Embed Size (px)

Citation preview

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 1 April 2012

Mining, trade and project finance in the current financial crisis

International Nickel Study Group Meetings

24-April- 2012

Lisboa, Portugal

Mariana Abrantes de Sousa

Financial Consultant - PPP Lusofonia

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 2

Presenter background

Mariana ABRANTES de Sousa

• Independent Financial Consultant and PPP Specialist in

advisory, training and evaluation of PPP projects and

programs, and in credit and banking

• Member of the Board and credit committee of Infrastructure

Crisis Facility, AUM €500mln (PIDG/KfW)

• Member of the Supervisory Board of FLO CERT GmbH

• Former Financial Controller in the Ministries of Transport and

Health reporting to the Minister of Finance, Portugal

• Former international banker with ABN AMRO Bank (Portugal),

European Investment Bank and The Chase Manhattan Bank,

in Lisbon, Luxembourg, New York and Mexico City

• Economist with BA -UC Berkeley and MPA - Princeton

University

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 3

Contents The minerals trade cycle and project

finance, expansion and contraction

Testing the limits of diverging trade

performances

Is this financial crisis different

Implications of the international crisis for

- big net exporters

- little net importers, like Portugal

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 4

Some commodity cycles are more

pronounced - Relatively inelastic

supply, marginal

producers

– Pro-cyclical

investment

– Long lead times

- Demand swings,

stockpiling

- High risk, high

reward

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 5

Mining projects benefit

from higher minerals prices and easier credit

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 6

MOMA Titanium Nampula Mozambique

Kenmare Resources

shareholder equity

Kenmare Moma Mining Ltd

Kenmare Moma Processing Ltd

Subordinated debt

EIB and others

Senior debt EIB, AfDB, FMO, KfW

Mineral license

royalties

Environmental

license

EPC contractor – turn-key

lump-sum contract,

dredging, jetty and barge

República de

Moçambique

Insurance

Customers – Off takers

Price - Volume Project Security

MIGA coverage

political risk

Mining of mineral sands and separation

of ilmenite, rutile and zircon. 800 000 t/y

Capex USD 450 mln, 2004, debt USD 270 mln

2001 study, 2004 financing, 2007 first shipment

Reserves,

assayer

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 7

Some mine development project risks

are more intractable than others

• Commodity price risk,

volatiliy (”rising exponentially”…)

• Sales volume risk

• Country, political risk

– Mining license

– Royalties

– Regulation

• Social, stakeholders

risks

• Reputation, governance

• Ore reserves

• Production technology risk

• Implementation, management

risk

• Construction, completion risk

• Infrastrucure transportation risk

• Environmental risks, water

• Financial risks, FX, transfer,

interest rate, funding availability

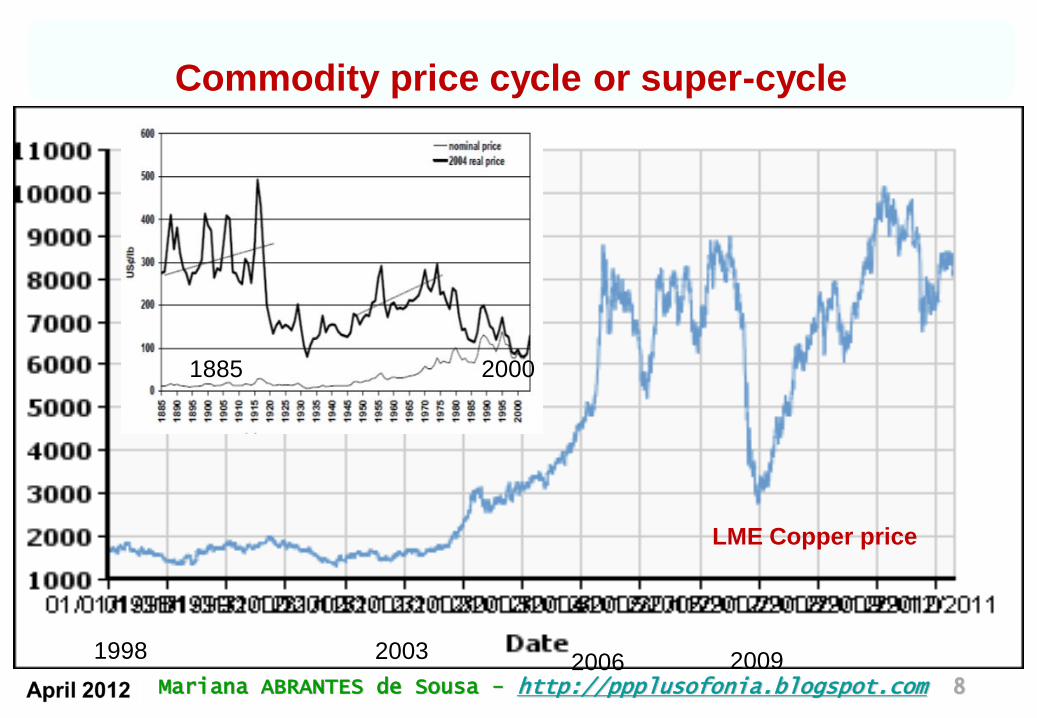

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 8

LME Copper price

1998 2003 2006 2009

Commodity price cycle or super-cycle

1885 2000

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 9 April 2012

Major Chinese mining investments in Africa

(2009)

Source: AUC-UNECA

Building a sustainable future for Africa’s

extractive industry, Dec 2011

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 10 April 2012

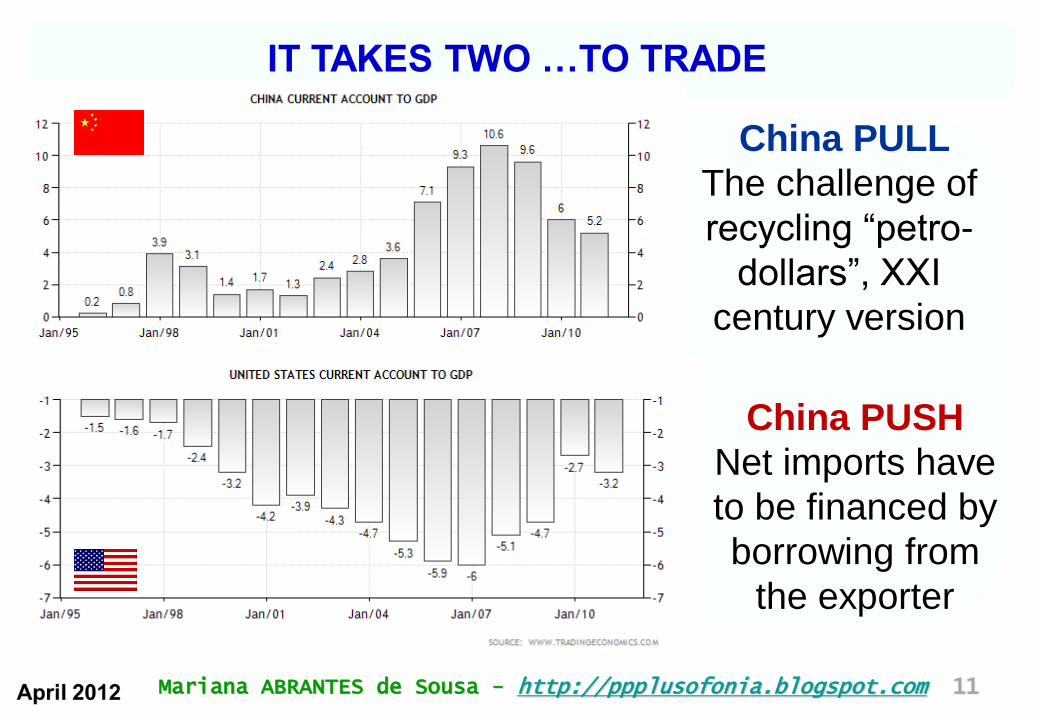

China PULL

China has become

the prime driver

of world mineral

prices

China PUSH

what comes in

must go out

Where do all the metals go

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 11

IT TAKES TWO …TO TRADE

China PUSH

Net imports have

to be financed by

borrowing from

the exporter

China PULL

The challenge of

recycling “petro-

dollars”, XXI

century version

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 12

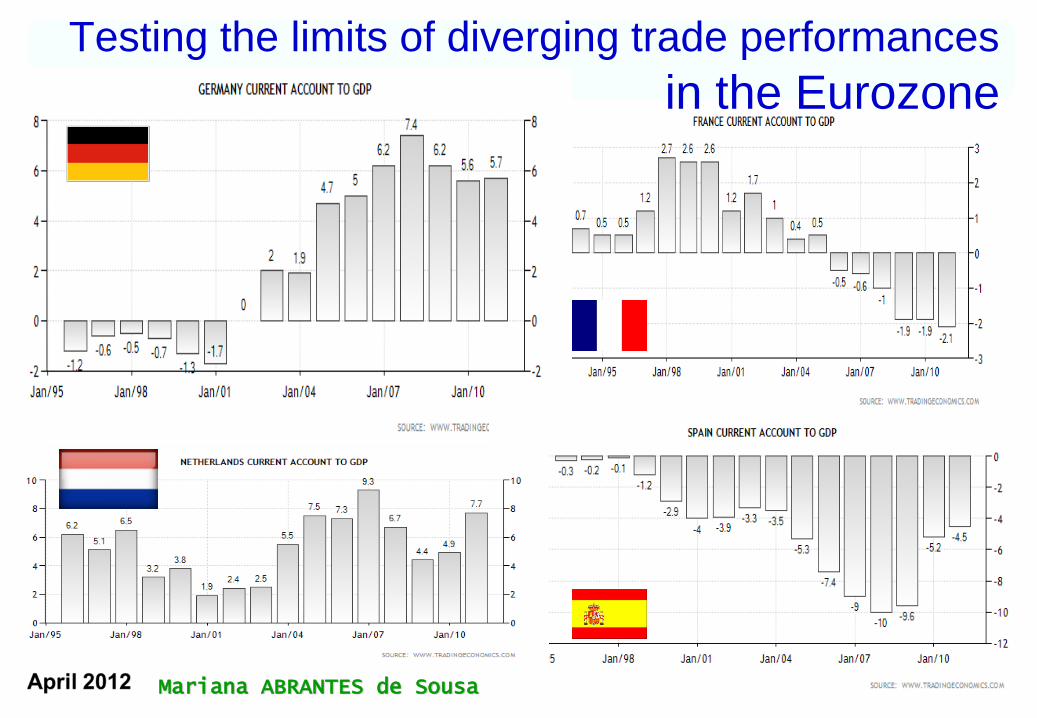

Testing the limits of diverging trade performances

in the Eurozone

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 13

Trade divergence feeds credit booms

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 14

This financial crisis is (not) different Balance-of-Payments imbalances - crisis with

multiple manifestations Sovereign debt crisis, due to excessive external debt

Banking crisis, as banks intermediate and take

excessive credit risks, poor prudential regulation

Growth crisis, economic dislocation due to high import

penetration and shifting trade patterns

• Surplus countries accumulate reserves, which their banks

recycle, overextending credit to the net importing countries,

which become overleveraged with excessive external debt,

leading to sovereign ratings collapse

• High net imports (X-M) become unsustainable provoking

growth recessions, first in net importing countries, and

eventually, in the net exporting countries

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 15

External Debt >>> Public Debt

% GDP

Divida

Pública

Directa

Divida

Externa

Bruta

Divida

Externa

Liquida

Espanha 55% 168% 81%

Irlanda 65% 979% 75%

Portugal 77% 233% 89%

Grecia 113% 168% 81%

Italia 115% 118% 88%

Fonte: R Cabral, www.voxeu.org, 8-Maio-2010

2009

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 16

The B-o-P adjustment will be different One-armed midget economies

External adjustment tools key to

BoP adjustment are missing

o FX policy

o Tariffs and trade policies

o Monetary policy

o Capital controls

Over-reliance on domestic tools

• Fiscal, tax, budget policies

• Incomes policy wage and

pension cuts of 20%+

Some policy tools ignored

• Credit and banking policies

Structural reforms necessary but

not sufficient

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 17

Cumulative challenges for Portugal:

unilateral adjustments will not be enough

Structural Business Financial

• Low returns to

invesment due to poor

investment decisions

and weak X-M, trade

deterioration

• Des-economies of

scale in trade with the

“big boys” (Krugman)

•Persistently high CAB

current account deficit,

propensity to import

• Big cuts in

domestic demand

to get negligible

import reductions

• Shifting stimulus

to export sector

•Low

competitiveness,

weak international

marketing and

sales

• Liquidity shrinking,

credit re-allocation

lagging

• Excessive leverage

• Low bargaining

power with external

creditors

• Low savings and

high dependency of

external funding

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 18

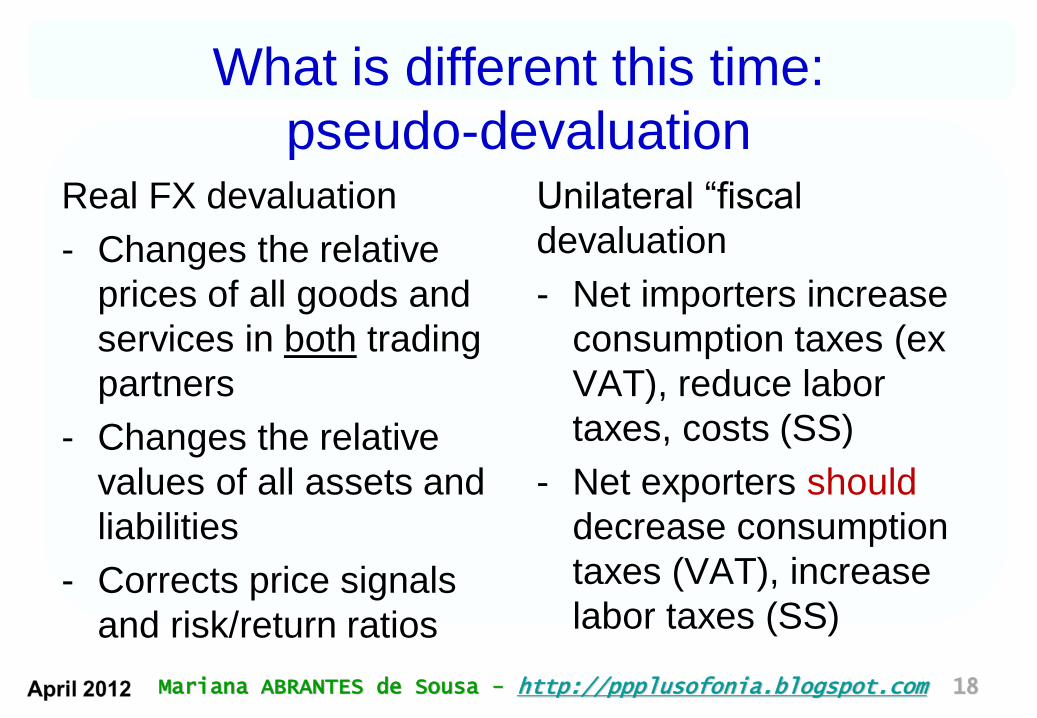

What is different this time:

pseudo-devaluation Real FX devaluation

- Changes the relative

prices of all goods and

services in both trading

partners

- Changes the relative

values of all assets and

liabilities

- Corrects price signals

and risk/return ratios

Unilateral “fiscal

devaluation

- Net importers increase

consumption taxes (ex

VAT), reduce labor

taxes, costs (SS)

- Net exporters should

decrease consumption

taxes (VAT), increase

labor taxes (SS)

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 19

What is different this time:

pseudo sovereign debt workout Real debt workout

- Debt service stand-still

- Borrower undertakes austerity

- Creditor shares sacrifice

- Restructuring with longer

tenors, lower interest rates

- New debt need assured,

revolving export finance

- “Haircut” to reduce external

debt to sustainable levels

- Domestic creditors favoured to

promote local savings

- Banks recapitalized

Debt workout – Eurozone

- Bailout allows shift of exposures

from private to official creditors

- BCE, EFSFacility

- EFSMechanism

- TARGET2 – Central Banks

- Little net debt relief to borrowers

- Emergency funding mostly ST

- No provisions for export finance

- Haircut tripples the threat to

local savers, feeds capital flight

- Banking recapitalization through

low cost official funding

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 20

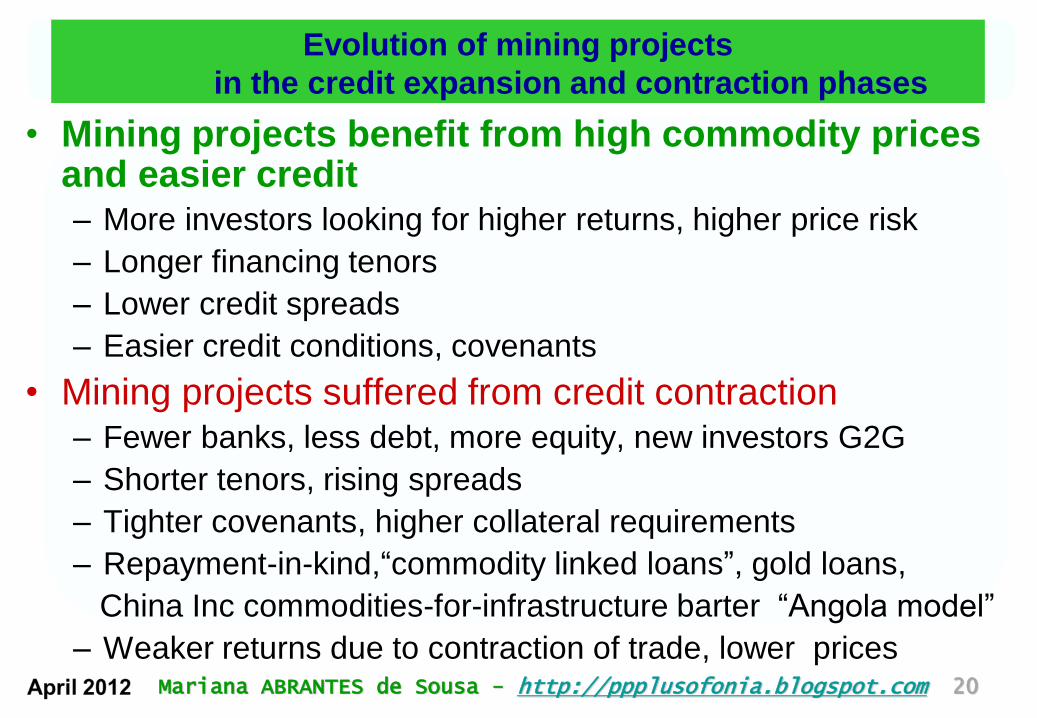

Evolution of mining projects

in the credit expansion and contraction phases

• Mining projects benefit from high commodity prices and easier credit – More investors looking for higher returns, higher price risk

– Longer financing tenors

– Lower credit spreads

– Easier credit conditions, covenants

• Mining projects suffered from credit contraction – Fewer banks, less debt, more equity, new investors G2G

– Shorter tenors, rising spreads

– Tighter covenants, higher collateral requirements

– Repayment-in-kind,“commodity linked loans”, gold loans,

China Inc commodities-for-infrastructure barter “Angola model”

– Weaker returns due to contraction of trade, lower prices

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 21

In conclusion • The mining boom and the excessive Portuguese

external debt are two faces of the same macro

problem:

“unsustainable international trade imbalances”

• Eurozone still “Testing the Limites of Divergence”

• Net importers, big or small, cannot undertake the

whole burden of Balance-of-Payments adjustment

unilaterally; exporters must raise export prices

• The adjustment by net exporters may be delayed,

but is inevitable. Meanwhile, “cash is king”

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 22

“ não há mal que sempre dure

nem bem que nunca acabe”, or

“what goes up must come down”

Obrigada!

Mariana Abrantes de Sousa

PPP Lusofonia, PORTUGAL

http://ppplusofonia.blogspot.com

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 23 23

May 2011 Mariana ABRANTES de Sousa - http://ppplusofonia.blogspot.com 24