Embed Size (px)

Citation preview

7/31/2019 Microequities High Income Value Microcap Fund July 2012 update

http://slidepdf.com/reader/full/microequities-high-income-value-microcap-fund-july-2012-update 1/1

MICROEQUITIES ASSET MANAGEMENT |AFSL 287526 |Suite 702, 109 Pitt Street, Sydney NSW 2000

Office: +61 2 9231 6169 Fax: +61 2 9475 1156 [email protected]

JULY 2012 PERFORMANCE UPDATE by Carlos Gil, Chief Investment Officer

MARKETS AND ECONOMY:

The risk free rate is an integral part of investing for two key reasons; it is the return that a “risk free” asset provides a n

investor that wants no exposure to risk, the bird in the hand. For those investors that are willing to assume an investment

with some level of risk, it is used to calculate expected future cash flow returns from that investment and therefore are

integral to calculating intrinsic value of the investment. The lower the risk free rate the higher the value of our investments

because future expected cash flows are discounted at a lower rate. The Australian Government 10 year bond yield is

currently around 3.10%, historically low levels. This low risk free rate is pushing up the intrinsic value of our owned

businesses whilst at the same time the alternative uses of our capital remaining in cash, are paying considerably lower

returns. These conditions are occurring at a time when poor market sentiment and risk aversion has driven market pricing

down for some very good businesses, this scenario provide us with a rather obvious conclusion, we have never experienced

risk free returns as low as these, whilst, for our owned businesses the gap between market value and intrinsic value

continues to widen. In all our Funds we will continue to deploy cash and new investment inflows because we consider the

current opportunities to be highly compelling from a long term, value investment perspective.

Microequities High Income Value Microcap Fund returned a positive +5.76% versus the All Ordinaries Accumulation

Index positive +3.74% in July.

We do not believe the Fund’s current forecast grossed up dividend yield of +12.16% will be sustainable over the medium to

long term. Not because the businesses we own will lower or cease their dividend payments, but because we believe that

the market prices of some of these businesses will rise as investors reassess risk assets. Given the risk free rate stands at

3.10%, our businesses are forecast to yield a grossed up dividend income of over 900 basis points higher than the risk free

rate. Logic would suggest that the gap will tighten though admittedly the market can stay illogical for a quite some time.

The good news though, is that if the scenario does eventuate our investors will derive capital appreciation via higher

market prices.

Current Forecast Grossed Up Dividend Yield of the Fund*: +12.16%*Forecast Grossed up Yield is based on internal forecasts and actual results may vary. Investors should note that Gross Dividend Yield is not a forecast

distribution as distributions will depend on actual dividend income received and actual number of units on issue at the time a distribution is made.

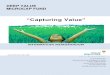

*High Income Value Microcap Portfolio as of 31st

of July

4.0%

50.9%

8.4%2.9%

8.1%

3.9%

4.7%

6.3%

6.3% 4.4% Cash

Software & Services

Consumer Durables

Apparel

Capital Goods

Media

Comercial Services &

Supplies

Diversified Financials

Retailing

Banks

Real Estate

Latest Unit Price

$1.0056Latest Fund Performance as at July 31, 2012

FUND AOAI* OP*

1 Month +5.76% +3.74% +2.02%

3 Month -0.62% -3.17% +2.55%6 Month

12 Month

Inception +3.70% -0.98% +4.68%

(Returns are calculated after all fees and expenses and

reinvestment of distributions. Inception of Fund March 1, 2012)

*AOAI: All Ordinaries Accumulation Index. *OP: Out-

performance.

Past performance is not indicative of future performance.