Embed Size (px)

Citation preview

2013 FORECAST: A LOOK AHEADPuget Sound Economic Forecast

Michael DuekerChief Economist

Russell Investments

V810

2013 Economic Outlook: Will we avoid over-exuberant near-term budget slashing?

Michael Dueker, Chief Economist

January 10, 2013

V308

Important Information and Disclosures

Nothing contained in this material is intended to constitute legal, tax, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. The general information contained in this publication should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Bond investors should carefully consider risks such as interest rate, credit, repurchase and reverse purchase transaction risks. Greater risk, such as increased volatility, limited liquidity, prepayment, non-payment and increased default risk, is inherent in portfolios that invest in high yield (“junk”) bonds or mortgage backed securities, especially mortgage backed securities with exposure to sub-prime mortgages.

Indexes are unmanaged and cannot be invested in directly. Past performance is not indicative of future results.

Copyright© Russell Investments 2011. All rights reserved. This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

Russell Investment Group is a Washington, USA corporation, which operates through subsidiaries worldwide, including Russell Investments, and is a subsidiary of The Northwestern Mutual Life Insurance Company.

The Russell logo is a trademark and service mark of Russell Investments.Date of first use: January 2013CORP-7323

3

This presentation was created for informational purposes only and is not meant for further distribution.

V308

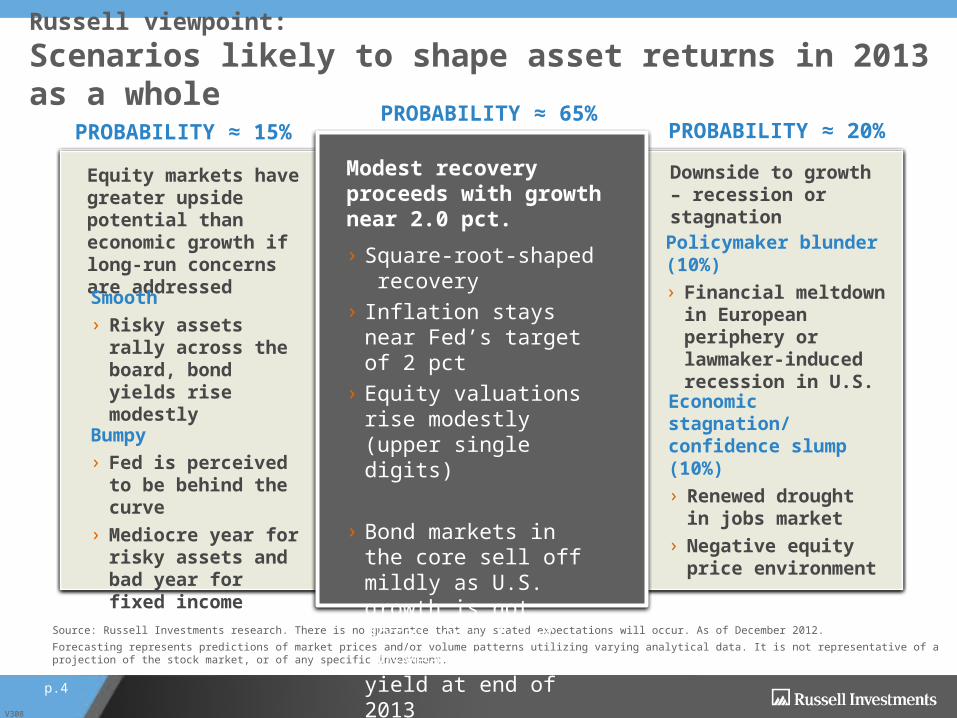

Russell viewpoint:Scenarios likely to shape asset returns in 2013 as a whole

Source: Russell Investments research. There is no guarantee that any stated expectations will occur. As of December 2012.Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

› Square-root-shaped recovery

› Inflation stays near Fed’s target of 2 pct

› Equity valuations rise modestly (upper single digits)

› Bond markets in the core sell off mildly as U.S. growth is not derailed; 2.15% 10-year Treasury yield at end of 2013

Modest recovery proceeds with growth near 2.0 pct.

Downside to growth – recession or stagnation

Equity markets have greater upside potential than economic growth if long-run concerns are addressed

Smooth› Risky assets rally

across the board, bond yields rise modestly

Bumpy › Fed is perceived to be

behind the curve› Mediocre year for

risky assets and bad year for fixed income

PROBABILITY ≈ 15%PROBABILITY ≈ 65%

PROBABILITY ≈ 20%

Policymaker blunder (10%)› Financial meltdown in

European periphery or lawmaker-induced recession in U.S.

Economic stagnation/confidence slump (10%)› Renewed drought in

jobs market› Negative equity price

environment

p.4

V810

5

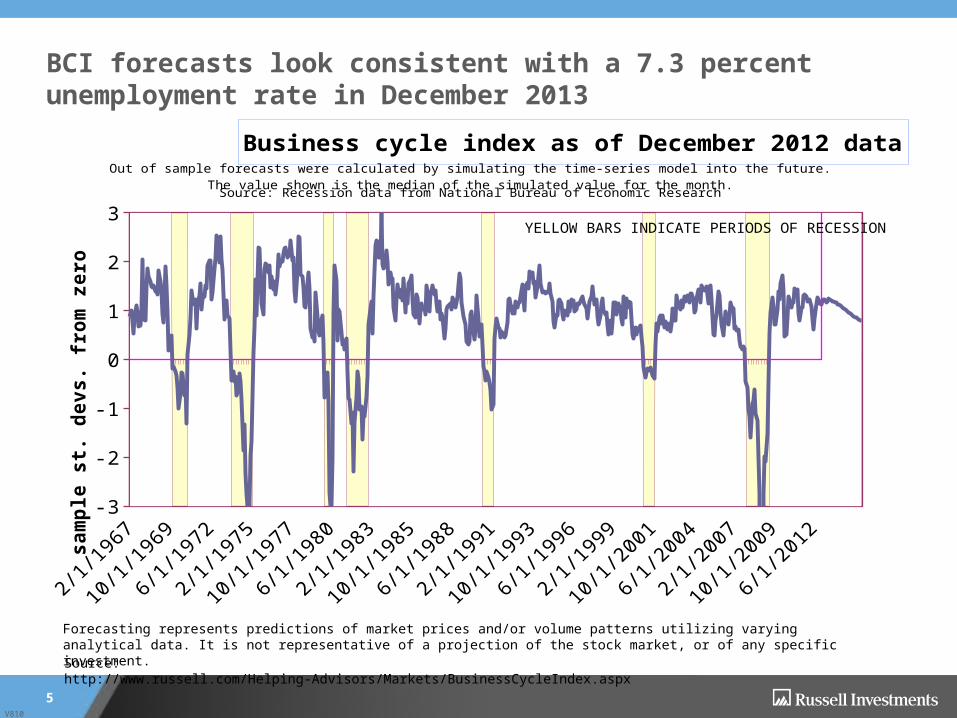

BCI forecasts look consistent with a 7.3 percent unemployment rate in December 2013

Source: http://www.russell.com/Helping-Advisors/Markets/BusinessCycleIndex.aspx

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

-3

-2

-1

0

1

2

3

Business cycle index as of December 2012 data

sam

ple

st. d

evs.

from

zer

o

YELLOW BARS INDICATE PERIODS OF RECESSION

Out of sample forecasts were calculated by simulating the time-series model into the future.The value shown is the median of the simulated value for the month.Source: Recession data from National Bureau of Economic Research

V810

6

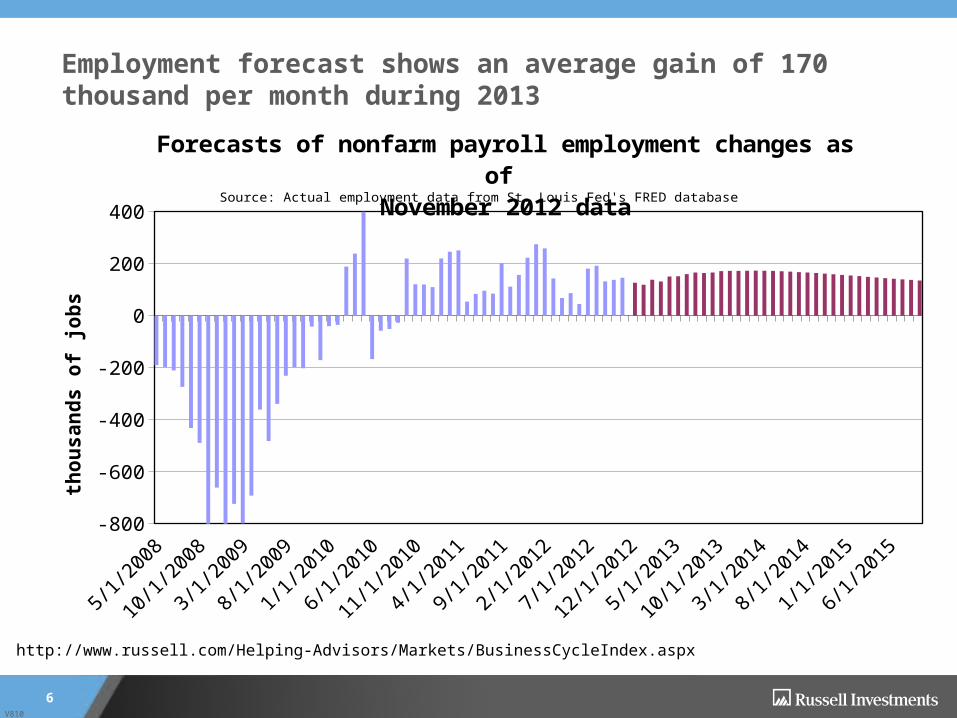

Employment forecast shows an average gain of 170 thousand per month during 2013

http://www.russell.com/Helping-Advisors/Markets/BusinessCycleIndex.aspx

May '0

8

Nov '0

8

May '0

9

Nov '0

9

May '1

0

Nov '1

0

May '1

1

Nov '1

1

May '1

2

Nov '1

2

May '1

3

Nov '1

3

May '1

4

Nov '1

4

May '1

5-800

-600

-400

-200

0

200

400

Forecasts of nonfarm payroll employment changes as of November 2012 data

thou

sand

s of

jobs

Source: Actual employment data from St. Louis Fed's FRED database

V810

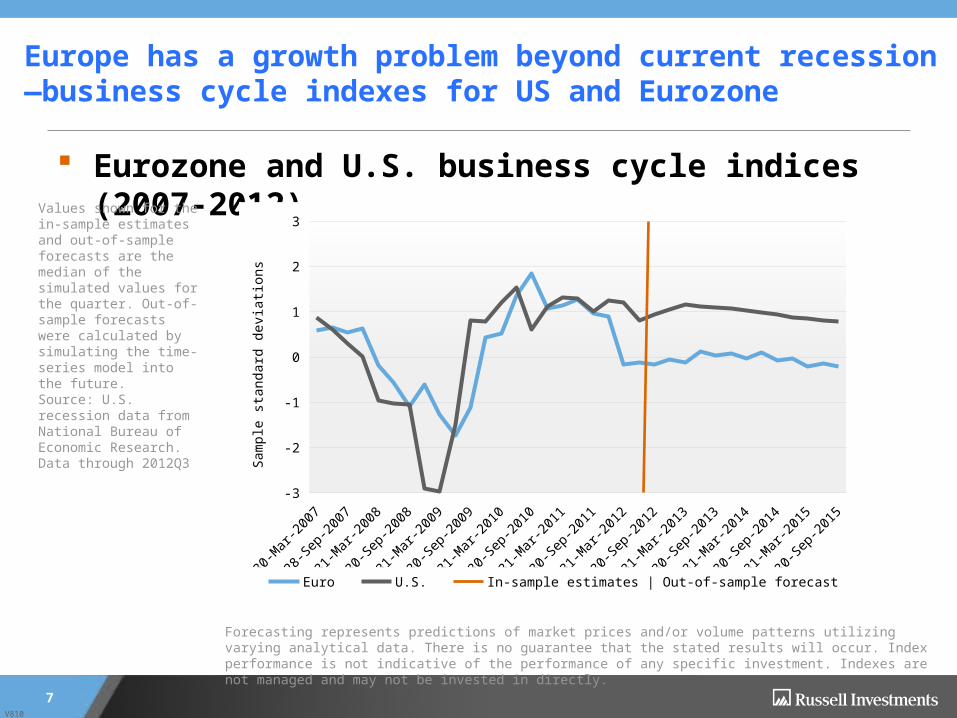

Europe has a growth problem beyond current recession—business cycle indexes for US and Eurozone

7

Eurozone and U.S. business cycle indices (2007-2012)Values shown for the in-sample estimates and out-of-sample forecasts are the median of the simulated values for the quarter. Out-of-sample forecasts were calculated by simulating the time-series model into the future.Source: U.S. recession data from National Bureau of Economic Research. Data through 2012Q3

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. There is no guarantee that the stated results will occur. Index performance is not indicative of the performance of any specific investment. Indexes are not managed and may not be invested in directly.

2007

2008

2009

2010

2011

2012

2013

2014

2015

-3

-2

-1

0

1

2

3

Euro U.S. In-sample estimates | Out-of-sample forecast

Sam

ple

stan

dard

dev

iatio

ns

V810

8

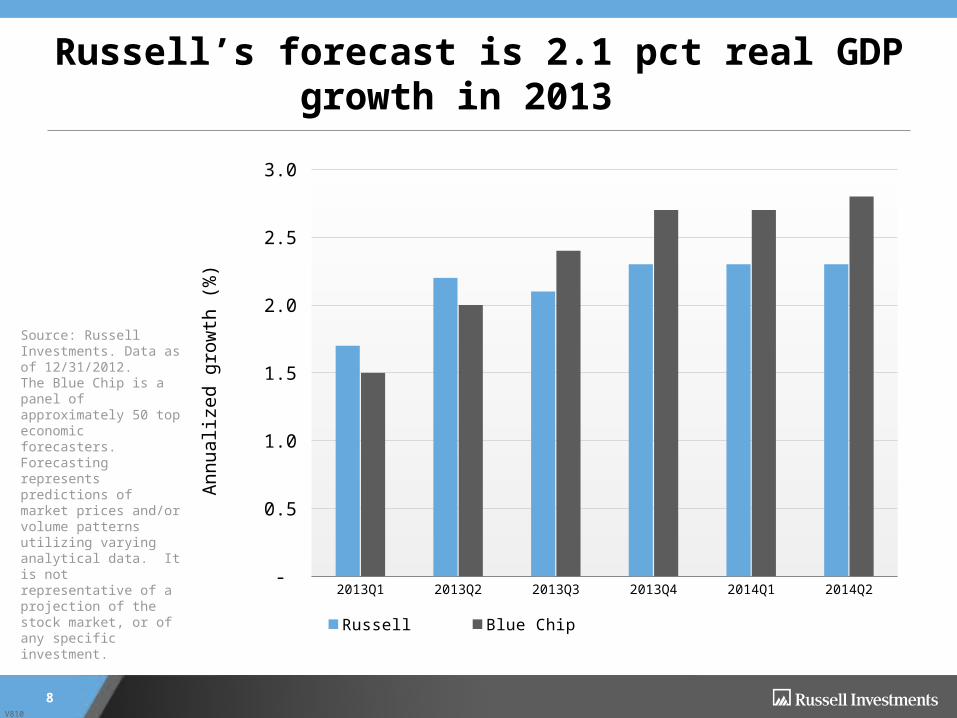

Russell’s forecast is 2.1 pct real GDP growth in 2013

Source: Russell Investments. Data as of 12/31/2012.The Blue Chip is a panel of approximately 50 top economic forecasters.Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

2013Q1 2013Q2 2013Q3 2013Q4 2014Q1 2014Q2 -

0.5

1.0

1.5

2.0

2.5

3.0

Russell Blue Chip

Ann

ualiz

ed g

row

th (%

)

V810

9

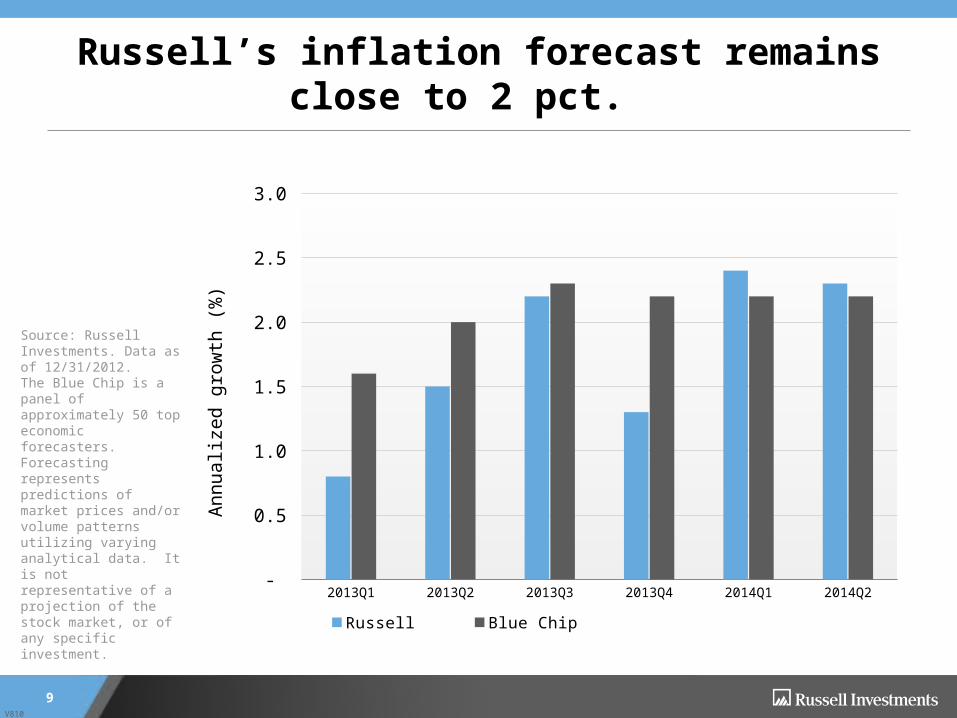

Russell’s inflation forecast remains close to 2 pct.

Source: Russell Investments. Data as of 12/31/2012.The Blue Chip is a panel of approximately 50 top economic forecasters.Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

2013Q1 2013Q2 2013Q3 2013Q4 2014Q1 2014Q2 -

0.5

1.0

1.5

2.0

2.5

3.0

Russell Blue Chip

Ann

ualiz

ed g

row

th (%

)

V810

Investor complaint:

p.10FINANCIAL PROFESSIONAL USE ONLY

For how long do we have to live in a world in which

Greece not getting its next installment of bailout money

could set off a financial crisis? We’re not supposed to be like an emerging-market

economy with recurrent crises? Include additional Greece-like political risk factors on

the list, such as our own fiscal cliff

Answer: for the indefinite future

V810

Political risk: not a one-off but a fact of life

p.11FINANCIAL PROFESSIONAL USE ONLY

It might not feel good to see politicians’ hands on the rudder, but with

debt-to-GDP ratios near 100 percent in the wake of the Great Recession,

auto-pilot does not work. We simply have to accept this increased role of politicians in our lives, as

much as we dislike the idea.

V810

Why QEternity? Nominal GDP growth has not made the grade

p.12

2006

-04-01

2006

-07-01

2006

-10-01

2007

-01-01

2007

-04-01

2007

-07-01

2007

-10-01

2008

-01-01

2008

-04-01

2008

-07-01

2008

-10-01

2009

-01-01

2009

-04-01

2009

-07-01

2009

-10-01

2010

-01-01

2010

-04-01

2010

-07-01

2010

-10-01

2011

-01-01

2011

-04-01

2011

-07-01

2011

-10-01

2012

-01-01

2012

-04-01

-4

-2

0

2

4

6

8

4 qtr nominal GDP growth

4 qtr nominal GDP growth

V81013

Tree-chopping analogy After two rounds of QE by the Fed, some people consider QE to

be a tried-and-failed strategy. Think of a tree-chopping analogy, however. If one takes two

swings at a tree with an axe, steps back and sees that the tree does not fall over, the conclusion is not that the axe cannot cut down the tree!

V810

The Fed’s ‘scary’ balance sheet: Will the Fed be caught holding the bag?

p.14

V810

How the Fed will shrink its balance sheet (when the time comes)

p.15 Illustration only for future 3-month T-bill yield

V810

V810

Super Mario (Draghi) is trying to change the game

Long Term Refinancing Operations Prevented liquidity squeeze on European banks

Outright Monetary TransactionsTo provide interest-rate subsidy to Spain, Italy

Longer term problems still not fixed European recession, grinding in periphery Ongoing fiscal austerity New acronym: NTGES (Never To Grow European

States)

17

V810

Greece is the Corvair of Europe:Insolvent at any interest rate

ECB bond purchases may solve Spain and Italy funding needs

Potential crisis solution: stronger growth, banking union, subsidized interest rates

p.18

V810

p.19

The pain in Spain....

0

5

10

15

20

25

30

Germany Italy France Ireland Portugal Greece Spain

%

Source: Datastream

Unemployment Rates

Latest 2007

V810

“You can always count on Americans to do the right thing—after they’ve tried everything else”

—Winston Churchill

20

V810

“You can always count on Americans to do the right thing—after they’ve tried everything else”

—Winston Churchill.

21

With respect to the current situation in Europe, try substituting Germans for Americans in the quote above and see how it looks.

V810

p.22

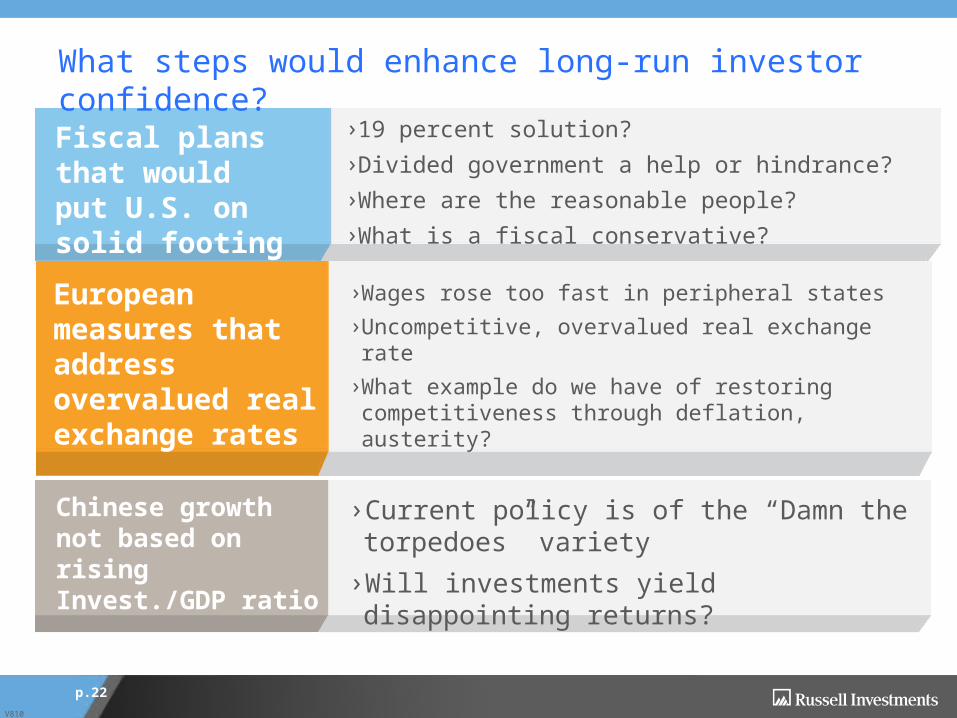

Fiscal plans that would put U.S. on solid footing

› 19 percent solution?›Divided government a help or hindrance?›Where are the reasonable people?›What is a fiscal conservative?

European measures that address overvalued real exchange rates

›Wages rose too fast in peripheral states›Uncompetitive, overvalued real exchange rate›What example do we have of restoring competitiveness through deflation, austerity?

Chinese growth not based on rising Invest./GDP ratio

›Current policy is of the “Damn the torpedoes” variety›Will investments yield disappointing returns?

What steps would enhance long-run investor confidence?

V810

p.23

China’s unbalanced economy

20

25

30

35

40

45

50

55

1980 1985 1990 1995 2000 2005 2010

% of GDP

Source: Datastream

China: Consumption & Investment % of GDP

Fixed Investment Consumption

V810

If you build it, will they come?

Austria in Guangdong The ghost city of Ordos

www.russell.com