Embed Size (px)

Citation preview

FISCAL RULES FISCAL RULES & Public Expenditure Management& Public Expenditure Management

Joaquim Joaquim Vieira LevyVieira LevySecretSecretááriorio do do Tesouro NacionalTesouro Nacional

MinistMinistéério da Fazendario da Fazenda

Workshop on Fiscal Management in Disadvantaged StatesWorkshop on Fiscal Management in Disadvantaged StatesNew Delhi New Delhi ---- January 2006January 2006

MINISTÉRIO DA FAZENDASecretaria do Tesouro Nacional

Summary

I – Importance of Subnational Governments

II – Macro Background for Fiscal Responsibility

III – Main Features of the Fiscal Responsibility Law

IV – Financial Programs between the Union and other Federative Units

V – Fiscal performance of subnational governments

RepRepúública Federativablica Federativa do do BrasilBrasil

Area:Area: 8,5 million km8,5 million km22

Population: 182 millionPopulation: 182 million

President: Luis President: Luis InacioInacio Lula Lula dada Silva Silva (2003(2003--2006)2006)

States: 26 + Federal DistrictStates: 26 + Federal District

Municipalities: 5,564Municipalities: 5,564

Autonomy: no unit, i.e., State or Autonomy: no unit, i.e., State or Municipality is subordinated: all Municipality is subordinated: all are are members members of the Federationof the Federation

GDP US$ 685,66 billion (5 % growth)Exchange Rate R$/US$ 2,65 (dec)GDP Per Capita US$ 3,77 milInflation 7,6% (IPCA)

Exports US$ 96,5 billionTrade Surplus US$ 33,4 billion Primary Surplus 4,58% of GDP

Tax Burden 36,74% of GDP

The economy in a glimpse (2004)

Public Debt/GDP 51% (dec)

Tax and Transfer Structure

1. Taxes

§Tax collection largely centralized (Federal level)

§ Decentralized use of resources (health & other services)

2. Transfers

§ Significant flows across levels of government

§ Significant flows across regions (SE, SUL, NE, CO, NO)

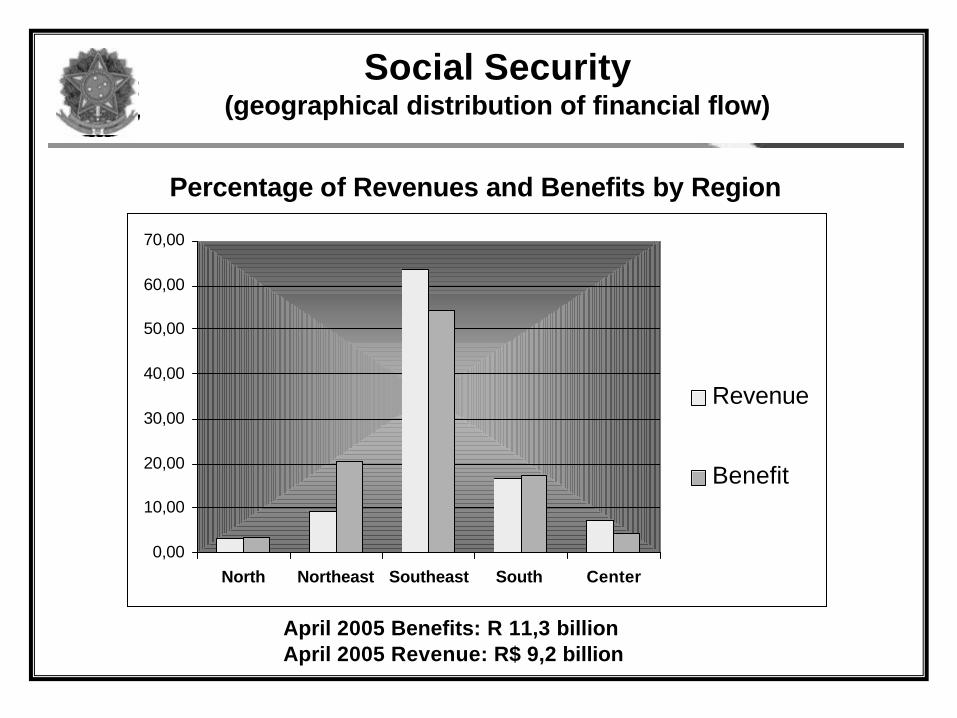

§ Social security benefits also showing flows across regions

BeforeBefore-- and Afterand After--transfer Revenuestransfer Revenues(2003 (2003 ----% of total taxes)% of total taxes)

67,1

26,4

6,4

54,7

26,8

18,5

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Antes das transferencias Após as transferencias

União Estados e DF Municípios

Federal

Municipal

State

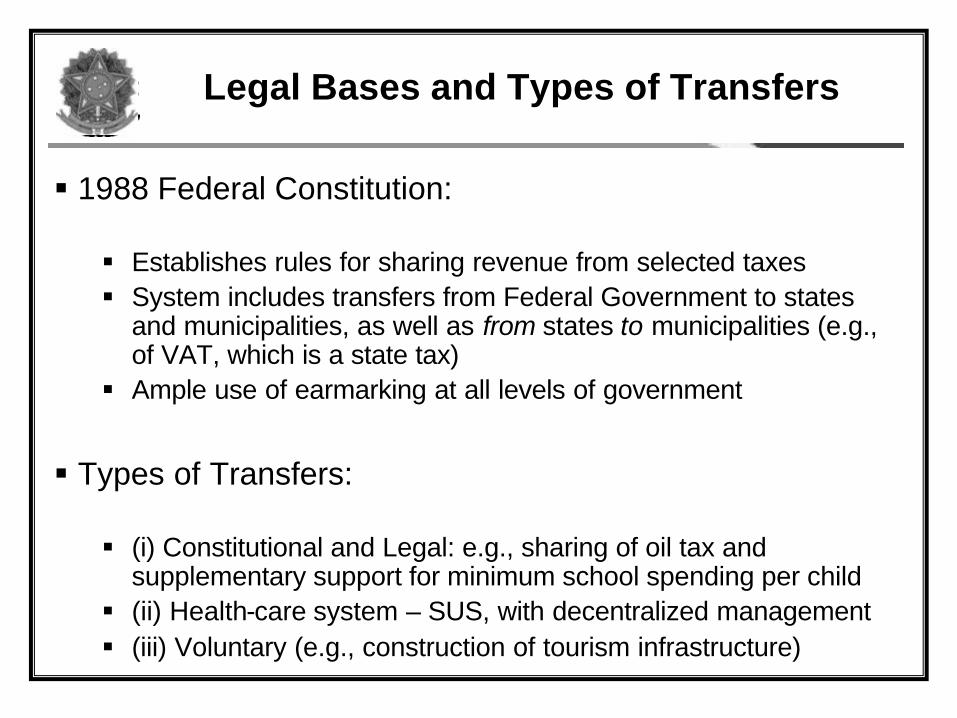

Legal Bases and Types of TransfersLegal Bases and Types of Transfers

§§ 1988 Federal Constitution: 1988 Federal Constitution:

§ Establishes rules for sharing revenue from selected taxes§ System includes transfers from Federal Government to states

and municipalities, as well as from states to municipalities (e.g., of VAT, which is a state tax)

§ Ample use of earmarking at all levels of government

§§ Types of Transfers: Types of Transfers:

§ (i) Constitutional and Legal: e.g., sharing of oil tax and supplementary support for minimum school spending per child

§ (ii) Health-care system – SUS, with decentralized management§ (iii) Voluntary (e.g., construction of tourism infrastructure)

Intergovernmental Transfers (2004)Intergovernmental Transfers (2004)

Valores em R$ milhõesTransferencias Estados Municípios Total

FPE/FPM* 20.346 23.472 43.817 IPI EXPORT.* 1.831 - 1.831 ITR - 141 141 IOF OURO 2 5 7 Desoneração ICMS* 2.173 718 2.891 FUNDEF 3.660 5.101 8.761 Complementação FUNDEF 109 376 485 CIDE 836 273 1.109 Salário Educação 1.417 1.328 2.745 Royalties Petróleo 3.518 2.151 5.669 Royalties Rec.Hídricos 390 390 780 Royalties Mineração 74 209 283 Transf. Voluntárias 2.734 3.010 5.744 SUS 6.847 12.389 19.236 Total 43.938 49.561 93.499 Participação % 47,0 53,0 100,0 Fonte: STN/SIAFI

*Valores já deduzidos de 15% para o FUNDEF

About5% of GDP

Social SecuritySocial Security(geographical distribution of financial flow)(geographical distribution of financial flow)

0,00

10,00

20,00

30,00

40,00

50,00

60,00

70,00

North Northeast Southeast South Center

Revenue

Benefit

Percentage of Revenues and Benefits by Region

April 2005 Benefits: R 11,3 billionApril 2005 Revenue: R$ 9,2 billion

Taxes = US$ 765Taxes = US$ 765 Transfers = US$ 115Transfers = US$ 115

< 110110 - 170170 - 270270 - 550> 550

US$

< 110110 - 170170 - 270270 - 550> 550

US$

Federal Taxes & Federal Taxes & IntergovIntergov. Transfers. Transfers(geographical distribution;per capita)(geographical distribution;per capita)

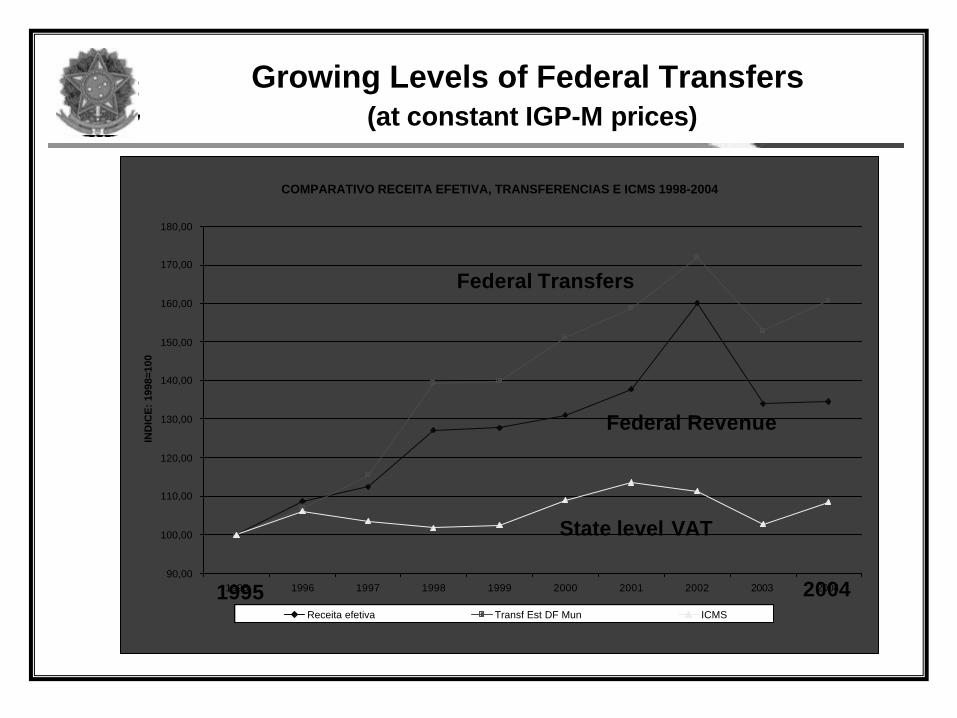

Growing Levels of Federal TransfersGrowing Levels of Federal Transfers(at constant IGP(at constant IGP--M prices)M prices)

COMPARATIVO RECEITA EFETIVA, TRANSFERENCIAS E ICMS 1998-2004

90,00

100,00

110,00

120,00

130,00

140,00

150,00

160,00

170,00

180,00

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

IND

ICE

: 19

98=1

00

Receita efetiva Transf Est DF Mun ICMS

State level VAT

Federal Revenue

Federal Transfers

1995 2004

I – Importance of Subnational Governments

II – Macro Background for Fiscal Responsibility

III – Main Features of the Fiscal Responsibility Law

IV – Financial Programs between the Union and other Federative Units

V – Fiscal performance of subnational governments

Macroeconomic Overhang

Monthly Inflation 1976/2004 – FIPE IPC (%)

1980s: democratization and need to accommodate higher social demands à sharp decline in GDP growth

1990s: price stabilization àfiscal imbalances become evident, especially at state level

Federal government refinances states and large municipalities

2000s: fiscal responsibility framework established and functioning

-10,0

0,0

10,0

20,0

30,0

40,0

50,0

60,0

70,0

80,0

90,0

abr/

76ab

r/77

abr/

78ab

r/79

abr/

80ab

r/81

abr/

82ab

r/83

abr/

84ab

r/85

abr/8

6ab

r/87

abr/8

8ab

r/89

abr/

90ab

r/91

abr/

92ab

r/93

abr/

94ab

r/95

abr/

96ab

r/97

abr/

98ab

r/99

abr/

00ab

r/01

abr/

02ab

r/03

abr/

04ab

r/05

%

Plano Collor I

Plano VerãoPlano Collor II

Pré-fixação da correção monetária e

câmbio

Plano Bresser

Plano Cruzado

Plano Real

Fiscal Responsibility: cornerstone of economic policies

General government: Primary surplus 2004 (% of GDP)

0,60

-0,20

1,10

2,40 2,10

5,10 3,98 3,6

2,20

Turkey

BB-

Brazil

BB-

Indonesia

BB-

Peru

BB

Colomb

BB

Phillippin

BB

Russia

BBB-

Mexico

BBB-

S.Africa

BBB

3,1

3,3 3,35

3,75

4,25

4,5

3,23

3,463,64

3,89

4,25

4,614,80

2,5

3,0

3,5

4,0

4,5

5,0

1999

2000

2001

2002

2003

2004

Feb-

05

% G

DP

Primary Result IMF Target

30

37

44

51

58

65

1997 1998 1999 2000 2001 2002 2003 2004

Net

Deb

t/GD

P (%

)

IPCA IER IGP-DI (*)

An effort shared by all levels of government

Public Sector Net Debt/GDP ratio

0,50,4

-0,3

0,6

2,4

1,9 1,8

2,42,5

3,0 3,1

0,1

0,7

1,1

0,6

-0,2

0,6

1,1

-0,1

0,1

-0,4

0,9

0,70,9 1,0

-0,2-0,5

-0,7

1,00,90,80,9

0,2

-1,0

-0,5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

dez/

95

dez/

96

dez/

97

dez/

98

dez/

99

dez/

00

dez/

01

dez/

02

dez/

03

dez/

04

set/0

5

% P

IB

Governo Central Estatais Estados/Municípios

• End of state financing by banks and recurrent help by Federal government: the 1997 renegotiation was accompanied by tight contractsrequiring adjustment programs monitored by the Federal government;

• Closure or sale of state banks: financial support to clean up institutions (PROES): no more back-door financing by government banks;

• 2000 Fiscal Responsibility Law (for all levels & branches of government)

• prohibition of intergovernmental debt financing

• limits on total debt & personnel expenditure, compensatory measures for tax expenditure and new entitlements

• verifiable fiscal targets and transparency rules

• adjustment rules and institutional penalties

• 2003 reform of the Public Servant Social Security framework (for all levels and branches of government).

Steps for Fiscal Strengthening

I – Importance of Subnational Governments

II – Macro Background for Fiscal Responsibility

III – Main Features of the Fiscal Responsibility Law

IV – Financial Programs between the Union and other Federative Units

V – Fiscal performance of subnational governments

Budget PlanningPPA LDO LOA

(fiscal targets voted)

RulesLimits on Personnel, carry over of commitments, etc

Correction MechanismsIntra-year adjustments in expenditure, personnel management tools, borrowing

limitations, targeted escape clauses

Transparency and ControlPublication of Reports &

their presentation to Lawmakers at hearings

SanctionsInstitutional (suspension of

transfers) and personal (criminal charges)

Building Blocks of the LRF operation

Rules that apply to all levels of government

Rules that are

ð structuralI - limits of personnel expenditure as % of revenue and borrowing

limits;II – compensatory measures for tax expenditure and entitlements

ð aimed at raising electoral accountability

I – no intergovernmental or government controlled bank lending

II -- borrowing and expenditure limits for last year of government

ð flexible: few and specific escaping clausesI - sharp economic slowdownII - drastic change in monetary/x-rate policies

Rules to LIMIT PERSONNEL EXPENDITURES BY BRANCH (% of Net Current Revenue)

Previous Law FRL

FEDERAL GOVERNMENT 50,0 50,0Executive 40,9

Federal District

0,6Others

3,0

Prosecutor`s Office 37,9

Legislative 2,5Judiciary 6,0

STATES 60,0 60,0Executive 49,0Prosecutor`s Office 2,0Legislative 3,0Judiciary 6,0

MUNICIPALITIES 60,0 60,0Executive 54,0Legislative 6,0

GOVERNMENT LEVEL / BRANCH

Limit (/ NCR) 15 years transition period from 2001

FEDERAL GOV. 3,5 (proposal) ---

STATES 2,0 Reduces 1/15 of the exceeding amount .

MUNICIPALITIES 1,2 Reduces 1/15 of the exceeding amount .

GOVERNMENT LEVEL

Rules to LIMIT PUBLIC DEBT(as a proportion of net current revenue)

?? Defined by the Federal Senate from President`s proposal, as a proportion of net current revenue – NCR

? Transition period for those exceeding ceiling at the end of 2001

? Same value for every municipality and every state

? May be revised annually or at any time by a President`s proposal

Rules to COMPENSATE NEW TAX EXPENDITURE AND ENTITLEMENTS

?? Any bill that creates new expendituresAny bill that creates new expenditures has has to to show how show how these will these will be be financedfinanced ((thethe PresidentPresident can veto a can veto a lawlaw thatthat failsfails thisthis testtest).).

?Any new tax expenditure or continued (+3 years) mandatory expenditure can be approved only if new tax revenues are securedor expenditure of similar nature are reduced

? “new tax revenues” are those from tax rate increases, new taxes or permanent new revenues

? Any new subsidy, guarantee or measure to benefit a particular group has to be approved by a specific law

•No unit of the Federation can lend or otherwise provide credit

to another unit, even with a view to renew, refinance or

lengthen the payment of outstanding debt

•The Central Bank cannot finance Federal, State or Municipal

Governments.

•Public financial institutions can not grant credit to those who

control them.

• The Senate has to authorize any credit operation (upon

recommendation of the National Treasury)

Rules to FORBID INTERGOVERNMENTAL and BANK FINANCING

§Personnel expenditures: No act that increases these

expenditure may occur on the 180 days before the end

of the administration (e.g., no hiring or compensation

increase).

§ Floating over the year: Any financial obligation left for

the following has to be backed by cash in the bank.

§ Credit Operations based on Anticipated Revenues: No

such operations can take place in the last year in office

Rules for the LAST YEAR IN OFFICE

PPA: multi-year plan (4 years) that includes ALL expenditure (including investment) on a consistent basis with fiscal targets

ð No program can be funded in the annual budget, if not included in the PPA

ð The PPA also aims at setting priorities, monitoring targets andevaluation procedures

LDO: annual law that establishes rules for budget preparation

ð 3-year fiscal targets for revenues, expenditures, primary and nominal results and public debt

ð Other rules for the budget preparation and execution

ð Financial and actuarial evaluation of social security and funds

ð Evaluation of fiscal risks, e.g., from contingent liabilities.

LOA: annual budget law prepared in line with the PPA and LDO

PLANNING MECHANISMSPLANNING MECHANISMS

CORRECTION MECHANISMS: Personnel Expenditure and Debt

•• While personnel expenditures are in excess of the prudential limit (95%):

ð no wage increase or adjustment to civil servants can take place

ðno new position can be created or overtime paid

• If ceiling is exceeded at the end of a quadrimester

ðexcess shall be eliminated in the next two quadrimester

ðexceptional cuts in personnel can take place

• If debt ceiling is exceeded

ðexcess shall be eliminated in the next three quadrimesters

ð failure to adjust forbids contracting any additional credit

•• In up to 30 days after the Budget is sanctioned, the government In up to 30 days after the Budget is sanctioned, the government shall prepare a monthly disbursement schedule consistent with shall prepare a monthly disbursement schedule consistent with targets for targets for quadrimesters quadrimesters ending on April, August and Decemberending on April, August and December

•• Every two months, the government prepares a report stating Every two months, the government prepares a report stating whether there are risks to fiscal targets. If so, it has to preswhether there are risks to fiscal targets. If so, it has to present a ent a new spending schedule with cuts in new spending schedule with cuts in ““discretionarydiscretionary”” spending; spending;

••Every four months fiscal performance and corrective measures Every four months fiscal performance and corrective measures are explained at Legislature hearings (Congress for Fed. Gov.)are explained at Legislature hearings (Congress for Fed. Gov.)

•• Adjustments can be delayed only according specific escape Adjustments can be delayed only according specific escape clauses (in the case of debt ceilings, upon Senate authorizationclauses (in the case of debt ceilings, upon Senate authorization))

•• WithinWithin--thethe--year adjustments strike a balance between overyear adjustments strike a balance between over--cautious spending patterns and strict observance of fiscal targecautious spending patterns and strict observance of fiscal targetsts

CORRECTION MECHANISMS: Budget Execution

• Social security receipts, expenditures and cash flow separated from those of the general budget (e.g., Treasury).

• Periodical publication of budgetary information in standard format on the press and internet

•National Treasury posts monthly report on States which debt exceeds the respective ceiling

•States and Municipalities send fiscal and financial data to National Treasury, which consolidates and makes them public on the Internet (NT does not audit those data)

• Public participation in the budgetary process and internet access to LDO, PPA, etc.

TRANSPARENCY AND CONTROLTRANSPARENCY AND CONTROL

• Fiscal Target Reports: summary report every two months and full report and hearings to legislative houses every four months, with explanation of corrective measures already taken (it includes state-owned enterprises!)

• Fiscal Administration Report (Relatórios de Gestão Fiscal): summary report every two months and full report every four months, with detailed information on personnel expenditure and the public debt; these are on accrual bases to ensure medium-term consistency.

• Consolidation of Subnatational Data – FIMBRA DATABANK: 96% of States and 94% of citie sent data to the National Treasury in 2004.

• Reports are the main tool for periodical auditing by Audit Courts(Tribunais de Contas). Federal Government is working with StateAudit Courts to enhance their operation and harmonize standards

TRANSPARENCY AND CONTROLTRANSPARENCY AND CONTROL: : How different reports work togetherHow different reports work together

• Sanctions can be Institutional and Personal

•Institutional sanctions affect the state or municipality

• Personal sanctions affect officials and can be administrative, electoral or crimminal

• Sanctions can be promoted by the

•Executive (institutional sanctions),

•Legislative (Audit Courts), or the

•Public Prossecutor, together with the Judiciary (e.g., personalcriminal sanctions)

• Any citizen can bring suit, e.g., based on published reports or other findings

SANCTIONSSANCTIONS

• Voluntary Transfers and Guarantees: Union can provide them onlyif other federation is complying with its debt service, revenue earmarking for health and education (within budgetary limits), and ceilings for personnel expenditure and debt.

• Credit operations: The National Treasury cannot recommend to theSenate any operation if debt is above limit or unit does not show ability to repay (according with previous and projected fiscal performance)

• Exception can be made to refinance (by third party) and operations to support reductions in personnel expenditure

• Also, the National Monetary Council has set caps for overall subnational lending operations and prudential limits for bank exposure to the subnational public sector (45% of bank capital)

INSTITUTIONAL SANCTIONS INSTITUTIONAL SANCTIONS and other control mechanismsand other control mechanisms

Criminal Component of LRF (Law 10.280/2000)Ø Arrest ( 3 months to 2 years) or imprisonment (1-4 years) Ø Fine of 30% of annual salary (for administrative faults

pointed out by the Audit Court)

More scope for applying existent legislation (DL 201/67) Ø Arrest ( 3 months to 3 years)Ø Removal from officeØ Ineligibility to be appointed or run to office for 5 years

PERSONAL SANCTIONSPERSONAL SANCTIONS

They apply to all responsible officials (elected or not) and cover actions as well as omission (e.g., not taking corrective measures)

I – Importance of Subnational Governments

II – Macro Background for Fiscal Responsibility

III – Main Features of the Fiscal Responsibility Law

IV – Financial Programs between the Union and other Federative Units

V – Fiscal performance of subnational governments

-- Adjustment programs underpin the debt refinancing occurred Adjustment programs underpin the debt refinancing occurred under Law n. 9496/97: under Law n. 9496/97:

-- contracts enabled states to pay their debts with the contracts enabled states to pay their debts with the private sector (high interest rates and short term), private sector (high interest rates and short term), providing for more predictability (ceilings for debt service) providing for more predictability (ceilings for debt service) and longand long--term payment schedules (30 years +)term payment schedules (30 years +)

-- Programs are a way to ensure consistent fiscal policies to Programs are a way to ensure consistent fiscal policies to facilitate the service of the rescheduled debtfacilitate the service of the rescheduled debt

-- Some contracts provide an allowance for new credit, Some contracts provide an allowance for new credit, which can be used only if programs are on trackwhich can be used only if programs are on track

-- Programs run for threePrograms run for three--year periods, but admit revisionsyear periods, but admit revisions

BASES AND FEATURES OF PROGRAMSBASES AND FEATURES OF PROGRAMS

Six targetsSix targets, of , of whichwhich firstfirst twotwo are crucial: are crucial:

1 1 –– CeilingCeiling onon Financial Financial DebtDebt; ; 2 2 –– PrimaryPrimary SurplusSurplus TargetTarget;;3 3 –– Ceiling on Ceiling on Civil Civil Servants ExpendituresServants Expenditures;;4 4 –– Projected StateProjected State´́s s Tax RevenueTax Revenue;;5 5 –– Objectives Objectives for for ReformsReforms; ; and and 6 6 –– Commitment Commitment toto Investiment ExpendituresInvestiment Expenditures. .

TargetsTargets are are agreed with Governor and reviewed every yearagreed with Governor and reviewed every year

FailureFailure to to meet targets may imply pecuniary penalties meet targets may imply pecuniary penalties ((acceleration acceleration of of debt paymentdebt payment for for sixsix monthsmonths) ) and restrictions on new credit and restrictions on new credit operationsoperations

PROGRAM CORE: Quantitative Targets

1 1 –– AgreementAgreement withwith GovernorGovernor, , includingincluding::

a)a) letterletter of of intentintent andand 5 5 annexes with annexes with macro macro andand fiscal fiscal projectionsprojectionsb) MOU b) MOU with targets and with targets and Fiscal Fiscal Appraisal by TreasuryAppraisal by Treasury

2 2 –– Annual ReviewAnnual Review, , based on based on aa Technical MissionTechnical Mission andand thethe analysisanalysis of of StateState General BalanceGeneral Balance and other and other datadata

3 3 –– Mission can Mission can face face one one of of three possibilitiesthree possibilities::

a) a) all targets all targets are are metmet, , and review can be completedand review can be completedb) some b) some targets other than targets other than 1 1 and and 2 are 2 are not metnot met, , which which still still allows allows Treasury Treasury to complete to complete the reviewthe reviewc) c) targetstargets 11 oror 2 are 2 are notnot metmet, , and review cannot be completedand review cannot be completed

4 4 –– In case (c), a In case (c), a waiverwaiver will only be granted will only be granted by the Ministerby the Minister of of Finance Finance upon Treasury recommendationupon Treasury recommendation, , usually usually at at the heels the heels of a of a strengthening strengthening in in the programthe program

PROGRAM IMPLEMENTATION PROGRAM IMPLEMENTATION

• Based on Provisional Act (MP) nº 1.811, of Feb/25/1999; update of certain rules by MP nº 2.185-35 of 2001

• Cover around 90 municipalities, which makes impractical to have individual adjustment programs

• In absence of yearly programs, rules are more stringent:• No new credit operation before debt/real revenues is below 1.0• Automatic penalty of raising debt service ceiling by 4 percentage

points above standard 13% of net real revenue in case:– Ceiling on civil servant pay is exceeded; – Pension outlays, obligations or provisions deviate from parameters in

MP n. 2185-35;– Any provision in the contract is breached

REFINANCE CONTRACTS WITH MUNICIPALITIES

I – Importance of Subnational Governments

II – Macro Background for Fiscal Responsibility

III – Main Features of the Fiscal Responsibility Law

IV – Financial Programs between the Union and other Federative Units

V – Fiscal performance of subnational governments

IMPACT OF LRF + PROGRAMS ON FISCAL PERFORMANCE

•• StateState ceilingsceilings onon personnelpersonnel expenditureexpenditure (50% of (50% of currentcurrent revenuerevenue):):

ØØ 6 states 6 states complied complied in 1996; 18 in 1996; 18 did did in 2000; in 2000; all have doneall have done sincesince 20012001

•• DebtDebt::

ØØ 5 states still 5 states still above ceiling above ceiling of 200% of of 200% of revenuesrevenues,, owingowing to 2002 to 2002 currency devaluationcurrency devaluation

ØØ 92% of 92% of municipalities below ceiling municipalities below ceiling of 1,2 times of 1,2 times revenues revenues ((only only a a handfull handfull of of large municipalities have large municipalities have real real problems with their debtproblems with their debt))

•• Primary surplusPrimary surplus::

ØØ Ten states Ten states were were still in still in deficit bydeficit by 2000; 2000; all were all were in in surplus bysurplus by 20042004

Primary Surplus as a proportion of GDP1998 1999 2000 2001 2002 2003 2004

Consolidated Public Sector -0,01% 3,19% 3,46% 3,64% 3,89% 4,25% 4,58%

Subnational Governments -0,29% 0,21% 0,69% 1,18% 1,05% 1,15% 1,12%

IMPACT: Steady Strengthening of State Finances

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

# of States with Program 0 0 3 16 22 25 25 25 25 25

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Debt Service \1 2,6 2,4 2,3 3,0 2,4 1,4 1,1 1,3 1,1 1,1

Financing SourcesPrimary Surplus -0,7 -0,4 -0,4 -1,0 0,2 0,5 0,5 0,6 0,8 0,8

Sale of Assets 0,0 0,3 1,3 1,1 0,8 0,6 0,2 0,1 0,1 0,0

Credit Operations 2,3 2,3 1,8 2,3 1,3 0,3 0,2 0,3 0,2 0,1

Arrears 0,9 0,2 -0,3 0,7 0,2 -0,1 0,3 0,3 0,1 0,1

Total 2,6 2,4 2,3 3,0 2,4 1,4 1,1 1,3 1,1 1,1

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Debt Service \1 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0

Financing SourcesPrimary Surplus -25,7 -15,1 -18,6 -34,3 6,7 37,8 47,1 45,5 69,1 74,7

Sale of Assets 1,6 11,5 54,3 35,5 32,4 44,4 13,8 6,7 5,0 2,3

Credit Operations 90,8 96,4 77,5 75,1 51,7 24,6 15,2 25,2 13,7 12,9

Arrears 33,3 7,3 -13,2 23,7 9,2 -6,8 23,8 22,6 12,1 10,2

% OF GDP

% of Debt Service

DISCRIMINATION

AGGREGATE FISCAL RESULTS

1 – Manual of the Fiscally Responsible Manager:: CD pCD presenting in plain language all the “do” and “don’t” for time-consistent, effective, lawful municipal administration. It also provides all pertinent legislation, rules, norms and manuals for preparation of the Budget, Fiscal Reports & Intergovernmental Transfers Applications

2 – Fiscal Management Computer Tool:: reads FIMBRA fiscal statistics for municipality of interest (1998-2003), provides rules to complete data for 2004, and helps project revenues for 2005-2008. The Computer Tool allows mayors and city managers to evaluate whether their government plans will be fiscally consistent, e.g., by satisfying the LRF ratios throughout the government period

Federal Federal GovernmentGovernment support support to LRF to LRF Implementation byImplementation by MunicipalitiesMunicipalities (Art. 64) (Art. 64)

Prepared by the National Treasury and distributed to

Municipalities in 2005

For more information, visit our web site For more information, visit our web site www.www.tesourotesouro..fazendafazenda..govgov..brbr

The Brazil we all know… and the Brazil we are building

Thank you !

§§ FPM and FPEFPM and FPE ((FundoFundo de de ParticipaParticipaççãoão dos dos EstadosEstados e e MunicMunicíípiospios; art. 159); art. 159): : shares the revenues from the Income Tax (47%) and the IPI Federashares the revenues from the Income Tax (47%) and the IPI Federal VAT on l VAT on industrial goods (53%)industrial goods (53%)

§ FUNDEF (Fundo de Manutenção e Desenvolvimento do Ensino Fundamental e de Valorização do Magistério; art. 212 and law 9424/96): provides for the financing of the 8-year basic education, particularly teacher compensation

§ The main sources of revenues are shared taxes, with the earmarking of 15% of FPE/FPM

§ In addition, the federal government makes up funds in the poorest states to ensure a minimum level of spending per student

§ Part of the Salário-Educação levied from firms (art 212 § 5 and law 9766/98)

§§ CIDECIDE ((ContribuiContribuiççãoão de de IntervenIntervenççãoão no no DomDomíínio Econômiconio Econômico; ; art. 177 § 4º and art.159 III): transfers 25% of the petrol tax to finance transport infrastructure

Main Constitutional TransfersMain Constitutional Transfers

§ Oil & gas royalties and participation (art. 20 and Laws 7990/89 and 9478/97): gives 5% of oil revenue (royalties) and a share of windfall gains (participação especial) to states and municipalities

§ Royalties for water resources used for power generation (art. 20 and Law 7990/89): 6% of electricity revenue for states and municipalities with associated rivers and lakes

§ Royalties on mineral resources (Law 8.001/90, art 2)

§§ IOFIOF Financial tax on gold transactions (Law 7766/89)Financial tax on gold transactions (Law 7766/89)

§§ Grants for exporting statesGrants for exporting states, after selected exports were exempt from , after selected exports were exempt from VAT, which is a state tax (Enabling Laws 87 and 115/2003)VAT, which is a state tax (Enabling Laws 87 and 115/2003)

Other Constitutional and Legal TransfersOther Constitutional and Legal Transfers

Other TransfersOther Transfers

§§ HealthHealth--carecare: SUS is a single provider system, which reimburses public and : SUS is a single provider system, which reimburses public and private providersprivate providers

§ Resources are distributed among states and municipalities on a formula-based system

§ Responsibility for specific resource allocation has been gradually transferred to states and municipalities

§§ Voluntary TransfersVoluntary Transfers: current or investment spending through cooperation : current or investment spending through cooperation agreements, or other type of financial support of states and munagreements, or other type of financial support of states and municipalitiesicipalities

§§ Shared management of Social Programs:Shared management of Social Programs: e.g., cash transfers for the very e.g., cash transfers for the very poor/poor/FomeFome Zero, although formulaZero, although formula--based, are managed with a strong based, are managed with a strong municipal participationmunicipal participation

§§ The The Federal Government is forbidden from Federal Government is forbidden from lendinglending to states and to states and municipalitiesmunicipalities

Significant dependency on TransfersSignificant dependency on Transfers(Federal Transfers as % current revenues (Federal Transfers as % current revenues ---- 2003)2003)

GRAU DE DEPENDENCIA DOS ESTADOS DAS TRANSFERÊNCIAS FEDERAIS - 2003

Estados Transf

União/RCL(%)

FPE/RCL (%)

FPE/Transf (%) Municípios

Nº de Municípios

Transf União/RC

(%)

FPM/RC (%)

FPM/Transf (%)

GRUPO 56,22 52,89 94,08 GRUPO 1.129 49,11 34,22 69,68 AP 71,90 68,89 95,81 RR 14 65,59 45,51 69,38 PI 68,06 59,10 86,83 PI 195 56,06 40,04 71,41 RR 66,10 65,62 99,28 MA 147 54,94 35,26 64,17 MA 66,21 58,14 87,81 PB 200 53,61 40,06 74,72 AC 62,36 62,05 99,50 AL 100 50,81 35,65 70,16 TO 53,72 53,16 98,96 TO 123 48,34 42,53 87,98 AL 49,11 47,13 95,97 AP 8 47,59 37,61 79,01 SE 44,44 43,37 97,60 AC 21 44,25 39,15 88,47 PB 42,11 40,23 95,52 PA 98 43,28 24,92 57,59

SE 70 43,15 30,70 71,15 RN 153 43,13 31,77 73,67

GRUPO 27,27 21,51 78,88 GRUPO 3.212 31,30 22,10 70,60 PA 40,67 32,19 79,16 CE 181 41,62 28,80 69,20 RO 40,55 36,61 90,28 PE 165 39,58 29,17 73,69 RN 38,97 35,79 91,84 RO 46 37,99 24,66 64,91 CE 36,99 30,91 83,58 BA 346 37,65 29,41 78,13 PE 28,58 24,26 84,87 GO 222 33,41 23,30 69,75 BA 26,12 20,90 80,00 MG 785 33,10 22,96 69,37 MT 23,03 15,98 69,36 MS 75 32,61 19,57 60,02 AM 22,35 17,72 79,28 MT 104 30,56 19,63 64,24 ES 16,94 8,05 47,53 PR 378 26,97 18,22 67,57 MS 18,39 11,10 60,35 SC 285 26,79 18,96 70,78 GO 16,18 11,57 71,47 AM 57 25,39 18,14 71,44

ES 77 24,78 17,19 69,39 RS 491 23,79 17,31 72,77

GRUPO 11,17 2,71 24,26 GRUPO 671 28,48 12,39 89,46 SC 15,22 4,44 29,18 RJ 82 15,36 4,44 28,90 DF** 14,92 3,91 26,19 SP 589 13,12 7,95 60,56 MG 14,69 6,44 43,89 PR 13,87 5,53 39,87 SP 11,49 0,49 4,29 RS 10,89 4,10 37,67 RJ 4,62 1,62 35,02

19,52 12,25 62,73 BRASIL 5.012 26,18 17,35 66,27 * Exceto royalties.Fontes: SIAFI e balanços de Estados e Municípios

GR

UP

O I-

ALT

A

DE

PE

ND

EN

CIA

GR

UP

O II

-ME

DIA

DE

PE

ND

EN

CIA

GR

UP

O II

I-B

AIX

A

DE

PE

ND

EN

CIA

BRASIL

Above 40%Avg > 55%

Below 15%Avg > 10%

15%-40%Avg around 25%

Transfers/Current Rev

States Municipalities

Municipalities are key partners for development and depend on transfers

% RECEITA BRUTA

Próprias IPTU ISS Transferências FPM SUS/FUNDEF Pessoal InvestimentoTOTAL 35,4 7,9 9,2 64,6 13,7 17,8 45,8 10,6 47,4POP > 1.000.000 51,9 13,4 16,7 48,1 3,5 14,0 46,7 10,7 122,61.000.000 > POP > 300.000 40,1 9,2 10,0 59,9 6,9 19,0 47,0 8,8 27,1300.000 > POP > 50.000 31,9 5,8 6,6 68,1 13,2 19,5 45,5 11,6 12,8POP < 50.000 15,9 2,4 2,4 84,1 30,9 20,0 44,2 10,4 3,5

ReceitasDívidaFaixas populacionais

Despesas

Share of Transfers in Revenues (2003)

Share of Municipalities in GDP (2003)

Expenditure: 7,95%

Investments: 0,87%

Education Spending: 4,22%

Next Challenge: improving the quality of spendingimproving the quality of spending

Transfer Rules (minimum conditions to receive voluntary transfers):(i) States and municipalities need to raise certain taxes on their own ;(ii) A budget allocation specifying use of resource is required;(iii) Transfers cannot support personnel expenditure;(iv) Documentation regarding compliance of tax, social security, labor

obligations, and debt service is to be provided;(v) Previous transfers ought to be ready for auditing;(vi) Earmarking to Health and Sanitation is observed (LRF);(vii) Limits for personnel expenditure and debt ceiling are observed;(viii) There are counterpart resources in the beneficiary budget;

Counterpart for Municipalities

· 5% -10%, for municipalities with up to 25.000 habitants;

· 10% - 20%, for other municipalities in SUDAN/SUDENE/CO regions;

· 10% - 40%, for voluntary Health transfers (e.g., to local clinics);

· 20% - 40%, all other.

Counterpart for States:

· 10% - 20%, for states in SUDAN/SUDENE/CO regions; 20% - 40%, for all other

Toward Improving the Quality of Spending

Strengthened targeting and evaluation mechanisms for public expenditure

(i) Increasing monitoring by CGU internal audit unit is helping improving record on use of FUNDEF and Bolsa Familia resources, especially in small towns;

(ii) SUS transfers follow federal guidelines; despite participation of stakeholders in the process, more accountability and cost/benefit selectivity can be achieved

(iii) Public expenditure on education is among the highest in the world, and FUNDEF has helped increase school enrolment; less rigid, better-monitored transfers might help raise productivity (e.g., more country-wide tests);

(iv) Transfer formulas are set in the Constitution, and are updated using IBGE statistics bureau data; some may be reviewed, rebalancing flows;

• Voluntary Transfers: Federal government can make voluntary transfers only to states and municipalities that comply with their debt obligations, tax payments, transparency requirements, earmarking obligations to Health and Education, as well as LRF limits on debts and personnel expenditure

• Credit: Only those bodies observing debt and other LRF ceilings cancontract new debt. All operations need authorization by the NationalTreasury and to satisfy requirements similar to those applying to transfers

• Guarantees: Federal government can provide guarantees (e.g., for external debt) under conditions similar to those applying to voluntarytransfers

•Note 1: regarding debts and guarantees, Treasury works as an agent of the Senate, as the Constitution requires all credit operation to be approved by the Senate

•Note 2: municipalities are required by LRF to send fiscal data to FIMBRA databank (above90% compliance so far), in addition to publish reports in the internet and newspapers

Enforcing Mechanisms Regarding Transfers and other Financial Flows to State and Municipalities

For more information, visit our web site For more information, visit our web site www.www.tesourotesouro..fazendafazenda..govgov..brbr

The Brazil we all know… and the Brazil we are building

Thank you !

![2006 Brazil Review visit report - Kimberley Process · Minas e Energia (MME) and the Secretaria da Receita Federal (SRF) within the Ministério da Fazenda (MF)] and an implementing](https://img.pdfslide.us/doc/110x75/5c5d0b8d09d3f2e04d8c42e9/2006-brazil-review-visit-report-kimberley-process-minas-e-energia-mme-and.jpg)