and a lack of sufficient revenue and financing tools. Coordinating land use and central and local government infrastructure investment is also a significant challenge. Note that many of the projects listed in Annex A are transport projects relying on funding in full or part by NZTA.

134. For growth-related infrastructure, development contributions front-load some of the cost onto the ‘first movers’ in an area (i.e. initial developers and subsequent homeowners), however, the local authority is typically required to cover the cost of the infrastructure capacity to service future development in the area (i.e. beyond that required by the initial development) but which still needs to be built up-front as part of the new project, given network dynamics and scale efficiencies. This requires councils to finance the debt, and absorb the development risk, including the risk of stranded assets should subsequent growth not occur.

135. Many local authorities are running up against debt ceilings and revenue constraints (especially in light of the recent COVID-19-fuelled drop in council income) affecting their ability to take these kinds of risks and fund this up-front growth infrastructure .This means infrastructure to support housing is often delivered on a ‘just in time’ basis or postponed – which delays the construction of new housing. Many councils, prominently Auckland, are re-evaluating their planned infrastructure investment commitments over coming years.

136. The recently enacted Infrastructure Funding and Financing Act provides an opportunity for more infrastructure to be financed by the private sector, and HUD will continue to work closely with Crown Infrastructure Partners to identify projects which might be suitable to use the new model. The infrastructure funding initiative proposed in this paper will also support more infrastructure delivery.

137. These solutions are unlikely to be sufficient as long-term responses to either: a) the fundamental political and institutional constraints on local government which limit investment; and/or, b) the lack of a clear, consistent investment framework and funding source for the very large (i.e. multi-billion $) investment that is required in things like rapid-transit to support large-scale greenfield growth and intensification in the larger urban centres. The latter is important for connecting communities and giving people access to opportunity, and a critical component of ensuring that future urban growth supports social wellbeing, climate change, and inclusive economic transformation objectives.

138. Long-term, addressing this will require either a change in how local government generates revenue and funds infrastructure (and underlying incentives to do so) or a larger and ongoing role for central government in local infrastructure investment.

139. We reported to you in December 2020, on the need to work closely with other agencies to address challenges underlying infrastructure funding and financing (BRF20/21120823 refers). HUD will work with key agencies (such as the Treasury, DIA, MOT and the Infrastructure Commission) to further explore these issues and prioritise where we want to focus in the short, medium and long term, including considering institutional settings and constraints. This means considering not just whether we have the right funding tools, but whether councils have sufficient political incentives to use the tools.

s 9(2)(f)(iv)

Sensitive – BRF20/2100838 24

Other tax rules which relate to housing or land 140. There are other tax rules which relate to housing or land which have not been included in the

shorter-term packages proposed by HUD, the Treasury and Inland Revenue. Some were considered by the most recent Tax Working Group and included in the Government’s tax policy work programme. Inland Revenue have committed as part of that work programme to review the current land rules, particularly in relation to investment property and speculators, land banking, and vacant land.

141. The objective would be to recommend ways to improve the efficient use of land, and ensure that the current tax settings are fair, balanced, and encourage and support productive investment and discourages speculation. The review will also look at whether Inland Revenue can do anything more around enforcement of the current rules.

Changing local council rating bases to land-only 142. The Treasury recommended that the Minister of Finance discuss with the Minister of Local

Government requesting further advice from officials on requiring local government to move to a land-only ratings basis (rather than land and capital improvements). This would increase the holding cost of unimproved urban land but may have the unintended consequence of also reducing rates for owners of expensive houses on small centrally located sections.

143. This issue has been considered for years, including by the most recent Tax Working Group, and the Productivity Commission in February 2020, who noted that they viewed a land-only rating system to be preferable to a capital value system. To the degree that rates act as a fee for service, capital value is a better proxy of benefits received.

144. We understand DIA will report to their Minister on this shortly. Resource Management reform 145. Reform of the RMA has the potential to better enable development and improve housing

supply, affordability and choice. However, there is a risk that the of setting environmental bottom lines and objectives around climate change could increase the cost of building houses or discourage building altogether. We will continue to work with MfE to ensure the new legislation expands opportunities for housing development and reduces barriers to development, and their associated costs.

Other Capitalising Accommodation Supplement (AS)/Working for Families (WFF) 146. You have asked for advice about whether capitalisation of the AS can be used to provide a

deposit and improve the mortgage service ability for first home buyers. 147. The key challenge with this approach is that even with the high cost of rental housing faced

by AS recipients, most would struggle to service a mortgage due to low incomes. Initially, housing costs may be higher due to meeting housing related costs (e.g. rates and insurance) and meeting principle repayments.

148. The maximum amount of accommodation supplement that can be capitalised is around $180,000 over a 16-year period (assumes a 5% discount rate). This amount will decline as household income increases. For a household earning $78,000 and receiving $100 in accommodation supplement the capitalised amount is around $60,000.

149. Two scenarios are shown in the table below for families living in Auckland paying median rent for a three-bedroom home and purchasing a $650,000 home:

Sensitive – BRF20/2100838 25

Scenario 1: Scenario 2:

Description Young couple with two children earning a combined income of $$78,854 receiving a Working for Families credit of $97

Single parent earning $27924 with three children, receiving a Working for Families credit of $532

Current rent $609, reduced to $508 with accommodation supplement

$609 reduced to $303 with accommodation supplement

Capitalisation amount

$59,998.96 $180,481.38

Mortgage and housing cost for a $650,000 house

$775 per week or 54% of after-tax income (including an equity component of $171)

$654 per week or 51% of after-tax income (including an equity component of $140)

150. Capitalisation of accommodation supplement is likely an ineffective way of extending the benefit of housing ownership to renters. Even with a large deposit, low incomes mean households are unlikely to be in a position to service a mortgage.

151. The Treasury has provided separate advice on the impact of capitalising WFF entitlements reaching similar conclusions.

152. The Governments Progressive Home Ownership scheme is likely to be more effective in supporting low to medium income renting households into ownership.

153. HUD does not recommend the proposal is progressed further. Compulsory acquisition of land as a demonstration tool 154. In their report to the Minister of Finance on 7 December 2020 (T2020/3529 refers), the

Treasury suggested using the Public Works Act 1981 (PWA) to compulsorily acquire land held by land bankers to demonstrate the Crown’s commitment to having houses built at pace and the efficient use of land. This aims to reduce the incidence of land-banking generally and encourage release of more land for housing.

155. The Treasury suggests it would only need to be utilised a limited number of times as it would have a high demonstration effect and encourage other landowners to develop and release their land for housing.

156. In summary, we do not recommend this option based on the following concerns:

a. the PWA is not intended to be used in this way, rather it is based on good faith negotiations to acquire land absolutely necessary for a public work

b. litigation risk and difficultly in proving the lack of practicable alternatives

c. difficultly in identifying suitable sites where the situation calls for acquisition

d. risk of unintended consequences

e. high costs and time involved in using compulsory acquisition process.

157. HUD and Kāinga Ora can still acquire land for housing development through the Housing Act 1955 and the Urban Development Act, on the open market or through negotiation. Compulsory acquisition could still be used to where agreement cannot be reached with landowners. This would likely occur in the context of larger projects where the land in question is needed for the project’s viability.

Sensitive – BRF20/2100838 26

Empty homes 158. Long term vacant dwellings make up only a proportion of unoccupied dwellings. Houses

recorded as being unoccupied during census will include holiday homes, homes normally occupied but which are between tenancies, homes empty as they are undergoing renovations, and homes at which the normal occupants were not there on census night. Unoccupied homes may also include known houses for which no census return was provided, and no occupancy recorded.

159. There has been periodic media interest in the number of "unoccupied" homes in New Zealand, and whether these homes could be accessed to increase rental supply to reduce homelessness and the public housing register.

160. It is difficult to accurately quantify the number of unoccupied houses. 2018 census data suggested there were close to 200,000 empty homes nationwide on census night, with approximately 39,000 unoccupied dwellings in the greater Auckland area, but this data is likely to overstate the size of the issue. For example, a 2015 study by MBIE and Vector (using electricity usage data) found that in 2015, 8,000 properties (1.6% of all dwellings) were vacant in Auckland, compared with 33,500 from the 2013 census. The biggest proportions of vacant homes were in northern beach suburbs and Waiheke where there is likely a higher proportion of holiday homes. Auckland has the most long-term vacant dwellings (estimated to be around 9,500).

161. In considering whether to recommend a tax on vacant properties, the most recent Tax Working Group referenced this study and recommended not doing further work. The Group noted that international evidence showed limited effectiveness of such taxes in reducing the number of vacant properties. MBIE is now working with the Electricity Authority to try and obtain electricity usage data more broadly, as part of an Energy Poverty initiative (in partnership with HUD, EECA and others). We understand that little progress has been made on this, in part due to concerns about commercial sensitivity of the data.

162. Wise Group has been in discussion with HUD and its predecessors since 2016, seeking funding for the development of the Empty Homes initiative. The original proposal sought funding for $2 million, over 2 years, to undertake a proof of concept and subsequent rollout of the initiative. In late 2019, Wise Group approached HUD with a unique unsolicited proposal to identify the scale of empty homes in Auckland, and to test property owners’ appetite and willingness to rent these properties to middle income families/New Zealand’s key workers. Ministers agreed to allocate $500,000 from the Budget 2019 homelessness contingency towards this initiative, as a grant. In consultation with HUD, Wise Group has refined the proposal to focus on Waikato instead of Auckland, and a grant offer was provided to Wise Group on 24 December 2020.

163. If the offer is accepted, the project will commence from 31 January 2021 and HUD will receive the first report back in early April. Wise Group's preference is not to do any significant announcement until the project is underway. HUD will keep Ministers updated on progress and results.

Impacts Construction sector capacity and capability 164. Capacity constraints in the construction sector could risk constraining delivery of additional

housing supply and increasing costs. The number of people employed in the construction sector remains high and increased over 2020. Job advertisements have also not dropped away. However, the ability to find enough skilled and semi-skilled labour, especially in certain trades or disciplines, is continually raised by the sector as an issue.

165. We are working with MBIE and the Tertiary Education Commission to seek further information on the pipeline of trainees and apprentices coming through. However, any new labour (through training or immigration) will take time to filter through to increased capacity and fill any capability gaps. As a result, additional measures may be necessary (for example potentially bringing in additional workers from overseas, similar to the Christchurch rebuild).

Sensitive – BRF20/2100838 27

166. MBIE has advised that any options to increase workforce capacity in order to increase or speed up housing supply will need to consider the extent to which other parts of the system (such as the need to build new infrastructure and the consenting system) also has capacity to respond – particularly given the record high levels of building consents currently being processed.

Implementation and next steps 167. The Minister of Finance is intending to take a cabinet paper on two tax measures to Cabinet

for its meeting of 15 February 2021. If you wish to proceed with any of the supply and first home buyer assistance measures in this paper, HUD will provide you with a draft cabinet paper on 4 February for that same Cabinet meeting. It may also be useful to have a short overarching paper that highlights the need for a coherent package of demand and supply side measures, including the impact of demand side measures on new builds.

168. Budget bids are being prepared for this funding and financing package, and you discussed these with the Minister of Finance in your Budget bilateral in December 2020. On 21 December 2020, the Minister of Finance invited you to submit a package of interventions to improve housing supply and affordability. The February cabinet paper could seek pre-commitments against Budget 2021 for this package, or an in-principle agreement to allow you to announce some supply-side measures when the Minister of Finance announces demand measures.

169. If you wish to proceed with the funding and financing package, we will work closely with Kāinga Ora on implementation and design issues, including a drawdown framework for funding, objectives, and detailed criteria for the non-market housing outcomes to be advanced, and the monitoring framework for tracking progress and reporting.

170. For the infrastructure fund, we will work with the Treasury, DIA, MOT and Crown Infrastructure Partners to ensure the proposed approach supports reforms already underway.

171. In developing, and implementing this package, we will be informed by the relationships established under the urban growth partnerships, place-based approach, and the MAIHI partnerships to ensure that this package works for a range of parties including Māori.

172. We will provide further advice in April 2021, on the above matters, and how to prioritise investment in projects across places, including how best to ensure investment is prioritised to areas where funding is reinforced by complementary commitments by local government and developers.

Annexes 173. Annex A contains a number of infrastructure projects which the Infrastructure Fund could be

used to support.

Sensitive – BRF20/2100838 28

Annex A

s 9(2)(j)

Sensitive – BRF20/2100838 29

s 9(2)(j)

Sensitive – BRF20/2100838 30

s 9(2)(j)