Embed Size (px)

Citation preview

MINEAfrica Seminar4th March 2008

2

Disclaimer

This presentation and the information contained herein are not an offer of securities for sale in the United States. This presentation is an advertisement and does not constitute or form part of, and should not be construed as, any offer for sale or subscription of, or solicitation of any offer to buy or subscribe for, any securities of Namakwa Diamonds Limited (“Namakwa” or the “Company”) nor should it or any part of it form the basis of or be relied on in connection with, any contract or commitment whatsoever.

Statements contained within this presentation may contain forward-looking comments, which involve risks and uncertainties that may cause actual results to vary from those contained in the forward-looking statements. In some cases, you can identify such forward-looking statements by terminology such as 'may', 'will', 'could', 'forecasts', 'expects', 'plans', 'anticipates', 'believes', 'estimates', 'predicts', 'potential', or 'continue'. Forward projections reflect management's best estimates based on information available at the time of issue.

This Presentation and its contents are confidential and may not be further distributed or passed onto any other person or published or reproduced, in whole or in part, by any medium or in any form for any purpose.

3

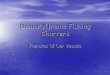

Overview

Namakwa Diamonds Limited / NADIssuer / Ticker

Full listing on London Stock Exchange main boardListing location

Shareholder Base

Expand existing producing mining operations Bring into production selected development projects Pursue further growth and consolidation opportunities Increase beneficiation inventory and expand diamond trading operation Repay existing debt and finance general corporate activities

Use of proceeds

Listing Date December 14, 2007

Founders, Management and Employees retain circa 20% 20 UK Institutional Shareholders 3 Swiss Institutional Shareholders 1 North American Shareholder

Market Cap* £170.51m

Outstanding Shares 116.386m

* as of January 29, 2008

4

Namakwa’s Non-Executive Board

Name Position Roles and Prior Experience

Hans Smith Chairman & Independent Non-Executive Director

Chairman of nomination committee and member of audit committee, remuneration committee and health and safety committee

Previously CEO and Executive Chairman of Iscor and Non-Executive Chairman of Kumba Resources. Served on the board of Western Areas

Thomas Kruger Deputy Chairman & Executive Director

Founder of Namakwa Diamonds 30 years’ experience in South African diamond industry and founding member

of the South African Rough Dealers Association

Edward Haslam Senior Independent Non-Executive Director

Member of audit committee and nomination committee Serves as Chairman of Talvivaara and Non-Executive Director at Aquarius

Platinum (Chairman of remuneration committee and member of audit committee). Previously CEO of Lonmin

John Coulter Independent Non-Executive Director

Chairman of audit committee and member of nomination committee and remuneration committee

Served as CEO of Brait, CEO of JP Morgan South Africa and Chairman of JP Morgan Investment Banking in CEEMA

Currently CEO of Morgan Stanley South Africa and Morgan Stanley Investment Banking in CEEMA

Alex Davidson Independent Non-Executive Director

Member of health & safety committee Serves as Executive President, Exploration and Corporate Development of

Barrick Gold Corporation

Con Fauconnier Independent Non-Executive Director

Chairman of remuneration committee and health & safety committee and member of nomination committee

Previously CEO of Exxaro Resources and CEO of Kumba Resources

Board is committed to be fully UK combined code compliant within 12 months of listing

5

Strong, Experienced Management Team

ApproximateExperience

Prior Experience

Average of almost 20 years experience

Name Position

Corporate

Nico Kruger 10 years CEO Corporate finance and investment banking in diamond related projects

Jean Nel 10 years CFO Corporate finance at Investec Bank and SA resource sector

Jacques Conradie 16 years Financial Manager Financial director of African Portland Industrial Holdings

Mining

Altie Krige 26 years COO Geologist and director of land operations at Trans Hex

Richard Hall 22 years Chief Geologist Exploration manager at De Beers, Namaqualand Mines, considered to be the single biggest alluvial mining operation in the world

Noel Botha 23 years Chief Metallurgist Metallurgical manager at De Beers and Trans Hex

Keith McCulloch 32 years General Manager Mining General mining manager at Trans Hex, experience in Angola

Beneficiation

Tom Kruger 30 years Deputy Chairman & Founder Founding member of the South African Rough Dealers Association with extensive experience in South African rough diamond trading

Heno Kruger 12 years Head of Beneficiation Beneficiation business at Namakwa

Andries Janzen 27 years Head of Cutting & Polishing Managing director at Ochta Diamonds, founded Elite Diamonds in 1980 and currently manages Elite Diamonds

Louis Janzen 6 years Sales of Polished Diamonds Works at Elite Diamonds focusing on acquisition of polished diamonds

Fred Strous 13 years Global Manager: Rough Diamonds Manager of buying stations in the DRC and in Angola for R. Steinmetz & Sons

6

Focus on Large, Gem Quality Fine Diamonds

7

Focus on Large, Gem Quality Fine Diamonds

8

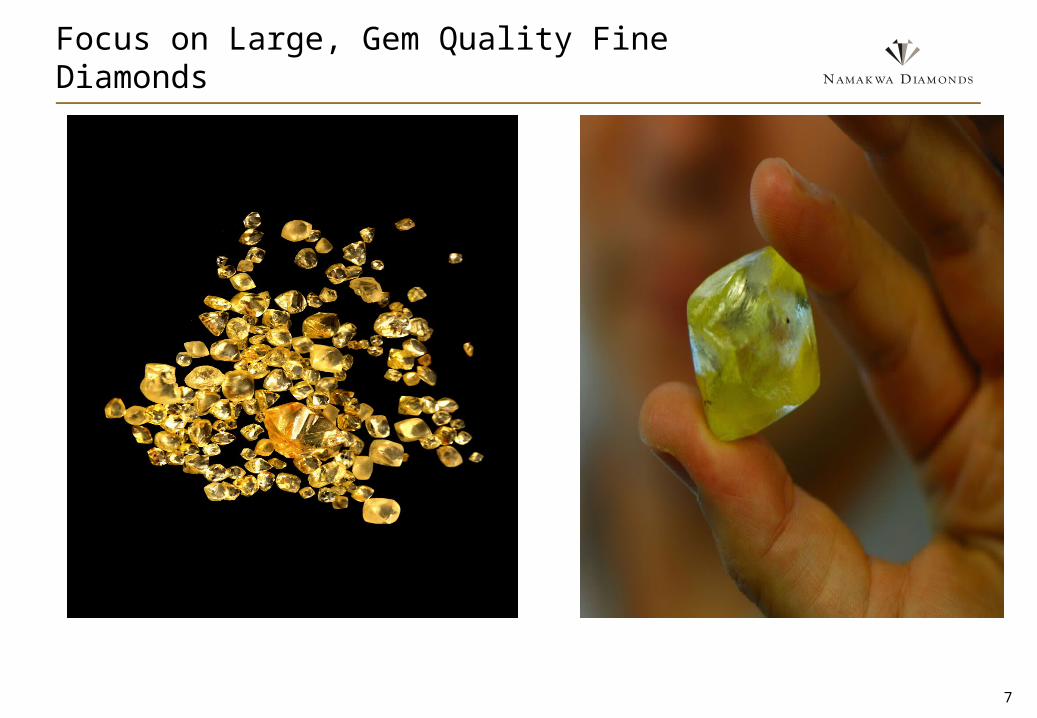

Namakwa’s Consistent Strategy for Growth

Huge opportunities in familiar territories (i.e. North West Province of SA)

BEE adds impetus in SA

Grow in each segment of diamond value chain

Small scale alluvial operations

Long-life mining assets

Beneficiation operations

Vision Summary

Consolidate

Vertical Integration

Gem Quality Focus

Afro-centric

Key differentiator

Increased margins

Trading knowledge adds value across operations

Blends stability with ability to capture opportunities

Direction of integration crucial to success – i.e. beneficiation mining

Focus on mining assets with high quality product, short lead times and favourable capital intensity

Grow beneficiation business

with additional capital

extending retail distribution

Stable and attractive pricing due to strong demand and inconsistent supply

Significant deposits of target stones

Focus on southern Africa – well known and respected family

Commitment to country of origin beneficiation

Well established local presence (30+ years)

9

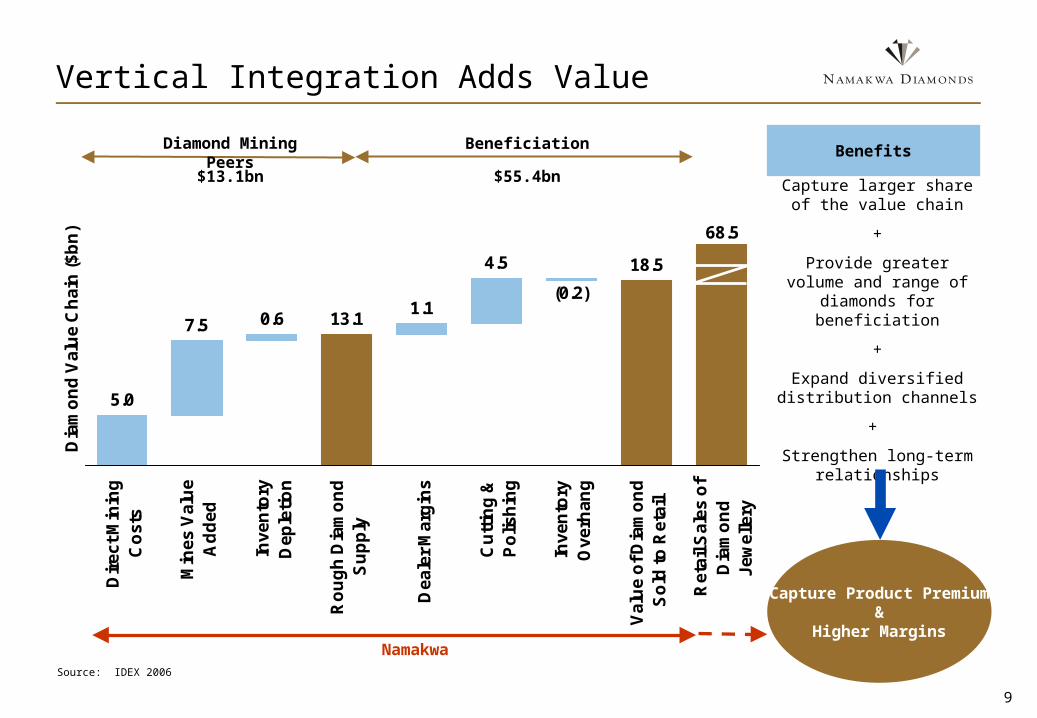

Vertical Integration Adds Value

5.0

7.5 0.6 13.11.1

4.5 18.5

68.5

(0.2)

Dir

ec

t M

inin

gC

os

ts

Min

es

Va

lue

Ad

de

d

Inv

en

tory

De

ple

tio

n

Ro

ug

h D

iam

on

dS

up

ply

De

ale

r M

arg

ins

Cu

ttin

g &

Po

lish

ing

Inv

en

tory

Ov

erh

an

g

Va

lue

of

Dia

mo

nd

So

ld t

o R

eta

il

Re

tail

Sa

les

of

Dia

mo

nd

Je

we

llery

Dia

mo

nd

Va

lue

Ch

ain

($

bn

)

Diamond Mining Peers Beneficiation

Source: IDEX 2006

Benefits

Capture larger share of the value chain

+

Provide greater volume and range of diamonds for

beneficiation

+

Expand diversified distribution channels

+

Strengthen long-term relationships

Capture Product Premium&

Higher MarginsNamakwa

$13.1bn $55.4bn

10

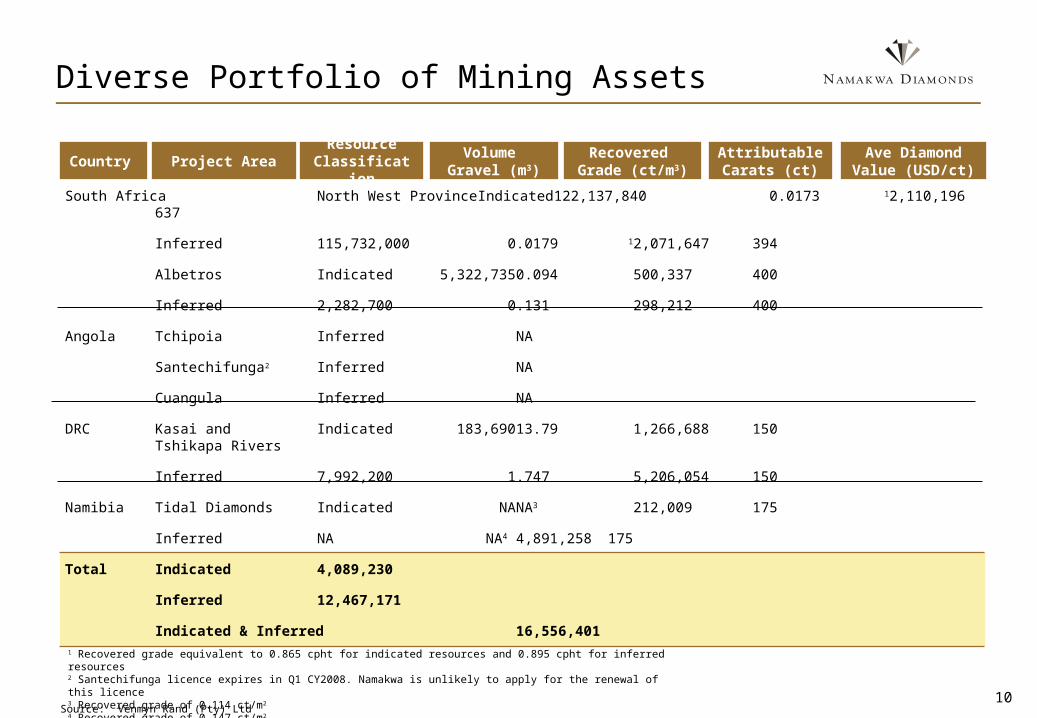

Diverse Portfolio of Mining Assets

South Africa North West Province Indicated 122,137,840 0.01731 2,110,196 637

Inferred 115,732,000 0.01791 2,071,647 394

Albetros Indicated 5,322,735 0.094 500,337 400

Inferred 2,282,700 0.131 298,212 400

Angola Tchipoia Inferred NA

Santechifunga2 Inferred NA

Cuangula Inferred NA

DRC Kasai and Indicated 183,690 13.79 1,266,688 150Tshikapa Rivers

Inferred 7,992,200 1.747 5,206,054 150

Namibia Tidal Diamonds Indicated NA NA3 212,009 175

Inferred NA NA4 4,891,258 175

Total Indicated 4,089,230

Inferred 12,467,171

Indicated & Inferred 16,556,401

Country Project AreaResource

ClassificationVolume

Gravel (m3)Recovered

Grade (ct/m3)Attributable Carats (ct)

Ave Diamond Value (USD/ct)

Source: Venmyn Rand (Pty) Ltd

1 Recovered grade equivalent to 0.865 cpht for indicated resources and 0.895 cpht for inferred resources 2 Santechifunga licence expires in Q1 CY2008. Namakwa is unlikely to apply for the renewal of this licence3 Recovered grade of 0.114 ct/m2

4 Recovered grade of 0.147 ct/m2

11

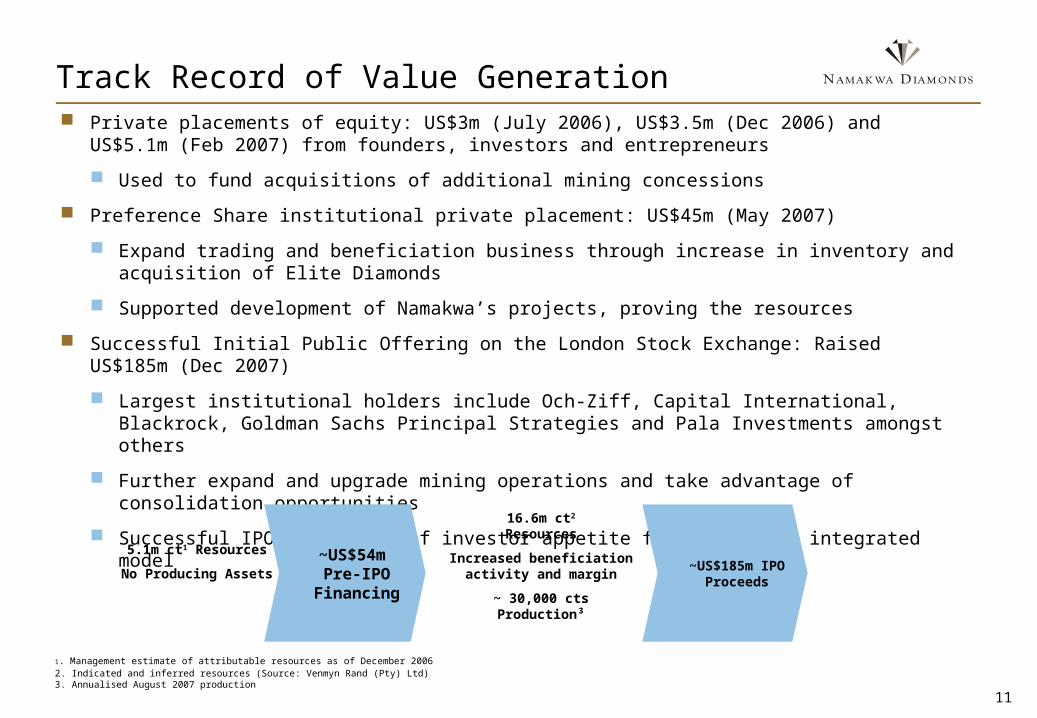

Track Record of Value Generation Private placements of equity: US$3m (July 2006), US$3.5m (Dec 2006) and US$5.1m (Feb 2007) from

founders, investors and entrepreneurs

Used to fund acquisitions of additional mining concessions

Preference Share institutional private placement: US$45m (May 2007)

Expand trading and beneficiation business through increase in inventory and acquisition of Elite Diamonds

Supported development of Namakwa’s projects, proving the resources

Successful Initial Public Offering on the London Stock Exchange: Raised US$185m (Dec 2007)

Largest institutional holders include Och-Ziff, Capital International, Blackrock, Goldman Sachs Principal Strategies and Pala Investments amongst others

Further expand and upgrade mining operations and take advantage of consolidation opportunities

Successful IPO indicative of investor appetite for vertically integrated model

~US$185m IPO Proceeds

~US$54m Pre-IPO

Financing

5.1m ct1 Resources

No Producing Assets

16.6m ct2

Resources

Increased beneficiation activity and margin

~ 30,000 ctsProduction³

1. Management estimate of attributable resources as of December 20062. Indicated and inferred resources (Source: Venmyn Rand (Pty) Ltd)3. Annualised August 2007 production

12

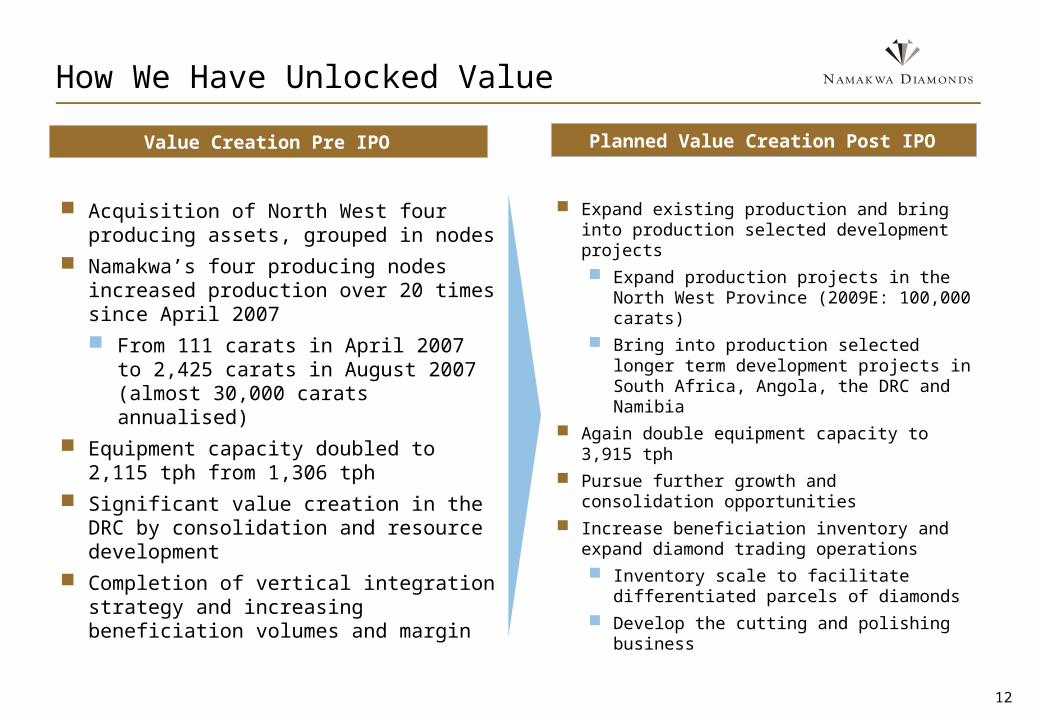

How We Have Unlocked Value

Acquisition of North West four producing assets, grouped in nodes

Namakwa’s four producing nodes increased production over 20 times since April 2007

From 111 carats in April 2007 to 2,425 carats in August 2007 (almost 30,000 carats annualised)

Equipment capacity doubled to 2,115 tph from 1,306 tph

Significant value creation in the DRC by consolidation and resource development

Completion of vertical integration strategy and increasing beneficiation volumes and margin

Expand existing production and bring into production selected development projects

Expand production projects in the North West Province (2009E: 100,000 carats)

Bring into production selected longer term development projects in South Africa, Angola, the DRC and Namibia

Again double equipment capacity to 3,915 tph

Pursue further growth and consolidation opportunities

Increase beneficiation inventory and expand diamond trading operations

Inventory scale to facilitate differentiated parcels of diamonds

Develop the cutting and polishing business

Value Creation Pre IPO Planned Value Creation Post IPO

1. Beneficiation Business Overview2. Mining Business Overview3. Financials and OtherAppendix: Relevant Information

14

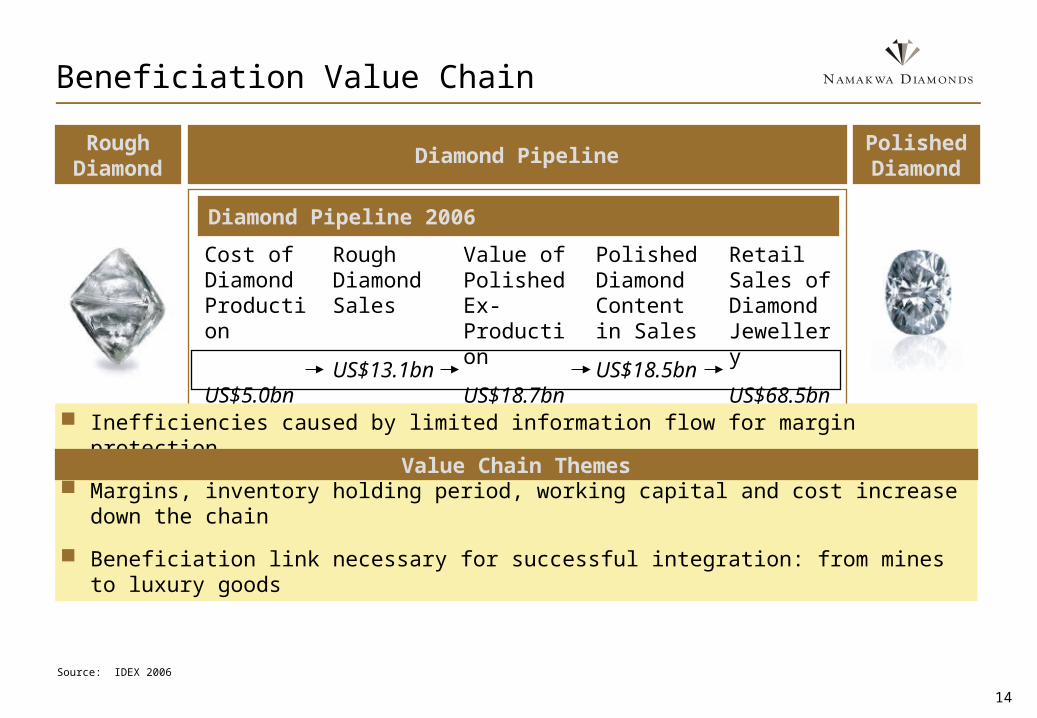

Beneficiation Value Chain

Inefficiencies caused by limited information flow for margin protection

Margins, inventory holding period, working capital and cost increase down the chain

Beneficiation link necessary for successful integration: from mines to luxury goods

Value Chain Themes

Rough Diamond

Polished Diamond

Diamond Pipeline

Diamond Pipeline 2006

Cost ofDiamondProduction

US$5.0bn

RoughDiamondSales

US$13.1bn

Value ofPolishedEx-Production

US$18.7bn

Polished Diamond Content in Sales

US$18.5bn

Retail Sales of Diamond Jewellery

US$68.5bn

Source: IDEX 2006

15

Beneficiation Overview

Diamond value chain margins

Key differentiating factor

Value maximization

RelationshipsProduct

KnowledgeMarket Insight

Distribution Channels

InformationFlow

IncreasedMargins

IndustryIntegration

Diamond Information Chain

16

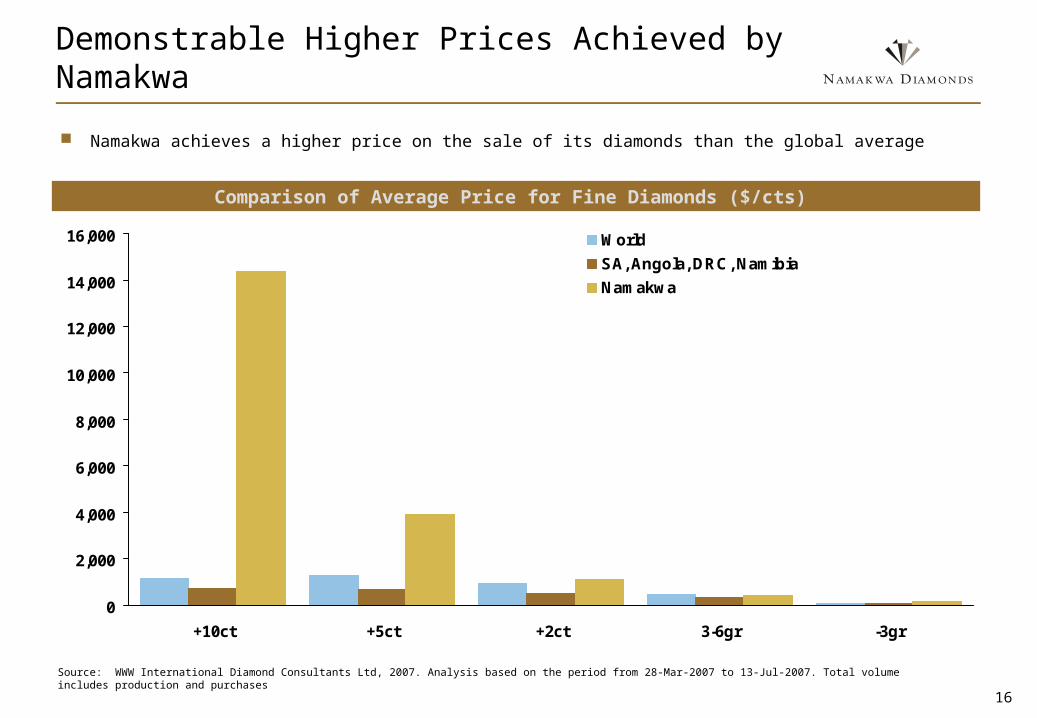

Demonstrable Higher Prices Achieved by Namakwa

Namakwa achieves a higher price on the sale of its diamonds than the global average

Comparison of Average Price for Fine Diamonds ($/cts)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

+10ct +5ct +2ct 3-6gr -3gr

World

SA, Angola, DRC, Namibia

Namakwa

Source: WWW International Diamond Consultants Ltd, 2007. Analysis based on the period from 28-Mar-2007 to 13-Jul-2007. Total volume includes production and purchases

1. Beneficiation Business Overview2. Mining Business Overview3. Financials and OtherAppendix: Relevant Information

18

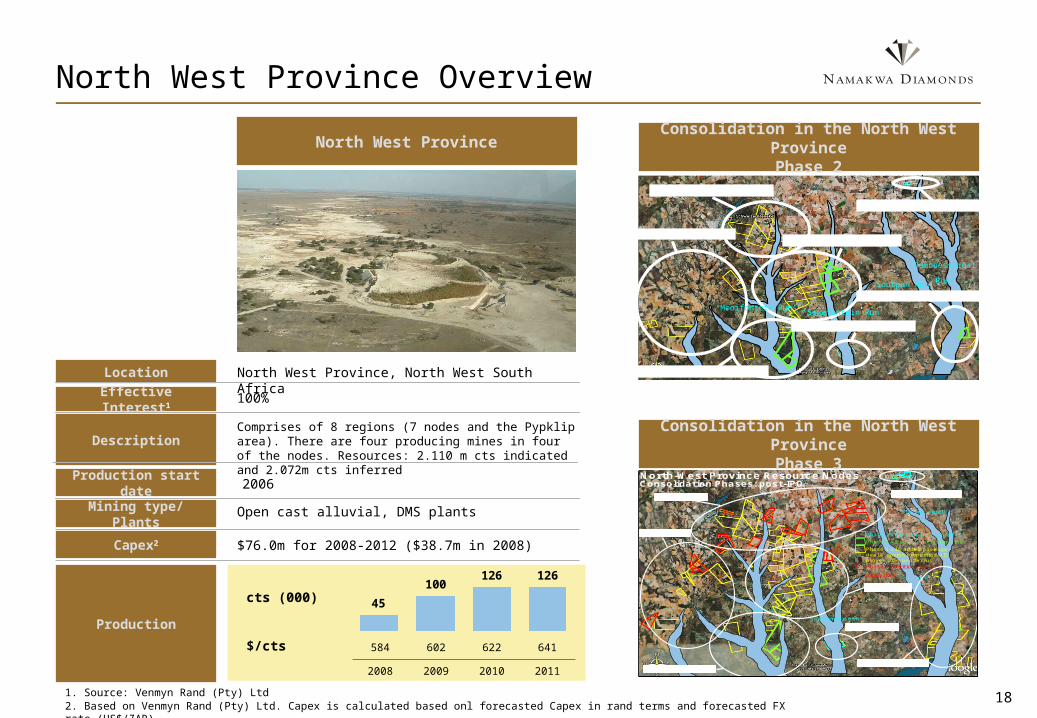

North West Province Overview

Location

Effective Interest1

Description

Production start date

Mining type/ Plants

Capex2

North West Province, North West South Africa

100%

Comprises of 8 regions (7 nodes and the Pypklip area). There are four producing mines in four of the nodes. Resources: 2.110 m cts indicated and 2.072m cts inferred

2006

Open cast alluvial, DMS plants

45

100126 126

cts (000)

$/cts

Production

$76.0m for 2008-2012 ($38.7m in 2008)

584 602 622 641

2008 2009 2010 2011

Consolidation in the North West ProvincePhase 2

North West Province

Consolidation in the North West ProvincePhase 3

‘Bamboesspruit

Run’‘Soutpan Run’

Western-NodeCentral Node

South Western-Node

Northern Node

South-Eastern Node

North-Eastern Node

Southern Node

‘Sewefontein Run’‘Mooifontein Run’

Northern Node

1. Source: Venmyn Rand (Pty) Ltd2. Based on Venmyn Rand (Pty) Ltd. Capex is calculated based onl forecasted Capex in rand terms and forecasted FX rate (US$/ZAR)

South African AssetsNorth-West Province Resource NodesConsolidation Phases: post-IPO

Phase 1-x1 mine plus 1 prospect

Phase 2-x3 addnl. operating mines

Phase 3-x46 addnl. package-deal & option properties-all proven diamondiferousPhase 4-additional option

properties

‘Bamboesspruit

Run’

‘Soutpan Run’

‘Sewefontein Run’

‘Mooifontein Run’

Western-Node

Central Node

South Western-Node

Northern Node

South-Eastern Node

Southern Node

North-Eastern Node

19

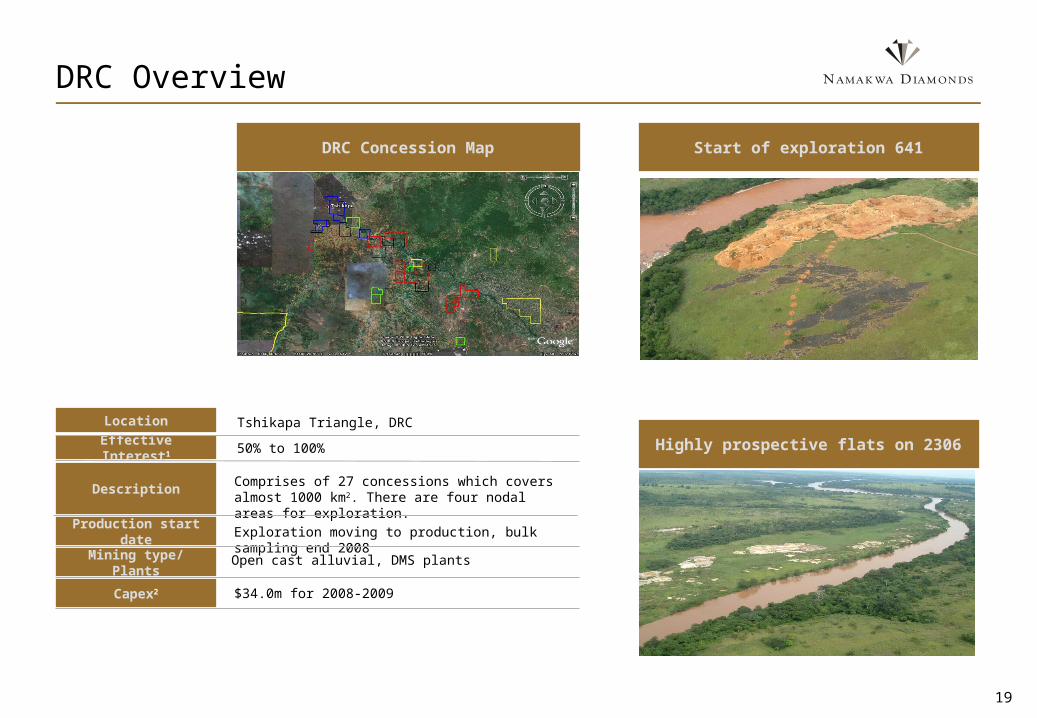

DRC Overview

Tshikapa Triangle, DRC

50% to 100%

Comprises of 27 concessions which covers almost 1000 km2. There are four nodal areas for exploration.

Exploration moving to production, bulk sampling end 2008

Open cast alluvial, DMS plants

$34.0m for 2008-2009

Start of exploration 641DRC Concession Map

Highly prospective flats on 2306

Western-Node

South Western-Node

Northern Node

Location

Effective Interest1

Description

Production start date

Mining type/ Plants

Capex2

20

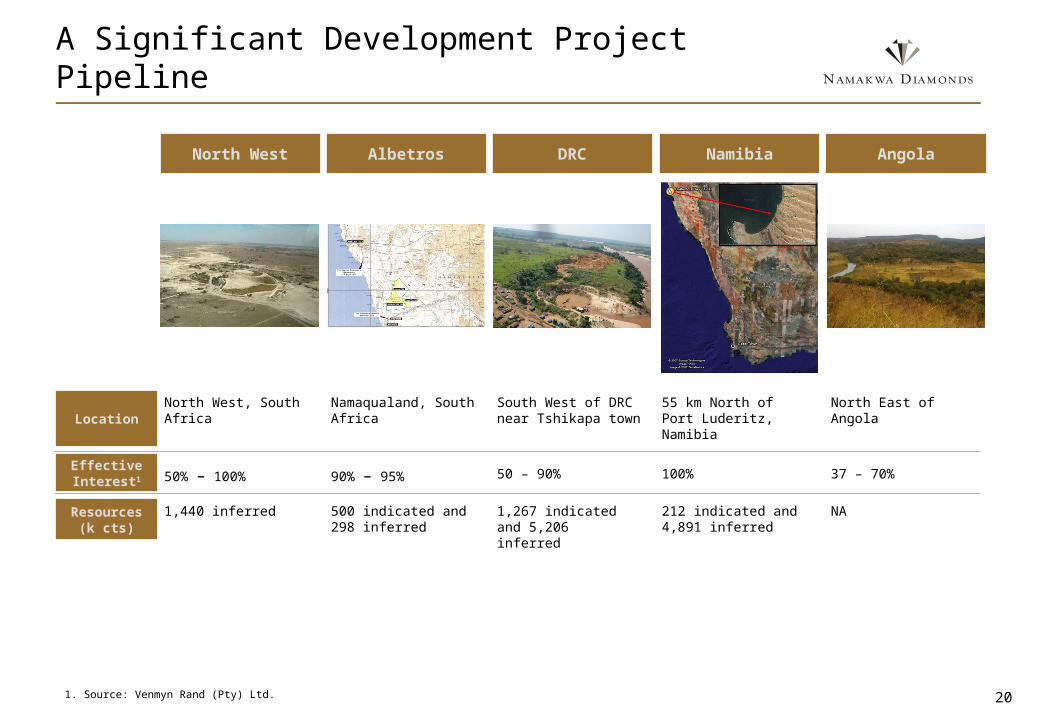

A Significant Development Project Pipeline

North West DRC

Location

Effective Interest1

North West, South Africa South West of DRC near Tshikapa town

50% – 100% 90% – 95%

Albetros Angola

Namaqualand, South Africa

North East of Angola

Namibia

55 km North of Port Luderitz, Namibia

50 – 90% 37 – 70%100%

Resources (k cts)

1,440 inferred 500 indicated and 298 inferred

1,267 indicated and 5,206 inferred

NA212 indicated and 4,891 inferred

1. Source: Venmyn Rand (Pty) Ltd.

21

BEE Considerations

The BEE Requirements require that a New Order Prospecting Right applicant must be at least 26% owned and controlled by historically disadvantaged South Africans (HDSAs)

For New Order Mining Right applications, the applicant must show how it will reach the targets of 15% BEE participation by May 2009 and 26% by May 2014

Namakwa has a registered HDSA trust for the benefit of all HDSA employees which will be the anchor project for all South African mining operations

This structure is currently being implemented with a view of finalisation by 2008

BEE requirements for the beneficiation industry have not yet been determined – once these are clear, Namakwa will implement an appropriate structure

22

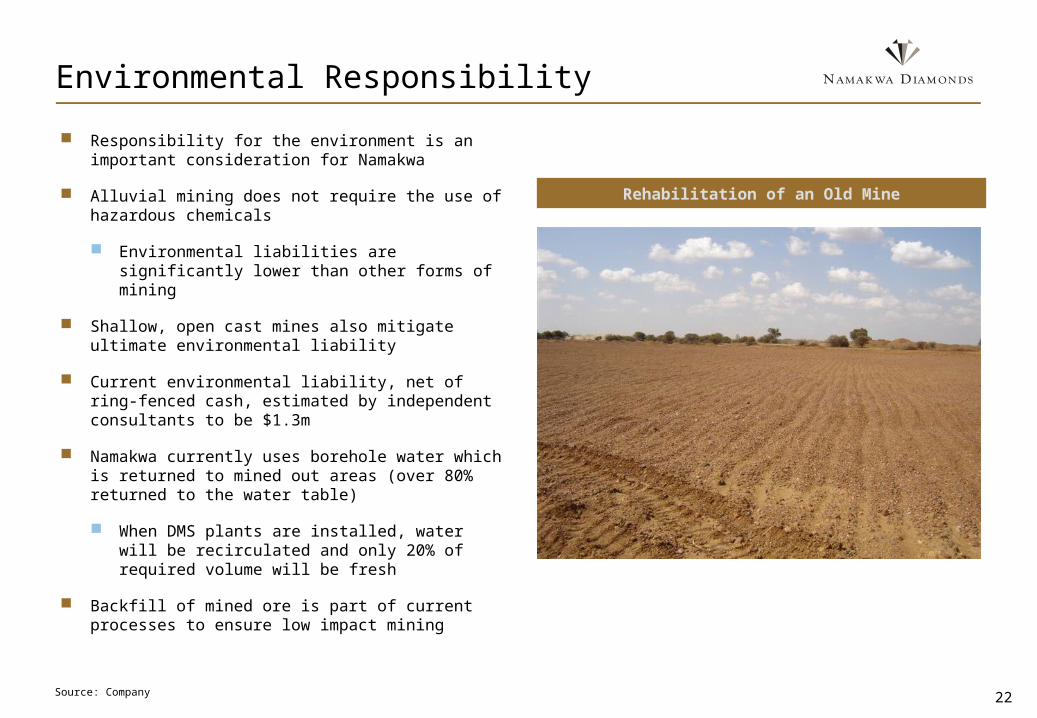

Environmental Responsibility

Responsibility for the environment is an important consideration for Namakwa

Alluvial mining does not require the use of hazardous chemicals

Environmental liabilities are significantly lower than other forms of mining

Shallow, open cast mines also mitigate ultimate environmental liability

Current environmental liability, net of ring-fenced cash, estimated by independent consultants to be $1.3m

Namakwa currently uses borehole water which is returned to mined out areas (over 80% returned to the water table)

When DMS plants are installed, water will be recirculated and only 20% of required volume will be fresh

Backfill of mined ore is part of current processes to ensure low impact mining

Source: Company

Rehabilitation of an Old Mine

1. Beneficiation Business Overview2. Mining Business Overview3. Financials and OtherAppendix: Relevant Information

24

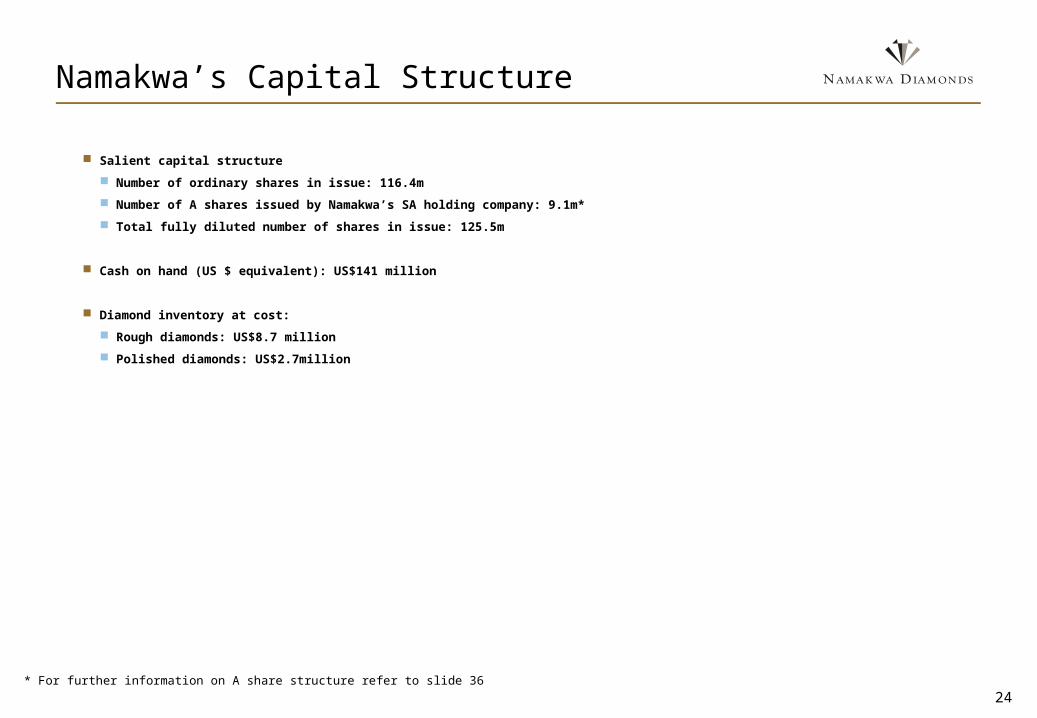

Namakwa’s Capital Structure

Salient capital structure

Number of ordinary shares in issue: 116.4m

Number of A shares issued by Namakwa’s SA holding company: 9.1m*

Total fully diluted number of shares in issue: 125.5m

Cash on hand (US $ equivalent): US$141 million

Diamond inventory at cost:

Rough diamonds: US$8.7 million

Polished diamonds: US$2.7million

* For further information on A share structure refer to slide 36

1. Beneficiation Business Overview2. Mining Business Overview3. Financials and OtherAppendix: Relevant Information

26

Position

26

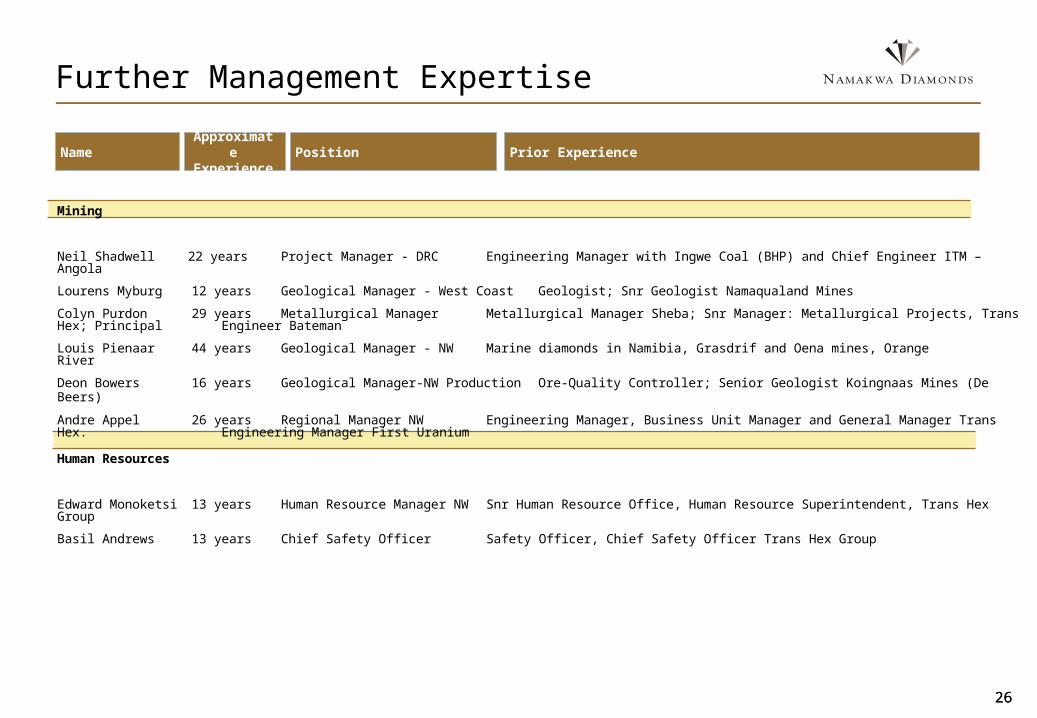

Further Management Expertise

ApproximateExperience

Prior ExperienceName

Mining

Neil Shadwell 22 years Project Manager - DRC Engineering Manager with Ingwe Coal (BHP) and Chief Engineer ITM – Angola

Lourens Myburg 12 years Geological Manager - West Coast Geologist; Snr Geologist Namaqualand Mines

Colyn Purdon 29 years Metallurgical Manager Metallurgical Manager Sheba; Snr Manager: Metallurgical Projects, Trans Hex; Principal Engineer Bateman

Louis Pienaar 44 years Geological Manager - NW Marine diamonds in Namibia, Grasdrif and Oena mines, Orange River

Deon Bowers 16 years Geological Manager-NW Production Ore-Quality Controller; Senior Geologist Koingnaas Mines (De Beers)

Andre Appel 26 years Regional Manager NW Engineering Manager, Business Unit Manager and General Manager Trans Hex.Engineering Manager First Uranium

Human Resources

Edward Monoketsi 13 years Human Resource Manager NW Snr Human Resource Office, Human Resource Superintendent, Trans Hex Group

Basil Andrews 13 years Chief Safety Officer Safety Officer, Chief Safety Officer Trans Hex Group

27

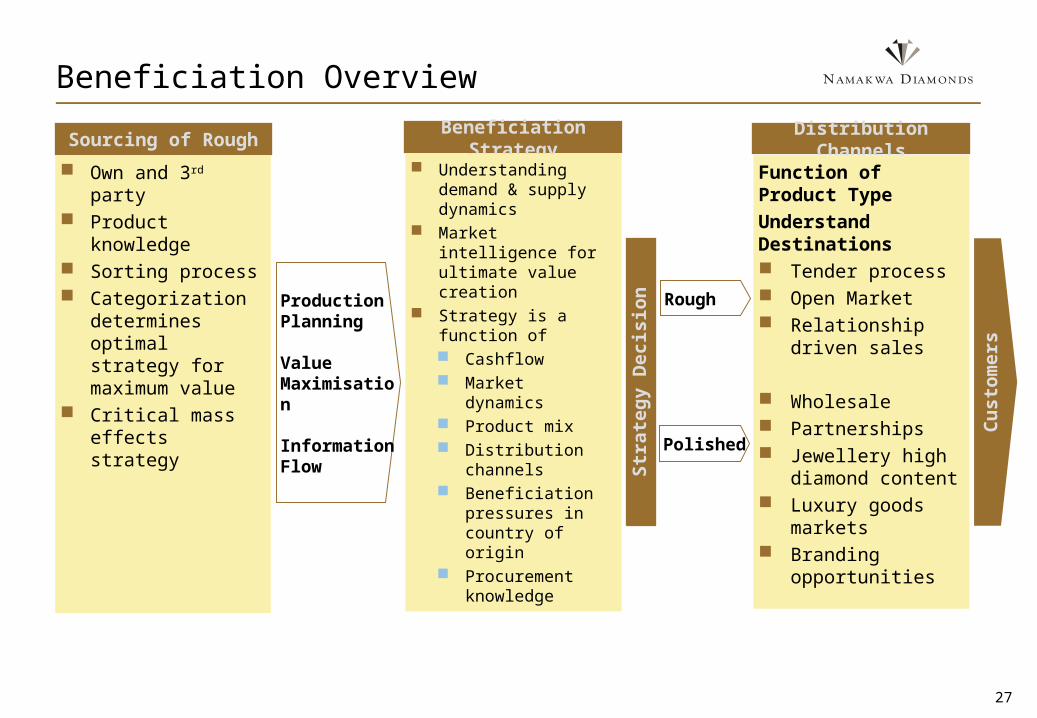

Beneficiation Overview

Sourcing of Rough

Own and 3rd party Product knowledge Sorting process Categorization

determines optimal strategy for maximum value

Critical mass effects strategy

Beneficiation Strategy

Understanding demand & supply dynamics

Market intelligence for ultimate value creation

Strategy is a function of Cashflow Market

dynamics Product mix Distribution

channels Beneficiation

pressures in country of origin

Procurement knowledge

Distribution Channels

Tender process Open Market Relationship driven

sales

Wholesale Partnerships Jewellery high

diamond content Luxury goods

markets Branding

opportunities

Rough

Polished

Production Planning

Value Maximisation

Information Flow S

trat

egy

Dec

isio

n

Cu

sto

mer

s

Function of Product Type

Understand Destinations

28

A share salient terms

Namakwa designed the A share structure to facilitate economic participation in Namakwa by SA shareholders

In terms of South African Exchange Control Regulations South African residents are precluded from owning shares in non-South African companies (save for some exemptions not relevant to Namakwa)

Namakwa’s South African subsidiary, Namakwa Diamond Holdings (Pty) Limited issued 9,05m A shares to SA residents

The A shares mirror the economic benefits accruing to Namakwa ordinary shares save that dividends and any proceeds from a sale are paid in SA in Rands to comply with Exchange Control Regulations

From a valuation perspective Namakwa views the A shares as part of the fully diluted share capital of Namakwa and hence the number of A shares (9,1m) should be added to the ordinary shares of Namakwa (116.4m) for total fully diluted number of shares for valuation purposes (125.5m)