Embed Size (px)

Citation preview

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Chapter Seventeen

Lending to Business Firms and Pricing Business Loans

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Types of Loans Made By Banks

•Real Estate Loans•Financial Institution Loans•Agriculture Loans•Commercial and Industrial Loans•Loans to Individuals•Miscellaneous Loans•Lease Financing Receivables

16-2

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Loans Outstanding for U.S. Banks (2007)

16-3

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

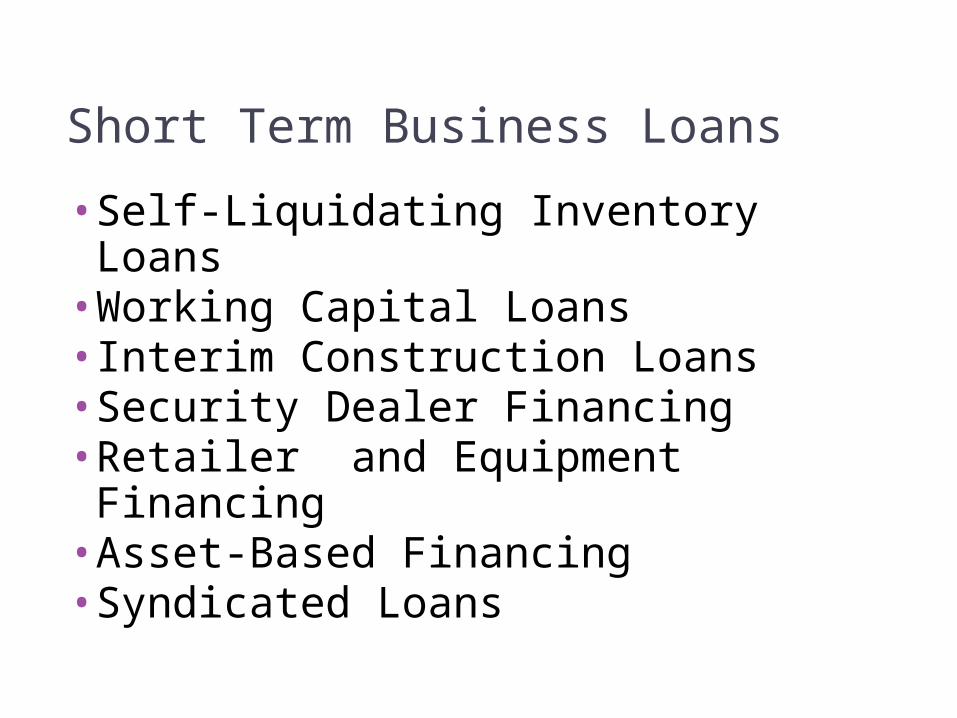

Short Term Business Loans

•Self-Liquidating Inventory Loans•Working Capital Loans•Interim Construction Loans•Security Dealer Financing•Retailer and Equipment Financing•Asset-Based Financing•Syndicated Loans

17-4

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Long Term Business Loans

•Term Loans•Revolving Credit Lines•Project Loans•Loans to Support Acquisitions of Other

Business Firms

•Question: What are the essential differences between various short- and long-term business loans?

17-5

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Sources of Repayment for Business Loans

•The Borrower’s Profits or Cash Flows•Business Assets Pledged as Collateral•Strong Balance Sheet With Ample Marketable Assets and Net Worth

•Guarantees Given By Businesses

17-6

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Common Types of Loan Collateral

Reasons for Taking CollateralTypes of Collateral:▫Accounts Receivables▫Factoring▫Inventory▫Real Property▫Personal Property▫Personal Guarantees

16-7

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

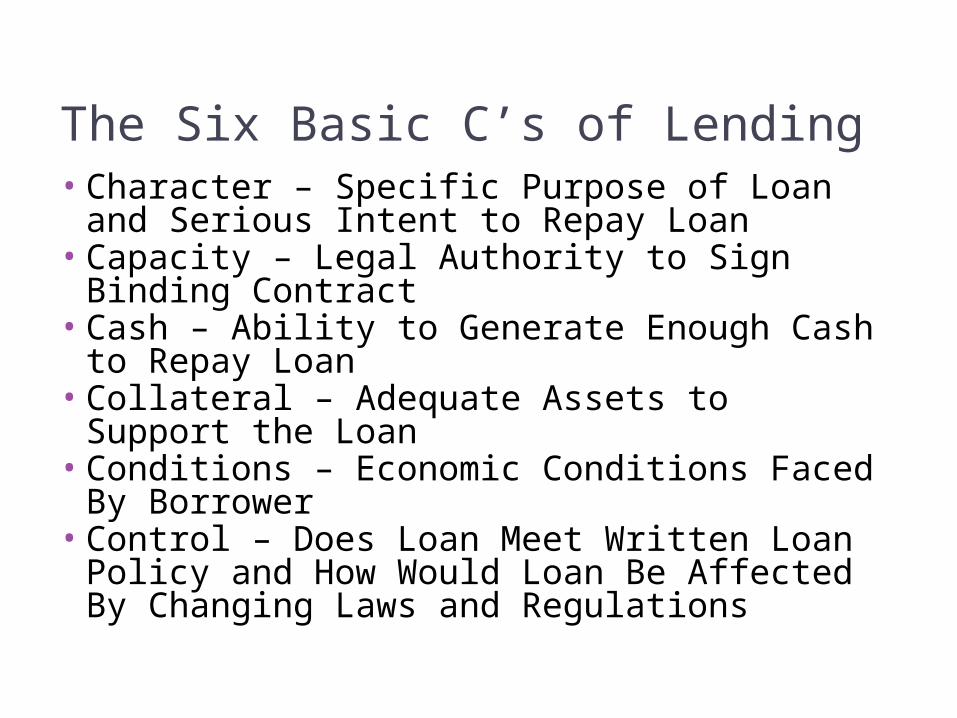

The Six Basic C’s of Lending•Character – Specific Purpose of Loan and

Serious Intent to Repay Loan•Capacity – Legal Authority to Sign Binding

Contract•Cash – Ability to Generate Enough Cash to

Repay Loan•Collateral – Adequate Assets to Support the

Loan•Conditions – Economic Conditions Faced By

Borrower•Control – Does Loan Meet Written Loan Policy

and How Would Loan Be Affected By Changing Laws and Regulations

16-8

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

16-9

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Analyzing Business Loan Applications

•Common Size Ratios of Customer Over Time

•Financial Ratio Analysis of Customer’s Financial Statements

•Current and Pro Forma Sources and Uses of Funds Statement

17-10

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Financial Ratio Analysis•Control Over Expenses•Operating Efficiency•Marketability of Product or Service•Coverage Ratios: Measuring Adequacy of

Earnings•Liquidity Indicators for Business Customers•Profitability Indicators•The Financial Leverage Factor as a Barometer

of a Business Firm’s Capital Structure

17-11

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Expense Control Measures

•Cost of Goods Sold/Net Sales•Selling, Administrative and Other

Expenses/Net Sales•Depreciation Expenses/Net Sales• Interest Expenses on Borrowed Funds

/Net Sales•Taxes/Net Sales

17-12

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Operating Efficiency

•Annual Costs of Goods Sold/Average Inventory

•Average Receivables Collection Period

•Net Sales/Net Fixed Assets•Net Sales/Total Assets•Net Sales/Accounts Receivables

17-13

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

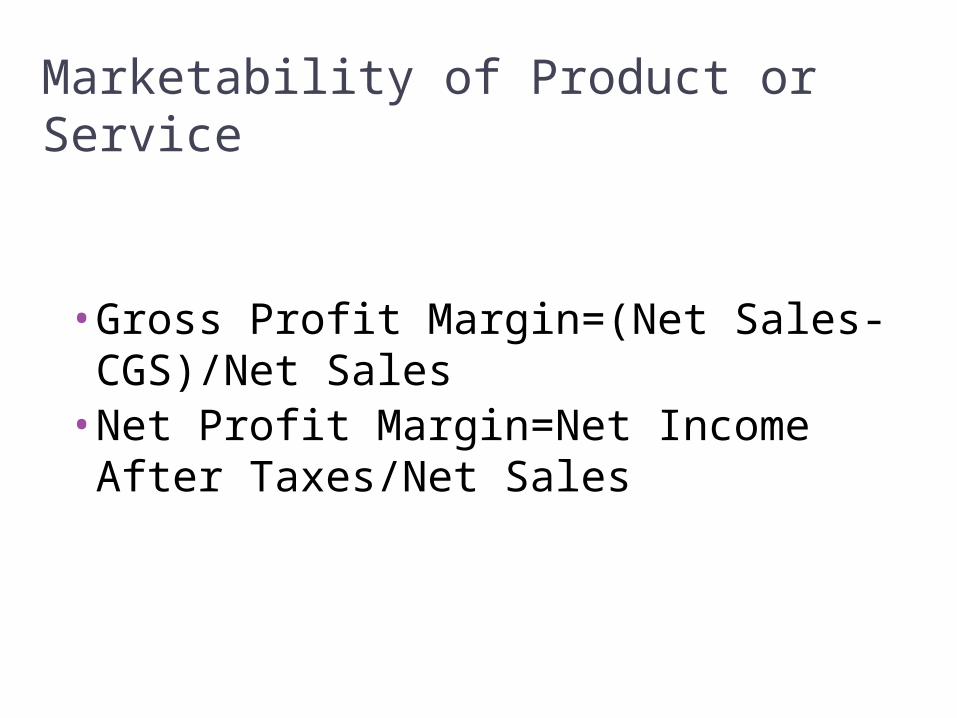

Marketability of Product or Service

•Gross Profit Margin=(Net Sales-CGS)/Net Sales

•Net Profit Margin=Net Income After Taxes/Net Sales

17-14

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Coverage Measures

•Interest Coverage•Coverage of Interest and Principal Payments

17-15

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Liquidity Measures

•Current Assets/Current Liabilities•Acid Test Ratio•Working Capital•Net Liquid Assets

17-16

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Profitability Measures

•Before Tax Net Income/Total Assets•After Tax Net Income/Total Assets•Before Tax Net Income/Net Worth•After Tax Net Income/Net Worth

17-17

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Leverage or Capital Structure Measures

•Leverage Ratio•Total Liabilities/Net Worth•Capitalization Ratio •Debt to Sales Ratio

17-18

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Types of Contingent Liabilities

•Guarantees or Warrantees Behind Products

•Litigation or Pending Lawsuits•Unfunded Pension Liabilities•Taxes Owed But Unpaid•Limiting Regulations

17-19

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Component of Sources and Uses of Funds Statement

•Cash Flows from Operations•Cash Flows from Investing Activities•Cash Flows from Financing Activities

17-20

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Traditional (Direct) Operating Cash Flows

Net Sales Revenue – Cost of Goods Sold – Selling, General and Administrative – Taxes Paid in Cash + Non Cash Expenses

17-21

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Indirect Operating Cash Flows

Net Income + Non Cash Expenses + Losses from the Sale of Assets – Gains from the Sale of Assets – Increases in Assets Associated with Operations + Increases in Current Liabilities Associated with Operations – Decreases in Current Liabilities Associated with Operations + Decreases in Current Assets Associated with Operations

17-22

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

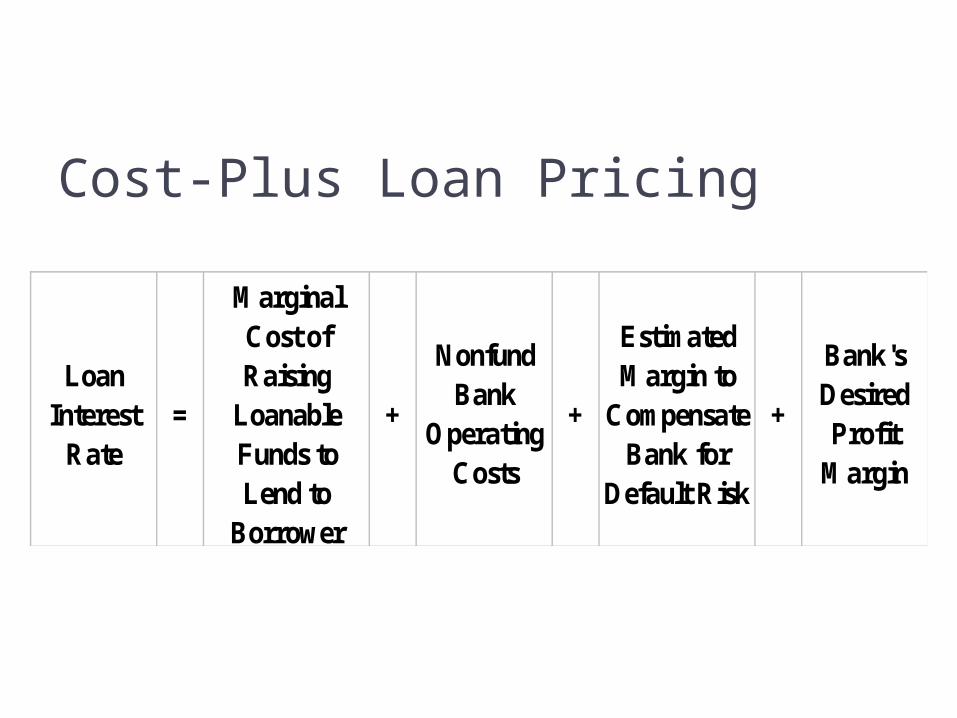

Methods Used to Price Business Loans

•Cost-Plus Loan Pricing Method•Price Leadership Model•Below Prime Market Pricing •Customer Profitability Analysis

17-23

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Cost-Plus Loan Pricing

Loan Interest

Rate=

Marginal Cost of Raising

Loanable Funds to Lend to

Borrower

+

Nonfund Bank

Operating Costs

+

Estimated Margin to

Compensate Bank for

Default Risk

+

Bank's Desired Profit

Margin

17-24

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Price Leadership Model

Loan Interest

Rate=

Base or Prime Rate

+

Default Risk

Premium for Non-

Prime Borrowers

+

Term Risk Premium for

Longer Term Credit

17-25

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Prime Rate

Major Banks Established a Base Lending Fee During the Great Depression. At that Time It Was the Lowest Interest Rate Charged Their Most Credit Worthy Customers for Short-Term Working Capital Loans

17-26

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

LIBOR

The London Interbank Offer Rate. The Rate Offered on Short-Term Eurodollar Deposits With Maturities Ranging From a Few Days to a Few Months

17-27

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Below-Prime Market Pricing

Loan Interest

Rate=

Interest Cost of Borrowing in the Money

Market

+Markup for Risk

and Profit

17-28

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Chapter EighteenConsumer Loans, Credit Cards, and Real Estate Lending

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Consumer Lending

•Has been among the most popular financial services offered in recent years

•One of the most important sources of revenues and deposits for banks and their competitors (credit unions, savings associations, and finance and insurance companies); a source of supplemental income

•On the other hand, presents a special challenge due to higher-than-average default rates.

18-30

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

0.91%

0.21%

4.67%

0.30%0.12%

1.57%

0.59%0.31% 0.25%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

InternationalBanks

AgriculturalBanks

Credit CardLenders

CommercialLenders

MortgageLenders

ConsumerLenders

OtherSpecialized <

$1 Billion

All Other <$1 Billion

All Other >$1 Billion

Performance and Chargeoffs by Bank Category, 12/2004

0.76%1.23%

4.01%

1.30% 1.18%1.66% 1.66%

1.10%1.35%

0.0%0.5%1.0%1.5%2.0%2.5%3.0%3.5%4.0%4.5%5.0%

InternationalBanks

AgriculturalBanks

Credit CardLenders

CommercialLenders

MortgageLenders

ConsumerLenders

OtherSpecialized <

$1 Billion

All Other <$1 Billion

All Other >$1 Billion

18-31

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Types of Consumer Loans

•Classify Consumer Loans by Purpose – What the Borrowed Funds are Used For, or by Type – Whether the Borrower Must Repay in Installments or in One Lump Sum

•Residential Mortgage Loans•Nonresidential Loans▫Installment Loans▫Noninstallment Loans

•Credit Card Loans and Revolving Credit

18-32

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Residential Mortgage Loans

Credit to Finance the Purchase of Residential Property in the Form of Houses and Multifamily Dwellings. This is Usually a Long-Term Loan (15-30 years) Which is Secured By the Property Itself. Fixed or Variable Rate of Interest

18-33

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Nonresidential Loans: Installment Loans

Short-Term to Medium-Term Loans Repayable in Two or More Consecutive Payments, Usually Monthly or Quarterly. These Are Often Used to Finance Big Ticket Purchases or Consolidate Existing Debt (automobile, furniture, appliances).

18-34

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Noninstallment Loans

Short-Term Loans By Individuals for Immediate Cash Needs and Repayable in One Lump Sum When the Borrower’s Note Matures (charge accounts, medical care, auto and home repairs)

18-35

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Credit Card Loans

• Credit Cards Offer Holders Access to Either Installment or Noninstallment Credit.

• Banks Find That the Installment Users of Credit Cards are the Most Profitable – Provide Higher Risk-Adjusted Returns Than Other Types of Loans.

• Card issuers earn income from: Cardholders’ annual fees Interest on outstanding loan balances Discounting the charges that merchants accept

on purchases.

18-36

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Credit Card Regulations•U.S. Regulators of Depository Institutions

-- OCC, Fed, FDIC, and OTS -- in 2003, Moved to Slow the Expansion of Card Offers to Customers with Low Credit Ratings

•More recently, May 2009: ▫ Strict limits on marketing to college students and

other prospective cardholders under the age of 21▫ Preventing cardholder accounts from being charged

beyond their limits▫Clearer disclosure of credit card interest rates and

repayment estimates, using standard text sizes and styles

▫ Tougher rules related to raising interest rates on delinquent cardholders, with clear paths to rehabilitate credit card accounts.

18-37

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Debit Cards

Debit Cards Can Be Used To Pay For Goods And Services, But Not To Extend Credit. They Are A Convenient Vehicle For Making Deposits Into And Withdrawals From ATMs And They Facilitate Check Cashing.

18-38

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Outstanding Consumer Debt as a Percent of Disposable Income

18-39

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Consumer Debt Service Ratio

18-40

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Characteristics of Consumer Loans

•Most Costly and Most Risky to Make Per Dollar

•Cyclically Sensitive•Interest Inelastic

18-41

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Evaluating a Consumer Loan Application

•Character and Purpose• Income Levels•Deposit Balances•Employment and Residential Stability•Pyramiding of Debt

18-42

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Credit Bureaus

•Credit Reporting Agencies or Credit Bureaus Assemble and Distribute to Lenders the Credit History of Millions of Borrowers

• Information▫Personal Identifying Data▫Personal Credit Histories▫Public Information That May Have Bearing

on Loan

18-43

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Credit Scoring

Credit Scoring Systems are Based on Sophisticated Statistical Models in Which Several Variables are Joined to Establish a Numerical Score to Separate Good Loans From Bad Loans. The Most Famous of These is the FICO Scoring System Developed by Fair Isaac.

18-44

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

18-45

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Laws and Regulations Applying to Consumer Loans1. Disclosure Rules▫Truth in Lending Act, passed in 1968,

simplified in 1981▫Fair Credit Reporting Act, 1974▫Fair Credit Billing Act▫Fair Debt Collection Practices Act

2. Antidiscrimination Laws▫Equal Credit Opportunity Act▫Community Reinvestment Act▫Home Ownership and Equity Protection Act

18-46

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Predatory Lending and Subprime Loans

An Abusive Practice Among Some Lenders That Consists of Granting Loans to Subprime Borrowers and Charging Them Excessive Interest Rates and Fees, Increasing the Risk of Default. Subprime Lending Played Important Role in the 2007 Credit Crisis.

18-47

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Real Estate Loans

•Among the Riskiest Loans Banks Can Make

•Average Size is Larger Than the Average Size of Other Loans

•Tend to Have Longer Maturities Than Other Loans

18-48

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Factors Used in Evaluating Real Estate Loans•Size of Down Payment Relative to

Purchase Price of Property•Should Be Evaluated in Terms of Total

Relationship•Need to Pay Attention to Particular Aspects

of Credit Application:▫Amount and Stability of Income (Gross Debt

Service)▫Available Savings and Source of Down Payment▫Track Record in Maintaining Property▫Outlook for Real Estate Market in Local Area▫Outlook for Interest Rates If Variable Rate Loan

18-49

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Home Equity Lending

•Home Owners Can Use the Difference in Home’s Estimated Value and Remaining Mortgages as a Borrowing Base

•Two Types of Credit▫Closed End Credit▫Lines of Credit

•Can Be Used for Any Legitimate Purpose•The 1986 Tax Reform Act Has Helped This

Type of Loan Grow in Popularity

18-50

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Interest Only Mortgages: The Most Controversial of Home Mortgage Loans •Many of these are Adjustable Rate Mortgages•Home Owner Can Pay the Interest Only for an

Initial Period•Mortgage Payments Can be Much Higher

When Principal Payments are Due Because of the Shorter Period to Repay the Loan

•Especially Problematic When House Prices Stop Climbing Upward

•During the Recent Crisis, the Fed Moved to Tighten the Rules on Mortgage Lending to Promote Greater Transparency in Loan Terms

18-51

McGraw-Hill/IrwinBank Management and Financial Services, 7/e

© 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Cost-Plus Model of Pricing Loans

Loan Rate Paid by

Consumer=

Lender's Cost of Raising Funds

+Nonfunding Operating

Costs+

Risk Premium

for Customer

Default

+

Risk Premium for Time

to Maturity

+Desired Profit

Margin

18-52