Embed Size (px)

Citation preview

Merger & Acquisition

MANAGEMENTBUYOUT

113. Personal Computer Division of Distress Ltd., a computer hardwaremanufacturing company has started facing financial difficulties for the last2 to 3 years. The management of the division headed by Mr. Smith isinterested in a buyout on 1 April 2013. However, to make this buy-outsuccessful there is an urgent need to attract substantial funds from venturecapitalists.Ven Cap, a European venture capitalist firm has shown its interest tofinance the proposed buy-out. Distress Ltd. is interested to sell the division for `180 crore and Mr. Smith is of opinion that an additional amount of ` 85 croreshall be required to make this division viable. The expected financing patternshall be as follows:Source Mode Amount

(` crore)ManagementVenCap VC

Total

Equity Shares of ` 10 eachEquity Shares of ` 10 each9% Debentures with attached warrant of ` 100 each8% Loan

60.0022.5022.50

160.00

265.00

The warrants can be exercised any time after 4 years from now for 10 equityshares @ ` 120 per share.The loan is repayable in one go at the end of 8th year. The debentures arerepayable in equal annual installment consisting of both principal and interestamount over a period of 6 years.Mr. Smith is of view that the proposed dividend shall not be kept morethan 12.5% of distributable profit for the first 4 years. The forecasted EBITafter the proposed buyout is as follows:

Year 2013-14 2014-15 2015-16 2016-17EBIT (` crore) 48 57 68 82

Applicable tax rate is 35% and it is expected that it shall remain unchanged atleast for 5-6 years. In order to attract VenCap, Mr. Smith stated that book

Sanjay Saraf Educational Institute Pvt. Ltd. Page 1

Merger & Acquisition

value of equity shall increase by 20% during above 4 years. Although,VenCap has shown their interest in investment but are doubtful about theprojections of growth in the value as per projections of Mr. Smith. FurtherVenCap also demanded that warrants should be convertible in 18 sharesinstead of 10 as proposed by Mr. Smith.You are required to determine whether or not the book value of equity isexpected to grow by 20% per year. Further if you have been appointed by Mr.Smith as advisor then whether you would suggest to accept the demand ofVenCap of 18 shares instead of 10 or not.

Answer :

Working Notes

Calculation of Interest Payment on 9% DebenturesPVAF (9%,6) = 4.486

Annual Installment = 22.50 crore 5.0156 crore4.486

Year BalanceOutstanding

(` Crore)

Interest(` Crore)

Installment(` Crore)

PrincipalRepayment(` Crore)

Balance(` Crore)

1 22.5000 2.025 5.0156 2.9906 19.50942 19.5094 1.756 5.0156 3.2596 16.24983 16.2498 1.462 5.0156 3.5536 12.69624 12.6962 1.143 5.0156 3.8726 8.8236

Sanjay Saraf Educational Institute Pvt. Ltd. Page 2

Merger & Acquisition

Statement showing Value of EquityParticulars 2013-14

(` Crore)2014-15

(` Crore)2015-16

(` Crore)2016-17

( ` Crore)EBITInterest on 9% DebenturesInterest on 8% LoanEBTTax* @ 35%EATDividend @ 12.5% of EAT*

Balance b/fBalance c/fShare Capital

48.00002.0250

12.8000

57.00001.7560

12.8000

68.00001.4620

12.8000

82.00001.1430

12.8000

33.175011.6110

42.444014.8550

53.738018.8080

68.057023.8200

21.56402.6955

27.58903.4490

34.93004.3660

44.23705.5300

18.8685Nil

24.140018.8685

30.564043.0085

38.707073.5725

18.868582.5000

43.008582.5000

73.572582.5000

112.279582.5000

101.3685 125.5085 156.0725 194.7795

*Figures have been rounded off.In the beginning of 2013-14 equity was ` 82.5000 crore which has been grown to` 194.7795 over a period of 4 years. In such case the compounded growth rate shallbe as follows:(194.7795/82.5000)¼ - 1 = 23.96%This growth rate is slightly higher than 20% as projected by Mr. Smith.If the condition of VenCap for 18 shares is accepted the expected share holdingafter 4 years shall be as follows:

No. of shares held by ManagementNo. of shares held by VenCap at the starting stageNo. of shares held by VenCap after 4 yearsTotal holding

6.00 crore2.25 crore4.05 crore6.30 crore

Thus, it is likely that Mr. Smith may not accept this condition of VenCap as thismay result in losing their majority ownership and control to VenCap. Mr. Smithmay accept their condition if management has further opportunity to increasetheir ownership through other forms.

Sanjay Saraf Educational Institute Pvt. Ltd. Page 3

Merger & Acquisition

WEALTHREDISTRIBUTIONEFFECT

114. Simple Ltd. and Dimple Ltd. are planning to merge. The total value of thecompanies are dependent on the fluctuating business conditions. Thefollowing information is given for the total value (debt + equity) structure ofeach of the two companies.

Business Condition Probability Simple Ltd.` Lacs

Dimple Ltd.` Lacs

High GrowthMedium GrowthSlow Growth

0.200.600.20

820550410

1050825590

The current debt of Dimple Ltd. is ` 65 lacs and of Simple Ltd. is ` 460 lacs.Calculate the expected value of debt and equity separately for the merged entity.

Answer :

Compute Value of EquitySimple Ltd.

` in LacsHigh Growth Medium Growth Slow Growth

Debt + EquityLess: DebtEquity

820460

550460

410460

360 90 -50

Since the Company has limited liability the value of equity cannot be negativetherefore the value of equity under slow growth will be taken as zerobecause of insolvency risk and the value of debt is taken at 410 lacs. Theexpected value of debt and equity can then be calculated as:

Sanjay Saraf Educational Institute Pvt. Ltd. Page 4

Merger & Acquisition

Simple Ltd.` in Lacs

High Growth Medium Growth Slow Growth ExpectedValue

Prob. Value Prob. Value Prob. ValueDebt

Equity0.200.20

460360

0.600.60

46090

0.200.20

4100

450123

820 550 410 576

Dimple Ltd.` in Lacs

High Growth Medium Growth Slow Growth ExpectedValue

Prob. Value Prob. Value Prob. ValueEquityDebt

0.200.20

98565

0.600.60

76065

0.200.20

52565

78565

1050 825 590 823

Expected Values` in Lacs

Equity DebtSimple Ltd.Dimple Ltd.

126758

Simple Ltd.Dimple Ltd.

45065

884 515

Sanjay Saraf Educational Institute Pvt. Ltd. Page 5

Merger & Acquisition

BREAKEVENEXCHANGERATIO

115. C Ltd. & D Ltd. are contemplating a merger deal in which C Ltd. will acquireD Ltd. The relevant information about the firms are given as follows:

C Ltd. D Ltd.Total Earnings (E) (in millions) `96 `30Number of outstanding shares (S)(in millions)

20 14

Earnings per share (EPS) (`) 4.8 2.143Price earnings ratio (P/E) 8 7Market Price per share (P) (`) 38.4 15

i. What is the maximum exchange ratio acceptable to the shareholders of cLtd., if the P/E ratio of the combined firm is 7 ?

ii. What is the minimum exchange ratio acceptable to the shareholders of DLtd., if the P/E ratio of the combined firm is 9 ?

Answer :

i. Maximum exchange rate (α) that C can payPAB =PA(P/E)AB × EPSAB=PA

= 7 A B

A B

PAT PATN N

= 38.40

= 96 30 38 4020 14 7

.

Solving the above equation α = 0.21

ii. Minimum exchange rate (β) that D can acceptβPAB = Pβ

β[(P/E)AB × EPSAB ] = PB

= 9 15A B

A B

PAT PATN N

Solving the above equationβ = 0.32

Sanjay Saraf Educational Institute Pvt. Ltd. Page 6

Merger & Acquisition

CASHDEAL

116. The equity shares of XYZ Ltd. are currently being traded at ` 24 per share in themarket. XYZ Ltd. has total 10,00,000 equity shares outstanding in number; andpromoters' equity holding in the company is 40%.PQR Ltd. wishes to acquire XYZ Ltd. because of likely synergies. The estimatedpresent value of these synergies is ` 80,00,000.Further PQR feels that management of XYZ Ltd. has been over paid. With bettermotivation, lower salaries and fewer perks for the top management, will lead tosavings of ` 4,00,000 p.a. Top management with their families are promoters ofXYZ Ltd. Present value of these savings would add ` 30,00,000 in value to theacquisition.Following additional information is available regarding PQR Ltd.:

Earnings per shareTotal number of equity shares outstandingMarket price of equity share

: ` 4: 15,00,000

: ` 40

Required:(i) What is the maximum price per equity share which PQR Ltd. can

offer to pay for XYZ Ltd.(ii) What is the minimum price per equity share at which the management of

XYZ Ltd. will be willing to offer their controlling interest?

Answer :

(a) Calculation of maximum price per share at which PQR Ltd. can offer to payfor XYZ Ltd.’s share

Market Value (10,00,000 x ` 24)Synergy GainSaving of Overpayment

Maximum Price (` 3,50,00,000/10,00,000)

` 2,40,00,000` 80,00,000` 30,00,000` 3,50,00,000

` 35Alternatively, it can also be computed as follows:Let ER be the swap ratio then,

Sanjay Saraf Educational Institute Pvt. Ltd. Page 7

Merger & Acquisition

24 10,00,000 40 15,00,000 80,00,000 30,00,0004015,00,000 10,00,000 ER

ER = 0.875

40MP PE EPS ER 4 x 0.875 = 354

` `

(b)Calculation of minimum price per share at which the management of XYZLtd.’s will be willing to offer their controlling interest.

Value of XYZ Ltd.’s Management Holding(40% of 10,00,000 x ` 24)Add: PV of loss of remuneration to top management

No. of SharesMinimum Price (` 1,26,00,000/4,00,000)

` 96,00,000

` 30,00,000` 1,26,00,000

4,00,000` 31.50

STOCKDEAL

117. The CEO of a company thinks that shareholders always look for EPS. Thereforehe considers maximization of EPS as his company's objective. Hiscompany's current Net Profits are ` 80.00 lakhs and P/E multiple is 10.5. Hewants to buy another firm which has current income of ` 15.75 lakhs & P/Emultiple of 10.What is the maximum exchange ratio which the CEO should offer so that hecould keep EPS at the current level, given that the current market price ofboth the acquirer and the target company are ` 42 and ` 105 respectively?If the CEO borrows funds at 15% and buys out Target Company by payingcash, how much should he offer to maintain his EPS? Assume tax rate of 30%.

Sanjay Saraf Educational Institute Pvt. Ltd. Page 8

Merger & Acquisition

Answer :

(i)Acquirer Company Target Company

Net ProfitPE MultipleMarket CapitalizationMarket PriceNo. of SharesEPS

` 80 lakhs10.50

` 840 lakhs` 42

20 lakhs` 4

` 15.75 lakhs10.00

` 157.50 lakhs` 105

1.50 lakhs` 10.50

Maximum Exchange Ratio 4 : 10.50 or 1 : 2.625Thus, for every one share of Target Company 2.625 shares of AcquirerCompany.

(ii) Let x lakhs be the amount paid by Acquirer company to TargetCompany. Then to maintain same EPS i.e. ` 4 the number of shares to beissued will be: 80lakhs 15.75lakhs 0.70 15% X

420lakhs

95.75 0.105x 420

x = ` 150 lakhsThus, ` 150 lakhs shall be offered in cash to Target Company to maintainsame EPS.

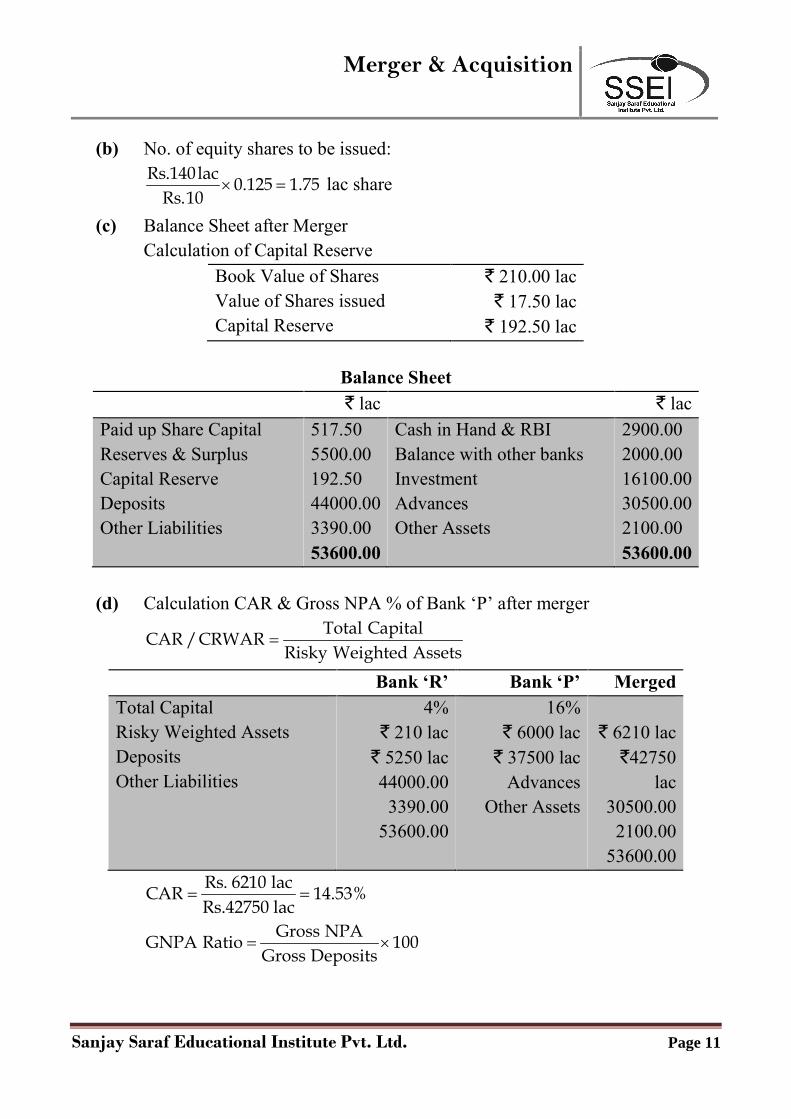

118. Bank 'R' was established in 2005 and doing banking in India. The bank is facingDO OR DIE situation. There are problems of Gross NPA (Non PerformingAssets) at 40% & CAR/CRAR (Capital Adequacy Ratio/ Capital RiskWeight Asset Ratio) at 4%. The net worth of the bank is not good. Shares arenot traded regularly. Last week, it was traded @` 8 per share.RBI Audit suggested that bank has either to liquidate or to merge with otherbank.Bank 'P' is professionally managed bank with low gross NPA of 5%.It has NetNPA as 0% and CAR at 16%. Its share is quoted in the market @ ` 128per share. The board of directors of bank 'P' has submitted a proposal to RBIfor take over of bank 'R' on the basis of share exchange ratio.

Sanjay Saraf Educational Institute Pvt. Ltd. Page 9

Merger & Acquisition

The Balance Sheet details of both the banks are as follows:Bank ‘R’

Amt. in ` lacsBank ‘P’

Amt. In ` lacsPaid up share capitalReserves & SurplusDepositsOther liabilitiesTotal Liabilities

14070

4,000890

5,100

5005,500

40,0002,500

48,500Cash in hand & with RBIBalance with other banksInvestmentsAdvancesOther AssetsTotal Assets

400-

1,1003,500

1005,100

2,5002,0001,100

27,0002,0005,100

It was decided to issue shares at Book Value of Bank 'P' to the shareholders ofBank 'R'. All assets and liabilities are to be taken over at Book Value.For the swap ratio, weights assigned to different parameters are as follows:

Gross NPACARMarket priceBook value

30%20%40%

Book value(a) What is the swap ratio based on above weights?(b) How many shares are to be issued?(c) Prepare Balance Sheet after merger.(d) Calculate CAR & Gross NPA % of Bank 'P' after merger.

Answer :

(a) Swap RatioGross NPA

CARMarket PriceBook Value

5 : 40 i.e.4 : 16 i.e.8 : 128 i.e.15 : 120 i.e

5/40 x 30% =4/16 x 20% =8/128 x 40% =15/120 x 10% =

0.03750.05000.0250.01250.125

Thus for every share of Bank ‘R’ 0.125 share of Bank ‘P’ shall be issued.

Sanjay Saraf Educational Institute Pvt. Ltd. Page 10

Merger & Acquisition

(b) No. of equity shares to be issued:Rs.140lac 0.125 1.75

Rs.10 lac share

(c) Balance Sheet after MergerCalculation of Capital Reserve

Book Value of SharesValue of Shares issuedCapital Reserve

` 210.00 lac` 17.50 lac` 192.50 lac

Balance Sheet` lac ` lac

Paid up Share CapitalReserves & SurplusCapital ReserveDepositsOther Liabilities

517.505500.00192.5044000.003390.0053600.00

Cash in Hand & RBIBalance with other banksInvestmentAdvancesOther Assets

2900.002000.0016100.0030500.002100.0053600.00

(d) Calculation CAR & Gross NPA % of Bank ‘P’ after mergerTotal CapitalCAR /CRWAR

Risky Weighted Assets

Bank ‘R’ Bank ‘P’ MergedTotal CapitalRisky Weighted AssetsDepositsOther Liabilities

4%` 210 lac` 5250 lac44000.00

3390.0053600.00

16%` 6000 lac` 37500 lac

AdvancesOther Assets

` 6210 lac`42750

lac30500.00

2100.0053600.00

Rs. 6210 lacCAR 14.53%Rs.42750 lac

Gross NPAGNPA Ratio 100Gross Deposits

Sanjay Saraf Educational Institute Pvt. Ltd. Page 11

Merger & Acquisition

GNPA (Given)

Gross NPA

0.40BGNPA0.40

Rs. 3500 lac

` 1400 lac

0.05sGNPA0.05

Rs. 27000 lac

` 1350 lac

` 6210 lac

` 2750 lac

119. The following information is provided relating to the acquiring company ELtd., and the target company H Ltd:

Particulars E Ltd.(`)

H Ltd.(`)

Number of shares (Face value ` 10 each)Market CapitalizationP/E Ratio (times)Reserves and surplus in `Promoter's Holding (No. of shares)

20 Lakhs1000 Lakhs

10.00600.00 Lakhs

9.50 Lakhs

15 Lakhs1500 Lakhs

5.00600.00 Lakhs10.00 Lakhs

The Board of Directors of both the companies have decided to give a fairdeal to the shareholders. Accordingly, the weights are decided as 40%, 25%and 35% respectively for earnings, book value and market price of share of eachcompany for swap ratio.

Calculate the following:(i) Market price per share, earnings per share and Book Value per share;(ii) Swap ratio;(iii) Promoter's holding percentage after acquisition;(iv) EPS of E Ltd. after acquisitions of H Ltd;(v) Expected market price per share and market capitalization of E Ltd.;

after acquisition, assuming P/E ratio of E Ltd. remains unchanged; and(vi) Free float market capitalization of the merged firm.

Sanjay Saraf Educational Institute Pvt. Ltd. Page 12

Merger & Acquisition

Answer :

1.(i)

E Ltd. H Ltd.Market capitalisationNo. of sharesMarket Price per shareP/E ratioEPSProfitShare capitalReserves and surplusTotalBook Value per share

1000 lakhs20 lakhs` 50

10` 5

` 100 lakh` 200 lakh` 600 lakh` 800 lakh

` 40

1500 lakhs15 lakhs` 100`5` 20

` 300 lakh` 150 lakh` 330 lakh` 480 lakh

` 32

(ii) Calculation of Swap RatioEPSBook valueMarket price

1 : 4 i.e.1 : 0.8 i.e1 : 2 i.e.

1.0× 40%0.8 × 25%2.0 × 35%Total

1.60.20.72.5

Swap ratio is for every one share of H Ltd., to issue 2.5 shares ofE Ltd. Hence, total no. of shares to be issued 15 lakh × 2.5 = 37.50 lakhshares

(iii) Promoter’s holding = 9.50 lakh shares + (10× 2.5 = 25 lakhshares) = 34.50 lakh i.e. Promoter’s holding % is (34.50 lakh/57.50lakh) × 100 = 60%.

(iv) Calculation of EPS after mergerTotal No. of shares 20 lakh + 37.50 lakh = 57.50 lakh

Total Profit 100 lakh 300lakh 400EPS 6.956No. of shares 57.50 lakh 57.50

`

(v) Calculation of Market price and Market capitalization after mergerExpected market priceMarket capitalization

EPS 6.956 × P/E 10 = ` 69.56= ` 69.56 per share ×57.50 lakh shares

= ` 3,999.70 lakh or ` 4,000 lakh

Sanjay Saraf Educational Institute Pvt. Ltd. Page 13

Merger & Acquisition

Free float of market capitalization = ` 69.56 per share × (57.50 lakh × 40%)= ` 1599.88 lakh

120. The following information relating to the acquiring Company AbhimanLtd. and the target Company Abhishek Ltd. are available. Both theCompanies are promoted by Multinational Company, Trident Ltd. Thepromoter’s holding is 50% and 60% respectively in Abhiman Ltd. and AbhishekLtd. :

Abhiman Ltd. Abhishek Ltd.Share Capital (`)Free Reserve and Surplus (`)Paid up Value per share (`)Free float Market Capitalisation (`)P/E Ratio (times)

200 lakh800 lakh

100400 lakh

10

100 lakh500 lakh

10128 lakh

4Trident Ltd. is interested to do justice to the shareholders of both theCompanies. For the swap ratio weights are assigned to different parameters bythe Board of Directors as follows:

Book Value 25%EPS (Earning per share) 50%Market Price 25%

(a) What is the swap ratio based on above weights?(b) What is the Book Value, EPS and expected Market price of Abhiman

Ltd. after acquisition of Abhishek Ltd. (assuming P.E. ratio of AbhimanLtd. remains unchanged and all assets and liabilities of Abhishek Ltd. aretaken over at book value).

(c) Calculate:(i) Promoter’s revised holding in the Abhiman Ltd.(ii) Free float market capitalization.(iii) Also calculate No. of Shares, Earning per Share (EPS) and Book

Value (B.V.), if after acquisition of Abhishek Ltd., Abhiman Ltd. decidedto :(a) Issue Bonus shares in the ratio of 1 : 2; and(b) Split the stock (share) as ` 5 each fully paid.

Sanjay Saraf Educational Institute Pvt. Ltd. Page 14

Merger & Acquisition

Answer :

(a) Swap RatioAbhiman Ltd. Abhishek Ltd.

Share CapitalFree ReservesTotalNo. of SharesBook Value per sharePromoter’s holdingNon promoter’s holdingFree Float Market Cap. i.e.relating to Public’s holdingHence Total market CapNo. of SharesMarket PriceP/E RatioEPSProfits (` 2 X 40 lakh)(` 8 X 10 lakh)

200 Lakh800 Lakh

1000 Lakh2 Lakh` 500

50%50%

400 Lakh

800 Lakh2 Lakh` 400

1040

` 80 lakh-

100 Lakh500 Lakh600 Lakh10 Lakh` 6060%40%

128 Lakh320 Lakh10 Lakh` 32

48-

` 80 lakh

Calculation of Swap RatioBook Value 1 : 0.12 i.e. 0.12 x 25% 0.03

EPS 1 : 0.2 0.20 x 50% 0.10Market Price 1 : 0.08 0.08 x 25% 0.02

Total 0.15Swap ratio is for every one share of Abhishek Ltd., to issue 0.15 shares ofAbhiman Ltd.Hence total no. of shares to be issued.10 Lakh x 0.15 = 1.50 lakh shares

(b) Book Value, EPS & Market PriceTotal No of Shares 2 Lakh + 1.5 Lakh = 3.5 LakhTotal Capital ` 200 Lakh + ` 150 Lakh = ` 350 LakhReserves ` 800 Lakh + ` 450 Lakh = ` 1,250 Lakh

Sanjay Saraf Educational Institute Pvt. Ltd. Page 15

Merger & Acquisition

Book Value 350 Lakh + 1,250 Lakh3.5 Lakh

` ` = ` 457.14 per

shareEPS Total Profit 80 Lakh 80 Lakh 160Lakh

No.of Share 3.5 Lakh 3.5 ` ` `

= ` 45.71Expected Market Price EPS (` 45.71) x P/E Ratio (10) = ` 457.10

(c)(1) Promoter’s holdingPromoter’s Revised Abhiman 50% i.e. 1.00 Lakh sharesHolding Abhishek 60% i.e. 0.90 Lakh shares

Total 1.90 Lakh sharesPromoter’s % = 1.90/3.50 x 100 = 54.29%

(2) Free Float Market CapitalisationFree Float Market = (3.5 Lakh – 1.9 Lakh) x ` 457.10Capitalisation = ` 731.36 Lakh

(3) (i) & (ii)Revised Capital ` 350 Lakh + ` 175 Lakh = ` 525 LakhNo. of shares before Split (F.V ` 100) 5.25 Lakh

No. of Shares after Split (F.V. ` 5 ) 5.25 × 20 = 105 Lakh

EPS 160 Lakh / 105 Lakh = 1.523Book Value Cap. ` 525 Lakh + ` 1075 Lakh

No. of Shares = 105 Lakh= ` 15.238 per share

121. XYZ Ltd. wants to purchase ABC Ltd. by exchanging 0.7 of its share foreach share of ABC Ltd. Relevant financial data are as follows:

Equity shares outstandingEPS (`)Market price per share (`)

10,00,00040

250

4,00,00028

160(i) Illustrate the impact of merger on EPS of both the companies.

Sanjay Saraf Educational Institute Pvt. Ltd. Page 16

Merger & Acquisition

(ii) The management of ABC Ltd. has quoted a share exchange ratio of 1:1for the merger. Assuming that P/E ratio of XYZ Ltd. will remainunchanged after the merger, what will be the gain from merger for ABCLtd.?

(iii) What will be the gain/loss to shareholders of XYZ Ltd.?(iv) Determine the maximum exchange ratio acceptable to shareholders of XYZ

Ltd.

Answer :

1. Working Notesa)

XYZ Ltd. ABC Ltd.Equity shares outstanding (Nos.)EPSProfitPE RatioMarket price per share

10,00,000` 40

` 400,00,0006.25` 250

4,00,000` 28

` 112,00,0005.71` 160

b) EPS after mergerNo. of shares to be issued (4,00,000 x 0.70)Exiting Equity shares outstandingEquity shares outstanding after mergerTotal Profit (` 400,00,000 + ` 112,00,000)EPS

2,80,00010,00,00012,80,000

` 512,00,000` 40

(i) Impact of merger on EPS of both the companiesXYZ Ltd. ABC Ltd.

EPS after MergerEPS before Merger

` 40` 40Nil

` 28` 28*

Nil* ` 40 x 0.70

Sanjay Saraf Educational Institute Pvt. Ltd. Page 17

Merger & Acquisition

(ii) Gain from the Merger if exchange ratio is 1: 1No. of shares to be issuedExiting Equity shares outstandingEquity shares outstanding after mergerTotal Profit (` 400,00,000 + ` 112,00,000)EPSMarket Price of Share (` 36.57 x 6.25)Market Price of Share before MergerImpact (Increase/ Gain)

4,00,00010,00,00014,00,000

` 512,00,000` 36.57` 228.56` 160.00` 68.56

(iii) Gain/ loss from the Merger to the shareholders of XYZ Ltd.Market Price of ShareMarket Price of Share before MergerLoss from the merger (per share)

` 228.56` 250.00` 21.44

(iv) Maximum Exchange Ratio acceptable to XYZ Ltd. shareholders` Lakhs

Market Value of Merged Entity (` 228.57 x 1400000)Less: Value acceptable to shareholders of XYZ Ltd.Value of merged entity available to shareholders of ABC Ltd.Market Price Per ShareNo. of shares to be issued to the shareholders of ABC Ltd. (lakhs)

3199.982500.00699.98

2502.80

Thus maximum ratio of issue shall be 2.80 : 4.00 or 0.70 share of XYZ Ltd. forone share of ABC Ltd.

122. Company X is contemplating the purchase of Company Y, Company X has3,00,000 shares having a market price of ` 30 per share, while Company Y has2,00,000 shares selling at ` 20 per share. The EPS are ` 4.00 and ` 2.25 forCompany X and Y respectively. Managements of both companies are discussingtwo alternative proposals for exchange of shares as indicated below:(i) in proportion to the relative earnings per share of two companies.(ii) 0.5 share of Company X for one share of Company Y (0.5:1).

Sanjay Saraf Educational Institute Pvt. Ltd. Page 18

Merger & Acquisition

You are required:(i) to calculate the Earnings Per share (EPS) after merger under two

alternatives; and(ii) to show the impact of EPS for the shareholders of two companies under both

the alternatives.

Answer :

Working Notes: Calculation of total earnings after mergerParticulars Company X Company Y TotalOutstanding shares 3,00,000 2,00,000EPS (`) 4 2.25Total earnings (`) 12,00,000 4,50,000 16,50,000

(i) (a) Calculation of EPS when exchange ratio is in proportion to relative EPS oftwo companies

Company X 3,00,000Company Y 2,00,000 x 2.25/4 1,12,500Total number of shares after merger 4,12,500

Company XEPS before mergerEPS after merger = ` 16,50,000/4,12,500 shares

= ` 4= ` 4

Company YEPS before mergerEPS after merger= EPS of Merged Entity after merger x Share Exchange ratio onEPS basis

2.254

`4

= ` 2.25

= ` 2.25

Sanjay Saraf Educational Institute Pvt. Ltd. Page 19

Merger & Acquisition

(b) Calculation of EPS when share exchange ratio is 0.5 : 1Total earnings after merger = ` 16,50,000Total number of shares after merger = 3,00,000 + (2,00,000 x 0.5)

= 4,00,000 shareEPS after merger = ` 16,50,000/4,00,000 = ` 4.125

(ii) Impact of merger on EPS for shareholders of Company X and Company Y(a) Impact on Shareholders of Company X

(`)EPS before mergerEPS after mergerIncrease in EPS

4.0004.1250.125

(b) Impact on Shareholders of Company Y(`)

Equivalent EPS before mergerEquivalent EPS after mergerDecrease in EPS

2.25002.06250.1875

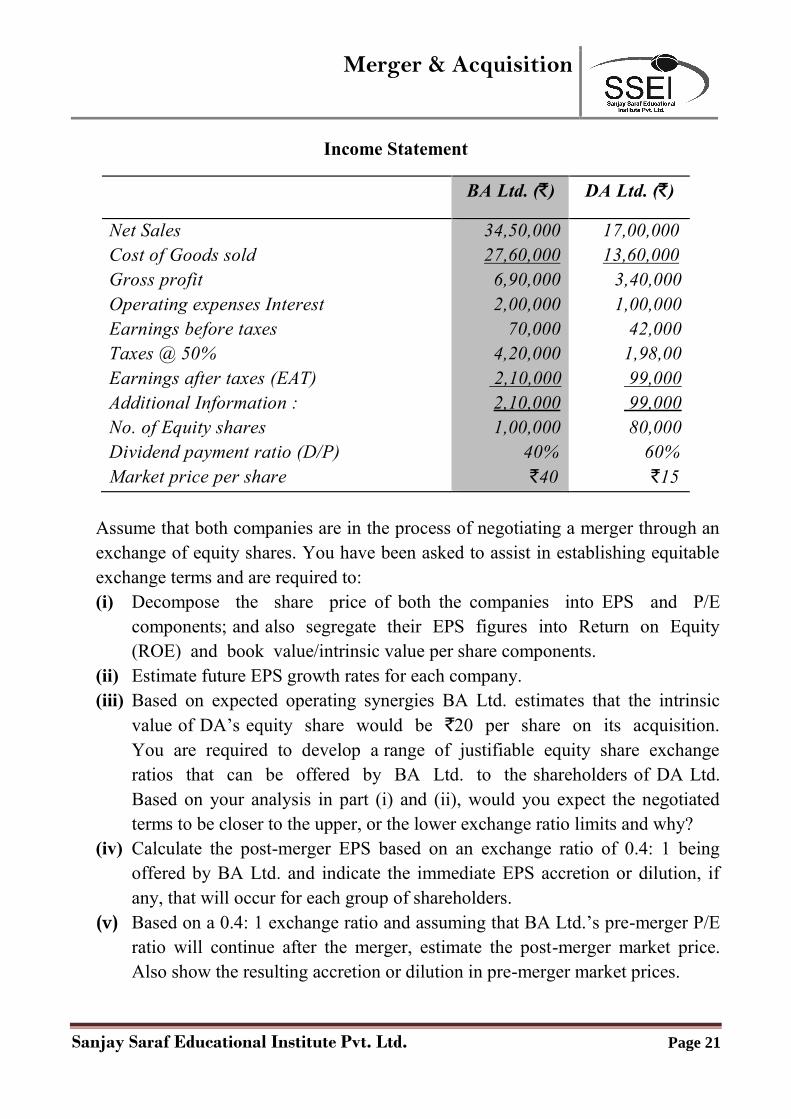

123. BA Ltd. and DA Ltd. both the companies operate in the same industry.The Financial statements of both the companies for the current financial year areas follows:

Balance SheetParticulars BA Ltd. (`) DA Ltd. (`)

Current AssetsFixed Assets (Net)

Total (`)Equity capital (`10 each)Retained earnings14% long-term debtCurrent liabilities

Total (`)

14,00,00010,00,00024,00,00010,00,0002,00,0005,00,0007,00,00024,00,000

10,00,000

5,00,00015,00,0008,00,000

--3,00,004,00,00015,00,000

Sanjay Saraf Educational Institute Pvt. Ltd. Page 20

Merger & Acquisition

Income Statement

BA Ltd. (`) DA Ltd. (`)

Net SalesCost of Goods soldGross profitOperating expenses InterestEarnings before taxesTaxes @ 50%Earnings after taxes (EAT)Additional Information :No. of Equity sharesDividend payment ratio (D/P)Market price per share

34,50,00027,60,0006,90,0002,00,00070,0004,20,0002,10,0002,10,0001,00,00040%`40

17,00,00013,60,0003,40,0001,00,00042,0001,98,0099,00099,00080,00060%`15

Assume that both companies are in the process of negotiating a merger through anexchange of equity shares. You have been asked to assist in establishing equitableexchange terms and are required to:(i) Decompose the share price of both the companies into EPS and P/E

components; and also segregate their EPS figures into Return on Equity(ROE) and book value/intrinsic value per share components.

(ii) Estimate future EPS growth rates for each company.(iii) Based on expected operating synergies BA Ltd. estimates that the intrinsic

value of DA’s equity share would be `20 per share on its acquisition.You are required to develop a range of justifiable equity share exchangeratios that can be offered by BA Ltd. to the shareholders of DA Ltd.Based on your analysis in part (i) and (ii), would you expect the negotiatedterms to be closer to the upper, or the lower exchange ratio limits and why?

(iv) Calculate the post-merger EPS based on an exchange ratio of 0.4: 1 beingoffered by BA Ltd. and indicate the immediate EPS accretion or dilution, ifany, that will occur for each group of shareholders.

(v) Based on a 0.4: 1 exchange ratio and assuming that BA Ltd.’s pre-merger P/Eratio will continue after the merger, estimate the post-merger market price.Also show the resulting accretion or dilution in pre-merger market prices.

Sanjay Saraf Educational Institute Pvt. Ltd. Page 21

Merger & Acquisition

Answer :

Market price per share (MPS) = EPS X P/E ratio or P/E ratio = MPS/EPS

(i) Determination of EPS, P/E ratio, ROE and BVPS of BA Ltd. and DA Ltd.BA Ltd. DA Ltd.

Earnings After TaxNo. of SharesEPSMarket price per shareP/E RatioEquity FundsBVPSROE

(EAT)(N)

(EAT/N)(MPS)

(MPS/EPS)(EF)

(EF/N)(EAT/EF) × 100

` 2,10,000100000` 2.10

4019.05

` 12,00,00012

17.50%

` 99,00080000` 1.2375

1512.12

` 8,00,00010

12.37%

(ii) Estimation of growth rates in EPS for BA Ltd. and DA Ltd.Retention Ratio (1-D/P ratio) 0.6 0.4Growth Rate (ROE × Retention Ratio) 10.50% 4.95%

(iii) Justifiable equity shares exchange ratioIntrinsic value basedMarket price based= MPSDA/MPSBA

= `20 / `40= `15 / ` 40

= 0.5:1 (upper limit)= 0.375:1

(lower limit)Since, BA Ltd. has a higher EPS, ROE, P/E ratio and even higher EPSgrowth expectations, the negotiable terms would be expected to be closerto the lower limit, based on the existing share prices.

(iv) Calculation of post merger EPS and its effectsParticulars BA Ltd. DA Ltd. CombinedEATShare outstandingEPSEPS Accretion (Dilution)

(`)

(`)(Re.)

(i)(ii)(i) /(ii)

2,10,000100000

2.10.241

99,000800001.2375

(0.301**)

3,09,000132000*

2.341

Sanjay Saraf Educational Institute Pvt. Ltd. Page 22

Merger & Acquisition

(v) Estimation of Post merger Market price and other effectsParticulars BA Ltd. DA Ltd. CombinedEPSP/E RatioMPSMPS Accretion

(`)

(`)(Re.)

(i)(ii)(i) /(ii)

2.119.05

404.6

1.237512.12

152.84***

2.34119.05

44.6

* Shares outstanding (combined) = 100000 shares + (.40 × 80000)= 132000shares

** EPS claim per old share = ` 2.34 × 0.4 ` 0.936EPS dilution = ` 1.2375 – ` 0.936 `

0.3015***S claim per old share (` 44.60 × 0.4) ` 17.84Less: MPS per old share ` 15.00

` 2.84

124. TK Ltd. and SK Ltd. are both in the same industry. The former is in negotiationfor acquisition of the latter. Information about the two companies as per theirlatest financial statements are given below :

TK Ltd. SK Ltd.` 10 Equity shares outstanding 24 Lakhs 12 LakhsDebt :10% Debentures (` Lakhs) 1160 -12.5% Institutional Loan ( ` Lakhs) - 480Earnings before interest, depreciation and tax(EBIDAT) (` Lakhs)

800.00 230.00

Market Price/Share (`) 220.00 110.00

TK Ltd. plans to offer a price for SK Ltd. business, as a whole, which will be 7times of EBIDAT as reduced by outstanding debt and to be discharged byown shares at market price.SK Ltd. is planning to seek one share in TK Ltd. for every 2 shares in SK Ltd.based on the market price. Tax rate for the two companies may be assumed as30%.Calculate and show the following under both alternatives - TK Ltd.'s offerand SK Ltd.'s plan :

Sanjay Saraf Educational Institute Pvt. Ltd. Page 23

Merger & Acquisition

i. Net consideration Payableii. No. of shares to be issued by TK Ltd.iii. EPS of TK Ltd. after acquisition.iv. Expected market price per share of TK Ltd. after acquisition.v. State briefly the advantages to TK Ltd. from the acquisition.Calculations may be rounded off to two decimals points.

Answer :

As per T Ltd.’s Offer` in lakhs

i. Net Consideration Payable7 times EBIDAT, i.e. 7 x ` 230 lakh 1610.00Less: Debt 480.00

1130.00ii. No. of shares to be issued by T Ltd` 1130 lakh/` 220 (rounded off) (Nos.) 5,13,636

iii.EPS of T Ltd after acquisitionTotal EBIDT (` 800 lakh + ` 230 lakh) 1030.00Less: Interest (` 116 lakh + ` 60 lakh) 176.00

854.00Less: 30% Tax 256.20Total earnings (NPAT) 597.80Total no. of shares outstanding (24 lakh + 5.14 lakh)EPS (` 597.80 lakh/ 29.14 lakh)

29.14 lakh` 20.51

iv. Expected Market Price:` in lakhs

Pre-acquisition P/E multiple:EBIDAT 800.00

Less: Interest 10100

116.00

684.00Less: 30% Tax 205.20

478.80

Sanjay Saraf Educational Institute Pvt. Ltd. Page 24

Merger & Acquisition

No. of shares (lakhs) 24EPS ` 19.95

Hence, PE multiple 22019 95.

11.03

Expected market price after acquisition (` 20.51 x 11.03) ` 226.23

As per E Ltd’s Plani. Net consideration payable 12 lakhs shares x ` 110 1320.00ii. No. of shares to be issued by T Ltd ` 1320 lakhs ÷ ` 220 6 lakhiii.EPS of T Ltd after Acquisition

NPAT (as per earlier calculations) 597.80Total no. of shares outstanding (24 lakhs + 6 lakhs) 30 lakhEarning Per Share (EPS) ` 597.80 lakh/30 lakh ` 19.93

iv. Expected Market Price (` 19.93 x 11.03) 219.83

v. Advantages of Acquisition to T LtdSince the two companies are in the same industry, the followingadvantages could accrue:- Synergy, cost reduction and operating efficiency.- Better market share.- Avoidance of competition.

VALUATION SUMSONMERGER

125. MK Ltd. is considering acquiring NN Ltd. The following information isavailable:

Company Earning afterTax (`)

No. of EquityShares

Market ValuePer Share (`)

MK Ltd.NN Ltd.

60,00,00018,00,000

12,00,0003,00,000

200.00160.00

Exchange of equity shares for acquisition is based on current market value asabove. There is no synergy advantage available.

Sanjay Saraf Educational Institute Pvt. Ltd. Page 25

Merger & Acquisition

(i) Find the earning per share for company MK Ltd. after merger, and(ii) Find the exchange ratio so that shareholders of NN Ltd. would not be at a

loss.

Answer :

(i) Earning per share of company MK Ltd after merger:-Exchange ratio 160 : 200 = 4 : 5.that is 4 shares of MK Ltd. for every 5 shares of NN Ltd.∴ Total number of shares to be issued = 4/5 × 3,00,000 = 2,40,000 Shares.∴Total number of shares of MK Ltd. and NN Ltd.=12,00,000 (MKLtd.)+2,40,000 (NN Ltd.)= 14,40,000 Shares

Total profit after tax = ` 60,00,000= ` 18,00,000= ` 78,00,000

MK Ltd.NN Ltd.∴ EPS. (Earning Per Share) of MK Ltd. after merger

` 78,00,000/14,40,000 = ` 5.42 per share(ii)To find the exchange ratio so that shareholders of NN Ltd. would not be at a

Loss:Present earning per share for company MK Ltd.= ` 60,00,000/12,00,000 = ` 5.00Present earning per share for company NN Ltd.= ` 18,00,000/3,00,000 = ` 6.00∴ Exchange ratio should be 6 shares of MK Ltd. for every 5 shares of NN Ltd.∴ Shares to be issued to NN Ltd. = 3,00,000 × 6/5 = 3,60,000 sharesNow, total No. of shares of MK Ltd. and NN Ltd. =12,00,000 (MKLtd.)+3,60,000 (NN Ltd.)= 15,60,000 shares∴ EPS after merger = ` 78,00,000/15,60,000 = ` 5.00 per shareTotal earnings available to shareholders of NN Ltd. after merger= 3,60,000 shares × ` 5.00 = ` 18,00,000This is equal to earnings prior merger for NN Ltd.∴ Exchange ratio on the basis of earnings per share is recommended.

Sanjay Saraf Educational Institute Pvt. Ltd. Page 26

Merger & Acquisition

126. The following information is relating to Fortune India Ltd. having twodivision, viz. Pharma Division and Fast Moving Consumer Goods Division(FMCG Division). Paid up share capital of Fortune India Ltd. is consisting of3,000 Lakhs equity shares of Re. 1 each. Fortune India Ltd. decided to de-merge Pharma Division as Fortune Pharma Ltd. w.e.f. 1.4.2009. Details ofFortune India Ltd. as on 31.3.2009 and of Fortune Pharma Ltd. as on1.4.2009 are given below:

Particulars Fortune PharmaLtd.`

Fortune India Ltd.`

Outside LiabilitiesSecured LoansUnsecured LoansCurrent Liabilities & ProvisionsAssetsFixed AssetsInvestmentsCurrent AssetsLoans & AdvancesDeferred tax/Misc. Expenses

400 lakh2,400 lakh1,300 lakh

7,740 lakh7,600 lakh8,800 lakh

900 lakh60 lakh

3,000 lakh800 lakh

21,200 lakh

20,400 lakh7,600 lakh

30,200 lakh7,300 lakh(200) lakh

Board of Directors of the Company have decided to issue necessary equityshares of Fortune Pharma Ltd. of Re. 1 each, without any consideration to theshareholders of Fortune India Ltd. For that purpose following points are to beconsidered:1. Transfer of Liabilities & Assets at Book value.2. Estimated Profit for the year 2009-10 is ` 11,400 Lakh for Fortune India

Ltd. & ` 1,470 lakhs for Fortune Pharma Ltd.3. Estimated Market Price of Fortune Pharma Ltd. is ` 24.50 per share.4. Average P/E Ratio of FMCG sector is 42 & Pharma sector is 25, which is to

be expected for both the companies.

Sanjay Saraf Educational Institute Pvt. Ltd. Page 27

Merger & Acquisition

Calculate:1. The Ratio in which shares of Fortune Pharma are to be issued to the

shareholders of Fortune India Ltd2. Expected Market price of Fortune India (FMCG) Ltd.3. Book Value per share of both the Companies immediately after Demerger.

Share holders’ funds(` Lakhs)

Particulars Fortune IndiaLtd.

FortunePharma Ltd.

Fortune India(FMCG) Ltd.

AssetsOutside liabilitiesNet worth

70,00025,00045,000

25,1004,10021,000

44,90020,90024,000

1. Calculation of Shares of Fortune Pharma Ltd. to be issued toshareholders of Fortune India Ltd.

Fortune PharmaLtd.

Estimated Profit (` in lakhs)Estimated market price (`)Estimated P/EEstimated EPS (`)No. of shares lakhs

1,47024.525

0.981,500

Hence, Ratio is 1 share of Fortune Pharma Ltd. for 2 shares of Fortune IndiaLtd.OR 0.50 share of Fortune Pharma Ltd. for 1 share of Fortune India Ltd.

2. Expected market price of Fortune India (FMCG) Ltd.Fortune India (FMCG) Ltd.

Estimated Profit (` in lakhs) 11,400No. of equity shares (` in lakhs) 3,000Estimated EPS (`) 3.8Estimated P/E 42Estimated market price (`) 159.60

Answer :

Sanjay Saraf Educational Institute Pvt. Ltd. Page 28

Merger & Acquisition

3. Book value per shareFortune Pharma

Ltd.Fortune India(FMCG) Ltd.

Net worth (`in lakhs) 21,000 24,000No. of shares (` in lakhs) 1,500 3,000Book value of shares ` 14 ` 8

Sanjay Saraf Educational Institute Pvt. Ltd. Page 29