Embed Size (px)

Citation preview

ICCTAug2017

i|P a g e

FinalReport

MEXICOFREIGHTASSESSMENT

GLOBALGREENFREIGHTACTIONPLAN

Authors:

JohnRogers,RobinKaenzigandStevenJ.RogersSubmittedto:

TheInternationalCouncilonCleanTransportation(ICCT)

SanFranciscoCABy:

TheSustainableTransportandEmissionsServicesCompanyTSTESSAdeCV.

Calz.deTlalpan5005ACol.LaJoya,TlalpanMexicoDFCP14090

Incollaborationwith:

IntegratedTransportPlanningLtd50NorthThirteenthStreetMiltonKeynesMK93BPUK

Date: Aug24,2017

ICCTAug2017

ii|P a g e

ContentsTables......................................................................................................................vi

Figures.....................................................................................................................ix

Abbreviations..........................................................................................................xi

Acknowledgements................................................................................................xii

Chapter1:-ExecutiveSummary................................................................................1

Chapter2:-FreightcontextinMexicoandtheUSA..................................................3

FreightbymodeinMexicoandtheUSA..................................................................................................4

DomesticFreightinMexicoandtheUSA.............................................................................................4

ImportandExportfreighttoUSAandCanada.....................................................................................9

TransportInfrastructureinMexico........................................................................................................11

RoadSystem.......................................................................................................................................11

RailSystem.........................................................................................................................................13

Multimodalfreight.............................................................................................................................15

Pipelines.............................................................................................................................................15

TransportActivitybymodesotherthanRoad.......................................................................................17

FreighttransportedbyRail.................................................................................................................17

RailEnergyEfficiency..........................................................................................................................19

Principalportsbytonnage(nationalandInternational)2015...........................................................20

AirOperations....................................................................................................................................21

Chapter3:-CharacteristicsofIn-useTractor-trailersinMexico............................24

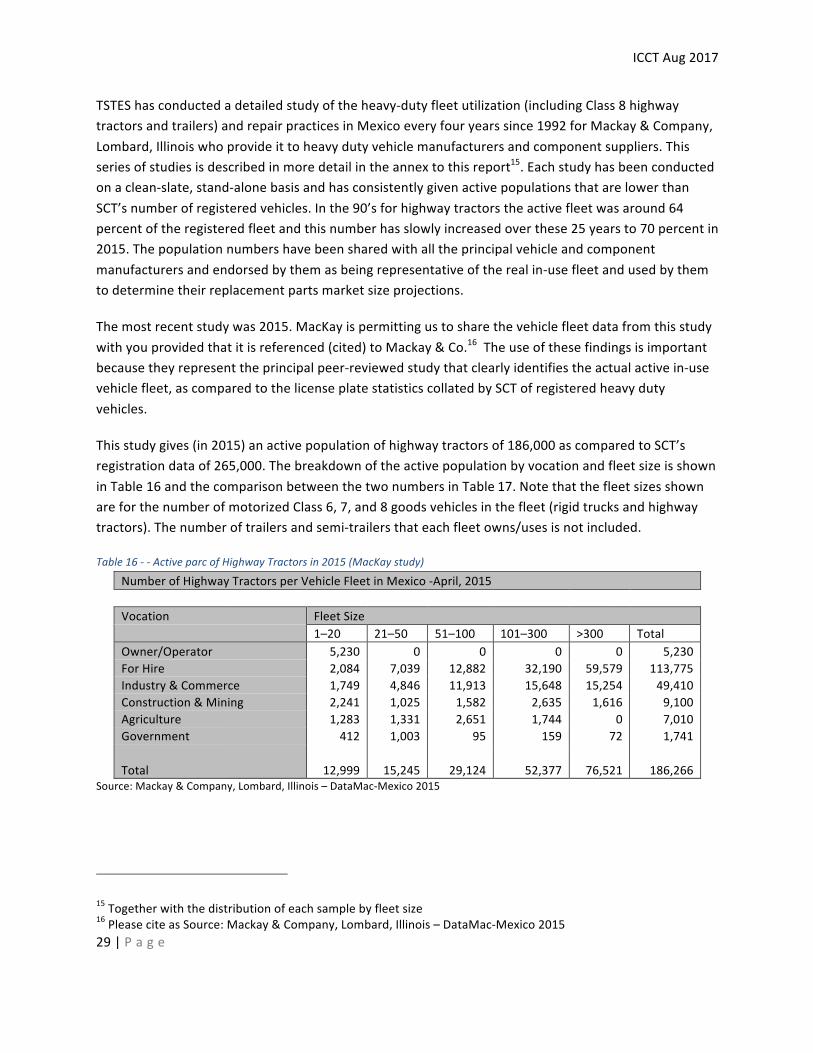

HighwayTractors....................................................................................................................................26

Registeredpopulation........................................................................................................................26

ActivepopulationofHighwayTractors..............................................................................................28

Highwaytractors–enginereplacementpractices.............................................................................38

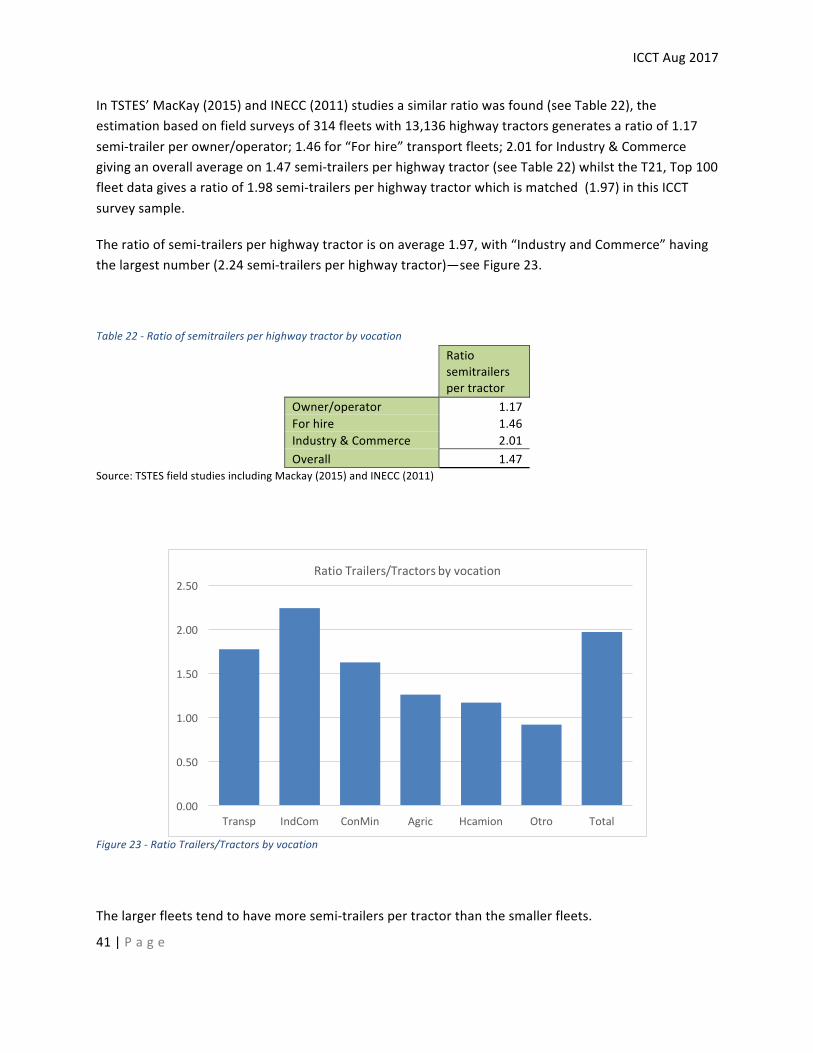

Semi-trailers...........................................................................................................................................40

ICCTAug2017

iii|P a g e

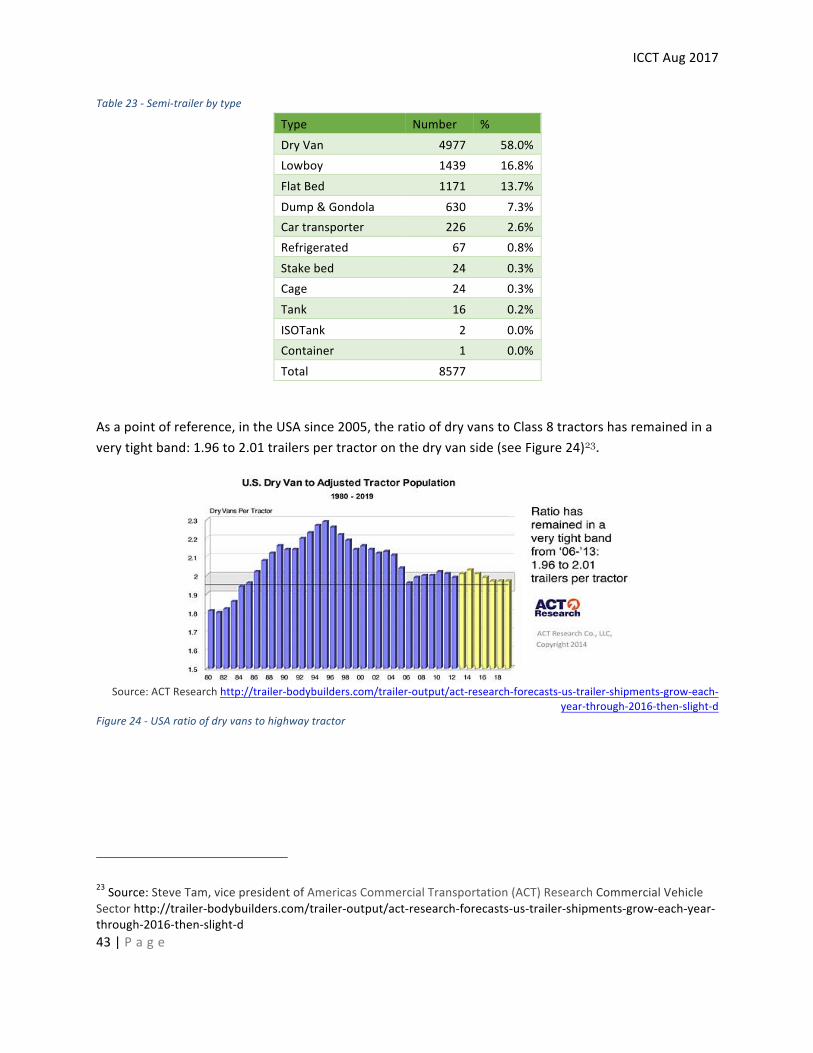

Semi-trailerpopulation......................................................................................................................40

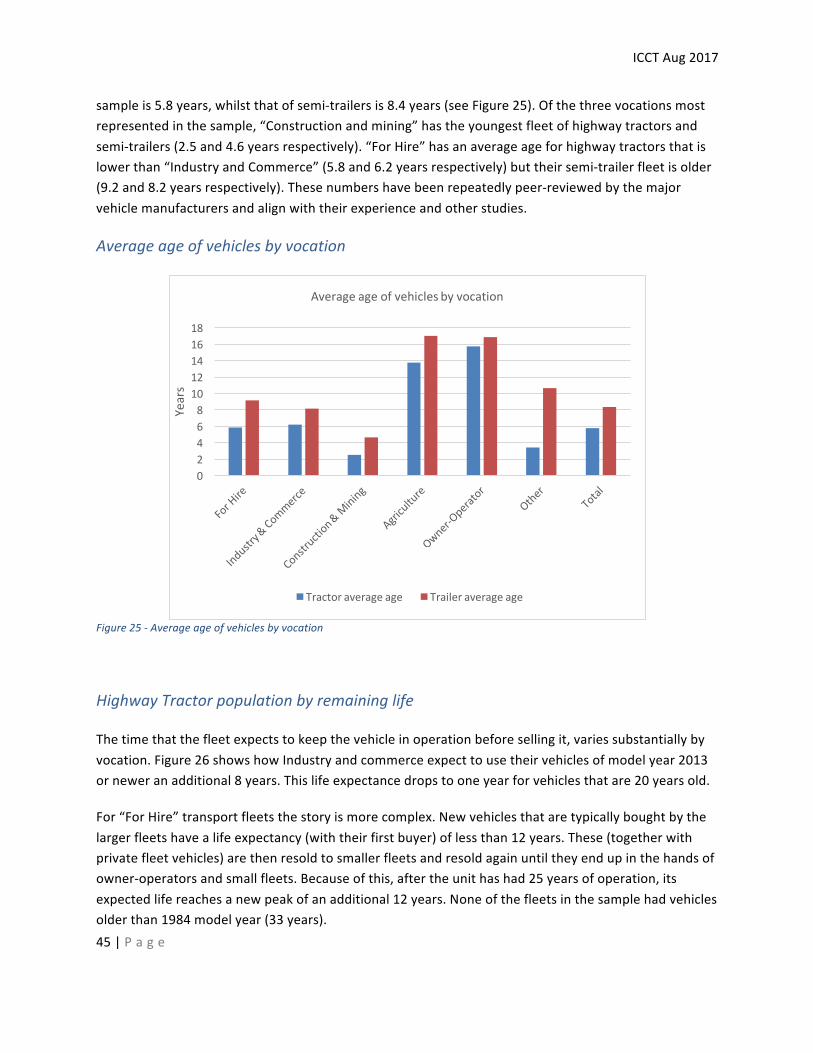

Ageandexpectedlifeofvehicles...........................................................................................................44

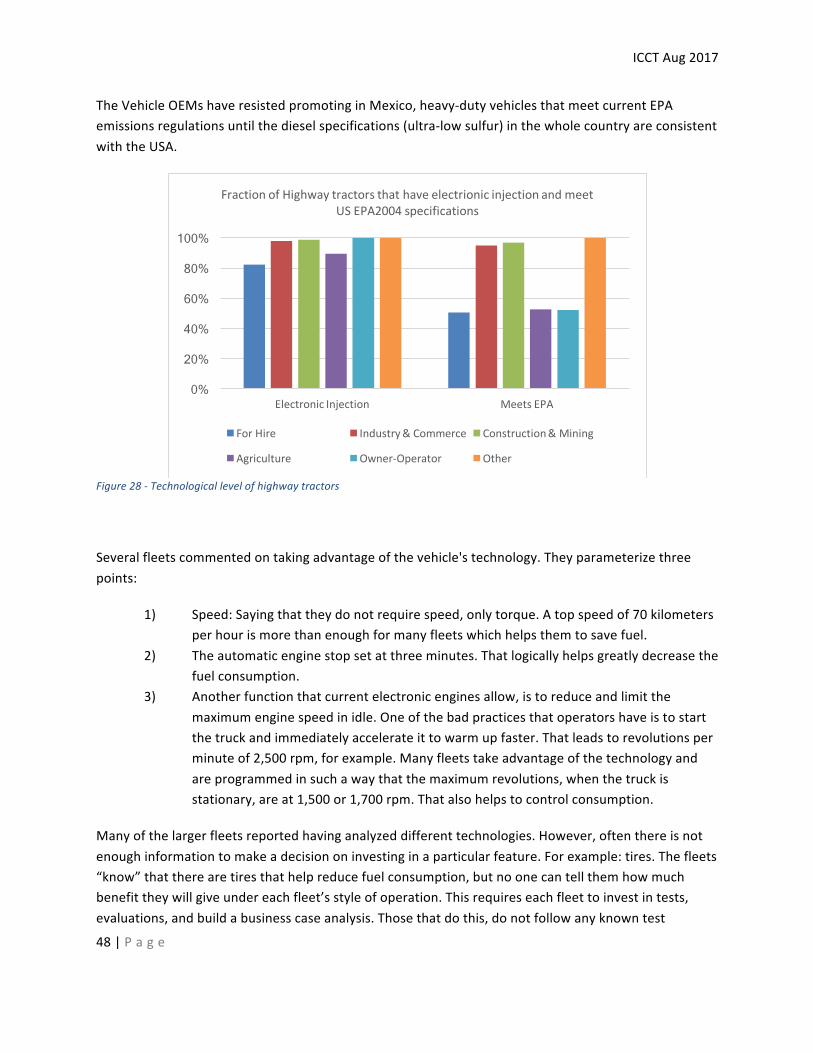

HighwayTractorTechnology..................................................................................................................47

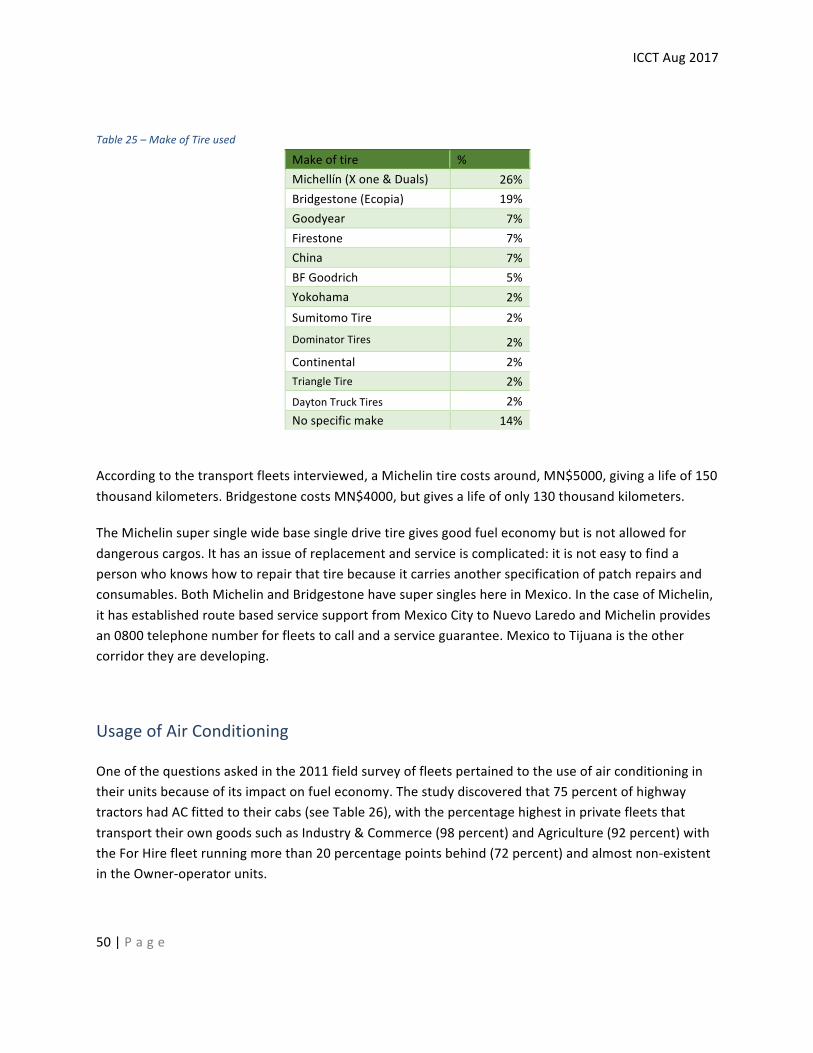

Tires....................................................................................................................................................49

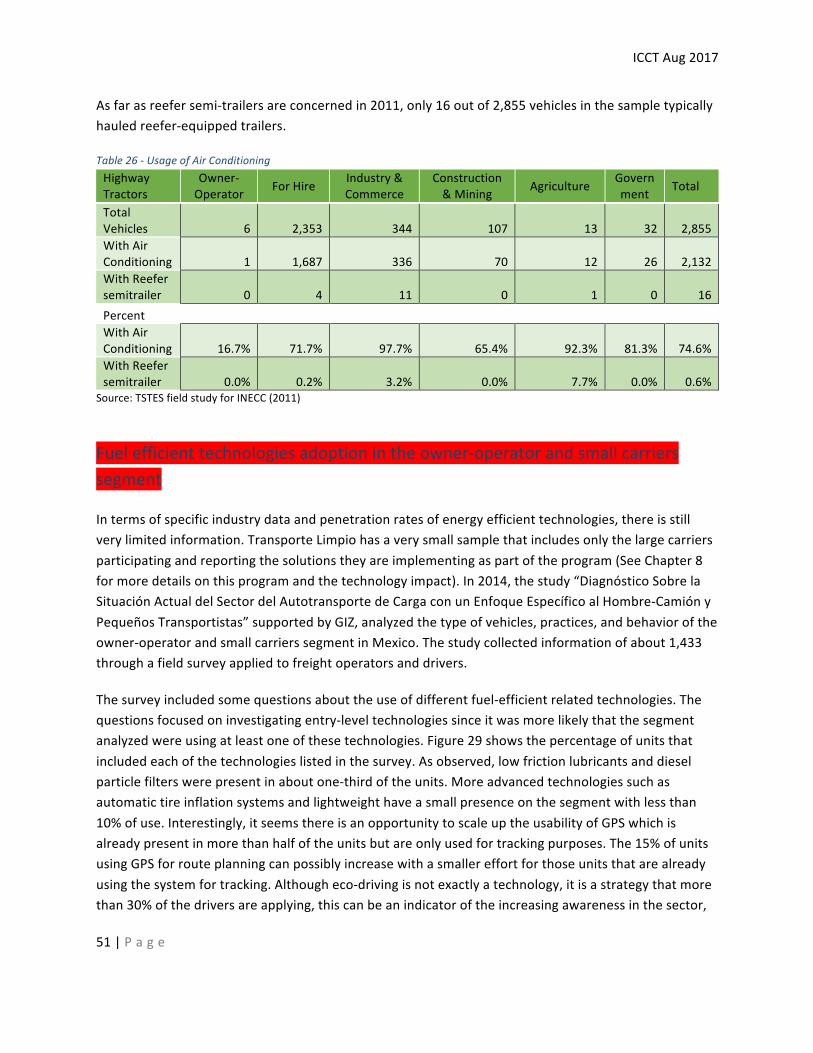

UsageofAirConditioning...................................................................................................................50

Chapter4:-VehiclePurchasing..............................................................................53

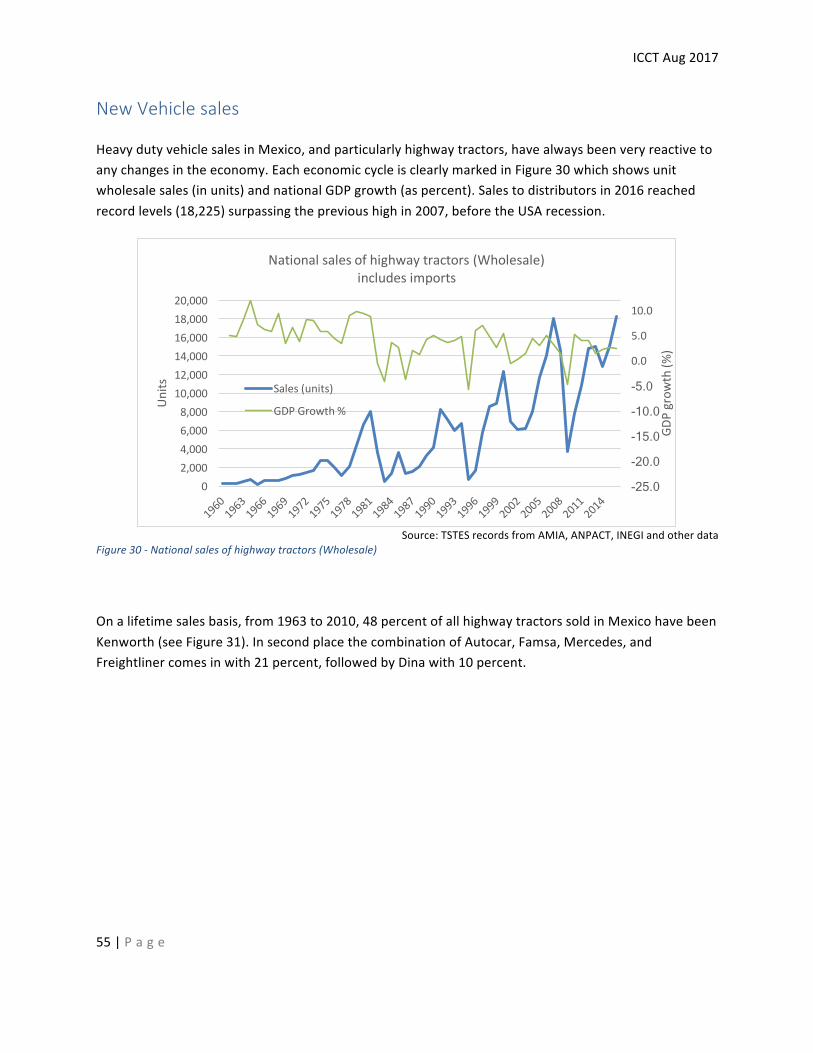

NewVehiclesales...................................................................................................................................55

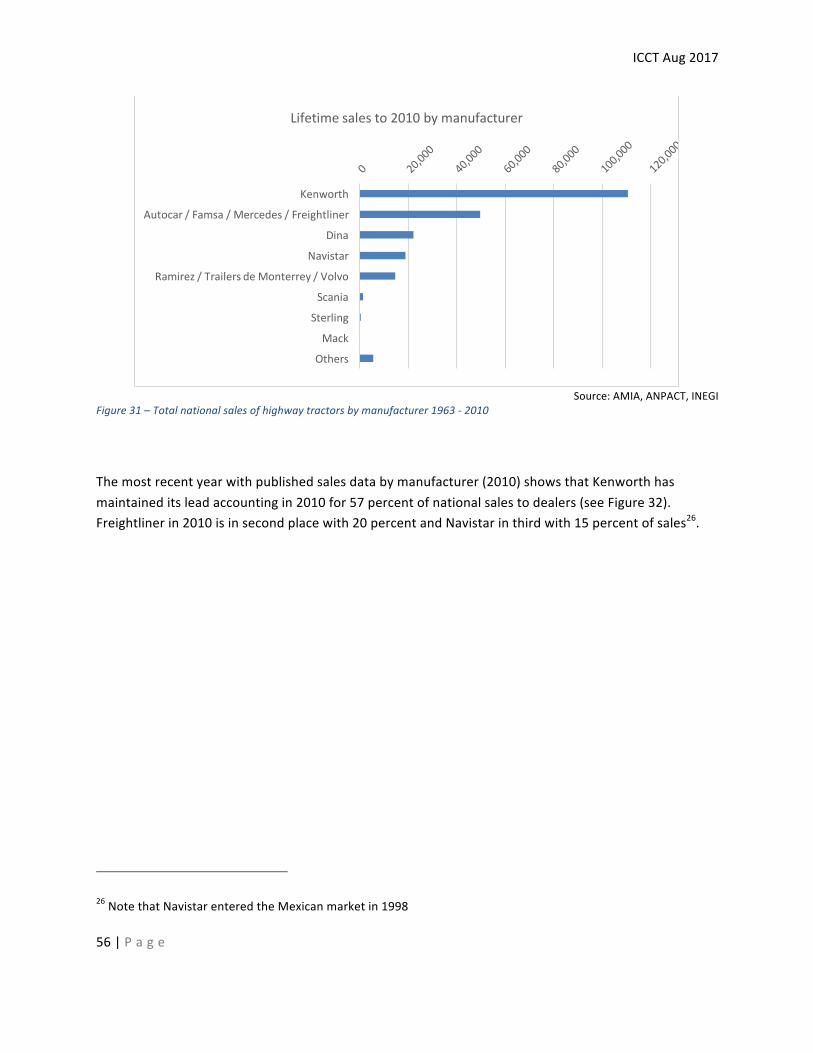

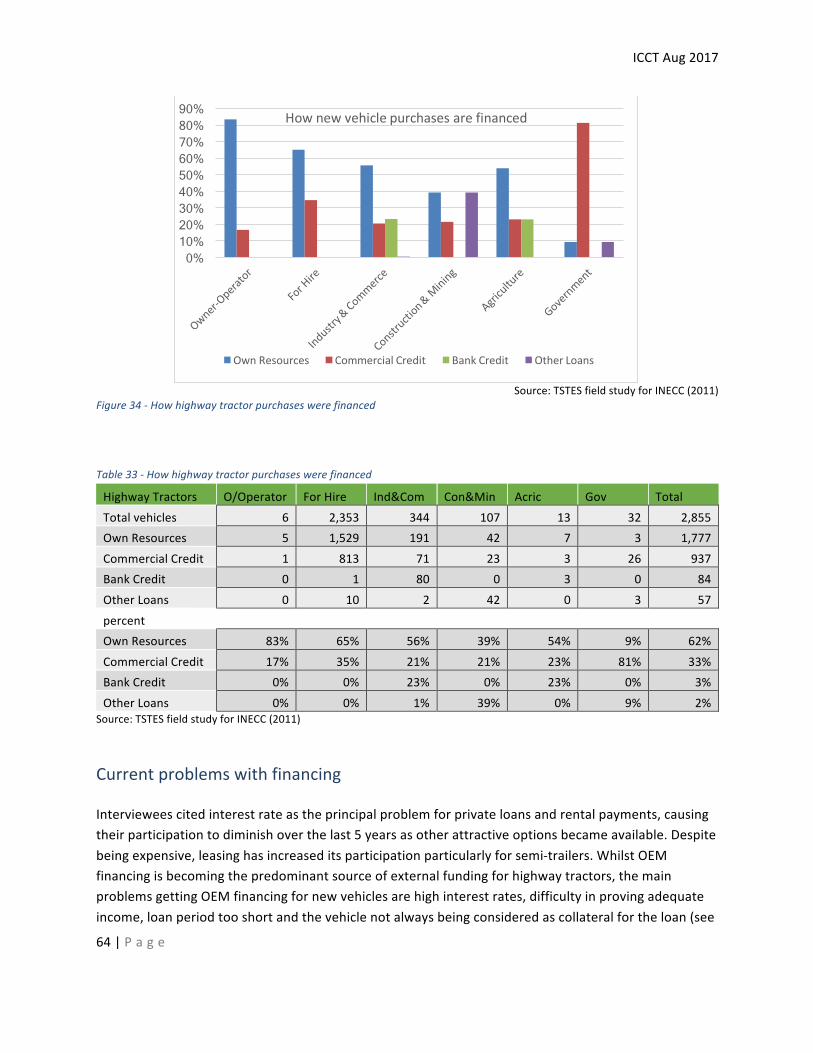

Purchasepatternsofvehicles................................................................................................................57

UsedVehiclesales..................................................................................................................................58

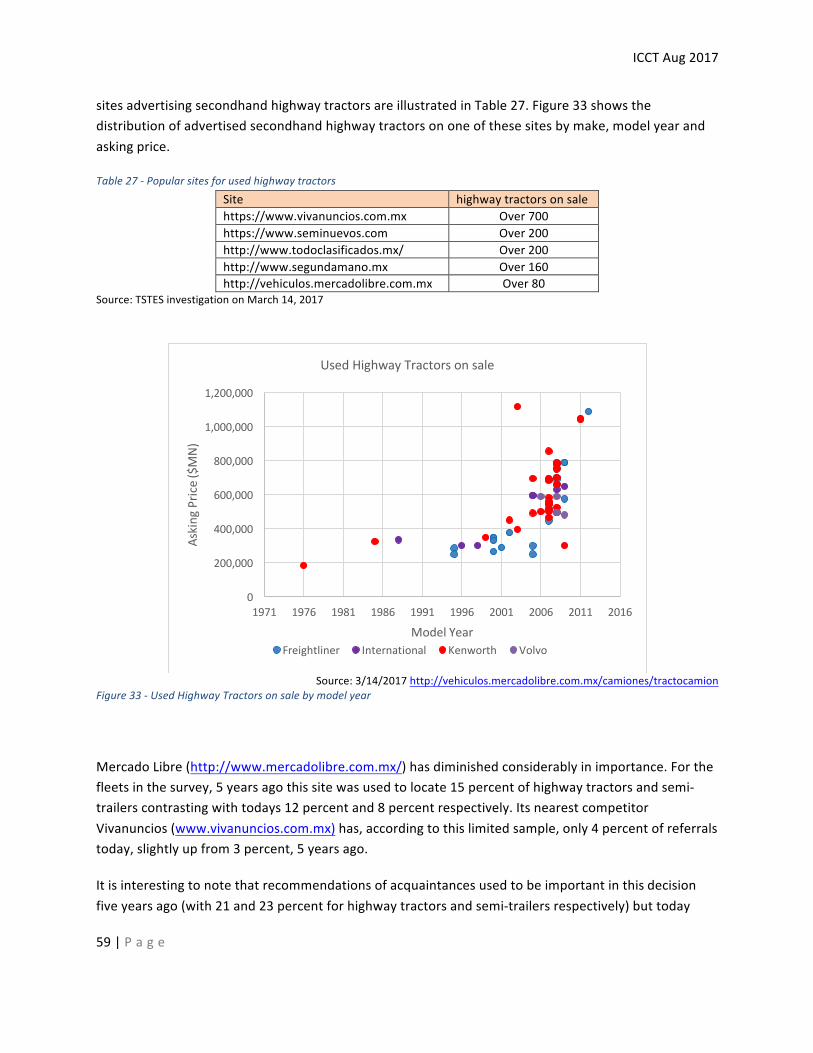

Howarevehiclesforsalelocated.......................................................................................................58

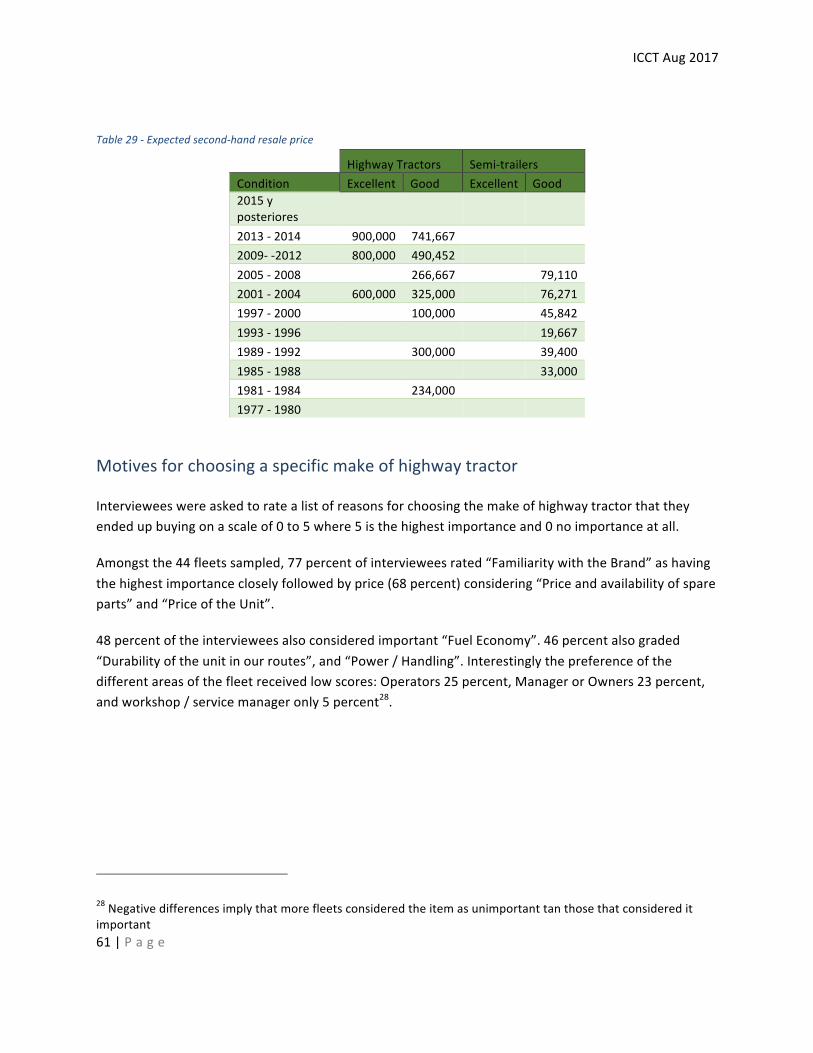

Expectedsalespriceforusedunits....................................................................................................60

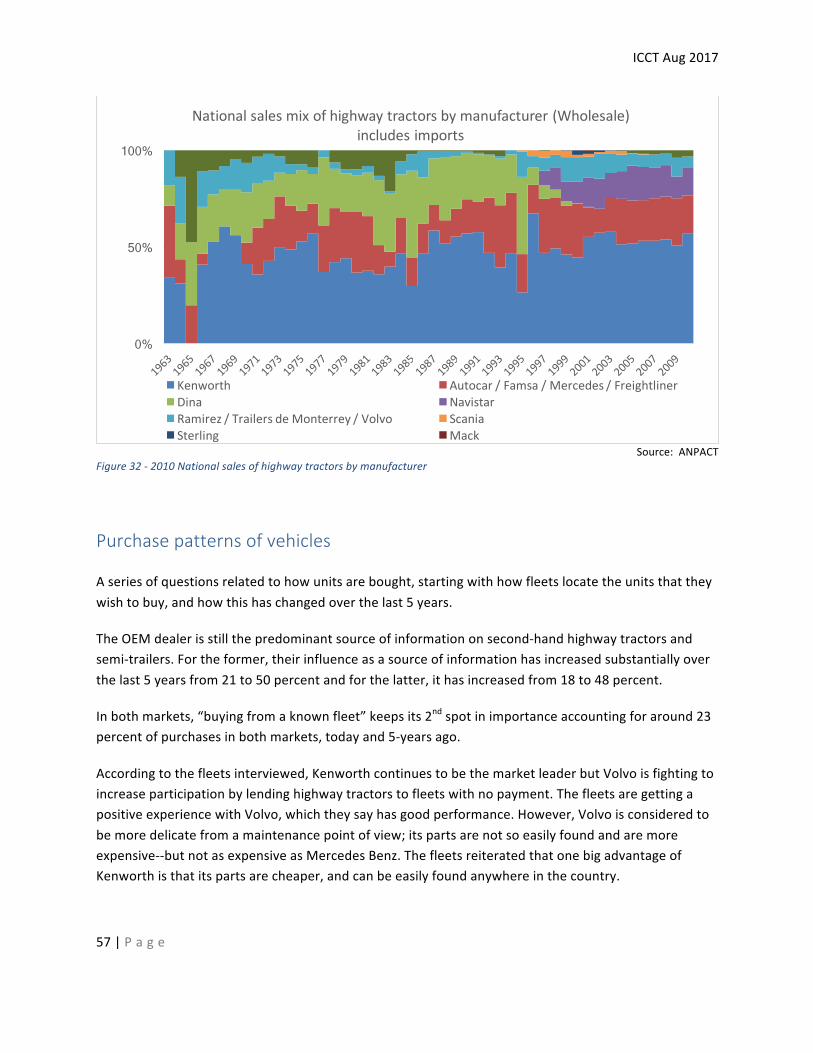

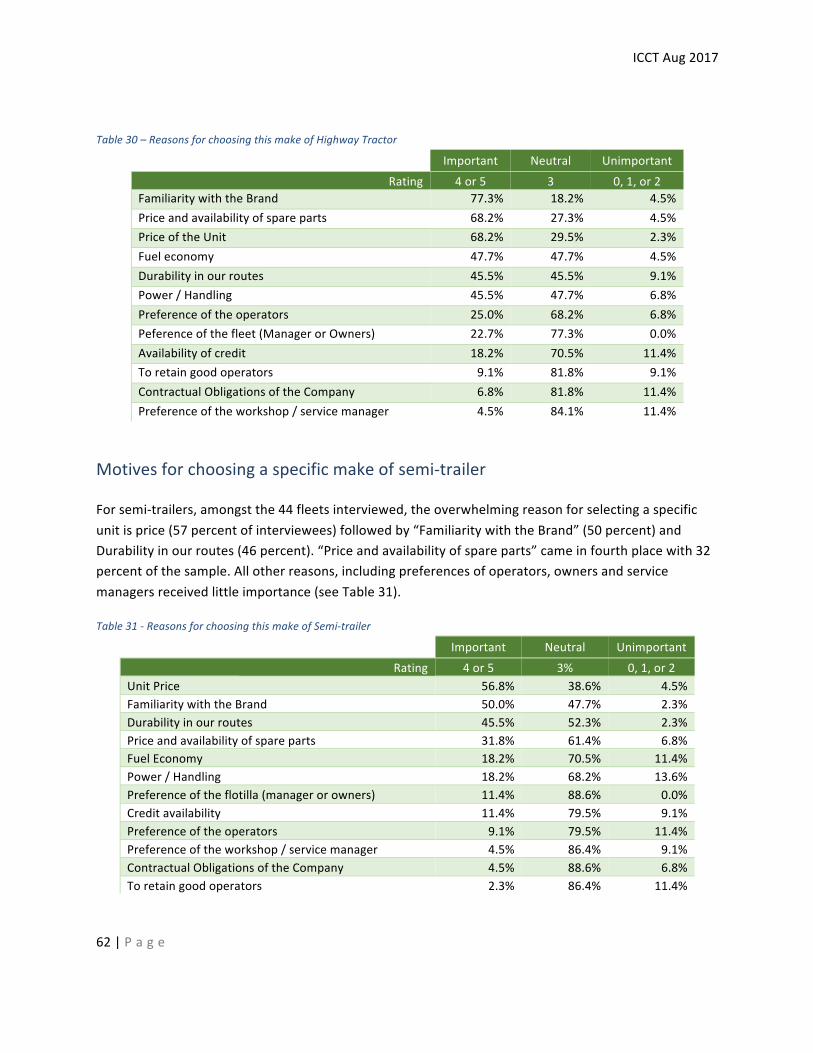

Motivesforchoosingaspecificmakeofhighwaytractor..................................................................61

Motivesforchoosingaspecificmakeofsemi-trailer.........................................................................62

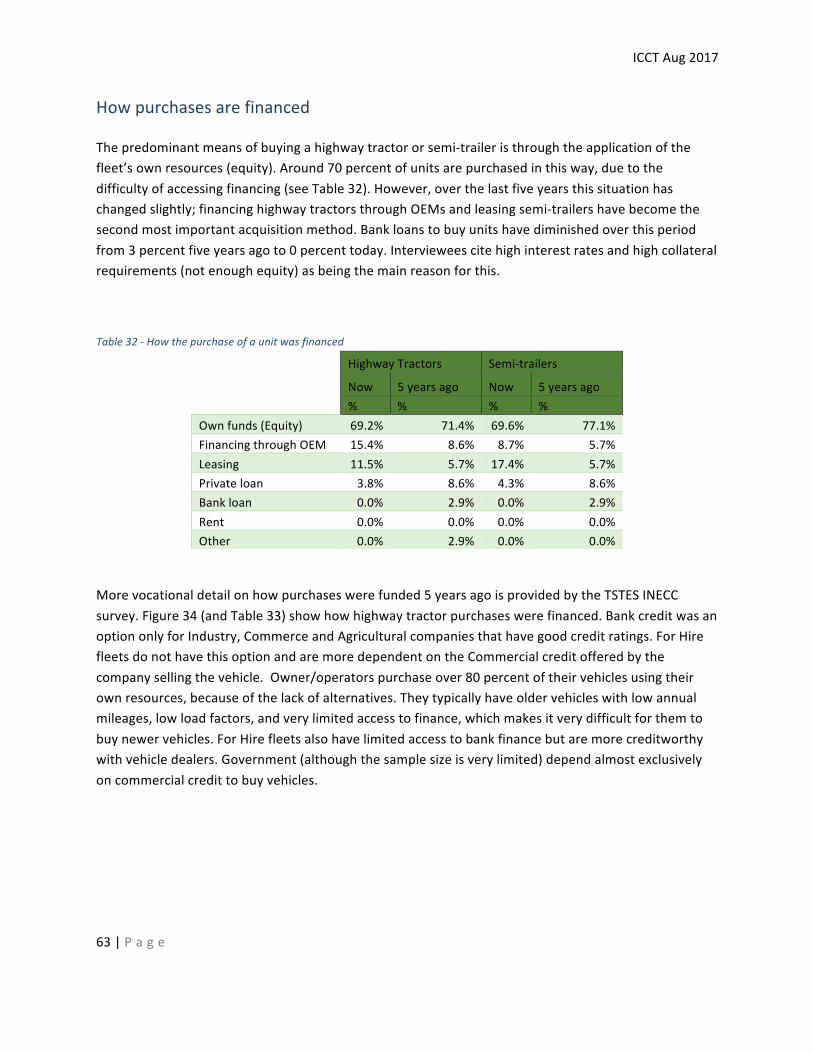

Howpurchasesarefinanced..............................................................................................................63

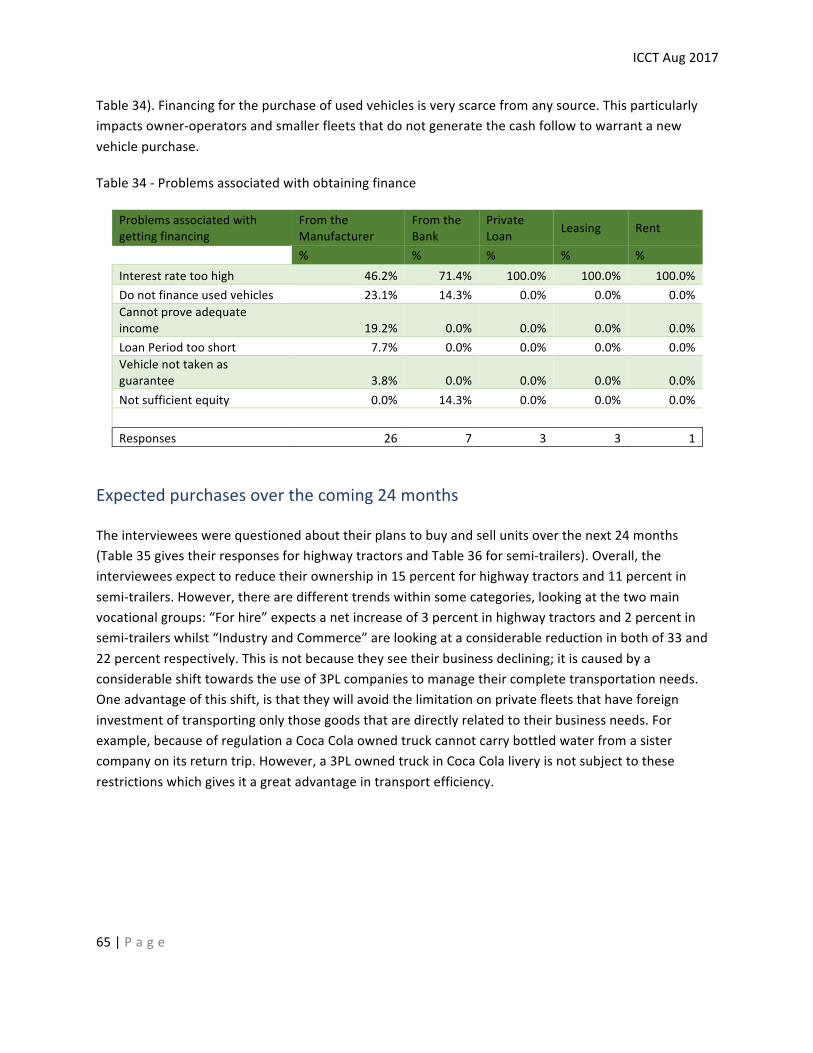

Currentproblemswithfinancing.......................................................................................................64

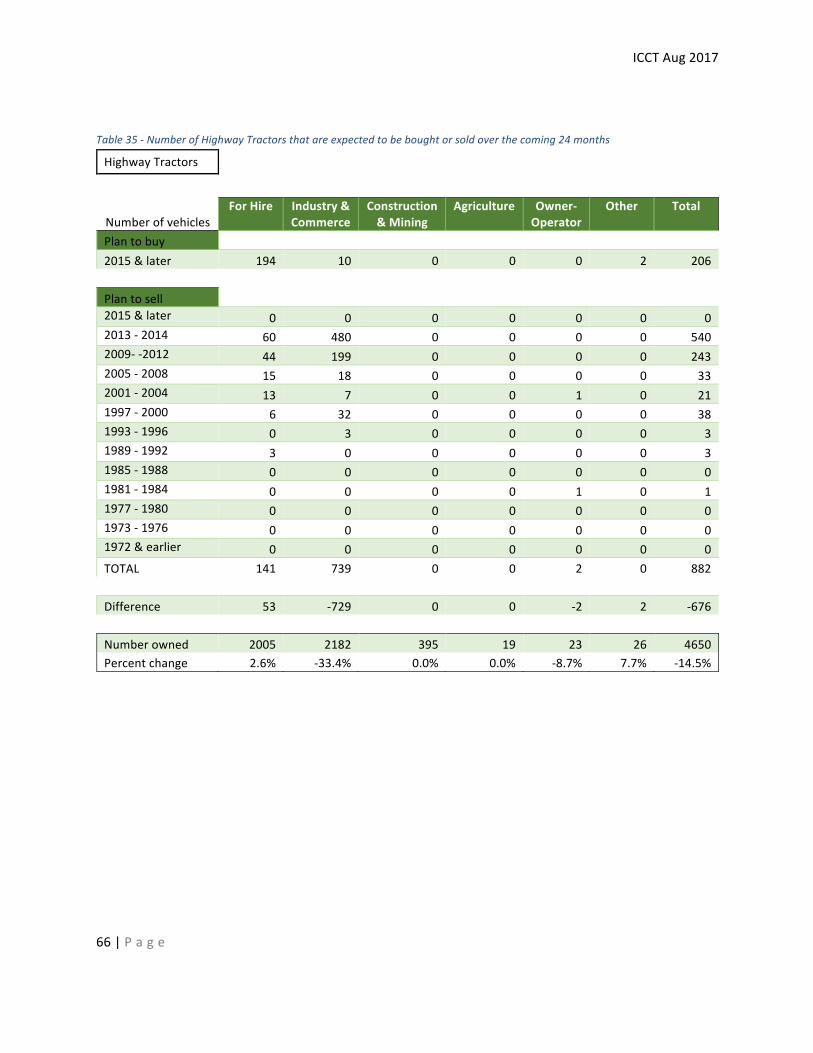

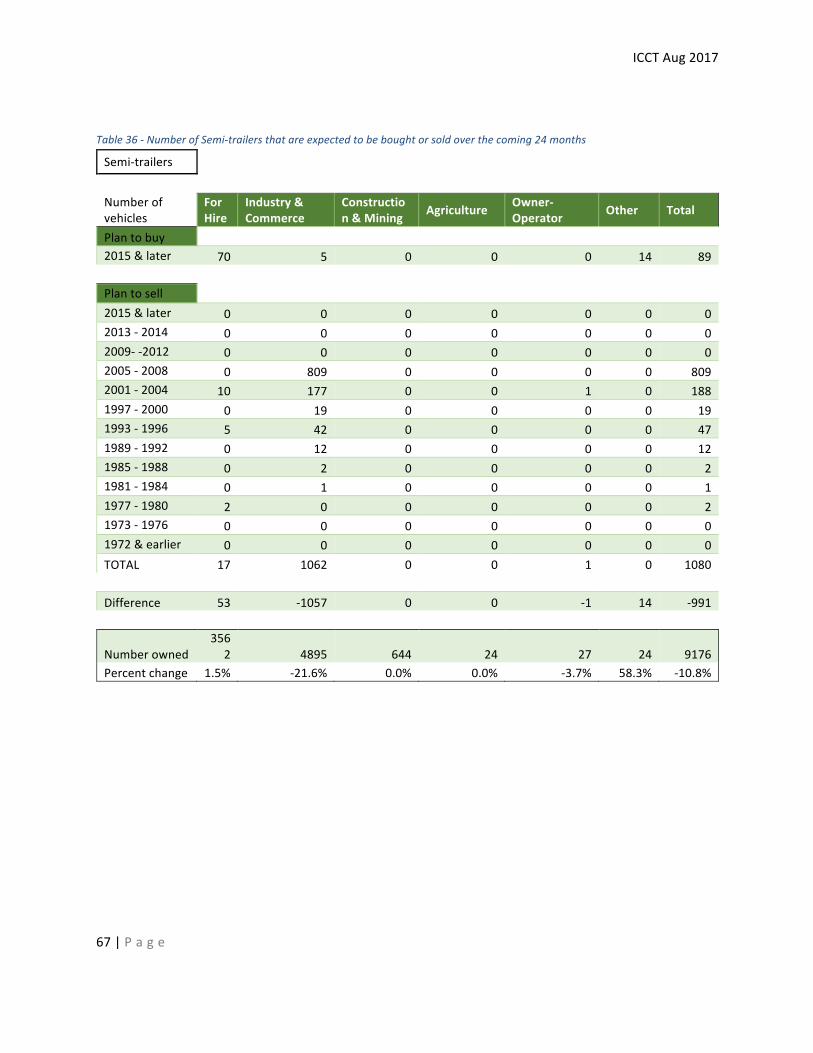

Expectedpurchasesoverthecoming24months..............................................................................65

Chapter5:-Tractor-trailerUsageandOperatingCosts..........................................68

Theroleofthedifferenttypesoffleets.............................................................................................71

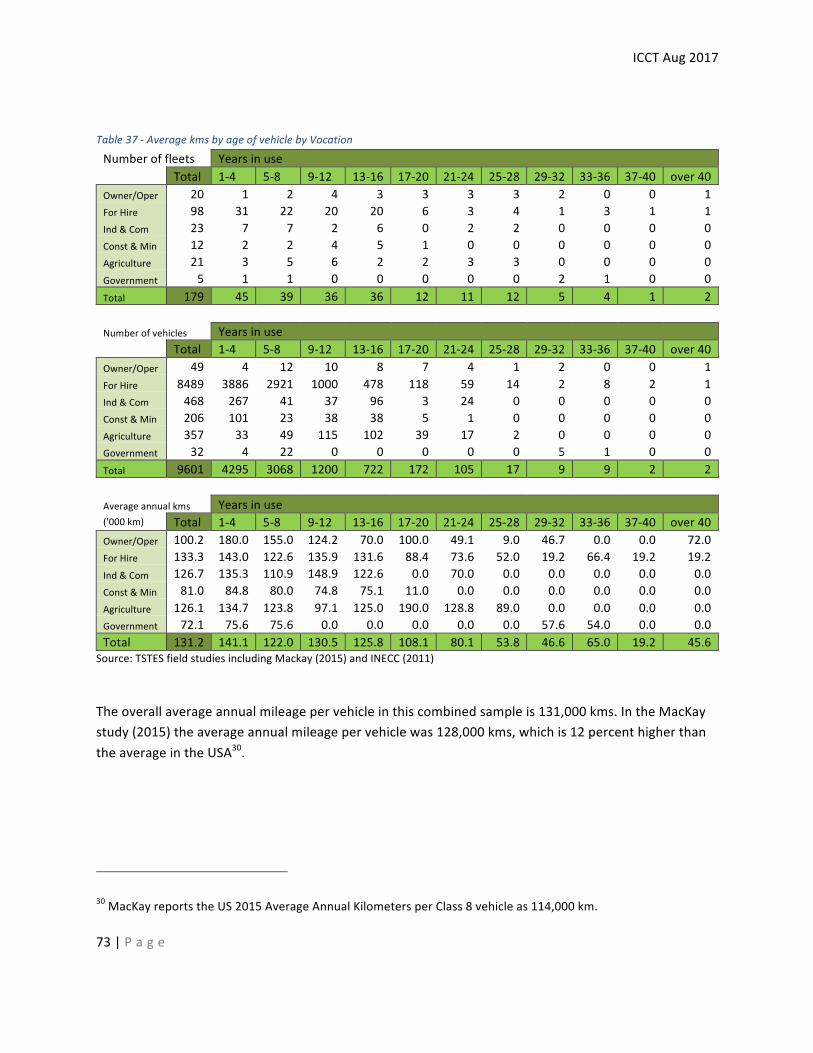

Highwaytractorkilometersperyear..................................................................................................72

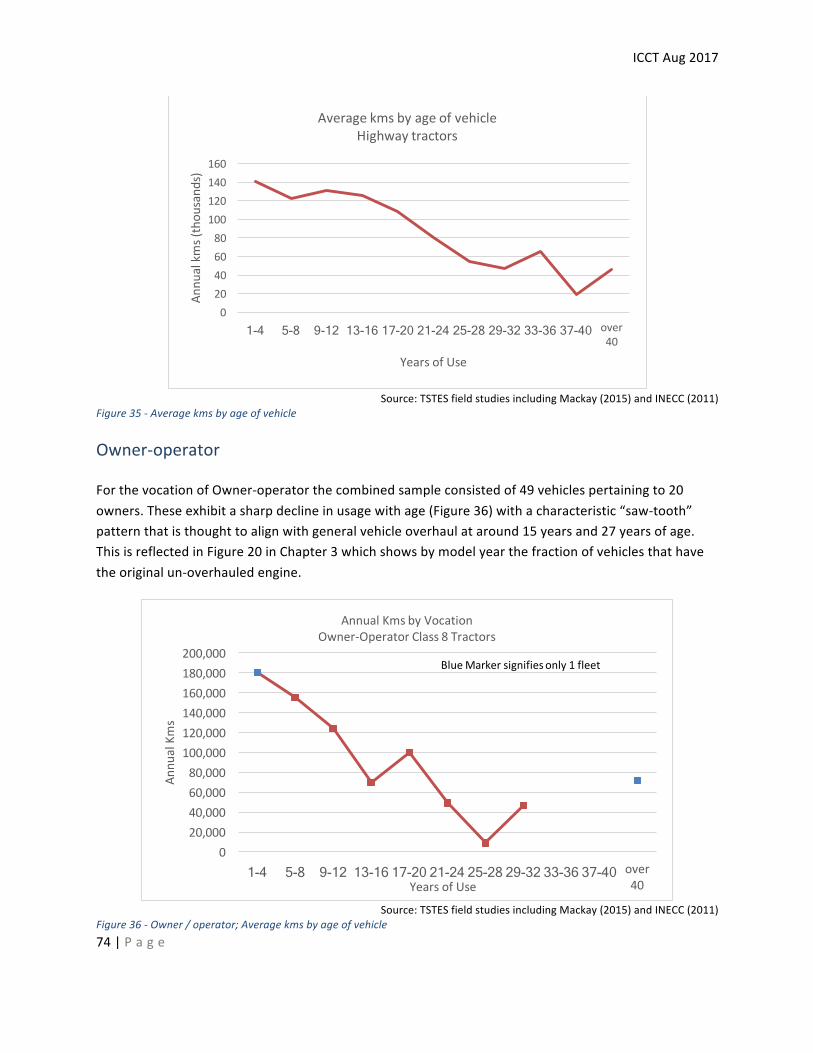

Owner-operator.................................................................................................................................74

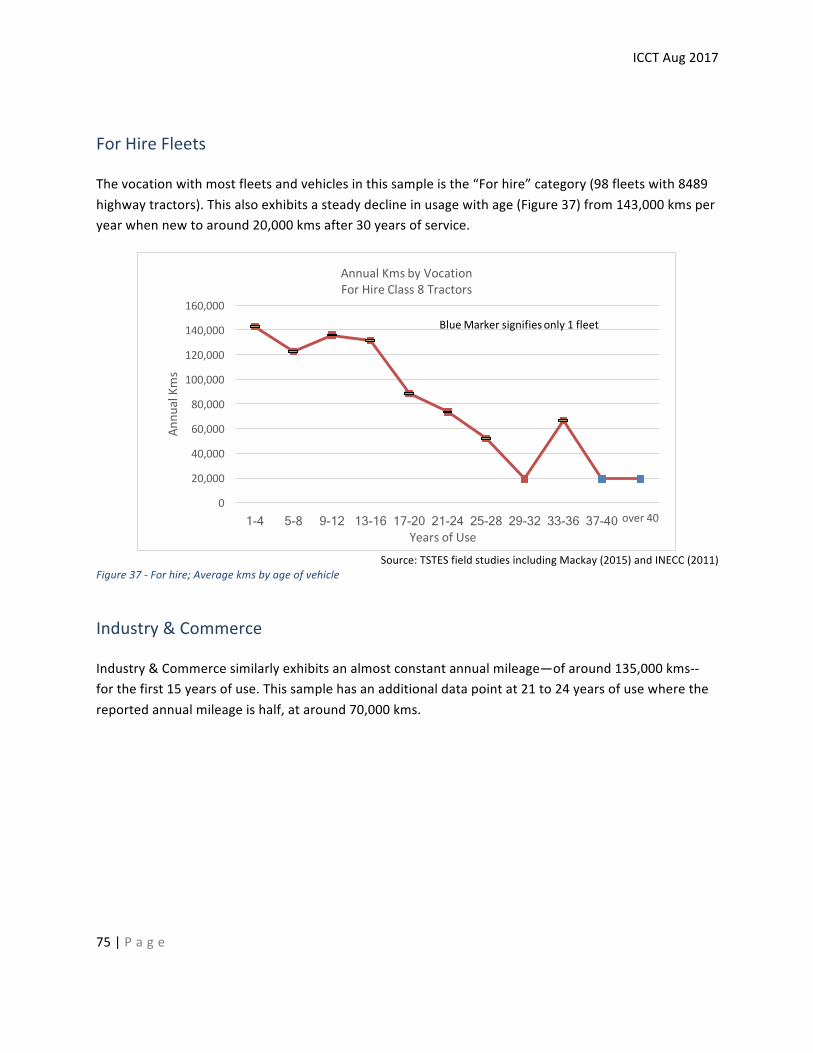

ForHireFleets....................................................................................................................................75

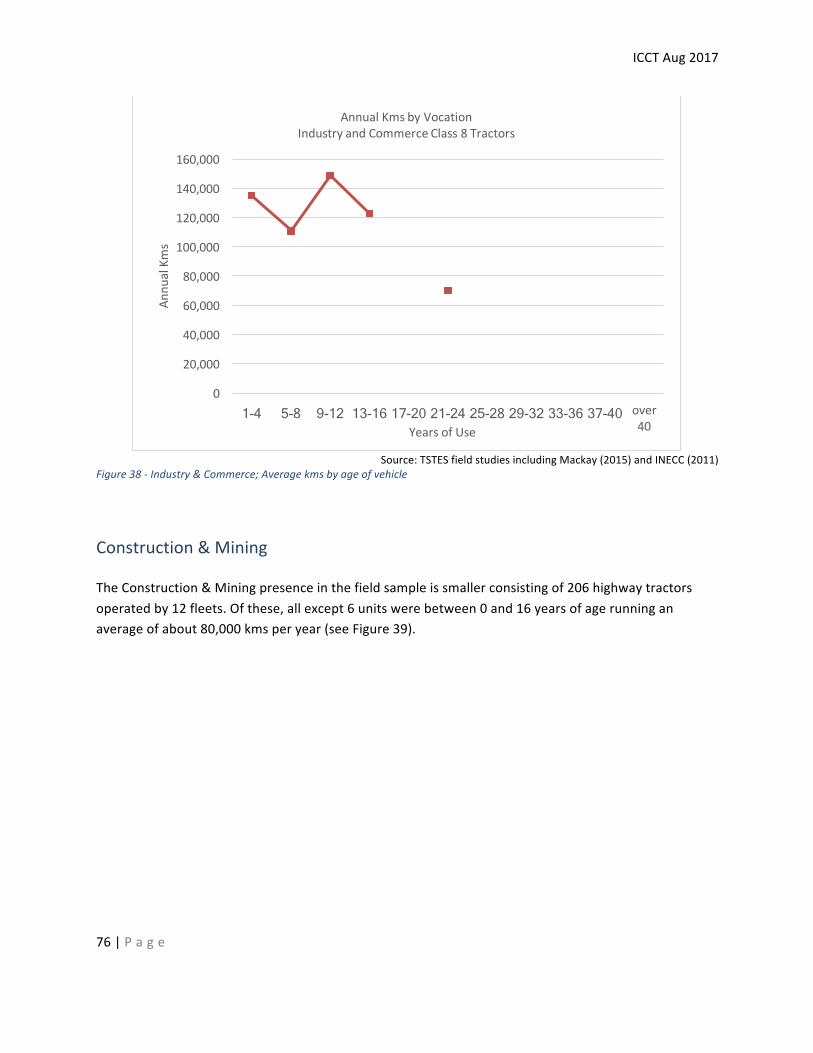

Industry&Commerce........................................................................................................................75

Construction&Mining.......................................................................................................................76

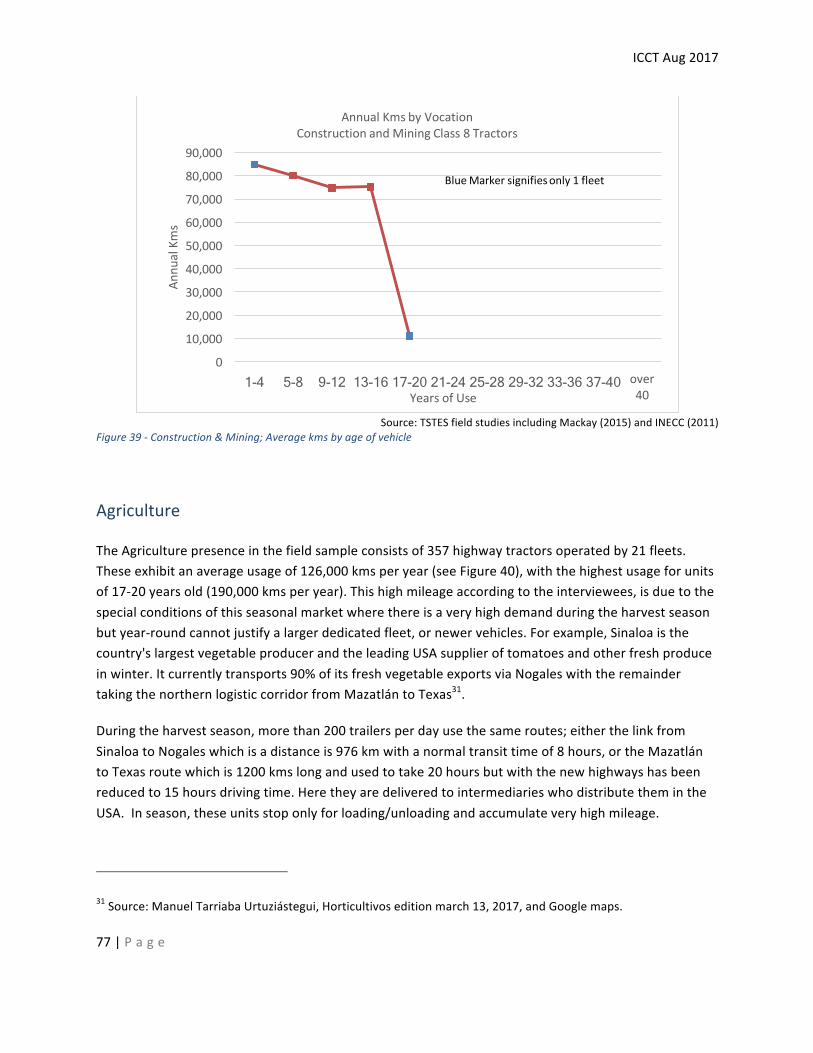

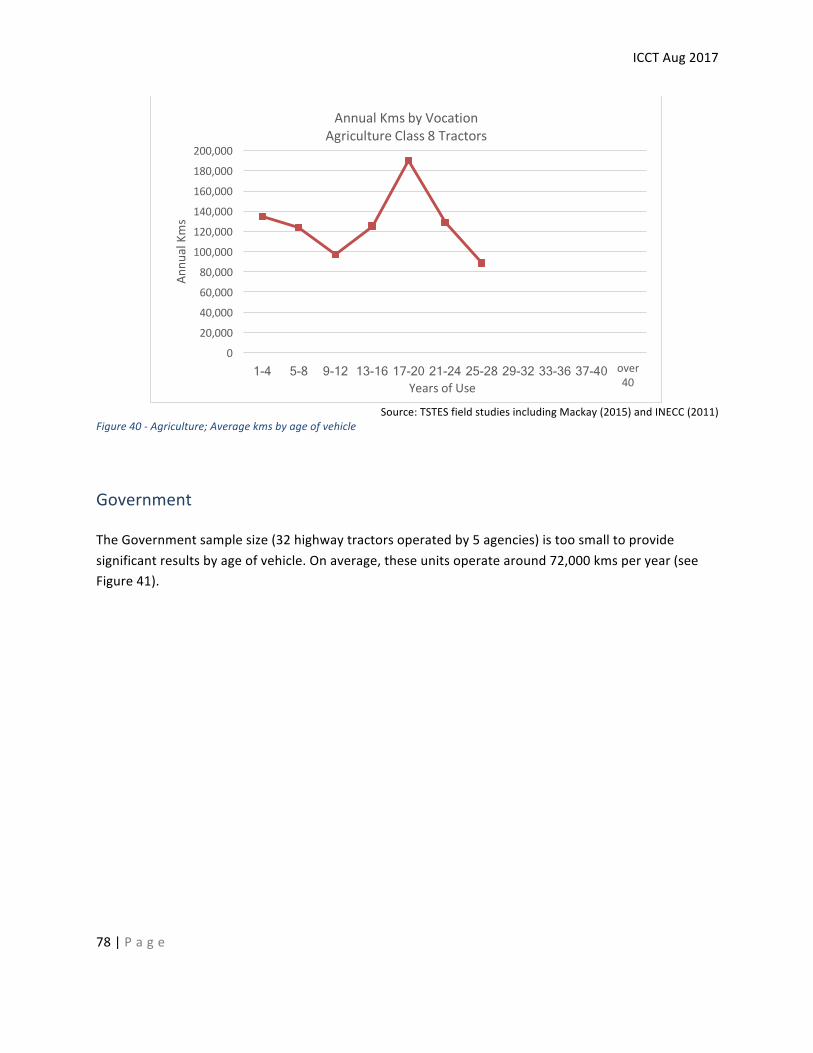

Agriculture..........................................................................................................................................77

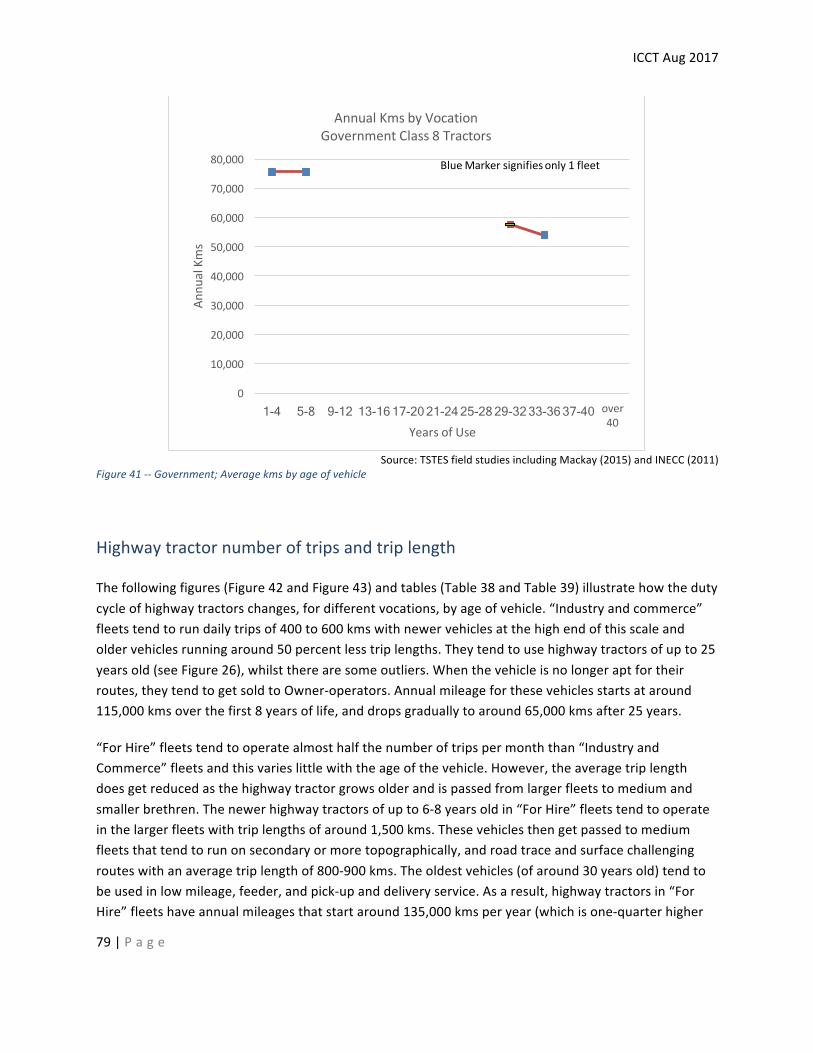

Government.......................................................................................................................................78

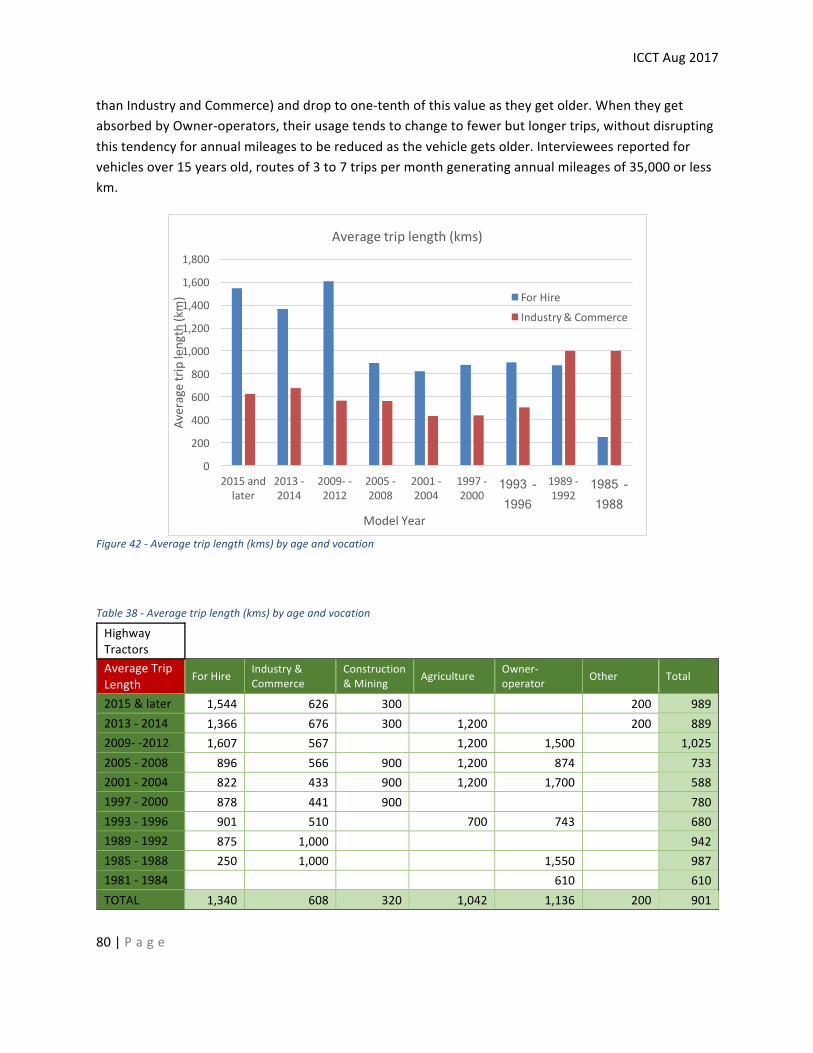

Highwaytractornumberoftripsandtriplength...............................................................................79

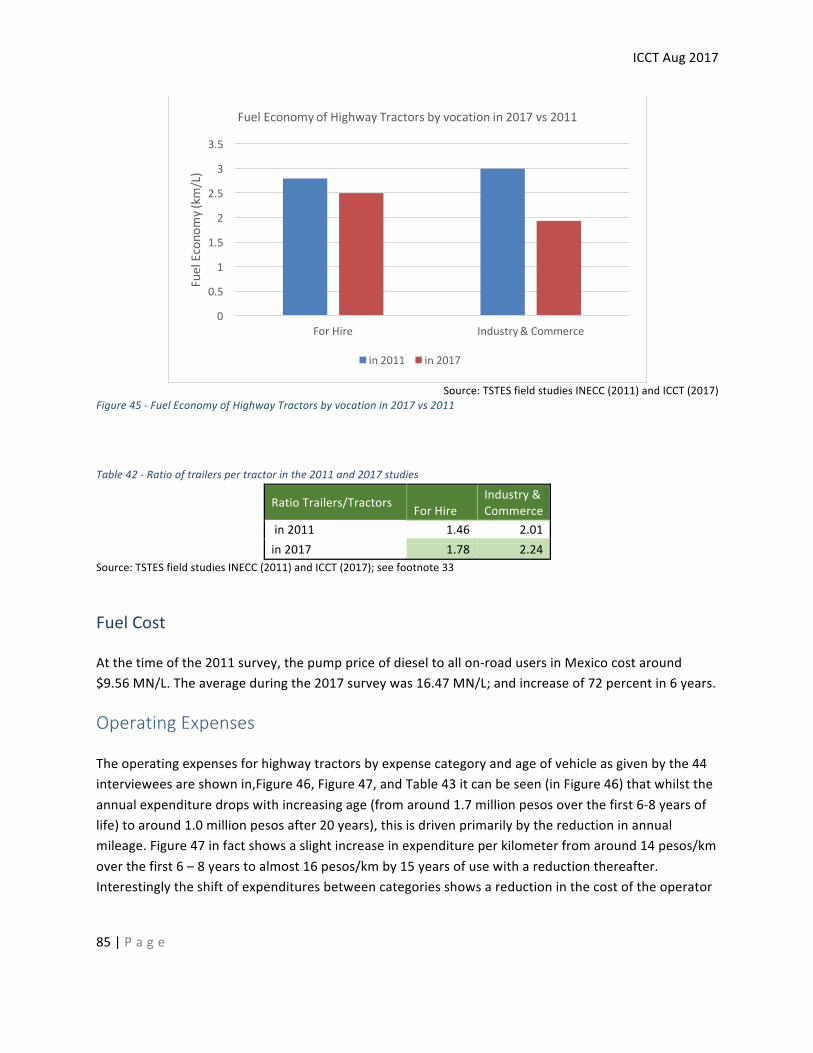

FuelEconomy.....................................................................................................................................81

FuelCost.............................................................................................................................................85

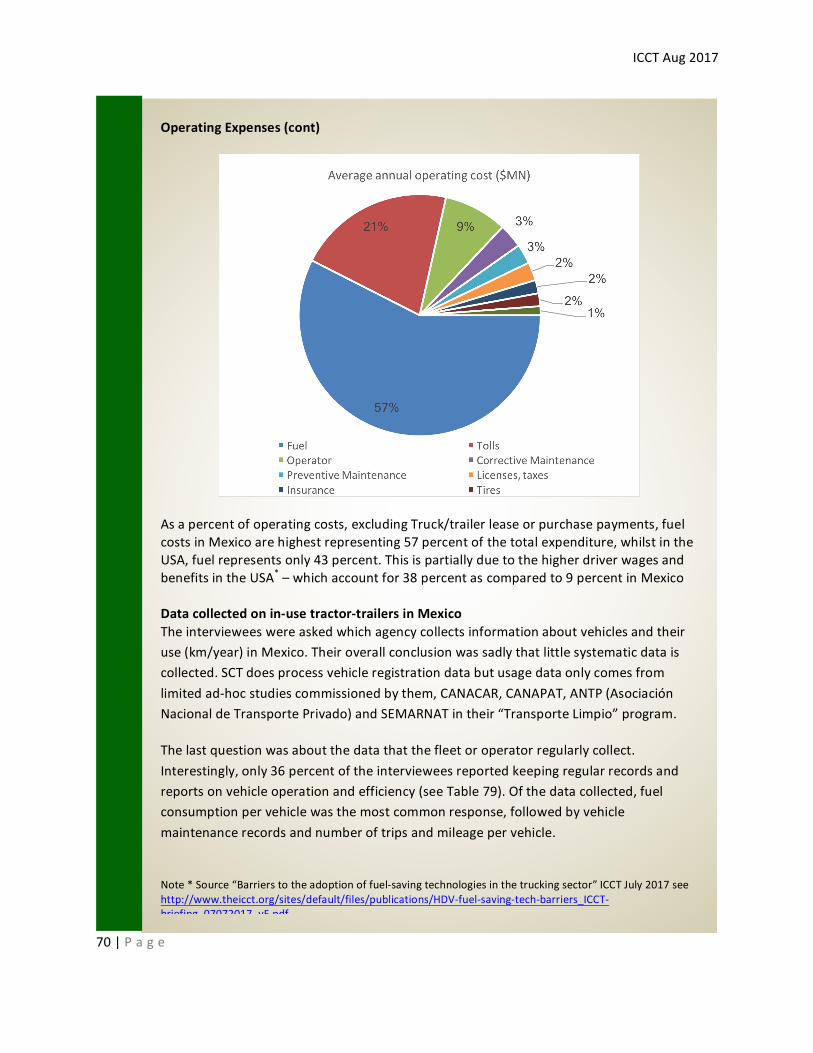

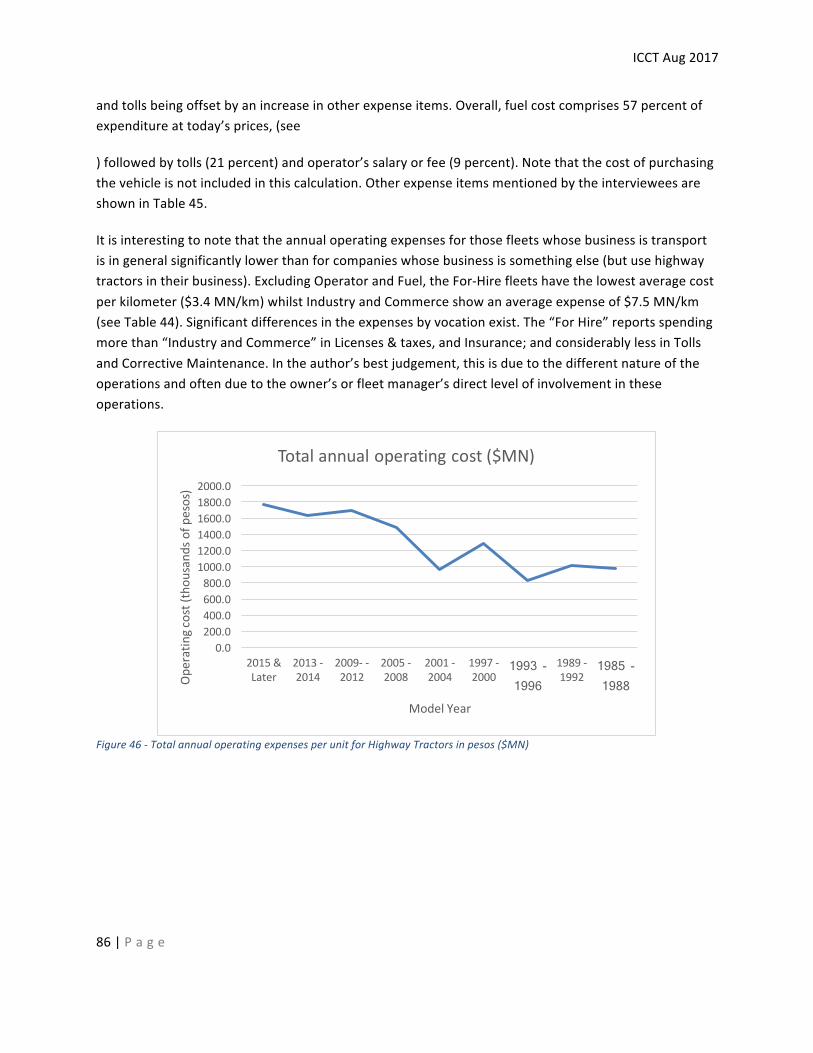

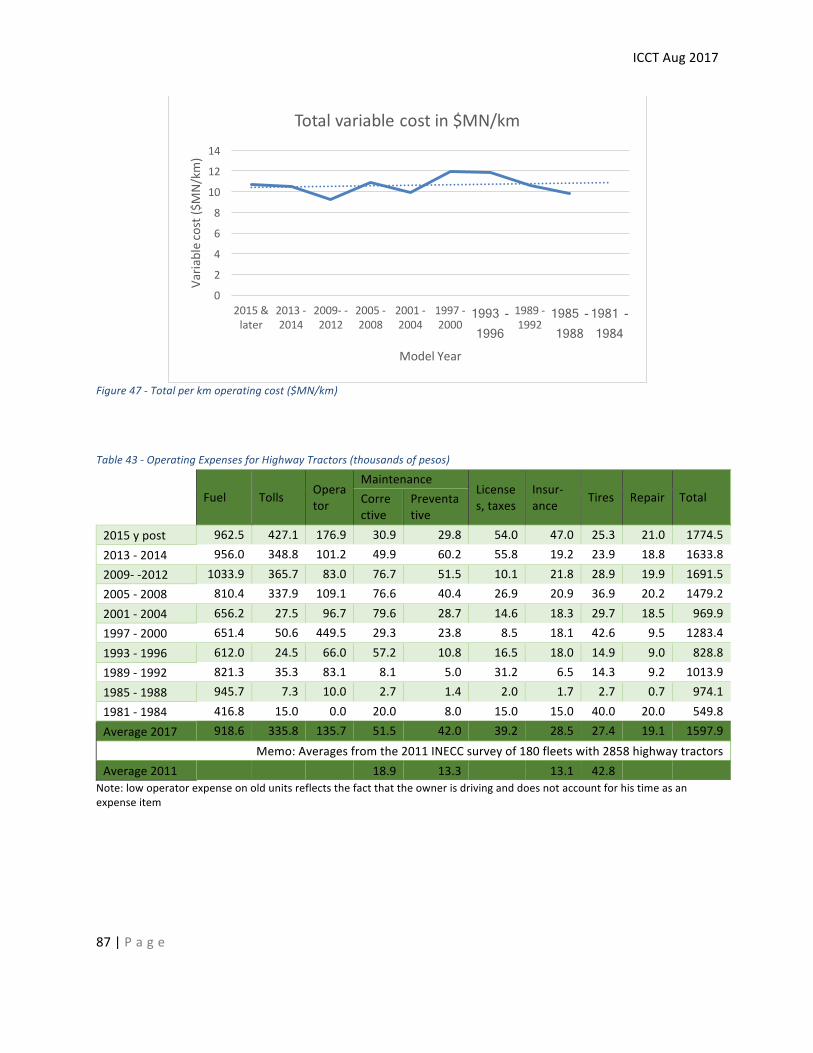

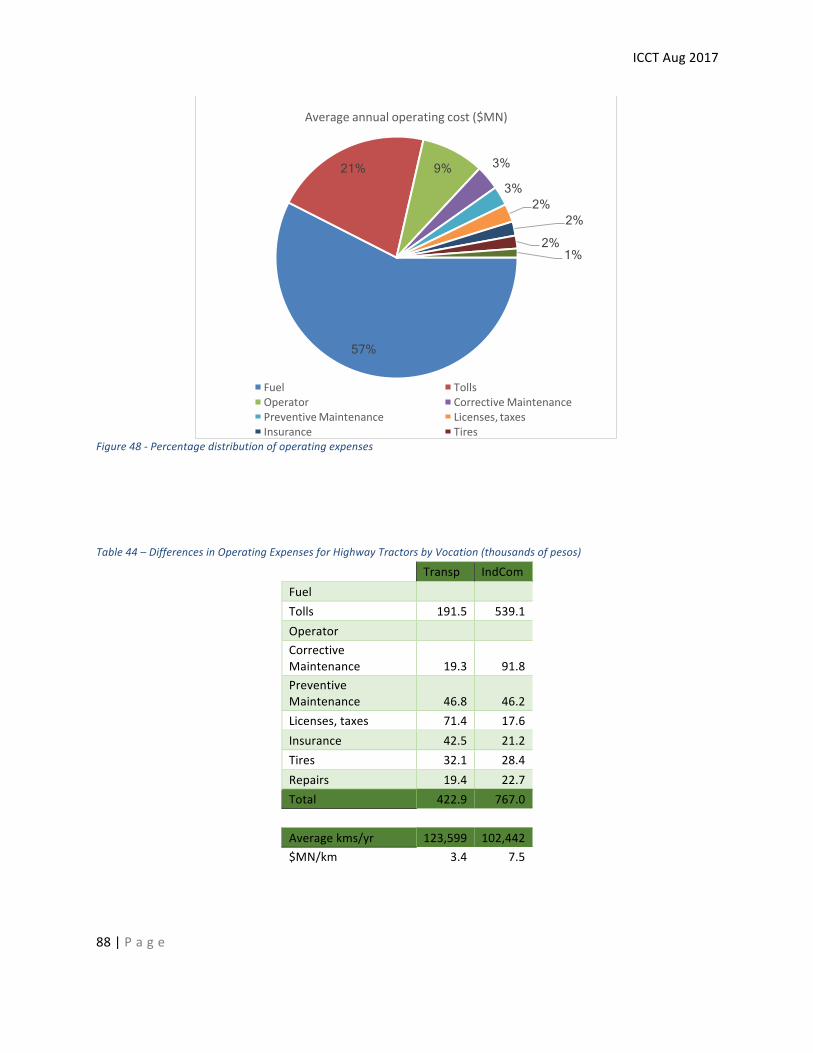

OperatingExpenses................................................................................................................................85

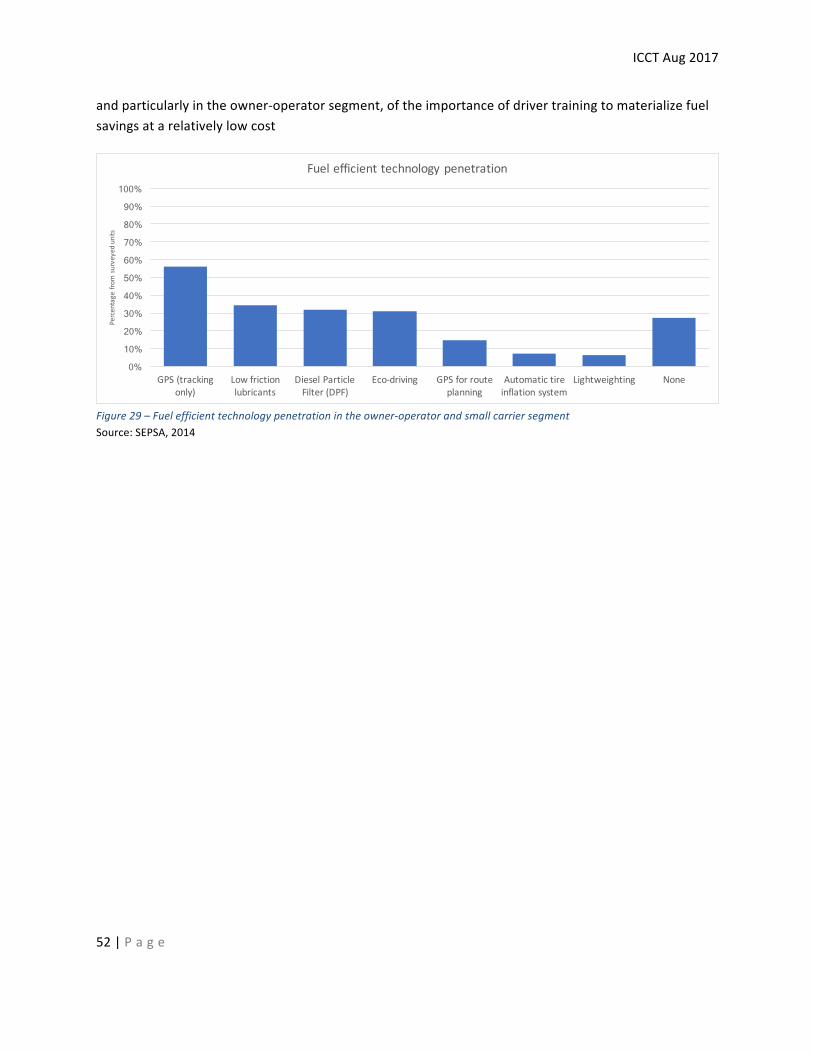

Datacollectedonin-usetractor-trailersinMexico................................................................................89

ICCTAug2017

iv|P a g e

NationalEmissionsRegister(RENE).......................................................................................................90

Chapter6:-Tariffs,FreighttypeandLogistics........................................................92

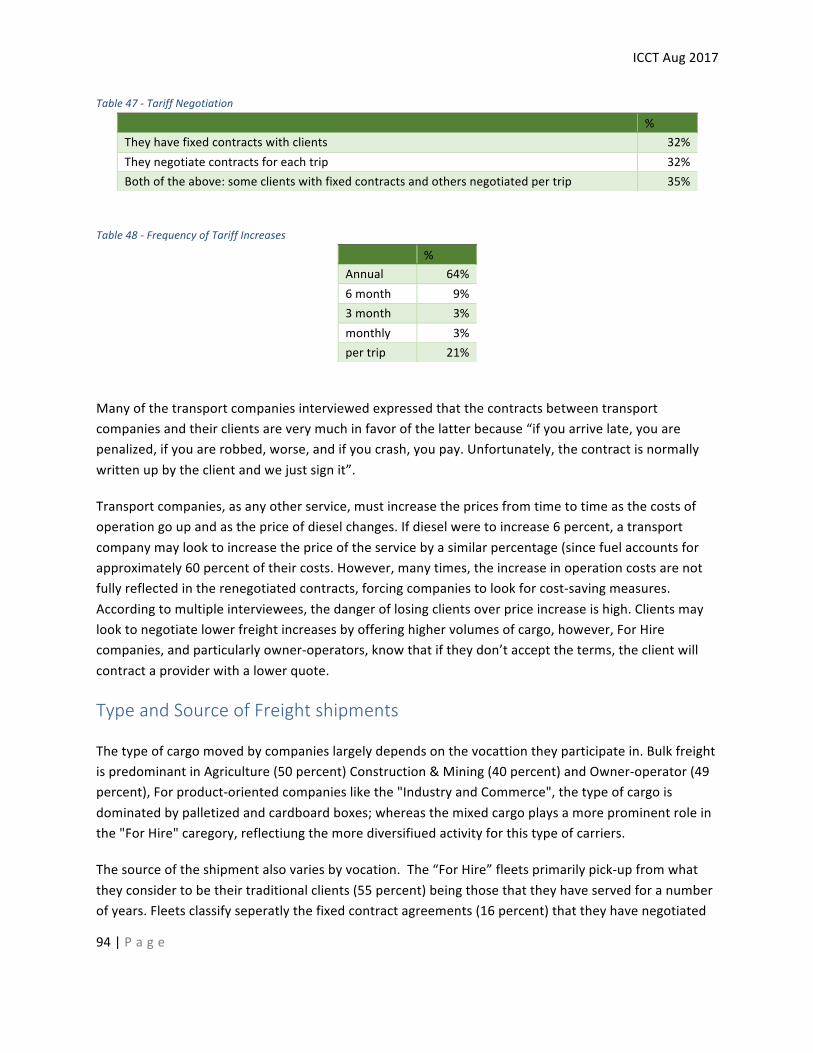

TariffNegotiationandIncreases........................................................................................................93

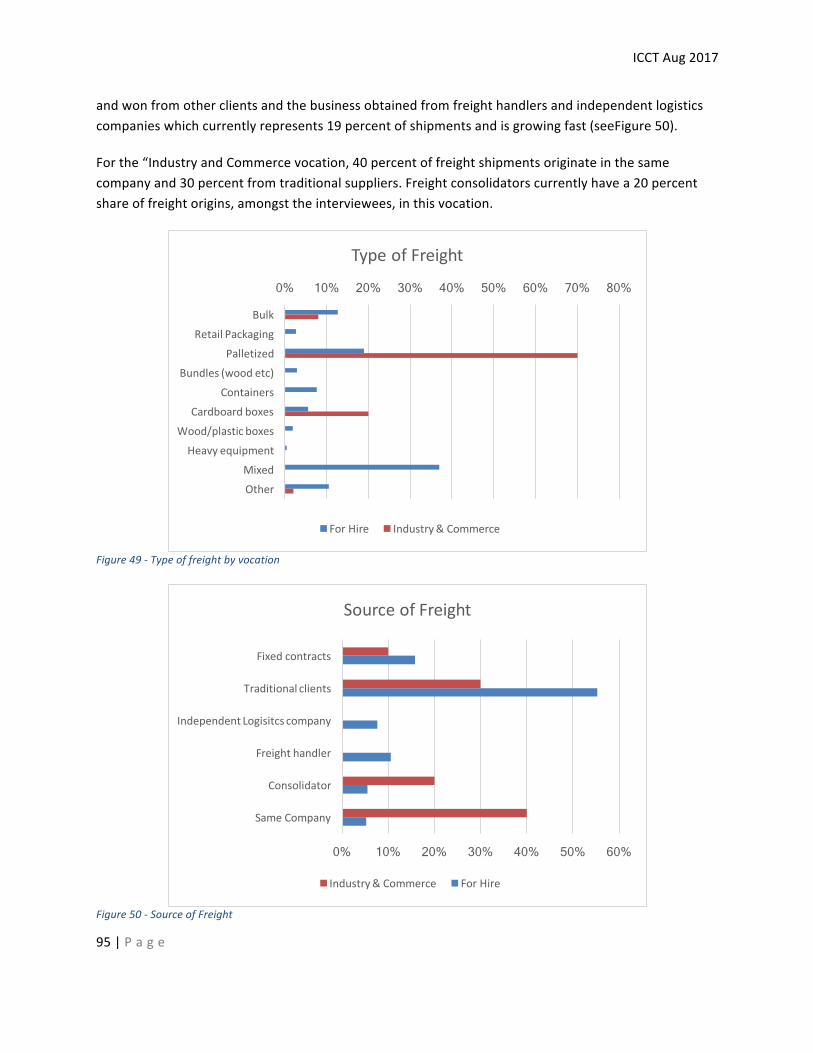

TypeandSourceofFreightshipments...................................................................................................94

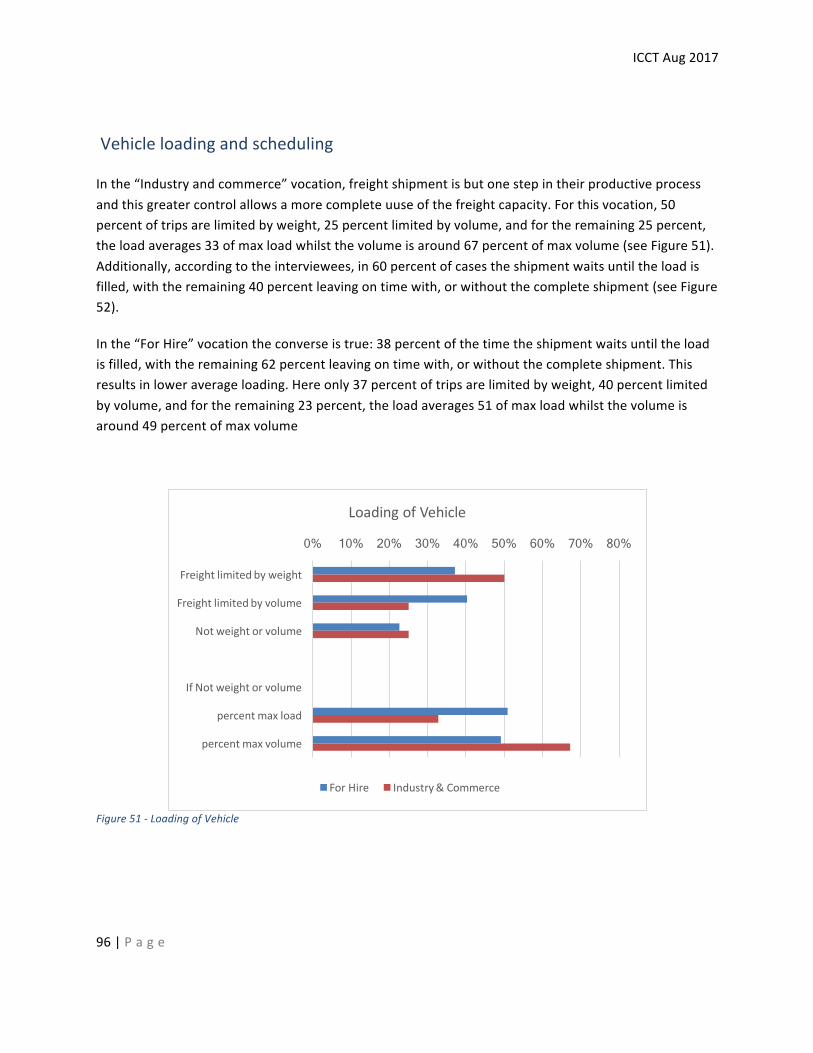

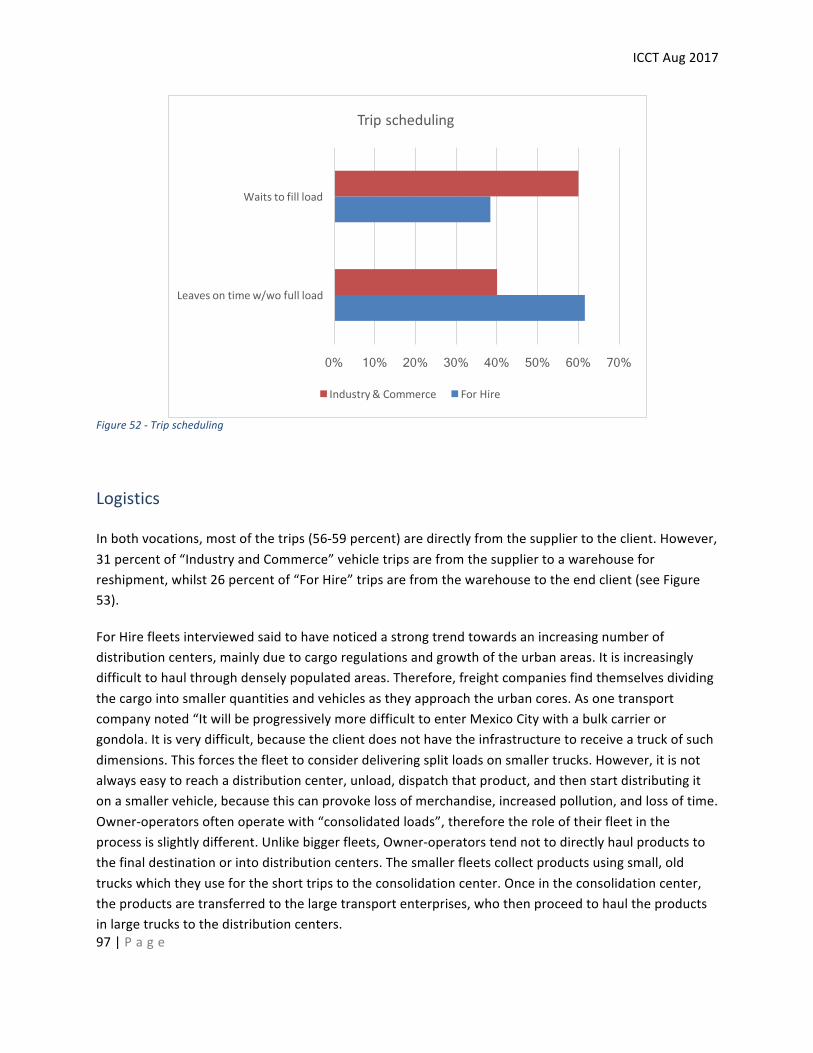

Vehicleloadingandscheduling..........................................................................................................96

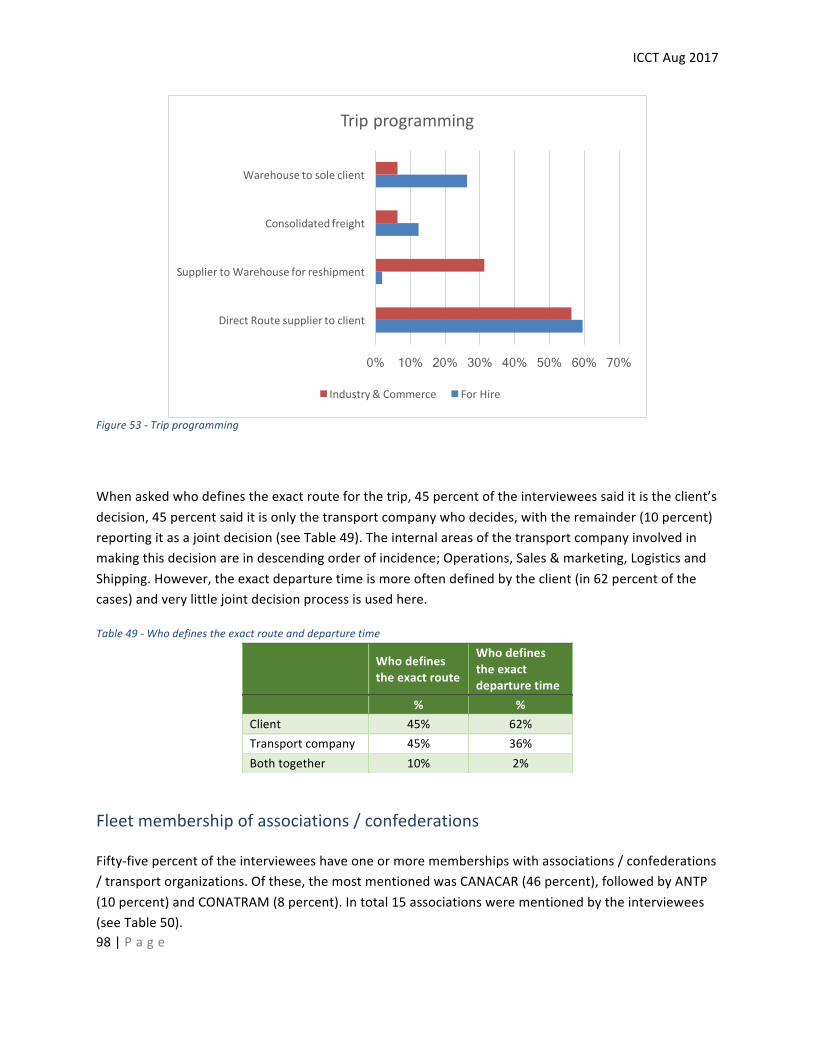

Logistics..............................................................................................................................................97

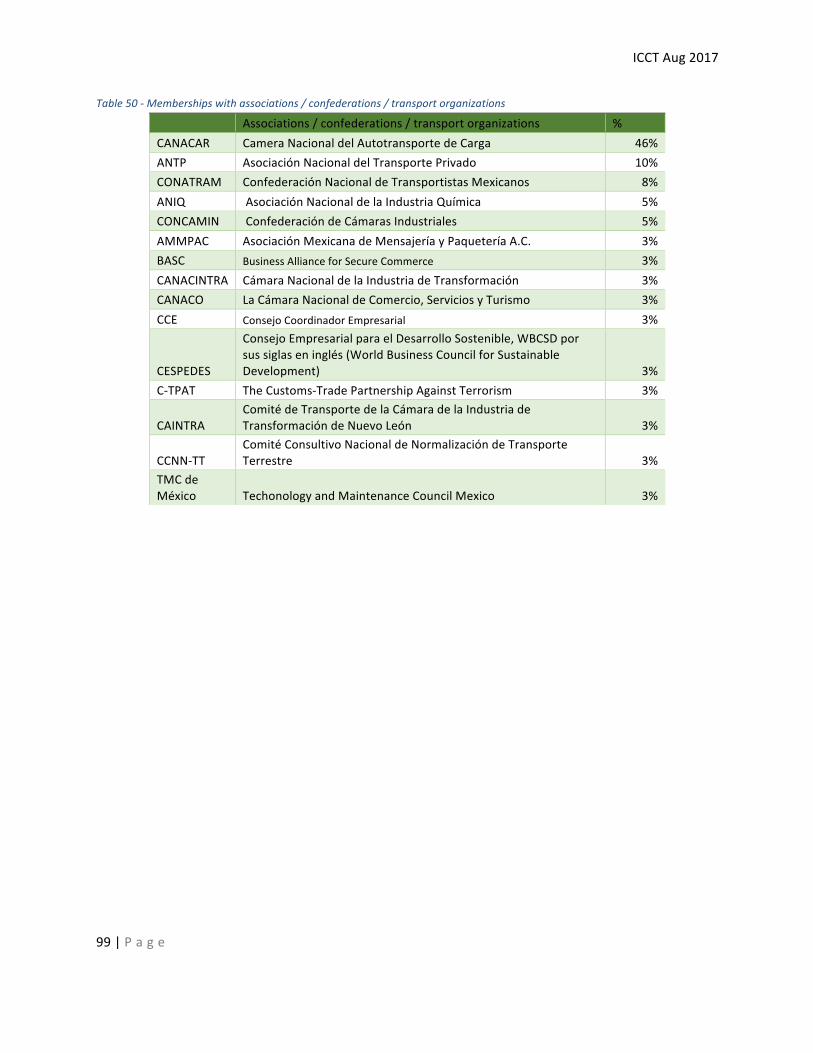

Fleetmembershipofassociations/confederations..........................................................................98

Chapter7:-InstitutionalandRegulatoryFramework...........................................100

ImpactofDeregulation........................................................................................................................100

PresentRegulation...............................................................................................................................101

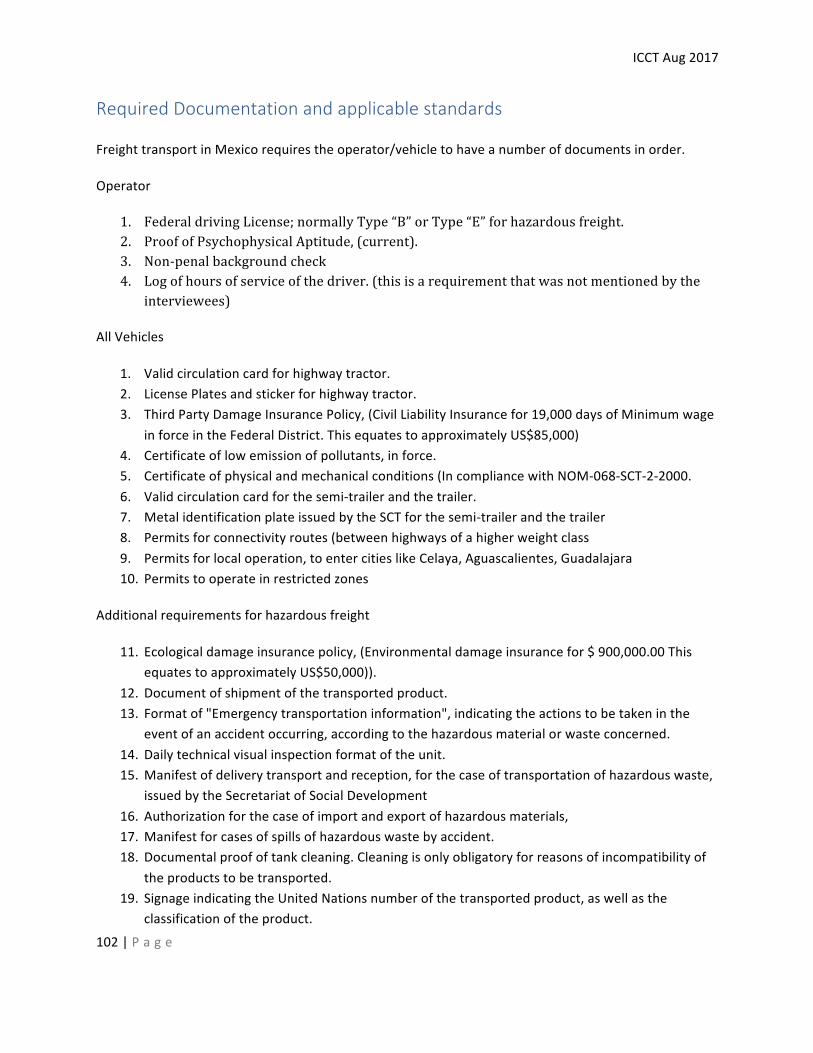

RequiredDocumentationandapplicablestandards............................................................................102

On-roadtransportpolicies(currentandfuture)..................................................................................104

Opportunitiesforapolicyframeworktopromotethegrowthofcleanfreight...............................105

Chapter8:-ProgramadeTransporteLimpioandrelatedprograms....................108

Currentpoliciesandprograms.............................................................................................................110

TransporteLimpio................................................................................................................................110

PurposeofTransporteLimpio..........................................................................................................110

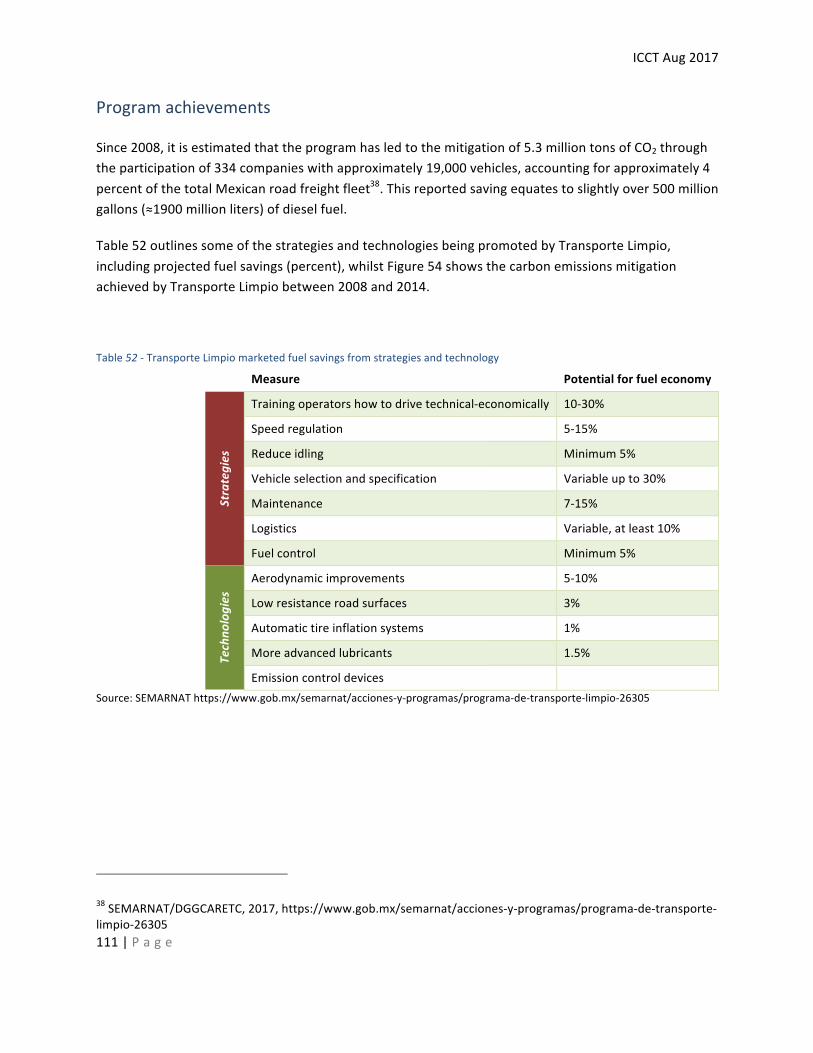

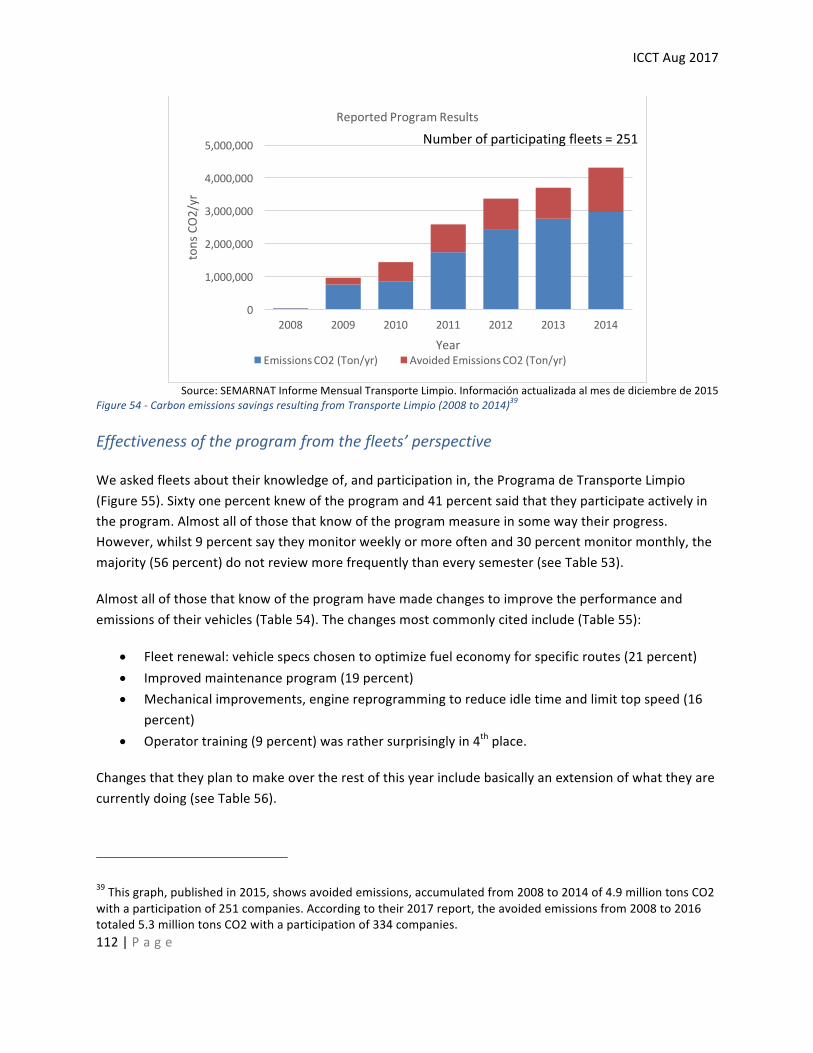

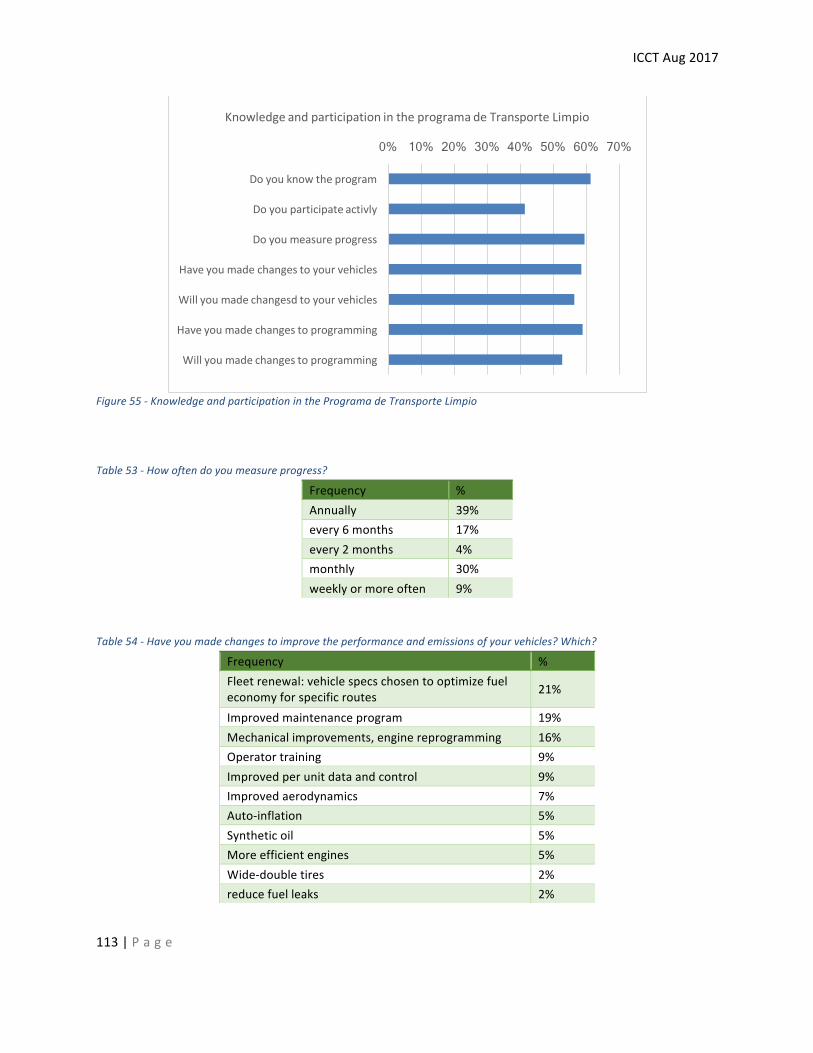

Programachievements....................................................................................................................111

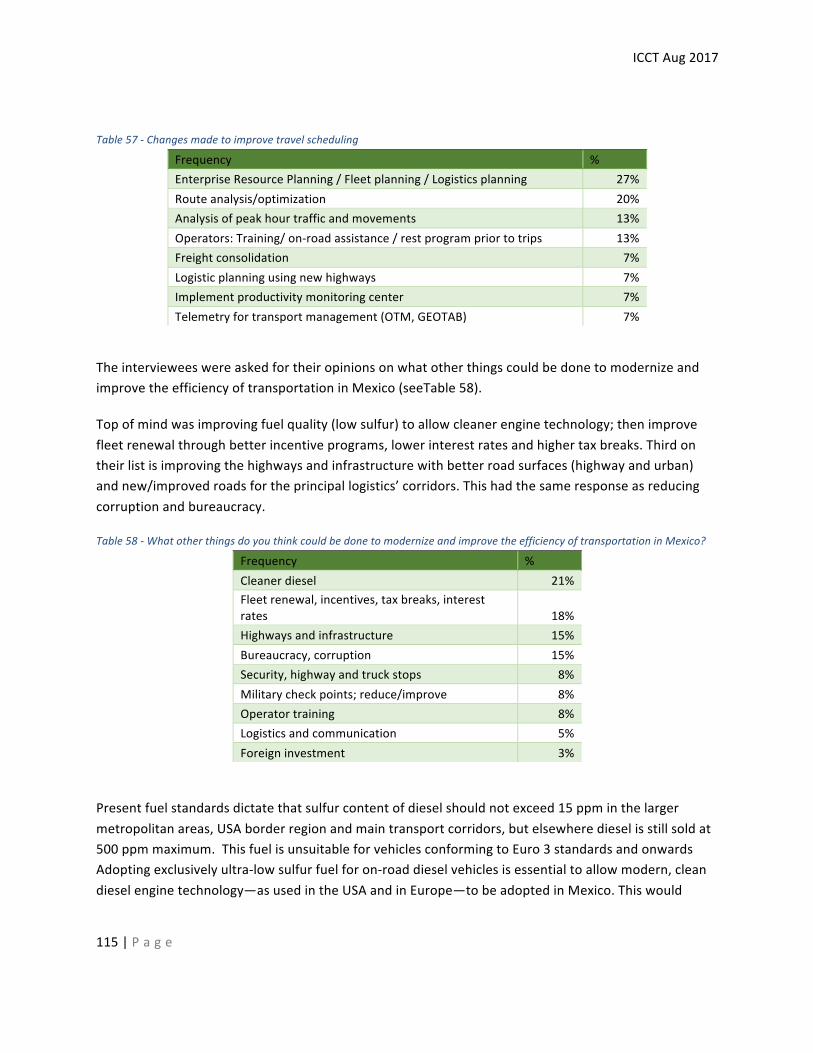

Challengesandbarriers....................................................................................................................116

Areasforfuturedevelopment..............................................................................................................119

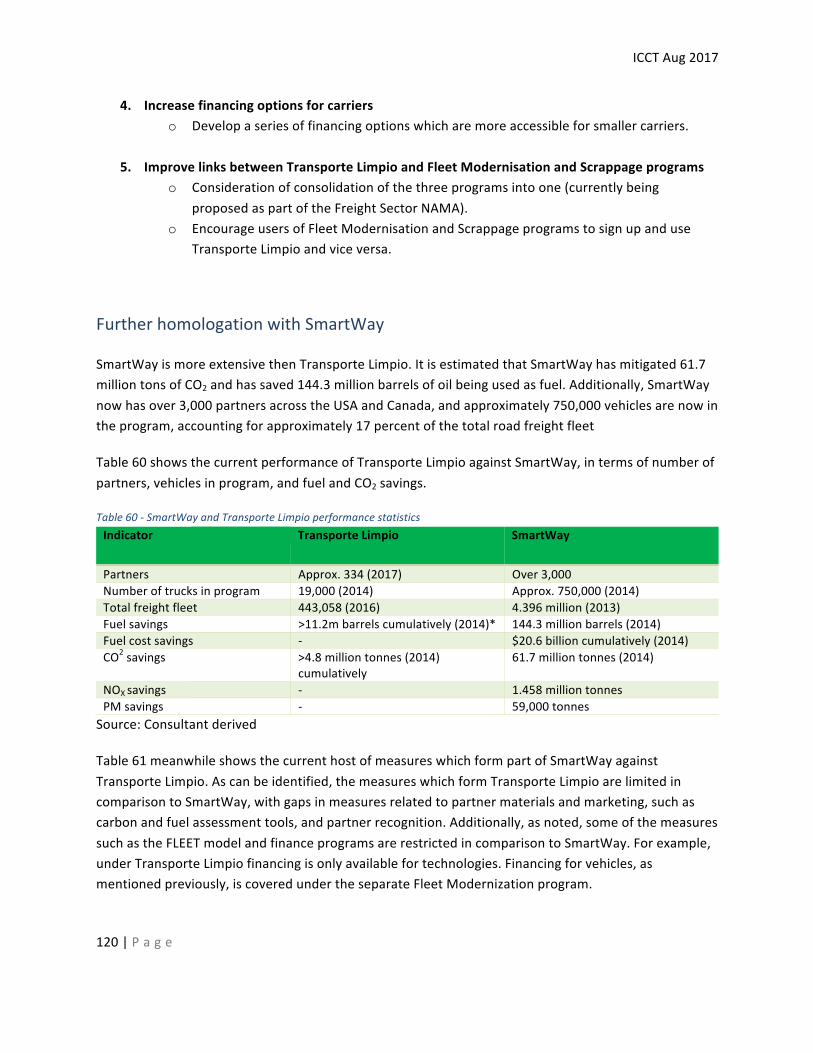

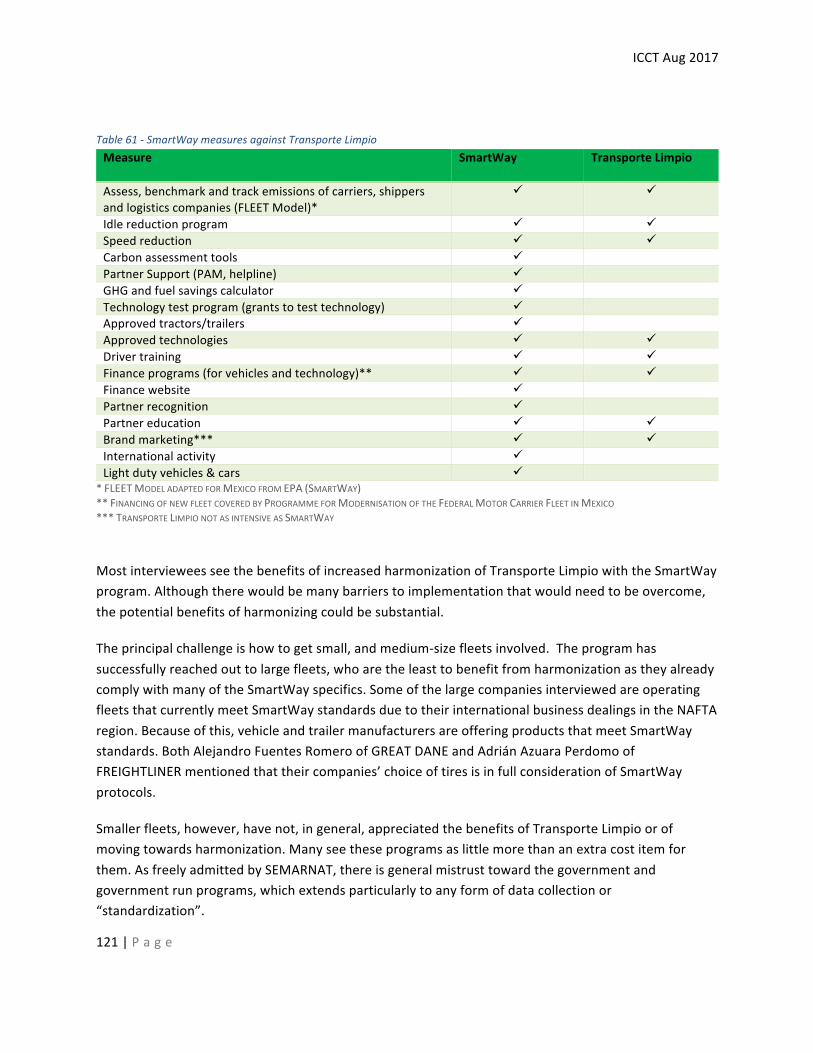

FurtherhomologationwithSmartWay............................................................................................120

HowfarcanTransporteLimpiogointhenext10years...................................................................122

ProgramfortheModernizationoftheFederalMotorCarrierFleet....................................................122

Challengesandbarriers....................................................................................................................123

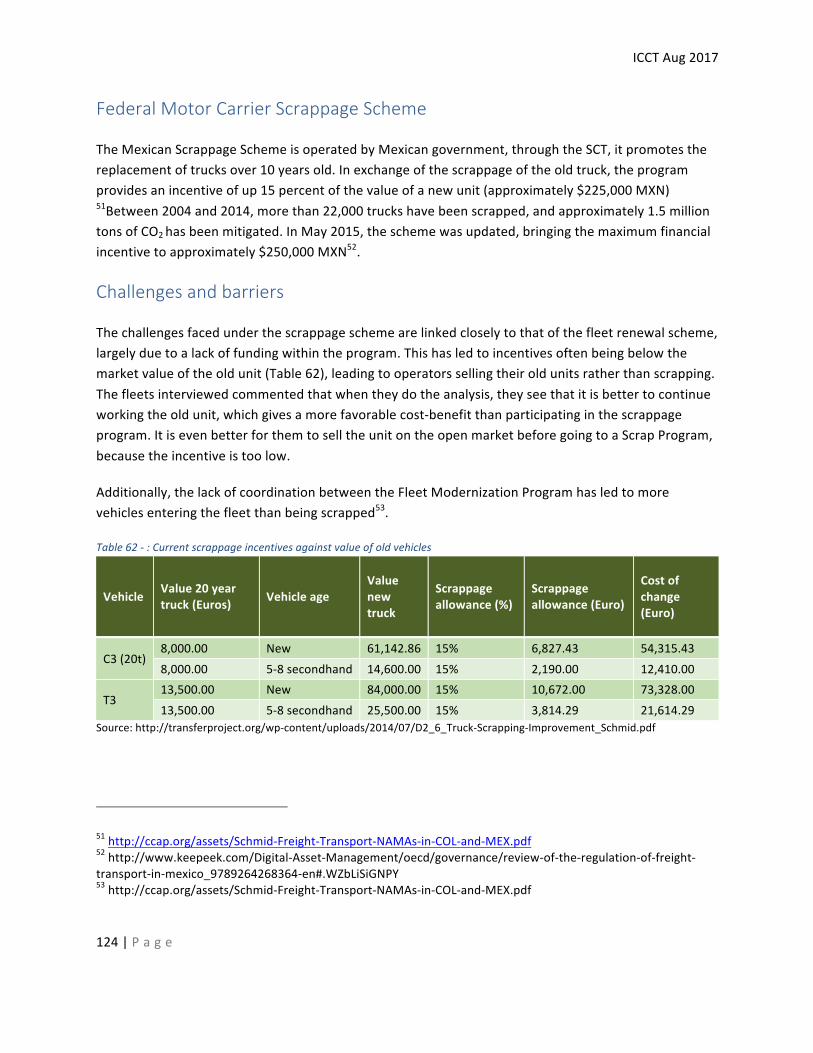

FederalMotorCarrierScrappageScheme...........................................................................................124

Challengesandbarriers........................................................................................................................124

Futurepoliciesandprograms...............................................................................................................125

MexicanOfficialStandardNOM-044................................................................................................125

FederalRoadFreightTransportNAMA(forowneroperatorsandsmallerfleetcarriers)...............126

ICCTAug2017

v|P a g e

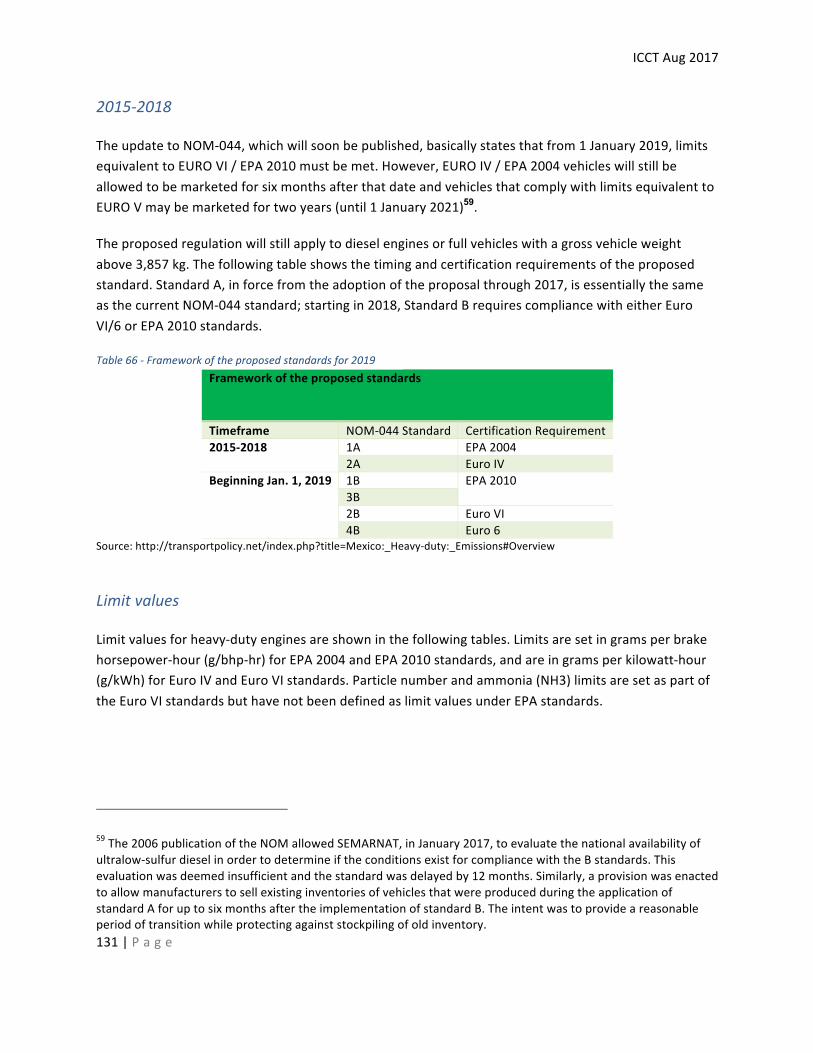

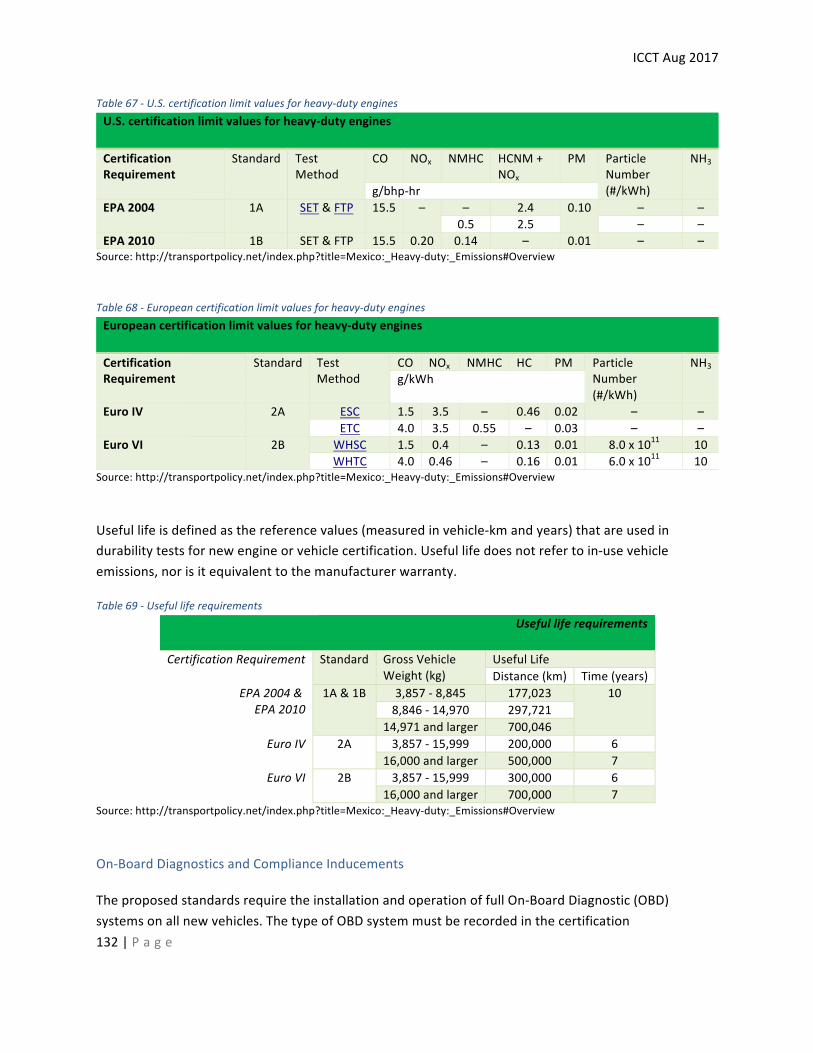

Chapter9:-Fuelefficiencyandemissionsstandards...........................................127

EmissionstandardsfornewheavydutydieselvehiclesinMexico......................................................128

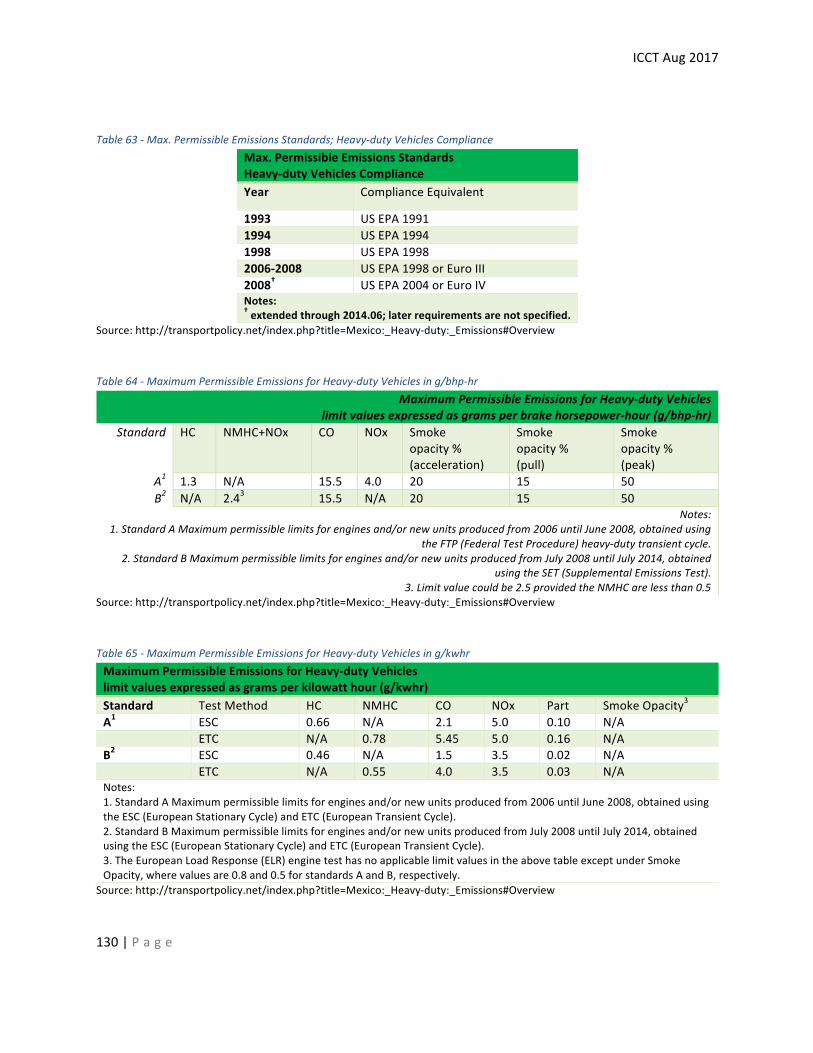

DieselEngineStandards...................................................................................................................129

EmissionstandardsforIn-useHeavyDutydieselvehiclesinMexico..................................................133

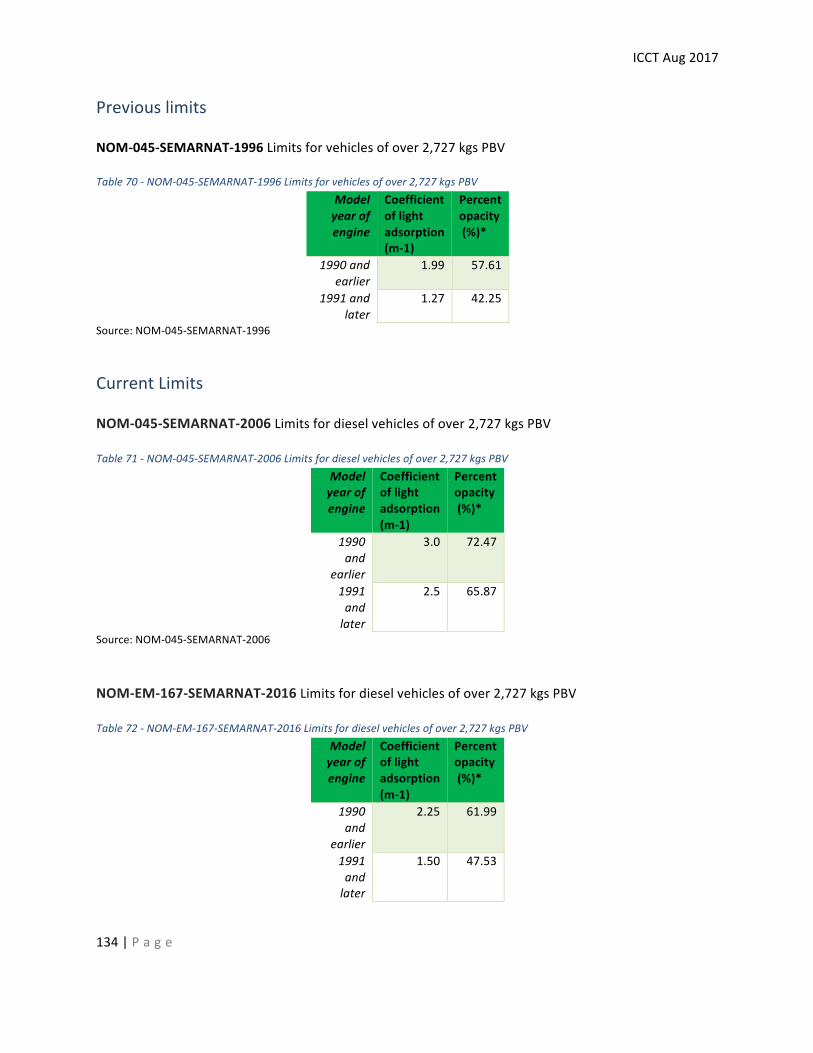

Previouslimits..................................................................................................................................134

CurrentLimits...................................................................................................................................134

Testprocedure.................................................................................................................................135

TestFrequency.................................................................................................................................135

TestFacilities....................................................................................................................................135

TestEffectiveness.............................................................................................................................135

TestResults......................................................................................................................................136

FuelefficiencystandardsintheUSA................................................................................................136

ANNEX:.................................................................................................................138

ApproachandMethodology................................................................................138

a) Informationavailablefrompublicsources...................................................................................138

b) InformationavailablefrompreviousstudiesconductedbyTSTES..............................................139

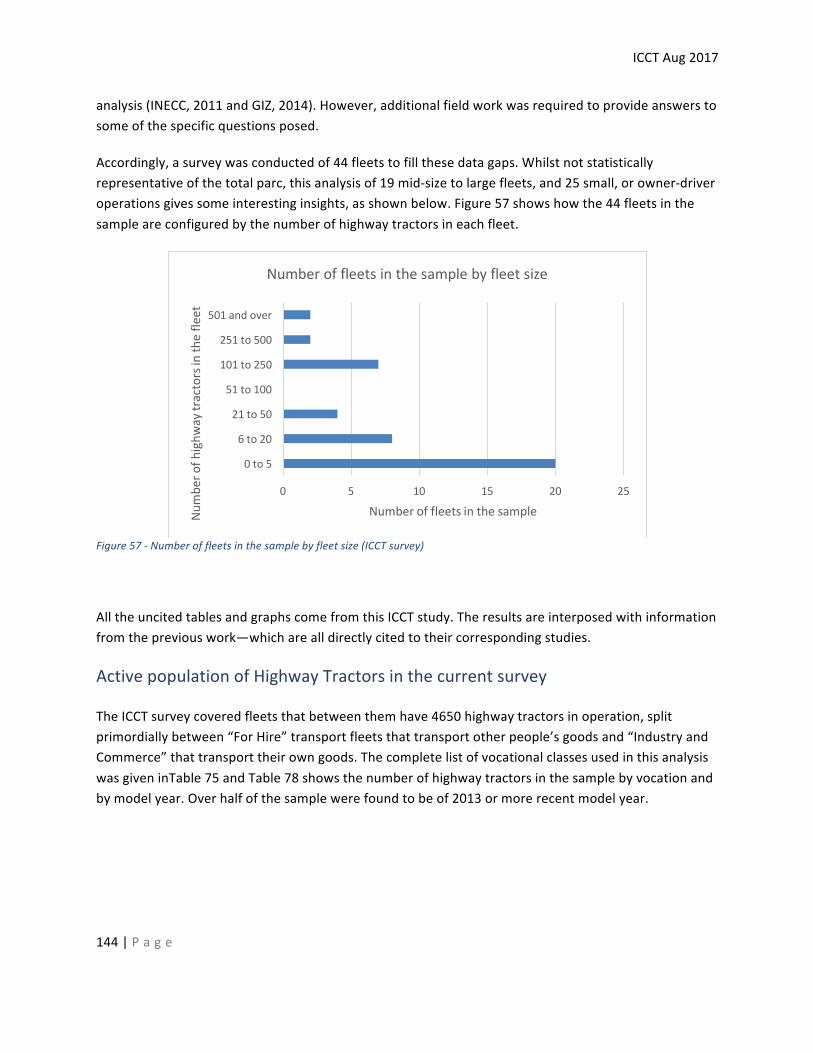

c) Newfieldsurveyandinterviewdata............................................................................................140

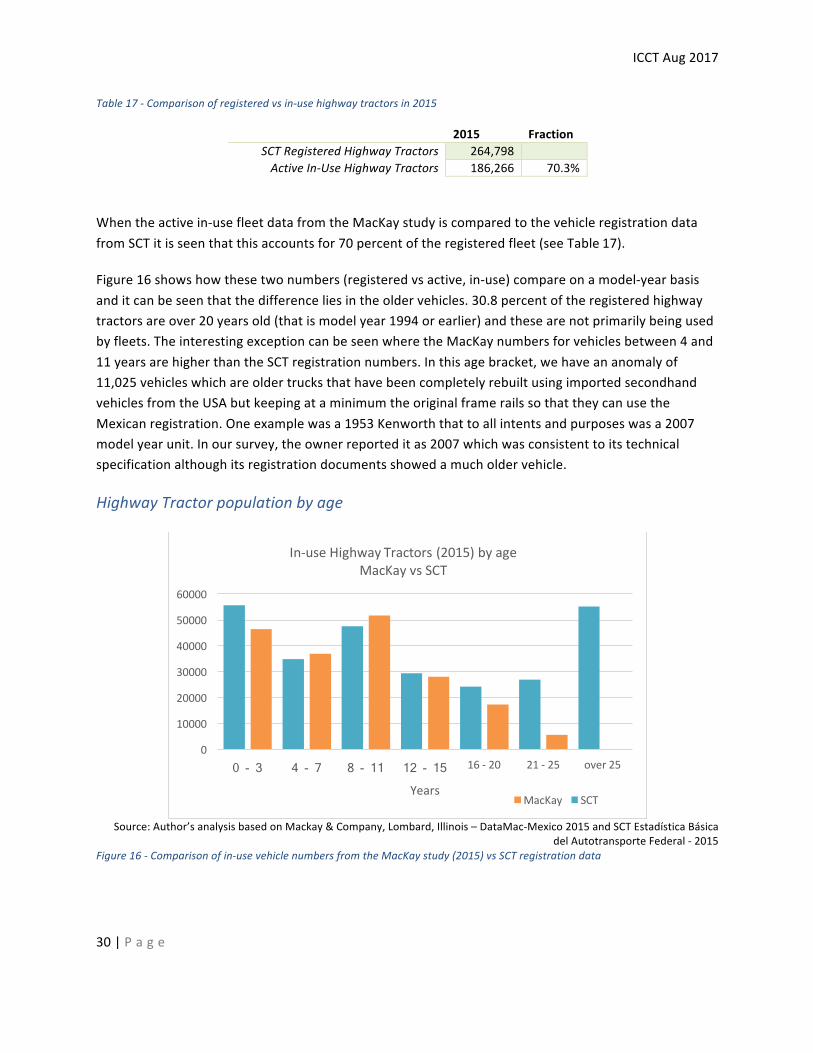

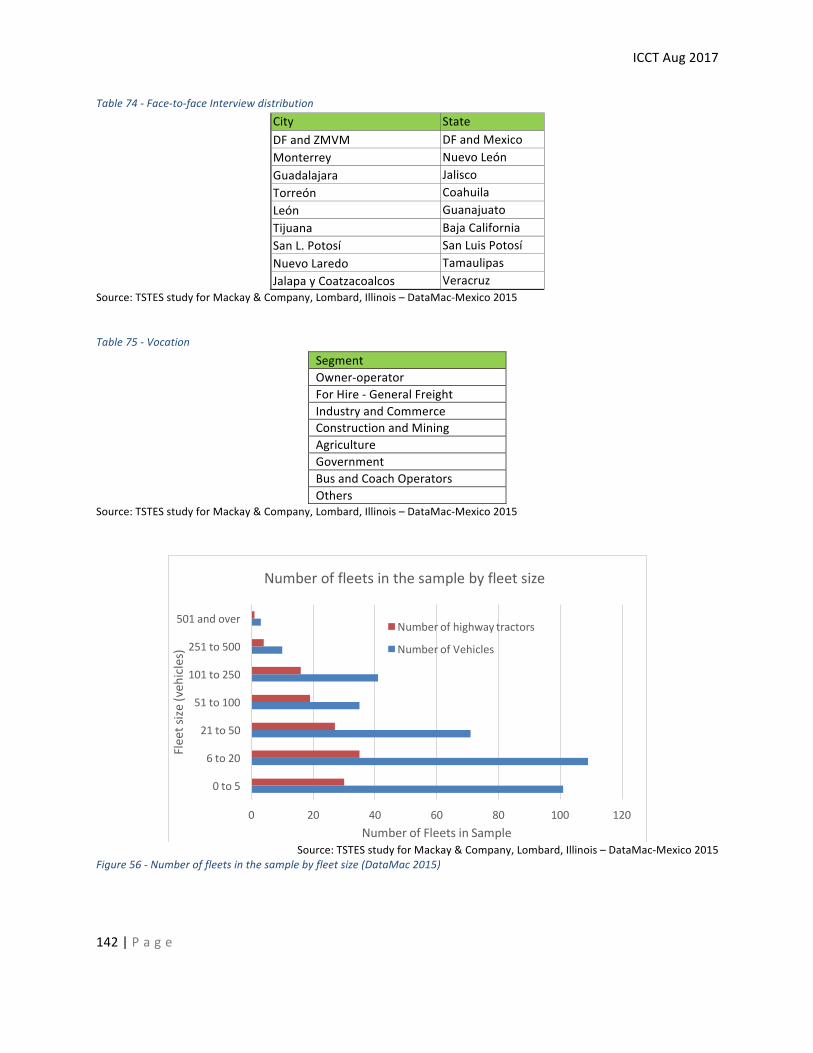

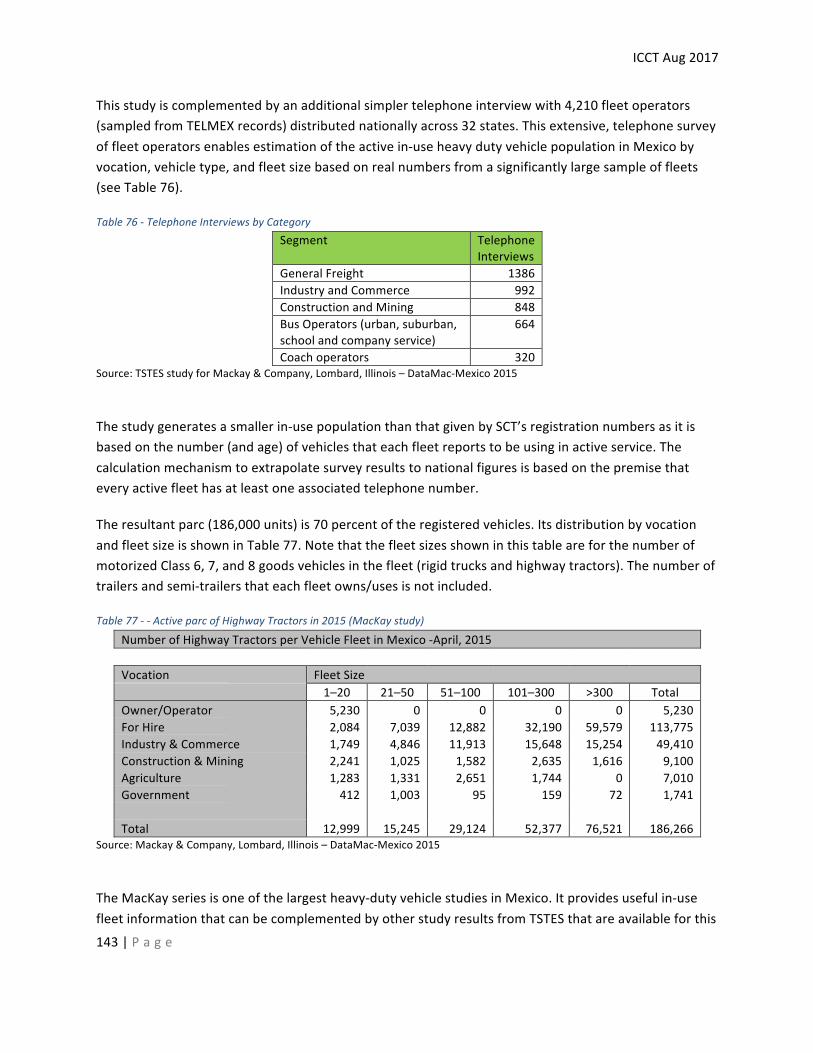

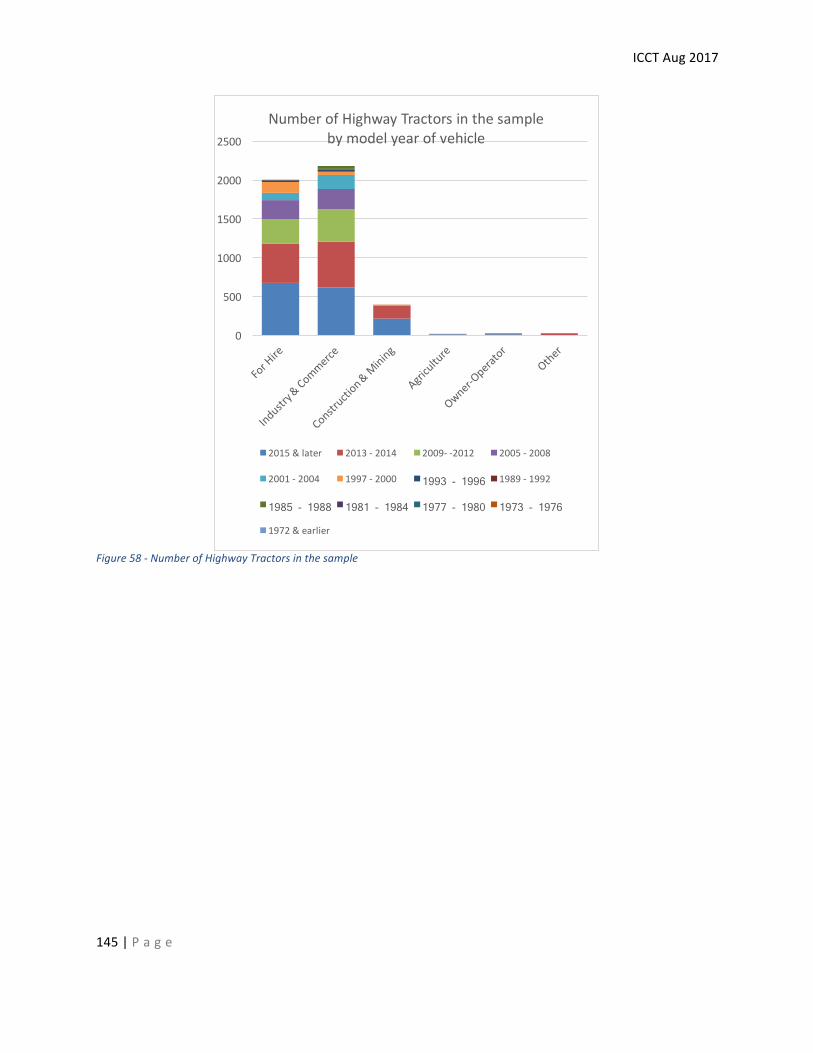

HowtheactivepopulationofHighwayTractorswasdetermined.......................................................141

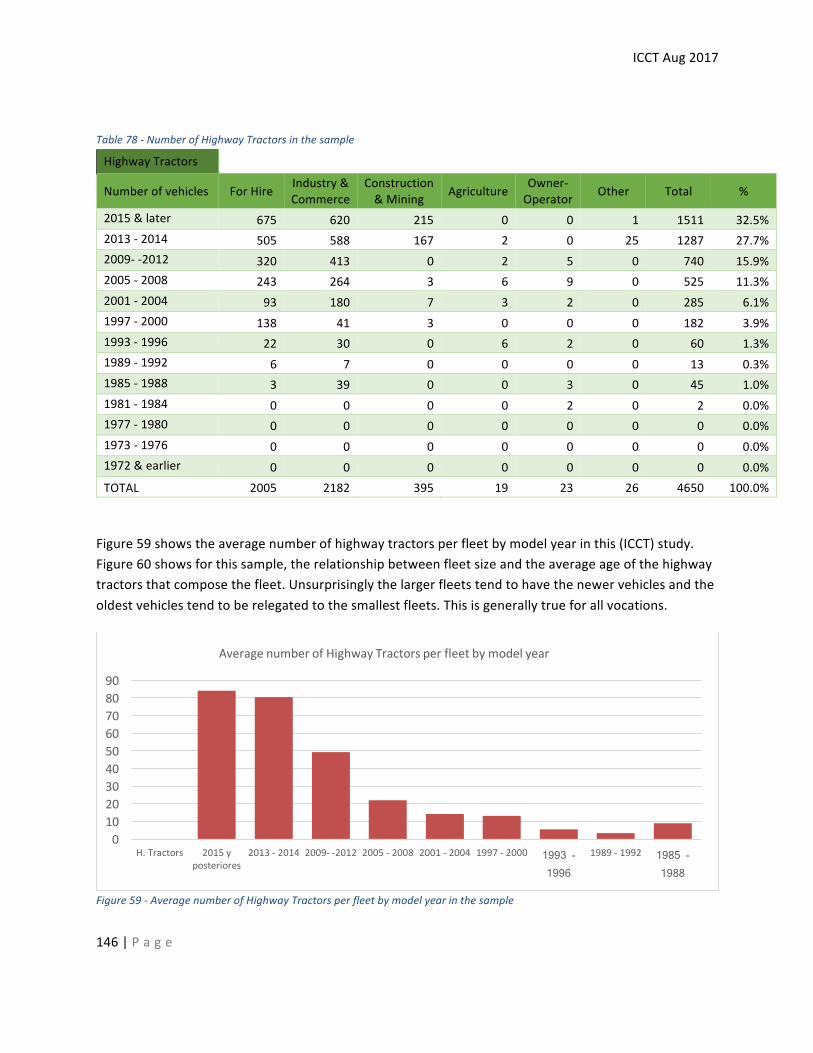

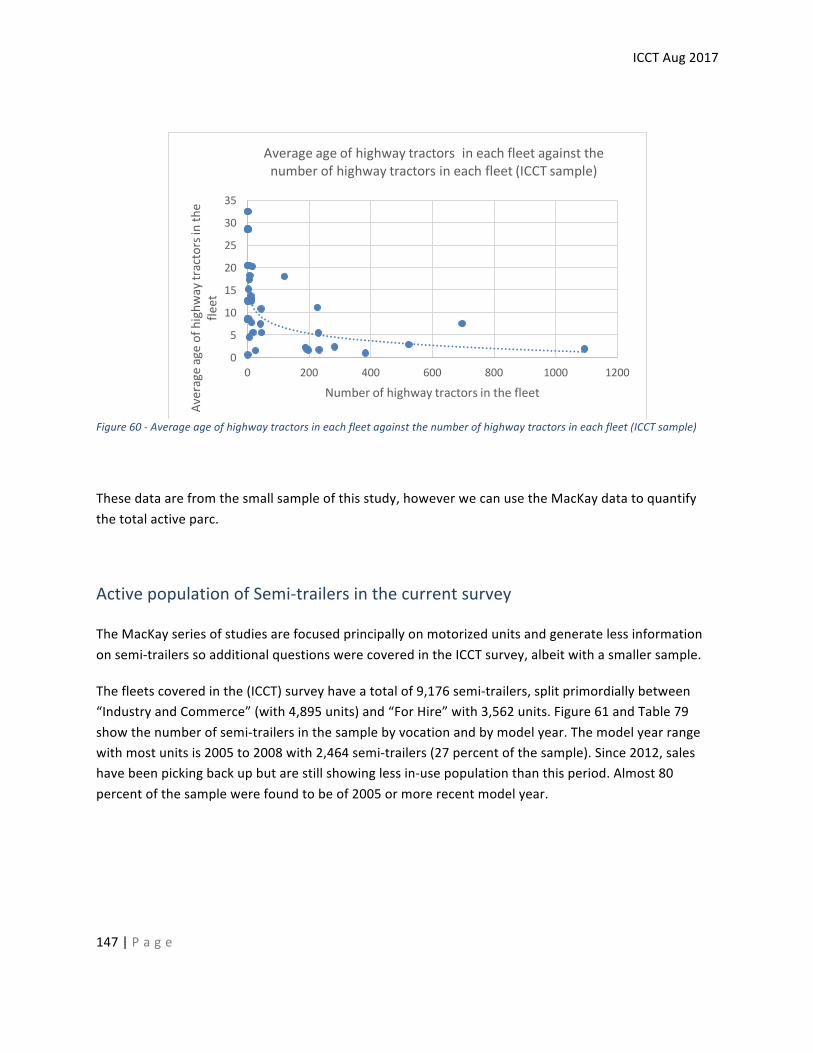

ActivepopulationofHighwayTractorsinthecurrentsurvey..........................................................144

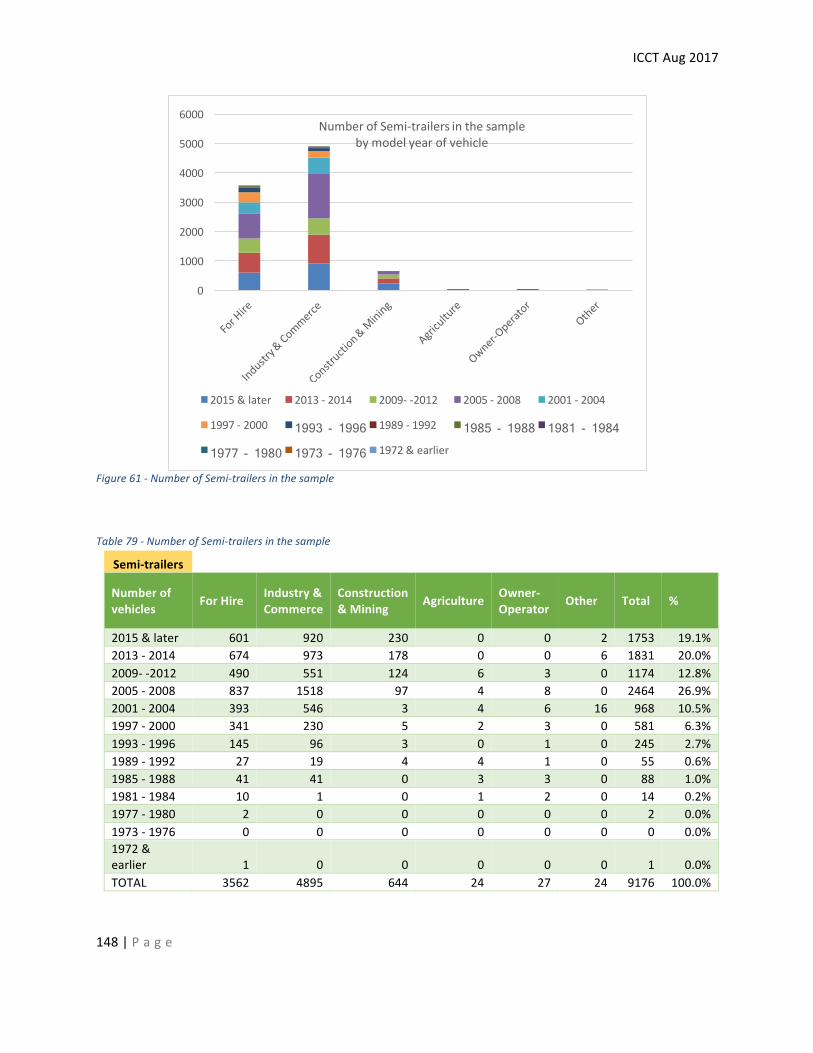

ActivepopulationofSemi-trailersinthecurrentsurvey.................................................................147

References............................................................................................................149

ICCTAug2017

vi|P a g e

Tables

Table1-DomesticfreighttransportbymodeinMexico.............................................................................8Table2-DomesticfreighttransportbymodeinUSA..................................................................................8Table3-DomesticfreighttrafficbymodeinMexico..................................................................................8Table4- DomesticfreighttransportbymodeinUSA.............................................................................9Table5-EXPORTMerchandisetradeofMexicotoNAFTAcountriesandtheworldbymajorproductgroup,2014..................................................................................................................................................9Table6-IMPORTMerchandisetradeofMexicofromNAFTAcountriesandtheworldbymajorproductgroup,2014..................................................................................................................................................9Table7-PrincipalportsofEntry/Exitforfreightto/fromNAFTAtradingpartners...................................10Table8-TransportInfrastructureinMexico.............................................................................................11Table9-ConstructionofnewpipelinesinMexicoupto2017..................................................................16Table10-PrincipalproductstransportedbyRailinMexico......................................................................18Table11-FreighttransportedbyRailandfuelefficiencyinMexico.........................................................19Table12-PrincipalportsbyfreighttonnageinMexico............................................................................21Table13-YearlyTradeRatiosofValuetoWeightbetweenUSA-MEXICO(importvaluetotheUSAincurrentU.S.dollarsandimportweightinKg)............................................................................................22Table14-PrincipalstatesforAirfreightinMexico...................................................................................23Table15StateswithmostregisteredHighwayTractors(2016)................................................................27Table16--ActiveparcofHighwayTractorsin2015(MacKaystudy).......................................................29Table17-Comparisonofregisteredvsin-usehighwaytractorsin2015..................................................30Table18-PopulationofHighwayTractorsinactivefleetusage...............................................................31Table19-Top100delautotransporteT21(10aEdición)Dec2016..........................................................34Table20-HighwayTractorsbymake........................................................................................................38Table21-Enginesbymake........................................................................................................................39Table22-Ratioofsemitrailersperhighwaytractorbyvocation..............................................................41Table23-Semi-trailerbytype...................................................................................................................43Table24-Semi-trailerbymake.................................................................................................................44Table25–MakeofTireused.....................................................................................................................50Table26-UsageofAirConditioning..........................................................................................................51Table27-Popularsitesforusedhighwaytractors....................................................................................59Table28-Howdoyoufindtheunittobeabletobuyit?..........................................................................60Table29-Expectedsecond-handresaleprice...........................................................................................61Table30–ReasonsforchoosingthismakeofHighwayTractor................................................................62Table31-ReasonsforchoosingthismakeofSemi-trailer........................................................................62Table32-Howthepurchaseofaunitwasfinanced.................................................................................63Table33-Howhighwaytractorpurchaseswerefinanced........................................................................64Table34-Problemsassociatedwithobtainingfinance.............................................................................65

ICCTAug2017

vii|P a g e

Table35-NumberofHighwayTractorsthatareexpectedtobeboughtorsoldoverthecoming24months.......................................................................................................................................................66Table36-NumberofSemi-trailersthatareexpectedtobeboughtorsoldoverthecoming24months67Table37-AveragekmsbyageofvehiclebyVocation..............................................................................73Table38-Averagetriplength(kms)byageandvocation.........................................................................80Table39-Averagenumberoftripspermonthbyageandvocation.........................................................81Table40-Averagefueleconomykm/L)byageandvocation...................................................................83Table41-Illustrativedrivecycleexamples.................................................................................................84Table42-Ratiooftrailerspertractorinthe2011and2017studies........................................................85Table43-OperatingExpensesforHighwayTractors(thousandsofpesos)..............................................87Table44–DifferencesinOperatingExpensesforHighwayTractorsbyVocation(thousandsofpesos)..88Table45-Otherexpenseitemsmentionedbytheinterviewees...............................................................89Table74-Whichcontrolsdofleetsregularlykeep?..................................................................................90Table46-TariffNegotiation......................................................................................................................94Table47-FrequencyofTariffIncreases....................................................................................................94Table48-Whodefinestheexactrouteanddeparturetime.....................................................................98Table50-Membershipswithassociations/confederations/transportorganizations............................99Table51-WeightandDimensions...........................................................................................................103Table52-TransporteLimpiomarketedfuelsavingsfromstrategiesandtechnology............................111Table57-Howoftendoyoumeasureprogress?....................................................................................113Table58-Haveyoumadechangestoimprovetheperformanceandemissionsofyourvehicles?Which?..................................................................................................................................................................113Table59-Changesmadetoimprovetheperformanceandemissionsoftheirvehicles........................114Table60-Changesintervieweesplanttomaketoimprovetheperformanceandemissionsoftheirvehicles.....................................................................................................................................................114Table61-Changesmadetoimprovetravelscheduling..........................................................................115Table56-EXAMPLESOFSMARTWAYBRANDING.EPA(2016)................................................................117Table54-SmartWayandTransporteLimpioperformancestatistics......................................................120Table55-SmartWaymeasuresagainstTransporteLimpio.....................................................................121Table53-:Currentscrappageincentivesagainstvalueofoldvehicles..................................................124Table64-Max.PermissibleEmissionsStandards;Heavy-dutyVehiclesCompliance.............................130Table65-MaximumPermissibleEmissionsforHeavy-dutyVehiclesing/bhp-hr..................................130Table66-MaximumPermissibleEmissionsforHeavy-dutyVehiclesing/kwhr.....................................130Table67-Frameworkoftheproposedstandardsfor2019.....................................................................131Table68-U.S.certificationlimitvaluesforheavy-dutyengines.............................................................132Table69-Europeancertificationlimitvaluesforheavy-dutyengines....................................................132Table70-Usefulliferequirements..........................................................................................................132Table71-NOM-045-SEMARNAT-1996Limitsforvehiclesofover2,727kgsPBV...................................134Table72-NOM-045-SEMARNAT-2006Limitsfordieselvehiclesofover2,727kgsPBV........................134Table73-NOM-EM-167-SEMARNAT-2016Limitsfordieselvehiclesofover2,727kgsPBV..................134

ICCTAug2017

viii|P a g e

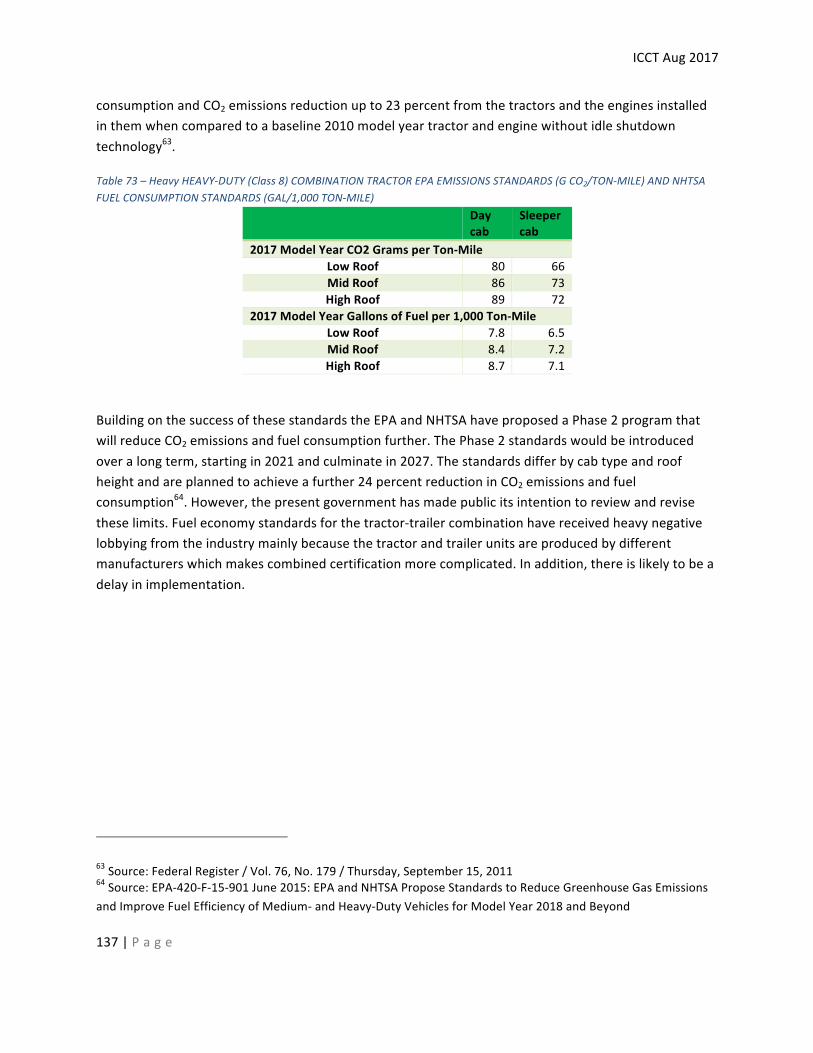

Table63–HeavyHEAVY-DUTY(Class8)COMBINATIONTRACTOREPAEMISSIONSSTANDARDS(GCO2/TON-MILE)ANDNHTSAFUELCONSUMPTIONSTANDARDS(GAL/1,000TON-MILE).......................137Table75-Face-to-faceInterviewdistribution.........................................................................................142Table76-Vocation..................................................................................................................................142Table77-TelephoneInterviewsbyCategory..........................................................................................143Table78--ActiveparcofHighwayTractorsin2015(MacKaystudy).....................................................143Table79-NumberofHighwayTractorsinthesample............................................................................146Table80-NumberofSemi-trailersinthesample...................................................................................148

ICCTAug2017

ix|P a g e

Figures

Figure1-DomesticfreighttransportinMexicoandtheUSA.....................................................................5Figure2-DomesticfreighttransportbymodeinMexicoandUSA.............................................................5Figure3-TotalfreighttransportbymodeinMexico..................................................................................6Figure4-DomesticfreighttrafficbymodeinMexicoandtheUSA............................................................7Figure5-PrincipalHighwaysinMexico.....................................................................................................12Figure6-HighwaysystemlengthinMexico..............................................................................................13Figure7-RailinfrastructureinMexico......................................................................................................14Figure8-Mexicanpipelineinfrastructure.................................................................................................16Figure9-FreighttransportedbyRailinMexico........................................................................................17Figure10-PrincipalproductstransportedbyRail.....................................................................................18Figure11-FuelefficiencyofRailfreightserviceinMexico.......................................................................20Figure12-PrincipalAirfreightroutes.......................................................................................................22Figure13--RegisteredParcofHighwayTractors(2016)SCTdata............................................................26Figure14-CompositionoftheParcofhighwayTractorsin2016bymodelyear.....................................27Figure15-PopulationofhighwayTractors(T2&T3)bystatein2016(SCTdata)....................................28Figure16-Comparisonofin-usevehiclenumbersfromtheMacKaystudy(2015)vsSCTregistrationdata....................................................................................................................................................................30Figure17-ParcHighwayTractors(2015)byvocation(MacKaystudy).....................................................33Figure18-ParcHighwayTractors(2015)byfleetsize(MacKaystudy).....................................................34Figure19-Distributionofthe2principalmakesofHighwayTractorbymodelyear................................38Figure20.Agraphtoshowreplacementofengines;istheengineoriginal?...........................................39Figure21-Registeredfleetofsemi-trailersinMexico..............................................................................40Figure22-RatioofSemi-trailersperhighwaytractor...............................................................................40Figure23-RatioTrailers/Tractorsbyvocation..........................................................................................41Figure24-USAratioofdryvanstohighwaytractor.................................................................................43Figure25-Averageageofvehiclesbyvocation........................................................................................45Figure26-Howmanyyearsmoreareyouplanningonusingyourhighwaytractor?...............................46Figure27-Semi-trailers:Howmanyyearsmoreareyouplanningonusingit?........................................47Figure28-Technologicallevelofhighwaytractors...................................................................................48Figure29–Fuelefficienttechnologypenetrationintheowner-operatorandsmallcarriersegment......52Figure30-Nationalsalesofhighwaytractors(Wholesale).......................................................................55Figure31–Totalnationalsalesofhighwaytractorsbymanufacturer1963-2010..................................56Figure32-2010Nationalsalesofhighwaytractorsbymanufacturer......................................................57Figure33-UsedHighwayTractorsonsalebymodelyear........................................................................59Figure34-Howhighwaytractorpurchaseswerefinanced.......................................................................64Figure35-Averagekmsbyageofvehicle.................................................................................................74Figure36-Owner/operator;Averagekmsbyageofvehicle...................................................................74Figure37-Forhire;Averagekmsbyageofvehicle...................................................................................75

ICCTAug2017

x|P a g e

Figure38-Industry&Commerce;Averagekmsbyageofvehicle............................................................76Figure39-Construction&Mining;Averagekmsbyageofvehicle...........................................................77Figure40-Agriculture;Averagekmsbyageofvehicle.............................................................................78Figure41--Government;Averagekmsbyageofvehicle..........................................................................79Figure42-Averagetriplength(kms)byageandvocation........................................................................80Figure43-Averagenumberoftripspermonthbyageandvocation.......................................................81Figure44-Averagefueleconomykm/L)byageandvocation..................................................................82Figure45-FuelEconomyofHighwayTractorsbyvocationin2017vs2011.............................................85Figure46-TotalannualoperatingexpensesperunitforHighwayTractorsinpesos($MN)....................86Figure47-Totalperkmoperatingcost($MN/km)...................................................................................87Figure48-Percentagedistributionofoperatingexpenses.......................................................................88Figure49-Typeoffreightbyvocation......................................................................................................95Figure50-SourceofFreight......................................................................................................................95Figure51-LoadingofVehicle....................................................................................................................96Figure52-Tripscheduling.........................................................................................................................97Figure53-Tripprogramming....................................................................................................................98Figure54-CarbonemissionssavingsresultingfromTransporteLimpio(2008to2014)........................112Figure55-KnowledgeandparticipationintheProgramadeTransporteLimpio...................................113Figure56-Numberoffleetsinthesamplebyfleetsize(DataMac2015)...............................................142Figure57-Numberoffleetsinthesamplebyfleetsize(ICCTsurvey)....................................................144Figure58-NumberofHighwayTractorsinthesample...........................................................................145Figure59-AveragenumberofHighwayTractorsperfleetbymodelyearinthesample.......................146Figure60-Averageageofhighwaytractorsineachfleetagainstthenumberofhighwaytractorsineachfleet(ICCTsample)...................................................................................................................................147Figure61-NumberofSemi-trailersinthesample..................................................................................148

ICCTAug2017

xi|P a g e

Abbreviations

3PL Third-partylogisticscompanyAMDA AsociaciónMexicanadeDistribuidoresdeAutomotoresAMIA AsociaciónMexicanadeLaIndustriaAutomotrizAMMPAC AsociaciónMexicanadeMensajeríayPaqueteríaA.C.ANPACT AsociaciónNacionaldeProductoresdeAutobuses,Camionesy

TractocamionesANTP AsociaciónNacionaldelTransportePrivadoCANACAR CameraNacionaldelAutotransportedeCargaCANACINTRA CámaraNacionaldelaIndustriadeTransformaciónCCAC ClimateandCleanAirCoalitionCESPEDES ConsejoEmpresarialparaelDesarrolloSostenibleCO CarbonmonoxideCO2 CarbondioxideCONATRAM ConfederaciónNacionaldeTransportistasMexicanosCONCAMIN ConfederacióndeCámarasIndustrialesDGAF DirecciónGeneraldeAutotransporteFederalDGGCARETC DirecciónGeneraldeGestióndelaCalidaddelAireyRegistrodeEmisionesy

TransferenciadeContaminantesEMBARQ EMBARQisnowtheWRIRossCenterforSustainableCitiesEPA UnitedStatesEnvironmentalProtectionAgencyGIZ DeutscheGesellschaftfürInternationaleZusammenarbeitGmbHHC hydrocarbonsICCT InternationalCouncilonCleanTransportationINECC InstitutoNacionaldeEcologiayCambioClimaticoITDP InstituteforTransportationandDevelopmentPolicyMN MonedaNacional(Mexicanpesos)NAFTA NorthAmericanFreeTradeAgreementNAMA NationallyAppropriateMitigationActionsNGO Non-governmentalorganizationNOM NormaOficialMexicanaNOx nitrogenoxidesOEM OriginalEquipmentManufacturerPM particulatematterSCT SecretaríadeComunicacionesyTransportesSEMARNAT SecretaríadeMedioAmbienteyRecursosNaturalesSHCP-SAT ServiciodeAdministraciónTributariadelaSecretaríadeHaciendayCréditoPúblicoSMAEM SecretaríadeMedioAmbientedelEstadodeMexicoSmartway USEPA'sSmartWayTransportPartnershipTELMEX TelefonosdeMexicoTPP TranspacificAssociationAgreementTransporteLimpio VoluntaryCleanTransportprogramdevelopedbySEMARNATandSCT.TSTES TheSustainableTransportandEmissionsServicesCompanyUNFCC UnitedNationsFrameworkConventiononClimateChange

ICCTAug2017

xii|P a g e

Acknowledgements

ThisreporthasbeenpreparedfortheInternationalCouncilonCleanTransportation(ICCT)bytheSustainableTransportandEmissionsServicesCompany(TSTESSAdeCV)incollaborationwithIntegratedTransportPlanningLtd.ThisworkissupportedbytheClimateandCleanAirCoalition(CCAC).TheCCACisavoluntarypartnershipofgovernments,intergovernmentalorganizations,businesses,scientificinstitutionsandcivilsocietyorganizationscommittedtoimprovingairqualityandprotectingtheclimatethroughactionstoreduceshort-livedclimatepollutants.

Theauthorswouldliketoexpresstheirsincereappreciationforthevaluablehelp,guidance,supportandpatiencefromthestaffatICCT,particularlyKateBlumberg,SeniorFellow/MexicoLead;BenSharpe,SeniorResearcherandCanadaLead;CristianoFaçanha,Roadmap,GreenFreightandBrazilLead;andKeriBrowning,GrantsManager.

AspecialthankyouisparticularlyduetoIng.JudithTrujilloMachado,SubdirectoradelSectorTransportedeSEMARNATwhosehelp,guidance,andsupportwaskeytorealizingthisstudy.

AsincereexpressionofgratitudeisduetoMackay&Company,Lombard,Illinoiswhopermittedustosharethemostrecentvehiclefleetdatafromthelatest(2015)DataMac-MexicostudyperformedbyTSTES.Thisstudyinvolvesinformationcollectedfromalmost5000fleetstogetherwithanin-depthanalysisofheavydutyfleetutilization(includingClass8highwaytractorsandtrailers)andrepairpracticesinMexico.Ithasbeenconductedeveryfouryearssince1992andprovides—amongstotherthings—adetailedviewoftheactivevehiclefleet,whichdiffersconsiderablyfromthestatic,registeredvehicledistribution

TheauthorswouldadditionallyliketothanktheInstitutoNacionaldeEcologiayCambioClimatico(INECC)forallowingustoquotefindingsfromthestudyaperformedforthembyTSTES(2011)entitled“Caracterizacióndelaflotamexicanadevehículos”andDeutscheGesellschaftfürInternationaleZusammenarbeit(GIZ)GmbHforallowingustoquotefindingsfromthetwo-part2014studyperformedforthembyTSTESlookedatcommercialvehiclescrappageprogramsinMexico,andcomparedtothoseinothercountries.

Thestudywouldnothavebeenpossiblewithoutinputfromfleetsandothergovernmentalandnon-governmentalorganizations.Therewereobtainedinperson-to-personinterviewsandaquantitativefieldsurveydesignedto(a)tofilldatagaps,(b)refreshsomeoftheolderinformation,and(c)validatewherepreviousfindingsarestillfunctional.

Theparticipantsincludedineachgroupareshownbelow.

ICCTAug2017

xiii|P a g e

Interviews

Name Company/Institution Functionl

AdriánAzuaraPerdomo

DaimlerVehículosComercialesMéxico(Freightliner)

GerentedeVentas

AdulfoVidalsRosas

Coca-ColaFEMSA Coord.Ctrol.Ambiental

AlejandroFuentesRomero

GreatDanedeMéxico DirectordeVentas,

AlexLongTheissen FemsaLogística PresidentedelaAsociaciónNacionaldeTransportePrivadoyDirectortécnicodeFemsaLogística

AlfonsoAyalaColín

TransportesAyalaColínSAdeCV Director

ArturoMassutierMorales

AsociaciónNacionaldeProductoresdeAutobuses,CamionesyTractocamiones

Formermanager

CarlosGilJiménez DirecciónGeneraldelAutotransporteFederalSCT

SubdireccióndeDesarrolloTecnológicoySeguridad

ChristanSánchezSantoyo

PETSTAR AdministradorTransporte

ClaudioGallegos ConfederaciónNacionaldeTransportistasMexicanos(COTRAM)

DirectorGeneral

CristinaSánchez TransportesElola CoordinadoraCTPAOEA

DanielGarcíaC. TracusalaRutadelSol Cacacitación

DanielaVillarreal Coca-ColaFEMSALogistica RelacionesInstitucionales

DavidHerreraLópezPortillo

AutoTransportesParadaHermanos CoordinadordeTráfico

ElenaZaldivar AutoExpressFronteraNorte GerentedeCalidad

ElizabethRamírez AutotransportesdeCargaTresguerras Ejec.Comercial

FabiolaDomínguezV.

TracusalaRutadelSol JefeCDiesel

FelipeJiménez AutoTransporteNacionaldeCargaTNC Gte.Operaciones

FranciscoBarrera SMAEdoMex DirectordeInvestigacioneImplementaciondeprotocolos

GabrielDeUriarteOccelli

UtilityTrailersdeMéxico DirectorComercialCorporativo

IgnaciodeJesúsMontoyaAyón

Bimbo-Barcel GerentedeEstudiosTécnicos

ICCTAug2017

xiv|P a g e

Name Company/Institution Functionl

IsabelAguiñaga AutotransportesdeCargaTresguerras JefeComercialMéxico

JaimeCaracheoR. TransportesEspecializadosAntoniodelaTorreeHijos

CoordinadorSHMA

JavierPadillaMartínez

BioPappel GerentedeLogística

JoséAntonioCortesMéndez

AlasdelMonte GerentedeMantenimiento

JuanManuelFloresEstrada

AutoTanquesOchoa(ATOSA) Coordinador

JuanManuelSalasMartínez

Transcooler Gerentedeoperaciones

JudithTrujilloMachado

SEMARNAT SubdirectoradelSectorTransporte

KarinaVillegas TransportadoraConsolidada EspecialistaenMarketing

LeonardoNúñez TransportesMexamerik Gte.Operaciones

LucianoAguilarCorona

FerrocarrilyTerminalValledeMéxico(FERROVALLE)

GerentedeOperaciones

LuisEnriqueRamírez

TransportadoraConsolidada EspecialistadeTransporteLimpio

LuisRubénFloresTapia

Coca-ColaFEMSA Gte.ControlAmbiental

MaribeldelCarmenPeñaLaurencio

AlasdelMonte Lic.Amb.

MaricelaHernándezHorta

TracusalaRutadelSol ControlleroperacionesCorporativo

MoisésDavidTellez

TransportesElola DirectordeOperaciones

MoisesOcaña FletesyTransportesRuíz Analista

MonserratRodríguezGarcía

AutotransportesOILSA JefedeProcesos

OmarGarcíaCuriel TransportesEspecializadosAntoniodelaTorreeHijos

SHMA

OswaldoMuñoz Flechisa Ventas

PabloJesúsMercado

SCT DirectordeNormatividad

PedroMenesesRetalsa

Cemex Rep.Legal

RafaelTapiaVelázquez

GrupoBimbo DireccióndeVehículos

RobertoMelchor FletesyTransportesRuíz JefedeMantenimiento

RodolfoRodríguezJiménez

Tracomex,S.A.DeC.V. Gte.deoperaciones

ICCTAug2017

xv|P a g e

Name Company/Institution Functionl

RodrigoPerrusquíaMáximo

SEMARNAT JefedeDepartamentodeGestiónAmbientaldelSectorTransporte

SergioZirath INECC Directordeinvestigaciónsobrelacalidaddelaireyloscontaminantesclimáticosdevidacorta

FieldSurveyParticipants

Fleet/Company Fleet/Company Fleet/Company

AguilasDelSureste GeodisGlobalSolutionsMéxicoS.A.deC.V. TransportesAyalaColínS.A.deC.V.

AlasDelMonteS.A.deC.V. LópezDomínguez TransportesBeltránAutoExpressFronteraNorteS.A.deC.V. LuisAltamirano TransportesBotello

AutotransportesOilsaS.A.DeC.V MejíaRodríguez TransportesDeCargaFortínBimboS.A.deC.V. Méndez TransportesElola,S.A.deC.V.BioPappel,S.A.deC.V. OrtegaMateriales TransportesFuentes

CemexTransporte PetstarReciclado(AvangardMexicoSdeRLdeCV) TransportesHernández

CésarHernández T.P. TransportesMares

DesperdicioIndustrialDelgado Tds,S.A.DeC:V. TransportesMexamerik,S.A.deC.V.

DestinoExpress TracomexS.A.deC.V. TransportesMon-Ro,S.A.deC.V.Diaz Transcooler TransportesParraEstafetaMexicanaS.A.deC.V.YEmpresasFiliales

TransportadoraConsolidadaS.A.deC.V. TransportesRoldán

FemsaLogística Transportec TransportesYMudanzasRuízFletesYTransportesRuiz TransportesAngeles Trasesu

ForrajesMadrigal TransportesAutoTanquesOchoa,S.A.deC.V.

ThestudywascoordinatedbyJohnRogersofTSTES;RobinKaenzig(ITP)ledtheInternationalandSmartWayanalysisassistedbyRubyStringerandothermembersoftheITPteam.ThefieldsurveyandinterviewswereorganizedandconductedbyJavierRodriguez(TSTES)withsupportfromArturoMassutier(GRUIDCO),JaimeMeza(TSTES)andothermembersoftheteam.StevenJ.Rogers(TSTES)managedinterviewanalysisandeditorialactivities.

ICCTAug2017

1|P a g e

Chapter1:-ExecutiveSummary

ThisMexicoFreightAssessmentwasconductedin2017fortheInternationalCouncilonCleanTransportation(ICCT)bytheSustainableTransportandEmissionsServicesCompany,TSTESSAdeCV,MexicoinconjunctionwithIntegratedTransportPlanningLtd,England.

ICCTsponsoredthisprojecttoassessthefreightsysteminMexico,withafocusonon-roadgoodsmovement,asakeycontributortotheClimateandCleanAirCoalition’s(CCAC)GlobalGreenFreightActionPlanfocusedondevelopingandharmonizinggreenfreighteffortsonaglobalscaleinordertogetmaximumreductionsofblackcarbonandimprovedefficiencyfromfreighttransport.

Theprimarymotivationforthisprojectwastodevelopamuchdeeperunderstandingoftheon-roadfreightsysteminMexico.Thisfreightassessmentbuildsuptheknowledgebaseinseveralareas,includingmarketdynamics,opportunitiesandbarriersfortruckfuel-savingtechnologiesandoperationalmeasures,andthepotentialbenefitsofbuildingamorerobustandextensiveTransporteLimpioprogram,andharmonizingitwithSmartWay.

Thescopeoftheprojectwasexclusivelyfocusedonfreighttransportationbytractor-trailers,andinclusiveofthevariousactorsthatimpactthefreightsystem.ThisresearchlookstopresentacompendiumofknowledgetogovernmentagenciesandotherstakeholdersinMexicowhoaredevelopingstrategiesforreducingtheenvironmentalimpactsofthetruckingsectorandgivethesedecision-makersbettertoolstoevaluatehowagreenfreightprogramfitsintotheoverallportfolioofpoliciesaimedatthefreightsector.

ThestudycompilespubliclyavailabledatawithfindingsfrompreviousstudiesconductedbyTSTES(andincludedwithoriginalclientagreement)andinputfromfleetsandothergovernmentalandnon-governmentalorganizations.Informationwasgatheredfromperson-to-personinterviewsandalimitedquantitativefieldsurveywith89stakeholdersfromdifferentlevelsoftheon-roadfreightsysteminMexicoto(a)filldatagaps,(b)updateolderinformation,and(c)validatepreviousfindingswhereadequate.Althoughresourceconstraintspreventedastatisticallysignificantanalysisofanswers,thestudyprovidesthemostrecentdataavailableontheMexicanon-roadfreightsector.

Thisdataiscollatedinto8thematicgroups,(inChapters2through9)andahighlightofeachispresentedatthebeginningofthecorrespondingchapters:

ICCTAug2017

2|P a g e

Chapter2:-FreightcontextinMexicoandtheUSA..................................................3onfreighttransportinMexicoinallmodes(road,rail,waterborneandair)tosetthecontextforthesub-sectorthatisthethemeofthisstudy,on-roadfreighttransportedbyhighwaytractor-trailers.

Chapter3:-CharacteristicsofIn-useTractor-trailersinMexico............................24ontheregistered,andactivein-usepopulationofhighwaytractorsandsemi-trailersinMexico.Itpresentsdatabysizeoffleetandbyvocation,andlooksattheexpectedlifeoftheseunits.

Chapter4:-VehiclePurchasing..............................................................................53onhowfleetsbuyhighwaytractorsandsemi-trailers.Itlooksatthesourcesofinformation,advertising,andpublicitythatisusedtopromotesecond-handvehiclesales,howpurchasesarefinanced,andthemotivesforselectingaspecificbrand

Chapter5:-Tractor-trailerUsageandOperatingCosts..........................................68ontheroleofthedifferentplayersinthissub-sector.Itlooksatvehicleusage,triplengthandfrequency.Itevaluatesfueleconomyandotheroperatingcosts,withdetailsbyageofvehicleandbyvocation.Italsolooksatwhoiscollectinginformationontrav¡ctor.traileropderationinMexico

Chapter6:-Tariffs,FreighttypeandLogistics........................................................92ontheinteractionbetweentransport(For-Hire)fleetsandtheirclients,lookingattariffnegotiations,fareincreasesandtripprogramming

Chapter7:-InstitutionalandRegulatoryFramework...........................................100ontheinstitutionalandregulatoryframeworkthatsurroundson-roadfreighttransportinMexico

Chapter8:-ProgramadeTransporteLimpioandrelatedprograms....................108onstandardsandprogramsinMexicothatpromotecleantransport—suchastheProgramadeTransporteLimpio—andlooktomodernizethevehiclefleet.

Chapter9:-Fuelefficiencyandemissionsstandards...........................................127onfuelefficiencyandemissionsstandardsintheUSAandMexico

AnANNEXprovidesinformationontheApproachandMethodologyandhowtheactivepopulationofHighwayTractorswasdetermined.

ICCTAug2017

3|P a g e

Chapter2:-FreightcontextinMexicoandtheUSA

ThischaptercompilesinformationonfreighttransportinMexicobymode(Road,Rail,WaterborneandAir)tosetthecontextforamoredetailedevaluationofon-roadfreighttransportedbyhighwaytractor-trailers.

OverallfreightmarketinMexicoAlthoughtheoverallfreightmarketinMexicoislessthanone-elevenththesizeofthatintheUS(intermsoftonnestransported),theon-roadshareinMexicoismuchgreateraccountingfor56percentofthedomesticandinternationalfreighttransportandthusitsrelativeimportancetotheeconomyismuchlarger.t-kmAveragetransportdistancesintheUSaretwiceaslongasthoseinMexico.RoadAccordingtotheMinistryofCommunicationsandTransport(SCT),MexicoinvestedmorethanUS$2.05billionininfrastructureinthefirsthalfof2015.Thecurrentgovernmenthasbuilt17motorways(US$3.975billion)andestimatesthat35morearerequired(US$7.2billion).Overthelastdecadehighwayextensionhasincreasedatacombined10-yearaverageannualgrowthratebetween3.1and3.5percentwithasurgein2015.Thisishigherthantheoverallfreightmarket,whichgrewby1.5percentperyearbetween2005and2015.However,whilethecountryisbuildingnewroads,maintenanceofexistingroadsisbelowexpectationswhichlimitstheefficiencyofthissector.AccordingtotheWorldEconomicForum,among140nations,Mexicoranks52ndinroadqualitycompetitiveness.RailThesecondmostimportantmodeintermsoffreighttrafficinMexicoisRail,whichaccountedfor30.5billiont-kmsofdomesticfreightin2015(versus245billionforRoad).In2015therewasa3.4percentincreaseinton-kilometerstransportedbyRail,risingto83.4billiont-km(includingimportfreightwhichgrewbyonethirdoverthepreviousyear).ThemainproductstransportedbyRailarecorn(11.8percent),cement(8.3percent),containers(7.5percent)andironandsteelsheetsandplates(6.3percent).OverthelastdecadesRailenergyefficiencyhasgenerallyimprovedtoitscurrent(2015)valueof118t-km/Lofdiesel.ThisissimilartothefuelefficiencyofrailfreightintheUSAin1985.In2015theUSFreightRailfuelefficiencywas201t-km/L(473ton-milesperUSgallon).

ChapterHighlights

ICCTAug2017

4|P a g e

FreightbymodeinMexicoandtheUSA

DomesticFreightinMexicoandtheUSA

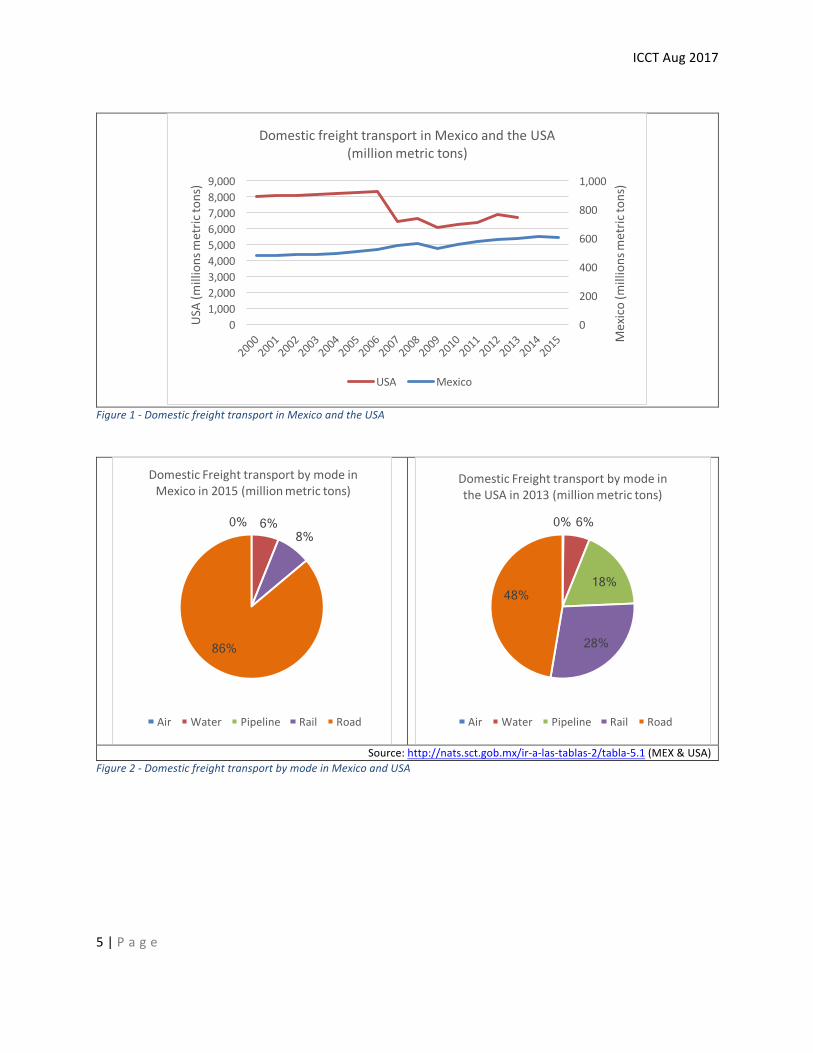

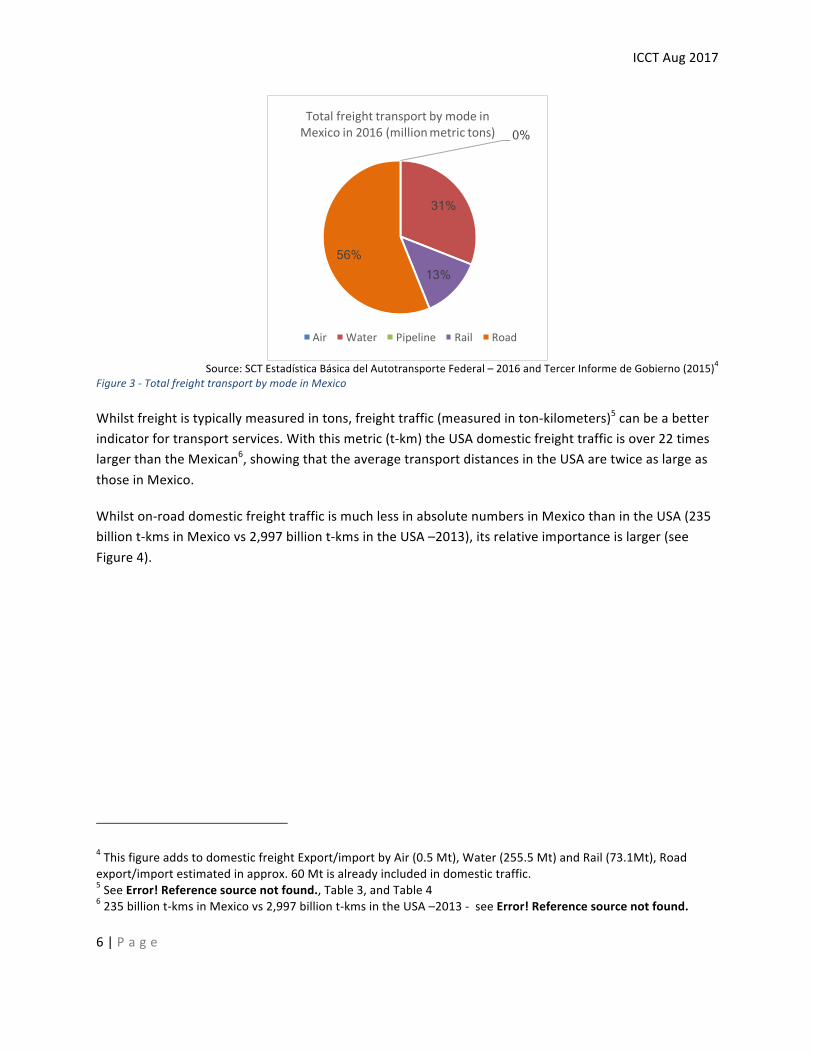

AlthoughtheoverallfreightmarketinMexicoislessthanone-elevenththesizeofthatintheUSA(intermsoftonstransported:seeFigure1)1,theon-roadshareismuchgreateraccountingfor56percentofthedomesticandinternationalfreighttransportandthusitsrelativeimportancetotheeconomyismuchlarger.In2015,86percentofdomesticfreightwascarriedbyRoad(comparedto48percentintheUSA);only8percentbyRailand6percentbySea2(seeFigure2).AccountingforInternationalfreight3,theproportionofMexicanfreightbySeaandRailincreasesto31percentand13percent,respectively,leavingRoadwithamodeshareof56percent(Figure3).

1In2013theUSdomesticmarketwas6,710vs600millionmetrictonsinMexico2ThefreightnumbersinMexicodonothavecomparablefiguresforpipelinetransport,whichisexcluded.3Internationalfreightisthatwhichhasthegoodoriginordestinationinadifferentcountry.Nationalfreighthasgoodsoriginanddestinationwithinthesamecountry.Onethirdofallfreighttransported(intons)inMexicoisinternational(import/export).

Themainrailroadcompanies-FerrocarrildeMéxico(Ferromex)andKansasCitySouthernofMexico(KCSM)-wereexpectedtoinvestaboutUS$3billionby2020toexpandthetractionofthelocomotivefleet,aswellasintherenovationoftracksandtrains.MultimodaltransportisconsideredanareaofopportunityinnationallogisticstoboostMexico'sdevelopment.SeaMexico’sprincipalportsarereachingthelimitoftheircapacityanddemandnewinvestments.PipelinesMexico’senergyreformin2013openedtheenergyindustrytovariousdegreesofprivateparticipationandcompetition.Oneresulthasbeenafastexpansionintheuseofimportedgas,withU.S.gasimportsasapercentageoftotaldemandclimbingfrom8percentin2000toaround44percentin2016creatingafastexpansionintheMexicanpipelinegridtohandlethisincreaseddemand.AirAirtonnagepalesincomparisontoothermodes(representingonly387thousandtonsin2015)concentratedin10states.

ICCTAug2017

5|P a g e

Figure1-DomesticfreighttransportinMexicoandtheUSA

Source:http://nats.sct.gob.mx/ir-a-las-tablas-2/tabla-5.1(MEX&USA)

Figure2-DomesticfreighttransportbymodeinMexicoandUSA

0

200

400

600

800

1,000

01,0002,0003,0004,0005,0006,0007,0008,0009,000

Mexico(m

illionsmetric

tons)

USA(m

illionsmetric

tons)

DomesticfreighttransportinMexicoandtheUSA(millionmetrictons)

USA Mexico

0% 6% 8%

86%

DomesticFreighttransportbymodeinMexicoin2015(millionmetrictons)

Air Water Pipeline Rail Road

0% 6%

18%

28%

48%

DomesticFreighttransportbymodeintheUSAin2013(millionmetrictons)

Air Water Pipeline Rail Road

ICCTAug2017

6|P a g e

Source:SCTEstadísticaBásicadelAutotransporteFederal–2016andTercerInformedeGobierno(2015)4

Figure3-TotalfreighttransportbymodeinMexico

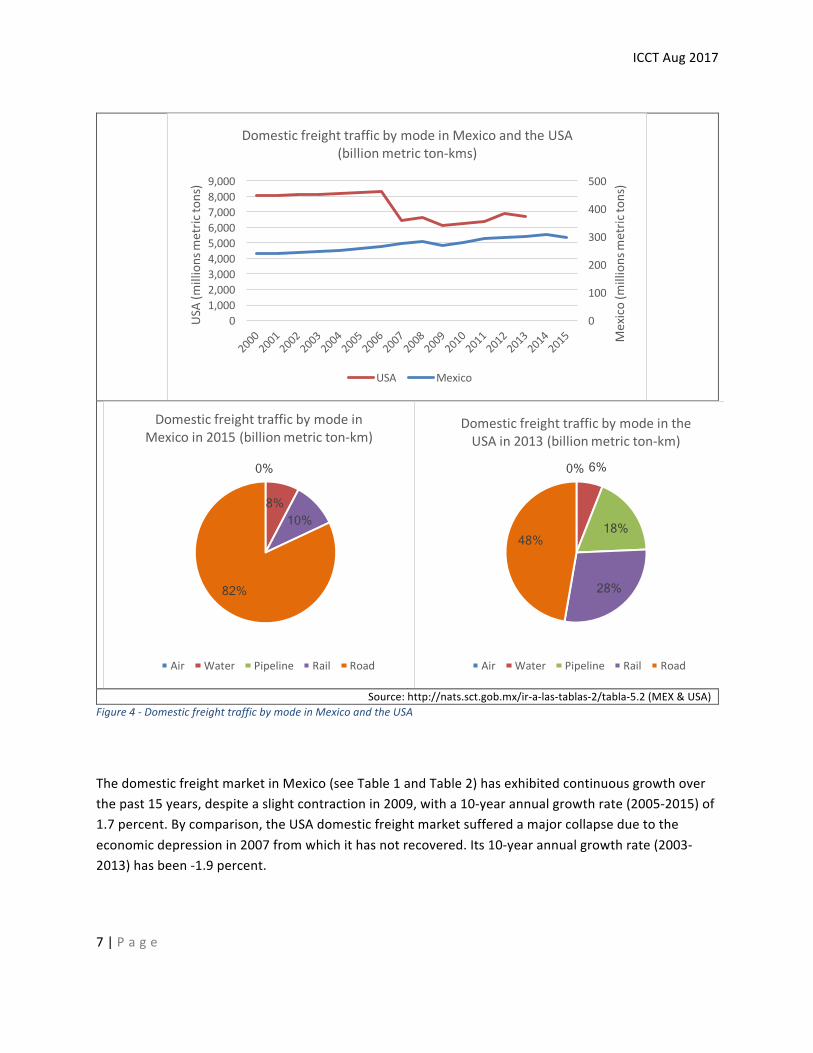

Whilstfreightistypicallymeasuredintons,freighttraffic(measuredinton-kilometers)5canbeabetterindicatorfortransportservices.Withthismetric(t-km)theUSAdomesticfreighttrafficisover22timeslargerthantheMexican6,showingthattheaveragetransportdistancesintheUSAaretwiceaslargeasthoseinMexico.

Whilston-roaddomesticfreighttrafficismuchlessinabsolutenumbersinMexicothanintheUSA(235billiont-kmsinMexicovs2,997billiont-kmsintheUSA–2013),itsrelativeimportanceislarger(seeFigure4).

4ThisfigureaddstodomesticfreightExport/importbyAir(0.5Mt),Water(255.5Mt)andRail(73.1Mt),Roadexport/importestimatedinapprox.60Mtisalreadyincludedindomestictraffic.5SeeError!Referencesourcenotfound.,Table3,andTable46235billiont-kmsinMexicovs2,997billiont-kmsintheUSA–2013-seeError!Referencesourcenotfound.

0%

31%

13% 56%

TotalfreighttransportbymodeinMexicoin2016(millionmetrictons)

Air Water Pipeline Rail Road

ICCTAug2017

7|P a g e

Source:http://nats.sct.gob.mx/ir-a-las-tablas-2/tabla-5.2(MEX&USA)

Figure4-DomesticfreighttrafficbymodeinMexicoandtheUSA

ThedomesticfreightmarketinMexico(seeTable1andTable2)hasexhibitedcontinuousgrowthoverthepast15years,despiteaslightcontractionin2009,witha10-yearannualgrowthrate(2005-2015)of1.7percent.Bycomparison,theUSAdomesticfreightmarketsufferedamajorcollapseduetotheeconomicdepressionin2007fromwhichithasnotrecovered.Its10-yearannualgrowthrate(2003-2013)hasbeen-1.9percent.

0

100

200

300

400

500

01,0002,0003,0004,0005,0006,0007,0008,0009,000

Mexico(m

illionsmetric

tons)

USA(m

illionsmetric

tons)

DomesticfreighttrafficbymodeinMexicoandtheUSA(billionmetricton-kms)

USA Mexico

0%

8% 10%

82%

DomesticfreighttrafficbymodeinMexicoin2015(billionmetricton-km)

Air Water Pipeline Rail Road

0% 6%

18%

28%

48%

DomesticfreighttrafficbymodeintheUSAin2013(billionmetricton-km)

Air Water Pipeline Rail Road

ICCTAug2017

8|P a g e

ThemostrecentnumbersfortheUSA(2013),showthat48percentofdomesticfreightwascarriedbyRoad,28percentbyRailand18percentbyPipeline.Wateraccountedfor6percentofthetotaltonnage.

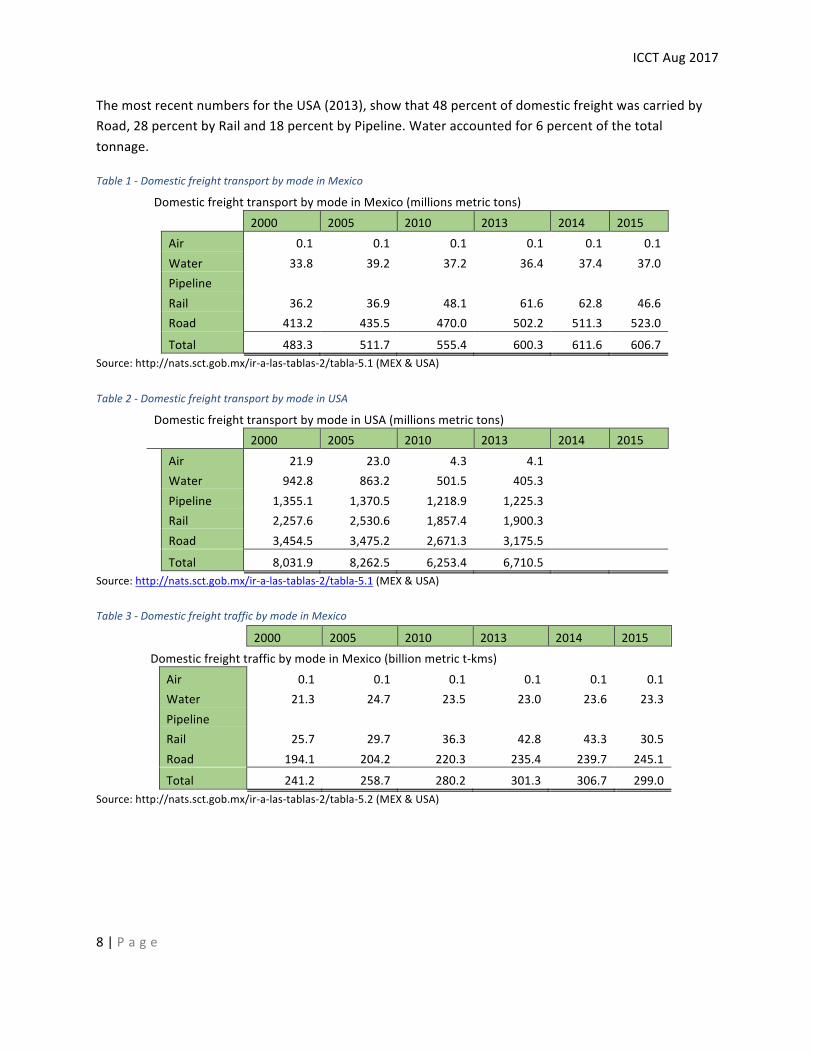

Table1-DomesticfreighttransportbymodeinMexico

DomesticfreighttransportbymodeinMexico(millionsmetrictons) 2000 2005 2010 2013 2014 2015 Air 0.1 0.1 0.1 0.1 0.1 0.1 Water 33.8 39.2 37.2 36.4 37.4 37.0 Pipeline Rail 36.2 36.9 48.1 61.6 62.8 46.6 Road 413.2 435.5 470.0 502.2 511.3 523.0

Total 483.3 511.7 555.4 600.3 611.6 606.7Source:http://nats.sct.gob.mx/ir-a-las-tablas-2/tabla-5.1(MEX&USA)Table2-DomesticfreighttransportbymodeinUSA

DomesticfreighttransportbymodeinUSA(millionsmetrictons) 2000 2005 2010 2013 2014 2015 Air 21.9 23.0 4.3 4.1 Water 942.8 863.2 501.5 405.3 Pipeline 1,355.1 1,370.5 1,218.9 1,225.3 Rail 2,257.6 2,530.6 1,857.4 1,900.3 Road 3,454.5 3,475.2 2,671.3 3,175.5

Total 8,031.9 8,262.5 6,253.4 6,710.5 Source:http://nats.sct.gob.mx/ir-a-las-tablas-2/tabla-5.1(MEX&USA)Table3-DomesticfreighttrafficbymodeinMexico

2000 2005 2010 2013 2014 2015DomesticfreighttrafficbymodeinMexico(billionmetrict-kms) Air 0.1 0.1 0.1 0.1 0.1 0.1 Water 21.3 24.7 23.5 23.0 23.6 23.3 Pipeline Rail 25.7 29.7 36.3 42.8 43.3 30.5 Road 194.1 204.2 220.3 235.4 239.7 245.1

Total 241.2 258.7 280.2 301.3 306.7 299.0Source:http://nats.sct.gob.mx/ir-a-las-tablas-2/tabla-5.2(MEX&USA)

ICCTAug2017

9|P a g e

Table4-DomesticfreighttransportbymodeinUSA

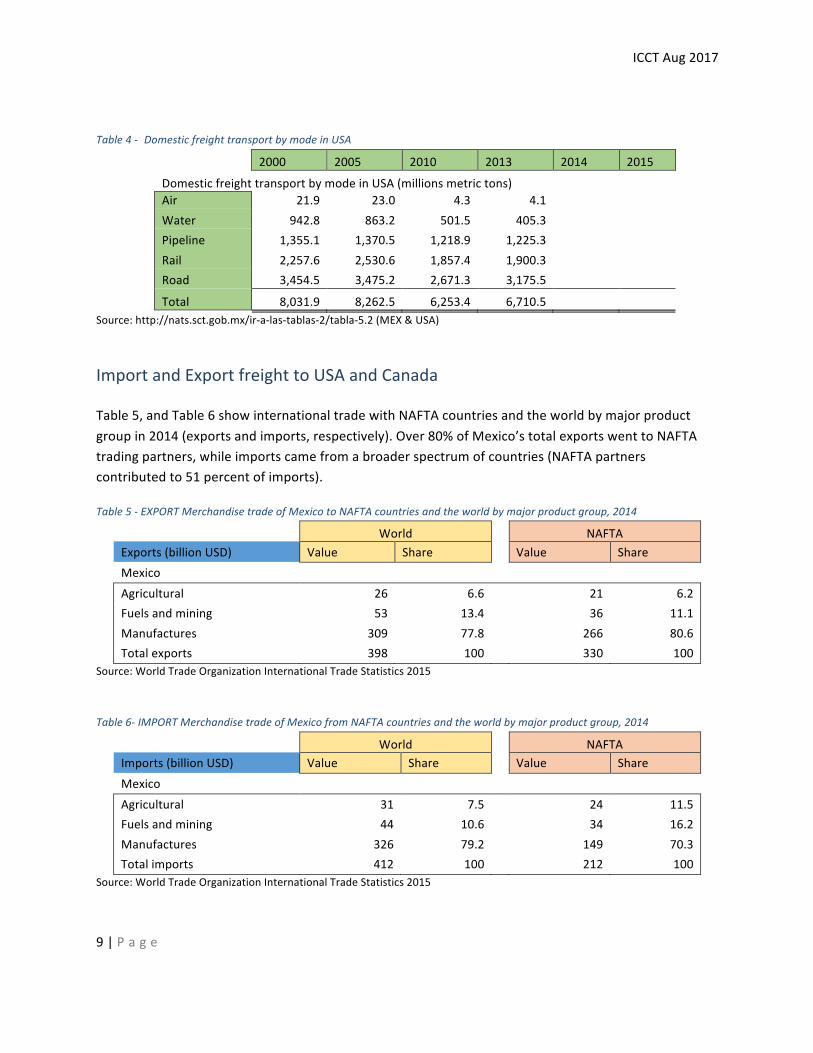

2000 2005 2010 2013 2014 2015

DomesticfreighttransportbymodeinUSA(millionsmetrictons) Air 21.9 23.0 4.3 4.1 Water 942.8 863.2 501.5 405.3 Pipeline 1,355.1 1,370.5 1,218.9 1,225.3 Rail 2,257.6 2,530.6 1,857.4 1,900.3 Road 3,454.5 3,475.2 2,671.3 3,175.5

Total 8,031.9 8,262.5 6,253.4 6,710.5 Source:http://nats.sct.gob.mx/ir-a-las-tablas-2/tabla-5.2(MEX&USA)

ImportandExportfreighttoUSAandCanada

Table5,andTable6showinternationaltradewithNAFTAcountriesandtheworldbymajorproductgroupin2014(exportsandimports,respectively).Over80%ofMexico’stotalexportswenttoNAFTAtradingpartners,whileimportscamefromabroaderspectrumofcountries(NAFTApartnerscontributedto51percentofimports).

Table5-EXPORTMerchandisetradeofMexicotoNAFTAcountriesandtheworldbymajorproductgroup,2014

World NAFTAExports(billionUSD) Value Share Value ShareMexico Agricultural 26 6.6 21 6.2Fuelsandmining 53 13.4 36 11.1Manufactures 309 77.8 266 80.6Totalexports 398 100 330 100

Source:WorldTradeOrganizationInternationalTradeStatistics2015

Table6-IMPORTMerchandisetradeofMexicofromNAFTAcountriesandtheworldbymajorproductgroup,2014

World NAFTAImports(billionUSD) Value Share Value ShareMexico Agricultural 31 7.5 24 11.5Fuelsandmining 44 10.6 34 16.2Manufactures 326 79.2 149 70.3Totalimports 412 100 212 100

Source:WorldTradeOrganizationInternationalTradeStatistics2015

ICCTAug2017

10|P a g e

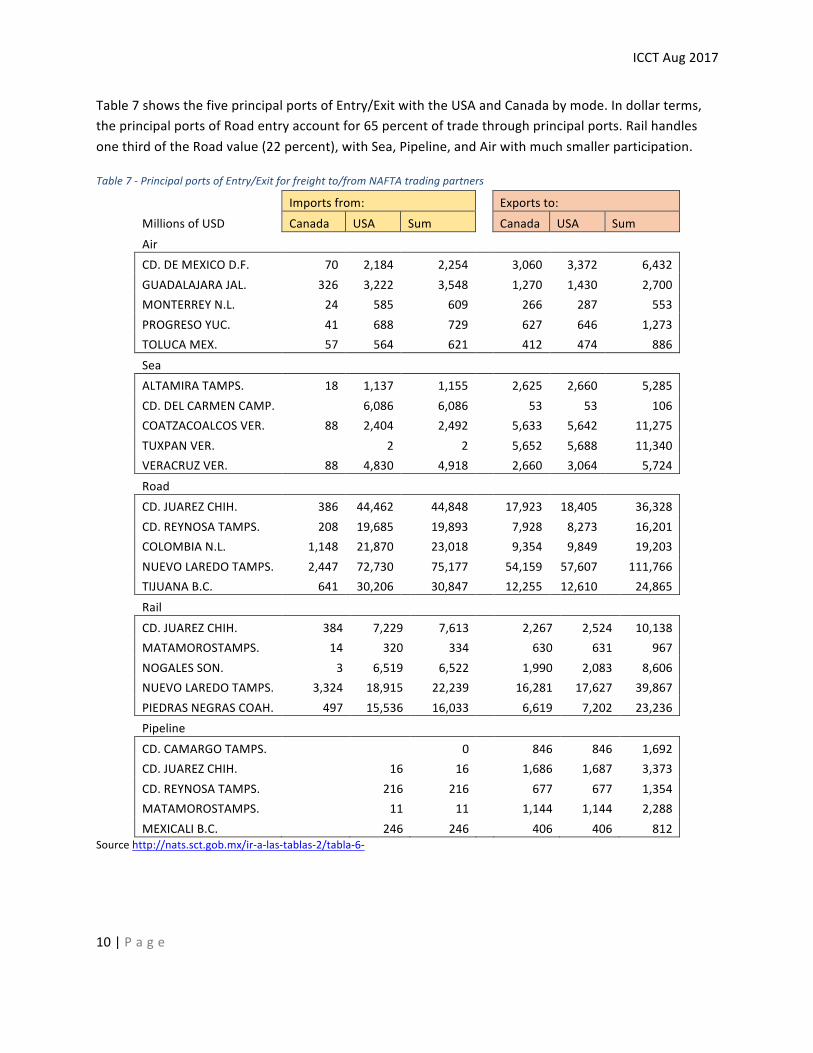

Table7showsthefiveprincipalportsofEntry/ExitwiththeUSAandCanadabymode.Indollarterms,theprincipalportsofRoadentryaccountfor65percentoftradethroughprincipalports.RailhandlesonethirdoftheRoadvalue(22percent),withSea,Pipeline,andAirwithmuchsmallerparticipation.

Table7-PrincipalportsofEntry/Exitforfreightto/fromNAFTAtradingpartners

Importsfrom: Exportsto:MillionsofUSD Canada USA Sum Canada USA SumAir CD.DEMEXICOD.F. 70 2,184 2,254 3,060 3,372 6,432GUADALAJARAJAL. 326 3,222 3,548 1,270 1,430 2,700MONTERREYN.L. 24 585 609 266 287 553PROGRESOYUC. 41 688 729 627 646 1,273TOLUCAMEX. 57 564 621 412 474 886Sea ALTAMIRATAMPS. 18 1,137 1,155 2,625 2,660 5,285CD.DELCARMENCAMP. 6,086 6,086 53 53 106COATZACOALCOSVER. 88 2,404 2,492 5,633 5,642 11,275TUXPANVER. 2 2 5,652 5,688 11,340VERACRUZVER. 88 4,830 4,918 2,660 3,064 5,724Road CD.JUAREZCHIH. 386 44,462 44,848 17,923 18,405 36,328CD.REYNOSATAMPS. 208 19,685 19,893 7,928 8,273 16,201COLOMBIAN.L. 1,148 21,870 23,018 9,354 9,849 19,203NUEVOLAREDOTAMPS. 2,447 72,730 75,177 54,159 57,607 111,766TIJUANAB.C. 641 30,206 30,847 12,255 12,610 24,865Rail CD.JUAREZCHIH. 384 7,229 7,613 2,267 2,524 10,138MATAMOROSTAMPS. 14 320 334 630 631 967NOGALESSON. 3 6,519 6,522 1,990 2,083 8,606NUEVOLAREDOTAMPS. 3,324 18,915 22,239 16,281 17,627 39,867PIEDRASNEGRASCOAH. 497 15,536 16,033 6,619 7,202 23,236Pipeline CD.CAMARGOTAMPS. 0 846 846 1,692CD.JUAREZCHIH. 16 16 1,686 1,687 3,373CD.REYNOSATAMPS. 216 216 677 677 1,354MATAMOROSTAMPS. 11 11 1,144 1,144 2,288MEXICALIB.C. 246 246 406 406 812

Sourcehttp://nats.sct.gob.mx/ir-a-las-tablas-2/tabla-6-

ICCTAug2017

11|P a g e

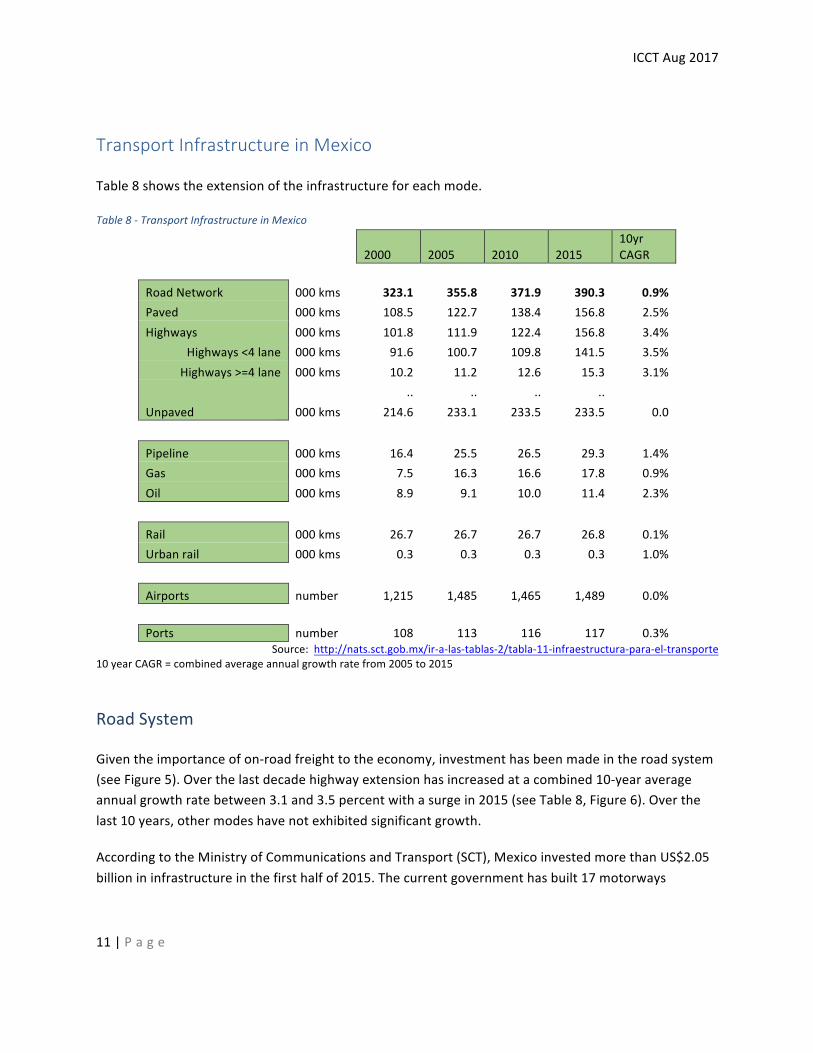

TransportInfrastructureinMexico

Table8showstheextensionoftheinfrastructureforeachmode.

Table8-TransportInfrastructureinMexico

2000 2005 2010 201510yrCAGR

RoadNetwork 000kms 323.1 355.8 371.9 390.3 0.9%Paved 000kms 108.5 122.7 138.4 156.8 2.5%Highways 000kms 101.8 111.9 122.4 156.8 3.4%

Highways<4lane 000kms 91.6 100.7 109.8 141.5 3.5%Highways>=4lane 000kms 10.2 11.2 12.6 15.3 3.1%

.. .. .. ..

Unpaved 000kms 214.6 233.1 233.5 233.5 0.0

Pipeline 000kms 16.4 25.5 26.5 29.3 1.4%Gas 000kms 7.5 16.3 16.6 17.8 0.9%Oil 000kms 8.9 9.1 10.0 11.4 2.3%

Rail 000kms 26.7 26.7 26.7 26.8 0.1%Urbanrail 000kms 0.3 0.3 0.3 0.3 1.0%

Airports number 1,215 1,485 1,465 1,489 0.0% Ports number 108 113 116 117 0.3%

Source:http://nats.sct.gob.mx/ir-a-las-tablas-2/tabla-11-infraestructura-para-el-transporte10yearCAGR=combinedaverageannualgrowthratefrom2005to2015

RoadSystem

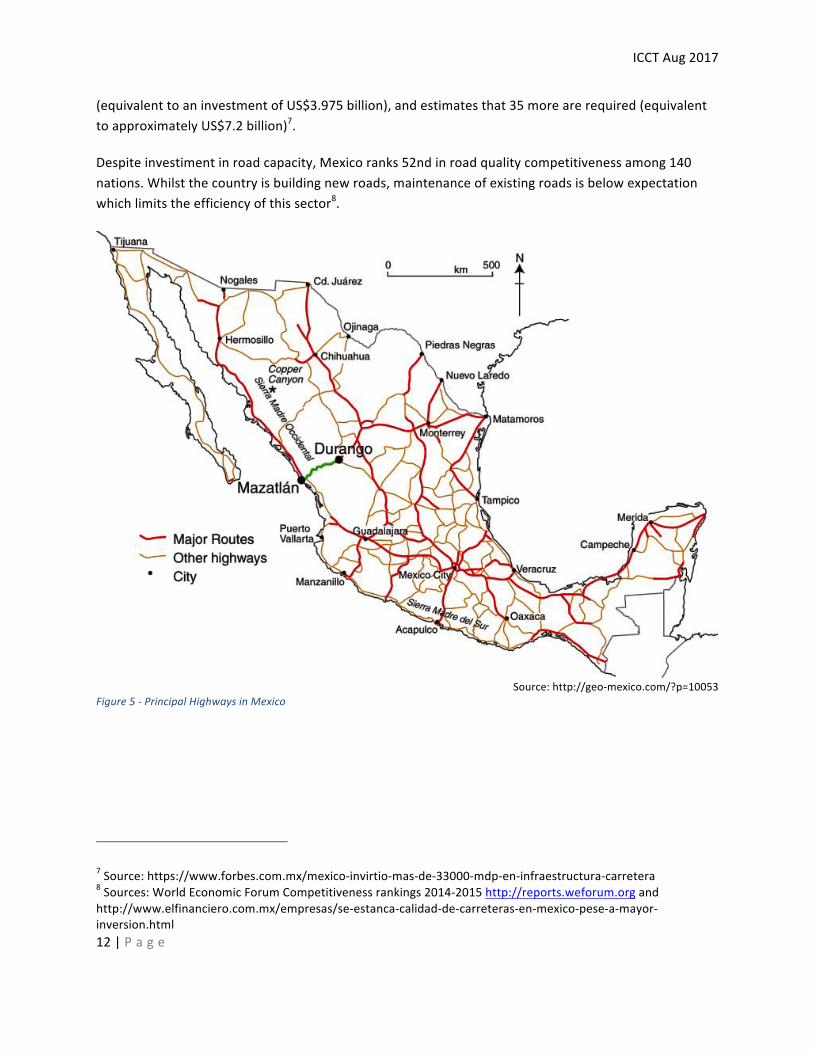

Giventheimportanceofon-roadfreighttotheeconomy,investmenthasbeenmadeintheroadsystem(seeFigure5).Overthelastdecadehighwayextensionhasincreasedatacombined10-yearaverageannualgrowthratebetween3.1and3.5percentwithasurgein2015(seeTable8,Figure6).Overthelast10years,othermodeshavenotexhibitedsignificantgrowth.

AccordingtotheMinistryofCommunicationsandTransport(SCT),MexicoinvestedmorethanUS$2.05billionininfrastructureinthefirsthalfof2015.Thecurrentgovernmenthasbuilt17motorways

ICCTAug2017

12|P a g e

(equivalenttoaninvestmentofUS$3.975billion),andestimatesthat35morearerequired(equivalenttoapproximatelyUS$7.2billion)7.

Despiteinvestimentinroadcapacity,Mexicoranks52ndinroadqualitycompetitivenessamong140nations.Whilstthecountryisbuildingnewroads,maintenanceofexistingroadsisbelowexpectationwhichlimitstheefficiencyofthissector8.

Source:http://geo-mexico.com/?p=10053

Figure5-PrincipalHighwaysinMexico

7Source:https://www.forbes.com.mx/mexico-invirtio-mas-de-33000-mdp-en-infraestructura-carretera8Sources:WorldEconomicForumCompetitivenessrankings2014-2015http://reports.weforum.organdhttp://www.elfinanciero.com.mx/empresas/se-estanca-calidad-de-carreteras-en-mexico-pese-a-mayor-inversion.html

ICCTAug2017

13|P a g e

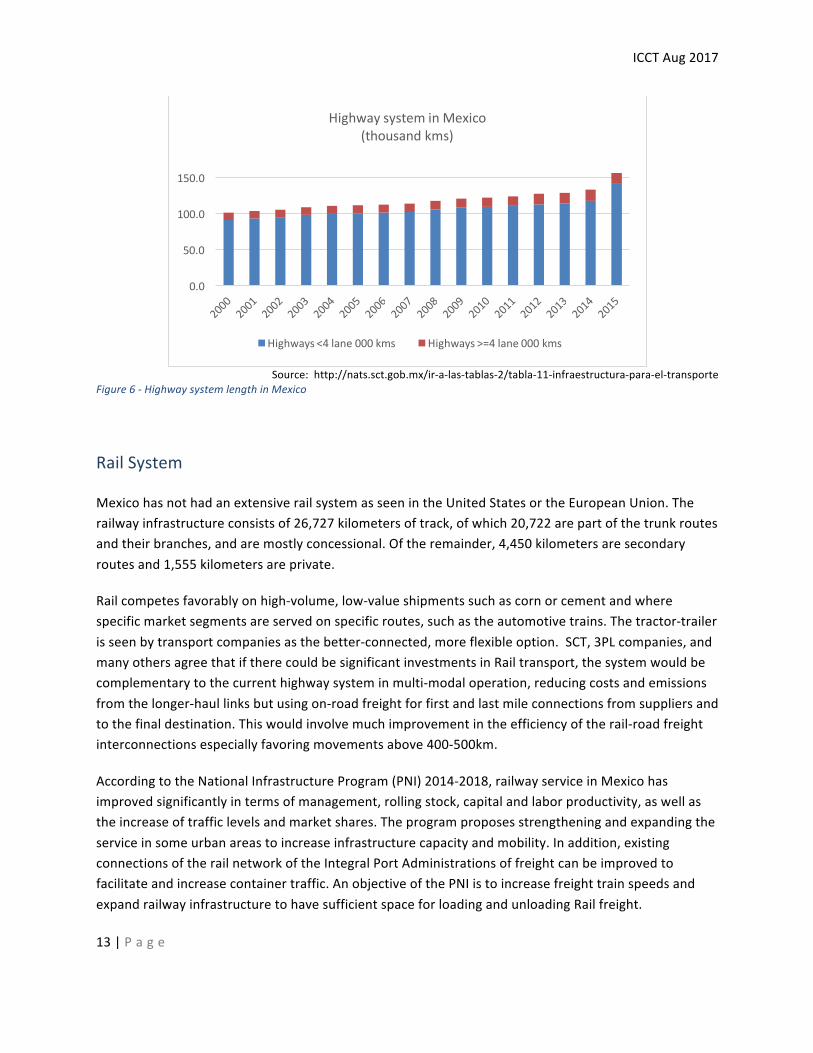

Source:http://nats.sct.gob.mx/ir-a-las-tablas-2/tabla-11-infraestructura-para-el-transporte

Figure6-HighwaysystemlengthinMexico

RailSystem

MexicohasnothadanextensiverailsystemasseenintheUnitedStatesortheEuropeanUnion.Therailwayinfrastructureconsistsof26,727kilometersoftrack,ofwhich20,722arepartofthetrunkroutesandtheirbranches,andaremostlyconcessional.Oftheremainder,4,450kilometersaresecondaryroutesand1,555kilometersareprivate.

Railcompetesfavorablyonhigh-volume,low-valueshipmentssuchascornorcementandwherespecificmarketsegmentsareservedonspecificroutes,suchastheautomotivetrains.Thetractor-trailerisseenbytransportcompaniesasthebetter-connected,moreflexibleoption.SCT,3PLcompanies,andmanyothersagreethatiftherecouldbesignificantinvestmentsinRailtransport,thesystemwouldbecomplementarytothecurrenthighwaysysteminmulti-modaloperation,reducingcostsandemissionsfromthelonger-haullinksbutusingon-roadfreightforfirstandlastmileconnectionsfromsuppliersandtothefinaldestination.Thiswouldinvolvemuchimprovementintheefficiencyoftherail-roadfreightinterconnectionsespeciallyfavoringmovementsabove400-500km.

AccordingtotheNationalInfrastructureProgram(PNI)2014-2018,railwayserviceinMexicohasimprovedsignificantlyintermsofmanagement,rollingstock,capitalandlaborproductivity,aswellastheincreaseoftrafficlevelsandmarketshares.Theprogramproposesstrengtheningandexpandingtheserviceinsomeurbanareastoincreaseinfrastructurecapacityandmobility.Inaddition,existingconnectionsoftherailnetworkoftheIntegralPortAdministrationsoffreightcanbeimprovedtofacilitateandincreasecontainertraffic.AnobjectiveofthePNIistoincreasefreighttrainspeedsandexpandrailwayinfrastructuretohavesufficientspaceforloadingandunloadingRailfreight.

0.0

50.0

100.0

150.0

HighwaysysteminMexico(thousandkms)

Highways<4lane000kms Highways>=4lane000kms

ICCTAug2017

14|P a g e

IncludedinthisprogramistheconstructionoftheCelayarailbypass,includinga19.4kmpatioforrail-roadfreightinterconnectionandtheshortsectionoftheAguascalientes-Guadalajararailroad,theManzanillo-TampicoandManzanillo-NuevoLaredorailcorridors.Thelatterwillhavealengthof188.1kilometers,becomingakeyplayerinfreightmovementsbetweentheGulfandthePacificandtotheUnitedStates.

Likewise,itisenvisagedintheNIPthemodernizationoftheChiapas-Mayabrailroad,TheCoatzacoalcoscorridorandtheuseoftheTranspeninsularTrain.

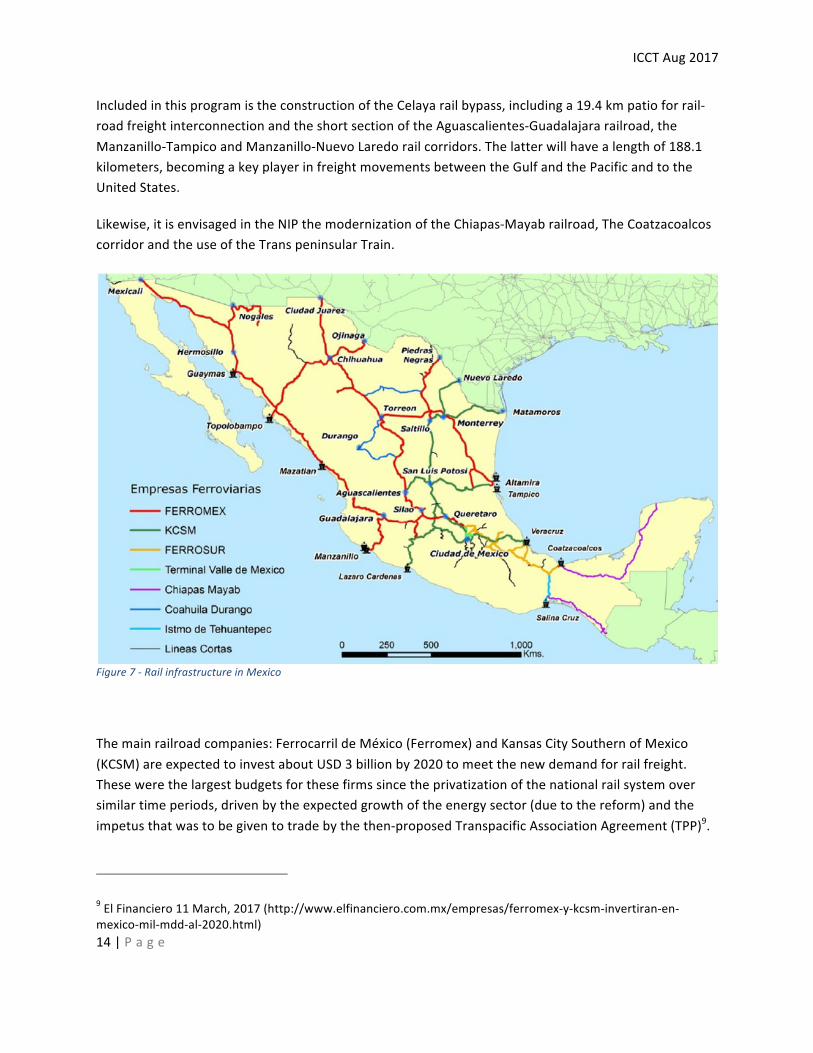

Figure7-RailinfrastructureinMexico

Themainrailroadcompanies:FerrocarrildeMéxico(Ferromex)andKansasCitySouthernofMexico(KCSM)areexpectedtoinvestaboutUSD3billionby2020tomeetthenewdemandforrailfreight.Thesewerethelargestbudgetsforthesefirmssincetheprivatizationofthenationalrailsystemoversimilartimeperiods,drivenbytheexpectedgrowthoftheenergysector(duetothereform)andtheimpetusthatwastobegiventotradebythethen-proposedTranspacificAssociationAgreement(TPP)9.

9ElFinanciero11March,2017(http://www.elfinanciero.com.mx/empresas/ferromex-y-kcsm-invertiran-en-mexico-mil-mdd-al-2020.html)

ICCTAug2017

15|P a g e

Theinvestmentswillbeusedtoexpandthetractionofthelocomotivefleet,aswellasintherenovationoftracksandtrains.

Despitetheseinvestments,mostfreightcompaniesintervieweddonotseeRailascompetingwithtractor-trailertrucksinMexico.ThelevelofRailinfrastructureinvestmenttobeabletocompetewithhighway,forgeneralfreight,wouldbeexpensiveandpoliticallycomplexduetotheconcessionsysteminplace.

Multimodalfreight

FreightterminalsinMexicomustbeauthorizedbytheMinistryofCommunicationsandTransport(SCT)andinadditiontoallowingtheloadingandunloadingoffreightbetweentherailwayandon-roadtransport,canprovideservicessuchasreception,storage,classification,consolidation,anddispatchoffreight.

In2015,therewere59railfreightterminalsoperatingwithpermits,mainlyinthestatesofNuevoLeón(25%),StateofMexico(15%),Jalisco(10%)Querétaro(10%),Hidalgo(8%)andS.L.P.(8%).

MultimodaltransportisconsideredanareaofopportunityinnationallogisticstoboostMexico'sdevelopment.Bothforthedomesticmarketandexports,manymultimodaltriplengthsaregreaterthan400-500kilometers,abovewhichRail,ifproperlyexploited,cangeneratebothcostandemissionssavings10.

Pipelines

InDecember2013,Mexico’senergyreformopenedtheenergyindustrytovariousdegreesofprivateparticipationandcompetition.ThishasnotledtoanincreaseinnationalgasproductionbecausemorethanhalfofMexico’snaturalgasproductionisassociatedgasfromoilandislocatedatthesouthernendofthecountry.Domesticgassupplyhasdeclinedbynearly0.9billioncubicfeetperday(Bcf/d)since2010to4.1Bcf/din2015asoilproductionlagged,butatthesametime,demandforgaspickedup,mostlyfromthepowersector,inwhich1,990MWofnewcombinedcyclenaturalgaspowerplantswillbeinstalled,andpipelineimportsfromtheU.S.havebeenutilizedtobalancethemarket.

Tomeetthisdemand,newpipelinesarebeingbuilt(seeTable9),andexistingpipelinesarebeingexpandedorhavingtheirflowcapabilityreversed.GasimportsfromtheU.S.accountedforonly8%ofMexicangasdemandin2000.By2010,U.S.gasimportsasapercentageoftotaldemandclimbedto14%.In2016pipelineimportssurgedtoaround44%andareexpectedtoaccountforhalf,ifnotmore,oftotaldemandin2017andbeyond.Bytheendof2017,twelvenewnaturalgaspipelinesareexpected

10Source:PNIandElEconomista29April2014(http://eleconomista.com.mx/industrias/2014/04/29/transporte-multimodal-impulsara-desarrollo-mexico)

ICCTAug2017

16|P a g e

tobeplacedinservice,facilitatingnaturalgasexportgrowthfromtheUSAtoMexicoandprovidingincreasedinterconnectivityfortheMexicannaturalgasgrid.

TheexpansionsplannedfortheMexicanpipelinegridareintendedtoprovidealong-termfoundationforincreasednaturalgasburn,withimportsgraduallyincreasingasprojectsarecompleted.

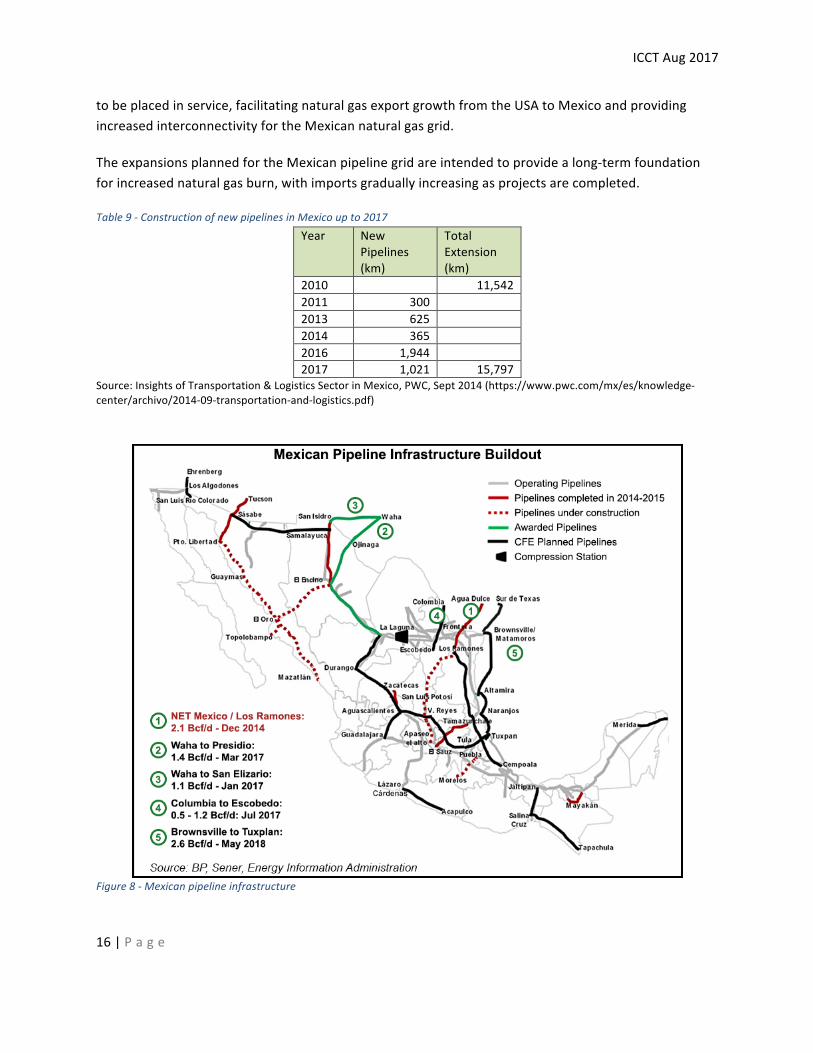

Table9-ConstructionofnewpipelinesinMexicoupto2017Year New

Pipelines(km)

TotalExtension(km)

2010 11,5422011 300 2013 625 2014 365 2016 1,944 2017 1,021 15,797

Source:InsightsofTransportation&LogisticsSectorinMexico,PWC,Sept2014(https://www.pwc.com/mx/es/knowledge-center/archivo/2014-09-transportation-and-logistics.pdf)

Figure8-Mexicanpipelineinfrastructure

ICCTAug2017

17|P a g e

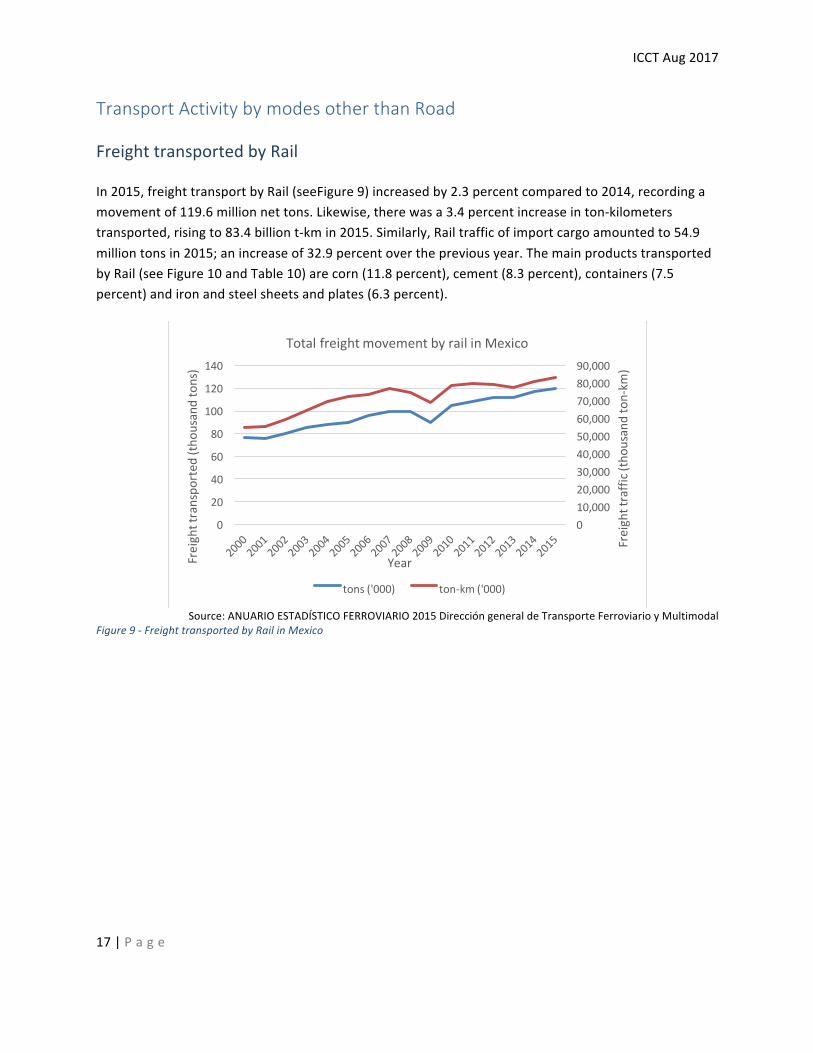

TransportActivitybymodesotherthanRoad

FreighttransportedbyRail

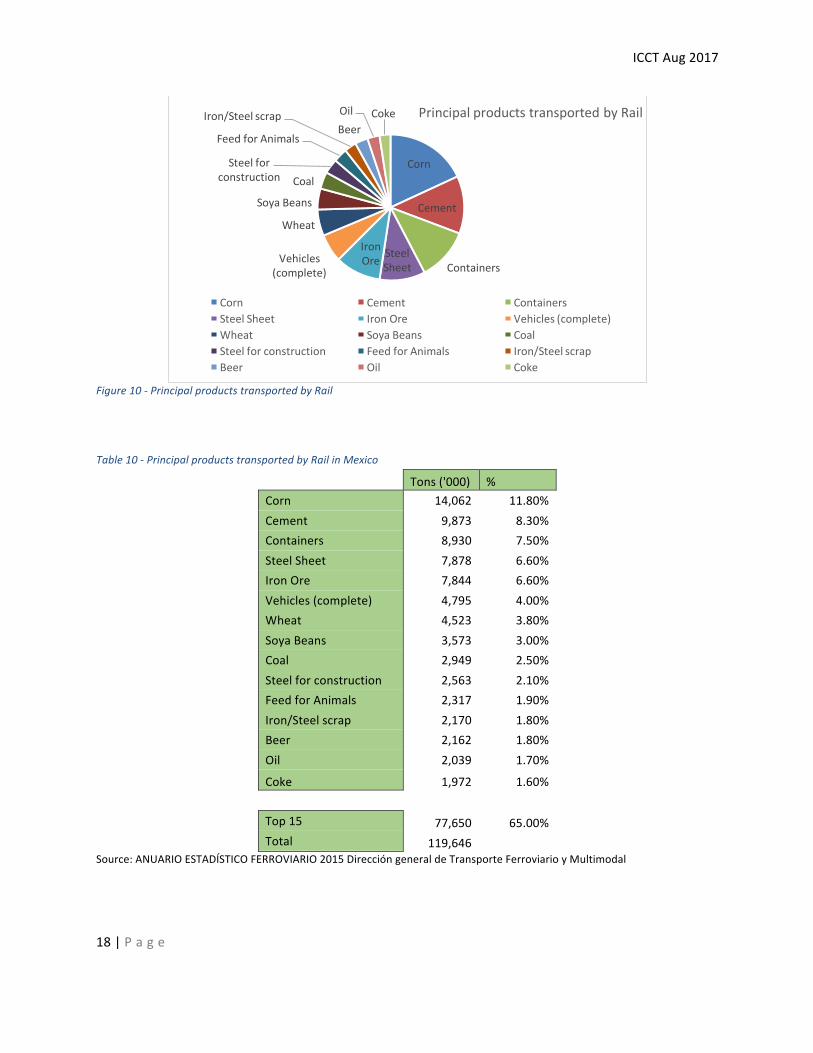

In2015,freighttransportbyRail(seeFigure9)increasedby2.3percentcomparedto2014,recordingamovementof119.6millionnettons.Likewise,therewasa3.4percentincreaseinton-kilometerstransported,risingto83.4billiont-kmin2015.Similarly,Railtrafficofimportcargoamountedto54.9milliontonsin2015;anincreaseof32.9percentoverthepreviousyear.ThemainproductstransportedbyRail(seeFigure10andTable10)arecorn(11.8percent),cement(8.3percent),containers(7.5percent)andironandsteelsheetsandplates(6.3percent).

Source:ANUARIOESTADÍSTICOFERROVIARIO2015DireccióngeneraldeTransporteFerroviarioyMultimodal

Figure9-FreighttransportedbyRailinMexico

010,00020,00030,00040,00050,00060,00070,00080,00090,000

0

20

40

60

80

100

120

140

Freighttraffic(thou

sand

ton-km

)

Freighttranspo

rted

(tho

usandtons)

Year

TotalfreightmovementbyrailinMexico

tons('000) ton-km('000)

ICCTAug2017

18|P a g e

Figure10-PrincipalproductstransportedbyRail

Table10-PrincipalproductstransportedbyRailinMexico

Tons('000) %Corn 14,062 11.80%Cement 9,873 8.30%Containers 8,930 7.50%SteelSheet 7,878 6.60%IronOre 7,844 6.60%Vehicles(complete) 4,795 4.00%Wheat 4,523 3.80%SoyaBeans 3,573 3.00%Coal 2,949 2.50%Steelforconstruction 2,563 2.10%FeedforAnimals 2,317 1.90%Iron/Steelscrap 2,170 1.80%Beer 2,162 1.80%Oil 2,039 1.70%

Coke 1,972 1.60% Top15 77,650 65.00%Total 119,646

Source:ANUARIOESTADÍSTICOFERROVIARIO2015DireccióngeneraldeTransporteFerroviarioyMultimodal

Corn

Cement

ContainersSteelSheet

IronOreVehicles

(complete)

Wheat

SoyaBeans

CoalSteelfor

construction

FeedforAnimals

Iron/SteelscrapBeerOil Coke PrincipalproductstransportedbyRail

Corn Cement ContainersSteelSheet IronOre Vehicles(complete)Wheat SoyaBeans CoalSteelforconstruction FeedforAnimals Iron/SteelscrapBeer Oil Coke

ICCTAug2017

19|P a g e

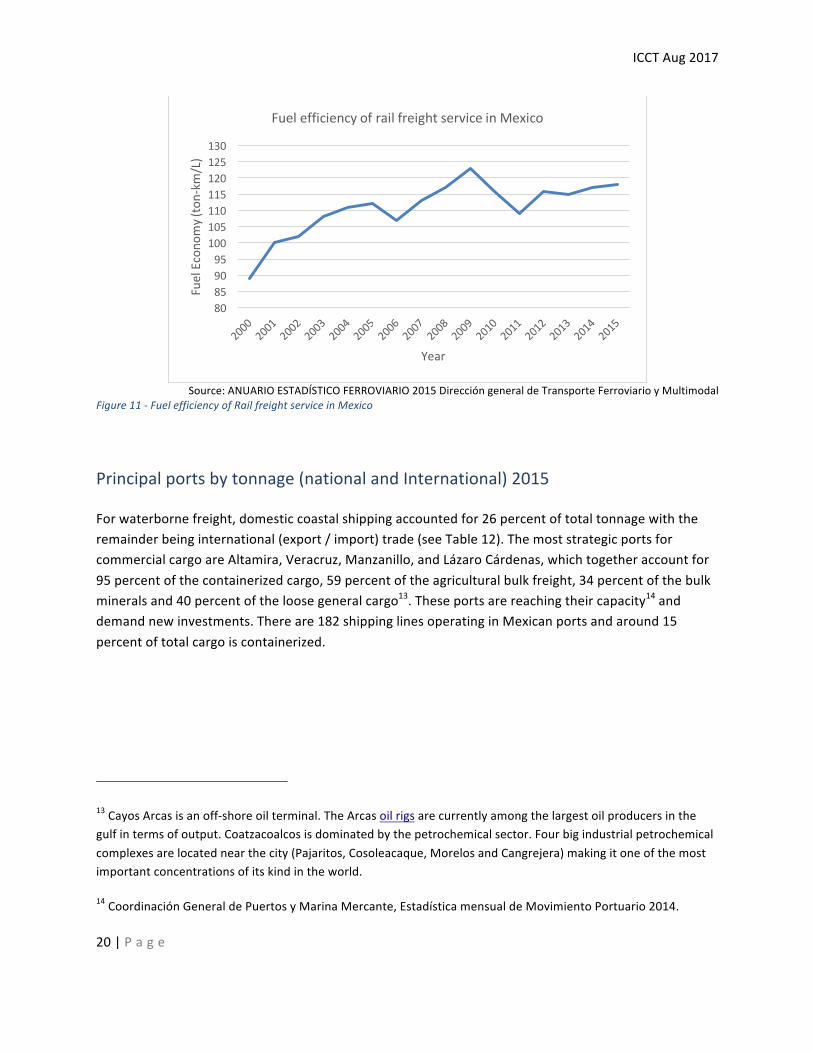

RailEnergyEfficiency

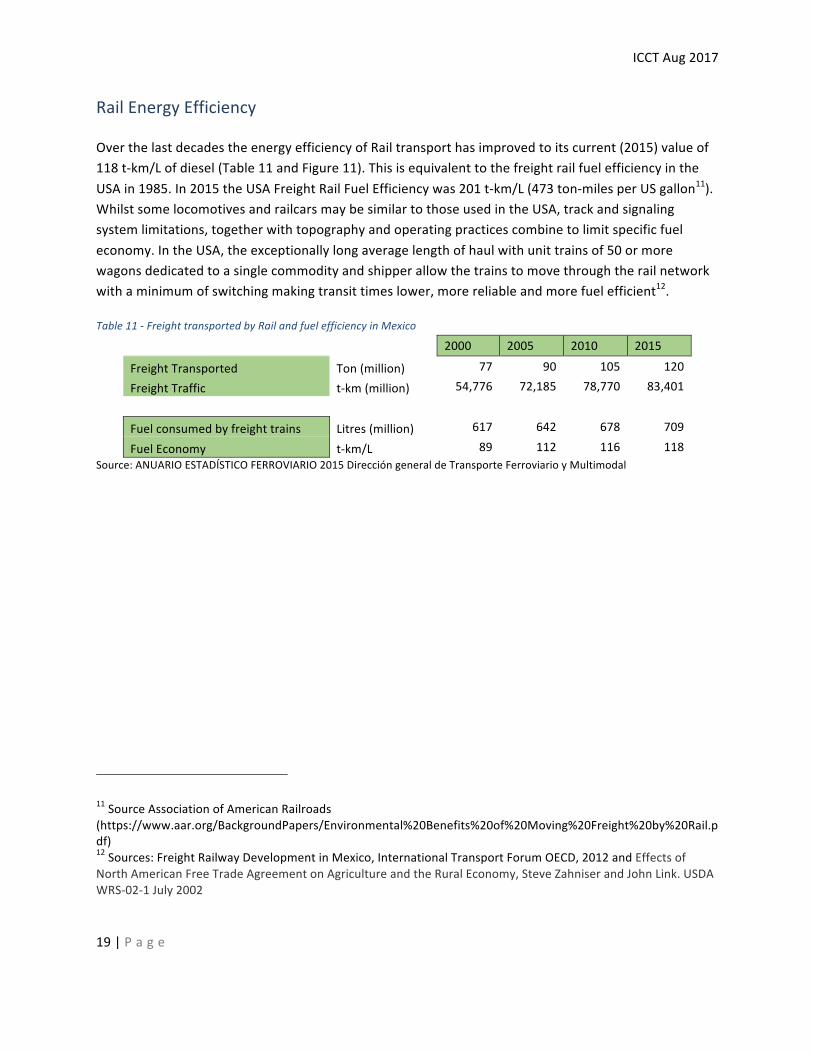

OverthelastdecadestheenergyefficiencyofRailtransporthasimprovedtoitscurrent(2015)valueof118t-km/Lofdiesel(Table11andFigure11).ThisisequivalenttothefreightrailfuelefficiencyintheUSAin1985.In2015theUSAFreightRailFuelEfficiencywas201t-km/L(473ton-milesperUSgallon11).WhilstsomelocomotivesandrailcarsmaybesimilartothoseusedintheUSA,trackandsignalingsystemlimitations,togetherwithtopographyandoperatingpracticescombinetolimitspecificfueleconomy.IntheUSA,theexceptionallylongaveragelengthofhaulwithunittrainsof50ormorewagonsdedicatedtoasinglecommodityandshipperallowthetrainstomovethroughtherailnetworkwithaminimumofswitchingmakingtransittimeslower,morereliableandmorefuelefficient12.

Table11-FreighttransportedbyRailandfuelefficiencyinMexico

2000 2005 2010 2015

FreightTransported Ton(million) 77 90 105 120

FreightTraffic t-km(million) 54,776 72,185 78,770 83,401

Fuelconsumedbyfreighttrains Litres(million) 617 642 678 709

FuelEconomy t-km/L 89 112 116 118Source:ANUARIOESTADÍSTICOFERROVIARIO2015DireccióngeneraldeTransporteFerroviarioyMultimodal

11SourceAssociationofAmericanRailroads(https://www.aar.org/BackgroundPapers/Environmental%20Benefits%20of%20Moving%20Freight%20by%20Rail.pdf)12Sources:FreightRailwayDevelopmentinMexico,InternationalTransportForumOECD,2012andEffectsofNorthAmericanFreeTradeAgreementonAgricultureandtheRuralEconomy,SteveZahniserandJohnLink.USDAWRS-02-1July2002

ICCTAug2017

20|P a g e

Source:ANUARIOESTADÍSTICOFERROVIARIO2015DireccióngeneraldeTransporteFerroviarioyMultimodal

Figure11-FuelefficiencyofRailfreightserviceinMexico

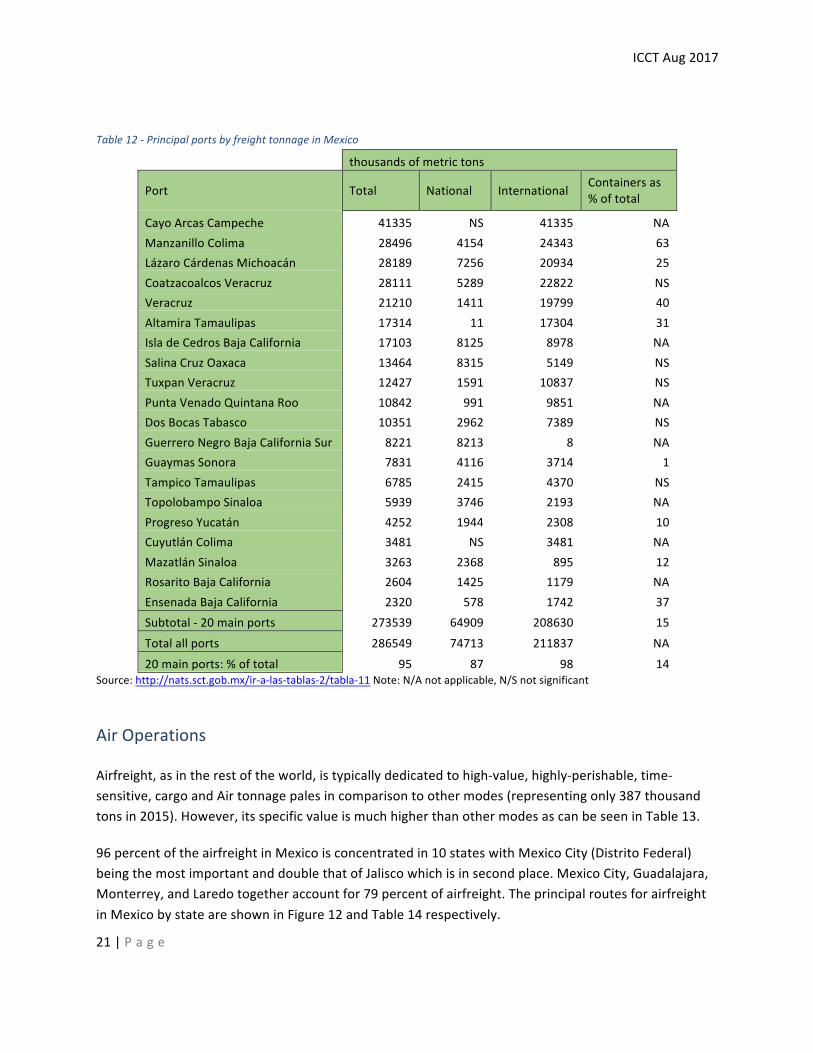

Principalportsbytonnage(nationalandInternational)2015

Forwaterbornefreight,domesticcoastalshippingaccountedfor26percentoftotaltonnagewiththeremainderbeinginternational(export/import)trade(seeTable12).ThemoststrategicportsforcommercialcargoareAltamira,Veracruz,Manzanillo,andLázaroCárdenas,whichtogetheraccountfor95percentofthecontainerizedcargo,59percentoftheagriculturalbulkfreight,34percentofthebulkmineralsand40percentoftheloosegeneralcargo13.Theseportsarereachingtheircapacity14anddemandnewinvestments.Thereare182shippinglinesoperatinginMexicanportsandaround15percentoftotalcargoiscontainerized.

13CayosArcasisanoff-shoreoilterminal.TheArcasoilrigsarecurrentlyamongthelargestoilproducersinthegulfintermsofoutput.Coatzacoalcosisdominatedbythepetrochemicalsector.Fourbigindustrialpetrochemicalcomplexesarelocatednearthecity(Pajaritos,Cosoleacaque,MorelosandCangrejera)makingitoneofthemostimportantconcentrationsofitskindintheworld.

14CoordinaciónGeneraldePuertosyMarinaMercante,EstadísticamensualdeMovimientoPortuario2014.

80859095

100105110115120125130

FuelEcono

my(ton-km

/L)

Year

FuelefficiencyofrailfreightserviceinMexico

ICCTAug2017

21|P a g e

Table12-PrincipalportsbyfreighttonnageinMexico

thousandsofmetrictons

Port Total National International Containersas%oftotal

CayoArcasCampeche 41335 NS 41335 NAManzanilloColima 28496 4154 24343 63LázaroCárdenasMichoacán 28189 7256 20934 25CoatzacoalcosVeracruz 28111 5289 22822 NSVeracruz 21210 1411 19799 40AltamiraTamaulipas 17314 11 17304 31IsladeCedrosBajaCalifornia 17103 8125 8978 NASalinaCruzOaxaca 13464 8315 5149 NSTuxpanVeracruz 12427 1591 10837 NSPuntaVenadoQuintanaRoo 10842 991 9851 NADosBocasTabasco 10351 2962 7389 NSGuerreroNegroBajaCaliforniaSur 8221 8213 8 NAGuaymasSonora 7831 4116 3714 1TampicoTamaulipas 6785 2415 4370 NSTopolobampoSinaloa 5939 3746 2193 NAProgresoYucatán 4252 1944 2308 10CuyutlánColima 3481 NS 3481 NAMazatlánSinaloa 3263 2368 895 12RosaritoBajaCalifornia 2604 1425 1179 NAEnsenadaBajaCalifornia 2320 578 1742 37Subtotal-20mainports 273539 64909 208630 15Totalallports 286549 74713 211837 NA20mainports:%oftotal 95 87 98 14

Source:http://nats.sct.gob.mx/ir-a-las-tablas-2/tabla-11Note:N/Anotapplicable,N/Snotsignificant

AirOperations

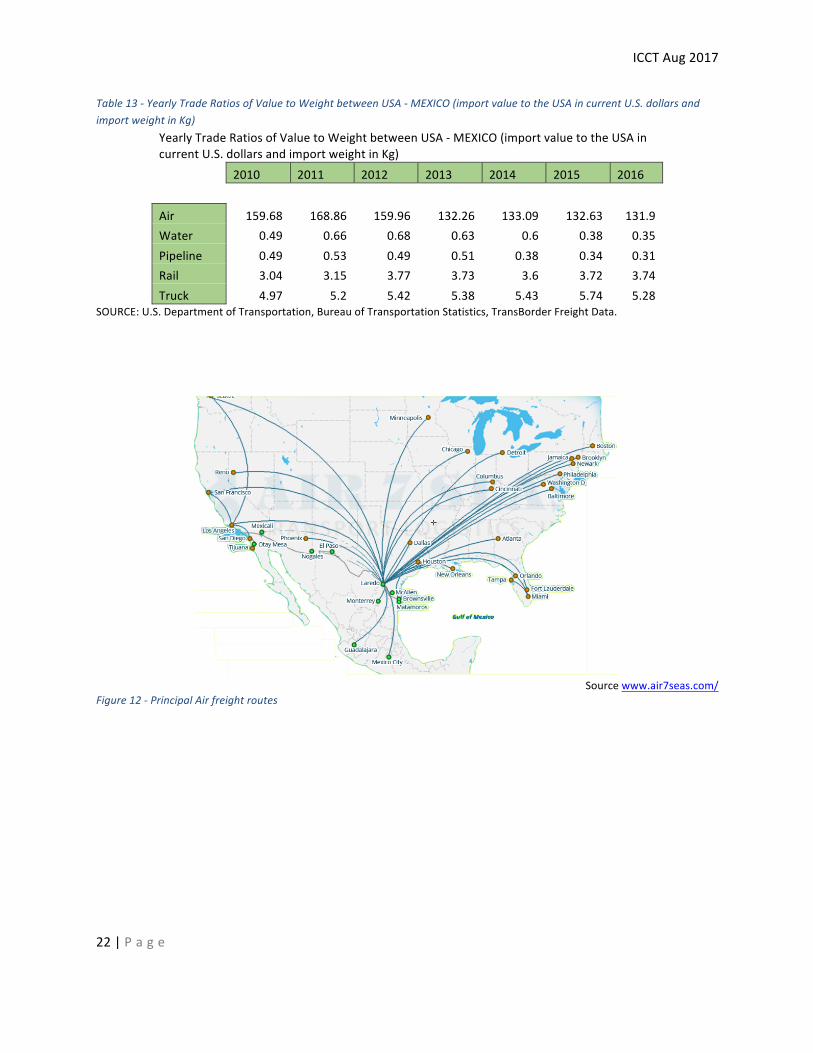

Airfreight,asintherestoftheworld,istypicallydedicatedtohigh-value,highly-perishable,time-sensitive,cargoandAirtonnagepalesincomparisontoothermodes(representingonly387thousandtonsin2015).However,itsspecificvalueismuchhigherthanothermodesascanbeseeninTable13.

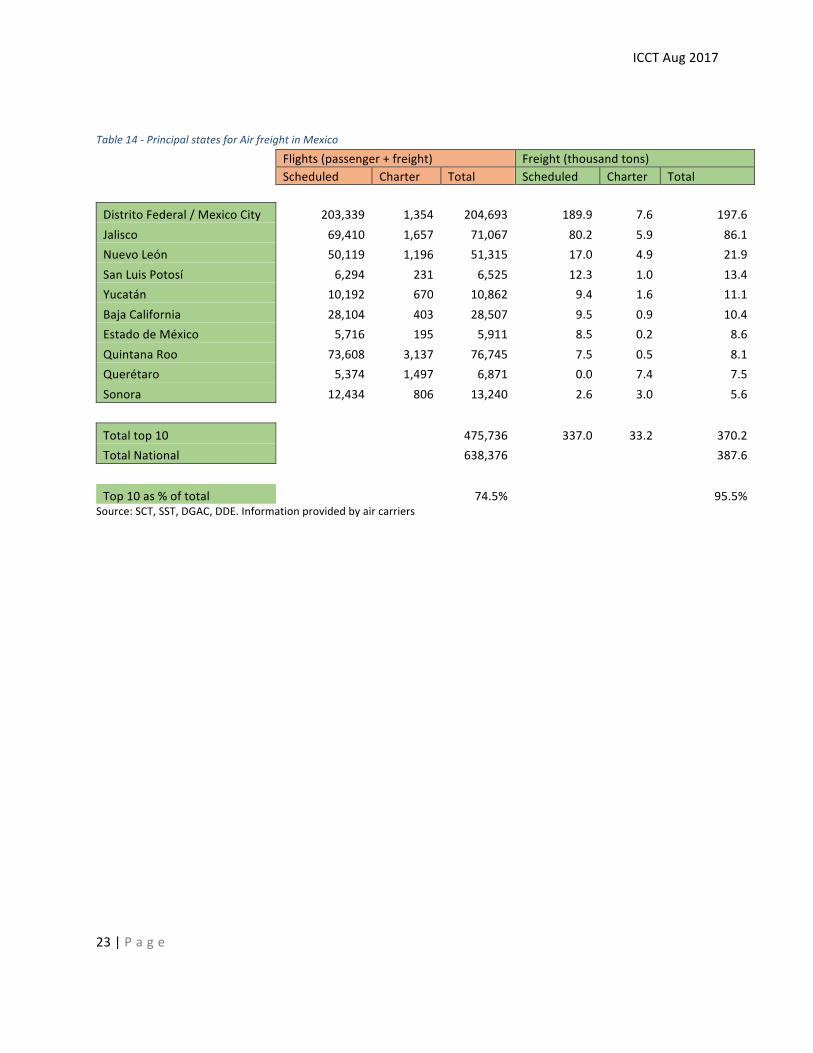

96percentoftheairfreightinMexicoisconcentratedin10stateswithMexicoCity(DistritoFederal)beingthemostimportantanddoublethatofJaliscowhichisinsecondplace.MexicoCity,Guadalajara,Monterrey,andLaredotogetheraccountfor79percentofairfreight.TheprincipalroutesforairfreightinMexicobystateareshowninFigure12andTable14respectively.

ICCTAug2017

22|P a g e

Table13-YearlyTradeRatiosofValuetoWeightbetweenUSA-MEXICO(importvaluetotheUSAincurrentU.S.dollarsandimportweightinKg)

YearlyTradeRatiosofValuetoWeightbetweenUSA-MEXICO(importvaluetotheUSAincurrentU.S.dollarsandimportweightinKg) 2010 2011 2012 2013 2014 2015 2016 Air 159.68 168.86 159.96 132.26 133.09 132.63 131.9Water 0.49 0.66 0.68 0.63 0.6 0.38 0.35Pipeline 0.49 0.53 0.49 0.51 0.38 0.34 0.31Rail 3.04 3.15 3.77 3.73 3.6 3.72 3.74Truck 4.97 5.2 5.42 5.38 5.43 5.74 5.28

SOURCE:U.S.DepartmentofTransportation,BureauofTransportationStatistics,TransBorderFreightData.

Sourcewww.air7seas.com/

Figure12-PrincipalAirfreightroutes

ICCTAug2017

23|P a g e

Table14-PrincipalstatesforAirfreightinMexico

Flights(passenger+freight) Freight(thousandtons) Scheduled Charter Total Scheduled Charter Total DistritoFederal/MexicoCity 203,339 1,354 204,693 189.9 7.6 197.6Jalisco 69,410 1,657 71,067 80.2 5.9 86.1NuevoLeón 50,119 1,196 51,315 17.0 4.9 21.9SanLuisPotosí 6,294 231 6,525 12.3 1.0 13.4Yucatán 10,192 670 10,862 9.4 1.6 11.1BajaCalifornia 28,104 403 28,507 9.5 0.9 10.4EstadodeMéxico 5,716 195 5,911 8.5 0.2 8.6QuintanaRoo 73,608 3,137 76,745 7.5 0.5 8.1Querétaro 5,374 1,497 6,871 0.0 7.4 7.5Sonora 12,434 806 13,240 2.6 3.0 5.6 Totaltop10 475,736 337.0 33.2 370.2TotalNational 638,376 387.6 Top10as%oftotal 74.5% 95.5%

Source:SCT,SST,DGAC,DDE.Informationprovidedbyaircarriers

ICCTAug2017

24|P a g e

Chapter3:-CharacteristicsofIn-useTractor-trailersinMexico

Thischaptercompilesinformationontheregistered,andactivein-usepopulationofhighwaytractorsandsemi-trailersinMexico.Itpresentsdatabysizeoffleetandbyvocation,andlooksattheexpectedlifeoftheseunits.

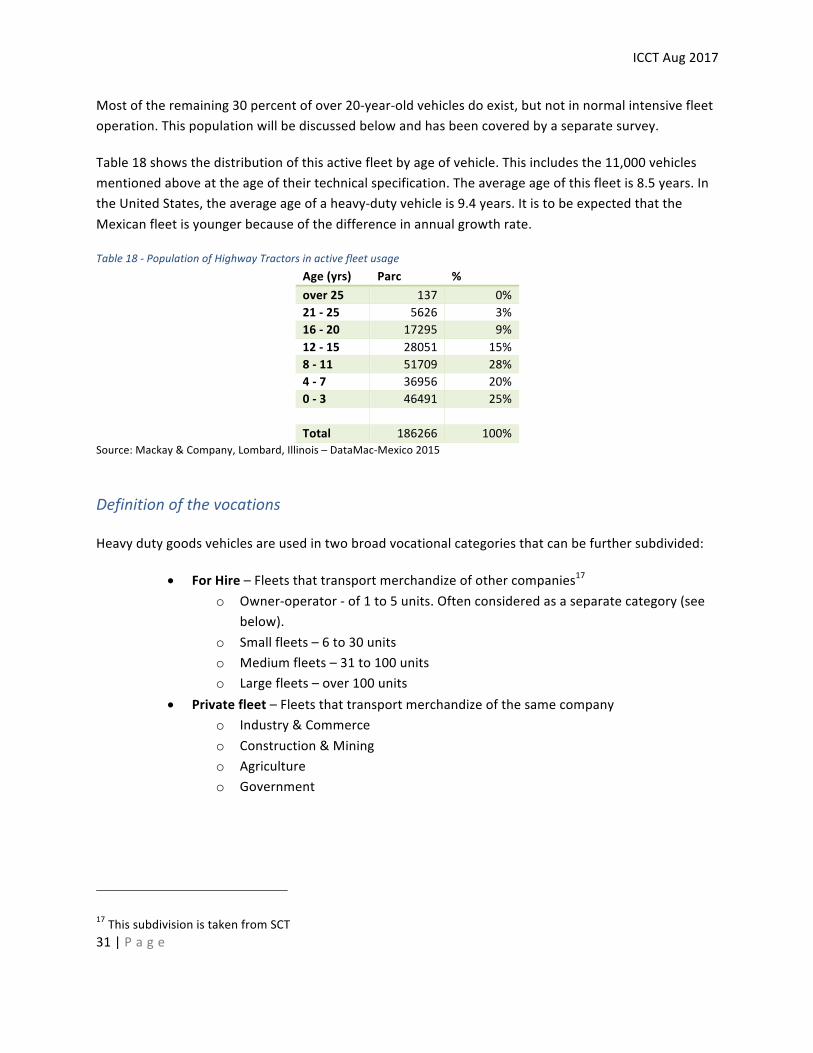

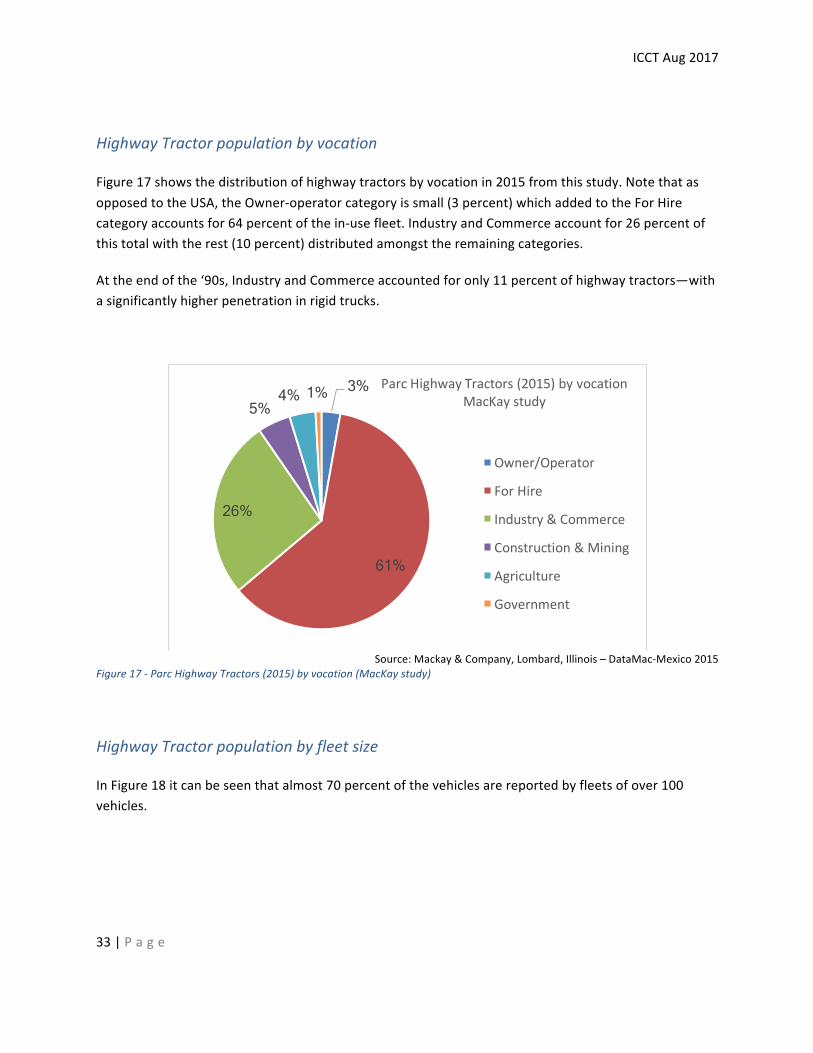

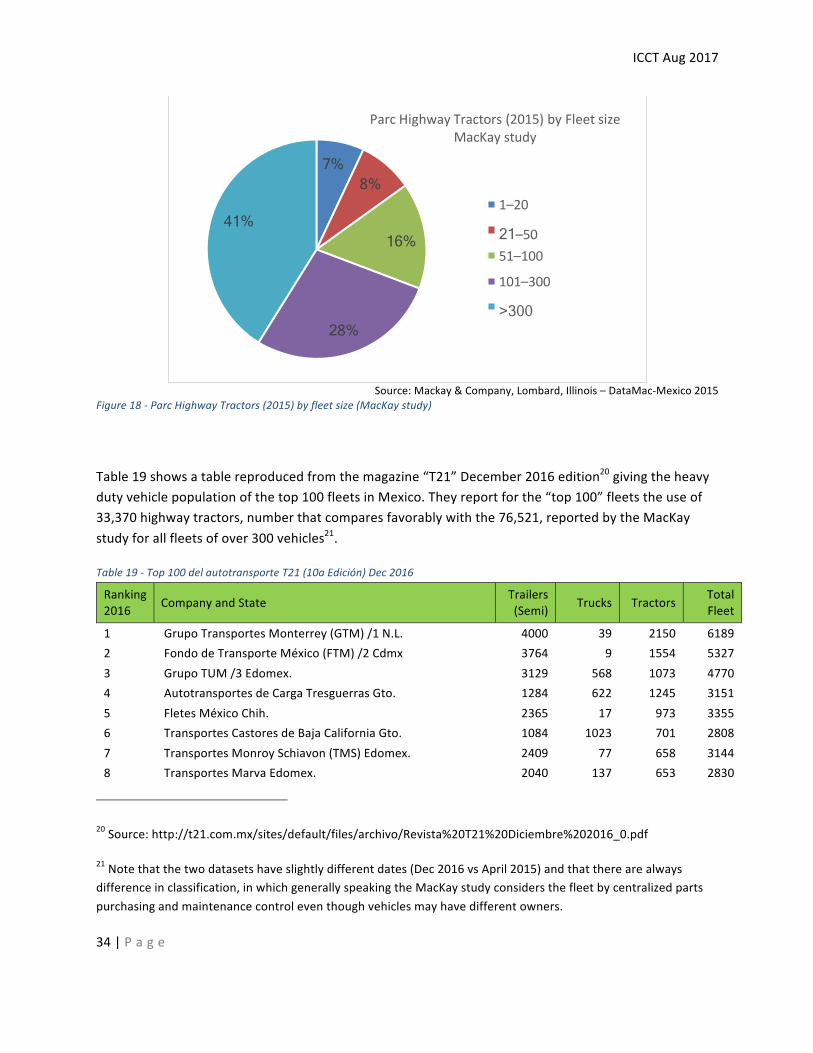

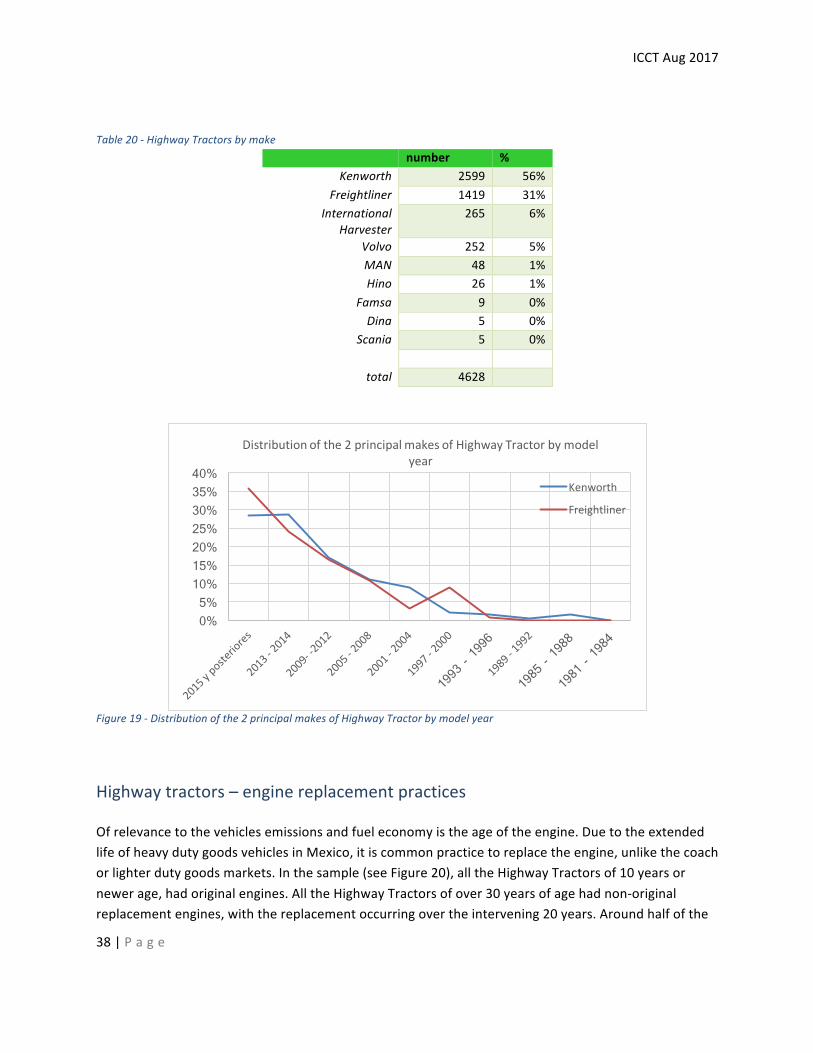

PopulationofIn-useHighwayTractorsThenationalpopulationofregisteredhighwaytractorsattheendof2016is284,349unitswhichhasgrownatanaveragerateof4.6percentperyearoverthelast10years.Thesenumbersgiveanin-usefleetaverageageof15.1yearswith30.3percentofthepopulationwithover20yearsofuse(thatismodelyear1995orearlier).However,theactivepopulationofhighwaytractorsasgivenbytheMacKayseriesofsurveysisaround70percentofthisfigure,upfrom64percentinthe‘90s.Theaverageageofthisactivefleetis8.5yearstobecomparedtotheaverageageofaheavy-dutyvehicleintheUSof9.4years.ItistobeexpectedthattheMexicanfleetisyoungerbecauseofthedifferenceinannualgrowthrate.Mostoftheremaining30percentofover20-year-oldvehiclesdoexist,butnotinnormalmain-linefleetoperation.Theprincipalvocationsoftheactivein-usefleetare“ForHire”61percentand“Industry&Commerce”26percentwithalmost70percentofthesevehiclesreportedbyfleetsofover100vehicles.Attheendofthe‘90s,IndustryandCommerceaccountedforonly11percentofhighwaytractors(withasignificantlyhigherpenetrationinrigidtrucks).Thishasgrownto26percent(in2015)andisnowdroppingagainwithincreasingusageof3PLlogisticscompaniestomanagetheirtransportneeds.Overthecoming24months,“Forhire”expectsanetincreaseof3percentinhighwaytractorsand2percentinsemi-trailerswhilst“IndustryandCommerce”arelookingataconsiderablereductioninbothof33and22percentrespectivelycausedbyapowerfulshifttowardstheuseof3PLlogisticscompanies.Onemainadvantageoftheseisthattheyareexemptfromthelimitationonprivatefleetsthathaveanyforeigninvestmentoftransportingonlythosegoodsthataredirectlyrelatedtotheirbusinessneeds,andalsohaveloweroperatingcoststhan“IndustryandCommerce”fleets.Inthemostrecentsurvey,overhalfoftheHighwayTractorsfoundinthesampleareKenworth,withFreightlinerinsecondplacewith31percent.Itisinterestingtonotethatforbothbrandsthemostrecentmodelyearsshowedthehighestpenetrations;36percentofallFreightlinersinthesamplewereof2015ornewermodelyear(comparedthe28percentofKenworth)

ChapterHighlights

ICCTAug2017

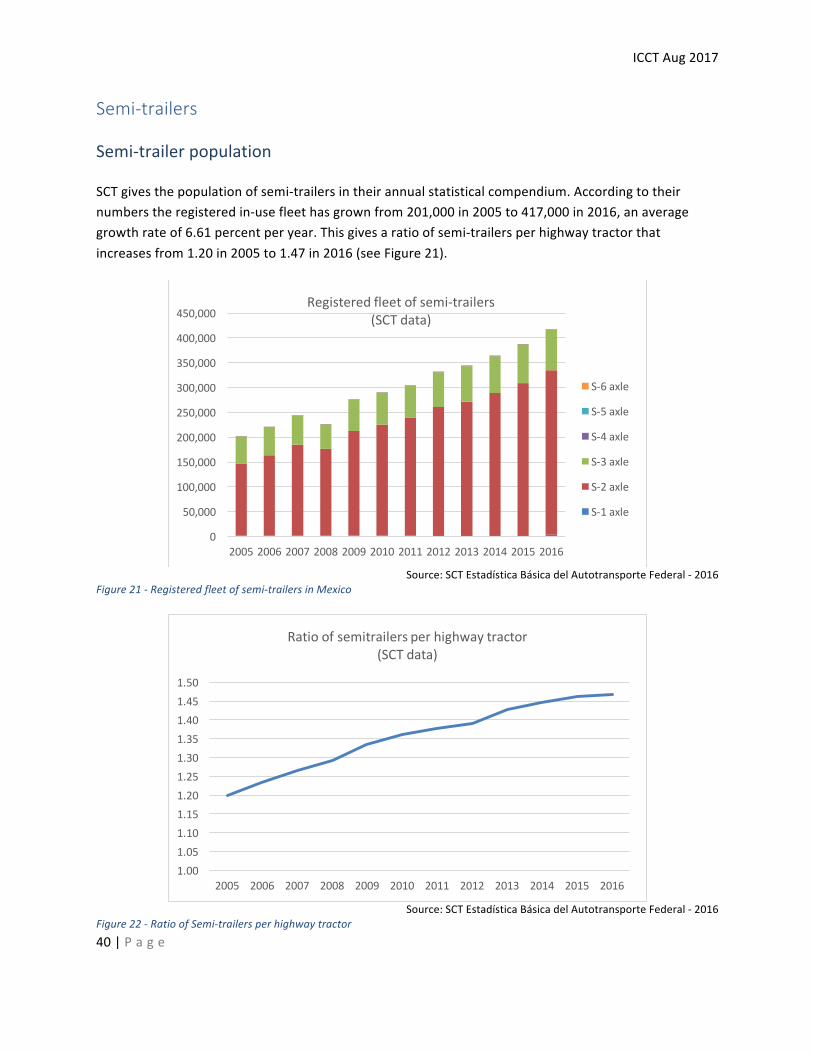

25|P a g e

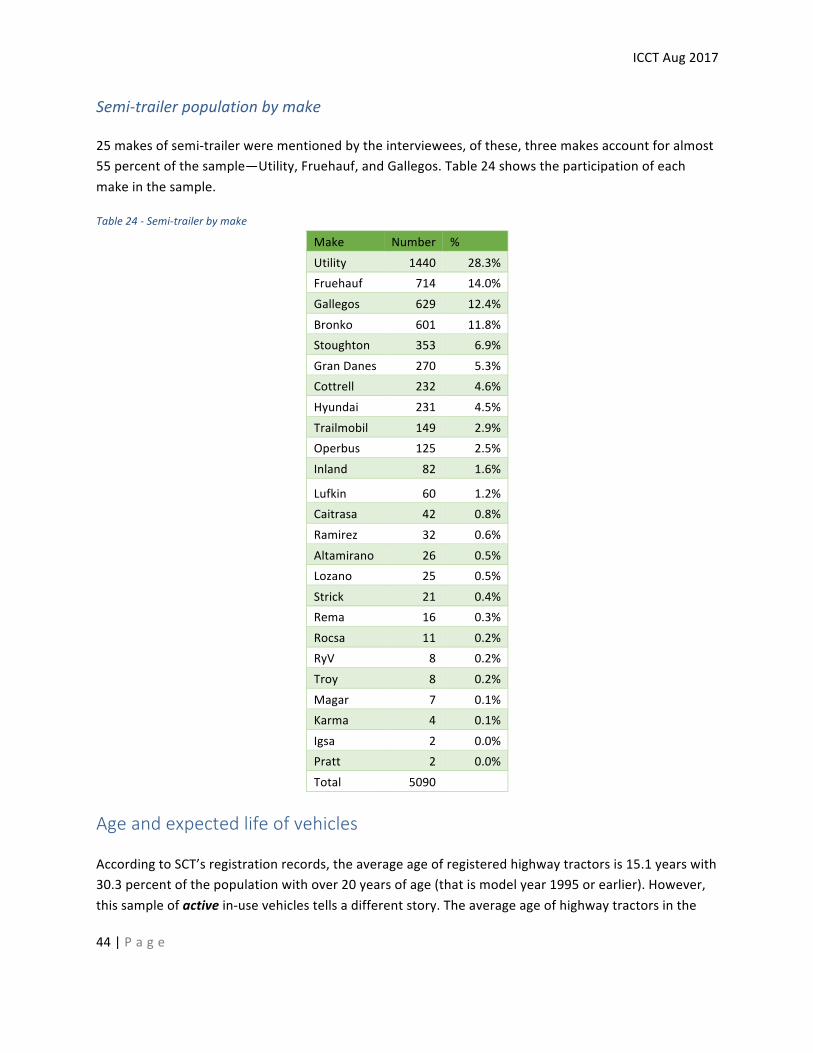

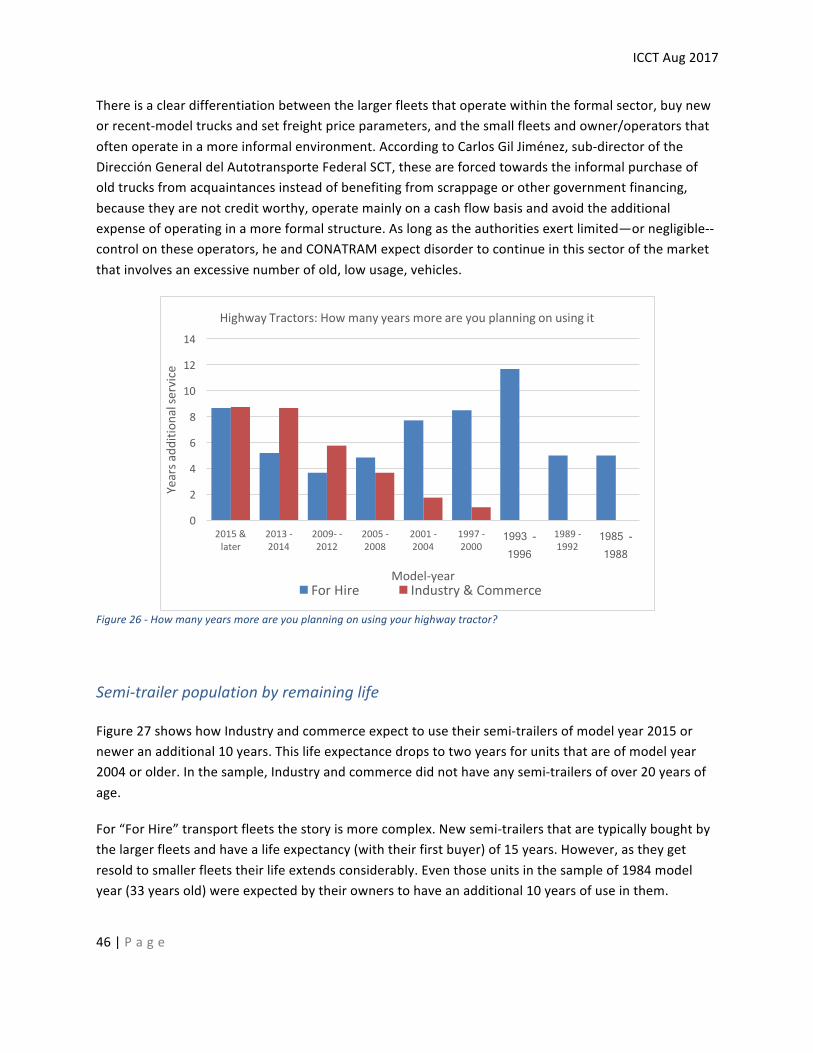

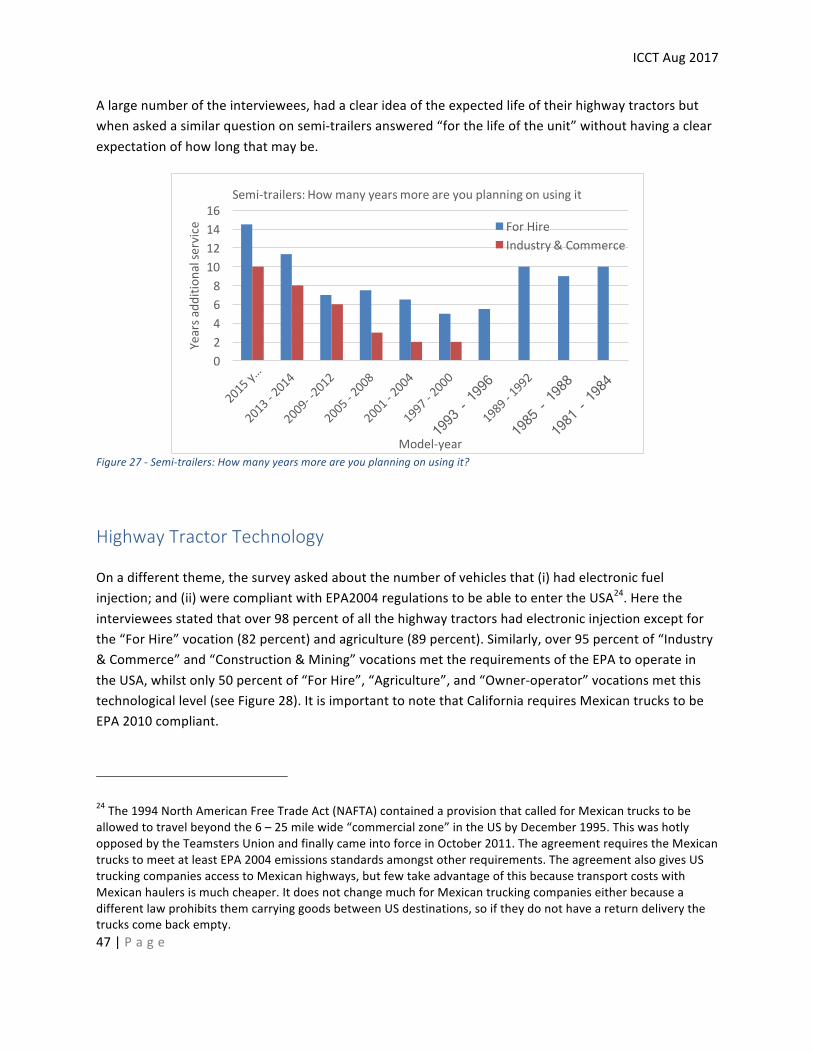

Populationofsemi-trailersThenationalpopulationofregisteredsemi-trailersattheendof2016is417,000unitswhichhasgrownatanaveragerateof6.6percentperyearoverthelast10years.Thisgivesanoverallratioofsemi-trailersperhighwaytractorthatincreasesfrom1.20in2005to1.47in2016.Byvocation,Owner/operatorhavearatioof1.17;“Forhire”transportfleets,1.46;andIndustry&Commerce2.01.TheTop100fleetsbysize(independentofvocation)givearatioof1.98semi-trailersperhighwaytractor.Asapointofreference,intheUSAsince2005,theratioofdryvanstoClass8tractorshasremainedinaverytightband:1.96to2.01trailerspertractor.Whilstfleetstendtocarefullychoosetheirtractorsbymake,trailersareconsideredmoreofacommoditywherepriceisthemaindifferencingfactor.Aswithhighwaytractors,thereisadifferenceforsemi-trailersbetweenthetotalnumberregisteredandthosefoundinfleetactiveservice.WhilsttheSCTregisterednumberswouldgiveanaverageageof16.1years,theactivefleethasanaverageageof6.9years.Inthemostrecentsurvey25makesofsemi-trailerwerementionedbytheinterviewees,ofthese,threemakesaccountforalmost55percentofthesample—Utility,Fruehauf,andGallegos.VehiclepopulationbyremaininglifeHighwaytractorsThetimethatthefleetexpectstokeepthevehicleinoperationbeforesellingit,variessubstantiallybyvocation.Industryandcommerceexpecttousetheirvehiclesofmodelyear2013orneweranadditional8years.Thislifeexpectancedropstooneyearforvehiclesthatare20yearsold.For“ForHire”transportfleetsthestoryismorecomplex.Newvehiclesthataretypicallyboughtbythelargerfleetshavealifeexpectancy(withtheirfirstbuyer)oflessthan12years.These(togetherwithprivatefleetvehicles)arethenresoldtosmallerfleetsandresoldagainuntiltheyendupinthehandsofowner-operatorsandsmallfleets.Becauseofthis,aftertheunithashad25yearsofoperation,itsexpectedlifereachesanewpeakofanadditional12years.Noneofthefleetsinthesamplehadvehiclesolderthan1984modelyear.Semi-trailersIndustryandcommerceexpecttousetheirsemi-trailersofmodelyear2015orneweranadditional10years.Thislifeexpectancedropstotwoyearsforunitsthatareofmodelyear2004orolder.Inthesample,Industryandcommercedidnothaveanysemi-trailersofover20yearsofage.

ICCTAug2017

26|P a g e

HighwayTractors

Registeredpopulation

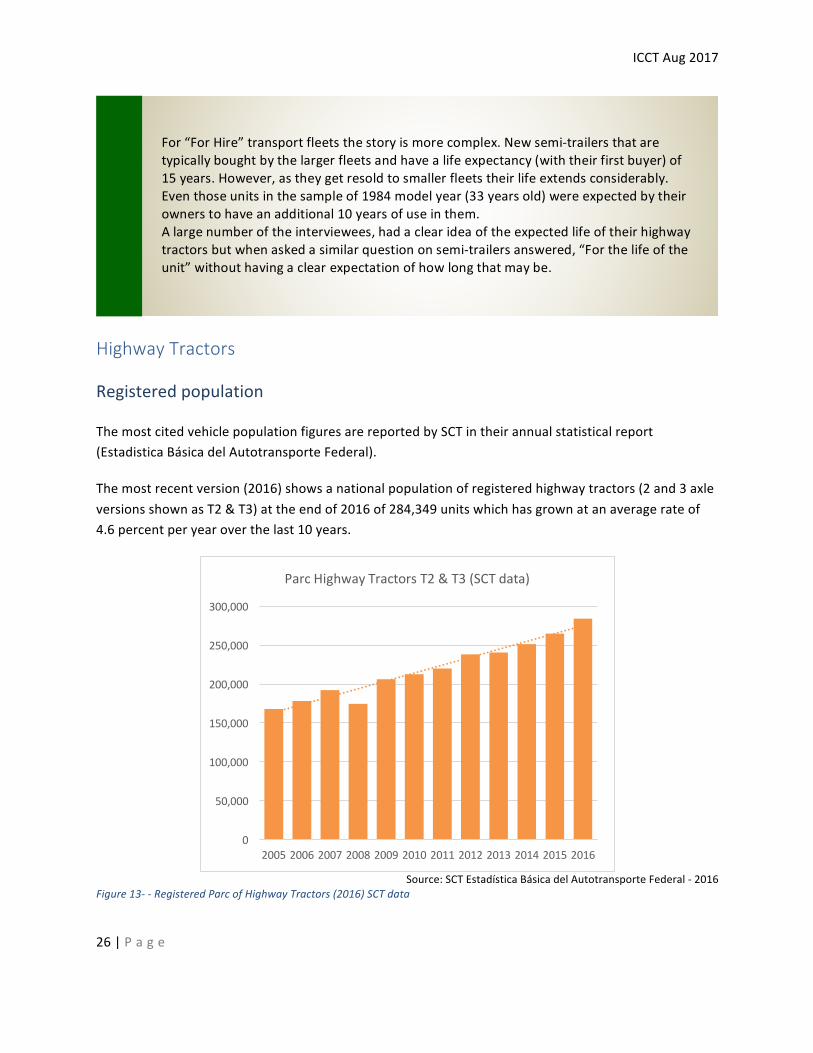

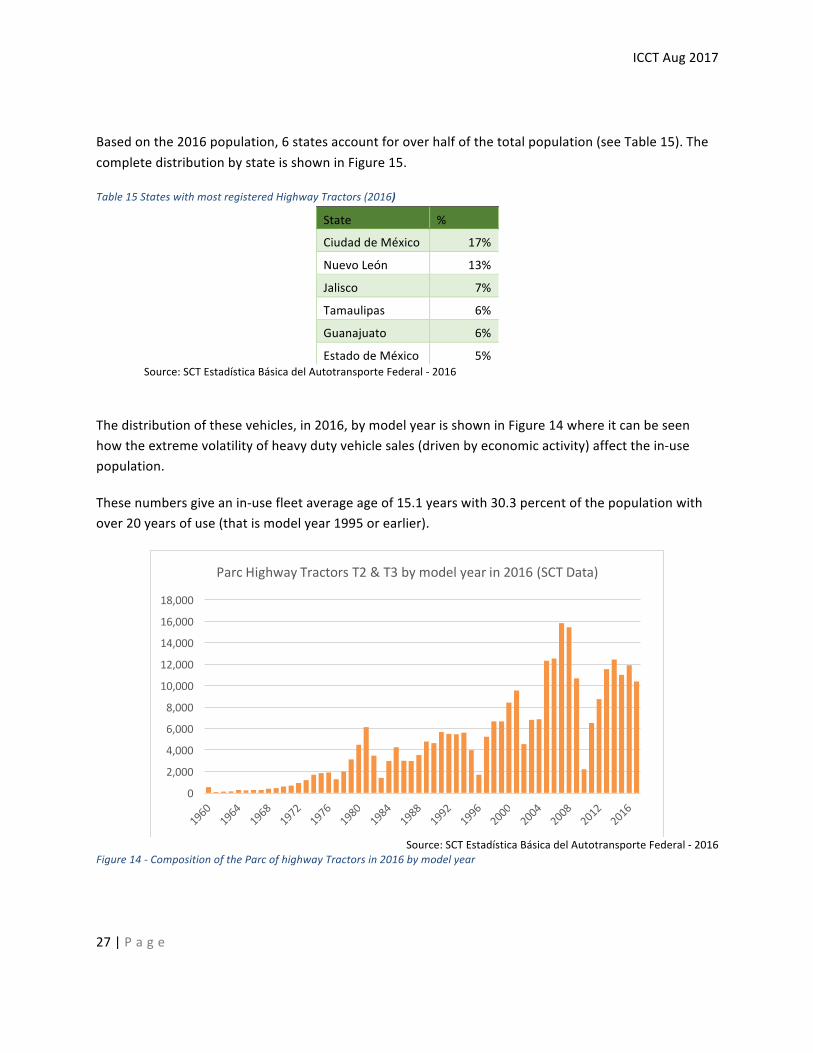

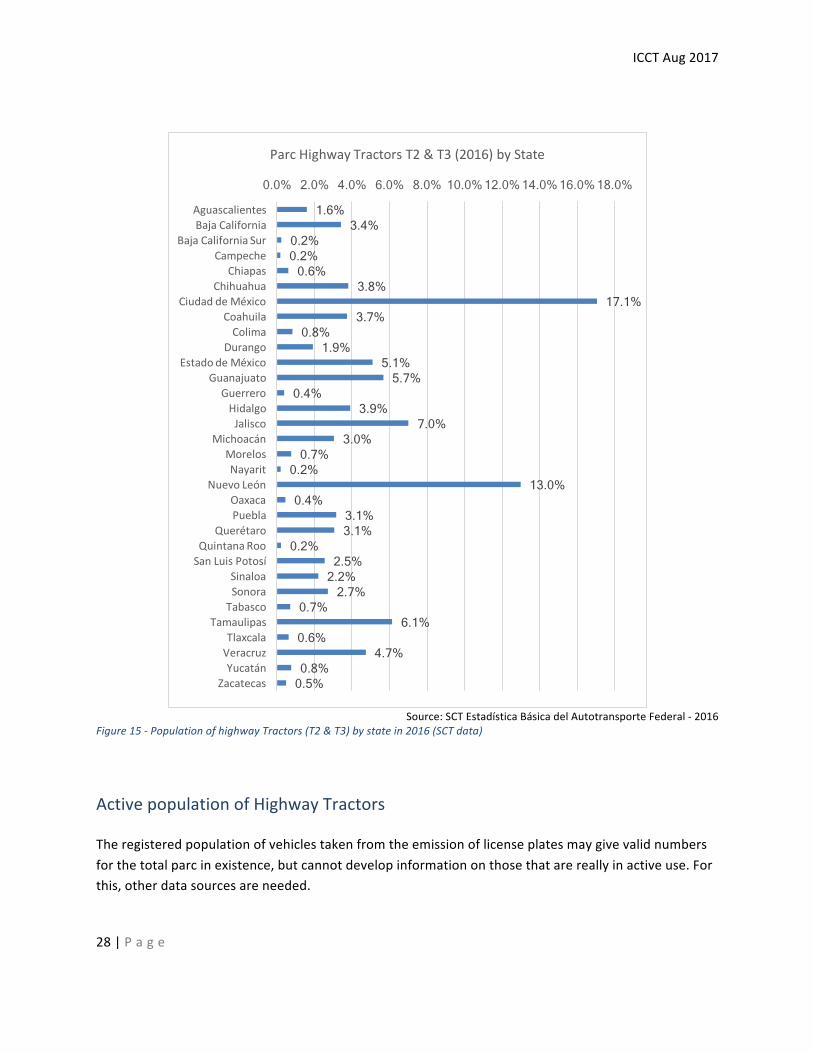

ThemostcitedvehiclepopulationfiguresarereportedbySCTintheirannualstatisticalreport(EstadisticaBásicadelAutotransporteFederal).

Themostrecentversion(2016)showsanationalpopulationofregisteredhighwaytractors(2and3axleversionsshownasT2&T3)attheendof2016of284,349unitswhichhasgrownatanaveragerateof4.6percentperyearoverthelast10years.

Source:SCTEstadísticaBásicadelAutotransporteFederal-2016

Figure13--RegisteredParcofHighwayTractors(2016)SCTdata

0

50,000

100,000

150,000

200,000

250,000

300,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

ParcHighwayTractorsT2&T3(SCTdata)