Embed Size (px)

Citation preview

Financial Management Step-by-Step

Financial Management Step-by-Step

V1.1 2 © Young Enterprise 2010

Contents

1. Introduction...........................................................................................................................3

2. The Young Enterprise Financial Management System at a Glance.........................................3

3. Regular Management Accounts.............................................................................................5

3.1 General Principles..........................................................................................................5

3.2 Receipts: money coming into your company.................................................................6

3.3 Payments: money going out of your company..............................................................7

3.4 Paying Surplus Cash into the Bank (Transfer)................................................................8

3.5 Drawing Cash out from the Bank (Transfer)...................................................................9

3.6 Reports.........................................................................................................................10

3.7 Balance Sheet..............................................................................................................12

4. End of Year Reports.............................................................................................................13

5. Completing End of Year Reports..........................................................................................15

5.1 Allocating Profit – Filling in the End of Year Accounts Input Form...............................15

5.2 A note about Bonuses and Donations..........................................................................18

5.3 Statement of Taxation Liabilities..................................................................................18

Financial Management Step-by-Step

V1.1 3 © Young Enterprise 2010

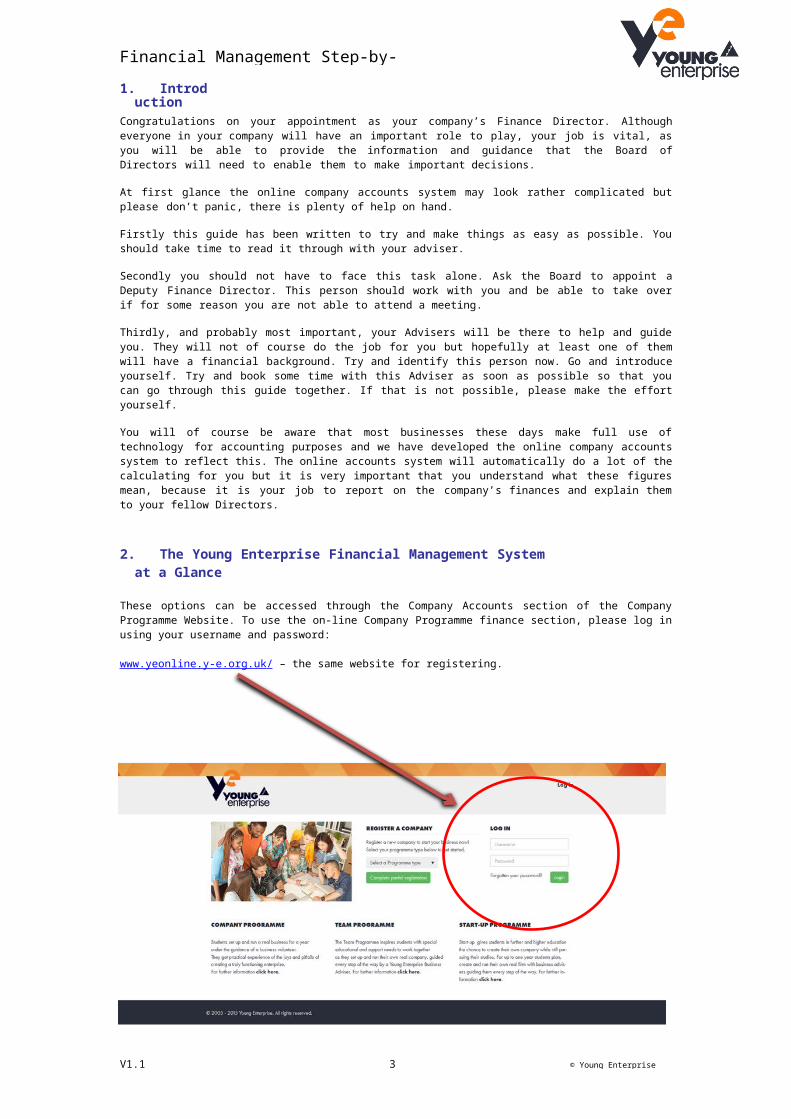

1. IntroductionCongratulations on your appointment as your company’s Finance Director. Although everyone in your company will have an important role to play, your job is vital, as you will be able to provide the information and guidance that the Board of Directors will need to enable them to make important decisions.

At first glance the online company accounts system may look rather complicated but please don’t panic, there is plenty of help on hand.

Firstly this guide has been written to try and make things as easy as possible. You should take time to read it through with your adviser.

Secondly you should not have to face this task alone. Ask the Board to appoint a Deputy Finance Director. This person should work with you and be able to take over if for some reason you are not able to attend a meeting.

Thirdly, and probably most important, your Advisers will be there to help and guide you. They will not of course do the job for you but hopefully at least one of them will have a financial background. Try and identify this person now. Go and introduce yourself. Try and book some time with this Adviser as soon as possible so that you can go through this guide together. If that is not possible, please make the effort yourself.

You will of course be aware that most businesses these days make full use of technology for accounting purposes and we have developed the online company accounts system to reflect this. The online accounts system will automatically do a lot of the calculating for you but it is very important that you understand what these figures mean, because it is your job to report on the company’s finances and explain them to your fellow Directors.

2. The Young Enterprise Financial Management System at a Glance

These options can be accessed through the Company Accounts section of the Company Programme Website. To use the on-line Company Programme finance section, please log in using your username and password:

www.yeonline.y-e.org.uk / – the same website for registering.

Financial Management Step-by-Step

V1.1 4 © Young Enterprise 2010

This is the welcome page once you have logged in. Now click on View to take you to your Company:

Now click on Company Finances:

This takes you to the Company Finances page. Here you can download the Accounts System Instructions or click on the Accounts System:

From here you can input details of all Receipts and Payments, as well as producing monthly, interim and final accounts for your company.

Financial Management Step-by-Step

V1.1 5 © Young Enterprise 2010

3. Regular Management Accounts

3.1 General Principles

R e cord a ll m on e y trans a c t io n s Each and every transaction must be recorded somewhere in the Receipts and Payments tables.

Rep o r t i n g of t r ansa ct i o ns One of your difficulties as Finance Director will be to ensure that all members of the company report to you all transactions they make.

Ban k ing your cash Each week when you receive cash, pay it into the bank right away. This is good business practice. It also makes book-keeping easier.

Kee p in g recor d s You must file and retain all receipts and invoices carefully. They are an important part of the company’s financial records. Always keep all documents which provide evidence of money received or paid out.

Why do things appear t w ice? You will see that the amount of money received appears on the forms twice, once on the left hand side of the form and again on the right hand side. This will be true for all amounts you enter in your accounting forms whether they are Payments or Receipts. You will have noticed that columns are headed DR (debit) or CR (credit). Any item that you enter in a debit column must have an equal or corresponding entry in a credit column. Similarly every credit item must always have an equal or corresponding debit. This is known as double entry book keeping.

Don’t forget that any cash that you are holding must be kept in a safe place.Try to borrow a cash box or even buy one if funds will allow. We recommend that when it is not being used the box is locked away in a secure place. Before you leave a meeting always ensure that you have personally handed the box over to whoever is going to be responsible and ensure that that

person is going to be available at your next meeting or when you will need cash.KEEP YOUR CASH SECURE

Financial Management Step-by-Step

V1.1 6 © Young Enterprise 2010

3.2 Receipts: money coming into your company

To enter details of money received in your receipts, click on the plus sign on the right of the screen. This will turn blue and you can enter the details. Remember to SAVE CHANGES after each transaction.

This Fo r m Is Used To Record all payments made to your company

F or E ach Tra n sa c t i on You S h o ul d Enter the Date of the transaction Complete the Where From column. This indicates where the money has come from. Enter the total amount paid in either the Cash or the Bank column.

o Use the Cash column if you have received casho Use the Bank column if you have received a cheque

‘Analyse’ the payment in columns 3 to 8. The totals of columns 1 and 2 must always equal the totals of columns 3 to 8.

Exam p l e R e c e ipts Tra n sactions

19th SeptemberYou sell 150 shares for a total of £150 cash (cash column)

19th SeptemberYou sell 6 clocks in cash for £36.

19th SeptemberYou sell a clock for £6. The clock is paid for by cheque (bank column).

See below for how these transactions should be entered into the receipts table.To delete an entry, click on the cross, and then Save changes.

To print a copy for your records, go to File and Print Preview, then Print.

Financial Management Step-by-Step

V1.1 7 © Young Enterprise 2010

3.3 Payments: money going out of your companyREPEAT THE ABOVE PROCESS TO ENTER DETAILS OF ALL PAYMENTS (Click on Payments)

To enter details of money paid out, click on the plus sign on the right of the screen. This will turn blue and you can enter the details. Remember to SAVE CHANGES after each transaction.

This Fo r m Is Used To Record all payments made from your company

F or E ach Tra n sa c t i on You S h o ul d Enter the Date for each transaction. Complete the What is it for column. This indicates where the money is being paid to. Enter the total amount paid out in either the Cash or the Bank column.

o Use the Bank column if you pay by cheque.o Use the Cash column if you pay by cash.

‘Analyse’ the payment in columns 9 to 13.

Exam p l e Pa y m en ts Tra n sa c t io ns

19th SeptemberYou pay your registration fee of £100 to Young Enterprise by cheque.

19th SeptemberYou pay for £35 of materials by cheque.

19th SeptemberYou pay £6.23 for some stationery by cash.

See below for how these transactions should be entered into the payments table:

Financial Management Step-by-Step

V1.1 8 © Young Enterprise 2010

3.4 Paying Surplus Cash into the Bank (Transfer)

This stage involves both the Receipts and Payments Tables.

Payments T a ble - you have wit h drawn y o ur cash to pay into your Bank Acco u n t • Enter the Date for each transaction.• Enter ‘Bank’ in the Where To column.• Enter the amount in column 8 - Cash.• Enter the amount in column 14 - Bank and Cash Transfers.

Rec e ipts Ta b le - your B a nk Acco u n t has r e cei v ed t h e m o ney • Enter the Date for each transaction.• Enter ‘Cash’ in the Where From column.• Enter the amount in column 1 - Bank.• Enter the amount in column 6 – Bank and Cash Transfers.

Exa m p l e – You pay £140 c a s h i n t o t h e bank on 15 t h O ct o b e r

Complete a slip in the Bank Paying-In Book ready to pay it into the bank. Paying surplus cash into the bank involves both handing money out (a payment), because you are reducing the amount of cash you hold, and receiving money into the Bank Account (a receipt).

Consequently this transaction needs to be recorded on both tables, Payments and Receipts

1. Payments T a ble : you have taken £140 cash out of the cash box to the bank account

Date Where To 7Bank

8Cash

............... 14Bank and

Cash Transfers

15-Oct-17 Bank £140 ............... £140

2. Rec e ipts Ta b le : You have paid £140 cash into the bank account from the cash box

Date Where From 1Bank

2Cash

............... 6Bank and

Cash Transfers

15-Oct-17 Cash £140 ............... £140

Remember to Save Changes.

Financial Management Step-by-Step

V1.1 9 © Young Enterprise 2010

3.5 Drawing Cash out from the Bank (Transfer)Should you ever need to draw cash out of the bank (for example you may need to draw out some change for a Trade Fair) the entries are similar but opposite to paying money into the bank.

This stage also involves both the Receipts and Payments Tables.

Payments T a ble - you have wit h drawn money from your B ank A c c o u n t to pay into the cash b ox • Enter the Date for each transaction.• Enter ‘Cash’ in the Where To column.• Enter the amount in column 7 - Bank.• Enter the amount in column 14 - Bank and Cash Transfers

Rec e ipts Ta b le - your c a sh box has re c ei v ed mo n e y • Enter the Date for each transaction.• Enter ‘Bank’ in the Where From column.• Enter the amount in column 2 - Cash.• Enter the amount in column 6 – Bank and Cash Transfers

Example – You withdraw £90 from your bank account on 15th October

Write a cheque to “CASH” for £90 which is what you need to withdraw the cash from your bank account. Take it to the bank.

Taking money out from the bank account involves both handing money out (a payment), because you are reducing the amount of cash in the bank, and receiving money into the cash box (areceipt). Consequently this transaction needs to be recorded on both tables, Payments and Receipts

1. Payments T a ble : you have taken £90 from the bank account into the cash box

Date Where To 7Bank

8Cash

............... 14Bank and

Cash Transfers

15-Oct-17 Cash £90 ............... £90

2. Rec e ipts Ta b le : You have paid £90 into the cash box from the Bank Account

Date Where From 1Bank

2Cash

............... 6Bank and

Cash Transfers

15-Oct-17 Bank £90 ............... £90

Remember to Save Changes.

Financial Management Step-by-Step

V1.1 10 © Young Enterprise 2010

3.6 Reports

To generate reports, click on Reports:

From here you can produce a number of reports:

Latest Monthly/Interim Reports

Click on Generate Reports to generate an up-to-date set of reports.

Then click on Profit and Loss Account/Balance Sheet as appropriate.

Financial Management Step-by-Step

V1.1 11 © Young Enterprise 2010

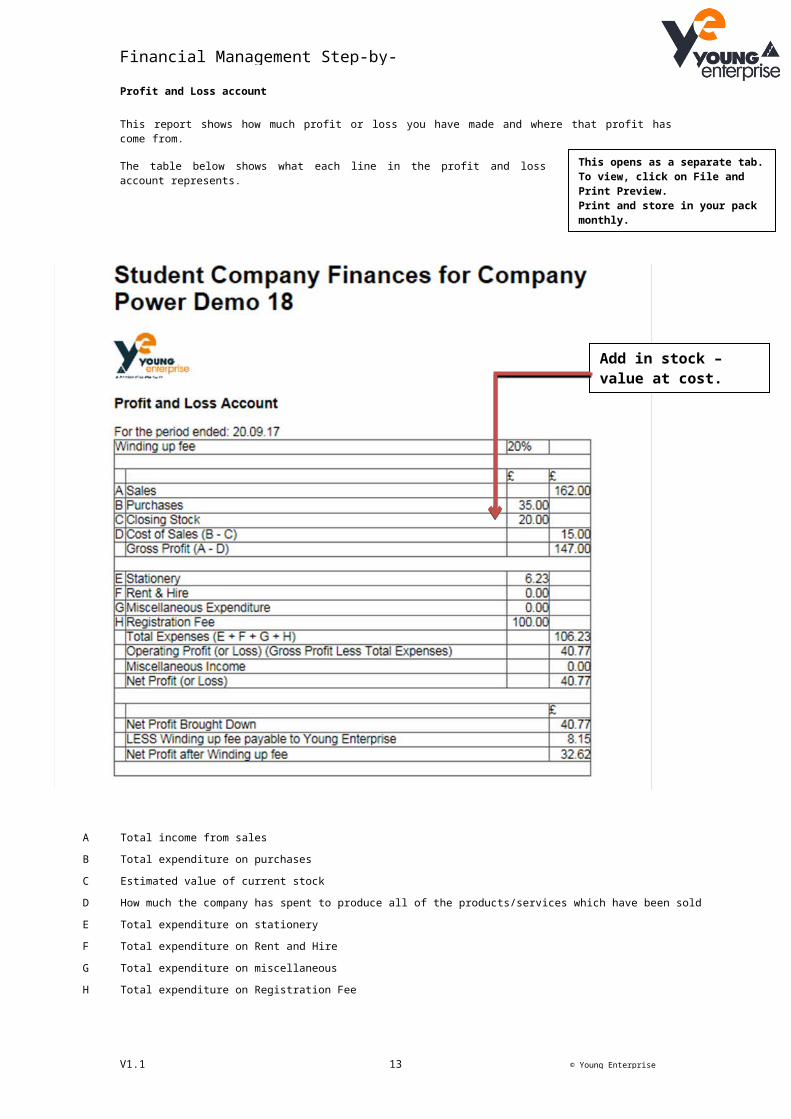

Profit and Loss account

This report shows how much profit or loss you have made and where that profit has come from.

The table below shows what each line in the profit and loss account represents.

A Total income from sales

B Total expenditure on purchases

C Estimated value of current stock

D How much the company has spent to produce all of the products/services which have been sold

E Total expenditure on stationery

F Total expenditure on Rent and Hire

G Total expenditure on miscellaneous

H Total expenditure on Registration Fee

Add in stock – value at cost.

This opens as a separate tab.To view, click on File and Print Preview.Print and store in your pack monthly.

Financial Management Step-by-Step

V1.1 12 © Young Enterprise 2010

3.7 Balance Sheet

This report shows the total ASSETS (what the company owns) and the total LIABILITIES (what the company owes).

The table below shows what each line in the Balance Sheet represents.

A Note about YE Winding Up Fee and Profits

At the end of the year a Winding Up Fee of 20% is calculated and companies must pay this to Young Enterprise. It is possible (but unlikely) that companies may be in a position at the end of the year where they would be owed money back to them. Unfortunately Young Enterprise is unable to pay any refunds back to companies at the end of the year.

The Balance Sheet should always balance!

This opens as a separate tab.To view, click on File and Print Preview.Print and store in your pack monthly.

Financial Management Step-by-Step

V1.1 13 © Young Enterprise 2010

4. End of Year ReportsIn order to generate a new set of End of Year Reports click on End of Year:

1. Generate and print out an updated "Profit and Loss Report" and "Balance Sheet" from Monthly Reports

Make sure that your payments and receipts tables have been updated as well as your closing stock value before you generate these reports. You should bring these reports to your next company meeting (see point 3).

2. Print out a blank copy of the End of Year Accounts Input Form

Print a blank copy of the End of Year Input form.

Financial Management Step-by-Step

V1.1 14 © Young Enterprise 2010

3. Discuss with your fellow company members how you want to distribute your profits and how you will complete the form

This should be done at a board meeting and decided jointly by the company members. See 5.1 below for more information on how to fill this in.

4. Complete the End of Year Accounts Input Form online

This should be done online by a company member who has permission to edit the company accounts. When you complete the End of Year Accounts Input Form online you will generate the following reports:

Statement of Taxation Liabilities (5.3) Liquidation Report

The Liquidation Report summarises the information you will have entered in your “End of Year Accounts Input Form” to record how you have decided to allocate your company’s profits.

5. Present your end of year accounts to your shareholders at the company’s AGM

Your shareholders will need to approve your end of year accounts which tells them what the return on their investment will be. They may also want to see your most up to date balance sheet and profit and loss account. If the shareholders do not approve your end of year accounts you will have to generate the end of year reports again to reflect the changes discussed at the AGM.

£

Cash in hand and at bank £422.00 Total cash held by the company

Accounts receivable £18.00 Total money owed to your company (Debtors)

Stock £0.00 Total value of your current stockTool, machinery andequipment £0.00 Total value of the tools, machinery and equipment you own

Other Assets £0.00 Other assets that belong to your company

Total £440.00

£

Final Expenses: Payroll Company Members £60.00 Money left to pay to company members as salary

AnnualReport £10.00

Cost of your annual report if not already included in your payments

BankCharges £0.00 Total bank charges left to pay

Creditors £0.00 Total money you owe to other people or organisations

Young Enterprise Taxation: Corporation Tax and VAT £25.00 Calculated automaticallyYoung Enterprisecontributions £15.00 Any other money owed to Young Enterprise

Total amount paid to company members in bonusesBonuses to companymembers

ShareholdersBalance Distributed to 30 Shareholders Number of shareholders

Holding a total of 150 £1 shares Total number of shares sold

Dividend out of profits per share x shares

shareReturn of capital at per share x

Total before donations

Donations (optional): Young Enterprise

Other

Total (must equal total of assets)

Financial Management Step-by-Step

V1.1 15 © Young Enterprise 2010

5. Completing End of Year Reports

5.1 Allocating Profit – Filling in the End of Year Accounts Input FormYou can fill in some of the entries straight away (highlighted below in green) before discussing the allocation of remaining profit with your fellow company members.

This part of the form shows your company’s remaining assets after liquidation Assets

Total assets

Because you have liquidated your company all of your company’s assets must be distributed.

This part of the form shows how your company’s remaining assets will be distributed.

Distribution

Total amount of dividend paid out to shareholders ontop of the amount they investedTotal amount of capital given to you by shareholders that should be repaid if you have made a profit

Total distribution before donations

Total amount donated to Young Enterprise (optional)

Total amount donated to other charities / organisations

Total of all distributions

To fill in the rest of the table your company needs to make some decisions about how much of your company’s remaining assets you will return to shareholders, pay your company members as bonuses and donate to charity.

However you choose to distribute your remaining assets you must make sure thatTotal Assets = Total of all distributions

Initially company members will decide exactly how to allocate your company’s assets at a board

Financial Management Step-by-Step

V1.1 16 © Young Enterprise 2010

meeting and the following two examples may help you understand how this can be done. An independent and responsible person (for example an Adviser) should be requested to verify the accuracy of the statement, and sign the auditor’s report at the bottom of the liquidation report.

Bear in mind that the final accounts and distribution of profits must be approved by your shareholders at the AGM before they are finalised.

Financial Management Step-by-StepExam p l e 1 – The c o mpany h as ma d e an o v erall profit

In this example the company’s total assets were £440 which must be distributed.

After the final expenses, Young Enterprise Taxation and Young Enterprise contributions they had £330

V1.1 17 © Young Enterprise 2010

remaining to distribute. (£440 – £60 - £10 - £25 - £15 = £330)

At the start of the year they had raised money from 150 shares at £1 each, a total of £150 share capital.

The company decides to distribute the remaining £330 in the following way:

Bonuses to company members: £100

ShareholdersDividend out of profits: £60Return of Capital £150

DonationsYoung Enterprise £10Other £10

You can see that they have chosen to pay back the shareholders their original £150 investment and also to pay them a “dividend” (extra payment) of £60.

It is standard practice in business to pay back shareholders a dividend if the company has made a significant profit to thank them for their investment and to encourage them to continue to be investors in the company. Usually the more profit a company makes the higher dividend it is able to pay back to its shareholders.

In total this company has sold 150 shares which means that each £1 share has a 40p dividend (£60 divided by 150). This represents a 40% dividend (40p is 40% of £1)

Distribution

£

Final Expenses: Payroll Company Members £60.00AnnualReport £10.00BankCharges £0.00

Creditors £0.00

Young Enterprise Taxation: Corporation Tax and VAT £25.00Young Enterprisecontributions £15.00Bonuses to companymembers £100

ShareholdersBalance Distributed to 30 Shareholders

Holding a total of 150 £1 shares

Dividend out of profits £0.40 per share x 150 shares

shares

£60.00

Return of capital at £1 per share x 150 £150.00

Total before donations

Donations (optional): Young Enterprise £10

Other £10Total (must equal total of assets) £440

The total of the distribution table = £440 which is the same as the total assets £440 which means that the company has calculated these figures correctly

Financial Management Step-by-Step

V1.1 18 © Young Enterprise 2010

Exam p l e 2 – The c o mpany h as ma d e an o v erall loss

In this example the company’s total assets were £170 which must be distributed.

After the final expenses, Young Enterprise Taxation and Young Enterprise contributions they had £120 remaining to distribute. (£170 – £10 - £5 - £35 = £120)

At the start of the year they had raised money from 150 shares at £1 each, a total of £150 share capital.

This means they do not have enough money to pay back their shareholders in full. The company decides to divide all the remaining assets amongst the shareholders (leaving no money left for bonuses or donations to charity).

The company decides to distribute the remaining £120 in the following way:

Bonuses to company members: £0

ShareholdersDividend out of profits: £0Return of Capital £120

DonationsYoung Enterprise £0Other £0

You can see that in this example the company has been unable to pay back shareholders any dividend. In fact, shareholders will get back less than what they invested.

In total this company has sold 150 shares which means that each £1 share will only be returned to the shareholders as 80p (£120 divided by 150 = 80p).

Distribution

£

Final Expenses: Payroll Company Members £0.00AnnualReport £10.00BankCharges £5.00

Creditors £0.00

Young Enterprise Taxation: Corporation Tax and VAT £35.00Young Enterprisecontributions £0.00Bonuses to companymembers

ShareholdersBalance Distributed to 30 Shareholders

Holding a total of 150 £1 shares

Dividend out of profits £0.00 per share x 150 shares

shares

£0.00

Return of capital at £0.80 per share x 150 £120.00

Total before donations

Donations (optional): Young Enterprise £0

Other £0Total (must equal total of assets) £170

The total of the distribution table = £170 which is the same as the total assets of £170 which means that the company has calculated these figures correctly.

Financial Management Step-by-Step

V1.1 19 © Young Enterprise 2010

5.2 A note about Bonuses and Donations

You can, of course, work out several different rates of dividend all of which will give different totals available for distribution as bonuses and donations.

You should consider how to calculate any bonus payable to students. It might be as a percentage of salary, or perhaps on the basis of hours worked, or meetings attended etc.

Although it is against Young Enterprise rules for you to trade on the fact that you intend to donate your profits to charity you can decide to donate your remaining assets to charity after you have liquidated the company.

You should bear in mind that the more money you pay yourselves as bonuses or donate to charity the less money you will be able to return to shareholders who are the people who first invested in your company. Decisions about how much to pay in bonuses and donations should be approved by the shareholders at your AGM before the accounts are finalised.

5.3 Statement of Taxation Liabilities

This form calculates the total tax (YE VAT and corporation tax) that your company owes to Young Enterprise. The total is shown in the “Total Tax Paid to YE” box. You will need to fill in your company address at the top and get this form signed and dated. Unless you are advised of alternative local arrangements for collection of the taxes send the form with a cheque to cover the total to Young Enterprise Support Centre made payable to Young Enterprise (or the Young Enterprise Scotland office for Scotland made payable to Young Enterprise Scotland).

YE Corporation Tax is a tax on the company’s profits and is calculated at the rate of 10% on the net profit of the company, as indicated in the final Profit & Loss Account. YE VAT is calculated as the YE VAT collected on sales minus the YE VAT paid on purchases.

Your YE Corporation Tax and YE VAT payments are very important to Young Enterprise as part of their funds to provide students next year with the experience you have (hopefully) enjoyed. As Young Enterprise is a charity these payments are an essential part of its charitable income.