Embed Size (px)

Citation preview

No. 105 February 2012

MERCATUS CENTER AT GEORGE MASON UNIVERSITY

MERCATUSON POLICY

The Deduction of State and Local Taxes from Federal Income Taxes

by Jeremy Horpedahl and Harrison Searles

Taxpayers who itemize theirdeductionsareallowedtodeductstateandlocaltaxesfromtheirfederaltaxableincome.Thisdeductionislimitedtoeitherincomeorsalestaxes,butnotboth.Personalprop-

ertytaxes,suchaslocaltaxesonhousingandrealestate,canalsobededucted.Themainbenefitofthisdeductionistoprovidesometaxrelieftotaxpayerslivinginstateswithhighertaxes,sincetheyhavelessdisposableincome.However,thisbenefitalsopointstothemaincostofthededuction:itsubsidizeshighertaxesandspendingatthelocallevel,sincetaxpay-ersinthosestateswillnotfeelthefullburdenofthetaxes.Instead,theburdenofthesetaxesisinsomesense“exported”totaxpayersinotherstates,sincefederaltaxratesmustbehigherthanotherwisetofundthesameleveloffederalspending.

WhendiscussingtaxationintheUnitedStates,itisimportanttoconsideralllevelsoftaxationratherthanjustfocusingononeatatime,suchasfederalincometaxes,becausethesetaxlevelsaffecteachother.Onewayinwhichthesetaxesinteractisfoundinthefed-eralincometaxcode,wherebytaxpayerswhoitem-izedeductionsareabletodeductavarietyofstateandlocaltaxeswhencalculatingtaxableincome.Inmostyearsitisoneofthefivelargesttaxexpendituresintheindividualincometax,anditisthusoneofthelargest“taxexpenditures”asdefinedbygovernmentagen-cies,suchastheOfficeofManagementandBudget.1OMBestimatesthatinfiscalyear2012,thisdeduc-tionreducedfederaltaxrevenuebyabout$45billion,andthisamountwillroughlydoubleoverthenextfiveyears.Asaresult,thisdeductionhashadalargeimpactupontheoveralltaxsystemofthenationatalllevelsofgovernment,whichwarrantsfurtheranalysisofitsoveralldesirability.

2 MERCATUS ON POLICY MARCH 2014

TWO CONCERNS FOR EQUITY

Thedistributionofthebenefitsofthistaxexpenditure,aswellasthecostsofremovingit,canbethoughtofintwoways.First,thereisthequestionofwhichtaxpay-erswithinthedistributionofincomebenefitthemost.AccordingtoestimatesbytheJointCommitteeonTaxa-tionfor2012,almost95percentofthebenefitsofthisdeductiongothoseearningover$75,000peryear,andoverhalf(55percent)ofthebenefitsareforthoseearn-ingover$200,000.Theaveragedeductionforthoseintheover$200,000incomegroupisover$5,000,whileitisonlyabout$250forthoseinthe$50,000to$75,000group(aroundthenationalmedian).2Theseaveragesonlyincludethosetaxpayersthatclaimedthededuc-tion,whichisonly27percentofalltaxpayerssincemostdonotitemizetheirdeductions.

Second,thereisthedistributionofbenefitsacrossthe50states,basedonhowhightaxesareineachstate.States

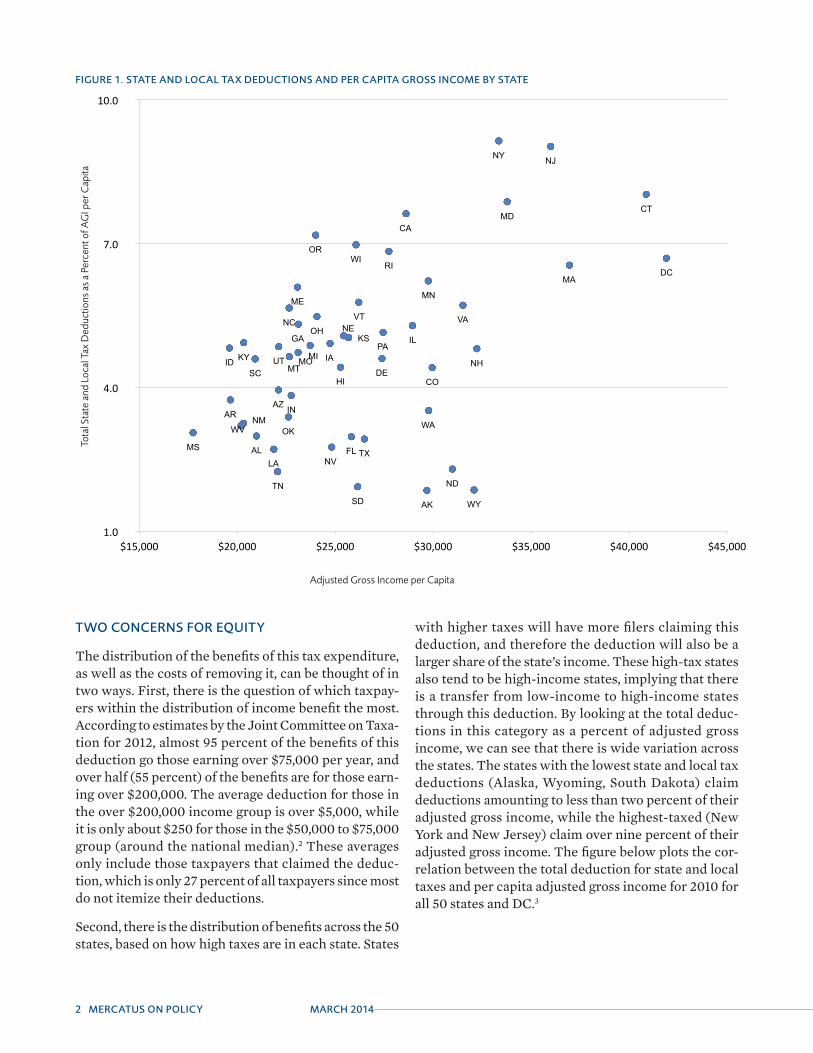

withhighertaxeswillhavemorefilersclaimingthisdeduction,andthereforethedeductionwillalsobealargershareofthestate’sincome.Thesehigh-taxstatesalsotendtobehigh-incomestates,implyingthatthereisatransferfromlow-incometohigh-incomestatesthroughthisdeduction.Bylookingatthetotaldeduc-tionsinthiscategoryasapercentofadjustedgrossincome,wecanseethatthereiswidevariationacrossthestates.Thestateswiththeloweststateandlocaltaxdeductions(Alaska,Wyoming,SouthDakota)claimdeductionsamountingtolessthantwopercentoftheiradjustedgrossincome,whilethehighest-taxed (NewYorkandNewJersey)claimoverninepercentoftheiradjustedgrossincome.Thefigurebelowplotsthecor-relationbetweenthetotaldeductionforstateandlocaltaxesandpercapitaadjustedgrossincomefor2010forall50statesandDC.3

FIGURE 1. STATE AND LOCAL TAX DEDUCTIONS AND PER CAPITA GROSS INCOME BY STATE

AK

AL

AR AZ

CA

CO

CT

DC

DE

FL

GA

HI

IA ID

IL

IN

KS

KY

LA

MA

MD

ME

MI

MN

MO

MS

MT

NC

ND

NE

NH

NJ

NM

NV

NY

OH

OK

OR

PA

RI

SC

SD

TN

TX

UT

VA VT

WA

WI

WV

WY

1.0

4.0

7.0

10.0

$15,000 $20,000 $25,000 $30,000 $35,000 $40,000 $45,000

Adjusted Gross Income per Capita

Tota

l Sta

te a

nd L

ocal

Tax

Ded

uctio

ns a

s a

Perc

ent o

f AG

I per

Cap

ita

MERCATUS CENTER AT GEORGE MASON UNIVERSITY 3

REDISTRIBUTION OR OFFSET FOR HIGHER TAXES?

Duringthe1985taxdebate,NYUlawprofessorsBrookesBillmanandNoelCunninghamofferedaneconomicjus-tificationforthededuction:stateandlocaltaxesreduceanindividual’sincomeandabilitytopayfederaltaxes,whichshouldthenbeconsideredbythefederaltaxcode.4Afterall,iffederaltaxesshouldbebasedonanindivid-ual’sabilitytopay,thenlocaltaxescouldreasonablybeconsideredasreducingone’sabilitytopayfederaltaxes.

EconomistBruceBartletttookacontrarypositiontoBillmanandCunningham,arguingthatthisdeductionisasubsidytohigh-taxstatesfromlow-taxstates,andhigh-taxstatestendtohavehigherpercapitaincomes.Healsofoundthat,ingeneral,thedeductionisasso-ciatedwithhigherstateandlocaltaxesbecausethefederalgovernmentispayingaportionofthesetaxes,withmostestimatessuggestingstateandlocaltaxesareabout13to14percenthigher.5Inthiscase,moreservicesmaybeprovidedpublicly,evenifitismoreefficienttoprovidethemprivately.Thisdeductionalsoinfluencesthetypesoftaxesthatstateandlocalgovernmentsuse,biasingthemtowardchoosingtaxesthataredeductibleratherthanthosethataremostefficient.6Morerecentestimatesconfirmthatstateandlocalspending“couldfallintheabsenceofdeductibility,”indicatingthatthedeductiondoesindeedincreasegovernmentspending.7

Furthermore,theability-to-payreasoningofBillmanandCunninghamoverlookswherestateandlocaltaxesgo,sincetaxesarenotonlycollected,butspent.Unlessoneviewsallgovernmentspendingascompletewaste,itisareasonableassumptionthatthelocaltaxesareprovidingsomeservicestothosethatpaythem(thoughlikelynotequaltothefullvalueoftaxespaidinmanycases).Thus,localtaxesdon’treduceanindividual’swillingnesstopaybythefullamountofthetax,orpos-siblyevenatall.Thelocaltaxesanindividualpaysarereturnedtotheindividualaslocalgovernmentservices,minusthecostsandwastesassociatedwithgovernmentprovisionofservices.

Forexample,incitieswheregarbagecollectionispro-videdbythelocalgovernment,thepropertyorsalestaxesthatfundthisservicearedeductible.Forcitieswheregarbagecollectionisprovidedprivately,thefeespaidtothegarbagecompanyarenottaxdeductible.Butfromaneconomicperspective,thesetwosituationsareidenticalandshouldbetreatedthesameinthetaxcode.Thecurrenttaxcodegivespreferencetocity-providedgarbage collection, which potentially violates both

equityandefficiency.Thetaxcodealsobiasesmunici-palitiestowardsprovidingservices,suchasgarbagecol-lection,eventhoughitmaybemoreefficientfortheseservicestobeprovidedprivately.

TAX RATES AND MACROECONOMIC EFFECTS

Eliminatingthedeductionforstateandlocaltaxeswilllikely lead to increasedmacroeconomicactivitybyremovingtheeconomicdistortionslistedabove.Itwillalsopotentiallyleadtomorefederaltaxrevenue,thoughthisdependsonhowindividualsreacttowhatwouldbe,ineffect,ataxincrease.Abetterpolicywouldbetosimultaneouslydecreasetaxratesatthesametimethatthisdeductioniseliminated,generatingadditionaleco-nomicactivitywithoutincreasingtheamountofrev-enueconcentratedatthefederalgovernment.

Estimatingtheeconomicandtax-revenueeffectsisadifficultmatter.TworecentstudiesbytheTaxFoun-dationattempttoexaminetheeffectsofremovingthedeductionforstateandlocalincome,sales,andpropertytaxes.Theseestimatesshouldnotbetakenasdefinitivepointestimates,butasindicativeofthedirectionoftheeffects.Forthestateandlocalincomeandsalestaxdeduction,theyestimatethateliminatingthedeductioncombinedwithanacross-the-boardcutinindividualincometaxratesby5.8percent(i.e.,the10percentratewoulddropto9.42percent)wouldresultinanincreaseintotalemploymentbyaround300,000jobs.8Theyfoundsimilareffectsforthepropertytaxdeduction,thoughthiswouldalsorequireadecreaseinbusinesspropertytaxesbecause“capital(evenowner-occupiedhousing)isquitesensitivetotaxes.”9

CONCLUSION

Removingthefederaltaxdeductionforstateandlocaltaxeswouldmaketaxesmoreequitablethroughoutthenation,asbothhigh-taxandlow-taxstatesaretreatedequallybythefederalgovernment.Itmayalsopro-videanefficiencyboostforstatesandlocalities,astheyabandonsomeservicesthatcouldbebetterprovidedbyprivatecompanies.Theremovalofthisdeductionwouldalsoallowfederalmarginaltaxratestobecutacrosstheboard,providingasecondaryboosttotheeconomywhilestillremainingrevenue-neutralatthefederallevel.

4 MERCATUS ON POLICY MARCH 2014

Jeremy Horpedahl is an assistant professor of economics at Buena Vista University in Storm Lake, Iowa. He received his PhD in economics from George Mason University in 2009. He has published articles in the Atlantic Economic Journal, Constitutional Politi-cal Economy, Public Finance and Management, and Defence and Peace Economics. Prior to entering academia, he was a senior economic analyst with the South Dakota Department of Labor, working on the unemployment statistics program.

Harrison Searles is an MA student in the department of economics at George Mason University

The Mercatus Center at George Mason University is the world’s premier university source for market-oriented ideas—bridging the gap between academic ideas and real-world problems. A university-based research center, Mercatus advances knowledge about how markets work to improve people’s lives by training graduate students, conducting research, and applying economics to offer solutions to society’s most pressing problems.

Our mission is to generate knowledge and under-standing of the institutions that affect the freedom to prosper and to find sustainable solutions that overcome the barriers preventing individuals from living free, prosperous, and peaceful lives. Founded in 1980, the Mercatus Center is located on George Mason University’s Arlington campus.

NOTES

1. For a discussion of the largest individual and corporate tax expendi-tures, see Jeremy Horpedahl and Brandon Pizzola, “A Trillion Little Subsidies: The Economic Impact of Tax Expenditures in the Federal Income Tax Code” (Mercatus Research, Mercatus Center at George Mason University, Arlington, VA, October 25, 2012).

2. See Table 3 of Joint Committee on Taxation, Estimates of Federal Tax Expenditures for Fiscal Years 2012–2017 (Washington, DC, February 1, 2013), JCS-1-13. The JCT estimates do not provide any further details on the about $200,000 group, but due to AMT and phase-outs of deductions, it is likely that the benefits are not flowing to taxpayers with extremely high incomes.

3. Deduction totals include property taxes and either income or sales taxes. Tax data from Internal Revenue Service, SOI Tax Stats—His-torical Table 2, updated April 23, 2013, http://www.irs.gov/uac /SOI-Tax-Stats---Historic-Table-2.

4. Brookes D. Billman Jr. and Noel B. Cunningham, “Nonbusiness State and Local Taxes: The Case for Deductibility,” Tax Notes 28 (Septem-ber 2, 1985): 1105–1120.

5. Bruce Bartlett, “The Case for Eliminating Deductibility of State and Local Taxes,” Tax Notes 28 (September 2, 1985): 1121–25.

6. Martin Feldstein and Gilbert Metcalf, “The Effect of Federal Tax Deductibility on State and Local Taxes and Spending,” Journal of Political Economy (1987): 710–36.

7. Gilbert Metcalf, “Assessing the Federal Deduction for State and Local Tax Payments,” National Tax Journal 64 (June 2011): 565–590.

8. Michael Schuyler and Stephen J. Entin, “Case Study #4: The Deduc-tion of State and Local Income Taxes or General Sales Taxes,” Tax Foundation Fiscal Fact, no. 382 (August 2013).

9. Stephen J. Entin and Michael Schuyler, “Case Study #2: Property Tax Deduction for Owner-Occupied Housing,” Tax Foundation Fiscal Fact, no. 380 (July 2013).