Embed Size (px)

Citation preview

MANAGEMENT’S REPORT – LIGHT S.A.- 2016

Message from Management

The first year of the new management has significantly changed Light’s business strategy,

already reflected in the positive results of 2016.

Based on a new diagnosis of the causes and areas of energy losses, we intensified combat

initiatives in regions inhabited by middle-income to high-income customers. These regions represent

90% of the load of the Distribution Company and 51% of the volume of energy stolen. As a result, the

volume of recovered energy increased significantly and total losses accounted for 22.54% of the grid

load in the twelve months ended December 31, 2016.

The success of the Company in the execution of this program is even more remarkable when we

take into account Brazil’s current adverse social and economic scenario, particularly in the State of Rio

de Janeiro, where the 31 cities of its concession area are included. We were able not only to decrease

losses, but also to prevent such losses from deteriorating the collection rate, which increased compared

to 2015.

The energy theft combat program is associated with the search for efficiency through an

improvement in the quality of services rendered and a better management of funds used by the

Distribution Company. Throughout the year, approximately R$170 million were invested in the

implementation of measures to improve the quality of services, resulting in a decrease in the electricity

duration of interruption (DEC) indicator to 11.70 hours.

In addition, 2017 begun with great news for the Light Group. Upon the execution of the 5th

amendment to the concession agreement, Light became the first company to voluntarily accede to the

new clauses of quality and economic and financial sustainability, which will translate into better services

rendered to consumers. This new amendment also allows the anticipation of the tariff review process of

the Distribution Company, ensuring the restoration of its economic and financial equilibrium.

The restoration of the economic and financial equilibrium of the Distribution Company

combined with prospects of improvement in Brazil’s economic scenario, with a drop in the base interest

rate, will result in a favorable scenario that will allow the Light Group to decrease indebtedness expenses

and strengthen its cash flow.

It is also fundamental for the Company to optimize its investment program, focusing on its core

business, i.e., distribution of electricity, and reviewing its portfolio of assets based on potential returns

and short-term cash and cash equivalents.

Finally, we reinforce our commitment to the search for efficiency in the management and

implementation of best practices in all different areas of Light. Our operation will focus on sustainable

results, privileging the skills and ethics of our employees and our transparency in our relationships with

shareholders, business partners, customers, and other stakeholders.

Company’s Profile

Light operates in 31 cities of the State of Rio de Janeiro, encompassing a region with

approximately 11 million people, ending 2016 with more than four million customers. Headquartered in

the city of Rio de Janeiro, the Light Group consists of the following companies: Light S.A. (holding

company); Light Serviços de Eletricidade S.A. (Light SESA) (power distribution company); Light

Energia S.A. (Light Energia) (power generation company), Lightger S.A. (Lightger) (the company in

charge of the Paracambi SHPP project); Itaocara Energia Ltda. (Itaocara); Amazônia Energia

Participações S.A. (Amazônia) (a company holding interest in the Belo Monte HPP project); Light Esco

MANAGEMENT’S REPORT – LIGHT S.A.- 2016

Prestação de Serviços S.A. (Light Esco) and Lightcom Comercializadora de Energia S.A. (Lightcom)

(both operating in the commercialization segment); Light Soluções em Eletricidade Ltda. (Light

Soluções); Energia Olímpica S.A. (Olímpica); Axxiom Soluções Tecnológicas S.A. (Axxiom) (service

provider); and Instituto Light (institute).

Operating Scenario

Operating Performance

Tariffs

The tariffs charged by Light S.E.S.A. are set forth pursuant to the Concession Agreement and

the regulations and decisions of the Brazilian Electricity Agency (Agência Nacional de Energia Elétrica)

(ANEEL), which has discretion over the exercise of its regulatory activities. The concession agreements

of distribution companies and Brazilian law set forth a tariff cap mechanism allowing three types of

tariff adjustment: (1) the annual tariff adjustment; (2) tariff reviews every five years; and (3) the

extraordinary tariff review. The Annual Tariff Adjustment took place on November 7, 2016. As of 2017,

upon the execution of the 5th amendment to the concession agreement, the date of the annual tariff

adjustment will be changed to March 15.

Annual Tariff Adjustment

On November 1, 2016, ANEEL approved the tariff adjustment rate for Light Serviços de

Eletricidade S.A., consisting of two items: the structural item (which is now included in the tariff),

adjusted by -1.24%; and the financial item (exclusively applied to the 12 months following the date of

the tariff adjustment), adjusted by -4.23%.

The annual tariff adjustment process consists of the transfer to consumers of non-manageable

concession costs (Parcel A items – purchase of energy, industry charges, and transmission charges) and

the adjustment for inflation of manageable costs (Parcel B items – distribution) based on the General

Market Price (IGP-M) index, less Factor X, which passes on to consumers the concessionaire’s annual

productivity gains.

The Parcel A items adjustment was -3,84%, primarily due to: (i) a decrease in the Energy

Development Account (CDE) by 16%; and (ii) the variation in costs with purchase of electricity by -

6.31%, especially due to the depreciation of the Real against the U.S. dollar, which affected the energy

tariff from Itaipu. The average transfer price under energy purchase agreements (Pmix) was set at

R$173.78/MWh.

The Parcel B items adjustment (which is effectively kept by Light to cover costs and remunerate

investments) reflects the accumulated variation of the IGP-M index from November 2015 to October

2016 (8.78%), less Factor X (1.22%), resulting in a final rate of 7.56%.

The average impact on consumers was a 12.25% decrease, where Parcel A items accounted for

a 13.98% decrease and Parcel B items accounted for a 1.72% increase. The new tariffs became effective

as of November 7, 2016.

Amendment to the Concession Agreement and Fourth Tariff Review

In February 2016, Light SESA filed with ANEEL a formal request to begin the Extraordinary

Tariff Review Process. In August 2016, pursuant to Order (Despacho) No. 2.194, ANEEL determined

MANAGEMENT’S REPORT – LIGHT S.A.- 2016

that distribution companies that were not initially covered by Law No. 12.783 could also accede to the

terms of the new concession agreement and change the date of the Tariff Review. Accordingly, in

October 2016, Light requested from ANEEL the execution of an amendment to the concession

agreement and the anticipation of the Tariff Review from November 2018 to November 2016. As a

result, in December 2016, ANEEL called Public Hearing (Audiência Pública) No. 89 to obtain further

information for the execution of an amendment to the concession agreement and the anticipation of the

Tariff Review of Light to March 2017. On March 15, 2017, the 4th Periodic Tariff Review process was

completed, ratifying an average tariff adjustment of 10.45%.

The execution of an amendment to the concession agreement and the anticipation of the 4th Tariff

Review are of public interest as it benefits:

Light, which will restore the equilibrium of its concession agreement pursuant to Brazilian Law

and the agreements in effect;

consumers, who will rely on a greater commitment of the Company’s shareholders and

management to the sustainability of the concession, in economic and financial terms and also

regarding the quality of services rendered;

the electricity sector because once the financial equilibrium of Light is restored, Light will be

able to meet its intra-sector obligations (charges, purchase and transmission of energy) without

delays; and

the economy of Rio de Janeiro and Brazil because once the financial equilibrium of Light is

restored, Light will be able to make more investments and offer more jobs.

In addition, the Company will also be required to meet new obligations under the new

amendment to the concession agreement, including:

Efficiency in terms of quality – an objective metric to improve the Duration of Interruption

(DEC) and Frequency of Interruption (FEC) indicators in the first five years:

DECi (hours) FECi (interruptions)

2018 2019 2020 2021 2022 2018 2019 2020 2021 2022

9.80 8.23 8.14 8.02 7.84 6.01 5.72 5.43 5.15 4.86

Efficiency in terms of economic parameters – an objective trajectory during the first years

according to which the Distribution Company, by complying with the indicators1 set forth by the

concession agreement, will reach economic and financial sustainability:

2018: {Net Debt / [EBITDA2 (-) QRR23]} ≤ 1 / (0,8 * SELIC4]) 2019 em diante: {Net Debt / [EBITDA (-) QRR]} ≤ 1 / (1,11 * SELIC)

1 Limits less restrictive than the company's current financial covenants 2 Calculated according to ANEEL methodology 3 Reflects Regulatory Depreciation 4 Long-term interest rate

MANAGEMENT’S REPORT – LIGHT S.A.- 2016

Corporate governance and transparency – the Distribution Company undertakes to maintain its

governance and transparency levels in line with best practices and in accordance with its status

of utility services provider.

Commitment of controlling shareholders – the controlling shareholders execute the concession

agreement as intervening parties and guarantors of the obligations and charges set forth

thereunder.

It is also worth mentioning that, upon the execution of the amendment to the concession

agreement, Light SESA’s usual tariff processes will take place every March 15, and the next Periodic

Tariff Review (“PTR”) is scheduled for March 15, 2022. The expiration date of Light SESA’s

concession agreement remains unchanged, i.e., June 4, 2026.

As a result of the 4th PTR, the items associated with energy distribution services included in the

tariffs of Light SESA (allocated to cover efficient operating costs, remuneration and depreciation of

investments, annual payments of non-electrical assets, and irrecoverable revenues, deducted from other

revenues), as ratified by ANEEL, total R$2,911 million.

These same items, included in Parcel B items that were passed on to the last Tariff Adjustment

of Light SESA, on November 7, 2016, totaled R$2,535 million on that date.

As to transfer of energy losses, the percentage of non-technical losses now accounts for 36.06%

of the low voltage market and the percentage of technical losses accounts for 6.34% of the regulatory

Grid Load. Both percentages will remain the same until the next PTR, scheduled to March 2022,

irrespective of the actual level of losses of the concessionaire during the period.

In addition to the recalculation of items associated with energy distribution services and the

redefinition of percentages for regulatory losses, Light SESA’s new tariffs also reflect an adjustment to

Parcel A items (associated with the purchase of energy, industry charges, and transmission costs) and to

financial items.

Average Effect for Consumer

-2.86%

4,26%

1.43%

2,81%

4,81% 10,45 %

Sector Charges

Transmission Costs

Energy Acquisition

Costs

Distribuition & Irrecoverable

Revenues

Financial Components Total

MANAGEMENT’S REPORT – LIGHT S.A.- 2016

Market Evolution

In 2016, Billed Energy decreased by 2.3% compared to 2015, primarily due to milder

temperatures and an unfavorable economic scenario. However, it is important to highlight the energy

recovered in all segments, i.e., 683 GWh in 2016 compared to 256 GWh in 2015, reflecting the

Company’s new strategy to combat energy losses.

The residential segment recorded a 0.8% increase in Billed Energy compared to the previous

year, irrespective of the drop in average temperature, due to increased efforts of the Company to combat

energy losses, resulting in significant billing of the energy recovered from the low voltage market. Of

the 683 GWh recovered in 2016, 600 GWh accounted for the recovery of energy from the residential

segment alone. Excluding the recovery of energy, the residential segment would have recorded a drop

of 6.0% compared to 2015.

The commercial segment recorded a 2.2% decrease compared to 2015, totaling 8,271 GWh at

the end of 2016. This drop is due to the migration of high voltage customers to the free market and the

4.4% decrease in the most significant commercial segment, i.e., the retail segment, reflecting the

economic downturn in terms of energy consumption.

The energy consumption of the industrial segment in Light’s concession area decreased by 6.7%,

in line with the drop recorded by other concessionaires of the southeast region. In 2016, total energy

consumption amounted to 4,901 GWh, representing a decrease of 350 GWh compared to 2015. In 2016,

22 industrial customers migrated to the free market.

MANAGEMENT’S REPORT – LIGHT S.A.- 2016

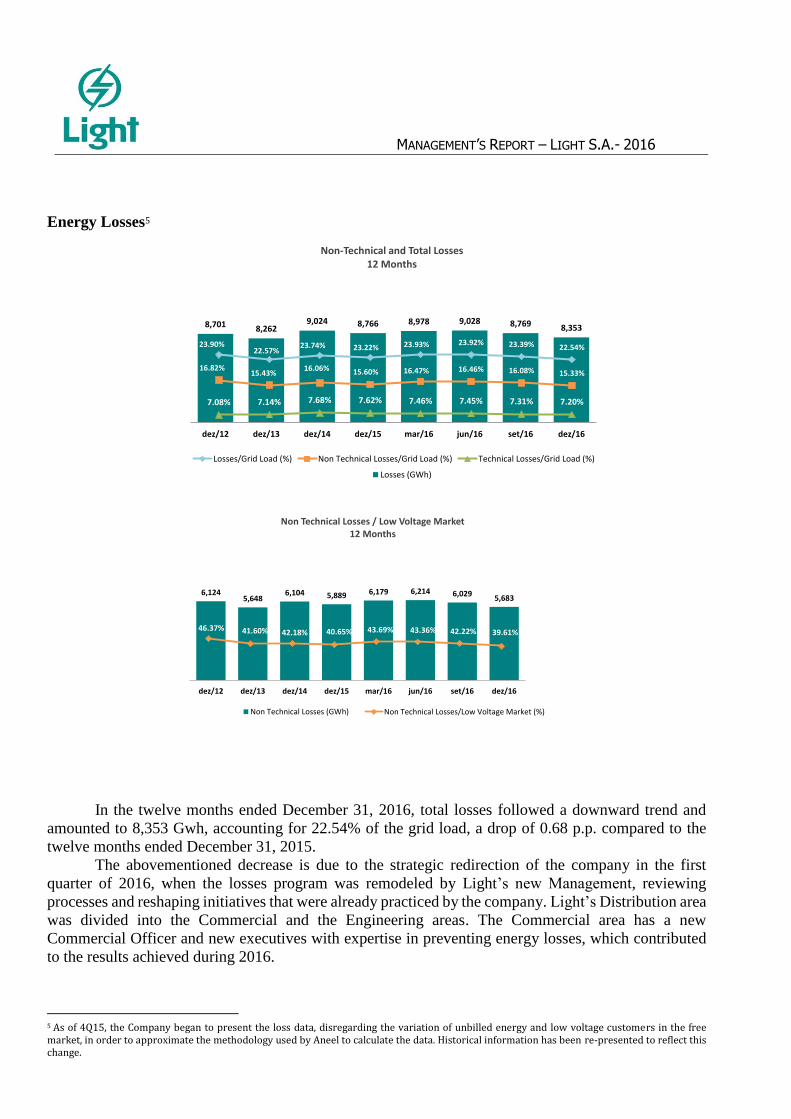

Energy Losses5

In the twelve months ended December 31, 2016, total losses followed a downward trend and

amounted to 8,353 Gwh, accounting for 22.54% of the grid load, a drop of 0.68 p.p. compared to the

twelve months ended December 31, 2015.

The abovementioned decrease is due to the strategic redirection of the company in the first

quarter of 2016, when the losses program was remodeled by Light’s new Management, reviewing

processes and reshaping initiatives that were already practiced by the company. Light’s Distribution area

was divided into the Commercial and the Engineering areas. The Commercial area has a new

Commercial Officer and new executives with expertise in preventing energy losses, which contributed

to the results achieved during 2016.

5 As of 4Q15, the Company began to present the loss data, disregarding the variation of unbilled energy and low voltage customers in the free market, in order to approximate the methodology used by Aneel to calculate the data. Historical information has been re-presented to reflect this change.

8,701 8,2629,024 8,766 8,978 9,028 8,769 8,353

dez/12 dez/13 dez/14 dez/15 mar/16 jun/16 set/16 dez/16

Non-Technical and Total Losses12 Months

Losses (GWh)

23.90%22.57%

23.74% 23.22% 23.93% 23.92% 23.39% 22.54%

16.82%15.43%

16.06% 15.60% 16.47% 16.46% 16.08% 15.33%

7.08% 7.14% 7.68% 7.62% 7.46% 7.45% 7.31% 7.20%

Losses/Grid Load (%) Non Technical Losses/Grid Load (%) Technical Losses/Grid Load (%)

6,1245,648

6,104 5,889 6,179 6,214 6,0295,683

dez/12 dez/13 dez/14 dez/15 mar/16 jun/16 set/16 dez/16

Non Technical Losses / Low Voltage Market12 Months

Non Technical Losses (GWh)

46.37% 41.60% 42.18% 40.65% 43.69% 43.36% 42.22% 39.61%

Non Technical Losses/Low Voltage Market (%)

MANAGEMENT’S REPORT – LIGHT S.A.- 2016

Other methods were adopted to combat non-technical losses in particular, based on studies and

detection of “theft” and its causes, resulting in new combat initiatives. According to its new strategy, the

Company chose to intensify the combat of energy loss in areas referred to as “possible” areas, i.e., areas

where Light can act, with a higher number of middle- and high-income consumers. We also continued

to combat energy loss in “risk areas,” however, at a less intense pace, including initiatives that require

less investments.

Below are the details of the new initiatives introduced in 2016 and the strategies that are already

in place:

Review of Processes

The review of processes included a reassessment of the procedures regarding losses and the

introduction of new technologies to hinder the access of fraudsters to the electronic meter, such as:

(i) increase in the number of collective shielding in residential buildings; and (ii) training provided to

electronic meter reading agents and relationship agents to help identifying frauds.

Advertisement Actions

The Company launched an advertisement campaign against energy theft directed at the upper,

middle, and lower classes, broadcast on TV, radio and billboards. This initiative gave fraudsters the

opportunity of correcting irregularities, upon the offer of special conditions. Moreover, the internal

channel was reformulated, allowing employees to report irregularities that cause energy losses.

Energy Losses Program

In 2016, the Energy Losses Program prevented the theft of 957.50 GWh, representing a 31.8%

improvement compared to 2015, of which 683.01 GWh refer to recovered energy (REN), 189.55 GWh

refer to incorporated energy (IEN), and 84.94 GWh refer to load reduction. In 4Q16 particularly, the

Energy Losses Program prevented the theft of 497.6 GWh, of which 382.9 GWh refer to recovered

energy (REN), 78.7 GWh refer to incorporated energy (IEN), and 36.0 GWh refer to load reduction,

exceeding additional losses of 151.6 GWh. It is worth mentioning the significant increase in the volume

of recovered energy (+166% vs. 2015) as a result of the new energy loss combat strategy focused on

areas where Light can act (Possible Areas), accounting for 90% of the grid load and 51% of losses. As

of now, as the energy losses program advances, the volume of recovered energy tends to be gradually

replaced by the additional consumption incorporated to the revenue base, i.e., the Incorporated Energy

– IEN.

MANAGEMENT’S REPORT – LIGHT S.A.- 2016

The new theft prevention initiatives in 2016 resulted in the recovery and incorporation of larger

volumes of energy per customer and lower expenses per MWh whose theft has been prevented,

representing an 36.2% decrease compared to 2015. We can also identify a continuing decrease in loss

indicators at “Possible Areas” compared to a slight increase at “Risk Areas” due to the deterioration of

the social and economic scenario in Rio de Janeiro.

The main initiatives in the Non-Technical Energy Losses Combat Program are as follows:

o Operativos

Operativos, also called “blitz,” are concentrated in Possible Areas and target clients selected by

the Light Intelligence Center, taking place more than once a week and involving approximately 700

professionals, including field teams, lawyers, military and civil police, and police stations. Barra da

Tijuca, Vargem Grande, Copacabana, Duque de Caxias, Ilha do Governador, Centro, and Lapa are some

-5.7%

Load Reduction

Dec/16 Losses (12 months)

151.65,683.0

Additional Losses

Energy Incorporation

-36.0

-78.7

Energy Recovery

-382.9

Sep/16 Losses (12 months)

6,029

Losses Combat Program

(GWh)

MANAGEMENT’S REPORT – LIGHT S.A.- 2016

of the neighborhoods where the Company intensified its

operations during the year. This strategy has high detection rates

concerning irregularities, not only in residences of these regions,

but also in restaurants, gyms, and ice cream shops, among

others, which confirms the efficacy of these initiatives as a

market discipline tool. In the event evidence of energy

consumption irregularities is detected, an Occurrence and

Inspection Notice (Termo de Ocorrência e Inspeção – TOI) and

a Police Report (Registro de Ocorrência – RO) are issued,

resulting in the imprisonment of those responsible in certain

cases. The results of these initiatives allow us to calculate and

bill the irregular energy consumption for the relevant period,

ensuring the recovered energy. These Operativos

have had repercussions in the areas where they are

conducted and also in the local media, as part of the

strategy to recover the concession ownership.

o Zero Loss Areas (Área de Perda

Zero – APZ)

Currently, the APZ project encompasses

850 thousand clients, with 39 operational APZs. In

APZs where Light’s activities are regular, average

non-technical losses over the grid load reached

13.7% in 2016, compared to 49.0% before the

beginning of the project.

In addition to these initiatives, Light

continues to invest in regularization procedures (rectifying the supply of electricity by eliminating

irregularities in the consumer unit or in Light’s network) and, at a slower pace, in the installation of

electronic meters.

Collection

In 2016, the collection rate reached 96.3%, representing a 1.6 p.p. increase compared to 2015

(94.7%). At the end of the year, we noted a decrease only in the collection rate of the Retail segment

due to the increase in Recovered Energy billed. This increase in Recovered Energy billed adversely

affects the global collection rate as a large portion of these payments is made in installments; on the

other hand, it increases revenue and global gross collections. Excluding the effect of Recovered Energy,

the collection rate of the Retail segment would reach 99.2% in 2016, 99.1% of Light’s total collection

rate in 2016.

Number of Normalizations 2016 2015 Var. %

= Total 135,375 51,041 165.2%

- High / Medium Voltage 1,135 905 25.4%

- Low Voltage 134,240 50,136 167.8%

Direct low voltage 126,120 40,333 212.7%

Indirect low voltage 2,835 9,803 -71.1%

Large Retail Clients (200A) 5,285 - -

Electronic Meters Installed

(thousand units)

480640 670

142

176218

888+72

+9%

Dec/16Dec/15

816

Dec/14

622

+31%

Outside of CommunitiesCommunities

Public Sector

100.8%

82.3%

98.4% 96.5%

Large ConsumersRetail

98.6% 96.3%94.7%

Total

94.6%96.1% 95.5%101.5%97.8%

201620152014

Collection Rate per SegmentAccumulated

99.1% 99.2%

Without Enery Recovery

MANAGEMENT’S REPORT – LIGHT S.A.- 2016

In 2016, the collection rates of the Public Sector and Large Consumers segments are noteworthy,

increasing by 13.2 p.p. and 2.4 p.p., respectively, compared to 2015, evidencing the collection initiatives

and negotiations conducted with clients of all segments.

Operating Quality

2016 was marked by the completion of the transformation works of Rio de Janeiro and by the

establishment of the structure required for the 2016 Olympic Games in Rio. Notwithstanding this

challenging scenario, Light continued to seek the improvement of its processes and was increasingly

focused on its operating management and assertiveness in the use of funds in networks.

DEC for the twelve months ended December 31,

2016 totaled 11.70 hours, an improvement of 7.2%

compared to 2015. FEC reached 6.48x, in line with 2015.

It is worth mentioning that, as a result of the

assertiveness in the establishment of operating

strategies, together with improved management

initiatives regarding field work, indicators continue to improve, reaffirming the commitment of Light in

achieving the targets of the Results Plan agreed with ANEEL in 2016. The Results Plan is a commitment

assumed by Light with the Regulator to adjust the quality indicators regarding supply, customer service,

and occupational safety.

A DEC of 11.70 hours for 2016 is already below the upper limit agreed with ANEEL under the

Results Plan (11.99 hours), according to which new targets were established for the period between 2018

and 2022, as set forth in the 5th Amendment to the Concession Agreement. This result reinforces our

confidence in the achievement of these targets through an investment plan designed for this challenge,

together with an efficient management of funds and

consistency with the new economic and financial

equilibrium following the tariff review.

Customer Service

In 2016, Light’s customer service channels

received investments of R$2.7 million. The strategy

consisted of reducing the costs of customer service

without affecting customers, increasing their

satisfaction and the quality of services provided. As

the main result, Light was the distribution company

in the southeast region with the highest growth in the ANEEL Customer Satisfaction Index (Índice Aneel

de Satisfação do Consumidor – IASC).

The company further increased the share of virtual customer service channels and ensured they

were fully operational, providing prompt responses to any abnormality, improving processes and

procedures, and focusing on access quality and convenience to contact Light.

The improvement in customer service, initiatives on the streets to prevent losses, and investments

made in the energy network show customers the Company’s efforts to provide quality service.

INDICATOR REGULATORY

TARGET

GLOBAL

AMOUNT

Global DEC 11.99 11.70

Global FEC 6.36 6.48

1.3%

1.0%

1.3%

dec-14 dec-15 dec-16

PDD/Gross Revenue Billed Sales - Quarter

+0,3 p.p.

MANAGEMENT’S REPORT – LIGHT S.A.- 2016

Generation

In 2016, the volume of energy sold totaled 4,227.0 GWh, representing a 3.0% increase compared

to 4,101.9 GWh in 2015. The volume of energy sold in the free market (“ACL”) continued to increase

in 2016 and totaled an amount 8.8% higher compared to that of 2015. This result is primarily due to:

(i) the seasonality strategy combined with the increase in the volume of existing agreements; and (ii) the

sale of the hydrological hedge amount in December, which did not occur in 2015.

Generation Projects

As of date, the Company has generation projects under development in its portfolio, aimed at

supplementing its installed capacity, which currently totals 1,024 MW. Below is a brief summary of

Light’s generation projects:

Lajes Small Hydro Power Plant – The project includes the construction of SHPP Lajes, with a generation

unit of 17 MW of installed capacity, at the same location of former HPP Fontes Velha, which was finally

deactivated in 1989. For the implementation, construction, operation and maintenance of SHPP Lajes,

Lajes Energia S.A., a special purpose entity, was established as a closely-held corporation (sociedade

anônima de capital fechado), wholly-owned by Light Energia S.A. Commencement of operations is

expected for the second semester of 2017.

Guanhães Energia – In February 2012, Light Energia acquired 51% of equity interest in Guanhães

Energia S.A. The remaining 49% is held by Cemig. Guanhães Energia is responsible for the

implementation and operation of SHPPs Dores de Guanhães (14MW), Senhora do Porto (12MW),

Fortuna II (9MW), and Jacaré (9MW), totaling 44MW of installed capacity. These SHPPs are located

in the Guanhães river and Corrente Grande river, in the State of Minas Gerais.

Belo Monte – In October 2011, Amazônia Energia, whose members are Light (25.5%) and Cemig

(74.5%), acquired 9.77% of Norte Energia, a company responsible for the construction and operation of

HPP Belo Monte. Located in the Xingu river, in the State of Pará, HPP Belo Monte is 100% Brazilian,

the fourth largest hydro power plant in the world and the largest in Brazil. Its installed capacity totals

11,233 MW, with an average Physical Guarantee of 4,571 MW, sufficient energy to service

approximately 18 million houses.

Renova Energia – Renova Energia operates in the segment of generation of electricity through renewable

alternative sources, such as small hydro power plants (SHPPs) and wind and solar power plants. Renova

Energia has an installed capacity of 1,979 MW, 683.3 MW of which is in operation. Light holds a 15.68%

equity interest in Renova Energia.

On January 12, 2017, Light Energia S.A., together with Renova Energia, entered into an agreement with

AES Tietê Energia to sell the wind farms that comprise the Alto Sertão II complex, with an installed

capacity of 386 MW. The base price of this transaction is R$650 million and includes the purchase of

Energy Sale (GWh) 2016 2015 Var. %

Free Contracting Environment Sales 4,669.9 4,291.0 8.8%

Spot Sales (CCEE) (442.9) (189.1) -134.2%

Total 4,227.0 4,101.9 3.0%

MANAGEMENT’S REPORT – LIGHT S.A.- 2016

shares issued by Renova Eólica Participações S.A. or Nova Energia Holding S.A., companies that

control all 15 special purpose entities that comprise the Alto Sertão II complex. The price is subject to

adjustments in the event certain conditions of the Transaction are met.

Commercialization

In 2016, the commercialization of energy totaled 5,711 GWh, representing a 10.7% increase

compared to 5,158 GWh sold in 2015 due to the following reasons: (i) new sales, especially to customers

that migrated from the captive market to the free market; (ii) the commencement of commercial

operations under the Light II subsidized energy agreement in 4Q16; and (iii) the sale of conventional

energy (hydrological hedge) in 2016.

EBITD6 A increased by 10.8% due to a higher volume of energy sold.

Investments

In 2016, investments made by Light totaled R$953.2 million. The largest amount of investments

was made in the Distribution segment (R$659.0 million), primarily in network reinforcements and

expansion (including investments related to the Olympic Games, in the amount of R$100.1 million) and

initiatives to combat losses. The decrease in Losses is noteworthy, totaling R$108 million, representing

a 30.1% decrease compared to 2015, due to the new strategy to prevent energy theft, which is more cost

intensive. Investments in the Distribution segment decreased by 14.8% in 2016 compared to 2015.

Accordingly, total investments made by the Company in 2016 (without contributions) decreased

by 13.5% compared to 2015, notwithstanding a significant improvement in quality indicators, losses and

payments.

In 2016, Light Energia made investments in the amount of R$45.2 million, representing a 19.7%

decrease compared to 2015, due to the postponement of the commencement of operations of SHPP

Lajes.

Contributions made in assets in which Light holds equity interest (Belo Monte, Renova,

Guanhães, Itaocara, and the Água Limpa Project) totaled R$180.6 million at the end of 2016.

Financial Comments

Financial Performance Net Revenue

Net revenue, excluding construction revenue, totaled R$8,755.6 million, representing a 12.2%

decrease compared to 2015, due to, among other factors, the decrease in the volume of energy sold by

the Distribution Company in 4Q16, affected by an average tariff adjustment of -12.25%, ratified on

November 7, 2016. The impact of this decrease was mitigated by the recovered energy, which added

R$164 million to this line item in the last quarter of the year.

6 EBITDA is not an acknowledged measure under BRGAAP or IFRS. Despite being used by the Company as an additional measure of its operations’ performance, it should not be

analyzed separately or as an alternative to net income or operating income, as a measure of operating performance, or as a liquidity indicator. CVM EBITDA is calculated in accordance with CVM Instruction 527/2012 and represents net income +income and social contribution tax + net financial expenses + depreciation and amortization.

MANAGEMENT’S REPORT – LIGHT S.A.- 2016

Moreover, we also note other deviations that are related to the activities of the Distribution

Company, including: (i) a decrease in non-billed energy; (ii) Spot Short-Term Revenue of R$91.9

million, which did not occur in 2015; and (iii) a worsening in the “Others” line item, which includes a

negative adjustment of R$155.6 million carried out in 4Q16. This adjustment in the “Others” line item

refers to the difference between the new repositioning value (VNR) ratified by ANEEL and the updated

balance of the concession financial asset due to the new regulatory remuneration base ratified in the

tariff review.

Light Energia helped increasing the net revenue of Light S.A., contributing with a higher number

of free market agreements and the sale of hydrological hedge, which totaled R$59.8 million in 2016.

Light Com also helped increasing the net revenue of Light S.A., as its Net Revenue reached R$951

million, representing a 16.5% increase compared to 2015, primarily due to (i) new clients, largely as a

result of their migration from the captive market to the free market, (ii) the effectiveness of a subsidized

energy sale agreement (average of 33 MW) in 4Q16, and (iii) the sale of hydrological hedge in December

2016.

Costs and Expenses

In 2016, consolidated operating costs and expenses, excluding construction costs, totaled

R$7,823.7 million, representing an 11.3% decrease compared to 2015, due to a decrease in losses,

provisions, and costs with the purchase of energy.

Adjusted EBITDA7

In 2016, Adjusted EBITDA totaled R$1,426.8 million, representing an 11.6% decrease

compared to R$1,614.4 million in 2015. EBITDA margin was 16.3%, representing a 0.1 p.p. decrease

compared to the previous year, primarily due to a decrease in revenue of the Distribution Company.

Net Result

In 2016, Light S.A. had a loss of R$312.9 million, primarily due to a 23.7% decrease in the

Adjusted EBITDA of the Distribution Company (which excludes equity in the results of subsidiaries

and non-operating result), affected by non-recurring effects in 4Q16, including: (i) the reversal of

R$144.8 million in Provisions for Contingencies; and (ii) the adjustment of -R$155.6 million regarding

the difference between the VNR ratified by ANEEL and the updated balance of the concession financial

asset. In addition to these factors, the result was also affected by Equity in the Results of Subsidiaries

by R$ 336.4, due to the impairment of Renova and Guanhães.

7 Adjusted EBITDA is calculated starting in the result before taxes and interest, equity pickup, other operating expenses/revenues (non-operating result), financial result,

depreciations and amortizations.

MANAGEMENT’S REPORT – LIGHT S.A.- 2016

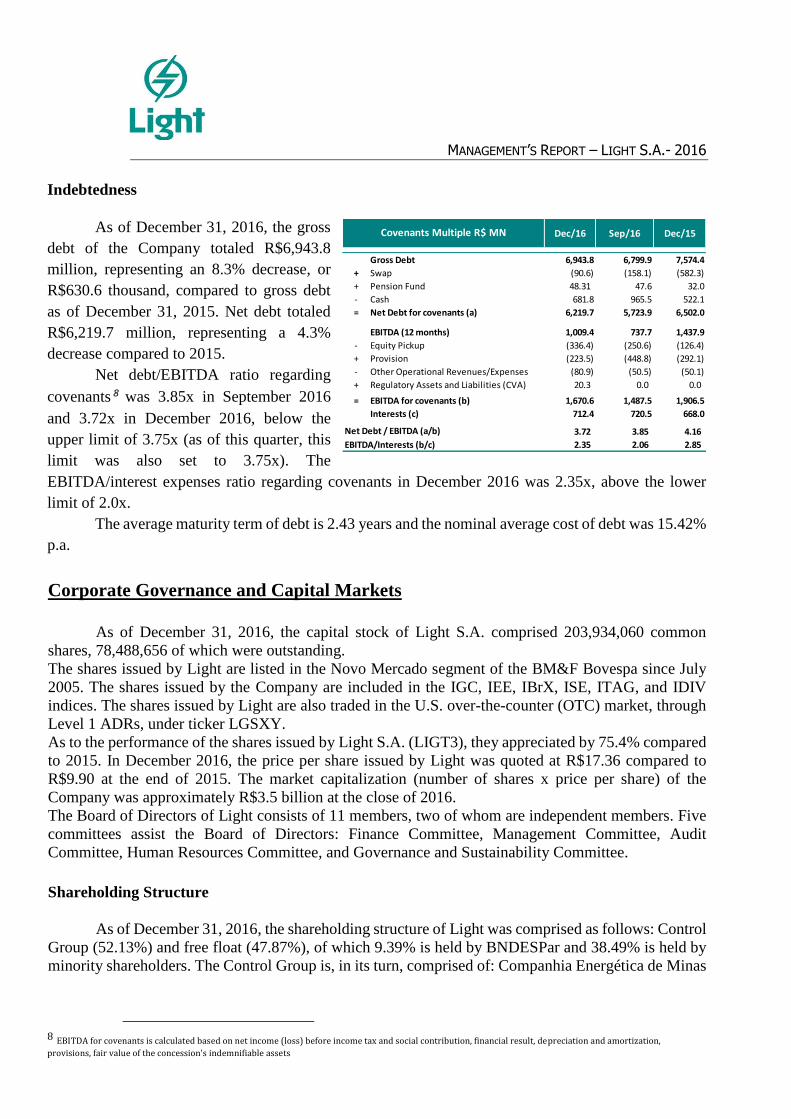

Indebtedness

As of December 31, 2016, the gross

debt of the Company totaled R$6,943.8

million, representing an 8.3% decrease, or

R$630.6 thousand, compared to gross debt

as of December 31, 2015. Net debt totaled

R$6,219.7 million, representing a 4.3%

decrease compared to 2015.

Net debt/EBITDA ratio regarding

covenants 8 was 3.85x in September 2016

and 3.72x in December 2016, below the

upper limit of 3.75x (as of this quarter, this

limit was also set to 3.75x). The

EBITDA/interest expenses ratio regarding covenants in December 2016 was 2.35x, above the lower

limit of 2.0x.

The average maturity term of debt is 2.43 years and the nominal average cost of debt was 15.42%

p.a.

Corporate Governance and Capital Markets

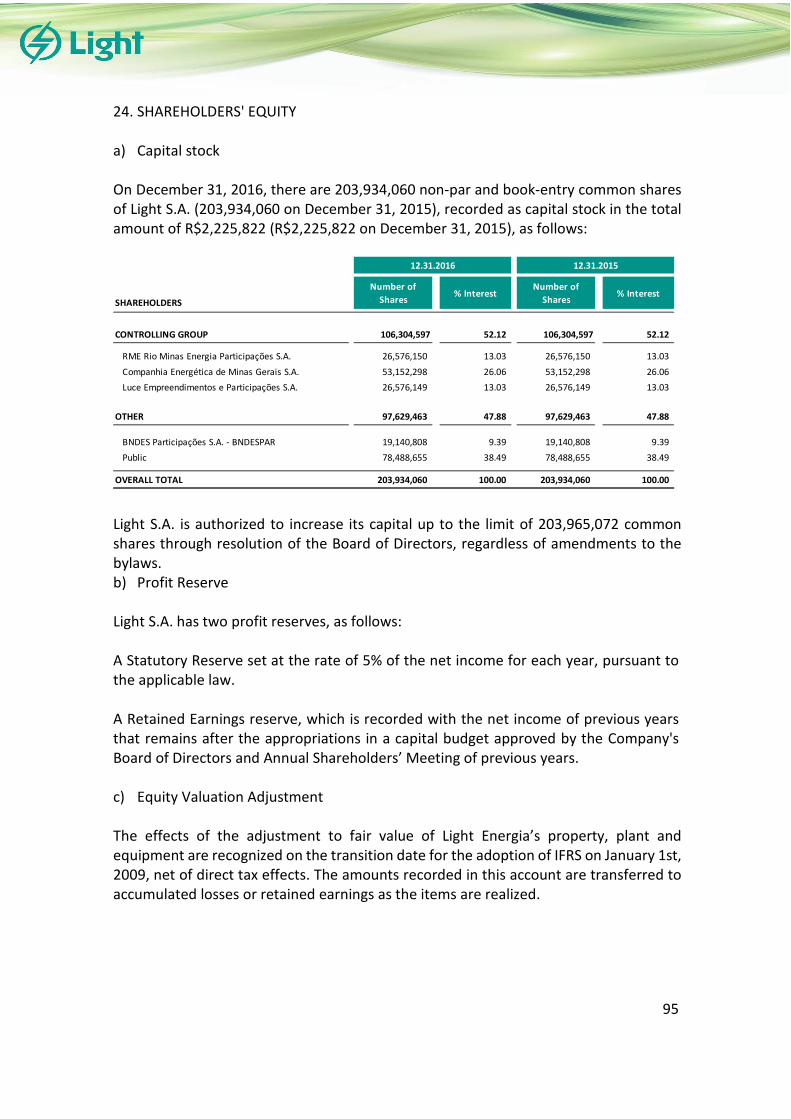

As of December 31, 2016, the capital stock of Light S.A. comprised 203,934,060 common

shares, 78,488,656 of which were outstanding.

The shares issued by Light are listed in the Novo Mercado segment of the BM&F Bovespa since July

2005. The shares issued by the Company are included in the IGC, IEE, IBrX, ISE, ITAG, and IDIV

indices. The shares issued by Light are also traded in the U.S. over-the-counter (OTC) market, through

Level 1 ADRs, under ticker LGSXY.

As to the performance of the shares issued by Light S.A. (LIGT3), they appreciated by 75.4% compared

to 2015. In December 2016, the price per share issued by Light was quoted at R$17.36 compared to

R$9.90 at the end of 2015. The market capitalization (number of shares x price per share) of the

Company was approximately R$3.5 billion at the close of 2016.

The Board of Directors of Light consists of 11 members, two of whom are independent members. Five

committees assist the Board of Directors: Finance Committee, Management Committee, Audit

Committee, Human Resources Committee, and Governance and Sustainability Committee.

Shareholding Structure

As of December 31, 2016, the shareholding structure of Light was comprised as follows: Control

Group (52.13%) and free float (47.87%), of which 9.39% is held by BNDESPar and 38.49% is held by

minority shareholders. The Control Group is, in its turn, comprised of: Companhia Energética de Minas

8 EBITDA for covenants is calculated based on net income (loss) before income tax and social contribution, financial result, depreciation and amortization,

provisions, fair value of the concession's indemnifiable assets

Dec/16 Sep/16 Dec/15

Gross Debt 6,943.8 6,799.9 7,574.4

+ Swap (90.6) (158.1) (582.3)

+ Pension Fund 48.31 47.6 32.0

- Cash 681.8 965.5 522.1

= Net Debt for covenants (a) 6,219.7 5,723.9 6,502.0

EBITDA (12 months) 1,009.4 737.7 1,437.9

- Equity Pickup (336.4) (250.6) (126.4)

+ Provision (223.5) (448.8) (292.1)

- Other Operational Revenues/Expenses (80.9) (50.5) (50.1)

+ Regulatory Assets and Liabilities (CVA) 20.3 0.0 0.0

= EBITDA for covenants (b) 1,670.6 1,487.5 1,906.5

Interests (c) 712.4 720.5 668.0

3.72 3.85 4.16

2.35 2.06 2.85

Covenants Multiple R$ MN

Net Debt / EBITDA (a/b)

EBITDA/Interests (b/c)

MANAGEMENT’S REPORT – LIGHT S.A.- 2016

Gerais (Cemig) (26.06%), Luce Empreendimentos e Participações S.A. (LEPSA) (13.03%), and Rio

Minas Energia S.A. (RME) (13.03%).

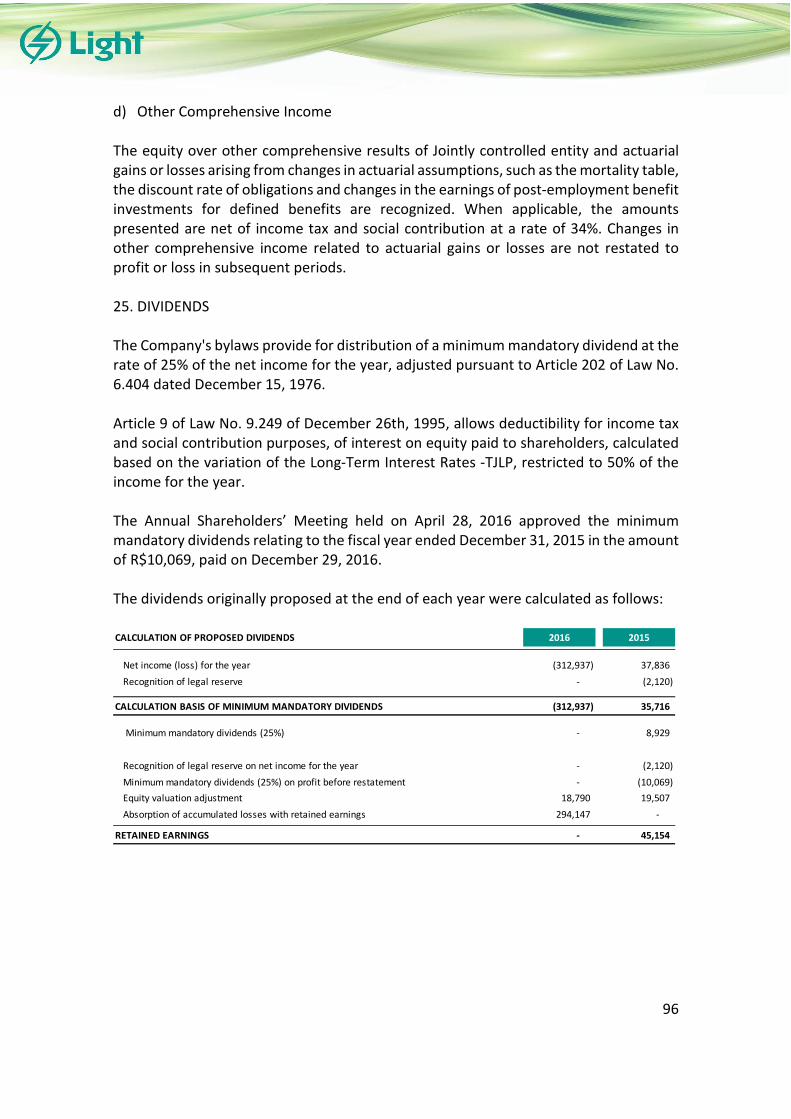

Distribution of Dividends

On December 29, 2016, dividends approved by the Shareholders’ Meeting held on April 28,

2016, in the amount of ten million, sixty-eight thousand, seven hundred seven Reais and forty-nine

centavos (R$10,068,707.49) were paid, representing R$0.049372368 per share. The dividend

distribution proposal approved by the Board of Directors on March 28, 2016, for the year ended

December 31, 2015, is compatible with the deleveraging strategy of the Company and cash

reinforcement, in view of the adverse economic scenario and the need to make investments in

distribution.

Commitment to the Future

People Management

In 2016, the company underwent a transition period towards the consolidation of a culture

strongly focused on results, aiming at continuous improvement, cost reduction, optimization of

processes or rethinking of operation models in order to obtain the best return possible. In view of the

crisis, we had to establish strategies to maintain the motivation, commitment, and alignment of

employees to the values of the company.

Accordingly, the company remained focused on its rules of conduct, centered in Safety, Ethics

and Result, i.e., the “Light Way of Being” (“Jeito de SER Light”).

Light started the Performance Management Cycle for Leaderships and Careers Y, whose main

objectives are the alignment between individual performance and business, reinforcement of a culture

of feedback and career self-management, and incentive to meritocracy.

Light maintained its initiatives to ensure quality of life within the company, investing in the

physical and mental health of employees, and contributing to their work motivation and balance between

personal and professional life. The Breastfeeding Support Room was opened, an initiative that, together

with the Healthy Baby (Bebê Saúde) program, the Motherhood Citizenship (Maternidade Cidadã)

program, and the day-care allowance, won Light a certification from the Ministry of Health, as a

company that supports working breastfeeding mothers.

We also highlight the corporate environment, which was assessed in partnership with Great

Place to Work, a world-renowned institute.

Occupational Safety

Light remains focused on the safety of its work force and population, prioritizing investments in

the promotion of health and prevention of accidents through the Vida! Program and communication

campaigns targeting the population about the risks of the energy network.

According to the Vida! Program, we continue to further awareness, training, and process reviews.

We also conduct inspections and audits and manage the performance of occupational health and safety.

These initiatives reduced the accident rate by 4.15% in 2016, from 3.30 to 3.16. The rate of

serious accidents decreased by 66%, from 1,057 to 359. Occupational abstentions decreased by 21%

compared to 2015, from 2.60 to 2.06.

MANAGEMENT’S REPORT – LIGHT S.A.- 2016

It is also worth noting the partnerships between employers’ associations and employees of the

civil construction sector, Senai, technical schools, and government agencies to multiply information on

the safe use of electricity, and further discuss the subject in communities, through lectures, visits, and

service shifts.

Research and Development (R&D)

The purpose of the R&D Program is to support all areas of the company in the development of

methods, software, and systems to improve the company’s activities and offer them to the market for

sale to the electricity sector in general, generating royalties to Light.

Investments in the R&D Program regulated by ANEEL totaled approximately R$8 million, of

which R$6 million was invested in Light SESA and R$2 million in Light Energia, meeting the regulatory

obligation regarding the accounting balance of the R&D account, which is required to total up to twice

the amount of annual mandatory investments.

Environmental Responsibility

The commitment of Light with the rational and adequate use of natural resources, including the

analysis of the company’s vulnerabilities to climate change and the mitigation of impacts, is expressed

in its Environmental Policy and in the Commitments to the Environment and Climate, which cover six

subjects: energy, technology, biodiversity, greenhouse gas emissions (GGE), solid waste, and the quality

of water.

Light’s Environmental Management System (Sistema de Gestão Ambiental – SGA), based on

ISO 14001, assesses and monitors aspects and impacts of its operational complex to ensure compliance

with applicable environmental law. In addition to the ISO 14001 certification, the Company’s power

plants also have ISO 9001 and OHSAS 18001 certifications, concerning quality, occupational health

and safety. This set of certifications comprises the Integrated Management System (Sistema de Gestão

Integrado – SGI), which, in the past 13 years, has been ensuring the excellence of the maintenance and

operation activities of generation of electricity.

Light also stood out in the works of the operations sites related the Olympic Games and in

obtaining environmental licenses for these places. Among others, we highlight the high voltage

distribution line Jacarepaguá-Curicica, responsible for the supply of the entire Olympic Complex. This

line crosses one environmental conservation unit, which required great efforts from Light with

environmental agencies to minimize the impacts generated during construction.

Social Responsibility

In view of the worsening of violence-related issues, Light expanded its partnerships with

Associations of Residents and established a relationship channel that allowed greater communication

with communities and facilitated energy recovery initiatives. Light also started to implement initiatives

in schools located in these communities and vicinities. As a result, meetings with parents, students and

teachers allowed the preparation of additional multiplying agents. These initiatives brought important

information about conscious consumption of energy and the Social Tariff, allowing the rectification of

clients and contributing to a sustainable development.

Under the Energy Efficiency Program (Programa de Eficiência Energética – PEE), Light

invested R$16.8 million in 19 projects and promoted a greater integration of energy efficiency initiatives

to combat energy losses and default. R$8 million was invested in Comunidade Eficiente, a project that

MANAGEMENT’S REPORT – LIGHT S.A.- 2016

involves the exchange of equipment for more efficient equipment and initiatives to foster changes in

habits in favor of a rational and safe consumption of electricity. R$1.5 million was invested in Light

Recicla, which consists of the exchange of recyclable waste for discounts in the energy bill.

As to sponsorships, Light seeks to foster sustainable development and improve the quality of life

of the population of the concession area. The decision to invest in certain projects is related to the

development of the concession area, the generation of income in pacified communities, and the visibility

of the Light brand, which also has an impact on the reduction of losses and default. In 2016, guided by

these criteria, the company raised approximately R$20 million, of which R$3 million was contributed

from Light’s own funds.

Other Information:

Independent Auditors

Pursuant to CVM Instruction No. 381/2003, we inform that Deloitte Touche Tohmatsu Auditores

Independentes provides external audit and quarterly review services to the Light Group and it did not

provide any other service to the Company that was not related to audit services in the year ended

December 31, 2016. The management’s report includes information related to projected investments

and non-financial data that is not part of the audit scope of the financial statements and was not reviewed

by the independent auditors.

MANAGEMENT’S REPORT – LIGHT S.A.- 2016

Balanço Social Anual / 2016Empresa: CONSOLIDADO1 - Base de Cálculo

Receita líquida (RL)

Resultado operacional (RO)

Folha de pagamento bruta (FPB)

2 - Indicadores Sociais Internos Valor (mil R$) % sobre FPB % sobre RL Valor (mil R$) % sobre FPB % sobre RL

Alimentação 31.335 8% 0% 29.139 9% 0%

Encargos sociais compulsórios 72.784 19% 1% 65.518 19% 1%

Previdência privada 9.068 2% 0% 9.261 3% 0%

Saúde 18.324 5% 0% 16.419 5% 0%

Segurança e saúde no trabalho 615 0% 0% 821 0% 0%

Educação 812 0% 0% 828 0% 0%

Cultura 0 0% 0% 0 0% 0%

Capacitação e desenvolvimento profissional 3.033 1% 0% 5.411 2% 0%

Creches ou auxílio-creche 1.311 0% 0% 1.198 0% 0%

Participação nos lucros ou resultados 26.859 7% 0% 25.088 7% 0%

Outros 6.092 2% 0% 4.677 1% 0%

Total - Indicadores sociais internos 170.233 46% 2% 158.360 47% 1%

3 - Indicadores Sociais Externos Valor (mil R$) % sobre RO % sobre RL Valor (mil R$) % sobre RO % sobre RL

Educação 5.402 1% 0% 6.814 1% 0%

Cultura 11.028 1% 0% 21.702 2% 0%

Saúde e saneamento 3.330 0% 0% 0 0% 0%

Esporte 8.924 1% 0% 29.432 3% 0%

Combate à fome e segurança alimentar 0 0% 0% 0 0% 0%

Outros 18.389 2% 0% 61.896 6% 1%

Total das contribuições para a sociedade 47.073 6% 0% 119.844 12% 1%

Tributos (excluídos encargos sociais) 5.446.210 638% 56% 3.816.727 390% 35%

Total - Indicadores sociais externos 5.493.283 644% 57% 3.936.571 402% 36%

4 - Indicadores Ambientais Valor (mil R$) % sobre RO % sobre RL Valor (mil R$) % sobre RO % sobre RL

Investimentos relacionados com a produção/ operação da empresa 51.574 6% 1% 55.374 6% 1%

Investimentos em programas e/ou projetos externos 0 0% 0% 0 0% 0%

Total dos investimentos em meio ambiente 51.574 6% 1% 55.374 6% 1%

Quanto ao estabelecimento de “metas anuais” para minimizar

resíduos, o consumo em geral na produção/ operação e aumentar

a eficácia na utilização de recursos naturais, a empresa5 - Indicadores do Corpo Funcional 2016 2015

Nº de empregados(as) ao f inal do período

Nº de admissões durante o período

Nº de empregados(as) terceirizados(as)

Nº de estagiários(as)

Nº de empregados(as) acima de 45 anos

Nº de mulheres que trabalham na empresa

% de cargos de chefia ocupados por mulheres

Nº de negros(as) que trabalham na empresa

% de cargos de chefia ocupados por negros(as)

Nº de pessoas com deficiência ou necessidades especiais

6 - Informações relevantes quanto ao exercício da

cidadania empresarial

Relação entre a maior e a menor remuneração na empresa

Número total de acidentes de trabalho

Os projetos sociais e ambientais desenvolvidos pela empresa

foram definidos por:

( ) direção ( X ) direção e

gerências

( ) todos(as)

empregados(as)

( ) direção ( X ) direção e

gerências

( ) todos(as)

empregados(as)

Os pradrões de segurança e salubridade no ambiente de trabalho

foram definidos por:

( ) direção e

gerências

( ) todos(as)

empregados(as)

( X ) todos(as) +

Cipa

( ) direção e

gerências

( ) todos(as)

empregados(as)

( X ) todos(as) +

Cipa

Quanto à liberdade sindical, ao direito de negociação coletiva e à

representação interna dos(as) trabalhadores(as), a empresa:

( ) não se envolve ( X ) segue as

normas da OIT

( ) incentiva e

segue a OIT

( ) não se

envolverá

( X ) seguirá as

normas da OIT

( ) incentivará e

seguirá a OIT

A previdência privada contempla:( ) direção ( ) direção e

gerências

( X ) todos(as)

empregados(as)

( ) direção ( ) direção e

gerências

( X ) todos(as)

empregados(as)

A participação dos lucros ou resultados contempla:( ) direção ( ) direção e

gerências

( X ) todos(as)

empregados(as)

( ) direção ( ) direção e

gerências

( X ) todos(as)

empregados(as)

Na seleção dos fornecedores, os mesmos padrões éticos e de

responsabilidade social e ambiental adotados pela empresa:

( ) não são

considerados

( ) são

sugeridos

( X ) são

exigidos

( ) não serão

considerados

( ) serão

sugeridos

( X ) serão

exigidos

Quanto à participação de empregados(as) em programas de

trabalho voluntário, a empresa:

( ) não se envolve ( ) apóia ( x ) organiza e

incentiva

( ) não se

envolverá

( ) apoiará ( X ) organizará e

incentivará

Número total de reclamações e críticas de consumidores(as): na empresa

251.158

no Procon

3.941

na Justiça

42.256

na empresa

Reduzir 10%

no Procon

Reduzir 10%

na Justiça

Reduzir 10%

% de reclamações e críticas atendidas ou solucionadas: na empresa

85%

no Procon

85%

na Justiça

57%

na empresa

100%

no Procon

100%

na Justiça

100%

Valor adicionado total a distribuir (em mil R$):

Distribuição do Valor Adicionado (DVA):

7 - Outras Informações

2016 Valor (mil reais) 2015 Valor (mil reais)

0

0

208

Metas 2017

ND

34

4.327

36,3

10.912.673

978.534

338.246

1.172

138

( ) não possui metas ( ) cumpre de 51 a 75%

( ) cumpre de 0 a 50% (X) cumpre de 76 a 100%

378

8.394

86,55% governo 4,63% colaboradores(as)

0,00% acionistas 11,82% terceiros -3,00% retido

Em 2015: 9.318.582

77,26% governo 3,99% colaboradores(as)

0,11% acionistas 18,35% terceiros 0,30% retido

9.645.237

853.002

373.352

( ) não possui metas ( ) cumpre de 51 a 75%

( ) cumpre de 0 a 50% (X) cumpre de 76 a 100%

1.061

23,60%

1.953

Em 2016: 8.725.810

2016

986

1.008

23,10%

1.910

19,30%

4.085

327

49

183

7.480

19,90%

1

NOTES TO THE PARENT COMPANY AND CONSOLIDATED

FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2016

2

1. OPERATIONS ................................................................................................................................................. 10

2. GROUP’S ENTITIES ........................................................................................................................................ 10

3. APPROVAL AND SUMMARY OF THE MAIN ACCOUNTING PRACTICES ADOPTED IN THE PREPARATION OF

THE FINANCIAL STATEMENTS ................................................................................................................................. 19

4. CASH AND CASH EQUIVALENTS .................................................................................................................... 39

5. MARKETABLE SECURITIES ............................................................................................................................. 39

6. CONSUMERS, CONCESSIONAIRES, PERMISSIONAIRES AND CLIENTS ............................................................ 40

7. RECOVERABLE TAXES .................................................................................................................................... 42

8. DEFERRED TAXES .......................................................................................................................................... 42

9. FINANCIAL ASSETS AND LIABILITIES OF THE SECTOR .................................................................................... 44

10. CONCESSION’S FINANCIAL ASSETS ................................................................................................................ 45

11. OTHER RECEIVABLES ..................................................................................................................................... 46

12. INVESTMENTS ............................................................................................................................................... 47

13. PROPERTY, PLANT AND EQUIPMENT ............................................................................................................ 57

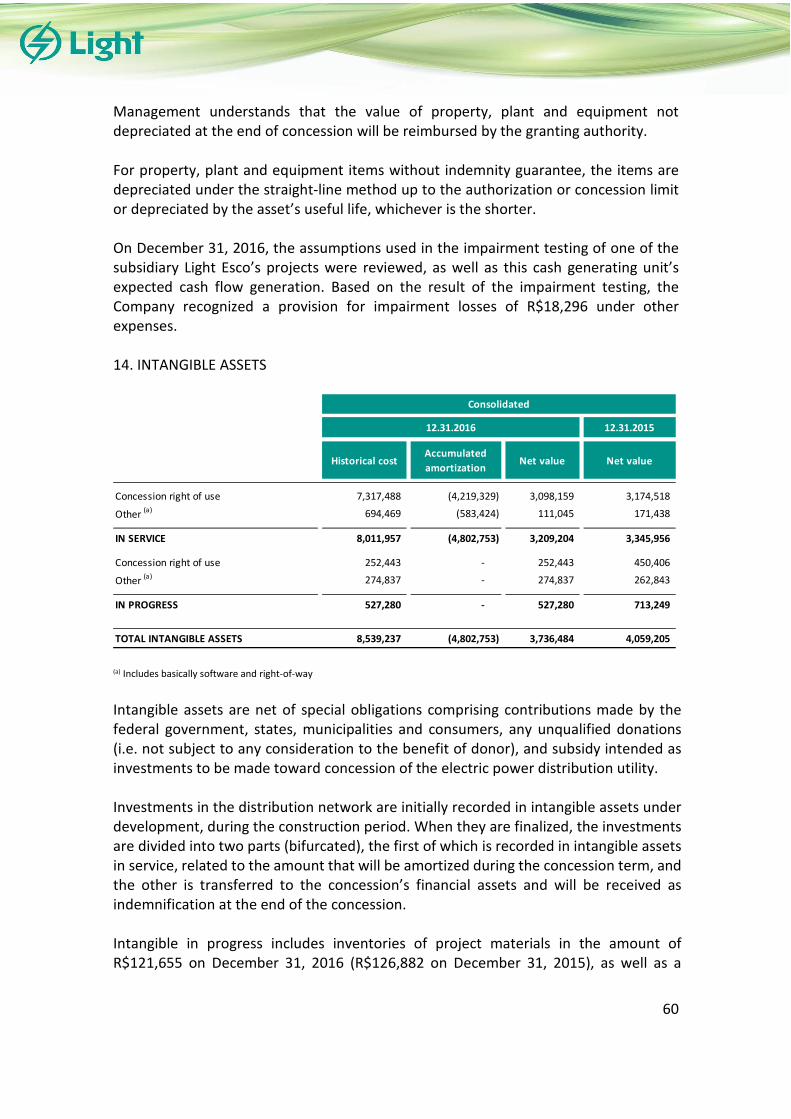

14. INTANGIBLE ASSETS ...................................................................................................................................... 60

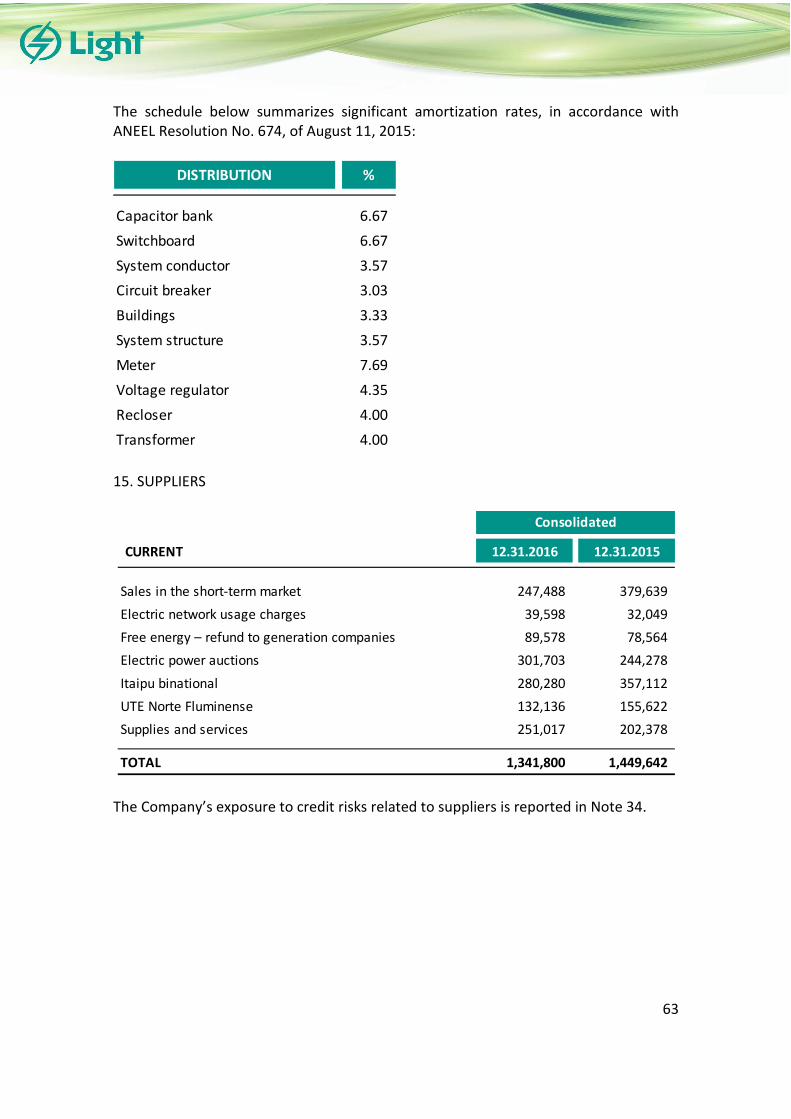

15. SUPPLIERS ..................................................................................................................................................... 63

16. TAXES PAYABLE ............................................................................................................................................. 64

17. LOANS AND FINANCING................................................................................................................................ 65

18. DEBENTURES ................................................................................................................................................ 70

19. PROVISIONS .................................................................................................................................................. 73

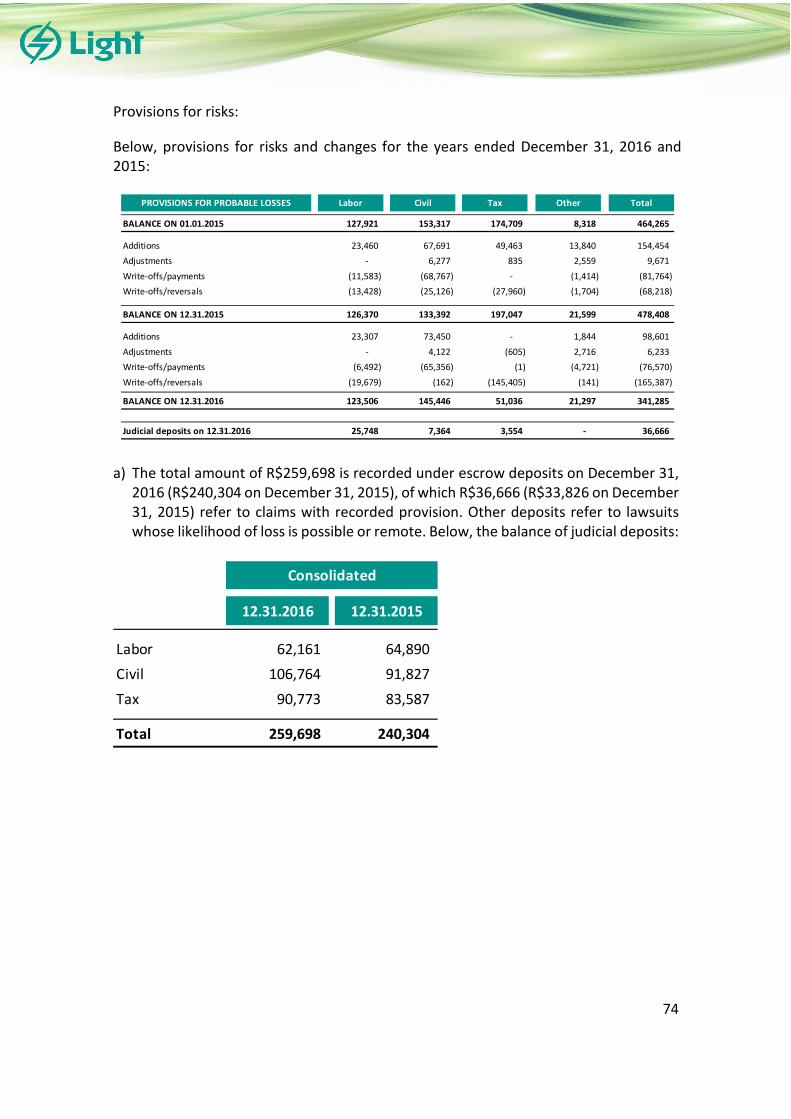

20. CONTINGENCIES ........................................................................................................................................... 79

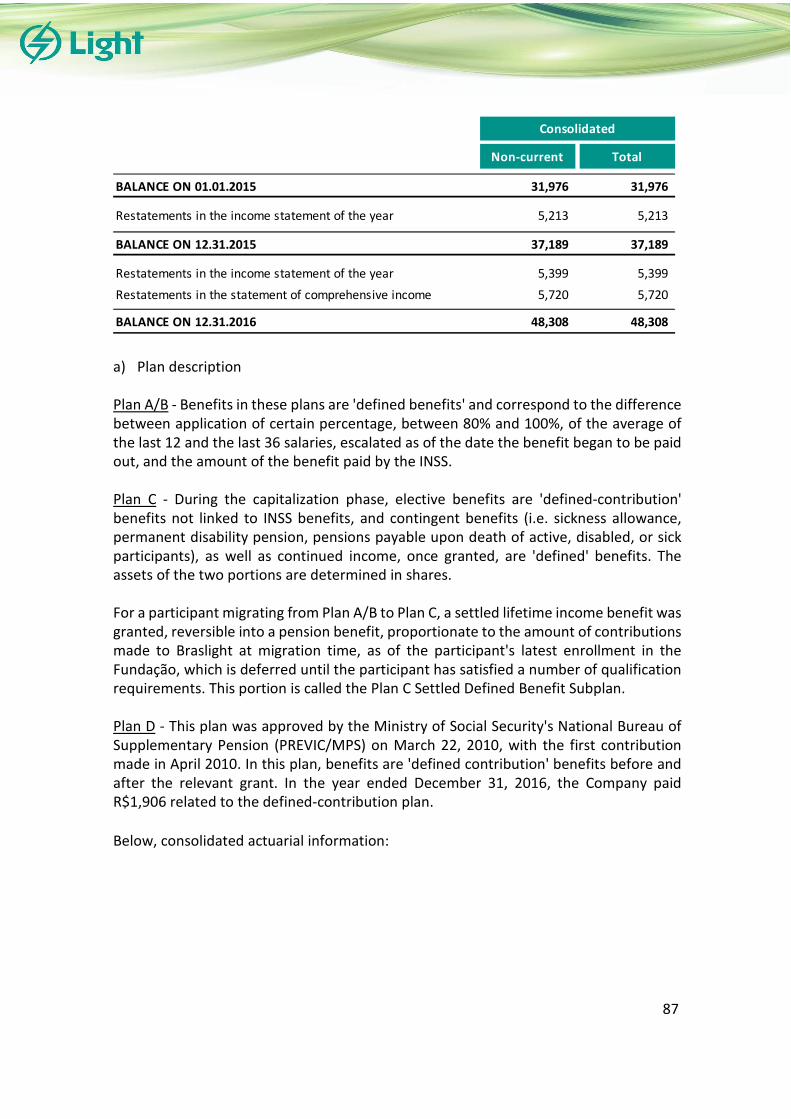

21. POST-EMPLOYMENT BENEFITS ..................................................................................................................... 86

22. OTHER PAYABLES .......................................................................................................................................... 92

23. RELATED-PARTY TRANSACTIONS .................................................................................................................. 92

24. SHAREHOLDERS' EQUITY .............................................................................................................................. 95

25. DIVIDENDS .................................................................................................................................................... 96

26. PROFIT SHARING ........................................................................................................................................... 97

27. EARNINGS PER SHARE .................................................................................................................................. 97

28. NET REVENUE ............................................................................................................................................... 98

29. ELECTRIC POWER SUPPLY ............................................................................................................................. 99

30. OPERATING COSTS AND EXPENSES ............................................................................................................. 100

31. ELECTRIC POWER PURCHASED FOR RESALE ............................................................................................... 100

32. FINANCIAL RESULT ...................................................................................................................................... 101

33. RECONCILIATION OF TAXES IN PROFIT OR LOSS ......................................................................................... 101

34. FINANCIAL INSTRUMENTS AND RISK MANAGEMENT................................................................................. 102

35. INSURANCE ................................................................................................................................................. 117

36. SEGMENT REPORTING ................................................................................................................................ 118

37. TARIFF ADJUSTMENT .................................................................................................................................. 120

38. LONG-TERM CONTRACTS ............................................................................................................................ 120

39. NON-CASH TRANSACTIONS ........................................................................................................................ 122

40. SUBSEQUENT EVENTS ................................................................................................................................. 122

3

ASSETS 12.31.2016 12.31.2015 12.31.2016 12.31.2015

Cash and cash equivalents 4 6,332 83,694 668,304 447,441

Marketable securities 5 - - 13,467 74,682

Consumers, concessionaires, permissionaires and clients 6 - - 2,271,871 2,199,230

Inventories - - 38,948 34,960

Taxes and contributions 7 - 86 120,561 90,443

Income tax and social contribution 7 801 561 80,715 86,237

Financial assets of the sector 9 - - - 568,675

Prepaid expenses 8 306 29,493 24,958

Dividends receivable 12 1,317 4,203 819 -

Receivables from services rendered 108 134 89,412 23,597

Receivables from swap transactions 34 - - 87,282 196,145

Other receivables 11 838 1,005 211,605 229,868

TOTAL CURRENT ASSETS 9,404 89,989 3,612,477 3,976,236

Consumers, concessionaires, permissionaires and clients 6 - - 418,068 218,527

Taxes and contributions 7 - - 75,344 85,939

Deferred taxes 8 - - 592,498 496,891

Prepaid expenses - - 148 201

Financial assets of the sector 9 - - - 43,001

Concessions' financial assets 10 - - 3,234,339 2,932,833

Deposits related to litigation 19 410 407 259,698 240,304

Receivables from swap transactions 34 - - 96,970 386,858

Other receivables 11 - - 1,322 2,147

Investments 12 3,345,985 3,628,749 664,440 749,645

Property, plant and equipment 13 672 672 1,638,441 1,709,633

Intangible assets 14 - - 3,736,484 4,059,205

TOTAL NON-CURRENT ASSETS 3,347,067 3,629,828 10,717,752 10,925,184

TOTAL ASSETS 3,356,471 3,719,817 14,330,229 14,901,420

The notes are an integral part of the financial statements.

LIGHT S.A.

(In thousands of reais)

Notes

Consolidated

STATEMENT OF FINANCIAL POSITION

AS AT DECEMBER 31, 2016 AND 2015

Parent Company

4

LIABILITIES 12.31.2016 12.31.2015 12.31.2016 12.31.2015

Trade accounts payable 15 249 526 1,341,800 1,449,642

Taxes and contributions 16 30 143 315,375 356,860

Income tax and social contribution 16 2 3 129,836 15,262

Loans and borrowings 17 - - 1,567,738 1,629,166

Debentures 18 - - 378,589 215,007

Financial liabilities of the sector 9 - - 440,533 -

Payable swap transactions 34 - - 43,312 -

Dividends payable 25 - 51,099 - 51,099

Estimated liabilities 1,563 1,210 60,897 54,478

Post-employment benefits 21 15 12 153 67

Other payables 22 816 860 593,172 627,790

TOTAL CURRENT LIABILITIES 2,675 53,853 4,871,405 4,399,371

Loans and borrowings 17 - - 1,871,001 2,547,976

Debentures 18 - - 3,126,431 3,182,236

Payable swap transactions 34 - - 50,341 720

Taxes and contributions 16 - - 169,789 183,183

Deferred taxes 8 - - 200,125 268,147

Financial liabilities of the sector 9 - - 84,168 -

Provisions 19 - - 417,874 541,434

Unsecured equity interest 12 - - 61,481 -

Post-employment benefits 21 - - 48,308 37,189

Other payables 22 - 901 75,510 76,101

TOTAL NON-CURRENT LIABILITIES - 901 6,105,028 6,836,986

SHAREHOLDERS' EQUITY

Capital stock 24 2,225,822 2,225,822 2,225,822 2,225,822

Profit reserves 24 843,824 1,137,971 843,824 1,137,971

Equity valuation adjustments 24 370,022 390,317 370,022 390,317

Other comprehensive income 24 (85,872) (89,047) (85,872) (89,047)

TOTAL SHAREHOLDERS' EQUITY 3,353,796 3,665,063 3,353,796 3,665,063

TOTAL LIABILITIES AND SHAREHOLDERS' EQUITY 3,356,471 3,719,817 14,330,229 14,901,420

The notes are an integral part of the financial statements.

LIGHT S.A.

Notes

Consolidated

(In thousands of reais)

STATEMENT OF FINANCIAL POSITION

AS AT DECEMBER 31, 2016 AND 2015

Parent Company

5

2016 2015 20162015

Restated

NET REVENUE 28 - - 9,645,237 10,912,673

COST OF OPERATIONS 30 - - (8,042,026) (8,987,319)

Electric power purchased for resale 31 - - (6,167,503) (7,160,923)

Personnel - - (231,420) (191,210)

Material - - (59,647) (17,976)

Outsourced services - - (343,865) (298,388)

Depreciation and amortization - - (452,260) (411,647)

Cost of construction - - (889,632) (936,829)

Other revenues and expenses / costs - - 102,301 29,654

GROSS PROFIT - - 1,603,211 1,925,354

OPERATING EXPENSES (12,565) (11,116) (752,243) (820,420)

General and administrative expenses 30 (10,531) (11,116) (671,321) (770,350)

Other revenues - - 2,126 1,276

Other expenses (2,034) - (83,048) (51,346)

EQUITY IN THE EARNINGS OF SUBSIDIARIES 12 (300,892) 47,078 (336,429) (126,400)

EARNINGS BEFORE THE FINANCIAL RESULT AND TAXES (313,457) 35,962 514,539 978,534

FINANCIAL RESULT 32 520 1,874 (797,514) (854,304)

Revenue 1,000 1,930 147,533 747,591

Expense (480) (56) (945,047) (1,601,895)

RESULT BEFORE INCOME TAX AND SOCIAL CONTRIBUTION (312,937) 37,836 (282,975) 124,230

Current income tax and social contribution 33 - - (190,871) (63,983)

Deferred income tax and social contribution 33 - - 160,909 (22,411)

NET INCOME (LOSS) FOR THE PERIOD (312,937) 37,836 (312,937) 37,836

Attributed to the controlling shareholders (312,937) 37,836 (312,937) 37,836

BASIC AND DILUTED EARNINGS (LOSSES) PER SHARE (R$ / Share) 27 (1.53) 0.19

The notes are an integral part of the financial statements.

Notes

Parent Company Consolidated

LIGHT S.A.

FISCAL YEARS ENDED DECEMBER 31, 2016 AND 2015

(In thousands of reais, except earnings (loss) per share)

STATEMENTS OF OPERATIONS

6

Notes 2016 2015 2016 2015

Profit (Loss) for the year 27 (312,937) 37,836 (312,937) 37,836

Other comprehensive income not reclassified to profit or loss in subsequent periods

Gains (losses) on actuarial liabilities, net of tax effects 21 (3,775) - (3,775) -

Equity accounting on other comprehensive income of jointly-owned subsidiary 12 6,950 8,671 6,950 8,671

TOTAL COMPREHENSIVE INCOME (309,762) 46,507 (309,762) 46,507

Attributed to the controlling shareholders (309,762) 46,507 (309,762) 46,507

The notes are an integral part of the financial statements.

Consolidated

FISCAL YEARS ENDED DECEMBER 31, 2016 AND 2015

STATEMENS OF COMPREHENSIVE INCOME

(In thousands of reais)

LIGHT S.A.

Parent Company

7

NotesCAPITAL

STOCK

LEGAL

RESERVE

RETAINED

EARNINGS

EQUITY

VALUATION

ADJUSTMENTS

OTHER

COMPREHENSIVE

INCOME

RETAINED

EARNINGS

(ACCUMULATED

LOSSES)

TOTAL

BALANCES ON JANUARY 1, 2015 2,225,822 259,516 831,181 409,824 (97,718) - 3,628,625

Total comprehensive income:

Profit for the year 27 - - - - - 37,836 37,836

Other comprehensive income not reclassified to profit or loss in subsequent periods

Equity accounting on other comprehensive income of jointly-owned subsidiary 12 - - - - 8,671 - 8,671

Realization of equity valuation adjustment, net of taxes - - - (19,507) - 19,507 -

Allocation of net income for the year:

Recognition of legal reserve - 2,120 - - - (2,120) -

Minimum mandatory dividends - 25% (R$0.0494 / share) - - - - - (10,069) (10,069)

Recognition of earnings retention reserve - - 45,154 - - (45,154) -

BALANCES ON DECEMBER 31, 2015 2,225,822 261,636 876,335 390,317 (89,047) - 3,665,063

Total comprehensive income:

Profit for the year 27 - - - - - (312,937) (312,937)

Other comprehensive income not reclassified to profit or loss in subsequent periods

Losses on actuarial liabilities, net of tax effects 21 - - - - (3,775) - (3,775)

Equity accounting on other comprehensive income of jointly-owned subsidiary 12 - - - - 6,950 - 6,950

Realization of equity valuation adjustment, net of taxes - - - (20,295) - 18,790 (1,505)

Absorption of loss for the year - - (294,147) - - 294,147 -

BALANCES ON DECEMBER 31, 2016 2,225,822 261,636 582,188 370,022 (85,872) - 3,353,796

The notes are an integral part of the financial statements.

PROFIT RESERVES

LIGHT S.A.

STATEMENTS OF CHANGES IN SHAREHOLDERS' EQUITY - PARENT COMPANY AND CONSOLIDATED

FISCAL YEARS ENDED DECEMBER 31, 2016 AND 2015

(In thousands of reais)

8

Notes 2016 2015 2016 2015

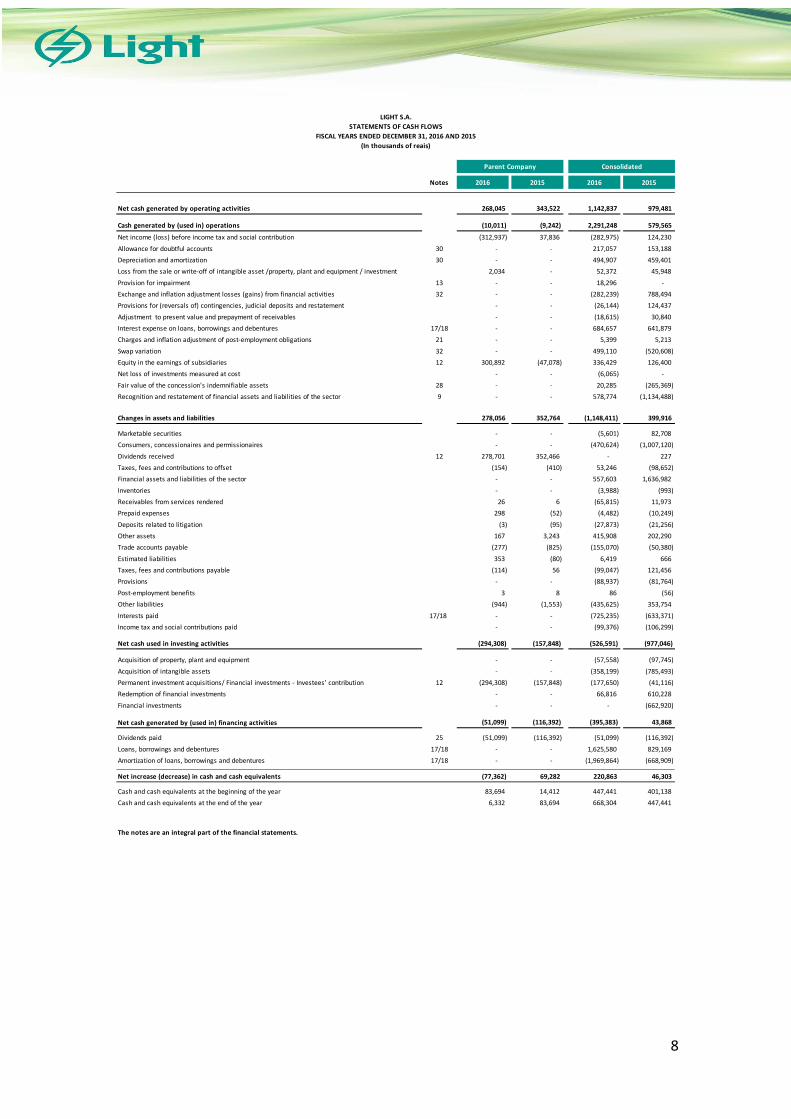

Net cash generated by operating activities 268,045 343,522 1,142,837 979,481

Cash generated by (used in) operations (10,011) (9,242) 2,291,248 579,565

Net income (loss) before income tax and social contribution (312,937) 37,836 (282,975) 124,230

Allowance for doubtful accounts 30 - - 217,057 153,188

Depreciation and amortization 30 - - 494,907 459,401

Loss from the sale or write-off of intangible asset /property, plant and equipment / investment 2,034 - 52,372 45,948

Provision for impairment 13 - - 18,296 -

Exchange and inflation adjustment losses (gains) from financial activities 32 - - (282,239) 788,494

Provisions for (reversals of) contingencies, judicial deposits and restatement - - (26,144) 124,437

Adjustment to present value and prepayment of receivables - - (18,615) 30,840

Interest expense on loans, borrowings and debentures 17/18 - - 684,657 641,879

Charges and inflation adjustment of post-employment obligations 21 - - 5,399 5,213

Swap variation 32 - - 499,110 (520,608)

Equity in the earnings of subsidiaries 12 300,892 (47,078) 336,429 126,400

Net loss of investments measured at cost - - (6,065) -

Fair value of the concession's indemnifiable assets 28 - - 20,285 (265,369)

Recognition and restatement of financial assets and liabilities of the sector 9 - - 578,774 (1,134,488)

Changes in assets and liabilities 278,056 352,764 (1,148,411) 399,916

Marketable securities - - (5,601) 82,708

Consumers, concessionaires and permissionaires - - (470,624) (1,007,120)

Dividends received 12 278,701 352,466 - 227

Taxes, fees and contributions to offset (154) (410) 53,246 (98,652)

Financial assets and liabilities of the sector - - 557,603 1,636,982

Inventories - - (3,988) (993)

Receivables from services rendered 26 6 (65,815) 11,973

Prepaid expenses 298 (52) (4,482) (10,249)

Deposits related to litigation (3) (95) (27,873) (21,256)

Other assets 167 3,243 415,908 202,290

Trade accounts payable (277) (825) (155,070) (50,380)

Estimated liabilities 353 (80) 6,419 666

Taxes, fees and contributions payable (114) 56 (99,047) 121,456

Provisions - - (88,937) (81,764)

Post-employment benefits 3 8 86 (56)

Other liabilities (944) (1,553) (435,625) 353,754

Interests paid 17/18 - - (725,235) (633,371)

Income tax and social contributions paid - - (99,376) (106,299)

Net cash used in investing activities (294,308) (157,848) (526,591) (977,046)

Acquisition of property, plant and equipment - - (57,558) (97,745)

Acquisition of intangible assets - - (358,199) (785,493)

Permanent investment acquisitions/ Financial investments - Investees’ contribution 12 (294,308) (157,848) (177,650) (41,116)

Redemption of financial investments - - 66,816 610,228

Financial investments - - - (662,920)

Net cash generated by (used in) financing activities (51,099) (116,392) (395,383) 43,868

Dividends paid 25 (51,099) (116,392) (51,099) (116,392)

Loans, borrowings and debentures 17/18 - - 1,625,580 829,169

Amortization of loans, borrowings and debentures 17/18 - - (1,969,864) (668,909)

Net increase (decrease) in cash and cash equivalents (77,362) 69,282 220,863 46,303

Cash and cash equivalents at the beginning of the year 83,694 14,412 447,441 401,138

Cash and cash equivalents at the end of the year 6,332 83,694 668,304 447,441

The notes are an integral part of the financial statements.

Parent Company Consolidated

LIGHT S.A.

STATEMENTS OF CASH FLOWS

FISCAL YEARS ENDED DECEMBER 31, 2016 AND 2015

(In thousands of reais)

9

Notes 2016 2015 20162015

Restated

Revenues - - 16,894,444 17,840,549

Sale of goods, products and services - - 16,179,697 17,000,708

Revenue related to the construction of own assets - - 931,804 993,029

Allowance/Reversal of allowance for doubtful accounts 30 - - (217,057) (153,188)

Inputs acquired from third parties (4,961) (4,414) (7,536,297) (8,683,757)

Cost of products, goods and services sold 31 - - (6,167,503) (7,160,923)

Materials, energy, outsourced services and others (4,961) (4,414) (1,368,794) (1,522,834)

Gross value added (4,961) (4,414) 9,358,147 9,156,792

Retentions - - (494,907) (459,401)

Depreciation and amortization 30 - - (494,907) (459,401)

Net value added produced (4,961) (4,414) 8,863,240 8,697,391

Value added received through transfer (299,892) 49,008 (188,896) 621,191

Equity in the earnings of subsidiaries 12 (300,892) 47,078 (336,429) (126,400)

Financial revenues 32 1,000 1,930 147,533 747,591

Total value added to distribute (304,853) 44,594 8,674,344 9,318,582

Distribution of value added (304,853) 44,594 8,674,344 9,318,582

Personnel 7,067 6,191 403,727 371,449

Direct remuneration 6,232 5,732 290,825 281,229

Benefits 261 309 65,909 61,270

Government Severance Fund for Employees (FGTS) 533 150 40,294 23,539

Other 41 - 6,699 5,411

Taxes, fees and contributions 608 609 7,552,438 7,199,286

Federal 608 609 3,600,552 3,505,237

State - - 3,935,841 3,683,047

Local - - 16,045 11,002

Value distributed to providers of capital 409 (42) 1,031,116 1,710,011

Interest 409 (42) 955,798 1,628,193

Rental - - 75,318 66,908

Other - - - 14,910

Value distributed to shareholders (312,937) 37,836 (312,937) 37,836

Dividends - 10,069 - 10,069

Retained earnings (accumulated losses) 27 (312,937) 27,767 (312,937) 27,767

The notes are an integral part of the financial statements.

ConsolidatedParent Company

FISCAL YEARS ENDED DECEMBER 31, 2016 AND 2015

STATEMENTS OF VALUE ADDED

LIGHT S.A.

(In thousands of reais)

10

In thousands of Brazilian reais – R$, unless stated otherwise

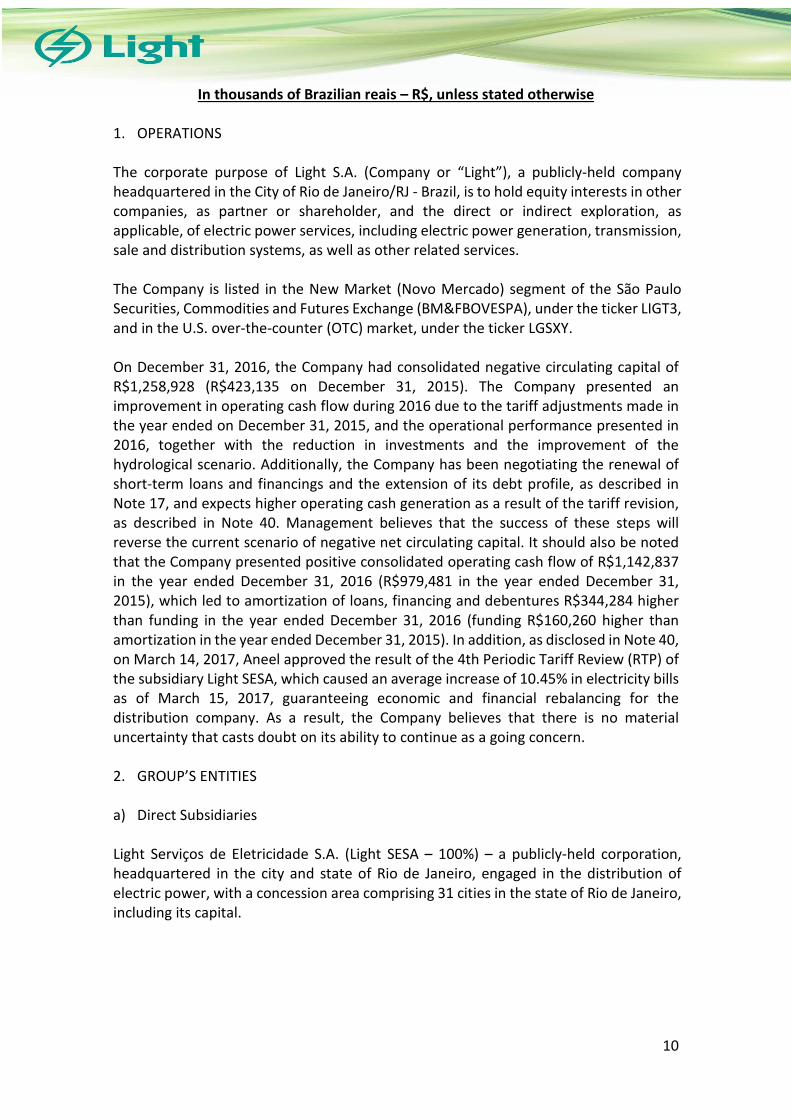

1. OPERATIONS The corporate purpose of Light S.A. (Company or “Light”), a publicly-held company headquartered in the City of Rio de Janeiro/RJ - Brazil, is to hold equity interests in other companies, as partner or shareholder, and the direct or indirect exploration, as applicable, of electric power services, including electric power generation, transmission, sale and distribution systems, as well as other related services. The Company is listed in the New Market (Novo Mercado) segment of the São Paulo Securities, Commodities and Futures Exchange (BM&FBOVESPA), under the ticker LIGT3, and in the U.S. over-the-counter (OTC) market, under the ticker LGSXY. On December 31, 2016, the Company had consolidated negative circulating capital of R$1,258,928 (R$423,135 on December 31, 2015). The Company presented an improvement in operating cash flow during 2016 due to the tariff adjustments made in the year ended on December 31, 2015, and the operational performance presented in 2016, together with the reduction in investments and the improvement of the hydrological scenario. Additionally, the Company has been negotiating the renewal of short-term loans and financings and the extension of its debt profile, as described in Note 17, and expects higher operating cash generation as a result of the tariff revision, as described in Note 40. Management believes that the success of these steps will reverse the current scenario of negative net circulating capital. It should also be noted that the Company presented positive consolidated operating cash flow of R$1,142,837 in the year ended December 31, 2016 (R$979,481 in the year ended December 31, 2015), which led to amortization of loans, financing and debentures R$344,284 higher than funding in the year ended December 31, 2016 (funding R$160,260 higher than amortization in the year ended December 31, 2015). In addition, as disclosed in Note 40, on March 14, 2017, Aneel approved the result of the 4th Periodic Tariff Review (RTP) of the subsidiary Light SESA, which caused an average increase of 10.45% in electricity bills as of March 15, 2017, guaranteeing economic and financial rebalancing for the distribution company. As a result, the Company believes that there is no material uncertainty that casts doubt on its ability to continue as a going concern. 2. GROUP’S ENTITIES a) Direct Subsidiaries

Light Serviços de Eletricidade S.A. (Light SESA – 100%) – a publicly-held corporation, headquartered in the city and state of Rio de Janeiro, engaged in the distribution of electric power, with a concession area comprising 31 cities in the state of Rio de Janeiro, including its capital.

11

Light Energia S.A. (Light Energia – 100%) – a publicly-held corporation, headquartered in the city and State of Rio de Janeiro, whose main activities are to (a) study, plan, construct, operate and explore systems of electric power generation, transmission, sales, and related services that have been legally granted or that may be granted or authorized to it or to companies in which it holds or may come to hold a controlling interest; (b) to hold interests in other companies as a partner, shareholder or quotaholder. It comprises the Pereira Passos, Nilo Peçanha, Ilha dos Pombos, Santa Branca and Fontes Novas plants, with a total installed capacity of 855 MW. Light Energia holds interest in the following subsidiaries and Jointly controlled entity:

• Central Eólica São Judas Tadeu Ltda. (São Judas Tadeu – 100%) - a company at the pre-operational stage whose main activity is the generation and sale of electric power through a wind power plant located in the state of Ceará, with 18 MW nominal power. On December 31, 2016, Management provisioned 100% of this investment because it did not expect future recoverability, considering the Company’s new strategic planning.

• Central Eólica Fontainha Ltda. (Fontainha – 100%) – a company at the pre-operational stage whose main activity is the generation and sale of electric power through a wind power plant located in the state of Ceará, with 16 MW nominal power. On December 31, 2016, Management provisioned 100% of this investment because it did not expect future recoverability, considering the Company’s new strategic planning.