Embed Size (px)

Citation preview

INITIATING COVERAGE (October 3, 2016)

Equity | Financial / Asset Management

© 2011-2015 SeeThruEquity, LLC. Important disclosures appear at the back of this report. 1 | P a g e

Millennium Investment and Acquisition Co. Inc. (OTC: SMCG, Target Price: $2.50)

We initiate coverage of Millennium Investment and Acquisition Co. Inc. (OTC: SMCG, “Millennium”) with a price target of $2.50 per share. Based in Old Bethpage, New York, Millennium is an intriguing special situation in the microcap space, which offers a combination of robust growth potential and a margin of safety from undervalued assets. Millennium has two key assets that appear to be steeply undervalued relative to its market capitalization. First, in 2015 the company purchased an active carbon (“AC”) biomass plant located in Kawaihae, Hawaii, which is capable of producing premium-grade activated carbon from macadamia nut shells. The Kawaihae plant was purchased out of bankruptcy at a significant discount to fair value (recently appraised at $13.9mn) and the original investment ($44mn) of its former owners. Millennium also has an 12% stake in in SMC Global, a privately held Indian financial services company, which has been marked at $7.7mn – well below the valuation of recent stock sale transactions by the company. In addition, Millennium also had approximately $2.8mn of cash ($0.26 / share) at the end of 2Q16. We see several potential catalysts for Millennium over the coming months as the company advances the upgrade of its activated carbon facility and moves to liquidate its holding in SMC Global. INVESTMENT HIGHLIGHTS Large market potential for activated carbon

Millennium is in the process of upgrading the Kawaihae plant to produce high grade premium activated carbon. Premium grade, low ash / high purity activated carbon has the potential to be a high impact product line for Millennium, as it has much more favorable pricing characteristics than the standard-grade activated carbon commodity, due to its use in advanced technologies in the energy storage, medical and information technology industries. The plant has two years of macadamia nut shell inventory on site, and is located in proximity to key logistics including a macadamia nut manufacturing facility, industrial zones and a port with shipping capabilities. Millennium management believes the plant should be capable of producing activated carbon from 12,000 tons of macadamia nut shells each year, which would generate more than $5mn of EBITDA as it reaches commercial operations – before the impact of any byproduct revenues.

Compelling valuation

We see Millennium as offering a compelling valuation, as each of the company’s strategic assets appear to be worth more than the company’s market capitalization. Millennium marked its 12% investment in SMC Global at $7.7mn, or $0.58 per SMC Global share. This compares to Millennium’s recent market capitalization of $7.1mn – and we note that company has recently sold more than 600,000 shares at $1.22 in privately negotiated transactions with affiliates of SMC Global. As part of exploring an asset-backed debt financing, Millennium received an “as is” appraised value of the Kawaihae plant at more than $13mn. Including the company’s cash on hand of $2.8mn at the end of 2Q16, and adjusting for liabilities, we estimate a sum-of-the-parts at valuation of $2.21 per share. We also note that Millennium’s CEO, David Lesser, owns a 30% equity stake in the company, which should align his interests with those of shareholders.

Initiate coverage with a price target of $2.50

Our analysis of Millennium Investment and Acquisition Co. Inc. indicates a fair value estimate of $2.50 per share, implying an upside of 262% from the recent price of $0.69. The company offers an attractive combination of undervalued assets and potential for robust growth in the emerging market for premium grade activated carbon. Stock Details (9/25/2016)

OTC: SMCG

Sector / Industry Financial / Asset Management

Price target $2.50 Recent share price $0.69

Shares o/s (mn) 11.0

Market cap (in $mn) 7.6

52-week high/low 0.80 / 0.42

Source: Bloomberg, SeeThruEquity Research

Key Financials ($mn unless specified)

FY15 FY16E FY17E

Revenues 0.2 0.3 1.2

EBITDA (0.1) (0.3) (1.7)

EBIT (0.1) (0.5) (3.0)

Net income 14.9 (0.5) (3.2)

EPS ($) 1.79 (0.04) (0.24)

Source: SeeThruEquity Research

Key Ratios

FY15 FY16E FY17E

Gross margin (%) 100.0 100.0 16.2

Operating margin (%) (46.3) (183.5) (244.5)

EBITDA margin (%) (46.3) (104.7) (139.4)

Net margin (%) 6,940.5 (183.5) (264.1)

P/Revenue (x) 35.2 29.8 6.2

EV/EBITDA (x) NM NM NM

EV/Revenue (x) 22.0 18.6 3.9

Source: SeeThruEquity Research

Share Price Performance ($, LTM)

Source: Bloomberg

0.00

0.25

0.50

0.75

1.00

1.25

1.50

Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Millennium Investment and Acquisition Co. Inc.

© 2011-2016 SeeThruEquity, LLC. Important disclosures appear at the back of this report. 2 | P a g e

Equity | Financial / Asset Management

October 3, 2016

SUMMARY TABLE Figure 1. Summary Table (As of September 25, 2016)

Share data B/S data (As of 2Q16) Key personnel: Recent price: $0.69 Total assets: 25.4mn CEO: David Lesser

Price target: $2.50 Total debt: 0.0mn

52-week range: 0.80 / 0.33 Total Liabilities: 0.2mn

Average volume:* 7,343 Equity: 25.2mn

Market cap: $7.6mn W/C: 2.7mn

Book value/share: $2.30 NAV 2.30

Cash/share $0.26 Current ratio: 13.0

Dividend yield: N/A Asset turnover: N/A

Risk profile: High / Speculative Debt/Cap: N/A

* three month average volume (number of shares)

Estimates Valuation FY December Rev ($mn) EBITDA ($mn) EPS ($) P/Rev (x) EV/Rev (x) P/E (x) 2015A 0.2 (0.1) 1.79 35.2x 22.0x 0.4x

2016E 0.3 (0.3) (0.04) 29.8x 18.6x NM

2017E 1.2 (1.7) (0.24) 6.2x 3.9x NM

2018E 18.1 2.9 0.05 0.4x 0.3x 13.8x

2019E 23.8 5.8 0.22 0.3x 0.2x 3.1x

2020E 27.4 6.7 0.27 0.3x 0.2x 2.6x

Source: SeeThruEquity Research

INVESTMENT THESIS We initiate coverage of Millennium Investment and Acquisition Co. Inc. (OTC: SMCG, “Millennium”) with a price target of $2.50 per share. Based in Old Bethpage, New York, Millennium is an intriguing special situation in the microcap space, which offers a combination of robust growth potential and a margin of safety from undervalued assets. Millennium has two key assets that appear to be steeply undervalued relative to its market capitalization. First, in 2015 the company purchased an active carbon (“AC”) biomass plant located in Kawaihae, Hawaii. The plant was purchased out of bankruptcy in June 2015, at a significant discount to fair value (recently appraised at $13.9mn) and the original investment ($44mn). Millennium is in the process of upgrading the plant to produce high grade premium activated carbon. Premium grade, low ash / high purity activated carbon has the potential to be a high impact product line for Millennium, as it has much more favorable pricing characteristics than the standard activated carbon commodity, due to its use in advanced technologies in the energy storage, medical and information technology industries. Millennium’s second strategic asset is its sizeable (~12%) stake in SMC Global, a privately held Indian financial services firm. The company acquired this investment as a result of a SPAC strategy under a prior management team, and carries the stake at $7.7mn, or $0.58 per share of SMC Global. The investment is non-core to Millennium and management has been seeking to monetize it in order to fund operations and the development of the activated carbon biomass plant. SMC Global has stated that it is pursuing a public

Millennium Investment and Acquisition Co. Inc.

© 2011-2016 SeeThruEquity, LLC. Important disclosures appear at the back of this report. 3 | P a g e

Equity | Financial / Asset Management

October 3, 2016

offering. If this occurs, it could be a significant liquidity event for Millennium. Thus far in 2016, Millennium has announced sales in excess of 600,000 shares to a promoter of SMC Global at prices of $1.22 per share, and the company has an ongoing agreement in place with the management sponsors of SMC Global to sell 100,000 shares per month. In our view the mark of $0.58 versus recent transaction prices is a prudently conservative liquidity discount; however, it is worth noting that even at the book value, which is considerably lower than recent transaction prices, the company’s stake in SMC Global of $7.7mn alone is greater than Millennium’s recent market capitalization of $7.6mn as of the market close on September 23, 2016.

Kawaihae high grade activated carbon plant represents significant opportunity While we believe the combination of its two undervalued strategic assets offers a defensible margin of safety in the short run, the key to the upside potential in Millennium is the degree to which it can execute as it seeks to complete the upgrade of its activated carbon pant in Kawaihae. This asset has significant potential both from a future cash flow and an “assets in place” perspective. As discussed in more detail later in this report, the plant was recently appraised “as is” at more than $13mn, which alone would represent a steeply undervalued asset relative to Millennium’s recent market capitalization. Indeed, the asset includes a two-year supply of macadamia nut shells and the plant’s former owners invested more than $40mn before the project entered bankruptcy.

Source: Company investor materials Millennium is in the process of upgrading the Kawaihae plant to produce high grade activated carbon samples, and is targeting production at scale by the end of 2017E. Management estimates that the plant will require $10mn to $15mn in capital to reach full scale production, and we expect the company to source this from sales of SMC Global and a combination of debt / equity new capital raising. While the plant is not fully operational, the company has achieved initial startup and produced carbon. The Kawaihae plant has several attractive attributes, which highlight its potential. The plant is located less than one mile from Kawaihae Port (a fuel depot and shipping terminal) and is adjacent to Hamakua Macadamia Nut Company, a natural supply source. Once operational the Kawaihae plant is expected to be able to process 12,000 tons of macadamia nut shells per year, and the company already has two years of macadamia nut shell inventory on site, which accompanied the asset purchase in June 2015. There appears to be a significant opportunity for revenue and cash generation for Millennium if it has access to the capital needed to complete the upgrade of the Kawaihae activated carbon plant. Initially, Millennium believes it can achieve $5mn in annual EBITDA once the plant is operating at scale, a figure which should rise as it improves yield, the mix of high grade activated carbon, and monetizes liquid and gas byproducts.

Millennium Investment and Acquisition Co. Inc.

© 2011-2016 SeeThruEquity, LLC. Important disclosures appear at the back of this report. 4 | P a g e

Equity | Financial / Asset Management

October 3, 2016

Activated carbon has high value attributes suited for advanced energy, medical markets Although the Kawaihae plant will also produce commodity-grade activated carbon, we expect management to focus on optimizing production of premium-grade activated carbon, which offers higher value and a much higher price than standard commoditized activated carbon, given its higher purity, low ash content, extraordinarily large surface area and porosity. These attributes are well-suited for demand from advanced technology applications in the new energy, medical and information technology industries. The first area where we expect Millennium to focus its sales efforts for premium-grade activated carbon is advanced energy storage applications, such as ultra-capacitors / advanced battery technologies and adsorbed natural gas storage, which are well-matched for its surface area and porosity. Initially Millennium is targeting the emerging market for ultra-capacitors, where premium-activated carbon is primary building block. Ultra-capacitors are a next-generation energy storage device that stores electricity through a physical charge, versus conventional batteries, which store electricity through reversible chemical reactions. Ultra-capacitors offer greater power density, higher cycle life (500,000 cycles versus 2,000 cycles) and charge/discharge efficiency, and faster discharge/charge time than conventional batteries, and have applications in renewables, the automotive industry, industrial products, and power grid storage, among others potential uses

Source: Company investor materials

As illustrated in the enclosed graphic, the market for ultra-capacitors is $500mn, but the potential is vast if the technology takes share from conventional and/or lithium battery markets.

Millennium Investment and Acquisition Co. Inc.

© 2011-2016 SeeThruEquity, LLC. Important disclosures appear at the back of this report. 5 | P a g e

Equity | Financial / Asset Management

October 3, 2016

Millennium Investment and Acquisition Co. Inc.

© 2011-2016 SeeThruEquity, LLC. Important disclosures appear at the back of this report. 6 | P a g e

Equity | Financial / Asset Management

October 3, 2016

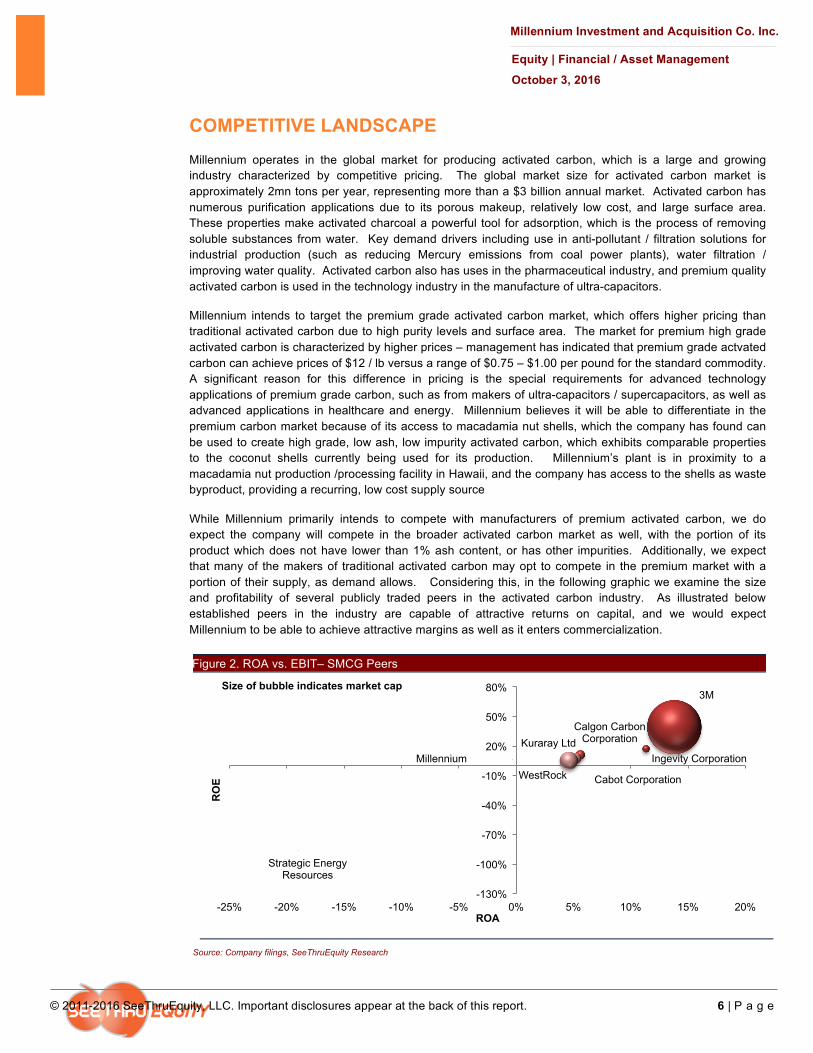

COMPETITIVE LANDSCAPE Millennium operates in the global market for producing activated carbon, which is a large and growing industry characterized by competitive pricing. The global market size for activated carbon market is approximately 2mn tons per year, representing more than a $3 billion annual market. Activated carbon has numerous purification applications due to its porous makeup, relatively low cost, and large surface area. These properties make activated charcoal a powerful tool for adsorption, which is the process of removing soluble substances from water. Key demand drivers including use in anti-pollutant / filtration solutions for industrial production (such as reducing Mercury emissions from coal power plants), water filtration / improving water quality. Activated carbon also has uses in the pharmaceutical industry, and premium quality activated carbon is used in the technology industry in the manufacture of ultra-capacitors.

Millennium intends to target the premium grade activated carbon market, which offers higher pricing than traditional activated carbon due to high purity levels and surface area. The market for premium high grade activated carbon is characterized by higher prices – management has indicated that premium grade actvated carbon can achieve prices of $12 / lb versus a range of $0.75 – $1.00 per pound for the standard commodity. A significant reason for this difference in pricing is the special requirements for advanced technology applications of premium grade carbon, such as from makers of ultra-capacitors / supercapacitors, as well as advanced applications in healthcare and energy. Millennium believes it will be able to differentiate in the premium carbon market because of its access to macadamia nut shells, which the company has found can be used to create high grade, low ash, low impurity activated carbon, which exhibits comparable properties to the coconut shells currently being used for its production. Millennium’s plant is in proximity to a macadamia nut production /processing facility in Hawaii, and the company has access to the shells as waste byproduct, providing a recurring, low cost supply source

While Millennium primarily intends to compete with manufacturers of premium activated carbon, we do expect the company will compete in the broader activated carbon market as well, with the portion of its product which does not have lower than 1% ash content, or has other impurities. Additionally, we expect that many of the makers of traditional activated carbon may opt to compete in the premium market with a portion of their supply, as demand allows. Considering this, in the following graphic we examine the size and profitability of several publicly traded peers in the activated carbon industry. As illustrated below established peers in the industry are capable of attractive returns on capital, and we would expect Millennium to be able to achieve attractive margins as well as it enters commercialization.

Figure 2. ROA vs. EBIT– SMCG Peers

Source: Company filings, SeeThruEquity Research

Ingevity Corporation

Calgon Carbon Corporation

Strategic Energy Resources

3M

Cabot Corporation

Kuraray Ltd

WestRock Millennium

-130%

-100%

-70%

-40%

-10%

20%

50%

80%

-25% -20% -15% -10% -5% 0% 5% 10% 15% 20%

RO

E

ROA

Size of bubble indicates market cap

Millennium Investment and Acquisition Co. Inc.

© 2011-2016 SeeThruEquity, LLC. Important disclosures appear at the back of this report. 7 | P a g e

Equity | Financial / Asset Management

October 3, 2016

FINANCIALS AND FUTURE OUTLOOK Key assumptions / Drivers

Our model for Millennium is based on our assumption that the company will be able to transition its Hawaii-based macadamia shell activated carbon operations into production by the end of 2017E, with 2018E being the first full year of production.

Production. Millennium management has stated that its plant can process up to 12,000 tons of macadamia nut shells per year, with an aim to convert this resource into high grade premium activated carbon. As part of the acquisition of its activated carbon plant in June 2015, the company also acquired 24,000 tons of macadamia nut shells –representing approximately two years of raw material inputs required to produce activated carbon. In 2018E, while the company is fine tuning its process, we estimate that Millennium’s production will process will yield 10 tons of activated carbon for every 100 tons of raw shells, improving over the course of our forecast to 14 tons of activated carbon for every 100 tons of raw shells by 2025E. While we believe the company will sell output that does not meet premium grade standards at prevailing prices on the market, and that management will also seek to monetize byproducts over the course of our forecast, we believe the focus of the company will (rightly) be on optimizing the production of premium-grade active carbon, which carries a substantial pricing advantage due to its makeup, high surface area, and applications in the technology and medical markets. Pricing. In our view the upside potential for Millennium hinges on the pricing outlook for premium grade activated carbon. We believe that industry-wide prices for standard grade activated carbon are approximately $1,500 / ton ($0.75/lb). Millennium management expects to be able to achieve significantly higher prices than this level if it is able to produce the premium grade of porous, high surface area activated carbon required by advanced technology and medical customers. We have assumed pricing of approximately $20,000 per ton ($10 / lb) for this high grade product at the beginning of our forecast, rising to $11.71/ lb by 2025E. Revenue Considering these inputs, we have forecast revenue to climb from $1.2mn in 2017E to reach $18.1mn in 2018E and $23.8mn in 2019E, with growth thereafter driven by improvements in the percentage of premium grade activated carbon as a part of total production, strong pricing, and new revenue streams from liquid and gas byproducts In the following graphic we illustrate the sales and production forecast for Millennium’s activated carbon plant beginning in 2017E when the company expects the plant to come online.

0.0

10.0

20.0

30.0

40.0

0

500

1,000

1,500

2,000

2017E 2018E 2019E 2020E 2021E 2022E

PremiumGrade(tons) StandardGrade(tons) Revenue($mn)

Millennium Investment and Acquisition Co. Inc.

© 2011-2016 SeeThruEquity, LLC. Important disclosures appear at the back of this report. 8 | P a g e

Equity | Financial / Asset Management

October 3, 2016

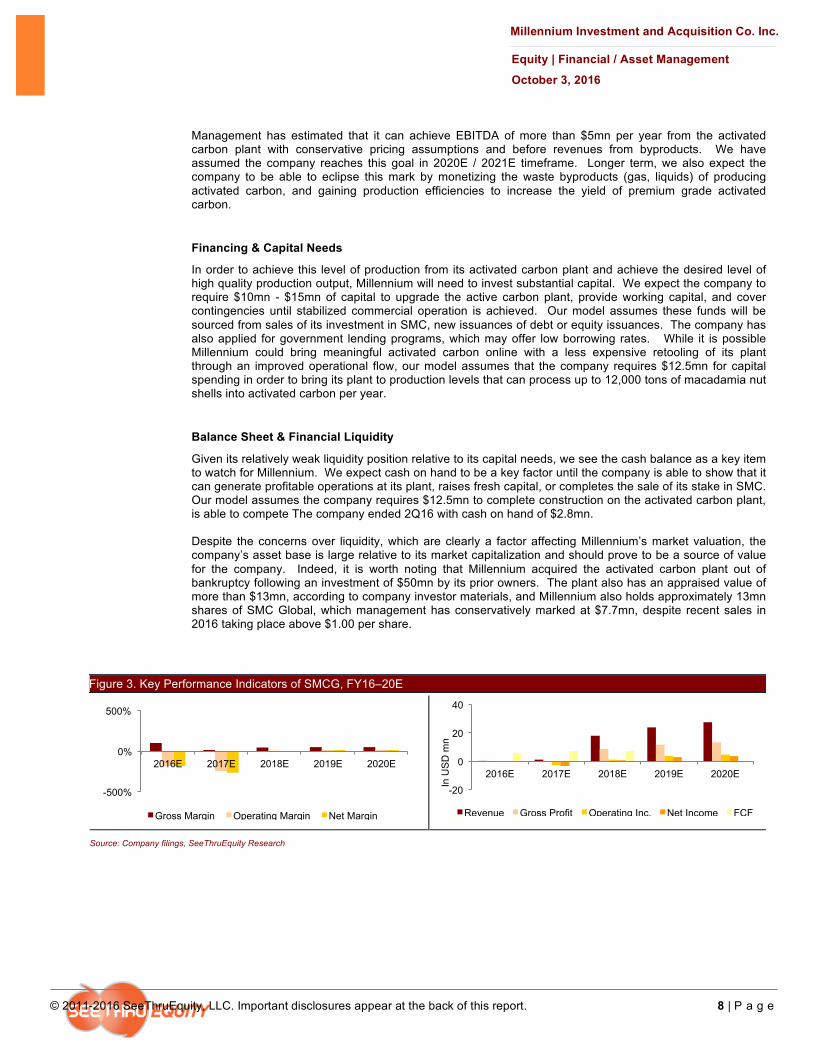

Management has estimated that it can achieve EBITDA of more than $5mn per year from the activated carbon plant with conservative pricing assumptions and before revenues from byproducts. We have assumed the company reaches this goal in 2020E / 2021E timeframe. Longer term, we also expect the company to be able to eclipse this mark by monetizing the waste byproducts (gas, liquids) of producing activated carbon, and gaining production efficiencies to increase the yield of premium grade activated carbon.

Financing & Capital Needs

In order to achieve this level of production from its activated carbon plant and achieve the desired level of high quality production output, Millennium will need to invest substantial capital. We expect the company to require $10mn - $15mn of capital to upgrade the active carbon plant, provide working capital, and cover contingencies until stabilized commercial operation is achieved. Our model assumes these funds will be sourced from sales of its investment in SMC, new issuances of debt or equity issuances. The company has also applied for government lending programs, which may offer low borrowing rates. While it is possible Millennium could bring meaningful activated carbon online with a less expensive retooling of its plant through an improved operational flow, our model assumes that the company requires $12.5mn for capital spending in order to bring its plant to production levels that can process up to 12,000 tons of macadamia nut shells into activated carbon per year.

Balance Sheet & Financial Liquidity

Given its relatively weak liquidity position relative to its capital needs, we see the cash balance as a key item to watch for Millennium. We expect cash on hand to be a key factor until the company is able to show that it can generate profitable operations at its plant, raises fresh capital, or completes the sale of its stake in SMC. Our model assumes the company requires $12.5mn to complete construction on the activated carbon plant, is able to compete The company ended 2Q16 with cash on hand of $2.8mn. Despite the concerns over liquidity, which are clearly a factor affecting Millennium’s market valuation, the company’s asset base is large relative to its market capitalization and should prove to be a source of value for the company. Indeed, it is worth noting that Millennium acquired the activated carbon plant out of bankruptcy following an investment of $50mn by its prior owners. The plant also has an appraised value of more than $13mn, according to company investor materials, and Millennium also holds approximately 13mn shares of SMC Global, which management has conservatively marked at $7.7mn, despite recent sales in 2016 taking place above $1.00 per share.

Figure 3. Key Performance Indicators of SMCG, FY16–20E

Source: Company filings, SeeThruEquity Research

-500%

0%

500%

2016E 2017E 2018E 2019E 2020E

Gross Margin Operating Margin Net Margin

-20

0

20

40

2016E 2017E 2018E 2019E 2020E

In U

SD

mn

Revenue Gross Profit Operating Inc. Net Income FCF

Millennium Investment and Acquisition Co. Inc.

© 2011-2016 SeeThruEquity, LLC. Important disclosures appear at the back of this report. 9 | P a g e

Equity | Financial / Asset Management

October 3, 2016

Millennium Investment and Acquisition Co. Inc.

© 2011-2016 SeeThruEquity, LLC. Important disclosures appear at the back of this report. 10 | P a g e

Equity | Financial / Asset Management

October 3, 2016

VALUATION In our view, Millennium represents an intriguing special situation, which combines a margin of safety with the potential for rapid growth if management is able to generate the sales and EBITDA leverage expected from its activated carbon plant. In the short run, Millennium presents a compelling case based on the collective value of its activated carbon plant assets (assessed at $13.9mn “as is”) and its 12% stake in SMC Global (a privately held financial services firm located in India which the company has valued at $7.7mn). These two assets combined represent potential asset value of $21.6mn, and even assuming a significant liquidity discount to the SMC Global stake, seems to offer a significant backstop to the recent market capitalization of $6mn, considering 11mn outstanding shares, no debt, and the recent closing price of $0.69.

Our price target for Millennium is based on a discounted cash flow model (DCF), which considers future cash flows that could be derived from successful activated carbon production and the liquidation of the company’s investment in SMC Global. We also considered a sum-of-the-parts valuation (SOTP) based on its SMC investment and its plant assets. Using a blend of these methods we arrived at a price target of $2.50, representing upside potential of 262% from the recent price of $0.69 on September 25, 2016. DCF

Our DCF assumes that SMCG is able to get its activated carbon plant operational by the end of 2017E, with capital spending of approximately $15mn over the next three years. We assumed this is partly funded by the sale of the company’s position in SMC Global and new capital raises through debt and equity issuances. We forecast a use of cash from 2016E – 2017E, operates at cash flow breakeven in 2018 (after capital spending), and assume that the company will begin generating significant cash flow beginning in 2019E an onward. This forecast relies on the assumption of improving plant utilization improves and an improving yield of premium activated carbon, as well as a strong pricing environment for activated carbon. Our forecast assumes a weighted average cost of capital of 17.5% and a terminal growth rate of 5% at the end of 2024E. The analysis yielded a fair value of $2.63 per share, as shown in detail below.

Figure 4.Discounted Cash Flow (DCF), FY16E–25E

$’ 000 FY16E FY17E FY18E FY19E FY20E FY21E FY22E FY23E FY24E FY25E EBIT (466.0) (3,001.2) 1,191.6 3,743.8 3,743.8 3,743.8 4,698.8 5,394.1 8,054.1 9,544.7

Less: Tax 0.0 0.0 35.6 261.1 261.1 261.1 506.3 835.4 1,855.7 3,172.6

NOPLAT (466.0) (3,001.2) 1,156.0 3,482.7 3,482.7 3,482.7 4,192.6 4,558.7 6,198.4 6,372.0

Changes in working capital (100.0) (766.5) (170.0) (143.0) (143.0) (143.0) (184.1) (24.7) 40.9 48.9 Depreciation & Amortization 200 1,290 1,672 2,080 2,080 2,080 1,974 1,882 1,802 1,734

Capex (1,500) (8,500) (5,000) (700) (700) (700) (756) (816) (882) (952)

SMC Global Investment 600 4,737 3,000 0 0 0 0 0 0 0

FCFF (1,266.0) (6,240.7) 658.0 4,719.7 4,719.7 4,719.7 5,226.7 5,599.1 7,159.1 7,202.2

Discount factor 0.96 0.81 0.69 0.59 0.50 0.50 0.43 0.36 0.31 0.26

PV of FCFE (1,210.2) (5,077.1) 455.6 2,781.2 2,367.0 2,367.0 2,230.8 2,033.8 2,213.2 1,894.9

Sum of PV of FCFE 10,056.2

Terminal cash flow 60,498.4

PV of terminal cash flow 15,917.3

Enterprise value 25,973.5

Less: Debt 0

Add: Cash 2,830

Equity value 28,803

Outstanding shares (mn) 11.0 Fair value per share ($) 2.63

Millennium Investment and Acquisition Co. Inc.

© 2011-2016 SeeThruEquity, LLC. Important disclosures appear at the back of this report. 11 | P a g e

Equity | Financial / Asset Management

October 3, 2016

Summary conclusions Key assumptions Fair Value per share assets 2.63 Beta 2.0 Recent price ($ per share) 0.69 Cost of equity 17.5% Upside (downside) 281.7% Cost of debt (post tax) 12.4% WACC 17.5% Terminal Growth Rate 5.0%

Source: SeeThruEquity Research

Figure 5. Sensitivity of Valuation – WACC vs. Terminal Growth Rate

WACC (%)

Term

inal

gro

wth

rate

(%

)

2.63 16.5% 17.0% 17.5% 18.0% 18.5%

4.00% 2.78 2.64 2.51 2.39 2.27

4.50% 2.86 2.70 2.57 2.44 2.32

5.00% 2.93 2.77 2.63 2.49 2.37

5.50% 3.02 2.85 2.70 2.55 2.42

6.00% 3.11 2.93 2.77 2.62 2.48

6.50% 3.22 3.02 2.85 2.69 2.55

Source: SeeThruEquity Research

Millennium Investment and Acquisition Co. Inc.

© 2011-2016 SeeThruEquity, LLC. Important disclosures appear at the back of this report. 12 | P a g e

Equity | Financial / Asset Management

October 3, 2016

Sum of the Parts / Asset backed valuation

In our view a practical way to examine Millennium’s valuation in the short run is to look at the assets on its balance sheet. At the recent price of $0.69, with its last disclosed share count at 11.0mn, Millennium has a market capitalization of $7.6mn, which appears to be a steep discount to fair value on this basis. The company ended the June quarter with total assets of $25.4mn on its balance sheet and just $0.2mn in liabilities, translating to net asset value per share of $2.30. Our analysis, which excludes certain balance sheet items, yields a SOTP valuation of $2.21 per share.

The most significant assets on Millennium’s balance sheet are: 1) its 12% investment in India-based financial services firm SMC Global, and 2) the activated carbon plant located in Hawaii. On June 30, 2016, Millennium valued its stake in SMC Global at $7.7mn, or approximately $0.58 per SMC share. There appears to be a possibility to that Millennium could realize more value than the level marked on its balance sheet. Millennium last reported owning 13.2mn shares of SMC Global, and in August completed a sale of 300,000 shares of SMC Global stock in a privately negotiated transaction with a promoter of SMC Global at $1.23 per share. During the first half of 2016, Millennium was also able to sell 300,000 shares to an SMC Global promoter at $1.23 per share. While we believe it unlikely the company could maintain this price if it tried to sell its entire SMC Global stake, it is worth noting that if Millennium were able to sell its entire position at this price it could potentially generate proceeds of $16.2mn, or $1.48 per Millennium share. Our sum-of-the-parts exercise maintains the valuation marked on Millennium’s balance sheet, of $7.7mn, or approximately $0.70 per share.

The other key asset on Millennium’s balance sheet worth consideration is its activated carbon plant in Kawaihae, Hawaii, consisting of 13 acres of land leased from the Department of Hawaiian Home Lands, the existing equipment, and 24,000 tons of dried macadamia nut shells, the primary raw material input for the plant’s production of activated carbon (representing a 2-year supply). Millennium was able to purchase this plant out of bankruptcy for $1.3mn, and benefits form its prior owners investing more than $40mn in the project before bankruptcy, between 2009 and 2012. Millennium has had the plant appraised for the purposes of exploring debt financing and received an “as-is and in-place” fair market value estimate of $13.9mn, which would represent a value of approximately $1.27 per Millennium share.

Figure 6. Sum of the Parts Valuation

Asset Est Value Per Millennium Share

Comments

SMC Global (12% stake) $7.7mn $0.70 Assumes Millennium has appropriately marked stake at $0.58 per share

Kawaihae Activated Carbon Plant – Under construction

$13.9mn $1.27 In line with company’s debt appraisal

Cash & Equivalents $2.8mn $0.26 As of end of 2Q16

Total – Liabilities ($0.2mn) ($0.02) Minimal liabilities on balance sheet

Sum of Parts Valuation $24.2mn $2.21 SOTP much higher than recent price of $0.69

Millennium Investment and Acquisition Co. Inc.

© 2011-2016 SeeThruEquity, LLC. Important disclosures appear at the back of this report. 13 | P a g e

Equity | Financial / Asset Management

October 3, 2016

Millennium Investment and Acquisition Co. Inc.

© 2011-2016 SeeThruEquity, LLC. Important disclosures appear at the back of this report. 14 | P a g e

Equity | Financial / Asset Management

October 3, 2016

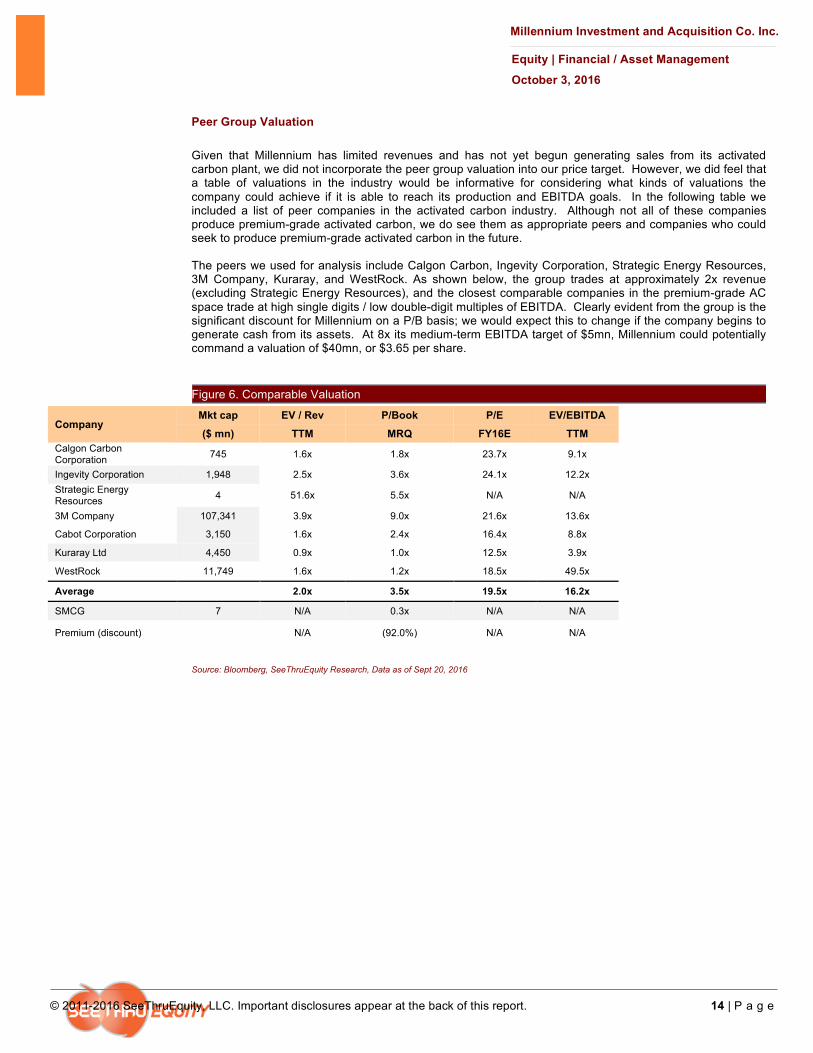

Peer Group Valuation Given that Millennium has limited revenues and has not yet begun generating sales from its activated carbon plant, we did not incorporate the peer group valuation into our price target. However, we did feel that a table of valuations in the industry would be informative for considering what kinds of valuations the company could achieve if it is able to reach its production and EBITDA goals. In the following table we included a list of peer companies in the activated carbon industry. Although not all of these companies produce premium-grade activated carbon, we do see them as appropriate peers and companies who could seek to produce premium-grade activated carbon in the future. The peers we used for analysis include Calgon Carbon, Ingevity Corporation, Strategic Energy Resources, 3M Company, Kuraray, and WestRock. As shown below, the group trades at approximately 2x revenue (excluding Strategic Energy Resources), and the closest comparable companies in the premium-grade AC space trade at high single digits / low double-digit multiples of EBITDA. Clearly evident from the group is the significant discount for Millennium on a P/B basis; we would expect this to change if the company begins to generate cash from its assets. At 8x its medium-term EBITDA target of $5mn, Millennium could potentially command a valuation of $40mn, or $3.65 per share. Figure 6. Comparable Valuation

Company Mkt cap EV / Rev P/Book P/E EV/EBITDA

($ mn) TTM MRQ FY16E TTM Calgon Carbon Corporation 745 1.6x 1.8x 23.7x 9.1x

Ingevity Corporation 1,948 2.5x 3.6x 24.1x 12.2x Strategic Energy Resources 4 51.6x 5.5x N/A N/A

3M Company 107,341 3.9x 9.0x 21.6x 13.6x

Cabot Corporation 3,150 1.6x 2.4x 16.4x 8.8x

Kuraray Ltd 4,450 0.9x 1.0x 12.5x 3.9x

WestRock 11,749 1.6x 1.2x 18.5x 49.5x

Average 2.0x 3.5x 19.5x 16.2x

SMCG 7 N/A 0.3x N/A N/A

Premium (discount) N/A (92.0%) N/A N/A

Source: Bloomberg, SeeThruEquity Research, Data as of Sept 20, 2016

Millennium Investment and Acquisition Co. Inc.

© 2011-2016 SeeThruEquity, LLC. Important disclosures appear at the back of this report. 15 | P a g e

Equity | Financial / Asset Management

October 3, 2016

RISK CONSIDERATIONS Financial Liquidity / Going-concern

In our view financial liquidity is a key risk area for Millennium. The company’s growth plans hinge on the completion of its activated carbon plant in Kawaihae, Hawaii, which management has estimated will require between $10mn and $15mn for capital spending, working capital investment and to cover contingencies until stabilized commercial operations are achieved. We expect Millennium to source this capital from selling its stake in SMC, capital raising activities, and potentially through government-backed lending programs for which the company is in the process of applying.

Asset Liquidity

Much of the implied value in Millennium stems from assets on its balance sheet that are illiquid. If the company is forced to sell either its activated carbon plant assets, or its stake in SMC Global under duress, it may find it difficult to sell these assets at the value recorded on its balance sheet.

The 1940 Act Effect

We believe Millennium is evaluating the possibility of deregistering as an investment company under the 1940 Act. The 1940 Act imposes certain restrictions that may limit MIAC’s ability to raise additional capital to fund its new investment strategy. Among other things, the 1940 Act and the related rules impose restrictions on the issuance of debt and equity securities, limit the extent of permissible borrowings and impose other restrictions on capital structure. In particular, a closed-end fund can have only one class of preferred stock and one class of debt securities in addition to common stock, both of which are subject to 1940 Act asset coverage requirements.

Dilution

To the extent their ability to issue debt or other senior securities is constrained, Millennium may choose to issue common stock or other equity instruments, such as warrants, convertible debt, or convertible preferred stock, to finance new investments. If Millennium chooses to raise additional funds by issuing common stock or convertible securities, then the percentage ownership of their stockholders at that time would decrease and stockholders may experience dilution.

Pricing & Execution

Much of the upside potential for Millennium rests on its ability to produce and sell premium grade activated carbon. The company has not completed the upgrade to its production facilities to show that it can do this consistently and profitably. Additionally, as is the case with all commodity-based businesses, Millennium’s profit model assumes predictable pricing for high grade premium activated carbon. There is no guarantee that this product will command recent or expected prices in the future.

Millennium Investment and Acquisition Co. Inc.

© 2011-2016 SeeThruEquity, LLC. Important disclosures appear at the back of this report. 16 | P a g e

Equity | Financial / Asset Management

October 3, 2016

Management Team & Directors

David Lesser, Chairman, Chief Executive Officer, Treasurer and Secretary

David Lesser has over 30 years of investment and operational experience in real-estate and alternative energy. Mr. Lesser has significant experience with acquisitions, management, financing including public capital markets, as a principal investor utilizing his own capital and managing capital on behalf of others. Mr. Lesser is currently the President of Hudson Bay Partners (“HBP”) which was established in 1996 to make investments in real estate and real estate related companies and alternative energy. As part of his current activities with HBP, Mr. Lesser currently serves as Chairman and CEO of Millennium Investment & Acquisition Company (ticker: SMCG) and Power REIT (ticker: PW). HBP has managed capital on behalf of institutional investors and high net worth individuals, including Crescent Real Estate Equities (REIT led by Richard Rainwater).

Mr. Lesser has experience building public companies. In 1997, HBP sponsored the reverse merger reorganization of a small Real Estate Investment Trust (“REIT”) (formerly American Real Estate Investments – “ARI”). HBP invested $25 million along with merging two real estate companies into ARI to ultimately form Keystone Property Trust which was listed on the American Stock Exchange (ticker: KTR). In 2004, KTR was sold to another REIT (ProLogis) for $1.7 Billion. Mr. Lesser served as a Director of the company during its formative building years and was instrumental in getting this transaction off the ground. In addition to serving as a Director for KTR as described above, Mr. Lesser has served as Director of Santa Fe Gaming Corp. (a public company).

Prior to forming Hudson Bay Partners, Mr. Lesser was Senior Vice President of Crescent Real Estate Equities, a publicly traded REIT headed by Richard Rainwater. Prior to Crescent, Mr. Lesser was a Director in Merrill Lynch’s real-estate investment banking division and was one of the principal bankers overseeing the IPO of Crescent.

Mr. Lesser holds an M.B.A. from Cornell University and a B.S. in Economics from Cornell University.

Dionisio D’Aguilar, Director

Mr. D’Aguilar has over twenty years of business experience and holds a designation as a CPA. He has served as President and CEO of Superwash Limited since 1993. Superwash Limited is the largest chain of self-service laundry facilities in the Bahamas. Since 2006, Mr. D’Aguilar has served as a Director of J.S. Johnson and Company Limited, which is the largest firm of insurance brokers and agents in the Bahamas and is publicly traded on the Bahamas International Stock Exchange (BISX). Since 2009, Mr. D’Aguilar has served as Chairman of the Board of AML Foods Limited, which is the second largest retailer of food in the Bahamas and is publicly traded on the BISX. Since 2008, Mr. D’Aguilar has served as Chairman of the Board of Insurance Company of The Bahamas Limited. Since 2009, Mr. D’Aguilar has served as Honorary Consul to the Kingdom of the Netherlands in the Commonwealth of the Bahamas. From 1987 to 1993, Mr. D’Aguilar served as President of the Bahamas Chamber of Commerce. From 1987 to 1993, Mr. D’Aguilar held various positions at KPMG US.

Mr. D’Aguilar holds a B.S. in Hotel Administration from Cornell University and a Masters of Business Administration (M.B.A.) from Cornell University. He is qualified as a CPA in the State of New York.

Millennium Investment and Acquisition Co. Inc.

© 2011-2016 SeeThruEquity, LLC. Important disclosures appear at the back of this report. 17 | P a g e

Equity | Financial / Asset Management

October 3, 2016

Jesse Derris, Director

Mr. Derris is the CEO of Derris & Company, which he founded in 2012. Derris & Company is a brand strategy and public relations firm headquartered in New York City. Mr. Derris serves as a crisis counselor for major corporations and executives in media, finance, fashion, entertainment and sports, and invests in and advises consumer-facing start-ups at various stages of development. Prior to founding Derris & Company, Mr. Derris had various positions with served as Senior Vice President and Partner at Sunshine Sachs starting in 2005, where he lead the firm’s work in a variety of verticals industries, including finance, crisis, digital, sports and real estate. Prior to Sunshine Sachs, Mr. Derris was associated with Rabinowitz-Dorf Communications, a boutique public relations and public affairs firm in Washington, D.C. Mr. Derris also served as a state spokesman on John Kerry’s 2004 Presidential Campaign.

Mr. Derris holds a B.A. from the University of Wisconsin-Madison.

Kevin McTavish, Director

Kevin McTavish has over 25 years experience in real estate investing including development, distressed debt, and bankruptcies for several widely recognized real estate funds. He also currently serves as Chairman of the Board for Institutional Real Estate, Inc. (IREI). Additionally, from 2003-2007 he served as a member of the Board of Directors of Lodgian, Inc. a publicly traded hotel company. At Lodgian he was Chairman of both the Compensation & Nominating Committees as a member of the Audit Committee. From 1995 - 2003 Mr. McTavish was a Principal at Colony Capital, LLC. He was a member of Investment Committee and Major Asset Review Committee. Colony has invested in and manages nearly $60 billion in real estate assets. As Chief Operating Officer he oversaw the 50 person asset management group responsible for more than 1,000 real estate assets comprising several billion dollars. From 1998-2002 he led Colony’s efforts in establishing offices in Japan & Korea. Additional responsibilities at Colony included Chairman of Aman Resorts and LaHotel Corporation (owner of the L’Ermitage Hotel in Beverly Hills, CA). He was an active member of the Board of Directors for publicly traded Verado Holdings, Inc. – an investment made with Texas Pacific Group and the Donald Sturm Group. Prior to Colony he was a founder of Brazos Asset Management (later renamed Lone Star Opportunity Fund) for the Robert Bass Group.

Mr. McTavish holds an M.B.A. in Real Estate from The Wharton School of Business and a B.S. from the United States Naval Academy (Superintendent’s List, 1980).

Millennium Investment and Acquisition Co. Inc.

© 2011-2016 SeeThruEquity, LLC. Important disclosures appear at the back of this report. 18 | P a g e

Equity | Financial / Asset Management

October 3, 2016

FINANCIAL SUMMARY Figure 7. Income Statement

Figures in $mn unless specified FY15A FY16E FY17E FY18E FY19E

Revenue 0.2 0.3 1.2 18.1 23.8 YoY growth (48.2%) 18.1% 383.2% 1377.3% 31.5%

Cost of sales 0.0 0.0 1.0 9.5 12.1

Gross Profit 0.2 0.3 0.2 8.6 11.7 Margin 100.0% 100.0% 16.2% 47.4% 49.3%

Operating expenses 0.3 0.7 3.2 7.4 8.0

EBIT (0.1) (0.5) (3.0) 1.2 3.7

Margin (46.3%) (183.5%) (244.5%) 6.6% 15.7%

EBITDA (0.1) (0.3) (1.7) 2.9 5.8 Margin (46.3%) (104.7%) (139.4%) 15.8% 24.4%

Other income/ (expense) 15.0 0.0 (0.2) (0.5) (0.5)

Profit before tax 14.9 (0.5) (3.2) 0.7 3.3

Tax 0.0 0.0 0.0 0.0 0.3

Net income 14.9 (0.5) (3.2) 0.7 3.0 Margin 6940.5% (183.5%) (264.1%) 3.7% 12.6%

EPS (per share) 1.79 (0.04) (0.24) 0.05 0.22

Source: SeeThruEquity Research

Figure 8. Balance Sheet

Figures in $mn, unless specified FY15A FY16E FY17E FY18E FY19E

Current assets 3.1 3.6 3.8 5.9 10.8

Intangibles 0.0 0.1 0.1 0.1 0.1

Other assets 22.2 22.5 23.6 22.8 19.3

Total assets 25.4 26.1 27.4 28.8 30.2 Current liabilities 0.2 0.2 0.8 1.3 1.4

Other liabilities 0.1 0.2 2.6 4.8 5.3

Shareholders’ equity 25.1 25.7 24.1 22.7 23.6

Total liab and shareholder equity 25.4 26.1 27.4 28.8 30.2

Source: SeeThruEquity Research

Figure 9. Cash Flow Statement

Figures in $mn, unless specified FY15A FY16E FY17E FY18E FY19E

Cash from operating activities 1.7 (0.4) (2.7) 2.2 4.9

Cash from investing activities 0.0 (0.9) (3.8) (2.0) (0.7)

Cash from financing activities 1.3 1.5 5.0 1.0 0.0

Net inc/(dec) in cash 3.0 0.2 (1.5) 1.2 4.2 Cash at beginning of the year 0.1 3.1 3.4 1.9 3.1

Cash at the end of the year 3.1 3.4 1.9 3.1 7.3

Source: SeeThruEquity Research

Millennium Investment and Acquisition Co. Inc.

© 2011-2016 SeeThruEquity, LLC. Important disclosures appear at the back of this report. 19 | P a g e

Equity | Financial / Asset Management

October 3, 2016

About Millennium Investment and Acquisition Co. Inc.

Millennium Investment and Acquisition Co. Inc. (MIAC) is an internally managed and closed-end asset management firm focusing on investment opportunities in alternative energy. The Company currently holds a 12% stake in SMC Global, an Indian financial services firm. The Company bought an activated-carbon plant in Hawaii on June 9, 2015 and plans to commercialize its activated carbon in the following years. MIAC’s revised investment strategy seeks to expand its portfolio in alternative energy.

For more information, please visit the Company’s website at www.millinvestment.com.

Millennium Investment and Acquisition Co. Inc.

© 2011-2016 SeeThruEquity, LLC. Important disclosures appear at the back of this report. 20 | P a g e

Equity | Financial / Asset Management

October 3, 2016

Contact

Ajay Tandon SeeThruEquity www.seethruequity.com (646) 495-0939 [email protected] Disclosure

This research report has been prepared and distributed by SeeThruEquity, LLC (“SeeThruEquity”) for informational purposes only and does not constitute an offer, solicitation or recommendation to acquire or dispose of any investment or to engage in any transaction. This report is based solely on publicly-available information about the company featured in this report which SeeThruEquity considers reliable, but SeeThruEquity does not represent it is accurate or complete, and it should not be relied upon as such. All information contained in this report is subject to change without notice. This report does not constitute a personal trading recommendation or take into account the particular investment objectives, financial situation or needs of an individual reader of this report, and does not provide all of the key elements for any reader to make an investment decision. Readers should consider whether any information in this report is suitable for their particular circumstances and, if appropriate, seek professional advice, including tax advice. This report contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 that involve risks and uncertainties, many of which are beyond the company’s control. Actual results could differ materially and adversely from those anticipated in such forward-looking statements as a result of certain industry, economic, regulatory or other factors. SeeThruEquity is not a FINRA registered broker-dealer or investment adviser and does not provide investment banking services. SeeThruEquity does not accept or receive fees or other compensation for preparing its research reports. SeeThruEquity has not been retained or hired by the company featured herein or by any other party to prepare this report. In some but not in all instances, SeeThruEquity and/or its officers, directors or affiliates may receive compensation from companies featured in its reports for non report-related services which may include charges for presenting at SeeThruEquity investor conferences, distributing press releases and performing certain other ancillary services. The company featured in this report paid SeeThruEquity its standard fee described below for distributing a press release on this report. Such compensation is received on the basis of a fixed fee and made without regard to the opinions and conclusions in its research reports. The fee to present at SeeThruEquity conferences is no more than seven thousand dollars, and the fee for distributing press releases is no more than fifteen hundred dollars. The fees for performing certain other ancillary services vary depending on the company and service provided but generally do not exceed five thousand dollars. In no event is a company on which SeeThruEquity has issued a report required to engage it with respect to these non report-related services. SeeThruEquity and/or its affiliates may have a long equity position with respect to a non-controlling interest in the publicly traded shares of companies featured in its reports, and follows customary internal trading restrictions pending the release of its reports. SeeThruEquity’s professionals may provide verbal or written market commentary that reflects opinions that are contrary to the opinions expressed in this report. This report and any such commentary belong to SeeThruEquity and are not attributable to the company featured in its reports or other communications. The price and value of a company’s shares referred to in this report may fluctuate. Past performance by one company is not indicative of future results by that company or of any other company covered by a report prepared by SeeThruEquity. This report is being disseminated primarily electronically and, in some cases, in printed form. An electronic report is made simultaneously available to all recipients. The information contained in this report is not incorporated into the contents of our website and should be read independently thereof. Please refer to the Disclosures section of our website for additional details. Copyright 2011-2016 SeeThruEquity, LLC. No part of this material may be (i) copied, photocopied or duplicated in any form or by any means or (ii) redistributed without the prior written consent of SeeThruEquity, LLC.