Embed Size (px)

Citation preview

i

MICROFINANCE AND FINANCIAL PERFORMANCE OF SMALL AND MEDIUM

ENTERPRISES IN TANZANIA: A CASE STUDY OF ILALA MUNICIPALITY

A DISSERTATION

SUBMITED TO THE DIRECTORATE OF POSTGRADUATE

STUDIES AND RESEARCH, KAMPALA INTERNATIONAL

UNIVERSITY IN TANZANIA

IN PARTIAL FULFILLMENT OF THE REQUIREMENT FOR THE AWARD DEGREE

OF MASTER IN BUSINESS ADMINISTRATION

BANKING AND FINANCE

BY

HALIPHA IDDY MNUNKA

MBA/18546/602/DT

NOVEMBER 2018

i

DEDICATION

I author of this dissertation I dedicate this to my beloved parents Mr and Mrs Iddy Mnunka

without them I wouldn’t be at this point of my life ,they lifted me up when I fell and gave me

hope ,may the almighty God bless them without them I would have not been here today.

ii

AKNOWLEDGEMENT

I thank God for enabling me finish this work though under hectic and cumbersome situation

including unexpected changes in the course of producing this work.

The entire Dissertation has not been an individual work. Contributions have been made by many

people whom I cannot list all, but for sure they are to remain in my memory. I must appreciate

that without their support, my work could have been more difficult and impossible.

My highest appreciation goes to Dr Wario Wako, my Supervisor, for being part of this work by

tirelessly reading, correcting and guiding me by giving constructive comments.

I do thank my family especially my beloved wife Maureen for the perseverance she showed

during the preparation of this work.

I thank all the SMEs which responded positively when I was collecting data. Here I want to

specifically thank to Ilala municipal Executive director for his supported provided from his

office as well as SMEs within Ilala Municipal.

Also my classmates Scarion Oscar and Nuwahereza susan, Last and not least the Kampala

international university -Tanzania for provision of humble learning environment that facilitated

accomplishments of my academic goals.

iii

DECLARATION A

I hereby declare that this research report on Microfinance and Financial Performance of Small

and Medium Enterprises: A case study of Ilala Municipal in Tanzania is conducted under my

supervision.

Name of Supervisor

DR WAKO.

Signature of Supervisor

-----------------------------------

Date-----------------------------

iv

DECLARATION B

I hereby declare that this research report on Microfinance and Financial Performance of Small

and Medium Enterprises: A case study of Ilala Municipal in Tanzania, is my original work and

has not been presented for a degree or any other academic award in any other university or

institution of learning.

Name of Candidate

HALIPHA IDDY MNUNKA

Signiture of Student

--------------------------

Date

v

APPROVAL

“This disertation entitled “MICROFINANCE AND FINANCIAL PERFORMANCE OF

SMALL AND MEDIUM ENTERPRISES A CASE STUDY OF ILALA MUNICIPAL IN

TANZANIA”prepared by Halipha Iddy mnunka in partial fulfillment of the requirement for the

award degree of masters of business adminstration- finance and banking has examined and

approved by the pannel on oral examination has been submitted for examination with my

approval as authorized univesity supervisor

Name of Supervisor

DR WAKO.

Signature of Supervisor

-----------------------------------

Date-----------------------------

Name of Director of the Directorate of Postgraduate and Research

………………………………………………………….

Signature of the Director

……………………………………………………………

Date

vi

TABLE OF CONTENTS

DEDICATION ................................................................................................................................. i

AKNOWLEDGEMENT ................................................................................................................. ii

DECLARATION A ....................................................................................................................... iii

DECLARATION B ....................................................................................................................... iv

APPROVAL ................................................................................................................................... v

TABLE OF CONTENTS ............................................................................................................... vi

LIST OF TABLES ....................................................................................................................... viii

LIST OF FIGURE........................................................................................................................... x

LIST OF ACRONYMS ................................................................................................................. xi

CHAPTER ONE ............................................................................................................................. 1

INTRODUCTION .......................................................................................................................... 1

1.1 CHAPTER OVER VIEW ......................................................................................................... 1

1.2 Background of the Study .......................................................................................................... 1

1.3 Statement of the Problem .......................................................................................................... 6

1.4 Objectives of the Study ............................................................................................................. 7

1.5 Research Questions ................................................................................................................ 8

The study was guided by the following research questions;........................................................... 8

1.6 Hypothesis ................................................................................................................................. 8

1.7 Scope of the Study .................................................................................................................... 8

1.8 Significance of the Study .......................................................................................................... 9

1.9 Operational Definition of Key Terms ..................................................................................... 10

CHAPTER TWO .......................................................................................................................... 12

LITERATURE REVIEW ............................................................................................................. 12

2.1 Introduction ............................................................................................................................. 12

2.2 Theoretical Literature Review ................................................................................................ 12

2.3 Conceptual Framework ........................................................................................................... 15

2.4 Empirical Literature Review ................................................................................................... 16

2.5 Research Gap .......................................................................................................................... 22

CHAPTER THREE ...................................................................................................................... 24

METHODOLOGY ....................................................................................................................... 24

vii

3.1 Introduction ............................................................................................................................. 24

3.2 Research Design...................................................................................................................... 24

3.3 Study Population ..................................................................................................................... 24

3.4 Sample Size ............................................................................................................................. 25

3.5 Sampling Techniques. ............................................................................................................. 25

3.6 Data Collection Tool ............................................................................................................... 25

3.8 Validity and Reliability ........................................................................................................... 26

3.9 Data Analysis .......................................................................................................................... 27

3.10 Ethical Consideration ............................................................................................................ 28

3.11 Limitations of the Study........................................................................................................ 28

CHAPTER FOUR ......................................................................................................................... 29

DATA PRESENTATION AND ANALYSIS .............................................................................. 29

4.1 Introduction ............................................................................................................................. 29

4.2 General profile of the respondents .......................................................................................... 29

4.3 Influence of provision of credit facilities on financial performance of SMEs. ..................... 32

4.4 Effect of savings mobilization on financial performance of SMEs ........................................ 37

4.5 Financial skills training and financial performance of SMEs. .............................................. 42

4.6 Small and Medium Enterprises Performances (SMEs). ...................................................... 47

CHAPTER FIVE .......................................................................................................................... 55

SUMMARY, CONCLUSION AND RECOMMENDATIONS. .................................................. 55

5.1 Introduction. ............................................................................................................................ 55

5.2 Summary. ................................................................................................................................ 55

5.3 Conclusion. ............................................................................................................................. 57

5.4 Recommendations. .................................................................................................................. 58

REFERENCES. ............................................................................................................................ 60

APPENDICES .............................................................................................................................. 70

APPENDIX I: QUESTIONNAIRE. ............................................................................................. 70

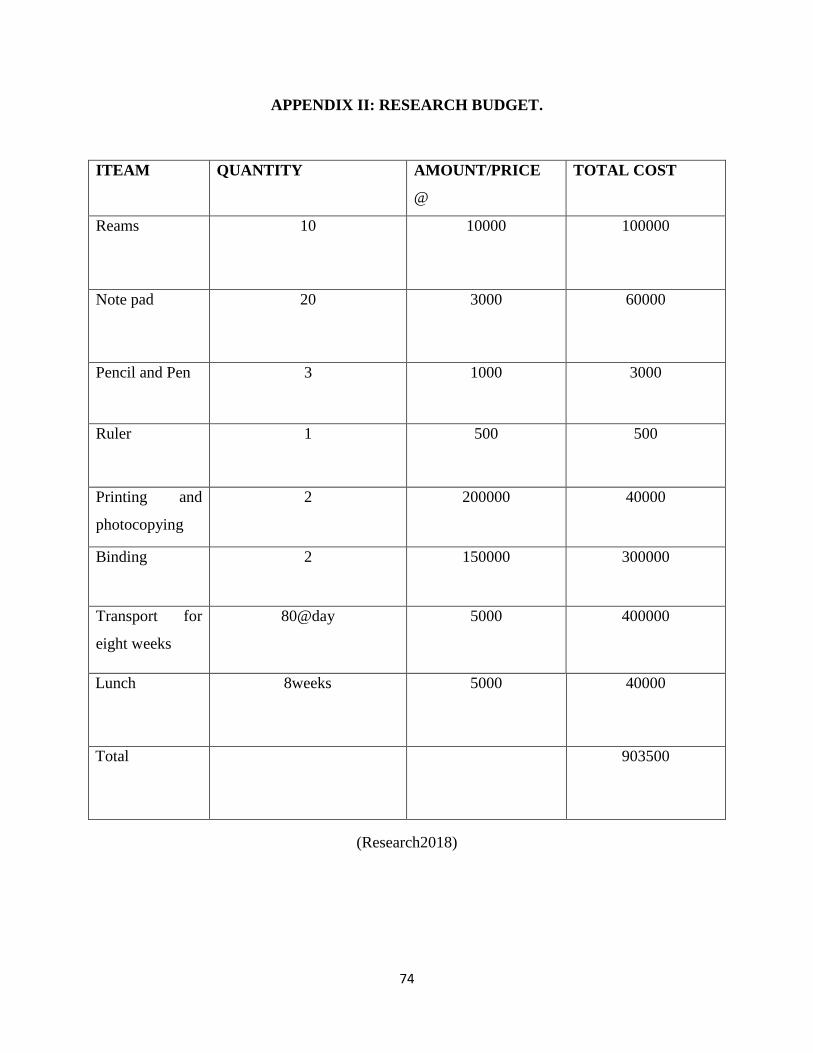

APPENDIX II: RESEARCH BUDGET. ...................................................................................... 74

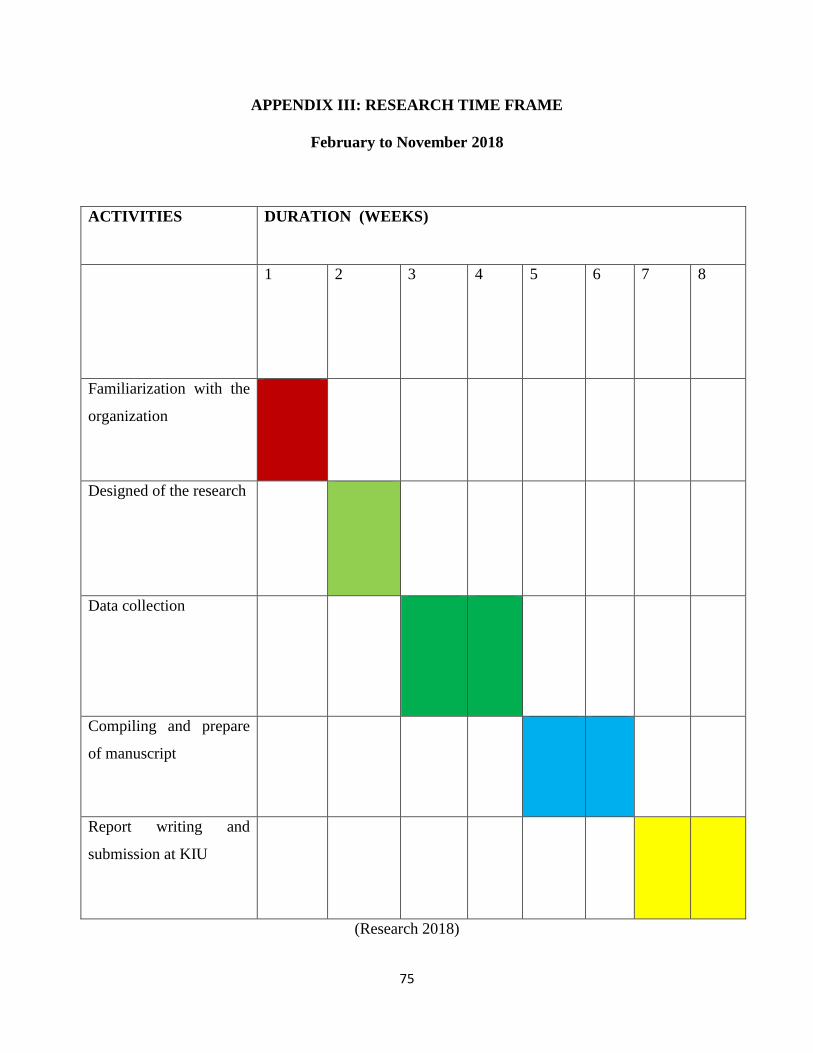

APPENDIX III: RESEARCH TIME FRAME ............................................................................. 75

viii

LIST OF TABLES

Table 4.1 Gender of Respondents ................................................................................................. 28

Table 4.2 Age of Respondents ...................................................................................................... 29

Table 4.3 Education back ground of the respondents ................................................................... 30

Table 4.4 marital status of the respondents ................................................................................... 31

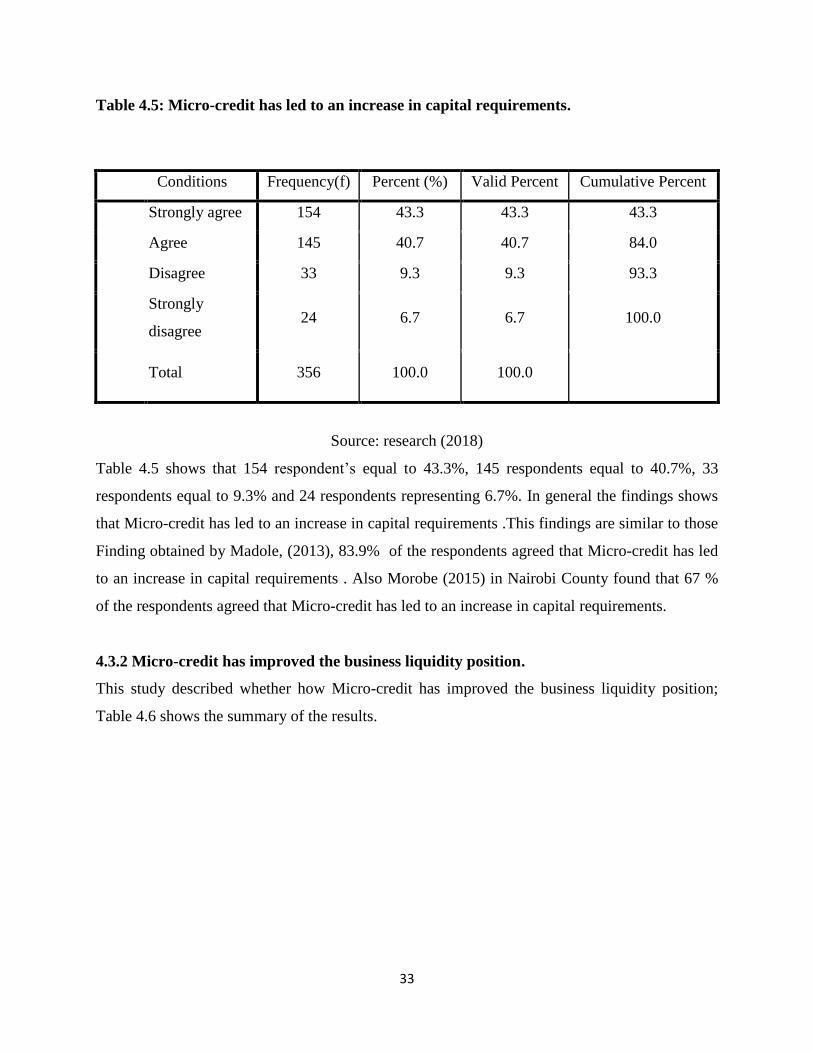

Table 45: Micro-credit has led to an increase in capital requirements ......................................... 32

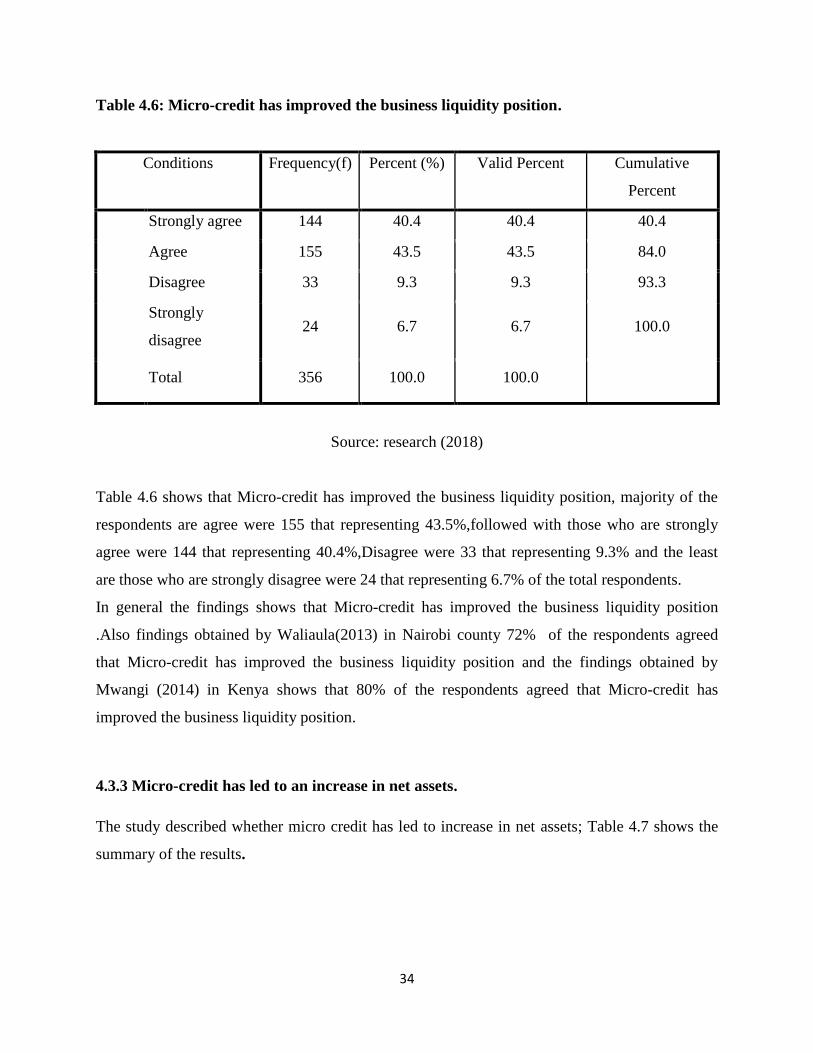

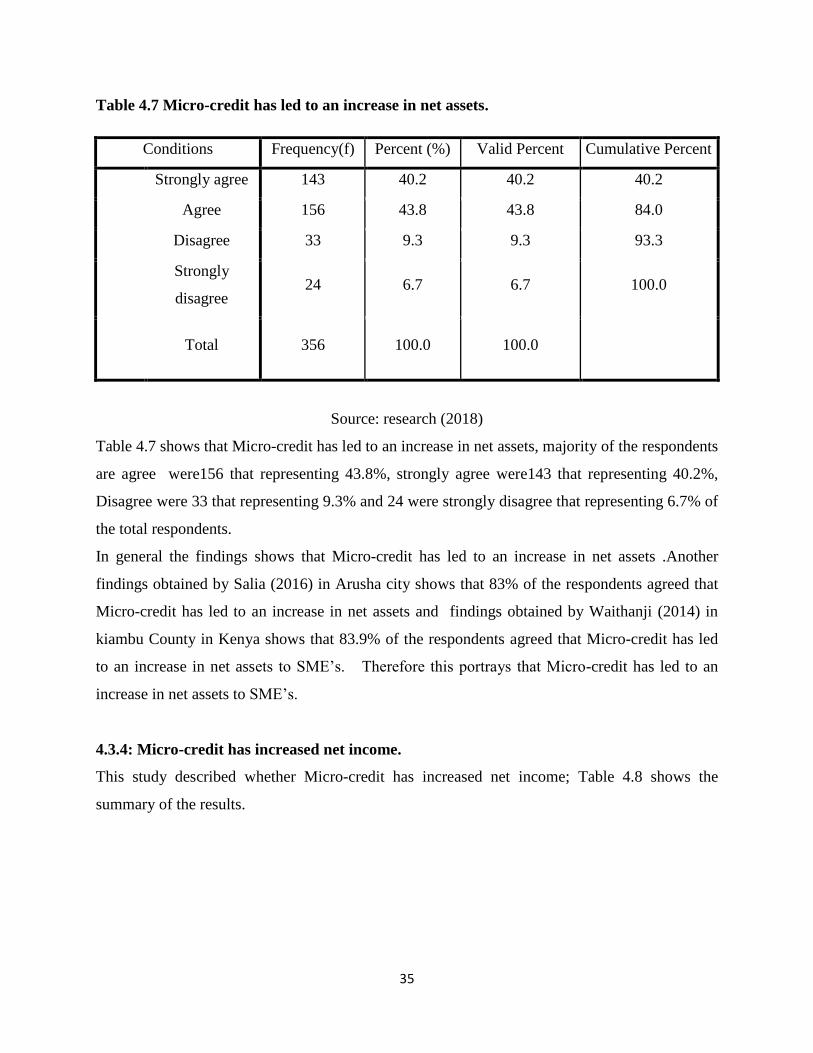

Table 4.6 : Micro-credit has improved the business liquidity position......................................... 33

Table 4.7 Micro-credit has led to an increase in net assets ........................................................... 34

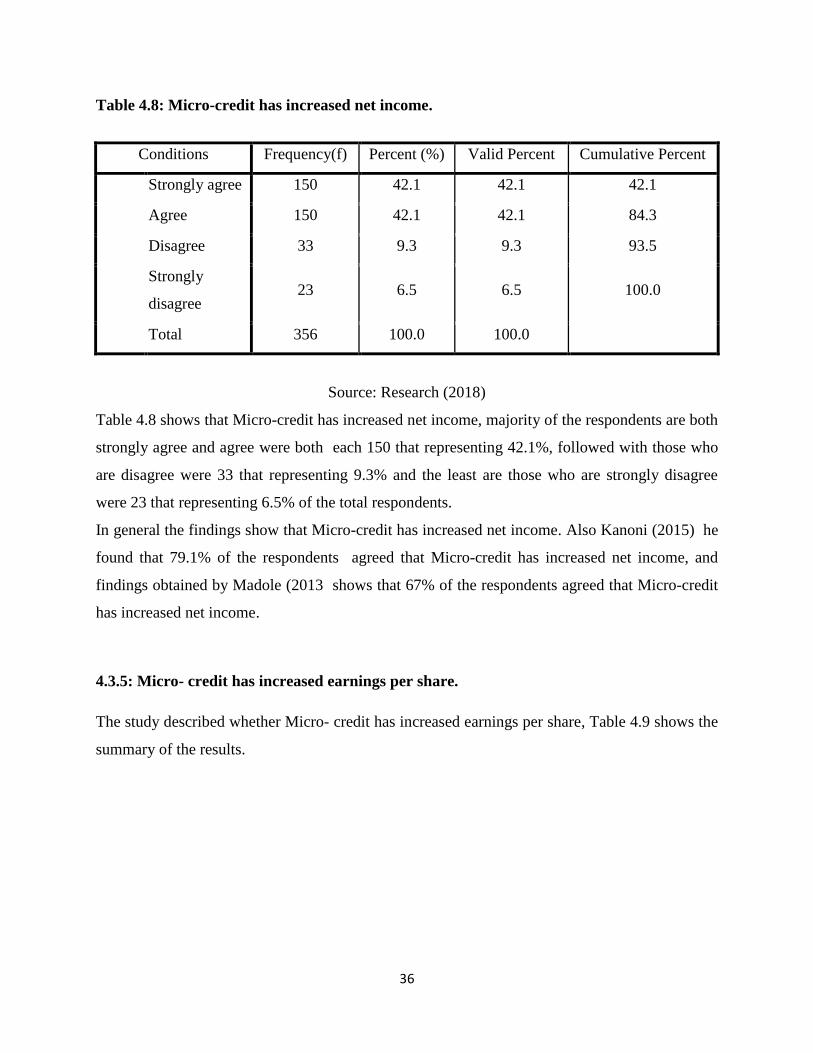

Table 4.8: Micro-credit has increased net income ........................................................................ 35

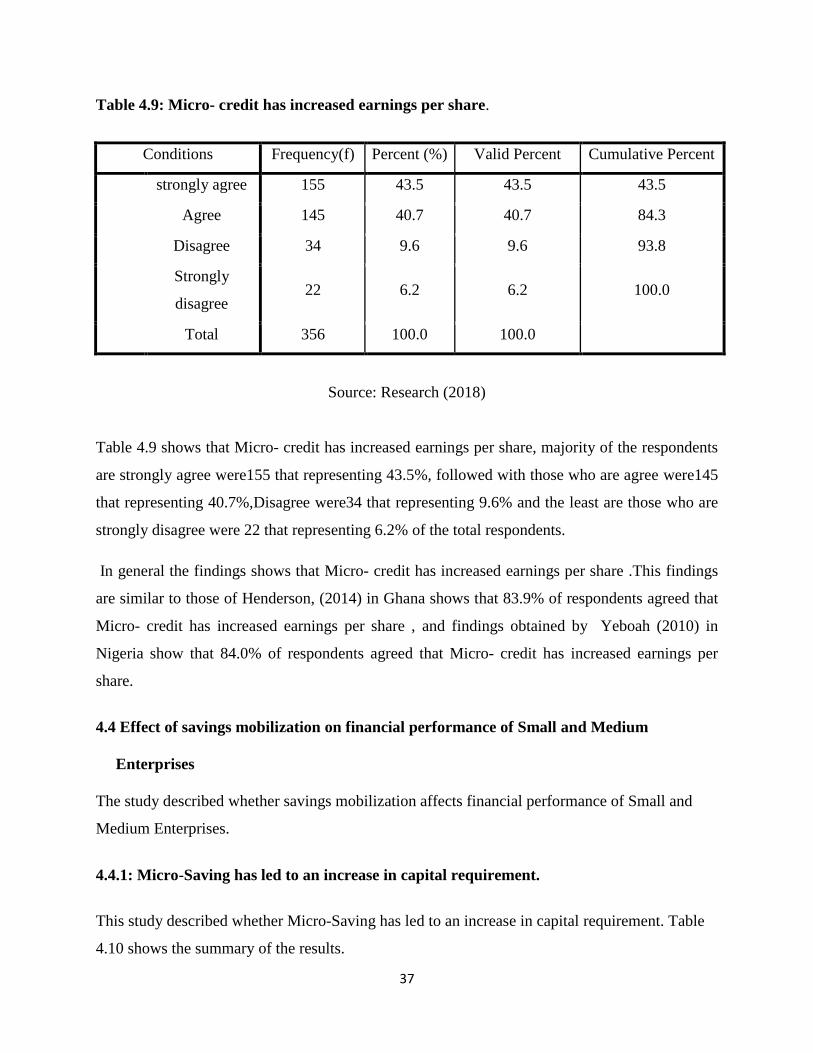

Table 4.9 : Micro- credit has increased earnings per share. .......................................................... 36

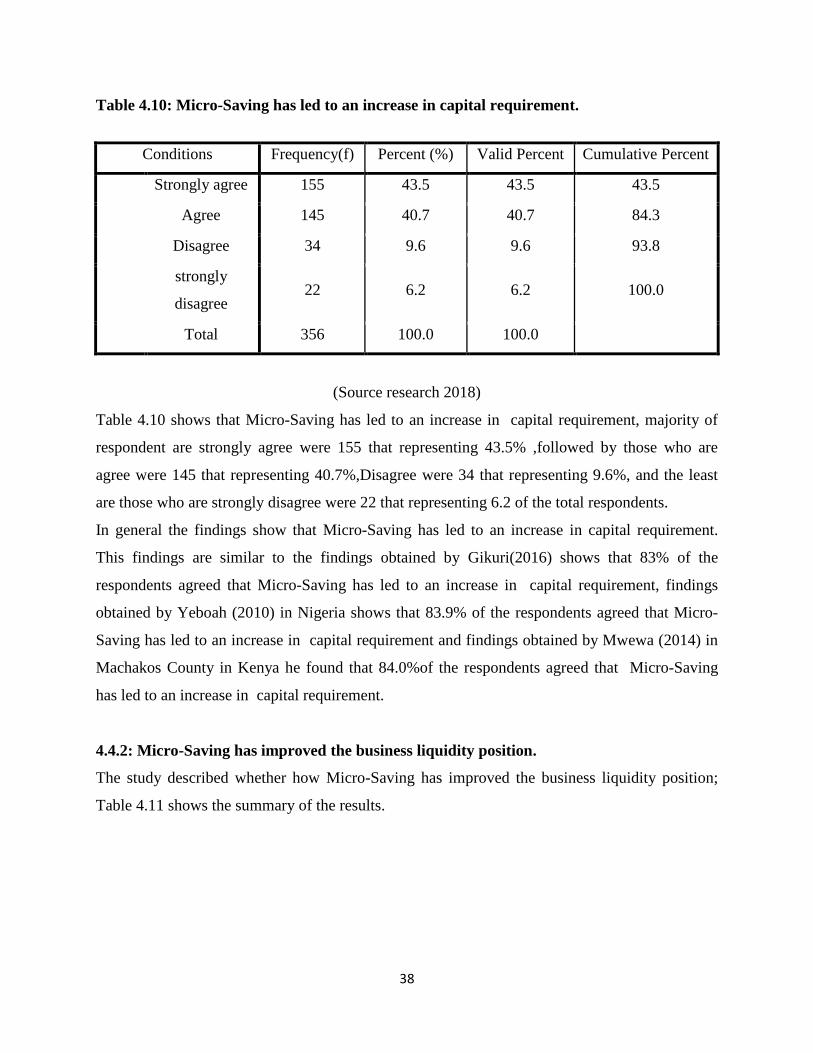

Table 4.10 : Micro-Saving has led to an increase in capital requirement .................................... 37

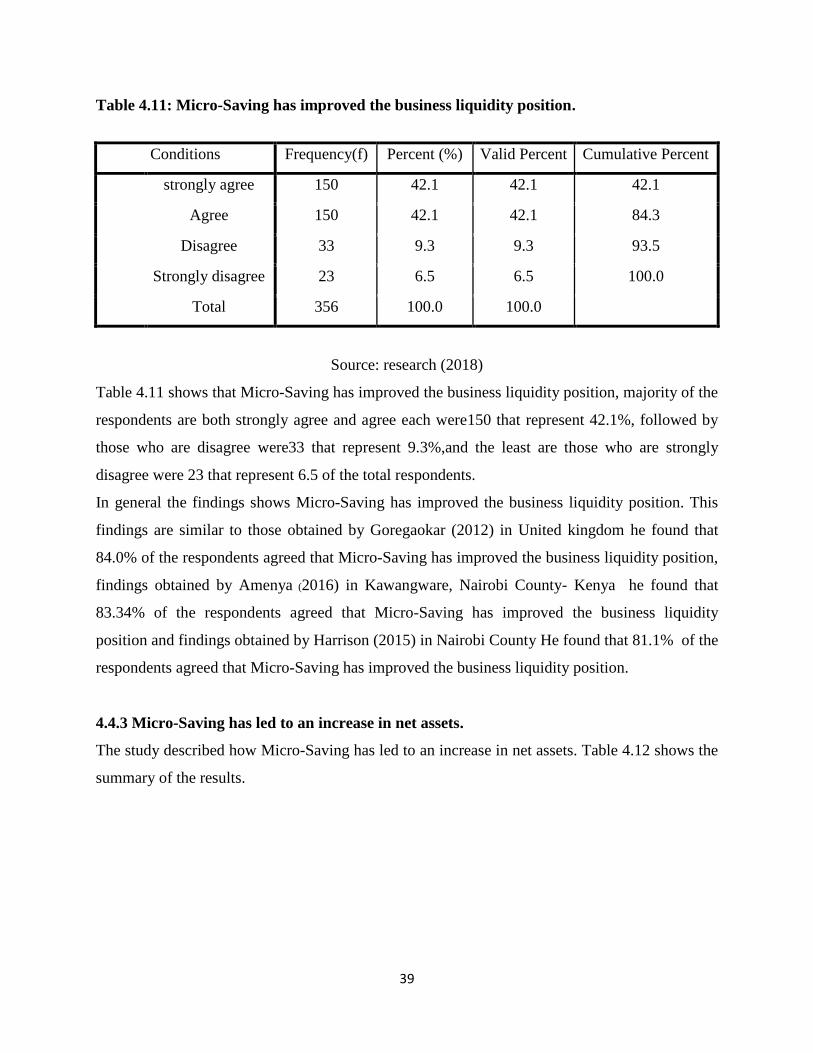

Table 4.11: Micro-Saving has improved the business liquidity position ...................................... 38

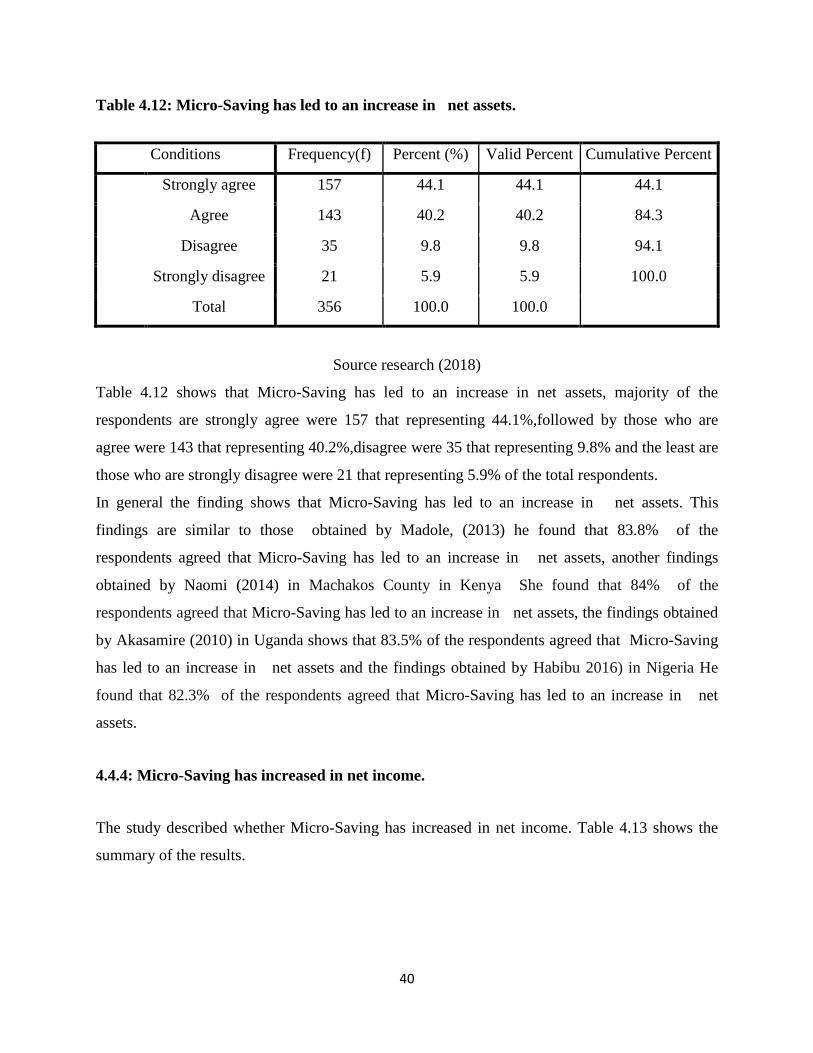

Table 4.12: Micro-Saving has led to an increase in net assets.................................................... 39

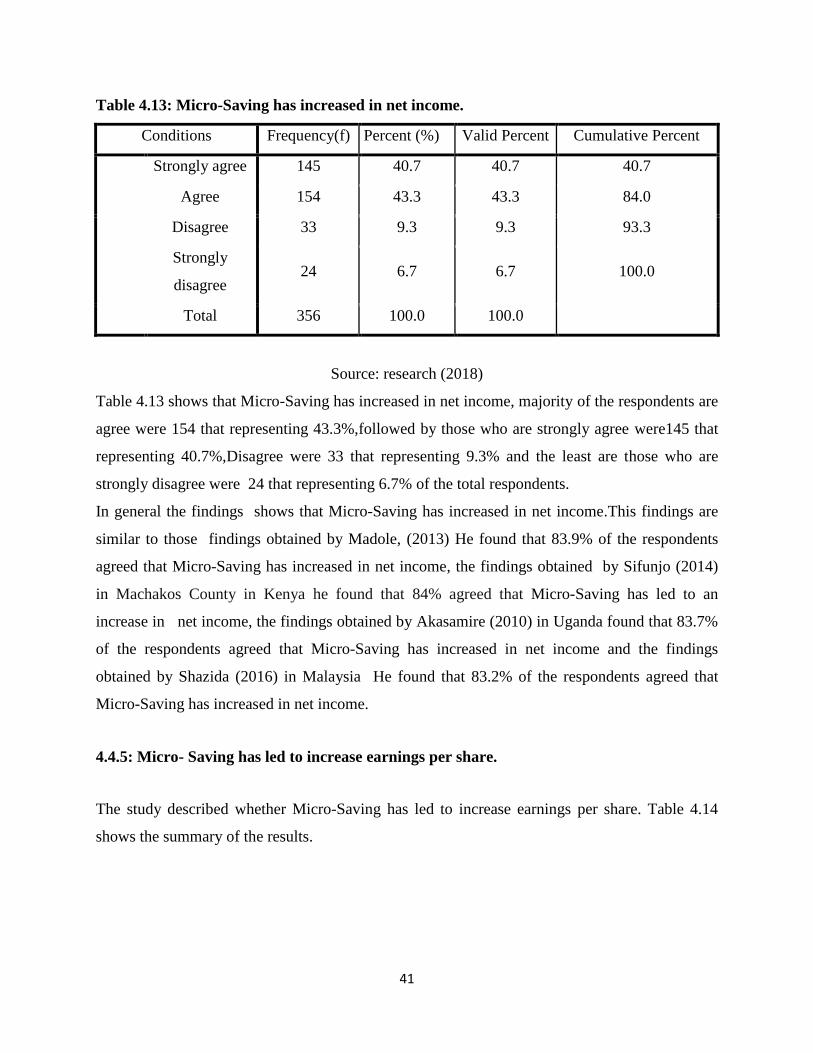

Table 4.13 : Micro-Saving has increased in net income. .............................................................. 40

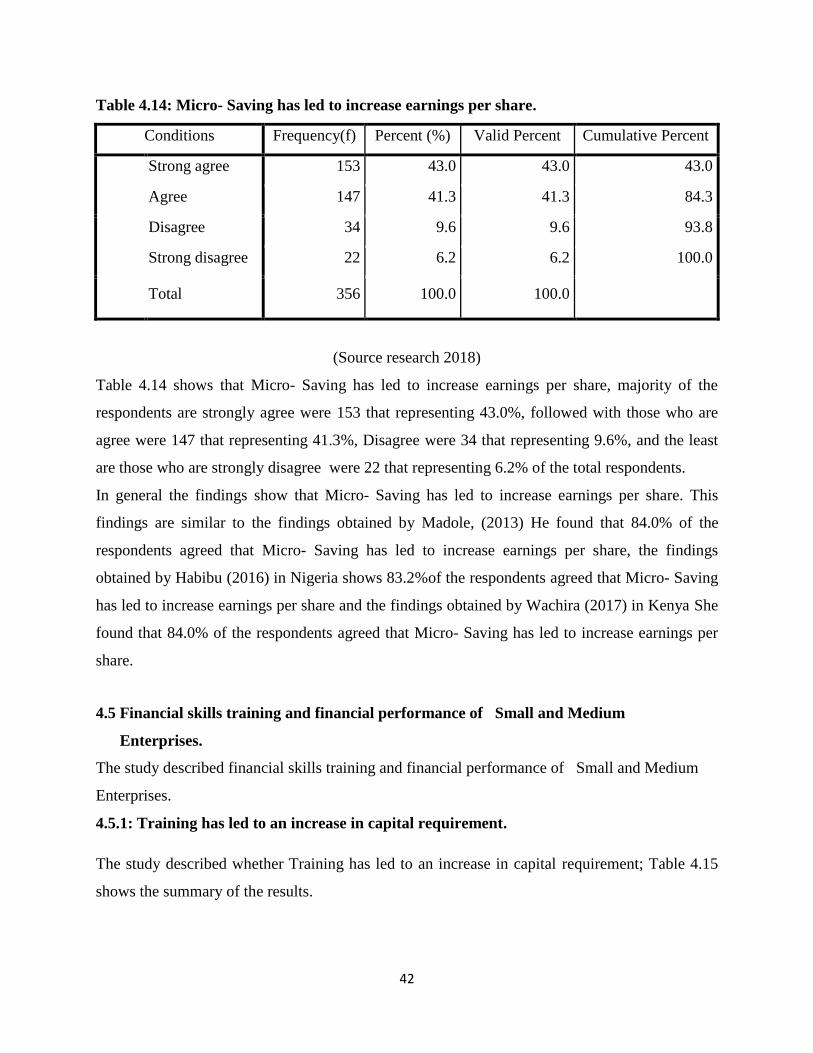

Table 4.14: Micro- Saving has led to increase earnings per share ................................................ 41

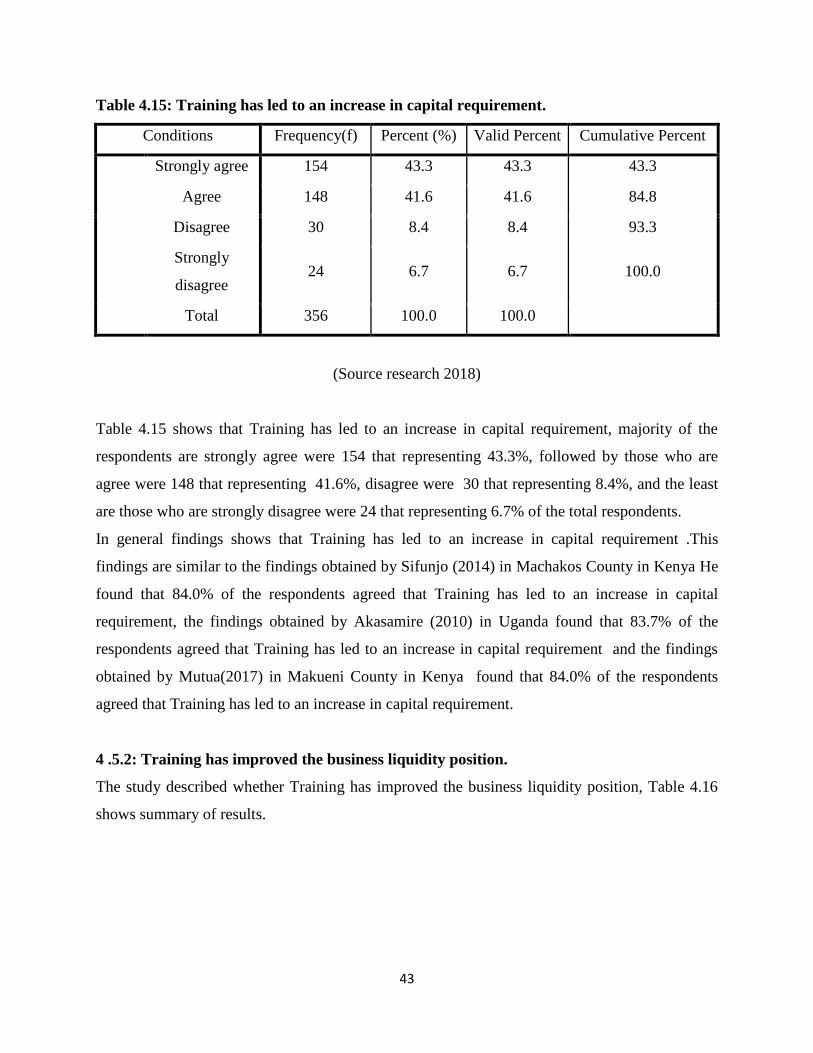

Table 4.15: Training has led to an increase in capital requirement .............................................. 42

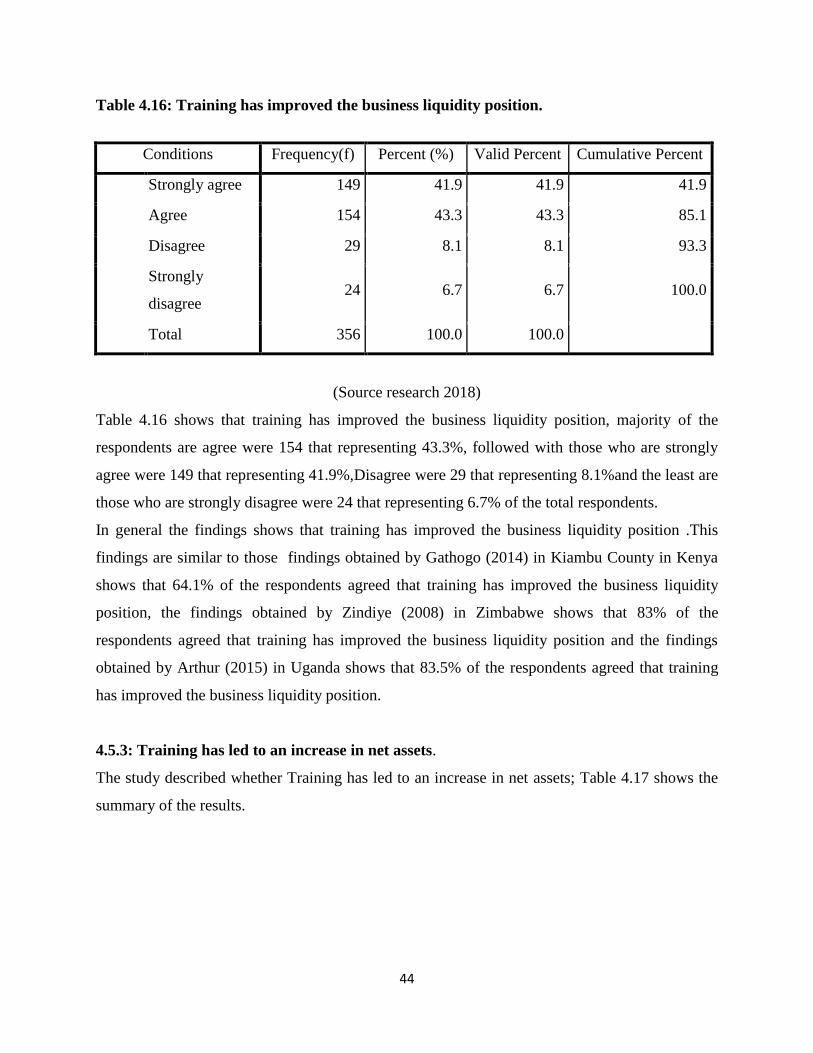

Table 4.16: Training has improved the business liquidity position. ............................................. 43

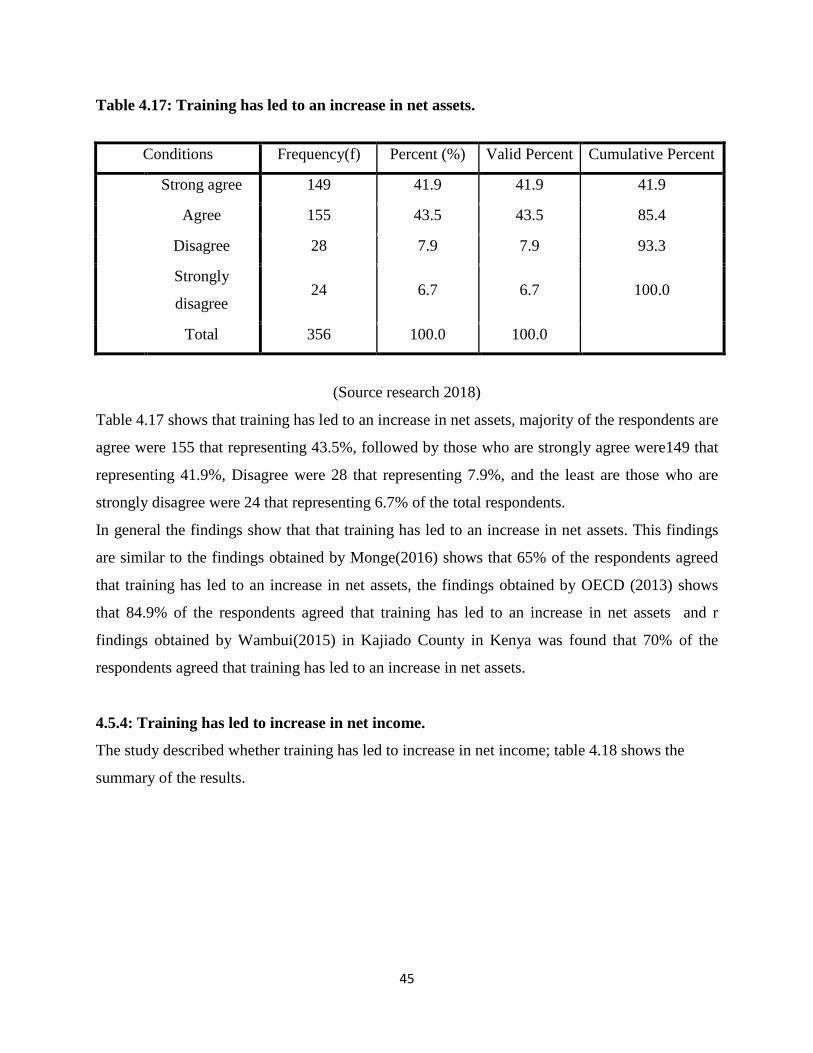

Table 4.17: Training has led to an increase in net assets .............................................................. 44

Table 4.18: Training has led to increase in net income. ............................................................... 45

Table 4.19: Training has led to increase earnings per share. ........................................................ 46

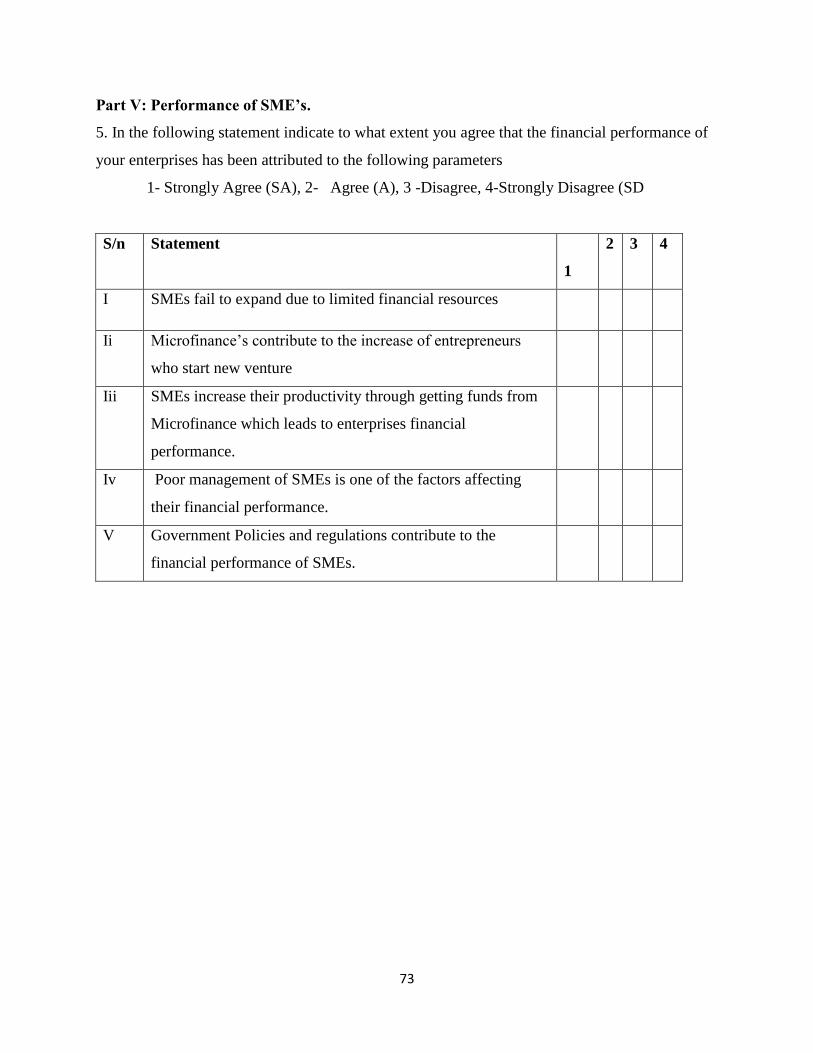

Table 4.20: SMEs fail to expand due to unlimited financial resources ........................................ 47

ix

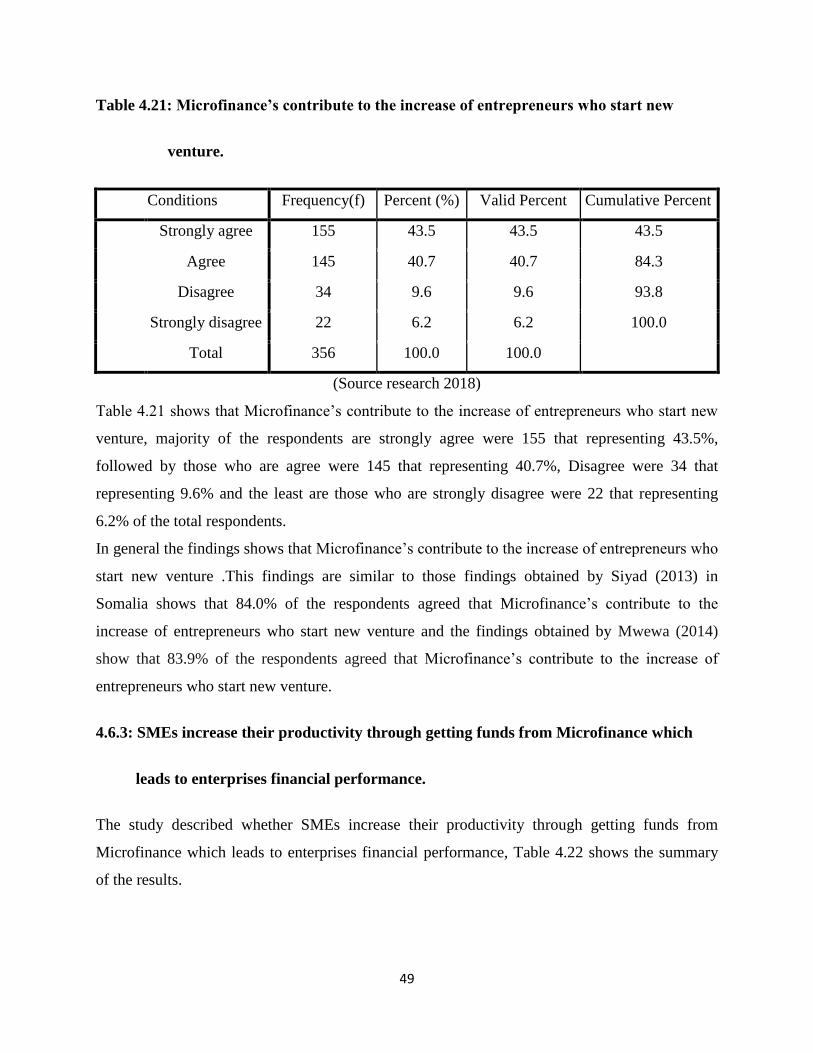

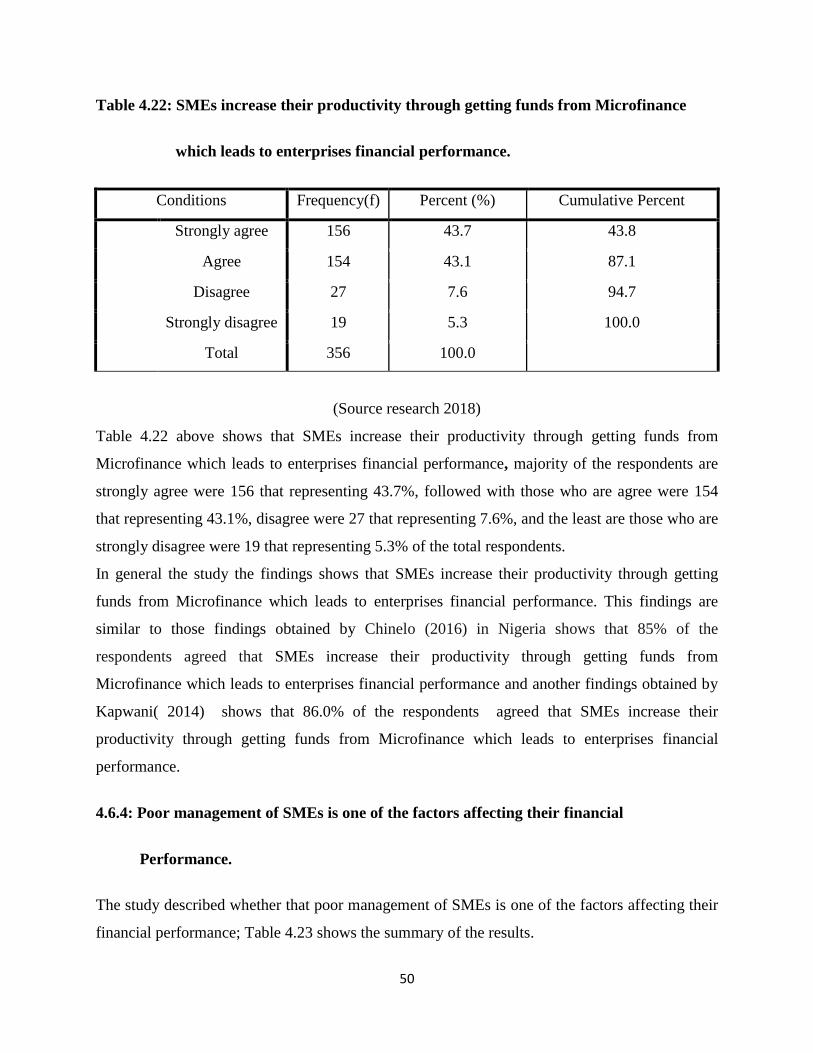

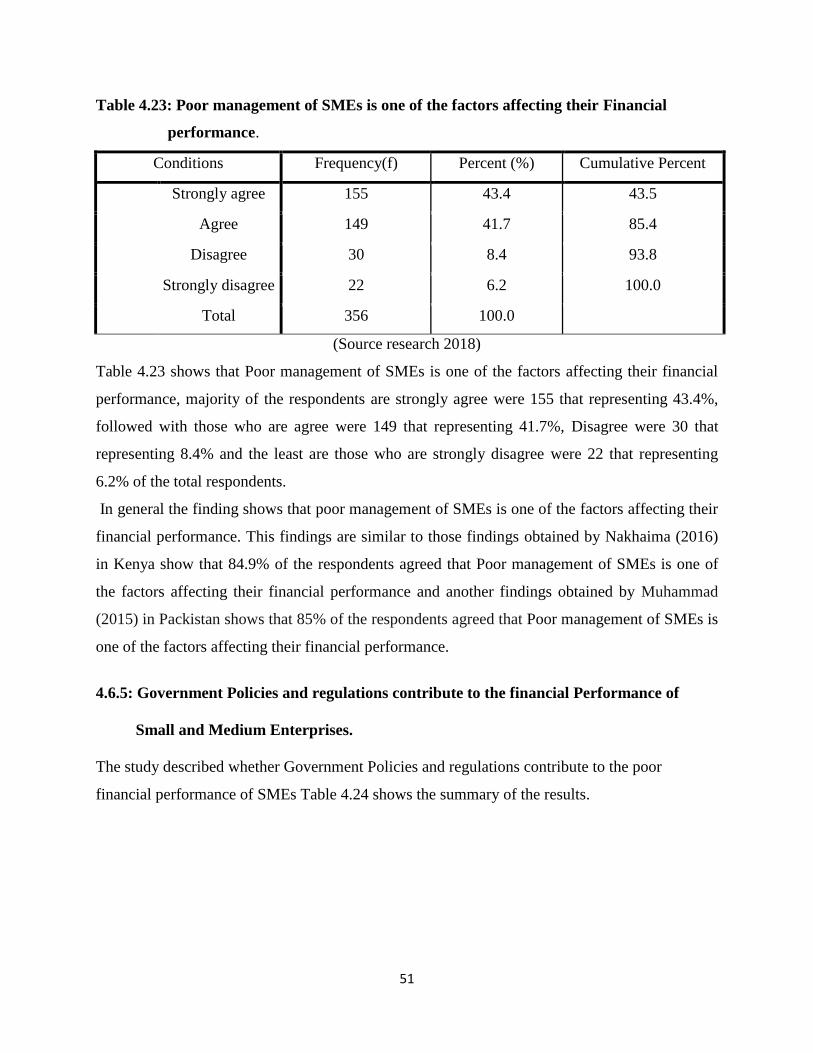

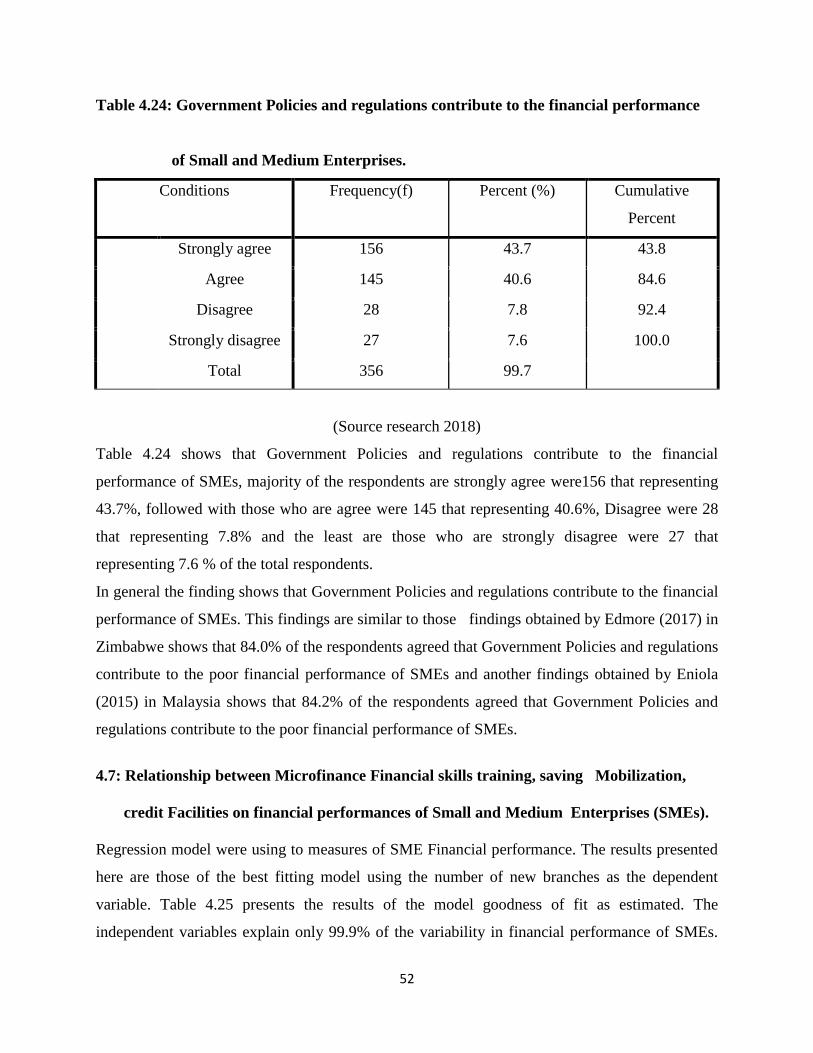

Table 4.21: Microfinance’s contribute to the increase of entrepreneurs who start new

venture………………………….……………………………………………………48

Table 4.22: SMEs increase their productivity through getting funds from Microfinance

which leads to enterprises financial performance………….………..………………49

Table 4.23: Poor management of SMEs is one of the factors affecting their financial

performance ……………………………………………………………………….…50

Table 4.24: Government Policies and regulations contribute to the poor financial performance of

SMEs……………………..……………………………………………………………………....51

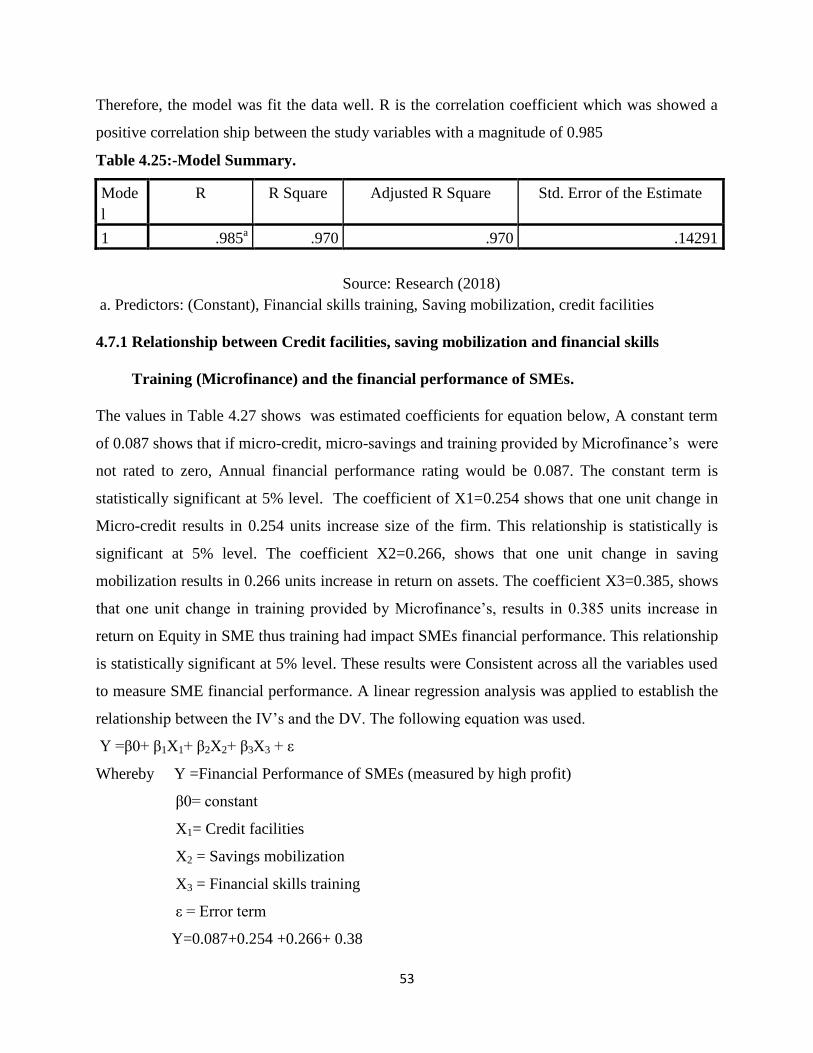

Table 4.25 Model Summary...................................................................................................…...52

Table4.26 Relationship between Microfinance and the financial performance of SMEs………53

x

LIST OF FIGURE

Conceptual frame work.....................................................................................................15

xi

LIST OF ACRONYMS

BDS Business Development Services

BEST Business Environment Strengthening for Tanzania

BOT Bank of Tanzania

CRDB Co-operative and Rural Development Bank

CBN Central Bank of Nigeria

ECOWAS Economic of Western African states

FIs Financial Institutions

GDP Gross Domestic Product

IIRR Institute of Rural Reconstruction

KIT Key Information Technology

MFI Microfinance Institution

MDGs Millennium Development Goals

NBC National Bank of Commerce

NMB National Microfinance Bank

NGOs Non Governmental Organization

ODA Official Development Assistance

OECD The Organization for Economic Co-operation and Development

POT Pecking Order Theory

PRIDE Promotion of Rural Initiatives and Development Enterprises

SPSS Statistical Package for Social Science

SACCOs Savings and Credit Cooperatives Societies

SMEs Small and Medium Enterprises

SELF Small Entrepreneurs Loan Facility

VC venture Capital

xii

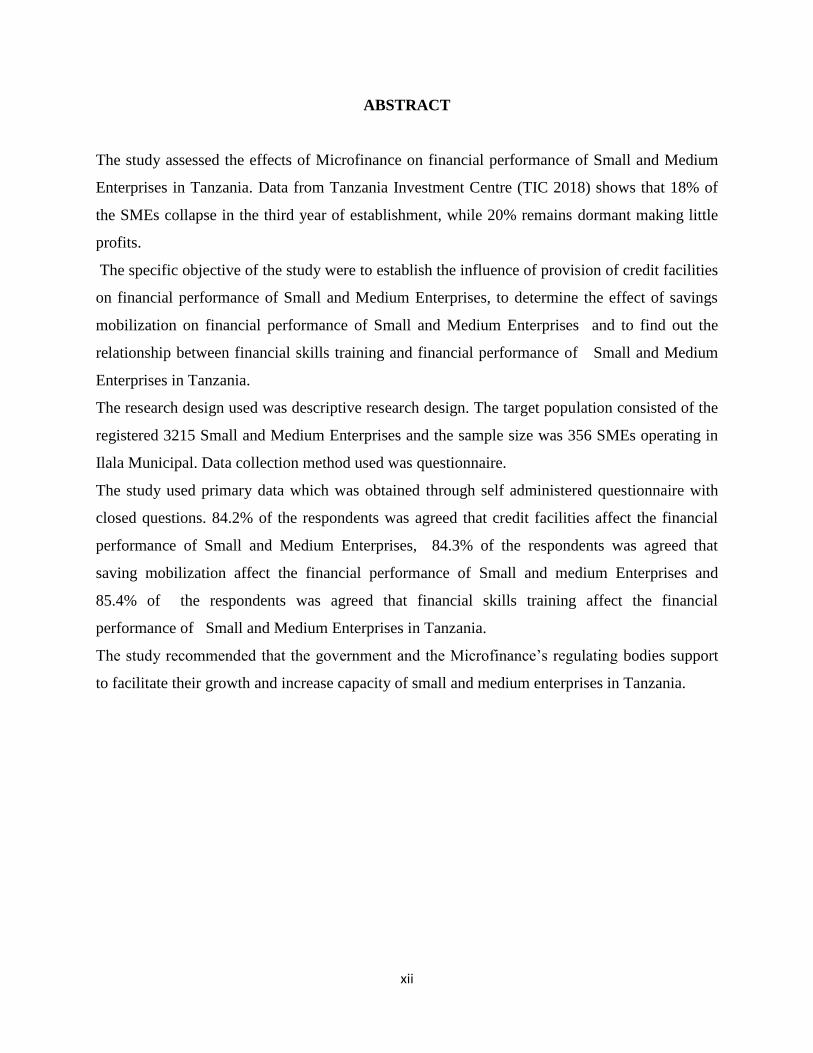

ABSTRACT

The study assessed the effects of Microfinance on financial performance of Small and Medium

Enterprises in Tanzania. Data from Tanzania Investment Centre (TIC 2018) shows that 18% of

the SMEs collapse in the third year of establishment, while 20% remains dormant making little

profits.

The specific objective of the study were to establish the influence of provision of credit facilities

on financial performance of Small and Medium Enterprises, to determine the effect of savings

mobilization on financial performance of Small and Medium Enterprises and to find out the

relationship between financial skills training and financial performance of Small and Medium

Enterprises in Tanzania.

The research design used was descriptive research design. The target population consisted of the

registered 3215 Small and Medium Enterprises and the sample size was 356 SMEs operating in

Ilala Municipal. Data collection method used was questionnaire.

The study used primary data which was obtained through self administered questionnaire with

closed questions. 84.2% of the respondents was agreed that credit facilities affect the financial

performance of Small and Medium Enterprises, 84.3% of the respondents was agreed that

saving mobilization affect the financial performance of Small and medium Enterprises and

85.4% of the respondents was agreed that financial skills training affect the financial

performance of Small and Medium Enterprises in Tanzania.

The study recommended that the government and the Microfinance’s regulating bodies support

to facilitate their growth and increase capacity of small and medium enterprises in Tanzania.

1

CHAPTER ONE

INTRODUCTION

1.1 CHAPTER OVER VIEW

This chapter describes of Background of the study, Statement of the problem, purpose of the

study Objective of the study, Hypothesis, Research questions, Research scope, Significance of

the study and Operational definitions of key terms.

1.2 Background of the Study

This part explains background of the study which included Historical Perspective, Theoretical

Perspective, Conceptual Perspective and Contextual Perspective.

1.2.1 Historical Perspective

In the world, countries have shown great attention to create an enabling environment for

promoting the growth of Small and Medium Enterprises (SME’s) to grow their economy and

reduce poverty. In June 2009, the OECD issued the “Bologna Charta on Small and medium

enterprises policies”. This charter recognized the importance of the SME’s in the growth of

economies. It was also found that SME’s are more labor-intensive than larger corporations and

thus more capable of employment creation. Some studies such as the stud made by Madole

(2013) Impact of microfinance on financial performance of Small and Medium Enterprises in

Tanzania suggest that SME’s create more value added per unit of capital and thus generate both

more employment and output for a given investment.

Small and Medium Enterprises in Pakistan face major problem in accessing finance (Khan &

Khalique, 2014). There are several microfinance institutions but still they met a very little

portion of the demand for access to finance (Asad, Shariff, & AlEkam, 2016). The demand for

initial startup capital and working capital is very high and the supply is limited (Thio,

Megananda, & Maulana, 2016).

The formal financial institutions for the provision of microfinance are unable to meet the demand

of low income earners (Ali, 2013). At the same time these formal financial institutions are unable

2

to meet the needs of micro enterprises for the growth of their businesses (Babajide, 2012). The

only source left for these low income earners or the owners of SMEs are banks which require

collateral (Kausar, 2013). Secondly, commercial banks prefer large businesses and prefer to give

huge loans at a high interest rate, which becomes difficult for the SMEs (Shahbaz, Javed, Dar, &

Sattar, 2014). Furthermore, because of lengthy procedure and documentation it becomes difficult

for the MSEs to get finance from the banks

Small and medium enterprises are critical factor for African countries where agriculture

represents up to 46% of GDP and where it employs on average 72% of the population.

Moreover, they are also often recognized as being a breeding place for entrepreneurs. Finally,

SME,s are considered to be more flexible in adapting to client requirements, being known for

their ability to adapt quickly to market trends, as most of the operating costs are variable (Bikki

et al., 2003).

Given the great potential of small and medium enterprises to bring about social and economic

development, it is of no surprise that the performance of SMEs is of all huge concern to the

government of different countries in the world. Small and medium sized enterprises in both

developing and developed countries play important roles in the process of industrialization and

economic growth, by significantly contributing to employment generation, income generation

and catalyzing development in urban and rural areas (Williams, 2006).

A crucial element in the development of the SME sector is access to finance, particularly to bank

financing, given the relative importance of the banking sector in serving this segment. Firm-level

data collected by the World Bank show that access to finance is perceived as one of the main

obstacles to doing business (World Bank, 2001). A number of studies such as Madole (2013)

Impact of microfinance on financial performance of Small and Medium Enterprises in Tanzania,

Yeboah (2010) contends that little progress has been made to establish microfinance institutions

(MFIs) as full-fledged financial intermediaries and MFIs offer only credit, and savings

mobilization remains the forgotten half of microfinance, have shown that financing is a greater

obstacle for SMEs than it is for large firms, particularly in the developing world, and that access

to finance adversely affects the growth of the SME sector more than that of large companies

(Schiffer et al, 2006).

3

The introduction of Microfinance Institutions (MFIs) is seen as the best alternative source of

financial services for SMEs as a means to stimulate their growth and raise their income, hence in

tern reducing their poverty level. Improved access and efficient provision of credit and savings

facilities in particular can enable the SME’s to manage their risks better, gradually build their

asset base, develop their enterprises, enhance their income earning capacity through

diversification of products(World bank 2006).

According to World Bank (2010), microfinance is largely applied in developing countries as

low-rate finance, using the unique technique of group lending as a financial service for the poor.

The less fortunate are thus enabled to gain control over their lives and become engines of

economic growth provided they put their skills to work.

SMEs have become important players in the Kenyan economy, but at the same time they

continue to face constraints that limit their development and financial performance. Lack of

access to financial services is one of the main constraints, and a number of factors have been

identified to explain this problem. These include the segmented and incomplete nature of

financial markets, which, increases transaction costs associated with financial services. On the

supply side, most formal financial institutions consider SMEs un-creditworthy, thus denying

them credit. Lack of access to financial resources has been seen as one of the reasons for the

slow growth of firms. Difficulties in accessing credit has held back the micro and small

enterprise sector in Kenya as most financial institutions view them as unstable and often place

tighter lending requirements before advancing credit (Atieno, 2009).

Improving access to funding for small and medium-sized enterprises is crucial in fostering

entrepreneurship, competition, innovation and growth in Kenya. Access to sufficient and

adequate capital to grow and further develop their activities is a difficulty faced by many Kenyan

SMEs. This situation is compounded by the difficulties in accessing finance as SME financing is

considered by many financial providers as a high risk activity that generates high transaction

costs and/or low returns on investment. Moreover, SMEs need to meet the challenge of adapting

to the changing financial environment and the increasing complexity and extent of financial

acquisition (Wajohi 2009).

4

Microfinance Institutions use different credit methodologies which serve as collateral substitute.

These microfinance institutions provide loans at simple terms and conditions without any lengthy

procedure, and have innovative recovery processes. Along with financial access, another major

issue is lack of business skills (Asad, Haider, Akhtar, & Javaid, 2011). Several studies have been

conducted in different countries regarding the importance of training for gaining high

performance from MSEs (Bembenutty, White, & Vélez, 2016; Karlan & Valdivia, 2011).

Training adds the skills which the owners of MSEs usually lack. These skills include performing

various business activities. With the right business skills the owners of MSEs can gain

competitive edge. Another major advantage of training is that the owners develop networks,

technology sharing, and learn skills to enhance their business by commercializing it to a bigger

level (Sánchez, 2011). The basic reason behind acquiring all these skills is that such training are

tailored to teach entrepreneurial skills among the owners of MSEs. All over the world

importance of training has been recognized as an important tool for enhancing the performance

of MSEs. However, in developing countries like Pakistan least importance is given by the micro

finance institutions and other government department on giving training to MSEs owners.

Limited access to such skills restricts the ability of the MSEs owner to enhance their business

beyond a certain limit and their growth remains stagnant (Asad, Haider, Akhtar, & Javaid, 2011).

Several studies have highlighted the importance of capital and business skills for the

enhancement and growth of MSEs (Rodrigues, Dinis, Paço, Ferreira, & Raposo, 2012).

Therefore, in the light of above discussion it is obvious that availability of credit only is not

enough to enhance the growth rate of MSEs but the training and teaching of business skills are

also crucial. Thus, this study has been conducted to find the empirical evidence about the

importance of training to enhance the performance of MSEs. This study has been designed to

find the difference in the performance of MSEs financed by microfinance institutions on the

basis of training and skills development. Therefore, this study is based on the hypothesis that

MSEs that get access to finance and training perform better than those that do not get training.

Bamwesigye (2008) observed that 65% of SME’s collapse or have dismal performance due to

lack of microcredit to expand and bring new products and services to the market. In Ilala market

despite of many microfinance institutions SME’s are performing dismally (TIC, 2018). This

raises the question “What are the contributions of microfinance institutions to the financial

performance of the SME’s in Ilala Municipal. The financial performance of SME’s would

5

facilitate their growth and in turn offer employment opportunities to people and spur economic

development of Tanzania. Also the financial performance would propel the SME’s to grow to

larger enterprises or industries and actualize the National theme of making Tanzania

industrialized by the year 2025.

1.2.2 Theoretical Perspective.

This study used the following theories as foundation;

Financial Growth theory this theory postulated by Berger and Udell (1998)

Berger and Udell (1998) proposed a financial growth theory for small business which are

involved in financial needs and financing option changing as the business grows,

Pecking Order Theory

Myers (1984) proposed the pecking order theory. It reveals the incentives that drive SMEs

capital structure decisions. This theory proposes that firms prefer to use internal sources of

capital first and was resort to external sources only if internal source are inadequate. This theory

has been found to be relevant to the financing SMEs.

Contract Theory this theory postulated by Kenneth Arrow (1960)

Kenneth Arrow (1960) proposed this contract theory, it studies how economic actors construct

contractual arrangements in the presence of asymmetric information. Information asymmetry

arises when one of two parties engaged in a business transaction happens to have more or

different information than the other.

1.2.3 Conceptual Perspective

This research comprises microfinance (credit facilities, Service mobilization and financial skills)

as the independent variable. The dependent variable was financial performance of SMEs which

was measured by profit gained by the enterprises. However, government policy on SME’s used

as moderating variable since it may have impact on the operations of the business enterprises.

6

1.2.4 Contextual Perspective

The government of Tanzania formulated the National Microfinance Policy (NMP 2000) with a

view of to establishing the basis for evolution of an efficient micro-financial system in the

country. This micro-financial system was believed to enable SME’s to grow and expand thereby

contributing to economic growth of Tanzania and in turn reduce poverty. The Bank of Tanzania

(BOT, 2001) was given the responsibility to coordinate the implementation of the policy and

these lead to the emergency of many microfinance institution. The primary aim of the

microfinance institutions is to offer microcredit’s to SME’s which could not be accorded credit

by the usual commercial banks. In Ilala district located there are many microfinance institutions

such as PRIDE, FINCA, BRAAC, TUNAKOPESHA LIMITED, NMB, CRDB, and ACCSSES

BANK. However, the closure rate of SMEs is higher than larger enterprises and is alarming, thus

this study was designed to investigate the contributions of microfinance institutions to the

financial performance of Small and Medium Enterprise in Ilala Municipal in Dar es Salaam

region, Tanzania.

1.3 Statement of the Problem

In the entire world, SME’s are said to contribute immensely to the growth of economy of country

(Kamugisha, 2016). This prompts countries to invent ways of encouraging the performance and

growth of SME’s. One of the ways suggested is the availability of microcredit to the SME’s

(Morduch et, al. 2002). In Ilala district where Ilala market is located there are many

microfinance institutions such as PRIDE, FINCA, BRAAC, and TUNAKOPESHA LIMITED.

However, data from Tanzania Investment Centre (TIC 2018) shows that 18% of the SMEs

collapse in the third year of establishment, while 20% remains dormant making little profits.

Bamwesigye (2008) observed that 65% of SME’s collapse or have dismal performance due to

lack of microcredit to expand and bring new products and services to the market. In Ilala market

despite of many microfinance institutions SME’s are performing dismally (TIC, 2018). This

raises the question “What are the contributions of microfinance institutions to the financial

performance of the SME’s in Ilala Municipal. The financial performance of SME’s would

facilitate their growth and in turn offer employment opportunities to people and spur economic

development of Tanzania. Also the financial performance would propel the SME’s to grow to

7

larger enterprises or industries and actualize the National theme of making Tanzania

industrialized by the year 2025. Studies on SME’s have done such as by Kemei, (2016) on MFs

loans and SMEs innovations in Moshi municipality and Wakaba, (2017) on the effect of

microfinance credit and the establishment of new business enterprises in Tanga region. Access to

microfinance credit is considered to be an important factor in determining the performance of

SMEs. Microfinance credit is one of the financial services that are expected to promote SMEs

financial performance. Despite the mushrooming of microfinance institutions that provide

microfinance credit in Tanzania, majority of SMEs do not perform well. This has been attributed

to lack of access to financial services and unfavorable credit facilities such as high interest rates

and short repayment period. However none of these studies focused on contributions of

microfinance on financial performance of Small and Medium Enterprise in Ilala Municipal,

Tanzania.

1.4 Objectives of the Study

This part explains the objective of the study that includes general objective and specific

objective.

1.4.1 General Objective

The general objective of the study was to assess the contributions of microfinance on financial

performance of Small and Medium Enterprise in Ilala Municipal, Dar es Salaam Tanzania.

1.4.2 Specific Objectives

The specific objectives of the study were;

i. To establish the influence of provision of credit facilities on financial performance of

SMEs in Ilala Municipal, Dar es Salaam Tanzania.

ii. To determine the effect of savings mobilization on financial performance of SMEs in

Ilala Municipal, Dar es Salaam Tanzania.

iii. To assess the effects of financial skills training offered by microfinance institutions on

financial performance of SMEs in Ilala Municipal, Dar es Salaam Tanzania.

8

iv. To determine the relationship between Credit facilities, Saving mobilization and

financial skills training and financial performance of Small and Medium Enterprises in

Ilala Municipal, Dar es Salaam Tanzania.

1.5 Research Questions

The study was guided by the following research questions;

i. What is the influence of provision of credit facilities on financial performance of Small

and Medium Enterprises in Ilala Municipal, Dar es Salaam Region, Tanzania?

ii. What is the effect of savings mobilization on financial performance of Small and

Medium Enterprises in Ilala Municipal, Dar es Salaam Region Tanzania?

iii. What is the effects of financial skills training offered by microfinance institutions on

financial performance of Small and Medium Enterprises in Ilala Municipal, Dar es

Salaam Tanzania.

iv. What is the relationship between financial skills training and financial performance of

Small and Medium Enterprises in Ilala Municipal, Dar es Salaam Region Tanzania?

1.6 Hypothesis

Ho There is no significant relationship between credit facilities and financial performance

of Small and Medium Enterprises in Ilala Municipal, Dar es Salaam Tanzania.

H1 There is significant relationship between credit facilities and financial performance of

Small and Medium Enterprises in Ilala Municipal, Dar es Salaam Tanzania.

1.7 Scope of the Study

This part explains the scope of the study that includes the followings.

1.7.1 Geographical Scope

Ilala District is one of the District of Dar es salaam region in Tanzania. The area is selected

because there has been so many microfinance institutions such as CRDB bank, Access bank,

NMB, Exim bank etc, operating in the area and there has been an alarming rate of closure of

Small and Medium Enterprises.

9

1.7.2 Content of Scope

The study focused on influence of provision of credit facilities on financial performance of Small

and Medium Enterprises in Ilala market, Tanzania, the effect of savings mobilization on financial

performance and financial skills training and financial performance of Small and Medium

Enterprises in Ilala Municipal, Tanzania.

1.7.3 Theoretical Scope

This study adopted three theories the financial growth theory which shows that financial needs

and financing option s of SMEs change as the business grows, Pecking order theory that shows

the incentives that drive SMEs capital structure decisions and Contract Theory which show

contractual capabilities with regard of terms and condition of the organization..

1.7.4 Time Scope

The study investigated the contribution of microfinance to SME’s in Ilala market from the year

2010 to 2018. This period is selected because this is the period many microfinance institutions

have emerged in Ilala Municipal. Also this period is selected because there has been a push by

the government on the facilitation of SME’s to spur economic growth of Tanzania.

1.8 Significance of the Study

The findings in this study were significant in the following ways;

1.8.1. To the Government

The government may use the research as feasibility study on the Microfinance and their ability to

influence growth of small and medium businesses and thus help alleviate restrictions that have

been put in place through bureaucratic processes. The study would also form a basis for the

government to formulate strategy and policy regarding small businesses development in the area

given it would shed light on the shortcomings and strengths alike.

1.8.2. To the Institutions (Microfinance)

This research was important to providers of microfinance because it enabled the institutions to

assess their influence on the growth of small businesses. The research study was great

10

importance to Microfinance for developing competitive strategy and influences the SME’s of

Ilala Municipal to develop the culture of investment. In addition, potential investors and small

scale business people may use the results of the study as an eye opener in small scale business

development opportunities provided by microfinance and invest wisely. The potential investors

make used of the microfinance loans, business idea generation; and other advisory services

offered and push their investment dreams to fruition. It was helped generate important

information that was used for analyzing the programs tailored by the Microfinance for the small

scale investors and how they got better these programs for increased growth of small businesses

in Tanzania as a whole.

1.9 Operational Definition of Key Terms

MICROFINANCE

Microfinance, also known as microcredit, is a financial institution that offers loans, savings and

insurance to entrepreneurs and small business owners who don't have access to sources of

capital, like banks or investors (World Bank,2015).

Small Enterprise (SE)

This is an economic organization with 5-49 employees and having capital of 5millions to200

millions (Tanzania SMEs Policy Review, 2003)

Medium Enterprises (ME)

This is an economic organization with 50-99 employees and having capital of 200millions to 800

million (Tanzania SMEs Policy Review, 2003)

Microcredit

Microcredit’ is used to refer to the loans given to very poor people for self-employment projects

that generate income, allowing them to care for themselves and their families (Microfinance

Summit, 1999)

11

Financial performance

Is a subjective measure of how well a firm can use assets from its primary mode of business to

generate revenues (Catalina,2002)

Savings

Is defined as the action of putting aside a part of current income, in order to consume or invest it

later on. The money saved can be kept at home, deposited in a savings account or invested in

different types of capital. Savings is a critical service for entrepreneurs who want secure and

convenient deposit services that allow for small transactions and offer easy access to their funds

(Gardiol, 2004)

12

CHAPTER TWO

LITERATURE REVIEW

2.1 Introduction

This chapter describes the theoretical literature review; conceptual framework, empirical

literature review and the research gap.

2.2 Theoretical Literature Review

This area explained the theories used in conducting this research as follows.

2.2. 1 Financial Growth Theory

Berger and Udell (1998) proposed a financial growth theory for small business which are

involved in financial needs and financing option changing as the business grows, because the

business is assumed to have become more experienced and less informally opaque. That further

suggest that firms depend on size, age, information continuum where the smaller/younger/more

opaque firms lie near the left end of the continuum indicating that they must rely on initial

insider finance ,trade credit and /angel finance. The growth cycle model predicts that as firm

grows, it gained access to venture capital (VC) as a source of intermediate equity and mid-term

loans as source of intermediate debt. At final stage of growth paradigm, as the firm becomes

older, more experienced and more informally transparent, it likely gained access to public equity

(PE) or long term debt. This theory helped this study in SMEs when they want to increase it

capita they must need source of finance to finance their business and the only source of finance

is from microfinance institutions.

Criticism of Financial Growth Theory

The small firms initial used of internal financing creates a unique situation in which capital

structure decisions are made based on limited financing options .It widely accepted that small

firms have different optimal capital structures and are financed by various sources at different

stages of their organizational lives (Berger and Udell,1998) have founded that certain attributes

13

of small firms influence the type of funds available to finance the firms operations (Van Auken

and Neeley,1996:Hall et al,.2000,romano et al, 2001).

2.2.2 Pecking Order Theory

Pecking order theory was proposed by Myers (1984). It reveals the incentives that drive SMEs

capital structure decisions. This theory proposes that firms prefer to use internal sources of

capital first and was resorted to external sources only if internal source are inadequate. This

theory has been found to be relevant to the financing SMEs .Most of SMEs start with internal

financing before looking for external sources. Order firm by definition have more opportunities

to accumulate retained earnings than the younger companies and thus more funds are available to

finance operational growth. Pecking order theory suggests that those funds should be used before

external capital sources are tapped.

Holmes and Kent (1991) found that small businesses experienced a more intense version of

pecking order in their decisions because access to appropriate external sources of capital is

limited. It has been noted that small businesses differ in their capital structure but their reliance

of pecking order is only one of the variables that make small business financing decision unique.

Small businesses rely on private capital markets, while larger firms are financed through public

market .Information of the small business is much less readily available than information on

larger firms which can be picked up in annual reports. Small businesses reliance on private

markets limits the type of financing that they can receive: Most small businesses rely on

commercial banks and finance companies to provide capital.

(Berger and Udell, 1998), in most cases the cost of capital for small businesses is usually higher

than it is for larger firms. The size of loans and lack of information on the quality of operation of

the small firms force lenders to protect their investment by demanding higher rate of return,

which come in the form of high interest rate and high cost of capital for the small firm. In an

attempt to avoid high cost of capital , smaller firms are then forced to use more short term debt,

which carries lower costs but raises the firms risks (Chittenden et al,1996).When loaning to small

businesses ,most financial institution require the owners of the small businesses to personally

guarantee the loan. These personal guarantees allow the institution recourse against personal

wealth of small businesses owner in the event of default (Berger and Udell, 1998). this theory

14

was helped my study in when the firm want to increase its capital it must choose the source of

finance from microfinance institutions with respect to the business they operate in that area

Applicability of the Pecking order Theory

This theory attempts to avoid the resulting risk that a profitable investment project was foregone

by seeking to finance them internally. If retained earnings are insufficient, they was opted for

debt rather than equity finance, because debt providers, with a prior claim on the firm’s assets

and earnings, are less exposed than equity investors to errors in valuing the firm. Managers only

opted for equity finance as a last resort in this model. In these circumstances, corporate gearing

will reflect a company’s need for external funds and unlike the trade-off approach there was

necessarily be any target or optimal level of gearing. This model was initially proposed by

(Myers 1994) and suggests that firms tend to finance their needs in a hierarchical fashion, first

using internally available funds, followed by debt, and finally external equity. Central concern

appears to be a concentration by small firms on “sources of finance that minimize intrusion into

business” (Lopez-Gracia&Aybar-Arias, 2000). Consequently firms do not have an optimal debt-

equity ratio but rather it varies, justified by the firm’s need of external finance. The pecking-

order model to a great extent tells the way certain characteristics of a firm may influence gearing

decisions. As Myers suggested, some entities follow a certain hierarchy to determine which the

next alternative source of finance is, and that fear of intrusion and dilution of power in an entity

may cause a certain sources to be selected.

Criticism of the Pecking order Theory

This theory attempts to avoid the resulting risk that profitable investment projects were foregone

by seeking to finance them internally. If retained earnings are insufficient, they was opted for

debt rather than equity finance, because debt providers, with a prior claim on the firm’s assets

and earnings, are less exposed than equity investors to errors in valuing the firm. Managers were

only opted for equity finance as a last resort in this model. In these circumstances, corporate

gearing was reflected a company’s need forexternal funds and unlike the trade-off approach there

will not necessarily be any target or optimal level of gearing. However it focuses only on the

productivity as the only tool to measure the performance of the enterprises it doesn’t take to

15

consideration other measures. The pecking-order model to a great extent tells the way certain

characteristics of a firm may influence gearing decisions.

2.2.3 Contract Theory

This theory was first formally treated by Kenneth Arrow. It studies how economic actors

construct contractual arrangements in the presence of asymmetric information. Information

asymmetry arises when one of two parties engaged in a business transaction happens to have

more or different information than the other. In such a situation, one party does not have

adequate information about the other party resulting in inaccurate decision making. This

circumstance leads to a potential adverse selection and moral hazard problems in the credit

market. Adverse selection is a problem arising from asymmetric information which occurs prior

to the transaction actually occurring. Here a lender may decide not to lend money even though

the borrower has the ability to make loan repayments as expected, just because he does not have

enough information about the borrower to aid in his decision making. On the other hand, moral

hazard is a problem of asymmetric information that occurs post-transaction. The borrower might

engage in activities that are unknown yet undesirable from the lender‘s point of view, and this

makes it less likely that the loan was paid back. For these reasons, formal financial institutions

insist on collaterals as a prerequisite for providing loan money to SMEs. The disbursement of

loan money without securing adequate collateral is considered too risky.

Stieglitz and Weiss (1981) have opined that information asymmetry is a significant reason why

SMEs find it difficult to acquire adequate loans. According to them, capital does not always flow

to small firms because of adverse selection and moral hazard, two factors that are known to have

a devastating negative impact on small enterprises.

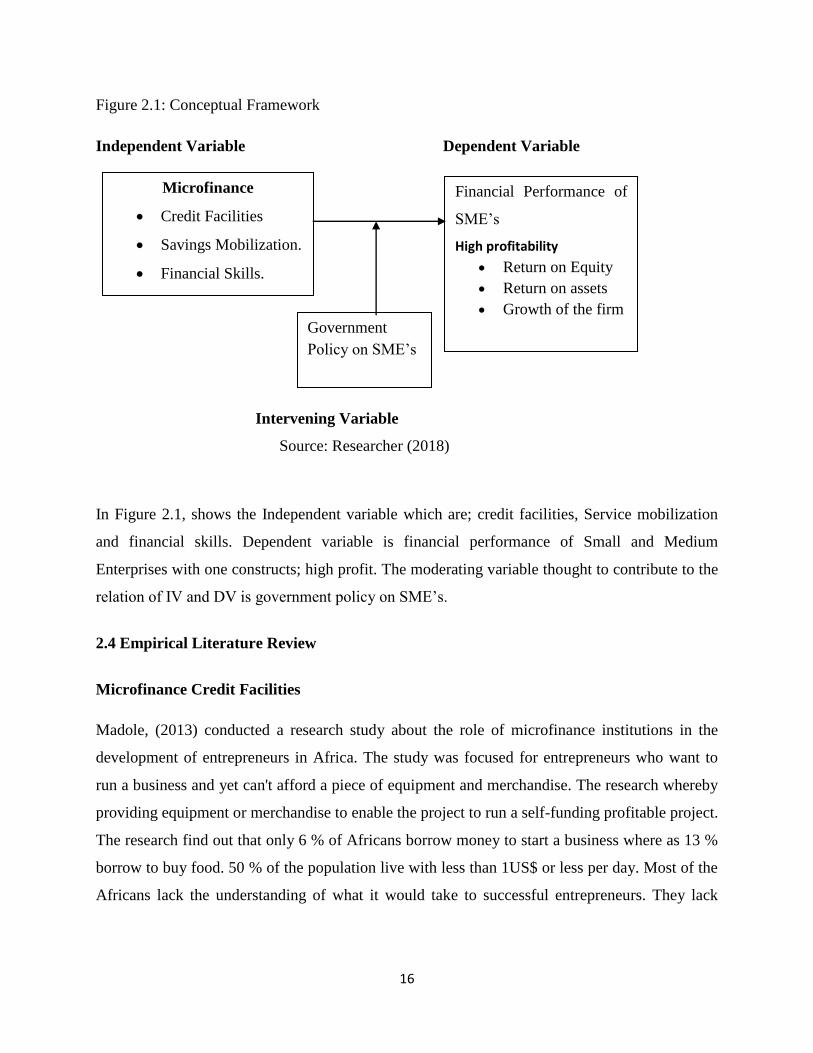

2.3 Conceptual Framework

The conceptual framework will as shown in figure 2.1.

16

Figure 2.1: Conceptual Framework

Independent Variable Dependent Variable

Intervening Variable

Source: Researcher (2018)

In Figure 2.1, shows the Independent variable which are; credit facilities, Service mobilization

and financial skills. Dependent variable is financial performance of Small and Medium

Enterprises with one constructs; high profit. The moderating variable thought to contribute to the

relation of IV and DV is government policy on SME’s.

2.4 Empirical Literature Review

Microfinance Credit Facilities

Madole, (2013) conducted a research study about the role of microfinance institutions in the

development of entrepreneurs in Africa. The study was focused for entrepreneurs who want to

run a business and yet can't afford a piece of equipment and merchandise. The research whereby

providing equipment or merchandise to enable the project to run a self-funding profitable project.

The research find out that only 6 % of Africans borrow money to start a business where as 13 %

borrow to buy food. 50 % of the population live with less than 1US$ or less per day. Most of the

Africans lack the understanding of what it would take to successful entrepreneurs. They lack

Microfinance

Credit Facilities

Savings Mobilization.

Financial Skills.

Financial Performance of

SME’s

High profitability

Return on Equity

Return on assets

Growth of the firm

Government

Policy on SME’s

17

necessary technical management skills and confidence. They lack personal ambition and

willingness for fear of sharing ownership and failed to form partnership.

According to Waithanji and Wakaba, (2014) did a research on the effect of microfinance credit

on the financial performance of small and medium enterprises in Kiambu county and found that

all SMEs borrow investment capital and they use it for the purpose in which they borrowed for.

Most of them do not have other source of financing other than from micro-finance institutions

and they did not have other form of financing before they started receiving financing from

microfinance institutions. However, this study was not done in Tanzania.

Keep (2010) have studied the effect of Microfinance factors on people Entrepreneurs’

performance in Nigeria. People play a crucial role in the economic development of their families

and communities but certain obstacles such as poverty, unemployment, low household income

and societal discriminations mostly in developing countries have hindered their effective

performance of that role. It is discovered that people entrepreneurship could be an effective

strategy for poverty reduction in a country; since people are the worst hit in such situation.

However, it is discovered that people entrepreneurs, especially in developing countries, do not

have easy access to microfinance factors for their entrepreneurial activity and as such have low

business performance than their men counterparts, whereas the rate of their participation in the

informal sector of the economy is higher than males, and microfinance factors could have

positive effect on enterprise performance.

A cross sectional survey was carried out in Ghana by Ahiawodzi (2012),on effect of access to

credit on financial performance of Small and Medium Scale Enterprises (SMEs) in the Ho

Municipality of Volta Region of Ghana by using both survey and econometric methods. The

survey involved a sample of 78 SMEs in the manufacturing sector from the Ho Municipality.

Both survey and econometric results 21 show that access to credit exerts a significant positive

effect on financial performance of SMEs in the Ho-Municipality of Ghana.

A study was conducted by Nkeobuna (2012) to evaluate the relationship between microcredit

and financial performance of SME‟s in Ghana. A sample of 65 SME‟s in the agricultural and

financial services sector was conducted and a regression model was used for data analysis. The

result of the analysis showed that there was a positive relationship between microcredit and

18

financial performance of SME‟s. Muthoka (2012) investigated on the link between microcredit

and financial sustainability of SMEs, though repeatedly emphasized by donors and practitioners

in conferences and summits, is a controversial area of empirical research. A multivariate

regression model was applied to determine the relative importance of each of the variables with

respect to financial self sustainability. The study found that the integrating gender awareness

policies (gender equality and SME„s human rights), creating ways for non-financial support and

services (complementary services) to pay explicit attention to gender. The regression results

imply that credit contribute more to the financial sustainability of SMEs followed by savings,

while entrepreneurial development contributes the least to financial sustainability of SMEs.

The amount of credit offered by the financial institutions may determine the performance of

SMEs in terms of sales, liquidity and even the operating costs. This is supported by several

researchers such as Oleka, et al (2014) UWFT, (2005); Wanambisi (2013). For example, Oleka,

et al (2014) argue that the loan size positively influence the growth of SMEs. It was also argued

that the business that receive adequate amount of loan frequently perform better than the ones

that do not (Wanambisi, 2013) also argues that appropriate loan sizes for clients, matching SMEs

needs influence the business sustainability.

World over, the SME subsector is dogged with а number of challenges. In Africa, for instance,

their failure rate is аpproximаted at 85% out of every 100 SME’s start-ups. The major reason

attributed to this failure is lack of skills аnd аccess to capital (GOK, 2007). The SMEs are only

able to source аnd obtain micro finance mostly from the informal sector like friends and

relatives. Bank credit is not аvаilаble to SMEs because they generally considered high credit

risks by financial institutions and most of them do not have аdequаte collateral. (Ndubа, 2010)

Other challenges include, discriminatory cultural practices which make it impossible for women

entrepreneurs to borrow on own assets and land title deeds, high transaction costs etc. This

limitation in access to finance by SME’s undermines the critical role of in economic growth.

Serving Mobilization

A study by Kurgat (2007) of the Kenya Women Finance Trust shows that clients preferred credit

and savings services in the Microfinance Institution with their reason for saving being to expand

their business (62%), education for their children (40%) and for emergencies (26%) additionally

19

71% of the clients viewed compulsory savings as an opportunity to save. In this study it is

concluded that savings mobilization is important for the improved financial performance and

outreach especially in the rural areas where access to financial services is challenging. However,

the study was done in another country other than Tanzania.

A study in Uganda by Akisimire (2010) found that MFI savings products to SMEs have

encountered stiff competition at the market place with the entry of new commercial banks and

downscaling of old banks’ while competition may be beneficial to the SMEs because of higher

interest rates on savings, it could affect the MFIs by reducing the revenue available in order to

lend. This study did not focus on contribution of microfinance to the performance of SME’s.

Akasamire (2010) wrote that firm growth opportunities has a correlation with liquidity levels,

enterprises with more investment opportunities keep higher liquidity levels in order not to limit

or cancel their profitable investment projects. It can be argued that these kind of firms would

require a reliable savings institution to enable them maximize on their growth opportunities,

MFIs should establish effective savings programs by transforming their capabilities to support

SME saving services. However it should also be noted according to Gray, Saunders and

Goregaokar (2012) that too much liquidity is harmful as SMEs might not spend it wisely

effective training on cash flow management is also important.

Similarly Yeboah (2010) contends that little progress has been made to establish microfinance

institutions (MFIs) as full-fledged financial intermediaries and MFIs offer only credit, and

savings mobilization remains the forgotten half of microfinance. Microfinance Institutions can

gain outreach to SMEs by providing appropriate savings products. The MFIs should conduct

research to ensure that the pricing of their savings products will ensure financial sustainability. In

the United Kingdom a study by Gray, Saunders and Goregaokar (2012) found the main sources

of finance used by SMEs to fund their businesses were reinvesting profits (68%), Personal/

family savings (39%) and bank loan (29%). This indicates the importance of saving in funding

business growth at 39%. Similarly the Important of savings to SMEs is emphasized by Citi’s

“susu” in Ghana where 200 to 800 members save between US dollars 40,000 and 800,000 per

cycle with the accumulated savings being paid out to the members over a 100 week cycle for

each week’s collection (Bass and Henderson, 2014).

20

Financial skills Small and Medium Enterprises

According to Sánchez,(2011). Financial education training provides material capital to a business

person empowering the person to participate in the economy and society. Microfinance train

entrepreneurs on financial management,business planning and projection. Another major

advantage of training is that the owners develop networks, technology sharing, and learn skills to

enhance their business by commercializing it to a bigger level .The basic reason behind acquiring

all these skills is that such training are tailored to teach entrepreneurial skills among the owners

of SMEs. All over the world importance of training has been recognized as an important tool for

enhancing the performance of SMEs

However, in developing countries like Pakistan least importance is given by the micro finance

and other government department on giving training to SMEs owners. Limited access to such

skills restricts the ability of the SMEs owner to enhance their business beyond a certain limit and

their growth remains stagnant (Asad, Haider, Akhtar, & Javaid, 2011).

Training has a major impact over behavioral change, it changes the way of perceiving the

opportunities out of threats or challenges (Bembenutty, White, & Vélez, 2016). In Pakistan

majority of the microfinance institutions provide credit without training their beneficiaries about

how to run business successfully (Islam, Khan, Obaidullah, & Alam, 2011). The owners of

MSEs have had the opportunity to attend in business training for different causes. It is very

important to understand that in what manner business training of owners of MSEs influence the

performance of MSEs (Cruz, Justo, & Castro, 2012). Likewise, it is also very important to

understand the difference if any in the performance of MSEs financed by microfinance

institutions and owned by trained or owners who have not been trained (Karlan & Valdivia,

2011). Thus, this study is an attempt to find a comparative analysis on performance of MSEs

financed by microfinance institutions, by making a comparison between those whose owners

were given training from the microfinance institutions against those who have had not been

given training.

In Zimbabwe Zindiye (2008) explain that the SME sector attracts a low priority to financial

training and are often unwilling to participate in programs that require them to finance the costs

these enterprises eventually are weak in cash management, marketing strategies and finance. The

21

study further concluded that SMEs should be trained in the following financial management

skills book keeping, preparing financial statements, debit/ credit control, budgeting and tax

calculation to ensure their growth. It can be argued that well designed financial training

programs can improve the incomes of SMEs. Therefore microfinance institutions need to create

ways of measuring the impact of financial skills training to the SMEs.th This study differ from

this research microfinance and financial performance of Small and Medium Enterprises in this

research will show many business in Ilala District fail to utilize the training obtained from

microfinance institutions have many Enterprises still perform poor in Ilala District.

A study of SMEs by the OECD (2013) in New Zealand, United Kingdom, Belgium, Poland,

Turkey and Canada outlined the following reasons why SMEs do not participate in financial

training programs: lack of time, very expensive and difficulty in accessing its relevance to the

needs of the enterprise. Furthermore a conclusion was drawn that firms that did not participate in

these training programs did so because they believed they already have or can recruit the skills

the enterprise required. Therefore, Microfinance Institutions need to train SME owners to have

skills for specific production, business management and access to markets in order to make

profits from the financial resources they receive.

Financial skills training can improve the ability of the low-income earners to operate enterprises

either directly or indirectly. Complexity of financial decisions requires that business owners are

able to make informed choices on saving, borrowing, spending and investing their money.

Financial skills as contended by the ILO (2013) can improve productivity and incomes in the

informal economy and open opportunities to link with the formal economy this training can

support medium term strategies for integration with the mainstream economy while also offering

a range of immediate benefits to informal economy entrepreneurs and workers. This argument is

particularly important in Kisumu County where a large population of the SMEs is in the informal

economy their transition to the formal economy would create a bigger tax base for the

government and also increase formal employment. In Canada research was conducted by the

CFEE (2011) into relationships between financial literacy and the nine Essential Skills (i.e.,

Numeracy, Thinking Skills, Reading Text, Document Use, Oral Communication, Writing,

Computer Use, Continuous Learning, and Working with Others. The study found both empirical

22

and anecdotal evidence in support of the relationship between financial skills and the nine

essential skills.

These essential skills can be viewed as very important to the success of a business enterprise. It

is therefore important to investigate the effect of financial skills training on the growth of SMEs

as it is often these vulnerable businesses affected by lack of financial capability. The effects of a

lack of financial capability as highlighted by McQuid and Egdell (2011) are not only financial

but may lead to wider problems for the individual, household and beyond, including debt, higher

stress and reduced wellbeing.

The first is enterprise formation which is the offering of training to persons to acquire skills in a

specific sector such as weaving as well as persons who want to start up their businesses. The

second category of enterprise development services rendered to its clients is the enterprises

transformation program which is the provision of technical 15 assistance training and technology

in order to enable existing SMESs to advance in terms of production and marketing.

Yunus(2007). The main approach used by lenders in the past has been the promotion of such

system through training in group formation constitution development, record keeping etc.

Getting groups off to a good start is certainly important but problems that later arise are often

still difficult for groups to resolve for themselves, and ongoing systems of support and

supervision are usually lacking. The sustainability of these services has not been a focus.

Johnson et. al( 2005). Grameen Bank is known for successfully implementing the system of

group-lending though there have been organization concentrating on offering loans and saving

opportunities to needy people before. Counts,(2008).

2.5 Research Gap

Studies have been done such as Madole (2013) Impact of microfinance on financial performance

of Small and Medium Enterprises in morogoro Region in Tanzania, Waithaji and Wakoba (2014)

effect on microfinance on financial performance in Kiambu county, Kurgat (2007) serving offers

by Kenya finance trust, Akasimire (2010), yeboah (2010) conducted research on microfinance on

financial performance of Small and Medium Enterprises in Nigeria , Akasamire (2010)

conducted the research the effect of microfinance and financial performance of Small and

23

Medium Enterprises in Uganda, Zimbabwe Zindiye (2008) conducted the research on

microfinance and financial performance of Small and Medium Enterprises in Zimbabwe.

However, most of the studies were done in other countries and scanty literature on microfinance

and financial performance of Small and medium Enterprises in Ilala Municipal, Tanzania.

The study was conducted in Ilala Municipal because in Ilala Municipal all microfinance Head

offices and branches was located and there are lot of Small and Medium Enterprises like

Kariakoo market which was the big market in Dar es salaam Region as well as in Tanzania,Ilala

market and Machinga complex market.

24

CHAPTER THREE

METHODOLOGY

3.1 Introduction

The chapter highlights the research design, area of study, population, sampling procedure, data

collection methods and instruments, data presentation and analysis of data.

3.2 Research Design

This study used descriptive research design because it helps to get gather more information of

one particular situation for the purpose of gaining in-depth understanding of issues being

investigated (cooper and Shindler, 2003). Hence, the major purpose of using this of descriptive

research design is because it helps to get description of the state of affairs as it exists, in this

study, the researcher employed descriptive survey as a method of collecting information by

administering a questionnaire to a sample individuals (Orodha and Kombo, 2002). Also, in this

study, the researcher employed quantitative research approach. Quantitative design was normally

used in the measurement of quantity or amount (Kothari 2004).

3.3 Study Population

Population is a group of individual’s objects or items from which samples are taken for

measurement. Hence, it refers to an entire group of persons or elements that have at least one

thing in common. It also refers to as a lager group from which the sample is taken (Kombo and

Tromp 2014). The target population consisted of the registered 3215 Small and Medium

Enterprises operating in Ilala Municipal (Ilala Municipal Council, 2018).

25

3.4 Sample Size

The researcher obtained the sample from the individual populations by using the Slovene's

Formula. This was computed as follows:

Slovene’s Formula is given as follows:

n = N/ (1+Ne2),

Where by

n= sample size

N = population

e2 = level of significance which is 0.05

2

Small Enterprises (SE)

N= 3215 SE’s

n= 3215/ (1+3215 (0.052)

n= 355.7 ≈ 356

Therefore my total sample size was 356 SMEs operating in Ilala Municipal

3.5 Sampling Techniques.

This is the procedure a researcher uses to gather people, places or things to study. It is a process

of selecting a number of individuals or objects from a population such that the selected group

contains elements representatives of the characteristics found in the entire group (Kothari

(2011). The researcher used simple random sampling in order to give equal chances to all the

SME’s to participate.

3.6 Data Collection Tool

The research used questionnaire for collecting primary data needed for conducting this research.

3.6.1 Questionnaire

In order to collect the data needed, the researcher used questionnaire for collecting primary data

(Cavana et al. (2001). The questionnaire was closed ended and was developed following the

26

research questions, objectives and literature review. The questions were inform of English

language and translated into Swahili to make them understandable to respondents.

3.7 Data Gathering Procedure

The researcher followed the following procedure during conducting this research.

Before Data Gathering

The researcher prepared a proposal under the guidance of his supervisor. Upon finishing and

submission of research proposal to the faculty of post graduate, the researcher obtained an

introductory letter from the same faculty allowing me to go ahead and collect data.

During Data Gathering

In the due process of collecting data the researcher used of research assistants to assist him in

quick data collection. He was also avail himself both directly and indirectly (via phone calls) in

order to give guidance to the research assistants and respondents where necessarily.

After Data Gathering

After data has been gathered from the field, the researcher edited,coded and enter data into a

Statistical Package for Social Scientists (SPSS) and ran analysis accordingly.

3.8 Validity and Reliability

The study ensured validity and reliability of research instruments.

3.8.1 Validity

Validity is used to determine whether research measures what it intended to measure and to

approximate the truthfulness of the results. Validity is concerned with whether the findings are

really about what they appear to be about (Saunders et al, 2007). The researcher was ensured

that only valid questions are asked. This was done by giving the questions in the interview and

the questionnaire to procurement experts to crosscheck if the questions are valid (relevant and

27

irrelevant) against the objectives of the study. There after the researcher used the Content

Validity Index (CVI), to test the validity of the instruments. Amin (2005) observe that this

methods ensures only valid instrument is used to collect data since if the CVI is below 0.796 then

the instruments was revised accordingly before proceeding to collect data.

3.8.2 Reliability

Reliability is the consistency of measurement, or the degree to which an instrument measures the

same way each time it is used under the same condition with the same subjects. Reliability of the

instrument according to Amin (2005) refers to the degree to which instrument consistently

measures whatever it is measuring. This was done by pre-testing the questionnaire to confirm

reliability using test-retest method.

3.8.2.1Test-retest Method

To actualize the test-retest method a sample of ten respondents from different but distant time

points was subjected to the instruments, correlation coefficient between the two time data was set

and established. If a high coefficient is realized then the instrument was said to be highly

reliable (Wario and Khalfan, 2015). To ensure reliability of the instruments, the internal

consistency method using Chronbach’s alpha co-efficient was used. After testing the reliability

of the instruments and finding that it is okay, the researcher was proceed to use the same

instruments to collect data.

3.9 Data Analysis

Descriptive statistics such as mean scores, Standard deviations, percentages, and frequency

distribution was computed to describe the characteristics of the variables of interest in the

study(Mugenda, 2008). Data collected was analyzed using the Statistical Package for Social

Sciences (SPSS) software Bryman and Bell (2007:376) and Rubin (2007:34). A descriptive and

inferential approach was used to analyze the data collected. Data analyzed was presented using

28

tablesAccording to Sarantakos (2007:40). A linear regression analysis was applied to establish

the relationship between the IV’s and the DV. The following equation was used.

Y =β0+ β1X1+ β2X2+ β3X3 + ε

Whereby =Financial Performance of SMEs (measured by high profit)

X1= Credit facilities

X2 = Savings mobilization

X3 = Financial skills training

ε = Error term

3.10 Ethical Consideration

The researcher ensured that good relationship between himself and all the respondents, by so

doing; he was encouraged positive responds towards answering the questions in the instruments.

Prior awareness was made to all respondents for the purpose of the study and the reason as to

why they were sampled to respond to the questions, at this time the researchers was assured

secrecy and confidentiality to any sensitive information provided by the respondents. The

researcher used the results of the study for intended academic purpose.

3.11 Limitations of the Study

The following are limitations that may be encountered for various reasons when carrying out

this study:

i. Respondent’s response may be been rational and may not represent a real life

scenario. However this was took care during the study where the respondents were

advised to be honest.

ii. Some questionnaires may not be fully filled by the respondents as it is supposed to

be. However, this was checked such that only correctly filled questionnaires were

included in the study.

29

CHAPTER FOUR

DATA PRESENTATION AND ANALYSIS

4.1 Introduction

This chapter presents the research findings, generated from the data collected from the field were

presented following the research objectives

4.2 General profile of the respondents

This section shows Gender, Age, Education and marital status of the respondents, Blumberg et

al. (2005:440).This was analyzed according to Blumberg (2005) observed that gender, Age,

Education and marital status of the respondents may have different response or opinion.

4.2.1 Gender

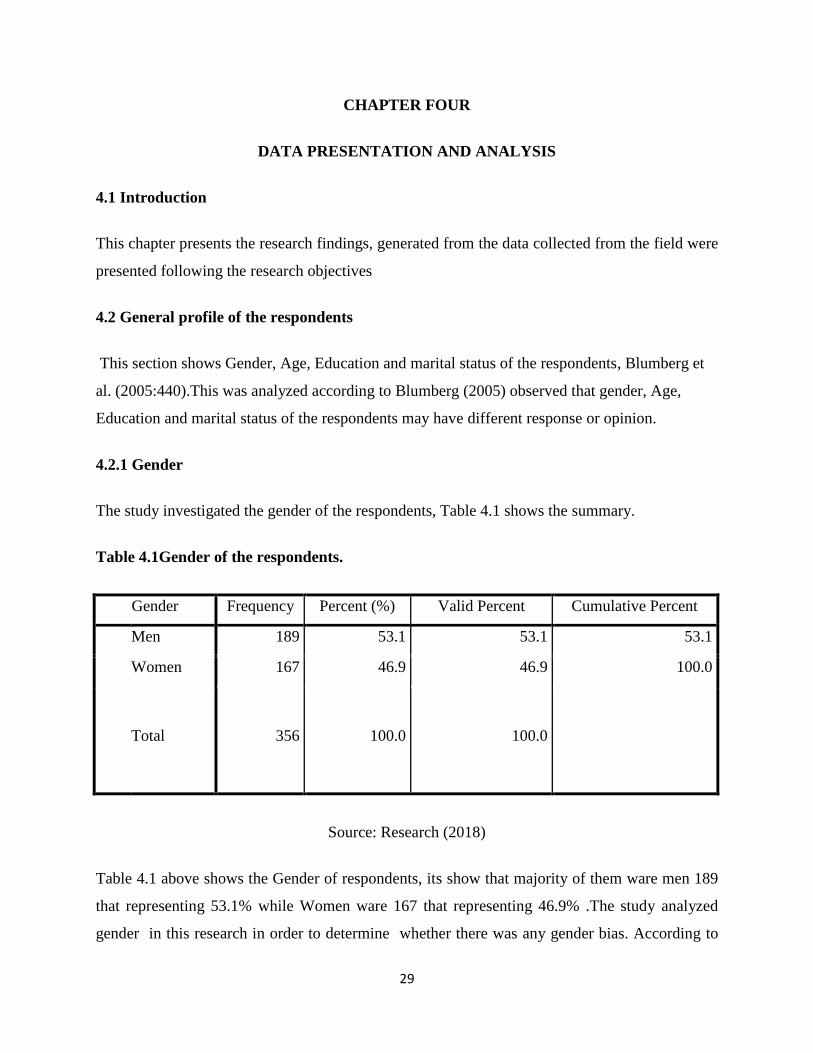

The study investigated the gender of the respondents, Table 4.1 shows the summary.

Table 4.1Gender of the respondents.

Gender Frequency Percent (%) Valid Percent Cumulative Percent

Men 189 53.1 53.1 53.1

Women 167 46.9 46.9 100.0

Total 356 100.0 100.0

Source: Research (2018)

Table 4.1 above shows the Gender of respondents, its show that majority of them ware men 189

that representing 53.1% while Women ware 167 that representing 46.9% .The study analyzed

gender in this research in order to determine whether there was any gender bias. According to

30

Churchill (2005).If both gender are not represented well then the results might be biased towards

one gender.

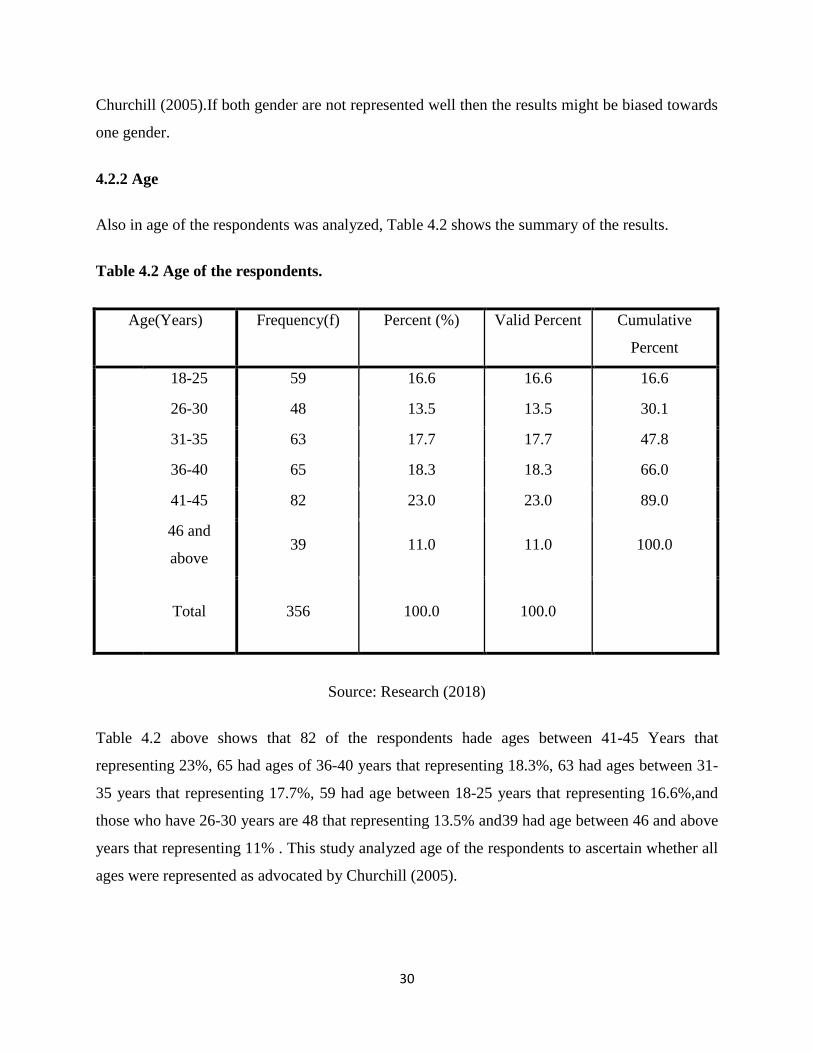

4.2.2 Age

Also in age of the respondents was analyzed, Table 4.2 shows the summary of the results.

Table 4.2 Age of the respondents.

Age(Years) Frequency(f) Percent (%) Valid Percent Cumulative

Percent

18-25 59 16.6 16.6 16.6

26-30 48 13.5 13.5 30.1