Embed Size (px)

Citation preview

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 1/45

The Theory of the Firm

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 2/45

The Costs of Production

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 3/45

Outline

• What are costs?

• Link between firm’s production process and its

total cost• Measures of Cost

• Costs in the short-run and costs in the long-run

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 4/45

Basic Concepts

• Total Revenue- Amount a firm receives for

the sale of its output• Total Cost- Market value of the inputs a firm

uses in production

• Profit = Total Revenue – Total Cost

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 5/45

Actual Cost & Opportunity Cost

• Explicit/Actual Costs

-Actual expenditure incurred for producing goods/services

-Costs that are generally recorded in the books of account,eg. Salaries paid, cost of materials/inputs purchased

- Input costs that require an outlay of money by the firm. Eg.X starts a business, pays Rs 100000 as salaries, Rs 100000is the actual cost

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 6/45

Actual Cost & Opportunity Cost

• Implicit/Opportunity Costs

-OC of a good/service is measured in terms of revenue whichcould have been earned by employing that good/service in

another alternative use-Eg. X could earn Rs 50000 a month as a software

professional, this foregone income is an opportunity cost

• An accountant would consider only explicit costs as visible

money flows are observed in business• An economist would also consider implicit costs like

foregone income

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 7/45

Cost of Capital as an Opportunity Cost

• Opportunity Cost of the financial capitalinvested in business

• Eg. X has invested 1000000 to start a business.

Opportunity cost is the income X forgoes hadhe kept this amount in a bank (at the rate of 5-

7%). This is the implicit opportunity cost of the

business

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 8/45

Economic Cost

• The key principle underlying thecomputation of economic cost isopportunity cost.

PRINCIPLE of Opportunity Cost The opportunity cost of something is what you

sacrifice to get it.

In economics, the notion of a firm’s costs

is based on the notion of economic cost.

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 9/45

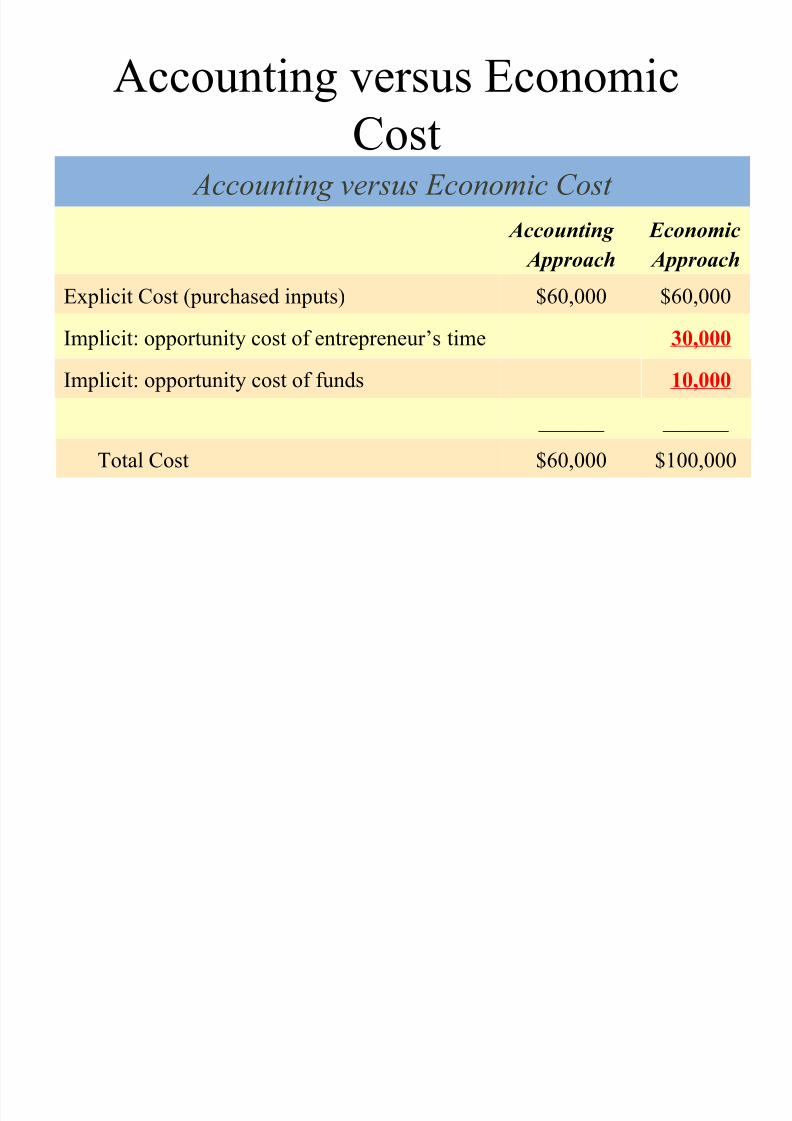

Accounting versus Economic

Cost

$100,000$60,000Total Cost

______ ______

10,000Implicit: opportunity cost of funds

30,000Implicit: opportunity cost of entrepreneur’s time

$60,000$60,000Explicit Cost (purchased inputs)

Economic

Approach

Accounting

Approach

Accounting versus Economic Cost

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 10/45

Economic Profit Vs Accounting Profit

• Economic Profit = Total Revenue minus

Total Cost, including both explicit and

implicit costs

• Accounting Profit = Total Revenue minusTotal explicit costs

• Economic Value-Added = NOPAT – Cost of

Capital (Cost of Debt + Cost of Equity)

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 11/45

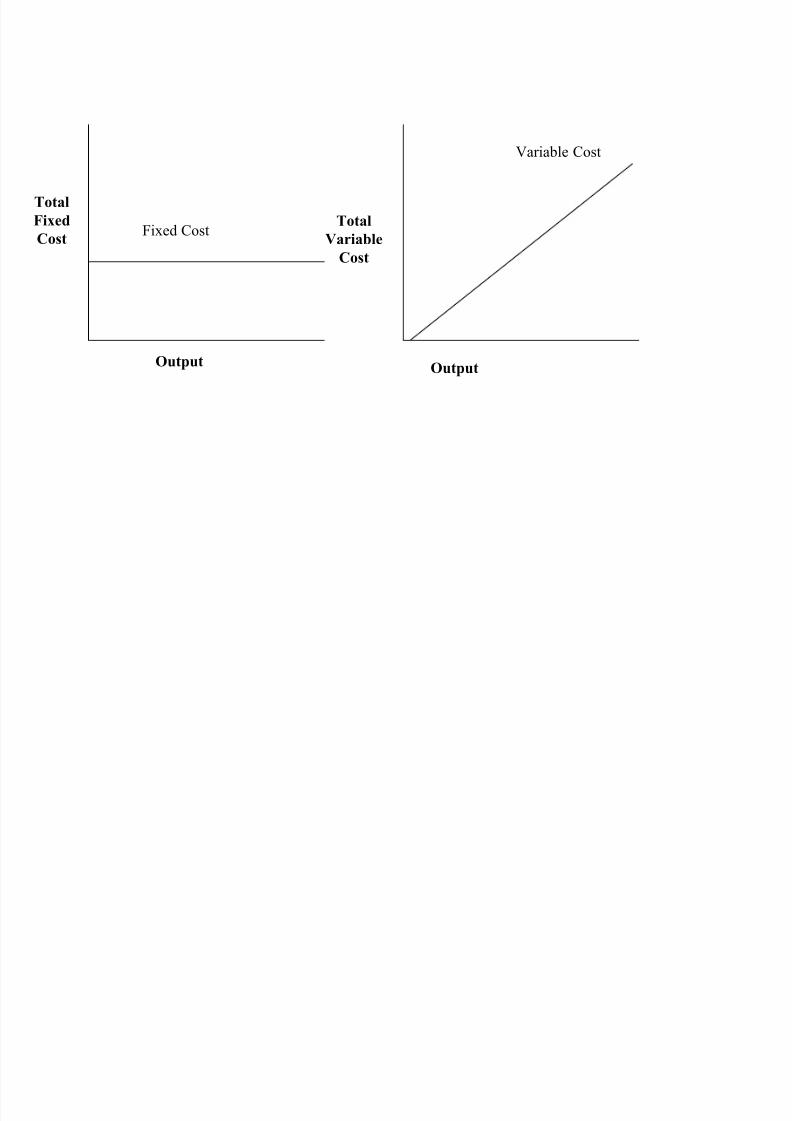

Fixed Costs & Variable Costs

• In buying factor inputs, the firm will incur costs

• Costs are Classified as:

– Fixed costs – costs that are not related directly to

production – rent, insurance costs, admin costs. Theycan change but not in relation to output/production.

– Fixed Costs are incurred even when output is nil

– Variable Costs – costs directly related to variations in

output. Raw materials, labour, primarily.

– Increase in volume means a proportionate increase in

total variable cost and vice versa

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 12/45

Total

Fixed

CostFixed Cost

Output

Total

Variable

Cost

Variable Cost

Output

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 13/45

Short-run & Long-run Costs

• Time Horizon key factor in dividing costs into short-run and

long-run costs• Short run – In the short-run increase in production results from

adding successive quantities of variable factors to a fixed factor

- Short-run costs are costs that vary with output when fixed plant

and capital equipment remain the same- Relevant when a firm decides whether or not to produce more in

the immediate future

• Long run – Increases in capacity results in increasing production.All costs become variable in the long-run

- Long-run costs are those which vary with output when all inputfactors including plant and equipment vary

- Relevant when a firm decides whether to set up a new plant.

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 14/45

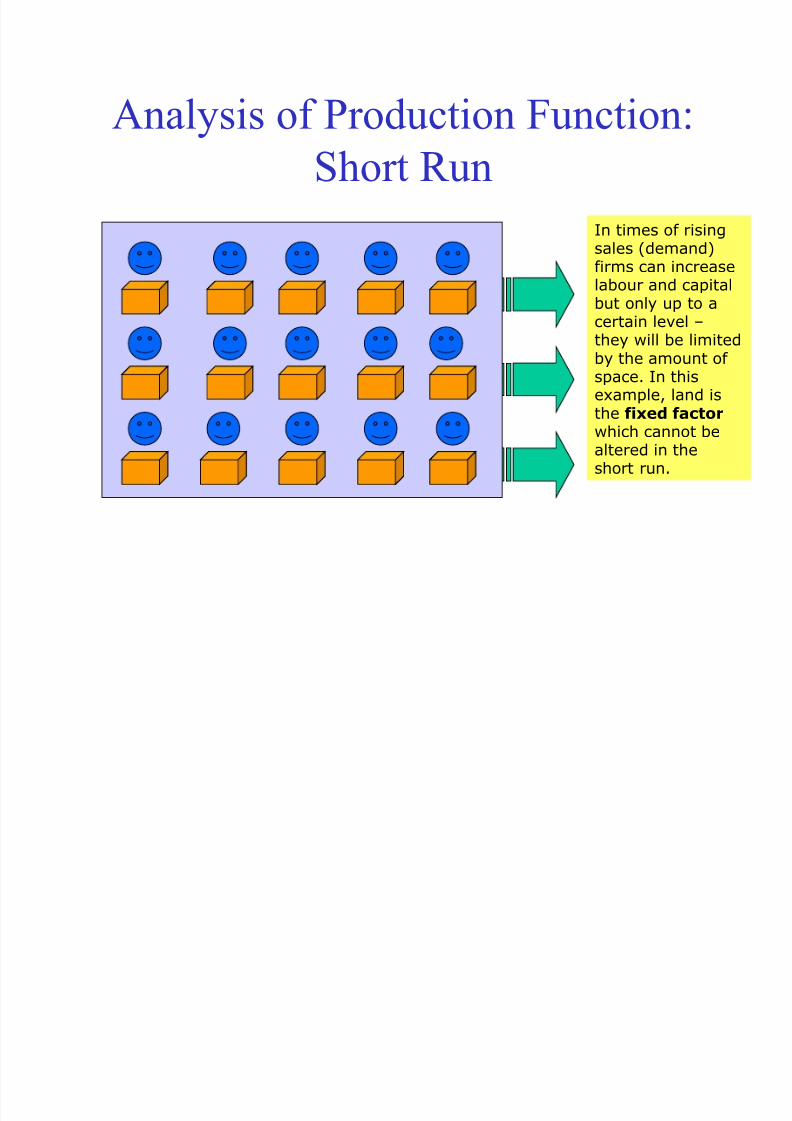

Analysis of Production Function:

Short Run

In times of risingsales (demand)firms can increaselabour and capitalbut only up to acertain level –they will be limitedby the amount of space. In thisexample, land is

the fixed factor which cannot bealtered in theshort run.

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 15/45

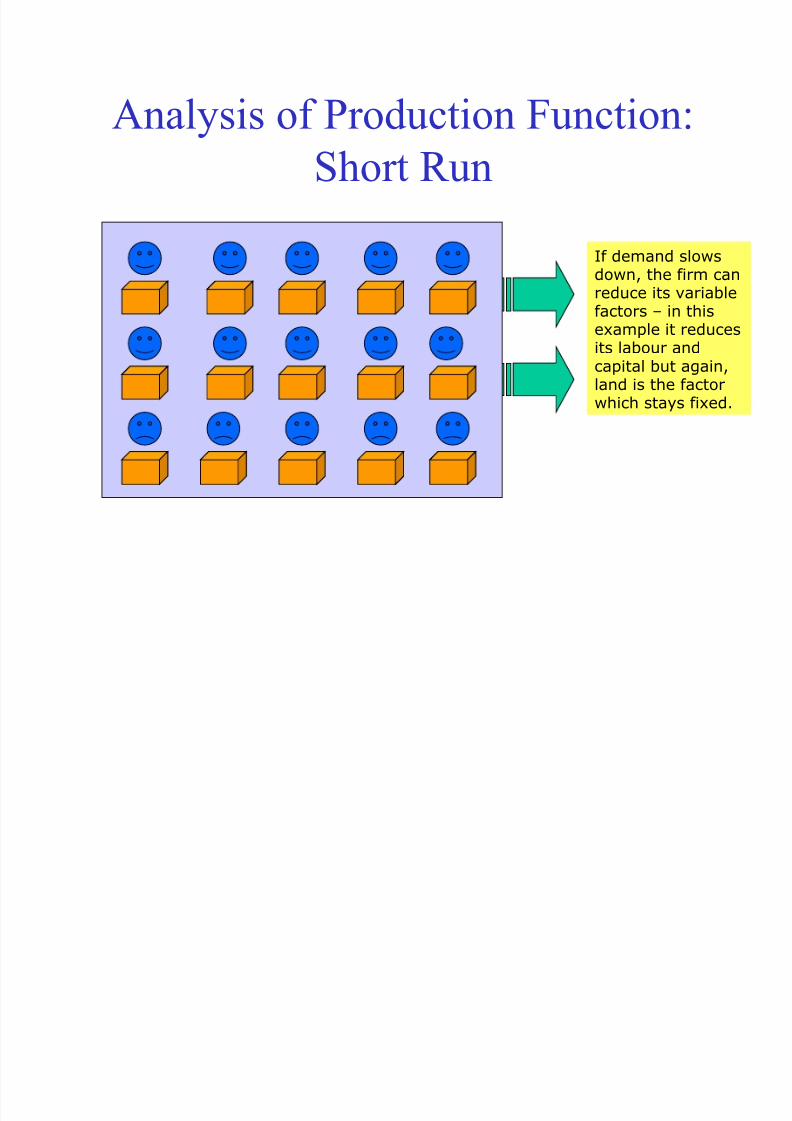

Analysis of Production Function:

Short Run

If demand slows

down, the firm canreduce its variablefactors – in thisexample it reducesits labour andcapital but again,land is the factorwhich stays fixed.

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 16/45

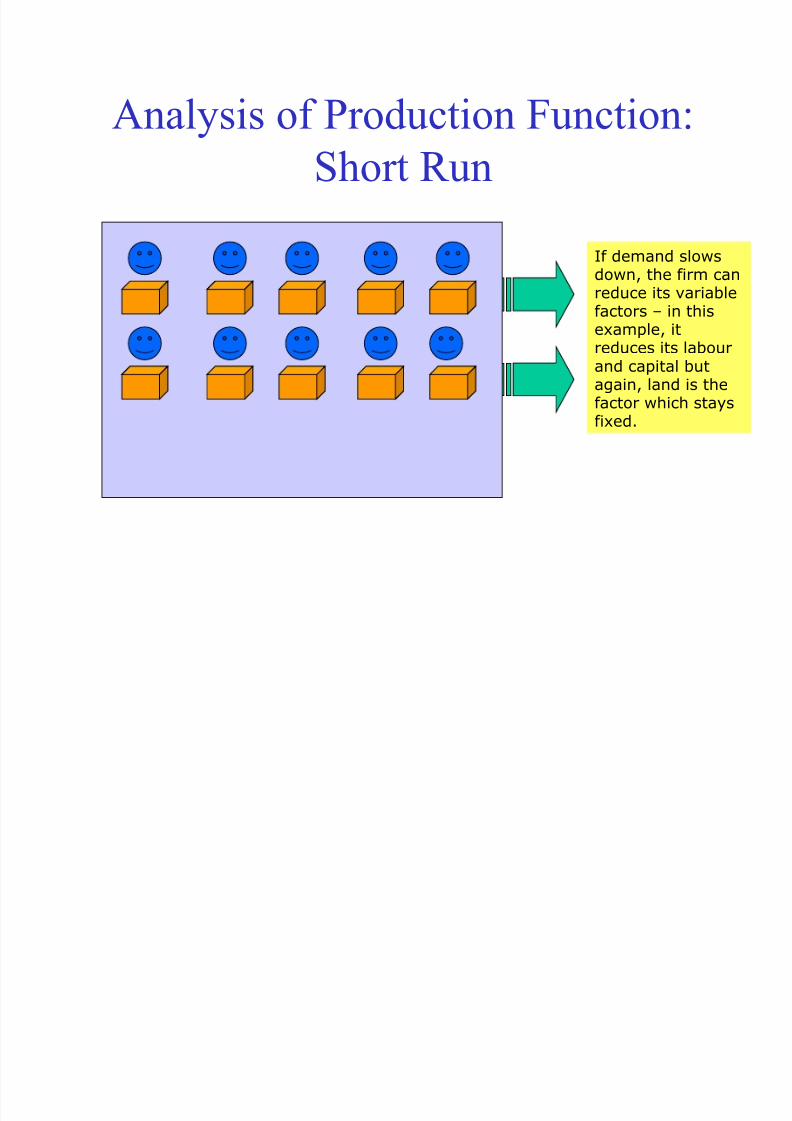

Analysis of Production Function:

Short Run

If demand slows

down, the firm canreduce its variablefactors – in thisexample, itreduces its labourand capital butagain, land is thefactor which stays

fixed.

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 17/45

Analysing the Production Function:

Long Run• The long run is defined as the period of time taken to vary

all factors of production.

– By doing this, the firm is able to increase its total

capacity – not just short term capacity

– Associated with a change in the scale of production

– The period of time varies according to the firm and the

industry.

– In electricity supply, the time taken to build new

capacity could be many years; for a market stall holder,

the ‘long run’ could be as little as a few weeks or

months!

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 18/45

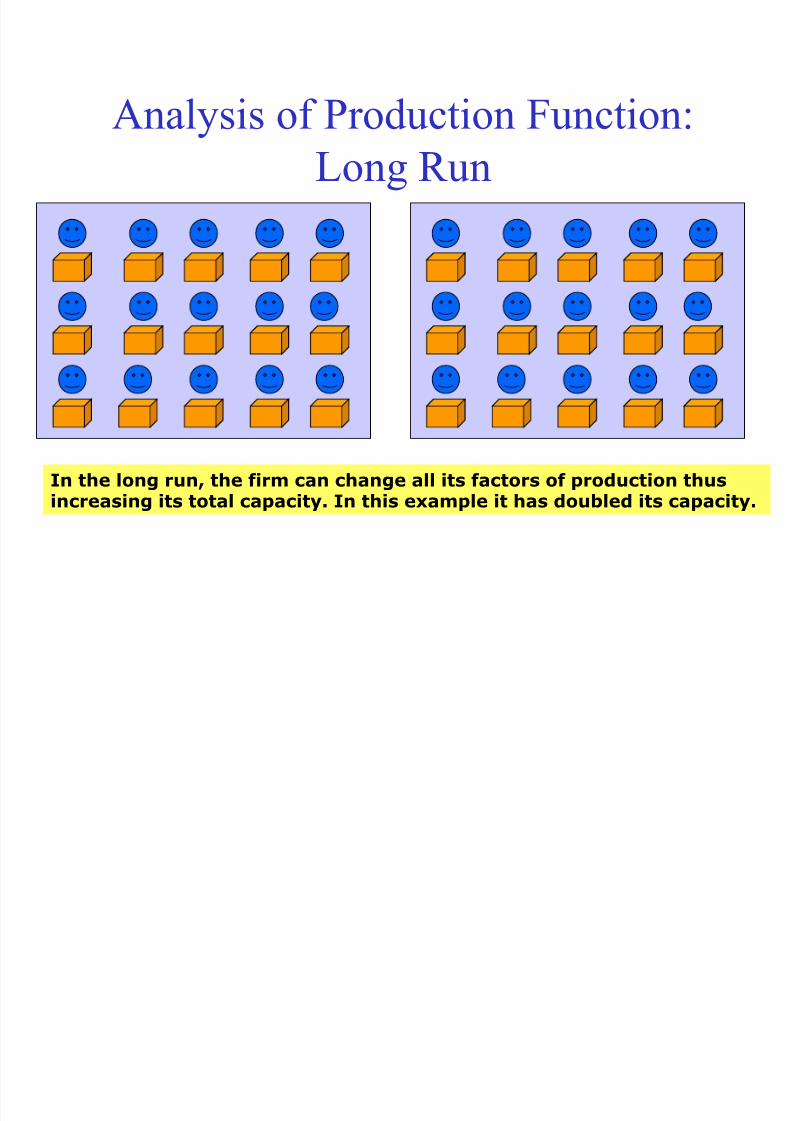

Analysis of Production Function:

Long Run

In the long run, the firm can change all its factors of production thusincreasing its total capacity. In this example it has doubled its capacity.

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 19/45

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 20/45

Incremental/Differential Costs & Sunk Costs

• Incremental cost is the additional cost due to a changein the level or nature of business activity

-Change may take several forms: addition of a new

product-line, changing channel of distribution, adding

of new machines, expansion into additional markets• Sunk Costs is one which is not affected/altered by a

change in the level or nature of business activity

-Remains the same whatever the level of activityEg operating costs and space and occupancy costs

remain the same whether equipment is purchased or

hired

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 21/45

Other Cost Categories

• Out-of-pocket and Book Costs-Out-of-pocket costs involve current cash payments to

outsiders

-Book costs do not require current cash payments, eg

depreciation• Direct and Indirect Costs

-Direct/traceable costs can be identified very easilywith a unit of operation eg salary of a divisionalmanager

-Indirect costs are those that are not easily traceable toa unit of operation eg salary of a general manager

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 22/45

…Other Cost Categories

• Replacement and historical costs

-Historical cost is the original price paid for

equipment, replacement cost means price

that would have to be paid currently for acquiring the same equipment

• Controllable and Uncontrollable costs

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 23/45

Production & Costs

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 24/45

Production Function

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 25/45

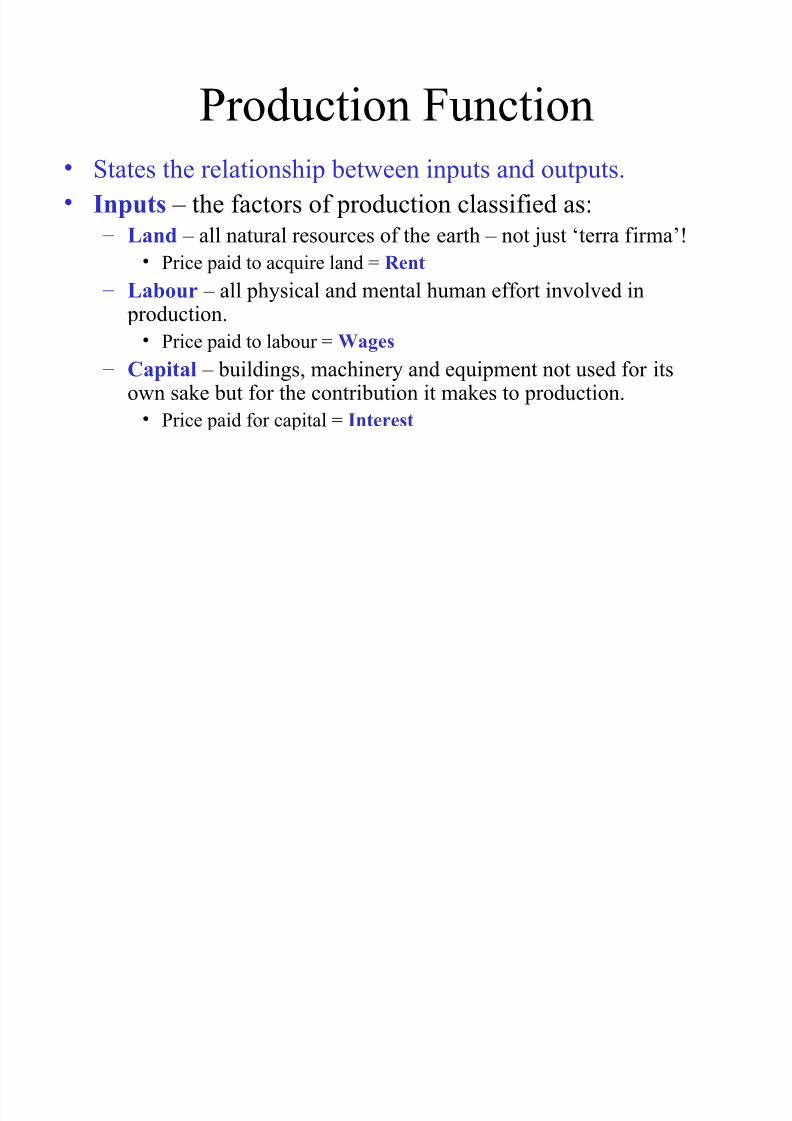

Production Function• States the relationship between inputs and outputs.

• Inputs – the factors of production classified as: – Land – all natural resources of the earth – not just ‘terra firma’!

• Price paid to acquire land = Rent

– Labour – all physical and mental human effort involved in production.

• Price paid to labour = Wages

– Capital – buildings, machinery and equipment not used for itsown sake but for the contribution it makes to production.

• Price paid for capital = Interest

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 26/45

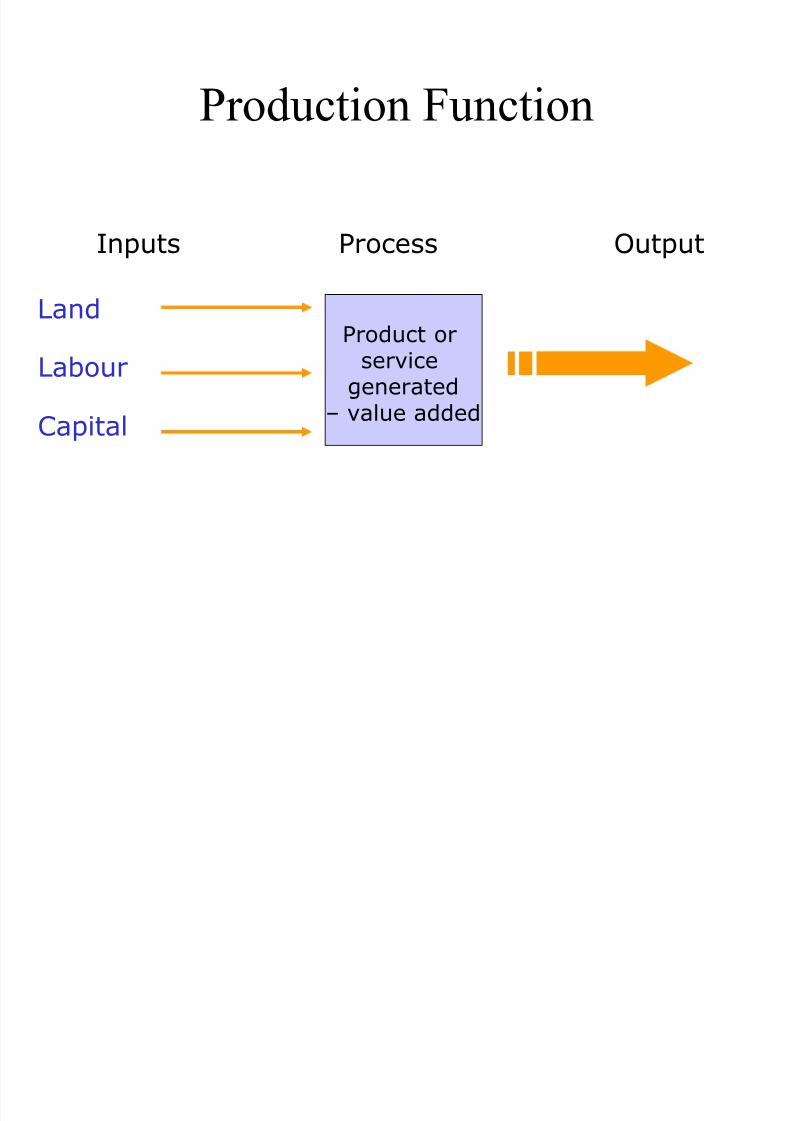

Production Function

Inputs Process Output

Land

Labour

Capital

Product orservice

generated

– value added

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 27/45

… Production Function

• Marginal Product: Increase in output that arisesfrom an additional unit of input

•Diminishing Marginal Product: Marginal Productof an input declines as the quantity of the inputincreases (Why?)

-Initially increasing returns due to efficient

utilisation of fixed factor as more units of variablefactor are applied to it (MP increasing)

-Subsequently diminishing returns as the fixed factor becomes more and more scarce in relation to the

variable factor (MP diminishing)

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 28/45

Analysis of Production Function:

Short Run

• In the short run at least one factor fixed in supply but all other

factors capable of being changed.

• Reflects ways in which firms respond to changes in output

(demand).

• Can increase or decrease output using more or less of some

factors but some likely to be easier to change than others.

• Increase in total capacity only possible in the long run

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 29/45

Production Function

• Mathematical representation of the

relationship:

• Q = f (K, L, La)

• Output (Q) is dependent upon the amount

of capital (K), Land (L) and Labour (La)

used.

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 30/45

Diminishing Returns and

Marginal Cost• The key principle behind the firm’s short-

run cost curves is the principle of

diminishing returns.PRINCIPLE of Diminishing ReturnsSuppose that output is produced with two or more

inputs and we increase one input while holding the

other inputs fixed. Beyond some point—called the

point of diminishing returns—output will increase at a

decreasing rate.

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 31/45

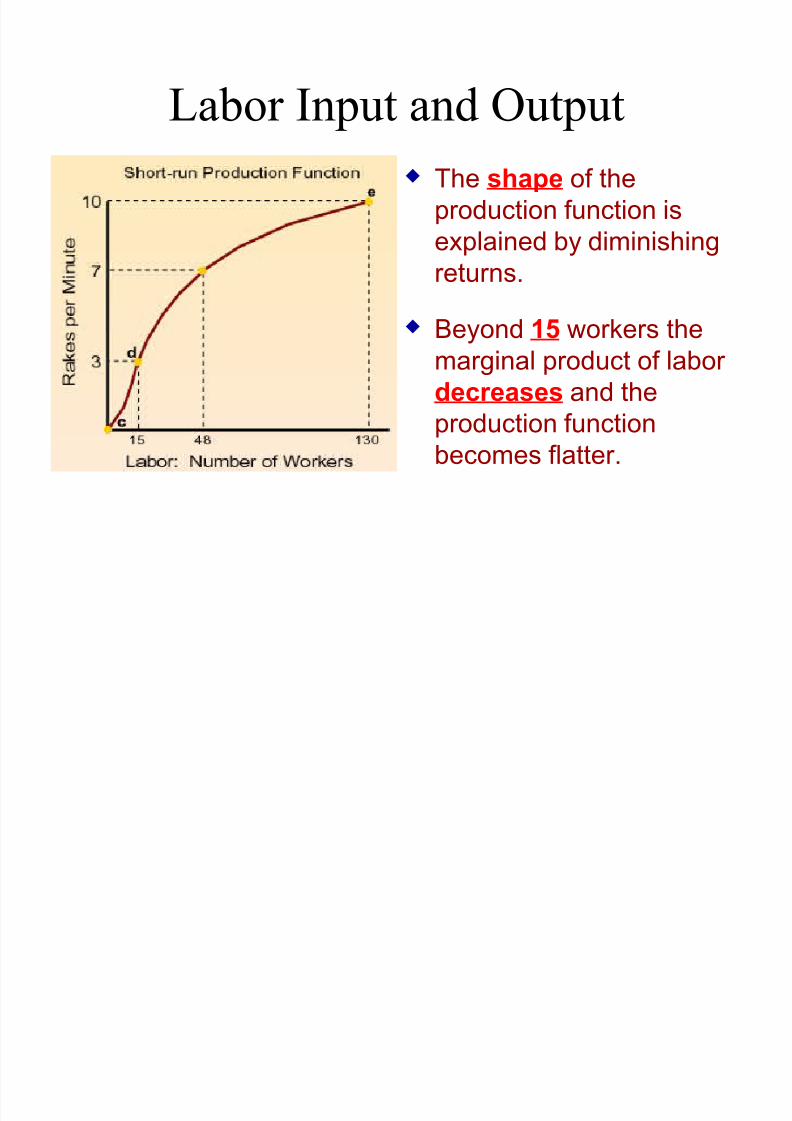

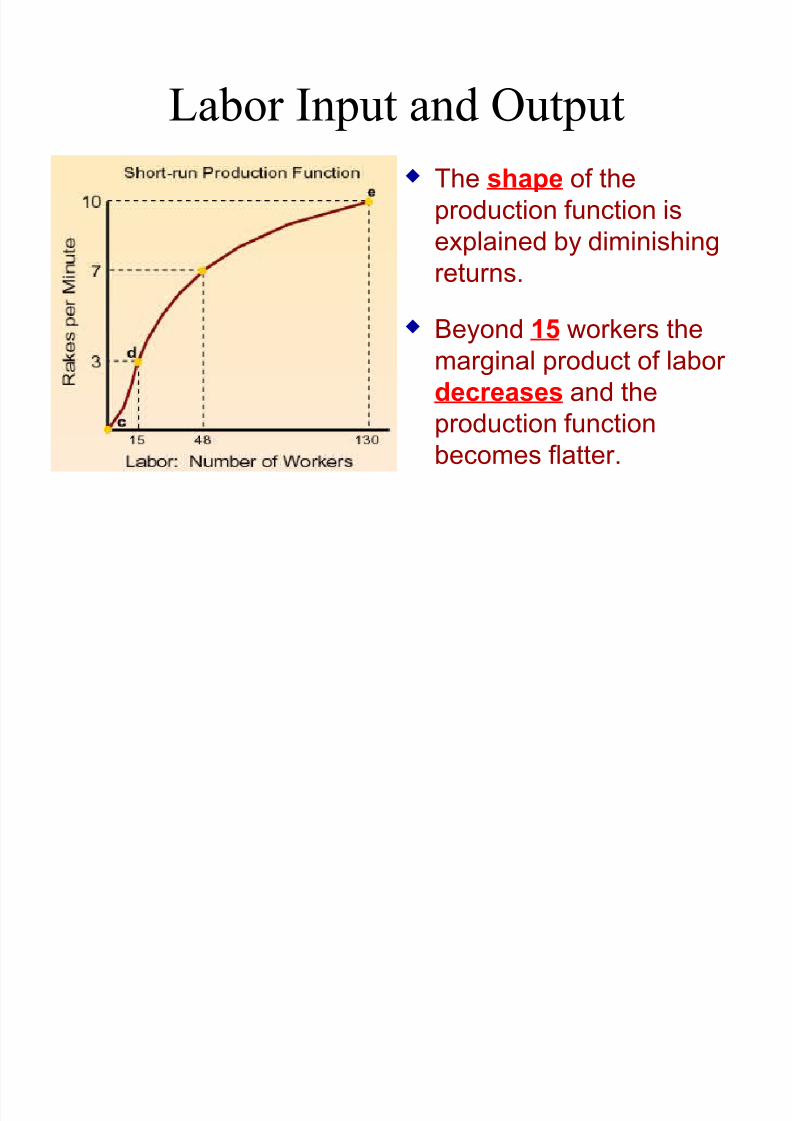

Labor Input and Output

The shape of the

production function is

explained by diminishing

returns.

Beyond 15 workers the

marginal product of labor

decreases and the

production functionbecomes flatter.

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 32/45

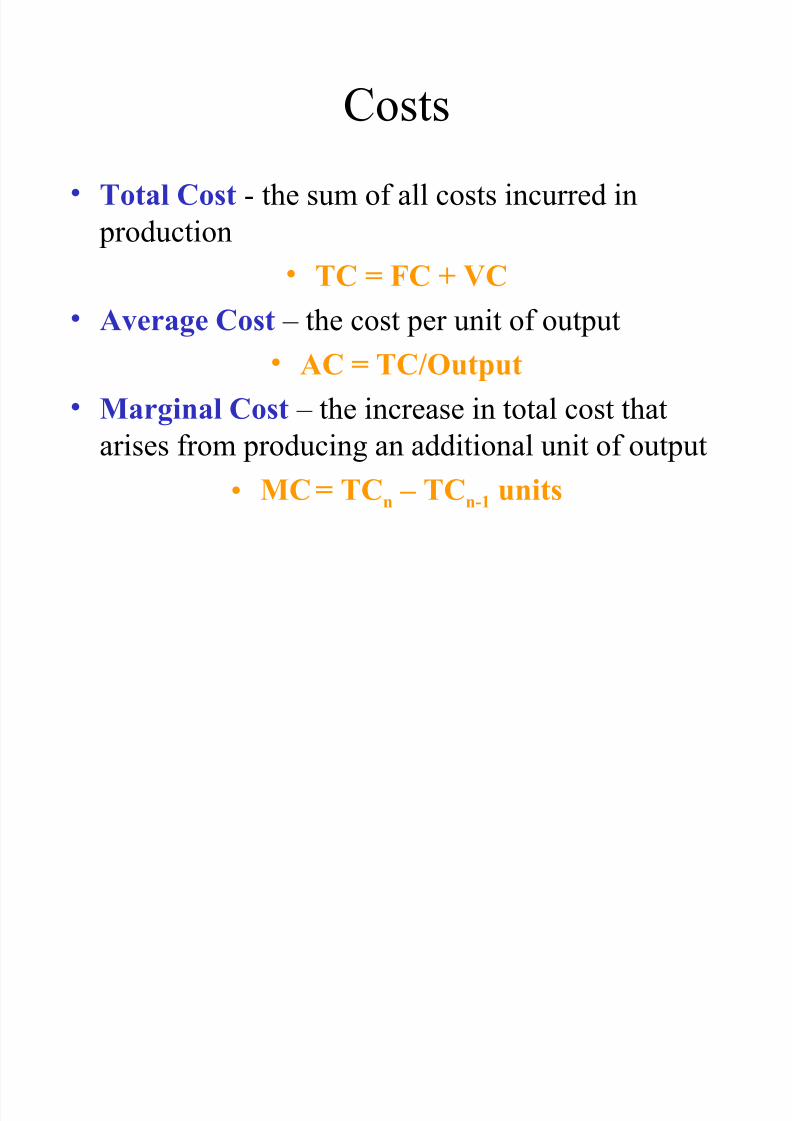

Costs

• Total Cost - the sum of all costs incurred in

production

• TC = FC + VC• Average Cost – the cost per unit of output

• AC = TC/Output

• Marginal Cost – the increase in total cost thatarises from producing an additional unit of output

• MC = TCn – TCn-1 units

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 33/45

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 34/45

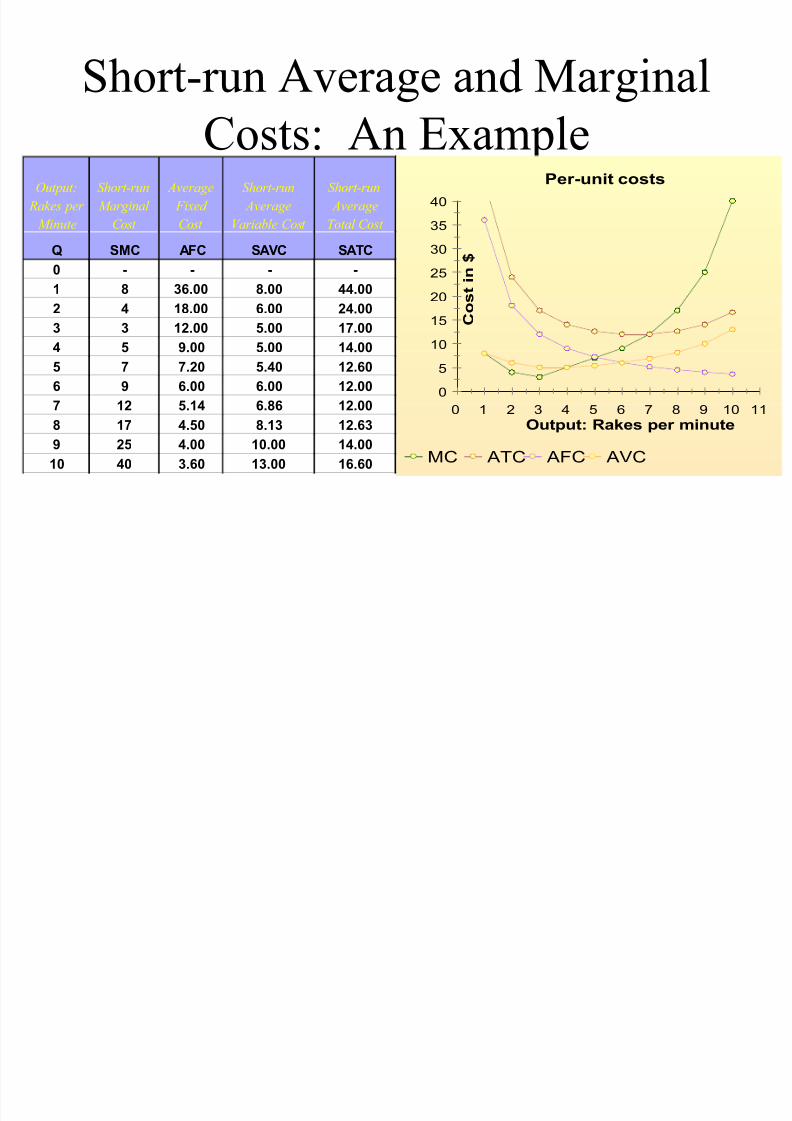

Short-run Average and Marginal

Costs: An Example

0

5

10

15

20

25

30

35

40

C o s t i

n $

0 1 2 3 4 5 6 7 8 9 10 11

Output: Rakes per minute

MC ATC AFC AVC

Per-unit costs

Total Cost

Average

Short-run

Variable Cost

Average

Short-run

Cost

Fixed

Average

Cost

Marginal

Short-run

Minute

Rakes per

Output:

SATCSAVCAFCSMCQ

----0

44.008.0036.0081

24.006.0018.0042

17.005.0012.0033

14.005.009.0054

12.605.407.2075

12.006.006.0096

12.006.865.14127

12.638.134.50178

14.0010.004.00259

16.6013.003.604010

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 35/45

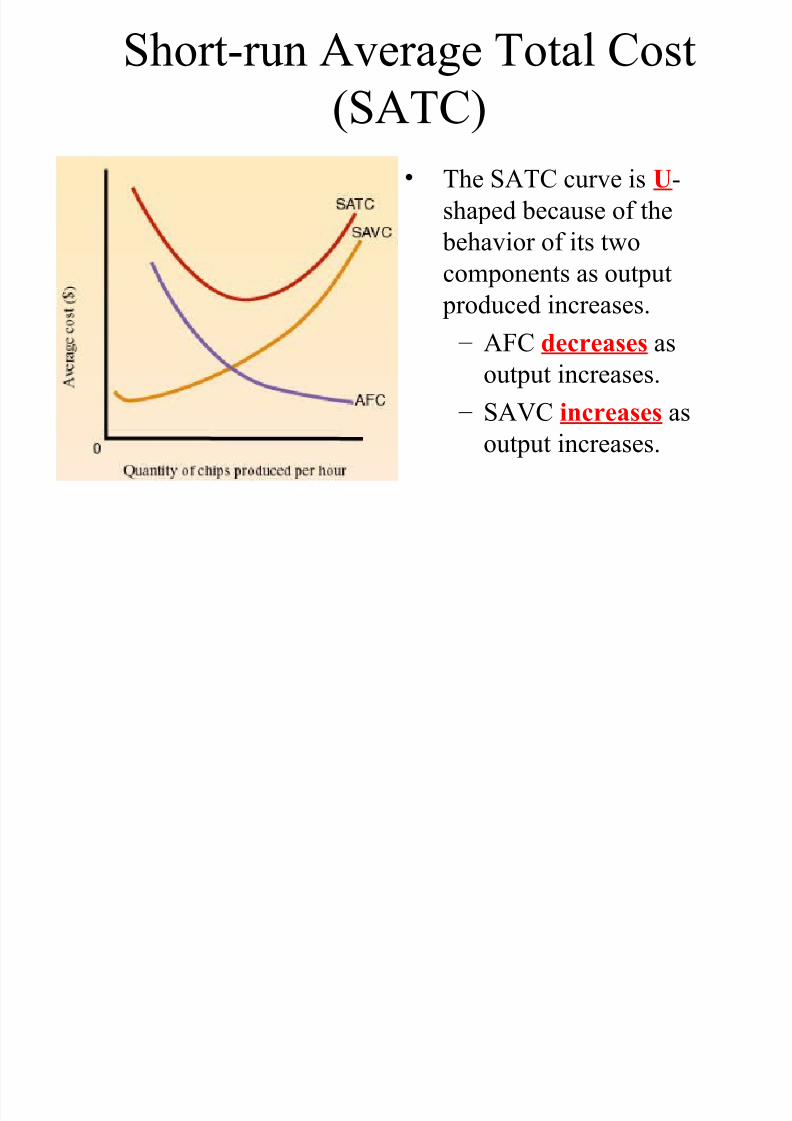

Short-run Average Total Cost

(SATC)

• The SATC curve is U-

shaped because of the

behavior of its two

components as output produced increases.

– AFC decreases as

output increases.

– SAVC increases asoutput increases.

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 36/45

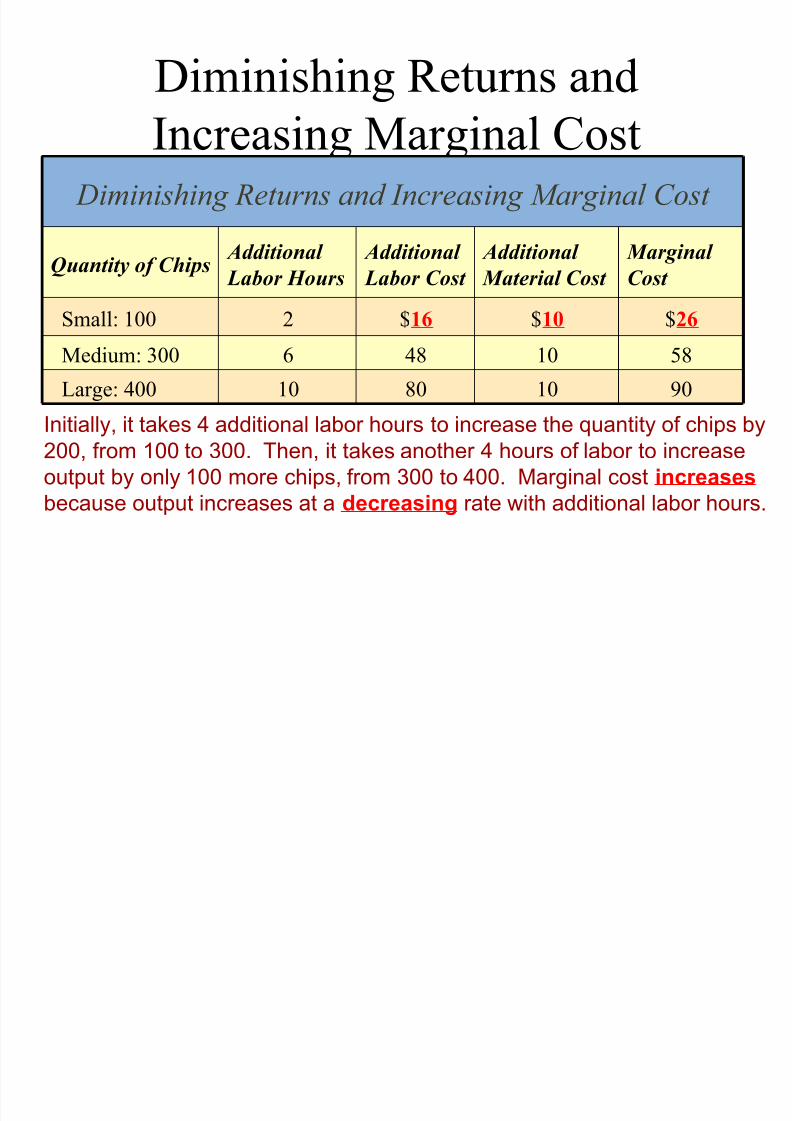

Diminishing Returns and

Increasing Marginal Cost

90108010Large: 400

5810486Medium: 300

$26$10$162Small: 100

Marginal

Cost

Additional

Material Cost

Additional

Labor Cost

Additional

Labor Hours

Quantity of Chips

Diminishing Returns and Increasing Marginal Cost

Initially, it takes 4 additional labor hours to increase the quantity of chips by200, from 100 to 300. Then, it takes another 4 hours of labor to increase

output by only 100 more chips, from 300 to 400. Marginal cost increases

because output increases at a decreasing rate with additional labor hours.

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 37/45

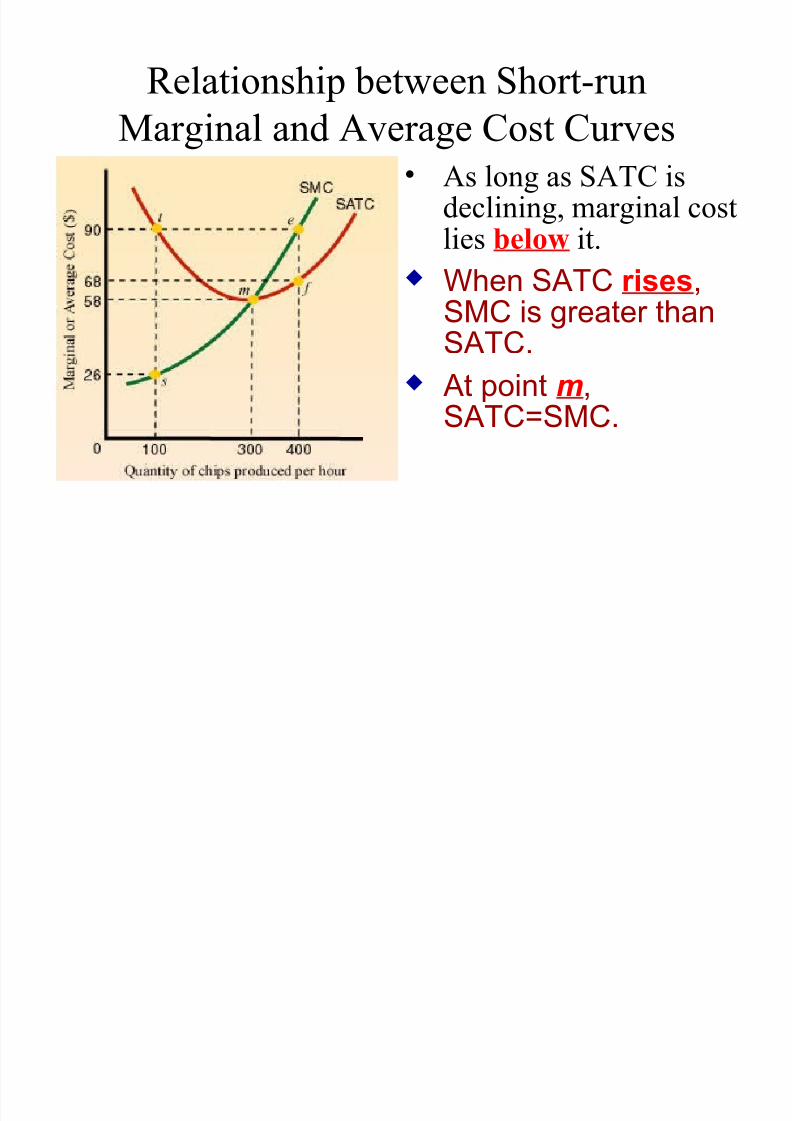

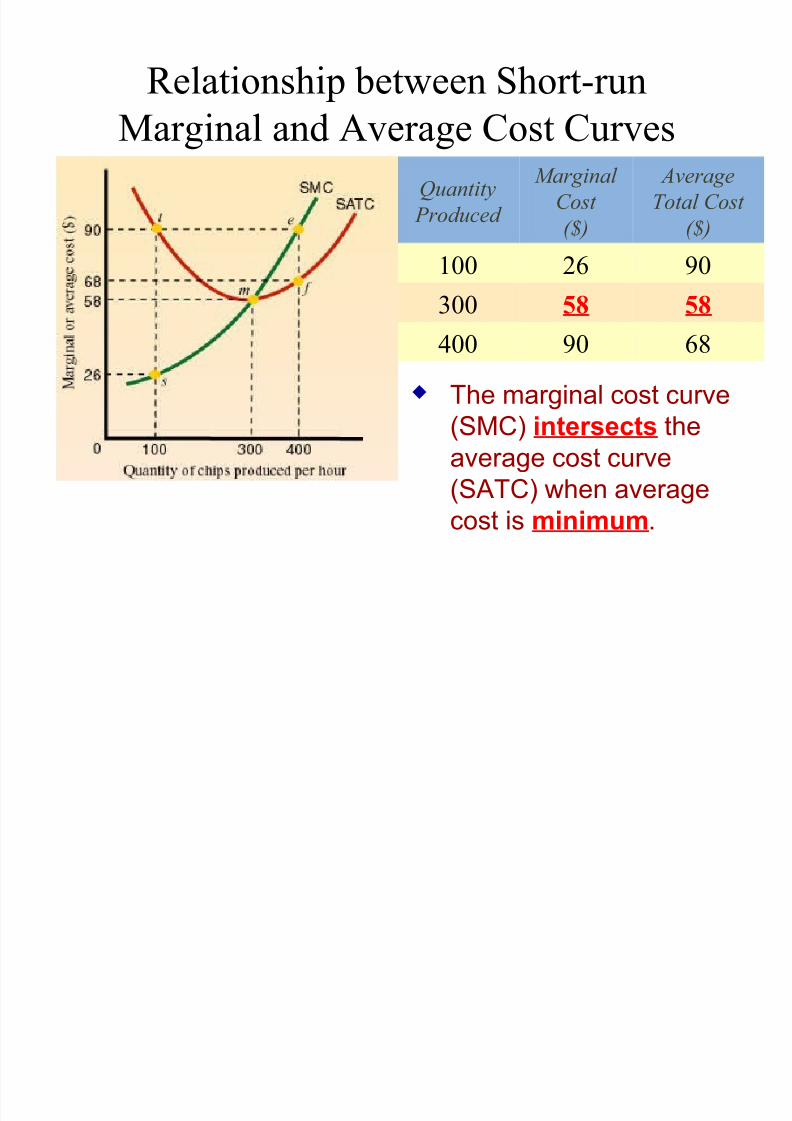

Relationship between Short-run

Marginal and Average Cost Curves• As long as SATC isdeclining, marginal costlies below it.

When SATC rises,SMC is greater thanSATC.

At point m,

SATC=SMC.

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 38/45

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 39/45

Production and Cost in the Long

Run• The key difference between the short run and thelong run is that there are no diminishing returns inthe long run.

Diminishing returns occur because workersshare a fixed facility. In the long run the firmcan expand its production facility as itsworkforce grows.

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 40/45

Long-run Average Cost

• Long-run average cost (LAC) is total cost

divided by the quantity of output when the firm

can choose a production facility of any size.

• The LAC curve describes the behavior of average

cost as the plant size expands. Initially, the curve

is negatively sloped, then beyond some point, it

becomes horizontal.

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 41/45

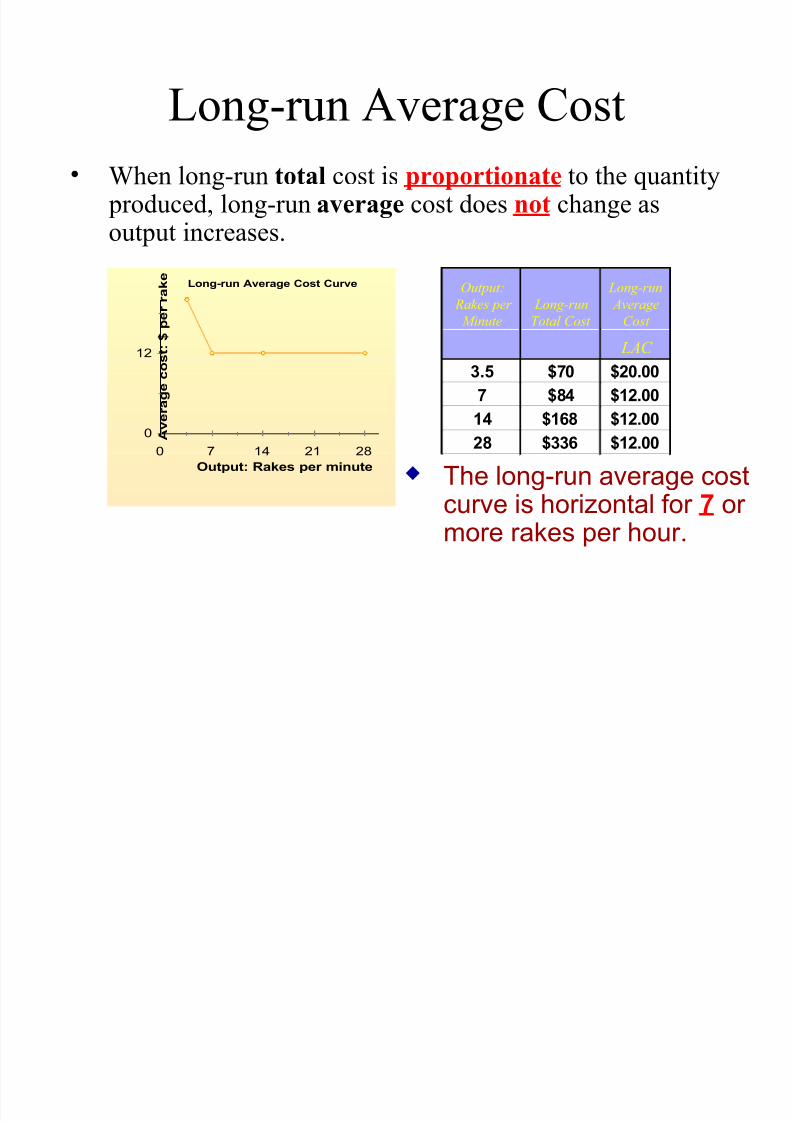

Long-run Average Cost

• When long-run total cost is proportionate to the quantity produced, long-run average cost does not change asoutput increases.

The long-run average costcurve is horizontal for 7 or more rakes per hour.

0

12

A v e

r a g e c o s t : $ p e r r a k e

0 7 14 21 28

Output: Rakes per minute

Long-run Average Cost Curve

Cost

Average

Long-run

Total Cost

Long-run

Minute

Rakes per

Output:

LAC

$20.00$703.5

$12.00$847

$12.00$16814$12.00$33628

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 42/45

Labor Specialization

• In a large operation, each worker specializes infewer tasks thus is more productive than his or her counterpart in a small operation.

• Higher productivity (more output per worker)means lower labor costs per unit of output, thuslower production costs (ever-decreasing averagecost).

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 43/45

Economies of Scale

• Economies of scale: a situation in which an increase in

the quantity produced decreases the long-run average

cost of production.

• Economies of scale refer to cost savings associated withspreading the cost of indivisible inputs and input

specialization.

• When economies of scale are present, the LAC curve will

be negatively sloped.

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 44/45

Minimum Efficient Scale

• The minimum efficient scale describes the

output at which economies of scale are exhausted

and the long-run average cost curve becomes

horizontal.

• Once the minimum efficient scale has been

reached, an increase in output no longer decreases

the long-run average cost.

8/14/2019 MCA Costs of Production

http://slidepdf.com/reader/full/mca-costs-of-production 45/45

Diseconomies of Scale

• A firm experiences diseconomies of scale when

an increase in output leads to an increase in long-

run average cost—the LAC curve becomes

positively sloped.

• Diseconomies of scale may arise for two reasons:

– Coordination problems

– Increasing input costs

![[3] Production and Costs](https://img.pdfslide.us/doc/110x75/55cf949c550346f57ba329fa/3-production-and-costs.jpg)