Embed Size (px)

Citation preview

Page 1 of 21

MAY 2019 PROFESSIONAL EXAMINATIONS MANAGEMENT ACCOUNTING (PAPER 2.2)

CHIEF EXAMINER’S REPORT, QUESTIONS AND MARKING SCHEME EXAMINER’S GENERAL COMMENTS The candidates were examined in the following subject areas of Management Accounting in the May 2019 exams.

Investment appraisal and decision making.

Cost behavior and flexible budgeting.

Overhead absorption and re-apportionment of service department overheads.

Break-even analysis and profitability under various options.

Calculation of mix and yield variances The questions were all within the approved syllabus of the Institute. Written questions and comments accounted for 32% of the total marks. However, no errors and ambiguities were noted in the questions. The following are the general weaknesses noted in the performance of the candidates.

Poor presentation of suggested solutions

Poor expression of the English language in answering the written questions.

Lack of understanding of the basic principles, concepts, methods and techniques of cost and management accounting.

Inability to analyse and comment on the results of their presentations.

Page 2 of 21

QUESTION ONE

a) Hukportie Ltd is a manufacturer of product “Okwada” which is sold for GH¢5 per unit.

Variable costs of production are currently GH¢3 per unit, and fixed costs excluding

depreciation is GH¢350,000. The current machine which was purchased for GH¢120,000

has a written down value of GH¢20,000 and a resale value of GH¢12,000. This can however

be used for the next four years.

A new machine is available which would cost GH¢90,000. This could be used to make

product “Okwada” for a variable cost of only GH¢2.50 per unit. Fixed costs, however,

would increase by GH¢7,500 per annum as a direct consequence of purchasing the

machine. The machine would have an expected life of 4 years and a resale value after that

time of GH¢8,000. Sales of product Okwada are estimated to be 75,000 units per annum.

Hukportie limited expects to earn at least 12% per annum from its investments. Taxation

and depreciation should be ignored.

Required:

Advise whether Hukportie Ltd should purchase the new machine. (10 marks)

b) Ayittey Ltd is an organization with two divisions: A and B, each with its own cost and

revenue streams. Each of the two divisions is classified as Investment center. The

company’s cost of capital is 12%. Historically, investment decisions have been made by

calculating the return on investment (ROI). A new manager who has recently been

appointed in division A has argued that using residual income (RI) to make investment

decisions would result in ‘better goal congruence’ throughout the company. The data below

shows the current position of the division as at the end of 31 December, 2016:

Details of Projects Project A Project B

Capital required GH¢ 82.8 million GH¢ 40.6 million

Sales generated GH¢44.6 million GH¢ 21.8 million

Net Profit margin 28% 33%

The company is seeking to maximize shareholders wealth. Assuming that, Division A

acquires a more efficient asset at GH¢15 million and Division B sold one of its assets with

written down value of GH¢24 million, and profits are expected to increase and decrease by

GH ¢11 million and GH¢5 million for division A and B respectively.

Required:

i) Calculate both the current Return on Investment (ROI) and Residual Income (RI) for each

of the divisions. (5 marks)

ii) Calculate and comment on the effect of the decision to invest in the new asset and disposal

of some assets will have on the current ROI and RI. (7 marks)

c) When negotiated transfer prices are used in the company, the managers who are involved

in the proposed transfer within the company meet to discuss the terms and conditions of

the transfer. They may decide not to go through with the transfer, but if they do, they must

agree to a transfer price.

Required:

Explain THREE (3) limitations of negotiated transfer prices. (3 marks)

(Total: 25 marks)

Page 3 of 21

QUESTION TWO

a) Komosa Ltd is reviewing the selling price of its product for the coming year. A forecast of

the annual costs that would be incurred by Komosa Ltd in respect of this product at differing

activity levels is as follows:

Annual production (unit) 100,000 160,000 200,000

GH¢000 GH¢000 GH¢000

Direct materials 200 320 400

Direct labour 600 960 1,200

Overhead 880 1,228 1,460

The cost behaviour represented in the above forecast will apply for the whole range of

output up to 300,000 units per annum of this product.

Required:

i) Calculate the total variable cost per unit and total fixed overhead. (4 marks)

ii) State the total cost function. (1 mark)

b) Otuo has recently opened a fast-food restaurant in a small town. Fast-food restaurants are

characterised by their quick food service. The fast-food restaurant market in the town is

dominated by a small number of long established restaurants. Otuo is seeking to grow its

business and attract the town’s residents with its burger meals.

The performance report for the first month of business is to be presented at the restaurant’s

monthly management meeting. A draft performance report for the first month of business

is reproduced below:

Budget Actual Variance

Sales (number of meals) 6,000 5,400 (600)

GH¢ GH¢ GH¢

Revenue 180,000 167,400 12,600 A

Direct Material 48,000 49,140 1,140 A

Direct Labour 33,000 27,000 6,000 F

Variable Production Overhead 21,000 18,900 2,100 F

Fixed costs 36,000 40,000 4,000 A

Profit 42,000 32,360 9,640 A

Required:

i) Explain the term flexible budget. (2 marks)

ii) Using a flexible budgeting approach, redraft the operating statement so as to provide a more

realistic indication of the variances. (7 marks)

(Note: You are not required to explain the causes of the variances)

iii) In TWO (2) ways, explain why the original operating statement was of little use to

management. (2 marks)

iv) Identify FOUR (4) non-financial measures that Otuo could use to monitor the performance

of the new fast-food restaurant. (4 marks)

(Total: 20 marks)

Page 4 of 21

QUESTION THREE

a) Bobich Ltd manufactures plastic containers for the pharmaceutical industry. The factory,

in which the company undertakes all its production has two production departments

namely: Cutting and Shaping and two service departments- Stores and Maintenance.

The information below was extracted from the company’s budget for its financial year

ended 31 March 2019.

Allocated Overhead Costs GH¢

Cutting Department (Cutting) 14,000

Shaping Department (Shaping) 16,000

Stores Department (Stores) 3,500

Maintenance Department (Maintenance) 2,800

Other Production Overheads GH¢

Factory rent 525,000

Factory building insurance 70,000

Plant & machinery insurance 39,000

Plant & machinery depreciation 58,500

Canteen subsidy 150,000

Direct Costs GH¢

Cutting Department 144,000

Shaping Department 210,000

The following additional information is also provided:

Cutting Shaping Stores Maintenance Floor area (square metres) 18,000 12,000 3,000 2,000

Value of Plant & Machinery (GH¢) 300,000 50,000 25,000 15,000

Number of stores requisitions 1,000 500 - -

Maintenance hours required 2,700 2,000 300 -

Number of employees 34 60 4 2

Machine hours 12,000 2,200 - -

Labour hour 9,000 15,000 - -

Required:

i) Explain what is meant by the term “blanket overhead rate”. (2 marks)

ii) Prepare an overhead analysis sheet based on the above information. You must clearly state

the basis used for any apportionments. (7 marks)

iii) Re-apportion the service department costs and calculate the most appropriate overhead rate

for each department. (Rate should be calculated to two decimal places). (3 marks)

iv) State THREE (3) reasons why companies calculate pre-determined overhead absorption

rates. (3 marks)

Page 5 of 21

b) Oria Software Ltd, a computer software company is developing a new accounting package,

“Future Accounting”. The following are the budgeted amounts for the product over a four-

year product life-cycle

Year 0 Year 1 Year 2 Year 3 Year 4

Estimated quantity in units 3,500 5,000 2,000 500

GH¢ GH¢ GH¢ GH¢ GH¢

Research & Dev’t costs 360,000

Design costs 240,000 250,000

Production costs:

Variable cost per unit 42 35 35 40

Fixed costs 150,000 150,000 120,000 100,000

Marketing costs:

Variable cost per unit 40 35 10 22

Fixed costs 30,000 20,000 12,000 15,000

Distribution:

Variable cost per unit 20 22 18 10

Fixed costs 50,000 60,000 40,000 30,000

Customer service:

Variable cost per unit 8 12 14 10

Fixed costs 80,000 85,000 45,000 -

To be profitable, Oria Software Ltd must generate revenues to cover costs for all six-

business functions taken together and, in particular, its high non-production costs. The

company has therefore proposed a selling price of GH¢ 250 per software over the entire

product life cycle.

Required:

i) Explain lifecycle costing and identify TWO (2) benefits Oria Software Ltd will derive from

using lifecycle costing. (3 marks)

ii) Calculate cost per software taking into account the entire lifecycle and comment on the

proposed selling price. (7 marks)

(Total: 25 marks)

Page 6 of 21

QUESTION FOUR

Boasiako Ltd manufactures high quality coffee biscuits that are sold to hotels and

restaurants in Koforidua. Two months ago it had prepared a budget for the forthcoming

financial year.

Details of the budget is presented below:

GH¢

Sales 6,000,000

Less:

Direct materials 2,080,000

Direct labour 1,160,000

Variable overheads 840,000

Fixed overheads 972,600

Total costs 5,052,600

Profit 947,400

The budget above has been prepared on the assumption that sales will be 800,000 packets

of biscuits. However, due to changing economic conditions, the sales forecast for the year

is now 720,000 packets of biscuits. It is expected that selling price per unit, direct costs per

unit and variable overhead cost per unit will not change from those budgeted. It is also

expected that fixed overheads will be the same as those budgeted.

Management is now considering a number of options so as to improve profitability for the

forthcoming financial year:

Option 1:

Decrease the selling price by 20%. It is anticipated that this would increase sales volume

by 25% on the forecast sales for the current year.

Option 2:

Decrease all variable costs by 10% and decrease fixed costs by 10%. This is not expected

to have any impact on the sales level.

Option 3:

Decrease the selling price by 10% and decrease fixed costs by 5%. This is expected to

increase sales volume by 25% on the forecast sales for the current year.

Required:

a) Calculate the expected profit for the current year (forecast sales). (2 marks)

b) Based on the forecast activity for the year, calculate:

i) The breakeven point in packets of biscuits.

ii) The margin of safety in percentage terms.

iii) The sales revenue required to earn a profit of GH¢1,440,000. (6 marks)

c) Evaluate the profitability of the three options and recommend the option that Boasiako Ltd

should adopt. (7 marks)

(Total: 15 marks)

Page 7 of 21

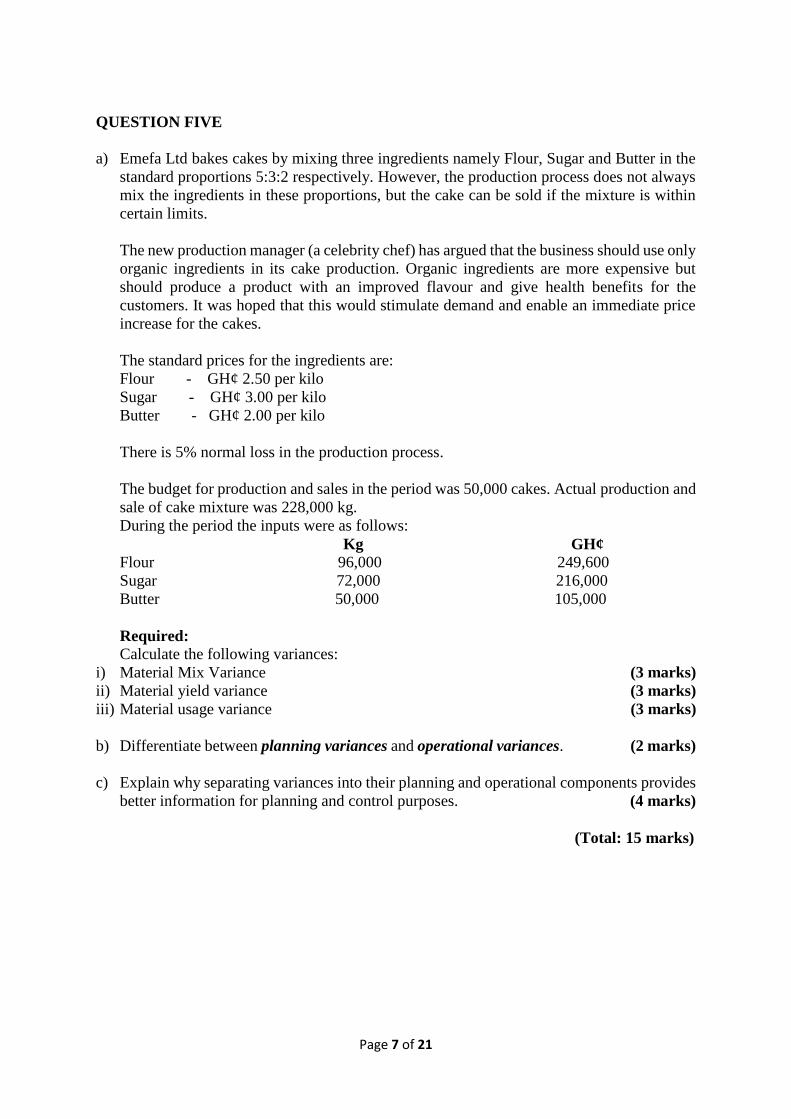

QUESTION FIVE

a) Emefa Ltd bakes cakes by mixing three ingredients namely Flour, Sugar and Butter in the

standard proportions 5:3:2 respectively. However, the production process does not always

mix the ingredients in these proportions, but the cake can be sold if the mixture is within

certain limits.

The new production manager (a celebrity chef) has argued that the business should use only

organic ingredients in its cake production. Organic ingredients are more expensive but

should produce a product with an improved flavour and give health benefits for the

customers. It was hoped that this would stimulate demand and enable an immediate price

increase for the cakes.

The standard prices for the ingredients are:

Flour - GH¢ 2.50 per kilo

Sugar - GH¢ 3.00 per kilo

Butter - GH¢ 2.00 per kilo

There is 5% normal loss in the production process.

The budget for production and sales in the period was 50,000 cakes. Actual production and

sale of cake mixture was 228,000 kg.

During the period the inputs were as follows:

Kg GH¢

Flour 96,000 249,600

Sugar 72,000 216,000

Butter 50,000 105,000

Required:

Calculate the following variances:

i) Material Mix Variance (3 marks)

ii) Material yield variance (3 marks)

iii) Material usage variance (3 marks)

b) Differentiate between planning variances and operational variances. (2 marks)

c) Explain why separating variances into their planning and operational components provides

better information for planning and control purposes. (4 marks)

(Total: 15 marks)

Page 8 of 21

SOLUTION TO QUESTIONS QUESTION ONE a) Determination of cost savings: GH¢

Existing variable cost per unit 3.00 Less new variable cost per unit 2.50 Savings in variable cost 0.50 Total savings in variable cost (GH¢75,000 x GH¢ 0.5) 37,500.00 Less additional cost per annum 7,500.00 Net cash savings in cost 30,000.00

The net investment should be 78,000. This is because the receipt on disposal of old asset should be deducted from the cost of the new machine. The resale value of the machine is GH¢ 8,000.

Candidates can use annuity due formula to determine the NPV Using Annuity Due, NPV is obtained as: = - Co + C x AF + C/ (1+ r) 𝑛 = - 78,000 .00 + 30,000.00 x 3.038 + 8,000.00 / (1.12) 4 = - 78,000.00 + 91,140.00 + 5,084.14 = 18,224.14

Alternatively, NPV can be calculated as: Year Cash flows DF (12%) PVs

0 (78,000.00) 1.000 (78,000.00)

1 30,000.00 0.893 26,790.00

2 30,000.00 0.797 23,910.00

3 30,000.00 0.712 21,360.00

4 8,000.00 + 30,000.00 0.636 24,168

NPV 18,224

Alternatively PV of Operating Cost. - Old Machine : VC = 3 x 75,000 225,000 Add FC 350,000 575,000 @ 3.038 = 1,746,850 - New Machine : VC 2.5 x 75,000 187,500 Add FC 357,500 545,000 @ 3.038 = 1,655,710 Net Investment (90,000 – 12,000) @ 1 78,000 Resale Value 8000 @ 0.636 (5,088) 1,728,622 Difference (NPV) 18,228

(8 marks evenly spread using ticks)

Page 9 of 21

Decision The NPV is positive and so the project is expected to earn more than 12% per annum and is therefore acceptable.

(2 marks) b)

i) Divisional performance measurement using ROI Division A: ROI = Net Profit / investment x 100

= 12.49 / 82.8 x 100 =15.085%

Division B: ROI = Net Profit / investment x 100

= 7.194 / 40.6 x 100 =17.72%

Divisional performance measurement using RI

Division A GH¢

Net Profit 12.49 Less imputed interest charge (12% @ 82.8) = (9.936) Residual Income (RI) 2.554

Division B

GH¢ RI =Net Profit 7.194 Less imputed interest charge (12% @ 40.6) = (4.872) Residual Income (RI) 2.322

(5 marks evenly spread using ticks)

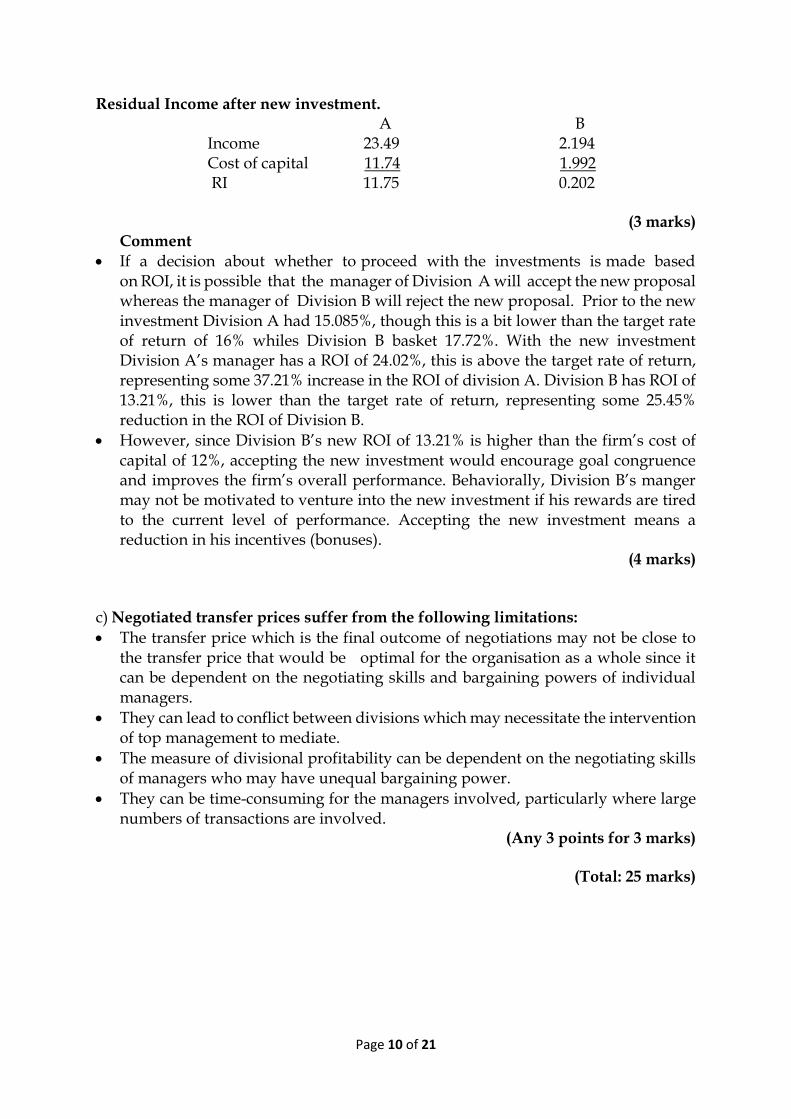

ii) Divisional performance after the new investment Division A

ROI = Net Profit / investment x 100

= 23.49 / 97.8 x 100 = 24.02 %

Division B ROI = Net Profit / investment x 100

= 2.194 / 16.6 x 100 = 13.21%

Page 10 of 21

Residual Income after new investment. A B Income 23.49 2.194 Cost of capital 11.74 1.992 RI 11.75 0.202

(3 marks) Comment

If a decision about whether to proceed with the investments is made based on ROI, it is possible that the manager of Division A will accept the new proposal whereas the manager of Division B will reject the new proposal. Prior to the new investment Division A had 15.085%, though this is a bit lower than the target rate of return of 16% whiles Division B basket 17.72%. With the new investment Division A’s manager has a ROI of 24.02%, this is above the target rate of return, representing some 37.21% increase in the ROI of division A. Division B has ROI of 13.21%, this is lower than the target rate of return, representing some 25.45% reduction in the ROI of Division B.

However, since Division B’s new ROI of 13.21% is higher than the firm’s cost of capital of 12%, accepting the new investment would encourage goal congruence and improves the firm’s overall performance. Behaviorally, Division B’s manger may not be motivated to venture into the new investment if his rewards are tired to the current level of performance. Accepting the new investment means a reduction in his incentives (bonuses).

(4 marks)

c) Negotiated transfer prices suffer from the following limitations:

The transfer price which is the final outcome of negotiations may not be close to the transfer price that would be optimal for the organisation as a whole since it can be dependent on the negotiating skills and bargaining powers of individual managers.

They can lead to conflict between divisions which may necessitate the intervention of top management to mediate.

The measure of divisional profitability can be dependent on the negotiating skills of managers who may have unequal bargaining power.

They can be time-consuming for the managers involved, particularly where large numbers of transactions are involved.

(Any 3 points for 3 marks)

(Total: 25 marks)

Page 11 of 21

EXAMINER’S COMMENTS Performance of the candidates is not satisfactory. Difficulties encountered include: inability to determine the net cash flows resulting from the cash savings in cost which is GH¢ 30,000 (ii) inability to factor in the resale value of the current and the new machine in arriving at the yearly cash flows of GH¢ 12,000 in year zero and GH¢ 8,000 in year four. None of the candidates could get the NPV of GH¢18,228 correctly. They have no difficulties in computing the RO1 for the divisions but some of them had problems calculating the R1 because they could not calculate the imputed interest charge to be deducted from the net profit. The imputed interest charge is the cost of capital (12%) of the capital required.

Page 12 of 21

QUESTION TWO a) i) Variable cost per unit

Material Cost GH¢ 200,000

100,000 = ¢2 per unit

Labour Cost 𝐺𝐻𝑆 600,000

100,000 = ¢ 6 per unit

Variable overhead cost can be arrived at using high and low method

Variable cost per unit = 𝐺𝐻𝑆 1,460,000−𝐺𝐻𝑆 880,000

200,000−100,000 = ¢ 5.8

Therefore, total variable cost per unit = ¢ 13.8 (3 marks)

Fixed cost = 1,460,000- (200,000 x 5.8) = ¢ 300,000. (1 mark)

ii) Y= 300,000 + 13.8x (1 mark) b) i) Flexible budget is a budget which recognises differences between fixed and

variable costs when volume of activity changes. Flexible budgets are useful for control purposes as the actual volume of activity may be compared to budget by flexing the budget so that it is based on actual activity. Flexible budget cannot be prepared until the end of a budget period. (2 marks)

ii) Budget Flexed Actual Variances 6,000 units per unit 5,400 units 5,400 units GH¢ GH¢ GH¢ GH¢ GH¢ Revenue 180,000 30 162,000 167,400 5,400 F Less Variable cost: Direct Material 48,000 8 43,200 49,140 5,940 A Direct Labour 33,000 5.5 29,700 27,000 2,700 F VP O/H 21,000 3.5 18,900 18,900 - Contribution 78,000 13 70,200 72,360 Fixed Cost 36,000 N/A 36,000 40,000 4,000 A Profit/(Loss) 42,000 34,200 32,360 1,840 A

(7 marks evenly spread using ticks)

iii) Reasons why the original operating segment is of little use to management

A static budget is fixed for the entire period covered by the budget, with no changes based on actual activity. Thus, even if actual sales volume changes significantly from the expectations documented in the static budget, the amounts listed in the budget are not changed.

Page 13 of 21

In more dynamic environments where operating results could change substantially, a static budget can be a hindrance, since actual results may be compared to a budget that is no longer relevant.

Static budget is not effective for evaluating the performance of cost centers as management may be comparing unlike terms.

(Any 2 points for 2 marks)

iv) Non-financial measures Otuo could use to monitor performance

Speed of food delivery. Customers at fast food restaurants expect their food order to be served quickly. If Otuo is to be successful, it must achieve fast food delivery. Therefore, a measure of time from customer order to food service is a key metric to monitor in ascertaining the restaurant’s success at this requirement.

Number of repeat customers. Otuo operates in a small town that offers a number of other choices of fast food restaurant to its residents. If Otuo is to establish itself and grow market share, the restaurant needs to develop a loyal customer base. Number of repeat customers is a measure that could indicate the sustainability of the business and future financial success.

Cleanliness of the environment

Curtesy of waiters and waitress

Responsiveness

Availability of food (Any 4 points for 4 marks)

(Total: 20 marks)

EXAMINER’S COMMENTS Performance of the candidates is satisfactory. Two problems were encountered.

Difficulties in calculating the Variable Overhead cost per unit using the High-Low method. Hence the TVC per unit was wrongly calculated.

Inability to flex the budget to performance before comparing with the actual results.

About 50% of the candidates got this correctly determined.

Page 14 of 21

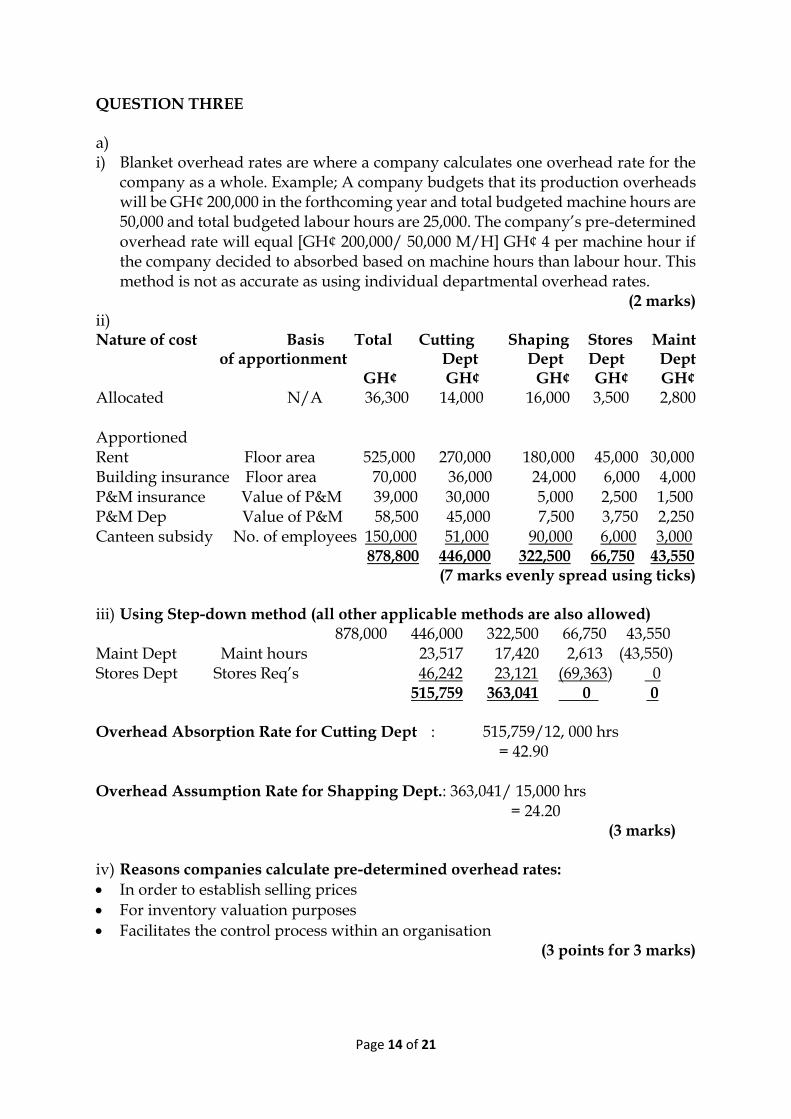

QUESTION THREE a) i) Blanket overhead rates are where a company calculates one overhead rate for the

company as a whole. Example; A company budgets that its production overheads will be GH¢ 200,000 in the forthcoming year and total budgeted machine hours are 50,000 and total budgeted labour hours are 25,000. The company’s pre-determined overhead rate will equal [GH¢ 200,000/ 50,000 M/H] GH¢ 4 per machine hour if the company decided to absorbed based on machine hours than labour hour. This method is not as accurate as using individual departmental overhead rates.

(2 marks) ii) Nature of cost Basis Total Cutting Shaping Stores Maint of apportionment Dept Dept Dept Dept GH¢ GH¢ GH¢ GH¢ GH¢ Allocated N/A 36,300 14,000 16,000 3,500 2,800 Apportioned Rent Floor area 525,000 270,000 180,000 45,000 30,000 Building insurance Floor area 70,000 36,000 24,000 6,000 4,000 P&M insurance Value of P&M 39,000 30,000 5,000 2,500 1,500 P&M Dep Value of P&M 58,500 45,000 7,500 3,750 2,250 Canteen subsidy No. of employees 150,000 51,000 90,000 6,000 3,000 878,800 446,000 322,500 66,750 43,550

(7 marks evenly spread using ticks)

iii) Using Step-down method (all other applicable methods are also allowed) 878,000 446,000 322,500 66,750 43,550 Maint Dept Maint hours 23,517 17,420 2,613 (43,550) Stores Dept Stores Req’s 46,242 23,121 (69,363) 0 515,759 363,041 0 0 Overhead Absorption Rate for Cutting Dept : 515,759/12, 000 hrs = 42.90 Overhead Assumption Rate for Shapping Dept.: 363,041/ 15,000 hrs = 24.20

(3 marks)

iv) Reasons companies calculate pre-determined overhead rates:

In order to establish selling prices

For inventory valuation purposes

Facilitates the control process within an organisation (3 points for 3 marks)

Page 15 of 21

b) i) Lifecycle costing is a concept which traces all costs to a product over its complete

lifecycle, from design through to cessation. It recognises that for many products there are significant costs to be incurred in the early stages of its lifecycle. This is probably very true for Oria Software Inc. The design and development of software is a long and complicated process and it is likely that the costs involved would be very significant.

(1 mark)

Benefits of lifecycle costing

The profitability of a product can then be assessed taking all costs into consideration.

It is also likely that adopting lifecycle costing would improve decision-making regarding product introduction, product mix and for discontinuation of the product

It is also considered a way to enhance cost control of manufacturing costs.

It helps in pricing decision therefore preventing underpricing at the launch point. (Any 2 points for 2 marks)

ii) Cost per software taking into account the entire life cycle GH¢’000

R&D 360 Design (240 +250) 490 Production – variable (147 +175+70+20) 412

-fixed (150 +150 +120+ 100) 520 Marketing -variable (140 +175 + 20 +11) 346

-fixed (30 + 20 + 12 + 15) 77 Distribution – Variable (70+ 110 + 36 + 5) 221

- fixed (50 +60 + 40 + 30) 180 Customer service – variable ( 28 + 60 + 28 + 5) 121

-fixed ( 80 +85 + 45) 210 Total life cycle costs 2,937 Production (‘000 units) (3.5 +5 +2 + 0.5) ÷ 11

Cost per unit GH¢ 267

(6 marks evenly spread using ticks)

Conclusion Clearly, proposed selling price per software of GH¢250 is not advisable as it is lower than cost of production. Oria Software Inc. may either increase the selling price or undertake cost reduction techniques like value engineering, quality cycle or alternative source of cheaper material to be able to reduce the cost to be lower than GH¢ 250 per unit.

(1 mark)

(Total: 25 marks)

Page 16 of 21

EXAMINER’S COMMENTS The performance of the candidates in this question are also satisfactory. The problem they have is using the appropriate basis for apportioning the other overhead costs to the various departments. Hence, some of them got the apportioned costs wrongly distributed which affected the total costs distributed to the various departments. Some level of difficulties were also noted when allocating the service departments costs to the production departments. Just because of selecting the inappropriate bases for the apportionment. The definition and benefits of Lifecycle costing by the candidates was also not satisfactory indicating that the candidates do not appreciate the importance of reading costing principles, methods and concepts.

Page 17 of 21

QUESTION FOUR a) Profit made by the company for the year Per unit

GH¢

Total 720,000

GH¢

Sales 7.50 5,400,000

Less: variable costs

Direct materials 2.60 1,872,000

Direct Labour 1.45 1,044,000

Variable Overheads 1.05 756,000

Total Variable Costs 5.10 3,672,000 Contribution 2.40 1,728,000

Less: Fixed Overheads 972,600

PROFIT 755,400

b) i) Breakeven points in packet of Biscuits, Margin of safety in % and revenue

required to earn a profit of GH¢1,440,000

Breakeven point in units (BEP) = Total Fixed Costs = GH¢972,600 = Contribution per units GH¢ 2.40

Break even Packets of biscuits = 405,250 (2 marks)

ii) Margin of Safety in % terms = Actual Sales – BEP sales x 100 = Actual sales

720,000-405,250 x100 = 43.7% 720,000

(2 marks) iii) Revenue required to earn Target Profit

= Total Fixed Costs + Target Profit Contribution to sales ratio = (GH¢972,600+ GH¢1,440,000)/ 0.32 =GH¢ 7,539,375

(2 marks)

Contribution to Sales ratio** 0.32 **Contribution to sales ration = Contribution = GH¢2.40 = 0.32 Sales 7.50

Page 18 of 21

c) Evaluation of 3 options

Option 1 SP-20%

Volume+25%

Option 2 VC-10%; FC-

10%

Option 3 SP-10%; FC-5%

Volume +25%

Current Situation

Units 900,000 720,000 900,000 720,000

GH¢ GH¢ GH¢ GH¢

Sales 5,400,000 5,400,000 6,075,000 5,400,000 Less: Variable Costs

4,590,000 3,304,800 4,590,000 3,672,000

Contribution 810,000 2,095,200 1,485,000 1,728,000 Less: Fixed Costs 972,600 875,340 923,970 9,72,600 Profit (162,600) 1,219,860 561,030 755,400

(6 marks evenly spread using ticks) Recommendation: The company should consider option 2 as this gives a higher profit. (1 mark)

(Total: 15 marks) EXAMINER’S COMMENTS The calculation of the expected profit for the current year was satisfactorily done by applying the sales and costs per unit to the new forecast sales figure of 720,000 units. Few candidates have problem calculating the C/S ratio needed to determine the revenue required to earn a target profit. The C/S Ratio is contribution/sales, that is GH¢2.40/7.50 which is 0.32.

Page 19 of 21

QUESTION FIVE a) i) Material Mix Variance

Flour (96,000 – (5/10 x 218000)@GH¢2.5 = 32,500 F Sugar (72,000 - (3/10 x218,000)@GH¢ 3.0 = 19,800 A Butter (50,000 - (2/10 X 218,000) @GH¢2.0 = 12,800 A Total Material Mix Variance 100A

(3 marks) ii) Material Yield Variance

Flour (109,000 – 120,000) @GH¢2.5 = 27,500F Sugar (65,400 - 72,000) @GH¢3.0 = 19,800F Butter (43,600 – 48,000) @ GH¢2.0 = 8,800F Total Material Yield 56,100F

Alternative solution to Yield variance. Total input 218,000 Less normal loss (5%) 10,900 Standard yield 207,100 Actual yield 228,000 Yield variance 20,900 F × WAC 2.6842 56,100 F WAC. Flour (5×2.5) 12.5 Sugar (3×3) 9.0 Butter (2×2) 4.0 Total 25.50 ÷9.5 2.6842

(3 marks) iii) Material Usage variance = Mixed Variance + Yield Variance Flour = 32,500 F + 27,500F = 60,0000 F Sugar =19,800A + 19,800F = - Butter = 12,800 A +8,800F = 4,000 A Total 100A + 56,100F 56,000 F Alternatively Flour = (96,000 -120,000) @GH¢2.5= 60,000F Sugar = (72,000 - 72,000) @GH¢3.0 = - Butter = (50,000 - 48,000) @GH¢2.0= 4000 A Total Usage 56,000F

(3 marks)

Page 20 of 21

ALTERNATIVE SOLUTION

MATERIAL FLOUR SUGAR BUTTER TOTAL

STANDARD MIX

5/10 3/10 2/10 10/10

AQAM 96,000 72,000 50,0000 218,000

AQSM 109,000 65,400 43,600 218,000

SQSM (ACTUAL PRODUCTION)

120,000 72,000 48,000 240,000

STANDARD PRICE

GH¢2.50 GH¢3.00 GH¢2.00

MIX VARIANCE

32,500F 19,800A 12,800A 100A

YEILD VARIANCE

27,500F 19,800F 8,800F 56,100F

USAGE 60,000F - 4,000A 56,000F

b) Planning Variance: (revision variance) - compares an original standard with

revised standard that would have been used if the planner had known what was to happen. The update to the original standard to reflect the change in conditions and environment. They are often deemed to be uncontrollable hence management cannot be held responsible. Planning variance is very useful for providing feedback on just how skilled management are interested in future prices and cost.

Operational Variance: (Operating variance) - compares an actual result with revised standard. They are often deemed to be controllable hence management be held responsible for operational variances. The operational variance is more meaningful in that it measures the efficiency of management given the market conditions that prevailed at the time. It therefore ignores factors that cannot be controlled, which in turn stop management from becoming demotivated.

(2 marks) c)

ORIGINAL STANDARD REVISED STANDARD ACTUAL Planning Operational

Page 21 of 21

Planning and operational variances provide better information for planning and control purposes for the following reasons:

The use of planning and operational variances will enable management to draw a distinction between variances caused by factors outside the control of the business and planning errors (planning variances) and variances caused by factors that are within the control of management (operational variances).

The managers’ performance can be compared with the adjusted standards that reflect the conditions the manager actually operated under during the reporting period. If planning and operational variances are not distinguished, there is potential for dysfunctional behaviour especially where the manager has been operating efficiently and effectively and performance is being judged by factors outside the manager’s control.

The use of planning variances will also allow management to assess how effective the company’s planning process has been. Where a revision of the budget is required due to changes that were not foreseeable at the time the budget was prepared, the planning variances are uncontrollable. However, budgets that failed to anticipate foreseeable market trends when they were set will reflect faulty planning. It could be argued that some of the planning variances are in fact controllable at the planning stage.

The information used in setting the ex-post standards can be used in future budget periods. The planning variances may also indicate problems in the standard setting process and the reasons for this can be identified and improvement made to the process.

(4 points for 4 marks)

(Total: 15 marks) EXAMINER’S COMMENTS The calculation of the Mix, Yield and Usage variances was well done. However, the candidates could not differentiate between planning variance and operational variance. Planning variance simply compares original standard with revised standard whilst operational variance compares actual results with revised standards.

![chapter 3 overheads - John D. Cresslercressler.ece.gatech.edu/courses/COE_3002/overheads/F19/chapter 3... · Title: Microsoft PowerPoint - chapter 3 overheads [Compatibility Mode]](https://img.pdfslide.us/doc/110x75/5fb70f40766c616ca64667e8/chapter-3-overheads-john-d-3-title-microsoft-powerpoint-chapter-3-overheads.jpg)