Embed Size (px)

Citation preview

8/12/2019 MCS 10th Session

http://slidepdf.com/reader/full/mcs-10th-session 1/11

8/12/2019 MCS 10th Session

http://slidepdf.com/reader/full/mcs-10th-session 2/11

8/12/2019 MCS 10th Session

http://slidepdf.com/reader/full/mcs-10th-session 3/11

Reward

Yes

measurements

revised revised actual No

vs plan feedback/communication

Goals &strategies

StrategicPlanning

ResponsibilityCenter

performance

Rules

ReportActual vs

plan

Performancesatisfactory

Otherinformation

Budgeting

8/12/2019 MCS 10th Session

http://slidepdf.com/reader/full/mcs-10th-session 4/11

Variances Analysis

disaggregationTotal variance

Nonmanufacturing

Manufacturing cost Sales

Adm Marketing R &DVariable

costFixedCost Volume Price

Directlabor

VariableOHMaterial

Marketshare

Industryvolume

8/12/2019 MCS 10th Session

http://slidepdf.com/reader/full/mcs-10th-session 5/11

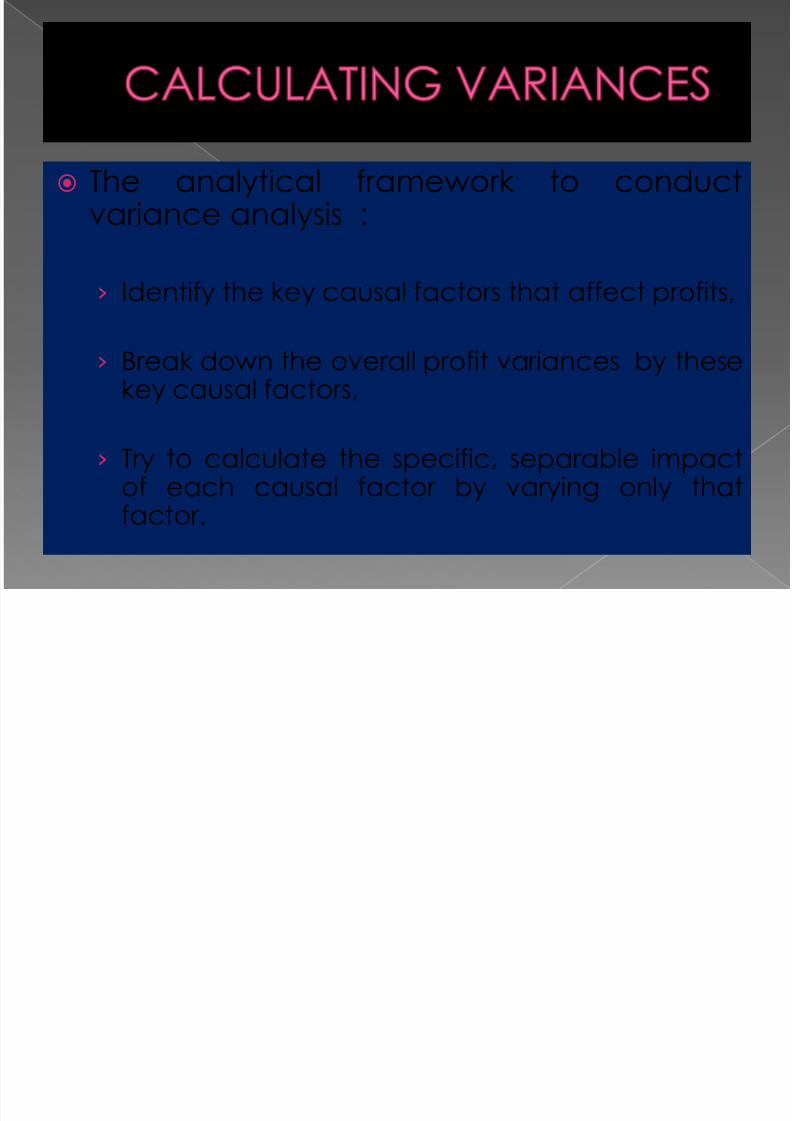

The analytical framework to conductvariance analysis :

› Identify the key causal factors that affect profits,

› Break down the overall profit variances by thesekey causal factors,

› Try to calculate the specific, separable impactof each causal factor by varying only thatfactor.

8/12/2019 MCS 10th Session

http://slidepdf.com/reader/full/mcs-10th-session 6/11

RevenueVariances

Selling priceVariance

Mix andVolume

variance

Mix

Variance

Volumevariance

Marketshare

Industryvolume

8/12/2019 MCS 10th Session

http://slidepdf.com/reader/full/mcs-10th-session 7/11

ExpenseVariances

Fixed CostVariances

Variable CostVariances

Adjustmentvolume ofproduction

8/12/2019 MCS 10th Session

http://slidepdf.com/reader/full/mcs-10th-session 8/11

8/12/2019 MCS 10th Session

http://slidepdf.com/reader/full/mcs-10th-session 9/11

Full-cost systems

› Fixed and variable overhead cost included in

inventory,› Production vs Sales volume,

› Level of inventory

Amount in detail Engineered and Discretionary Costs

› Favorable in engineered cost is usually an indicationgood performance.

› The performance of discretionary expense center judged to be satisfactory if actual expense equal thebudgeted.

8/12/2019 MCS 10th Session

http://slidepdf.com/reader/full/mcs-10th-session 10/11

Limitations of Variances Analysis :

› It does not tell why the variance occured.

› To decide whether a variance is significant,› Performance reports become more highly

aggregated, offsetting variances might mislead thereader.

› The reports show only what has happened , do notshow the future effects of actions that manager hastaken.

Formal reports are worthless unless they lead toaction.

8/12/2019 MCS 10th Session

http://slidepdf.com/reader/full/mcs-10th-session 11/11