Embed Size (px)

Citation preview

Medium Term Prospects for EU Dairy Markets under Agenda 2000 and the Midterm Review Proposals – A Quantitative Analysis for the

Spanish Dairy Sector with the CAPRI Modelling System

Christine Wieck, Ignacio Perez, Wolfgang Britz

Institute for Agricultural Policy, Market Research and Economic Sociology, Bonn University

Prepared for AEEA Seminar, March 13-14, Lugo (Spain)

1. Introduction

European Dairy Policy has been subject to reform ever since. Even with challenges as the milk quota

reform still ahead, the Agenda 2000 policy package introduced already new policy instruments as to offset

substantial cuts in market price support. The motives behind the Common Agricultural Policy (CAP)

reform were to foster a more competitive farming industry by lowering intervention prices and bringing

production more closely into line with demand. In the Midterm Review (MTR) of the Agenda 2000, the

EU Commission proposed further CAP changes, which will affect the competitiveness of dairy farms and

industry. Whereas the Agenda 2000 broke with the traditional line in dairy policy through the introduction

of compensation payments for dairy cows, the MTR proposal affects dairy policy mainly in an indirect

way. The main thrust of the MTR proposals is about decoupling support from production decisions by

means of the introduction of a singled decoupled income payment per farm. Hence, all compensation

payments1 regardless if they are attached to area or number of animals, shall be converted in an income

payment allowing for complete farming flexibility and increasing market orientation of each farm. Results

from the analysis of both policy proposals will be presented in the following.

With 14% of total value of agricultural production in 2000, milk production is the most important activity

both in the EU as a whole and for a majority of the Member States. The share of milk in agricultural

output varies however widely between Member States and regions reaching 30-50% in some Spanish

regions such as Galicia or Cantabria. Traditionally, there exists a strong link between the dairy and beef

sector due to dual-purpose breeds and dairy market reform will hence affect beef markets as well.

Worldwide, the EU is both the biggest producer and consumer of milk, with a share of 21% in

production. These facts underline that reforms in the dairy sector impacts on farm income, domestic

consumption and the competitive positions of the EU in agricultural world markets.

The following quantitative analysis based on the CAPRI modelling system compares developments of

production, demand and agricultural income projected for 2009 under the policy set of the MTR proposal

to the results of the reference run shown above, which represents the full implementation of the Agenda

2000 proposal in the year 2009. The analysis for the dairy sector is based on the so called “Option 1” of

the Commissions proposal regarding possible future avenues for the development of the dairy sector

(European Commission 2000). Hence, a continuation of Agenda 2000 for the dairy sector is assumed.

The paper is organised as follows: after this brief introduction, the second section presents the CAPRI

modelling system with which the analysis is conducted. The third part describes policy implementation

and scenario assumptions for both, reference and simulation run. Chapter four presents the results for

dairy and beef markets as well as regional developments in Spain and some conclusions are drawn in

section five.

1 No rule without exceptions: Some payments are not included (durum wheat quality premium, protein crop supplement,

payments for rice and some payments for processors of specific products).

2

2. The CAPRI modelling system

The CAPRI modelling system is designed as a projection and simulation tool for the agricultural sector

based on:

(1) A physical consistency framework, covering balances for agricultural area, young animals and feed

requirements for animals as well as nutrient requirement for crops, realised as constraints in the

regional supply models. The market model ensures that fat and protein comprised in the milk

delivered to dairies is equal to the fat and protein comprised in the processed dairy products.

(2) Economic accounting principles according to the definition of the Economic Accounts for

Agriculture (EAA). The model covers all outputs and inputs included in the national EAAs for the

Member States, with revenues and costs broken down consistently to regions and production

activities.

(3) A detailed policy description. The regional supply models capture all relevant payment schemes with

their respective ceilings as well as set-aside obligations and sales quotas. The market side covers

tariffs, intervention purchases and subsidised exports. The policy of non-EU regions is based on

OECD PSE/CSE data bank.

(4) Behavioural functions and allocation steering are strictly in line with micro-economic theory.

Functional forms are chosen to be globally well behaved, allowing for a consistent welfare analysis.

The model distinguishes a supply and a market module, iteratively coupled. The supply module consists

of aggregate programming models at NUTS II level, working with exogenous prices during each

iteration. After being solved, the regional results of these NUTS II models – crop areas, herd sizes,

input/output coefficients etc. –are aggregated into Member State level models, which are then calibrated to

these results by using techniques borrowed from Positive Mathematical Programming. Young animal

prices are then determined by linking these Member State models into a non-spatial EU model with

market balances for young animals. Afterwards, supply and feed demand functions of the market module

are calibrated to prices and results from the supply module on feed use and production of the current

iteration. The market model is then solved and the resulting producer prices at Member State level drive

the next iteration with the supply models. Equally, in between iterations, premiums for activities are

adjusted if ceilings are overshot according to the results laid down in the Common Market Organisations.

The underlying methodology of supply for yearly crops and animals assumes a two-stage decision

process. In the first stage, producers determine optimal variable input coefficients (nutrient needs for

crops and animals, seed, plant protection, energy, pharmaceutical inputs, etc.) per hectare or head for

given yields which are determined exogenous by trend analysis. Nutrient requirements enter as constraints

in the supply models, whereas all other variable inputs together with their prices define the so-called

accounting costs. The proceeding reflects the calculation of gross margins in farm management. In the

second stage, the profit maximising crop mix and animal numbers are determined simultaneously with

cost minimising feed and fertiliser mix in the supply models. Availability of grass and arable land as well

as sales quotas restrict production possibilities and the crop mix is further on influenced by set-aside

obligations. Animal requirements (energy, protein etc.) are covered by a cost minimised feed mix

combination, whereas fertiliser needs of crops are met by either organic nutrients found in manure or

purchased fertiliser. Fodder (grass, straw, fodder maize, root crops, silage, milk from suckler cows or

mother goat and sheep) is assumed to be non-tradable, and hence animal processes are linked to the crop

production and regional land availability. All other outputs and inputs can be sold and purchased at fixed

prices. Selling of milk cannot exceed the quota and for sugar production an A,B,C quota system is

embedded.

3

Graph 1. Link of modules in the CAPRI modelling system

Supply

200 Regional

optimisation

models

Perennial

sub-module

Output Markets

Multi-commodity

spatial market model

with 11 regional

aggregates

and all EU MS

Young Animal

Markets

Linked optimisation

models

at Member

State level

Supply

Feed demand

Prices

Aggregation

to Member States

Premium calculator

Calculate

premiums

depending

on CMOs

(ceilings,

base areas ..)

Levels

The use of a mathematical programming approach has the advantage to directly embed compensation

payments, set-aside obligations, voluntary set-aside and sales quotas, as well as to capture important

relations between agricultural production activities. The programming models are calibrated to observed

set-aside hectares, including voluntary set-aside, and non food production on set-aside land is treated as a

separate production activity. Fallow land not falling into set-aside programs reflects the difference

between land reported as idling in national statistics and data from commission services on actual hectares

in set-aside programs. Not at least, environmental indicators as N,P,K balances and output of gases linked

to global warming are implemented in the system.

Output coefficients for the high final weight activities (dairy cows, male and female adult fattening) are

created by increasing average milk and meat yield by 20 %, for the low intensive variants by decreasing

them by 20 %. All intermediate inputs with the exception of feed and young animal are corrected

accordingly. The requirement functions are directly applied to the changed final weights. Input

coefficients for young animals are identical across the variants.

In the case of feeding stuff, a set of requirement functions defines the need of each animal category

depending on, for example, live weight, weight increase per day, milk yield. These requirement function

are mostly derived under experimental conditions and define a technological frontier from which actual

technology on farm level can be expected to deviate, not at least due to for example control and

management costs usually not taken into account in experiments. These requirements must be covered by

feeding an appropriate mix of feeding stuff to each animal herd. As sectoral availability of feeding stuff is

known ex-post, a complex non-linear optimisation program distributes the available feeding stuff

resources to the animals, simultaneously ensuring that the distribution leads to plausible feeding costs. If

necessary, the requirement functions are shifted to account for differences between actual feeding

practises of the farms and the technological frontier defined by the requirement functions.

In order to describe the relationships in between cattle production activities and to define the effective

number of animals bred (flow) at regional level, a so-called herd module has been developed. At national

level, data on slaughtering, imports and exports of live animals and meat (CRONOS, COMEXT,

INTRASTAT) as well as herd size statistics (stocks) (CRONOS, REGIO) allow quite well to describe

4

livestock activity levels (e.g. numbers of milk cows, suckler cows, calves raised, calves fatted, heifers

raised, heifers and beef fatted) and their inter-relationships (see Graph 2 above)2.

Graph 2. Modelling of young animal flow in the cattle sector

Beef

Beef

Veal

Raising

female

Calves

Fattening

male

Calves

Breeding

Heifers

Milk Cows

Suckler

Cows

Male adult

cattle

High/Low

Fattening

Heifers

High/Low

Fattening

female

Calves

Raising

male

Calves

Male

Calf

Young

heifer

Young

bull

Young

cow

Female

Calf

The market module breaks down the world into 12 country aggregates3, each aggregate featuring systems

of supply, human consumption, feed and processing functions. The parameters of these functions are

derived from elasticities borrowed from other studies and modelling systems, and calibrated to projected

quantities and prices in the simulation year, where the choice of the functional form (normalised quadratic

for feed and supply, Generalised Leontief Expenditure function for human consumption) and further

restrictions (homogeneity of degree zero in prices, symmetry, correct curvature) ensure regularity.

Accordingly, the demand system allows for the calculation of welfare changes for the consumers. Policy

instruments in the market module include (bi-)lateral tariffs and Producer/Consumer Subsidy Equivalent

price wedges (PSE/CSE). Some important Tariff Rate Quotas (TRQs) as well as explicit modelling of

intervention sales and subsidised exports under WTO commitment restrictions are implemented for the

EU.

Special attention is given to the processing stage of dairy products for the EU Member states. First of all,

balancing equations for fat and protein ensure that processed products use up exactly the amount of fat and

protein comprised in the raw milk. Production of processed dairy products is based on a normalised

quadratic function driven by the difference between the dairy product’s market price and the value of its

fat and protein content. Lastly, prices of raw milk are equal to its fat and protein content valued with fat

and protein prices.4

The Armington assumption drives the composition of demand from domestic sales and the different

import origins depending on price relations and thus determines bilateral trade streams. The model

comprises a two stage Armington system: on the top level, the composition of total demand from imports

and domestic sales is determined, whereas the lower stage determines the import shares from different

origins. Due to the Armington assumption, product markets for different regions are linked by import

2 A detailed description can be found in : Britz, W., Setti, M. Wieck, C. (2002): Improvements of the Dairy and Beef sub-module.,

CAPRI working paper 02-06, available on the project web site. 3 EU, East European Candidate Countries, Mediterranean countries, U.S., Canada, Australia & New Zealand, Free trade

developing countries, High tariff traders (as Japan), India, China, ACP countries, Rest of the World 4 A detailed description can be found in : Britz, W., Wieck, C. (2002): Modelling the processing of dairy products, CAPRI

working paper 02-08, available on the project web site

5

streams and import prices when they were observed in the base year. Accordingly, no uniform world

market price is found in the system.

3. Scenario assumptions

3.1. Scenario assumptions reference run: Agenda 2000

The policy for the status quo scenario of the reference run reflects the Agenda 2000 policy extended to the

year 2009. It is taken as the comparison point for the Mid term Review impact analysis. Therefore, it is

necessary to reflect carefully the status quo policy representation and scenario assumptions and exogenous

shifters for this run. The most crucial policy parameters for the reference run can be listed as follows:

(1) Administered prices for cereals, beef and milk products fall decrease according to the Berlin decisions

regarding the Agenda 2000 by 15%, 20% and 15% respectively.

(2) Due to its activity based layout, the CAPRI supply model is well suited to deal with the compensation

payment scheme. A detailed modelling component allows for the definition of payment schemes

linked to outputs (current or historic yields) or activity levels in combination with ceilings in physical

and/or valued terms. The following payments are included in the reference run: COP premiums for

cereals, oilseeds, pulses and energy crops; traditional and established durum wheat premiums; direct

income support for dairy cows; direct payments to sheep and goat; national envelopes for dairy cows,

sheep & goat and bovine meat cattle; slaughter premiums for adult cattle and calves; and national

premiums to dairy cows in northern Sweden and Finland. Many of these premium schemes are

restricted by ceilings in value and maximum amount of eligible hectares or heads defined at national

or regional level. Premiums are therefore cut in the model if these ceilings are exceeded.

(3) The modelling system considers set-aside obligations as a constraint in the regional programming

models. Official mandatory set-aside rates ex-post and in the reference run (10 %) are corrected

downwards to reflect the small producer scheme, based on information of Commission Services. The

small producer shares are trend forecasted for the simulation year. In some cases, data at regional level

regarding small producer shares were available for early years of the McSharry reform and the

resulting regional differentiation was kept unchanged over time.

(4) Milk quotas are supposed to increase with Member States specific rates, for the EU as a whole by

2.4 %. Percentages of under- and over-utilisation of quotas at regional level are kept constant as

observed in the base year. Sugar quotas are kept at base year levels, but the system of A and B levies

as well as production of C sugar is embedded in the analysis.

Exogenous development of yields are based on trend analysis at EU Member State level, covering the

years 1980-1999. For cereals, they are harmonised with the latest DG Agri’s Market Outlook.5 Variable

inputs are first shifted proportionally with the yields and then reduced by input saving technical progress

of -0.2 % p.a.. Exceptions are nutrient needs of crops (N,P,K) and animal requirements (energy, protein,

fibre etc.) which are driven by yield dependent engineering functions.

The demand system for the EU is calibrated to observed member state data on per capita consumption,

income and population levels6. Changes in demand behaviour not linked to these factors have to be based

5 It should be noted that the DG-AGRI market outlook expect a cut in cereal yield growth rate between 2000-2009 of 50 % against

the 1993-1999 period. This assumption, taken over in the current analysis, has considerable impacts on the development of cereals

markets, as the difference between long term trends and the ones applied adds up to some 20 Mio t by the end of 2009 6 In most cases in line with the data found in DG-Agri’s publication “Prospects for Agricultural Markets 2002-2009”.

6

on assumptions and trend analysis and the baselines of the EU commission and FAPRI. Inflation is set to

1.9 % p.a. and nominal GDP growth for the EU to 2.7 % p.a. and is used as a proxy for consumers’

available income. The assumptions for the EU as a whole are taken over to the individual Member States.

Population growth at Member States level are taken from EUROSTAT.

The price framework in the market part of the model is based on representative long-term time series for

world market prices of major raw and processed agricultural products, which are trend forecasted. These

trends had been compared and partially revised to medium term forecasts by OECD, FAPRI and the EU

Commission. Developments of domestic prices are based on these world market price developments,

border protection and domestic market policies.

Behavioural functions for intervention stocks and subsidised exports in the market model are calibrated

to observed quantities and price relations between domestic, export and administrative prices for a three

year average around 1998.

Data relating to other world regions stem ex post from the WATSIM modelling system, shifted to the

year 2009 based on results of other studies. The resulting data set is adjusted to fulfil consistency

conditions, both in the base and the simulation year. Main data source for the shifters in supply and

demand for non-EU regions is the @2030 framework of FAO’s global perspective unit.

3.2. Scenario assumptions: MTR run

The MTR proposal aims at (1) economic viability, (2) social balance, (3) environmental integration and

animal health and welfare concerns as well as (4) rural development. In order to achieve the goals, the

main thrust of the proposal lies in the decoupling of income support from production decisions. In the

following, the model specification of the MTR proposal will be presented.

(1) In order to calculate the so-called uniform premium, premiums paid under Agenda 2000 were

modified according to the MTR proposal: An increase by 3 €/t of historic yield to 66 €/ton for

‘Grandes Cultures’ reflect a 50 % compensation of the cut in cereals intervention prices. A reduction

of the supplementary payment in durum wheat to 250 €/ha in “traditional areas” bundled with an

abolishment of the supplement in “established areas”. Introduction of an income payment of 102 €/t in

rice (177 €/t – 75 €/t remaining as a crop specific premium)7.

(2) These partially redefined premiums for arable crops, cattle and sheep falling under the new uniform

per farm premium and labelled “decoupled” were applied to the three year average 1998 areas or herd

sizes, and cut if respective ceilings were overshot.

(3) The premiums were “dynamically modulated” until 2009, i.e. six steps of -3 % cuts from the original

level to a final maximal cut of -18 %. As only payments above a certain ceiling – 5.000 € per farm

plus 3.000 € per Annual Working Unit (AWU) exceeding two AWUs –are subject to the modulation,

smaller reduction were applied for groups of payments according to information provided by

Commission Services based on the European Farm Accounting Data Network.

(4) Afterwards, the resulting premium sum at regional level is distributed over eligible hectares and

converted into a regional specific uniform premium per ha in the MTR run. The resulting regional

premium sum was introduced as a ceiling in values at regional level, so that regional premiums per

eligible hectare would be cut if a premium overshot takes place. The following top-ups are added to

the uniform premiums: durum wheat (15 €/t), rice (75 €/t), protein (9.5 €/t) and energy crops

(45 €/ha). According to the proposal, vegetable and fruits are not eligible, and it was assumed that the

7 Support to nuts is not included in the runs, as well as direct payments for dehydrated or sun dried fodder.

7

same is valid for table olives and olives for oils, nurseries, flowers, vineyards and the so-called “other

crops”.

(5) Cereals intervention prices were reduced by 7.5% - the combined effect of a drop by 5% to 95,35 €/t

and the abolishment monthly reports. Further on, rye intervention was abolished and rice intervention

prices reduced to 150 €/ton.

Set-aside obligations are defined as a “continuation of the individual historic set-aside obligation”. That

obligation was calculated at NUTS II level based on the regional crop mix in the base year and on an

obligatory set-aside rate of 10 %, corrected by national or regional small producer shares.

The costs of compulsory farm audits on all relevant material flows and on-farm processes for all farm

receiving more than 5000 € are not included in the study. The error is deemed not important, especially as

financial support covering operation costs is eligible under Rural Development, and the dynamic

modulation will increase budgets available under the second pillar. It can be expected that regional

government will at least partially redirect the budgetary funds into new agri-environmental programs,

especially the proposed “temporary and degressive aid (max 200 €/ha) to farms to help them

implementing statuary standards”.

4. Results

This section discusses the simulation results, both in the reference run as well as in the MTR run for a

number of key items on the EU, as well as at national and regional level. The first part presents medium

term prospects on EU dairy and beef markets and economic impacts of the proposals followed by a

detailed assessment of regional impacts.

4.1. Medium term prospects on dairy and beef markets

4.1.1. Dairy markets

Total raw milk output follows the quota expansion determined by Agenda 2000 of 2.4% to about 125

Mio. t of fresh milk.8 The main factors affecting dairy markets are thus autonomous trends in milk yields –

21.4% in the period 1998 to 2009 - and demand developments for milk products.

On the supply side for processed milk products, different trends can be observed. Whereas cheese

production expands strongly, mainly driven by an increasing demand for cheese by around 13% in the

reference run (or 18.3 kg cheese per capita consumption), supply for butter remains stable and skimmed

milk powder production declines heavily. On the demand side a consumption shift towards fresh and

processed milk products with a lower fat content can be observed. Additionally, the demand shift to

products with lower fat content increase the net exports of butter substantially, as new markets must be

found outside of EU. Net trade of skimmed milk powder decreases drastically, and the EU becomes a net

importer. Net trade of cheese remains stable whereas a strongly increasing share of imports of fresh milk

products can be observed.

8 Note that the figure raw milk presented in table 1 includes the whole milk produced on farm and not only the share of milk

delivered to dairies. Therefore, the simulated increase of 2.5%, higher than the global quota expansion by Agenda 2000, is due to

an increase on farm consumption of milk.

8

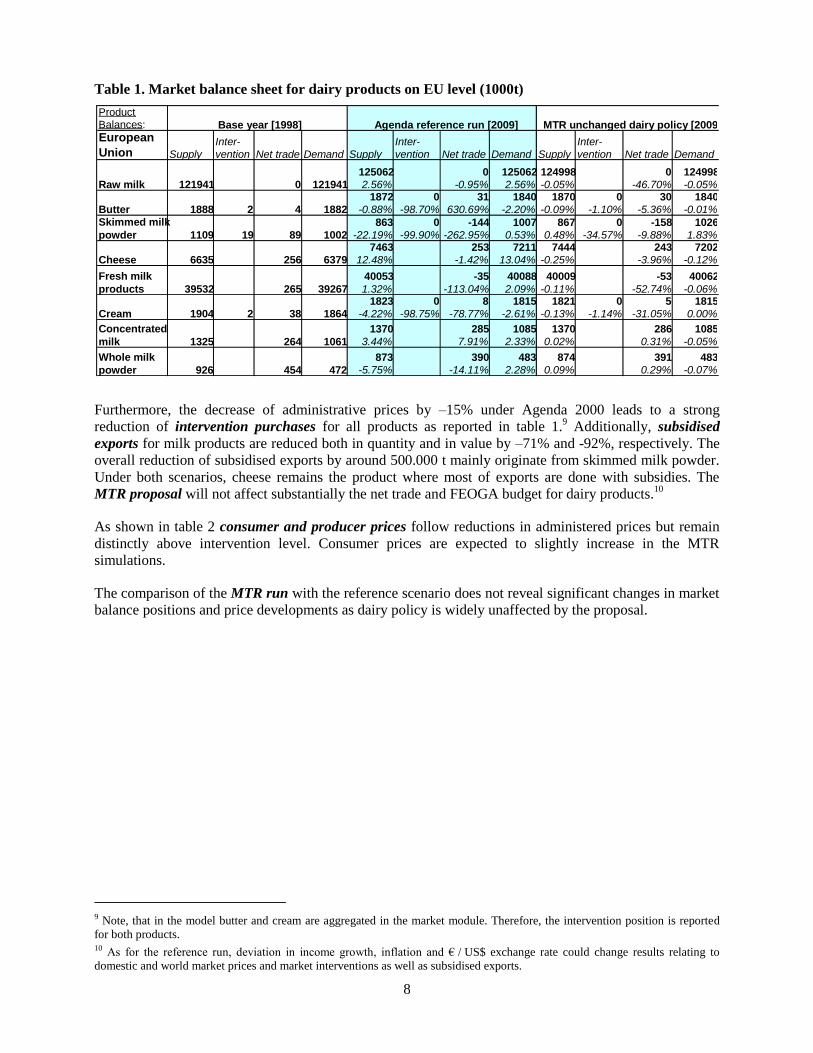

Table 1. Market balance sheet for dairy products on EU level (1000t)

ProductBalances:

125062 0 125062 124998 0 124998

2.56% -0.95% 2.56% -0.05% -46.70% -0.05%1872 0 31 1840 1870 0 30 1840

-0.88% -98.70% 630.69% -2.20% -0.09% -1.10% -5.36% -0.01%

863 0 -144 1007 867 0 -158 1026

-22.19% -99.90% -262.95% 0.53% 0.48% -34.57% -9.88% 1.83%7463 253 7211 7444 243 7202

12.48% -1.42% 13.04% -0.25% -3.96% -0.12%

40053 -35 40088 40009 -53 40062

1.32% -113.04% 2.09% -0.11% -52.74% -0.06%1823 0 8 1815 1821 0 5 1815

-4.22% -98.75% -78.77% -2.61% -0.13% -1.14% -31.05% 0.00%

1370 285 1085 1370 286 1085

3.44% 7.91% 2.33% 0.02% 0.31% -0.05%

873 390 483 874 391 483

-5.75% -14.11% 2.28% 0.09% 0.29% -0.07%

Net trade Demand

European

Union Supply

Inter-

vention Net trade Demand Supply

Base year [1998] Agenda reference run [2009] MTR unchanged dairy policy [2009]

Cheese

1888 2

Raw milk 121941

Inter-

vention

Inter-

vention Net trade DemandSupply

Butter

Concentrated

milk

6635

Fresh milk

products 39532

4 1882

1002

472

256

Skimmed milk

powder 1109 19 89

265

Cream 1904 2 38

1325 264

Whole milk

powder 926 454

0 121941

1061

1864

6379

39267

Furthermore, the decrease of administrative prices by –15% under Agenda 2000 leads to a strong

reduction of intervention purchases for all products as reported in table 1.9 Additionally, subsidised

exports for milk products are reduced both in quantity and in value by –71% and -92%, respectively. The

overall reduction of subsidised exports by around 500.000 t mainly originate from skimmed milk powder.

Under both scenarios, cheese remains the product where most of exports are done with subsidies. The

MTR proposal will not affect substantially the net trade and FEOGA budget for dairy products.10

As shown in table 2 consumer and producer prices follow reductions in administered prices but remain

distinctly above intervention level. Consumer prices are expected to slightly increase in the MTR

simulations.

The comparison of the MTR run with the reference scenario does not reveal significant changes in market

balance positions and price developments as dairy policy is widely unaffected by the proposal.

9 Note, that in the model butter and cream are aggregated in the market module. Therefore, the intervention position is reported

for both products. 10 As for the reference run, deviation in income growth, inflation and € / US$ exchange rate could change results relating to

domestic and world market prices and market interventions as well as subsidised exports.

9

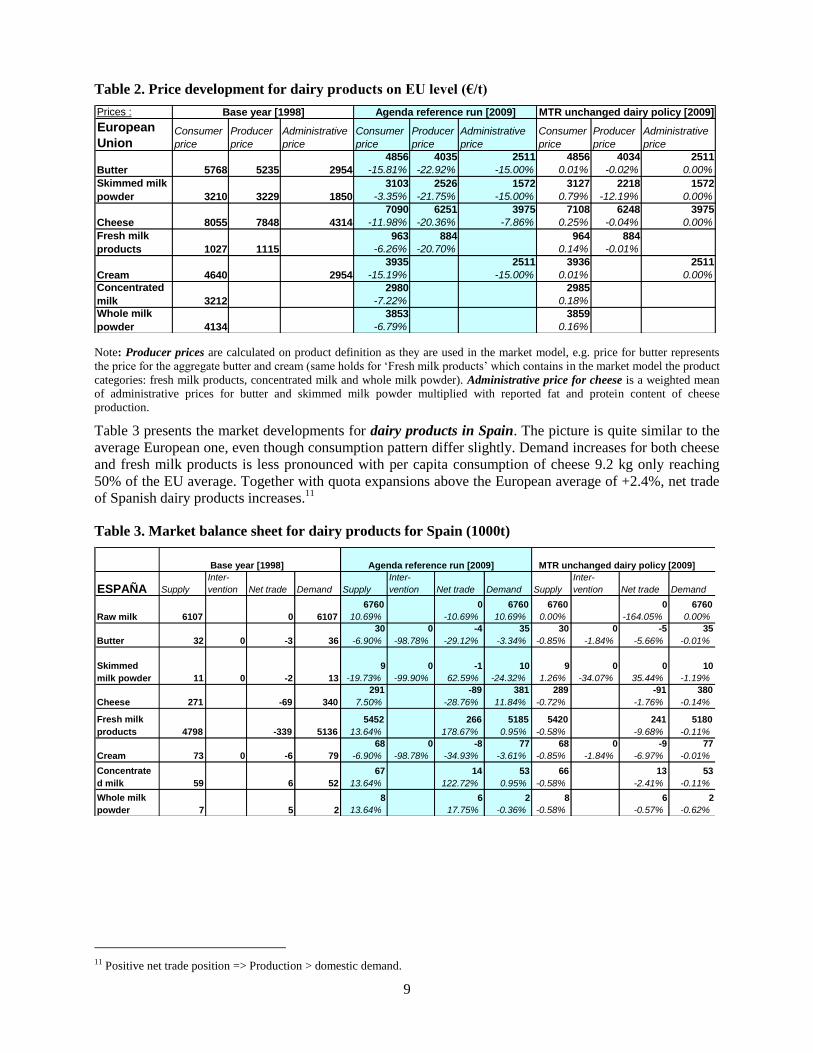

Table 2. Price development for dairy products on EU level (€/t)

Prices :

4856 4035 2511 4856 4034 2511

-15.81% -22.92% -15.00% 0.01% -0.02% 0.00%

3103 2526 1572 3127 2218 1572

-3.35% -21.75% -15.00% 0.79% -12.19% 0.00%

7090 6251 3975 7108 6248 3975

-11.98% -20.36% -7.86% 0.25% -0.04% 0.00%

963 884 964 884

-6.26% -20.70% 0.14% -0.01%

3935 2511 3936 2511

-15.19% -15.00% 0.01% 0.00%

2980 2985

-7.22% 0.18%

3853 3859

-6.79% 0.16%

Producer

price

Administrative

price

Whole milk

powder 4134

Concentrated

milk 3212

Cream 4640 2954

Fresh milk

products 1027

3229

1115

7848 4314

Producer

price

European

UnionConsumer

price

Cheese 8055

Butter 5768

1850

Skimmed milk

powder 3210

Consumer

price

5235 2954

MTR unchanged dairy policy [2009]

Producer

price

Administrative

price

Base year [1998] Agenda reference run [2009]

Administrative

price

Consumer

price

Note: Producer prices are calculated on product definition as they are used in the market model, e.g. price for butter represents

the price for the aggregate butter and cream (same holds for ‘Fresh milk products’ which contains in the market model the product

categories: fresh milk products, concentrated milk and whole milk powder). Administrative price for cheese is a weighted mean

of administrative prices for butter and skimmed milk powder multiplied with reported fat and protein content of cheese

production.

Table 3 presents the market developments for dairy products in Spain. The picture is quite similar to the

average European one, even though consumption pattern differ slightly. Demand increases for both cheese

and fresh milk products is less pronounced with per capita consumption of cheese 9.2 kg only reaching

50% of the EU average. Together with quota expansions above the European average of +2.4%, net trade

of Spanish dairy products increases.11

Table 3. Market balance sheet for dairy products for Spain (1000t)

6760 0 6760 6760 0 6760

10.69% -10.69% 10.69% 0.00% -164.05% 0.00%

30 0 -4 35 30 0 -5 35

-6.90% -98.78% -29.12% -3.34% -0.85% -1.84% -5.66% -0.01%

9 0 -1 10 9 0 0 10

-19.73% -99.90% 62.59% -24.32% 1.26% -34.07% 35.44% -1.19%

291 -89 381 289 -91 380

7.50% -28.76% 11.84% -0.72% -1.76% -0.14%

5452 266 5185 5420 241 5180

13.64% 178.67% 0.95% -0.58% -9.68% -0.11%

68 0 -8 77 68 0 -9 77

-6.90% -98.78% -34.93% -3.61% -0.85% -1.84% -6.97% -0.01%

67 14 53 66 13 53

13.64% 122.72% 0.95% -0.58% -2.41% -0.11%

8 6 2 8 6 2

13.64% 17.75% -0.36% -0.58% -0.57% -0.62%

36

ESPAÑA Supply

Inter-

vention Net trade Demand

Butter 32 0 -3

-2 13

Cheese 271 -69 340

Skimmed

milk powder 11 0

Fresh milk

products 4798 -339 5136

-6 79

Concentrate

d milk 59 6 52

Cream 73 0

Whole milk

powder 7 5 2

Raw milk 6107 0 6107

Agenda reference run [2009]Base year [1998]

Inter-

vention Net trade Demand

Supply Net trade Demand

Inter-

vention

MTR unchanged dairy policy [2009]

Supply

11 Positive net trade position => Production > domestic demand.

10

4.1.2. Beef markets

Due to the close production linkages of dairy and beef activities, simulation impacts for beef and veal will

be briefly presented as well.

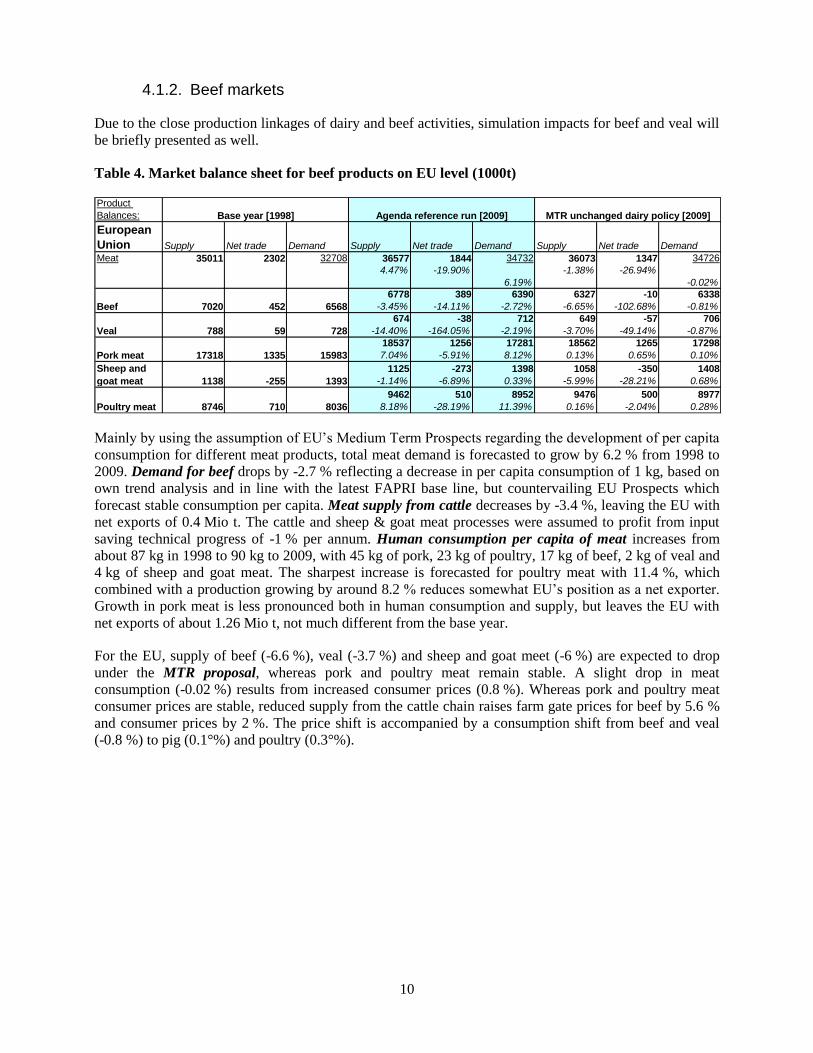

Table 4. Market balance sheet for beef products on EU level (1000t)

Product

Balances:

36577 1844 36073 1347

4.47% -19.90% -1.38% -26.94%

6.19% -0.02%

6778 389 6390 6327 -10 6338

-3.45% -14.11% -2.72% -6.65% -102.68% -0.81%

674 -38 712 649 -57 706

-14.40% -164.05% -2.19% -3.70% -49.14% -0.87%

18537 1256 17281 18562 1265 17298

7.04% -5.91% 8.12% 0.13% 0.65% 0.10%

1125 -273 1398 1058 -350 1408

-1.14% -6.89% 0.33% -5.99% -28.21% 0.68%

9462 510 8952 9476 500 8977

8.18% -28.19% 11.39% 0.16% -2.04% 0.28%

Base year [1998] Agenda reference run [2009] MTR unchanged dairy policy [2009]

710 8036

1335 15983

34726

Net trade DemandSupply

34732

Net trade DemandSupply

Poultry meat 8746

-255 1393

Sheep and

goat meat 1138

Pork meat 17318

59 728Veal 788

Beef 7020 452 6568

Meat 35011 2302 32708

European

Union Supply Net trade Demand

Mainly by using the assumption of EU’s Medium Term Prospects regarding the development of per capita

consumption for different meat products, total meat demand is forecasted to grow by 6.2 % from 1998 to

2009. Demand for beef drops by -2.7 % reflecting a decrease in per capita consumption of 1 kg, based on

own trend analysis and in line with the latest FAPRI base line, but countervailing EU Prospects which

forecast stable consumption per capita. Meat supply from cattle decreases by -3.4 %, leaving the EU with

net exports of 0.4 Mio t. The cattle and sheep & goat meat processes were assumed to profit from input

saving technical progress of -1 % per annum. Human consumption per capita of meat increases from

about 87 kg in 1998 to 90 kg to 2009, with 45 kg of pork, 23 kg of poultry, 17 kg of beef, 2 kg of veal and

4 kg of sheep and goat meat. The sharpest increase is forecasted for poultry meat with 11.4 %, which

combined with a production growing by around 8.2 % reduces somewhat EU’s position as a net exporter.

Growth in pork meat is less pronounced both in human consumption and supply, but leaves the EU with

net exports of about 1.26 Mio t, not much different from the base year.

For the EU, supply of beef (-6.6 %), veal (-3.7 %) and sheep and goat meet (-6 %) are expected to drop

under the MTR proposal, whereas pork and poultry meat remain stable. A slight drop in meat

consumption (-0.02 %) results from increased consumer prices (0.8 %). Whereas pork and poultry meat

consumer prices are stable, reduced supply from the cattle chain raises farm gate prices for beef by 5.6 %

and consumer prices by 2 %. The price shift is accompanied by a consumption shift from beef and veal

(-0.8 %) to pig (0.1°%) and poultry (0.3°%).

11

Table 5. Market balance sheet for beef products in Spain (1000t)

Product

Balances:

4800 192 4752 138

5.07% -11.11% -1.00% -28.03%

5.88% 0.13%

593 55 538 554 19 534

-4.18% 1.81% -4.75% -6.68% -64.80% -0.74%

18 0 18 18 1 18

-13.88% -109.07% -4.78% 3.17% 426.93% -0.74%

2872 226 2647 2877 228 2649

6.99% 5.16% 7.15% 0.17% 1.00% 0.10%

243 5 237 226 -12 237

-1.01% -25.87% -0.27% -6.95% -323.12% 0.03%

1074 -94 1168 1077 -98 1175

7.55% -52.82% 10.16% 0.27% -4.57% 0.61%

MTR unchanged dairy policy [2009]Agenda reference run [2009]Base year [1998]

4614

Net trade DemandSupply

-61 1060

Poultry

meat 999

7 238

Sheep and

goat meat 245

215 2470Pork meat 2685

2 19Veal 20

Beef 619 54 565

Demand

Meat 4569 216 4352

ESPAÑA Supply Net trade Demand

4608

Supply Net trade

The market balance sheet for meat in Spain presents similar trends as the one for the European Union.

Overall supply of meat in the reference run increases slightly less (5%) than the European average. The

expansion is mostly due to increases in pork and beef production. Beef meat supply is expected to

decrease a little bit stronger than for the EU, accompanied by more pronounced drops in demand for beef

and veal. In opposite to dairy products, the MTR proposal will affect the meat supply, whereas demand

remains far more stable due to high marketing margins between producer and consumer prices. Especially

beef production processes are affected by the MTR proposal, mainly by the shift in premium allocation

from a per head basis to a decoupled area payment. Reduced herd sizes, especially for suckler cows,

decrease meat supply and provokes increases in producer price for beef by +5.4%.

4.1.3. Impact on agricultural income, budget and welfare

As discussed above, almost all prices for agricultural outputs are forecasted to fall in real terms in the

reference run for the EU. As seen in table 6, output value from agricultural production at EU level is

forecasted to drop by –7.3 %, whereas input value decreases by –1.3 %, mostly due to falling prices for

feeding stuff. Overall, gross value added at basic prices (agricultural income) reaches 146.7 Billion €, a

decrease in real terms of around –12.2 %. Given long term trends in the agricultural labour force, income

per AWU in agriculture could still increase in real terms. Consumers gain from decreasing consumer

prices in the reference run – a long term trend as cost reductions in agriculture reduce food prices.

Total premium payments decrease by -8.5°% in the MTR run. Agricultural income nevertheless stays

stable, as input drops by some –3.2°% in value whereas output value falls by –1.3°% only as prices

increase. Consumer losses due to slight increasing prices are offset by stronger savings in the FEOGA

budget. Overall, welfare is almost not affected. A more detailed view on the FEOGA budget positions

shows a shift in the compensation payments from cereals and oilseeds to fodder crops on arable land. The

MTR proposal foresees the transfer of budget savings of the modulation from the first to the second pillar

As far as farmers benefit from increased rural development programs, that could offset income losses from

the modulation.

12

Table 6. Welfare analysis for EU and Spain (Mio €)

Base year Reference

run MTR Base year

Reference

runMTR

EU EU EU ESPAÑA ESPAÑA ESPAÑA

31126 2976

1 -6.43% -6.60%

27666 25198 2793 2585

2 -2.78% -8.92% -12.94% -7.46%

308466 304448 35592 35143

3 -7.34% -1.30% -10.72% -1.26%

189132 182997 16321 15859

7 -1.31% -3.24% -4.58% -2.83%

27399 25082 2768 2577

11 5.99% -8.46% -8.23% -6.92%

146733 146533 22039 21861

12=3-7+11 -12.20% -0.14% -14.50% -0.81%

152461 22252

13=1-2+12 152332 0.08% 22432 -0.80%

17104

3017

25777

22568

3186

3209

39864

Equivalent

variation

Feoga

budget

33265

28457

EAA Output 332902

EAA Input 191634

Premiums 25850

Agricultural

income 167118

Total 138661

For Spain the welfare analysis shows a decrease in agricultural income of –14.5% in the reference run

under Agenda policy. This is slightly more than the EU average. In opposite to the EU average,

modifications in the premium scheme lead to a reduction in overall premium payments for Spain

originating from the animal sector. Increasing payments to the beef and cattle in the Spanish meat sector

(+150% compared to only 130% at EU average), mostly due to the newly introduced dairy cow payment

cannot offset the reduced premiums to the sheep & goat sector. This explains, why the FEOGA budget

reduction in the Agenda reference run is so pronounced in Spain. Crop production has to face cuts in area

premium payments which cannot be compensated by the newly introduced cattle and dairy cow premiums,

due to lower production density in the national average. Decreasing consumer prices cannot offset the

welfare effect of decreased agricultural income.

Overall welfare change in the MTR proposal is small hiding a redistribution within the agricultural sector

and a shift of budget positions from the first to the second pillar. As consumers loose slightly more than

the EU average, in opposite to the EU result a small welfare loss can be observed.

The following map shows the changes in premium payments per hectare at NUTS°2 level for the EU from

reference run to MTR proposal. Compared to the foreseen 18°% drop in premiums due to modulation, the

overall cut is smaller as (a) part of the premiums e.g. national envelopes are not included in the

modulation and (b) farm specific ceilings prevent a full cut for included ones. Therefore, especially

regions with high cattle density will be at the lower end of premium reductions.

13

Map 1 Comparison of changes in total premium payments per hectare, MTR against

Agenda 2000

Note: From dark green to light green: between –21°% and -10°%, white around -9°% and from light red to dark red between –

2°% and 26°% income per hectare. Percentage changes with respect to Agenda 2000 reference run.

4.2. Developments in regional production structure in Spain

In this section, developments in the production structure of Spain will be presented. As the CAPRI model

is designed to work on NUTS II level, data and simulation results can be consistently provided on a

detailed regional level. A selection of the available data with special focus on dairy and suckler cow

activities will be reported in this section.

4.2.1. Herd size and regional income for cattle activities

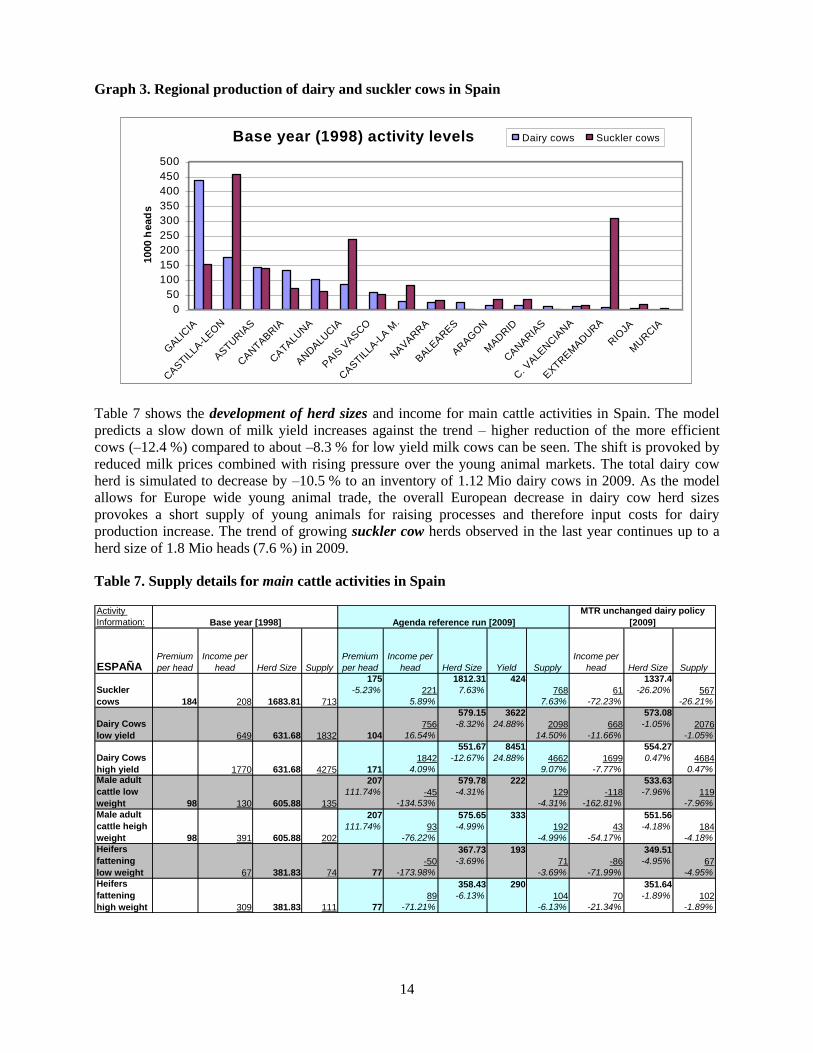

The base period of the model is a three-year-average around 1998. The following graph shows regional

herd sizes for dairy and suckler cow herds. The milk production is focused in northern regions. Galicia is

by far themost important region with twice the number of dairy cows than the next important region

Castilla-Leon. High suckler cow herds are found in Castilla-Leon but also in the center and south of Spain,

namely Extremadura and Andalucia.

14

Graph 3. Regional production of dairy and suckler cows in Spain

Base year (1998) activity levels

0

50

100

150

200

250

300

350

400

450

500

GALI

CIA

CASTIL

LA-L

EO

N

ASTU

RIA

S

CANTA

BRIA

CATA

LUNA

ANDALU

CIA

PAIS

VASCO

CASTIL

LA-L

A M

.

NAVARRA

BALE

ARES

ARAG

ON

MADRID

CANARIA

S

C. V

ALE

NCIA

NA

EXTR

EM

ADURA

RIO

JA

MURCIA

10

00

hea

ds

Dairy cows Suckler cows

Table 7 shows the development of herd sizes and income for main cattle activities in Spain. The model

predicts a slow down of milk yield increases against the trend – higher reduction of the more efficient

cows (–12.4 %) compared to about –8.3 % for low yield milk cows can be seen. The shift is provoked by

reduced milk prices combined with rising pressure over the young animal markets. The total dairy cow

herd is simulated to decrease by –10.5 % to an inventory of 1.12 Mio dairy cows in 2009. As the model

allows for Europe wide young animal trade, the overall European decrease in dairy cow herd sizes

provokes a short supply of young animals for raising processes and therefore input costs for dairy

production increase. The trend of growing suckler cow herds observed in the last year continues up to a

herd size of 1.8 Mio heads (7.6 %) in 2009.

Table 7. Supply details for main cattle activities in Spain

Activity

Information:

175 1812.31 424 1337.4

-5.23% 7.63% -26.20%

5.89% 7.63% -72.23% -26.21%

579.15 3622 573.08

-8.32% 24.88% -1.05%

16.54% 14.50% -11.66% -1.05%

551.67 8451 554.27

-12.67% 24.88% 0.47%

4.09% 9.07% -7.77% 0.47%

207 579.78 222 533.63

111.74% -4.31% -7.96%

-134.53% -4.31% -162.81% -7.96%

207 575.65 333 551.56

111.74% -4.99% -4.18%

-76.22% -4.99% -54.17% -4.18%

367.73 193 349.51

-3.69% -4.95%

-173.98% -3.69% -71.99% -4.95%

358.43 290 351.64

-6.13% -1.89%

-71.21% -6.13% -21.34% -1.89%

SupplyESPAÑAPremium

per head

Income per

head Herd Size Supply

Premium

per head

Income per

head Herd Size Yield

Suckler

cows 184 208 1683.81 713

221 768

631.68 1832

Dairy Cows

low yield 649

Dairy Cows

high yield 1770

4662

104

756 2098

1842

4275

-45

631.68Male adult

cattle low

weight 98 130

171

Heifers

fattening

high weight

129

Male adult

cattle heigh

weight 98 391 605.88 202

605.88 135

93 192

Heifers

fattening

low weight 67 381.83 74

309 381.83 77

89

111

104

77

-50 71

Supply

Income per

head Herd Size

56761

119

1699 4684

668 2076

Base year [1998]

70 102

Agenda reference run [2009]

MTR unchanged dairy policy

[2009]

-86 67

43 184

-118

15

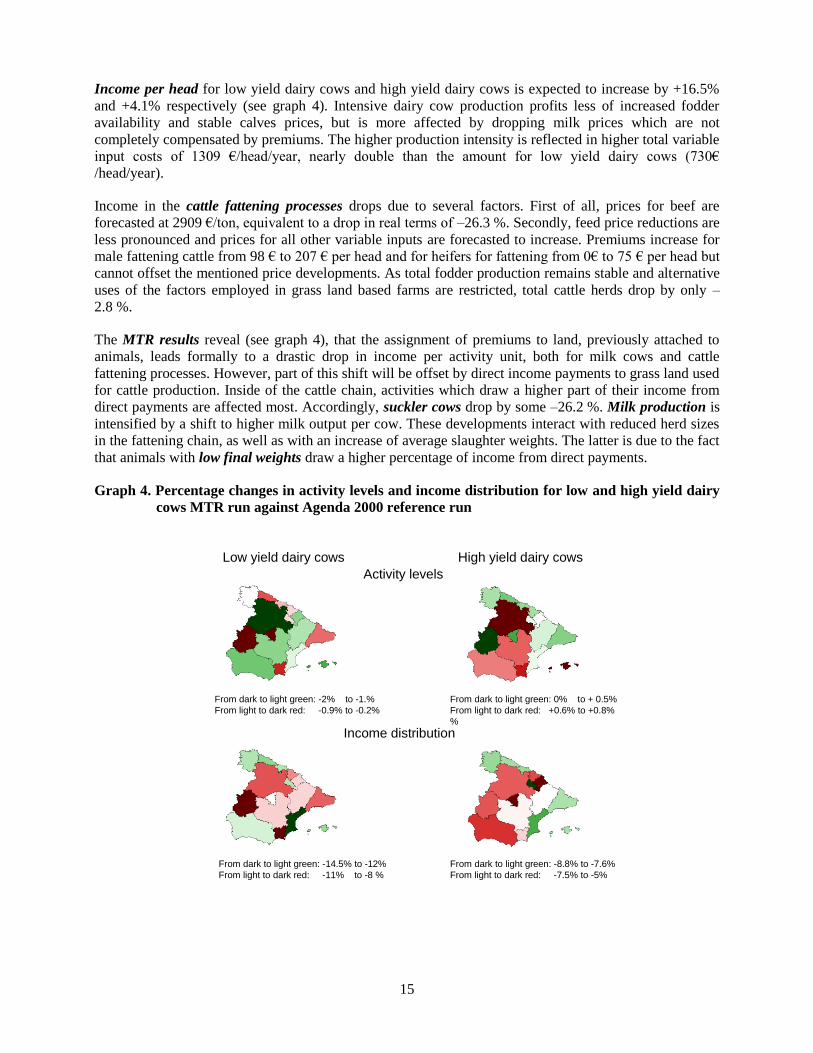

Income per head for low yield dairy cows and high yield dairy cows is expected to increase by +16.5%

and +4.1% respectively (see graph 4). Intensive dairy cow production profits less of increased fodder

availability and stable calves prices, but is more affected by dropping milk prices which are not

completely compensated by premiums. The higher production intensity is reflected in higher total variable

input costs of 1309 €/head/year, nearly double than the amount for low yield dairy cows (730€

/head/year).

Income in the cattle fattening processes drops due to several factors. First of all, prices for beef are

forecasted at 2909 €/ton, equivalent to a drop in real terms of –26.3 %. Secondly, feed price reductions are

less pronounced and prices for all other variable inputs are forecasted to increase. Premiums increase for

male fattening cattle from 98 € to 207 € per head and for heifers for fattening from 0€ to 75 € per head but

cannot offset the mentioned price developments. As total fodder production remains stable and alternative

uses of the factors employed in grass land based farms are restricted, total cattle herds drop by only –

2.8 %.

The MTR results reveal (see graph 4), that the assignment of premiums to land, previously attached to

animals, leads formally to a drastic drop in income per activity unit, both for milk cows and cattle

fattening processes. However, part of this shift will be offset by direct income payments to grass land used

for cattle production. Inside of the cattle chain, activities which draw a higher part of their income from

direct payments are affected most. Accordingly, suckler cows drop by some –26.2 %. Milk production is

intensified by a shift to higher milk output per cow. These developments interact with reduced herd sizes

in the fattening chain, as well as with an increase of average slaughter weights. The latter is due to the fact

that animals with low final weights draw a higher percentage of income from direct payments.

Graph 4. Percentage changes in activity levels and income distribution for low and high yield dairy

cows MTR run against Agenda 2000 reference run

Low yield dairy cows High yield dairy cows

Activity levels

Income distribution

From dark to light green: -2% to -1.%

From light to dark red: -0.9% to -0.2%

From dark to light green: -14.5% to -12%

From light to dark red: -11% to -8 %

From dark to light green: -8.8% to -7.6%

From light to dark red: -7.5% to -5%

From dark to light green: 0% to + 0.5%

From light to dark red: +0.6% to +0.8%

%

16

4.2.2. Trends on young animal markets

The mathematical programming approach on the supply side of the model allows to assess the impacts of

policy or price changes in the cattle chain. When looking at young animal markets, it is important to note,

that the model allows to trade young animals within the EU. As shown in table 8, reduced cow herds in

Spain allow to reduce the number of female and male raised calves (-4.9% and –1.7% respectively) and

heifers (-8%) in the reference run. Reduced meat prices combined with less calves born affect the calves

fattening processes as well, which drop by around -15%.

The reduction in both the beef fattening processes and suckler cows with premiums allocated to grass land

under the MTR proposal reduces the demand for calves in the EU, and therefore the number of raised

calves and heifers drops further.

Table 8. Supply details for young animal activities in Spain

Activity

Information:

354.89 328.91

-8.15% -7.32%

-30.26% -8.15% -31.51% -7.32%

34.51 256 36.41

-16.13% 5.50%

-68.73% -16.11% 40.24% 5.51%

16.31 538 16.44

-11.50% 0.82%

-36.26% -11.50% -0.69% 0.82%

1214.85 1101.93

-1.77% -9.30%

-3.53% -1.77% -15.13% -9.30%

1103.85 1040.93

-4.93% -5.70%

-9.97% -4.93% -9.62% -5.70%

Base year [1998] Agenda reference run [2009]

MTR unchanged dairy policy

[2009]

ESPAÑAPremium

per head

Income per

head Herd Size Supply

Premium

per head

Income per

head Herd Size SupplyHerd Size Yield Supply

Income per

head

Heifers

breeding 381 386.4 386

266 355 182 329

Fattening

male calves 356 41.15 11 25

111 9 156 9

Fattening

female

calves 1086 18.43 10 25

692 9 687 9

Raising

male calves 429 1236.69 1237

414 1215

1161

327 1104

Raising

female

Calves 363 1161.11

296 1041

351 1102

5. Conclusions

Medium term drivers in European dairy markets are the developments of consumption patterns and CAP

instruments. With the quota system unharmed by both the Agenda 2000 package and the MTR proposal,

and quota quantities almost unchanged, price developments for dairy products reflect the interaction

between consumption trends towards low-fat dairy products and cheese, and market interventions

depending on administrative price levels. In the reference run, reflecting the Agenda 2000 package, cuts in

administrative prices for butter and skimmed milk powder let market prices decrease, and producer

income drops despite the introduction of compensation payments.

The MTR proposal from July 2002 certainly leads to a higher market orientation of European farmers.

Due to less coupled premiums, allocation efficiency increases with farming decisions closer linked to

market prices. Additionally, the proposal reduces scope and frequency of market interventions as

intervention prices are further reduced below expected average world market prices. However, a stronger

European currency or temporary imbalances in world markets could still provoke a built up of intervention

stocks. The continuation of the CAP reform path of shifting from price to direct income support further

detaches budget outlays from market developments and stabilises the FEOGA budget as direct support is

bounded to value ceilings.

In the recently published draft of legal texts for the MTR proposals (Commission of the European

Communities 2003) the European Commission suggests the prolongation of the system of dairy reference

quantities until the year 2014/15 combined with a 1% quota increase in the years 2007/8. An additional

asymmetric price cut for skimmed milk powder (-3.5%) and butter (-7%) beyond Agenda 2000 is

17

foreseen, stepwise over five years. Based on the simulation results for the MTR package as defined last

summer, the additional stipulations are not likely to change the picture dramatically. The quota increase

will depress somewhat prices, and hence trigger additional demand. Higher market interventions are

unlikely, as administrative prices are further reduced, so that the FEOGA budget should not be affected.

Producers will gain from increased milk quantities, and loose somewhat from lower prices. If cleverly

managed, the higher quotas could help some farmers to profit from scale effects and speed up structural

adjustments. Increased dairy cow herds will depress calves’ prices, and are likely to reduce the suckler

cow herd.

Even if the model does not feature back- and forward linkages with other sectors of the economy, it should

be noted that both agricultural output in quantities and values as well as input use are reduced under the

MTR proposal affecting rural economic activities linked to agriculture, but counteracted by higher budgets

for rural development under the second pillar resulting from modulation.

6. References

Commission of the European Communities (2002): Mid-Term Review of the Common Agricultural Policy,

Communication from the Commission to the Council and the European Parliament, 10.7.02, COM(2002) 394,

Brussels.

Commission of the European Communities (2002a): Report on Milk Quotas, Commission working document,

SEC(2002) 789 final.

Commission of the European Communities (2003): Proposal for a Council Regulation establishing common rules for

direct support schemes under the common agricultural policy and support schemes for producers of certain

crops, 21.1.2003 COM(2003) 23 final.

European Commission Directorate for Agriculture (2000): The CAP reform: Milk and Milk products, Brussels

European Commission Directorate for Agriculture (2002): Prospects for Agricultural Markets 2002-2009,

Luxembourg: Office for Official Publications of the European Communities.

European Commission Directorate for Agriculture (2000): Agenda 2000 CAP Reform decisions - Impact Analyses,

Luxembourg: Office for Official Publications of the European Communities.

FAPRI (2002): World Agricultural Outlook. Iowa State University – University of Missouri-Columbia

INRA-WAGENINGEN (2002): Study on the impact of future options for the Milk Quota system and the common

market organisation for milk and milk products, INRA Consortium – University of Wageningen.