Embed Size (px)

Citation preview

2

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

MELBOURNE MINING CLUB

LUNCHEON SERIESThe Copper Industry and Codelco:

Opportunities and Challenges

Diego Hernández C.

CEO

August 4th, 2011

3

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

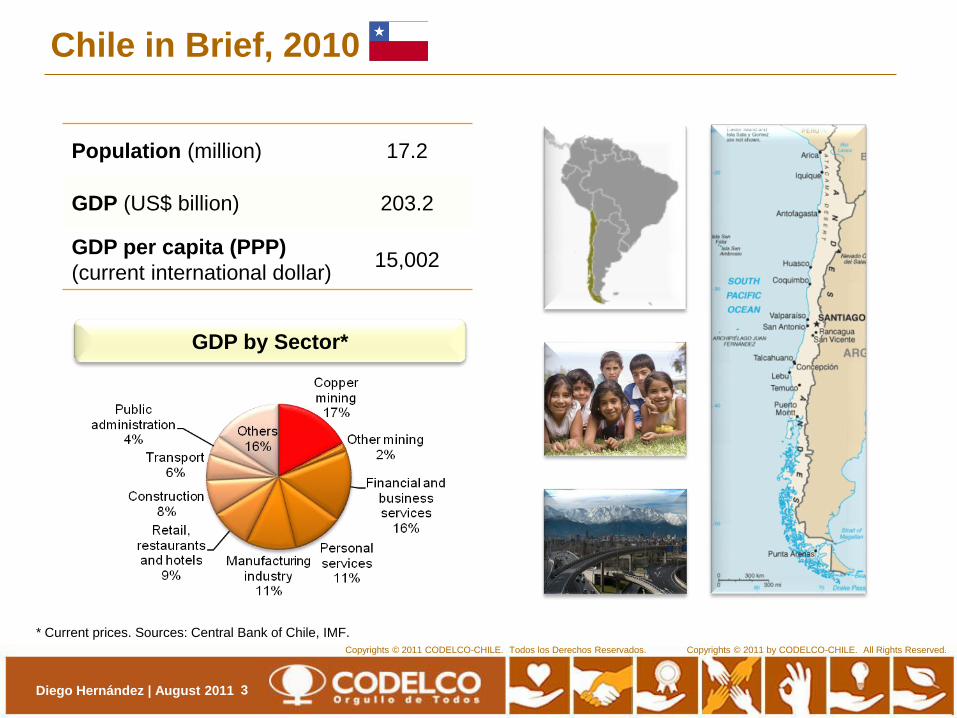

Chile in Brief, 2010

Population (million) 17.2

GDP (US$ billion) 203.2

GDP per capita (PPP)

(current international dollar)15,002

GDP by Sector*

* Current prices. Sources: Central Bank of Chile, IMF.

Diego Hernández | August 2011

4

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

Chile: An Attractive Mining District Selected Products

Selected Products

(Tonnes)

2010

Production

Global

Position

Share in

Global

Production

Share in

Global

Reserves

Metal Mining

Copper 5,349,099 1st 34% 30%

Molybdenum 37,186 3rd 16% 13%

Rhenium 25.0 1st 52% 52%

Silver 1,276 7th 6% n/a

Gold 38.4 18th 2% 4%

Industrial Minerals

Natural Nitrates 1,058,712 1st 100% 100%

Lithium Carbonate 8,800 1st 35% 58%

Iodine 18,000 1st 62% 60%

Diego Hernández | August 2011

5

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

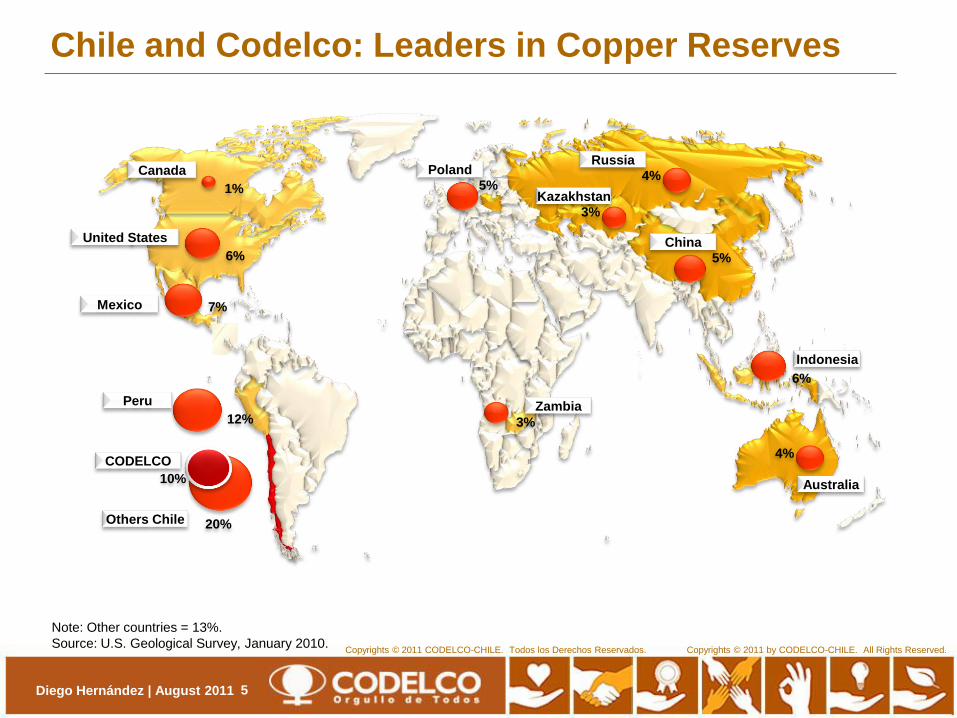

Chile and Codelco: Leaders in Copper Reserves

Note: Other countries = 13%.

Source: U.S. Geological Survey, January 2010.

1%

Canada

United States

6%

Mexico 7%

12%

Peru

20%Others Chile

CODELCO

5%Poland 4%

Russia

3%

Kazakhstan

5%

China

3%

4%

6%

Indonesia

Australia

Zambia

10%

Diego Hernández | August 2011

6

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

Codelco: Operations and Global Commercial Presence*

* Commercial subsidiaries.

Diego Hernández | August 2011

Chuquicamata

Copper

Division

New York - USA

Codelco Group Inc.Düsseldorf - Germany

Codelco KupferhandelGMHB

London - UK

Chile Copper Ltd.Radomiro Tomic

Copper

Division

Andina

Copper

Division

Salvador

Copper

Division

El Teniente

Copper

Division

Gabriela Mistral

Copper

Mine Ventanas

Smelter & Refinery

Division

Shanghai - China

RepresentativeOffice

Santiago

Headquarters

Ministro Hales

Copper

Division

7

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

Chile and Codelco: Leaders in Copper Production

Share of World Copper ProductionChile‟s Copper Production

„000 tonnes

Diego Hernández | August 2011

8

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

Contribution to Fiscal RevenuesCodelco and Large-Scale Private Mining CompaniesUS$ million, nominal

(1) Total income tax paid by 10 largest private copper mining companies.

Source: Budget Office.

Diego Hernández | August 2011

9

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

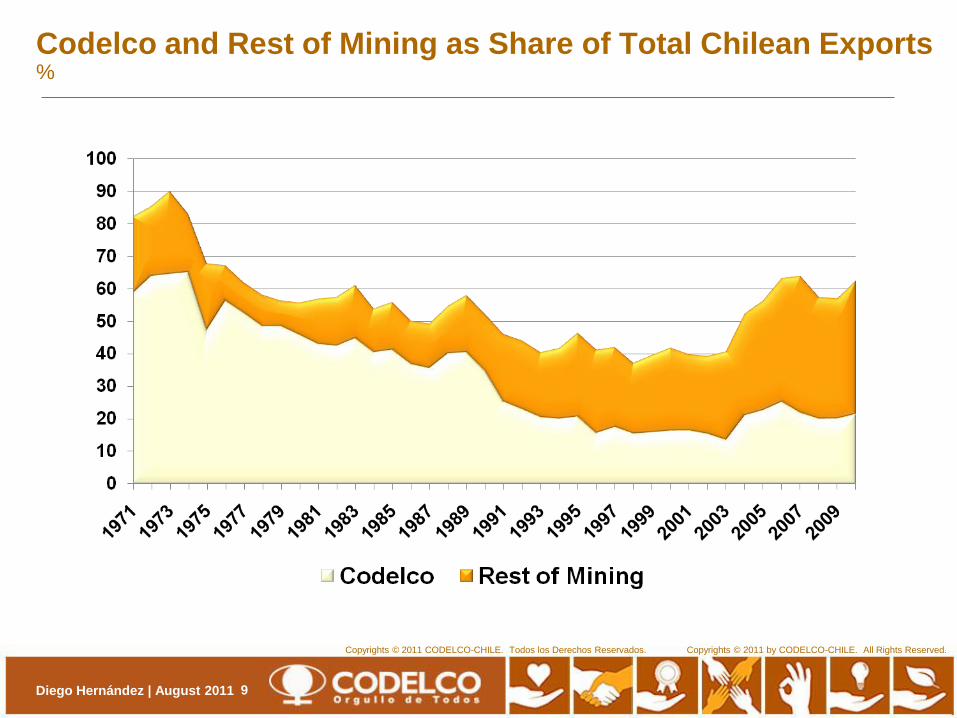

Codelco and Rest of Mining as Share of Total Chilean Exports%

Diego Hernández | August 2011

10

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

Structural Demand Changes and Copper Price, 1908-2011*c/lb, 2010

0

50

100

150

200

250

300

350

400

450

19

08

19

11

19

14

19

17

19

20

19

23

19

26

19

29

19

32

19

35

19

38

19

41

19

44

19

47

19

50

19

53

19

56

19

59

19

62

19

65

19

68

19

71

19

74

19

77

19

80

19

83

19

86

19

89

19

92

19

95

19

98

20

01

20

04

20

07

20

10

* 2011, average to July 25th.

World War I:

Military demand

Post-World War II:

Golden years in USA

European reconstruction

Japanese miracle

Oil crisis

Substitution

Emergence of China,

India and Other

Developing Economies

Great

Depression

Diego Hernández | August 2011

11

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

World Refined Copper Consumption, 1950-2010

Solid Medium and Long-Term Market Fundamentals

Urbanisation and Copper Consumption per Capita, 1950-2010

Sources: WBMS, IMF, World Bank, United Nations and Codelco. * PPP, 2005 US$.

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

1950 1960 1970 1980 1990 2000 2010

Developed Countries

Developing

Countries

China

„000 tonnes

—

2

4

6

8

10

12

14

10 20 30 40 50 60 70 80 90

Kg of copper per capita

Urbanisation rate (%)

USA

China

India

Japan

World

0

4

8

12

16

20

24

28

32

0 10,000 20,000 30,000 40,000

GDP per Capita and Consumption per Capita, 1980-2010

China

USAJapan

South

Korea Germany

Russia

Kg of copper per capita

GDP per capita*

Taiwan

0

2

4

6

0 6,000 12,000

GDP per capita*

Kg of copper per capita

China

Brazil

India

Diego Hernández | August 2011

12

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

The Challenge of GrowthWorld Mine Copper Production Potential*‘000 tonnes

*: Without disruptions and market adjustments.

**: Net of secondary production.

Source: Brook Hunt (2ndQ 2011). Assumes annual refined consumption growth rate of 3.6% in 2011-2020.

Operations

Probable projects

Possible projects

Possible greenfield projects

Possible brownfield projects

Probable greenfield projects

Probable brownfield projects

Consumption**

Operations

Consumption**

Diego Hernández | August 2011

13

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

Downward Trend in Average Copper Grades Puts Upward Pressure on Costs

Sources: Codelco and Brook Hunt.

-20

0

20

40

60

80

100

120

140

160

180

200

220

240

260

280

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

2010

19852000

19951990

2005

Accumulated production (million tonnes)

c/lb, nominal

Diego Hernández | August 2011

Average Copper GradeCopper Industry Supply

Curve Cash Cost (C1)

14

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

Rising Project Development Costs

COPPER PROJECT CAPEX HAS INCREASED

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

1995 2000 2005 2010 2015

Collahuasi

Los Pelambres

Cerro Verde Mill

Tenke Fugurume

Oyu Tolgoi

Lumwana

Capex/average production

US$ 2010 / tonne

Salobo I

Toromocho

Caserones

Gaby

RT Sulphides

Andina Phase I

MH

MAJOR EQUIPMENT PRICE ESCALATION*

* Equipment data includes principally manufactured equipment (e.g. heavy-walled vessels, large heaters or exchangers, coker drums and metal

tanks). Cost escalation trends are shown in US$. Updated to May, 2011. Source: IPA.

Global trend as from January 2003

(January 2003 = 1.00)

Diego Hernández | August 2011

15

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

Long-Term Copper Price Expectations Increasec/lb, 2011

Bank & Analysts‟ Forecasts Recent Forecasts*

*: Published during 2011.

Diego Hernández | August 2011

16

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

Codelco: Key Strategic Objectives

To maintain the company's reputation and leadership position: “its licence to operate”

To assure its planned level of production during the coming years so as to take advantage of the current

high-price cycle

To materialise its Key Structural Projects to develop Codelco‟s mining resources and maintain its leadership

in world copper production

To assure medium and long-term competitiveness, introducing new technologies, rationalising its

organisation and improving its decision-making process

Diego Hernández | August 2011

17

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

Codelco‟s 2011 Business and Development Plan Copper production‘000 tonnes

ENMS

Closure

Salvador

Oxides

Closure

RT Oxides

Closure

Chuqui Pit

Closure

Rajo Sur

MH

San

Antonio

Quetena

RT Phase II

NEW MINE

LEVEL

PDA

PHASE II

CHUQUI

U/G.

Diego Hernández | August 2011

18

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

Description

• New copper deposit near Chuquicamata (Calama).

• Important content of silver.

• Open pit, concentrator and roaster.

Capacity* • 170,000 fmt/year.

Start-Up Date • 2013.

Status

• MH Division created.

• Investment approved.

• In execution.

Structural Projects as the Priority (I)

MH

Diego Hernández | August 2011

*: Average production during the first 10 years at design capacity

19

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

Description

• Development of a new level of extraction at El Teniente.

• Increase the extraction rate to 137,000 tpd, avoiding the descent of

production in the Division.

Capacity* • 430,000 fmt/year.

Start-Up Date • 2017.

Status

• Investment approved.

• Early works in construction

(Platform, Decline).

Structural Projects as the Priority (II)

El Teniente New Mine Level

Diego Hernández | August 2011

*: Average production during the first 10 years at design capacity

20

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

Description• Development of an underground mine at Chuquicamata.

• Production of copper and molybdenum.

Capacity* • 315,000 fmt/year.

Start-Up Date • 2018.

Status

• In feasibility (conclusion in 2013).

• Beginning of early works

in the fourth quarter of 2011.

Structural Projects as the Priority (III)

Chuquicamata Underground

Diego Hernández | August 2011

*: Average production during the first 10 years at design capacity

21

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

Description• Capacity increase from 94,000 to 244,000 tpd.

• Open pit and underground operations.

Capacity* • >350,000 fmt/year (additional to current level of production).

Start-Up Date • 2018.

Status • In feasibility.

Structural Projects as the Priority (IV)

Andina Phase II

Diego Hernández | August 2011

*: Average production during the first 10 years at design capacity

22

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

Structural Projects as the Priority‘000 tonnes

Note: Includes 49% stake in El Abra.

Source of projections: 2011: budget; 2012: Triennial Plan proposed to Finance and Mining Ministries; 2020: 2011 Business and Development Plan and

2011 Plan without Development, plus El Abra.

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2005 2006 2007 2008 2009 2010 2011 2012 2020

History

Projection

With

Projects

Without

Projects

Diego Hernández | August 2011

23

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

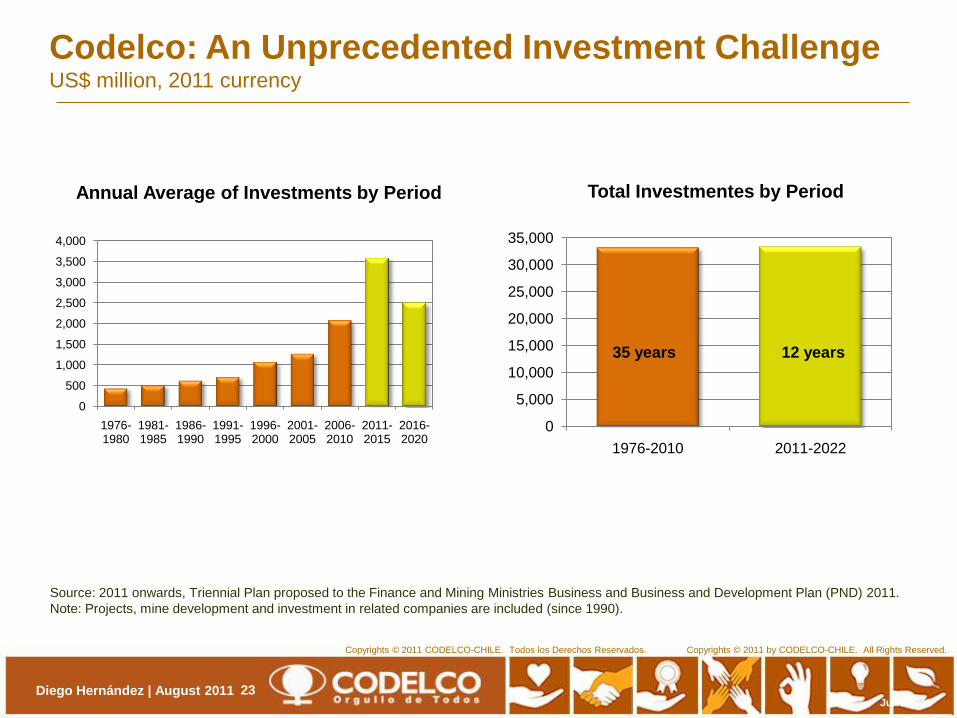

Source: 2011 onwards, Triennial Plan proposed to the Finance and Mining Ministries Business and Business and Development Plan (PND) 2011.

Note: Projects, mine development and investment in related companies are included (since 1990).

Codelco: An Unprecedented Investment ChallengeUS$ million, 2011 currency

June 2011

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1976-1980

1981-1985

1986-1990

1991-1995

1996-2000

2001-2005

2006-2010

2011-2015

2016-2020

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1976-2010 2011-2022

Annual Average of Investments by Period Total Investmentes by Period

35 years 12 years

Diego Hernández | August 2011

24

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

0

500

1,000

1,500

2,000

2,500

Codelco (1) Xstrata Freeport McMoran BHP Billiton Anglo American Southern Copper Chinese Companies Rio Tinto Vale Antofagasta Plc

2010 2015 2020

Maintaining Leadership in the Copper Industry: Expected Production of Codelco and Other Companies*‘000 fmt

Source: Codelco.

Notes:

* Attributable copper production. Codelco figures correspond to 2011 Business and Development Plan. Projections for rest of the industry updated to May 2011.

(1) Includes 49% stake in El Abra; figures correspond to 2011 Business and Development Plan. (2) Own production and stake in Yunnan Copper; excludes stake in Rio Tinto.

(3) Corriente Resources is a joint venture between Tongling and China Railways.

Diego Hernández | August 2011

25

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

Ensuring the Very Long Term Codelco‟s Exploration Activities Focus

Exploration Budget 2011

US$ 62 million (up by 42% on 2010)

Exploration in Chile (81%)

• Priority is around existing Codelcooperations (brownfield).

• Discovery of new areas of interestwithin the main metallogenic belts,located mostly in covered areas(greenfield).

International exploration (19%)

• Opportunities in early stages ofdevelopment. Growth determined byresults.

• Prospects in Brazil, Ecuador andColombia.

Discoveries that are not part of the corebusiness could be developed with thirdparties as joint ventures.

Diego Hernández | August 2011

BRAZIL:

Active since 2000. Operated by Codelco do Brasil Mineração, based in Rio de Janeiro.

ECUADOR:

Active since 2009. Agreement with government to evaluate areas of mining interest. Under development.

COLOMBIA:

In process of identifying business opportunities in exploration.

Underway.

CHILE:

Where all the company’s operations are located and the main focus of its exploration efforts.

In the past, Codelco has explored in:

Mexico (2000-2008), Argentina and Peru (not systematically) and Zambia (1998).

26

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

Codelco International: Spreading the Company‟s Wings

Creation of a Special Purpose Vehicle (SPV) with assets in

exploration, development and production

Focused on leveraging the value of the company’s current

portfolio and taking advantage of new investment

opportunities

The SPV will give Codelco the financial flexibility to develop

new operations

Permits investment in an SPV with assets in one of the

world’s most attractive mining jurisdictions

Diego Hernández | August 2011

27

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

Codelco‟s Licence to Operate:

Safety and Occupational Health

Management Focus

Safety and

Occupational

Health at

Codelco

Standards of control of

professional illnesses

Learning

Behavioural safety

Leadership

Standards of control of fatalities

Diego Hernández | August 2011

28

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

Codelco‟s Licence to Operate:

Environment and Communities

Operational

Discipline

Communications

Strategic

Framework

and Culture

Socio-Environmental Vulnerabilities

Socio-environmental

culture

Compliance with regulation and

corporate standards

Skills

Management of knowledge and

innovation

Community development

Management Focus

Diego Hernández | August 2011

29

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

Creating Competitive Advantage through People

Human

Capital

Generational

Change

Attraction,

Development and

Retention of

Talent

Cultural Change

Labour

Relations

Organisational

Effectiveness

Workforce

Optimisation

Diego Hernández | August 2011

30

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

Codelco: A Great Future

Useful Life

YearsChuquicamata 50RT 30MH 40Salvador 25Andina 67El Teniente 68Gaby 13

Diego Hernández | August 2011

31

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.Copyrights © 2011 CODELCO-CHILE. Todos los Derechos Reservados. Copyrights © 2011 by CODELCO-CHILE. All Rights Reserved.

MELBOURNE MINING CLUB

LUNCHEON SERIESThe Copper Industry and Codelco:

Opportunities and Challenges

Diego Hernández C.

CEO

August 4th, 2011