Embed Size (px)

Citation preview

Investor Relations BM&FBOVESPA: MILS3 and OTC-US: MILTY

Mills 2Q14 Results

Mills: Net cash flow becomes positive

Rio de Janeiro, August 6, 2014 – Mills Estruturas e Serviços de Engenharia S.A. (Mills) presented in the second quarter of 2014

(2Q14) growth in net revenues and EBITDA, showing higher gross and EBITDA margins, compared to the same period of last

year. Main highlights of Mills 2Q14 performance:

Rental revenues of R$ 175.7 million, 5.3% higher than the second quarter of 2013 (2Q13).

Net revenue of R$ 213.0 million, 0.6% above 2Q13.

EBITDA(a)

of R$ 105.9 million, an increase of 7.0% in relation to 2Q13.

EBITDA margin of 49.7%, versus 46.7% in 2Q13.

Net earnings of R$ 33.4 million, impacted by R$ 7.1 million in expenses related to the former business unit Industrial

Services. Excluding those, there was a reduction of 15.7% compared to earnings from continuing operations of 2Q13.

Return on invested capital (ROIC)(b)

of 9.2%, or 10.4% excluding non-recurring items, against 14.2% in 2Q13.

Capex(c)

of R$ 54.7 million, of which R$ 48.7 million in rental equipment.

Positive net cash flow(d)

of R$ 10.9 million; first quarter with a positive net cash flow since the IPO.

Issuance of debentures totaling R$ 200 million, with a 5 year term and interest rate of 108.75% of CDI.

Proposal for shareholder remuneration totaling a gross amount of R$ 25.1 million, equivalent to R$ 0.196 per share, to be

paid as interest on equity, subject to approval at Mills’ Shareholders Meeting.

Succession plan announced: Sergio Kariya, current Rental Officer, will assume the position of CEO from January 1, 2015,

when Ramon Vazquez will begin to advise the Board of Directors for five years.

in R$ million 2Q13 1Q14 2Q14 (C)/(A) (C)/(B)

(A) (B) (C) % %

Net revenue 211.8 207.8 213.0 0.6% 2.5%

EBITDA 98.9 107.5 105.9 7.0% -1.5%

EBITDA margin (%) 46.7% 51.7% 49.7%

Earnings from continuing operations 44.6 33.9 33.4 -25.1% -1.4%

Earnings from discontinued operations 3.5 - -

Net earnings 48.1 33.9 33.4 -30.5% -1.4%

ROIC (%) 14.2% 11.5% 9.2%

Capex 150.3 102.3 54.7 -63.6% -46.5%

Invested Capital(e)

1,447.6 1,627.8 1,725.8 19.2% 6.0%

Net rental PP&E 1,023.2 1,163.8 1,189.0 16.2% 2.2%

Others 424.4 464.0 536.8 26.5% 15.7%

Table 1 - Key financial indicators reclassified, for comparison. The financial and operational information presented in this release, except when otherwise indicated, is in accordance with accounting policies adopted in Brazil, which are in accordance with international accounting standards (International Financial Reporting Standards - IFRS).

2 Mills 2Q14 Results

Business perspective

The level of activity in the heavy construction sector remained lower than normal in the first half of 2014 (1H14), with stable

perspective, as indicated by the expected level of activity, according to research conducted by the National Confederation of

Industry (CNI - Confederação Nacional da Indústria), which reached 50.01 points in July 2014.

Investments related to the World Cup totaled R$ 25.6 billion, of which 83.6% from public resources. Only 26% of urban mobility

construction projects were concluded, according to the Brazilian Ministry of Planning (Ministério do Planejamento), 31% are

partially under operation, and 43% still being executed, such as the Light Rail Vehicle in Cuiabá.

BNDES (Banco Nacional de Desenvolvimento Econômico e Social) disbursements for infrastructure totaled R$ 21.6 billion in

the first four months of 2014, equal to 48% year-over-year (yoy) growth. According to BNDES, ministries and sectors’ agencies,

concessions will account for R$ 300 billion in investments between 2015 and 2017 in infrastructure, allowing for a 40% increase

in annual investments – from R$ 74.0 million in 2013 to R$ 104.0 million in 2017.

We believe that the transfer of infrastructure investments to the private sector will contribute with (i) an expansion in the level of

investments in Brazil, (ii) increased pace of construction execution, and (iii) a greater appreciation of engineering solutions that

bring productivity gains through cost or project term reduction.

In the residential construction market, the balance of housing credit in May 2014 was 30% higher than the same period of 2013,

according to the Brazilian Central Bank (Bacen). Even though the activity level is below normal, real estate companies believe

there will be market improvement, as indicated by the index for expected level of activity, which reached 53.31 points in July

2014, according to a CNI study. According to consulting company Criactive, there was an increase of 13.5% in constructed

square meters in 1H14, compared to the first half of 2013 (1H13) and it is estimated that the total value of 2014 will be about 5%

higher than in 2013. New building announced by the listed real estate2 companies presented yoy growth of 13.9% in 1H14, but

sales fell by 8.5% in the same period.

Regarding the market for motorized access equipment, 3,000 new machines entered the Brazilian market in 1H14, an increase

of 11% compared to the end of 2013, bringing the fleet to a total of 32,800 aerial work platforms and telescopic handlers in

Brazil. The main driver for market growth is the penetration of the use of this equipment, by replacing less safe and less

productive access methods.

Revenue

Net revenue reached R$ 213.0 million in 2Q14, 2.5% higher quarter-over-quarter (qoq), but in line with the same period of 2013,

since the growth of R$ 8.8 million in rental revenues was offset by a decrease in other revenue items.

Sales revenues registered a higher expansion between quarters, R$ 8.7 million, while rental revenues decreased slightly,

impacted by slower activity in the Rental spot market, due to the higher number of holidays and the World Cup.

Costs and Expenses

The cost of goods and services sold (COGS), excluding depreciation, totaled R$ 51.5 million in 2Q14, with a 11.0% yoy

reduction, due to lower sales costs and material expenses, allowing for gross margin expansion, excluding depreciation, from

72.6% to 75.8%.

Excluding sales costs, there was a qoq increase of R$ 2.9 million, or 8.6%, of COGS, impacted by increased maintenance

activity in the Rental and Heavy Construction business units.

1 Values above 50 indicate a prospect of growth of activity in the sector for the next six months.

2 Cyrela, Direcional, Even, Eztec, Gafisa, Helbor, MRV, PDG and Rodobens.

3 Mills 2Q14 Results

General, administrative and operating expenses (G&A), excluding depreciation, totaled R$ 55.6 million3 in 2Q14, remaining

stable between quarters.

EBITDA

Cash generation, as measured by EBITDA, reached R$ 105.9 million in 2Q14, 7.0% higher yoy and in line with the amount

registered in the previous quarter. The accumulated EBITDA in the last twelve months ended June 30, 2014, LTM EBITDA,

totaled R$ 421.9 million. The EBITDA margin was 49.7% in 2Q14, against 46.7% in 2Q13 and 51.7% in the first quarter of 2014

(1Q14).

Non-recurring items

In 2Q14, there were non-recurring items related to the former Industrial Services business unit, sold in 2013, with a negative net

effect of R$ 4.2 million, due to the recognition of indemnity in this quarter, related to events that happened before the completion

of the sale.

Net Earnings

Net earnings totaled R$ 33.4 million in 2Q14, in line with the previous quarter. Excluding the effects of the non-recurring items

mentioned above, net earnings would have totaled R$ 37.6 million, 10.9% higher qoq. Tax benefit for the recognition of interest

on capital (JCP) payment more than offset the reduction in EBITDA (R$ 1.5 million) and the increase in depreciation (R$ 2.5

million) and in the negative net financial result (R$ 1.9 million). The net financial result was a negative R$ 18.4 million in 2Q14,

against a negative R$ 16.5 million in 1Q14, due to increased net debt.

ROIC

ROIC was 9.2%4 in 2Q14, or 10.4% excluding non-recurring items, against 11.5% in 1Q14, negatively impacted, primarily by

lower utilization in Rental and higher maintenance activity in the Heavy Construction and Rental business units.

Debt indicators

Mills’ total debt was R$ 748.4 million as of June 30, 2014. At the end of 2Q14 our net debt(f)

position was R$ 654.7 million,

versus R$ 626.6 million at the end of 1Q14.

Our debt is 21% short-term and 79% long-term, with an average maturity of 2.9 years, at an average cost of CDI+0.79%. In

terms of currency, 100% of Mills’ debt is in Brazilian reais.

This quarter, we raised R$ 200 million through our third issuance of non-convertible debentures, with a maturity of five years

and interest rate equal to 108.75% of CDI (interbank interest rate). The net proceeds from the offering were used for the

redemption of promissory notes of the Company, in the same amount, issued on April 2014, which were used to (i) finance the

investment in rental equipment; (ii) pay existing debt and for (iii) general corporate purposes and expenses of the Company.

Our leverage, as measured by the net debt/LTM EBITDA, was at 1.6x as of June 30, 2014. The total debt/enterprise value(g)

was 18.8%, while interest coverage, as measured by the LTM EBITDA/LTM interest payments, was 7.3x.

We believe that, as our investment matures, our operating cash flow will increase and, as a result, our leverage will return to a

level close to its target of 1.0x at the end of 2014. In this quarter, the cash flow generated by operations was above the level of

necessary investments, with a net balance of R$ 10.9 million.

3 G&A which is the sum of Rental, Heavy Construction and Real Estate business units, excluding the effects described in the “Non-recurring items” section.

4 Calculated using theoretical income tax of 30%, therefore not affected by the recognition of interest on equity payment.

4 Mills 2Q14 Results

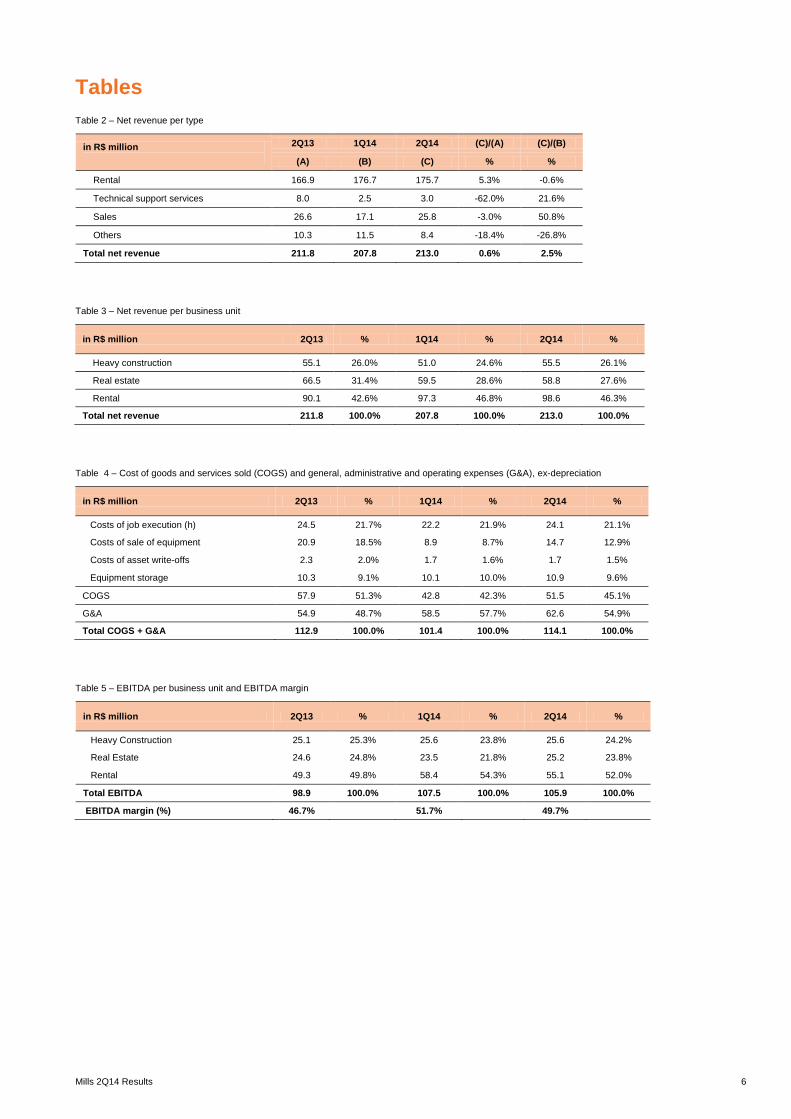

Capex

Mills invested R$ 54.7 million in 2Q14, of which R$ 48.7 million in rental equipment. The Rental business unit was responsible

for 53.9% of the investments, Heavy Construction for 21.0% and Real Estate for 17.2%.

Subject to the pace of development of the motorized access equipment market and of the process to open new Rental branches

in the following months, we may take advantage of the existing fleet to equip these new branches; which would reduce the

amount of investments for this year.

Performance of the business units

Heavy Construction

Net revenue of Heavy Construction totaled R$ 55.5 million in 2Q14, with an 8.8% qoq increase and in line with the same quarter

of the previous year. Rental revenue amounted to R$ 45.9 million, an expansion of 11.8% yoy and 4.8% qoq.

In 1H14 there were several construction projects in the mobilization stage, such as the Vale’s project S11D, Belo Monte

hydroelectric power plant, north beltway, and São Paulo, Rio de Janeiro and Salvador subway lines, and also in the

demobilization stage, such as the airports, Jirau hydroelectric power plant and BRT Transcarioca, which led to higher than

normal turnover of equipment, resulting in lower utilization rate and higher maintenance activity in the period.

In this quarter we signed important new contracts, including Comperj-Reduc pipeline, in Rio de Janeiro; new stretches in the

transposition of the São Francisco river, in the Transnordestina and Leste-Oeste railways, and in the Belo Monte hydroelectric

power plant; new stretches of subway line 5, Gold and Silver monorail lines and north beltway, cable-stayed bridge in Salto, in

São Paulo; Vale and CSN projects, in Minas Gerais; and Ambev factory, in Paraná.

For the north beltway, we signed contracts to launch nearly 1,300 beams, approximately 90% of the total construction work, and

also the supply of formwork, shoring and access. We started mobilizing equipment in June, with estimated execution time of 25

months.

In this quarter we sold equipment to Lauca hydroelectric power plant, in Angola, and to Sir Solomon Hochoy highway, in

Trinidad & Tobago, doubling sales revenue between quarters.

The new equipment lifting cart is already being employed in construction work of the Laguna Bridge in Santa Catarina.

The main projects of 2Q14, in terms of revenue were:

South and Southeastern regions: Comperj complex, Olympic Park, BRT Transcarioca, Metropolitan Arch and subway line 4,

in Rio de Janeiro; Guarulhos and Viracopos airports, Gold and Silver monorail lines, north beltway and Jacu-Pêssego road

complex, in São Paulo; Vale and CSN projects, and Belo Horizonte BRT, in Minas Gerais; and the expansion of a pulp plant,

in Rio Grande do Sul.

Midwest, North and Northeastern regions: the Belo Monte, Colíder, Jirau and Teles Pires hydroelectric plants; the Norte-Sul

railway; Brasília airport, in the Federal District; the Abreu e Lima refinery, in Pernambuco; transposition of the São Francisco

river; the Paraguaçu shipyard and an acrylic industrial pole, in Bahia; the Companhia Siderúrgica do Pecém steel mill, in

Ceará; Vale projects, in Pará and in Maranhão; and the Cuiabá light rail, in Mato Grosso.

COGS was in line with the same period of the previous year. There was a qoq expansion of R$ 4.1 million in COGS due to

higher: (i) sales volume, which accounted for 34% of the increase; (ii) formwork maintenance activity, resulting in additional

expenses with material (28%) and personnel (12%); and (iii) employment of freight to transfer the equipment from the Southeast

to the North and Northeast (10%). The maintenance cost was stable yoy, remaining in the historical range of 15% to 20% of

rental revenues. G&A remained stable yoy and qoq.

5 Mills 2Q14 Results

EBITDA amounted to R$ 25.6 million in 2Q14, with 2.3% yoy growth. The EBITDA margin was 46.2%, versus 45.5% in 2Q13,

while ROIC was 12.5%, against 17.8% in 2Q13, mainly impacted by lower operational income, as a result of increased

depreciation and lower utilization rate in the period.

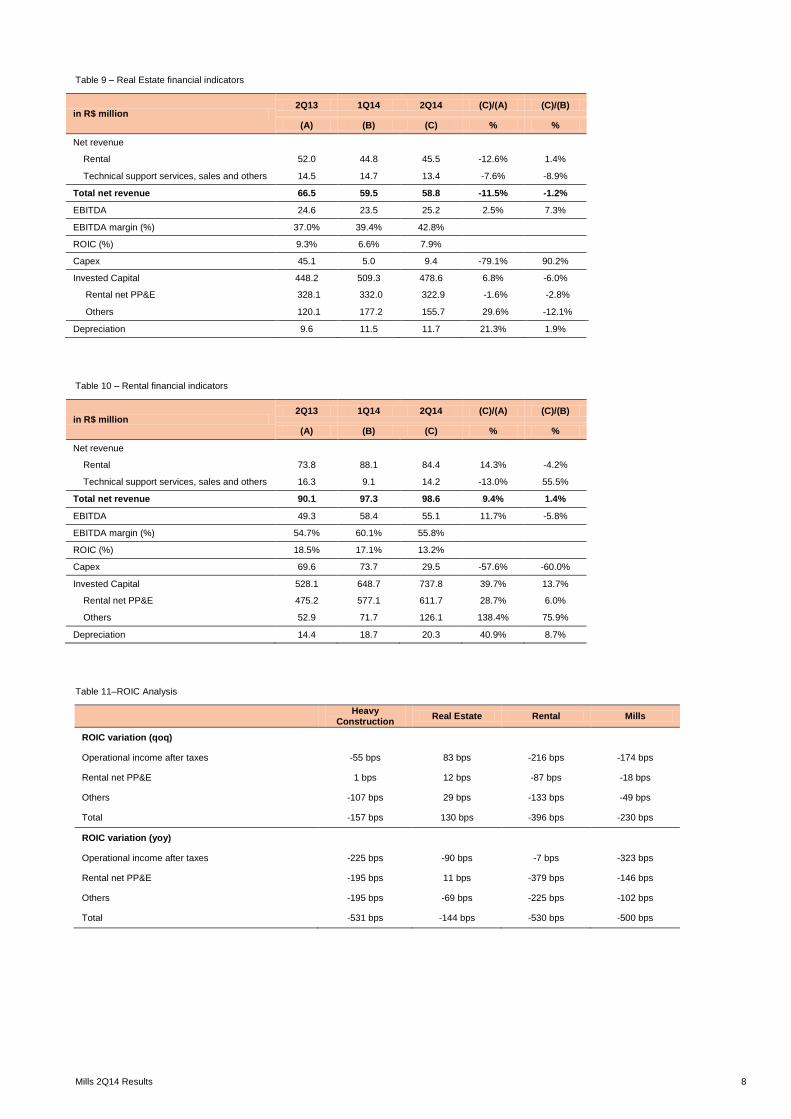

Real Estate

Net revenue for Real Estate totaled R$ 58.8 million in 2Q14, in line with 1Q14 and 11.5% lower yoy. Rental revenue presented

a slight qoq increase and yoy decrease of 12.6%, due to a utilization rate still low.

We are participating in a residential project in Rio Grande do Sul, with 23 towers of 21 floors each, using our flying table for

execution of each 600m² floor in five days, for eleven towers, a reduction up to 50% of the labor work compared to the

conventional system.

There was a yoy reduction in COGS due to lower sales costs, accounting for 68% of the reduction, maintenance activity (15%)

and freight expenses (11%), enabling expansion of gross margin. There was small qoq increase in COGS due to higher sales

volume. There was a reduction in G&A yoy and qoq.

EBITDA reached R$ 25.2 million in 2Q14, a 2.5% yoy growth, returning to the historical level of profitability, with an EBTIDA

margin of 42.8%. ROIC was 7.9%, with improvement qoq, due to higher operating profit.

Rental

The net revenue of Rental amounted to R$ 98.6 million in 2Q14, a new quarterly record, with 9.4% yoy growth and stable qoq

numbers. Rental revenue reached R$ 84.4 million, with an increase of 14.3% yoy, but a 4.2% qoq decrease, negatively

impacted by the several holidays and World Cup event which caused a decline in the motorized access equipment rental spot

market, with maturities below 28 days. Therefore the utilization rate remained below normal level.

Revenue from sales, technical assistance, and others increased R$ 5.1 million qoq, offsetting the reduction in equipment rental

revenue. We delivered to the Belo Monte consortium platforms of the model ZX-135, one of the biggest in the world, which can

reach 43 meters high, increasing productivity and offering safety for the operators to work in the construction and assembling of

18 turbines of the hydroelectric power plant, which will be the third largest in the world.

This quarter we opened two new branches: one at Três Lagoas, in Mato Grosso do Sul, and another at Belém, in Pará, totaling

28 branches in the Rental business unit.

There was a qoq increase of R$ 4.1 million in COGS, due to higher cost of sales, which accounted for 79% of the increase, and

higher maintenance activity, resulting in higher expenses with material (16%) and personnel (15%). G&A remained stable qoq.

EBITDA reached R$ 55.1 million in 2Q14, with 11.7% yoy growth. EBITDA margin was 55.8%, versus 54.7% in 2Q13, while

ROIC was 13.2%, versus 18.5% in 2Q13, negatively impacted by lower utilization rate.

Teleconference and Webcast

Date: Thursday, August 7, 2014

Time: 11:00 (Brasília time)

Teleconference: +1 786 924-6977 (Dial-in) or +1 888 700-0802 (Toll-free); Code: Mills

Replay: +55 11 3193-1012 or +55 11 2820-4012, Code: 7234428# or www.mills.com.br/ri

Webcast: www.mills.com.br/ri

6 Mills 2Q14 Results

Tables

Table 2 – Net revenue per type

in R$ million

2Q13 1Q14 2Q14 (C)/(A) (C)/(B)

(A) (B) (C) % %

Rental 166.9 176.7 175.7 5.3% -0.6%

Technical support services 8.0 2.5 3.0 -62.0% 21.6%

Sales 26.6 17.1 25.8 -3.0% 50.8%

Others 10.3 11.5 8.4 -18.4% -26.8%

Total net revenue 211.8 207.8 213.0 0.6% 2.5%

Table 3 – Net revenue per business unit

in R$ million 2Q13 % 1Q14 % 2Q14 %

Heavy construction 55.1 26.0% 51.0 24.6% 55.5 26.1%

Real estate 66.5 31.4% 59.5 28.6% 58.8 27.6%

Rental 90.1 42.6% 97.3 46.8% 98.6 46.3%

Total net revenue 211.8 100.0% 207.8 100.0% 213.0 100.0%

Table 4 – Cost of goods and services sold (COGS) and general, administrative and operating expenses (G&A), ex-depreciation

in R$ million 2Q13 % 1Q14 % 2Q14 %

Costs of job execution (h) 24.5 21.7% 22.2 21.9% 24.1 21.1%

Costs of sale of equipment 20.9 18.5% 8.9 8.7% 14.7 12.9%

Costs of asset write-offs 2.3 2.0% 1.7 1.6% 1.7 1.5%

Equipment storage 10.3 9.1% 10.1 10.0% 10.9 9.6%

COGS 57.9 51.3% 42.8 42.3% 51.5 45.1%

G&A 54.9 48.7% 58.5 57.7% 62.6 54.9%

Total COGS + G&A 112.9 100.0% 101.4 100.0% 114.1 100.0%

Table 5 – EBITDA per business unit and EBITDA margin

in R$ million 2Q13 % 1Q14 % 2Q14 %

Heavy Construction 25.1 25.3% 25.6 23.8% 25.6 24.2%

Real Estate 24.6 24.8% 23.5 21.8% 25.2 23.8%

Rental 49.3 49.8% 58.4 54.3% 55.1 52.0%

Total EBITDA 98.9 100.0% 107.5 100.0% 105.9 100.0%

EBITDA margin (%) 46.7% 51.7% 49.7%

7 Mills 2Q14 Results

Table 6 – Reconciliation of EBITDA

in R$ million

2Q13 1Q14 2Q14 (C)/(A) (C)/(B)

(A) (B) (C) % %

Results of continuing operations 44.6 33.9 33.4 -25.1% -1.4%

Financial result -11.8 -16.5 -18.4 56.1% 11.2%

Income tax and social contribution expenses -11.3 -16.5 -5.0 -56.1% -69.8%

Operational Results before Financial Result 67.7 66.9 56.8 -16.1% -15.1%

Depreciation 31.3 39.6 42.1 34.5% 6.3%

Expenses (revenues) related to the Industrial services former business unit

- 1.1 7.1

EBITDA 98.9 107.5 105.9 7.0% -1.5%

Table 7 – Investment per business unit

in R$ million

Realized Budget

2Q13 1Q14 2Q14 1S14 2014 (A)/(B)

(A) (B) %

Rental equipment

Heavy Construction 28.8 15.0 11.3 26.3 37.0 71.0%

Real Estate 44.8 4.5 8.9 13.4 25.0 53.4%

Rental 69.3 73.3 28.5 101.9 169.0 60.3%

Rental equipment 142.9 92.8 48.7 141.5 231.0 61.3%

Corporate and use goods 7.4 9.5 6.0 15.5 42.1 36.9%

Capex Total 150.3 102.3 54.7 157.0 273.1 57.5%

Table 8 – Heavy Construction financial indicators

in R$ million 2Q13 1Q14 2Q14 (C)/(A) (C)/(B)

(A) (B) (C) % %

Net revenue

Rental 41.0 43.8 45.9 11.8% 4.8%

Technical support services, sales and others 14.1 7.3 9.7 -31.5% 32.7%

Total net revenue 55.1 51.0 55.5 0.7% 8.8%

EBITDA 25.1 25.6 25.6 2.3% 0.1%

EBITDA margin (%) 45.5% 50.2% 46.2%

ROIC (%) 17.8% 14.0% 12.5%

Capex 29.1 15.0 11.5 -60.3% -23.0%

Invested Capital 281.5 324.3 350.8 24.6% 8.2%

Rental net PP&E 219.9 254.7 254.5 15.7% -0.1%

Others 61.6 69.6 96.3 56.2% 38.3%

Depreciation 7.2 9.4 10.0 39.5% 7.1%

8 Mills 2Q14 Results

Table 9 – Real Estate financial indicators

in R$ million 2Q13 1Q14 2Q14 (C)/(A) (C)/(B)

(A) (B) (C) % %

Net revenue

Rental 52.0 44.8 45.5 -12.6% 1.4%

Technical support services, sales and others 14.5 14.7 13.4 -7.6% -8.9%

Total net revenue 66.5 59.5 58.8 -11.5% -1.2%

EBITDA 24.6 23.5 25.2 2.5% 7.3%

EBITDA margin (%) 37.0% 39.4% 42.8%

ROIC (%) 9.3% 6.6% 7.9%

Capex 45.1 5.0 9.4 -79.1% 90.2%

Invested Capital 448.2 509.3 478.6 6.8% -6.0%

Rental net PP&E 328.1 332.0 322.9 -1.6% -2.8%

Others 120.1 177.2 155.7 29.6% -12.1%

Depreciation 9.6 11.5 11.7 21.3% 1.9%

Table 10 – Rental financial indicators

in R$ million 2Q13 1Q14 2Q14 (C)/(A) (C)/(B)

(A) (B) (C) % %

Net revenue

Rental 73.8 88.1 84.4 14.3% -4.2%

Technical support services, sales and others 16.3 9.1 14.2 -13.0% 55.5%

Total net revenue 90.1 97.3 98.6 9.4% 1.4%

EBITDA 49.3 58.4 55.1 11.7% -5.8%

EBITDA margin (%) 54.7% 60.1% 55.8%

ROIC (%) 18.5% 17.1% 13.2%

Capex 69.6 73.7 29.5 -57.6% -60.0%

Invested Capital 528.1 648.7 737.8 39.7% 13.7%

Rental net PP&E 475.2 577.1 611.7 28.7% 6.0%

Others 52.9 71.7 126.1 138.4% 75.9%

Depreciation 14.4 18.7 20.3 40.9% 8.7%

Table 11–ROIC Analysis

Heavy

Construction Real Estate Rental Mills

ROIC variation (qoq)

Operational income after taxes -55 bps 83 bps -216 bps -174 bps

Rental net PP&E 1 bps 12 bps -87 bps -18 bps

Others -107 bps 29 bps -133 bps -49 bps

Total -157 bps 130 bps -396 bps -230 bps

ROIC variation (yoy)

Operational income after taxes -225 bps -90 bps -7 bps -323 bps

Rental net PP&E -195 bps 11 bps -379 bps -146 bps

Others -195 bps -69 bps -225 bps -102 bps

Total -531 bps -144 bps -530 bps -500 bps

9 Mills 2Q14 Results

Glossary

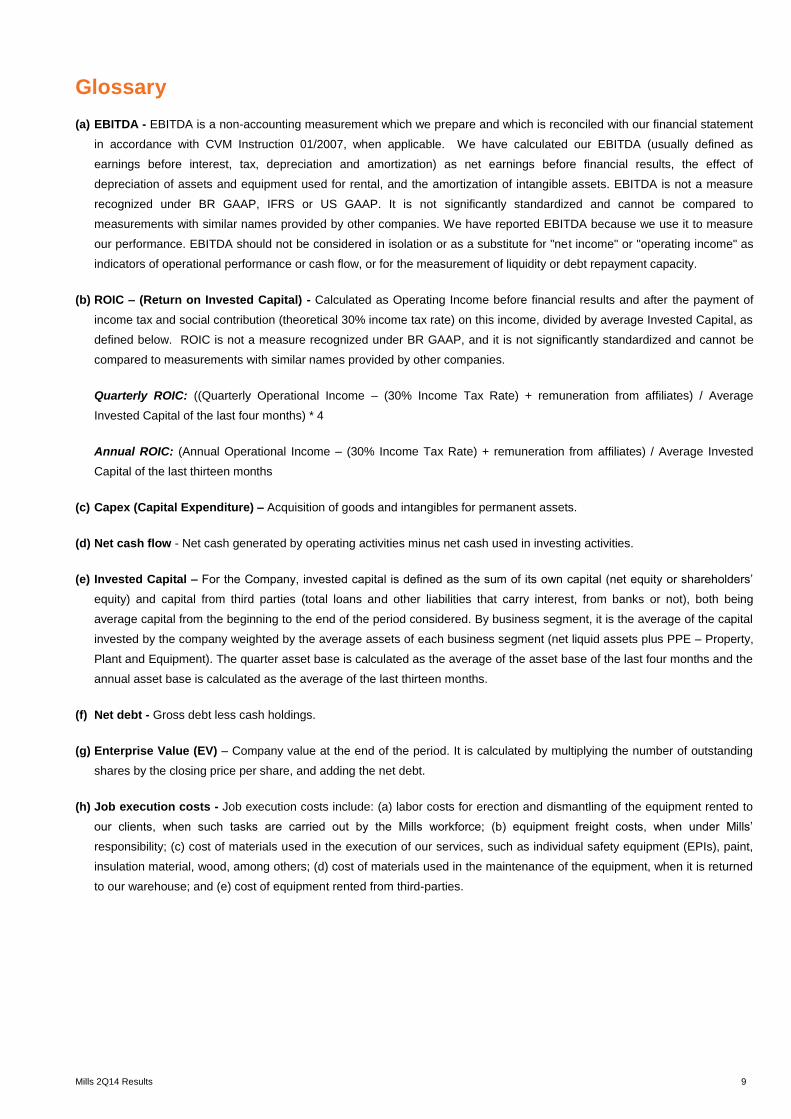

(a) EBITDA - EBITDA is a non-accounting measurement which we prepare and which is reconciled with our financial statement

in accordance with CVM Instruction 01/2007, when applicable. We have calculated our EBITDA (usually defined as

earnings before interest, tax, depreciation and amortization) as net earnings before financial results, the effect of

depreciation of assets and equipment used for rental, and the amortization of intangible assets. EBITDA is not a measure

recognized under BR GAAP, IFRS or US GAAP. It is not significantly standardized and cannot be compared to

measurements with similar names provided by other companies. We have reported EBITDA because we use it to measure

our performance. EBITDA should not be considered in isolation or as a substitute for "net income" or "operating income" as

indicators of operational performance or cash flow, or for the measurement of liquidity or debt repayment capacity.

(b) ROIC – (Return on Invested Capital) - Calculated as Operating Income before financial results and after the payment of

income tax and social contribution (theoretical 30% income tax rate) on this income, divided by average Invested Capital, as

defined below. ROIC is not a measure recognized under BR GAAP, and it is not significantly standardized and cannot be

compared to measurements with similar names provided by other companies.

Quarterly ROIC: ((Quarterly Operational Income – (30% Income Tax Rate) + remuneration from affiliates) / Average

Invested Capital of the last four months) * 4

Annual ROIC: (Annual Operational Income – (30% Income Tax Rate) + remuneration from affiliates) / Average Invested

Capital of the last thirteen months

(c) Capex (Capital Expenditure) – Acquisition of goods and intangibles for permanent assets.

(d) Net cash flow - Net cash generated by operating activities minus net cash used in investing activities.

(e) Invested Capital – For the Company, invested capital is defined as the sum of its own capital (net equity or shareholders’

equity) and capital from third parties (total loans and other liabilities that carry interest, from banks or not), both being

average capital from the beginning to the end of the period considered. By business segment, it is the average of the capital

invested by the company weighted by the average assets of each business segment (net liquid assets plus PPE – Property,

Plant and Equipment). The quarter asset base is calculated as the average of the asset base of the last four months and the

annual asset base is calculated as the average of the last thirteen months.

(f) Net debt - Gross debt less cash holdings.

(g) Enterprise Value (EV) – Company value at the end of the period. It is calculated by multiplying the number of outstanding

shares by the closing price per share, and adding the net debt.

(h) Job execution costs - Job execution costs include: (a) labor costs for erection and dismantling of the equipment rented to

our clients, when such tasks are carried out by the Mills workforce; (b) equipment freight costs, when under Mills’

responsibility; (c) cost of materials used in the execution of our services, such as individual safety equipment (EPIs), paint,

insulation material, wood, among others; (d) cost of materials used in the maintenance of the equipment, when it is returned

to our warehouse; and (e) cost of equipment rented from third-parties.

10 Mills 2Q14 Results

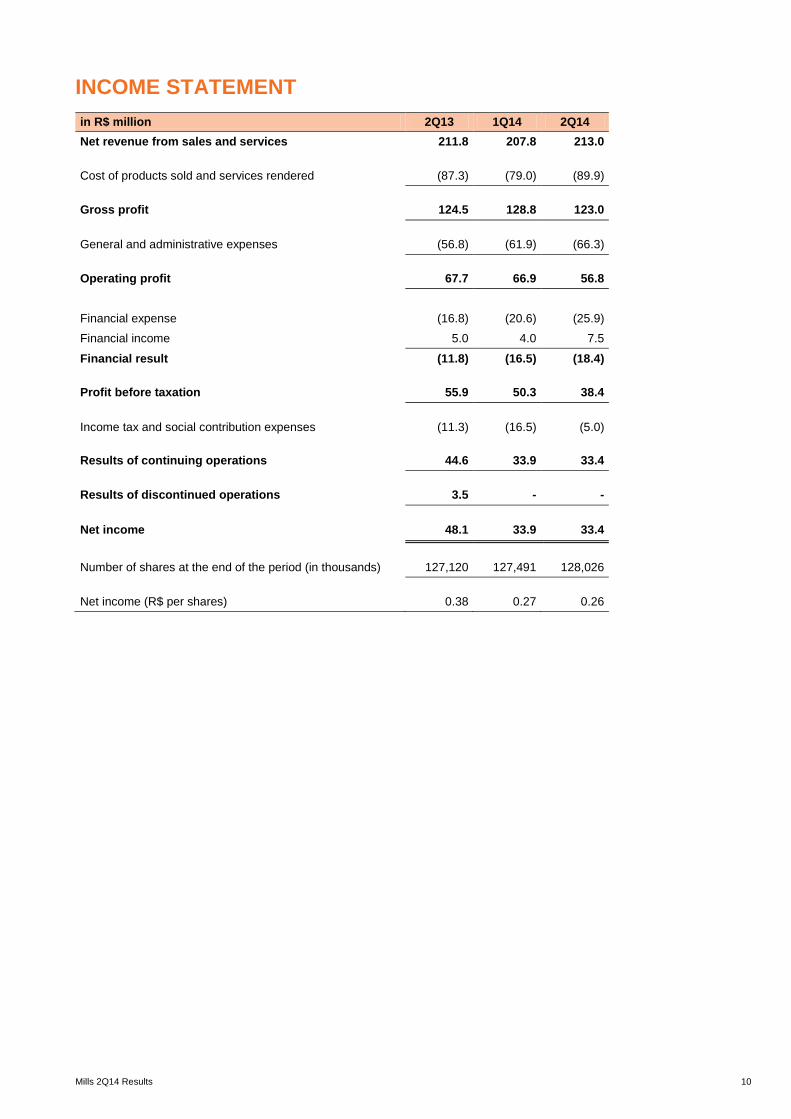

INCOME STATEMENT

in R$ million 2Q13 1Q14 2Q14

Net revenue from sales and services 211.8 207.8 213.0

Cost of products sold and services rendered (87.3) (79.0) (89.9)

Gross profit 124.5 128.8 123.0

General and administrative expenses (56.8) (61.9) (66.3)

Operating profit 67.7 66.9 56.8

Financial expense (16.8) (20.6) (25.9)

Financial income 5.0 4.0 7.5

Financial result (11.8) (16.5) (18.4)

Profit before taxation 55.9 50.3 38.4

Income tax and social contribution expenses (11.3) (16.5) (5.0)

Results of continuing operations 44.6 33.9 33.4

Results of discontinued operations 3.5 - -

Net income 48.1 33.9 33.4

Number of shares at the end of the period (in thousands) 127,120 127,491 128,026

Net income (R$ per shares) 0.38 0.27 0.26

11 Mills 2Q14 Results

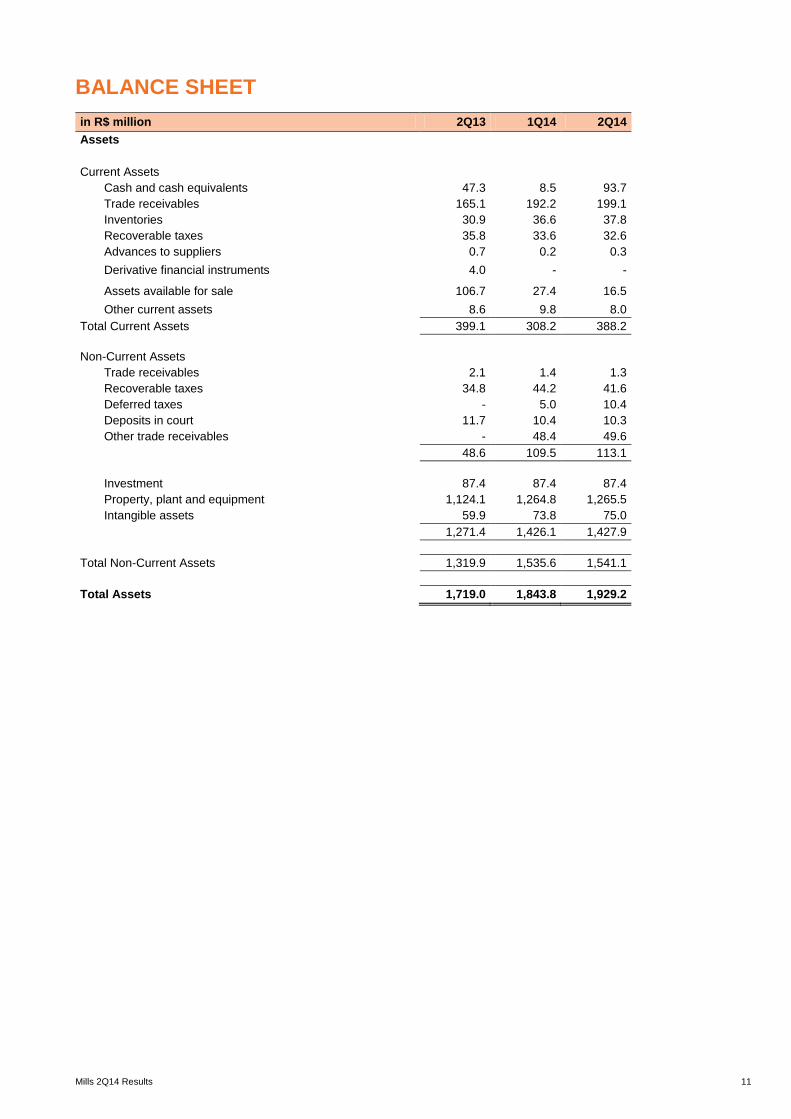

BALANCE SHEET

in R$ million 2Q13 1Q14 2Q14

Assets

Current Assets

Cash and cash equivalents 47.3 8.5 93.7

Trade receivables 165.1 192.2 199.1

Inventories 30.9 36.6 37.8

Recoverable taxes 35.8 33.6 32.6

Advances to suppliers 0.7 0.2 0.3

Derivative financial instruments 4.0 - -

Assets available for sale 106.7 27.4 16.5

Other current assets 8.6 9.8 8.0

Total Current Assets 399.1 308.2 388.2

Non-Current Assets

Trade receivables 2.1 1.4 1.3

Recoverable taxes 34.8 44.2 41.6

Deferred taxes - 5.0 10.4

Deposits in court 11.7 10.4 10.3

Other trade receivables - 48.4 49.6

48.6 109.5 113.1

Investment 87.4 87.4 87.4

Property, plant and equipment 1,124.1 1,264.8 1,265.5

Intangible assets 59.9 73.8 75.0

1,271.4 1,426.1 1,427.9

Total Non-Current Assets 1,319.9 1,535.6 1,541.1

Total Assets 1,719.0 1,843.8 1,929.2

12 Mills 2Q14 Results

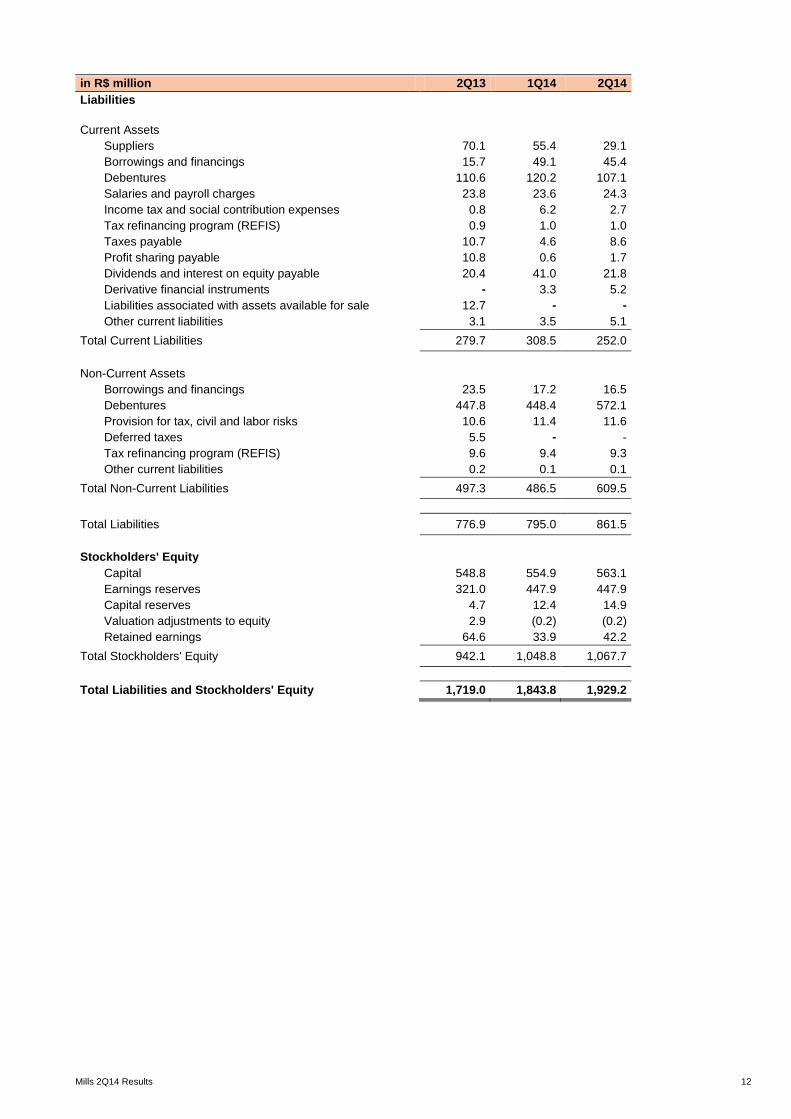

in R$ million 2Q13 1Q14 2Q14

Liabilities

Current Assets

Suppliers 70.1 55.4 29.1

Borrowings and financings 15.7 49.1 45.4

Debentures 110.6 120.2 107.1

Salaries and payroll charges 23.8 23.6 24.3

Income tax and social contribution expenses 0.8 6.2 2.7

Tax refinancing program (REFIS) 0.9 1.0 1.0

Taxes payable 10.7 4.6 8.6

Profit sharing payable 10.8 0.6 1.7

Dividends and interest on equity payable 20.4 41.0 21.8

Derivative financial instruments - 3.3 5.2

Liabilities associated with assets available for sale 12.7 - -

Other current liabilities 3.1 3.5 5.1

Total Current Liabilities 279.7 308.5 252.0

Non-Current Assets

Borrowings and financings 23.5 17.2 16.5

Debentures 447.8 448.4 572.1

Provision for tax, civil and labor risks 10.6 11.4 11.6

Deferred taxes 5.5 - -

Tax refinancing program (REFIS) 9.6 9.4 9.3

Other current liabilities 0.2 0.1 0.1

Total Non-Current Liabilities 497.3 486.5 609.5

Total Liabilities 776.9 795.0 861.5

Stockholders' Equity

Capital 548.8 554.9 563.1

Earnings reserves 321.0 447.9 447.9

Capital reserves 4.7 12.4 14.9

Valuation adjustments to equity 2.9 (0.2) (0.2)

Retained earnings 64.6 33.9 42.2

Total Stockholders' Equity 942.1 1,048.8 1,067.7

Total Liabilities and Stockholders' Equity 1,719.0 1,843.8 1,929.2

13 Mills 2Q14 Results

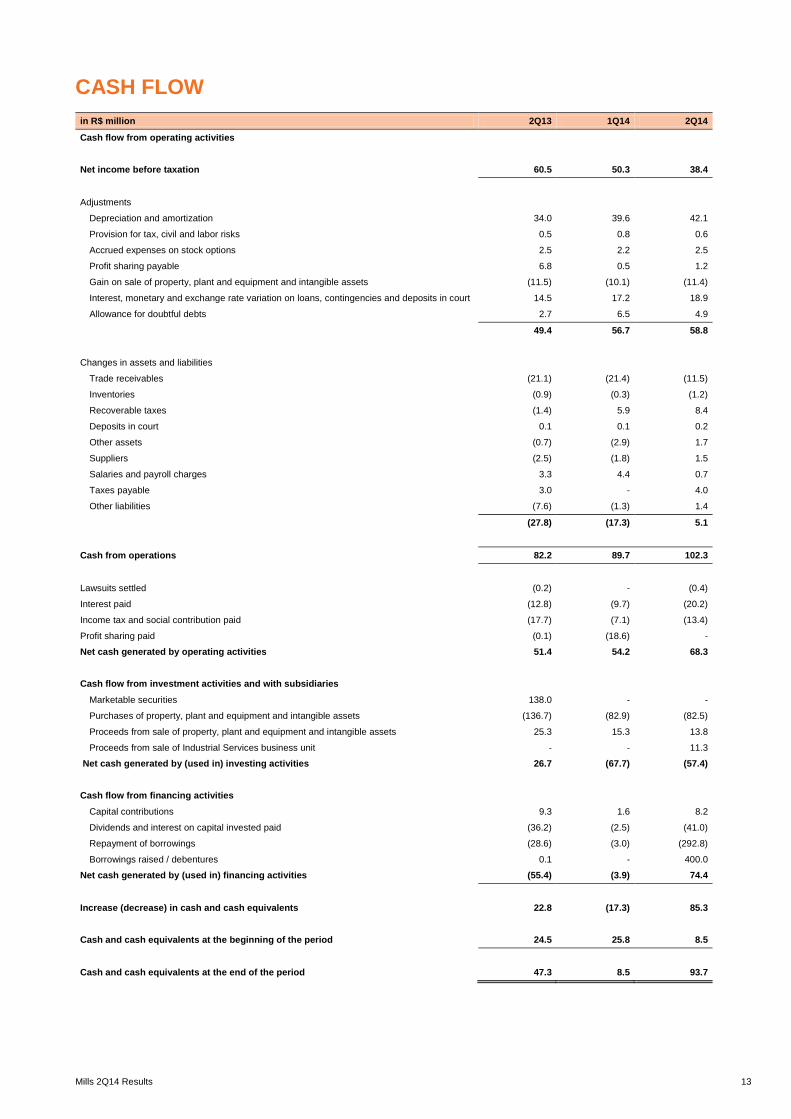

CASH FLOW

in R$ million 2Q13 1Q14 2Q14

Cash flow from operating activities

Net income before taxation 60.5 50.3 38.4

Adjustments

Depreciation and amortization 34.0 39.6 42.1

Provision for tax, civil and labor risks 0.5 0.8 0.6

Accrued expenses on stock options 2.5 2.2 2.5

Profit sharing payable 6.8 0.5 1.2

Gain on sale of property, plant and equipment and intangible assets (11.5) (10.1) (11.4)

Interest, monetary and exchange rate variation on loans, contingencies and deposits in court 14.5 17.2 18.9

Allowance for doubtful debts 2.7 6.5 4.9

49.4 56.7 58.8

Changes in assets and liabilities

Trade receivables (21.1) (21.4) (11.5)

Inventories (0.9) (0.3) (1.2)

Recoverable taxes (1.4) 5.9 8.4

Deposits in court 0.1 0.1 0.2

Other assets (0.7) (2.9) 1.7

Suppliers (2.5) (1.8) 1.5

Salaries and payroll charges 3.3 4.4 0.7

Taxes payable 3.0 - 4.0

Other liabilities (7.6) (1.3) 1.4

(27.8) (17.3) 5.1

Cash from operations 82.2 89.7 102.3

Lawsuits settled (0.2) - (0.4)

Interest paid (12.8) (9.7) (20.2)

Income tax and social contribution paid (17.7) (7.1) (13.4)

Profit sharing paid (0.1) (18.6) -

Net cash generated by operating activities 51.4 54.2 68.3

Cash flow from investment activities and with subsidiaries

Marketable securities 138.0 - -

Purchases of property, plant and equipment and intangible assets (136.7) (82.9) (82.5)

Proceeds from sale of property, plant and equipment and intangible assets 25.3 15.3 13.8

Proceeds from sale of Industrial Services business unit - - 11.3

Net cash generated by (used in) investing activities 26.7 (67.7) (57.4)

Cash flow from financing activities

Capital contributions 9.3 1.6 8.2

Dividends and interest on capital invested paid (36.2) (2.5) (41.0)

Repayment of borrowings (28.6) (3.0) (292.8)

Borrowings raised / debentures 0.1 - 400.0

Net cash generated by (used in) financing activities (55.4) (3.9) 74.4

Increase (decrease) in cash and cash equivalents 22.8 (17.3) 85.3

Cash and cash equivalents at the beginning of the period 24.5 25.8 8.5

Cash and cash equivalents at the end of the period 47.3 8.5 93.7

14 Mills 2Q14 Results

This press release may include declarations about Mills’ expectations regarding future events or results. All declarations based upon future expectations. rather than historical facts. are subject to various risks and uncertainties. Mills cannot guarantee that such declarations will prove to be correct. These risks and uncertainties include factors related to the following: the Brazilian economy. capital markets. infrastructure. real estate and oil & gas sectors. among others. and government rules that are subject to change without previous notice. To obtain further information on factors that may give rise to results different from those forecasted by Mills. please consult the reports filed with the Brazilian Comissão de Valores Mobiliários (CVM. equivalent to U.S. “SEC”).

![The Interregnum (1649-1660) The “Interregnum” Period [ 1649-1660 ] †The Commonwealth (1649-1653) †The Protectorate (1654-1660)](https://img.pdfslide.us/doc/110x75/56649e725503460f94b718c7/the-interregnum-1649-1660-the-interregnum-period-1649-1660-the.jpg)