Embed Size (px)

Citation preview

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 1/30

CIO Summit

November, 2012

CONFIDENTIAL AND PROPRIETARY Any use of this material without specific permission

of McKinsey & Company is strictly prohibited

William Forrest

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 2/30

McKinsey & Company

L a s t M o d i f i e d

1 1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d

3 1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

|

What I will talk about today

1

!

“Current IT” as we know it is no longer a game-changer

! We already see significant disruption in many

business models

! “New IT” is rising to fill the place of “Current IT”

! How to take advantage of “New IT”

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 3/30

McKinsey & Company

L a s t M o d i f i e d

1 1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d

3 1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

| 2

IT spend by industr

y

0

1

2

3

4

5

6

7

8

9

0 3 6 9 12 15 18 21 24 27 30

IT spending as % of revenue

Operating marginPercent

Construction, materialsand natural resources

Food and beverageprocessing

Chemicals

Retail and wholesale

Media andentertainmentTransportation

Industrial electronicsand electrical equipment

Healthcareproviders

Software publishingand internet services

Banking andfinancial services

Professionalservices

Education

Telecomm-unicationsInsurance

Industrialmanufacturing

Utilities

Pharmaceuticals,life sciences andmedical products

Consumer products

Energy

Current IT has become table stakes - spending on IT is not a differentiator

R2 = 0.0726

Note: Banking specific data points are sourced from actual benchmarkedMcKinsey clients, and have been adjusted to include an industry standard of~30% capex, which is included in the Gartner IT spend by industry data

SOURCE: Gartner “IT Metrics: IT Spending and Staffing Report”, 2012;McKinsey Business Support Function (BSF) proprietary database

0

2

4

6

8

403020100

R2 = -0.3958

Confirms belief that IT spend does notcorrelate with business success

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 4/30

McKinsey & Company

L a s t M o d i f i e d

1 1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d

3 1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

| 3

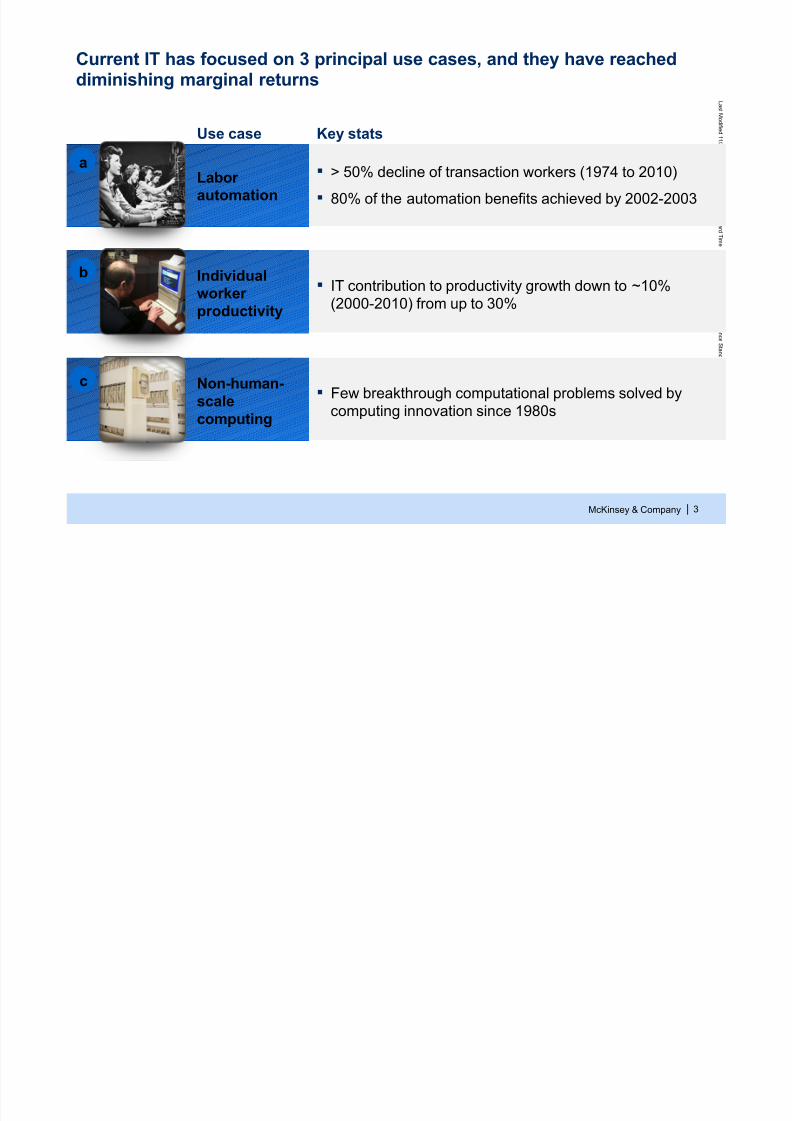

Current IT has focused on 3 principal use cases, and they have reacheddiminishing marginal returns

!

IT contribution to productivity growth down to ~10%(2000-2010) from up to 30%

Individualworkerproductivity

! Few breakthrough computational problems solved by

computing innovation since 1980s

Non-human-scale

computing

Key statsUse case

! > 50% decline of transaction workers (1974 to 2010)

! 80% of the automation benefits achieved by 2002-2003

Laborautomation

a

b

c

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 5/30

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 6/30

McKinsey & Company

L a s t M o d i f i e d

1 1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d

3 1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

|

Share of total workforce Percent

! despite increasin

g share of

knowledge workers

5

IT-driven productivity growth is actually shrinking, despite growth inknowledge workers

0

10

20

30

40

50

Time period

200520001990198019720

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Time period

2005200019901972

Productivity growthattributable to IT

Average laborproductivity growth

INDIVIDUAL WORKER PRODUCTIVITY

1 Information technology includes computer hardware, software, and communications equipment. Share Attributed to Information Technology is the average contributionof information technology capital deepening plus the average contribution of information technology total factor productivity divided by average labor productivity foreach period.

2 Job types involving complex problem solving, special knowledge, experience, context (e.g., doctors, salespeople, project teams)Notes: Data are for the U.S. private economy. All figures are average annual growth rates. A contribution of an input reflects the share weighted growth rate.

SOURCE: Bureau of Labor Statistics, Bureau of Economic Analysis, 1970-2010, Jorgenson, Ho, Stiroh, “A Retrospective Look at theU.S. Productivity Growth Resurgence”, Federal Reserve Bank of New York Staff Reports, February 2007

b

Productivity growth Percent

IT1 contribution to productivity growth

is decreasing!

Knowledgeworkers2

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 7/30

McKinsey & Company

L a s t M o d i f i e d

1 1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d

3 1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

| 6

Few breakthrough computational problems have been solved bycomputing innovation since the emergence of the microprocessor

NON-HUMAN-SCALE COMPUTING

1971 1975 1978 2011

MicroprocessorsMainframes

Businesscomputationalproblems solved

! A broader base

of departmentalusage

! Completinganalytics faster

! None! Back-end for

bankingtransactionprocessing

! Financial analytics

and risk modeling! Pricing changes

! Foreign currencyexchanges

Airline industryexample

! Computerizedreservation andticketing e.g.

SABRE for AA

! ComputerizedReservationSystems (CRS)

!

Yield management

! Demandforecasting

! Customer

profitabilityanalysis, leadingto frequent flyerprograms

! Network,luggage,and crew

planningandoptimization

SOURCE: McKinsey; Maurer, “Internet for the Retail Travel Industry”, 2003; team analysis

c

Mini computers

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 8/30

McKinsey & Company

L a s t M o d i f i e d

1 1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d 3 1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

|

Thought leaders in the technology world are advocatingfor a rethink of enterprise and corporate IT

SOURCE: Press search

"[Technology is] shifting more of the power in the tech industry awayfrom those who deploy and support apps to those who build them.

– Jason Hiner, Editor in Chief of TechRepublic

The success of companies like Google, Facebook, Amazon, andNetflix, not to mention Wall Street firms and industries frommanufacturing to retail and healthcare, is increasingly driven bybetter tools for extracting meaning from very large quantities ofdata.

– Tim O'Reilly, Industry Thought Leader

The status quo [of Corporate IT] is unacceptable and this rethinkneeds to take place – it should have taken place a long time ago.

– John Thorp, author of The Information Paradox

Enterprise software companies sell bad software for huge amounts of

money. They get away with it for a variety of reasons that link together toform a sort of protective wall. But the software world is changing.

– Paul Graham, Co-founder of Ycombinator

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 9/30

McKinsey & Company

L a s t M o d i f i e d

1 1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d 3 1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

|

The highest IT priority for most companies should be to move IT spend toindustry average

4.5%

1.5%

1.5%

2%

IT spending as % of revenue – range by industry%, 2012

0 1 2 3 4 5 6 7 8 9 10

Banking

Healthcare

Insurance

Otherindustries

Potential op. marginincrease by reducingaverage IT costs for topquartile to the average% points

Op. marginimprovement% increase

Industryop. marginrange1

%

12-30%

7-14%

5-25%

6-15% ~10-25%

~7-17%

~11-21%

~18-90%1

SOURCE: Gartner “IT Metrics: IT Spending and Staffing Report”, 2012, Bloomberg, team analysis

1 Operating margin range taken from the range of first and last quartiles of top 100 companies in each industry by revenueNote: IT spend = opex plus capex (no depreciation)

Bottomquartile

Average Topquartile

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 10/30

McKinsey & Company

L a s t M o d i f i e d

1 1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d 3 1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

|

Cloud is a key lever to decrease costs and reach industry averagecost levels

91 Benefits beyond IT spend reduction were not quantified

Non x86

Telecom

Facilities and FabricHardware

Software

Internal Service

IT Services

Cloud services

Hybrid cloud

76

Pure publiccloud

80

Pure privatecloud

82

Legacy IT

100

Annual total IT spend, 100=Total IT spend with all on-premise infrastructure

! Moving to the cloud can yield ~20-25% savings in current IT spend

! Cloud should be used primarily for cost reductions (not agility and other efforts)

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 11/30

McKinsey & Company

L a s t M o d i f i e d

1 1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d 3 1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

|

What I will talk about today

10

! “Current IT” as we know it is no longer a game-changer

! We already see significant disruption in many

business models

! “New IT” is rising to fill the place of “Current IT”

! How to take advantage of “New IT”

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 12/30

McKinsey & Company

L a s t M o d i f i e d

1 1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d 3 1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

| 11

Historical and expected revenuesgenerated from new sources

The world is changing: CEOs recognize that future revenue growth willcome from new business models

25-30%

+50-67%

10-’15

expected

04-’09

15-20%

Increase in % ofMcKinsey engagements focused on innovation2 between ‘05 –’11

Increase in Google searchvolume3 for “business model

innovation” between ‘07 –’11

117%

183%

1 Estimates based on survey responses of ~1,500 CEOs globally, conducted in 2010 by IBM2 Engagements with “Innovation” as the primary or secondary functional classification3 Sourced from Google Insights for Search; indexed to 100 as peak search volume

SOURCE: McKinsey FPIS; Google Insights for Search worldwide (data pulled on March 14th, 2012); 2010 IBM GlobalCEO Study; McKinsey research

% of overall revenues1

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 13/30

McKinsey & Company

L a s t M o d i f i e d

1 1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d 3 1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

| 12

“Current IT” models are transforming: Amazon ispursuing business model change across the value chain

Business model change lever Amazon.com example

Changing the cost ofinputs

Utilize a sophisticated supply chain managementsystem to improve operational efficiency

Eliminating value chainintermediaries

Providing a digital publishing platform bypassingtraditional publishing houses and keeping ~70%of sales

Driving customerpreference in anexisting market

Leveraged large amounts of data aroundcustomer behaviors to offer Prime

Serving an underservedmarket in a new way

Creating a single marketplace across thousandsof sellers of out of print books

AWS selling rented timeslot on the cloud, insteadof physical computer

Introducing newmonetization model

SOURCE: McKinsey, team analysis, Amazon.com, press releases

AMAZON.COM EXAMPLENOT EXHAUSTIVE

Enables changes e.g. real-time behavior and data tracking,scale and flexibility and multi-device connectivity

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 14/30

McKinsey & Company

L a s t M o d i f i e d

1 1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d 3 1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

|

Need new ways to

delivershareholder value

13

A perfect storm is approaching: economic conditions arechanging, demanding business model transformation

SOURCE: McKinsey; client interviews

Emerging markets predominant in future

growth, with lower costpoints and differentconsumption models(e.g., bank-less, SMS-based money transfer)

Growing performancegap between leadersand laggards

Industries unable tomeet investorexpectations (e.g., insurance)

Increasingly competitiveenvironment putsincumbent players at risk (~65% surviving S&P500today vs. 90% in 1970s)

CROSS-INDUSTRYMODEL

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 15/30

McKinsey & Company

L a s t M o d i f i e d

1 1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d 3

1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

| 14

Business model innovation can lead to success

20112005

4%

16%

+279%

18%

+468%

20112005

3%

Revenue

Performance of Apple, Amazon, and Google vs. remainder of NASDAQ-100% contribution to NASDAQ-100 aggregate

SOURCE: Bloomberg and public financial data

Some “pure play” New IT companies are already achieving major top- and

bottom-line advantage!

EBITDA

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 16/30

McKinsey & Company

L a s t M o d i f i e d

1 1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d 3

1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

|

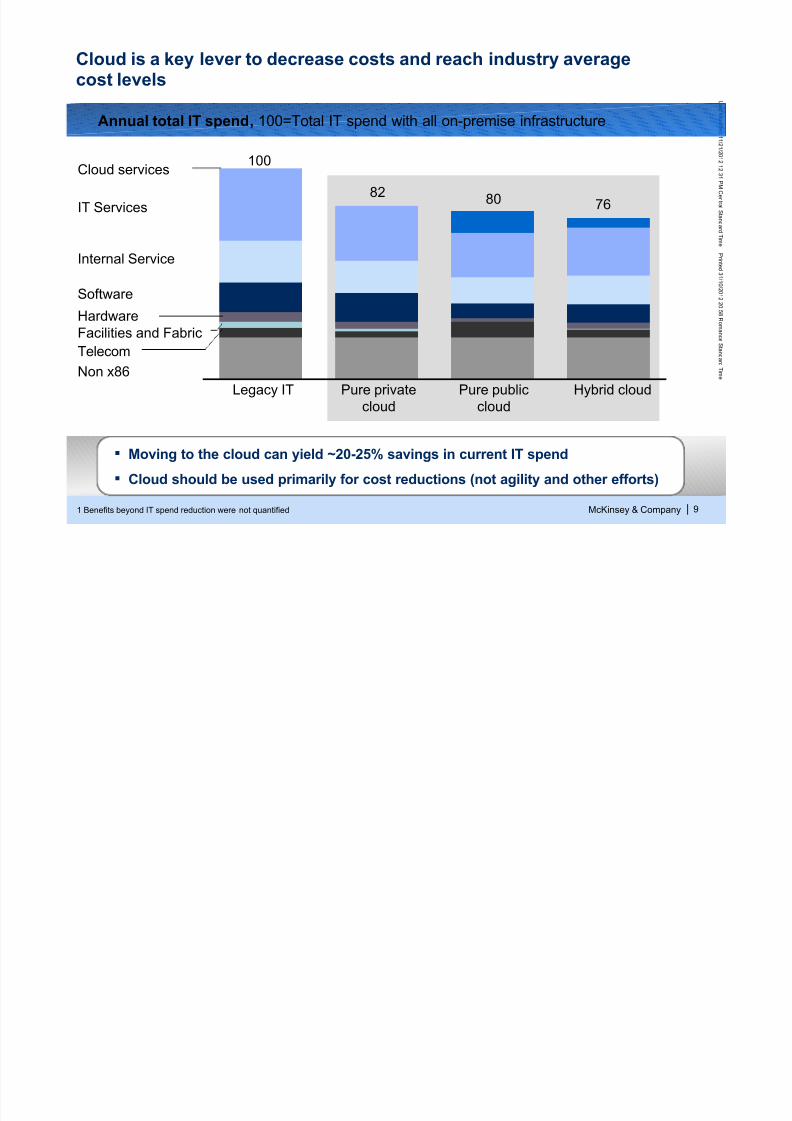

The drive to innovate continues: successful top firms are perceived insocial media as more innovative than non-successful top firms

15

64

108

155

Ø 93

47

The 100 largest firmsglobally ranked andgrouped by total return toshareholders (TRS) andtheir average Innovation

Sentiment Score1

2nd quartile TRS

Average Innovation Sentiment Score1 by TRS quartile2

Hundreds web articles; global social media; Mar – Aug 2011

Top quartile TRS

Bottom quartile TRS

3rd quartile TRS

1 Number of positive-sentiment articles and blog posts linking company with the words “innovation” or “innovative” over the last 6 months2 Performance measured by average TRS over the last 5 years (2006 – 2011)

SOURCE: Sysomos Web Analytics; Bloomberg; Datastream; team analysis

x3

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 17/30

McKinsey & Company

L a s t M o d i f i e d 1 1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d 3

1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

|

What I will talk about today

16

! “Current IT” as we know it is no longer a game-changer

! We already see significant disruption in many

business models

! “New IT” is rising to fill the place of “Current IT”

! How to take advantage of “New IT”

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 18/30

McKinsey & Company

L a s t M o d i f i e d 1 1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d 3

1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

|

“New IT” enables new business models and sources of growth

!

Online collaboration tools(e.g., internal wikis) helpteams work together

Individualworkerproductivity

! Google’s AdWords deliverscustomized, personalized ads

Non-human-scale

computing

! Amazon.com uses heavy“push” for cross-sellingrelated products

Laborautomation

Example usesCurrent IT use cases “New IT” use cases

Team &corporateproductivitygrowth

Digital only

products

Businessmodeltransfor-mation

a

b

c

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 19/30

McKinsey & Company

L a s t M o d i f i e d 1 1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d 3

1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

| 18

Example: Amazon transforming e-retail by driving customerpreference and share of wallet gains

Approach

!

Collection and analysis of datato offer recommendations andgenerate “push” based sales

! 5X investment in internal IT toenable innovation

BUSINESS MODEL TRANSFORMATION

1 The only year this figure is available for – not reported separately in financial reports

SOURCE: Company web site, company reports, press and literature search

a

Amazon is the market leaderamong online retailers inaverage order size, drivenby “push” sales

35% of all sales (~$3.8B) in FY20061 came fromrecommendations

New businesses enabled

by investments in“NewIT” e.g. AWS ($1B),Kindle(10% of revenue) andinstant video to drive Prime

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 20/30

McKinsey & Company

L a s t M o d i f i e d 1 1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d 3

1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

|

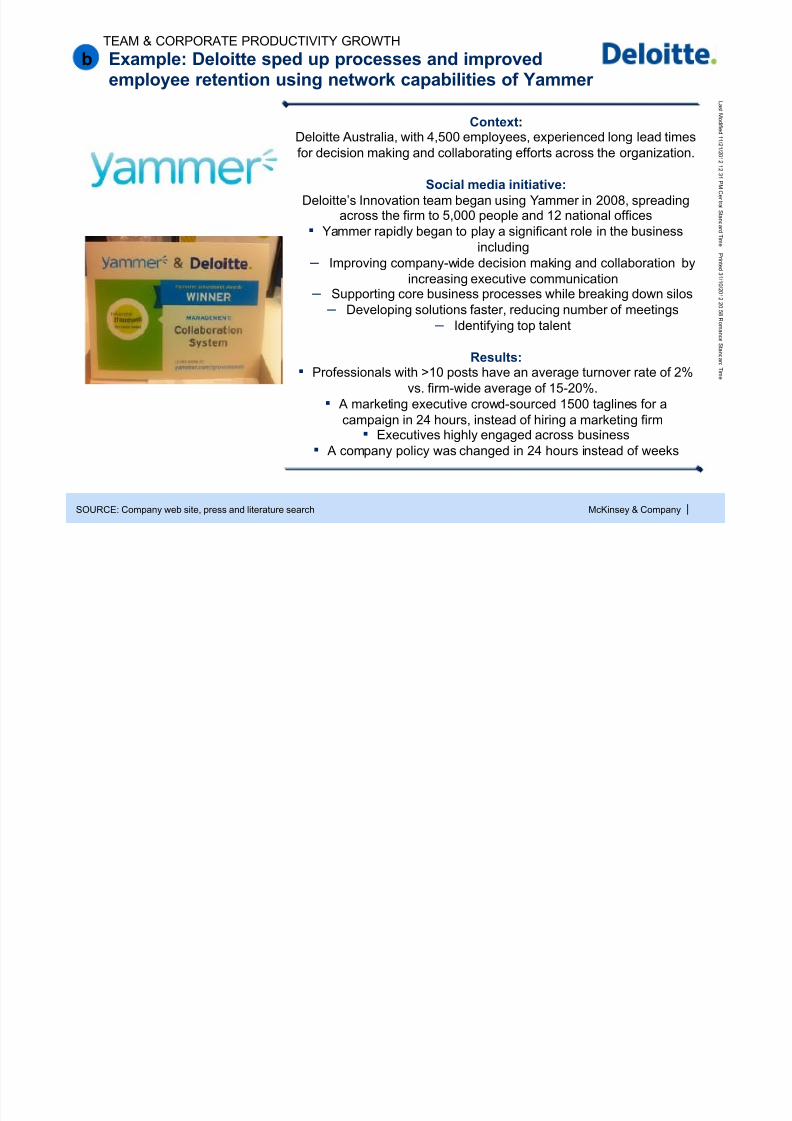

Example: Deloitte sped up processes and improvedemployee retention using network capabilities of Yammer

Context:

Deloitte Australia, with 4,500 employees, experienced long lead timesfor decision making and collaborating efforts across the organization.

Social media initiative: Deloitte’s Innovation team began using Yammer in 2008, spreading

across the firm to 5,000 people and 12 national offices! Yammer rapidly began to play a significant role in the business

including – Improving company-wide decision making and collaboration by

increasing executive communication – Supporting core business processes while breaking down silos

– Developing solutions faster, reducing number of meetings – Identifying top talent

Results:! Professionals with >10 posts have an average turnover rate of 2%

vs. firm-wide average of 15-20%.! A marketing executive crowd-sourced 1500 taglines for a

campaign in 24 hours, instead of hiring a marketing firm! Executives highly engaged across business

! A company policy was changed in 24 hours instead of weeks

TEAM & CORPORATE PRODUCTIVITY GROWTH

b

SOURCE: Company web site, press and literature search

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 21/30

McKinsey & Company

L a s t M o d i f i e d 1 1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d 3

1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

| 20

Example: AdWords and AdSense deliver data-driven, customadvertisements, resulting in $36B of annual revenues for Google

(2012)Now(pre 2000)Then

!

Text-based custom ads delivered based on searchdata and page content

! In 2011, Google represented 6.5% of total

advertising industry, and 35.3% of the onlineadvertising industry

– In 2011 the total online advertising industry sizeis $78.6B, up from $10.5B in 2000

!

Offline advertisingdominated online ads

! Online ads were

untargeted andineffective, primarilydriven by display bannerand popup ads

DIGITAL-ONLY PRODUCTS

SOURCE: Interactive Advertising Bureau, Google finances, Magna Global forecasts 2012

c

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 22/30

McKinsey & Company

L a s t M o d i f i e d 1 1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d 3

1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

|

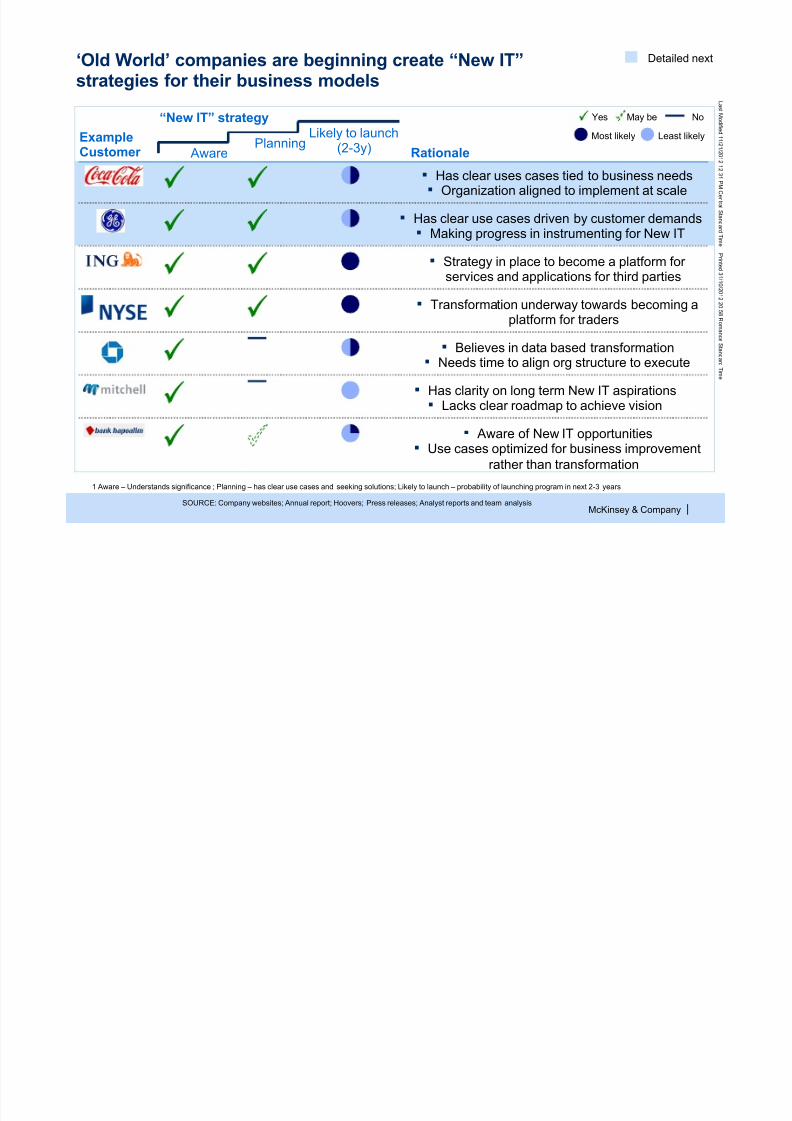

‘Old World’ companies are beginning create “New IT”strategies for their business models

1 Aware – Understands significance ; Planning – has clear use cases and seeking solutions; Likely to launch – probability of launching program in next 2-3 years

Rationale

“New IT” strategy

Likely to launch(2-3y) Aware PlanningExampleCustomer

Yes May be No

SOURCE: Company websites; Annual report; Hoovers; Press releases; Analyst reports and team analysis

! Has clear uses cases tied to business needs! Organization aligned to implement at scale

! Has clear use cases driven by customer demands! Making progress in instrumenting for New IT

! Strategy in place to become a platform for

services and applications for third parties

! Transformation underway towards becoming aplatform for traders

! Believes in data based transformation! Needs time to align org structure to execute

! Has clarity on long term New IT aspirations! Lacks clear roadmap to achieve vision

! Aware of New IT opportunities! Use cases optimized for business improvement

rather than transformation

Most likely Least likely

Detailed next

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 23/30

McKinsey & Company

L a s t M o d i f i e d 1 1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d 3

1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

|

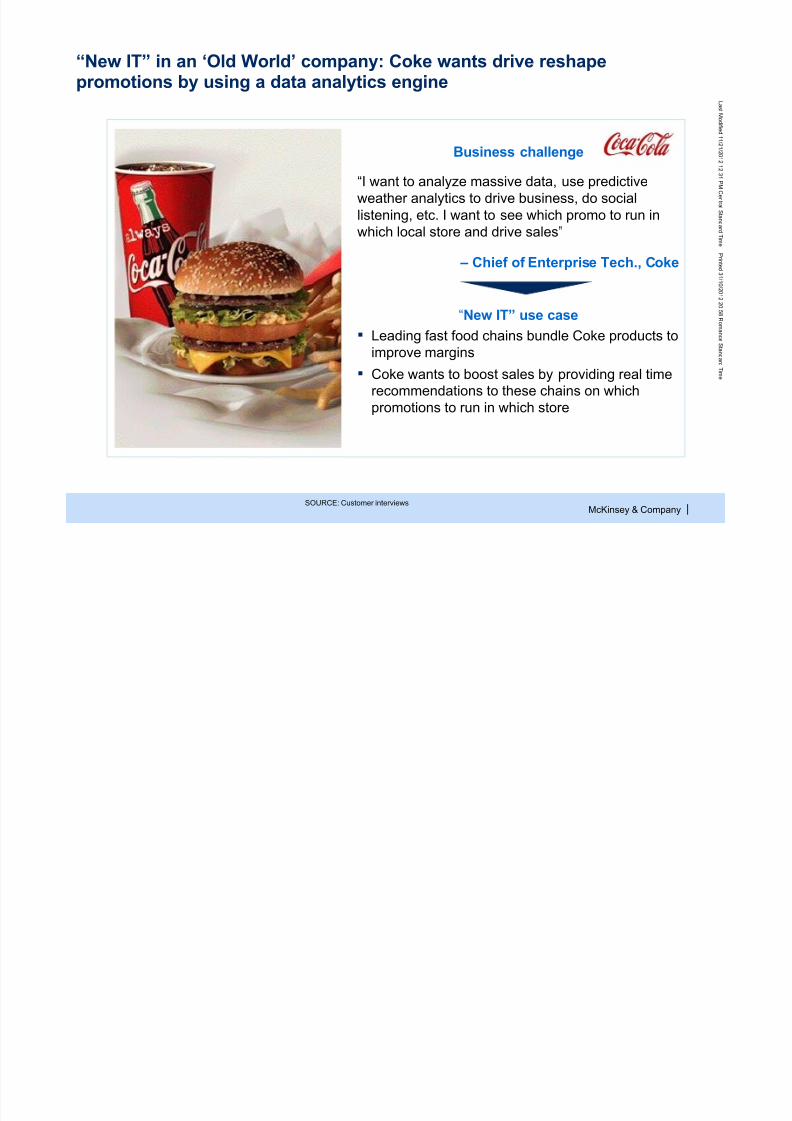

“New IT” in an ‘Old World’ company: Coke wants drive reshapepromotions by using a data analytics engine

SOURCE: Customer interviews

! Leading fast food chains bundle Coke products toimprove margins

!

Coke wants to boost sales by providing real timerecommendations to these chains on whichpromotions to run in which store

Business challenge

“New IT” use case

“I want to analyze massive data, use predictiveweather analytics to drive business, do sociallistening, etc. I want to see which promo to run inwhich local store and drive sales”

– Chief of Enterprise Tech., Coke

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 24/30

McKinsey & Company

L a s t M o d i f i e d 1

1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d 3

1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

|

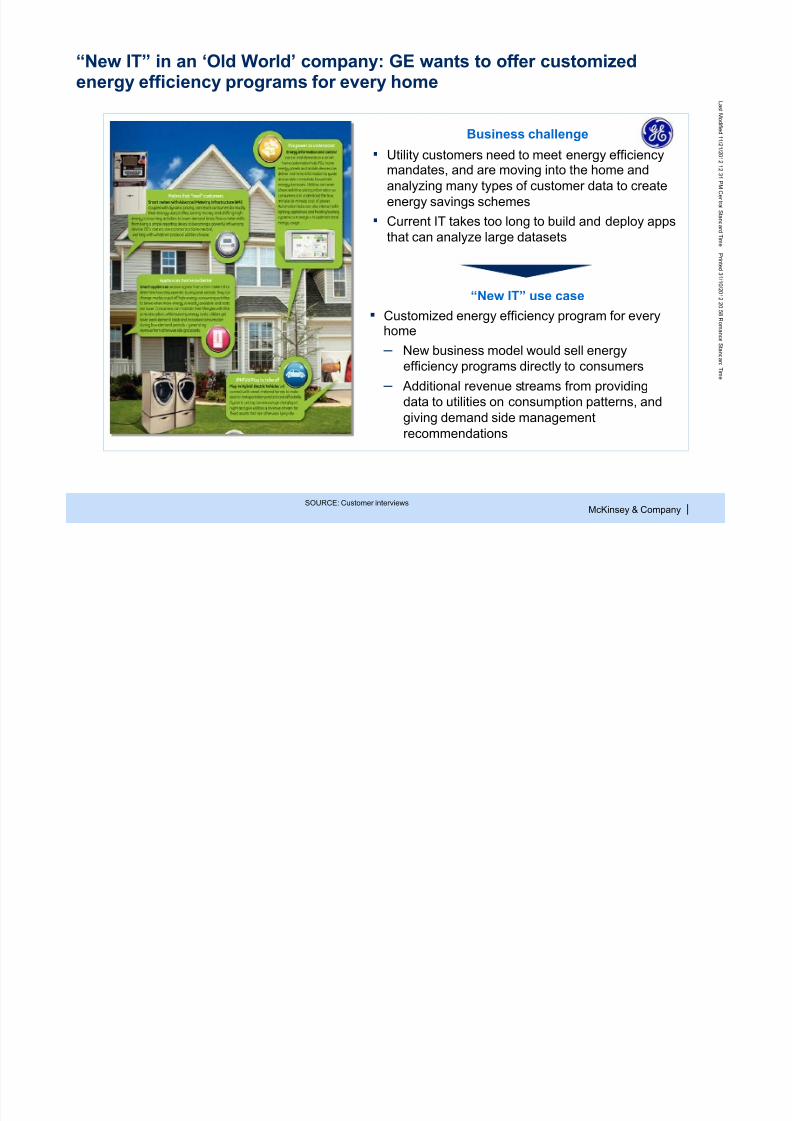

Business challenge

“New IT” in an ‘Old World’ company: GE wants to offer customizedenergy efficiency programs for every home

! Customized energy efficiency program for everyhome

– New business model would sell energyefficiency programs directly to consumers

– Additional revenue streams from providingdata to utilities on consumption patterns, and

giving demand side managementrecommendations

! Utility customers need to meet energy efficiencymandates, and are moving into the home andanalyzing many types of customer data to createenergy savings schemes

! Current IT takes too long to build and deploy appsthat can analyze large datasets

“New IT” use case

SOURCE: Customer interviews

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 25/30

McKinsey & Company

L a s t M o d i f i e d 1

1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d 3

1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

|

What I will talk about today

24

! “Current IT” as we know it is no longer a game-changer

! We already see significant disruption in many

business models

! “New IT” is rising to fill the place of “Current IT”

! How to take advantage of “New IT”

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 26/30

McKinsey & Company

L a s t M o d i f i e d 1

1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d 3 1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

|

CIO’s need to invest in “New IT” to enable business innovationand drive new monetization opportunities

25

Architect the Cloud for futureneeds so as to monetize thesenew business models

Envision the Cloud as avehicle that can delivernew revenue streams

Do not bow down todata silos

Select vendors withintegrated apps plusdata solutions

Engineer the Cloud to deriveinsights from data collectedacross multiple sources and BU’s

Choose solutions that provide anintegrated application and dataplatform, as independent dataand application offerings mightnot provide best in class results

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 27/30

McKinsey & Company

L a s t M o d i f i e d 1

1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d 3 1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

|

Double click page on each next step

26SOURCE: Source

Text

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 28/30

McKinsey & Company

L a s t M o d i f i e d 1

1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d 3 1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

|

Next steps!

27

! How does your organization currentlyview the role of IT?

! How aligned are your businessobjectives for IT and your IT

objectives?

! What kind of transformation do you seeNew IT leading towards in yourorganization

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 29/30

McKinsey & Company

L a s t M o d i f i e d 1

1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d 3 1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

|

Appendix

28

7/26/2019 McKinsey Report NewIT Oct2012

http://slidepdf.com/reader/full/mckinsey-report-newit-oct2012 30/30

McKinsey & Company

L a s t M o d i f i e d 1

1 / 2 1 / 2 0 1 2 1 2 : 3 1 P M C en t r al S t an d ar d T i m e P r i n t e d 3 1 / 1 0 / 2 0 1 2 2 0 : 5 8 R om an c e S t an d ar d T i m e

| 29

CEOs are hoping to see improvements from cloud other than current ITcost reductionsPercent of respondents

SOURCE: McKinsey Quarterly Survey on information and technology strategy, 2010 (BTO strategy Q24, 25)

No

Do notknow

Yes

5

22

29

55

70

Other

Increased ability for ITto scale up (or shrink)to meet business needs

Disaster recovery andbusiness continuity

Lower unit cost of IT

Increased businessflexibility

(N = 332) Multiple selections allowed (N = 252)

Do you believe that cloudcomputing could drive valueat your company?

What are the most significant ways youexpect your company to realize value?

9

1675

Cloud is mainly

a cost reductionplay for CIOs