Embed Size (px)

Citation preview

154

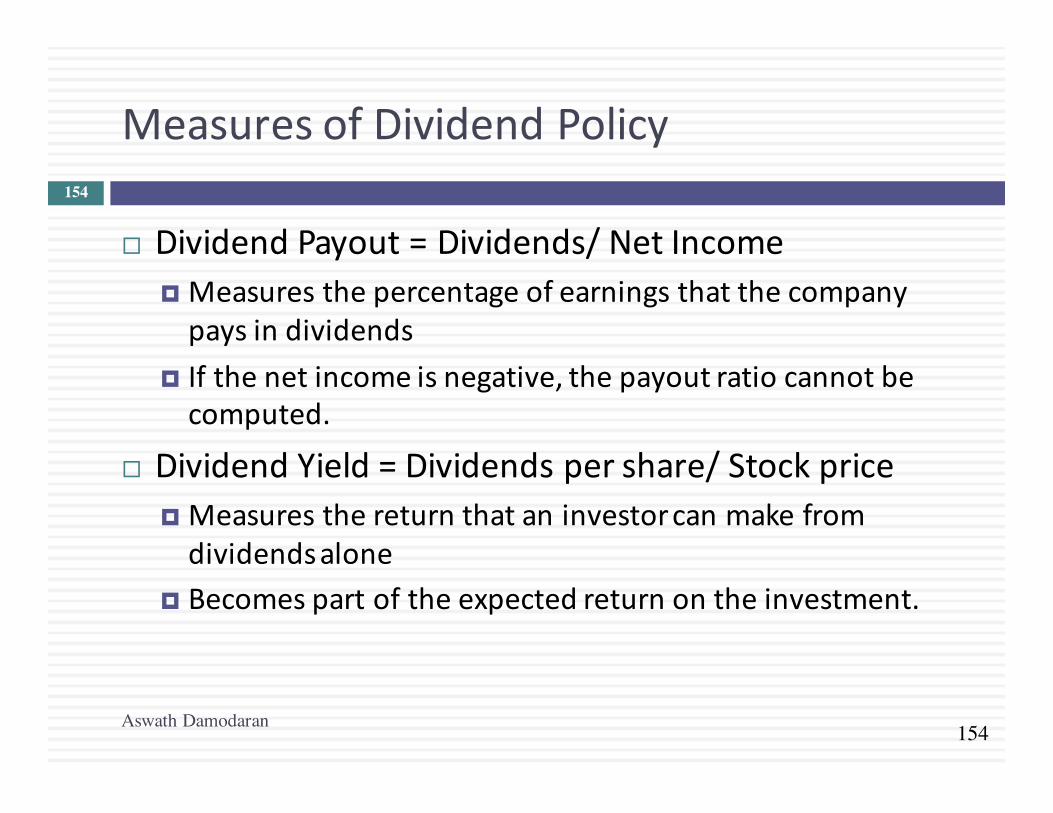

MeasuresofDividendPolicy

Aswath Damodaran

154

¨ DividendPayout=Dividends/NetIncome¤ Measuresthepercentageofearningsthatthecompanypaysindividends

¤ Ifthenetincomeisnegative,thepayoutratiocannotbecomputed.

¨ DividendYield=Dividendspershare/Stockprice¤ Measuresthereturnthataninvestorcanmakefromdividendsalone

¤ Becomespartoftheexpectedreturnontheinvestment.

155

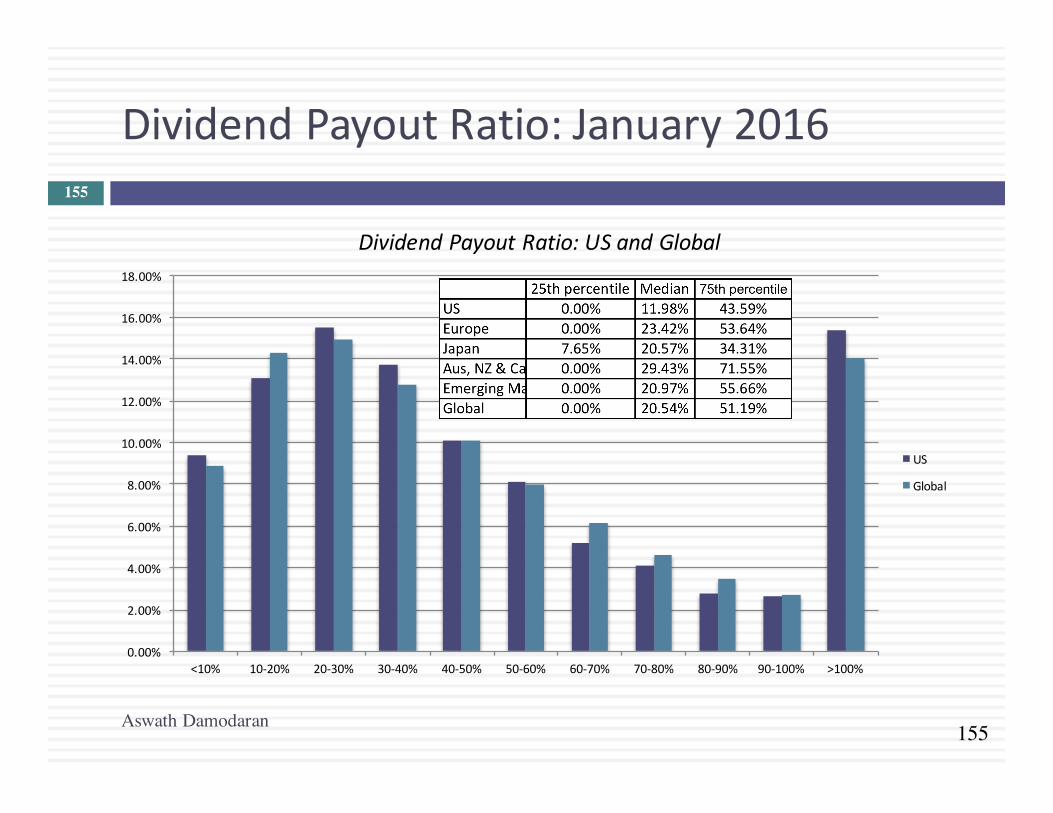

DividendPayoutRatio:January2016

Aswath Damodaran

155

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

<10% 10-20% 20-30% 30-40% 40-50% 50-60% 60-70% 70-80% 80-90% 90-100% >100%

DividendPayoutRatio:USandGlobal

US

Global

156

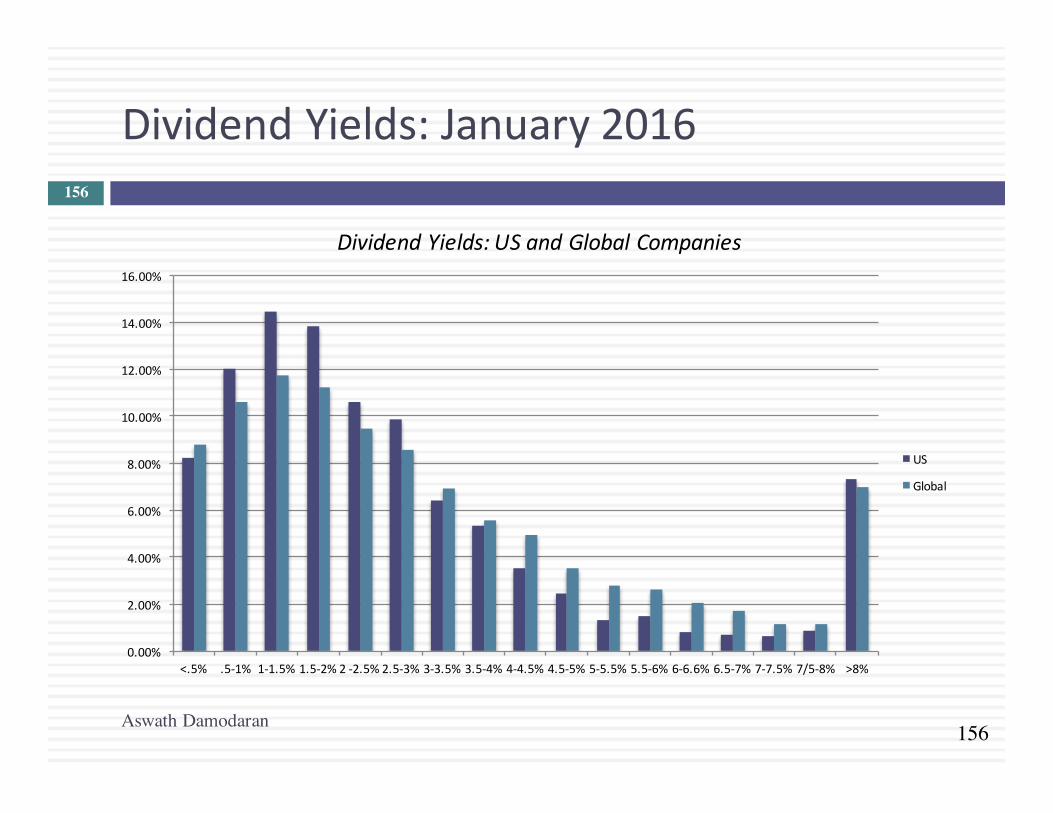

DividendYields:January2016

Aswath Damodaran

156

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

<.5% .5-1% 1-1.5% 1.5-2% 2-2.5% 2.5-3% 3-3.5% 3.5-4% 4-4.5% 4.5-5% 5-5.5% 5.5-6% 6-6.6% 6.5-7% 7-7.5% 7/5-8% >8%

DividendYields:USandGlobalCompanies

US

Global

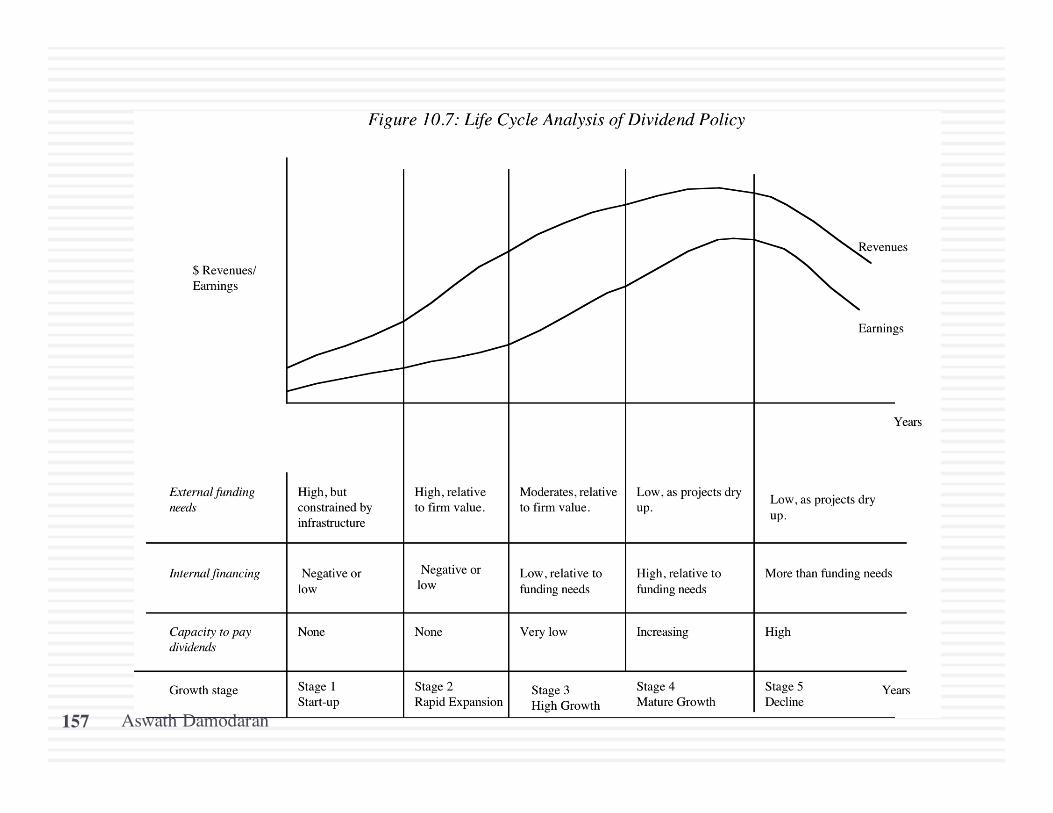

Aswath Damodaran157

158

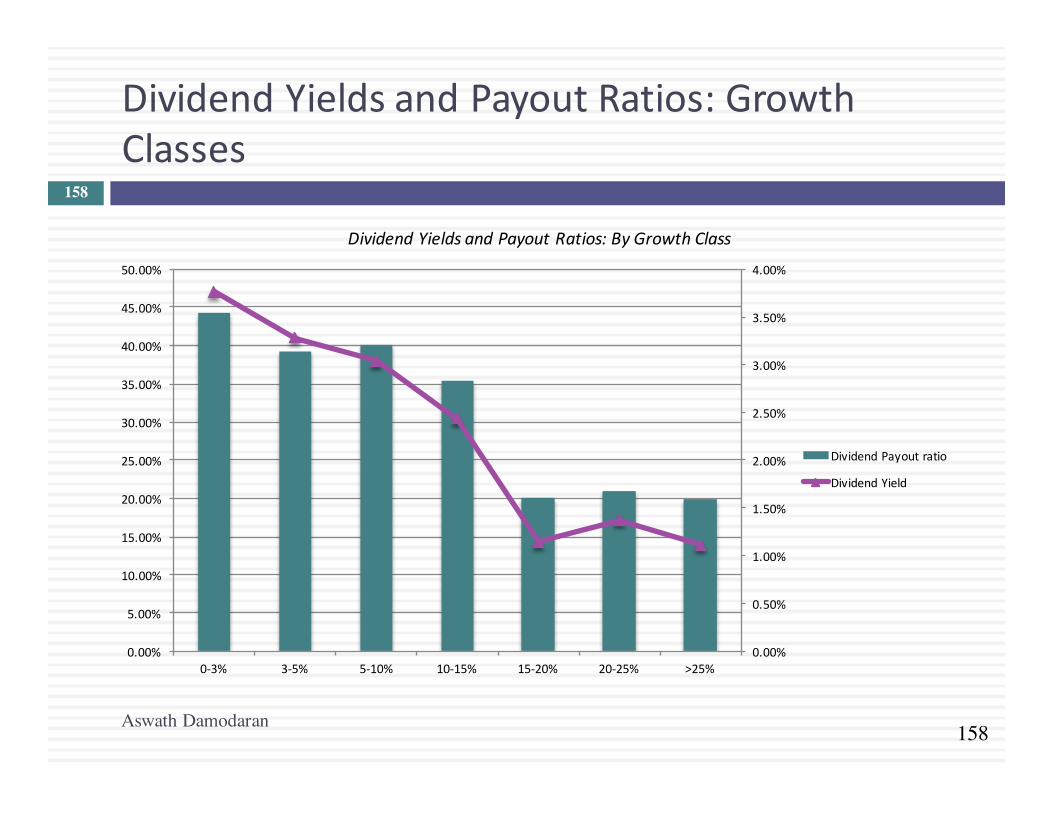

DividendYieldsandPayoutRatios:GrowthClasses

Aswath Damodaran

158

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

50.00%

0-3% 3-5% 5-10% 10-15% 15-20% 20-25% >25%

DividendYieldsandPayoutRatios:ByGrowthClass

DividendPayoutratio

DividendYield

159

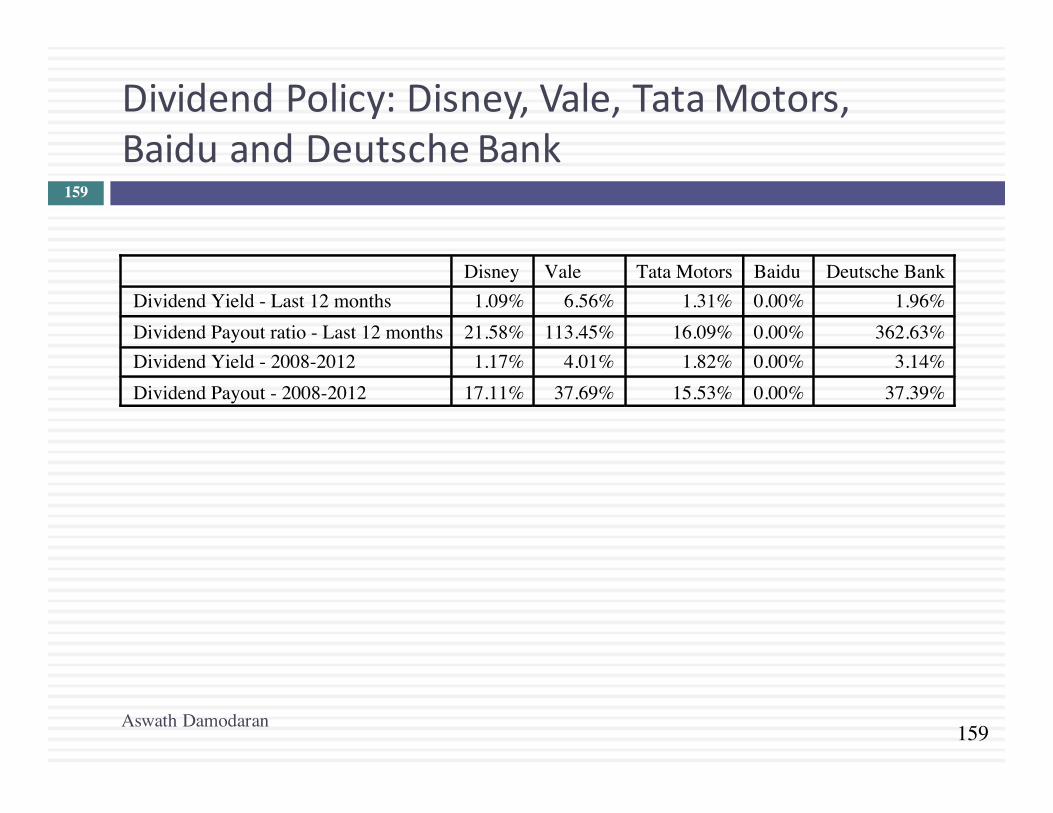

DividendPolicy:Disney,Vale,TataMotors,Baidu andDeutscheBank

Aswath Damodaran

159

Disney Vale Tata Motors Baidu Deutsche Bank Dividend Yield - Last 12 months 1.09% 6.56% 1.31% 0.00% 1.96% Dividend Payout ratio - Last 12 months 21.58% 113.45% 16.09% 0.00% 362.63% Dividend Yield - 2008-2012 1.17% 4.01% 1.82% 0.00% 3.14% Dividend Payout - 2008-2012 17.11% 37.69% 15.53% 0.00% 37.39%

160

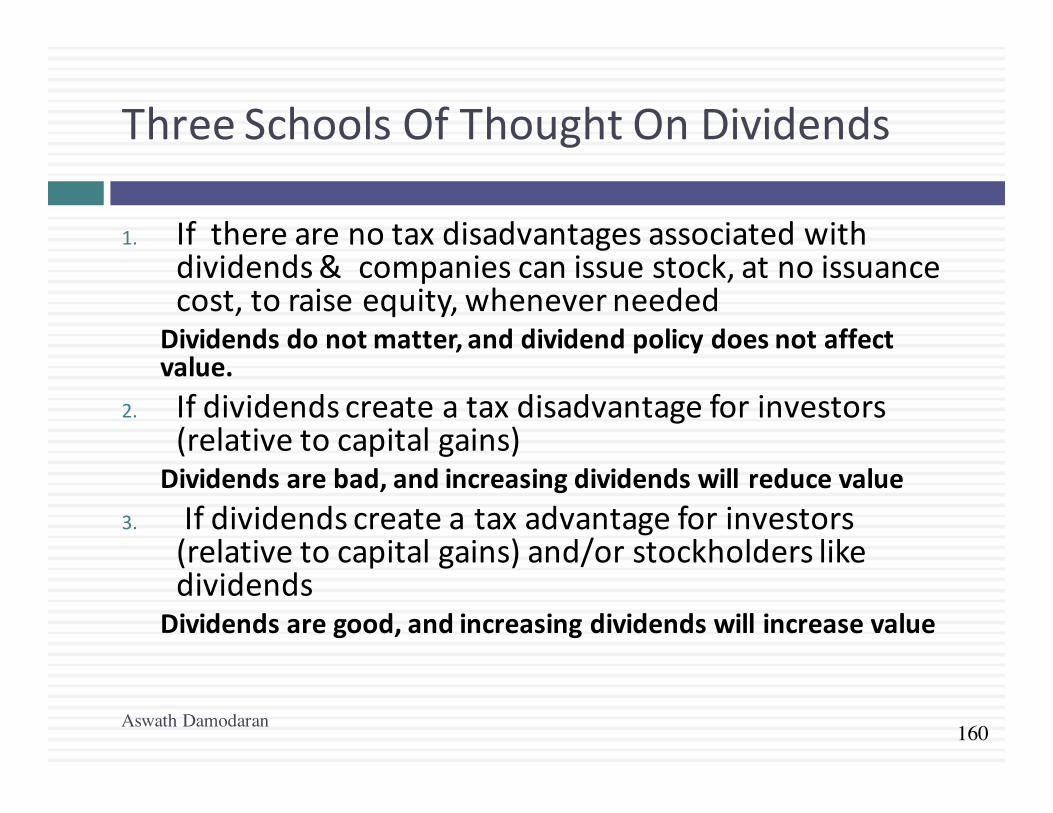

ThreeSchoolsOfThoughtOnDividends

1. Iftherearenotaxdisadvantagesassociatedwithdividends& companiescanissuestock,atnoissuancecost,toraiseequity,wheneverneeded

Dividendsdonotmatter,anddividendpolicydoesnotaffectvalue.

2. Ifdividendscreateataxdisadvantageforinvestors(relativetocapitalgains)

Dividendsarebad,andincreasingdividendswill reducevalue3. Ifdividendscreateataxadvantageforinvestors

(relativetocapitalgains)and/orstockholderslikedividends

Dividendsaregood,andincreasingdividendswillincreasevalue

Aswath Damodaran

161

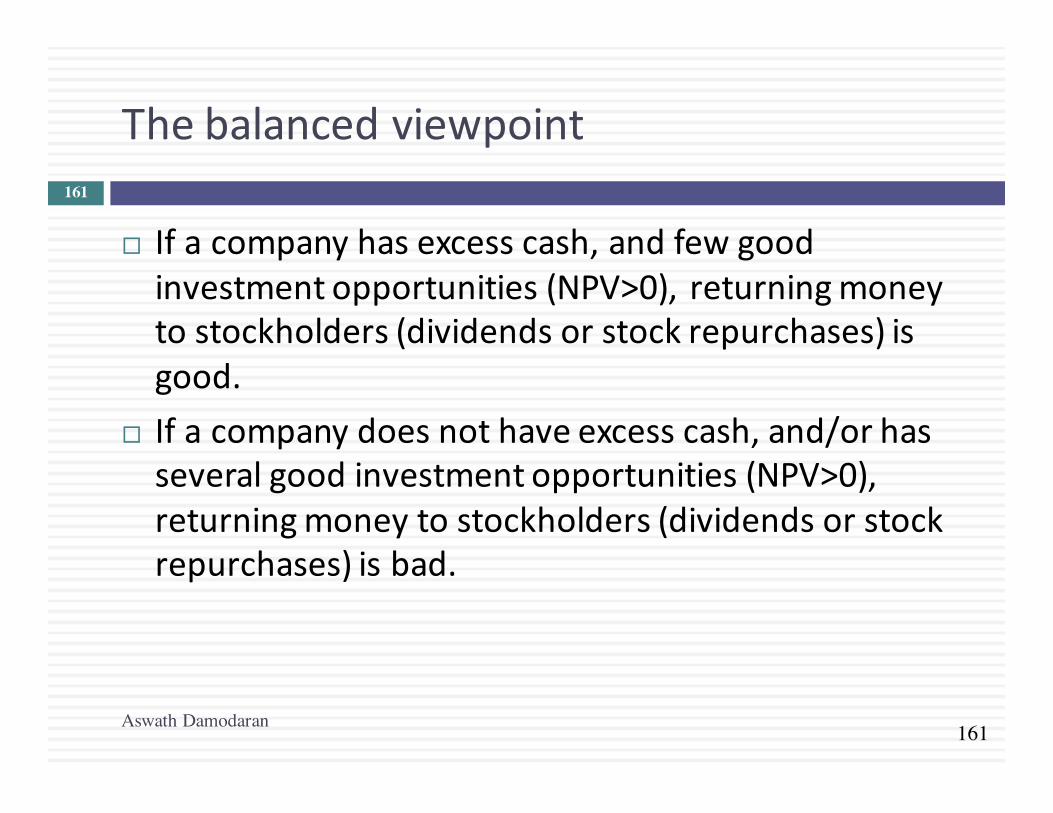

Thebalancedviewpoint

Aswath Damodaran

161

¨ Ifacompanyhasexcesscash,andfewgoodinvestmentopportunities(NPV>0), returningmoneytostockholders(dividendsorstockrepurchases)isgood.

¨ Ifacompanydoesnothaveexcesscash,and/orhasseveralgoodinvestmentopportunities(NPV>0),returningmoneytostockholders(dividendsorstockrepurchases)isbad.

162

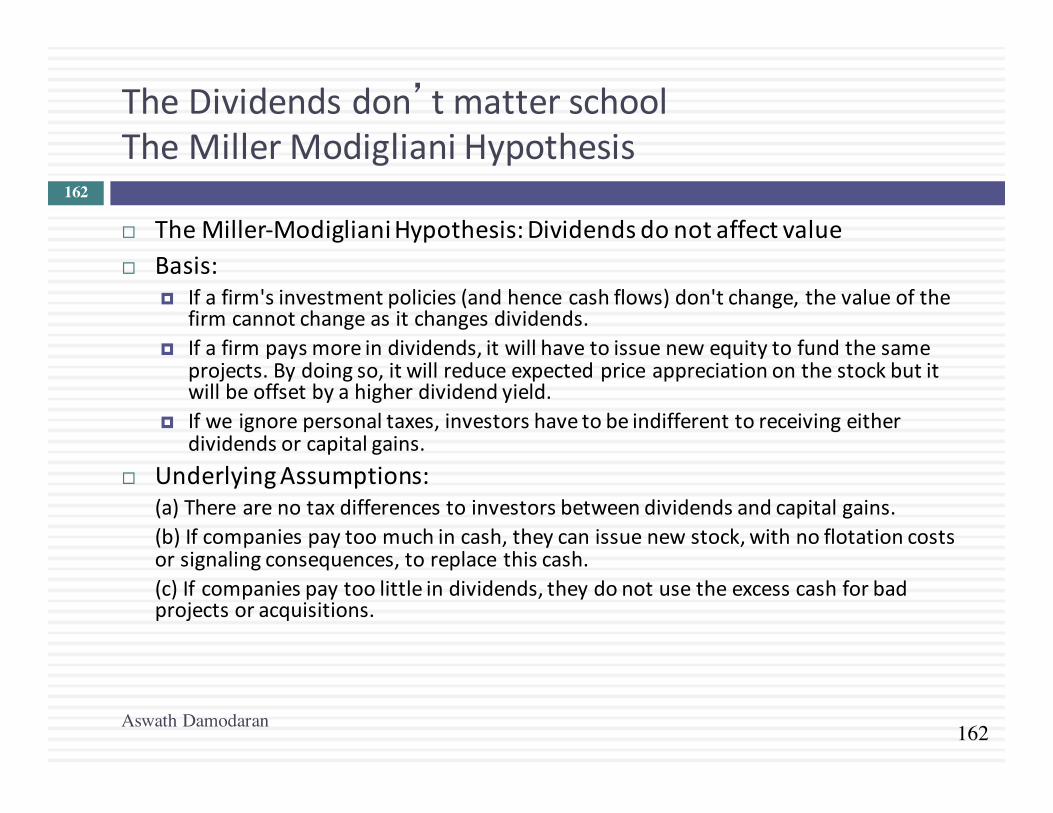

TheDividendsdon’tmatterschoolTheMillerModiglianiHypothesis

Aswath Damodaran

162

¨ TheMiller-ModiglianiHypothesis:Dividendsdonotaffectvalue¨ Basis:

¤ Ifafirm'sinvestmentpolicies(andhencecashflows)don'tchange,thevalueofthefirmcannotchangeasitchangesdividends.

¤ Ifafirmpaysmoreindividends,itwillhavetoissuenewequitytofundthesameprojects.Bydoingso,itwillreduceexpectedpriceappreciationonthestockbutitwillbeoffsetbyahigherdividendyield.

¤ Ifweignorepersonaltaxes,investorshavetobeindifferenttoreceivingeitherdividendsorcapitalgains.

¨ UnderlyingAssumptions:(a)Therearenotaxdifferencestoinvestorsbetweendividendsandcapitalgains.(b)Ifcompaniespaytoomuchincash,theycanissuenewstock,withnoflotationcostsorsignalingconsequences,toreplacethiscash.(c)Ifcompaniespaytoolittleindividends,theydonotusetheexcesscashforbadprojectsoracquisitions.

163

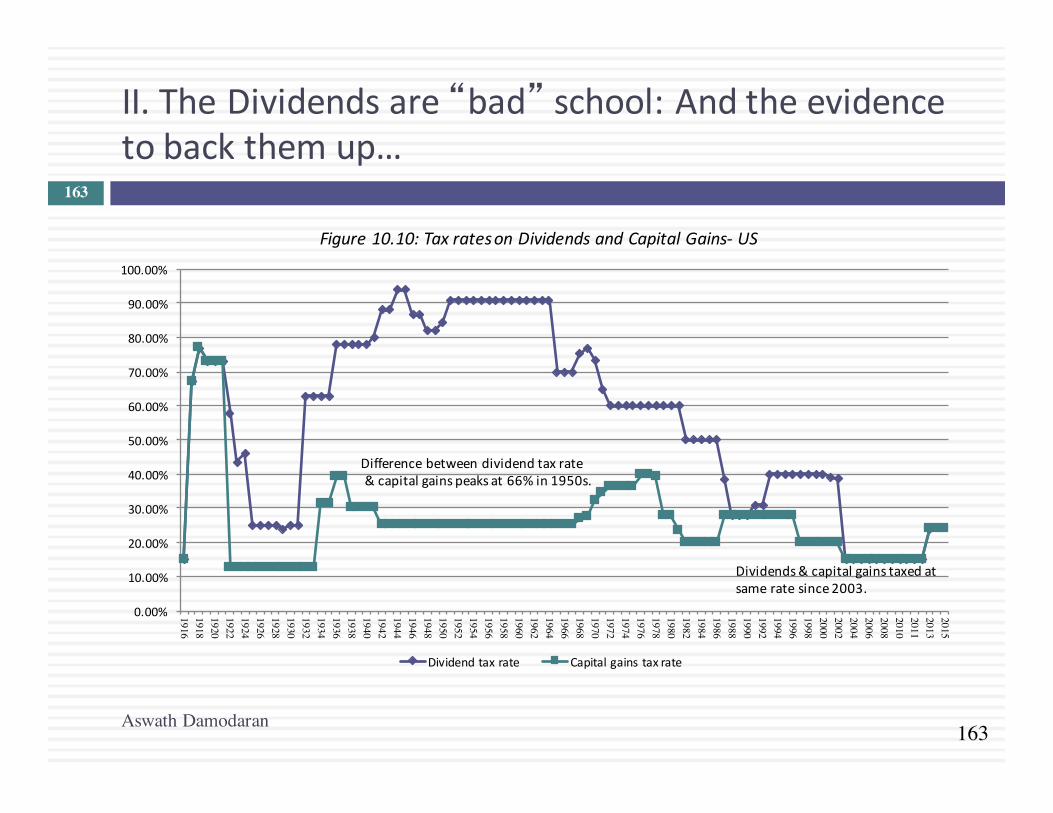

II.TheDividendsare“bad” school:Andtheevidencetobackthemup…

Aswath Damodaran

163

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

191619181920192219241926192819301932193419361938194019421944194619481950195219541956195819601962196419661968197019721974197619781980198219841986198819901992199419961998200020022004200620082010201120132015

Figure10.10:TaxratesonDividendsandCapitalGains- US

Dividendtaxrate Capitalgainstaxrate

Difference betweendividendtaxrate&capitalgainspeaksat66%in1950s.

Dividends&capital gainstaxedatsameratesince2003.

164

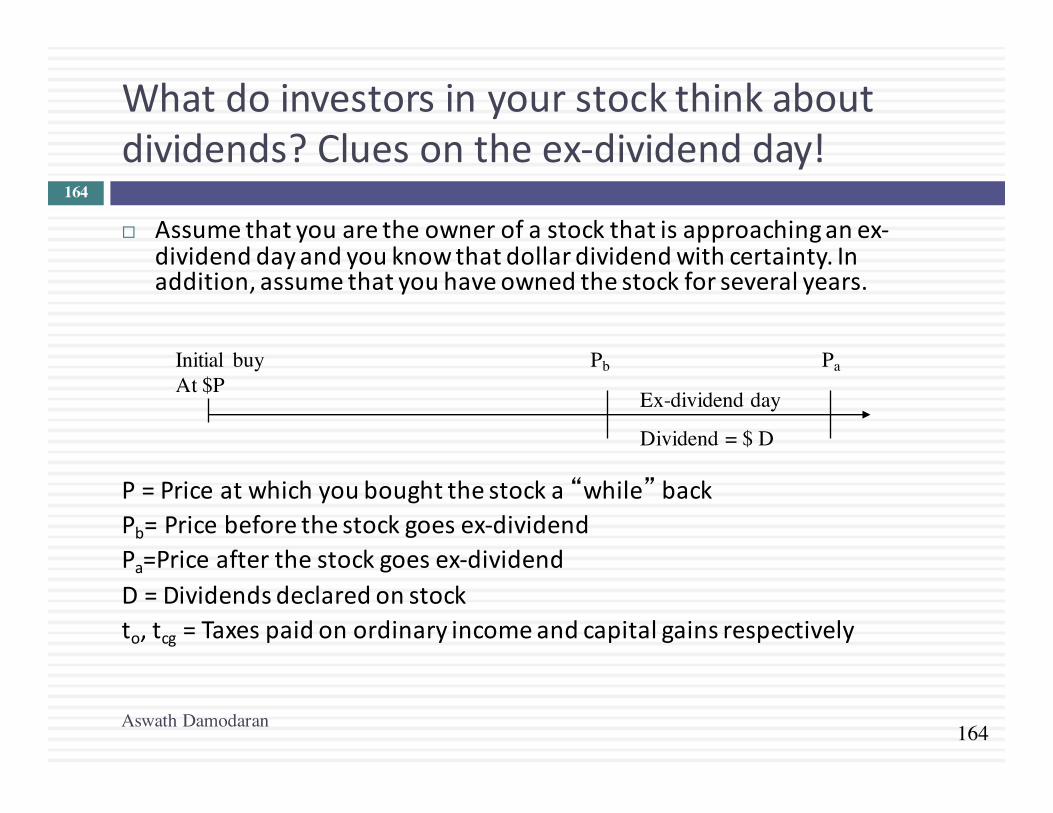

Whatdoinvestorsinyourstockthinkaboutdividends?Cluesontheex-dividendday!

Aswath Damodaran

164

¨ Assumethatyouaretheownerofastockthatisapproachinganex-dividenddayandyouknowthatdollardividendwithcertainty.Inaddition,assumethatyouhaveownedthestockforseveralyears.

P=Priceatwhichyouboughtthestocka“while” backPb=Pricebeforethestockgoesex-dividendPa=Priceafterthestockgoesex-dividendD=Dividendsdeclaredonstockto,tcg =Taxespaidonordinaryincomeandcapitalgainsrespectively

Ex-dividend day

Dividend = $ D

Initial buyAt $P

Pb Pa

165

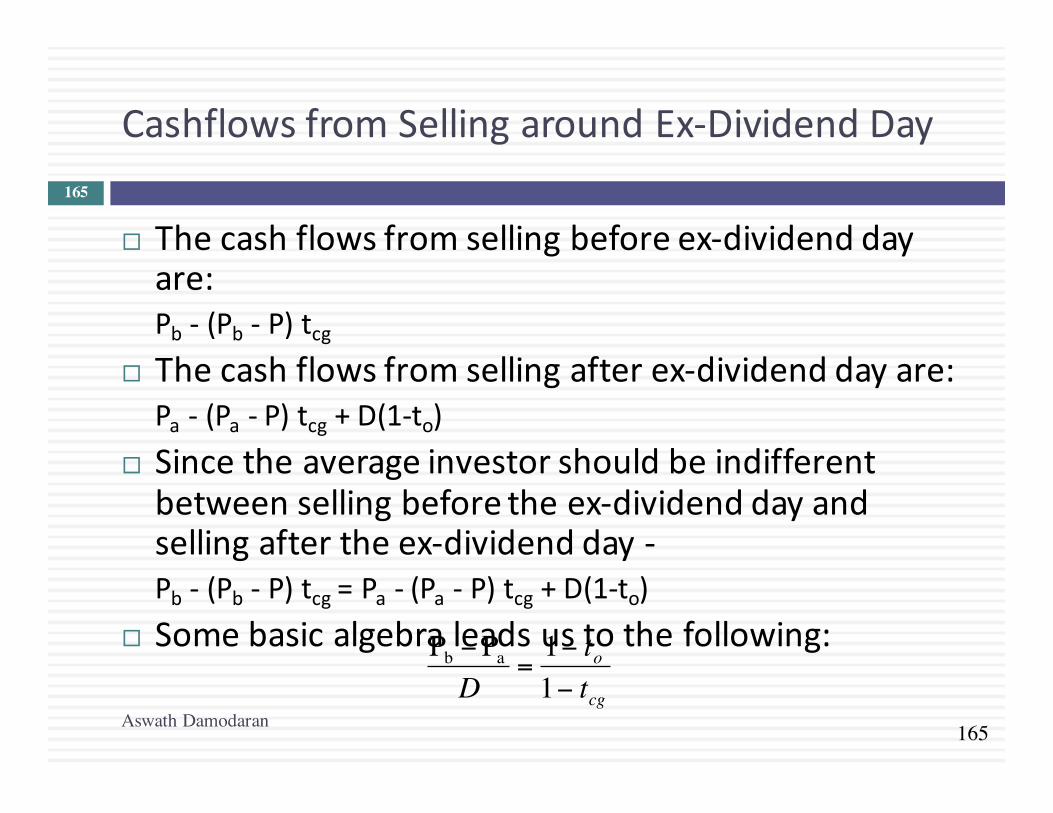

CashflowsfromSellingaroundEx-DividendDay

Aswath Damodaran

165

¨ Thecashflowsfromsellingbeforeex-dividenddayare:Pb - (Pb - P)tcg

¨ Thecashflowsfromsellingafterex-dividenddayare:Pa - (Pa - P)tcg +D(1-to)

¨ Sincetheaverageinvestorshouldbeindifferentbetweensellingbeforetheex-dividenddayandsellingaftertheex-dividendday-Pb - (Pb - P)tcg =Pa - (Pa - P)tcg +D(1-to)

¨ Somebasicalgebraleadsustothefollowing:

€

Pb −PaD

=1− to1− tcg

166

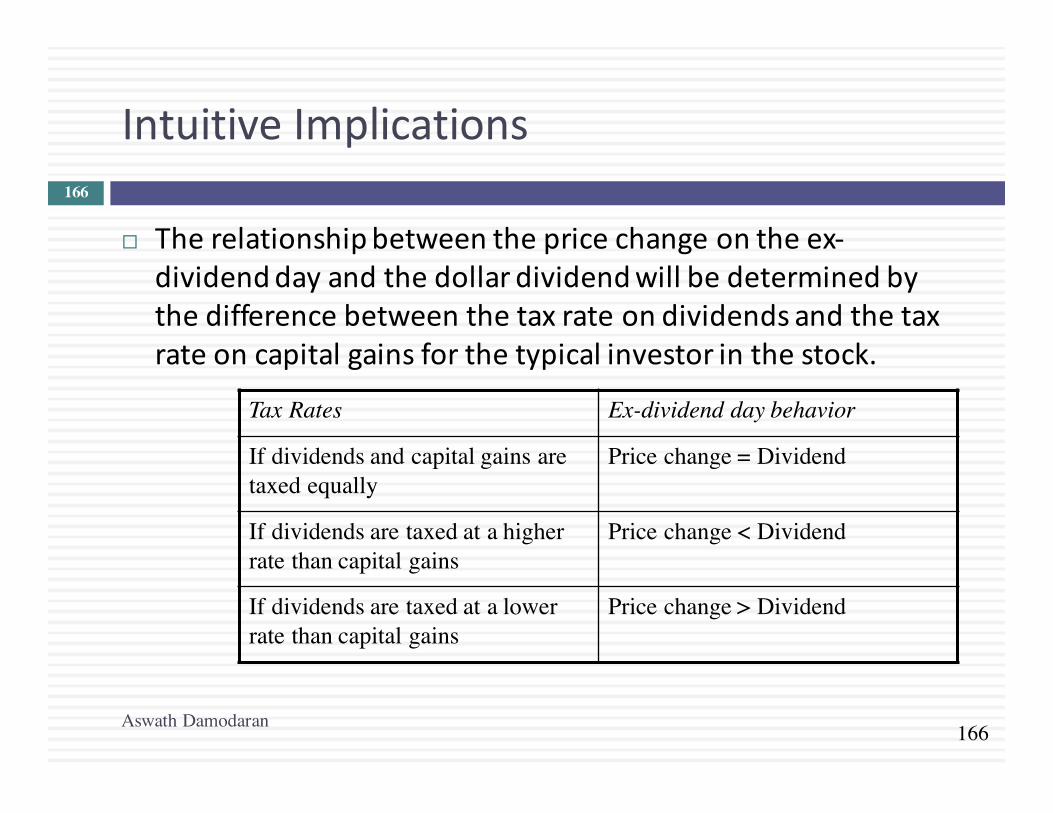

IntuitiveImplications

Aswath Damodaran

166

¨ Therelationshipbetweenthepricechangeontheex-dividenddayandthedollardividendwillbedeterminedbythedifferencebetweenthetaxrateondividendsandthetaxrateoncapitalgainsforthetypicalinvestorinthestock.

Tax Rates Ex-dividend day behavior

If dividends and capital gains are taxed equally

Price change = Dividend

If dividends are taxed at a higher rate than capital gains

Price change < Dividend

If dividends are taxed at a lower rate than capital gains

Price change > Dividend

167

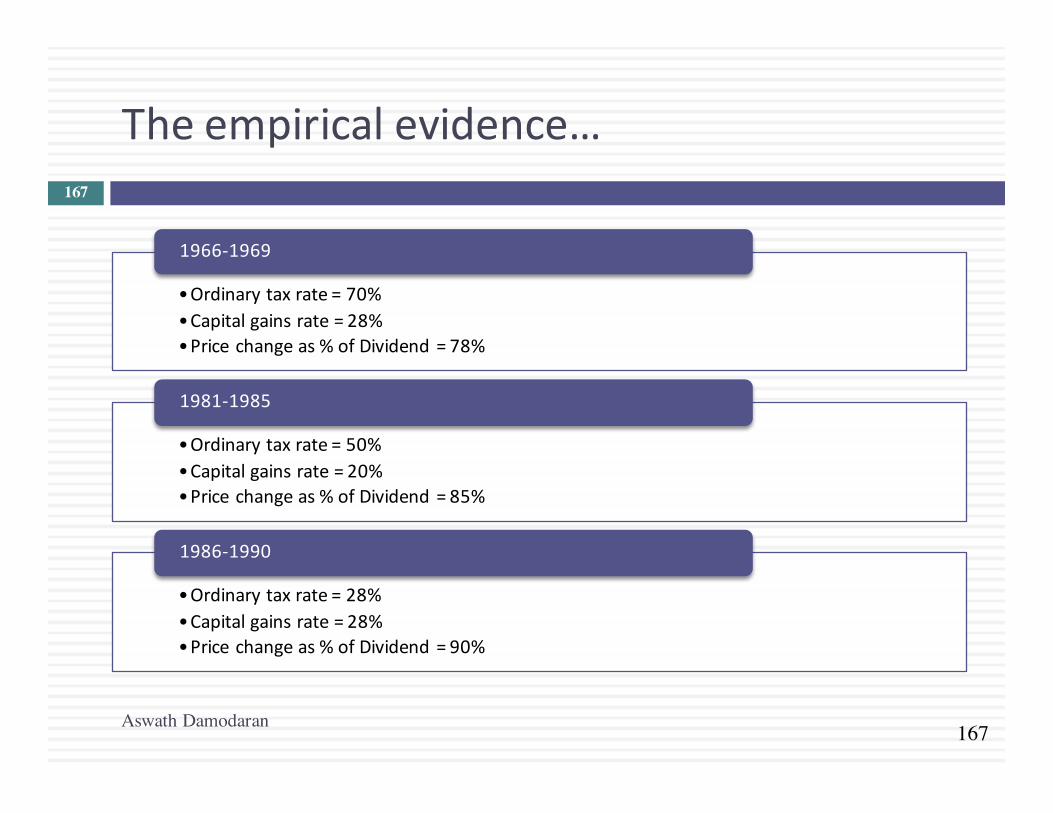

Theempiricalevidence…

Aswath Damodaran

167

•Ordinarytaxrate=70%•Capitalgainsrate=28%•Pricechangeas%ofDividend=78%

1966-1969

•Ordinarytaxrate=50%•Capitalgainsrate=20%•Pricechangeas%ofDividend=85%

1981-1985

•Ordinarytaxrate=28%•Capitalgainsrate=28%•Pricechangeas%ofDividend=90%

1986-1990

168

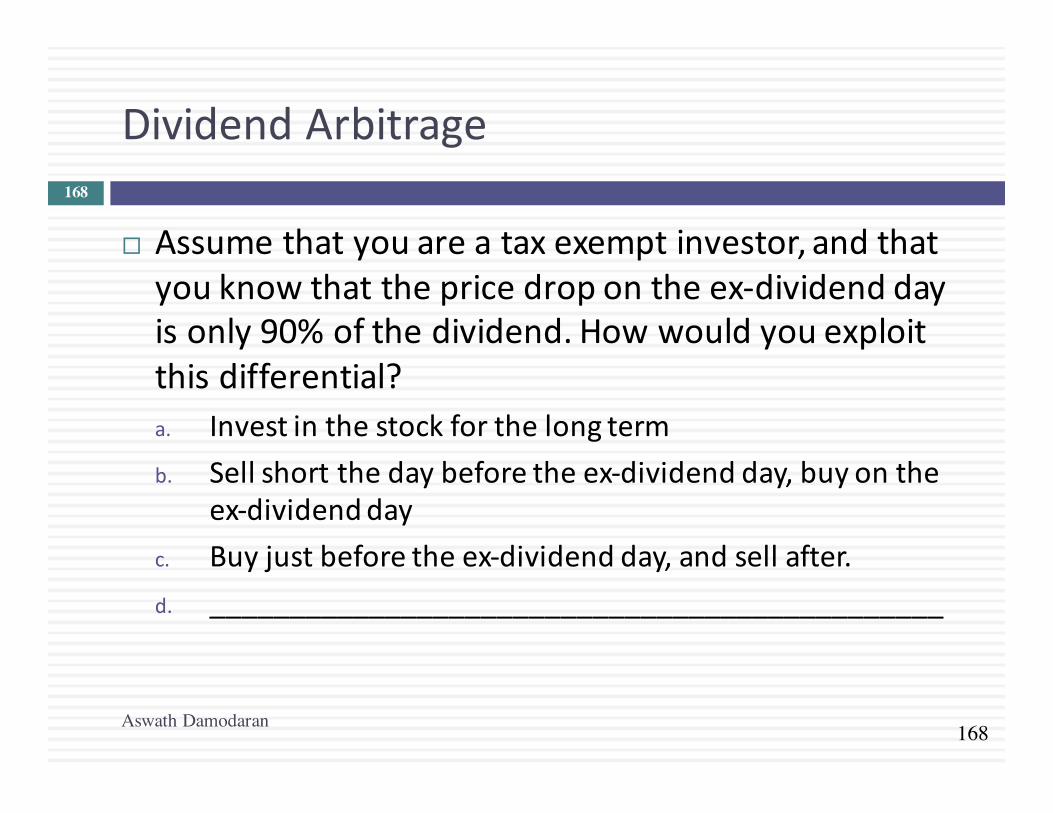

DividendArbitrage

Aswath Damodaran

168

¨ Assumethatyouareataxexemptinvestor,andthatyouknowthatthepricedropontheex-dividenddayisonly90%ofthedividend.Howwouldyouexploitthisdifferential?a. Investinthestockforthelongtermb. Sellshortthedaybeforetheex-dividendday,buyonthe

ex-dividenddayc. Buyjustbeforetheex-dividendday,andsellafter.d. ______________________________________________

169

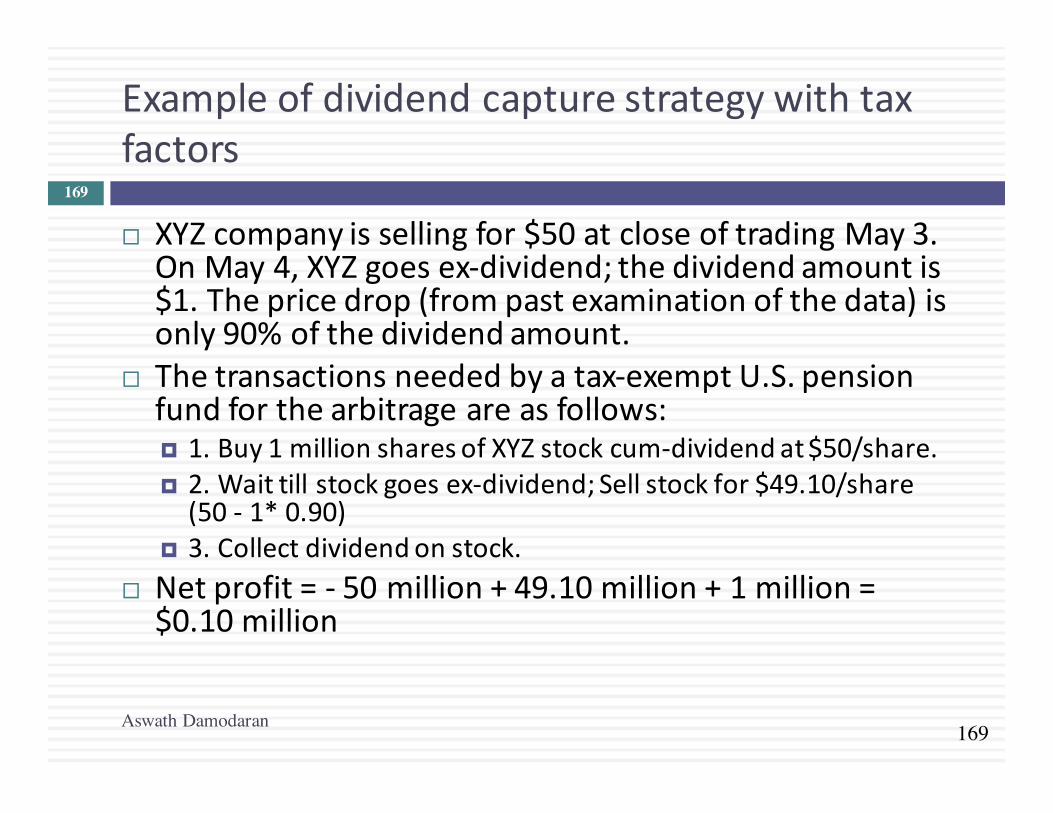

Exampleofdividendcapturestrategywithtaxfactors

Aswath Damodaran

169

¨ XYZcompanyissellingfor$50atcloseoftradingMay3.OnMay4,XYZgoesex-dividend;thedividendamountis$1.Thepricedrop(frompastexaminationofthedata)isonly90%ofthedividendamount.

¨ Thetransactionsneededbyatax-exemptU.S.pensionfundforthearbitrageareasfollows:¤ 1.Buy1millionsharesofXYZstockcum-dividendat$50/share.¤ 2.Waittillstockgoesex-dividend;Sellstockfor$49.10/share(50- 1*0.90)

¤ 3.Collectdividendonstock.¨ Netprofit=- 50million+49.10million+1million=$0.10million

170

Twobadreasonsforpayingdividends1.Thebirdinthehandfallacy

Aswath Damodaran

170

¨ Argument:Dividendsnowaremorecertainthancapitalgainslater.Hencedividendsaremorevaluablethancapitalgains.Stocksthatpaydividendswillthereforebemorehighlyvaluedthanstocksthatdonot.

¨ Counter:Theappropriatecomparisonshouldbebetweendividendstodayandpriceappreciationtoday.Thestockpricedropsontheex-dividendday.

171

2.Wehaveexcesscashthisyear…

Aswath Damodaran

171

¨ Argument:Thefirmhasexcesscashonitshandsthisyear,noinvestmentprojectsthisyearandwantstogivethemoneybacktostockholders.

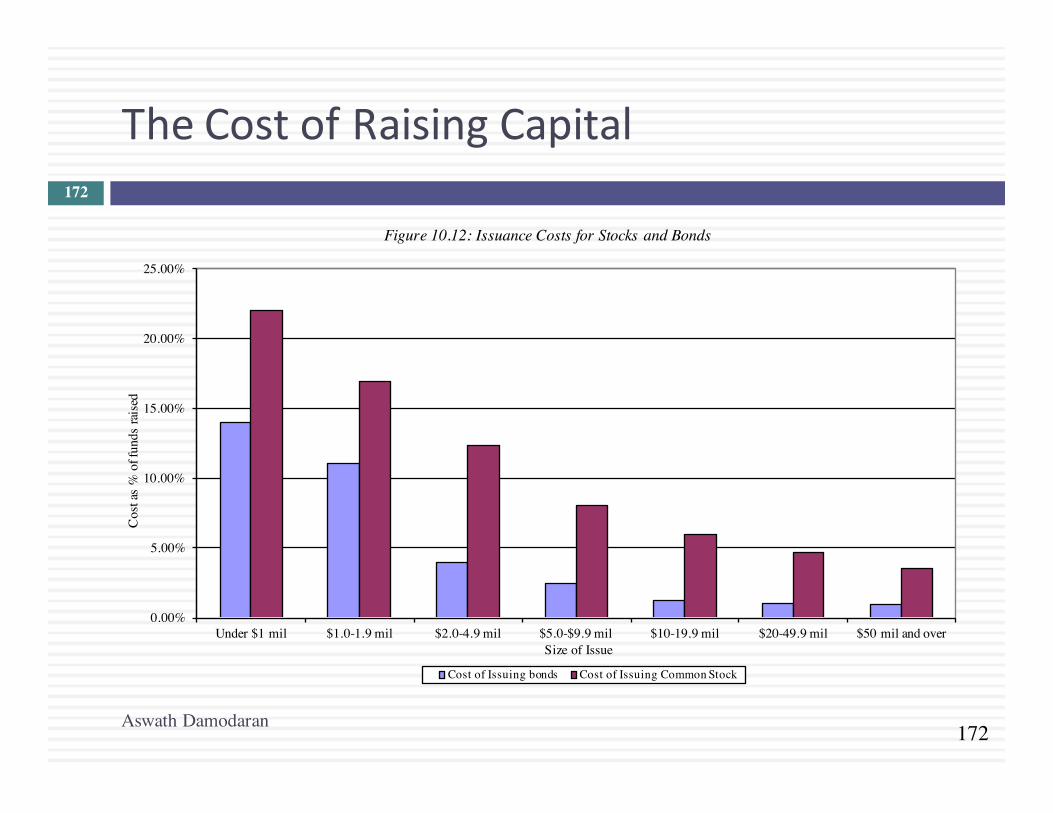

¨ Counter:Sowhynotjustrepurchasestock?Ifthisisaone-timephenomenon,thefirmhastoconsiderfuturefinancingneeds.Thecostofraisingnewfinancinginfutureyears,especiallybyissuingnewequity,canbestaggering.

172

TheCostofRaisingCapital

Aswath Damodaran

172

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Under $1 mil $1.0-1.9 mil $2.0-4.9 mil $5.0-$9.9 mil $10-19.9 mil $20-49.9 mil $50 mil and over

Cos

t as

% o

f fun

ds ra

ised

Size of Issue

Figure 10.12: Issuance Costs for Stocks and Bonds

Cost of Issuing bonds Cost of Issuing Common Stock