Embed Size (px)

Citation preview

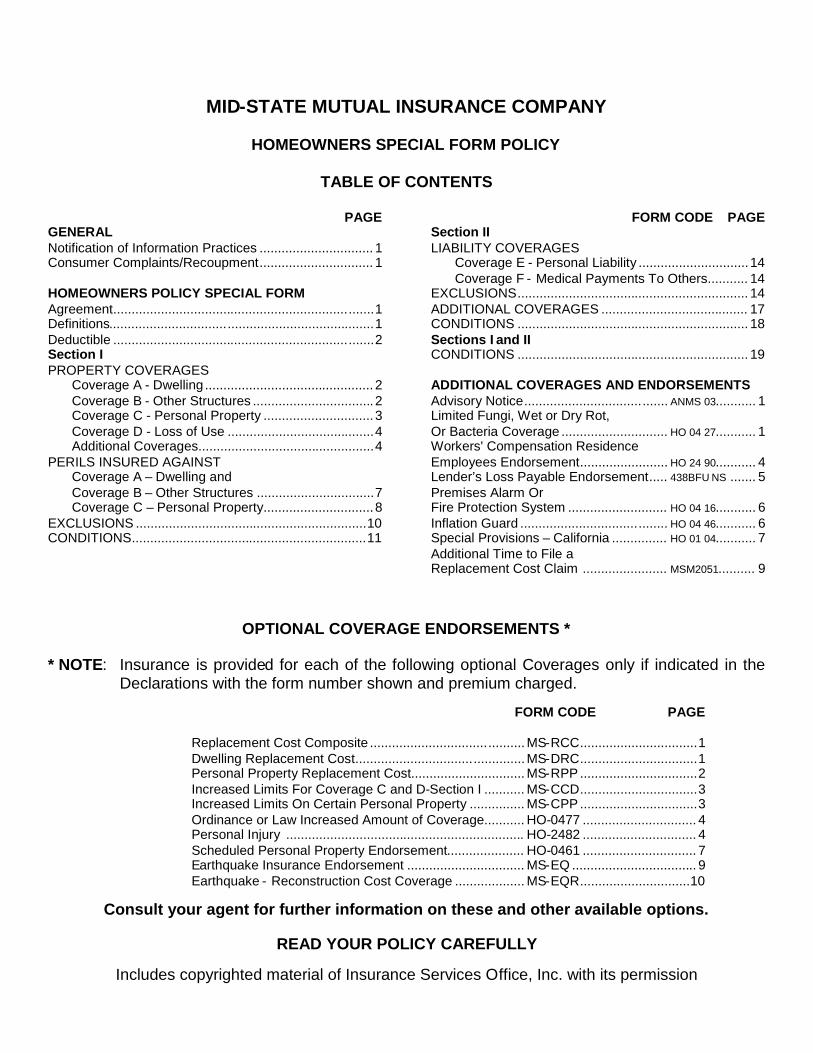

MID-STATE MUTUAL INSURANCE COMPANY

HOMEOWNERS SPECIAL FORM POLICY

TABLE OF CONTENTS

PAGEGENERALNotification of Information Practices ............................... 1Consumer Complaints/Recoupment............................... 1

HOMEOWNERS POLICY SPECIAL FORMAgreement.......................................................................1Definitions........................................................................1Deductible .......................................................................2Section IPROPERTY COVERAGES

Coverage A - Dwelling .............................................. 2Coverage B - Other Structures .................................2Coverage C - Personal Property ..............................3Coverage D - Loss of Use ........................................4Additional Coverages................................................4

PERILS INSURED AGAINSTCoverage A – Dwelling andCoverage B – Other Structures ................................7Coverage C – Personal Property..............................8

EXCLUSIONS ...............................................................10CONDITIONS................................................................11

FORM CODE PAGESection IILIABILITY COVERAGES

Coverage E - Personal Liability ..............................14Coverage F - Medical Payments To Others........... 14

EXCLUSIONS............................................................... 14ADDITIONAL COVERAGES ........................................ 17CONDITIONS ............................................................... 18Sections I and IICONDITIONS ............................................................... 19

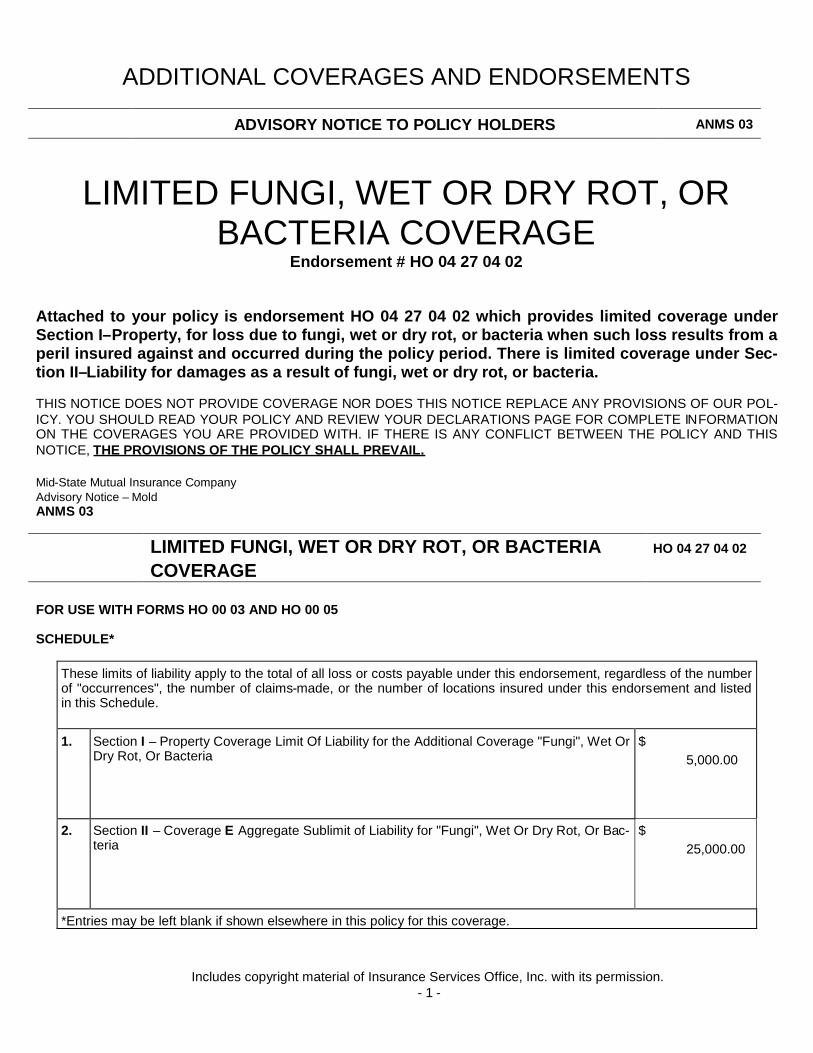

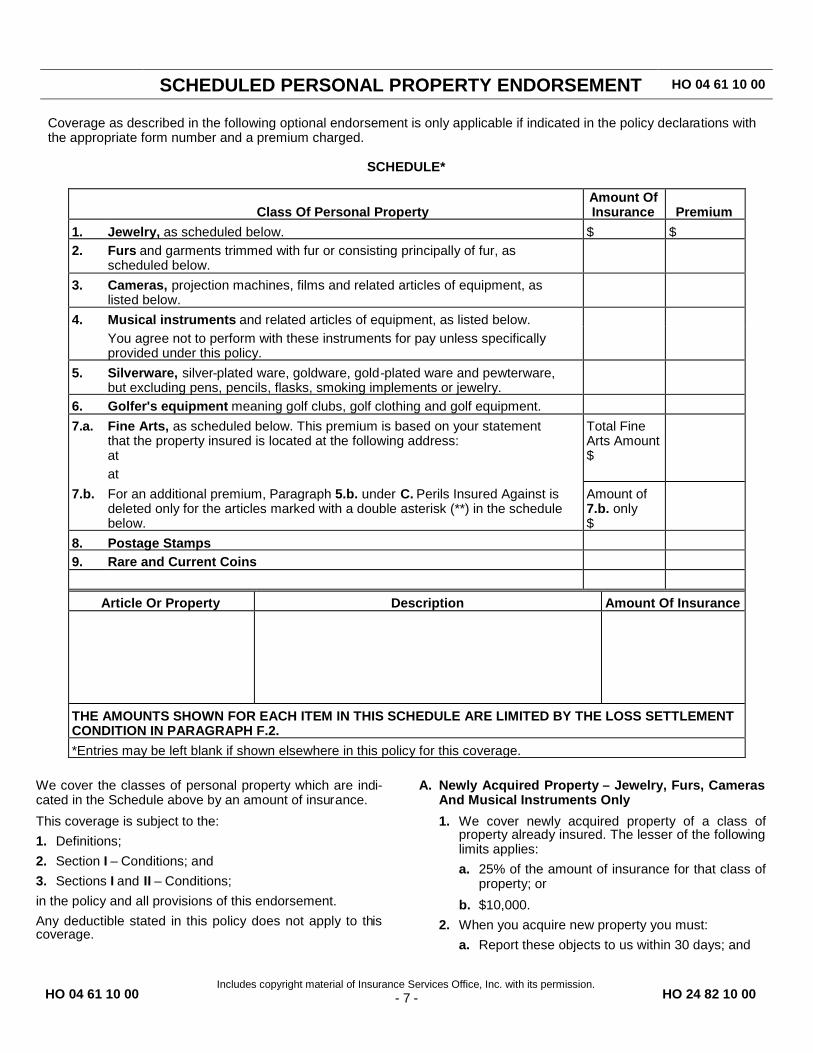

ADDITIONAL COVERAGES AND ENDORSEMENTSAdvisory Notice....................................... ANMS 03........... 1Limited Fungi, Wet or Dry Rot,Or Bacteria Coverage ............................. HO 04 27........... 1Workers' Compensation ResidenceEmployees Endorsement........................ HO 24 90........... 4Lender’s Loss Payable Endorsement..... 438BFU NS ....... 5Premises Alarm OrFire Protection System ........................... HO 04 16........... 6Inflation Guard ........................................ HO 04 46........... 6Special Provisions – California ............... HO 01 04........... 7Additional Time to File aReplacement Cost Claim ....................... MSM2051.......... 9

OPTIONAL COVERAGE ENDORSEMENTS *

* NOTE: Insurance is provided for each of the following optional Coverages only if indicated in theDeclarations with the form number shown and premium charged.

FORM CODE PAGE

Replacement Cost Composite .......................................... MS-RCC................................1Dwelling Replacement Cost..............................................MS-DRC................................1Personal Property Replacement Cost............................... MS-RPP ................................2Increased Limits For Coverage C and D-Section I ........... MS-CCD................................3Increased Limits On Certain Personal Property ............... MS-CPP ................................3Ordinance or Law Increased Amount of Coverage........... HO-0477 ............................... 4Personal Injury ................................................................. HO-2482 ............................... 4Scheduled Personal Property Endorsement..................... HO-0461 ............................... 7Earthquake Insurance Endorsement ................................ MS-EQ .................................. 9Earthquake - Reconstruction Cost Coverage ................... MS-EQR..............................10

Consult your agent for further information on these and other available options.

READ YOUR POLICY CAREFULLY

Includes copyrighted material of Insurance Services Office, Inc. with its permission

- 1 -Amended MSM 0406

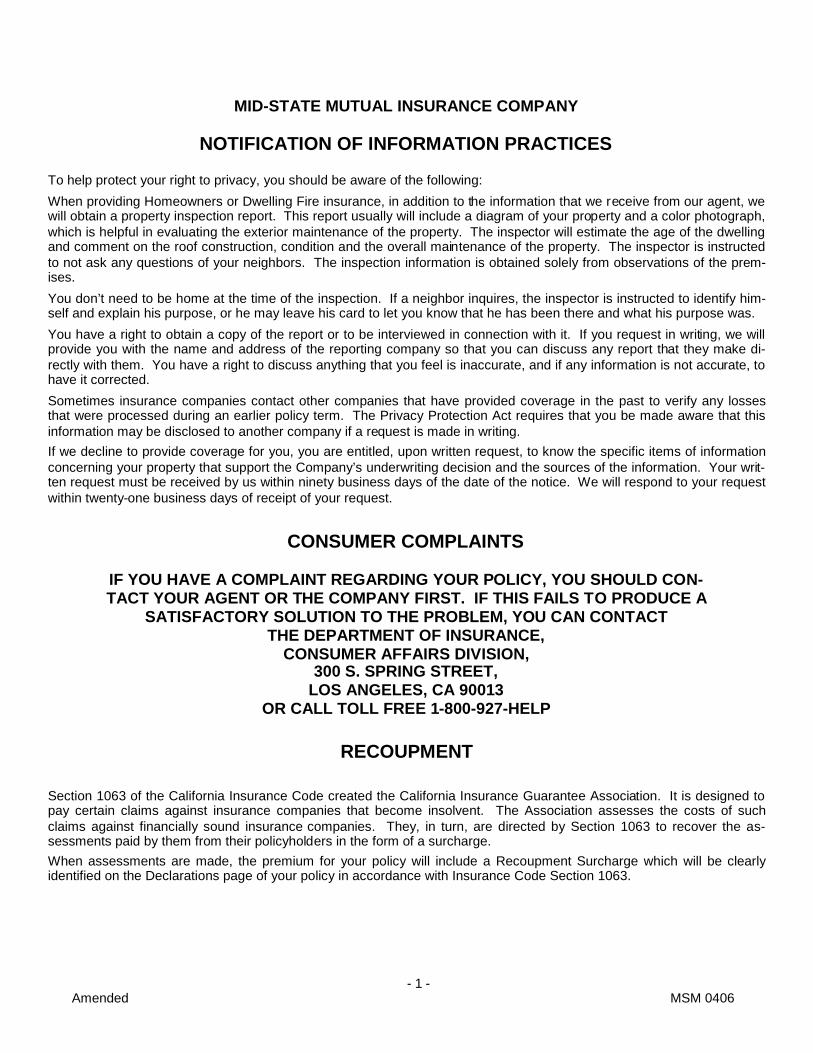

MID-STATE MUTUAL INSURANCE COMPANY

NOTIFICATION OF INFORMATION PRACTICES

To help protect your right to privacy, you should be aware of the following:

When providing Homeowners or Dwelling Fire insurance, in addition to the information that we receive from our agent, wewill obtain a property inspection report. This report usually will include a diagram of your property and a color photograph,which is helpful in evaluating the exterior maintenance of the property. The inspector will estimate the age of the dwellingand comment on the roof construction, condition and the overall maintenance of the property. The inspector is instructedto not ask any questions of your neighbors. The inspection information is obtained solely from observations of the prem-ises.

You don’t need to be home at the time of the inspection. If a neighbor inquires, the inspector is instructed to identify him-self and explain his purpose, or he may leave his card to let you know that he has been there and what his purpose was.

You have a right to obtain a copy of the report or to be interviewed in connection with it. If you request in writing, we willprovide you with the name and address of the reporting company so that you can discuss any report that they make di-rectly with them. You have a right to discuss anything that you feel is inaccurate, and if any information is not accurate, tohave it corrected.

Sometimes insurance companies contact other companies that have provided coverage in the past to verify any lossesthat were processed during an earlier policy term. The Privacy Protection Act requires that you be made aware that thisinformation may be disclosed to another company if a request is made in writing.If we decline to provide coverage for you, you are entitled, upon written request, to know the specific items of informationconcerning your property that support the Company’s underwriting decision and the sources of the information. Your writ-ten request must be received by us within ninety business days of the date of the notice. We will respond to your requestwithin twenty-one business days of receipt of your request.

CONSUMER COMPLAINTS

IF YOU HAVE A COMPLAINT REGARDING YOUR POLICY, YOU SHOULD CON-TACT YOUR AGENT OR THE COMPANY FIRST. IF THIS FAILS TO PRODUCE A

SATISFACTORY SOLUTION TO THE PROBLEM, YOU CAN CONTACTTHE DEPARTMENT OF INSURANCE,

CONSUMER AFFAIRS DIVISION,300 S. SPRING STREET,

LOS ANGELES, CA 90013OR CALL TOLL FREE 1-800-927-HELP

RECOUPMENT

Section 1063 of the California Insurance Code created the California Insurance Guarantee Association. It is designed topay certain claims against insurance companies that become insolvent. The Association assesses the costs of suchclaims against financially sound insurance companies. They, in turn, are directed by Section 1063 to recover the as-sessments paid by them from their policyholders in the form of a surcharge.When assessments are made, the premium for your policy will include a Recoupment Surcharge which will be clearlyidentified on the Declarations page of your policy in accordance with Insurance Code Section 1063.

HomeownersPolicy

Special Form

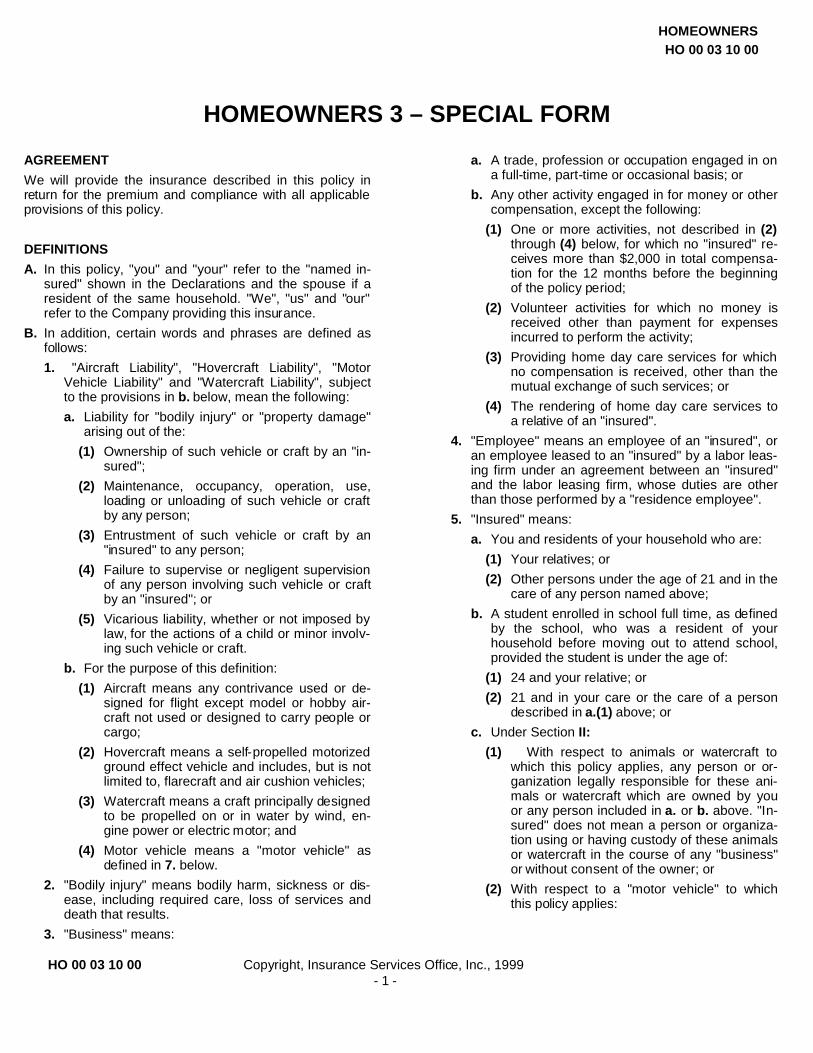

HOMEOWNERSHO 00 03 10 00

HO 00 03 10 00 Copyright, Insurance Services Office, Inc., 1999- 1 -

HOMEOWNERS 3 – SPECIAL FORM

AGREEMENTWe will provide the insurance described in this policy inreturn for the premium and compliance with all applicableprovisions of this policy.

DEFINITIONSA. In this policy, "you" and "your" refer to the "named in-

sured" shown in the Declarations and the spouse if aresident of the same household. "We", "us" and "our"refer to the Company providing this insurance.

B. In addition, certain words and phrases are defined asfollows:1. "Aircraft Liability", "Hovercraft Liability", "Motor

Vehicle Liability" and "Watercraft Liability", subjectto the provisions in b. below, mean the following:a. Liability for "bodily injury" or "property damage"

arising out of the:(1) Ownership of such vehicle or craft by an "in-

sured";(2) Maintenance, occupancy, operation, use,

loading or unloading of such vehicle or craftby any person;

(3) Entrustment of such vehicle or craft by an"insured" to any person;

(4) Failure to supervise or negligent supervisionof any person involving such vehicle or craftby an "insured"; or

(5) Vicarious liability, whether or not imposed bylaw, for the actions of a child or minor involv-ing such vehicle or craft.

b. For the purpose of this definition:(1) Aircraft means any contrivance used or de-

signed for flight except model or hobby air-craft not used or designed to carry people orcargo;

(2) Hovercraft means a self-propelled motorizedground effect vehicle and includes, but is notlimited to, flarecraft and air cushion vehicles;

(3) Watercraft means a craft principally designedto be propelled on or in water by wind, en-gine power or electric motor; and

(4) Motor vehicle means a "motor vehicle" asdefined in 7. below.

2. "Bodily injury" means bodily harm, sickness or dis-ease, including required care, loss of services anddeath that results.

3. "Business" means:

a. A trade, profession or occupation engaged in ona full-time, part-time or occasional basis; or

b. Any other activity engaged in for money or othercompensation, except the following:

(1) One or more activities, not described in (2)through (4) below, for which no "insured" re-ceives more than $2,000 in total compensa-tion for the 12 months before the beginningof the policy period;

(2) Volunteer activities for which no money isreceived other than payment for expensesincurred to perform the activity;

(3) Providing home day care services for whichno compensation is received, other than themutual exchange of such services; or

(4) The rendering of home day care services toa relative of an "insured".

4. "Employee" means an employee of an "insured", oran employee leased to an "insured" by a labor leas-ing firm under an agreement between an "insured"and the labor leasing firm, whose duties are otherthan those performed by a "residence employee".

5. "Insured" means:a. You and residents of your household who are:

(1) Your relatives; or(2) Other persons under the age of 21 and in the

care of any person named above;b. A student enrolled in school full time, as defined

by the school, who was a resident of yourhousehold before moving out to attend school,provided the student is under the age of:

(1) 24 and your relative; or(2) 21 and in your care or the care of a person

described in a.(1) above; orc. Under Section II:

(1) With respect to animals or watercraft towhich this policy applies, any person or or-ganization legally responsible for these ani-mals or watercraft which are owned by youor any person included in a. or b. above. "In-sured" does not mean a person or organiza-tion using or having custody of these animalsor watercraft in the course of any "business"or without consent of the owner; or

(2) With respect to a "motor vehicle" to whichthis policy applies:

HOMEOWNERSHO 00 03 10 00

HO 00 03 10 00 Copyright, Insurance Services Office, Inc., 1999- 2 -

(a) Persons while engaged in your employ orthat of any person included in a. or b.above; or

(b) Other persons using the vehicle on an"insured location" with your consent.

Under both Sections I and II, when the word an im-mediately precedes the word "insured", the wordsan "insured" together mean one or more "insureds".

6. "Insured location" means:a. The "residence premises";b. The part of other premises, other structures and

grounds used by you as a residence; and(1) Which is shown in the Declarations; or(2) Which is acquired by you during the policy

period for your use as a residence;c. Any premises used by you in connection with a

premises described in a. and b. above;d. Any part of a premises:

(1) Not owned by an "insured"; and(2) Where an "insured" is temporarily residing;

e. Vacant land, other than farm land, owned by orrented to an "insured";

f. Land owned by or rented to an "insured" onwhich a one, two, three or four family dwelling isbeing built as a residence for an "insured";

g. Individual or family cemetery plots or burialvaults of an "insured"; or

h. Any part of a premises occasionally rented to an"insured" for other than "business" use.

7. "Motor vehicle" means:a. A self-propelled land or amphibious vehicle; orb. Any trailer or semitrailer which is being carried

on, towed by or hitched for towing by a vehicledescribed in a. above.

8. "Occurrence" means an accident, including con-tinuous or repeated exposure to substantially thesame general harmful conditions, which results,during the policy period, in:a. "Bodily injury"; orb. "Property damage".

9. "Property damage" means physical injury to, de-struction of, or loss of use of tangible property.

10. "Residence employee" means:a. An employee of an "insured", or an em-

ployee leased to an "insured" by a laborleasing firm, under an agreement betweenan "insured" and the labor leasing firm,whose duties are related to the maintenanceor use of the "residence premises", includinghousehold or domestic services; or

b. one who performs similar duties elsewherenot related to the "business" of an "insured".

A "residence employee" does not include a tempo-rary employee who is furnished to an "insured" tosubstitute for a permanent "residence employee" onleave or to meet seasonal or short-term workloadconditions.

11. "Residence premises" means:a. The one family dwelling where you reside;b. The two, three or four family dwelling where you

reside in at least one of the family units; orc. That part of any other building where you reside;and which is shown as the "residence premises" inthe Declarations."Residence premises" also includes other structuresand grounds at that location.

DEDUCTIBLEUnless otherwise noted in this policy, the following de-ductible provision applies:Subject to the policy limits that apply, we will pay only thatpart of the total of all loss payable under Section I that ex-ceeds the deductible amount shown in the Declarations.

SECTION I – PROPERTY COVERAGESA. Coverage A – Dwelling

1. We cover:a. The dwelling on the "residence premises" shown

in the Declarations, including structures attachedto the dwelling; and

b. Materials and supplies located on or next to the"residence premises" used to construct, alter orrepair the dwelling or other structures on the"residence premises".

2. We do not cover land, including land on which thedwelling is located.

B. Coverage B – Other Structures1. We cover other structures on the "residence prem-

ises" set apart from the dwelling by clear space.This includes structures connected to the dwellingby only a fence, utility line, or similar connection.

2. We do not cover:a. Land, including land on which the other struc-

tures are located;b. Other structures rented or held for rental to any

person not a tenant of the dwelling, unless usedsolely as a private garage;

c. Other structures from which any "business" isconducted; or

HOMEOWNERSHO 00 03 10 00

HO 00 03 10 00 Copyright, Insurance Services Office, Inc., 1999- 3 -

d. Other structures used to store "business" prop-erty. However, we do cover a structure that con-tains "business" property solely owned by an"insured" or a tenant of the dwelling providedthat "business" property does not include gase-ous or liquid fuel, other than fuel in a perma-nently installed fuel tank of a vehicle or craftparked or stored in the structure.

3. The limit of liability for this coverage will not bemore than 10% of the limit of liability that applies toCoverage A. Use of this coverage does not reducethe Coverage A limit of liability.

C. Coverage C – Personal Property1. Covered Property

We cover personal property owned or used by an"insured" while it is anywhere in the world. After aloss and at your request, we will cover personalproperty owned by:a. Others while the property is on the part of the

"residence premises" occupied by an "insured";or

b. A guest or a "residence employee", while theproperty is in any residence occupied by an "in-sured".

2. Limit For Property At Other ResidencesOur limit of liability for personal property usually lo-cated at an "insured's" residence, other than the"residence premises", is 10% of the limit of liabilityfor Coverage C, or $1,000, whichever is greater.However, this limitation does not apply to personalproperty:a. Moved from the "residence premises" because it

is being repaired, renovated or rebuilt and is notfit to live in or store property in; or

b. In a newly acquired principal residence for 30days from the time you begin to move the prop-erty there.

3. Special Limits Of LiabilityThe special limit for each category shown below is

the total limit for each loss for all property in thatcategory. These special limits do not increase theCoverage C limit of liability.a. $200 on money, bank notes, bullion, gold other

than goldware, silver other than silverware, plati-num other than platinumware, coins, medals,scrip, stored value cards and smart cards.

b. $1,500 on securities, accounts, deeds, evi-dences of debt, letters of credit, notes other thanbank notes, manuscripts, personal records,passports, tickets and stamps. This dollar limitapplies to these categories regardless of themedium (such as paper or computer software)on which the material exists.This limit includes the cost to research, replaceor restore the information from the lost or dam-aged material.

c. $1,500 on watercraft of all types, including theirtrailers, furnishings, equipment and outboardengines or motors.

d. $1,500 on trailers or semitrailers not used withwatercraft of all types.

e. $1,500 for loss by theft of jewelry, watches, furs,precious and semiprecious stones.

f. $2,500 for loss by theft of firearms and relatedequipment.

g. $2,500 for loss by theft of silverware, silver-plated ware, goldware, gold-plated ware, plati-numware, platinum-plated ware and pewter-ware. This includes flatware, hollowware, teasets, trays and trophies made of or including sil-ver, gold or pewter.

h. $2,500 on property, on the "residence prem-ises", used primarily for "business" purposes.

i. $500 on property, away from the "residencepremises", used primarily for "business" pur-poses. However, this limit does not apply to lossto electronic apparatus and other property de-scribed in Categories j. and k. below.

j. $1,500 on electronic apparatus and accessories,while in or upon a "motor vehicle", but only if theapparatus is equipped to be operated by powerfrom the "motor vehicle's" electrical system whilestill capable of being operated by other powersources.Accessories include antennas, tapes, wires, re-cords, discs or other media that can be usedwith any apparatus described in this Category j.

k. $1,500 on electronic apparatus and ac-cessories used primarily for "business" whileaway from the "residence premises" and not inor upon a "motor vehicle". The apparatus mustbe equipped to be operated by power from the"motor vehicle's" electrical system while still ca-pable of being operated by other power sources.Accessories include antennas, tapes, wires, re-cords, discs or other media that can be usedwith any apparatus described in this Category k.

4. Property Not CoveredWe do not cover:a. Articles separately described and specifically

insured, regardless of the limit for which they areinsured, in this or other insurance;

b. Animals, birds or fish;c. "Motor vehicles".

(1) This includes:(a) Their accessories, equipment and parts;

or

HOMEOWNERSHO 00 03 10 00

HO 00 03 10 00 Copyright, Insurance Services Office, Inc., 1999- 4 -

(b) Electronic apparatus and accessoriesdesigned to be operated solely by powerfrom the electrical system of the "motorvehicle". Accessories include antennas,tapes, wires, records, discs or other me-dia that can be used with any apparatusdescribed above.

The exclusion of property described in (a)and (b) above applies only while such prop-erty is in or upon the "motor vehicle".

(2) We do cover "motor vehicles" not required tobe registered for use on public roads or prop-erty which are:

(a) Used solely to service an "insured's" resi-dence; or

(b) Designed to assist the handicapped;d. Aircraft meaning any contrivance used or de-

signed for flight including any parts whether ornot attached to the aircraft.We do cover model or hobby aircraft not used ordesigned to carry people or cargo;

e. Hovercraft and parts. Hovercraft means a self-propelled motorized ground effect vehicle andincludes, but is not limited to, flarecraft and aircushion vehicles;

f. Property of roomers, boarders and other ten-ants, except property of roomers and boardersrelated to an "insured";

g. Property in an apartment regularly rented or heldfor rental to others by an "insured", except asprovided in E.10. Landlord's Furnishings underSection I – Property Coverages;

h. Property rented or held for rental to others offthe "residence premises";

i. "Business" data, including such data stored in:(1) Books of account, drawings or other paper

records; or(2) Computers and related equipment.We do cover the cost of blank recording or stor-age media, and of prerecorded computer pro-grams available on the retail market;

j. Credit cards, electronic fund transfer cards oraccess devices used solely for deposit, with-drawal or transfer of funds except as provided inE.6. Credit Card, Electronic Fund Transfer CardOr Access Device, Forgery And CounterfeitMoney under Section I – Property Coverages; or

k. Water or steam.D. Coverage D – Loss Of Use

The limit of liability for Coverage D is the total limit forthe coverages in 1. Additional Living Expense, 2. FairRental Value and 3. Civil Authority Prohibits Use below.

1. Additional Living ExpenseIf a loss covered under Section I makes that part

of the "residence premises" where you reside not fitto live in, we cover any necessary increase in livingexpenses incurred by you so that your householdcan maintain its normal standard of living.

Payment will be for the shortest time required torepair or replace the damage or, if you permanentlyrelocate, the shortest time required for your house-hold to settle elsewhere.

2. Fair Rental ValueIf a loss covered under Section I makes that part

of the "residence premises" rented to others or heldfor rental by you not fit to live in, we cover the fairrental value of such premises less any expensesthat do not continue while it is not fit to live in.Payment will be for the shortest time required to re-pair or replace such premises.

3. Civil Authority Prohibits UseIf a civil authority prohibits you from use of the "resi-dence premises" as a result of direct damage toneighboring premises by a Peril Insured Against, wecover the loss as provided in 1. Additional LivingExpense and 2. Fair Rental Value above for nomore than two weeks.

4. Loss Or Expense Not CoveredWe do not cover loss or expense due to cancella-tion of a lease or agreement.

The periods of time under 1. Additional Living Expense,2. Fair Rental Value and 3. Civil Authority Prohibits Useabove are not limited by expiration of this policy.

E. Additional Coverages1. Debris Removal

a. We will pay your reasonable expense for theremoval of:

(1) Debris of covered property if a Peril InsuredAgainst that applies to the damaged propertycauses the loss; or

(2) Ash, dust or particles from a volcanic erup-tion that has caused direct loss to a buildingor property contained in a building.

This expense is included in the limit of liabilitythat applies to the damaged property. If theamount to be paid for the actual damage to theproperty plus the debris removal expense ismore than the limit of liability for the damagedproperty, an additional 5% of that limit is avail-able for such expense.

b. We will also pay your reasonable expense, up to$1,000, for the removal from the "residencepremises" of:

(1) Your tree(s) felled by the peril of Windstormor Hail or Weight of Ice, Snow or Sleet; or

HOMEOWNERSHO 00 03 10 00

HO 00 03 10 00 Copyright, Insurance Services Office, Inc., 1999- 5 -

(2) A neighbor's tree(s) felled by a Peril InsuredAgainst under Coverage C;

provided the tree(s):(3) Damage(s) a covered structure; or(4) Does not damage a covered structure,

but:(a) Block(s) a driveway on the "residence

premises" which prevent(s) a "motor ve-hicle", that is registered for use on publicroads or property, from entering or leav-ing the "residence premises"; or

(b) Block(s) a ramp or other fixture designedto assist a handicapped person to enteror leave the dwelling building.

The $1,000 limit is the most we will pay in anyone loss regardless of the number of fallentrees. No more than $500 of this limit will bepaid for the removal of any one tree.This coverage is additional insurance.

2. Reasonable Repairsa. We will pay the reasonable cost incurred by you

for the necessary measures taken solely to pro-tect covered property that is damaged by a PerilInsured Against from further damage.

b. If the measures taken involve repair to otherdamaged property, we will only pay if that prop-erty is covered under this policy and the damageis caused by a Peril Insured Against. This cov-erage does not:

(1) Increase the limit of liability that applies tothe covered property; or

(2) Relieve you of your duties, in case of a lossto covered property, described in B.4. underSection I – Conditions.

3. Trees, Shrubs And Other PlantsWe cover trees, shrubs, plants or lawns, on the"residence premises", for loss caused by the follow-ing Perils Insured Against:a. Fire or Lightning;b. Explosion;c. Riot or Civil Commotion;d. Aircraft;e. Vehicles not owned or operated by a resi-

dent of the "residence premises";f. Vandalism or Malicious Mischief; org. Theft.We will pay up to 5% of the limit of liability that ap-plies to the dwelling for all trees, shrubs, plants orlawns. No more than $500 of this limit will be paidfor any one tree, shrub or plant. We do not coverproperty grown for "business" purposes.This coverage is additional insurance.

4. Fire Department Service ChargeWe will pay up to $500 for your liability assumed bycontract or agreement for fire department chargesincurred when the fire department is called to saveor protect covered property from a Peril InsuredAgainst. We do not cover fire department servicecharges if the property is located within the limits ofthe city, municipality or protection district furnishingthe fire department response.This coverage is additional insurance. No deducti-ble applies to this coverage.

5. Property RemovedWe insure covered property against direct loss fromany cause while being removed from a premisesendangered by a Peril Insured Against and for nomore than 30 days while removed.This coverage does not change the limit of liabilitythat applies to the property being removed.

6. Credit Card, Electronic Fund Transfer Card OrAccess Device, Forgery And Counterfeit Moneya. We will pay up to $500 for:

(1) The legal obligation of an "insured" to paybecause of the theft or unauthorized use ofcredit cards issued to or registered in an "in-sured's" name;

(2) Loss resulting from theft or unauthorized useof an electronic fund transfer card or accessdevice used for deposit, withdrawal or trans-fer of funds, issued to or registered in an "in-sured's" name;

(3) Loss to an "insured" caused by forgery oralteration of any check or negotiable instru-ment; and

(4) Loss to an "insured" through acceptance ingood faith of counterfeit United States or Ca-nadian paper currency.

All loss resulting from a series of acts committedby any one person or in which any one person isconcerned or implicated is considered to be oneloss.This coverage is additional insurance. No de-ductible applies to this coverage.

b. We do not cover:(1) Use of a credit card, electronic fund transfer

card or access device:(a) By a resident of your household;(b) By a person who has been entrusted with

either type of card or access device; or(c) If an "insured" has not complied with all

terms and conditions under which thecards are issued or the devices ac-cessed; or

(2) Loss arising out of "business" use or dishon-esty of an "insured".

HOMEOWNERSHO 00 03 10 00

HO 00 03 10 00 Copyright, Insurance Services Office, Inc., 1999- 6 -

c. If the coverage in a. above applies, the followingdefense provisions also apply:

(1) We may investigate and settle any claim orsuit that we decide is appropriate. Our dutyto defend a claim or suit ends when theamount we pay for the loss equals our limit ofliability.

(2) If a suit is brought against an "insured" forliability under a.(1) or (2) above, we will pro-vide a defense at our expense by counsel ofour choice.

(3) We have the option to defend at our expensean "insured" or an "insured's" bank againstany suit for the enforcement of payment un-der a.(3) above.

7. Loss Assessmenta. We will pay up to $1,000 for your share of loss

assessment charged during the policy periodagainst you, as owner or tenant of the "resi-dence premises", by a corporation or associationof property owners. The assessment must bemade as a result of direct loss to property,owned by all members collectively, of the typethat would be covered by this policy if owned byyou, caused by a Peril Insured Against underCoverage A, other than:

(1) Earthquake; or(2) Land shock waves or tremors before, during

or after a volcanic eruption.The limit of $1,000 is the most we will pay withrespect to any one loss, regardless of the num-ber of assessments. We will only apply one de-ductible, per unit, to the total amount of any oneloss to the property described above, regardlessof the number of assessments.

b. We do not cover assessments charged againstyou or a corporation or association of propertyowners by any governmental body.

c. Paragraph P. Policy Period under SectionI – Conditions does not apply to this coverage.

This coverage is additional insurance.8. Collapse

a. With respect to this Additional Coverage:(1) Collapse means an abrupt falling down or

caving in of a building or any part of a build-ing with the result that the building or part ofthe building cannot be occupied for its cur-rent intended purpose.

(2) A building or any part of a building that is indanger of falling down or caving in is not con-sidered to be in a state of collapse.

(3) A part of a building that is standing is notconsidered to be in a state of collapse even ifit has separated from another part of thebuilding.

(4) A building or any part of a building that isstanding is not considered to be in a state ofcollapse even if it shows evidence of crack-ing, bulging, sagging, bending, leaning, set-tling, shrinkage or expansion.

b. We insure for direct physical loss to coveredproperty involving collapse of a building or anypart of a building if the collapse was caused byone or more of the following:

(1) The Perils Insured Against named underCoverage C;

(2) Decay that is hidden from view, unless thepresence of such decay is known to an "in-sured" prior to collapse;

(3) Insect or vermin damage that is hidden fromview, unless the presence of such damage isknown to an "insured" prior to collapse;

(4) Weight of contents, equipment, animals orpeople;

(5) Weight of rain which collects on a roof; or(6) Use of defective material or methods in con-

struction, remodeling or renovation if the col-lapse occurs during the course of the con-struction, remodeling or renovation.

c. Loss to an awning, fence, patio, deck, pave-ment, swimming pool, underground pipe, flue,drain, cesspool, septic tank, foundation, retain-ing wall, bulkhead, pier, wharf or dock is not in-cluded under b.(2) through (6) above, unless theloss is a direct result of the collapse of a buildingor any part of a building.

d. This coverage does not increase the limit of li-ability that applies to the damaged coveredproperty.

9. Glass Or Safety Glazing Materiala. We cover:

(1) The breakage of glass or safety glazing ma-terial which is part of a covered building,storm door or storm window;

(2) The breakage of glass or safety glazing ma-terial which is part of a covered building,storm door or storm window when caused di-rectly by earth movement; and

(3) The direct physical loss to covered propertycaused solely by the pieces, fragments orsplinters of broken glass or safety glazingmaterial which is part of a building, stormdoor or storm window.

b. This coverage does not include loss:(1) To covered property which results because

the glass or safety glazing material has beenbroken, except as provided in a.(3) above; or

HOMEOWNERSHO 00 03 10 00

HO 00 03 10 00 Copyright, Insurance Services Office, Inc., 1999- 7 -

(2) On the "residence premises" if the dwellinghas been vacant for more than 60 consecu-tive days immediately before the loss, exceptwhen the breakage results directly from earthmovement as provided in a.(2) above. Adwelling being constructed is not consideredvacant.

c. This coverage does not increase the limit of li-ability that applies to the damaged property.

10. Landlord's FurnishingsWe will pay up to $2,500 for your appliances, car-peting and other household furnishings, in eachapartment on the "residence premises" regularlyrented or held for rental to others by an "insured",for loss caused by a Peril Insured Against in Cover-age C, other than Theft.This limit is the most we will pay in any one loss re-gardless of the number of appliances, carpeting orother household furnishings involved in the loss.

This coverage does not increase the limit of liabil-ity applying to the damaged property.

11. Ordinance Or Lawa. You may use up to 10% of the limit of liability

that applies to Coverage A for the increasedcosts you incur due to the enforcement of anyordinance or law which requires or regulates:

(1) The construction, demolition, remodeling,renovation or repair of that part of a coveredbuilding or other structure damaged by aPeril Insured Against;

(2) The demolition and reconstruction of the un-damaged part of a covered building or otherstructure, when that building or other struc-ture must be totally demolished because ofdamage by a Peril Insured Against to anotherpart of that covered building or other struc-ture; or

(3) The remodeling, removal or replacement ofthe portion of the undamaged part of a cov-ered building or other structure necessary tocomplete the remodeling, repair or replace-ment of that part of the covered building orother structure damaged by a Peril InsuredAgainst.

b. You may use all or part of this ordinance or lawcoverage to pay for the increased costs you in-cur to remove debris resulting from the construc-tion, demolition, remodeling, renovation, repairor replacement of property as stated in a. above.

c. We do not cover:(1) The loss in value to any covered building or

other structure due to the requirements ofany ordinance or law; or

(2) The costs to comply with any ordinance orlaw which requires any "insured" or others totest for, monitor, clean up, remove, contain,treat, detoxify or neutralize, or in any way re-spond to, or assess the effects of, pollutantsin or on any covered building or other struc-ture.Pollutants means any solid, liquid, gaseousor thermal irritant or contaminant, includingsmoke, vapor, soot, fumes, acids, alkalis,chemicals and waste. Waste includes mate-rials to be recycled, reconditioned or re-claimed.

This coverage is additional insurance.12. Grave Markers

We will pay up to $5,000 for grave markers, includ-ing mausoleums, on or away from the "residencepremises" for loss caused by a Peril Insured Againstunder Coverage C.This coverage does not increase the limits of liabilitythat apply to the damaged covered property.

SECTION I – PERILS INSURED AGAINSTA. Coverage A – Dwelling And Coverage B – Other

Structures1. We insure against risk of direct physical loss to

property described in Coverages A and B.2. We do not insure, however, for loss:

a. Excluded under Section I – Exclusions;b. Involving collapse, except as provided in E.8.

Collapse under Section I – Property Coverages;or

c. Caused by:(1) Freezing of a plumbing, heating, air condi-

tioning or automatic fire protective sprinklersystem or of a household appliance, or bydischarge, leakage or overflow from withinthe system or appliance caused by freezing.This provision does not apply if you haveused reasonable care to:

(a) Maintain heat in the building; or(b) Shut off the water supply and drain all

systems and appliances of water.However, if the building is pro-

tected by an automatic fire protective sprin-kler system, you must use reasonable care tocontinue the water supply and maintain heatin the building for coverage to apply.For purposes of this provision a plumbingsystem or household appliance does not in-clude a sump, sump pump or related equip-ment or a roof drain, gutter, downspout orsimilar fixtures or equipment;

HOMEOWNERSHO 00 03 10 00

HO 00 03 10 00 Copyright, Insurance Services Office, Inc., 1999- 8 -

(2) Freezing, thawing, pressure or weight of wa-ter or ice, whether driven by wind or not, to a:

(a) Fence, pavement, patio or swimmingpool;

(b) Footing, foundation, bulkhead, wall, orany other structure or device that sup-ports all or part of a building, or otherstructure;

(c) Retaining wall or bulkhead that does notsupport all or part of a building or otherstructure; or

(d) Pier, wharf or dock;(3) Theft in or to a dwelling under construction,

or of materials and supplies for use in theconstruction until the dwelling is finished andoccupied;

(4) Vandalism and malicious mischief, and anyensuing loss caused by any intentional andwrongful act committed in the course of thevandalism or malicious mischief, if the dwell-ing has been vacant for more than 60 con-secutive days immediately before the loss. Adwelling being constructed is not consideredvacant;

(5) Mold, fungus or wet rot. However, we do in-sure for loss caused by mold, fungus or wetrot that is hidden within the walls or ceilingsor beneath the floors or above the ceilings ofa structure if such loss results from the acci-dental discharge or overflow of water orsteam from within:

(a) A plumbing, heating, air conditioning orautomatic fire protective sprinkler system,or a household appliance, on the "resi-dence premises"; or

(b) A storm drain, or water, steam or sewerpipes, off the "residence premises".

For purposes of this provision, a plumbingsystem or household appliance does not in-clude a sump, sump pump or related equip-ment or a roof drain, gutter, downspout orsimilar fixtures or equipment; or

(6) Any of the following:(a) Wear and tear, marring, deterioration;(b) Mechanical breakdown, latent defect, in-

herent vice, or any quality in property thatcauses it to damage or destroy itself;

(c) Smog, rust or other corrosion, or dry rot;(d) Smoke from agricultural smudging or in-

dustrial operations;

(e) Discharge, dispersal, seepage, migration,release or escape of pollutants unless thedischarge, dispersal, seepage, migration,release or escape is itself caused by aPeril Insured Against named under Cov-erage C.Pollutants means any solid, liquid, gase-ous or thermal irritant or contaminant, in-cluding smoke, vapor, soot, fumes, acids,alkalis, chemicals and waste. Waste in-cludes materials to be recycled, recondi-tioned or reclaimed;

(f) Settling, shrinking, bulging or expansion,including resultant cracking, of bulkheads,pavements, patios, footings, foundations,walls, floors, roofs or ceilings;

(g) Birds, vermin, rodents, or insects; or(h) Animals owned or kept by an "insured".

Exception To c.(6)Unless the loss is otherwise excluded, we coverloss to property covered under Coverage A or Bresulting from an accidental discharge or over-flow of water or steam from within a:(i) Storm drain, or water, steam or sewer pipe,

off the "residence premises"; or(ii) Plumbing, heating, air conditioning or

automatic fire protective sprinkler system orhousehold appliance on the "residence prem-ises". This includes the cost to tear out andreplace any part of a building, or other struc-ture, on the "residence premises", but onlywhen necessary to repair the system or ap-pliance. However, such tear out and re-placement coverage only applies to otherstructures if the water or steam causes ac-tual damage to a building on the "residencepremises".

We do not cover loss to the system or appliancefrom which this water or steam escaped.For purposes of this provision, a plumbing sys-tem or household appliance does not include asump, sump pump or related equipment or aroof drain, gutter, down spout or similar fixturesor equipment.

Section I – Exclusion A.3. Water Damage, Para-graphs a. and c. that apply to surface water and wa-ter below the surface of the ground do not apply toloss by water covered under c.(5) and (6) above.Under 2.b. and c. above, any ensuing loss to prop-erty described in Coverages A and B not precludedby any other provision in this policy is covered.

B. Coverage C – Personal PropertyWe insure for direct physical loss to the property de-scribed in Coverage C caused by any of the followingperils unless the loss is excluded in Section I – Exclu-sions.

HOMEOWNERSHO 00 03 10 00

HO 00 03 10 00 Copyright, Insurance Services Office, Inc., 1999- 9 -

1. Fire Or Lightning2. Windstorm Or Hail

This peril includes loss to watercraft of all typesand their trailers, furnishings, equipment, and out-board engines or motors, only while inside a fullyenclosed building.

This peril does not include loss to the propertycontained in a building caused by rain, snow, sleet,sand or dust unless the direct force of wind or haildamages the building causing an opening in a roofor wall and the rain, snow, sleet, sand or dust en-ters through this opening.

3. Explosion4. Riot Or Civil Commotion5. Aircraft

This peril includes self-propelled missiles andspacecraft.

6. Vehicles7. Smoke

This peril means sudden and accidental damagefrom smoke, including the emission or puffback ofsmoke, soot, fumes or vapors from a boiler, furnaceor related equipment.This peril does not include loss caused by smokefrom agricultural smudging or industrial operations.

8. Vandalism Or Malicious Mischief9. Theft

a. This peril includes attempted theft and loss ofproperty from a known place when it is likely thatthe property has been stolen.

b. This peril does not include loss caused by theft:(1) Committed by an "insured";(2) In or to a dwelling under construction, or of

materials and supplies for use in the con-struction until the dwelling is finished and oc-cupied;

(3) From that part of a "residence premises"rented by an "insured" to someone otherthan another "insured"; or

(4) That occurs off the "residence premises" of:(a) Trailers, semitrailers and campers;(b) Watercraft of all types, and their furnish-

ings, equipment and outboard engines ormotors; or

(c) Property while at any other residenceowned by, rented to, or occupied by an"insured", except while an "insured" istemporarily living there. Property of an"insured" who is a student is coveredwhile at the residence the student occu-pies to attend school as long as the stu-dent has been there at any time duringthe 60 days immediately before the loss.

10. Falling ObjectsThis peril does not include loss to property con-tained in a building unless the roof or an outsidewall of the building is first damaged by a falling ob-ject. Damage to the falling object itself is not in-cluded.

11. Weight Of Ice, Snow Or SleetThis peril means weight of ice, snow or sleet whichcauses damage to property contained in a building.

12. Accidental Discharge Or Overflow Of Water OrSteama. This peril means accidental discharge or over-

flow of water or steam from within a plumbing,heating, air conditioning or automatic fire protec-tive sprinkler system or from within a householdappliance.

b. This peril does not include loss:(1) To the system or appliance from which the

water or steam escaped;(2) Caused by or resulting from freezing except

as provided in Peril Insured Against 14.Freezing;

(3) On the "residence premises" caused by ac-cidental discharge or overflow which occursoff the "residence premises"; or

(4) Caused by mold, fungus or wet rot unlesshidden within the walls or ceilings or beneaththe floors or above the ceilings of a structure.

c. In this peril, a plumbing system or householdappliance does not include a sump, sump pumpor related equipment or a roof drain, gutter,downspout or similar fixtures or equipment.

d. Section I – Exclusion A.3. Water Damage, Para-graphs a. and c. that apply to surface water andwater below the surface of the ground do notapply to loss by water covered under this peril.

13. Sudden And Accidental Tearing Apart,Cracking, Burning Or BulgingThis peril means sudden and accidental tearingapart, cracking, burning or bulging of a steam or hotwater heating system, an air conditioning or auto-matic fire protective sprinkler system, or an appli-ance for heating water.We do not cover loss caused by or resulting fromfreezing under this peril.

14. Freezinga. This peril means freezing of a plumbing, heating,

air conditioning or automatic fire protective sprin-kler system or of a household appliance but onlyif you have used reasonable care to:

(1) Maintain heat in the building; or(2) Shut off the water supply and drain all sys-

tems and appliances of water.

HOMEOWNERSHO 00 03 10 00

HO 00 03 10 00 Copyright, Insurance Services Office, Inc., 1999- 10 -

However, if the building is protected by an auto-matic fire protective sprinkler system, you mustuse reasonable care to continue the water sup-ply and maintain heat in the building for cover-age to apply.

b. In this peril, a plumbing system or householdappliance does not include a sump, sump pumpor related equipment or a roof drain, gutter,downspout or similar fixtures or equipment.

15. Sudden And Accidental Damage FromArtificially Generated Electrical CurrentThis peril does not include loss to tubes, transistors,electronic components or circuitry that are a part ofappliances, fixtures, computers, home entertain-ment units or other types of electronic apparatus.

16. Volcanic EruptionThis peril does not include loss caused by earth-quake, land shock waves or tremors.

SECTION I – EXCLUSIONSA. We do not insure for loss caused directly or indirectly

by any of the following. Such loss is excluded regard-less of any other cause or event contributing concur-rently or in any sequence to the loss. These exclusionsapply whether or not the loss event results in wide-spread damage or affects a substantial area.1. Ordinance Or Law

Ordinance Or Law means any ordinance or law:a. Requiring or regulating the construction, demoli-

tion, remodeling, renovation or repair of prop-erty, including removal of any resulting debris.This Exclusion A.1.a. does not apply to theamount of coverage that may be provided for inE.11. Ordinance Or Law under Section I – Prop-erty Coverages;

b. The requirements of which result in a loss invalue to property; or

c. Requiring any "insured" or others to test for,monitor, clean up, remove, contain, treat, detox-ify or neutralize, or in any way respond to, or as-sess the effects of, pollutants.Pollutants means any solid, liquid, gaseous orthermal irritant or contaminant, including smoke,vapor, soot, fumes, acids, alkalis, chemicals andwaste. Waste includes materials to be recycled,reconditioned or reclaimed.

This Exclusion A.1. applies whether or not the prop-erty has been physically damaged.

2. Earth MovementEarth Movement means:a. Earthquake, including land shock waves or trem-

ors before, during or after a volcanic eruption;b. Landslide, mudslide or mudflow;c. Subsidence or sinkhole; or

d. Any other earth movement including earth sink-ing, rising or shifting;

caused by or resulting from human or animal forcesor any act of nature unless direct loss by fire or ex-plosion ensues and then we will pay only for theensuing loss.This Exclusion A.2. does not apply to loss by theft.

3. Water DamageWater Damage means:a. Flood, surface water, waves, tidal water, over-

flow of a body of water, or spray from any ofthese, whether or not driven by wind;

b. Water or water-borne material which backs upthrough sewers or drains or which overflows oris discharged from a sump, sump pump or re-lated equipment; or

c. Water or water-borne material below the surfaceof the ground, including water which exerts pres-sure on or seeps or leaks through a building,sidewalk, driveway, foundation, swimming poolor other structure;

caused by or resulting from human or animal forcesor any act of nature.Direct loss by fire, explosion or theft resulting fromwater damage is covered.

4. Power FailurePower Failure means the failure of power or otherutility service if the failure takes place off the "resi-dence premises". But if the failure results in a loss,from a Peril Insured Against on the "residencepremises", we will pay for the loss caused by thatperil.

5. NeglectNeglect means neglect of an "insured" to use allreasonable means to save and preserve property atand after the time of a loss.

6. WarWar includes the following and any consequence ofany of the following:a. Undeclared war, civil war, insurrection, rebellion

or revolution;b. Warlike act by a military force or military person-

nel; orc. Destruction, seizure or use for a military pur-

pose.Discharge of a nuclear weapon will be deemed awarlike act even if accidental.

7. Nuclear HazardThis Exclusion A.7. pertains to Nuclear Hazard tothe extent set forth in M. Nuclear Hazard Clauseunder Section I – Conditions.

HOMEOWNERSHO 00 03 10 00

HO 00 03 10 00 Copyright, Insurance Services Office, Inc., 1999- 11 -

8. Intentional LossIntentional Loss means any loss arising out of anyact an "insured" commits or conspires to commitwith the intent to cause a loss.In the event of such loss, no "insured" is entitled tocoverage, even "insureds" who did not commit orconspire to commit the act causing the loss.

9. Governmental ActionGovernmental Action means the destruction, con-fiscation or seizure of property described in Cover-age A, B or C by order of any governmental or pub-lic authority.This exclusion does not apply to such acts orderedby any governmental or public authority that aretaken at the time of a fire to prevent its spread, if theloss caused by fire would be covered under this pol-icy.

B. We do not insure for loss to property described in Cov-erages A and B caused by any of the following. How-ever, any ensuing loss to property described in Cover-ages A and B not precluded by any other provision inthis policy is covered.1. Weather conditions. However, this exclusion only

applies if weather conditions contribute in any waywith a cause or event excluded in A. above to pro-duce the loss.

2. Acts or decisions, including the failure to act or de-cide, of any person, group, organization or govern-mental body.

3. Faulty, inadequate or defective:a. Planning, zoning, development, surveying, sit-

ing;b. Design, specifications, workmanship, re-

pair, construction, renovation, remodeling, grad-ing, compaction;

c. Materials used in repair, construction, renovationor remodeling; or

d. Maintenance;of part or all of any property whether on or off the"residence premises".

SECTION I – CONDITIONSA. Insurable Interest And Limit Of Liability

Even if more than one person has an insurable interestin the property covered, we will not be liable in any oneloss:1. To an "insured" for more than the amount of such

"insured's" interest at the time of loss; or2. For more than the applicable limit of liability.

B. Duties After LossIn case of a loss to covered property, we have no dutyto provide coverage under this policy if the failure tocomply with the following duties is prejudicial to us.These duties must be performed either by you, an "in-sured" seeking coverage, or a representative of either:

1. Give prompt notice to us or our agent;2. Notify the police in case of loss by theft;3. Notify the credit card or electronic fund transfer card

or access device company in case of loss as pro-vided for in E.6. Credit Card, Electronic Fund Trans-fer Card Or Access Device, Forgery And CounterfeitMoney under Section I – Property Coverages;

4. Protect the property from further damage. If repairsto the property are required, you must:a. Make reasonable and necessary repairs to pro-

tect the property; andb. Keep an accurate record of repair expenses;

5. Cooperate with us in the investigation of a claim;6. Prepare an inventory of damaged personal property

showing the quantity, description, actual cash valueand amount of loss. Attach all bills, receipts and re-lated documents that justify the figures in the inven-tory;

7. As often as we reasonably require:a. Show the damaged property;b. Provide us with records and documents we re-

quest and permit us to make copies; andc. Submit to examination under oath, while not in

the presence of another "insured", and sign thesame;

8. Send to us, within 60 days after our request, yoursigned, sworn proof of loss which sets forth, to thebest of your knowledge and belief:a. The time and cause of loss;b. The interests of all "insureds" and all others in

the property involved and all liens on the prop-erty;

c. Other insurance which may cover the loss;d. Changes in title or occupancy of the property

during the term of the policy;e. Specifications of damaged buildings and de-

tailed repair estimates;f. The inventory of damaged personal property

described in 6. above;g. Receipts for additional living expenses incurred

and records that support the fair rental valueloss; and

h. Evidence or affidavit that supports a claim underE.6. Credit Card, Electronic Fund Transfer CardOr Access Device, Forgery And CounterfeitMoney under Section I – Property Coverages,stating the amount and cause of loss.

HOMEOWNERSHO 00 03 10 00

HO 00 03 10 00 Copyright, Insurance Services Office, Inc., 1999- 12 -

C. Loss SettlementIn this Condition C., the terms "cost to repair or re-place" and "replacement cost" do not include the in-creased costs incurred to comply with the enforcementof any ordinance or law, except to the extent that cov-erage for these increased costs is provided in E.11.Ordinance Or Law under Section I – Property Cover-ages. Covered property losses are settled as follows:1. Property of the following types:

a. Personal property;b. Awnings, carpeting, household appliances, out-

door antennas and outdoor equipment, whetheror not attached to buildings;

c. Structures that are not buildings; andd. Grave markers, including mausoleums;at actual cash value at the time of loss but not morethan the amount required to repair or replace.

2. Buildings covered under Coverage A or B at re-placement cost without deduction for depreciation,subject to the following:a. If, at the time of loss, the amount of insurance in

this policy on the damaged building is 80% ormore of the full replacement cost of the buildingimmediately before the loss, we will pay the costto repair or replace, after application of any de-ductible and without deduction for depreciation,but not more than the least of the followingamounts:

(1) The limit of liability under this policy that ap-plies to the building;

(2) The replacement cost of that part of thebuilding damaged with material of like kindand quality and for like use; or

(3) The necessary amount actually spent to re-pair or replace the damaged building.

If the building is rebuilt at a new premises, thecost described in (2) above is limited to the costwhich would have been incurred if the buildinghad been built at the original premises.

b. If, at the time of loss, the amount of insurance inthis policy on the damaged building is less than80% of the full replacement cost of the buildingimmediately before the loss, we will pay thegreater of the following amounts, but not morethan the limit of liability under this policy that ap-plies to the building:

(1) The actual cash value of that part of thebuilding damaged; or

(2) That proportion of the cost to repair or re-place, after application of any deductible andwithout deduction for depreciation, that partof the building damaged, which the totalamount of insurance in this policy on thedamaged building bears to 80% of the re-placement cost of the building.

c. To determine the amount of insurance requiredto equal 80% of the full replacement cost of thebuilding immediately before the loss, do not in-clude the value of:

(1) Excavations, footings, foundations, piers, orany other structures or devices that supportall or part of the building, which are below theundersurface of the lowest basement floor;

(2) Those supports described in (1) above whichare below the surface of the ground insidethe foundation walls, if there is no basement;and

(3) Underground flues, pipes, wiring and drains.d. We will pay no more than the actual cash value

of the damage until actual repair or replacementis complete. Once actual repair or replacementis complete, we will settle the loss as noted in2.a. and b. above.However, if the cost to repair or replace thedamage is both:

(1) Less than 5% of the amount of insurance inthis policy on the building; and

(2) Less than $2,500;we will settle the loss as noted in 2.a. and b.above whether or not actual repair or replace-ment is complete.

e. You may disregard the replacement cost losssettlement provisions and make claim under thispolicy for loss to buildings on an actual cashvalue basis. You may then make claim for anyadditional liability according to the provisions ofthis Condition C. Loss Settlement, provided younotify us of your intent to do so within 180 daysafter the date of loss.

D. Loss To A Pair Or SetIn case of loss to a pair or set we may elect to:1. Repair or replace any part to restore the pair or set

to its value before the loss; or2. Pay the difference between actual cash value of

the property before and after the loss.

HOMEOWNERSHO 00 03 10 00

HO 00 03 10 00 Copyright, Insurance Services Office, Inc., 1999- 13 -

E.AppraisalIf you and we fail to agree on the amount of loss, eithermay demand an appraisal of the loss. In this event,each party will choose a competent and impartial ap-praiser within 20 days after receiving a written requestfrom the other. The two appraisers will choose an um-pire. If they cannot agree upon an umpire within 15days, you or we may request that the choice be madeby a judge of a court of record in the state where the"residence premises" is located. The appraisers willseparately set the amount of loss. If the appraiserssubmit a written report of an agreement to us, theamount agreed upon will be the amount of loss. If theyfail to agree, they will submit their differences to theumpire. A decision agreed to by any two will set theamount of loss.Each party will:1. Pay its own appraiser; and2. Bear the other expenses of the appraisal and um-

pire equally.F. Other Insurance And Service Agreement

If a loss covered by this policy is also covered by:1. Other insurance, we will pay only the proportion of

the loss that the limit of liability that applies underthis policy bears to the total amount of insurancecovering the loss; or

2. A service agreement, this insurance is excess overany amounts payable under any such agreement.Service agreement means a service plan, propertyrestoration plan, home warranty or other similar ser-vice warranty agreement, even if it is characterizedas insurance.

G. Suit Against UsNo action can be brought against us unless there hasbeen full compliance with all of the terms under SectionI of this policy and the action is started within two yearsafter the date of loss.

H. Our OptionIf we give you written notice within 30 days after we re-ceive your signed, sworn proof of loss, we may repairor replace any part of the damaged property with mate-rial or property of like kind and quality.

I. Loss PaymentWe will adjust all losses with you. We will pay youunless some other person is named in the policy or islegally entitled to receive payment. Loss will be payable60 days after we receive your proof of loss and:1. Reach an agreement with you;2. There is an entry of a final judgment; or3. There is a filing of an appraisal award with us.

J. Abandonment Of PropertyWe need not accept any property abandoned by an "in-sured".

K. Mortgage Clause1. If a mortgagee is named in this policy, any loss pay-

able under Coverage A or B will be paid to themortgagee and you, as interests appear. If morethan one mortgagee is named, the order of paymentwill be the same as the order of precedence of themortgages.

2. If we deny your claim, that denial will not apply to avalid claim of the mortgagee, if the mortgagee:a. Notifies us of any change in ownership, occu-

pancy or substantial change in risk of which themortgagee is aware;

b. Pays any premium due under this policy on de-mand if you have neglected to pay the premium;and

c. Submits a signed, sworn statement of loss within60 days after receiving notice from us of yourfailure to do so. Paragraphs E. Appraisal, G. SuitAgainst Us and I. Loss Payment under Section I– Conditions also apply to the mortgagee.

3. If we decide to cancel or not to renew this policy,the mortgagee will be notified at least 10 days be-fore the date cancellation or nonrenewal takes ef-fect.

4. If we pay the mortgagee for any loss and deny pay-ment to you:a. We are subrogated to all the rights of the mort-

gagee granted under the mortgage on the prop-erty; or

b. At our option, we may pay to the mortgagee thewhole principal on the mortgage plus any ac-crued interest. In this event, we will receive a fullassignment and transfer of the mortgage and allsecurities held as collateral to the mortgagedebt.

5. Subrogation will not impair the right of the mort-gagee to recover the full amount of the mortgagee'sclaim.

L. No Benefit To BaileeWe will not recognize any assignment or grant any cov-erage that benefits a person or organization holding,storing or moving property for a fee regardless of anyother provision of this policy.

M. Nuclear Hazard Clause1. "Nuclear Hazard" means any nuclear reaction, ra-

diation, or radioactive contamination, all whethercontrolled or uncontrolled or however caused, orany consequence of any of these.

2. Loss caused by the nuclear hazard will not be con-sidered loss caused by fire, explosion, or smoke,whether these perils are specifically named in orotherwise included within the Perils Insured Against.

HOMEOWNERSHO 00 03 10 00

HO 00 03 10 00 Copyright, Insurance Services Office, Inc., 1999- 14 -

3. This policy does not apply under Section I to losscaused directly or indirectly by nuclear hazard, ex-cept that direct loss by fire resulting from the nu-clear hazard is covered.

N. Recovered PropertyIf you or we recover any property for which we havemade payment under this policy, you or we will notifythe other of the recovery. At your option, the propertywill be returned to or retained by you or it will becomeour property. If the recovered property is returned to orretained by you, the loss payment will be adjustedbased on the amount you received for the recoveredproperty.

O. Volcanic Eruption PeriodOne or more volcanic eruptions that occur within a 72hour period will be considered as one volcanic erup-tion.

P. Policy PeriodThis policy applies only to loss which occurs during thepolicy period.

Q. Concealment Or FraudWe provide coverage to no "insureds" under this policyif, whether before or after a loss, an "insured" has:1. Intentionally concealed or misrepresented any ma-

terial fact or circumstance;2. Engaged in fraudulent conduct; or3. Made false statements;relating to this insurance.

R. Loss Payable ClauseIf the Declarations show a loss payee for certain listedinsured personal property, the definition of "insured" ischanged to include that loss payee with respect to thatproperty.If we decide to cancel or not renew this policy, that losspayee will be notified in writing.

SECTION II – LIABILITY COVERAGESA. Coverage E – Personal Liability

If a claim is made or a suit is brought against an "in-sured" for damages because of "bodily injury" or "prop-erty damage" caused by an "occurrence" to which thiscoverage applies, we will:1. Pay up to our limit of liability for the damages for

which an "insured" is legally liable. Damages in-clude prejudgment interest awarded against an "in-sured"; and

2. Provide a defense at our expense by counsel of ourchoice, even if the suit is groundless, false orfraudulent. We may investigate and settle any claimor suit that we decide is appropriate. Our duty tosettle or defend ends when our limit of liability forthe "occurrence" has been exhausted by paymentof a judgment or settlement.

B. Coverage F – Medical Payments To OthersWe will pay the necessary medical expenses that areincurred or medically ascertained within three yearsfrom the date of an accident causing "bodily injury".Medical expenses means reasonable charges formedical, surgical, x-ray, dental, ambulance, hospital,professional nursing, prosthetic devices and funeralservices. This coverage does not apply to you or regu-lar residents of your household except "residence em-ployees". As to others, this coverage applies only:1. To a person on the "insured location" with the per-

mission of an "insured"; or2. To a person off the "insured location", if the "bodily

injury":a. Arises out of a condition on the "insured loca-

tion" or the ways immediately adjoining;b. Is caused by the activities of an "insured";c. Is caused by a "residence employee" in the

course of the "residence employee's" employ-ment by an "insured"; or

d. Is caused by an animal owned by or in the careof an "insured".

SECTION II – EXCLUSIONSA. "Motor Vehicle Liability"

1. Coverages E and F do not apply to any "motor ve-hicle liability" if, at the time and place of an "occur-rence", the involved "motor vehicle":a. Is registered for use on public roads or property;b. Is not registered for use on public roads or prop-

erty, but such registration is required by a law, orregulation issued by a government agency, for itto be used at the place of the "occurrence"; or

c. Is being:(1) Operated in, or practicing for, any prear-

ranged or organized race, speed contest orother competition;

(2) Rented to others;(3) Used to carry persons or cargo for a charge;

or(4) Used for any "business" purpose except for a

motorized golf cart while on a golfing facility.2. If Exclusion A.1. does not apply, there is still no

coverage for "motor vehicle liability" unless the "mo-tor vehicle" is:a. In dead storage on an "insured location";b. Used solely to service an "insured's" residence;c. Designed to assist the handicapped and, at the

time of an "occurrence", it is:(1) Being used to assist a handicapped person;

or(2) Parked on an "insured location";

HOMEOWNERSHO 00 03 10 00

HO 00 03 10 00 Copyright, Insurance Services Office, Inc., 1999- 15 -

d. Designed for recreational use off public roadsand:

(1) Not owned by an "insured"; or(2) Owned by an "insured" provided the "occur-

rence" takes place on an "insured location"as defined in Definitions B. 6.a., b., d., e. orh.; or

e. A motorized golf cart that is owned by an "in-sured", designed to carry up to 4 persons, notbuilt or modified after manufacture to exceed aspeed of 25 miles per hour on level ground and,at the time of an "occurrence", is within the legalboundaries of:

(1) A golfing facility and is parked or storedthere, or being used by an "insured" to:

(a) Play the game of golf or for other recrea-tional or leisure activity allowed by the fa-cility;

(b) Travel to or from an area where "motorvehicles" or golf carts are parked orstored; or

(c) Cross public roads at designated pointsto access other parts of the golfing facil-ity; or

(2) A private residential community, including itspublic roads upon which a motorized golf cartcan legally travel, which is subject to the au-thority of a property owners association andcontains an "insured's" residence.

B. "Watercraft Liability"1. Coverages E and F do not apply to any "watercraft

liability" if, at the time of an "occurrence", the in-volved watercraft is being:a. Operated in, or practicing for, any prearranged

or organized race, speed contest or other com-petition. This exclusion does not apply to a sail-ing vessel or a predicted log cruise;

b. Rented to others;c. Used to carry persons or cargo for a charge; ord. Used for any "business" purpose.

2. If Exclusion B.1. does not apply, there is still nocoverage for "watercraft liability" unless, at the timeof the "occurrence", the watercraft:a. Is stored;b. Is a sailing vessel, with or without auxiliary

power, that is:(1) Less than 26 feet in overall length; or(2) 26 feet or more in overall length and not

owned by or rented to an "insured"; orc. Is not a sailing vessel and is powered by:

(1) An inboard or inboard-outdrive engine or mo-tor, including those that power a water jetpump, of:

(a) 50 horsepower or less and not owned byan "insured"; or

(b) More than 50 horsepower and not ownedby or rented to an "insured"; or

(2) One or more outboard engines or motorswith:

(a) 25 total horsepower or less;(b) More than 25 horsepower if the outboard

engine or motor is not owned by an "in-sured";

(c) More than 25 horsepower if the outboardengine or motor is owned by an "insured"who acquired it during the policy period;or

(d) More than 25 horsepower if the outboardengine or motor is owned by an "insured"who acquired it before the policy period,but only if:(i) You declare them at policy inception;

or(ii) Your intent to insure them is reported

to us in writing within 45 days afteryou acquire them.

The coverages in (c) and (d) above apply forthe policy period.

Horsepower means the maximum power ratingassigned to the engine or motor by the manufac-turer.

C. "Aircraft Liability"This policy does not cover "aircraft liability".

D. "Hovercraft Liability"This policy does not cover "hovercraft liability".

E. Coverage E – Personal Liability And Coverage F –Medical Payments To OthersCoverages E and F do not apply to the following:1. Expected Or Intended Injury

"Bodily injury" or "property damage" which is ex-pected or intended by an "insured" even if the re-sulting "bodily injury" or "property damage":a. Is of a different kind, quality or degree than ini-

tially expected or intended; orb. Is sustained by a different person, entity, real or

personal property, than initially expected or in-tended.

However, this Exclusion E.1. does not apply to"bodily injury" resulting from the use of reasonableforce by an "insured" to protect persons or property;

HOMEOWNERSHO 00 03 10 00

HO 00 03 10 00 Copyright, Insurance Services Office, Inc., 1999- 16 -

2. "Business"a. "Bodily injury" or "property damage" arising out

of or in connection with a "business" conductedfrom an "insured location" or engaged in by an"insured", whether or not the "business" isowned or operated by an "insured" or employsan "insured".This Exclusion E.2. applies but is not limited toan act or omission, regardless of its nature orcircumstance, involving a service or duty ren-dered, promised, owed, or implied to be pro-vided because of the nature of the "business".

b. This Exclusion E.2. does not apply to:(1) The rental or holding for rental of an "insured

location";(a) On an occasional basis if used only as a

residence;(b) In part for use only as a residence, unless

a single family unit is intended for use bythe occupying family to lodge more thantwo roomers or boarders; or

(c) In part, as an office, school, studio or pri-vate garage; and

(2) An "insured" under the age of 21 years in-volved in a part-time or occasional, self-employed "business" with no employees;

3. Professional Services"Bodily injury" or "property damage" arising out ofthe rendering of or failure to render professionalservices;

4. "Insured's" Premises Not An "Insured Location""Bodily injury" or "property damage" arising out of apremises:a. Owned by an "insured";b. Rented to an "insured"; orc. Rented to others by an "insured";that is not an "insured location";

5. War"Bodily injury" or "property damage" caused directlyor indirectly by war, including the following and anyconsequence of any of the following:a. Undeclared war, civil war, insurrection, rebellion

or revolution;b. Warlike act by a military force or military person-

nel; orc. Destruction, seizure or use for a military pur-

pose.Discharge of a nuclear weapon will be deemed awarlike act even if accidental;

6. Communicable Disease"Bodily injury" or "property damage" which arisesout of the transmission of a communicable diseaseby an "insured";

7. Sexual Molestation, Corporal Punishment OrPhysical Or Mental Abuse"Bodily injury" or "property damage" arising out ofsexual molestation, corporal punishment or physicalor mental abuse; or

8. Controlled Substance"Bodily injury" or "property damage" arising out ofthe use, sale, manufacture, delivery, transfer orpossession by any person of a Controlled Sub-stance as defined by the Federal Food and DrugLaw at 21 U.S.C.A. Sections 811 and 812. Con-trolled Substances include but are not limited to co-caine, LSD, marijuana and all narcotic drugs. How-ever, this exclusion does not apply to the legitimateuse of prescription drugs by a person following theorders of a licensed physician.

Exclusions A. "Motor Vehicle Liability", B. "WatercraftLiability", C. "Aircraft Liability", D. "Hovercraft Liability"and E.4. "Insured's" Premises Not An "Insured Loca-tion" do not apply to "bodily injury" to a "residence em-ployee" arising out of and in the course of the "resi-dence employee's" employment by an "insured".

F. Coverage E – Personal LiabilityCoverage E does not apply to:1. Liability:

a. For any loss assessment charged against youas a member of an association, corporation orcommunity of property owners, except as pro-vided in D. Loss Assessment under Section II –Additional Coverages;

b. Under any contract or agreement entered into byan "insured". However, this exclusion does notapply to written contracts:

(1) That directly relate to the ownership, mainte-nance or use of an "insured location"; or

(2) Where the liability of others is assumed byyou prior to an "occurrence";

unless excluded in a. above or elsewhere in thispolicy;

2. "Property damage" to property owned by an "in-sured". This includes costs or expenses incurred byan "insured" or others to repair, replace, enhance,restore or maintain such property to prevent injuryto a person or damage to property of others,whether on or away from an "insured location";

3. "Property damage" to property rented to, occupiedor used by or in the care of an "insured". This ex-clusion does not apply to "property damage" causedby fire, smoke or explosion;

HOMEOWNERSHO 00 03 10 00

HO 00 03 10 00 Copyright, Insurance Services Office, Inc., 1999- 17 -

4. "Bodily injury" to any person eligible to receive anybenefits voluntarily provided or required to be pro-vided by an "insured" under any:a. Workers' compensation law;b. Non-occupational disability law; orc. Occupational disease law;

5. "Bodily injury" or "property damage" for which an"insured" under this policy:a. Is also an insured under a nuclear energy liabil-

ity policy issued by the:(1) Nuclear Energy Liability Insurance Associa-

tion;(2) Mutual Atomic Energy Liability Underwriters;(3) Nuclear Insurance Association of Canada;or any of their successors; or

b. Would be an insured under such a policy but forthe exhaustion of its limit of liability; or

6. "Bodily injury" to you or an "insured" as defined un-der Definitions 5.a. or b.This exclusion also applies to any claim made orsuit brought against you or an "insured":a. To repay; orb. Share damages with;another person who may be obligated to pay dam-ages because of "bodily injury" to an "insured".

G. Coverage F – Medical Payments To OthersCoverage F does not apply to "bodily injury":1. To a "residence employee" if the "bodily injury":

a. Occurs off the "insured location"; andb. Does not arise out of or in the course of the

"residence employee's" employment by an "in-sured";

2. To any person eligible to receive benefits voluntarilyprovided or required to be provided under any:a. Workers' compensation law;b. Non-occupational disability law; orc. Occupational disease law;

3. From any:a. Nuclear reaction;b. Nuclear radiation; orc. Radioactive contamination;all whether controlled or uncontrolled or howevercaused; ord. Any consequence of any of these; or

4. To any person, other than a "residence employee"of an "insured", regularly residing on any part of the"insured location".

SECTION II – ADDITIONAL COVERAGESWe cover the following in addition to the limits of liability:

A. Claim ExpensesWe pay:1. Expenses we incur and costs taxed against an "in-

sured" in any suit we defend;2. Premiums on bonds required in a suit we defend,

but not for bond amounts more than the CoverageE limit of liability. We need not apply for or furnishany bond;

3. Reasonable expenses incurred by an "insured" atour request, including actual loss of earnings (butnot loss of other income) up to $250 per day, forassisting us in the investigation or defense of aclaim or suit; and