Embed Size (px)

Citation preview

Mining Exploration Companies

Understanding Exploration Company Financial Statements

Douglas TaylorWits Business School

Agenda1. Objectives2. Principles3. Financial Statements4. Assumptions & Definitions5. Trends6. Reporting Exploration Results7. Valuation issues8. Flow-through shares9. Additional Information10. Earnings “Management”

Objectives of Financial Statements

• Provide information about the:– Financial position– Performance– Changes in financial position

• Comprise:– Balance sheet– Income statement– Statement of changes in equity– Cash flow statement– Notes

What about ……

• Financial review by management• Environmental reports• Value added statements• Employee reports• CSI reports• SHE reports• BEE information

What about ……

• Project review / Exploration report• Resources statement• Operating review / Management

Discussion and Analysis

Users Information Needs

• Investors: risk and return; buy, hold or sell; ability to pay dividends.

• Employees: stability and profitability; ability to provide remuneration, retirement benefits and employment opportunities

• Public: employment; environment; economy; community

SAMREC CodeMain Principles

• Materiality: all the relevant information required to make a reasoned and balanced judgement regarding results, resources & reserves

• Transparency: clear and unambiguous information

• Competency: the work and responsibility of suitably qualified and experienced persons

• Impartiality: no undue influence; adequate disclosure

Qualitative Characteristics of Financial Statements

• Understandable • Relevant• Reliable• Comparable

• GAAP / IFRS

IFRS 6

• Exploration and evaluation assets to be tested for impairment when the carrying amount of the assets may exceed their recoverable amount.

• Disclose information that identifies and explains the amounts recognised in financial statements arising from the exploration for and evaluation of mineral resources, including – accounting policies – amounts of assets, liabilities, income and expense and

operating and investing cash flows arising from the exploration for and evaluation of mineral resources

How else could this be treated? What is its real value?

Minimal loan funding, if any

Theoretical NAV. Could also be 30,900!

BALANCE SHEETS

ASSETSCurrent Assets

Cash and equivalents 33,900 Accounts receivable 500 Inventory 1,000 Prepaid expenses 500

35,900

Capital assets / Equipment 2,500 Mineral property 135,000 Other long-term assets 100

173,500

LIABILITIES AND SHAREHOLDERS' EQUITYCurrent

Accounts payable and accrued liabilities 1,300 Long-term

Loans and deferred taxation 6,300

Shareholders' EquityShare capital and premium 201,500 Contributed surplus 8,700 Deficit (44,300)

165,900 173,500

STATEMENT OF LOSS / STATEMENT OF OPERATIONS

RevenueInterest and other income (1,300)Foreign exchange profit (1,900)

(3,200)Expenses

Corporate and administration costs 4,200Exploration and development 8,000Foreign exchange lossOther expenses 600Stock-based compensation 3,600Travel 1,100

17,500Operating loss 14,300Capital adjustments (gains) / losses (400)Taxation (2,400)Loss for the year 11,500Deficit, beginning of year 32,800Deficit, end of year 44,300

Arises mostly with SA interested companies

Development stage; impairment

Largely share options - Black Scholes

Deferred

STATEMENT OF CASH FLOW

Operating ActivitiesLoss for the period 11,600Items not involving cash

Amortization and impairment (3,200)Deferred taxation 2,400Stock-based compensation (3,600)Foreign exchange profit (1,900)Capital adjustments (gains) / losses 400

Changes in working capitalAccounts receivable 200Inventory 1,100Prepaid expenses 500Accounts payable and accrued liabilities (600)

Cash used in operating activities 6,900

Investing ActivitiesEquipment acquired 2,300Mineral property acquisitions 14,700Other long-term assets acquired 100

Cash used in investing activities 17,100

Financing ActivitiesShares issued 40,200

Cash from financing activities 40,200

Change in cash and cash equivalents 16,200Cash and equivalents at beginning of year 17,700

Cash and equivalents at end of year 33,900

Where’s it gone to?

Where’s it come from?

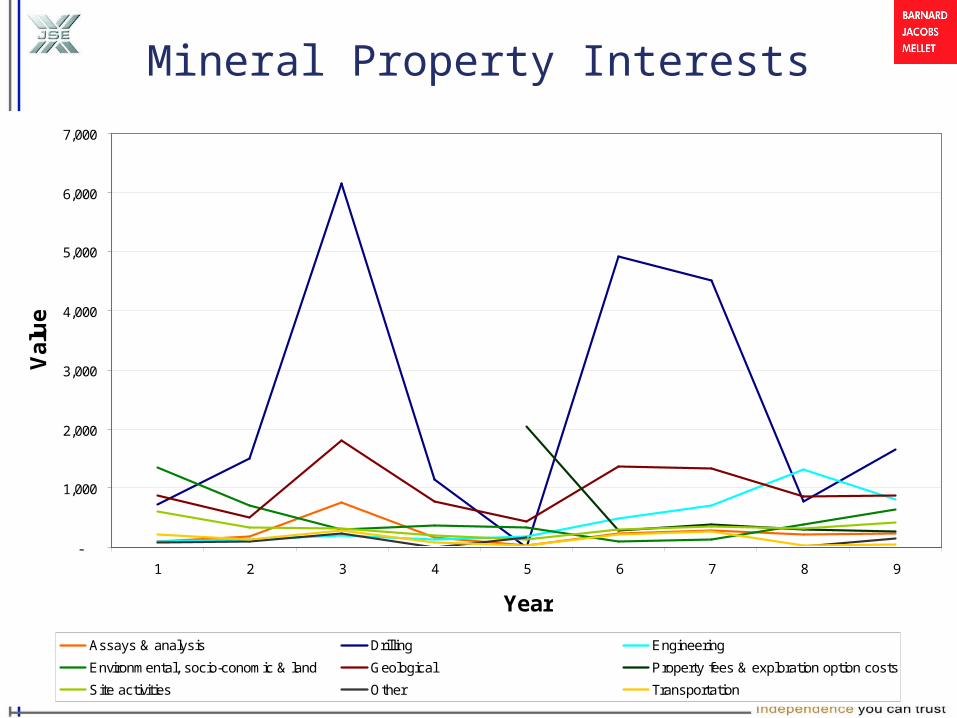

Mineral Property Interests

Assays & analysisAmortizationDrillingEngineeringEnvironmental, socio-conomic & landEquipment rentalGeologicalGraphicsProperty fees & exploration option costsSite activitiesProvision for site reclamationTransportation

Stock based compensation

Cumulative

Caveat• The Company is in the process of exploring its

mineral property interests and has not yet determined whether these properties contain economically recoverable mineral reserves

• The underlying value and the recoverability of the amounts shown for mineral property interests and equipment are entirely dependent upon the existence of economically recoverable mineral reserves and the ability of the company to obtain the necessary financing to complete the exploration and development of the properties

Critical Accounting Estimates• Some estimates:

– the value of mineral resources & reserves– the carrying values of mineral properties,– the carrying values of property, plant & equipment– the valuation of stock-based compensation expense– determination of future income tax assets & liabilities– asset retirement & reclamation obligations

• Actual amounts could differ from the estimates used and, accordingly, affect the results of operations

Mineral Property Interests• Mineral property acquisition costs capitalized on a

property-by-property basis.• Exploration expenditures incurred prior to

determination of feasibility - expensed as incurred• Development expenditures incurred subsequent to

a development decision - capitalized and amortized / impaired over the estimated life of the property

• Mineral property acquisition costs include the cash and/or the fair market value of shares issued

• The amount shown for mineral property interests represents costs incurred to date and accumulated acquisition costs, less write-downs, and does not necessarily reflect present or future values

Stock-based Compensation• Share option plans - record all stock-based

payments using the fair value method.• Stock-based payments measured at the fair

value the equity instruments issued and are charged to operations over the vesting period.

• The offset is credited to contributed surplus.• Consideration received on the exercise of

stock options is recorded as share capital and the related contributed surplus is transferred to share capital.

TIME

Target Generation

• Planning

• Historical data

• Remote sensing

• Geological

Primary Exploration

• Geochemical

• Geophysical

• Trenching

• Drilling

Advanced Exploration

• In-fill drilling

• Geological modeling

• Metallurgical testing

• Pre-feasibility study

Project Development

•Feasibility study

•Geological modeling

• Metallurgical testing

• Mine planning

Mine Construction

• Engineering design

• Build the plant

• Build the mine

• Mine planning details

Development Stages

RISK PROFILE

Target Generation

Primary Exploration

Advanced Exploration

Project development

Operating mines

BALANCE SHEETS

ASSETSCurrent Assets

Cash & equivalents 82% 54% 20% 17%Accounts receivable 1% 1% 1% 1%Inventory 2%

83% 55% 21% 20%

Capital equipment 2%Mineral property 16% 45% 79% 78%

100% 100% 100% 100%

CurrentAccounts payable 1% 4% 1% 2%

Long-term 2% 4%

Shareholders' EquityShare capital & premium 103% 116% 120% 117%Contributed surplus 3% 5%Deficit -4% -20% -26% -28%

99% 96% 97% 94%100% 100% 100% 100%

LIABILITIES AND SHAREHOLDERS' EQUITY

TIME

Mineral Property Interests

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1 2 3 4 5 6 7 8 9

Year

Va

lue

Assays & analysis Drilling Engineering

Environmental, socio-conomic & land Geological Property fees & exploration option costs

Site activities Other Transportation

Reporting of Exploration Results

• Mineral tenement and land tenure status• Exploration done by other parties• Geology• Data aggregation methods• Relationship between mineralisation widths

and intercept lengths• Diagrams• Balanced reporting• Other substantive exploration data• Further work

General Relationship between Exploration Results, Mineral Resources and Ore Reserves

Source: SAMREC

Mineral Resources• Inferred mineral resources: estimated on

limited information; geologically speculative; no certainty that mineral resources will be upgraded to mineral reserves through continued exploration

• Indicated mineral resources: sufficiently well defined to allow geological and grade continuity to be reasonably assumed and assessed

• Mineral resources: not mineral reserves; not demonstrated economic viability; have reasonable prospects for economic extraction

Estimation and reporting of Mineral Resources

• Database integrity.• Geological interpretation.• Dimensions.• Estimation and modelling techniques.• Moisture.• Cut-off parameters.• Mining factors or assumptions.• Metallurgical factors or assumptions.• Bulk density.• Classification.• Audits or reviews.• Discussion of relative accuracy/confidence.

Rough Guide to (Gold) Value

• Early stage; some inferred resources - about 3.5% of gold in the ground

• Later stages; more tangible assets – about 10%

• Early stages of production – value between 15% and 25% of value of ounces in the round

Rough Guide to Value

• Commodity price leverage– Value = PV of future cash flows– Cost to mine $400; gold price $500

value is PV based on $100 margin– Gold price increases 20% to $600 -

margin doubles and value doubles

• Move to option pricing and real options

Rough Guide to Value

• Weighted Average Cost of Capital (WACC)

• Early years = cost of equity• Risk / Return trade-off• NAV or V NA?

Intangibles

• Management track record• How is the money being spent?• Economic reality• How long before the bubble bursts?

It’s the Management, stupid

• Clearly defined objectives & strategies (87%)

• Full disclosure - transparent, open & honest (85%)

• Reputable, honest & trustworthy (82%)• Financially sound & secure (78%)• Chief executive & senior management

always approachable (78%)• Communicates well with the investment

community (69%)Source: Campbell Belman

Flow-Through Shares

• Stimulate exploration & improve access to capital

• Exploration company incurs expenses – tax deduction deemed to flow through to shareholders

• Costs claimed sooner, and at higher rates

Flow-Through Shares

• Advantages for individual investors - receive 100% tax deduction for share investment

• Shown to enhance investment returns

• In the last three years alone, more than $350 million raised through the flow-through share mechanism

Additional Information

• Technical report - Goldstream Mining;; Nickel Australia; Great Basin presentation; Jubilee Platinum; Minotaur Exploration

• Deliberately not commenting on SA Financial Statements – the standards seem high but need a fair review before comment

• Corporate Governance

Earnings Management or Manipulation?

• Revenue – Record future revenues before earned – Defer current revenue – Fictitious

• Expenses – Record future expenses early – Defer current expenses – Don’t record or disclose liabilities

• Non-recurring transactions – Record in operating income – Geography matters (especially when not disclosed) – “Big Bath”

So Who’s Doing It?

• Most companies DO NOT intentionally distort their financial reports

• Warnings – Poor internal controls

Lack of independent directors Competence of external auditor

– Extreme competitive pressure Decelerating real growth Survival in doubt Private companies

– Management’s character in question Greed

• Why?– It pays – It’s easy – It’s unlikely they’ll get caught