Embed Size (px)

Citation preview

MIDDL E M ARKE T ON S T RONG PACE UPPER MIDDL E M ARKE T P OISED F OR BIG Y E AR

League TablesPAGE 14»

MIDDLEMARKETREPORT

3Q 2015

U.S.

S P O N S O R E D B Y

Fundraising ActivityPAGE 12-13»

Built for growth.Communicate. Commit. Deliver.™

To learn more about our � nancial strength and disciplined approach, call 312-596-6900 or visit mc� lc.com.MANUFACTURING | DISTRIBUTION | SERVICES | CONSUMER PRODUCTS | HEALTHCARE | INSURANCE/FINANCIAL SERVICES | AEROSPACE & DEFENSE | TECHNOLOGY SERVICES

© 2015 NYL Investors LLC. All rights reserved. Madison Capital Funding is a division of NYL Investors LLC. MC007-15 34752 10/16

We have the longevity, products, and expertise to support your transactions from start to � nish.

Undisclosed

Sole Lead Arranger and Administrative AgentAdd-on Acquisition

May 2015

$67,500,000

Sole Lead Arranger and Administrative AgentAdd-on Acquisition

June 2015

$82,000,000

Co-Lead Arranger and Administrative AgentAdd-on Acquisition

June 2015

$108,400,000

Co-Lead Arranger and Co-Syndication Agent

Add-on Acquisition

June 2015

$179,000,000

Co-Lead Arranger and Administrative AgentAdd-on Acquisition

June 2015

Undisclosed

Syndication Agent

Add-on Acquisition

April 2015

$142,000,000

Sole Lead Arranger and Administrative AgentAdd-on Acquisition

March 2015

Undisclosed

Sole Lead Arranger and Administrative AgentAdd-on Acquisition

March 2015

Undisclosed

Sole Lead Arranger and Administrative AgentAdd-on Acquisition

June 2015

Sole Lead Arranger and

Consumer Products Company

$332,600,000

Administrative Agent

Add-on Acquisition

June 2015Private Equity

Company

Undisclosed

Sole Lead Arranger and Administrative AgentAdd-on Acquisition

April 2015

$57,900,000

Syndication Agent

Add-on Acquisition

July 2015

CONTENTSIntroduction

Middle Market Overview

Activity by Region

Middle Market Breakdown

Exit Activity

Fundraising Activity

League Tables

Methodology

4

5

7

8-10

11

12-13

14

15

CREDITS & CONTACT

PitchBook Data, Inc.

JOHN GABBERT Founder, CEO

ADLEY BOWDEN Senior Director, Analysis

Content, Design, Editing & Data

ALEX LYKKEN Editor

ANDY WHITE Lead Data Analyst

DANIEL COOK Senior Data Analyst

GARRETT BLACK Senior Financial Writer

NIZAR TARHUNI Financial Writer

BRIAN LEE Data Analyst

CHELSEA HARRIS Data Analyst

JENNIFER SAM Senior Graphic Designer

JESS CHAIDEZ Graphic Designer

Contact PitchBook

www.pitchbook.com

RESEARCH

EDITORIAL

SALES

COPYRIGHT © 2015 by PitchBook Data, Inc. All rights reserved. No part of this publication may be reproduced in any form or by any means—graphic, electronic, or mechanical, including photocopying, recording, taping, and information storage and retrieval systems—without the express written permission of PitchBook Data, Inc. Contents are based on information from sources believed to be reliable, but accuracy and completeness cannot be guaranteed. Nothing herein should be construed as any past, current or future recommendation to buy or sell any security or an offer to sell, or a solicitation of an offer to buy any security. This material does not purport to contain all of the information that a prospective investor may wish to consider and is not to be relied upon as such or used in substitution for the exercise of independent judgment.

3 PITCHBOOK 3Q 2015

U.S . PE MIDDLE MARKET REPORT

IntroductionMarkets worldwide are rife with uncertainty. The Eurozone struggles to contain ongoing

ramifications of the financial crisis, China contends with a market crash; the list goes on. Private equity investors, gearing up for investments that will last at least a couple business cycles, are hard-pressed to deploy their ample stores of dry powder, especially with persistently high multiples.

Yet there are some relatively bright spots, such as the U.S. middle market, to which investors are still turning in mass droves. The middle market’s percentage of buyout activity is holding steady at a record high through the first half of 2015, even as the decline in overall U.S. PE activity entailed a slight softening in middle-market numbers. That softening illustrates how the middle market isn’t immune from industry pressures, however. As it grows ever more popular as an investment destination, competition is mounting. We’ve heard of firms with a traditional middle-market investment focus shifting their attention to the lower and core reaches of the market as the upper end grows more heated. The numbers seen in the upper middle market (UMM) in particular are some of the strongest in the middle market as a whole, an outcome we anticipated by how

much limited partner (LP) interest in the UMM has been evidenced by commitments to funds in the $1 billion to $5 billion range.

It wasn’t just fundraising foreshadowing strong UMM numbers. The rise of alternative lending supplanting banks’ traditional role in financing buyouts has long been heralded as regulatory pressure increased. With GE Capital’s pending sale portending a gap in the market, top contenders in the space are jockeying for

position. Consequently, lenders are competing to win financings with ever-more favorable terms and structures, contributing to sustained PE activity in the UMM even as multiples inflate. Investors are employing larger debt components in capital structures in response. With a hike in interest rates anticipated as eventual

yet slight, that may shift things somewhat yet not substantially. The middle market—in particular its upper reaches—looks set for continued strong if not record-busting numbers.

We hope the data and commentary in this report prove helpful and informative in your decision-making process in the coming quarters. If you have any questions, comments or suggestions, please reach out to us at [email protected].

The middle market remains popular, even as investors

contend with growing competition.

Madison Capital’s focus is to provide superior financing solutions to a wide range of private equity sponsors. Our products and services support the acquisition, recapitalization and growth investment efforts of private equity firms focused on middle market companies.

Our reputation is built on key relationships and effective communication.

We build relationships by concentrating on the needs of our clients and delivering outstanding services.

4 PITCHBOOK 3Q 2015

U.S . PE MIDDLE MARKET REPORT

Middle Market Overview

Current middle-market numbers mask underlying

pressures. The figures are strong still, with an uptick in completed investments and capital invested pushing 1H 2015 numbers to a hefty 895 deals worth a total of $159 billion. Those sums are hardly lackluster, although overshadowed by the towering totals of 2014—however, declines tend to occur in the wake of record-setting activity. Growing investor participation in middle-market investing and consequent competition is bearing fruit in the form of elevated multiples. Even if the wheels of dealmaking are still heavily greased by deep liquidity within capital markets and amenable lenders, an easing of pace is to be expected as the field grows more crowded and costly.

MIDDLE MARKET DEAL FLOW BY QUARTER

Source: PitchBook

MIDDLE MARKET DEAL FLOW BY YEAR

Source: PitchBook

$50

$50

$50

$80

$64

$66

$60

$71

$60

$65

$66

$97

$70

$59

$85

$89

$105

$94

$101

$100

$75

$84

236

234

258

401

301

361

303

337

335

363362

542

317274

467

439

534

465

498

414

431464

0

100

200

300

400

500

600

$0

$20

$40

$60

$80

$100

$120

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q

2010 2011 2012 2013 2014 2015Capital Invested ($B) # of Deals Closed

$274

$352

$204

$84

$229

$261

$288

$303

$399

$159

1,421

1,793

1,195

652

1,129 1,302

1,601

1,497

1,911

895

0

500

1,000

1,500

2,000

2,500

$0

$100

$200

$300

$400

$500

2006 2007 2008 2009 2010 2011 2012 2013 2014 1H 15

Capital Invested ($B) # of Deals Closed

1H 2015 DEALS BY SECTOR AND SEGMENT

Source: PitchBook

47%

22%

37%

18%

26%

21%

5%

13%

16%

13%

7%

11%

3%

9%

5%

11%

15%

3%

7%

11%

0% 20% 40% 60% 80% 100%

LMM

CMM

UMM

B2B B2C Energy Financial Services Healthcare IT Materials and Resources

5 PITCHBOOK 3Q 2015

U.S . PE MIDDLE MARKET REPORT

Search companies, firms, or people... Live Chat

DASHBOARD COMPANIES & DEALS INVESTORS & BUYERS FUNDS & IRR LIMITED PARTNERS ADVISORS PEOPLE PUBLIC FINANCIALS CRM MORE

CAPITAL INVESTED & DEAL COUNT DEALS BY REGIONS

SEARCH RESULTS

SAVED SEARCHES

Europe League Table 40,672

Funds w/ Dry Powder 12,948

Open Funds 89

Recent IT Deals 51,176

500 Startups 114,382

NEWS & LIBRARY

Katzen Eye Group Goes Varsity

Energy

VCs Doing Better Than Ever

PE Breakdown

European Activity Highlights

2010 Vintage Buyout Funds

Top Exits by Industry

Brightside Acquisition AnaCap’d

Super Uber Round

Meritech Closes $500M Fund

Limited Partners

2,716 LP’s

Limited Partners Name (2,716)# Limited Partner Type # Affiliated Funds

# Affiliated Investors

1

2

3

4

5

6

7

8

9

10

11

12

13

New York State Common Retirement Fund

Pennsylvania State Employee’s Retirement S...Pennsylvania Public School Employee Retire...

Bell Atlantic Master Trust

Teachers Insurance and Annuity Assocation...

Massachusetts Pendon Reserves Investment...

Metropolitan Life Insurance

New York State Teachers Retirement System

Metlife Insurance Company of ConnecticutMassachusetts Mutual Life Insurance Company

China Insurance Company

Public Pension Fund

Public Pension Fund

Public Pension Fund

Corporate Pension

Insurance Company

Public Pension Fund

Insurance CompanyPublic Pension Fund

Insurance Company

Insurance Company

Public Pension Fund

594502

348333

328313

312308

304

274373

Download SalesforceDeselect All

Select Top 25

Select Page

Select All

Invert Selected

Show Selected Only

Remove Selected

New York State Teachers Retirement System Public Pension Fund 308

Bell Atlantic Master Trust Corporate Pension 333

AUM Private Equity

Private Equity (%) HQ Location HQ Ph

312192

158157

169136

185126

212

163147

Add Column

176,200.00

25,900.00

50,500.00103.35

178.50

59,700.00

516,206.00104,300.00

405,900.00

24,700.00181,980.00

13,919.80

25,900.00

8,040.00103.35

178.50

5,916.00

516,206.007,800.00

405,900.00

24,700.0018,371.00

8%

12%22%17%

42%

12%

7%8%

4.5%

7.3%10%

Albany, NY

Harrisburg, PA

Harrisburg, PA

Basking Ridge, NJ

New York, NY

Boston, MA

New York, NYAlbany, NY

Bloomfield, Ct

Springfield, MA

Quebec, Canada

Layouts:

LP Summary Layout Save Save As

126 104,300.00 7,800.00 8% Albany, NY

157 103.35 103.35 17% Basking Ridge, NJ

COMPANY SIGNALS

LiquidPlanner Seattle, WashingtonBusiness/ Productivity Software... -

Series BLast Inv. Type

May-2014Last Inv. Date

4Investor

Growth RateSize Multiple

45People

$24.32MVal. May 2014

Company Name

The Stiller

Bonobos

Growth Rate

10.2%

19.65%

Size Multiple

1.32K

150K

Total Capital Invested (millions, USD) Deal Count

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

2.73xx avg.

76th %ile

115%98th %ile

weekly

DON’T LET INCOMPLETE DATA LEAVE YOU

IN THE DARKPitchBook offers more visibility of the middle market landscape than any other source

Contact us for a demo of the financial

information technology trusted by leading

investors, companies and advisors

pitchbook.com | US + 1 206.623.1986 | UK +44 (0) 207.190.9809

Bet ter Data. Bet ter Decisions.PitchBook

Companies & Deals

Service Providers

Valuations & Multiples

InvestorsFunds & Performance

FinancialsLimited Partners

People

W E S T C O A S T

M O U N T A I N

M I D W E S T

S O U T H S O U T H E A S T

G R E A T L A K E S M I D - A T L A N T I C

N E W E N G L A N D

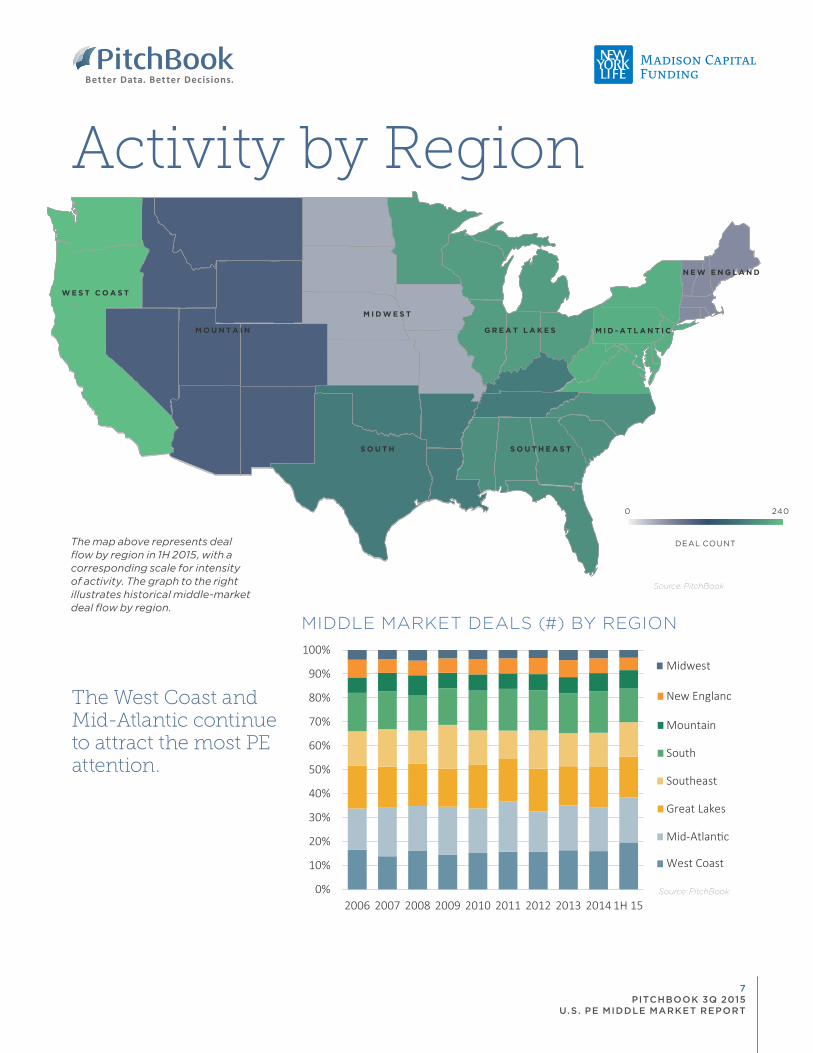

Activity by Region

MIDDLE MARKET DEALS (#) BY REGION

Source: PitchBook

The map above represents deal flow by region in 1H 2015, with a corresponding scale for intensity of activity. The graph to the right illustrates historical middle-market deal flow by region.

LEGEND

Source: PitchBook

0 240

DEAL COUNT

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014 1H 15

Midwest

New England

Mountain

South

Southeast

Great Lakes

Mid-Atlantic

West Coast

The West Coast and Mid-Atlantic continue to attract the most PE attention.

7 PITCHBOOK 3Q 2015

U.S . PE MIDDLE MARKET REPORT

Lower Middle MarketLMM DEAL FLOW BY QUARTER

SELECT LMM DEALS IN 2Q 2015

Source: PitchBook

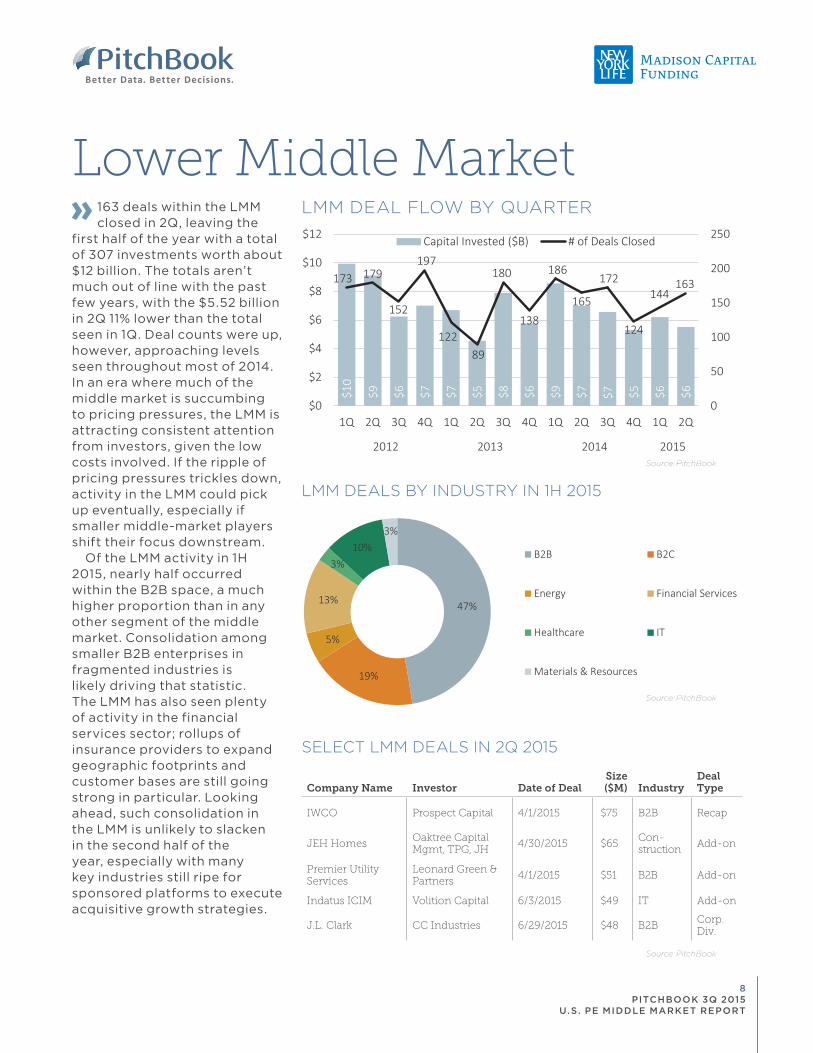

163 deals within the LMM closed in 2Q, leaving the

first half of the year with a total of 307 investments worth about $12 billion. The totals aren’t much out of line with the past few years, with the $5.52 billion in 2Q 11% lower than the total seen in 1Q. Deal counts were up, however, approaching levels seen throughout most of 2014. In an era where much of the middle market is succumbing to pricing pressures, the LMM is attracting consistent attention from investors, given the low costs involved. If the ripple of pricing pressures trickles down, activity in the LMM could pick up eventually, especially if smaller middle-market players shift their focus downstream.

Of the LMM activity in 1H 2015, nearly half occurred within the B2B space, a much higher proportion than in any other segment of the middle market. Consolidation among smaller B2B enterprises in fragmented industries is likely driving that statistic. The LMM has also seen plenty of activity in the financial services sector; rollups of insurance providers to expand geographic footprints and customer bases are still going strong in particular. Looking ahead, such consolidation in the LMM is unlikely to slacken in the second half of the year, especially with many key industries still ripe for sponsored platforms to execute acquisitive growth strategies.

LMM DEALS BY INDUSTRY IN 1H 2015

Company Name Investor Date of DealSize ($M) Industry

Deal Type

IWCO Prospect Capital 4/1/2015 $75 B2B Recap

JEH HomesOaktree Capital Mgmt, TPG, JH

4/30/2015 $65 Con-struction

Add-on

Premier Utility Services

Leonard Green & Partners

4/1/2015 $51 B2B Add-on

Indatus ICIM Volition Capital 6/3/2015 $49 IT Add-on

J.L. Clark CC Industries 6/29/2015 $48 B2BCorp. Div.

$10

$9 $6 $7 $7 $5 $8 $6 $9 $7 $7 $5 $6 $6

173 179

152

197

122 89

180

138

186

165

172

124

144 163

0

50

100

150

200

250

$0

$2

$4

$6

$8

$10

$12

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q

2012 2013 2014 2015

Capital Invested ($B) # of Deals Closed

47%

19%

5%

13%

3%10%

3%

B2B B2C

Energy Financial Services

Healthcare IT

Materials & Resources

Source: PitchBook

Source: PitchBook

8 PITCHBOOK 3Q 2015

U.S . PE MIDDLE MARKET REPORT

Core Middle MarketCMM DEAL FLOW BY QUARTER

CMM DEALS BY INDUSTRY IN 1H 2015

Source: PitchBook

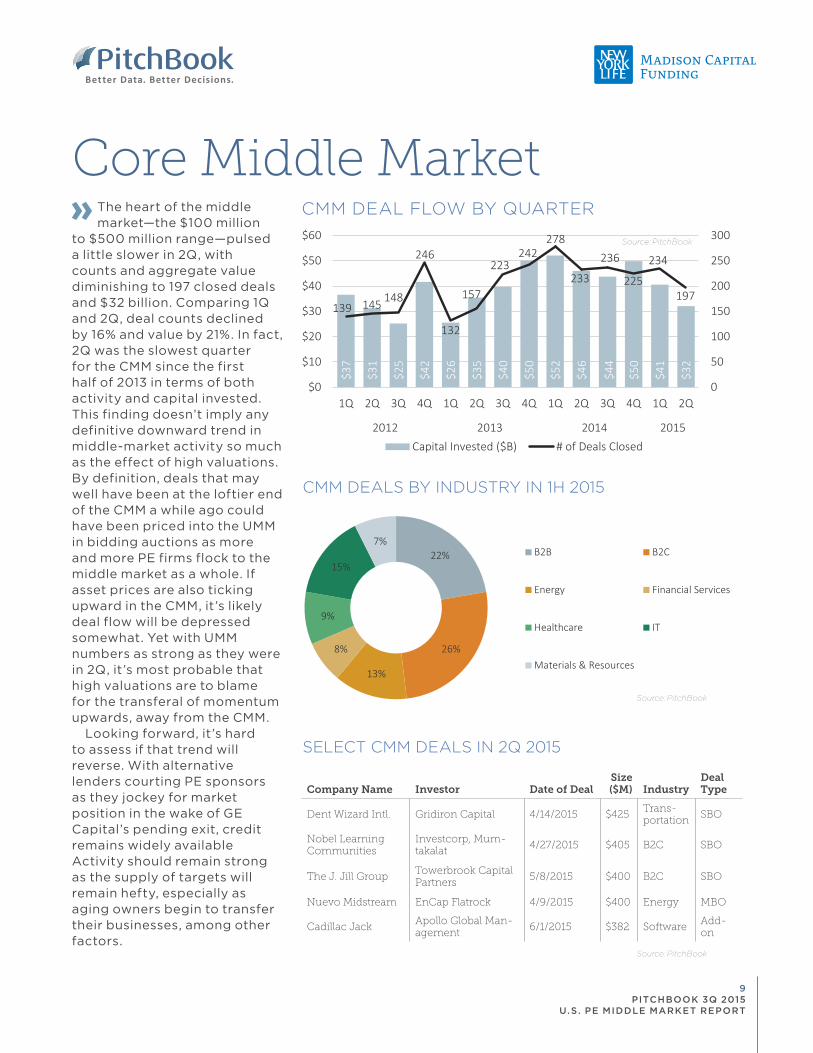

The heart of the middle market—the $100 million

to $500 million range—pulsed a little slower in 2Q, with counts and aggregate value diminishing to 197 closed deals and $32 billion. Comparing 1Q and 2Q, deal counts declined by 16% and value by 21%. In fact, 2Q was the slowest quarter for the CMM since the first half of 2013 in terms of both activity and capital invested. This finding doesn’t imply any definitive downward trend in middle-market activity so much as the effect of high valuations. By definition, deals that may well have been at the loftier end of the CMM a while ago could have been priced into the UMM in bidding auctions as more and more PE firms flock to the middle market as a whole. If asset prices are also ticking upward in the CMM, it’s likely deal flow will be depressed somewhat. Yet with UMM numbers as strong as they were in 2Q, it’s most probable that high valuations are to blame for the transferal of momentum upwards, away from the CMM.

Looking forward, it’s hard to assess if that trend will reverse. With alternative lenders courting PE sponsors as they jockey for market position in the wake of GE Capital’s pending exit, credit remains widely available Activity should remain strong as the supply of targets will remain hefty, especially as aging owners begin to transfer their businesses, among other factors.

SELECT CMM DEALS IN 2Q 2015

Company Name Investor Date of DealSize ($M) Industry

Deal Type

Dent Wizard Intl. Gridiron Capital 4/14/2015 $425Trans-portation

SBO

Nobel Learning Communities

Investcorp, Mum-takalat

4/27/2015 $405 B2C SBO

The J. Jill GroupTowerbrook Capital Partners

5/8/2015 $400 B2C SBO

Nuevo Midstream EnCap Flatrock 4/9/2015 $400 Energy MBO

Cadillac JackApollo Global Man-agement

6/1/2015 $382 SoftwareAdd-on

$37

$31

$25

$42

$26

$35

$40

$50

$52

$46

$44

$50

$41

$32

139 145 148

246

132

157

223242

278

233

236

225

234

197

0

50

100

150

200

250

300

$0

$10

$20

$30

$40

$50

$60

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q

2012 2013 2014 2015Capital Invested ($B) # of Deals Closed

22%

26%

13%

8%

9%

15%

7%B2B B2C

Energy Financial Services

Healthcare IT

Materials & Resources

Source: PitchBook

Source: PitchBook

9 PITCHBOOK 3Q 2015

U.S . PE MIDDLE MARKET REPORT

Source: PitchBook

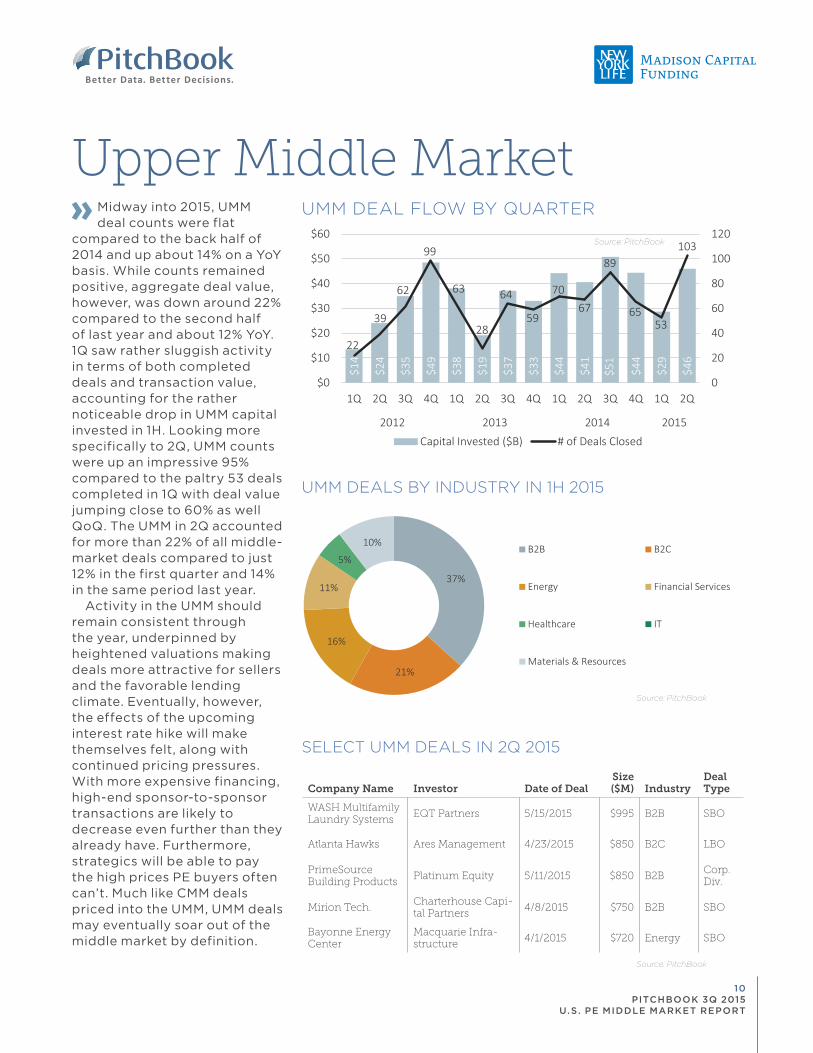

Upper Middle MarketUMM DEAL FLOW BY QUARTERMidway into 2015, UMM

deal counts were flat compared to the back half of 2014 and up about 14% on a YoY basis. While counts remained positive, aggregate deal value, however, was down around 22% compared to the second half of last year and about 12% YoY. 1Q saw rather sluggish activity in terms of both completed deals and transaction value, accounting for the rather noticeable drop in UMM capital invested in 1H. Looking more specifically to 2Q, UMM counts were up an impressive 95% compared to the paltry 53 deals completed in 1Q with deal value jumping close to 60% as well QoQ. The UMM in 2Q accounted for more than 22% of all middle-market deals compared to just 12% in the first quarter and 14% in the same period last year.

Activity in the UMM should remain consistent through the year, underpinned by heightened valuations making deals more attractive for sellers and the favorable lending climate. Eventually, however, the effects of the upcoming interest rate hike will make themselves felt, along with continued pricing pressures. With more expensive financing, high-end sponsor-to-sponsor transactions are likely to decrease even further than they already have. Furthermore, strategics will be able to pay the high prices PE buyers often can’t. Much like CMM deals priced into the UMM, UMM deals may eventually soar out of the middle market by definition.

SELECT UMM DEALS IN 2Q 2015

Company Name Investor Date of DealSize ($M) Industry

Deal Type

WASH Multifamily Laundry Systems

EQT Partners 5/15/2015 $995 B2B SBO

Atlanta Hawks Ares Management 4/23/2015 $850 B2C LBO

PrimeSource Building Products

Platinum Equity 5/11/2015 $850 B2B Corp. Div.

Mirion Tech.Charterhouse Capi-tal Partners

4/8/2015 $750 B2B SBO

Bayonne Energy Center

Macquarie Infra-structure

4/1/2015 $720 Energy SBO

$14

$24

$35

$49

$38

$19

$37

$33

$44

$41

$51

$44

$29

$46

22

39

62

99

63

28

64

59

7067

89

6553

103

0

20

40

60

80

100

120

$0

$10

$20

$30

$40

$50

$60

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q

2012 2013 2014 2015

Capital Invested ($B) # of Deals Closed

UMM DEALS BY INDUSTRY IN 1H 2015

37%

21%

16%

11%

5%

10%B2B B2C

Energy Financial Services

Healthcare IT

Materials & Resources

Source: PitchBook

Source: PitchBook

10 PITCHBOOK 3Q 2015

U.S . PE MIDDLE MARKET REPORT

Exit ActivityMIDDLE MARKET EXITS BY YEAR

Source: PitchBook

We noted in our 2Q Middle Market report that between

1Q 2013 and the end of 2014, PE sellers enjoyed a nearly uninterrupted QoQ increase in exit counts; the first half of 2015 appears to have ended this trend. Midway through this year we’ve seen middle-market counts decline from the 266 high we saw in the fourth quarter of 2014 to just 190 exits in 2Q 2015, offset by both a YoY and QoQ increase in UMM exits. Capital exited was also down in 1H 2015 when looking at the UMM, yet the second quarter helped recapture some of the momentum lost since the end of last year, with 2Q exit values jumping just over 61% QoQ to $28.9 billion.

More than half of exits occurred in the CMM, however, UMM deals jumped noticeably looking at both 1H and 2Q 2015. UMM accounted for about 24% of exits in 1H compared to 18% in 2H 2014 and just 34% in 2Q compared to 16% in 1Q. Complementing this observation, strategic acquisitions remained the most popular exit ramp for middle-market transactions thus far into 2015, responsible for about 63% and 57% of deals in 1H and 2Q, respectively. As strategic acquirers continue looking for growth, acquisitions in the UMM segment make the most sense, giving the increased likelihood companies in that size bucket can be immediately accretive to acquirers’ bottom lines. Further, PE-backed IPOs continued to slip throughout the front half of this year overall; while 2Q did see an uptick, we expect PE-backed IPOs to remain sluggish due to

changing corporate focuses and better alternative exit routes for portfolio companies. Corporate balance sheets continue to hold healthy cash accounts along with various financing

resources to pay top dollar for UMM companies. Accordingly, it seems reasonable to expect such transactions to remain in the sights of strategic acquirers through year end.

$27

$37

$26

$11

$39

$46$48

$36

$62

$30

$13

$11

$4

$7

$8

$8$9

$16

$19

$5

$21

$28

$8

$3

$18

$17

$25

$20

$31

$12

0

100

200

300

400

500

600

700

$0

$20

$40

$60

$80

$100

$120

2006 2007 2008 2009 2010 2011 2012 2013 2014 1H 15

Corporate Acquisition ($B) IPO ($B)Secondary Buyout ($B) Corporate Acquisition # of ExitsSecondary Buyout # of Exits IPO # of Exits

11 PITCHBOOK 3Q 2015

U.S . PE MIDDLE MARKET REPORT

Fundraising Activity

Source: PitchBook

Source: PitchBook

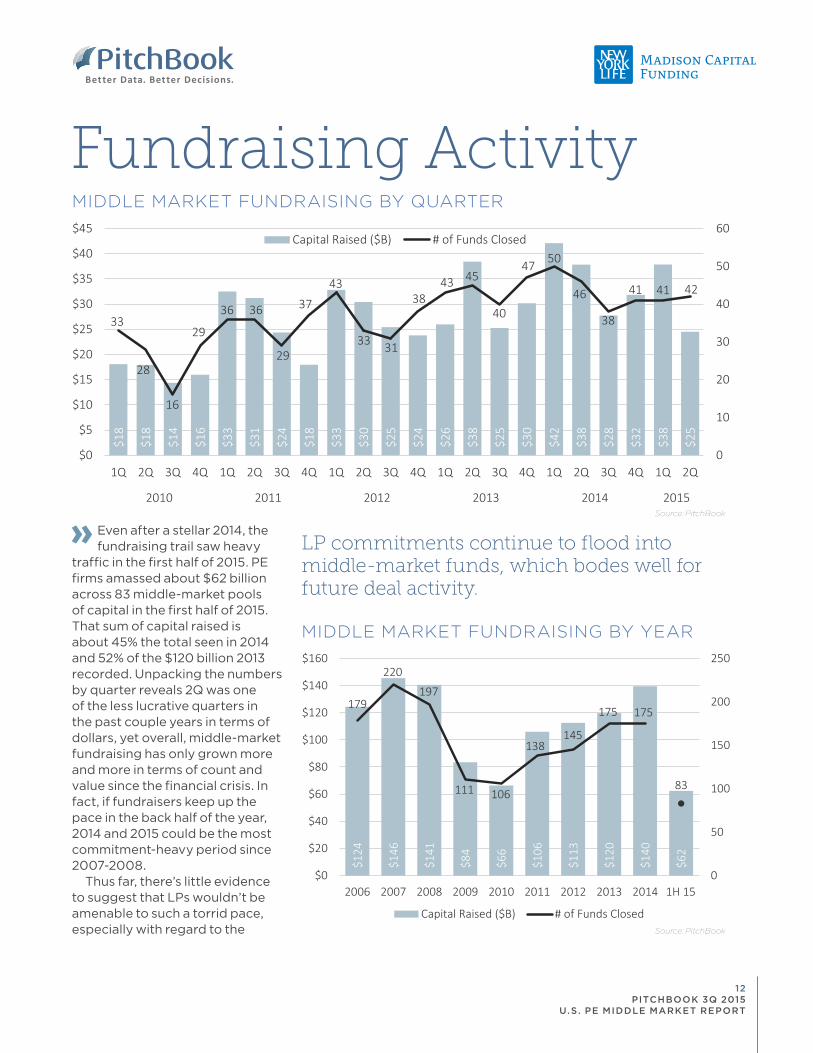

Even after a stellar 2014, the fundraising trail saw heavy

traffic in the first half of 2015. PE firms amassed about $62 billion across 83 middle-market pools of capital in the first half of 2015. That sum of capital raised is about 45% the total seen in 2014 and 52% of the $120 billion 2013 recorded. Unpacking the numbers by quarter reveals 2Q was one of the less lucrative quarters in the past couple years in terms of dollars, yet overall, middle-market fundraising has only grown more and more in terms of count and value since the financial crisis. In fact, if fundraisers keep up the pace in the back half of the year, 2014 and 2015 could be the most commitment-heavy period since 2007-2008.

Thus far, there’s little evidence to suggest that LPs wouldn’t be amenable to such a torrid pace, especially with regard to the

MIDDLE MARKET FUNDRAISING BY QUARTER

MIDDLE MARKET FUNDRAISING BY YEAR

LP commitments continue to flood into middle-market funds, which bodes well for future deal activity.

$18

$18

$14

$16

$33

$31

$24

$18

$33

$30

$25

$24

$26

$38

$25

$30

$42

$38

$28

$32

$38

$25

33

28

16

29

36 36

29

37

43

33 31

38 43 45

40

47 50

46

38

41 41 42

0

10

20

30

40

50

60

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q

2010 2011 2012 2013 2014 2015

Capital Raised ($B) # of Funds Closed

$124

$146

$141

$84

$66

$106

$113

$120

$140

$62

179

220

197

111 106

138145

175 175

83

0

50

100

150

200

250

$0

$20

$40

$60

$80

$100

$120

$140

$160

2006 2007 2008 2009 2010 2011 2012 2013 2014 1H 15

Capital Raised ($B) # of Funds Closed

12 PITCHBOOK 3Q 2015

U.S . PE MIDDLE MARKET REPORT

MIDDLE MARKET FUNDS (#) BY FUND SIZE

MIDDLE MARKET BUYOUT FUNDS AVERAGE TIME TO CLOSE (IN MONTHS)

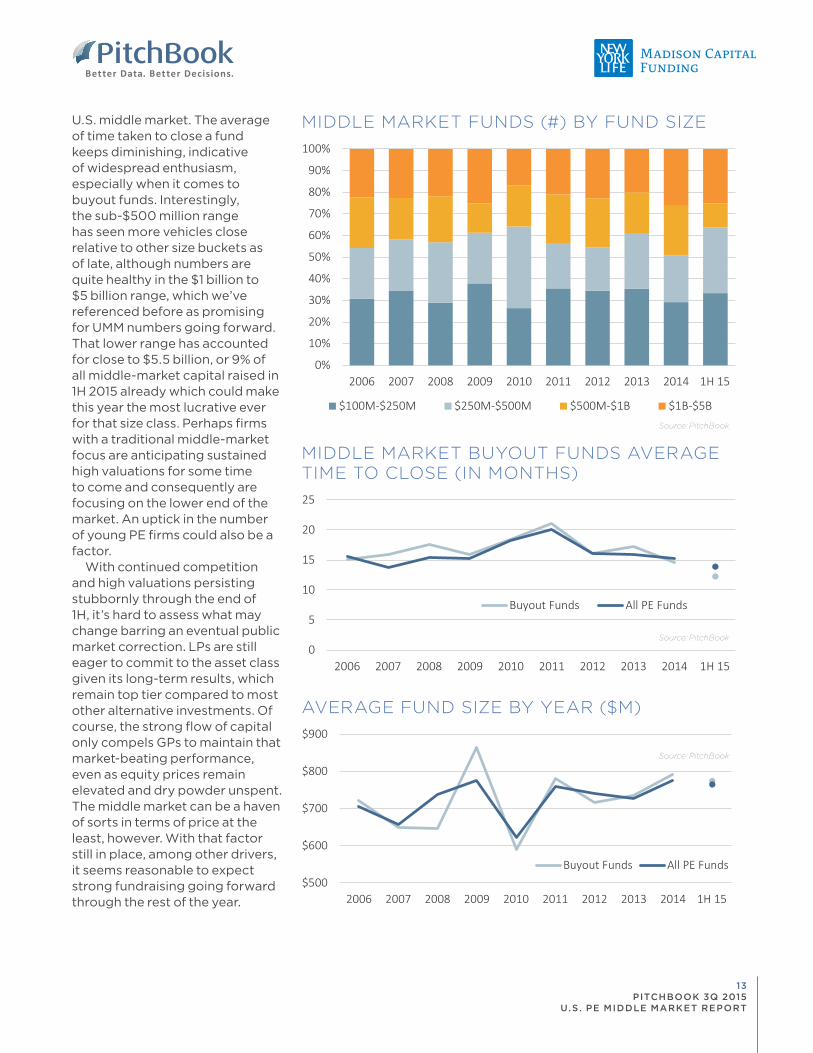

U.S. middle market. The average of time taken to close a fund keeps diminishing, indicative of widespread enthusiasm, especially when it comes to buyout funds. Interestingly, the sub-$500 million range has seen more vehicles close relative to other size buckets as of late, although numbers are quite healthy in the $1 billion to $5 billion range, which we’ve referenced before as promising for UMM numbers going forward. That lower range has accounted for close to $5.5 billion, or 9% of all middle-market capital raised in 1H 2015 already which could make this year the most lucrative ever for that size class. Perhaps firms with a traditional middle-market focus are anticipating sustained high valuations for some time to come and consequently are focusing on the lower end of the market. An uptick in the number of young PE firms could also be a factor.

With continued competition and high valuations persisting stubbornly through the end of 1H, it’s hard to assess what may change barring an eventual public market correction. LPs are still eager to commit to the asset class given its long-term results, which remain top tier compared to most other alternative investments. Of course, the strong flow of capital only compels GPs to maintain that market-beating performance, even as equity prices remain elevated and dry powder unspent. The middle market can be a haven of sorts in terms of price at the least, however. With that factor still in place, among other drivers, it seems reasonable to expect strong fundraising going forward through the rest of the year.

Source: PitchBook

Source: PitchBook

AVERAGE FUND SIZE BY YEAR ($M)

Source: PitchBook

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014 1H 15

$100M-$250M $250M-$500M $500M-$1B $1B-$5B

0

5

10

15

20

25

2006 2007 2008 2009 2010 2011 2012 2013 2014 1H 15

Buyout Funds All PE Funds

$500

$600

$700

$800

$900

2006 2007 2008 2009 2010 2011 2012 2013 2014 1H 15

Buyout Funds All PE Funds

13 PITCHBOOK 3Q 2015

U.S . PE MIDDLE MARKET REPORT

MOST ACTIVE INVESTORS MOST ACTIVE LAW FIRMS

MOST ACTIVE ADVISORS

Source: PitchBook Source: PitchBook

Source: PitchBook

MOST ACTIVE LENDERS

Source: PitchBook

Madison Capital Funding

GE Capital

Ares Capital

CIT Group

BMO Harris Bank

Golub Capital

NewStar Financial

PNC Financial Services Group

Abacus Finance Group

Babson Capital Management

J.P. Morgan

MidCap Financial

Firm

2Q 2015 Middle Market League Tables

13

10

6

6

5

5

3

3

3

3

3

3

Deals

ABRY Partners

GTCR Golder Rauner

Hellman & Friedman

Ares Capital

The Carlyle Group

Audax Group

Kohlberg Kravis Roberts

The Jordan Company

The Riverside Company

TPG Capital

Vista Equity Partners

Huron Capital Partners

KRG Capital Partners

PNC Erieview Capital

Summit Partners

Warburg Pincus

Firm

21

11

11

9

8

7

7

7

7

7

7

6

6

6

6

6

Deals

Kirkland & Ellis

Jones Day

Latham & Watkins

Goodwin Procter

Morgan, Lewis & Bockius

DLA Piper

Paul, Weiss, Rifkind, Wharton

Paul Hastings

Ropes & Gray

Weil, Gotshal & Manges

Greenberg Traurig

Willkie Farr & Gallagher

McDermott Will & Emery

Sidley Austin

Debevoise & Plimpton

Dechert

Simpson Thacher & Bartlett

Firm

29

16

12

12

11

11

11

10

10

10

9

8

6

6

5

5

5

Deals

Houlihan Lokey

William Blair & Company

KPMG

Moelis & Company

Robert W. Baird & Co.

Raymond James Financial

Harris Williams & Co.

TM Capital

BB&T Capital Markets

Duff & Phelps

Lazard Middle Market

Goldman Sachs

Morgan Stanley

Firm

20

12

8

7

6

6

6

6

5

5

5

4

4

Deals

14 PITCHBOOK 3Q 2015

U.S . PE MIDDLE MARKET REPORT

MethodologyMIDDLE MARKET DEFINITION

For this report, the middle market (MM) is defined as U.S.-based companies acquired through buyout transactions between $25 million and $1 billion. Note that minority deals are not included. The middle market is further broken down into the lower middle market (LMM; $25 million to $100 million), the core middle market (CMM; $100 million to $500 million) and the upper middle market (UMM; $500 million to $1 billion). This report covers only U.S.-based middle-market companies that have received some type of private equity investment.

TOTAL CAPITAL INVESTED Total amount of equity and debt used in the private equity investment

Ex. $10 million of equity and $20 million of debt = $30 million of total capital investment

PitchBook’s total capital invested figures include deal amounts that were not collected by PitchBook but have been estimated using a multi-dimensional estimation matrix, which takes into account year of investment, deal type, platform v. add-on, industry and sector. Some data sets will include these extrapolated numbers while others will be compiled using only data collected directly by PitchBook; this explains any potential discrepancies that may be noticed.

FUNDRAISINGPitchBook defines middle-market funds as PE investment vehicles with between $100 million and $5 billion in capital commitments. The report only includes private equity funds that have held their final close. Funds-of-funds and LP secondary funds are not included.

EXITSThe report includes both full and partial exits of middle-market companies via corporate acquisition, secondary private equity buyout and initial public offering (IPO). PitchBook has utilized its multi-dimensional substitution and estimation matrix to estimate transaction sizes where the deal amount is unknown.

LEAGUE TABLESAll League Tables are compiled using deal counts for middle-market transactions. For example, the Most Active Advisors League Table shows the number of U.S.-based middle-market deals that a firm advised on during the second quarter of 2015. Deals on which a firm advised multiple parties will only be counted once for that firm.

15 PITCHBOOK 3Q 2015

U.S . PE MIDDLE MARKET REPORT