Embed Size (px)

Citation preview

MICHIGAN REAL ESTATE TRENDS REPORT 2013

acknowledgementstom wackerman | astI environmental | Um/UlI Real estate ForumBrittany Foley | dPoP!

david allen | msHdaBrad clard | medcJennifer Rigterink | medcJoe martin | medcBryan Robb | medcshannon sclafani | UlI michigandon taylor | Um/UlI Real estate Forum

tom wackerman | astI environmental | Um/UlI Real estate Forum chairshannon sclafani | UlI michigandon taylor | Um/UlI Real estate ForumPeter allen | Peter allen & associates | University of michiganmargaret dewar | University of michiganwilliam watch | First commercial Realty | UlI michigan chair

Jamie simchik | simchik Planning and development | student coordinatorBenjamin levitt chip koziara Yang lin aaron desatnik Jared kessel alexander schapira Paige shesterkin Brian wackerman

aUtHoRs

data commIttee

Um/UlI Real estate FoRUm

execUtIve BoaRd

stUdent InteRvIeweRs

special thanks to medc and msHda for sharing state wide statistics, to all online survey respondents and individual interviewees for participating in this first annual event, and to the michigan Real estate club at the University of michigan for providing the student volunteers.

Brad Clark

MHSDA

acknowledgementstom wackerman | astI environmental | Um/UlI Real estate ForumBrittany Foley | dPoP!

david allen | msHdaBrad clard | medcJennifer Rigterink | medcJoe martin | medcBryan Robb | medcshannon sclafani | UlI michigandon taylor | Um/UlI Real estate Forum

tom wackerman | astI environmental | Um/UlI Real estate Forum chairshannon sclafani | UlI michigandon taylor | Um/UlI Real estate ForumPeter allen | Peter allen & associates | University of michiganmargaret dewar | University of michiganwilliam watch | First commercial Realty | UlI michigan chair

Jamie simchik | simchik Planning and development | student coordinatorBenjamin levitt chip koziara Yang lin aaron desatnik Jared kessel alexander schapira Paige shesterkin Brian wackerman

aUtHoRs

data commIttee

Um/UlI Real estate FoRUm

execUtIve BoaRd

stUdent InteRvIeweRs

special thanks to medc and msHda for sharing state wide statistics, to all online survey respondents and individual interviewees for participating in this first annual event, and to the michigan Real estate club at the University of michigan for providing the student volunteers.

acknowledgementstom wackerman | astI environmental | Um/UlI Real estate ForumBrittany Foley | dPoP!

david allen | msHdaBrad clard | medcJennifer Rigterink | medcJoe martin | medcBryan Robb | medcshannon sclafani | UlI michigandon taylor | Um/UlI Real estate Forum

tom wackerman | astI environmental | Um/UlI Real estate Forum chairshannon sclafani | UlI michigandon taylor | Um/UlI Real estate ForumPeter allen | Peter allen & associates | University of michiganmargaret dewar | University of michiganwilliam watch | First commercial Realty | UlI michigan chair

Jamie simchik | simchik Planning and development | student coordinatorBenjamin levitt chip koziara Yang lin aaron desatnik Jared kessel alexander schapira Paige shesterkin Brian wackerman

aUtHoRs

data commIttee

Um/UlI Real estate FoRUm

execUtIve BoaRd

stUdent InteRvIeweRs

special thanks to medc and msHda for sharing state wide statistics, to all online survey respondents and individual interviewees for participating in this first annual event, and to the michigan Real estate club at the University of michigan for providing the student volunteers.

acknowledgementstom wackerman | astI environmental | Um/UlI Real estate ForumBrittany Foley | dPoP!

david allen | msHdaBrad clard | medcJennifer Rigterink | medcJoe martin | medcBryan Robb | medcshannon sclafani | UlI michigandon taylor | Um/UlI Real estate Forum

tom wackerman | astI environmental | Um/UlI Real estate Forum chairshannon sclafani | UlI michigandon taylor | Um/UlI Real estate ForumPeter allen | Peter allen & associates | University of michiganmargaret dewar | University of michiganwilliam watch | First commercial Realty | UlI michigan chair

Jamie simchik | simchik Planning and development | student coordinatorBenjamin levitt chip koziara Yang lin aaron desatnik Jared kessel alexander schapira Paige shesterkin Brian wackerman

aUtHoRs

data commIttee

Um/UlI Real estate FoRUm

execUtIve BoaRd

stUdent InteRvIeweRs

special thanks to medc and msHda for sharing state wide statistics, to all online survey respondents and individual interviewees for participating in this first annual event, and to the michigan Real estate club at the University of michigan for providing the student volunteers.

acknowledgementstom wackerman | astI environmental | Um/UlI Real estate ForumBrittany Foley | dPoP!

david allen | msHdaBrad clard | medcJennifer Rigterink | medcJoe martin | medcBryan Robb | medcshannon sclafani | UlI michigandon taylor | Um/UlI Real estate Forum

tom wackerman | astI environmental | Um/UlI Real estate Forum chairshannon sclafani | UlI michigandon taylor | Um/UlI Real estate ForumPeter allen | Peter allen & associates | University of michiganmargaret dewar | University of michiganwilliam watch | First commercial Realty | UlI michigan chair

Jamie simchik | simchik Planning and development | student coordinatorBenjamin levitt chip koziara Yang lin aaron desatnik Jared kessel alexander schapira Paige shesterkin Brian wackerman

aUtHoRs

data commIttee

Um/UlI Real estate FoRUm

execUtIve BoaRd

stUdent InteRvIeweRs

special thanks to medc and msHda for sharing state wide statistics, to all online survey respondents and individual interviewees for participating in this first annual event, and to the michigan Real estate club at the University of michigan for providing the student volunteers.

INTRODUCTION

Although sometimes described as a single market, the Michigan real estate market consists of many diverse and unique development opportunities. To provide a forum for describing and analyzing those opportunities, The UM/ULI Real Estate Forum [“the Forum”] and the Urban Land Institute [ULI] Michigan District Council developed this first annual Michigan Real Estate Trends Report to identify and compare real estate trends across the state. The report focuses on the major metropolitan areas in the state, but is intended to represent state-wide trends. The objective of this report is to supplement the annual National ULI Emerging Trends Report by focusing on local markets. The National ULI Emerging Trends Report is a tremendous resource and historical perspective on national economic and real estate trends, and is presented each year at the Forum.

However, it does not focus on smaller and local markets, markets which comprise most of the real estate activity in Michigan. More importantly, it appears to have undervalued the Michigan market, and Detroit in particular, in recent years. This report was prepared from a combination of an online survey and interviews with real estate professional in the private and public sectors. The information includes quantitative data from the surveys and quote from the interviews and survey comments.

This year, 62 responses to the survey were collected. Professional service firms made up the majority of the responses [27%], which seems to be a trend among similar state real estate reports, but there were good responses from private developers [19%], government [18%], brokerage [14%], and property managers [14%]. Almost half of the respondents developed residential real estate [46%], and a third were business owners [33%].

TOM WACKERMANCHAIR | UM/ULI REAL ESTATE FORUM

BY JOB

33%

18%18%

15%

8%6%

2%OWNER

ASSOCIATE

DIRECTOR

PRESIDENTCEO

OTHER

VPCOO | CFO

BY CATEGORY

25%

21%14%

13%

13%

8%6%

RESIDENTIALRENTAL

RESIDENTIALFOR SALE

OFFICE

RETAIL

INDUSTRIAL

LAND

INST./PUBLIC

BY SECTOR

27%

19%18%

14%

4%

2%2%

14%PROPERTYMANAGEMENT

UNIVERSITY

BUILDER

BROKERAGE

GOVERNMENTPRIVATEDEVELOPER

PROFESSIONALSERVICES

INST. INVESTOR

CONTENTS

BACKGROUND

[JOB GROWTH] 1

3BACKGROUND [HOUSING

+ POPULAITON]

5BUSINESS PROSPECTS IN

MICHIGAN

9TRENDS BY SECTOR

13TRENDS IN CAP RATE

15TRENDS IN CAPITAL

MARKETS

17TRENDS IN SUBMARKETS

22IMPEDIMENTS

PAGE1

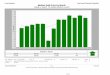

BACKGROUNDJOB GROWTH

t is no news to anyone that real estate is affected by general economic conditions around the state. Although a review of state-wide economic trends is beyond

12345

67

8910

$ 1

0,0

00

$ 2

0,0

00

$ 3

0,0

00

$ 4

0,0

00

$ 5

0,0

00

$ 6

0,0

00

$ 7

0,0

00

JOBS BY REGION

10,0

00

20,0

00

30

,00

0

40

,00

0

50,0

00

60

,00

0

70,0

00

NU

MB

ER

OF

JO

BS

AV

ER

AG

E W

AG

E

Ithe scope of this report, the following indicators provide insight into the real estate sector in Michigan and its various regions. These indicators are based on the ten economic development regions as indicated on the map.

One measure of the health of the real estate market is job growth in the construction and real estate sectors. As can be expected, jobs in those sectors are concentrated in the most populous regions, particularly Regions 10 and 4. Real estate jobs across the state are expected to decline

slightly from 2013 to 2018 [-2.77%] with the greatest negative changes in Regions 3, 6, and 10. Real estate jobs in Regions 1 and 5 are expected to grow during the same period.

A recently released document from the Research Seminar in Quantitative Economics entitled “Some highlights from the most recent RSQE Michigan forecast, released on October 8, 2013” states that “The top job producers over the next two years are: professional and business services; trade, transportation, and utilities; and construction.”

Earnings for these real estate related jobs are somewhat related to market size, with Regions 10, 9, and 4 having the highest earnings. However, Region 1 shows earnings higher than would be expected by its relatively low number of construction jobs. This may indicate the influence of non-construction/real estate work falling under a listed NAICS code.

PAGE2

1

2 3

45

6

7

8 9

10

8% 4% 8% 7%4% 2% 1% 6%

CHANGES IN JOBS BY REGION | 2013 - 2018, % CHANGE

1 2 3 4 5 6 7 8 9 10

0% 0%

PAGE3

"We have turned the corner. Net population is expected to increase over the next couple of decades which will be a huge story for real estate."

There is some indication of improvement in the economic condition of the state over the past two years, specifically in employment and population growth.

Other indicators, such as household income and owner occupation, are still negative, but with some signs of a slowdown in the decline. However, the change in the number of households and housing units have both trended negative with declines over the past two years after growth in the previous five years. The ten regions show mixed improvements, or at least reductions in declines. Employment improved for all regions except 1 and 5 over the

last two years, after devastating declines the previous five years. Regions 2, 4, 7 and 9 had increases in population over the last two years, but the positive change was less than decline of the previous five years.

Regions 3 and 10 have had consistent population loss over the past 12 years. But with the increase in state-wide population, this not just migration between regions.

Change in household income have been negative for the past 12 years for all regions, but the rate of decline is substantially less over the last two years for all regions except Region 1.

BACKGROUNDHOUSING + POPULATION

210-1-2-3-4-5-6-7-8-9-10-11-12

POPULATIONHOUSEHOLD

INCOMEOWNER

OCCUPATIONHOUSEHOLDS

STATEWIDE CHANGES [% CHANGE]

2000-2005

2005-2010

2010-2012

PAGE41 2 3 4 5 6 7 8 9 10REGION 1 2 3 4 5 6 7 8 9 10REGION

2000-

2005

2010 -

2012

2005-

2010

0%

-2%

-4%

-6%

-8%

-10%

-12%

-14%

-16%

HOUSEHOLD INCOME

3%

2%

1%

0%

-1%

-2%

-3%

-4%

-5%

OWNER OCCUPATION

RE

GIO

NA

L C

HA

NG

ES

| H

OU

SIN

G

-8%

8%

6%

4%

2%

0%

-2%

-4%

-6%

POPULATION

HOUSEHOLDS6%

4%

2%

0%

-2%

-4%

-6%

-8%

10%

8%

6%

4%

2%

0%

-2%

HOUSING UNITS

RE

GIO

NA

L C

HA

NG

ES

| P

OP

UL

AT

ION

-20%

20%

15%

10%

5%

0%

-5%

-10%

-15%

EMPLOYMENT

PAGE5

BUSINESS PROSPECTS IN MICHIGAN

hen asked to look forward and predict business conditions, respondents all expect their own business sector to do

Not surprisingly, new commercial development and homebuilding ranked at the bottom of the list, each just barely above a good performance.

Comparing Michigan to other markets provides only a slightly different perspective. Overall, all sectors expect to do somewhat better in Michigan in 2014 than they would elsewhere, without a clear difference between the segments.

General construction and investment lead the list, with real estate services being a little less enthusiastic. Homebuilding is anticipated to have a stronger year in Michigan compared to elsewhere—possibly a comment on how far home prices actually fell, as well as real economic recovery in the sector. Commercial new development and land development round out the list middle-of-the-road scores each.

“This is a long term test for development.”

“We are seeing 16 million units in domestic sales. Haven’t seen that since ‘06.”

“Prices have risen substantially within the last 12-15 months, attributable to substantial decline in

inventory.”

Wsomewhat better in 2014 than 2013 and to do even better in 2015. They generally feel that Michigan is a good place to continue to do business, expecting their business to do somewhat better here than they would elsewhere.

All sectors expect business to be fair in 2014. Leading the list is real estate services, which may suggest an expectation of improvement across all segments. This is followed closely by a fair year in general construction, investment and multi-family new development.

PAGE6

2014 BUSINESS PROSPECTS | BY INDUSTRY

BUSINESS PROSPECTS VS. OTHER MARKETS | BY TYPE

ABYSMALPOOR

GOODFAIR

EXCELLENT

GENERAL CONSTRUCTION [3.76]REAL ESTATE SERVICES [3.93]

REAL ESTATE INVESTMENT [3.73]

MULTI-FAMILY NEW DEVELOPMENT [3.71]

FINANCING AS A LENDER [3.68]

LAND DEVELOPMENT [3.51]

COMMERCIAL NEW DEVELOPMENT [3.49]

HOMEBUILDING [3.43]

GENERAL CONSTRUCTION

REAL ESTATE INVESTMENT

REAL ESTATE SERVICES

MULTI-FAMILY NEW DEVELOPMENT

FINANCING AS A LENDER

HOME BUILDING

COMMERCIAL NEW DEVELOPMENT

LAND DEVELOPMENT

3.94

3.90

3.84

3.84

3.74

3.61

3.60

3.50

MUCH BETTER

SAME

MUCH WORSE

AVG

1

2

3

4

5

5

3

1

PAGE7

When looking at market segments, respondents predict that overall Michigan markets should produce slightly better business prospects than the same segment elsewhere.

When asked “How would you expect to rate the business prospects for Michigan in 2014 compared to other markets?” the responses ranged from about the same [land] to somewhat better [residential rental]. The lowest ranking for land development may reflect the backlog of existing buildings still in the pipeline.

Respondents indicated that the residential, industrial, and hospitality segments are most likely to perform as well as or somewhat better than the same segments in other markets,

BUSINESS PROSPECTS VS. OTHER MARKETS | BY SECTOR

All other segments will remain about the same, with slightly better business prospects in Michigan than elsewhere, an indication of a renewed optimism amongst Michigan developers and investors, especially when compared to the past few years, or maybe an indicate that things have reached bottom.

“There has been modest growth in a variety of areas, but

there has been growth.”

"We will continue to struggle against markets on the coasts"

RESIDENTIAL | RENTAL

INDUSTRIAL

HOSPITALITY

RESIDENTIAL | FOR SALE

RETAIL

INSTITUTION / PUBLIC

OFFICE

LAND

MUCH BETTER

SAME

MUCH WORSE

AVG

3.69

3.53

3.46

3.40

3.36

3.31

3.06

2.93

5

3

1

PAGE8

Profitability in 2014 is predicted to be good to fair for the business categories surveyed.

Builders were the most optimistic in 2014, followed by brokers and professional service, who expect profitability to be fair. All other categories expect good results.

In addition to surveying respondents on expected 2014 profitability, responses were requested for 2015. By 2015 all categories expect improvement

2014 + 2015 BUSINESS PROFITABILITY | BY CATEGORY

5.04.03.02.01.0

ABYSMAL POOR GOOD FAIR EXCELLENT

in profitability, except for builders who continue to see prospects as good, with brokerages increasing expectations to excellent in 2015.

The greatest expected change in profitability ratings between 2014 and 2015 is for the professional services [+ 16%] while brokers expect to see the highest overall likelihood of profitability by 2015. Builders, who enjoy the highest expected profitability in 2014, experience the lowest year-over-year change as the expectations stagnate in 2015 [+ 0%].

“The perception about Michigan is hurting the reality. We need to tell a better story...emphasize quality of life and opportunity.”

1.0

5.0

3.53.8

3.3

3.5

4.0

2014 2015

3.8

4.2

3.6

4.0BUILDER

PROFESSIONAL SERVICES

BROKERAGE

PROPERTY MANAGEMENT

PRIVATE DEVELOPER

4.0

PAGE9

“Tax credit and moderate apartments can’t be built fast enough, there are huge waiting lists looking for well managed, high quality properties. As a

result many developers are reentering this market making competition fierce for the tax credits as well as private bridge and permanent financing.”

ost of the market sectors [60%)] are in recovery [averaging a score of 4.41 on a scale of 1-6]. These range from early recovery for single family lot development and home building, to advanced recovery and growth for CBD office and tax-credit apartments. The remaining sectors have bottomed out, ranging from self-storage which is very close to advanced decline, to farm land which is trending toward recovery.

TRENDS BY REAL ESTATE SECTOR

MPEAKEARLY DECLINEADVANCED DECLINEBOTTOMED OUTRECOVERYGROWTH

BUSINESS CYCLE

PAGE10

HOSPITALITY These sectors are all showing overwhelming signs of recovery. Although overwhelming in both cases, the recovery of full-service hospitality appears stronger than that of limited-service, as some respondents indicate that the latter may have peaked.

LAND Development is generally entering recovery since some respondents have reservations that it is bottoming out. Respondents are less sure about the status of farmland, where significant numbers indicate it is in advanced decline while others rank it in recovery or growth.

HOUSING All residential rental categories are clearly in recovery and growth stages. Student housing appears to be doing better than the other rental categories, as it shows the strongest signs of being in a growth stage, followed by low-income/tax-credit apartments. Only luxury apartments show any significant likelihood of being on decline.

RETAIL In retail trends converge, with regional malls, power centers, and neighborhood shopping centers having all bottomed out. Additionally, both regional malls and neighborhood centers show some indications of recovery, whereas there is no clear consensus for power centers.

REGIONAL MALL

POWER CENTERS

NEIGHBORHOOD CENTERS

RE

TAIL

HO

SPIT

ALI

TY

FULL-SERVICE LIMITED-SERVICE

STUDENTHO

USI

NG

| R

EN

TAL

LUXURY MARKET-RATE LOW-INCOME

HO

USI

NG

| FO

R S

ALE

SINGLE-FAMILY LOT DEV.

SINGLE-FAMILY HOMEBUILDING

TOWNHOME

DEVELOPMENT FARM

LAN

D

PAGE11

OFFICE CBD office is tending toward full recovery with some respondents seeing growth, while suburban office and medical office are still largely bottomed out. Overall the responses are generally optimistic for CBD office while not as confident in other forms of office space.

INDUSTRIAL General industrial is clearly in full recovery, while bulk/distribution space is tending strongly toward recovery or growth. There is no clear trend for self-storage, but it is trending toward bottoming out as a near majority of responses indicate the sector being in some stage of decline.

INSTITUTIONAL + PUBLIC Measured by expected construction activity rather than business cycle expectations, institutional and public real estate is expected to stagger. State-funded development will see the most construction activity, but that will only be slightly better than fair. At the lower end of the scale, K-12 education will see only poor-to-fair construction activity.

"Retail strip town shopping centers at about 10,000 to 15,000 square feet will have the greatest level of development activity in 2014.”

EDUCATION K-12

LOCALLY-FUNDED [RE]DEVELOPMENT

HIGHER EDUCATION

STATE-FUNDED [RE]DEVELOPMENT 3.13

3.07

2.67

2.33

INSTITUTIONAL + PUBLIC CONSTRUCTION

LOW [2.0] FAIR [3.0]

OFF

ICE

CBD SUBURBAN MEDICAL

BULK/ DISTRIBUTION

GENERALINDUSTRIAL

SELF-STORAGEIND

UST

RIA

L

PAGE12

SE

LF S

TOR

AG

E

SU

BU

RB

AN

OF

FIC

E

ME

DIC

AL

OF

FIC

E

PO

WE

R C

EN

TE

RS

NE

IGH

BO

RH

OO

D R

ETA

IL

RE

GIO

NA

L M

ALL

S

LIM

ITE

D-S

ER

VIC

E H

OT

ELS

FAR

M G

RO

UN

D

SIN

GLE

-FA

MIL

Y L

OT

DE

VE

LOP

ME

NT

SIN

GLE

-FA

MIL

Y H

OM

EB

UIL

DIN

G

LAN

D F

OR

DE

VE

LOP

ME

NT

BU

LK/D

IST

RIB

UT

ION

SPA

CE

LUX

UR

Y A

PAR

TM

EN

TS

GE

NE

RA

L IN

DU

STR

Y

STU

DE

NT

HO

US

ING

FU

LL S

ER

VIC

E H

OT

ELS

TOW

NH

OM

E/C

ON

DO

MIN

IUM

MA

RK

ET-

RA

TE

APA

RT

ME

NT

LOW

-IN

CO

ME

APA

RT

MN

ET

S

CB

D O

FF

ICE

3.6

9

3.83

3.9

2

4.0

0

4.0

0

4.0

9

4.17

4.2

7

4.3

1

4.4

4

4.4

5

4.5

3

4.5

6

4.6

4

4.8

1

4.8

3

4.8

8

4.8

8

4.9

3

5.0

0

BUSINESS CYCLES

GR

OW

TH

BO

TTO

M O

UT

AD

V. D

EC

LIN

ER

EC

OV

ER

YEA

RLY

DEC

LIN

E

AVG

PAGE13

n general, cap rates in 2013 were perceived as stable or very only slightly increasing [average 3.13 out of 5]. For these indicators the scale was 1.0 [fall] to 5.0 [increase]

TRENDS INCAP RATE

Iwith 3.0 representing stable. Respondents indicated that in general cap rates in 2014 will continue to be stable but are likely to increase more than this year in certain sectors [average 3.20].

Commercial cap rates are anticipated to remain stable-to-slightly-falling, with the exception of CBD office, where although the rate is expected to increase, it is expected to do so at a slower pace than in 2013. Suburban office is likely to become more stable next year after seeing a slight fall in 2013.

The cap rate for general industrial is expected to increase only slightly in 2014 while rates for bulk/distribution space are expected to dramatically increase before stabilizing. Cap rates in all other commercial categories are anticipated to have the same stability in 2014 as they did in 2013 or begin to fall slightly, as is particularly the case in retail.

Regional malls are expected to have a declining rate as the 2014 score averaged 2.63. Power centers closely followed at 2.75

2013

2.71 2.67

2014 2013

3.00 3.18

2014

FALL AT FASTER RATE

RISE

2013

3.33 3.25

2014

RISE BUT STABILIZING

IND

UST

RIA

L

SELF-STORAGE GENERAL BULK/DISTRIBUTION

2013

2.86 2.88

2014 2013

2.75 2.89

2014

FALL BUT STABILIZING

FALL BUT STABILIZING

2013

3.38 3.25

2014

RISE BUT STABILIZING

OFF

ICE

MEDICAL SUBURBAN CBD

2013

3.00 2.89

2014 2013

2.88 2.75

2014

FALL FALL

2013

2.71 2.63

2014

FALL

RET

AIL

NEIGHBORHOOD POWER CENTER REGIONAL MALL

2013

3.60 3.40

2014 2013

3.60 3.40

2014

RISE BUT STABILIZING

RISE BUT STABILIZING

HO

SPIT

ALI

TY

LIMITED SERVICE FULL SERVICE

5

3

1

RANGE

PAGE14

and neighborhood/community centers remained stable-to-slightly-declining at 2.89. For residential properties, all cap rates are anticipated to increase faster in 2014, from slightly to moderately.

While rental cap rates increased more than for-sale rates in 2013, for-sale residential rates are expected to increase faster than

rental residential during 2014.

The largest residential year-over-year change is excpected for single-family lot development [moving from an expected 3.00, or stable, to 3.50, or moderate increase], while the greatest rate of increase in 2014 is expected in townhouse and condominium construction [from 3.20 to 3.55].

Hospitality cap rates are expected to become more stable in 2014 as they move from a moderately increasing rate to a slightly increasing rate [3.60 to 3.40 for both full- and limited-service hotels].

Cap rates for land are also anticipated to be stable-to-slightly-increasing in 2014.

2013

3.20 3.55

2014 2013

3.20 3.45

2014

RISE RISE

2013

3.00 3.50

2014

RISE

RES

IDEN

TIA

L | F

OR

SA

LE

TOWNHOME/ CONDO SINGLE-FAMILY HOMEBUILDING

SINGLE-FAMILY LOT DEV.

2013

3.14 3.38

2014 2013

3.00 3.33

2014

RISE RISE

LAN

D

FARM GROUND DEVELOPMENT

RES

IDEN

TIA

L | R

ENTA

L

2013

3.40 3.44

2014

RISE

STUDENT HOUSING

2013

3.30 3.40

2014

RISE

TAX-CREDIT

2013

3.38 3.46

2014

RISE

MARKET RATE

2013

3.10 3.40

2014

RISE

LUXURY

PAGE15

TRENDS IN CAPITAL MARKETS + REGULATORY AFFAIRS

“Compared to last year, there is more capital invested into the market and more demand for retail, office and apartments.”

apital market indicators show expectations of an increasing economic climate. While inflation and interest rates are

to further enhance the investment climate while increasing cost of borrowing and the need to hedge against price increases may chill development.

Because respondents indicated that they see an increase in all factors, at very similar levels from one metric to another [with the exception of underwriting standards, which are not expected to change significantly] it is difficult to discern what the expected impacts capital markets and regulatory affairs are likely to have on investment. Undoubtedly the expected increases in available captial will encourage development, while the expected outcomes from monetary policy decisions will likely impact development costs.

Cexpected to increase, respondents also indicate that they expect additional sources of equity and debt to be available for projects.

No significant changes are expected in regulatory affairs as underwriting standards are expected to remain significantly unchanged.

Additional debt and equity sources are likely

PAGE16

INFLATION + INTEREST RATESInflation is expected to increase slightly in 2014 and then to moderately increase over the next five years. Both short- and long-term interest rates are also expected to increase faster than inflation in 2014, increasing slightly to moderately. In the long-term both interest rates are expected to increase aggressively over the next five years. Short term interest rates are expected to have the greatest change in rate of increase from 2014 to 2019.

UNDERWRITING STANDARDSUnderwriting standards are expected to remain about the same over the next eighteen months for both real estate development and acquisition [2.95, 3.00, respectively].

EQUITY CAPITALPrivate companies and individual and individual investors are expected to lead the charges in available equity in 2014. Overall, respondents were optimistic that more capital will be available in 2014 for real estate ventures from all sources, with the exception of government enterprises[2.94, or slight decline].

Hedge funds, institutional investors, and public companies and REITs are all expected to show moderate increases [3.70, 3.65, and 3.59, respectively] in available equity moving forward, while syndicators are only somewhat less likely to produce capital [3.41].

DEBT CAPITALSimilar to equity capital, respondents expect to see an increase in availability of debt capital from all sources except government [2.88, or a slight decline]. Non-bank financial institutions and securitized lenders are expected to show the largest increase in available debt sources [3.71 and 3.66, respectively].

INFLATION

SHORT-TERM INTEREST

LONG-TERM INTEREST

2014 5 YEARS

CHANGE IN INFLATION + INTEREST RATESFALL REMAIN STABLE RISE

MORE STRINGENT

SAME RISE

REAL ESTATE ACQUISITION | 2.95

REAL ESTATE DEVELOPMENT | 3.00

UNDERWRITING STANDARDS | 18 MONTHS

LARGE DECLINE

SAME LARGE INCREASE

ALL SOURCES | 3.62PUBLIC COMPANES + REITS | 3.59PRIVATE COMPANIES | 3.88INSTITUTIONAL INVESTORS | 3.65OPPORTUNITY/HEDGE FUNDS | 3.70SYNDICATORS/TICS/1031 FUNDS | 3.41GOVERNMENTS | 2.94INDIVIDUAL INVESTORS | 3.76

EQUITY CAPITAL

LARGE DECLINE

SAME LARGE INCREASE

MEZZANINE LENDERS | 3.50

COMMERCIAL BANKS | 3.53

SECURITIZED LENDERS/CMBS | 3.66

INSURANCE COMPANIES | 3.52

NON-BANK FINANCIAL INST | 3.71

GOVT. SOURCES | 2.88

DEBT CAPITAL

3.26 3.85

3.51 4.12

3.73 4.24

PAGE17

TRENDS IN SUBMARKETS

GRAND RAPIDS-WYOMING

ANN ARBOR

TRAVERSE CITY

HOLLAND-GRAND HAVEN

LANSING-EAST LANSING

KALAMAZOO-PORTAGE

MARQUETTE

DETROIT-WARREN-LIVONIA

MUSKEGON-NORTON SHORES

BAY CITY

BATTLE CREEK

NILES-BENTON HARBOR

MONROE

JACKSON

SAGINAW-SAGINAW TWP. N

FLINT

AVG

2.0

3.0

4.0

5.0 EXCELLENT

FAIR

GOOD

POOR

OUTLOOK BY LOCATION

1.0 ABYSMAL2.20NT

2.43NT

2.67

2.75

2.86

3.08

3.14

3.20

3.38

3.40

3.60

3.80

3.94

4.22

4.38

4.60

PAGE18

"Detroit vacancy rate is 24%, lower than Southfield market

for Class A, and the Renaissance Center has the lowest vacancy

rate in its history."

"It is pretty remarkable how Detroit has remained a major influence in the auto industry and the cause is that there are

indigenous companies and great universities here."

lmost a third of the areas in the survey rated fair or excellent for development. Half of the areas in the

"With occupancy rates above 95% downtown [Detroit], new

apartments are being proposed behind the Westin to meet

demand."

“The real irony is that in Detroit, smart money found its way here while the City is going through

bankruptcy. This City has tremendous potential.”

"With $12B in private investment and 12K new jobs, the governor touts Detroit as the comeback

city."

DETROIT CONFIDENCEAsurvey were rated as good opportunities and only two area rated poor. Overall, the average for all the areas was in the high-good to low-fair range at 3.35. According to the survey results, the Grand Rapids-Wyoming area is the best prospect in the state for real estate activity in 2014 with a very strong rating of 4.60 out of 5.00. This area is followed closely by Ann Arbor with 4.38. Both of these areas were rated as excellent development opportunities

Areas for fair development opportunities in 2014 are dispersed throughout the state and included Traverse City [4.22], Holland-Grand Haven [3.94], Lansing-East Lansing [3.80] and Kalamazoo-Portage [3.60].

Of the areas rated good, Marquette and Detroit-Warren-Livonia led the rankings as the top two in this range, scoring 3.40 and 3.38, respectively.

For Detroit, this is a significant change from ratings in previous ULI national reports [Emerging Trends in Real Estate]. Compared to previous national prospect rankings [2012 at 2.88, 2011 at 2.00, 2010 at 1.79, 2009 at 2.24, and 2008 at 2.58] where Detroit ranked last each year, this indicates either a strengthening of the prospects for Detroit, and/or an underestimation of the real potential for Detroit by the national survey.

The impact of the bankruptcy on real estate development is beyond the scope of this report, but it is worth noting that the survey was conducted while the emergency manager was in place, and may reflect opportunities in spite of any bankruptcy. Considered by some investors to be rich with opportunity, sections for Detroit are clearly investment opportunities.

PAGE19

WALKSCORE BY LOCATION

TRAVERSE CITYHOLLANDNILESGRAND HAVENBENTON HARBORANN ARBORBAY CITYEAST LANSINGJACKSONMARQUETTEMONROEGRAND RAPIDSKALAMAZOODETROITFLINTLANSINGMUSKEGONSAGINAWWYOMINGBATTLE CREEKPORTAGENORTON SHORES TO

P 5

WA

LKS

CO

RE

MA

JOR

CIT

IES

One oft-cited criticism of Michigan development is the lack of walkability. Although walkability is not directly measured in the survey, many of the questions, such as the impediments to development, indirectly measure the impact of various modes of transportation on development.

If walkability is a consideration in the development of urban areas, and if urban areas are a focus of development in Michigan, then it is important to point out that some of the metropolitan areas included in the survey rated well when compared to the most walk able urban areas in the country.

A review of the walk score [from www.walkscore.com] for the major cities in the metropolitan areas included in the survey, indicate that four rank at, or above, the top five walkalble major cities in the country. New York [85], San Francisco [85], Boston [79], Chicago (74) and Philadelphia [74].

Traverse City, Holland, Niles, and Grand Haven rank as very or extremely walkalble.

Fourteen of the twenty-two cities [64%] rank as somewhat walkalble or higher. Both Traverse City and Holland rated in the “walker’s paradise” category where daily errands do not require a car. However, none of these cities even qualify for a Transit Score under the same ranking system, and only Grand Rapids qualifies for a Bike Score [50].

The only two metropolitan areas to rank in one of the top two categories for both the 2014 Outlook for Real Estate by Location and Walk Score by Location are Traverse City and Holland-Grand Haven, possibly indicating unique urban redevelopment opportunities..

PARADISE [100]

CAR DEPENDENT [0]

98948280665959575655545451

504948484544402924

SOMEWHAT WALKABLE [50]

PAGE20

opportunities in Ann Arbor [4.38], Traverse City [4.22], and Marquette [3.40].

The southern and eastern portions of the lower peninsular generally rated lower [averaging a score of 2.78, or good], with only Detroit-Warren-Livonia and Bay City ranking above 3.00, or good, at 3.38 and 3.14, respectively.

When presented geographically, the rankings for development indicate a focus around the south central and western portions of the lower peninsula.

In this area, the six cities around and including Grand Rapids all ranked 3.00 or above [averaging 3.70, or fair]. Elsewhere there are isolated

3.40

2.43

2.20

3.14

3.38

2.75

3.20

2.86

2.67

4.22

3.94

3.80

3.60 4.38

MARQUETTE

BAY CITYSAGINAWFLINT

ANN ARBORDETROITMONROEJACKSON

LANSING-EAST LANSINGBATTLE CREEK

KALAMAZOO-PORTAGENILES-BENTON HARBOR

MUSKEGON-NORTON SHORES

GRAND RAPIDS-WYOMING

TRAVERSE CITY

3.08

HOLLAND-GRAND HAVEN 4.60

PAGE21

The up-and-coming areas for the next five years were only slightly different than the opportunities for next year.

As has been often mentioned, although ranking as a good opportunity in the near term, Detroit ranked as the highest five year potential, with 50% of the respondents indicating that it will be the most exciting for real estate development.

Not surprising, given the short term prognosis, Grand Rapids-Wyoming, Ann Arbor, and Traverse City each continued to be seen as good prospects over the next five years.

All four of these areas share significant recent investments in real estate development, but each is serving a unique mix of market segments that include young urban professionals, retires, students, and travelers.

MOST EXCITING AREAS FOR NEXT FIVE YEARS

DETROIT-WARREN-LIVONIA [50%]

GRAND RAPIDSWYOMING [14%]

ANN ARBOR [14%]

TR

AV

ER

SE

CIT

Y [

11%

]

LANSINGEAST

LANSING [4%]

HO

LLAN

DG

RA

ND

HA

VEN

[4%]

JACKSON [3%]

PAGE22

IMPEDIMENTS

mmediately following the great-recession, the most frequently cited impediment to redevelopment in Michigan was the lack of access to capital. Respondents listed that as the second most important impediment.

initiatives, will be a model of the Michigan cities, but regional and city-wide transportation challenges remain.

Though likely due to a host of reasons, this may be indicating a lack of available urban locations. It may be that this is not so much an impediment, but an opportunity, as urban areas in the state are increasingly desirable locations for redevelopment.

Lack of financing remains a major concern with 21% of the respondents listing it as the most important impediment.

Maybe not so surprising, given the urban redevelopment focus of the last few years, respondents listed the top impediment as the lack of alternative modes of transportation.

But what is surprising, is that the lack of alternative modes of transportation was selected by more than a third of the respondents, and is fourteen points more critical than the still challenging lack of financing.

In the birthplace of the auto industry, with its history of suburban development, Michigan has a challenge in providing transportation alternatives. Detroit and Grand Rapids, with their light-rail and fixed-wheel public transportation

I35%

21%

17%

10%

7%

4%3%3%

LACK ALT. MODES OF TRANSPORTATION

LACK OF FINANCING

BUILDING + ZONING REGULATIONS

LACK OF AVAILABLE SITES

FINDING QUALIFIED WORKFORCE

IMPACT-RELATED FEES

LACK OF DEMANDIMAGE