Embed Size (px)

Citation preview

Merger Antitrust Law Fundamentals

Dale CollinsShearman & Sterling LLP April 18, 2013

Section 7 of the Clayton Act

•The FTC uses Section 7 as the antitrust standard to test acquisitions:

•Simple summary: Prohibits transactions that— may substantially lessen competition or tend to create a monopoly in any line of commerce (product market) in any part of the country (geographic market)

April 18, 2013 2

No person engaged in commerce or in any activity affecting commerce shall acquire, directly or indirectly, the whole or any part of the stock or other share capital and no person subject to the jurisdiction of the Federal Trade Commission shall acquire the whole or any part of the assets of another person engaged also in commerce or in any activity affecting commerce, where in any line of commerce or in any activity affecting commerce in any section of the country, the effect of such acquisition may be substantially to lessen competition, or to tend to create a monopoly.

What does all mean?

•The purpose of merger antitrust law is to prevent the creation or facilitation of market power to the harm to some identifiable group of customers in the market as a whole through—

Increased prices Decreased product or service quality Decreased rate of technological innovation or product improvement

•The deal’s likely effect on prices is key This is where the FTC is likely to focus almost all of its attention

April 18, 2013 3

If the FTC concludes that one of these bad effects—especially an increase in price—is likely occur as a result of the

transaction, they will challenge the deal

What does all mean?

•Threat of harm to customers Does not have to be to all customers Sufficient if some identifiable group of customers Some common groups

Customers in a particular geography Customers of a particular type of product Customers of a particular type of product in a particular geography

April 18, 2013 4

The FTC believes that no group is too small not to be protected

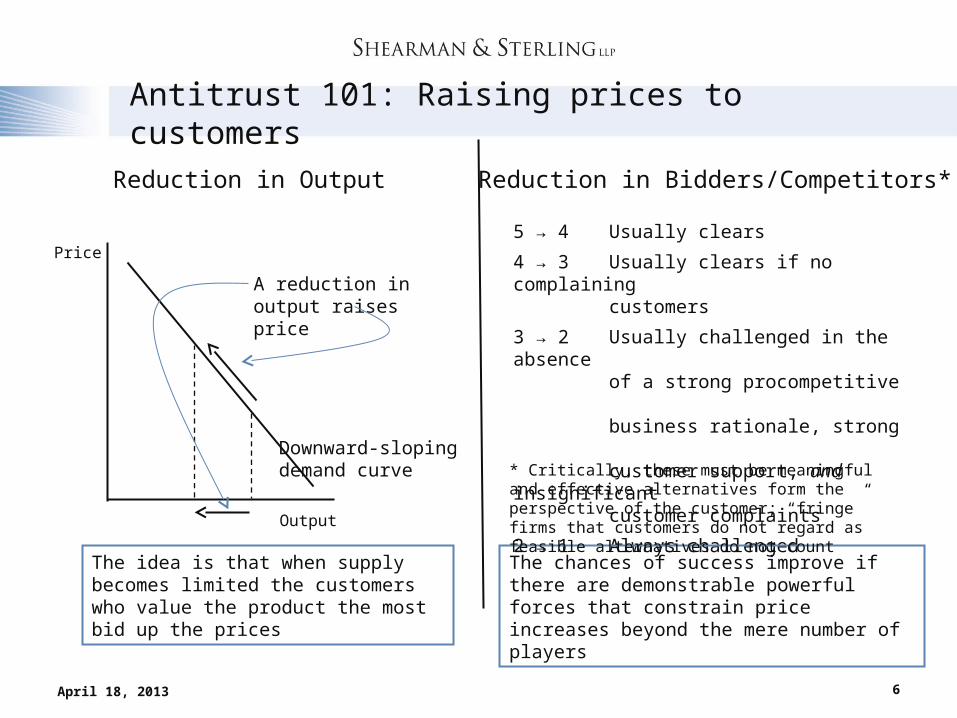

Antitrust 101: Raising prices to customers

•Five ways the FTC thinks a transaction can raise price:1. Eliminate competition between two uniquely close and intense

competitors (“unilateral effects”)2. Reduce significant output in the market—creating an artificial scarcity—

and so raise prices3. Reduce significant capacity in the market, reducing the incentive of

suppliers to aggressively chase business4. Reduce the number of bidders, resulting in higher bid prices5. Reduce the number of competitors, permitting the remaining firms to raise

their prices even without express coordination (“coordinated effects”)

April 18, 2013 5

Antitrust 101: Raising prices to customers

April 18, 2013 6

Price

Output

A reduction in output raises price

Reduction in Output Reduction in Bidders/Competitors*

5 → 4 Usually clears

4 → 3 Usually clears if no complaining customers

3 → 2 Usually challenged in the absence of a strong procompetitive business rationale, strong customer support, and insignificant customer complaints

2 → 1 Always challenged

The chances of success improve if there are demonstrable powerful forces that constrain price increases beyond the mere number of players

* Critically, these must be meaningful and effective alternatives form the perspective of the customer; “fringe” firms that customers do not regard as feasible alternatives do not count

The idea is that when supply becomes limited the customers who value the product the most bid up the prices

Downward-slopingdemand curve

Critical questions that the FTC staff are asking

•Do the parties have an increased ability to increase prices as a result of the merger?•Is output (or capacity) likely to decrease postmerger?•Are the merging companies strong and close competitors with one another?•How many other effective competitors does each merging party have?•Do customers play the merging parties off of one another to get better prices or other deal terms?•Is one of the merging party likely to enter into competition in the future with the other merging party in the absence of the transaction?•Is the rate of innovation or product improvement likely to decrease postmerger?

April 18, 2013 7

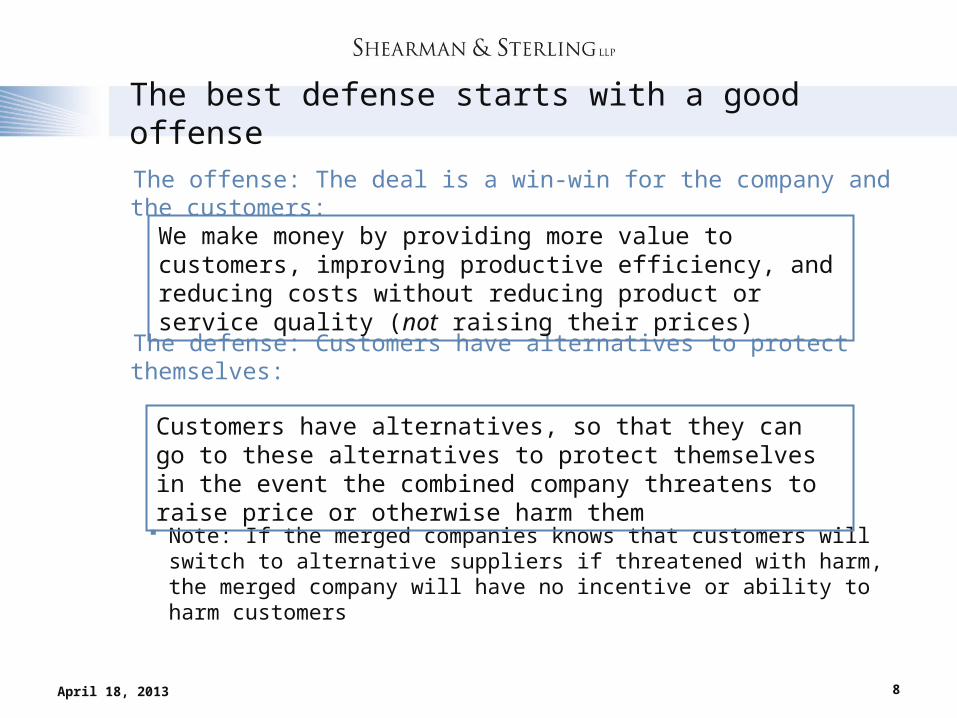

The best defense starts with a good offense

•The offense: The deal is a win-win for the company and the customers:

•The defense: Customers have alternatives to protect themselves:

Note: If the merged companies knows that customers will switch to alternative suppliers if threatened with harm, the merged company will have no incentive or ability to harm customers

April 18, 2013 8

We make money by providing more value to customers, improving productive efficiency, and reducing costs without reducing product or service quality (not raising their prices)

Customers have alternatives, so that they can go to these alternatives to protect themselves in the event the combined company threatens to raise price or otherwise harm them

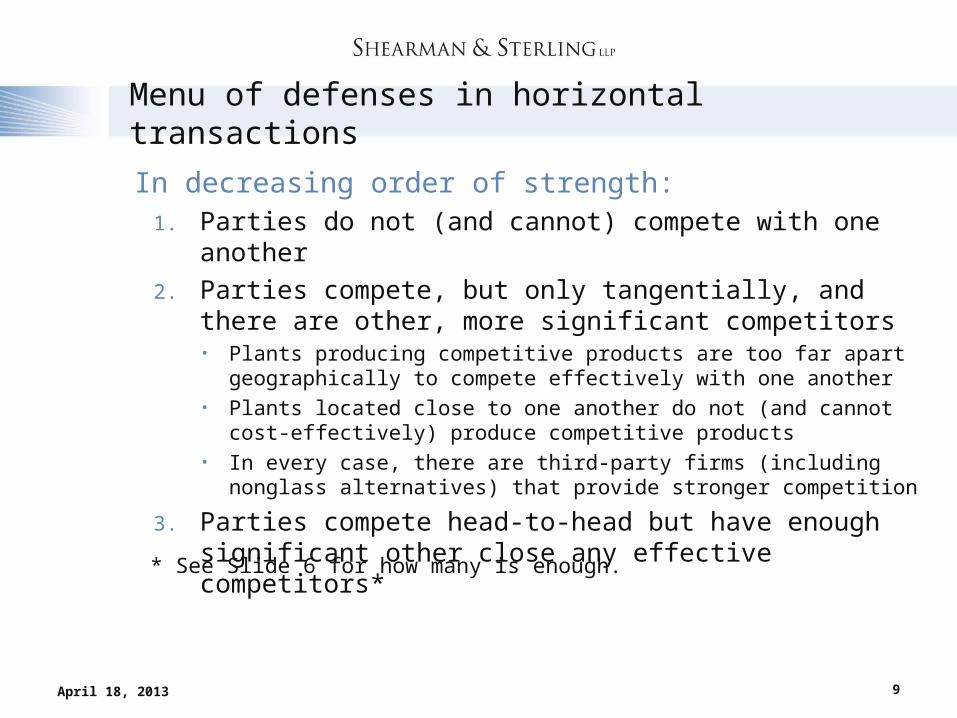

Menu of defenses in horizontal transactions

•In decreasing order of strength:1. Parties do not (and cannot) compete with one another 2. Parties compete, but only tangentially, and there are other, more

significant competitors• Plants producing competitive products are too far apart geographically to compete

effectively with one another• Plants located close to one another do not (and cannot cost-effectively) produce

competitive products• In every case, there are third-party firms (including nonglass alternatives) that provide

stronger competition

3. Parties compete head-to-head but have enough significant other close any effective competitors*

April 18, 2013 9

* See Slide 6 for how many is enough.

Menu of defenses in horizontal transactions

•A helpful fact: Powerful buyers BUT usually not a complete defense—what about smaller customers? AND the FTC insists on a carefully reasoned explanation of the mechanics

of how powerful buyers can protect themselves in bargaining with the combined company

•An unhelpful (but by no means fatal) fact: High barriers to entry

April 18, 2013 10

11

Assessing the defense—Exacerbating factors

•“Hot” company documents Suggest that a strategy of the merged firm will be to raise prices, reduce

production or capacity, or reduce the rate of innovation or product improvement

Suggest the merging companies are close competitors of one another in some overlapping product

Suggest that customers have few realistic alternatives to merging firm Suggest that the competitors pay attention to each other’s prices and are

careful not to destabilize high prices Suggest that the target company is a “maverick” that does not go along with

the higher prices that other companies want to charge

April 18, 2013

12

Assessing the defense—Exacerbating factors

•Customer complaints The merging companies are close competitors of one another in some

overlapping product Customer “plays” the companies off one another to get better prices Insufficient number of realistic alternatives to preserve price competition

post-merger Customer conclusion: Customer will pay higher prices as a result of the

merger

April 18, 2013

13

Synergies

•Types of synergies enabled by the deal Customer value-enhancing synergies

Make existing product better or cheaper, or Create new products or product improvement better, cheaper, or faster

Cost-saving synergies Reductions in duplicative costs Increases in the productive efficiency of the combined operation (e.g., through

best practices, transfer of more efficient production technology)•Synergies play two roles in an antitrust merger analysis

They provide an explanation why the acquiring firm is pursuing the deal (and probably paying a significant premium) that does not depend on price increases to customers

In close cases, large synergies can tip the FTC into not challenging the deal

April 18, 2013