Embed Size (px)

Citation preview

1

Mihovil Andelinovic

Faculty of Economics and Business Zagreb, Croatia

Ivana Vucemil

Faculty of Economics and Business Zagreb, Croatia

Comparative Fundamental Analysis of Stock Market Indices in Ex-Yugoslavia

Countries

Abstract:

Comparative fundamental analysis of stock market indices in former Yugoslavia in 2011 is

conducted in this paper. The comparison is conducted on the basis of the fundamental indicators

which have been calculated from the financial reports of the companies that are part of the market

index. Fundamental analysis was performed, initially, by making fundamental analysis of each

company’s stock in the index and then, based on the weight of the company’s stock in the market

index, fundamental analysis of the index is performed. For the purpose of thorough comparative

analysis of the markets in Croatia, Slovenia, Serbia, Bosnia and Herzegovina, Montenegro and

Macedonia, the fundamental indicators of investment, liquidity and profitability, which are

considered to give a relevant insight of the stock market, were calculated.

Key Words: Fundamental analysis, Stock exchange, Ex – Yugoslavia, Stock index, Comparative

analysis, Investment decision.

1. INTRODUCTION

Investment decision could be bring on the various bases. Economic theory and practice recognize

plenty of different models which function is to bring quality decision wheter to invest in company’s

stock and/or stock market in analized country, or not. Several authors of such models even won the

Nobel Prize, many analysts were very successful in practice, and many analysts, including some

Nobel Prize winners, failed to recognize market trends and went bankrupt.

Fundamental analysis is one of the most common tools to compare the indicators of different

companies and/or different markets and to bring the investment decision. This paper studies

comparative fundamental analysis of stock market indices in former Yugoslavia in 2011. The aim

of the paper is to compare the stock markets in the countries of former Yugoslavia on the basis of

the fundamental indicators which have been calculated from the financial reports of the companies

that are part of the market index.

Fundamental analysis is performed initially by making fundamental analysis of each company’s

stock in the index and then, based on the weight of the company’s stock in the market index, the

2013 International Journal of Economic Sciences Vol. II (No. 1)

The International Institute of Social and Economic Sciences ISSN 1804-9796

2

fundamental analysis of the index is performed. Research is conducted in following countries:

Croatia, Slovenia, Serbia, Bosnia and Herzegovina, Montenegro and Macedonia. Fundamental

indicators of investment, liquidity and profitability, which are considered to give a relevant

comparison basis, are calculated.

2. STOCK MARKETS IN THE COUNTRIES OF FORMER YUGOSLAVIA

According to Orsag (2003) stronger development of the capital markets in analyzed countries

begins with the exit from the socialism into capitalism. This paper brings an analysis of stock

markets in former Yugoslavia and respective stock indices.

REPUBLIC OF CROATIA - ZAGREB STOCK EXCHANGE

Stock exchange in Croatia was founded in 1991, when 25 banks and 2 insurance companies set

Zagreb Stock Exchange (ZSE) as a central place for stock trading in Republic of Croatia. Members

of ZSE are private brokerage companies and banks. Securities (stocks and bonds) are traded on the

ZSE via electronic trading system (ZSE, 2012).

Brokerage companies that are Exchange members are connected with the Exchange head office via

special telecommunication lines; they enter their sell and buy orders and conclude transactions with

other brokers directly from their offices. This means that the physical place where securities are

traded (traditional trading floor) no longer exists, but rather trading takes place among electronically

connected traders. All member brokers have access to the trading system in real time (with not time

delay/shift) so that they can enjoy equal status with respect to the receipt of information on the

current securities offer at exactly the same time.

According to ZSE (2012) the Exchange is open for trading between 10 a.m. and 4. p.m. every day,

with the exception of holidays, and trading reports with daily stock prices are available to any

interested party in daily newspapers, from specialist financial data vendors as well as on the

Exchange's website and via a specialized exchange information distribution system, named the ZSE

Monitor.

The ZSE Monitor is a system that distributes exchange-related information in real time. It enables

users to access the information on total trade and to monitor current price movements with no delay.

ZSE had used different trading platforms and the new trading platform, NASDAQ OMX's X-

Stream, was launched in autumn 2007.

Stocks trading in ZSE are possible using Regulated Market and Multilateral Trading

Facility (MTF). Regulated market is a trading segment managed by the Zagreb Stock Exchange in

which it is possible to trade listed instruments. As stated by ZSE (2012) the principal difference

between the regulated market and the MTF is in the level of transparency. Transparency involves

the submission of all the information stipulated by law and Exchange Rules concerning the issuer

and the listed financial instruments which may affect the price of the respective instruments.

Regulated market is divided into the following segments:

Prime Market

Official Market

Regular Market

Prime Market is the most demanding market segment with regard to the requirements set before the

issuer, especially in relation to transparency. Regular Market commits the issuer to submit only a

minimum of information stipulated by the Capital Market Act while the Exchange Rules stipulate

additional requirements applicable to the Official and the Prime Market. In addition, when listing

instruments on the regulated market, it is generally necessary to prepare a Prospectus, aimed at

providing the information which may be required for the purpose of instrument evaluation by

investors. Currently, stocks of the 21 stock companies are listed on official market; while stocks of

the 45 stock companies are on regular market.

In accordance with the provisions of the Capital Market Act, the MTF does not have the same status

as the regulated market. In view of lower requirements set before the issuer with regard to

2013 International Journal of Economic Sciences Vol. II (No. 1)

The International Institute of Social and Economic Sciences ISSN 1804-9796

3

the instruments traded on the MTF, the risk of investment into such instruments may be higher than

the risk of investing into the instruments traded on the regulated market. Nevertheless, there is a

minimum of publicly available information on the instruments admitted to trading on the MTF to

enable investors to take well-grounded investment decisions.

The Zagreb Stock Exchange’s MTF is divided into:

Domestic MTF

International MTF

Domestic MTF serves for admission to trading of the instruments whose issuers have a registered

place of business in Croatia, with no obligation of a parallel listing on some other market.

The International MTF serves for admission to trading of the instruments whose issuers are

domiciled in other countries, where the instrument to be admitted to trading must be listed on an

exchange or a regulated market of the respective country. (ZSE 2012)

Basic information to be submitted by the issuers whose instruments trade on the MTF:

invitation to the company’s AGM

annual financial statement

information on capital reduction or capital increase

2.1. Status Changes of the Issuer

STOCK INDICES OF ZAGREB STOCK EXCHANGE In Republic of Croatia exchange indices are differentiated, of which two are stock indices:

CROBEX: it is official ZSE stock index published on September 1, 1997, with base value

1000. Index is weighted by free float adjusted market capitalization, where the weight of any

individual issuer in index is limited to 10% of the index capitalization. If a stock was not

traded on the given day, the previous last price is used (ZSE, 2012).

Stocks are ranked by the market share and the top 25 stocks are selected to be included into

the CROBEX index. Stocks which were traded on more then 90% of the available trading

days in the previous six month period are qualified for CROBEX selection.

In the selection process stocks are ranked by the following two criteria:

1. Free float market capitalization

2. Order book turnover in proceeding 6 month period

According to ZSE (2012) following is not considerd as free float:

Ownership stakes exceeding 5%

Treasury stocks.

CROBEX10: it is an index which was published on September 7, 2009, with base value 1000.

CROBEX10 is weighted by free float adjusted market capitalization, where the weight of any

individual issuer in index is limited to 20% of the index capitalization. If a stock was not traded

on the given day, the previous last price is used. CROBEX10 contains 10 stocks with the

highest free float adjusted market capitalization and trade, included in CROBEX index.

Figure 1: Structure of stock index CROBEX10

STOCKS

NUMBER

OF

STOCKS

FREE FLOAT

MARKET

CAPITALIZATION

WEIGHT

AD PLASTIK ADPL-R-A 2.939.709 298.351.066 5,58%

ADRIS GRUPA ADRS-P-A 5.518.394 1.208.473.102 22,62%

ATLANTIC GRUPA ATGR-R-A 633.517 316.758.500 5,93%

ATLANTSKA PLOVIDBA ATPL-R-A 1.186.192 392.629.552 7,35%

DALEKOVOD DLKV-R-A 1.949.740 251.516.460 4,71%

2013 International Journal of Economic Sciences Vol. II (No. 1)

The International Institute of Social and Economic Sciences ISSN 1804-9796

4

ERICSSON NIKOLA TESLA ERNT-R-A 599.243 647.182.440 12,11%

HRVATSKI TELEKOM HT-R-A 4.610.281 1.115.688.002 20,88%

INGRA INGR-R-A 12.867.940 86.343.877 1,62%

KONČAR-ELEKTROINDUSTRIJA KOEI-R-A 900.242 462.724.388 8,66%

PODRAVKA PODR-R-A 2.439.001 563.409.231 10,54%

Source: www.zse.hr

2.2. REPUBLIC OF SERBIA – Begrade Stock Exchange

Belgrade Stock Exchange has been in operation in the Republic of Serbia since January, 1985. It

performs activities of organizing securities and financial derivatives trade, and includes following:

1. organising securities public offering and connecting securities demand and suply

2. publishing information about securities demand, suply, market price and other significant

data

3. establishing and publishing lists of securities

4. other acitivities in accordance with Law on Capital Market.

As proposed by Beogradska berza (2012) the Belgrade Stock Exchange indices were created for the

purpose of improving the information process and the transparency and comparison of the market

data. The Exchange currently maintains the following two indices:

BELEXline: it is general, “benchmark” index of the Belgrade Stock Exchange, calculated at

the end of a trading day

BELEX15: it is set as leading index of the Belgrade Stock Exchange, describes the

movement of prices of the most liquid Serbian stocks and is calculated in real time.

Stock market is divided on Regulated market and Multilateral Trading Facility (MTF). Regulated

market consists of Prime Listing, Standard Listing and Open Market. Prime Listing contains stocks

of five stock companies and represents first quotation, i.e. quotation A. Standard Listing, i.e.

quotation B, contains stocks of three stock companies, while 217 stock companies are active on

Open Market. The biggest number of stock companies, 963, does business on MTF. With new

Rules on Listing and Quotation, conditions for companies to become the most liquid were made

stricter. Necessary minimum of equity and securities issuers has doubled and now is 20 million

euros. For companies to come to quotation A the time of being active remains the same, three years.

In free trade there have to be at least 25 % of total issued stocks or the equity has to be at least 10

million euros owned by at least 500 shareholders. That is twice the previous stock trading.

Conditions to come to quotation B remain the same, which means the least amount of total equity

has to to be four million euros but being active as a company is reduced from three to two years.

REPUBLIC OF MAKEDONIA – MAKEDONIAN STOCK EXCHANGE

Macedonian Stock Exchange began with work in 1995. Until then the Republic of Macedonia had

never before had a stock exchange. The total number of the initial founders of the Macedonian

Stock Exchange was 19. Although the Exchange was open for trading twice a week (Tuesdays and

Thursdays) in the beginning, it has developed by time, mostly because of the international

cooperation and foreign investments. The most successful year for Macedonian Stock Exchange

was 2007, when it realized record turnover of 41, 7 billions euros and MBI 10 index achieved its

biggest value. According to Macedonian Stock Exchange (2012) one of the most important events

for the year 2007 was signing the Memorandum of partnership between the exchanges in Belgrade,

Skopje, Zagreb and Ljubljana. The partnership primarily aims to contribute towards further

developement the regional and national markets and thus serve the needs of major regional and

international market players. On the Exchange, trading is active on two markets, Official and

Regulated market. Macedonian Stock Exchange contains three indices, of which two refer to stocks:

2013 International Journal of Economic Sciences Vol. II (No. 1)

The International Institute of Social and Economic Sciences ISSN 1804-9796

5

MBID is a stock exchange index that was cretaed in 2007 with based value 10,000. It is a

price index, which elements are being chosen according to the following criteria; number of

trading days and turnover in the period between two revisions of the index.

2.3. MBI10: it is a stock exchange index that was introduced in 2005 with based value 1000. It

represents substitution for former index MBI. It is consisted of up to 10 listed ordinary

stocks, chosen by the Stock Exchange Index Commission, according to the criteria from the

Methodology. REPUBLIC SLOVENIA – Ljubljana Stock Exchange

Ljubljana Stock Exchange was founded in August 1924. As stated by BORZA (2012) upon the

opening of the Exchange, 27 securities were traded, the majority of which were state securities, and

the rest were securities of Slovenian financial institutions and industrial enterprises. After the World

War II the Exchange was banned by decree and started working again after 50 years, in 1988. There

are two stock indices that give information about market position, stock companies and market

fluctuations:

LJSE Composite: it represents general market index including all the stocks listed on the

market. It gives general market overview. Its main purpose is to provide information about

general performances of Slovenian regulated stock market.

The blue-chip SBI TOP index: it is an index which measures the performance of the most

liquid and highly capitalized stocks on the Ljubljana Stock Exchange Market. It was

introduced in 2006 with based value 1000. According to BORZA (2012) the purpose of SBI

TOP is to follow the performance of LJSE’s most important equities and thus serve as

underlying for advanced financial products. Inclusion of stocks into the index increases their

reputation and creates their profile, which results with longer-term liquidity. To be included

in SBITOP index, stock has to fullfil fllowing conditions:

o Minimum free float market capitalization – 50 million euros

o Minimum average daily trading value – 50,000 euros

2.4. REPUBLIC OF MONTENEGRO – Montenegro Stock Exchange

As stated by MONTENEGRO BERZA (2012) Montenegro Stock Exchange was established in June

1993, pursuant to the Law on Money and the Capital Market. The first shareholders of the Stock

Exchange were the Republic of Montenegro and four banks from Montenegro. Since September

2006 the Exchange became completely private ownership, which means that Montenegro

government sold 5% of its ownership for 1,100 euros per share or five times more than nominal

value, which is 1.4 million euros of market capitalization. On December 31, 2010, the two

Montenegrin stock exchanges were integrated, through the merge of the New Securities Exchange

of Montenegro to the Montenegro Stock Exchange.

According to MONTENEGRO BERZA (2012) market on the Montenegro Stock Exchange consists

of Official market and Free market. Official market is a prestigious segment of the market. In order

for issuers to be able to list on the official market, in addition to the general requirements, they must

meet certain criteria regarding the amount of capital, number of shareholders, financial condition

etc. Official market consists of A i B list, which have their extra conditions to fullfil depending on

the list. Free market includes all other securities not included on the official market and trading in

securities that are allocated to the free market is performed by the method of continuous trading.

MONEX20 is Montenegro Stock Exchange index. The Exchange uses market liquidity indicator

while including stock companies into the index. Therefore, index is formed with the most liquid

stocks on market in its structure. According to contemporary stock markets, free float capitalization

was introduced as a base to determine stocks proportion within the index.

2013 International Journal of Economic Sciences Vol. II (No. 1)

The International Institute of Social and Economic Sciences ISSN 1804-9796

6

2.5. REPUBLIC OF BOSNIA AND HERZEGOVINA – Sarajevo and Banja Luka Stock Exchange

2.5.1. Sarajevo Stock Exchange

Sarajevo Stock Exchange was established in September 2001 by eight brokerage houses and it

started trading in 2002. Trading can be done on Official and Free market. As proposed by SASE

(2012) the Official market is the place where “blue-chips”, the highest quality stocks are beeing

traded. In order to be listed at this market segment, an issuer has to meet certain requirements:

Minimum size of capital - 4.000.000 KM

Minimum size of class of stocks - 2.000.000 KM

Listing on the Official market is not just a prestige; it includes many privileges for the issuer. If the

company operates in a transparent and successful way, then investors have confidence in their

management and company has the option of issuing new securities to finance their upcoming

projects. Other benefits for the issuer include less possibility for manipulations of price of their

stocks. If security is listed on the Official market, trading is not possible if the price differs more

than 10% in regards to the last trading day's official price.

Free market consists of primary, secondary and tertiary markets. Primary market consists of 30

most traded stocks that are not listed on the Official market, which satisfy their obligations in

regards to the regulations of the Securities Comission on disclosing the financial reports. Secondary

market consists of the issuers that are not listed on the Official market, do not meet the conditions

for the Primary Free market and are not in the bankruptcy proceedings. Tertiary market consists of

issuers that have open stock company status and do not publish periodical financial reports

regularly. There are three stock indices active on the Exchange:

SASX-10: it is the main index on the Sarajevo Stock Exchange and it depicts the price

movement of the top 10 issuers on the Exchange (excluding investment funds) ranked by

market capitalization and frequency of trading. The index is not limited for one segment

only and issuers from Official and Free market can be included into the index. SASX-10 is

price, weighted index, where the maximum influence of an individual issuer is capped at

20%.

SASX-30: it is price index and it depicts the price movement of the issuers on the Primary

Free market, which is reserved for the most liquid issuers from the Free market. The index is

an unweighted index, where all the consistents have the same influence on the index

movement (SASE, 2012). To be included in the index, an issuer must be listed on the

Primary Free market. The index can include maximum 30 stock companies within its

structure.

BATX: it is an index that observes price movements six largest and most liquidity

companies from Sarajevo and Banja Luka Stock Exchange, which allows this index to serve

as the basis for the issuance of structured products and standardized derivatives. Including

the largest and the most liquid stocks of the Bosnian and Herzegovinian stock market,

BATX index is a tradable/investible index, i.e. it is a basis for indices products. Emission of

new products, based on this index, can significantly increase the liquidity of BH capital

markets.

a) 2.7.2. Banja luka stock exchange

Banja Luka Stock Exchange was founded in 2001 and the first trading was done following year.

According to Banja Luka Stock Exchange (2012) the trading methods that the Exchange uses are

continuous trading and single price auction. Trading on Banja Luka Stock Exchange is performed

on Official and Free market.

To be listed on the Official market stocks have to fullfil general criteria:

They can be used for organized trading

They need to be funded completely

They need to be assignable unlimitedly

2013 International Journal of Economic Sciences Vol. II (No. 1)

The International Institute of Social and Economic Sciences ISSN 1804-9796

7

They need to be issued in immaterial form

In accordance with A and B list stock has to fullfil additional conditions depending on the list.

Stocks listed on the Free market fullfil following general criteria:

They need to be funded completely

They need to be assignable unlimitedly

Including fee need to be paid

Inclusion of stocks on the Free market is performed by issuer request. There were 780 issuers

registered in 2010.

BIRS, the stock index of Serbian Republic, which is Bosnian and Herzegovonian entity, was

formed in 2004. It represents price and weighted index with maximum proportion of 25% per

issuer. Its based value is 1000 and in the begining 11 stock companies were included into the index.

Moreover, BATX index was introduced, which was already explained within the Sarajevo Stock

Exchange.

3. FUNDAMENTAL ANALYSIS OF STOCK MARKET INDICES Fundamental analysis implies thorough analysis of companies’ financial reports and connects with

complete economic analysis of the company’s management capabilities, economic sector the

company is in, and total micro and macroeconomic environment in which the company exists

(Žager, et al., 2008). The aim of the fundamental analysis is to detect stocks which are still

underestimated according to the criteria above. Its task is to recognize positive qualities of the

company analysed, as well as its weaknesses, and to acquire impression of the company’s value, its

assets and business processes. Evaluation of every company is done according to estimated value

of its future gain. Fundamental analysis aims to the future and it stresses company’s business

aspects critical for its existance, primarily security and efficacy. Fundamental indicators are related

to assets structure and their financing, efficacy, liquidity and profitability. Analysis using

fundamental indicators is one of the best known and most often used financial analysis and can give

a valuable insight into the company and point out its strengths and weaknesses. This type of

analysis represents the first part of financial analysis. Connecting items from one or two reports,

respectively bookkeeping and marketing data, shows connection between financial accounts and

enables evaluation of financial position of the company.

Žager, et al. (2008) found several groups of fundamental financial indicators:

A. Business security indicators

(a) Liquidity indicators

(b) Indebtedness indicators

B. Activity indicators or turnover ratios

C. Business efficacy indicators

(a) Economy indicators

(b) Profitability indicators

(c) Investment indicators

Fundamental analysis of stock market indices in former Yugoslavia shown in this paper is based on

the analysis of individual companies contained in stock index of individual country. The analysis

covers stock market indices containing the most liquid stocks of the respective stock market.

For every company fundamental indicators have been calculated based on reports from 2011. The

price of company stock is the price achieved on December 30, 2011. Calculated indicators

multiplied with the company proportion in stock index show fundamental indicators of stock market

index.

The indicators calculated for every company and used in further calculations are:

1. EPS (Earnings per share) – is an indicator showing how much net profit a

company has earned per share. EPS is calculated by dividing net profit (profit after

taxes) with number of regular stocks, subtracted for treasury stocks. It is one of the

2013 International Journal of Economic Sciences Vol. II (No. 1)

The International Institute of Social and Economic Sciences ISSN 1804-9796

8

most important profitability indicators and therefore one of the most used indicators

investors use to value stock growing potential. As investment indicator it shows

company’s ability to attract investments, respectively it expresses its capability to

make profit. High values of EPS indicate company’s efficacy to make profit.

2. P/E ratio (Price-to-earnings ratio) - is an indicator calculated relating actual

market price and earning per share during the business year. Simply, P/E ratio shows

how much the market is willing to pay per share per every unit of net profit,

respectively the price of the stocks in relation to the possible gain if they are sold.

The lower the P/E, the cheaper the stock. It means the stock is undervalued, because

investors pay less per stock making bigger profit selling it. The higher P/E, the more

expensive the stock and the lower its growth potential. (Reilly and Brown, 2003).

3. P/S ratio (Price-to-sales ratio) - is an indicator calculated relating actual market

price and total income per share. It is used to identify underrated/overrated stocks.

The lower P/S, the cheaper the stock, because investors pay less per stock per every

unit of stock income. However, one has to be careful when interpreting this

indicator. Companies near the bankruptcy can also have low P/S ratio.

4. P/B ratio (Price-to-book ratio) - is a ratio of market price and book stock value.

P/B indicates how much the market is willing to pay per stock per every unit of

company book value. As well as other similar indicators (P/E, P/S), it indicates

overvalued/undervalued stock. Values lower than the averages of sector are

desirable. These values indicate possible undervalue of the stocks and as such they

have higher growth potential than the overvalued ones.

5. Total stock profitability - is a ratio of earning per share (EPS) and price per share

(PPS). The higher the ratio, the better and more profitable the investment in stock.

6. Return on assets (ROA) - is the basic indicator of company profitability and it

measures achieved gain per every unit of invested asset. In this way the indicator

shows how big a profit a company can achieve per one unit of asset in its ownership.

Having in mind that the values of these indicators differ from industry to industry, it

is necessary to observe it in relation with the average of sector. The higher the ratio,

industrial standards usually indicate more efficient usage of the resources. ROA

gives investors an insight into how effectively a company invests the money it owns

into investments using its net profit. ROA ratio higher than the average of sector is

considered positive. The higher the ratio, the better it is. That value shows that a

company is more successful than its competition in making profit per every unit of

its asset.

7. Return on equity (ROE) - is an indicator of company’s achievement in turning

shareholders’ money into profit. It indicates how successfully a company uses its

equity to make a profit. It is used to compare profitability of companies in the same

sector. Having in mind that the values of these indicators differ from industry to

industry, it is necessary to observe it in relation with the average of sector. Higher

ROE value shows good profitability. It is desirable to have ROE values higher than

the average of sector. They show that a company is more successful than its

competition in making profit per every unit of its equity.

8. Current ratio – is a ratio of current assets and current liabilities. According to rule-

of-thumb estimates sometimes used by traditional bankers, it is considered that 2:1

ratio of current assets and current liabilities is optimal for company. It is coverage

for current liabilities and to preserve normal liquidity of a company part of current

assets has to bi financed out of quality long-term sources. As with other estimates,

their usage depends on many factors, such as industry branch and its perspectives. If

a company has fast stock turnover and is able to charge its realisation, acceptable

2013 International Journal of Economic Sciences Vol. II (No. 1)

The International Institute of Social and Economic Sciences ISSN 1804-9796

9

ratio of current assets and liabilities can be lower. However, it should not be lower

than 1:1.

9. Financial stability coefficient – is a ratio of long-term assets and equity enlarged

for long-term liabilities. Decrease of coefficient is a positive tendency; it means that

more current assets are financed from long-term funding sources, giving good

estimates for financial stability. If the coefficient is lower than 1 it means that this

short-term assets has to bi financed from long-term sources. If higher than 1 it means

that long-term assets are financed from short-term liabilities or there is working

capital deficit (Žager, et al., 2008).

10. Net profit margin - is a ratio of net profit and income. It is the most precise

indicator of final effects of realised and charged transactions. It shows what

percentage of income remains in the form of profit at our disposal.

11. Interest margin – is an indicator showing the relation between the difference of

interest revenues and expenses, and total assets. It is used in analysis of banks and it

depends on many factors, such as development of financial sector of a country, their

size and position in relation to competition etc. The influence on profit decrease is

the most obvious when the non-profitable assets are financed from interest liabilities.

We get the opposite when non-interest liabilities increase profit if they are used to

finance assets that bring high interests.

Fundamental analysis has been carried for each ex-Yugoslavia country. In the Republic of

Montenegro, company Solana Bajo Sekulić in MONEX20 index, is in bankruptcy. It did not submit

annual report for 2011 and its influence has been disregarded during the indicator calculations.

Earnings per share have been expressed in euros according to exchange rate on December 30, 2011.

The results are following:

2013 International Journal of Economic Sciences Vol. II (No. 1)

The International Institute of Social and Economic Sciences ISSN 1804-9796

10

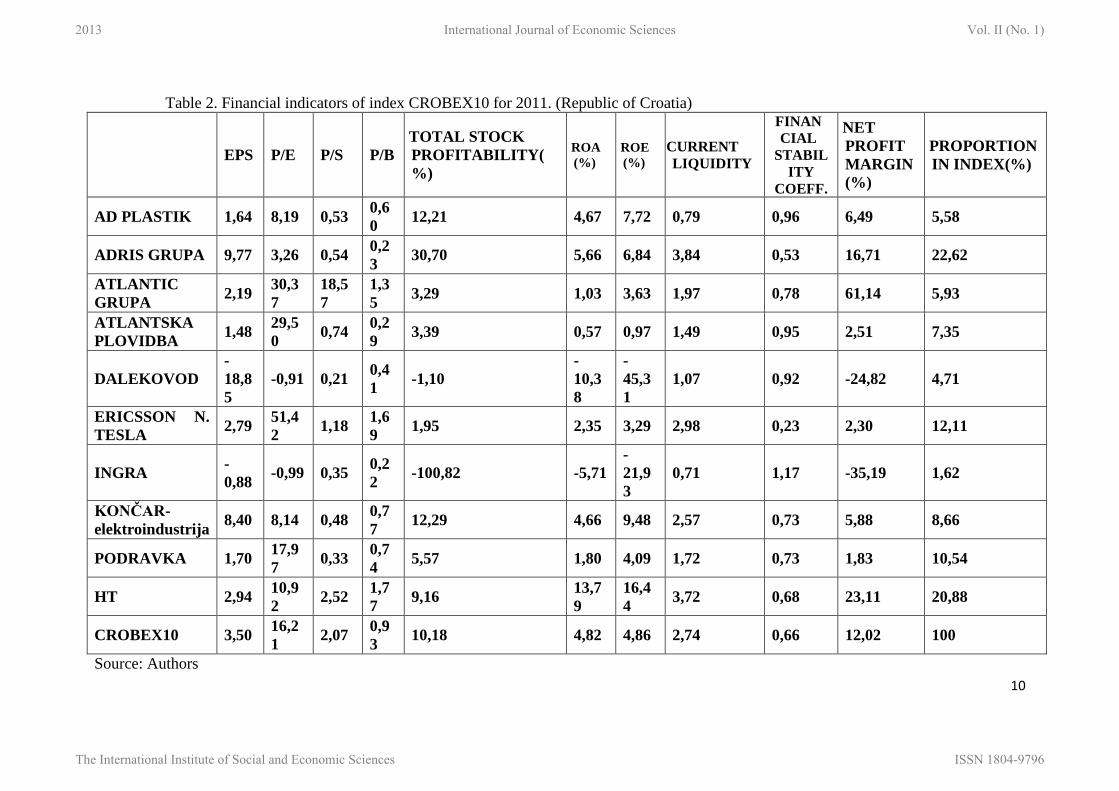

Table 2. Financial indicators of index CROBEX10 for 2011. (Republic of Croatia)

EPS P/E P/S P/B

TOTAL STOCK

PROFITABILITY(

%)

ROA

(%)

ROE

(%)

CURRENT

LIQUIDITY

FINAN

CIAL

STABIL

ITY

COEFF.

NET

PROFIT

MARGIN

(%)

PROPORTION

IN INDEX(%)

AD PLASTIK 1,64 8,19 0,53 0,6

0 12,21 4,67 7,72 0,79 0,96 6,49 5,58

ADRIS GRUPA 9,77 3,26 0,54 0,2

3 30,70 5,66 6,84 3,84 0,53 16,71 22,62

ATLANTIC

GRUPA 2,19

30,3

7

18,5

7

1,3

5 3,29 1,03 3,63 1,97 0,78 61,14 5,93

ATLANTSKA

PLOVIDBA 1,48

29,5

0 0,74

0,2

9 3,39 0,57 0,97 1,49 0,95 2,51 7,35

DALEKOVOD

-

18,8

5

-0,91 0,21 0,4

1 -1,10

-

10,3

8

-

45,3

1

1,07 0,92 -24,82 4,71

ERICSSON N.

TESLA 2,79

51,4

2 1,18

1,6

9 1,95 2,35 3,29 2,98 0,23 2,30 12,11

INGRA -

0,88 -0,99 0,35

0,2

2 -100,82 -5,71

-

21,9

3

0,71 1,17 -35,19 1,62

KONČAR-

elektroindustrija 8,40 8,14 0,48

0,7

7 12,29 4,66 9,48 2,57 0,73 5,88 8,66

PODRAVKA 1,70 17,9

7 0,33

0,7

4 5,57 1,80 4,09 1,72 0,73 1,83 10,54

HT 2,94 10,9

2 2,52

1,7

7 9,16

13,7

9

16,4

4 3,72 0,68 23,11 20,88

CROBEX10 3,50 16,2

1 2,07

0,9

3 10,18 4,82 4,86 2,74 0,66 12,02 100

Source: Authors

2013 International Journal of Economic Sciences Vol. II (No. 1)

The International Institute of Social and Economic Sciences ISSN 1804-9796

11

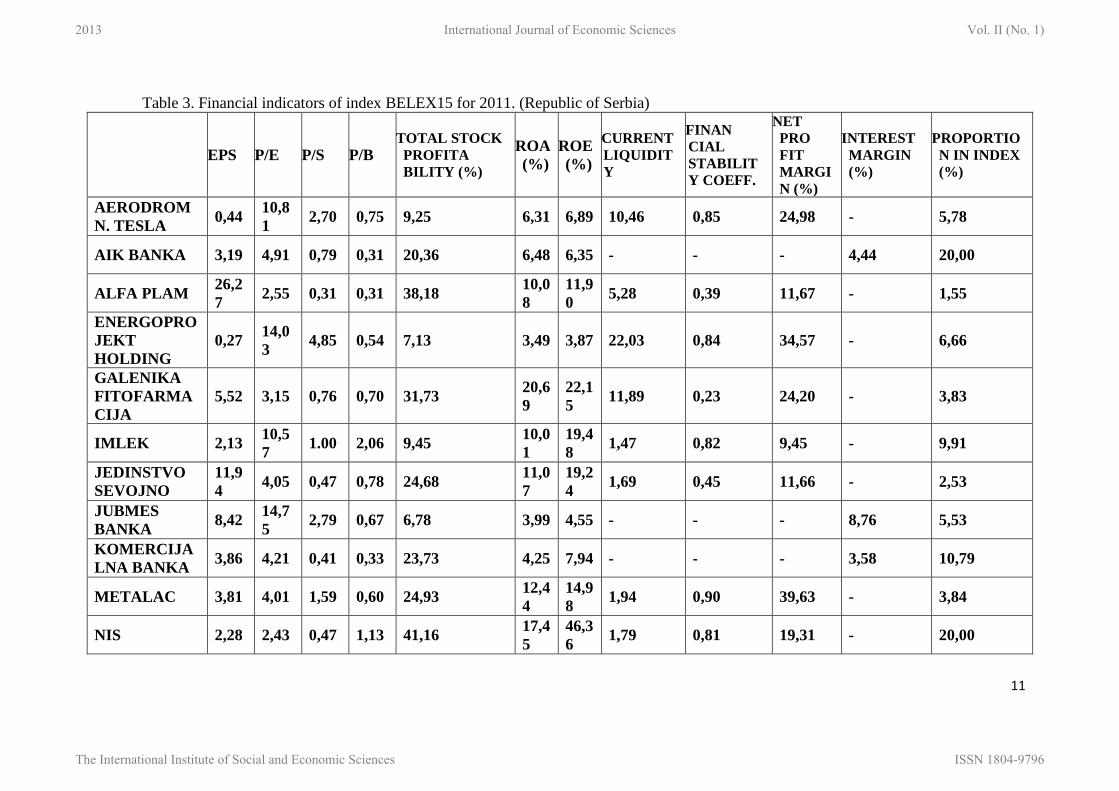

Table 3. Financial indicators of index BELEX15 for 2011. (Republic of Serbia)

EPS P/E P/S P/B TOTAL STOCK

PROFITA

BILITY (%)

ROA

(%)

ROE

(%)

CURRENT

LIQUIDIT

Y

FINAN

CIAL

STABILIT

Y COEFF.

NET

PRO

FIT

MARGI

N (%)

INTEREST

MARGIN

(%)

PROPORTIO

N IN INDEX

(%)

AERODROM

N. TESLA 0,44

10,8

1 2,70 0,75 9,25 6,31 6,89 10,46 0,85 24,98 - 5,78

AIK BANKA 3,19 4,91 0,79 0,31 20,36 6,48 6,35 - - - 4,44 20,00

ALFA PLAM 26,2

7 2,55 0,31 0,31 38,18

10,0

8

11,9

0 5,28 0,39 11,67 - 1,55

ENERGOPRO

JEKT

HOLDING

0,27 14,0

3 4,85 0,54 7,13 3,49 3,87 22,03 0,84 34,57 - 6,66

GALENIKA

FITOFARMA

CIJA

5,52 3,15 0,76 0,70 31,73 20,6

9

22,1

5 11,89 0,23 24,20 - 3,83

IMLEK 2,13 10,5

7 1.00 2,06 9,45

10,0

1

19,4

8 1,47 0,82 9,45 - 9,91

JEDINSTVO

SEVOJNO

11,9

4 4,05 0,47 0,78 24,68

11,0

7

19,2

4 1,69 0,45 11,66 - 2,53

JUBMES

BANKA 8,42

14,7

5 2,79 0,67 6,78 3,99 4,55 - - - 8,76 5,53

KOMERCIJA

LNA BANKA 3,86 4,21 0,41 0,33 23,73 4,25 7,94 - - - 3,58 10,79

METALAC 3,81 4,01 1,59 0,60 24,93 12,4

4

14,9

8 1,94 0,90 39,63 - 3,84

NIS 2,28 2,43 0,47 1,13 41,16 17,4

5

46,3

6 1,79 0,81 19,31 - 20,00

2013 International Journal of Economic Sciences Vol. II (No. 1)

The International Institute of Social and Economic Sciences ISSN 1804-9796

12

SOJA

PROTEIN 0,73 7,36 0,65 0,75 13,58 6,61

10,1

5 3,15 0,06 8,83 - 7,81

TIGAR 0,68 7,24 0,19 0,31 13,81 1,64 4,23 1,00 1,00 2,74 - 0,95

VETERINARS

KI ZAVOD

SUBOTICA

0,29 10,5

0 0,23 0,28 9,52 1,97 2,66 2,72 0,67 2,20 - 0,81

BELEX15 3,36 6,49 1,19 0,78 21,84 9,31 17,1

9 3,51 0,43 12,20 1,76 100

Source: Authors

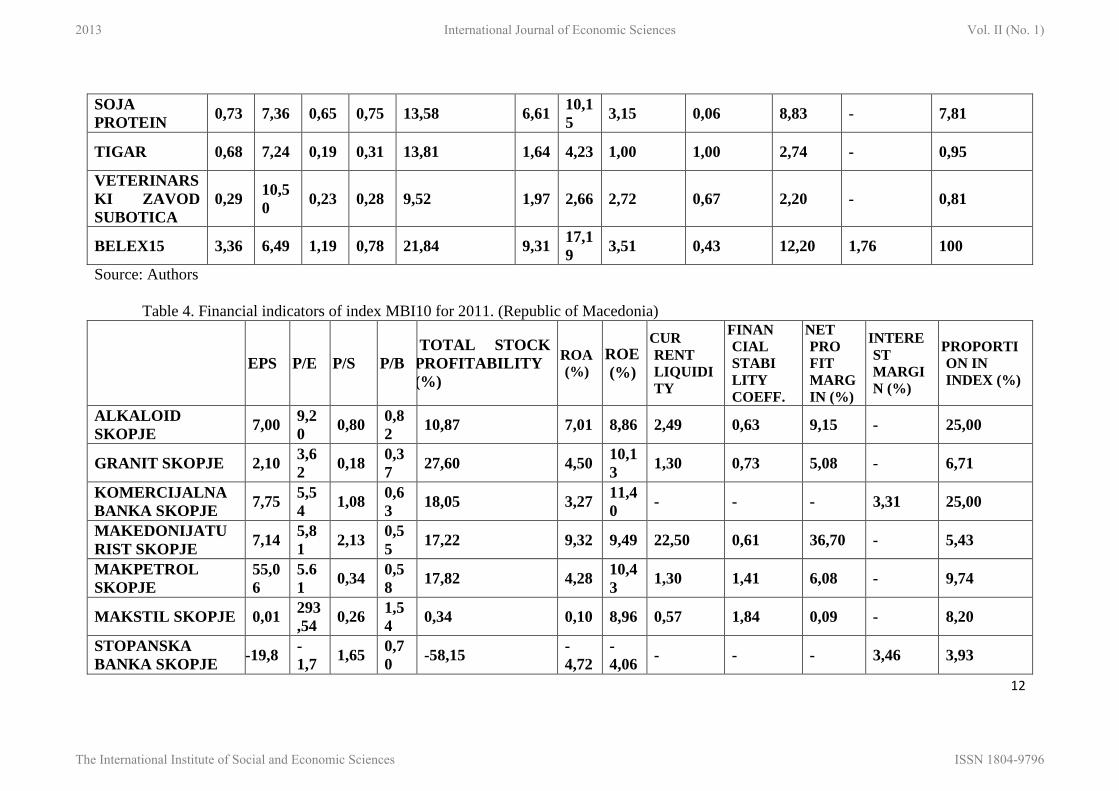

Table 4. Financial indicators of index MBI10 for 2011. (Republic of Macedonia)

EPS P/E P/S P/B

TOTAL STOCK

PROFITABILITY

(%)

ROA

(%) ROE

(%)

CUR

RENT

LIQUIDI

TY

FINAN

CIAL

STABI

LITY

COEFF.

NET

PRO

FIT

MARG

IN (%)

INTERE

ST

MARGI

N (%)

PROPORTI

ON IN

INDEX (%)

ALKALOID

SKOPJE 7,00

9,2

0 0,80

0,8

2 10,87 7,01 8,86 2,49 0,63 9,15 - 25,00

GRANIT SKOPJE 2,10 3,6

2 0,18

0,3

7 27,60 4,50

10,1

3 1,30 0,73 5,08 - 6,71

KOMERCIJALNA

BANKA SKOPJE 7,75

5,5

4 1,08

0,6

3 18,05 3,27

11,4

0 - - - 3,31 25,00

MAKEDONIJATU

RIST SKOPJE 7,14

5,8

1 2,13

0,5

5 17,22 9,32 9,49 22,50 0,61 36,70 - 5,43

MAKPETROL

SKOPJE

55,0

6

5.6

1 0,34

0,5

8 17,82 4,28

10,4

3 1,30 1,41 6,08 - 9,74

MAKSTIL SKOPJE 0,01 293

,54 0,26

1,5

4 0,34 0,10 8,96 0,57 1,84 0,09 - 8,20

STOPANSKA

BANKA SKOPJE -19,8

-

1,71,65

0,7

0 -58,15

-

4,72

-

4,06 - - - 3,46 3,93

2013 International Journal of Economic Sciences Vol. II (No. 1)

The International Institute of Social and Economic Sciences ISSN 1804-9796

13

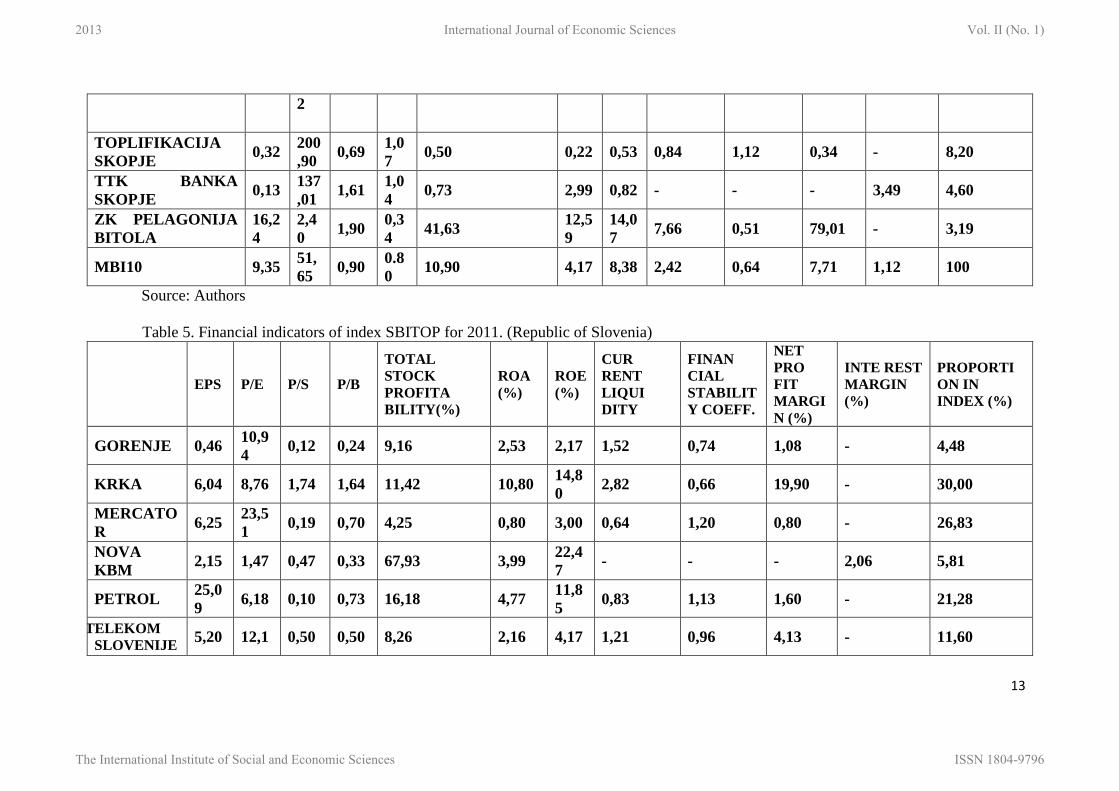

2

TOPLIFIKACIJA

SKOPJE 0,32

200

,90 0,69

1,0

7 0,50 0,22 0,53 0,84 1,12 0,34 - 8,20

TTK BANKA

SKOPJE 0,13

137

,01 1,61

1,0

4 0,73 2,99 0,82 - - - 3,49 4,60

ZK PELAGONIJA

BITOLA

16,2

4

2,4

0 1,90

0,3

4 41,63

12,5

9

14,0

7 7,66 0,51 79,01 - 3,19

MBI10 9,35 51,

65 0,90

0.8

0 10,90 4,17 8,38 2,42 0,64 7,71 1,12 100

Source: Authors

Table 5. Financial indicators of index SBITOP for 2011. (Republic of Slovenia)

EPS P/E P/S P/B

TOTAL

STOCK

PROFITA

BILITY(%)

ROA

(%)

ROE

(%)

CUR

RENT

LIQUI

DITY

FINAN

CIAL

STABILIT

Y COEFF.

NET

PRO

FIT

MARGI

N (%)

INTE REST

MARGIN

(%)

PROPORTI

ON IN

INDEX (%)

GORENJE 0,46 10,9

4 0,12 0,24 9,16 2,53 2,17 1,52 0,74 1,08 - 4,48

KRKA 6,04 8,76 1,74 1,64 11,42 10,80 14,8

0 2,82 0,66 19,90 - 30,00

MERCATO

R 6,25

23,5

1 0,19 0,70 4,25 0,80 3,00 0,64 1,20 0,80 - 26,83

NOVA

KBM 2,15 1,47 0,47 0,33 67,93 3,99

22,4

7 - - - 2,06 5,81

PETROL 25,0

9 6,18 0,10 0,73 16,18 4,77

11,8

5 0,83 1,13 1,60 - 21,28

TELEKOM

SLOVENIJE 5,20 12,1 0,50 0,50 8,26 2,16 4,17 1,21 0,96 4,13 - 11,60

2013 International Journal of Economic Sciences Vol. II (No. 1)

The International Institute of Social and Economic Sciences ISSN 1804-9796

14

SBITOP 9,58 12,2 0,68 0,92 13,32 5,07 9,65 1,40 0,90 7,05 0,12 100

Source: Authors

Table 6. Financial indicators of index MONEX20 for 2011. (Republic of Montenegro)

EPS P/E P/S P/B TOTAL STOCK

PROFITABILI

TY(%)

ROA

(%)

ROE

(%)

CURRENT

LIQUIDI

TY

FINAN

CIAL

STABILIT

Y COEFF.

NET

PRO

FIT

MARGI

N (%)

INTEREST

MARGIN

(%)

PROPOR

TION IN

INDEX (%)

13 JUL

PLANTAŽE

PODGORICA

0,02 12,8

6

0,8

7 0,37 7,78

21,2

2 2,84 1,88 0,82 6,75 - 6,61

BUDVANSKA

RIVIJERA 0,11

24,4

7

0,6

7 0,14 3,85 0,52 0,58 4,59 0,99 2,59 - 2,73

CRNOGORSKI

TELEKOM 0,35 7,74

1,0

6 0,77 12,92 8,38 9,91 2,56 0,74 13,74 - 19,90

ELEKTROPRIV

REDA CRNE

GORE

-0,53 -

5,09

1,2

0 0,39 -19,66

-

6,34

-

7,75 2,04 0,94 -23,59 - 3,98

HIPOTEKARNA

BANKA

48,6

2

13,3

7

1,3

2 0,88 7,48 3,47 6,59 - - - 4,84 5,96

HTP

PRIMORIJE

TIVAT

-0,39

-

12,9

3

2,9

8 0,50 -7,73

-

3,79

-

3,89 21,27 0,66 -23,04 - 1,65

INSTITUT SIMO

MILOSEVIC -2,72

-

12,1

3

1,2

0 0,21 -8,25

-

1,47

-

1,71 0,83 1,02 -9,90 - 1,52

JADRANSKO

BRODOGRADIL

IŠTE

-1,11 -

1,30

0,1

4 0,09 -76,99

-

3,45

-

6,73 0,51 1,22 -10,77 - 0,67

2013 International Journal of Economic Sciences Vol. II (No. 1)

The International Institute of Social and Economic Sciences ISSN 1804-9796

15

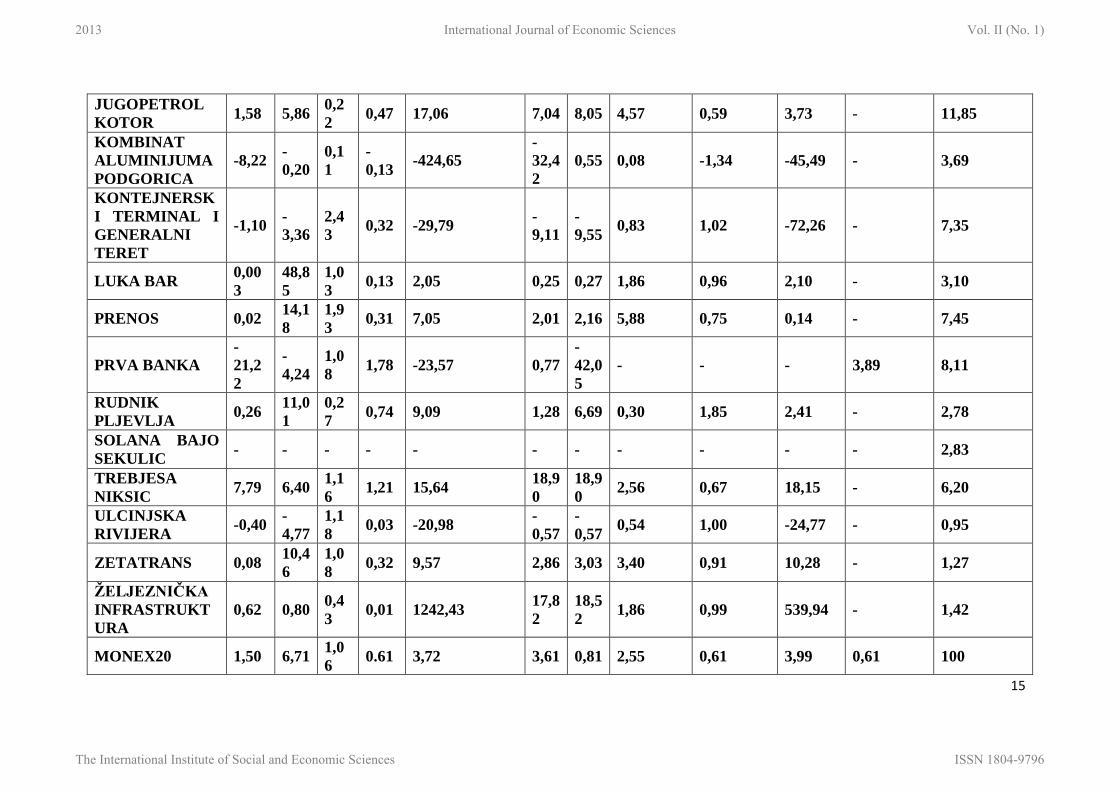

JUGOPETROL

KOTOR 1,58 5,86

0,2

2 0,47 17,06 7,04 8,05 4,57 0,59 3,73 - 11,85

KOMBINAT

ALUMINIJUMA

PODGORICA

-8,22 -

0,20

0,1

1

-

0,13 -424,65

-

32,4

2

0,55 0,08 -1,34 -45,49 - 3,69

KONTEJNERSK

I TERMINAL I

GENERALNI

TERET

-1,10 -

3,36

2,4

3 0,32 -29,79

-

9,11

-

9,55 0,83 1,02 -72,26 - 7,35

LUKA BAR 0,00

3

48,8

5

1,0

3 0,13 2,05 0,25 0,27 1,86 0,96 2,10 - 3,10

PRENOS 0,02 14,1

8

1,9

3 0,31 7,05 2,01 2,16 5,88 0,75 0,14 - 7,45

PRVA BANKA

-

21,2

2

-

4,24

1,0

8 1,78 -23,57 0,77

-

42,0

5

- - - 3,89 8,11

RUDNIK

PLJEVLJA 0,26

11,0

1

0,2

7 0,74 9,09 1,28 6,69 0,30 1,85 2,41 - 2,78

SOLANA BAJO

SEKULIC - - - - - - - - - - - 2,83

TREBJESA

NIKSIC 7,79 6,40

1,1

6 1,21 15,64

18,9

0

18,9

0 2,56 0,67 18,15 - 6,20

ULCINJSKA

RIVIJERA -0,40

-

4,77

1,1

8 0,03 -20,98

-

0,57

-

0,57 0,54 1,00 -24,77 - 0,95

ZETATRANS 0,08 10,4

6

1,0

8 0,32 9,57 2,86 3,03 3,40 0,91 10,28 - 1,27

ŽELJEZNIČKA

INFRASTRUKT

URA

0,62 0,80 0,4

3 0,01 1242,43

17,8

2

18,5

2 1,86 0,99 539,94 - 1,42

MONEX20 1,50 6,71 1,0

6 0.61 3,72 3,61 0,81 2,55 0,61 3,99 0,61 100

2013 International Journal of Economic Sciences Vol. II (No. 1)

The International Institute of Social and Economic Sciences ISSN 1804-9796

16

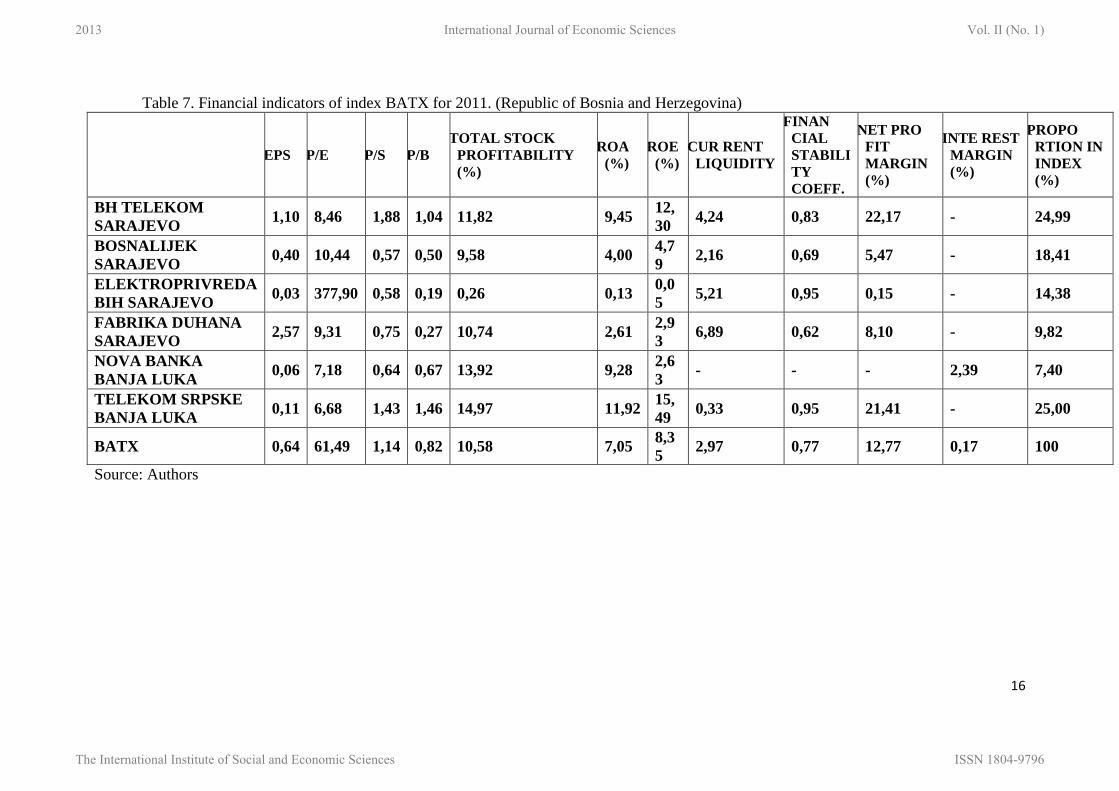

Table 7. Financial indicators of index BATX for 2011. (Republic of Bosnia and Herzegovina)

EPS P/E P/S P/B

TOTAL STOCK

PROFITABILITY

(%)

ROA

(%)

ROE

(%)

CUR RENT

LIQUIDITY

FINAN

CIAL

STABILI

TY

COEFF.

NET PRO

FIT

MARGIN

(%)

INTE REST

MARGIN

(%)

PROPO

RTION IN

INDEX

(%)

BH TELEKOM

SARAJEVO 1,10 8,46 1,88 1,04 11,82 9,45

12,

30 4,24 0,83 22,17 - 24,99

BOSNALIJEK

SARAJEVO 0,40 10,44 0,57 0,50 9,58 4,00

4,7

9 2,16 0,69 5,47 - 18,41

ELEKTROPRIVREDA

BIH SARAJEVO 0,03 377,90 0,58 0,19 0,26 0,13

0,0

5 5,21 0,95 0,15 - 14,38

FABRIKA DUHANA

SARAJEVO 2,57 9,31 0,75 0,27 10,74 2,61

2,9

3 6,89 0,62 8,10 - 9,82

NOVA BANKA

BANJA LUKA 0,06 7,18 0,64 0,67 13,92 9,28

2,6

3 - - - 2,39 7,40

TELEKOM SRPSKE

BANJA LUKA 0,11 6,68 1,43 1,46 14,97 11,92

15,

49 0,33 0,95 21,41 - 25,00

BATX 0,64 61,49 1,14 0,82 10,58 7,05 8,3

5 2,97 0,77 12,77 0,17 100

Source: Authors

2013 International Journal of Economic Sciences Vol. II (No. 1)

The International Institute of Social and Economic Sciences ISSN 1804-9796

17

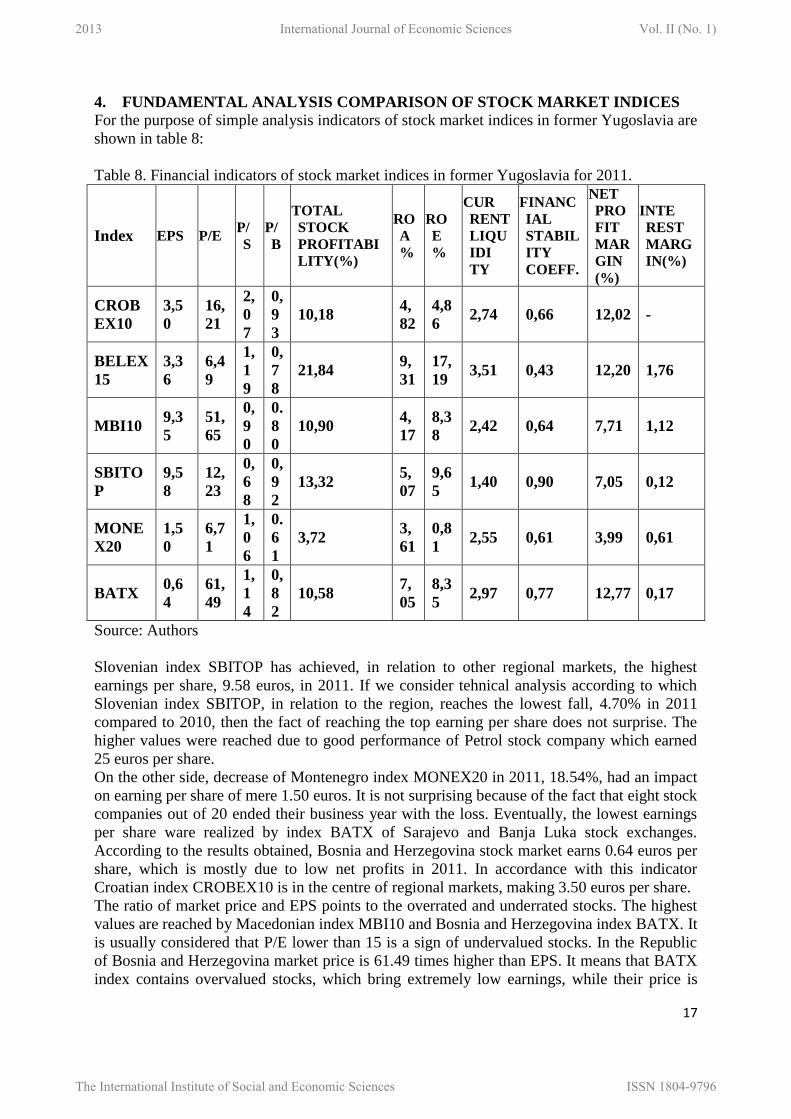

4. FUNDAMENTAL ANALYSIS COMPARISON OF STOCK MARKET INDICES

For the purpose of simple analysis indicators of stock market indices in former Yugoslavia are

shown in table 8:

Table 8. Financial indicators of stock market indices in former Yugoslavia for 2011.

Index EPS P/E P/

S

P/

B

TOTAL

STOCK

PROFITABI

LITY(%)

RO

A

%

RO

E

%

CUR

RENT

LIQU

IDI

TY

FINANC

IAL

STABIL

ITY

COEFF.

NET

PRO

FIT

MAR

GIN

(%)

INTE

REST

MARG

IN(%)

CROB

EX10

3,5

0

16,

21

2,

0

7

0,

9

3

10,18 4,

82

4,8

6 2,74 0,66 12,02 -

BELEX

15

3,3

6

6,4

9

1,

1

9

0,

7

8

21,84 9,

31

17,

19 3,51 0,43 12,20 1,76

MBI10 9,3

5

51,

65

0,

9

0

0.

8

0

10,90 4,

17

8,3

8 2,42 0,64 7,71 1,12

SBITO

P

9,5

8

12,

23

0,

6

8

0,

9

2

13,32 5,

07

9,6

5 1,40 0,90 7,05 0,12

MONE

X20

1,5

0

6,7

1

1,

0

6

0.

6

1

3,72 3,

61

0,8

1 2,55 0,61 3,99 0,61

BATX 0,6

4

61,

49

1,

1

4

0,

8

2

10,58 7,

05

8,3

5 2,97 0,77 12,77 0,17

Source: Authors

Slovenian index SBITOP has achieved, in relation to other regional markets, the highest

earnings per share, 9.58 euros, in 2011. If we consider tehnical analysis according to which

Slovenian index SBITOP, in relation to the region, reaches the lowest fall, 4.70% in 2011

compared to 2010, then the fact of reaching the top earning per share does not surprise. The

higher values were reached due to good performance of Petrol stock company which earned

25 euros per share.

On the other side, decrease of Montenegro index MONEX20 in 2011, 18.54%, had an impact

on earning per share of mere 1.50 euros. It is not surprising because of the fact that eight stock

companies out of 20 ended their business year with the loss. Eventually, the lowest earnings

per share ware realized by index BATX of Sarajevo and Banja Luka stock exchanges.

According to the results obtained, Bosnia and Herzegovina stock market earns 0.64 euros per

share, which is mostly due to low net profits in 2011. In accordance with this indicator

Croatian index CROBEX10 is in the centre of regional markets, making 3.50 euros per share.

The ratio of market price and EPS points to the overrated and underrated stocks. The highest

values are reached by Macedonian index MBI10 and Bosnia and Herzegovina index BATX. It

is usually considered that P/E lower than 15 is a sign of undervalued stocks. In the Republic

of Bosnia and Herzegovina market price is 61.49 times higher than EPS. It means that BATX

index contains overvalued stocks, which bring extremely low earnings, while their price is

2013 International Journal of Economic Sciences Vol. II (No. 1)

The International Institute of Social and Economic Sciences ISSN 1804-9796

18

unusually high. This is supported by the fact that four stock companies out of six earn less

than one euro per share.

The above is followed by Macedonian index MBI10. High value according to which market

price is 51.65 times higher than EPS, MBI10 index accomplishes mostly due to extremely low

net profits of Makstil and Toplifikacija companies and TTK bank, which have relatively high

proportion in the index structure.

Serbian index BELEX15 and Montenegro index MONEX20 show the lowest P/E values.

However, MONEX20 P/E indicator is not relevant in this case considering many companies

within the index, showed a loss in 2011, which directly decreases indicator values not

providing correct information on overvaluation and undervaluation of their stocks. We can

therefore say there are extremely underrated stocks only within Belgrade index BELEX15,

whose price is just 6.48 times higher than EPS. SBITOP and CROBEX10 indices achieve

average values showing potential undervaluation of stocks.

To provide analysis of stocks overvaluation and undervaluation, P/S and P/B ratios are carried

out. These indicators do not bring the same results as those shown in P/E ratio. Macedionian

index MBI10 showing extremely high P/E ratio indicating overvaluation of stocks, shows

different results based on P/S ratio, 0.90, and P/B ratio, 0.80. In other words, investors pay

0.90 of monetary unit per every unit of income per share and 0.80 per every unit of company

book value respectively. These results indicate stock undervaluation within the MBI10 index.

Of all regional indices, Slovenian SBITOP index is the most underrated and its P/S ratio,

which is 0.68, and P/B ratio, which is 0.92, are in accordance with P/E ratio. P/S and P/B

ratios follow the P/E ratio in the case of Belgrade index also and show stock undervaluatiom

within the BELEX15 index. According to P/S and P/B ratios Croatian index CROBEX10

indicates stock overvaluation in relation to the other stock exchange indices in the region and

it has the highest values. Market price is 2.07 times higher than the income per share and 0.93

higher than the company book value per share respectively.

The most significant investment indicator is stock profitability because one uses market

values and not book values in its calculations. It is very important information for investors.

Total stock profitability has been calculated in this paper. Belgrade index BELEX15 achieves

the highest total stock profitability, 21.84%. It indicates positive effect of financial leverage

and companies’ business stability. The lowest total stock profitability, 3.72%, is realized by

Montenegro index MONEX20. Ragarding poor business results this profitability could be

expected. Other indices have achieved satisfactory values within 8-14%.

Provided total stock profitability is connected with rentability on assets, which is a ratio of net

profit and total assets, significant differences can be seen. They are achieved because

rentability on assets calculation uses book values. ROA is a good indicator for investors but

insufficient for company evaluation. The lowest ROA value, 3.61%, is achieved by

Montenegro index MONEX20 and that result is in accordance with the results mentioned

above which show negative index position in 2011. However, calculations of this indicator

point out Serbian index BELEX15, which has the highest ROA ratio, followed by Bosnian

and Herzegovinian BATX. Precisely, BELEX15 realizes 9.31% of net profit per every asset

unit, while BATX realizes 7.05%. Macedonian, Croatian and Slovenian indices ahieve ROA

value within 3-7%.

Rentability on equity is in accordance with rentability on assets, so index values rank almost

as in the case above. BELEX15 achieves the highest ROE value, 17.19%, followed by

MBI10, 8.38%. These results indicate efficient use of shareholders resources which gives

certain security to potential investors. MONEX20 continues to show low results with ROE

ratio 0.81%, which means companies within the index earn 0.81% per every unit of equity.

2013 International Journal of Economic Sciences Vol. II (No. 1)

The International Institute of Social and Economic Sciences ISSN 1804-9796

19

Croatian index CROBEX10 does not show good results while calculating this indicator.

Precisely, it realizes ROE ratio 4,86%.

Two indicators that measure liquidity, company’s ability to cover its due short-term liabilities

are calculated. Current liquidity and financial stability coefficient have been calculated for

that purpose. Current liquidity is a ratio of current assets and current liabilities, so the optimal

ratio is 2:1. All the indices in this region show high values, with the most liquid companies in

BELEX15 index with ratio 3.51, and of BATX index with ratio 2.97. The least liquid

companies are those of Slovenian index SBITOP with current liquidity coefficient 1.40. It

indicates potential problems with covering due short-term liabilities.

Financial stability coefficient by default has to be lower than 1 because part of current assets

has to be financed from long-term resources. All indices in former Yugoslavia have values

less than 1, where stocks of Belgrade index BELEX15 have the lowest value, 0.43. It

indicates the highest financial stability and liquidity in relation to stocks within indices of

countries of former Yugoslavia. On the other side, the financial stability coefficient, 0.90,

shown by stocks within Slovenian index SBITOP, is acceptable and desirable. However, they

ensure the lowest financial stability in relation to other stocks within indices of former

Yugoslavia. One should consider the fact that financial reports of banks within the index were

insufficient for current liquidity and financial stability coefficients so they were left out of the

calculations.

To show company profitability as well as the index, net profit margin and interest margin

indicators have been calculated. Interest margin refers to banks. The highest net profit margin

was realized by Bosnian and Herzegovinian index BATX, 12.77%, which means that 12.77%

of total revenues can be used for future investment. BATX is followed by BELEX15, with

value of 12.20%, and CROBEX10 with value of 12.02%. The least resources to be used from

total revenues remain in Motenegro, where the net profit margin is 3.99%. SBITOP and

MBI10 indices reached acceptable values of net profit margin of about 7%.

According to interest margin, the most profitable is Serbian market with value 1.76%, while

the least profitable is Slovenian market with value 0.12%. Analizing this indicator one should

take in the consideration the number of banks within the index and with what proportion.

Therefore, the highest interest margin value of BELEX15 is the result of the high proportion

of three banks within the index. On the other hand, Slovenian market has a bank within the

index SBITOP with low proportion so the interest margin value is extremely low. To avoid

this, it is necessary to consider more indicators to get wider general conclusion.

5. CONCLUSION

This paper shows fundamental analysis of stock market indices in former Yugoslavia. It has

been done firstly with fundamental analysis of companies within the indices and,

consequently, the fundamental analysis of indices, based on companies’ proportion in the

index, has been made. For better overview of differences between Croatian, Slovenian,

Serbian, Bosnian and Herzegovinian, Montenegro and Macedonian market, investment,

liquidity and profitability indicators have been calculated for 2011.

Serbian market, Belgrade stock market respectively, provided the best business picture and

security of investment. It shows very good results in all the calculated indicators. Stocks

within the Serbian index BELEX15 show high values in calculations of stock profitability,

rentability on assets (ROA), rentability on equity (ROE), net profit margin and interest

margin.

Unlike Belgrade stock market, Montenegro market proved to be the most unfavorable market.

It gave negative results in all segments. While stocks of index MONEX20 show low earnings

2013 International Journal of Economic Sciences Vol. II (No. 1)

The International Institute of Social and Economic Sciences ISSN 1804-9796

20

per share, they also show extremely low values in stocks profitability, rentability on assets

and on equity, in relation to stocks within the indices in other countries of former Yugoslavia.

Croatian, Slovenian, Bosnian and Herzegovinian and Macedonian stock markets vary from

indicator to indicator while at the same time Bosnian and Herzegovinian index shows slightly

better results within those named here. However, markets yield relatively good results despite

economic and financial crisis and have growth potential in the following years.

LITERATURE

Books:

1. Orsag, S., 2003. Vrijednosni papiri. Sarajevo: Revicon.

2. Žager, L. et al., 2008. Analiza financijskih izvještaja. 2nd ed. Zagreb. Masmedia.

3. Reilly, F.K., Brown, C.K., 2003. Investment Analysis and Portfolio Management. 7.

ed. Thomson: South-Western.

Websites:

1. Zse.hr, 2012. Croatian Stock Exchange History. [online] Available at:

<http://zse.hr/default.aspx?id=32877> (Accessed 04 July 2012)

2. Zse.hr, 2012. MTF: About MTF. [online] Available at:

<http://zse.hr/default.aspx?id=36803> (Accessed 04 July 2012)

3. Zse.hr, 2012. Trading data and statistics: Indices. [online] Available at:

<http://zse.hr/default.aspx?id=109> (Accessed 04 July 2012)

4. Belex.rs, 2012. Products and services: Indices. [online] Available at:

<http://www.belex.rs/eng/proizvodi_i_usluge/indeksi_opste> (Accessed 05 July 2012)

5. Mse.mk, 2012. About MSE: History. [online] Available at:

<http://www.mse.mk/en/content/22/1/2008/history> (Accessed 05 July 2012)

6. Ljse.si, 2012. About LJSE: History. [online] Available at: <http://www.ljse.si/cgi-

bin/jve.cgi?doc=2327> (Accessed 06 July 2012)

7. Ljse.si, 2012. Products and services: Indices. [online] Available at:

<http://www.ljse.si/cgi-bin/jve.cgi?doc=8340> (Accessed 06 July 2012)

8. Montenegroberza.com, 2012. About us: General data: About MNSE. [online]

Available at: <http://www.montenegroberza.com/code/navigate.asp?Id=944>

(Accessed 07 July 2012)

9. Montenegroberza.com, 2012. Market: Organization of the market. [online] Available

at: <http://www.montenegroberza.com/code/navigate.asp?Id=905> (Accessed 07 July

2012)

10. Sase.ba, 2012. Market: Organization of the market: Market structure. [online]

Available at: <http://195.222.43.81/sase-final/language/en-

US/Market/Organization_of_the_Market/Market_Structure.aspx> (Accessed 07 July

2012)

11. Sase.ba, 2012. Market: Index: Index SASX-30. [online] Available at:

<http://195.222.43.81/sase-final/language/en-US/Market/Index/Index_SASX-

30.aspx> (Accessed 07 July 2012)

12. Blberza.com, 2012. About us: Trading system. [online] Available at:

<http://www.blberza.com/v2/Pages/docview.aspx?page=sp6> (Accessed 08 July

2012)

2013 International Journal of Economic Sciences Vol. II (No. 1)

The International Institute of Social and Economic Sciences ISSN 1804-9796

![Sveti Mihovil 2018. - HPS Mini GP · 2018. 10. 14. · Sveti Mihovil 2018.- HPS Mini GP ŠIBENIK 13.10.2018. 14.10.2018. od god. [from YOB] do god. [to YOB] 9. 100m SLOBODNO, Plivačice](https://img.pdfslide.us/doc/110x75/610f1d1e62153716247dc33a/sveti-mihovil-2018-hps-mini-gp-2018-10-14-sveti-mihovil-2018-hps-mini.jpg)