Embed Size (px)

Citation preview

Meaning of Bill of Exchange and Promissory Note

A negotiable instrument is a commercial document in writing, that

contains an order for payment of money either on demand or after a

certain time. There are of three types, namely, bills of exchange,

promissory notes and cheques. Bill of Exchange carries an order to

pay the money while Promissory Note contains a promise to pay

money.

Bill of Exchange

A bill of exchange is a binding agreement by one party to pay a fixed

amount of cash to another party on a predetermined date or on

demand.

Promissory Notes

A promissory note is a written agreement to pay a specific amount at a

future date or on demand to a specific party. This could be a set date

or a date chosen by the lender. Acceptance is not required in

promissory notes because the maker of the promissory notes

himself/herself promises to make the payment.

Some key features of promissory notes are as follows,

● It must be in writing

● It must contain an unconditional promise to pay.

● The sum payable must be certain.

● The promissory notes must be signed by the maker.

● It must be payable to a certain person.

● It should be properly stamped.

Parties to the Promissory Note

1. Maker or drawer: Also called the promisor, he/she is the person

makes or draws the promissory note to pay the specified the

amount as mentioned in the promissory note.

2. Payee or drawee: Also called the promise, he/she is the person

in whose favour promissory note is drawn. Usually, the drawer

is also the payee.

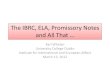

A Specimen of Promissory Note

Now, as per the

specimen above, Mr Shyam Kumar is the maker/drawer of the

promissory note and Mr Prem Chand Jain is the payee/drawee of the

promissory note.

However, if this promissory note is transferred by Mr Prem Chand

Jain in favour of say, Mr Vinod Jain, then Mr Vinod Jain will be the

payee.

Learn more about Dishonor of Bills here in detail.

Components of a Promissory Notes

● Principal amount: It is the amount which is given by the payee

and taken/borrowed by the maker of the note.

● Interest rate: The percentage rate that is multiplied by the

principal amount and the period of promissory notes in

computing for the interest.

● Interest: Interest is the revenue/income for the payee for

loaning out the principal & is an expense for the maker for

borrowing the amount.

● Maturity date or due date: The date on which final payment is

to be done by the maker of the promissory note.

● Maturity value: The principal amount due at the maturity date

of note in case of non-interest bearing promissory note. And

the sum of principal and interest due at the maturity date of

note in the case of interest-bearing promissory notes.

● Place of issue: The place where the maker executed the

promissory note.

Types of Promissory Notes

● Non-interest bearing note: They are promissory notes which do

not carry any interest rate with it. The amount that will be paid

at the time of maturity is equal to the face value of the

promissory note.

● Interest-bearing Note: Promissory notes which carry an interest

rate with it. The amount that will be paid at the time of

maturity is the sum of the face value & interest.

Learn more about Accounting Treatment here in detail.

Accounting Treatment

In case of a promissory note for the maker or drawer (the person who

draws the promissory note to pay the specified the amount), it is a bill

payable and for payee or drawee (the person in whose favour the

promissory notes are drawn), it is a bill receivable. Bills receivables

are assets fand Bills payable are liabilities.

Solved Example for You

Question 1: Promissory notes contains a promise to ………….

a. pay within one year of the issuing of the promissory notes.

b. pay with terms and conditions that include when and how much

to pay.

c. get a job

d. pay whenever you can and whenever you want.

Answer: The correct answer is option B. A promise to pay with terms and conditions that include when and how much to pay.

Maturity, Discounting, Due Date and Endorsement of Bills

In the business world, bills of exchange are an important tool to

facilitate transactions and deals. It is hence important to learn about

them and their terms. Let us learn about Maturity, Discounting, Due

Date and Endorsement of Bills.

Bill of Exchange

Transactions are the cornerstone of the business. They occur on a

daily basis in every business. As business is based upon transactions,

they are either done in cash or credit. A cash transaction is an upfront

and immediate. Whereas, credit transaction is done in the future.

To support the assurance of payment in the future, the seller urges the

buyer to sign an agreement known as Bill of Exchange. It is a legal

writing written by one side (maker or drawer) ordering the other side

(payer or drawee) to pay a certain amount within or on the decided

date.

Browse more Topics under Bill Of Exchange

● Meaning of Bill of Exchange and Promissory Note

● Basics of Accounting Treatment

● Bills Receivable, Bills Payable Books and Accommodation

Bills

● Renewal and Retiring of the Bill

● Dishonour of a Bill

As per the Negotiable Instruments Act 1881, a bill of exchange is an

instrument in writing containing an unconditional order, signed by the

maker, directing a certain person to pay a certain sum of money only

to, or to the order of a certain person or to the bearer of the

instrument. Further are the characteristics of the bill of exchange;

● A bill of exchange is in writing.

● It is an order to make payment.

● The order to make payment is unconditional.

● The maker of the bill of exchange must sign it.

● The payment to be made must be certain.

● The date on which payment is made must also be certain.

● The bill of exchange must be payable to a certain person.

● The amount mentioned in the bill of exchange is payable either

on demand or on the expiry of a fixed period of time.

● It must be stamped as per the requirement of law.

A bill of exchange is issued by the lender (creditor) upon his debtor

(indebted person). It needs to be acknowledged by the drawee (debtor)

or somebody on his behalf. It is only a draft until its acceptance is

confirmed.

Maturity of Bill and Due Date

Here we will learn about the maturity of the bill of exchange. In the

commercial world maturity means ‘date when payment is due’. The

date that comes after adding the 3 days of grace to the due date of the

bill is known as ‘date of maturity’. To understand the maturity of bill

better, first, you need to under the concept of a due date.

● Due date – It is a date on which the payment is expected/due.

● Bill at Sight – Due date is the date on which a bill is presented

for the payment.

● Bill after Sight –Here, the due date is the date of acceptance

plus terms of the bill. For example, if the bill is drawn on 1st

March and it is accepted on 5th March. In that case, if the

maturity of the bill is 1 month after sight. Then the due date

would be 5th March + 1 month = 5th April.

● Bill after Date – Here, the due date is the date of drawing plus

the terms of the bill. For example, if the bill is drawn on 1st

January and its maturity is 30 days after date then its due date

would be 1st January + 30 days = 31st January.

● Days of Grace – Drawee is given three extra days following the

due date of the bill for making payment. These 3 days are

known as ‘Days of Grace’. It is a custom to add the days of

grace. For example, if the bill is drawn on 1st January and its

maturity is 1 month then the due date would be 1st January + 1

month + 3 days = 4th February.

Discounting of Bill

On the off chance that the holder of the bill needs money, then he can

go to the bank for encashment of the bill before the due date. The bank

will give money to the holder of the bill after cutting some interest.

That interest deducted is called discounting.

Endorsement of Bill

Endorsement of the bill implies the procedure by which the maker or

holder of bill transfers the title of the bill in assistance of his/her

creditors. The individual transferring the title is called “Endorser” and

the individual to whom the bill is exchanged called “Endorsee”. An

endorsement is done by signing at the back of the bill.

Solved Question for You

Question. State 3 essential features of the bill of exchange

Answer: Three essential features are as follows

● The maker of the bill of exchange must sign it

● The payment to be made must be certain

● The date on which payment is made must also be certain.

Bills Receivable, Bills Payable Books and Accommodation Bills

At the point when the transactions are vast their account by methods

of the journal entry for each exchange identifying with the bills turns

out to be a very tedious and tiresome exercise. For this situation, they

are recorded independently in unique subsidiary books. The bills

receivables in the Bills Receivable Book and the bills payable in the

Bills Payable Book. A crucial point regarding bill receivables and bills

payable books is that they don’t record the transactions identifying

with the bills. For example, identifying with bills discounted,

endorsement, retirement, renewal and so forth, basically, have a

passing reference in these books.

Bills Receivable

It is utilized to record the full subtle elements of bills got from clients

and others. Every one of the points of interest of the bill-date,

acceptor’s name, sum, term, place of payment, and so on are entered

in the bills receivable book for introduction and further reference.

Browse more Topics under Bill Of Exchange

● Meaning of Bill of Exchange and Promissory Note

● Maturity, Discounting, and Endorsement of Bill

● Basics of Accounting Treatment

● Renewal and Retiring of the Bill

● Dishonour of a Bill

The performa of a bills receivable book is given below

No. of Bill

Date received

Date of Bill

From whom received

Drawer

Acceptor

Where payable

Term

Due date

Ledger folio

Amount Cash book folio Remarks

The bills receivable book, similar to some other subsidiary book, is

totaled intermittently.

This total is charged to the “Bills Receivable Account” although the

account of each individual indebted person whom the bills received is

credited in the books.

The Bills Receivable Account is the account of an asset and would in

any condition have a debit balance. This equalization on any date

would show the number of bills receivable un-matured and on hand.

Bills Payable

It is kept up like a bills receivable book. It is intended to record every

one of the detailed elements, identifying with the bills acknowledged

by an entity or a party, which are held for being utilized later on, in the

event of need.

The performa of a bills receivable book is given below

No. of Bill

Date of Bill

To whom given

Drawer

Payee

Where Payable

Term

Due Date

Ledger Folio

Amount paid

Date Cash book folio Remarks

Entries are made in the bills payable book at whenever bills payable

are acknowledged. Quickly, the individual account in the record is

debited.

Toward the month’s end, the aggregate of bills payable book is

presented creditor to whom to the credit of bills payable account is in

the ledger, along these lines finishing the double entry for bills

payable in the record.

Learn more about Bills of Exchange and Promissory Notes in detail.

Accommodation Bills

More often than not, bills of exchange or promissory notes are drawn

to finance the real exchanges in goods. An acknowledgment is made

to settle a trade debt owing to the drawer by the drawee in case of a

bill of exchange. The bill is called a trade bill.

As it begins from real trade transaction it is for value got and is

enforceable. Be that as it may, aside from financing transaction in

products, bills of exchange and promissory notes may likewise be

utilized for raising finance temporarily.

Such a bill is called ‘accommodation bill’ as it is acknowledged by

the drawee to accommodate the drawer. Consequently, the drawee is

known as the ‘accommodating party’ and the drawer is known as the

‘accommodating party’.

Renewal and Retiring of a Bill of Exchange

A Bills of Exchange is an instrument in writing, containing an

unconditional order, signed by the maker, directing a certain person to

pay a certain sum of money only to, all the order of the certain person

or to the bearer of the instrument. Let us see about the renewal of bills

of exchange.

When a person sells some good to a party, then he /she wants to take

some written assurance that payment will be received within a

specified period. Various type of negotiable instrument admit for this

purpose, but the most commonly used instruments are bills of

exchange.

Learn Basic Accounting Treatment here.

Renewal of Bills of Exchange

Bills of exchange have some specified time period. Drawee/acceptor

has to make payments within that specified time period to

Drawer/maker. But sometimes when they are not able to pay for the

bill on the due date then he/she may ask the drawer to extend the

period of credit.

If the drawer agrees then the drawer may cancel the old bill and draw

a fresh bill for the extended period which the acceptor accepts.

Cancelling the old bill and drawing of a fresh bill for an extended

period is called Renewal of Bill. For the extended period, drawee is

asked to pay interest which can be paid in cash or added to the amount

of a new bill.

How to make entry of Renewal of Bills of Exchange

As when a new bill of exchange is issued, it affects both parties. Entry

for renewal is passed in the books of the drawer as well as acceptor. If

the drawer has discounted or dishonoured bill, the same entries are

made as for dishonour.

Thereafter second entry is passed for interest. Interest may be paid in

cash by cheque. If interest is paid in cash, then drawer debits the cash

a/c and credits the interest a/c. If interest is paid by cheque then

drawer debits the bank a/c and credits interest a/c.

On the other hand, acceptor debits the interest and credits the cash or

bank a/c. For drawer, interest is the income and for acceptor, interest

is an expense. Cash or cheque is received by the drawer and is paid by

the acceptor.

If the acceptor does not pay interest on cash but agreed to pay later

then instead of debiting cash/bank, drawer debits the amount of the

acceptor. Whereas acceptor credits the amount of drawer instead of

cash/bank.

Because of the amount of interest drawer becomes the creditor and

acceptor becomes the debtor. Interest is debited and credited in the

same way whether paid in cash or not. A third entry is for renewal of

the bill. Is dentist has been paid in the case then the bill of an amount

of the new bill will be same as that of the old bill. If interest is not

paid in cash then a new bill will include the old bill amount and

interest.

(Source: yourarticlelibrary)

Renewal in case of Partial Payment

If acceptor is unable to pay for the bill in full, he/she can also pay

partially. In this case, a new bill will be for the remaining amount.

Interest will then be charged on the remaining amount for the

extended period of credit. The amount of the new bill will include

unpaid amount, interest and nothing charges if any.

First main entry is made to cancel the old bill. A second entry is made

for partial payment. The third entry is made for interest. And the

fourth entry is for drawing and accepting the new bill.

Renewal in case of Dishonour of a Bill

Sometimes bill can be renewed by the drawer even after dishonour of

bill. In this case, the acceptor is the debtor of the drawer for the

amount of bill, noting charges and interest. If interest and noting

charges or paid in cash by the acceptor, the drawer debits cash/bank

and credits the interest and noting charges a/c.

On the other hand, acceptor debits the noting charges and interest a/c

and credits the cash/ bank a/c. If these amounts are paid in cash, a

fresh bill is drawn by the total of old bill amount, interest and noting

charges.

Following entries are passed in this case:-

In the book of Drawer

1] Entry for Cancellation of the Bill:

Acceptor’s Personal A/c………………. Dr

To Bills Receivable A/c

2] Entry for Receipt of Cash:

Cash A/c ……………………………………….Dr

To Acceptor’s Personal A/c

3] Entry for Interest Received:

Cash A/c ……………………………………….Dr

To Interest A/c

4] Entry for Interest not yet received but due:

Acceptor’s personal A/c ……………………Dr

To Interest A/c

5] Entry for New Acceptance:

Bills Receivable A/c ………………………….Dr

To Acceptor’s Personal A/c

In the books of Acceptor

1] Entry for Cancellation of Bill:

Bills Payable A/c …………………………….. Dr

To Drawer Personal A/c

2] Entry for part payment in cash:

Drawer’s Personal A/c………………………………… Dr

To Cash A/c

3] Entry for Interest Paid:

Interest A/c …………………………………………. Dr

To Cash A/c

4] Interest not paid:

Interest A/c …………………………………………. Dr

To Drawer’s Personal A/c

5] Entry for Accepting New Bill:

Drawer’s Personal A/c ……………………………. Dr

To Bills Payable A/c

Solved Example

Que. A bill of Exchange is drawn by-

a. Debtor

b. Creditor

c. Holder

d. none of these

Ans. The correct answer is B. The creditor draws the bill of exchange.

This bill has to be accepted before it becomes enforceable.

Dishonour of Bill

When the drawee (a person who is liable to pay) is not able to make

the payment on the date of maturity of a bill, a bill is said to be

dishonoured. In this situation liability of drawee is restored. Dishonour

of a bill can be either by non-acceptance or non-payment. A

dishonoured bill is equivalent to the bounced cheque.

Dishonour by Non-Acceptance

Bill of exchange requires acceptance by the drawee when it is

presented, however, if on presenting the bill of exchange, it gets

non-acceptance, it will amount to dishonour.

Dishonour by Non-Payment

When the drawee of the bill of exchange commit default in making the

payment of the bill on maturity to the drawer, it is said to be

dishonoured of a bill of exchange by non-payment.

Possible reasons why the bill is dishonoured by non-payment?

● Due to insufficient funds in the drawee’s a/c.

● The drawee is unable to pay because of insolvency, or

● The drawee simply does not want to pay

When the bill gets dishonoured, entries that were made at the time of

receipt of a bill are reversed.

Solved Examples for You

Example 1

Rashi (drawer) received a bill of exchange duly accepted by Ayushi

(drawee), which was dishonoured. The entries of dishonour will be as

follows in the books of Rashi (drawer):

When the bill was kept by Rashi till maturity

Ayushi a/c Dr

To Bill Receivables A/c

When the bill had been endorsed by Rashi in favour of Raghav

Ayushi a/c Dr

To Raghav A/c

When the bill was discounted by Rashi with her bank

Ayushi a/c Dr

To Bank A/c

When the bill was sent for collection by Rashi

Ayushi a/c Dr

To Bill Sent for Collection A/c

Example 2

On April 01, 2018 Pinky sold goods to Shreya for Rs. 20,000 and

drew upon her a bill of exchange for 3 months. Shreya accepted the

bill and returned it to Pinky. On the date of maturity, the bill was

dishonoured by Shreya. Entries in all the cases listed below in the

books of Pinky and Shreya will be:

Case 1: When the bill is kept by Pinky till its maturity;

Books of Pinky

Journal Date Particulars L.

F Amount Amount

April 01, 2018 Shreya a/c D

r 20,000

To Sales A/c 20,000

(Sold goods to Shreya)

April 01, 2018 Bills Receivable A/c D

r 20,000

To Shreya 20,000

(Received Shreya’s acceptance)

July 04, 2018 Shreya a/c D

r 20,000

To Bills Receivable A/c 20,000

Case 2: When the bill is discounted by Pinky with the bank for Rs.

19,600

Books of Pinky

Journal Date Particulars L.

F Amount Amount

April 01, 2018 Shreya a/c D

r 20,000

To Sales A/c 20,000

(Sold goods to Shreya)

April 01, 2018 Bills Receivable A/c D

r 20,000

To Shreya 20,000

(Received Shreya’s acceptance)

April 01, 2018 Bank a/c D

r 19,600

Discount a/c Dr 400

To Bills Receivable A/c 20,000

(Bill discounted by Pinky in the bank)

July 04, 2018 Shreya a/c D

r 20,000

To Bank a/c 20,000

(Discounted bill dishonoured by Shreya)

When the bill is endorsed to Navin by Pinky.

Books of Pinky

Journal Date Particulars L.

F Amount Amount

April 01, 2018 Shreya a/c D

r 20,000

To Sales A/c 20,000

(Sold goods to Shreya)

April 01, 2018 Bills Receivable A/c D

r 20,000

To Shreya 20,000

(Received Shreya’s acceptance)

April 01, 2018 Navin a/c D

r 20,000

To Bills Receivable A/c 20,000

(Shreya acceptance endorsed in favour of Navin)

July 04, 2018 Shreya a/c D

r 20,000

To Navin a/c 20,000

(Endorsed bill dishonoured by Shreya)

Whereas, in the book of Shreya, the following entries will be

recorded

Books of Shreya

Journal Date Particulars L.

F Amount Amount

April 01, 2018 Purchases a/c D

r 20,000

To Pinky A/c 20,000

(Purchased good from Pinky)

April 01, 2018 Pinky a/c D

r 20,000

To Bills Payable 20,000

(Accepted Pinky’s draft)

July 04, 2018 Bills Payable a/c D

r 20,000

To Pinky a/c 20,000

(Acceptance in favor of Pinky dishonoured)