Embed Size (px)

Citation preview

1 September 2014 — Metals Monitor

1

Metals Monitor

1 September 2014 — Metals Monitor

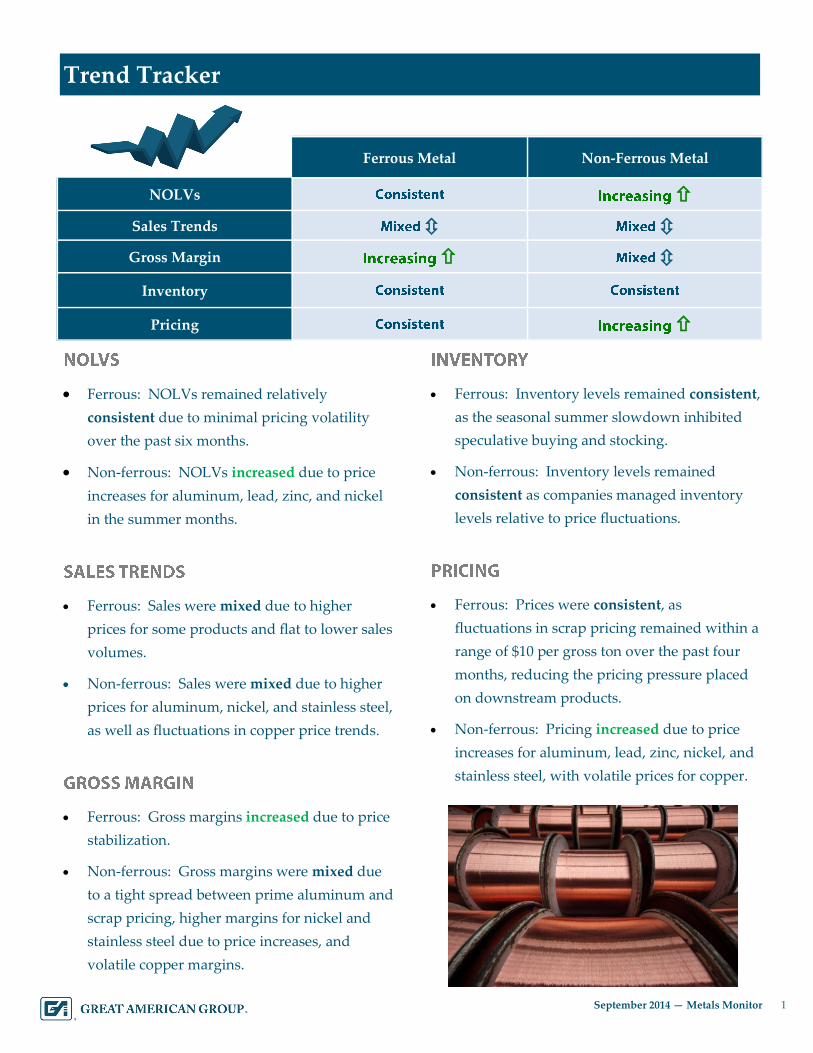

1 Trend Tracker

Ferrous: NOLVs remained relatively

consistent due to minimal pricing volatility

over the past six months.

Non-ferrous: NOLVs increased due to price

increases for aluminum, lead, zinc, and nickel

in the summer months.

Ferrous: Sales were mixed due to higher

prices for some products and flat to lower sales

volumes.

Non-ferrous: Sales were mixed due to higher

prices for aluminum, nickel, and stainless steel,

as well as fluctuations in copper price trends.

Ferrous: Gross margins increased due to price

stabilization.

Non-ferrous: Gross margins were mixed due

to a tight spread between prime aluminum and

scrap pricing, higher margins for nickel and

stainless steel due to price increases, and

volatile copper margins.

Ferrous: Inventory levels remained consistent,

as the seasonal summer slowdown inhibited

speculative buying and stocking.

Non-ferrous: Inventory levels remained

consistent as companies managed inventory

levels relative to price fluctuations.

Ferrous: Prices were consistent, as

fluctuations in scrap pricing remained within a

range of $10 per gross ton over the past four

months, reducing the pricing pressure placed

on downstream products.

Non-ferrous: Pricing increased due to price

increases for aluminum, lead, zinc, nickel, and

stainless steel, with volatile prices for copper.

Ferrous Metal Non-Ferrous Metal

NOLVs

Sales Trends

Gross Margin

Inventory

Pricing

2 September 2014 — Metals Monitor

2 Overview

Over the summer, the demand outlook for steel brightened

slightly, although the steel market remains clouded by excess

capacity and economic uncertainty. Meanwhile, supply

pressures boosted prices for many base metals in recent months.

In the U.S., prices for flat rolled coil and rebar

slipped in June amid the seasonal summer

slowdown. Hot rolled coil prices recovered in

July, joined by cold rolled coil prices in

August, while rebar prices held firm. Plate

pricing, meanwhile, continued its steady

ascent. Steel buyers demonstrated healthy

demand despite a high level of imports.

However, shifts in the economic or political

landscape, as well as the announced addition

of steel capacity through 2020, could pose a

threat to the domestic steel market.

Base metals have experienced tightness in the

physical markets due to supply and demand

factors, lifting prices for aluminum, zinc, and

lead more than expected.

The elevation in prices may be short-lived,

however, as the volumes of metals held in

and out of official exchange warehouses

distort the physical markets. In addition,

demand remains tepid, and supplies of base

metal scrap are readily available, with the

exception of stainless steel scrap.

3 September 2014 — Metals Monitor

3 Overview

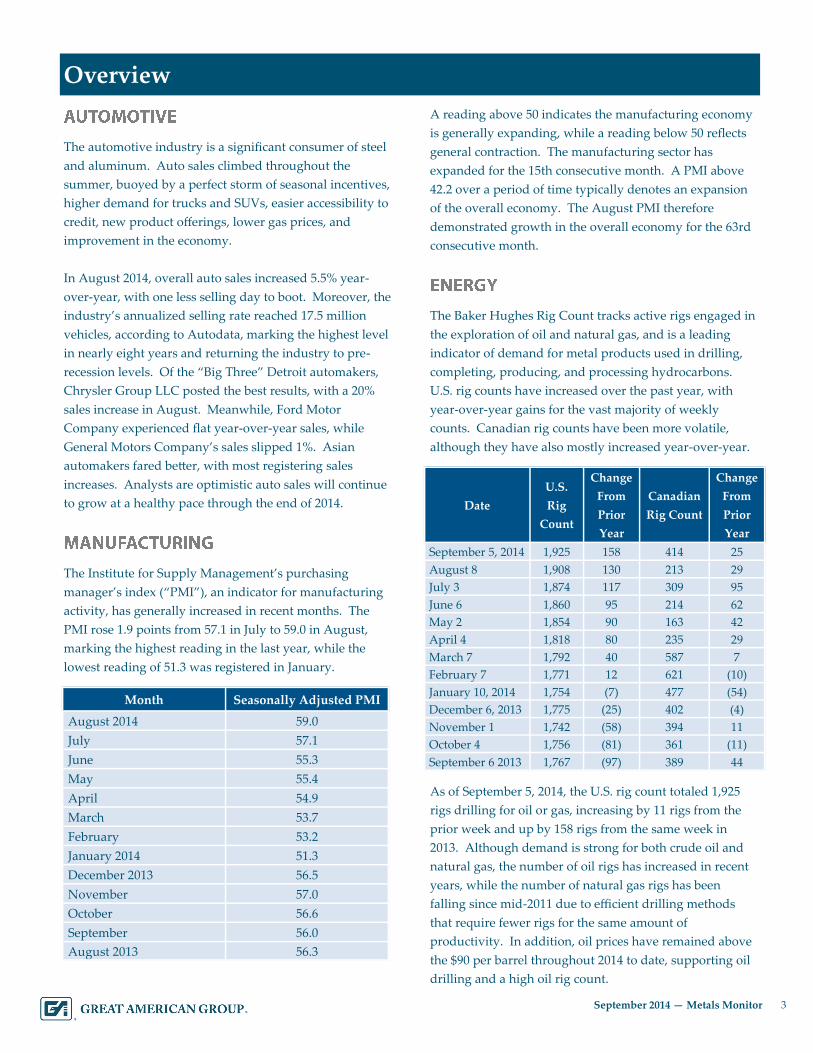

The automotive industry is a significant consumer of steel

and aluminum. Auto sales climbed throughout the

summer, buoyed by a perfect storm of seasonal incentives,

higher demand for trucks and SUVs, easier accessibility to

credit, new product offerings, lower gas prices, and

improvement in the economy.

In August 2014, overall auto sales increased 5.5% year-

over-year, with one less selling day to boot. Moreover, the

industry’s annualized selling rate reached 17.5 million

vehicles, according to Autodata, marking the highest level

in nearly eight years and returning the industry to pre-

recession levels. Of the “Big Three” Detroit automakers,

Chrysler Group LLC posted the best results, with a 20%

sales increase in August. Meanwhile, Ford Motor

Company experienced flat year-over-year sales, while

General Motors Company’s sales slipped 1%. Asian

automakers fared better, with most registering sales

increases. Analysts are optimistic auto sales will continue

to grow at a healthy pace through the end of 2014.

The Institute for Supply Management’s purchasing

manager’s index (“PMI”), an indicator for manufacturing

activity, has generally increased in recent months. The

PMI rose 1.9 points from 57.1 in July to 59.0 in August,

marking the highest reading in the last year, while the

lowest reading of 51.3 was registered in January.

A reading above 50 indicates the manufacturing economy

is generally expanding, while a reading below 50 reflects

general contraction. The manufacturing sector has

expanded for the 15th consecutive month. A PMI above

42.2 over a period of time typically denotes an expansion

of the overall economy. The August PMI therefore

demonstrated growth in the overall economy for the 63rd

consecutive month.

The Baker Hughes Rig Count tracks active rigs engaged in

the exploration of oil and natural gas, and is a leading

indicator of demand for metal products used in drilling,

completing, producing, and processing hydrocarbons.

U.S. rig counts have increased over the past year, with

year-over-year gains for the vast majority of weekly

counts. Canadian rig counts have been more volatile,

although they have also mostly increased year-over-year.

As of September 5, 2014, the U.S. rig count totaled 1,925

rigs drilling for oil or gas, increasing by 11 rigs from the

prior week and up by 158 rigs from the same week in

2013. Although demand is strong for both crude oil and

natural gas, the number of oil rigs has increased in recent

years, while the number of natural gas rigs has been

falling since mid-2011 due to efficient drilling methods

that require fewer rigs for the same amount of

productivity. In addition, oil prices have remained above

the $90 per barrel throughout 2014 to date, supporting oil

drilling and a high oil rig count.

Month Seasonally Adjusted PMI

August 2014 59.0

July 57.1

June 55.3

May 55.4

April 54.9

March 53.7

February 53.2

January 2014 51.3

December 2013 56.5

November 57.0

October 56.6

September 56.0

August 2013 56.3

Date

U.S.

Rig

Count

Change

From

Prior

Year

Canadian

Rig Count

Change

From

Prior

Year

September 5, 2014 1,925 158 414 25

August 8 1,908 130 213 29

July 3 1,874 117 309 95

June 6 1,860 95 214 62

May 2 1,854 90 163 42

April 4 1,818 80 235 29

March 7 1,792 40 587 7

February 7 1,771 12 621 (10)

January 10, 2014 1,754 (7) 477 (54)

December 6, 2013 1,775 (25) 402 (4)

November 1 1,742 (58) 394 11

October 4 1,756 (81) 361 (11)

September 6 2013 1,767 (97) 389 44

4 September 2014 — Metals Monitor

4 Recent Appraisal Trends

Appraisals valuing metals inventory typically rely on

market prices, which are affected by input costs,

supply levels, and demand from metal-consuming

industries such as the automotive, industrial, and oil

and gas drilling sectors.

Based on industry trends, NOLVs for ferrous metals

remained relatively consistent due to minimal

pricing volatility over the past six months. NOLVs

for non-ferrous metals increased, as supply-side

pressure drove up pricing for aluminum, lead, zinc,

and nickel throughout the summer months, while

other base metal prices were fairly volatile.

Sales of ferrous inventory were mixed, with no major

shift in demand for downstream products. Higher

prices this year versus last year helped stabilize

dollar sales trends, while sales volumes remained flat

to down. A number of companies expect demand

increases from the construction market in the third

quarter. Sales of non-ferrous inventory were also

mixed, as increases in aluminum, nickel, and

stainless steel pricing drove up dollar sales trends for

these metals versus last year, while copper sales

trends continue to fluctuate with pricing. However,

there were no major changes in sales volume trends.

Gross margins increased for ferrous metals as a result

of continued price stabilization, allowing mills and

distributors to rely on stable inventory costs and

maintain margins. Gross margin trends for non-

ferrous metals were mixed due to global pressures.

Continued increases in aluminum prices have

allowed companies to boost selling prices, but a tight

spread between prime aluminum and scrap pricing

has hindered gains in margin. Meanwhile, nickel

and stainless steel margins have gained steam from

price increases, while copper margins remain

volatile.

Inventory levels for ferrous metals were consistent,

as the seasonal summer slowdown inhibited

speculative buying and stocking. However, moving

into the fall season, restocking will begin to take

place in the market. Inventory levels for non-ferrous

metals also remained relatively consistent, as

companies continue to manage inventory levels

relative to pricing fluctuations.

Prices for ferrous metals were consistent, as

fluctuations in scrap pricing remained within a range

of $10 per gross ton over the past four months,

reducing the pricing pressure placed on downstream

products. Despite slight downward pricing pressure

for flat rolled coil products in certain months, the

declines were slight, as were the recent increases.

Plate and pipe/tube pricing have experienced slight

price increases over the past six months, while rebar

pricing remained largely unchanged.

Prices for non-ferrous metals increased domestically

due to tight supplies and anticipated demand

increases for aluminum, as well as tight nickel

supplies, which boosted pricing for both nickel and

stainless steel. Supply pressures also buoyed pricing

for lead and zinc in recent months. While copper

exhibited volatile prices, there had been no major

movement in the past few months.

For commodity-based appraisals, the gross recovery

rates are based on discounts from market pricing.

Specialized grades, sizes, and forms of metals with

limited distribution channels typically require

increased discounts off market price, or may be sold

at scrap market value. GA recognizes recovery

values are unique for each company based on

costing, gross margin trends, inventory mix and

levels, and other company-specific factors. In

addition, as market prices are volatile, a change in

metals market price trends would have an impact on

recovery values.

5 September 2014 — Metals Monitor

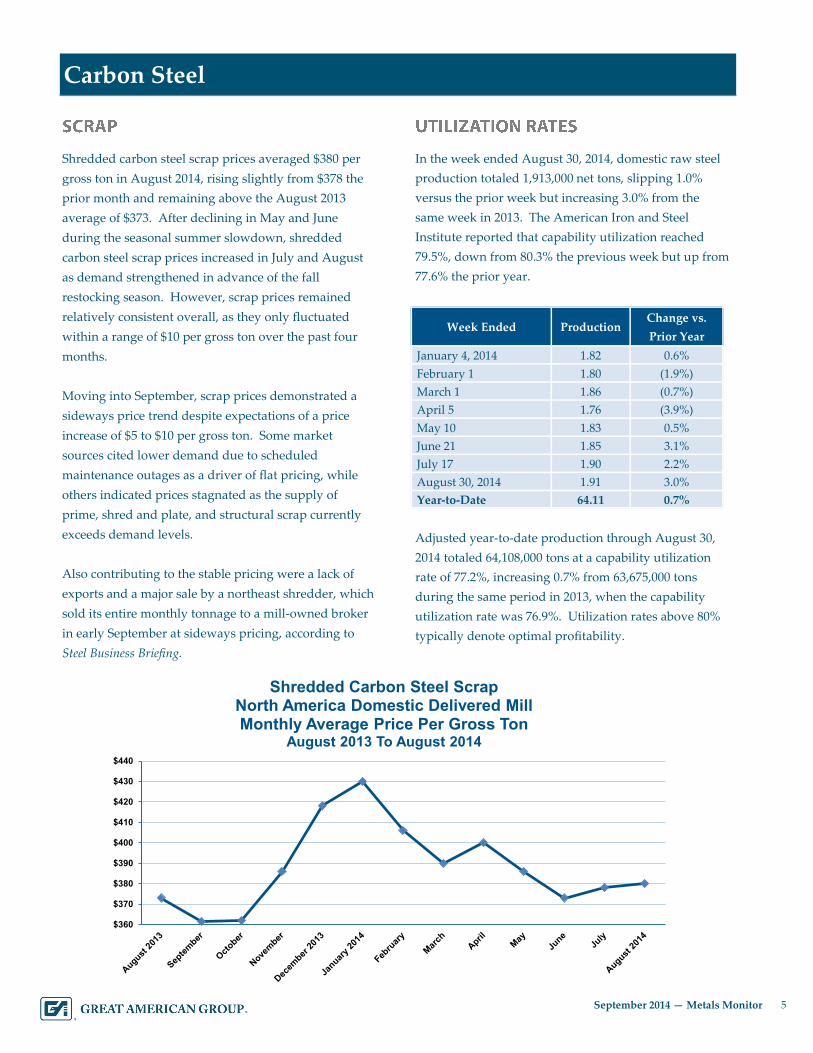

5 Carbon Steel

Shredded carbon steel scrap prices averaged $380 per

gross ton in August 2014, rising slightly from $378 the

prior month and remaining above the August 2013

average of $373. After declining in May and June

during the seasonal summer slowdown, shredded

carbon steel scrap prices increased in July and August

as demand strengthened in advance of the fall

restocking season. However, scrap prices remained

relatively consistent overall, as they only fluctuated

within a range of $10 per gross ton over the past four

months.

Moving into September, scrap prices demonstrated a

sideways price trend despite expectations of a price

increase of $5 to $10 per gross ton. Some market

sources cited lower demand due to scheduled

maintenance outages as a driver of flat pricing, while

others indicated prices stagnated as the supply of

prime, shred and plate, and structural scrap currently

exceeds demand levels.

Also contributing to the stable pricing were a lack of

exports and a major sale by a northeast shredder, which

sold its entire monthly tonnage to a mill-owned broker

in early September at sideways pricing, according to

Steel Business Briefing.

In the week ended August 30, 2014, domestic raw steel

production totaled 1,913,000 net tons, slipping 1.0%

versus the prior week but increasing 3.0% from the

same week in 2013. The American Iron and Steel

Institute reported that capability utilization reached

79.5%, down from 80.3% the previous week but up from

77.6% the prior year.

Adjusted year-to-date production through August 30,

2014 totaled 64,108,000 tons at a capability utilization

rate of 77.2%, increasing 0.7% from 63,675,000 tons

during the same period in 2013, when the capability

utilization rate was 76.9%. Utilization rates above 80%

typically denote optimal profitability.

Week Ended Production Change vs.

Prior Year

January 4, 2014 1.82 0.6%

February 1 1.80 (1.9%)

March 1 1.86 (0.7%)

April 5 1.76 (3.9%)

May 10 1.83 0.5%

June 21 1.85 3.1%

July 17 1.90 2.2%

August 30, 2014 1.91 3.0%

Year-to-Date 64.11 0.7%

$360

$370

$380

$390

$400

$410

$420

$430

$440

Shredded Carbon Steel ScrapNorth America Domestic Delivered MillMonthly Average Price Per Gross Ton

August 2013 To August 2014

6 September 2014 — Metals Monitor

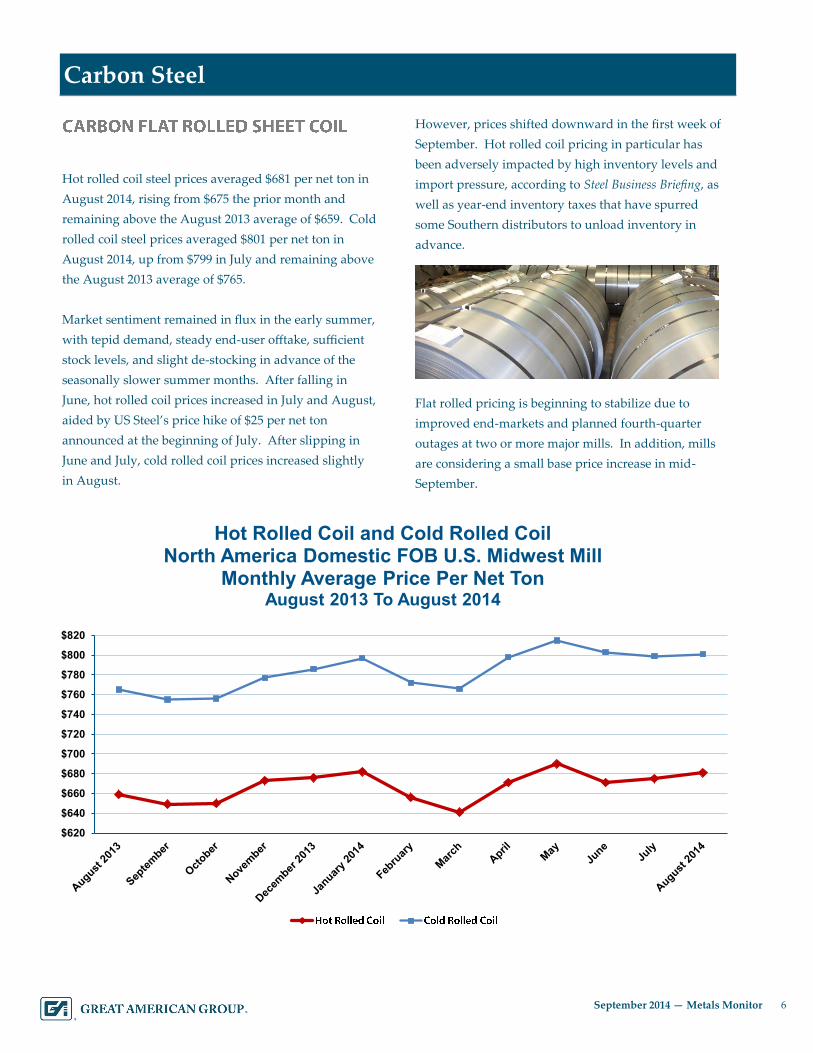

6 Carbon Steel

Hot rolled coil steel prices averaged $681 per net ton in

August 2014, rising from $675 the prior month and

remaining above the August 2013 average of $659. Cold

rolled coil steel prices averaged $801 per net ton in

August 2014, up from $799 in July and remaining above

the August 2013 average of $765.

Market sentiment remained in flux in the early summer,

with tepid demand, steady end-user offtake, sufficient

stock levels, and slight de-stocking in advance of the

seasonally slower summer months. After falling in

June, hot rolled coil prices increased in July and August,

aided by US Steel’s price hike of $25 per net ton

announced at the beginning of July. After slipping in

June and July, cold rolled coil prices increased slightly

in August.

However, prices shifted downward in the first week of

September. Hot rolled coil pricing in particular has

been adversely impacted by high inventory levels and

import pressure, according to Steel Business Briefing, as

well as year-end inventory taxes that have spurred

some Southern distributors to unload inventory in

advance.

Flat rolled pricing is beginning to stabilize due to

improved end-markets and planned fourth-quarter

outages at two or more major mills. In addition, mills

are considering a small base price increase in mid-

September.

$620

$640

$660

$680

$700

$720

$740

$760

$780

$800

$820

Hot Rolled Coil and Cold Rolled CoilNorth America Domestic FOB U.S. Midwest Mill

Monthly Average Price Per Net TonAugust 2013 To August 2014

7 September 2014 — Metals Monitor

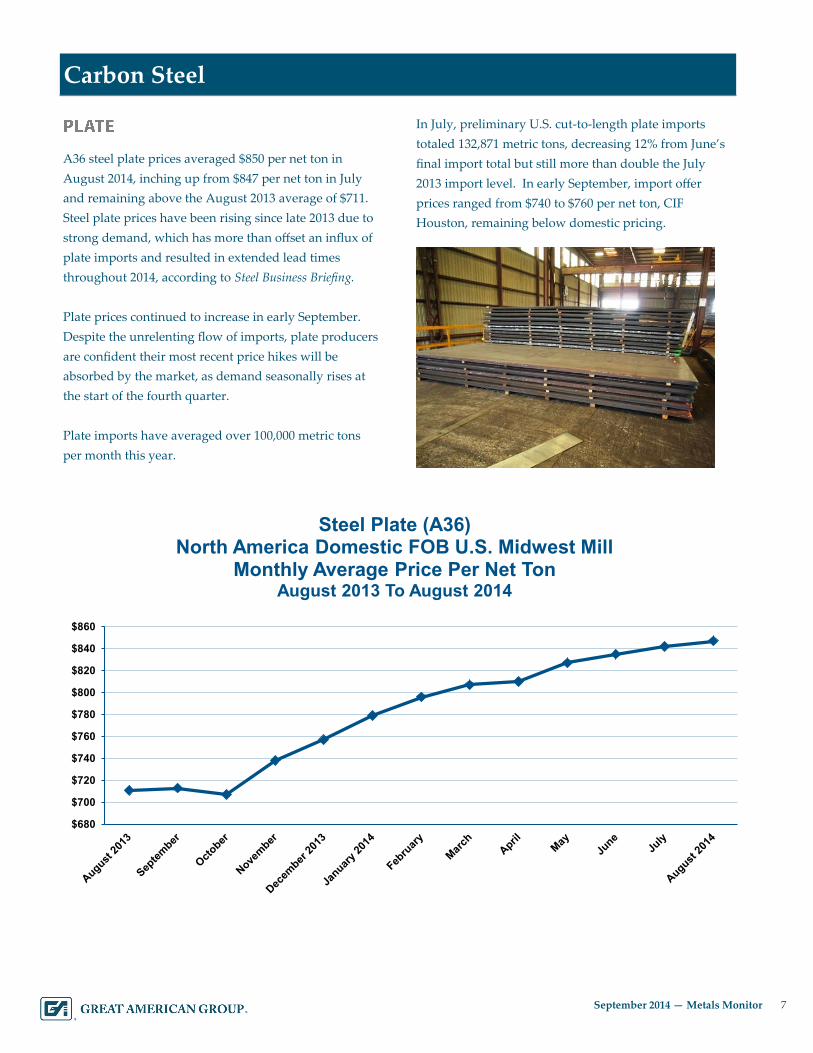

7 Carbon Steel

A36 steel plate prices averaged $850 per net ton in

August 2014, inching up from $847 per net ton in July

and remaining above the August 2013 average of $711.

Steel plate prices have been rising since late 2013 due to

strong demand, which has more than offset an influx of

plate imports and resulted in extended lead times

throughout 2014, according to Steel Business Briefing.

Plate prices continued to increase in early September.

Despite the unrelenting flow of imports, plate producers

are confident their most recent price hikes will be

absorbed by the market, as demand seasonally rises at

the start of the fourth quarter.

Plate imports have averaged over 100,000 metric tons

per month this year.

In July, preliminary U.S. cut-to-length plate imports

totaled 132,871 metric tons, decreasing 12% from June’s

final import total but still more than double the July

2013 import level. In early September, import offer

prices ranged from $740 to $760 per net ton, CIF

Houston, remaining below domestic pricing.

$680

$700

$720

$740

$760

$780

$800

$820

$840

$860

Steel Plate (A36)North America Domestic FOB U.S. Midwest Mill

Monthly Average Price Per Net TonAugust 2013 To August 2014

8 September 2014 — Metals Monitor

8 Carbon Steel

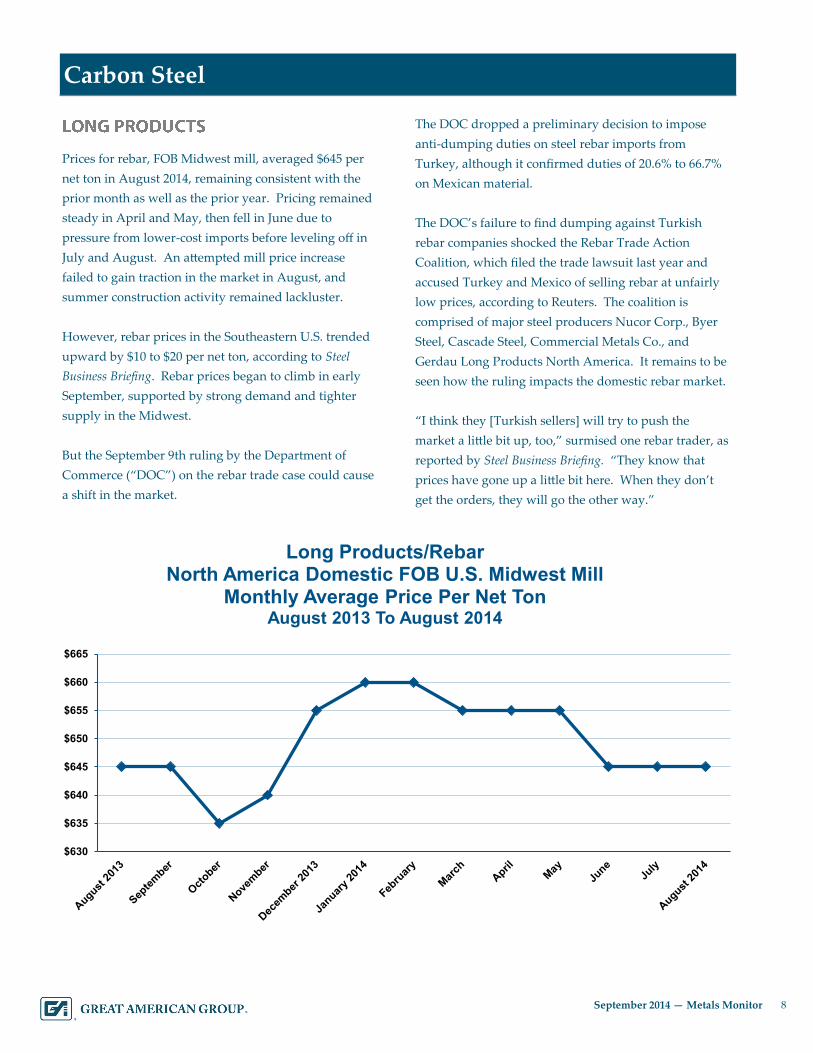

Prices for rebar, FOB Midwest mill, averaged $645 per

net ton in August 2014, remaining consistent with the

prior month as well as the prior year. Pricing remained

steady in April and May, then fell in June due to

pressure from lower-cost imports before leveling off in

July and August. An attempted mill price increase

failed to gain traction in the market in August, and

summer construction activity remained lackluster.

However, rebar prices in the Southeastern U.S. trended

upward by $10 to $20 per net ton, according to Steel

Business Briefing. Rebar prices began to climb in early

September, supported by strong demand and tighter

supply in the Midwest.

But the September 9th ruling by the Department of

Commerce (“DOC”) on the rebar trade case could cause

a shift in the market.

The DOC dropped a preliminary decision to impose

anti-dumping duties on steel rebar imports from

Turkey, although it confirmed duties of 20.6% to 66.7%

on Mexican material.

The DOC’s failure to find dumping against Turkish

rebar companies shocked the Rebar Trade Action

Coalition, which filed the trade lawsuit last year and

accused Turkey and Mexico of selling rebar at unfairly

low prices, according to Reuters. The coalition is

comprised of major steel producers Nucor Corp., Byer

Steel, Cascade Steel, Commercial Metals Co., and

Gerdau Long Products North America. It remains to be

seen how the ruling impacts the domestic rebar market.

“I think they [Turkish sellers] will try to push the

market a little bit up, too,” surmised one rebar trader, as

reported by Steel Business Briefing. “They know that

prices have gone up a little bit here. When they don’t

get the orders, they will go the other way.”

$630

$635

$640

$645

$650

$655

$660

$665

Long Products/RebarNorth America Domestic FOB U.S. Midwest Mill

Monthly Average Price Per Net TonAugust 2013 To August 2014

9 September 2014 — Metals Monitor

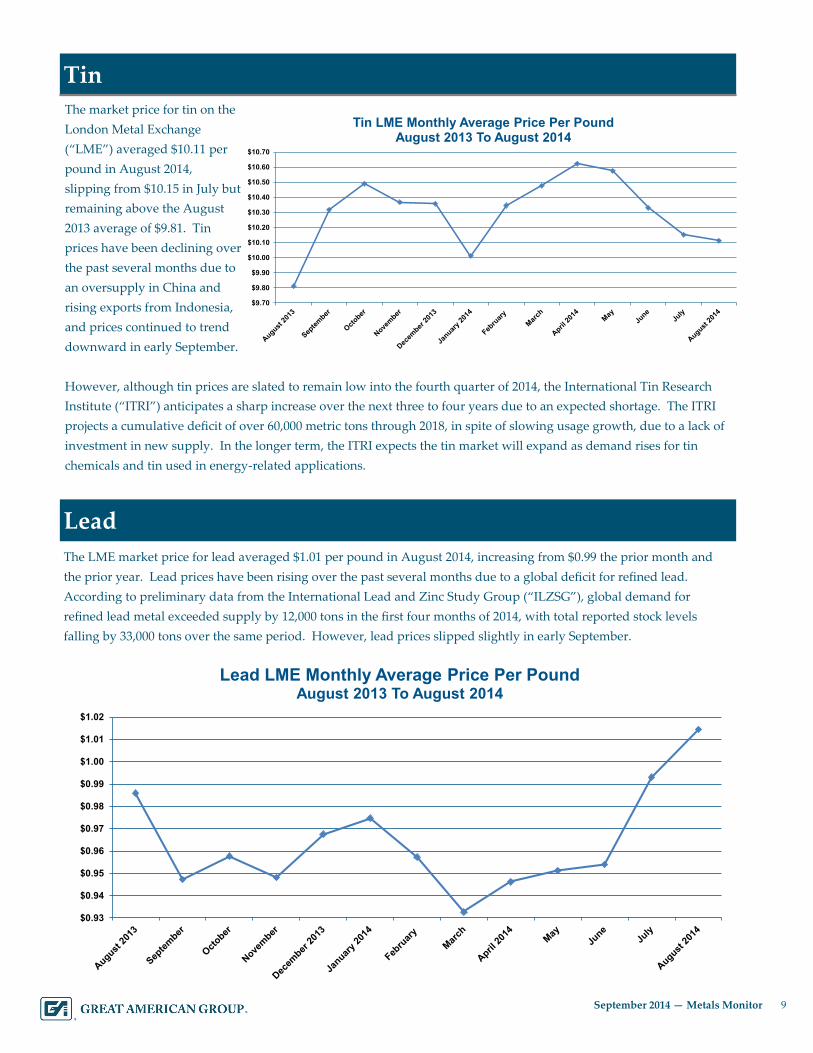

9 Tin

The market price for tin on the

London Metal Exchange

(“LME”) averaged $10.11 per

pound in August 2014,

slipping from $10.15 in July but

remaining above the August

2013 average of $9.81. Tin

prices have been declining over

the past several months due to

an oversupply in China and

rising exports from Indonesia,

and prices continued to trend

downward in early September.

However, although tin prices are slated to remain low into the fourth quarter of 2014, the International Tin Research

Institute (“ITRI”) anticipates a sharp increase over the next three to four years due to an expected shortage. The ITRI

projects a cumulative deficit of over 60,000 metric tons through 2018, in spite of slowing usage growth, due to a lack of

investment in new supply. In the longer term, the ITRI expects the tin market will expand as demand rises for tin

chemicals and tin used in energy-related applications.

The LME market price for lead averaged $1.01 per pound in August 2014, increasing from $0.99 the prior month and

the prior year. Lead prices have been rising over the past several months due to a global deficit for refined lead.

According to preliminary data from the International Lead and Zinc Study Group (“ILZSG”), global demand for

refined lead metal exceeded supply by 12,000 tons in the first four months of 2014, with total reported stock levels

falling by 33,000 tons over the same period. However, lead prices slipped slightly in early September.

Lead

$9.70

$9.80

$9.90

$10.00

$10.10

$10.20

$10.30

$10.40

$10.50

$10.60

$10.70

Tin LME Monthly Average Price Per PoundAugust 2013 To August 2014

$0.93

$0.94

$0.95

$0.96

$0.97

$0.98

$0.99

$1.00

$1.01

$1.02

Lead LME Monthly Average Price Per PoundAugust 2013 To August 2014

10 September 2014 — Metals Monitor

10 Zinc

The market price for zinc on

the LME averaged $1.06 per

pound in August 2014, rising

slightly from the prior month

and remaining above the

August 2013 average of $0.86.

Pricing continued to inch up

in early September. Zinc

prices have increased nearly

25% over the year to a three-

year high, fueled by

improvement in the industrial

sector for China, which

accounts for 44% of global consumption of refined zinc, as well as a supply deficit.

According to Goldman Sachs, zinc production is slated to fall short of demand this year for the first time since 2007,

with several major mines (equal to 7% of global production) scheduled to close next year. Any replacement mines

would be fewer in number and much smaller by comparison. In addition, the ILZSG indicated global zinc demand

climbed 7.7% in the first six months of 2014 to 6.8 million metric tons, as new demand for galvanized steel (steel coated

with zinc) has ramped up amid a rebound in the U.S. property market and rising global auto sales.

The LME market price for copper averaged $3.18 per pound in August 2014, down from $3.22 the prior month and

$3.26 the prior year. Prices continued to erode slightly in early September. Copper prices have fluctuated in recent

months as hedge funds, commodity trading advisors (CTAs), and other financial participants made strategic purchases

in the second quarter, and fund profit taking also accounted for certain price drops in the third quarter. In addition, the

slowdown in the economy of China, the world’s largest copper consumer, has had a negative impact on the market

given China’s sluggish property and service sectors.

Despite lower copper demand, premiums remain steady, and the outlook for the remainder of the year is brightening.

Glencore PLC recently forecasted

strong copper demand from both

China and the West, given

another anticipated Chinese

economic stimulus as well as

better-than-expected

manufacturing data from the

U.S., the world’s second-largest

copper consumer. U.S. copper

demand is projected to grow by

4.4% this year, according to

Morgan Stanley, marking the

fastest pace since 2010.

Copper

$0.80

$0.85

$0.90

$0.95

$1.00

$1.05

$1.10

Zinc LME Monthly Average Price Per PoundAugust 2013 To August 2014

$3.00

$3.05

$3.10

$3.15

$3.20

$3.25

$3.30

$3.35

Copper LME Monthly Average Price Per PoundAugust 2013 To August 2014

11 September 2014 — Metals Monitor

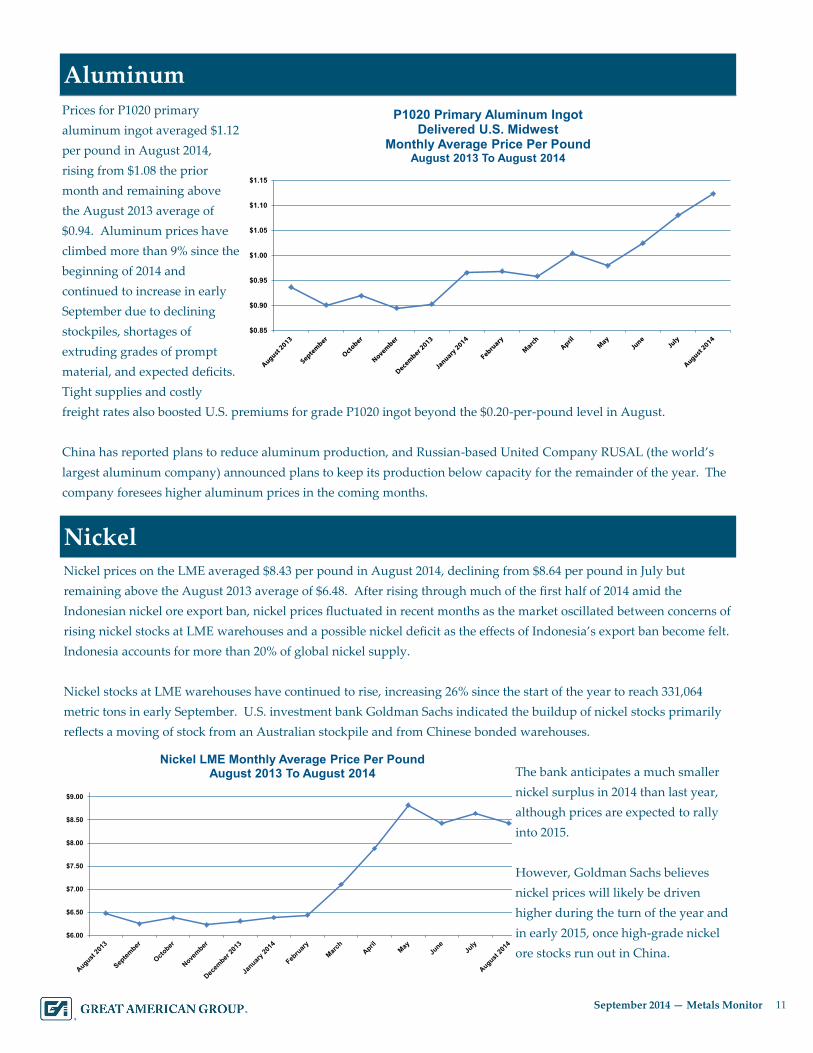

11 Aluminum

Prices for P1020 primary

aluminum ingot averaged $1.12

per pound in August 2014,

rising from $1.08 the prior

month and remaining above

the August 2013 average of

$0.94. Aluminum prices have

climbed more than 9% since the

beginning of 2014 and

continued to increase in early

September due to declining

stockpiles, shortages of

extruding grades of prompt

material, and expected deficits.

Tight supplies and costly

freight rates also boosted U.S. premiums for grade P1020 ingot beyond the $0.20-per-pound level in August.

China has reported plans to reduce aluminum production, and Russian-based United Company RUSAL (the world’s

largest aluminum company) announced plans to keep its production below capacity for the remainder of the year. The

company foresees higher aluminum prices in the coming months.

Nickel prices on the LME averaged $8.43 per pound in August 2014, declining from $8.64 per pound in July but

remaining above the August 2013 average of $6.48. After rising through much of the first half of 2014 amid the

Indonesian nickel ore export ban, nickel prices fluctuated in recent months as the market oscillated between concerns of

rising nickel stocks at LME warehouses and a possible nickel deficit as the effects of Indonesia’s export ban become felt.

Indonesia accounts for more than 20% of global nickel supply.

Nickel stocks at LME warehouses have continued to rise, increasing 26% since the start of the year to reach 331,064

metric tons in early September. U.S. investment bank Goldman Sachs indicated the buildup of nickel stocks primarily

reflects a moving of stock from an Australian stockpile and from Chinese bonded warehouses.

The bank anticipates a much smaller

nickel surplus in 2014 than last year,

although prices are expected to rally

into 2015.

However, Goldman Sachs believes

nickel prices will likely be driven

higher during the turn of the year and

in early 2015, once high-grade nickel

ore stocks run out in China.

Nickel

$0.85

$0.90

$0.95

$1.00

$1.05

$1.10

$1.15

P1020 Primary Aluminum IngotDelivered U.S. Midwest

Monthly Average Price Per PoundAugust 2013 To August 2014

$6.00

$6.50

$7.00

$7.50

$8.00

$8.50

$9.00

Nickel LME Monthly Average Price Per PoundAugust 2013 To August 2014

12 September 2014 — Metals Monitor

12 Stainless Steel

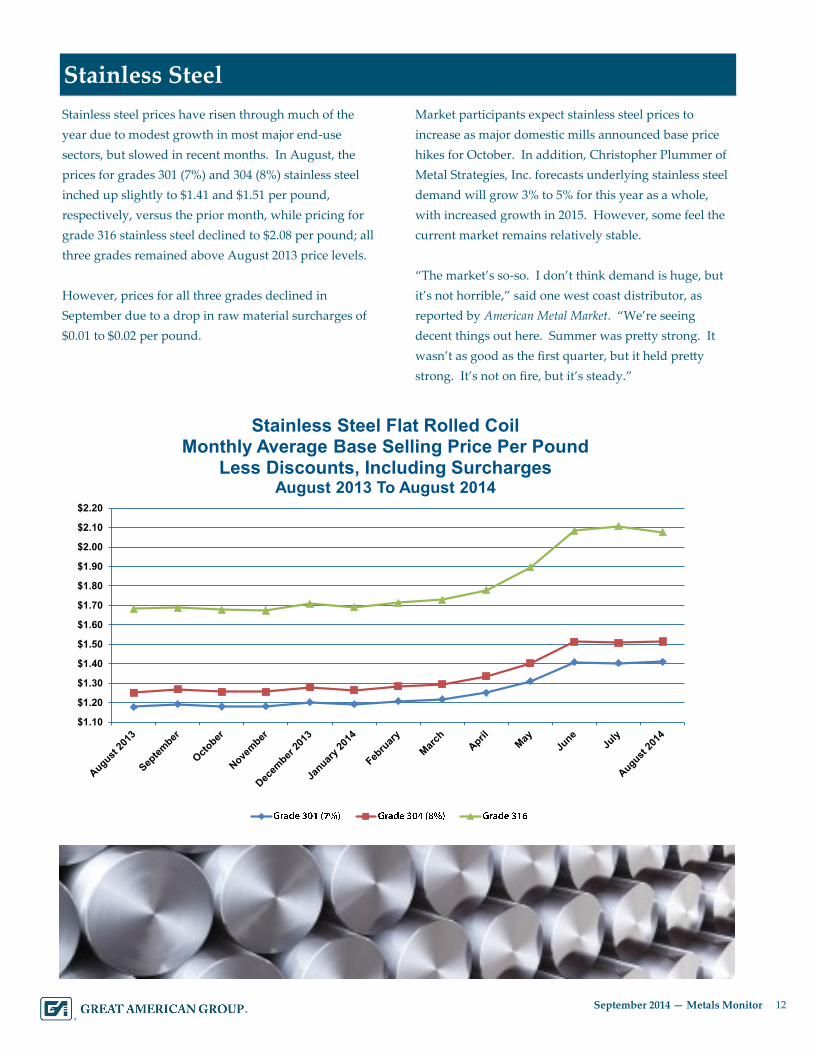

Stainless steel prices have risen through much of the

year due to modest growth in most major end-use

sectors, but slowed in recent months. In August, the

prices for grades 301 (7%) and 304 (8%) stainless steel

inched up slightly to $1.41 and $1.51 per pound,

respectively, versus the prior month, while pricing for

grade 316 stainless steel declined to $2.08 per pound; all

three grades remained above August 2013 price levels.

However, prices for all three grades declined in

September due to a drop in raw material surcharges of

$0.01 to $0.02 per pound.

Market participants expect stainless steel prices to

increase as major domestic mills announced base price

hikes for October. In addition, Christopher Plummer of

Metal Strategies, Inc. forecasts underlying stainless steel

demand will grow 3% to 5% for this year as a whole,

with increased growth in 2015. However, some feel the

current market remains relatively stable.

“The market’s so-so. I don’t think demand is huge, but

it’s not horrible,” said one west coast distributor, as

reported by American Metal Market. “We’re seeing

decent things out here. Summer was pretty strong. It

wasn’t as good as the first quarter, but it held pretty

strong. It’s not on fire, but it’s steady.”

$1.10

$1.20

$1.30

$1.40

$1.50

$1.60

$1.70

$1.80

$1.90

$2.00

$2.10

$2.20

Stainless Steel Flat Rolled CoilMonthly Average Base Selling Price Per Pound

Less Discounts, Including SurchargesAugust 2013 To August 2014

13 September 2014 — Metals Monitor

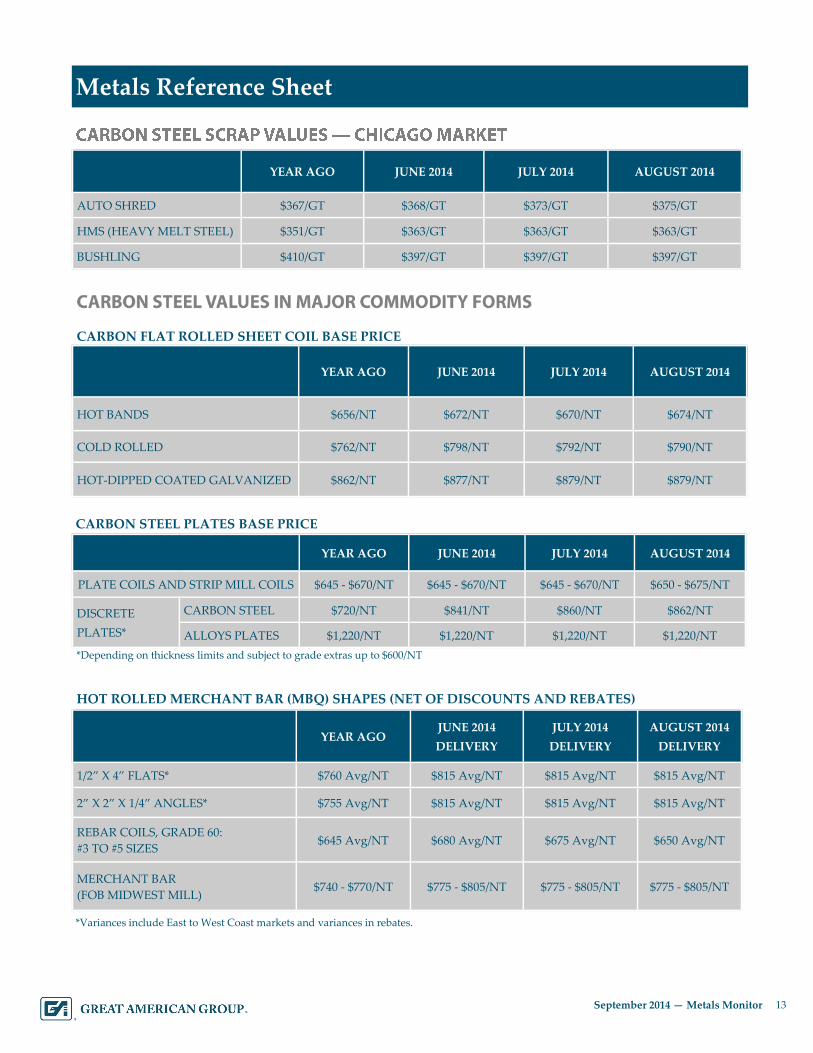

13 Metals Reference Sheet

YEAR AGO JUNE 2014 JULY 2014 AUGUST 2014

AUTO SHRED $367/GT $368/GT $373/GT $375/GT

HMS (HEAVY MELT STEEL) $351/GT $363/GT $363/GT $363/GT

BUSHLING $410/GT $397/GT $397/GT $397/GT

CARBON FLAT ROLLED SHEET COIL BASE PRICE

YEAR AGO JULY 2014 AUGUST 2014 JUNE 2014

HOT BANDS $656/NT $670/NT $674/NT $672/NT

COLD ROLLED $762/NT $792/NT $790/NT $798/NT

HOT-DIPPED COATED GALVANIZED $862/NT $879/NT $879/NT $877/NT

CARBON STEEL PLATES BASE PRICE

YEAR AGO JUNE 2014 JULY 2014 AUGUST 2014

PLATE COILS AND STRIP MILL COILS $645 - $670/NT $645 - $670/NT $645 - $670/NT $650 - $675/NT

DISCRETE

PLATES*

CARBON STEEL $720/NT $841/NT $860/NT $862/NT

ALLOYS PLATES $1,220/NT $1,220/NT $1,220/NT $1,220/NT

HOT ROLLED MERCHANT BAR (MBQ) SHAPES (NET OF DISCOUNTS AND REBATES)

YEAR AGO AUGUST 2014

DELIVERY

JUNE 2014

DELIVERY

JULY 2014

DELIVERY

1/2” X 4” FLATS* $760 Avg/NT $815 Avg/NT $815 Avg/NT $815 Avg/NT

2” X 2” X 1/4” ANGLES* $755 Avg/NT $815 Avg/NT $815 Avg/NT $815 Avg/NT

REBAR COILS, GRADE 60:

#3 TO #5 SIZES $645 Avg/NT $650 Avg/NT $680 Avg/NT $675 Avg/NT

MERCHANT BAR

(FOB MIDWEST MILL) $740 - $770/NT $775 - $805/NT $775 - $805/NT $775 - $805/NT

*Variances include East to West Coast markets and variances in rebates.

*Depending on thickness limits and subject to grade extras up to $600/NT

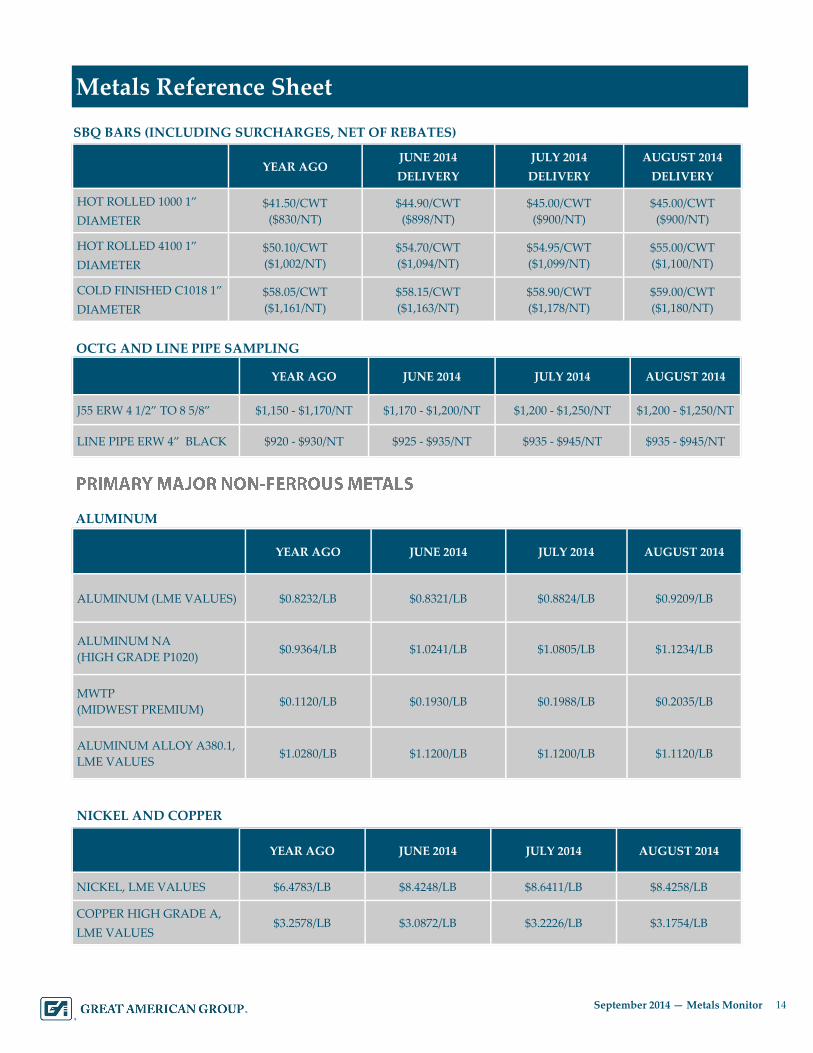

14 September 2014 — Metals Monitor

14 Metals Reference Sheet

YEAR AGO JUNE 2014 JULY 2014 AUGUST 2014

ALUMINUM (LME VALUES) $0.8232/LB $0.8321/LB $0.8824/LB $0.9209/LB

ALUMINUM NA

(HIGH GRADE P1020) $0.9364/LB $1.0241/LB $1.0805/LB $1.1234/LB

MWTP

(MIDWEST PREMIUM) $0.1120/LB $0.1930/LB $0.1988/LB $0.2035/LB

ALUMINUM ALLOY A380.1,

LME VALUES $1.0280/LB $1.1200/LB $1.1200/LB $1.1120/LB

ALUMINUM

YEAR AGO JUNE 2014 JULY 2014 AUGUST 2014

NICKEL, LME VALUES $6.4783/LB $8.4248/LB $8.6411/LB $8.4258/LB

COPPER HIGH GRADE A,

LME VALUES $3.2578/LB $3.0872/LB $3.2226/LB $3.1754/LB

NICKEL AND COPPER

YEAR AGO JULY 2014 JUNE 2014 AUGUST 2014

J55 ERW 4 1/2” TO 8 5/8” $1,150 - $1,170/NT $1,200 - $1,250/NT $1,170 - $1,200/NT $1,200 - $1,250/NT

LINE PIPE ERW 4” BLACK $920 - $930/NT $935 - $945/NT $925 - $935/NT $935 - $945/NT

YEAR AGO JUNE 2014

DELIVERY

JULY 2014

DELIVERY

AUGUST 2014

DELIVERY

HOT ROLLED 1000 1”

DIAMETER

$41.50/CWT

($830/NT)

$44.90/CWT

($898/NT)

$45.00/CWT

($900/NT)

$45.00/CWT

($900/NT)

HOT ROLLED 4100 1”

DIAMETER

$50.10/CWT

($1,002/NT)

$54.70/CWT

($1,094/NT)

$54.95/CWT

($1,099/NT)

$55.00/CWT

($1,100/NT)

COLD FINISHED C1018 1”

DIAMETER

$58.05/CWT

($1,161/NT)

$58.15/CWT

($1,163/NT)

$58.90/CWT

($1,178/NT)

$59.00/CWT

($1,180/NT)

OCTG AND LINE PIPE SAMPLING

SBQ BARS (INCLUDING SURCHARGES, NET OF REBATES)

15 September 2014 — Metals Monitor

15 Metals Reference Sheet

(Product prices using current average distributor discount)

“0.044” X 48/60’ WIDE

X COIL YEAR AGO

JUNE 2014

DELIVERY

JULY 2014

DELIVERY

AUGUST 2014

DELIVERY

T304* $1.2514/LB $1.5126/LB $1.5073/LB $1.5138/LB

T316/316L* $1.6819/LB $2.0835/LB $2.1066/LB $2.0768/LB

*The above changes in product prices are driven by changes in monthly elemental metallic surcharges. These are most heavily impacted by

changes in nickel values but result from the combined impact of nickel, chrome, molybdenum, titanium, ferrous scraps, and energy (natural

gas). Surcharges are established from the monthly averages of the elements two months prior to the affected month.

YEAR AGO JUNE 2014 AUGUST 2014 JULY 2014

T304/304L $0.6354/LB $0.8966/LB $0.8978/LB $0.8913/LB

T316/316L $0.8839/LB $1.2855/LB $1.2788/LB $1.3086/LB

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

550,000

600,000

LME Copper Warehouse StocksMonthly Average Metric Tons

August 2013 Through August 2014

4,800,000

4,900,000

5,000,000

5,100,000

5,200,000

5,300,000

5,400,000

5,500,000

LME Aluminum Warehouse StocksMonthly Average Metric Tons

August 2013 Through August 2014

16 September 2014 — Metals Monitor

16 Experience

GA has worked with and appraised a number of companies within the metals industry, including industry leaders in

steel and aluminum production and processing. GA’s extensive record of metals inventory valuations also features

appraisals for companies throughout the entire metal supply chain, including foreign and domestic metal- and steel-

producing mills; metal converters that produce tubing and pipe, as well as expanded, grating, and perforated metal

types; metal service centers/processors as well as distributors; structural and custom fabricators and stampers;

manufacturers that utilize metals as raw materials; and scrap yards, recyclers, dealers, and brokers.

Over the past six months, GA performed appraisals of

companies with annual revenues ranging from $18.7

million to $2.8 billion, including the following sampling:

A supplier of metal inputs to ferrous foundries;

A manufacturer of high-quality light gauge common

alloy sheet, foil, and coated aluminum products;

An importer and master distributor of industrial

stainless steel and nickel alloy products;

A major UK producer of long steel products;

A producer of calcined petroleum coke;

A distributor of mill-length and processed steel;

A producer of carbon and alloy steel castings;

A producer of welded and seamless OCTG;

A steel distributor and service center;

A producer of lightweight aluminum die castings;

A manufacturer of mechanical steel tubing, chrome-

plated bars, tubular parts, and precision components;

A steel service center focused on flat rolled slit coil;

A master distributor of stainless steel products; and

A processor and recycler of scrap metals.

GA’s extensive appraisal experience also includes

valuations of the following major businesses in the

metals industry:

Globally recognized vertically integrated steel tube

manufacturers;

A vertically integrated aluminum producer including

both the upstream and downstream sides of the

industry, with over $1 billion in sales annually and

over $130 million in inventory;

One of the U.S.’s largest scrap recycling processors,

with nearly $550 million in sales annually; and

Well-known service centers across the nation, including

a multi-division full line steel service center consisting

of over 50 locations across the U.S., with $2.6 billion in

annual sales and over $500 million in inventory.

Moreover, GA has liquidated a number of companies with metal products, including Advanced Composites,

Aluminum Skylight & Specialty Corporation, Anello Corporation, Apex Pattern, Balox Fabricators, BJS Industries,

Buckner Foundry, Crown City Plating, GE Roto Flow, Laird Technology, Maddox Metal Works, Miller Pacific

Steel, R.D. Black Sheet Metal, Valley Brass Foundry, and Southline Steel.

GA has also been involved in liquidations of metalworking equipment for companies such as Adams Campbell

Company, CAMtech Precision Manufacturing, Inc., Gregg Industries, Inc., International Piping Systems, Heat

Transfer Products, PMC Machining and Manufacturing, Sherrill Manufacturing, Trans-Matic Manufacturing,

Veristeel, Inc., and Weiland Steel, Inc.

In addition to our vast appraisal and liquidation experience, GA maintains a staff of experienced metals experts

with personal contacts within the metals industry that we utilize for insight and perspective on recovery values.

GA additionally maintains appraisal experience involving precious metals and specialty metals, allowing GA to

provide experience-based valuations across the entire metals industry. The metal products that GA has appraised

have maintained applications throughout a wide variety of industries, including the automotive, construction,

aerospace, industrial machinery and equipment, and appliance and electrical equipment markets.

17 September 2014 — Metals Monitor

17 Monitor Information

The Metals Monitor provides market value trends in both

ferrous and non-ferrous metals. The commodity nature of

steel scrap, aluminum ingot, copper cathode, and nickel often

results in volatile market values. Our semi-annual Metals

Monitor reflects pricing and market trends over the prior six

months, as well as forward-looking projections, in order to

reflect significant developments in the metals markets.

The Metals Monitor includes a sampling covering most metals projects. GA’s metals expertise

is not confined to use on pure metals projects, but is always utilized in assuring the accuracy

and insight for all manufacturing projects where metals are the primary or significant raw

materials, regardless of the sector of the finished products. This assures that all appraisals

from GA reflect the full scope of our experience and insight. GA internally tracks additional

specialty and tool steels, all raw materials for steel, specialty steel, and primary aluminum

production and manufacturing, but we are mindful to adhere to your request for a simple

reference document. Should you need any further information or wish to discuss recovery

ranges for a particular segment, please feel free to contact your GA Business Development

Officer.

GA’s Metals Monitor provides market value and industry trend information for a variety of

metals products. The information contained herein is based on a composite of GA’s industry

expertise, contact with industry personnel, industry publications, liquidation and appraisal

experience, and data compiled from a variety of well-respected sources believed to be reliable.

We do not guarantee the completeness of such information or make any representation as to

its accuracy.

18 September 2014 — Metals Monitor

18 Appraisal & Valuation Team

About Great American Group

Great American Group is a leading provider of asset disposition solutions and valuation and appraisal services to

a wide range of retail, wholesale, and industrial clients, as well as lenders, capital providers, private equity

investors, and professional services firms. In addition to the Metals Monitor, GA also provides clients with industry

expertise in the form of monitors for the chemicals and plastics, food, and building products sectors, among many

others. GA also offers various industry monitors via its subsidiary, GA Europe Valuations Limited.

Headquarters

21860 Burbank Blvd. Suite 300 South

Woodland Hills, CA 91367 800-45-GREAT www.greatamerican.com

Mike Marchlik

National Sales & Marketing Director

(818) 746-9306

David Seiden

Executive Vice President, Southeast Region

(770) 551-8114

Ryan Mulcunry

Executive Vice President - Northeast Region, Canada & Europe

(617) 692-8310

Bill Soncini

Senior Vice President, Midwest Region

(312) 777-7945

Drew Jakubek

Managing Director, Southwest Region

(972) 265-7981

Jennie Kim

Vice President, Western Region

(818) 746-9370

Ken Bloore

Chief Operating Officer

(818) 884-3737

Michael Petruski

Executive Vice President, General Manager

(818) 884-3737

Greg Trilevsky

Senior Appraiser—Metals and Manufacturing

(909) 559-8135

Alex Tereszcuk

Senior Appraiser—Metals and Manufacturing

(336) 854-7859

Dan Tracy

Senior Appraiser—Metals and Manufacturing

(412) 953-6357

John Little

Senior Appraiser—Scrap Recycling

(864) 630-4799

Ryan Lutz

Senior Project Manager—Metals Specialist

(781) 429-4052 Daniel Williams

Managing Director, New York Region

(646) 381-9221

![New Approach of Metals Ductility in Tensile Test...Aluminium 2024 –T4 3.1 303 476 20 35 Table 1: Mechanical properties of some metals [57]. Metals A Z Ductile Iron A536 (65-45-12)](https://img.pdfslide.us/doc/110x75/609990b023f002571748a778/new-approach-of-metals-ductility-in-tensile-test-aluminium-2024-at4-31-303.jpg)