Embed Size (px)

Citation preview

s

0

5

10

15

20

25

30

35

5-O

ct-1

1

5-N

ov-1

1

5-D

ec-1

1

5-J

an-1

2

5-F

eb-1

2

5-M

ar-1

2

5-A

pr-

12

5-M

ay-1

2

5-J

un

-12

5-J

ul-

12

5-A

ug-1

2

5-S

ep-1

2

5-O

ct-1

2

5-N

ov-1

2

PGOLD PSEi (rebased) MSCI (rebased)

Midas Investments Research

This report is published for educational purposes only

by students competing in the CFA Institute Research

Challenge.

29 November 2012

Exchange Rate USD/PHP: 40.88

Market Capitalization P 89,078,281,250

Shares Outstanding 2,766,406,250

Free Float 34%

52week Price Range P 14.98 - P33.00

Ave. Monthly Volume 78,233,692

Beta 0.81

Ticker: PGOLD

Price: PHP 32.20 (USD 0.79)

Recommendation: BUY

Price Target: PHP 40.16 (USD 1.00)

Pure consumer play outpacing market on defensive

growth

We recommend a BUY for PGOLD, the Philippines‟ fastest growing grocery retailer and

the only pure, direct and broad-based domestic consumer play in the market, at a price

target of Php 40.16, a 24.72% upside from current price of P32.20. Our positive outlook is

based on growing and resilient domestic consumption that is captured by an EDLP (Every

Day Low Prices) Strategy targeting low to middle-income consumers bringing in traffic of

18 million each week. Through the Tindahan ni Aling Puring (TNAP) reseller program, it

is the only major retailer to focus on the widely popular traditional sari-sari store. By

acquiring membership shopping club S&R, it also captures a growing niche of high-income

consumer spending. With aggressive store expansion underway, we forecast sustainable

long-term growth for this defensive stock.

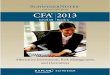

Focus on domestic consumption driving resilient earnings against volatile global

financial system: As the only pure direct and broad-based domestic consumer play on

the local market, PGOLD‟s stock price has outpaced the Philippine stock market by

77.2% (see Figure 1) driven by revenue growth of 39.69% (2012E) on the back of

16% growth in domestic consumption. With consumption expected to continue to

grow by 8% annually through 2016, we forecast same store sales growth (SSSG) to

grow by a five-year CAGR of 6.41%. As a defensive stock, PGOLD‟s earnings

growth is cushioned from risk surrounding Western economies with 70% of product

revenues from essential spending on food items and 90% of customer revenues

expected to come from low-income consumer segments and traditional re-sellers. The

surge in the local economy has benefited the S&R format, which is expected to boost

consolidated net margins to 5.58% (from 4.83% in 2011) with its high-margin product

portfolio.

Aggressive national roll-out catalyzing revenue growth: By adding 51 stores outside

Metro Manila this year alone, Puregold revenues are slated to grow by 39.69% in

2012. Four-year revenue CAGR of 23.6% is expected on the back of aggressive

expansion raising total store count to 260 by 2016 (See Figure 2). A key catalyst will

be expansion into the unsaturated and attractive market of Visayas and Mindanao

where we calculate a potential of 91 hypermarkets to be added. With a hypermarket

opening in Palawan today, it has already begun operating its first store outside of the

island of Luzon.

Scalable asset-light model translating to strong margins and abundance of free

cash: PGOLD has a scalable asset-light model that relies on property leasing and

third-party logistics from suppliers. Fixed Asset Turnover is seen to improve from

6.49 to 10.96 (2011-16E), showing potential for growth. This translates to impressive

ROE and profit margin at 21.95% and 8.85% respectively, both above industry

averages. PGOLD generates an abundance of free cash enough to meet the expected

yearly annual capex of Php 3.46B allocated for expansion from 2013 to 2016. With

issuance of additional debt, special Dividend Payout Ratio (DPR) at 2016E is 43.82%

on top of the actual DPR of 14.91%, giving a total DPR of 58.73%

Valuation confirms BUY rating: FCFE analysis indicates a price of Php 40.16 at a

24.72% upside from current price, supporting our positive long-term outlook. PER

analysis with Asia-Pacific grocery retailers indicates a discount of 20.75%, confirming

the attractiveness of PGOLD. Investment risks include: execution of VisMin

expansion and competitive risks from SM Retail.

Puregold Price Club, Inc.

YTD 1m 3m 12m

Abs 79.2% 7.5% 10.1% 111.1%

Rel 50.3% 3.0% 1.5% 77.2%

Figure 1: Share Price Performance

Source: PSE, MSCI Asia-Pacific

In Php mil 2009 2010 2011 2012E 2013E 2014E 2015E 2016E

Revenues 24,112 29,108 38,988 59,541 81,273 100,718 122,258 148,707

EBIT 458 985 2,216 4,682 7,985 10,899 14,465 19,097

Net Income 132 510 1,545 3,156 5,384 7,423 9,919 13,160

Ratios

EPS N/A N/A 1.10 1.29 1.95 2.68 3.59 4.76

Profit Margin 0.56% 1.97% 4.83% 5.58% 6.62% 7.37% 8.11% 8.85%

Cur. Ratio 0.93 0.76 1.10 1.11 1.24 1.28 1.37 1.47

ROA 0.96% 5.28% 11.29% 7.47% 9.64% 10.77% 11.80% 12.75%

ROE 11.28% 29.48% 21.74% 12.24% 16.10% 18.50% 20.34% 21.95%

Services Sector

Retail Industry

Figure 2: Market Data

CFA Institute Research Challenge November 29, 2012

41 62

100

156

182 208

234 260

0

50

100

150

200

250

300

Puregold Price Club Puregold Jr.

Puregold Extra S&R

Parco

Figure 3: Expansion Plans

Source: Company, Team’s Estimates

Business Description Puregold Price Club, Inc. (PGOLD) is the Philippines‟ fastest growing grocery retail chain.

Since establishing its first store in 1998, it has reached a total store count of 151 stores as of

Nov. 29, 2012. In a matter of 14 years, it has overtaken established retailers in terms of store

count and revenue to be the second-largest grocery retailer in the country. Behind the

company‟s remarkable growth (see Figure 3) is a strategic customer focus on low-income

consumers and sari-sari stores.

Store Formats and Locations

PGOLD‟s operates in four store formats: 74 hypermarkets (Puregold Price Club), 56

supermarkets (Puregold Jr. and Parco), 15 discounters (Puregold Extra) and 6 membership

shopping clubs (S&R) (see Figure 4 and Appendix 8). These are strategically located in key

commercial districts and residential areas with access to major transportation hubs. All stores

are geographically located in Metro Manila and Luzon except for a single S&R outlet in Cebu.

Expansion to VisMin is forecasted to begin by 2013 (see Appendix 9). The first hypermarket

outside the Luzon island in Palawan is already in operation.

PGOLD has a highly-scalable asset-light operations model with direct-delivery outsources

logistics to suppliers and third-party agents, and minimizes warehousing and distribution costs.

Hypermarkets function as warehouses for supermarket and discounter formats. The different

store formats allow PGOLD to quickly enter new locations with minimal upfront costs.

Broad Customer Focus through “Tindahan ni Aling Puring” PGOLD is the first and only modern retailer to strategically target sari-sari stores and other re-

sellers as customers through the Tindahan ni Aling Puring (TNAP) program. By selling to

sari-sari stores, PGOLD penetrates the DE market which comprises 90% of the Philippine

population. TNAP provides rebates, delivery services, training seminars, and even travel

incentives for its members. From its beginnings in 2005, TNAP has grown its member base

from 30,000 to 220,000 by 2012, representing around 20% of the growing number of sari-sari

stores in the country (see Appendix 10 and 11). Re-sellers contribute 35% of PGOLD‟s annual

revenues (see Figure 5).

Strategic Acquisitions Complete Spectrum of Consumer Segments

By acquiring S&R Membership Shopping and Parco Supermarkets last May 2012, PGOLD

covers the entire spectrum of consumers. S&R membership shopping club which currently

boasts of 215,000 members taps the high spending power of the AB socio-economic class.

Parco, a supermarket chain with 19 stores, will be integrated and rebranded to PGOLD‟s

supermarket format Puregold Junior. This will strengthen Puregold‟s reach to households

belonging to the CDE socio-economic classes.

Growth Drivers: Same Store Sales Growth and Store Expansion

PGOLD‟s robust revenue generation is heavily supported by competitive pricing, high-margin

products, and steady domestic consumption through population growth. Its EDLP strategy

keeps PGOLD store pricing attractive over local competitors, thus fueling an estimated 6.41%

annual same-store sales growth from 2012 to 2016.

The company has set its organic growth rate at 25 stores per year for the next 5 years.

PGOLD‟s 2011 IPO and 2012 notes issuance which raised P2B and P5B respectively will

accelerate growth through acquisitions on top of organic expansion within the next 5 years.

Experienced Ownership and Management Team

Puregold Price Club, Inc. was founded by Lucio Co, an experienced entrepreneur with

businesses in different industries spanning from retail to consumer finance. From 1998 to

2011, the company was managed and wholly-owned by the Co family. In April 2011, the

company launched an initial public offering, issuing 3,000,000 shares. PGOLD is now 33%

publicly-owned, while the Co family retained 67% of ownership (see Appendix 12).

The Board of Directors has an average of 9 years of working experience in PGOLD and the

retail industry, while Executive Officers and Key Managers have an average of 8-9 years of

working experience with PGOLD (see Appendix 13). As they architecture PGOLD‟s dramatic

growth, they are well positioned to take PGOLD to new heights.

Industry Overview and Competitive Analysis Macro-economic analysis shows security of PGOLD’s sources of growth

Revenue cushioned by strong domestic consumption amidst uncertainty in global economy

Driven by resilient domestic consumption, PGOLD‟s revenues are cushioned from the risk of a

double-dip recession in the global economy brought about by uncertainty in the US and EU

Figure 4: Store Format Overview

Type of Store Hyper-

market

Super-

market

Dis-

counter

No. of Stores (as of

11/29/12)

74 37 15

Average Net

Selling Area (sqm)

1,500-

7,800

800-

1,500

300-

700

No. of SKUs

(in „000s) 30-50 8-10 1.5-2

Source: Company Data

Figure 5: PGOLD Revenue Breakdown

by Consumer Segments

Source: Company Data

6.2

7.8

5.5

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

E

Grocery Consumption

Private Consumption

GDP Growth

Source: Euromonitor

Figure 6: Grocery Industry vs. GDP

Growth Rates and Consumption

CFA Institute Research Challenge November 29, 2012

Figure 10: Revenue Share of Modern vs.

Traditional Retailers among Regional

Peers

0%

20%

40%

60%

80%

100%

Modern Traditional

Source: Euromonitor Trade Statistics

6.2%

11.9%

16.6%

17.7%

Rustan Group of Cos

SM Retails Inc

Robinsons Retail

Group

Puregold Price Club

Inc

Figure 9: Revenue CAGR of PGOLD vs.

Local Competitors (2006-2011)

Source: Euromonitor

economies. While unhealthy peso appreciation is unfavorable for dollar-earning export

industries, PGOLD is cushioned as revenues are based on growing domestic consumption.

Value of OFW remittances may be impacted but this has been historically shown to grow even

during the financial crisis. OFW remittances grew during the 2008 and 2009 financial crisis

at13.68% and 5.61% respectively, before rising again to 8.16% in 2010. Remittances also

impact disposable income which will not cause a decline in essential spending on grocery

items like food (Figure 6)i. 70% of PGOLD‟s items are food products.

Private consumption in the Philippines is expected to grow by an average of 7% with about

20% dedicated on grocery spending.ii At worst, grocery consumption will grow along with

population growth which is stable at 2.0%iii, higher than the Asia Pacific average of 1.0%.iv

Historic cuts in local interest rates to reduce cost of debt accelerating PGOLD expansion

Puregold‟s aggressive expansion plan of opening 25 stores per year is expected to accelerate

with all-time lows in the country‟s interest rates. Driven by a credit upgrade of Philippine

sovereign debt by S&P and Moody‟s to only one-notch below investment grade, interest rates

are at an all-time low of 3.5% and are expected to decrease by 2013. This reduces the cost of

capital to fund expansion and Puregold has responded to this opportunity by issuing a

corporate note of P5 billion for expansion and acquisition.

Industry analysis shows PGOLD’s distinct competitive advantage

Strong presence of traditional retailers turned competitor to customer

Traditional retailers currently occupy the larger share of grocery retailing in the Philippines.

Sari-sari stores pose the biggest threat to modern retail (See Appendix 15 for complete

Porter‟s Five Forces Analysis). They are estimated to number around 1 million stores and

account for 70% of grocery revenues overall. Through the TNAP program, PGOLD has

leveraged the threat of the strong presence of these sari-sari stores by becoming the top

supplier for their merchandise. PGOLD has already reached 20% of sari-sari stores nationwide

while still remaining in Luzon.

The sari-sari store is popular in the Philippine market due to its informal credit system and

sachet size SKUs. The informal credit system allows for consumers within the CDE class to

have easy access to consumer credit which drives consumption. The sachet sizes sold in sari-

sari stores match consumption with the day-to-day wage earnings for the CDE market. 47%

of consumers buy from sari-sari stores as the main source of groceries. PGOLD is the first and

only retailer in the industry to strategically target sari-sari stores as a customer base. They

contribute 35% of PGOLD‟s revenues.

We expect them to continue stable growth given strong support from micro-finance industry.

Sari-sari stores are a popular small enterprise that keeps many home-based women employed,

the Philippines‟ burgeoning micro-finance industry, ranked 6th in the world, (see Figure 7) has

lent financial muscle to ensure their stability for many years to come.

Philippine modern retailing transitioning to opening stages of growth cycle Amid the strong presence of traditional retail, modern grocery retailing in the Philippines

posted robust growth amidst the global financial crisis. Between 2006 and 2011, value sales of

modern grocery retailing grew by a CAGR of 7.4% with hypermarkets posting double-digit

growth at 17%. With the bulk of PGOLD‟s stores in the hypermarket format, revenue grew by

a CAGR of 18% (see Figure 8).

We identified the Philippines to be in the opening stage of global retail development using AT

Kearney‟s Global Retail Development Index (GRDI) (Appendix 16). The country meets the

four indicators of this stage: 1) middle class growing at 9% per yearv; 2) Consumers exploring

organized formats evidenced by growth in modern retailing; 3) government reducing

restrictions through the liberalization of foreign ownership; and 4) minority investment by

foreign retailers in local retailers with Hong Kong-based retailer Dairy Farm Holdings

acquiring a stake in Rustan‟s SuperCenter.

In this stage, growth potential for modern retailers will not only come from a growing market

but by a shake-out of smaller players. PGOLD has already capitalized by acquiring Parco

chain of supermarkets and has set aside P2 billion for acquisitions for 2013.

PGOLD has focused growth, differentiated against competitors

While major players in grocery retailing such as SMvi, Robinsonsvii, and Rustan‟sviii have

witnessed robust growth (Figure 9), PGOLD has outperformed competitors with its broad-

based consumer play. While other retailers have diversified into non-grocery goods (See

Appendix 17), PGOLD has focused on essential spending, targeting low-income segments and

traditional re-sellers, cushioning it from vulnerability to the global economy.

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0

1000

2000

3000

4000

5000

6000

7000

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

Gross Loan Portfolio (in PHP millions)

Active borrowers (in '000 People)

Figure 7: Microfinance Loan Portfolio and

Number of Borrowers (2001-2011)

Source: MixMarket.Org

AB

1%

C

9%

D

60%

E

30%

Figure 11: Distribution of Households by

Economic Classes

Source: NSO

3.4%

3.7%

7.4%

17.7%

Retailing

Grocery Retailing

Modern Grocery

Retailing

Puregold Price Club

Inc

Figure 8: Revenue CAGR of PGOLD vs.

Industry (2006-2011)

Source: MixMarket.org

CFA Institute Research Challenge November 29, 2012

Metro

Manila

28%

Luzon

37%

Vis.

16%

Min.

19%

Figure 12: Geographical Distribution of

Sari-Sari Stores

Source: DTI, Team’s Estimates

7.4%

6.7%

8.4%

8.8%

NCR

Luzon

Visayas

Mindanao

Figure 13: Wholesale and Retail Industry

Profit Margin by Geographic Area

Source: DTI, Team’s Estimates

SM and Robinsons are focused on middle-income segments, whereas Rustan‟s is focused on

upscale consumer segments. While these segments have higher purchasing power, they only

comprise 10% of the entire population and remain heavily concentrated in Metro Manila

(Figure 11). PGOLD‟s focus on essential spending allows it to grow even during recessionary

cycles and aggressively expand stores regardless of long-term economic outlook.

The acquisition of S&R represents a diversified customer base but PGOLD‟s focus remains on

grocery retailing. On the other hand, SM also operates a department store which contributes

42.70% of retail value (See Appendix 18). Robinsons operates a department store, hardware

store business, as well as convenience store Ministop. Rustan‟s also operates department

stores and high-scale specialist stores which retail imported brands. Rustan‟s is partnering with

Ayala Land to develop department stores and convenience stores in 2013.

Regional analysis supports upside of aggressive national expansion Expansion into Visayas and Mindanao is a key catalyst for revenue growth. Our in-depth

analysis into the local modern retailing sector shows a potential for 91 hypermarkets in the

Vis-Min region (See Appendix 19 for breakdown of computation based on the Index of Retail

Saturation formula).

Infrastructure Developments in Vis-Min Provide Opportunity for Modern Retail

We estimate the growing potential for hypermarkets to be spurred by development of major

road infrastructure projects especially in Mindanao. By 2013, the government will have

allocated P70B for infrastructure projects in the Mindanao over the past three years, the

highest of any region. The World Bank has 7 road infrastructure projects in the region that are

in the process of completion.ix The Bangsamoro peace treaty between the government and the

insurgent MILF in Mindanao promises better security for the road network. The development

of infrastructure allows PGOLD to replicate its operational model in Luzon to Mindanao.

Unsaturated and Fragmented Market Open Opportunities for Puregold

The market in Visayas and Mindanao is unsaturated with modern retail at 49% and 38%

saturation of Metro Manila, respectively. The only strong competitor is the Gaisano Grand

Group with 24 outlets spread across the nation. Local retail chains operate on average 9 stores.

The fragmented nature makes it strategic for PGOLD to acquire local chains to expedite Vis-

Min expansion (see Appendix 20 for competitive landscape).

Untapped Re-seller Market to Drive Revenue Growth PGOLD‟s revenues will grow as it captures an untapped market of re-sellers. 35% of

traditional sari-sari stores, PGOLD‟s key customer segment, is located in Visayas and

Mindanao (see Figure 12). We expect PGOLD‟s entry with the TNAP program to have a

dynamic effect on the growth of re-sellers in the regions, increasing the volume of re-sellers.

Higher Commodity Prices in Vis-Min to boost PGOLD long-term profit margins

Commodity prices outside Metro Manila are about 8% higher on average (See Figure 14).

Increasing commodity prices make large modern retailers who have the scale to negotiate

better prices with suppliers attractive. With PGOLD‟s position as the price leader in the

industry, it is well-positioned to compete against smaller local retail chains in Visayas and

Mindanao by introducing lower prices. This price-cutting strategy is possible as the retail and

wholesale industries in Visayas and Mindanao have higher average profit margins of 8.44%

and 8.84% respectively compared to NCR at 7.41%, due to lower operational costs (see Figure

13). Expansion will not only add revenue but also improve margins in the long-term.

Investment Summary Pure consumer play outpacing market on defensive growth

We recommend a BUY for PGOLD, the Philippines‟ fastest growing grocery retailer and the

only pure, direct, and broad-based domestic consumer play in the market, at a price target of

Php 40.16, a 24.72% upside from current price of P32.20 (Figure 15). Our positive outlook is

based on growing and resilient domestic consumption that is captured by an EDLP (Every Day

Low Prices) strategy targeting lower- to middle-income consumers, bringing in traffic of 18

million each week. Through the Tindahan ni Aling Puring (TNAP) reseller program, it is the

only major retailer to focus on the widely popular traditional sari-sari store. By acquiring

membership shopping club S&R, it also captures a growing niche of high-income consumer

spending (Figure 16). With aggressive store expansion underway, we forecast sustainable

long-term growth for this defensive stock.

Focus on domestic consumption driving resilient earnings against volatile global financial

system

As the only pure direct and broad-based domestic consumer play on the local market,

PGOLD‟s stock price has outpaced the Philippine stock market by 77.2% (see Figure 1) driven

by revenue growth of 39.69% (2012E) on the back of 16% growth in domestic consumption.

Figure 14: Consumer Price Index (Metro

Manila vs. Provincial)

100

105

110

115

120

125

130

135

Metro Manila Provincial

Source: DTI

Figure 15: Valuation Summary

Target Price PHP 40.16

Price as of

11/29/2012 PHP 32.20

Upside 24.72%

Rating BUY

Source: Team’s Estimates

Figure 16: Broad-based Consumer Target

Source: SWS, Company data, Team’s

Estimates

CFA Institute Research Challenge November 29, 2012

41 62

100

156 182

208 234

260

0

50

100

150

200

250

300

Puregold Price Club Puregold Jr.

Puregold Extra S&R

Parco

2.0%

4.0%

6.0%

8.0%

2012E 2013E 2014E 2015E 2016E

SSSG Private Consumption

With consumption expected to continue to grow by 8% annually through 2016, we forecast

same store sales growth (SSSG) to grow by a five-year CAGR of 6.44%. As a defensive stock,

PGOLD‟s earnings growth is cushioned from risk surrounding Western economies with 70%

of product revenues from essential spending on food items and 90% of customer revenues

expected to come from low-income consumer segments and traditional re-sellers. The surge in

the local economy has benefited the S&R format, which is expected to boost consolidated net

margins to 5.58% (from 4.83% in 2011) with its high-margin product portfolio.

Steady SSSG to sustain long-term growth: PGOLD is confidently enjoying stable same-store-

sales growth (SSSG) which contributes to long-term revenue growth. Company forecasts place

2013 SSSG at 4% for Puregold and 15% for S&R. Same-store sales is estimated to grow by a

CAGR of 6.41% from 2012-16 and 3.755% (equal to the terminal growth rate) for 2017

onwards driven by increasing domestic consumption and strong population growth.

Aggressive national roll-out catalyzing revenue growth By adding 51 stores outside Metro Manila this year alone, Puregold revenues are slated to

grow by 39.69% in 2012. Four-year revenue CAGR of 23.6% is expected on the back of

aggressive expansion raising total store count to 260 by 2016 (Figure 18). A key catalyst will

be expansion into the unsaturated and attractive market of Visayas and Mindanao where we

calculate a potential of 91 hypermarkets to be added (See Appendix 19 for computations).

With a hypermarket opening in Palawan today, it has already begun operating its first store

outside of the island of Luzon.

PGOLD targets a roll-out of 25 new Puregold stores every year through 2016, focused on

hypermarket expansion in underpenetrated areas outside of Metro Manila. Expanding the

horizons of store operations towards Vis-Min will drive revenue growth. This area represents

35% of sari-sari stores, PGOLD‟s key target market.

S&R to simultaneously drive growth and profitability: Recent acquisition S&R, the only

membership shopping club in the Philippines, is projected to expand to 10 stores by 2016,

addressing the small but highly-profitable segment of upscale consumers in the AB segment.

While this segment only comprises 1% of the Philippine population, it is expected to

contribute to 10% of company revenues, closely matching its income contribution to the local

economy at 9%. The portfolio of high-margin products from S&R will contribute to increased

consolidated margins, forecasted to grow from 14.79% to 20% in gross margins and from

4.83% to 8.85% in net margins by 2016.

Scalable asset-light model translating to strong margins and abundance of free cash

PGOLD has a scalable asset-light model that relies on property leasing and third-party logistics

from suppliers. Fixed Asset Turnover is seen to improve from 6.49 to 10.96 (2011-16E),

showing potential for growth. This translates to impressive ROE and profit margin at 21.95%

and 8.85% respectively which are both above industry average. PGOLD generates an

abundance of free cash enough to meet the expected yearly annual capex of Php 3.46B

allocated for expansion from 2013 to 2016. With issuance of additional debt, special Dividend

Payout Ratio (DPR) at 2016E is 43.82% on top of the actual DPR of 14.91%, giving a total

DPR of 58.73%

Valuation confirms BUY rating

FCFE analysis indicates a price of Php 40.16 at a 24.72% upside from current price,

supporting our positive long-term outlook. PER with Asia-Pacific grocery retailers indicate

discounts of 20.75%, confirming the attractiveness of PGOLD (Figure 21).

PGOLD is the only listed grocery retailer, with other retailers listed under the holdings of their

conglomerates (SM and Robinsons). Comparables in the local bourse are consumer-themed

stocks like URC. PGOLD‟s 2012E P/E is at 28.01, which is 16.57% above the local average of

24.03 (Figure 22). This margin is reasonable given PGOLD‟s huge growth trajectory as

compared to other companies, engaged in the more mature and competitive food and beverage

industry where growth prospects are foreign rather than domestic (See Appendix 18).

Strong fundamentals affirm positive outlook: Indicative of profitability and efficiency,

PGOLD has registered an impressive 27.43% sales revenue CAGR in 2008-11 while key

profit-margin ratios (gross, operating, and net) have all been steadily increasing, driven by the

company‟s aggressive expansion and efficient cost control.

As for efficiency in asset management important in the retail industry, PGOLD comes second

only after regional conglomerate Dairy Farm in terms of ROA in the region and its upward

trajectory is seen to continue with dramatic increases in ROA as a result of aggressive

expansion resulting to economies of scale (Figure 23). This implies a larger growth potential

for PGOLD than for other groceries in other regional markets (Appendix 22).

Figure 17: Consumption growth vs. SSSG

Source: Euromonitor, Company data,

Team’s Estimates

Figure 21: Regional Peers‟ P/E and PEG P/E (2012E) PEG

Big C 23.94 1.26

Siam Makro 29.57 1.48

Sumber Alfaria

Trijaya 35.57 -

Sun Art Retail Group

34.96 1.94

Dairy Farm 26.66 1.62

Peer Average 30.14 1.58

Puregold 27.03 1.18

Source: Bloomberg

Figure 20: Summary of Capex

Projections and Estimated Returns

Year CAPEX

(in PHP mn)

Payback

Period

(in years)

2012E 3,185.00 0.40

2013E 3,459.74 0.46

2014E 3,459.74 0.50

2015E 3,459.74 0.46

2016E 3,459.74 0.43

Source: Team’s Estimates

Figure 18: Expansion Plans

Source: Company Data, Team’s Estimates

Figure 19: 2012-2016 DPS Forecast

Source: Team’s Estimates

CFA Institute Research Challenge November 29, 2012

Investment Risks Execution of Vis-Min expansion: PGOLD will venture into new waters in its expansion into

the Vis-Min region. Although this will be a key catalyst for growth, this would also serve to

test the execution of PGOLD‟s asset-light supply chain. Disruptions in the supply chain could

increase cost of operations, deplete margins, and limit the expansion potential of 91

hypermarkets in Vis-Min. PGOLD addresses this risk in its partnership with third-party agents

and regional distributors.

Competitive risks from SM: Growing competition with its largest rival, SM Retail, is seen to

intensify as SM undertakes expansion plans across the country, which can lead to a price war

as well as drive up leasing costs. This threat can be mitigated through PGOLD‟s stronghold on

resellers with the TNAP program which has a membership base of 220,000. An asset-light

model leading to healthy profit margins also equips PGOLD for a possible price war with SM.

Adherence to corporate governance standards seen to improve

Concerns on corporate governance are set to ease as the company transitions from a family

business to a public company. While PGOLD is compliant with all corporate governance

guidelines of the Securities and Exchanges Commission and as of October 2012 has committed

no violations of its Revised Manual on Corporate Governance, full compliance with PSE good

corporate governance guidelines remains to be seen (see Appendix 23). Primary concerns

raised are regarding the board composition consisting mostly of Co family members. This is

financially materialized over concerns of related-party transactions composed of leasing deals

by family-owned properties and the brand licensing rights owned by Lucio Co. The financial

exposure to these transactions is set to decline as a percent of operational expenses from 18%

to just 11% from 2011 to 2016 (Appendix 23). The company also provides continuous

education and seminars for its board and senior management to improve governance practices.

Valuation BUY rating: Target Price of PHP 40.16 Upside of 24.72% PGOLD‟s target price of PHP 40.16 is based on the DCF method of Free Cash Flow to Equity

(FCFE) which is able to capture PGOLD‟s long-term value based on strong organic growth

and store expansion plans. Our strong BUY rating is further validated through PER analysis

based on the average regional PER of 30.14x.

The Free Cash Flow to Equity (FCFE) Model

The FCFE model assumes that most of the company‟s value comes from long-term future

value. We consider this assumption suitable for PGOLD as its revenue growth will be

maximized only after the stability of its new stores in their respective areas (see Appendix 24

and 25 for the tools used in the projection model).

FCFE’s Two Major Components: Projected Free Cash Flows & Terminal Value The discounted five-year projected free cash flows per share is PHP 4.50 whereas the

discounted terminal value per share is PHP 35.66. (See Figure 25 for a breakdown of the FCFE

model‟s components.)

FCFE’s Assumptions

1. Php 3.0 B will be spent every year from 2013-2016 for Puregold capital expenditures.

(This is based on company historical data.)

0%

2%

4%

6%

8%

10%

12%

14%

16%

2008 2009 2010 2011

Big C Siam Makro

Sumber Alfaria Trijaya Sun Art Retail Group

Dairy Farm Puregold

Figure 23: ROA Trends across the Region

Source: Businessweek

Source: Company Data, Team’s

Research

Figure 24: PGOLD Events Timeline

Figure 22: Local Peers 2012 P/E Ratios

Retail Company P/E

Jollibee Foods (JFC) 30.53

Pepsi-Cola Products (PIP) 21.72

RFM Corp. (RFM) 19.52

Universal Robina (URC) 24.34

AVERAGE 24.03

Puregold 28.01

Source: Bloomberg

Figure 25: FCFE‟s Major Components

and Subcomponents

5-year Projected

Free Cash Flows PHP 4.50

EBIT less tax

Depreciation

Less: Change in Working

Capital

Less: CAPEX

Terminal Value PHP 35.66

Terminal Growth Rate

WACC

Source: Team Estimates

CFA Institute Research Challenge November 29, 2012

2. Php 0.459 B will be spent every year from 2013-2016 for S&R capital expenditures. (This

is based on company historical data.)

3. All new stores' sales will be fully realized and maximized after six to eight months of full

operations. If there is no data available on the finished construction, the store's sales were

assumed to be realized after one year of full operations. (This is backed by company data.)

4. Sales revenue for each store format (including S&R) is assumed to grow each year by:

6.25% for hypermarkets, 8.00% for supermarkets, 3.00% for discounters, and 6.50% for

S&R. (See Figure 26 for the bases for and derivation of these rates.)

5. Puregold financial statement items grow with store selling area.

6. S&R financial statement items grow with the number of stores.

7. There will be 25 new Puregold stores--specifically, 14 hypermarkets, 9 supermarkets, and

2 discounters--every year from 2013-2016. (This is based on company projections and

retaining the proportion of new stores per store format from 2012, as seen below.)

8. There will be 1 new S&R store every year from 2013-2016. (This is based on company

projections.)

9. The terminal growth rate is 3.7550%. (See derivation in subsection below).

Projected Free Cash Flows (FCF): Drivers of Growth

PGOLD‟s increasing five-year FCF projections is driven by: (1) revenue growth from SSSG

due to rising domestic consumption, (2) additional revenue from aggressive store expansion

particularly in Vis-Min, and (3) improving profitability from increasing scale of operations.

Strong Growth in Domestic Consumption Driving Strong Same Store Sales Growth

Same store sales growth (SSSG) is expected to increase at a rate of 6.41%, driven by the strong

growth in domestic consumption of 4.40% (Euromonitor). This is pushed by the country‟s

above-average population growth of 2%.

Aggressive Expansion Driving Revenue Growth

Aggressive store roll-out expected to add 104 stores by 2016, will drive revenue growth.

Venturing into the Vis-Min markets would lead to increasing profitability in the long-run since

profits and revenues would increase as PGOLD gains familiarity and stability in new areas.

Scalability and Strategic Acquisitions Driving Profitability

The stable growth of operating expenses vis-à-vis rapid sales growth leads to higher margins,

which contributes to PGOLD‟s increasing future value. Opposing movements of naturally

increasing expansion-related costs and lower operating costs in Visayas and Mindanao balance

each other out leading to stability.

With its preference for lease arrangements and partnership with suppliers and third-party

cross-docking providers, PGOLD‟s asset-light scalable model leads to higher profitability

because of the minimum investment required for store expansion. This is reflected in the

shorter payback period (see Appendix 26) and minimal logistical costs such as distribution

costs as these are mostly shouldered by PGOLD‟s third-party suppliers.

Economies of scale would result from rapid expansion via organic growth and acquisitions and

should lead to higher rebates and discounts from suppliers. (See Figure 18 for an illustration of

the expansion plans.) The increasing number of PGOLD stores would scale the expenses

accordingly, leading to higher operating expenses especially. This, however, is cancelled out

by lower operating costs, as it is easier to source manpower and real estate at relative lower

costs outside of Metro Manila.

Projected margins show strong growth, which is crucial for PGOLD‟s position as the low-price

leader in the modern retail sector. Strong margin growth is attainable due to PGOLD‟s

strategic acquisitions and rapid expansion plans. Strategic acquisitions, such as S&R, boost

consolidated margins, with its portfolio of higher margin items sold to the AB market.

Terminal Value: Assumptions

The weighted average cost of capital (WACC) is calculated to be 7.95%. The terminal growth

rate was estimated to be 3.7550%, factoring in S&R growth driven by consumption of AB

socio-economic segment and PGOLD‟s broad customer base of resellers and retail consumer.

Derivation: Terminal Growth Rate The computation of the terminal growth rate was based on 1) reseller value growth, 2) growth

of household consumption of essentials, and 3) growth of AB private consumption to reflect

same-store sales growth from Puregold and S&R‟s customers. Growth rate for household

consumption is based on steady growth of grocery spending despite long-term economic

outlook while the rate for re-seller growth is based on the growth rate of traditional retailers, a

mature industry which we expect to remain a staple in the Philippine economy. The weights

were derived from PGOLD data on revenue contribution based on customer type (35% for re-

Figure 27: Terminal Growth Rate

Computation

Re-seller Value Growth 3.00%

Weight 32%

Household Consumption

of Essentials 4.00%

Weight 59%

AB Private Consumption 4.70%

Weight 10%

Terminal Growth Rate 3.755%

Source: Euromonitor

Figure 28: WACC Breakdown

Cost of Equity (re) 6.43%

Risk-free rate 6.5%

Beta 0.81

Risk Premium 5.0%

Equity/Asset 60.99%

Cost of Debt (rd) 1.51%

Weighted average

cost of debt 5.53%

Tax rate 30%

Debt/Asset 39.01%

WACC 7.95%

Source: Company Data, Team’s

Estimates

Figure 26: Bases for Same Store Sales Growth

(SSSG) rate per store format

Store

Format

Basis for

Growth Rate

Rate/

Formula

Hypermar-

ket

35% Resellers,

65% CDE

market (retail)

(0.35)*3%

+

(0.65)*8%

Supermar-

ket

Short-term

Household

Consumption

Growth

8.00%

Discounter

Short-term

Reseller Value

Growth

3.00%

S&R

Short-term AB

Consumption

Growth

6.50%

Source: Euromonitor

Figure 29: PER Analysis

Number of Shares

(in millions) 2,766

EPS 1.29

P/E 30.14

Target Price 38.88

Upside 20.75%

Source: Company Data,

Team’s Estimates

CFA Institute Research Challenge November 29, 2012

sellers and 65% for retail consumers) as well as a conservative estimate of S&R contributing to

approximately 10% of sales. (See Figure 27 for the computation).

Derivation: Weighted Average Cost of Capital (WACC)

For the WACC calculation, the CAPM model was used to calculate the cost of equity (re),

using the 20-year government bond rate for the risk-free rate of 6.5%, a 5% market risk

premium, and an adjusted beta of 0.81 based on team‟s estimates. (See Figure 28 for the

breakdown of the WACC calculation.)

Price-to-Earnings Ratio (PER) Analysis

PER analysis validates PGOLD‟s strong BUY rating as it shows that PGOLD is slightly

undervalued compared to most local and regional industry competitors, based on an average

local and regional PER of 30.14x. (See Figures 21 and 22 for the PER comparison with Asia

Pacific grocery retail and local peers.) Further computation yielded an optimistic target price

of PHP 38.88 with an upside of 20.75%. (See Figure 29 for the PER Analysis calculation.)

Financial Analysis

Income Statement

Robust sales growth driven by all-out national expansion

PGOLD‟s revenues are slated to grow at about 39.69% for 2012, primarily attributable to the

consolidation of earnings from newly acquired retail chains, Parco and S&R, on top of

execution of organic growth plans. For the succeeding years, sales are also expected to post a

2012-2016 CAGR of 23.59% with the aggressive store roll-out which will grow the number of

stores to 260 by 2016, and greater sales contribution from S&R at about 10% (Figure 30).

Same store sales will continue to rise from 2012 to 2016 at a rate of 6.41% on the back of

increasing private consumption, but growth is expected to slow down to 3.755% when new

stores begin to mature and competition enters the same geographical areas. Targeting re-sellers

will be a strategic driver of growth as shown in the revenue impact of expanding network of

the TNAP program (see Appendix 27).

Healthy margins support price leadership strategy

PGOLD will continue improvements in gross margin to 20% in 2016 due to: 1) allocation of

20-25% (higher than the current 10-15%) of the selling area in new stores for high margin

items and 2) higher margin products of S&R. On top of the sustained relationships with

suppliers which give them a 4% rebate, this stronger performance of the gross margin will

allow the company to competitively price its grocery products.

Scale economies back profitable expansion

The scalable operations of the company gives PGOLD the capability to open new stores with a

minimal investment of P120 million per store (See Appendix 26). Expanding store network

allows the company to maintain an average operating margin of 11% as a result of lower

selling and labor expenses in the Vis-Min area. This is partially offset if warehousing will be

set-up in Vis-Min (Figure 31).

Expansion will lead to a continual increase in the bottom line of 61% for 2012 and 39% CAGR

for the years 2012-2016, equivalent to a healthy profit margin of 8.9% which remains well

above the industry average of 1.5%-2% (see Appendix 21). This translates to an impressive

growth trend in EPS projected at 38.7% CAGR for 2012 through 2016 (Figure 32). Estimated

payback for investments averages 5-6 months (see Appendix 26).

Cash Flows capable of driving expansion initiatives and high dividend payouts

Free cash is expected to grow dramatically due to healthy earnings stream, as EBIT is expected

to grow at an average rate of 44% from 2012 to 2016. Cash flows from operating activities will

continue to increase at a CAGR of 36% as operations expand. The CapEx trend is seen to be

sustained, with a yearly CapEx is forecasted to increase to Php 3.46B due to aggressive store

expansion, and maintenance and renovation costs of existing stores. A double-digit times

interest earned (TIE) ratio gives room for PGOLD to fund expansion with debt. Stronger cash

flows and increase in leverage allow the company to drive further growth with acquisitions or

increase dividend payouts per share at a 15% CAGR through 2016 (see Figure 19).

Balance Sheet shows scalable operations

With higher cash flows, PGOLD retains a cash-rich position allowing the company to improve

liquidity, as seen in a higher current ratio of 1.47x and quick ratio of 1.23x by 2016E.

Moreover, maintaining stable relationships with suppliers gives PGOLD the ability to not only

keep a negative Cash Conversion Cycle which minimizes capital tied to the business, but also

rely on their third-party logistics which reduces warehousing and distribution costs. This asset-

0%

10%

20%

30%

40%

50%

60%

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

Revenues Growth

Source: Company Data, Team’s Estimates

Figure 30: PGOLD Revenue and Growth

Figure 31: PGOLD Gross and Operating

Margins

Source: Company Data, Team’s Estimates

Figure 32: PGOLD EPS Growth and

Profit Margins

Source: Company Data, Team’s Estimates

0.00%

10.00%

20.00%

30.00%

Gross Margin EBIT Margin

0%

10%

20%

30%

40%

50%

60%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2012E 2013E 2014E 2015E 2016E

Profit Margin EPS Growth

CFA Institute Research Challenge November 29, 2012

light strategy allows PGOLD to capitalize on the scalability of its operations, which translates

to a higher ROE of 21.95% by 2016E. With the recent issuance of P5B worth of notes to fund

store roll-outs, PGOLD‟s D/E ratio average 0.69x for the years 2012E through 2016E.

The Upside Potential of Social Sustainability PGOLD‟s approach to growing the business shows a socially sustainable model that can be

used to create a further upside. Sustainability initiatives will create long-term value that

secures growth and even attract new investors like socially-responsible investments (SRIs).

PGOLD: Regional Model for Sustainable Development of Modern Retail Modern retailing in Asia Pacific faces sustainable development challenges as its expansion

threatens the livelihood of small traditional store owners. Strong pressure from this sector has

spurred government regulation to protect small traditional retailers. In Thailand, the Retail and

Wholesale Act introduced zoning restrictions that limit large retailers from operating in the

central zone of cities. In Indonesia, new licenses for modern retailers have been limited to

control the location of stores (See Appendix 22 for government regulation across Asia Pacific).

PGOLD answers the challenge of sustainable development with a business model that

approaches traditional retailers as customers rather than competitors. Through the TNAP

program, it supports sari-sari stores that provides livelihood to hundreds of thousands of

Filipino women and their families. Rather than threaten the livelihood of traditional retailers, it

has made them partners in business growth. With this, we are confident that Puregold‟s

expansion are not only free from regulatory threats but will enjoy strong support from the local

community.

Partnerships with Micro-finance Organizations Can Boost Re-seller Program An upside to growing re-seller customers can be captured with a tie-up between PGOLD‟s

TNAP program and micro-finance organizations. Micro-finance programs offer financial

support to many small enterprises like sari-sari stores but are interested in providing business

support to ensure feasibility of loan repayments. An attractive opportunity exists for TNAP to

take over business support and training for these micro-finance programs while capturing re-

sellers under micro-finance programs as customers. A tie-up with micro-finance programs

already in Visayas and Mindanao could be a strong entry strategy for the TNAP program into

the region and complement store expansion (see Appendix 27).

Building Long-Term Value: Understanding the Cost of Private Label Expansion PGOLD has made a conscious decision to limit selection of private label products to maintain

strong relationships with suppliers. It is limited to fresh goods and basic commodities and

contributes only 2% of sales. While private label may be quickly growing, there is an unseen

cost of straining relationships with suppliers. We view the decision to limit private label

expansion positively as a sustainable strategy given PGOLD‟s rapid expansion relies on

supplier commitment of getting the best prices from suppliers at uniform rates and providing

logistical support. Protecting relationships with suppliers creates long-term value for Puregold

in terms of strong margins and a favorable cash conversion cycle.

Investment Risks Remittance Risks: Minimal on PGOLD’s Broad-Based Play Slow-down in the global economy can affect OFW remittances which drive growth of

domestic consumption. 53% of remittances come from the United States while 17% come

from Europe, thus putting a significant portion of remittances at risk due the current recession

in countries within the same region.

Remittances growth rates run in correlation with global macroeconomic condition, as

expressed by the world GDP growth rate. However even during recessions, OFW remittances

exhibit positive growth (see Figure 33). Though this resilience of OFW remittances contributes

to the aggressive growth of domestic consumption, it is the Philippines‟ above-average

population growth of 2.0% that secures a steady rise of consumption. Private consumption will

rise along a booming population, projected to hit P7.68B at 2012 year-end (see Figure 34).

PGOLD is positioned to limit remittance risks because of its broad-based play. Consumption

of essentials such as food, which comprises 70% PGOLD‟s SKUs, are expected to grow

regardless of economic fluctuations.

Competitive Risks: Local Player SM expands grocery retail business Heightened competition with SM is expected as modern grocery retail develops. SM plans to

expand at a growth of 30 stores yearly, more than PGOLD‟s 25 store a year target, while also

keying strategic acquisitions. Backed by the deep pockets of the SM conglomerate headed by

tycoon Henry Sy, expansion targets are financially feasible. This may create a competition for

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

2006 2007 2008 2009 2010 2011

World GDP Growth Rate

OFW Remittances Growth Rate

Figure 33: World GDP Growth Rate and

OFW Remittances Growth Rate

Source: IndexMundi, Banko Sentral ng

Pilipinas

0

2000

4000

6000

8000

10000

12000

8486889092949698

100102104

Population (Millions)

Private Consumption (PhP Billions)

Figure 34: Philippine Population and

Philippine Private Consumption

Source: Euromonitor, TradingEconomic,

Team’s Estimates

CFA Institute Research Challenge November 29, 2012

0%

5%

10%

15%

20%

25%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Operation Expenses (PhP Thousands)

Rel. Party Transactions / Oper.

Expenses (%)

prime locations, drive up leasing costs and limit organic expansion, as well as enter into a

price-cutting war which could hurt margins.

PGOLD addresses the threat of heightened competition by maintaining its Everyday Low Price

(EDLP) strategy through introducing more high-margin products and building on supplier

relationships. The company is planning to allot more space for its high-margin items (15-25%

margin) such as freshly produced goods, general merchandise, and small apparel, from 10-15%

of per-store net selling space to 20-25%. Unlike SM, PGOLD maintains strong relationships

with suppliers by limiting private label products and thus allowing the company to negotiate

low prices. Its asset-light model also improves margins equipping it for possible price wars.

PGOLD‟s strong hold on re-sellers is a distinct advantage that SM does not have. TNAP is the

only existing major move by a modern retailer to capture the dominant traditional retailing

industry seen in the ubiquitous sari-sari store. The discounter format Puregold Extra offers

competitive pricing on top-selling SKUs, thus servicing the needs of sari-sari stores.

Regulatory Risks: Trade Liberalization Sees Potential for Entry of Foreign Retailers Regulatory risks involve potential entry of foreign players in the grocery retail market. The

Trade Liberalization Act implemented in 2000 lessened restrictions for foreign ownership of

businesses leaving the door open for international players to enter the Philippines. No

international retailer has yet entered the hypermarket and supermarket formats, but Hong

Kong-based retailer Dairy Farm acquired a 50% stake in Rustan‟s retail group. Dairy Farm is

the leading retailer in the Asia Pacific region operating in 10 countries.

Risk is mitigated because of PGOLD strategic customer focus on low-income segments and re-

sellers that is very well adapted to the local market. It has a first-mover advantage in capturing

sari-sari stores through the 220,000 member-strong TNAP program.

Operational Risk: Expansion to the Vis-Min region Expansion to the Vis-Min region is a key catalyst to the company‟s projected growth but

presents a substantial operations risk. PGOLD‟s asset-light supply chain model which has been

successful in Metro Manila and Luzon is yet to be tested in the Vis-Min region. Disruptions in

supply chain could increase cost of operations, deplete margins and limit the expansion

potential of 91 hypermarkets in Vis-Min.

PGOLD tries to reduce the risk by relying on regional distribution of suppliers who have

regional depots A store in Palawan has opened to simulate operations outside of Luzon before

a full store roll-out in Vis-Min. The option of setting up warehousing in VisMin Is also a

possibility. To ease the transition of learning a new market environment, senior management

from established stores in Metro Manila and Luzon are expected to be assigned to new store

locations in VisMin. Mindanao can be prioritized for expansion given it has a strong potential

to replicate PGOLD‟s existing operational model given similar geography with Luzon and

lower retail saturation compared to Visayas.

Governance Risk: Related-Party Transactions Related-party transactions represent a governance risk. The company is currently in a 30-year

licensing agreement with the owner Lucio Co, stipulating annual payment of 0.02% of the

company‟s net sales for use of the trademark names by PGOLD. A huge bulk of related party

outflows is from leasing of 25 store locations to property owned by the Co family. Risk

primarily stems from the uncertain renewal with both the licensing and leasing agreements

leading to disputes between public shareholders and the Co Family. Furthermore PGOLD has

rendered only partial compliance to the Manual of Corporate Governance of the SEC as of

2011, particularly in audit-related regulations.

To ensure policies against dubious transactions, the company has put up three new board

committees in compliance with the Manual of Corporate Governance of the SEC, namely an

Audit Committee, Nomination Committee, and Compensation Committee. A charter for the

Audit Committee has also been approved and now in effect. These, together with other policy

changes, put the company in full compliance with the Manual of Corporate Governance as of

3Q 2012, compared to a compliance average among the 30 PSE index companies of 95% of

the 75 total compliance guidelines. Furthermore, the company is currently managing its lease

transactions more strictly, thus related party transactions are estimated to decline as a percent

of operating expenses from 19% (2011) to 10% by 2016 (see Figure 35 and Appendix 23).

Valuation Risks Given 89% of PGOLD‟s intrinsic value is in the long-term, valuation is sensitive to the

terminal growth rate. A Monte Carlo simulation on such resulted in a minimum probability of

a SELL at 2% while the level of confidence to recommend BUY is at a high 61% (See Figure

37 and Appendix 28). In case perpetual growth rate falls below target, the possibility of a Hold

at 37% reflects the stability of PGOLD as a defensive stock to invest in.

0

2

4

6

Slowdown in

Remittances

Local

Competition

Entry of Int'l

Competitor

Expansion to

VisMin

Related-Party

Transactions

Level of Risk Level of Mitigation

Source: Team’s Estimates

Figure 36: Levels of Investment Risks

and PGOLD‟s Mitigation Efforts

Figure 35: Related Party Transactions as

% of Operating Expenses

Source: Company Data, Team’s Research

Figure 37: Result of Monte Carlo Simulation

Source: Team’s Estimates

CFA Institute Research Challenge November 29, 2012

i Grocery Retailers in the Philippines, Euromonitor International, February 2012 ii Private Final Consumption Expenditure: Euromonitor International from national statistics/Eurostat/OECD/UN/International Monetary Fund (IMF), International Financial Statistics (IFS) iii Philippine Census 2010, National Statistics Office. iv United Nations ESCAP “Statistical Yearbook for Asia and the Pacific” http://www.unescap.org/stat/data/syb2011/I-People/Population.asp v CLSA Asia-Pacific Study vi SM Retail is a subsidiary of SM Holdings listed in the Philippine Stock Exchange (PSE) vii Robinsons Retail Group is a subsidiary of JG Summit Holdings listed in the PSE viii Rustans through minority stakeholder Dairy Farms Holdings is listed in the Hong Kong Stock Exchange ix “Mindanao to get biggest infra budget in 2013”, Philippine Daily Inquirer. September 2012

Appendix

Appendix 1 Income Statements ............................................................................................................ 1

Appendix 2 Balance Sheets .................................................................................................................. 3

Appendix 3 Statements of Cash Flows ................................................................................................. 6

Appendix 4 Key Financial Ratios (Consolidated) .............................................................................. 10

Appendix 5 Income Statements (Common-Size) ............................................................................... 11

Appendix 6 Balance Sheet (Common-Size) ....................................................................................... 13

Appendix 7 S&R Financial Statements .............................................................................................. 16

Appendix 8 Puregold Store Formats ................................................................................................... 19

Appendix 9 Current Locations of Puregold Stores ............................................................................. 20

Appendix 10 Puregold Customer Base ............................................................................................. 21

Appendix 11 Tindahan Ni Aling Puring (TNAP) Program .............................................................. 22

Appendix 12 Puregold Ownership Structure .................................................................................... 23

Appendix 13 Puregold Board of Directors and Management ........................................................... 24

Appendix 14 Puregold Store Roll-Out Plans .................................................................................... 25

Appendix 15 Porter’s Five Forces Analysis ..................................................................................... 26

Appendix 16 Global Retail Development Index ............................................................................... 27

Appendix 17 Profiles of Major Grocery Retailers ............................................................................ 28

Appendix 18 Revenue Breakdown of Local Company Stocks ......................................................... 29

Appendix 19 Store Growth Potential ................................................................................................ 30

Appendix 20 List of Local and Provincial Competitors ................................................................... 32

Appendix 21 Retail Performance Benchmarks ................................................................................. 33

Appendix 22 Modern Grocery Retail in Southeast Asia................................................................... 34

Appendix 23 Corporate Governance ................................................................................................ 35

Appendix 24 M&A And FCFE Method ........................................................................................... 36

Appendix 25 Regression Analysis .................................................................................................... 37

Appendix 26 Investment Costs and Returns ..................................................................................... 39

Appendix 27 Sensitivity Analysis ..................................................................................................... 41

Appendix 28 Monte Carlo Simulation .............................................................................................. 42

Appendix 29 SWOT Matrix of Current and Potential Strategies ..................................................... 43

Appendix 30 Investment Ratings Definition .................................................................................... 43

1

Appendix 1 INCOME STATEMENTS

Appendix 1.1: PGOLD (Consolidated) Income Statement

2008 2009 2010 2011 2012E 2013E 2014E 2015E 2016E (in PHP 000,000)

Net Sales 18,842 24,112 29,108 38,988 59,541 81,273 100,718 122,258 148,707

Hypermarkets 18,842 24,112 27,584 33,557 47,310 60,466 75,081 91,288 111,848

Supermarkets - - 1,481 4,695 7,062 9,387 12,039 15,055 18,477

Discounter - - 43 737 966 1,137 1,317 1,508 1,708

S&R - - - - 8,407 10,283 12,280 14,408 16,674

Cost of Sales 17,451 21,893 25,577 33,453 49,847 67,148 82,343 98,885 118,965

Gross Profit 1,391 2,219 3,531 5,535 9,695 14,125 18,375 23,373 29,741

Other Operating Income 892 785 781 1,052 1,330 2,030 2,536 3,102 3,806

Selling Expenses 1,711 2,082 2,696 3,568 5,061 6,456 7,937 9,552 11,535

General and Administrative

Expenses 131 183 261 382 662 937 1,148 1,378 1,655

Other Operating Expenses 144 282 370 421 620 778 927 1,080 1,260

Operating Expenses 1,986 2,546 3,326 4,371 6,343 8,170 10,012 12,010 14,450

Operating Income 297 458 985 2,216 4,682 7,985 10,899 14,465 19,097

Other Expense (Income) 119 (21) 12 (57) 10 18 18 18 21

Interest Expense - 290 230 68 68 325 328 332 355

Earnings Before Taxes 178 189 743 2,205 4,604 7,642 10,553 14,115 18,722

Tax Expense 48 58 233 660 1,448 2,293 3,166 4,234 5,616

Net Income 129 132 510 1,545 3,156 5,384 7,423 9,919 13,160

Appendix 1.2: Consolidated: Puregold Price Club, Inc.; Puregold Jr.; Puregold Extra

Income Statement 2008 2009 2010 2011 2012E 2013E 2014E 2015E 2016E

(in PHP 000,000)

Net Sales 18,842 24,112 29,108 38,988 55,338 70,990 88,438 107,850 132,033

Hypermarkets 18,842 24,112 27,584 33,557 47,310 60,466 75,081 91,288 111,848

Supermarkets - - 1,481 4,695 7,062 9,387 12,039 15,055 18,477

Discounter - - 43 737 966 1,137 1,317 1,508 1,708

Cost of Sales 17,451 21,893 25,577 33,453 46,484 58,922 72,519 87,359 105,626

Gross Profit 1,391 2,219 3,531 5,535 8,854 12,068 15,919 20,492 26,407

Other Operating Income 892 785 781 1,052 1,284 1,938 2,428 2,979 3,667

Selling Expenses 1,711 2,082 2,696 3,568 5,004 6,342 7,805 9,401 11,365

General and Administrative

Expenses 131 183 261 382 541 695 865 1,055 1,292

Other Operating Expenses 144 282 370 421 601 740 883 1,030 1,203

Operating Expenses 1,986 2,546 3,326 4,371 6,146 7,776 9,553 11,485 13,860

Operating Income 297 458 985 2,216 3,992 6,230 8,794 11,985 16,215

Other Expense/Income 119 (21) 12 (57) 10 18 18 18 21

Interest Expense - 290 230 68 46 277 277 277 277

Earnings Before Taxes 178 189 743 2,205 3,936 5,935 8,500 11,690 15,917

Tax Expense 48 58 233 660 1,181 1,781 2,550 3,507 4,775

Net Income 129 132 510 1,545 2,755 4,155 5,950 8,183 11,142

2

Appendix 1.3: S&R

Income Statement 2012E 2013E 2014E 2015E 2016E

(in PHP 000,000)

Net Sales 4,204 10,283 12,280 14,408 16,674

Cost of Sales 3,363 8,226 9,824 11,526 13,339

Gross Profit 841 2,057 2,456 2,882 3,335

Other Operating Income 46 92 108 123 138

Selling Expenses 57 114 133 151 170

General and Administrative Expenses 121 242 282 323 363

Other Operating Expenses 19 38 44 51 57

Operating Expenses 197 394 459 525 590

Operating Income 690 1,755 2,105 2,480 2,883

Other Expense (Income) - - - - -

Interest Expense 22 49 51 55 78

Earnings Before Taxes 668 1,707 2,053 2,425 2,804

Tax Expense 268 512 616 727 841

Net Income 401 1,229 1,473 1,736 2,018

Source: Company Data, Team’s Estimates

3

Appendix 2 BALANCE SHEETS

Appendix 2.1: PGOLD (Consolidated)

Balance Sheet 2008 2009 2010 2011 2012E 2013E 2014E 2015E 2016E

(in Php 000,000)

ASSETS

Cash and Cash Equivalents 1,225 1,136 1,838 1,955 4,855 9,949 16,621 25,269 36,467

Receivables 809 645 242 410 613 877 1,018 1,160 1,319

Merchandise Inventory 1,901 1,904 2,934 4,523 6,273 8,730 10,442 12,225 14,276

Other Current Assets 4,034 6,230 402 560 805 1,105 1,379 1,785 3,003

Current Assets 7,969 9,916 5,416 7,449 12,546 20,661 29,461 40,440 55,065

NET PPE 1,592 2,166 4,146 6,006 8,115 10,450 11,933 13,129 13,998

Deferred Tax Assets 67 101 165 220 295 356 417 477 549

Other Noncurrent Assets 235 285 397 3,005 8,330 8,349 11,081 13,955 17,574

Goodwill - - - - 16,054 16,054 16,054 16,054 16,054

Total Noncurrent Assets 1,894 2,552 4,708 9,231 32,794 35,209 39,485 43,616 48,175

Total Assets 9,863 12,468 10,124 16,680 45,340 55,871 68,946 84,055 103,240

LIABILITIES AND SHAREHOLDER EQUITY

Short-Term Borrowing 4,241 6,114 2,092 - 569 1,381 2,570 2,984 3,614

Accounts Payable 3,252 3,793 5,109 6,421 9,662 13,089 16,321 19,948 24,495

Other Current Liabilities 1,015 960 328 208 1,048 2,181 4,145 6,547 9,336

Total Current Liabilities 8,508 10,867 7,529 6,629 11,280 16,651 23,036 29,479 37,445

Noncurrent Accrued Rent 218 318 508 663 663 663 663 663 663

5-year bonds (5.4881% p.a.) - - - - 4,000 4,000 4,000 4,000 4,000

7-year bonds (5.8673% p.a.) - - - - 1,000 1,000 1,000 1,000 1,000

Retirement Benefits Liability 3 17 39 76 89 110 129 147 169

Total Noncurrent Liabilities 221 335 547 739 5,752 5,773 5,792 5,810 5,832

Total Liabilities 8,729 11,202 8,076 7,368 17,031 22,424 28,828 35,289 43,276

Capital Stock 796 796 1,450 7,169 23,233 23,243 23,243 23,243 23,243

Retained Earnings 338 470 598 2,143 5,076 10,203 16,875 25,523 36,721

Total Equity 1,134 1,266 2,048 9,312 28,309 33,446 40,118 48,766 59,964

Total Liabilities and Equity 9,863 12,468 10,124 16,680 45,340 55,871 68,946 84,055 103,240

4

Appendix 2.2: Consolidated: Puregold Price Club, Inc.; Puregold Jr.; Puregold Extra Balance Sheet

2008 2009 2010 2011 2012E 2013E 2014E 2015E 2016E (in Php 000,000)

ASSETS

Cash and Cash Equivalents 1,225 1,136 1,838 1,955 4,157 7,324 12,523 19,435 28,615

Receivables 809 645 242 410 491 591 692 793 912

Merchandise Inventory 1,901 1,904 2,934 4,523 5,456 6,577 7,699 8,820 10,139

Other Current Assets 4,034 6,230 402 560 719 877 1,035 1,194 1,352

Current Assets 7,969 9,916 5,416 7,449 10,823 15,370 21,949 30,242 41,017

NET PPE 1,592 2,166 4,146 6,006 7,557 9,071 10,330 11,337 12,045

Deferred Tax Assets 67 101 165 220 295 356 417 477 549

Other Noncurrent Assets 235 285 397 3,005 8,320 8,325 11,054 13,925 17,541

Goodwill - - - - 16,054 16,054 16,054 16,054 16,054

Total Noncurrent Assets 1,894 2,552 4,708 9,231 32,226 33,806 37,855 41,793 46,189

Total Assets 9,863 12,468 10,124 16,680 43,049 49,176 59,804 72,035 87,206

LIABILITIES AND SHAREHOLDER EQUITY

Short-Term Borrowing 4,241 6,114 2,092 - - 100 1,221 1,527 1,552

Accounts Payable 3,252 3,793 5,109 6,421 9,144 11,879 14,938 18,392 22,766

Other Current Liabilities 1,015 960 328 208 588 696 1,927 3,468 5,039

Total Current Liabilities 8,508 10,867 7,529 6,629 9,732 12,674 18,086 23,387 29,357

Noncurrent Accrued Rent 218 318 508 663 663 663 663 663 663

5-year bonds - - - - 4,000 4,000 4,000 4,000 4,000

7-year bonds - - - - 1,000 1,000 1,000 1,000 1,000

Retirement Benefits Liability 3 17 39 76 86 104 122 139 160

Total Noncurrent Liabilities 221 335 547 739 5,749 5,767 5,785 5,802 5,823

Total Liabilities 8,729 11,202 8,076 7,368 15,481 18,441 23,871 29,189 35,180

Capital Stock 796 796 1,450 7,169 23,223 23,223 23,223 23,223 23,223

Retained Earnings 338 470 598 2,143 4,345 7,512 12,710 19,623 28,802

Total Equity 1,134 1,266 2,048 9,312 27,568 30,735 35,933 42,846 52,025

Total Liabilities and Equity 9,863 12,468 10,124 16,680 43,049 49,176 59,804 72,035 87,206

5

Appendix 2.3: S&R Balance Sheet

2012E 2013E 2014E 2015E 2016E (in Php 000,000)

ASSETS

Cash and Cash Equivalents 698 2,625 4,098 5,834 7,852

Receivables 122 285 326 367 408

Merchandise Inventory 817 2,153 2,744 3,405 4,137

Other Current Assets 87 228 344 592 1,651

Current Assets 1,724 5,291 7,512 10,198 14,048

NET PPE 558 1,380 1,603 1,792 1,953

Deferred Tax Assets - - - - -

Other Noncurrent Assets 10 23 27 30 33

Goodwill - - - - -

Total Noncurrent Assets 568 1,403 1,630 1,822 1,987

Total Assets 2,291 6,695 9,142 12,020 16,035

LIABILITIES AND SHAREHOLDER EQUITY

Short-Term Borrowing 569 1,281 1,350 1,457 2,063

Accounts Payable 519 1,210 1,383 1,556 1,729

Other Current Liabilities 460 1,486 2,218 3,079 4,296

Total Current Liabilities 1,547 3,977 4,950 6,092 8,087

Noncurrent Accrued Rent - - - - -

5-year bonds (5.4881% p.a.) - - - - -

7-year bonds (5.8673% p.a.) - - - - -

Retirement Benefits Liability 3 6 7 8 9

Total Noncurrent Liabilities 3 6 7 8 9

Total Liabilities 1,550 3,983 4,957 6,100 8,096

Capital Stock 10 20 20 20 20

Retained Earnings 731 2,691 4,165 5,900 7,918

Total Equity 741 2,712 4,185 5,921 7,939

Total Liabilities and Equity 2,291 6,695 9,142 12,020 16,035

Source: Company Data, Team’s Estimates

6

Appendix 3 STATEMENTS OF CASH FLOWS

Appendix 3.1: PGOLD (Consolidated)

Statement of Cash Flows 2009 2010 2011 2012E 2013E 2014E 2015E 2016E

(in Php 000,000)

CASH FLOWS FROM OPERATING ACTIVITIES

Income before Income Tax

189

743

2,205

4,604

7,642

10,553

14,115

18,722

Adjustments for:

Depreciation and amortization 297 279 457 1,305 1,682 1,977 2,264 2,590

Interest Expense 290 220 65 68 325 328 332 355

Accrued rent 100 190 155 - - - - -

Retirement benefits cost 15 22 37 10 19 19 19 22

Loss on pretermination of lease contract - - 9 - - - - -

Impairment losses on receivables (5) (11) (0) - - - - -

Unrealized valuation gain in trading

securities 0 2 1 - - - - -

Loss (gain) on disposal of property and

equipment (13) 3 (0) - - - - -

Dividend Income (1) (1) (1) - - - - -

Interest Income (2) (2) (25) (46) (92) (108) (123) (138)

Loss on sale of investments in trading

securities 1 - - - - - - -

Gain on insurance claim - - (27) - - - - -

Loss on goodwill written-off - 33 - - - - - -

Operating Income before changes in

working capital 870 1,478 2,876 5,941 9,576

12,769 16,606 21,550

(Increase)decrease in:

Investments in trading securities (8) (0) (0) (2) (3) (3) (3) (3)

Receivables 164 285 (200) (101) (142) (142) (142) (159)

Merchandise invetory (3)

(1,030)

(1,589) (1,158)

(1,641)

(1,512)

(1,583) (1,851)

Due from related parties

(2,10

5)

- - - - - - -

Prepaid expenses and other current

assets

(133) (238) (154) (224) (213) (274) (406) (1,217)

Increase (decrease) in:

Accounts payable and accrued expenses 537 1,225 1,218 2,911 3,051 3,300 3,734 5,153

Trust receipts payable - - 9 - - - - -

Other current liabilities - 31 (10) 380 107 1,232 1,541 1,571

Due to a related party (284) (258) (119) (776) (253) (253) (253) (298)

Cash generated from operations

1,143 1,493 2,032 1,031 906 2,347 2,888 3,195

Interest received 2 2 25 - - - - -

Interest paid (290) (230) (68) (46) (277) (277) (277) (277)

Income taxes paid (46) (163) (631) (1,268)

(1,835)

(2,666) (3,641) (5,151)

Net cash provided by (used in) operating

activities (334) (391) (674) 5,658 8,370

12,173 15,576 19,318

CASH FLOWS FROM INVESTING ACTIVITIES

Additions to property and equipment (870) (2,266) (2,325) (2,239) (3,206) (3,206) (3,206) (3,162)

Decrease (increase) in other noncurrent

assets (45) (130) (2,617) (21,444) (66) (2,789) (2,932) (3,687)

Decrease (increase) in due from related

parties

(2,105

) 6,004 - - - - - -

Decrease (increase) in due to related

parties 229 - - - - - - -

Investment in subsidiary - - - - - - - -

Dividends received 1 1 1 46 92 108 123 138

Proceeds from sale of investments in 7 - - - - - - -

7

Statement of Cash Flows 2009 2010 2011 2012E 2013E 2014E 2015E 2016E

(in Php 000,000)

trading securities

Proceeds from insurance claim 9 - 57 - - - - -

Proceeds from disposal of property and

equipment 4 7 17 - - - - -

Net cash provided by (used in) investing

activities

(2,770

) 3,617 (4,867) (23,636) (3,180) (5,888) (6,015) (6,710)

CASH FLOWS FROM FINANCING ACTIVITIES

Proceeds from (payments of ) loans

payable

1,873 (4,022) (2,092) 4,978 51 1,070 251 (54)

Cash Dividend Paid - (383) - (452) (845) (683) (1,164) (1,356)

Proceeds from issuance and subscriptions

of capital stock - 388 5,719 16,054 - - - -

Net cash provided by (used in) financing

activities

1,873 (4,017) 3,626 20,580 (794) 387 (913) (1,410)

NET INCREASE (DECREASE) IN

CASH AND CASH EQUIVALENTS (89) 702 117 2,603 4,396 6,672 8,648 11,198

CASH AND CASH EQUIVALENTS

AT BEGINNING OF YEAR

1,225 1,136 1,838 2,253 5,554 9,949 16,621 25,269

CASH AND CASH EQUIVALENTS

AT END OF YEAR

1,136 1,838 1,955 4,855 9,949

16,621 25,269 36,467

Appendix 3.2: Consolidated: Puregold Price Club, Inc.; Puregold Jr.; Puregold Extra

Statement of Cash Flows 2009 2010 2011 2012E 2013E 2014E 2015E 2016E

(in Php 000,000)

CASH FLOWS FROM OPERATING ACTIVITIES

Income before Income Tax 189 743 2,205 3,936 5,935 8,500 11,690 15,917

Adjustments for: